Embed Size (px)

Citation preview

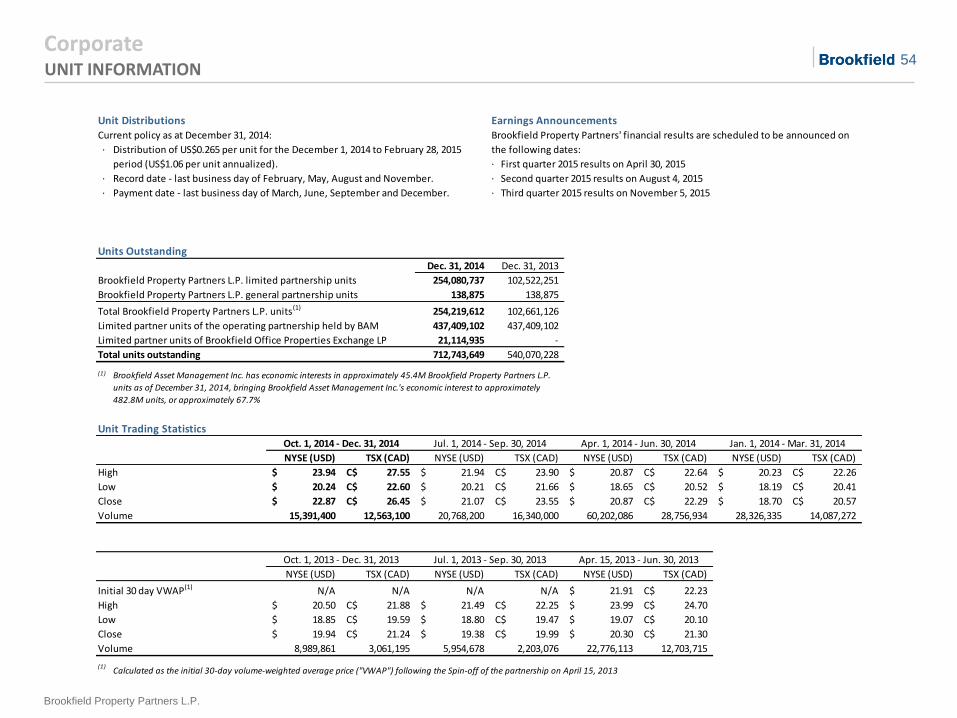

Brookfield Property Partners L.P. NYSE: BPY TSX: BPY.UN

Supplemental Information For the quarter ended December 31

20

14

1

Brookfield Property Partners L.P.

FORWARD-LOOKING STATEMENTS

This supplemental information package contains “forward-looking information” within the meaning of Canadian provincial securities laws and applicable regulations and forward-looking statements within the meaning of “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements that are predictive in nature, depend upon or refer to future events or conditions, include statements regarding our operations, business, financial condition, expected financial results, performance, prospects, opportunities, priorities, targets, goals, ongoing objectives, strategies and outlook, as well as the outlook for North American and international economies for the current fiscal year and subsequent periods, and include words such as “expects”, “anticipates”, “plans”, “believes”, “estimates”, “seeks”, “intends”, “targets”, “projects”, “forecasts”, “likely”, or negative versions thereof and other similar expressions, or future or conditional verbs such as “may”, “will”, “should”, “would” and “could”.

Although we believe that our anticipated future results, performance or achievements expressed or implied by the forward-looking statements and information are based upon reasonable assumptions and expectations, the reader should not place undue reliance on forward-looking statements and information because they involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, which may cause our actual results, performance or achievements to differ materially from anticipated future results, performance or achievement expressed or implied by such forward-looking statements and information.

