Embed Size (px)

Citation preview

C:\Users\Tom\Dropbox\2012 Talk\2012 Talks .docx

Session 1

Dealing with ‘reluctant’ witnesses Forensic Evidence & Motive

Evidence Issues - Technology

Session 2

General Principles when dealing with the ICA The standard of proof required to determine to substantiate a fraud allegation and;

the standard of the evidence required of fraud allegations The concept of a ‘breach’ of ICA and the resultant ‘remedy’ as it relates to s56

PRESENTED TO

SUNCORP METWAY LIMITED GI INVESTIGATIONS

FRIDAY 12 OCTOBER 2012

David Courtenay Courtenay & Co

Solicitors 100A Longueville Road

LANE COVE NSW 2066 DX 23316 LANE COVE

Tel: 9420 1622 Fax: 9420 1655

2 Session 1 – Combined session – Max 1.5 hours (L28 boardroom) starting approx. 10.30am Dealing with ‘reluctant’ witnesses

• Cooperation - overview • What information can we compel the insured to provide with regard to any

alibi/witness • What information can we record if witnesses are reluctant to provide a statement? • Will these hold up?

Forensic Evidence

• An increasing number of suspected staged accident claims seem to have a strong forensic report, but are deficient in opportunity and motive.

• Are there other enquiries we could we have explored? • Any new trends? • Is it reasonable to expect that we will be able to determine the motive? • What other options are available to us e.g. Allege that the insured has failed to

establish that an ‘event’ (as defined by the policy has occurred) has occurred? Other options?

Evidence Issues

• VOIP and other smart phone communication apps • GPRS, IMEI and URL’s etc • E Tags – a significant resource • CCTV – increased retention. • Seizure of devices

Session 2 - With some of our ‘newer’ IROs – Max 1 hour starting at 1pm Fraud ‘102’ (slightly more advanced than 101)

• General Principles when dealing with the ICA • Discuss the 'balance of probabilities' and the standard of proof required to

determine whether there is sufficient evidence to substantiate a fraud allegation and;

• the Briginshaw test and the standard of the evidence required of fraud allegations • The concept of a ‘breach’ of ICA and the resultant ‘remedy’ as it relates to s56

Note: I have, as usual, provided far too much written material. Use it for summary and reference purposes – I will not be reading it out but merely use as a guide.

3 Session 1 – Combined session – Max 1.5 hours (L28 boardroom) starting approx. 10.30am Dealing with ‘reluctant’ witnesses

• Cooperation - overview • What information can we compel the insured to provide with regard to any

alibi/witness • What information can we record if witnesses are reluctant to provide a statement? • Will these hold up?

1.1 NON COOPERATION- OVERVIEW In an investigation you want cooperation from your insured and relevant witnesses. Critical to your ability to investigate are issues as to:

• What information are you entitled to get? • Who can you get it from?

The answer to these questions turns upon principles of contract law as that law applies to policies of insurance. Your position will often be difficult. You may be faced with a reluctant fraudster and hobbled by the fact that Section 54 (1), which provides the remedy for non cooperation is uncertain in its application and was never intended to deal with non cooperation.. On the flip side:

• Your insured has the onus of proof. • IDR, EDR and FOS all agree that you can decline for non – cooperation.

1.2 PROOF OF POLICY, EVENT AND LOSS An insured seeking to claim against an insurer must prove: 1. There was a valid contract with the insurer at the time of an event. 2. An event insured under the contract has occurred. 3. The insured has suffered loss as a proximate cause of the insured event. If the insured fails to prove the existence of any of these elements they ought not to be compensated by an award of damages or have payment made under a policy. The insurer, if it wishes to deny a claim, must either rely upon the insured failing to prove one of the above elements1 or it must positively prove; A. A breach of a contractual duty enabling the insurer to avoid liability

1 Which it may assist by destroying the insured’s credibility or credit.

4 OR B. That the claim comes within an exception to the policy and is thereby excluded. Non co-operation may mean that the insured has failed to prove 1, 2 or 3 or might be a Category A Defence. 1.3 COOPERATION - WHAT MAY BE REQUIRED In every case the relationship between an insurer and its insured is contractual. The contract is the key document. Review what the contract says about the insured’s duty to cooperate. Can an insured refuse to undergo a record of interview and instead rely upon answering written questions put to his solicitor? It depends upon the policy, the nature of the claim and who is answering the question. A judge or arbiter such as FOS will generally look first at the contract to see what it says before deciding if the duty under the contract has been breached. Often policies are unclear about the extent of the duty. Have a very close look at the “Giving assistance” provisions. If a contractual policy provision is ambiguous or uncertain it is read against whoever drafted the contract. This principle, known as contra proferentem is bad for insurers. Going back to interviews the AAMI policy says that the obligation to assist may include:

• Undergoing an interview or interviews about the circumstances of the claim; The GIO equivalent says:

• You must assist us in handling your claim. This can include agreeing to be interviewed and/or providing relevant documents we ask for (e.g. proof of ownership);

Is there a difference? You bet there is. I have had a CTTT member suggest that the fact that an insured underwent an initial CIRCS call was of itself enough to comply with the policy obligation. Fortunately for you FOS is pro interview. In FOS decision 240128 it was held:

“A written statement cannot be tested. In an interview, there is opportunity to check, to clarify and to confirm a statement.”

Now for an ugly thought. What is the remedy for failure to assist? What is the AAMI remedy if the insured refuses to undergo an interview? The remedy lies in section 54(1) in Division 3 of the ICA. Section 54 says:

“If the act done in breach of policy complained of is not causative of the loss then the insurer may not refuse to pay the claim but its liability in respect of the claim is reduced the amount which fairly represents the extent to which the interests of the insurer were prejudiced as a result of the act.”

5

Section 54 (2) says;

“Where the act could reasonably be regarded as being capable of causing or contributing to the loss the insurer may refuse to pay the claim.”

Section 54 (3) says;

“Where the insured proves that no part of the loss was caused by the act, the insurer may not refuse the claim by reason only of the act.”

1.4 CASES NON COOPERATION

FAI Insurance Limited v Aust Hospital Care Pty Ltd [2001] HCA 38. Section 54 is remedial in nature. Judges ought to apply its provisions broadly and give effect to its terms. Superchem Products Ltd v American Life and General Insurance Company Ltd [2004] UKPC2 The Privy Council on appeal from the Court of Appeal of Trinidad and Tobago applied Challenge Financial Ltd v State Insurance General Manager [1982] 1 NZLR 762. A condition in a policy required an insured to provide particulars of loss. The Court held that the particulars required vary with the nature of the insurance and the type of claim and stated, as a general proposition, that an insured did not perform his duty adequately unless he furnished the best particulars that the circumstances permitted. Whether the details given were sufficient in any case or not was to be a matter of degree depending on the material available but was stated:

“Where an insured has the mechanisms available to obtain and provide the information that he must take every reasonable step to gather that information and put it before the insurer and that failure to do so may amount to a breach of the duty of the utmost good faith.”

