Embed Size (px)

Citation preview

SINGAPORE STOCK EXCHANGE.

PRESENTED BY:-

GROUP NO 8

GROUP MEMBERS:

Presented By:-

Farhin Ghanchi 14

Shagufta Quershi 41

Rohit Sharma 47

Namrata Singh 49

Mohit Surana 53

Chit Desai 57

INTRODUCTION

Formed on 1st Dec.1999 by the merger of the Stock Exchange of Singapore (SES) and the Singapore International Monetary Exchange Ltd. (SIMEX)

“ The SGX is the only stock exchange in Singapore. “

SGX provides trading, clearing and depository services for equities, equity options, warrants, covered warrants, bonds, loan stocks, depository receipts and derivative products.

Singapore Exchange Limited (SGX, SGX: S68) is an investment holding company located in Singapore and providing different services related to securities and derivatives trading and others. [3] SGX is a member of the World Federation of Exchanges[4] and the Asian and Oceanian Stock Exchanges Federation[5]

Singapore Exchange trades continuously from 9am to 5pm. From 1 August 2011, Singapore Exchange introduced continuous all-day trading for the securities market.[6] As a result, the lunch break, between12:30pm to 2.00pm, was scrapped.

OVERVIEW

Internationally recognised marketplace

Enjoy the prestige of being listed on an international marketplace. Join more than 200 international companies from over 20 different countries listed in Singapore since the early 1990s.

Transparent and well-regulated market

Enhance your profile as a listed company on an international exchange.

Research coverage

Expand your visibility through more than 100 research analysts and over 20 research houses based in Singapore.

Investor familiarity and interest in international companies.

Benefit from the higher trading turnover enjoyed traditionally by foreign companies listed in Singapore.

WHY SINGAPORE

SINGAPORE - ASIA'S FINANCIAL GATEWAY

Singapore is recognised today as a global financial centre. Its thriving financial services industry serves, not only a vibrant domestic economy, but the much wider Asia-Pacific region and the rest the world. Within Singapore, more than 700 local and foreign financial institutions come together to offer a wide range of products and services, contributing to the vibrancy and sophistication of the financial services scene.

Supported by a stringent but market-oriented regulatory regime, Singapore has earned international repute in many areas. As a global foreign exchange trading hub, Singapore has consistently ranked as the world’s fourth most active trading centre, after London, New York and Tokyo. It is also fast emerging as the region’s risk management centre and derivative trading hub, recording successes in Asian index futures such as the Nikkei and MSCI Taiwan index futures. Index futures in CNX Nifty (India) and FTSE/Xinhua A50 China have been added to the wide range of product offerings on the Singapore Exchange, which also includes energy and commodity derivatives.

Due to its policy of welcoming foreign companies and the available liquidity pool from international funds, Singapore is now the international capital market in Asia for the listing and trading of bonds and equities. It is also an internationally recognised fund management centre, with total assets of more than US$1.5 trillion under

management at the end of 2009, which provides ready funding support for the growth of international companies seeking to raise capital in Singapore.Resulting from its sound regulation, efficient business environment and diversity of instruments and service, Singapore is widely recognised as Asia’s financial gateway.

SGX - ASIA'S LISTING PLATFORM FOR GROWTH

As an international exchange and listing hub, Singapore has won the confidence of many global companies with foreign origins. More than 300 international companies from over 20 countries are listed on SGX, accounting for more than 40% of all equity listings. As at 30 June 2012, there are 769 companies listed with total market cap of US$662 billion.

While most of these foreign companies are from Greater China, Southeast Asia and North Asia, SGX has also listed companies from Australia, the India sub-continent, and from countries as far as Europe and North America. Apart from their diverse origins across the globe, these companies represent a full spectrum of industries covering manufacturing, transportation and logistics, finance, infrastructure and property, mining and resources, as well as various services sectors.

Although such companies have management, operations and distribution networks in various counties, SGX has provided a de facto home market for them. In fact, many of these companies have chosen

to list on SGX to establish a stronger Asian profile and presence.

With a critical mass of foreign listings, SGX is today recognised as the Asian listing hub for growth companies, supported by a well-developed research industry to reach the global investment community. This has in turn created a marketplace that captures the close attention of global investors seeking exposure into regional opportunities. With the consistent ability to attract such global funds, foreign companies will continue to find themselves well-received and traded in Singapore.

