Embed Size (px)

Citation preview

Solar | Semiconductor | LED

This Presentation may contain certain statements or information that constitute “forward-looking statements” (as defined in

Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as

amended). In some but not all cases, forward-looking statements can be identified by terminology such as, for example,

“may,” “will,” “should,” “would,” “expects,” “plans,” “anticipates,” “intends,” “believes,” “estimates,” “predicts,” “potential,”

“continue,” or the negative of these terms or other comparable terminology. Examples of forward-looking statements include

statements regarding Amtech System, Inc.’s (the “Company”) future financial results, operating results, business strategies,

projected costs, products under development, competitive positions and plans and objectives of the Company and its

management for future operations. Such forward-looking statements and information are provided by the Company based

on current expectations of the Company and reflect various assumptions of management concerning the future

performance of the Company, and are subject to significant business, economic and competitive risks, uncertainties and

contingencies, many of which are beyond the control of the Company. Accordingly, there can be no guarantee that such

forward-looking statements or information will be realized. Actual results may vary from any anticipated results included in

such forward-looking statements and information and such variations may be material. No representations or warranties are

made as to the accuracy or reasonableness of any expectations or assumptions or the forward-looking statements or

information based thereon. Only those representations and warranties that are made in a definitive written agreement

relating to a transaction, when and if executed, and subject to any limitations and restrictions as may be specified in such

definitive agreement, shall have any effect, legal or otherwise. Each recipient of forward-looking statements should make

an independent assessment of the merits of and should consult its own professional advisors. Except as required by law,

we undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future

events, or otherwise.

Safe Harbor Statement

2

� Solar Growth Business

� Globalization of solar drives continued growth

� Reaching parity with conventional energy sources

� Recognized technology provider in solar market

� Major market share in top tier solar companies

� Expanded SAM 3x during solar market downturn through investments in� Expanded product offerings (PECVD, ALD)

� P and N-type cell technologies (PERC, n-PERT)

� Flexible manufacturing base to deal with market fluctuations

� Semi/LED Value Business

� Strong operational performance

� Positive earnings and cash-flow

� Leading market position in globally-served markets

� Asia-based manufacturing

Investment Highlights

3

� Global supplier of solar, semiconductor, & electronics process equipment technology and automation systems

� Headquartered in Tempe, Arizona

� Global presence in:

North America, Europe, Asia

� Providing leading edge equipment provider driven by acquisition of technology and products

� Continuous innovation� Successful development of solar PECVD, high

density diffusion systems, n-PERT and PERC cell solutions

� Successful deployment of next generation solar N-type cell technologies

� Successful development of new generation reflow equipment and technologies

� Leading equipment and technology provider

AMTECH Group

4

Amtech Group business model

Strategic Acquisition

2009 2012 2013 2014 20152010 2011

HD-POCl33200 w/h

production

Gen 1600MW n-PASHA

production

Batch PECVD1850w/h

Gen 2 100MW n-PASHA

production

Innovation

ALD/PECVD PERCPECVD 3600w/h

PID free PECVDLow cost

Ion implanter

1994 2007 2010 2014 20151996 2004

5

LED | ElectronicsSolar

Spatial ALD for PERC

Amtech markets

LED templates and carriers

High TempCustom and Belt Systems

N-PERT / PERC Diffusion and PECVD Systems

Semiconductor

Furnace & Automation

Reflow ProductsSemi Packaging & SMT

6

Amtech Group locations

Main officeTempe Arizona, USA

7

LED | ElectronicsSolar

Spatial ALD for PERC

Amtech Markets

LED templates and carriers

High TempCustom and Belt Systems

N-PERT / PERC Diffusion and PECVD Systems

Semiconductor

Furnace & Automation

Reflow ProductsSemi Packaging & SMT

8

AMTECH integrated offering

Solar value chain

Solar CellSilicon Ingot / Wafer Module

Cleaning Texturing

Diffusion

Screen Printing Metallization

Edge IsolationTesting Sorting

PSG Etching Removal

PECVDCoating

AMTECH GROUP

Products

Integrated Offering

Partnerships

Tech

no

log

yALD - AL2O3

Passivation

9

Solar technology approach

DIFFUSION• POCl3• BBr3• Annealing/Oxidation

DEPOSITION• PECVD ARC

Ox-Poly• ALD Al2O3

SO

LA

R

Taking semiconductor technologies and known-how

10

in partnership with renowned solar institutes

to solar high volume manufacturing

DIFFUSION• Oxide• POCl3• BBr3• Solid source Doping• Sintering / Alloying• Annealing / Drive-In

DEPOSITION• Poly Silicon• SIPOS• PECVD Nitride, Oxy-Nitride• LPCVD, LS Nitride, Oxy-Nitride• TEOS• LTO• HTO• Ta2O5S