Norwood v Ian Dickson Ltd (1993) 7 ANZ Insurance Cases 61-176 The Master of the New Zealand High Court [a junior judge] concluded that an insurer was entitled to deny indemnity to an insured upon the basis that the insured had been uncooperative and had refused to provide information to the insurer as to policy inception in support of the claim, as to the risk held covered, that was in the possession of the insured. The case is useful support for the proposition that information concerning the entry into the policy can be obtained at the time a claim is made. The Master at page 78, 007 said; “I see the issue in very simplistic terms. Mr Dickson wants an insurance

cover. Before liability is accepted he must establish the ground and basis for that cover. It is insufficient to say a property in which he has worked has been damaged. There are so many factors likely to have caused problems it is reasonable for the company to seek the most basic information, such as, plans, specifications and pictures of the damage, before it can assess its

6

liability and probably its underwriters…. The Defendant Company and Mr Dickson have mechanisms available to obtain the information and bearing this in mind the difficulties and responsibilities that may accrue in this area, Mr Dickson must take and must also satisfy the insurer that he has taken every step to gather and put before the insurer the information on which it can make an informed assessment of its risk.”

Napier Discount Meats Ltd v Commercial Union General Insurance Company Ltd (1993) 7 ANZ Insurance Cases 61-60 No term can be implied2 into a policy of insurance, as a condition precedent to liability, requiring the insured to lodge a completed claim form giving the information requested therein. AMP Fire and General Insurance Company Ltd v Collie (1991) 6 ANZ Insurance Cases 61-182 Where there has been reasonable cooperation by the assured, but the information obtained is scanty, the insurer must make the best estimate he or she can for the amount of the loss suffered on the material available. This case was applied in the Napier Discount Meats case.

Akai Pty Ltd V Peoples Insurance Company Ltd [1996] 8CA 39 In this case the majority of the High Court made an “off the cuff” comment concerning Section 54 of the Act after mentioning the Ferrcom decision. Their Honours said; “If the act or omission is not of a type which could cause or contribute to a

loss, but nevertheless causes prejudice to the insurer (for example, one may suppose by making investigation of a claim more difficult3), the insurer may reduce its liability in respect of the claim by an amount which fairly represents the extent to which the interests of the insurer were prejudiced.”

This is the only High Court pronouncement of which I am aware concerning the effect of making claims investigation problematic in the context of section 54(1). In Ferrcom Pty Ltd v Commercial Union Assurance Co of Australia Ltd (1993) 7 ANZ Insurance Cases ¶61-156; (1993) 176 CLR 332, in a case concerning whether Crane Policy A or Crane Policy B would apply, the High Court observed that prejudice under s 54(1);

``will consist in the existence of a liability which, in whole or in part, would not have been borne by the insurer if the act had not been done or the omission had not been made''.

The Ferrcom case supports the test of “lost opportunity”. I think failure to cooperate denies the ability of an insurer adequate ability to decide if it should to pay a claim having regard to the relevant onuses. By denying reasonable assistance an insured denies to an insurer the ability to investigate the validity of the claim event and/or the policy inception which might be viewed as relevant to as the determination of an “existence of the 2 As is clear from L’Union an express term could do so. 3 My underlining.

7 liability under the policy” in the sense that cover ought not to be “borne” by reason of prejudice to the fair operation of the insurers decision making process. If so the claim ought to be payable for a nil amount. 1.5 COOPERATION OVERVIEW The harsh reality, whether you look at section 54 in isolation or if you link it to section 13 is that the insurer must, to reduce the claim, in accordance with the words of the section prove:

“an amount which fairly represents the extent to which the interests of the insurer were prejudiced.”

An amount means money and this is hard to do. The good old days of claim refusal for failure of condition precedent are long gone. If the insured proves Policy, Event and Loss to the satisfaction of a judge, the fact that he or she has told your investigator to place their dictation machine where the sun does not shine will not help you. They are likely to win their case unless you can knobble them in some way. To have a remedy under section 54 you must prove prejudice. I think you can reduce a claim to nil only if you have enough mud to make a court suspect the bona fides of the claim. In effect, to make something of your prejudice you must raise doubt as to whether there has, indeed, been proven Policy, Event and Loss and claim a loss of opportunity to deny the claim on some other basis such as fraud.

• What information can we compel the insured to provide with regard to any alibi/witness o The best particulars that the circumstances permit.

o The full name of the alibi witness (if known).

o The address of the alibi witness (if known).

o The contact details of the alibi witness (if known).

o If these details are not known an explanation as to why the information is not

known.

o A statement to the effect that the alibi refuses to permit this information to be provided to the insurer is, in my view not good enough – this is not a Privacy Issue.

• What information can we record if witnesses are reluctant to provide a

statement?

o As much information as you can with, hopefully, much of it in “first person speech”.

• Will these hold up?

8

o It depends entirely on what you are attempting to prove. If you are attempting to get into evidence, evidence that can only be given by the witness who refuses to attend then the best diary notes and even a voice recording of what the witness is saying will be utterly useless – it cannot be admitted into evidence.

o If, however, you are recording the fact of a failure to co-operate then the

fact that you believe the witness knows something of importance, has an ability to prove your point and cannot obtain assistance all may be relevant.

2.1 FORENSIC EVIDENCE MOTIVE AND ONUS

• An increasing number of suspected staged accident claims seem to have a strong forensic report, but are deficient in opportunity and motive.

• Are there other enquiries we could we have explored? • Any new trends? • Is it reasonable to expect that we will be able to determine the motive? • What other options are available to us?

o Allege that the insured has failed to establish that an ‘event’ (as defined by the policy has occurred) has occurred?

o Other options? 2.2 SUMMARY Some decades ago it became popular when training fire investigators to explain to them that they should search for arson, opportunity and motive before having a person charged for having committed the crime of arson. A triangle is a very good way to display a clear message and in the field of arson triangles have proliferated so that they include air, heat and fuel to explain the combustion process and detection, investigation and prosecution to explain the overall process. When one looks at an equilateral triangle explaining what is to be proven one quickly gains the impression that each of the three points is as strong and significant as the other. This might rapidly lead to one concluding that a defence cannot be made out or an allegation cannot be made without the existence of one of the three significant pillars. The real world is, however, more complex. In the following I make some general comments concerning the onus of proof in civil fraud cases and then focus upon issues of motive. What an insured needs to prove is at 1.2 above. At court, in respect of the matters that the plaintiff insured must prove, he bears both a legal and evidential burden. Though evidential burdens may shift the legal burden always remains with the plaintiff insured. At the close of evidence the onus is upon the plaintiff insured to prove the above matters. This onus must be satisfied before consideration of any of the defences raised. If the plaintiff fails that is the end of the matter, see Simon v NRMA Insurance Limited, NSW Court of Appeal (unreported) 22 October 1991, Nasa v AAMI (CANSW No. 40253) (unreported) 22 October, 2001, To v Australian Associated Motor Insurers Limited

9 (2001) B VR 279 and Hammoud Bros Pty Limited v Insurance Australia Limited [2004] NSWCA 366.