INTELLIGENT REGULATORY APPROACH

Singapore’s financial market has been built on a robust and efficient legal and judicial framework. In fact, Singapore is one of the few Asian countries with a "AAA" rating, and for the sixth year running, the Political and Economic Risk Consultancy survey named Singapore as having the best judicial systems in Asia.

Correspondingly, SGX is viewed as an efficiently regulated marketplace based on a disclosure based regime. Recognising that good corporate governance is essential to market integrity, SGX continues to lead its marketplace to the forefront of regulatory best practices. This intelligent regulatory approach is an attractive consideration for companies striving to be recognised on good corporate governance and transparency. In fact, a listing on SGX today bears a quality mark that is recognised internationally.

In its pursuit for more foreign listings, SGX has introduced listing rules that are market-oriented. These rules provide flexibility for companies with diverse backgrounds to source for public financing in Singapore. While SGX maintains its position of attracting more companies, its listing standards and the quality of listed companies are never compromised.

BENEFITS AND DRAWBACKS OF LISTING YOUR COMPANY

Going public is not an easy task. In deciding whether to seek a listing, a company should consider the alternative financing needs available and the benefits versus the drawbacks of listings.

Benefits

There are many advantages that accrue to companies that attain a public listing of their shares. Some of the key considerations and benefits are:

Creating a market for the company’s shares; Enhancing the status and financial standing of the company; Increasing public awareness and public interest in the company

and its products; Providing the company with an opportunity to implement share

option schemes for their employees; Accessing to additional fund raising in the future by means of new

issues of shares or other securities; Facilitating acquisition opportunities by use of the company’s

shares; and

Offering existing shareholders a ready means of realising their investments.

Drawbacks

While there are benefits to going public, it also means additional obligations and reporting requirements on the companies and its directors:

Increasing accountability to public shareholders Need to maintain dividend and profit growth trends Becoming more vulnerable to an unwelcome takeover Need to observe and adhere strictly to the rules and regulations

by governing bodies Increasing costs in complying with higher level of reporting

requirements Relinquishing some control of the company following the public

offering Suffering a loss of privacy as a result of media interest

As the owner or major shareholder of a private company, it is important to outweigh the benefits and costs of listing in the light of the plans and goals that have been set for the company. Discussions with lawyers, independent accountants and other professional advisors will also provide you with better considerations.

TRANSFORMING SINAGPORE.

SGX steps up Singapore stock market transformation

SGX introduced higher Mainboard admission standards as it continues the transformation of the Singapore stock market, ensuring SGX remains a competitive and relevant global exchange.

The new criteria extend market transformation to the quality of the primary (IPO) market, making it attractive for larger companies seeking to list. This builds on earlier structural initiatives in the secondary (trading) market such as the launch of Reach technology, continuous all-day trading and the reduction in minimum bid sizes.

SGX will also look to increase the proportion of IPO tranches allocated to retail investors, particularly for listings which draw high retail subscription.

New Mainboard admission criteria

Companies intending to join SGX’s Mainboard must meet one of the following quantitative requirements:

Have a market capitalisation at IPO of not less than S$150 million if they are profitable in the last financial year and have an operating track record of at least three years

Have a market capitalisation at IPO of not less than S$300 million if they only have operating revenue in the latest completed financial year.

Have minimum consolidated pre-tax profit of at least S$30 million for the latest financial year and have operating track record of at least three years;

In addition, the IPO shares issued must be at least S$0.50 each.

The new admission criteria take into account feedback and suggestions SGX received from the public consultation concluded in February 2010. The new criteria are effective 10 August 2012.

For more information on this announcement and details on the new criteria for Mainboard applicants and transitional arrangements for Catalist companies seeking to transfer to Mainboard, please click here.

For SGX-ST Listing Manual Amendments,

Methods of Listing

Primary Listing

Companies must meet SGX’s initial listing requirements outlined below for either a Mainboard or Catalist listing.