Factors that could cause actual results to differ materially from those contemplated or implied by forward-looking statements include, but are not limited to: risks incidental to the ownership and operation of real estate properties including local real estate conditions; the impact or unanticipated impact of general economic, political and market factors in the countries in which we do business; the ability to enter into new leases or renew leases on favourable terms; business competition; dependence on tenants’ financial condition; the use of debt to finance our business; the behavior of financial markets, including fluctuations in interest and foreign exchanges rates; uncertainties of real estate development or redevelopment; global equity and capital markets and the availability of equity and debt financing and refinancing within these markets; risks relating to our insurance coverage; the possible impact of international conflicts and other developments including terrorist acts; potential environmental liabilities; changes in tax laws and other tax related risks; dependence on management personnel; illiquidity of investments; the ability to complete and effectively integrate acquisitions into existing operations and the ability to attain expected benefits therefrom; operational and reputational risks; catastrophic events, such as earthquakes and hurricanes; and other risks and factors detailed from time to time in our documents filed with the securities regulators in Canada and the United States.

We caution that the foregoing list of important factors that may affect future results is not exhaustive. When relying on our forward-looking statements or information, investors and others should carefully consider the foregoing factors and other uncertainties and potential events. Except as required by law, we undertake no obligation to publicly update or revise any forward-looking statements or information, whether written or oral, that may be as a result of new information, future events or otherwise.

CAUTIONARY STATEMENT REGARDING USE OF NON-IFRS ACCOUNTING MEASURES This supplemental information package makes reference to net operating income ("NOI"), funds from operations ("FFO") and Company funds from operations (“Company FFO") on a total and per unit basis. These terms do not have any standardized meaning prescribed by International Financial Reporting Standards as issued by the International Accounting Standards Board ("IFRS") and therefore may not be comparable to similar measures presented by other companies. Brookfield Property Partners L.P. ("BPY" or the "partnership") defines NOI as revenues from commercial and hospitality operations of consolidated properties less direct property expenses. Our definition of FFO includes all of the adjustments that are outlined in the National Association of Real Estate Investment Trusts ("NAREIT") definition of funds from operations, including the exclusion of gains (or losses) from the sale of investment property, the add back of any depreciation and amortization related to real estate assets and the adjustment to reflect our interest in unconsolidated partnerships and joint ventures. In addition to the adjustments prescribed by NAREIT, we also make adjustments to exclude any unrealized fair value gains (or losses) that arise as a result of reporting under IFRS, and income taxes that arise as certain of our subsidiaries are structured as corporations as opposed to real estate investment trusts ("REIT"). These additional adjustments result in an FFO measure that is similar to that which would result if the partnership was organized as a REIT that determined net income in accordance with U.S. generally accepted accounting principles ("U.S. GAAP"), which is the type of organization on which the NAREIT definition is premised. Our FFO measure will differ from other organizations applying the NAREIT definition to the extent of certain differences between the IFRS and U.S. GAAP reporting frameworks, principally related to the recognition of lease termination income, which do not have a significant impact on the FFO measure reported. The partnership uses NOI and FFO to assess its operating results. NOI is important in assessing operating performance and FFO is a widely used measure to analyze real estate. The partnership reconciles FFO to net income attributable to Unitholders (see the glossary of terms for definition) as opposed to cashflow from operating activities as it believes net income attributable to Unitholders is the most comparable measure. Company FFO is defined as FFO before the impact of depreciation and amortization of non-real estate assets, transaction costs, gains (losses) associated with non-investment properties plus the FFO that would have been attributable to the partnership's shares of General Growth Properties, Inc. ("GGP") if all outstanding warrants of GGP were exercised on a cash-less basis. It also includes dilution adjustments to undiluted FFO as a result of the net settled warrants. Refer to last page of this supplemental package for certain definitions.

2

Brookfield Property Partners L.P.