In Vidal v NRMA Insurance [2004] NSWSC 123 (5 March 2004) Master Harrison, as she then was, was dealing with an appeal from a Magistrate in which a defence of fraud had been raised. At paragraph 10 the Master stated:

“The Magistrate correctly stated that the plaintiff must prove on the balance of probabilities that her vehicle was stolen and that the defendant must prove fraud on the balance of probabilities in the manner formulated in Briginshaw v Briginshaw [1938] HCA 34.”

This statement which was recently repeated with approval by Hall J in Daoud v GIO General Limited [2011] NSWSC 1001 (1 September 2011). On the actual appeal from the Master

On appeal from the decision of the Master Handley JA in Vidal v NRMA Insurance [2005] NSWSCA 390 in a succinct judgment which was approved of by Mason P and Brownie AJA said:

“Sometimes an insurer simply puts the insured to proof without having a positive case. At other times, such as here, the insurer may have a positive case, what may be described as a negative pregnant. An insurer is fully entitled to run a positive case, without undertaking anything more than an evidentiary burden of displacing the plaintiff’s prima facie case.”

The fact that the insured plaintiff must establish a prima facie case the elements of which are set out above is significant not only for the way it may effect the operation of a particular piece of litigation but goes to the heart of how insurance is underwritten and insurance claims investigated.

At the time a policy of insurance is effected and arranged an intending insured is asked questions but is not required to prove that the answers to those questions are true. When a claim is investigated, however, the insurer is entitled to ask questions relating to and to obtain information upon all of the matters that a plaintiff insured must prove which thus entitles an insurer, for example, in a motor vehicle collision case to ascertain whether or not the plaintiff insured had a criminal record. The issue of a criminal record does not relate to issues of causation concerning the accident but rather relates to issues as to whether or not a valid policy of insurance existed as it may be that at the time of making and processing the claim in respect of the car accident that the insurance company will find out that had it known the true situation that it would never have issued a policy of insurance at all.

In short, the ability of an insurer to put the insured plaintiff to proof so as to establish a prima facie case is extremely significant in so far as the way insurance claims are managed and, were it otherwise, pre-policy investigation issues would give rise to enormous expense.

THE FRAUD ONUS

Once the Court is satisfied that the plaintiff has established a prima facie case the defendant must satisfy a burden if it has raised a defence. At this point if that defence raises a matter of serious misconduct such as the commission of fraud or arson then

10

the standard of proof that the defendant must meet is still the civil standard of balance of probabilities but the Court should proceed with added care before finding fraud. In general courts rely upon the general statement of principle set down by Justice Dickson in Briginshaw v Briginshaw (1938) 60 CLR 336 at page 361 as modified by the more recent re-statement of Justices Brennan, Dean and Gaudron in Neat Holdings Pty Ltd v Karajan Holdings Pty Ltd (1992) 67 ALJR 170 at 170, 171 where it was said:

“The ordinary standard of proof required of the party who bears the onus in civil litigation in this country is proof on the balance of probabilities. That remains so even where the matter to be proved involves criminal conduct or fraud. On the other hand, the strength of the evidence necessary to establish a fact or facts on the balance of probabilities may vary according to the nature of what is sought to prove. Thus, authoritative statements have often been made to the effect that clear or cogent or strict proof is necessary “where so serious a matter as fraud is to be found.” A statement to that effect should not, however, be understood as directed to the standard of proof. Rather they should be understood as merely reflecting a conventional perception that members of our society do not ordinarily engage in fraudulent or criminal conduct and a judicial approach that the Court should not likely make a finding that, on the balance of probabilities, a party to civil litigation has been guilty of such conduct… There are, however, circumstances in which generalisations about the need for clear and cogent evidence to prove matters of the gravity of fraud or crime are, even when understood as not directed to the standard of proof likely to be unhelpful and even misleading.”

Cases are generally litigated when the evidence in respect of a particular proposition is not clear. If there is CCTV footage of an insured setting fire to a car then it can be established that the insured set fire to the car and questions of motive become irrelevant.

Generally however, cases in this area involve the inference that something did or did not occur and are themselves therefore cases involving circumstantial evidence.

A general statement as to circumstantial evidence of some use was made by the High Court in Luxton v Vines (1955) 85 CLR 352 at page 358 where Their Honours adopted an earlier statement of the Court and said:

“…As far as logical consistency goes many hypotheses may be put which the evidence does not exclude positively. This is a civil and not a criminal case. We are concerned with probabilities, not with possibilities. The difference between the criminal standard of proof in its application to circumstantial evidence and the civil is that in the former the facts must be such as to exclude reasonable hypotheses consistent with innocence, while in the latter you need only circumstances raising a more probable inference in favour of what is alleged. In questions of this sort, where direct proof is not available, it is enough if the circumstances appearing in evidence give rise to a reasonable and definite inference:

They must do more than give rise to conflicting interests of equal degrees of probability so that the choice between is a mere matter of conjecture: see per Lord Robson “Richard Evans & Co v Astley” (1911) AC 674 page 687. But if circumstances are proved in which it is reasonable to find a balance of probabilities in favour the conclusion sought then, though the conclusion

11

may fall short of certainty, it is not to be regarded as a mere conjecture or surmise.”

Commonly in cases of this sort there are a set of circumstances suggesting that one outcome is more probable than the other. The way of dealing with sets of circumstances was discussed by Mahoney JA in Seymour v Australian Broadcasting Commission (1990) 19 NSWLR 219 particularly at 232-234. A summary of His Honour’s judgment on this issue might be stated as follows:

(a) The circumstantial matters are to be treated cumulatively. It is incorrect to examine each circumstantial matter individually in order to see whether it is capable of innocent explanation alone.

(b) The tribunal should consider the circumstantial matters against the tribunal’s experience of the world in considering whether inferences from these matters, as sought to be drawn by the defendant, add to the proof of fraud.

(c) It is important, in the testing of circumstantial evidence, to consider whether there is any evidence inconsistent with the guilty inference, that is, whether the plaintiff’s conduct, or any of the facts are not merely consistent with innocence, but inconsistent with guilt.