After listing, companies have to comply with all SGX’s continuing listing obligations

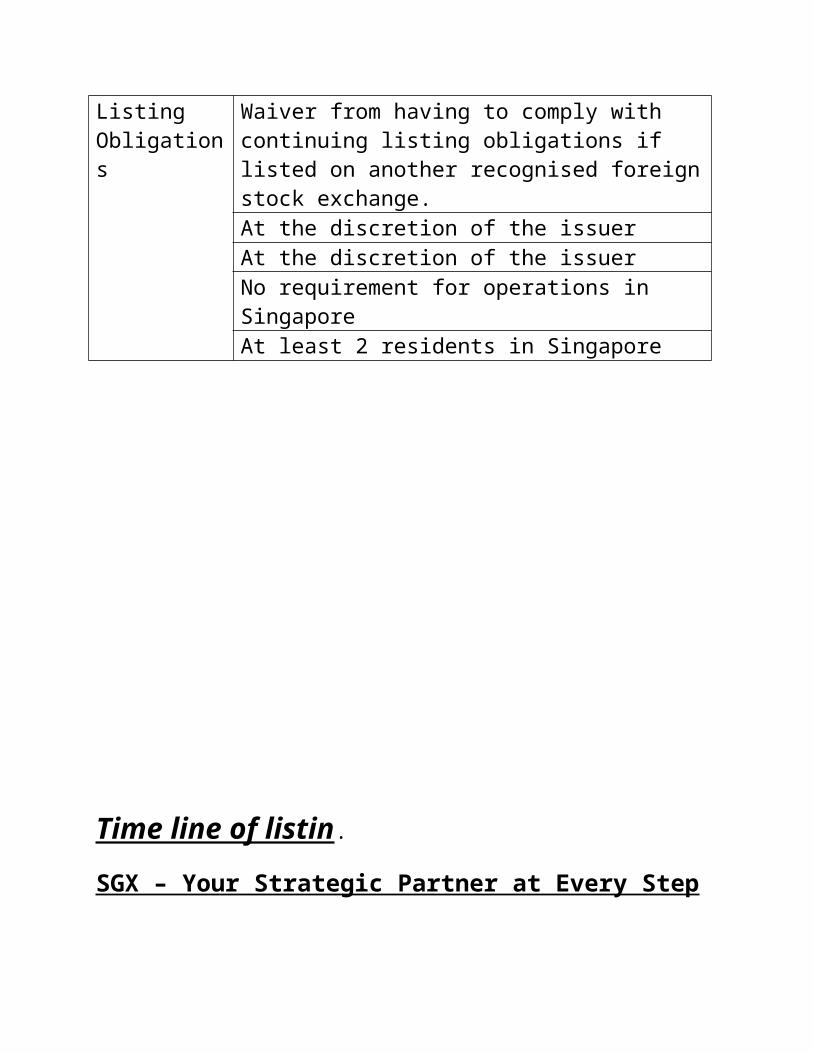

Secondary Listing

Companies that are already listed on another exchange of equivalent rules as SGX are able to seek a secondary listing on SGX without having to comply with SGX’s continuing listing obligations.

Global Depository Receipts

An international company that is already listed on its home exchange can also choose to list and raise funds on SGX via GDRs.

As GDRs are specialist products offered only to institutional and accredited investors, GDR listing requirements are relatively less demanding compared with primary and secondary listings where retail participation is allowed.

Please click here for details.

IPO or Introduction

Whether a company is listing on SGX on a primary or secondary basis, the offering at the point of listing can be done in following ways:

IPO

Issue of new shares or offer of existing shares to the investing public.

A prospectus has to be lodged with MAS and prepared in accordance with the Securities and Futures Regulations (SFR).

During the course of the listing process, the prospectus will be subject to public comments for approximately 3 to 4 weeks. (This may be extended at the discretion of MAS.)

Introduction

No shares are offered to the investing public. Suitable for companies that may not require funds at the point of

listing. An introductory document needs to be lodged with SGX and

prepared in accordance with SFR. The introductory document is not subject to public comments.