EM

ICO

ND

UC

TO

R

Amtech technology in solar production lineSAM increased from 12% to 55%

� Standard multi – cell efficiency 18%

inspection Texture POCl3 Single side etch PECVD Print/fire/Flash

� PERC – cell efficiency multi 19%, mono 21%

inspection Texture POCl3 Single side etch PECVDrear

Print/fire/FlashALD Al2O3 PECVD front

Laser

1. Innovation� wph increase� new product

2. Acquisition� Solaytec ALD

3. Technology� new flow

� N-type – cell efficiency 21 – 23%

inspection Texture BBr3 Single side etch PECVDfront

Print/fire/FlashImplant PECVD rear

ALD Al2O3Anneal ox

1800 ���� 4000wph

Amtech SAM=12% (2011) SAM=55% (2016)

� N-type – cell efficiency 21 – 23%

inspection Texture BBr3 Single side etch PECVDfront

Print/fire/FlashImplant PECVD rear

ALD Al2O3Anneal oxOx-Poly

11

Global demand 2016 & 2017 forecast

IHSGTM

researchMercom

2015 59GW 59GW 58GW

2016 77GW 74GW 76GW

2017 79GW 69GW 70GW

DELTA +2GW -5GW -6GW

Highlights• 77 GW of global installations in 2016• China maintains position as largest end market• India set to become the 3rd largest market in 2017• European market stagnation• Strong demand supports new wave of expansions

� Each year since 2006 actual installations have been consistently higher than consensus forecasts, primarily driven by the globalization of solar

� Lower $/kWh solar prices will drive increased adoption in the future

Huge swings in forecasted numbers

12

Solar market impact on PECVDStrong adoption of double-side PECVD based technology

13

IHSGTMMercom

Market growth 2015 ���� 2020

Analyst more bullish than our modelOur mode: CAGR of 10 – 17%

Market growth 40GW; 10GW/year

Technology adoption

PERC and n-PERT are growing faster than market � large upgrade market

13

Notes: Actual 2016 demand was 75GW; Demand increased an avg. of 20% per year for last 10 years.

0

50

100

150

200

250

300

1 2 3

US

$ m

illi

on

s

Diffusion PECVD ALD

Tempress/SoLayTec Marketshare per SAM

Solar Marketshare$540 million SAM opportunity

35%

95%

5%

93%

7%

Strategy =ATTACK !Strategy =ATTACK !

Strategy =DEFEND !

14

Tempress Diffusion

Tempress PECVDPECVD SiNx, SiO2

LPCVD Poly

HD POCL3

BBr3

Annealing, Oxidation

SoLayTec ALD

ALD Al2O3

Position in Serviceable Available Markets

15

• POCl3 diffusion specialist

• Number 2 position; 35% market share

• Strong competition from Chinese with LP-POCl3 and lower CAPEX

• BBr3 position 1 with >90% market share

• Anneal/oxidation low market share

• PECVD launch SNEC May, 2016

• Number 5 position, 5% market share

• New platform Spectrum enables market share growth; strong adoption to >20% MS

• LP-Poly number 1 position

• N-PERT IP position enables larger market share

• ALD Al2O3 specialist

• Number 2 position, 7% market share

• ALD based PERC enables higher efficiencies

• PERC technology know-how enables larger market share

LED | ElectronicsSolar

Spatial ALD for PERC

Amtech Markets

LED templates and carriers

High TempCustom and Belt Systems

N-PERT / PERC Diffusion and PECVD Systems

Semiconductor

Furnace & Automation

Reflow ProductsSemi Packaging & SMT

16

Electronics Value Chain – Where we Compete

AssemblyPackagingSemiconductor

17

Wafer bumping

Solder reflow

Underfill and cure

fluxing

Solder reflow

Tech

no

log

yVision and placement

Screen print

Test & inspect

Placement

Solder reflow

Tech

no

log

y

AMTECH GROUP

Products

BTU Thermal Products

18

Pyramax

� The world’s best performing reflow oven

� Thermal uniformity

� Atmosphere control

� Static pressure

� Top choice of semiconductor assembly and test subcontractors (SATS) companies

� Demanding thermal and atmosphere requirements

� Very high brand loyalty/reputation

� Thousands of systems installed worldwide

High temp, fast fire

� High volume continuous thermal processing experts

� Serving Electronics, Automotive, and Medical markets

� Broad process experience solving critical process problems

� Multiple heating technologies including: IR, convection (high and low temp)

BTU’s Diverse Customer Base

19C O N F I D E N T I A L

Analog / Power Chip Sector

� Serve top players in Analog, Power Chip and Sensor Sectors, including #1 Infineon, Texas Instruments (including TI Aizu and Miho), Analog Devices (ADI), Samsung, UMC, Vanguard, SEH, SUMCO, Dongbu-ANAM, Soitec