Dicta to a similar effect appears in the judgment of the Court of Appeal of the Supreme Court of Victoria in Transport Industries Insurance Company v Longmuir (1997) 1 VR 125 at 129, 129 where Winneke P said:

“in cases of circumstantial evidence each proven fact may gain support from the others, although each, considered in isolation, might not provide a sound basis from which to draw that inference. The onus of proof is only to be applied at the final stage of the reasoning process. It is erroneous to divide the process into stages …”

At 141 Tadgell JA said:

“The overall effect of the detailed picture can sometimes be best appreciated by standing back and viewing it from a distance, making an informed, considered, qualitative appreciation of the whole. The overall effect of the detail is not necessarily the same as the sum total of the individual details.”

MOTIVE

The proof of a sufficient motive is not a requisite for the success of a defendant in any case in which fraud is alleged.

In AMP Fire and General Insurance Company Limited v Collie (1991) 6 ANZ Insurance Cases 61-082 at 77,282 Teague J of the Supreme Court of Victoria cited with approval what was said by Viscount Tilhorne in Onassis and Calogeropoulos v Vergottis [1968] 2 Lloyds Rep. 403 at 415:

“Where a motive for dishonesty is established, it assists in determining whether there has been dishonesty in fact, but seldom, if ever, is the proof of motive essential to establish dishonesty or fraud.”

12

In the decision of the New South Wales Court of Appeal in Rama Furniture Pty Limited v QBE Insurance Limited, 20 June 1986, unreported, Kirby P said in his judgment at 18, 19:

“Like Rogers J. I was in doubt as to whether the evidence establishes that the Arnolds had a motive. There is evidence both ways. Its interpretation is uncertain. But the failure of the respondent (defendant) to establish affirmatively that the Arnold’s had a motive can only be a minor consideration in judging the probabilities about the commencement of the fire. The evidence does not exclude the possibility of a motive. The presence or absence of motive will often be difficult to prove because of the limitations which trials necessarily place upon the exploration of the complex, financial, personal and even psychological considerations effecting human conduct. It certainly cannot be said that the evidence was left in such a state that it was established that the appellants had no conceivable motive for commencing the fire. Nor can it be said that all of their conduct belies the existence of such a motive. Some of it supports the theory of motive, some is equivocal and some (especially the under insurance) points in the opposite direction. It is therefore necessary to pass to other considerations. But it is to overstate the appellant’s case to conclude that the failure of the insurer to establish motive by positive evidence, in some way destroys the insurer’s defence, if it can be made out otherwise. In such a circumstance, it will be concluded that although the motive could not be provided, it must have existed because it is demonstrated by objective facts.”

In the final two sentences of that statement the president was, in effect, restating the point made out concerning CCTV footage above, namely that there must have been a motive because it is demonstrated by the fact that the act was done.

In McHugh v NRMA Insurance Company Limited [1996] NSWSC 315 an appeal was made to the court of appeal against a verdict in favour of an insurer upon the basis that no motive for the commission of fraud had been established. The court upheld the trial judge’s decision even though no motive for the fraud had been established and no motive for the fraud was referred to in the court’s conclusion.

In summary, though the existence of a clear and established motive may assist a court in determining that one set of events is more likely than another it is not essential to a finding of fraud or indeed any finding that a motive exists. Further, motive on its own can never be sufficient to prove fraud Dominion Trust Company v New York Life Insurance Company (1918) 3 WWR 850 per Lord Dunedin at page 84.

In determinations of the financial ombudsman there are often paragraphs to the following effect:

“A. The FSB bases its allegation of fraud substantially upon the applicants……….

B. An allegation of fraud is a serious allegation. If established, it has major impact on an individual’s ability to obtain the insurance and in some circumstances, finance. In view of the significance of the allegation, it is important that the evidence provided by the FSB is clear and cogent evidence. An allegation will not be satisfied by inexact proofs, indirect testimony or speculation. Whilst the onus on the FSB before the

13

Ombudsman is not the same as the onus before a court, nevertheless the Ombudsman is guided by the principles laid down by the courts. The FSB will normally need to produce evidence of motive, opportunity, character and credibility, supported by expert evidence where appropriate.”

The above statement, as a general statement of principle, is unarguably correct.

It is, however, one that may give rise to error if it leads to a situation in which the Ombudsman in a suitable case would fail to find fraud simply because the motive for committing the fraud cannot be established.

People do things for a variety of reasons and in cases involving an allegation of fraud it is unlikely that the person who has committed the fraud will divulge their true circumstances and explain why they chose to commit the fraud.

As stated by President Kirby it is often, therefore, difficult to establish motive and the ombudsman, court or tribunal should have regard to all of the evidence to determine whether an event has, or has not, occurred.

3.1 EVIDENCE ISSUES

• VOIP and other smart phone communication apps • GPRS, IMEI and URL’s etc • E Tags – a significant resource • CCTV – increased retention. • Seizure of devices

Problems posed by VOIP and other smart phone communication apps In July of 2012 the federal Attorney General’s department released a discussion paper entitled “Equipping Australia Against Emerging and Evolving Threats” which relates to proposals to amend telecommunications and national security legislation and currently there is an inquiry being run by the Parliamentary Joint Committee on Intelligence and Security to see if telecommunications organisations should be required to keep for a period of one, two or five years data that passes through telecommunications systems when one device links to another. Currently there is information that is available to and utilised by telecommunications providers that is essential to the operation of the telecommunications network but which is not recorded and is therefore not available for subsequent investigation. Take, for example, your telephone’s International Mobile Equipment Identity. Your telephone’s IMEI number is used by a GSM network to allow it to make calls and the IMEI can be used in real time to locate the physical position of the phone with great accuracy if the phone is switched on. The IMEI which can be located on your device by dialling *#06# lies at the heart of a number of Smartphone apps which can be used to trace the phone, or if it is stolen, to either locate it or to remotely wipe it off its contents or place a remote password control over it. If you get access to another person’s mobile telephone even for a very short time you can access the IMEI, set up global surveillance on it and track it forever. When you request that the phone be tracked you will receive an SMS confirming that the phone is now being tracked by another person. Wipe the received SMS from the phone