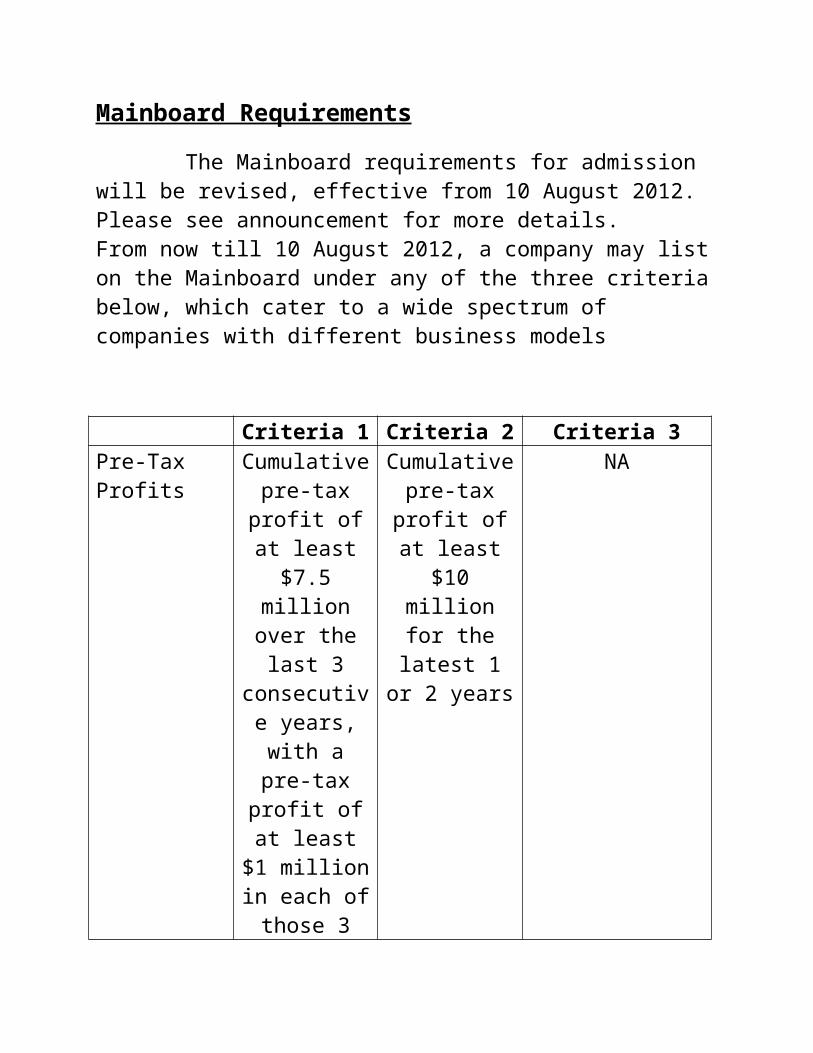

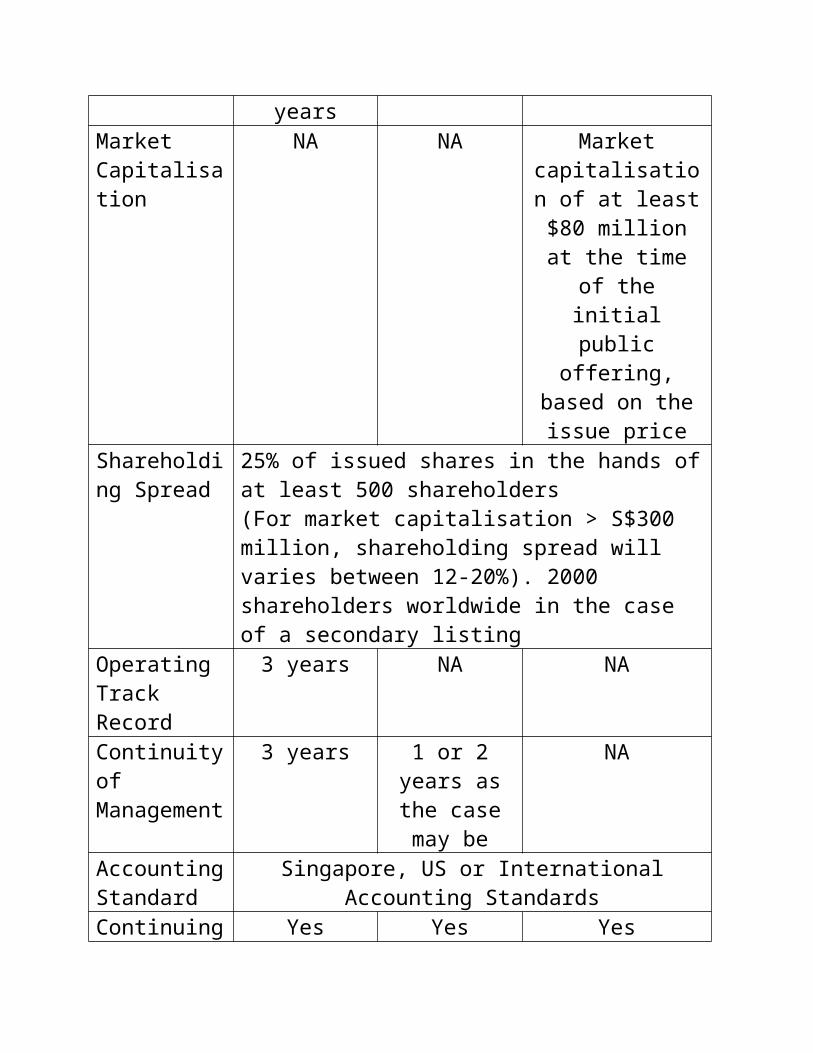

Mainboard Requirements

The Mainboard requirements for admission will be revised, effective from 10 August 2012. Please see announcement for more details. From now till 10 August 2012, a company may list on the Mainboard under any of the three criteria below, which cater to a wide spectrum of companies with different business models

Criteria 1 Criteria 2 Criteria 3Pre-Tax Profits

Cumulative pre-tax profit

of at least $7.5 million over the last

3 consecutive years, with a pre-tax profit of at least $1

million in each of those

3 years

Cumulative pre-tax profit

of at least $10 million

for the latest 1 or 2 years

NA

Market Capitalisation

NA NA Market capitalisation of at least $80 million at the time of the

initial public offering, based on

the issue priceShareholding Spread

25% of issued shares in the hands of at least 500 shareholders(For market capitalisation > S$300 million, shareholding spread will varies between 12-20%). 2000 shareholders worldwide in the case of a secondary listing

Operating Track Record

3 years NA NA

Continuity of Management

3 years 1 or 2 years as the case

may be

NA

Accounting Standard

Singapore, US or International Accounting Standards

Continuing Listing Obligations

Yes Yes YesWaiver from having to comply with continuing listing obligations if listed on another recognised foreign stock exchange.At the discretion of the issuerAt the discretion of the issuerNo requirement for operations in SingaporeAt least 2 residents in Singapore

Time line of listin.

SGX – Your Strategic Partner at Every Step

SGX is a dedicated partner to grow with its listed companies. As a listed company itself, SGX understands the concerns and the value of a listing. It understands that its business is to help its listed companies get the most value out of a listing, which goes beyond raising capital. At every step of the joining process, SGX ensures a potential listed company has all the support and information needed to make the right decisions for the business. As such, SGX continually strives to create an international marketplace where its listed companies can realise their full potential.