TABLE OF CONTENTS

Page Page

Financial Overview Retail Segment, Cont'd

Current Quarter Highlights 4 Portfolio Summary 34

Income Statement 5 Historical Metrics 35

Balance Sheet 8 Leasing Metrics 36

Components of Net Asset Value 10 Top Tenants 37

Fair Value Continuity 11 Developments 38

Capital Recycling 13 Debt 39

Summary Statement of Cash Flows 14 Other Segments

Office Segment Financial Overview 41

Financial Overview 16 Summary of Industrial Properties 42

Net Operating Income 17 Industrial Developments and Land 43

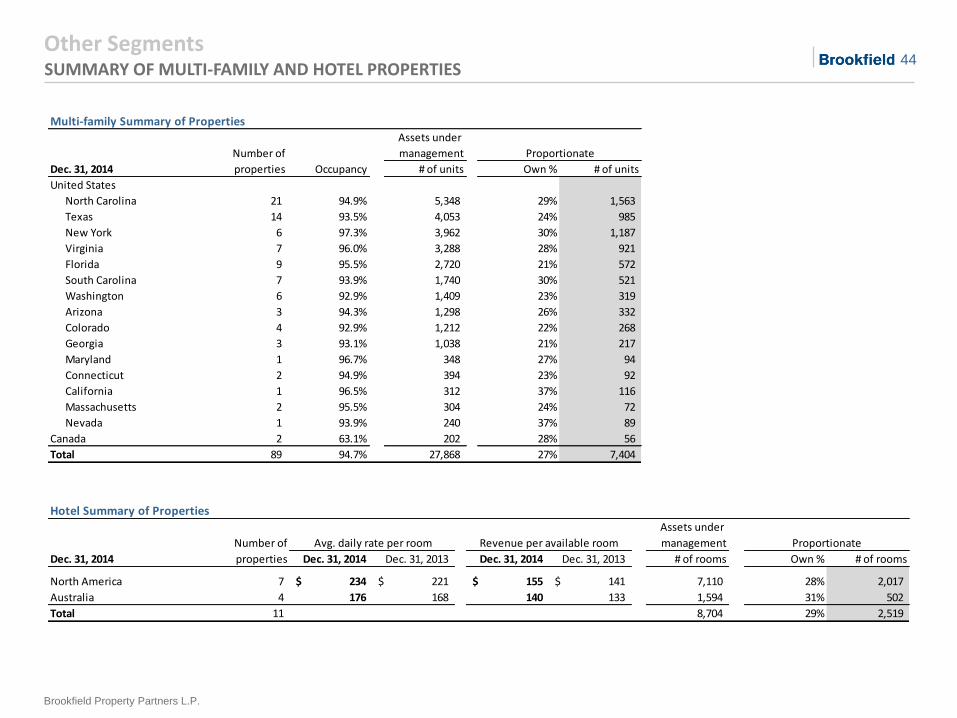

Summary of Properties 19 Summary of Multi-family and Hotel Properties 44