14 and the owner of the phone will be none the wiser unless they use data retrieval on the phone to discover deleted and erased messages. For present purposes, however, retention of IMEI data would enable reconstruction of past positioning of a phone so that one could, over, say, a 24 hour period plan a complete route of precisely where that phone had travelled within a degree of accuracy of less than a couple of metres. The fact is, however, that IMEI data is not recorded and access to IMEI information is therefore only relevant to police officers conducting current surveillance of a particular subject or, alternatively, to people who have had their phone stolen. Going back to the current Smartphone I think it is fair to say that most criminals will remember why they were found guilty and what evidence caused them to go to jail. Any criminal convicted by evidence as to position based upon the use of a telephone will, no doubt, have thought long and hard about how they might be able to communicate in a way that does not leave a trace. It is developments in this area of untraceable communication that have got security forces worldwide hot and bothered as the reason for secrecy may range from personal preference or a privacy issue such as concealing an affair to making decisions as to the best way to blow up parliament. Currently if one cell phone makes a telephone call to another cell phone then permanent records for billing purposes are kept by telecommunications providers at a number of levels and the fact that a call was made can be traced for seven years and the available date can also indicate the position from which the actual call was made with a fair degree of accuracy. If, however, the maker of the communication uses the Smartphone in a different way to communicate then the traceability of and the recording of information concerning the communication will vary depending upon the services utilised and whether or not billing or connection information in relation to them is recorded. If you have a data package attached to your telephone most telecommunication providers do not record the URL’s (Uniform Resource Locators) of the device that you have contacted. They merely record the amount of data that passed in or out of your device through the system with a view to charging you for the amount of data received. The Telco providers can, however, record what URL’s were visited and, for example, on 26 June 2012 there was an article in www.itnews.com.au whereby Telstra confirmed that it had been capturing web addresses visited by millions of subscribers on its Next G network for the purpose of releasing an as yet unreleased feature called “Smart Controls” that would allow users to access mobile internet browsing restrictions and call restrictions on Telstra mobile services. Currently if you have a Telstra or Vodafone service and use your telephone to access database information it is likely that this will be reflected in your bill by the fact that you have been charged for having a data pack. There will, however, be no record of how much data passed through any particular call or visit to a website. If I issue a subpoena to Telstra or Vodafone for all details of incoming and outgoing calls it is likely that I will, in relation to access to the internet, locate calls bearing the reference GPRS which indicates that the phone has used the general packet radio service which is a mobile data service used on the 2G and 3G cellular communications systems to get data. I will not, however, be able to find out who you called but may, if I am lucky, be able to issue a subpoena, telephone a recipient to see if they have also incurred data charges at the same time as most such apps use both ingoing and outgoing data so that if there is, for example, a

15 Skype telephone call between two hand-held mobiles that both will incur a data charge at the same time. The big question is, however, as to whether data communications can be made without the incurring of a data charge. A very commonly used application is viber which enables phone calls and text messages to be made to any other viber users for free. On the website www.viber.com the statement that calls are “free” is modified by the statement which says:

“when you use viber on a 3G network you might incur operator data charges or internet access fees.”

If, however, you have a viber connection with another viber phone and you both disable 3G access then, as I understand it, the fact that one telephone contacted another telephone will not be recorded. There are literally hundreds of such applications available. Some of them, like viber, mimic the normal telephone system while others such as Heytel act more like a CB radio sending SMS and voice messages and other such as WhatsApp send text messages. Even Face Time and some MMS are untraceable. For present purposes I think that it is fair to say that any individual with a concern for their privacy with a basic knowledge of some of these applications will be able to communicate in a way that would make it impossible for you to determine what communications they have, or have not, made using that device and that information obtained from telephone and other records will not assist your enquiry. What to do? It is probably worthwhile opening this up for discussion but as a practical matter I think that it is worthwhile undertaking the following: 1. Attempt to determine what data pack the phone uses.

2. When your investigator interviews the insured get the investigator to physically look

at the phone, find out what apps are on the phone and in relation to any of the communication apps ask for the phone to be opened so that the investigator can be taken to messages to see if communications on days of interest or to persons of interest have been recorded.

3. The fact that there has been a refusal to allow access to the telephone may be

significant if the case is litigated and, in particular, if access to the telephone is requested on discovery.

In Palavi v Radio 2UE Sydney Pty Limited [2011] NSW CA 264 the NSW Court of Appeal examined an earlier judgment in respect of which a statement of claim in defamation had been struck out because a person had failed to produce their telephone for discovery and it appeared that they had in fact destroyed one earlier telephone to wipe the data from it. This then leads to what the future may hold in respect of such litigation which would involve not only the discovery of and examination of relevant mobile telephones but using IMEI data, if it becomes recorded, for the purpose of determining that it was that particular

16 physical phone that made the particular telephone calls or made access with the computer on the day in question. I would be able, with IMEI data, to say that a particular phone was used to make a particular call regardless of what SIM card was in the phone at the time and if, for example, the phone was used to send and retrieve SMS messages or if it was used with viber. A number of private investigators and agencies now advertise that they are able to recover information from mobile telephones and given the amount of storage space on such devices it seems extremely likely that data would be, for a considerable period of time, recoverable. There are a number of programs such as old classics such as File Scavenger which operate on the premise that when a person with a computer “deletes” an item that they merely remove the restriction on that part of the storage device which preclude recording over the data that was saved. Most devices have, however, a predilection for storing data on “clean” or “unused” storage space so that data remains for many years capable of being recovered through appropriate programs. Such data exists in a variety of places and one very good one is a standard photocopier where the copier has storage and abilities to receive faxes and other communications. A modern photocopier or document centre may keep hundreds of thousands of old documents in its storage system. CCTV – INCREASED RETENTION Old CCTV utilised video. Now most utilise digital storage. Furthermore the amount of digital storage available is increasing rapidly and many businesses retain much longer periods of CCTV coverage than was previously the case. As a consequence it’s probably a more significant area of examination than it was in the past. E-TAGS – SAFETY CAM For some providers an e-tag contains a transponder chip which triggers a device which bills the e-tag account when the device is driven through a collection point and the triggering of the device stops a camera from taking a photograph of the number plate. For others, all are photographed but only some billed. With some e- tag providers you cannot determine what vehicle went through the collection point. With some you can. It is important in examining a person’s version of events to see if they or their vehicle ought to have travelled through the e-tag collection points particularly as there is the possibility that you will be able to get a photograph of a number plate matching the transaction. The difficulty with this sort of exercise is that there are a number of separate and distinct e-tag providers with different systems.

17 Session 2 - With some of our ‘newer’ IROs – Max 1 hour starting at 1pm Fraud ‘102’ (slightly more advanced than 101)

• General Principles when dealing with the ICA • Discuss the 'balance of probabilities' and the standard of proof required to

determine whether there is sufficient evidence to substantiate a fraud allegation and;

• the Briginshaw test and the standard of the evidence required of fraud allegations • The concept of a ‘breach’ of ICA and the resultant ‘remedy’ as it relates to s56

PART 1 – ONUS WHO PROVES WHAT? An insured seeking to claim against an insurer must prove and an insurer may therefore legitimately investigate whether: 1. There was a valid contract with the insurer at the time of an event. 2. An event insured under the contract has occurred. 3. The insured has suffered loss as a proximate cause of the insured event.