Pre-Joining

Step 1: Introduction to SGX

Understand the company’s capital needs Help the company understand SGX and the benefits of various

listing options Support the company to decide whether joining one of SGX’s

markets is right

Step 2: Pre-Submission Consultation

Provide guidance on the listing process, regulatory framework and corporate governance best practices

Work with the issuer to resolve potential issues

Post-Joining

Step 3: Profile Enhancement

Help the company raise its profile in the investment community through the Research Incentive Scheme, investor seminars and overseas roadshows to meet institutional investors

Step 4: Secondary Fund-Raising

·Provide a conducive marketplace for the company to raise secondary funds efficiently to support its continual growth

Listing Process

A company initiates the listing process by appointing a Singapore-based financial institution to be its sponsor and lead manager. The lead manager is usually a member company of SGX, a merchant bank or other similar institutions acceptable to SGX.

The lead manager will assume an active role and prepare the company for listing. Besides managing the launch, the lead manager also submits the listing application on behalf of the company. In addition, the lead manager will liaise with SGX on all matters arising from the application for listing.

Apart from the lead manager, the company needs to appoint a lawyer to oversee the legal aspects of listing. In addition, the appointed Certified Public Accountant will provide the company with an initial evaluation of its readiness to go public, assist in upgrading its management capabilities and in preparing the launch. Prior to and during the launch, the company will have to engage the service of an

experienced public relations firm to help enhance its appeal and convey its corporate messages effectively to the investing public.