� Potential migration from 6”(2/3rd) to 8”(1/3rd) to 12” wafers

� Future opportunities on fast growing Robotics and Automotive

LED & Optics

� LED consumable growth

� LED and Optics equipment opportunities

Semiconductor & LED

20

Solar | Semiconductor | LED

Financial Overview

21

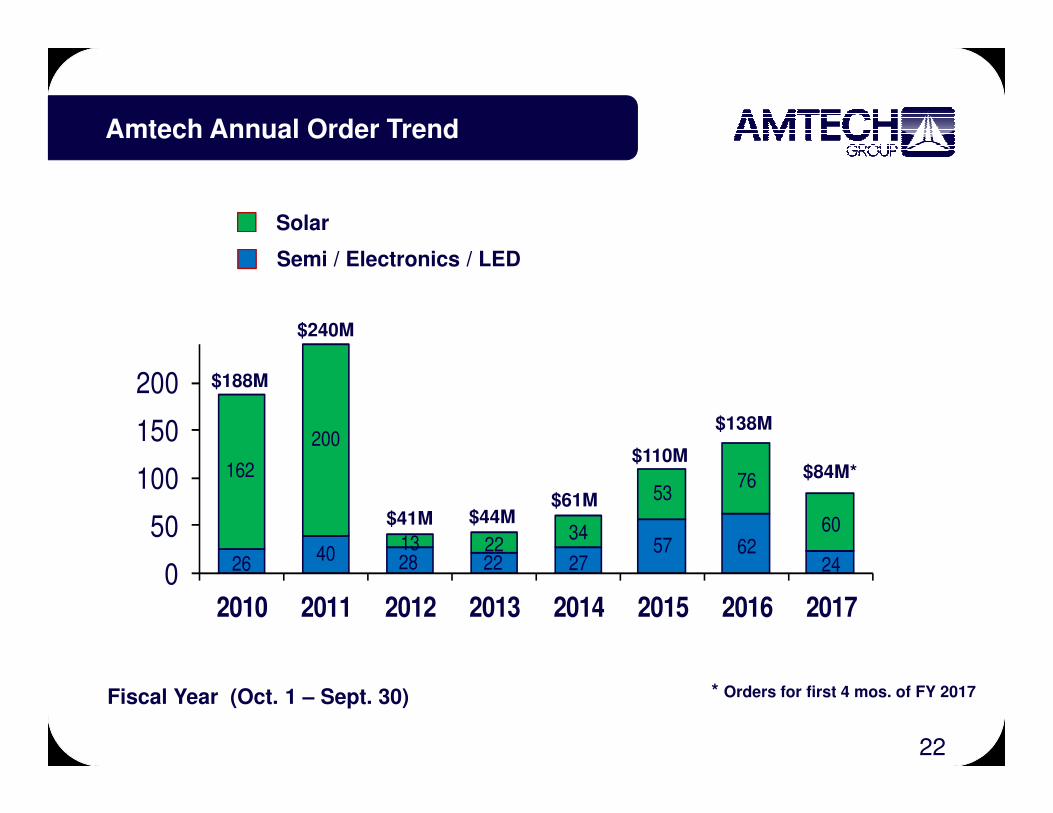

Amtech Annual Order Trend

26 40 28 22 2757 62

24

162

200

13 2234

5376

60

0

50

100

150

200

2010 2011 2012 2013 2014 2015 2016 2017

Solar

$61M

$188M

Fiscal Year (Oct. 1 – Sept. 30)

$240M

$41M

Semi / Electronics / LED

$44M

22

$110M

$138M

$84M*

* Orders for first 4 mos. of FY 2017

December 31, 2016

(in millions)

Balance Sheet – Financial Strength

Total Cash $26.9

Working Capital $45.4

Total Assets $115.9

Long-term Debt $9.1

Total Liabilities $51.5

Stockholders’’’’ Equity $64.4

23

Note: At the end of January 2017, cash balance was ~ $45.8M, due primarily to a large turn-key project deposit.

� Solar Growth Business

� Globalization of solar drives continued growth

� Reaching parity with conventional energy sources

� Recognized technology provider in solar market

� Major market share in top tier solar companies

� Expanded SAM 3x during solar market downturn through investments in� Expanded product offerings (PECVD, ALD)

� P and N-type cell technologies (PERC, n-PERT)

� Flexible manufacturing base to deal with market fluctuations

� Semi/LED Value Business

� Strong operational performance

� Positive earnings and cash-flow

� Leading market position in globally-served markets

� Asia-based manufacturing

Investment Highlights

24