I call this Policy, Event and Loss. Generally, if there is litigation:

• the insured must prove the insurers non payment amounts to breach of contract and/or

• the insurer must prove any exclusion – including exclusion by reason of fraud. If you are investigating a claim it is important to know what the contract says about the insured’s duty to cooperate. Can an insured refuse to undergo a record of interview and instead rely upon answering written questions put to his solicitor? Why do they have to hand over telephone records? Can they withhold them? It depends upon the policy, the nature of the claim and who is answering the question. In a dispute a judge or arbiter such as FOS will generally look first at the contract to see what it says before deciding if the duty to cooperate under the contract has been breached. Many policies are unclear about the extent of the duty. PART 2 – FRAUD – ICA FRAMEWORK There are remedies for fraud contained in Sections 28 and 56 of the ICA. Section 28 lies within Division of Part IV of ICA and provides the remedy for fraudulent non-disclosure and misrepresentation at policy inception. Section 56 is contained within Part VI of the Act and deals with fraudulent claims. The logic is – step 1 get the policy s.28 – step 2 make a claim s.56. Remember – policies are renewed. Other sections apply so as to re –apply to the renewal the original duty of disclosure and to not make misrepresentations.

18 Section 28 provides a remedy for non-disclosure and misrepresentation. In a policy of insurance the insurance company is, like a bookie, taking on a risk and there are many factors which may or may not influence its decision to accept that risk. Misrepresentation occurs when the insured is asked a question about a material matter and gives an incorrect answer. Non-disclosure occurs when the insured despite an obligation to provide the insurance company with material information keeps silent or otherwise fails to disclose the truth so that the insurance company acts without knowledge information. Note my use of the word “material”. See below. Materiality is critical to section 28. For section 56 the fraud needs to not be “minimal or insignificant” As a practical matter at the time a policy of insurance is effected and arranged the insurance company asks an intending insured a series of questions. The fact that it asks those questions almost invariably leads a Court to conclude that the answers to them are matters that are material to the contact – even when they might in fact be irrelevant. At the same time, depending the nature and class of the risk the insured may be under an obligation to provide disclosure. The duty of disclosure has fairly limited application in relation to policies of motor vehicle insurance by operation of Section 21A of ICA. This section applies to “eligible contracts of insurance”. It applies to domestic and motor vehicle policies that you will encounter. The section essentially waives compliance with a general duty to disclose information unless the insurance company asks specific questions and raises specific areas of non-disclosure for consideration. This is not easy to do. The effect of Section 21A is to reduce the occurrence of “non-disclosure” largely to situations where a direct question is put and the insured fails to answer or provides an obviously incomplete answer and, in most cases, the failure of the insured to answer or to provide an incorrect or incomplete answer would, under normal law, be regarded as a misrepresentation. Take, for example, the underwriting question: “Have you had your license suspended or cancelled in the last 3 years?” If your license was cancelled as a result of an accrual of points two years ago then the answer: (i) “No” is incorrect and may be false. [Not false if the licence holder didn’t know].

(ii) The answer “I don’t know” even if deliberately untrue, because the insured does

know, will generally, by itself, never be regarded as false as you’d never prove otherwise, even if a reasonable person in their position would have remembered whether they did, or did not, lose their license within the 3 year period.

Rather than get involved in the intricacies of Section 21A and non disclosure I simply note that you must, in general, focus your interest upon actual misrepresentations and not bother with non-disclosures unless the area was specifically raised – which will be rare.

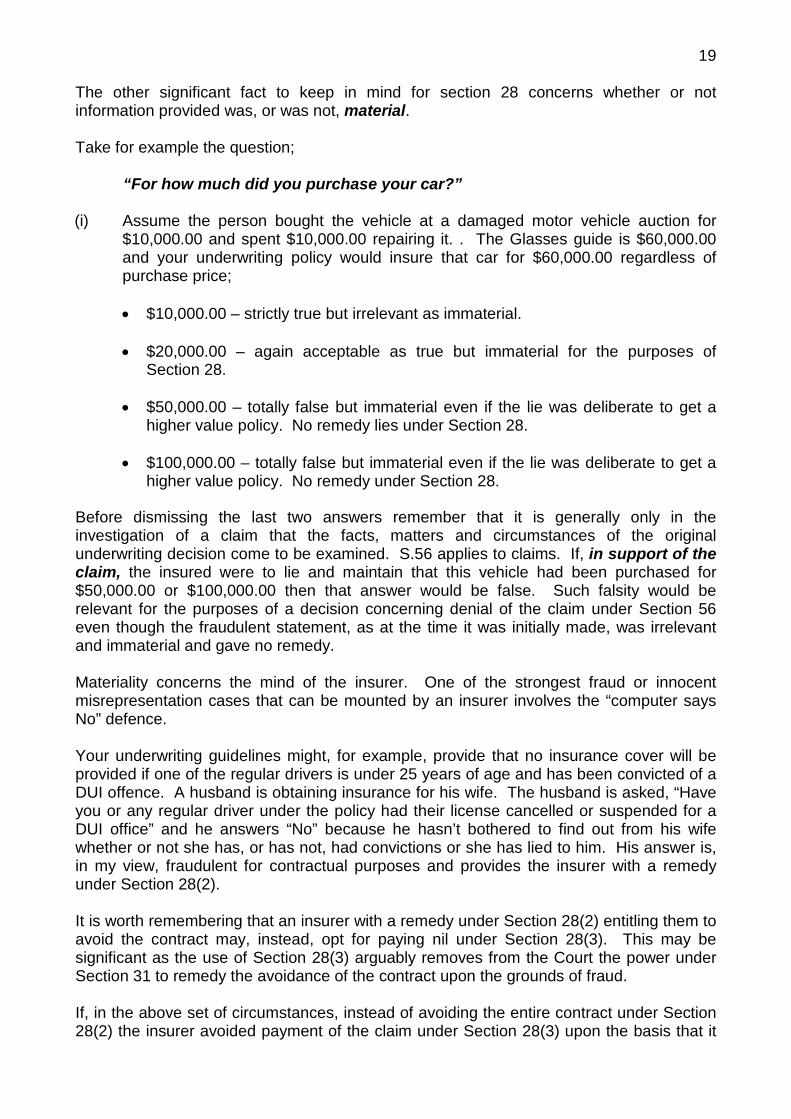

19 The other significant fact to keep in mind for section 28 concerns whether or not information provided was, or was not, material. Take for example the question; “For how much did you purchase your car?” (i) Assume the person bought the vehicle at a damaged motor vehicle auction for

$10,000.00 and spent $10,000.00 repairing it. . The Glasses guide is $60,000.00 and your underwriting policy would insure that car for $60,000.00 regardless of purchase price; • $10,000.00 – strictly true but irrelevant as immaterial.