IPO Timeline

Prior to submission of the listing application, the company is advised to consult SGX to resolve any specific issues. This will speed up the listing process and reduce any additional costs that may arise due to a delay. The timeframe for a listing varies for different companies, ranging from two months to two years. On the average, the whole process should last about 12 to 18 weeks. Given that time is of the essence, the company should budget a reasonable amount of management time and appoint the appropriate professionals to assist in the listing process.

CATALIST LISTIN REAQUIREMENT

A company seeking a listing on Catalist must meet the following admission requirements.

(1) Sponsorship

A listing applicant must be sponsored by an approved Sponsor of Catalist. Catalist companies are listed based on the Sponsor's assessment that they are suitable. SGX does not set any minimum quantitative entry criteria, but Sponsors will use their own deal selection criteria.

(2) Offer Document

A listing applicant must produce an "Offer Document". We have obtained an exemption from the Monetary Authority of Singapore (MAS) for the relevant sections in the Securities & Futures Act (SFA), such that an offer of securities on Catalist will not require a prospectus.

However, there is no change to the disclosure standards in Catalist, as it is the basis for investors to make informed decisions. Therefore, the Offer Document will be subject to the same disclosure requirements as a prospectus. To support this disclosure requirement, provisions relating to civil and criminal liability in the SFA will still apply to an Offer Document.

The prospectus exemption also means that the requirement to lodge and register the Offer Document with MAS will no longer apply. Instead, it will be lodged with SGX. Offer Documents will be posted on SGX's Catalodge website, for a period of at least 14 days. This will provide an avenue for the public to air any serious concerns they may have, and act as an additional safeguard.

(3) Working Capital Statement

The Sponsor and directors of the company must include a statement in the Offer Document that the company has sufficient working capital for the present requirements and for at least 12 months after IPO.

(4) Shareholding Spread

To promote healthy post-IPO trading activity, the shareholding spread requirement is set at 15% of issued capital in public hands with a minimum of 200 shareholders.

(5) Moratorium Period

To secure the commitment of promoters* and pre-IPO investors, restrictions on the sale of their shareholdings will apply. At the time of IPO, if promoters as a group hold more than 50% of the post-invitation share capital, they may sell but must retain at least 50%. If they hold less than 50% of the post-invitation share capital at IPO, they may not sell any. After IPO, promoters are not to sell any of their shareholdings 6 months after IPO. They may sell up to 50% of their shareholdings for the next 6 months.

For Pre-IPO investors who had acquired their shares within the 12-month period prior to IPO, the “profit portion” of their shareholdings will be subject to a moratorium period of 12 months after IPO. The “profit portion” is calculated as the number of shares derived from the difference between the cash paid by the investor for the shares and the value of the shareholdings based on the IPO price.

* “Promoters” are controlling shareholders & their associates and executive directors with more than 5% of share capital at the time of listing.

E-SUBMISSION

Welcome to the SGX e-Submission portal!

This is a web-based portal for you, to enjoy greater convenience and efficiency when making your regulatory submissions to the Risk Management and Regulation department of SGX.

Benefits of the online portal:-

With the new e-Submission portal, you will derive benefits such as:-

A secure and easy-to-use platform to make your submissions to SGX.

Greater convenience as you can make submissions at any time. Enhanced interaction with the SGX team, facilitated by built-in

discussion board. Shortened turnaround time for submissions with streamlined

administrative procedures. Easy to use database to retain and retrieve important

information, documenting all submissions and communications within the system.

Standard submission templates, thereby enables greater efficiency in the review and approval processes.

Greater transparency that allows you to follow the progress of your submission.

Enhanced Communication:-

The e-Submission portal creates an effective avenue for you to have your questions answered and keep track of your SGX applications. You are able to freely interact with the SGX team and engage in discussions on your submission.

To Begin the e-Submission :-

(www.sgx.com/regulation/esubmission)

At your convenience, you can log onto the e-submission portal to submit the following:-

Company Circulars (excluding those where new securities are issued)

Fixed Income Securities Structured Warrants

You will also find these links to other related documents useful:-

Account Opening Forms Terms and Conditions for Use of the System Issuer Undertaking Form FAQs