• $20,000.00 – again acceptable as true but immaterial for the purposes of

Section 28. • $50,000.00 – totally false but immaterial even if the lie was deliberate to get a

higher value policy. No remedy lies under Section 28. • $100,000.00 – totally false but immaterial even if the lie was deliberate to get a

higher value policy. No remedy under Section 28.

Before dismissing the last two answers remember that it is generally only in the investigation of a claim that the facts, matters and circumstances of the original underwriting decision come to be examined. S.56 applies to claims. If, in support of the claim, the insured were to lie and maintain that this vehicle had been purchased for $50,000.00 or $100,000.00 then that answer would be false. Such falsity would be relevant for the purposes of a decision concerning denial of the claim under Section 56 even though the fraudulent statement, as at the time it was initially made, was irrelevant and immaterial and gave no remedy.

Materiality concerns the mind of the insurer. One of the strongest fraud or innocent misrepresentation cases that can be mounted by an insurer involves the “computer says No” defence. Your underwriting guidelines might, for example, provide that no insurance cover will be provided if one of the regular drivers is under 25 years of age and has been convicted of a DUI offence. A husband is obtaining insurance for his wife. The husband is asked, “Have you or any regular driver under the policy had their license cancelled or suspended for a DUI office” and he answers “No” because he hasn’t bothered to find out from his wife whether or not she has, or has not, had convictions or she has lied to him. His answer is, in my view, fraudulent for contractual purposes and provides the insurer with a remedy under Section 28(2). It is worth remembering that an insurer with a remedy under Section 28(2) entitling them to avoid the contract may, instead, opt for paying nil under Section 28(3). This may be significant as the use of Section 28(3) arguably removes from the Court the power under Section 31 to remedy the avoidance of the contract upon the grounds of fraud. If, in the above set of circumstances, instead of avoiding the entire contract under Section 28(2) the insurer avoided payment of the claim under Section 28(3) upon the basis that it

20 would never have issued the policy of insurance had it known the truth after treating the husband’s statement as “innocent” this removes from the Court the ability to, in effect “forgive” the husband for his incorrect answer. PART 3 – FRAUD - WHAT IS IT? Under our law there are three different types or categories of “fraud”. These are: • equitable fraud; • Common Law contractual fraud; and • criminal fraud. To investigate insurance claims you need to know about Common Law fraud. Common Law - Contractual Fraud The classic definition of this sort of fraud was laid down by the common lawyers who spoke in Derry v Peek (1889) 14 App Cas 337 in which Lord Hershel said:

“First in order to sustain an action of deceit, there must be proof of fraud, and nothing short of that will suffice. Secondly, fraud is proven when it is shown that a false representation has been made (1) knowingly or (2) without belief in its truth or (3) recklessly, careless whether it be true or false. Although I have treated the second and third as distinct cases, I think the third is but an instance of the second for one who makes a statement under such circumstances can have no real belief in the truth of what he states.”

Common law contractual fraud therefore encompasses a false representation made by a person: • Who knows that what they have said is false – i.e. akin to criminal fraud

OR • Who is reckless or careless about whether the representation is true. Fraud of the type dealt with by the ICA occurs when a positive untrue representation of some fact, matter or circumstance is made in a situation where the maker of the statement either deliberately knew that it was false when they made the statement OR the maker of the statement made it recklessly with indifference as to the truth of the representation. Some judges, and at times FOS, have taken the view that to be “fraudulent” in the insurance context that a representation must:

• Be made with an intent to obtain financial benefit OR • Be relevant to the claim; that is, to the insured event OR • Give rise to prejudice.

I think such judges and panel members have been wrong. They are implying in to the civil context notions applicable to criminal fraud. To me reckless = reckless. If you look at Lord Herschel’s tests 2 and 3 you don’t see a whiff of “guilty mind” in either. You see that a positive assertion upon the part of someone plus sloppiness as amounting to fraud in a contractual context.

21 There is, however, a line to be crossed. Not every lie is material or relevant. You must appreciate that due to the high onus in proving fraud that catching someone out in a lie in one part of the claim does not automatically catch them out overall see Insurers Manufacturers of Australia Ltd v Heron (2006) 14 ANZ Ins Cas 61 – 1669. On the upside, in Alexander Raymond Walton v The Colonial Mutual Life Assurance Society Limited [2004] NSWSC 616 (19 July 2004), Einstein J, said

The test for fraud is satisfied if the insured has a dishonest intent to induce a false belief in the insurer for the purpose of obtaining payment or some other benefit under the policy. As such, where the insured makes a false statement with knowledge in a claim to induce the insurer to meet the claim, the claim is made fraudulently. The fraudulent statement need not be material to the insured’s claim nor is the insured absolved of any responsibility by asserting that he considered his claim to be valid. It is not necessary to show prejudice as having been suffered by the insurer for s 56 to be relied upon. The only restriction upon an insurer’s right to refuse payment of the claim is the discretion granted within s 56(2) of the Insurance Contracts Act.

Though Einstein J was considering category 1 “knowing” fraud he spells out that fraud under the Act need not be “material” and that the insurer need not show “prejudice” In making his finding his honour specifically referred to Tiep Thi To v Australian Associated Motor Insurers Ltd [2001] VSCA 48; (2001) 3 VR 279; This is a most important case. In 1997 To invented a false story. A magistrate held that she had made false statements as a result of a mistaken belief. He held her claim to be not “fraudulent” within the meaning of section 56 as she had always been entitled to make a “truthful” claim. Justice Mandie of the Victorian Supreme Court, disagreed. He stated at paragraph 16 of his judgment:

“If a person knowingly makes false statements believing that they have an invalid claim in order to mislead the insurer into believing that they have a valid claim, it seems to me not to matter whether in fact the claim is valid or invalid. The claim is made dishonestly and hence fraudulently within the meaning of the Act.”

The matter was appealed to the Court of Appeal of the Supreme Court of Victoria. The leading judgment was that of Buchanan JA who expressly rejected the argument that any insured who was lawfully entitled to indemnity could not make a fraudulent claim. At paragraph 19 His Honour held:

“In my opinion if a false statement is knowingly made in connection with a claim for the purpose of inducing the insurer to meet the claim, the claim is one made fraudulently within the meaning of section 56(1). It is not necessary to analyse the false statement to determine whether or not the falsity attaches to the basis upon which the insured is claimed to be liable.”

22

DEFENDANT’S BURDEN – ONUS

Once the Court is satisfied that the plaintiff has established a prima facie case the defendant must satisfy a burden if it has raised a defence. At this point if that defence raises a matter of serious misconduct such as the commission of fraud or arson then the standard of proof that the defendant must meet is still the civil standard of balance of probabilities but the Court should proceed with added care before finding fraud. In general courts rely upon the general statement of principle set down by Justice Dickson in Briginshaw v Briginshaw (1938) 60 CLR 336 at page 361 as modified by the more recent re-statement of Justices Brennan, Dean and Gaudron in Neat Holdings Pty Ltd v Karajan Holdings Pty Ltd (1992) 67 ALJR 170 at 170, 171 where it was said:

“The ordinary standard of proof required of the party who bears the onus in civil litigation in this country is proof on the balance of probabilities. That remains so even where the matter to be proved involves criminal conduct or fraud. On the other hand, the strength of the evidence necessary to establish a fact or facts on the balance of probabilities may vary according to the nature of what is sought to prove. Thus, authorative statements have often been made to the effect that clear or cogent or strict proof is necessary “where so serious a matter as fraud is to be found.” A statement to that effect should not, however, be understood as directed to the standard of proof. Rather they should be understood as merely reflecting a conventional perception that members of our society do not ordinarily engage in fraudulent or criminal conduct and a judicial approach that the Court should not likely make a finding that, on the balance of probabilities, a party to civil litigation has been guilty of such conduct… There are, however, circumstances in which generalisations about the need for clear and cogent evidence to prove matters of the gravity of fraud or crime are, even when understood as not directed to the standard of proof likely to be unhelpful and even misleading.”

Cases are generally litigated when the evidence in respect of a particular proposition is not clear. If there is CCTV footage of an insured setting fire to a car then it can be established that the insured set fire to the car and questions of motive become irrelevant.

Generally however, cases in this area involve the inference that something did or did not occur and are themselves therefore cases involving circumstantial evidence.

A general statement as to circumstantial evidence of some use was made by the High Court in Luxton v Vines (1955) 85 CLR 352 at page 358 where Their Honours adopted an earlier statement of the Court and said:

“…As far as logical consistency goes many hypotheses may be put which the evidence does not exclude positively. This is a civil and not a criminal case. We are concerned with probabilities, not with possibilities. The difference between the criminal standard of proof in its application to circumstantial evidence and the civil is that in the former the facts must be such as to exclude reasonable hypotheses consistent with innocence, while in the latter you need only circumstances raising a more probable inference in favour of what is alleged. In questions of this sort, where direct proof is not available, it is enough if the circumstances appearing in evidence give rise to a reasonable and definite inference:

23

They must do more than give rise to conflicting interests of equal degrees of probability so that the choice between is a mere matter of conjecture: see per Lord Robson, Richard Evans & Co v Astley (1911) AC 674 page 687. But if circumstances are proved in which it is reasonable to find a balance of probabilities in favour the conclusion sought then, though the conclusion may fall short of certainty, it is not to be regarded as a mere conjecture or surmise.”

Commonly in cases of this sort there are a set of circumstances suggesting that one outcome is more probable than the other. The way of dealing with sets of circumstances was discussed by Mahoney JA in Seymour v Australian Broadcasting Commission (1990) 19 NSWLR 219 particularly at 232-234. A summary of His Honour’s judgment on this issue might be stated as follows:

(d) The circumstantial matters are to be treated cumulatively. It is incorrect to examine each circumstantial matter individually in order to see whether it is capable of innocent explanation alone.

(e) The tribunal should consider the circumstantial matters against the tribunal’s experience of the world in considering whether inferences from these matters, as sought to be drawn by the defendant, add to the proof of fraud.

(f) It is important, in the testing of circumstantial evidence, to consider whether there is any evidence inconsistent with the guilty inference, that is, whether the plaintiff’s conduct, or any of the facts are not merely consistent with innocence, but inconsistent with guilt.

Dicta to a similar effect appears in the judgment of the Court of Appeal of the Supreme Court of Victoria in Transport Industries Insurance Company v Longmuir (1997) 1 VR 125 at 129, 129 where Winneke P said:

“in cases of circumstantial evidence each proven fact may gain support from the others, although each, considered in isolation, might not provide a sound basis from which to draw that inference. The onus of proof is only to be applied at the final stage of the reasoning process. It is erroneous to divide the process into stages …”

At 141 Tadgell JA said:

“The overall effect of the detailed picture can sometimes be best appreciated by standing back and viewing it from a distance, making an informed, considered, qualitative appreciation of the whole. The overall effect of the detail is not necessarily the same as the sum total of the individual details.”

SUMMARY Going back to the idea of the “line to be crossed” an understanding of these principles is of importance when investigating and dealing with fraudulent claims. This is particularly important when you consider most battles are fought in the “grey” zone between criminal fraud and category two “reckless fraud. In general if you have a good chance of proving criminal style fraud the case, unless your opponent is mad, simply goes away. The insured gives up.

24 Conversely, if you only have a mere suspicion of fraud, or the unsupported allegation of a witness who will not come forward you ought to pay the claim. The downside in running a weak fraud case is;

• You won’t win, • You won't be seen to have had the ethical ability to allege fraud, • It will cost you a lot of money to investigate, fight and lose, • You may attract adverse publicity of the Today Tonight type which may upset senior

management way up to Board level and beyond – remember senior directors have mothers,

• Your company may attract and keep a reputation with FOS and judicial officers of improperly alleging fraud when no fraud exists.

These are sins that can take years to rectify. What do you do? Take a deep breath. Before you get carried away with every “error” or slip or even a bald faced lie take in to account that human error or frailty will, generally, not amount to fraud. People make mistakes. They lie to protect friends and cover sins. In and old case Justice Kirby even said that it was in the cultural nature of some peoples to lie to investigators. In addition many mere errors, such as to what time an event happened are not, in general, representations which can be relied upon to prove fraud. Personally, I am reluctant to run or allege fraud in any case unless I can produce to a tribunal a few clear false statements that are significant in the sense that they ought not to have been made. They are not explicable for a good reason and give off an odour of evil. They are, in short, blatant lies or gross carelessness with no good reason for them having been made. Judges and FOS do not like insurers persecuting the foolish and weak but are perfectly willing to gun down liars. Getting the balance right is something of an art and depends upon your audience, the actors and, more often than you might credit, the events of the day. A good solid seeming forensic case of “the car must have been driven with your key” without motive when made against a person of good repute is pretty weak. In running such a case you run the long term risk of having that judge conclude that your forensic experts are not to be trusted. A weak or non-existent forensic case against someone who has told a number of blatant lies about even seemingly irrelevant matters, such as where he garaged the car, is far stronger. They are the plaintiff. They have the onus of proof. Destroying their credit may give you all you need. They, not you, have the primary onus. I am unwilling to run a fraud case unless a false statement is both legally material and gives off an odour of evil. Judges and FOS do not like insurers persecuting the foolish. 10.10.2012 David Courtenay