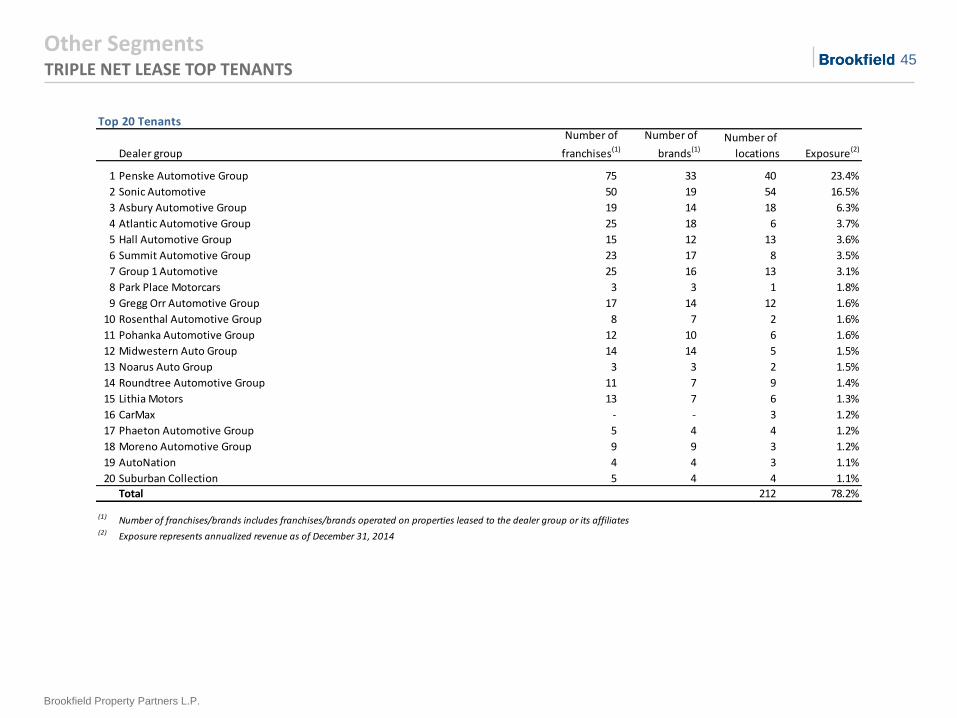

Historical Occupancy 20 Triple Net Lease Top Tenants 45

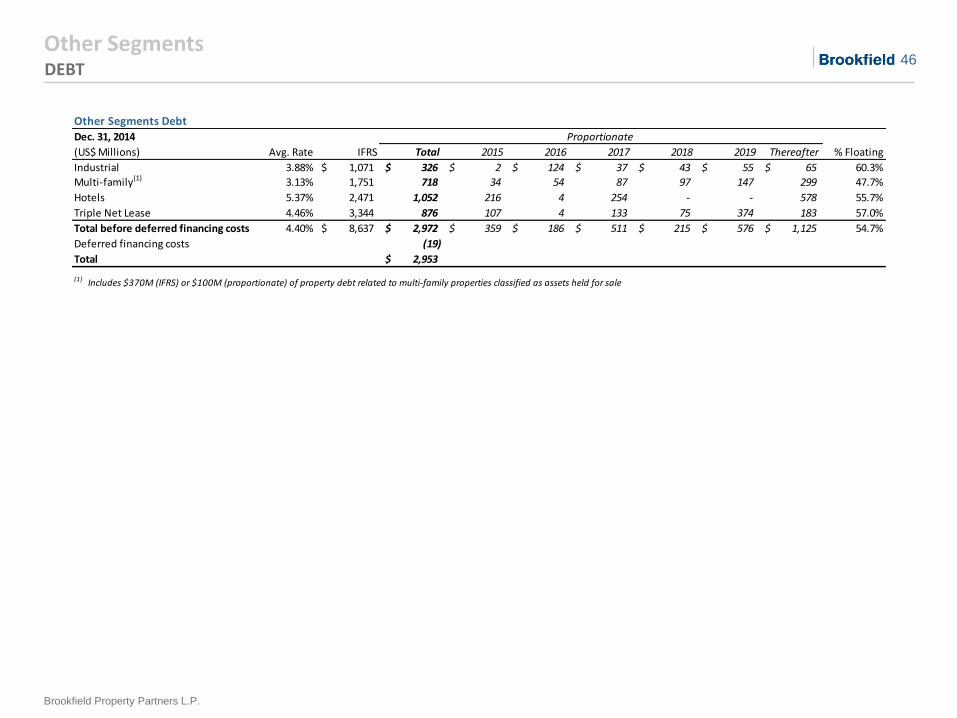

Historical Rents 21 Debt 46

Leasing Activity 22 Corporate

Lease Expiry Analysis 24 Financial Overview 48

Top Tenants 25 Liquidity 49

Development Sites 26 Proportionate Debt Summary 50

Debt 27 Foreign Currency Hedge Position 51

Capital Expenditures 30 Capital Securities & Preferred Equity 52

Retail Segment Per Unit Information 53

Financial Overview 32 Unit Information 54

Net Operating Income 33 Glossary of Terms 55

Financial Overview

4

Brookfield Property Partners L.P.

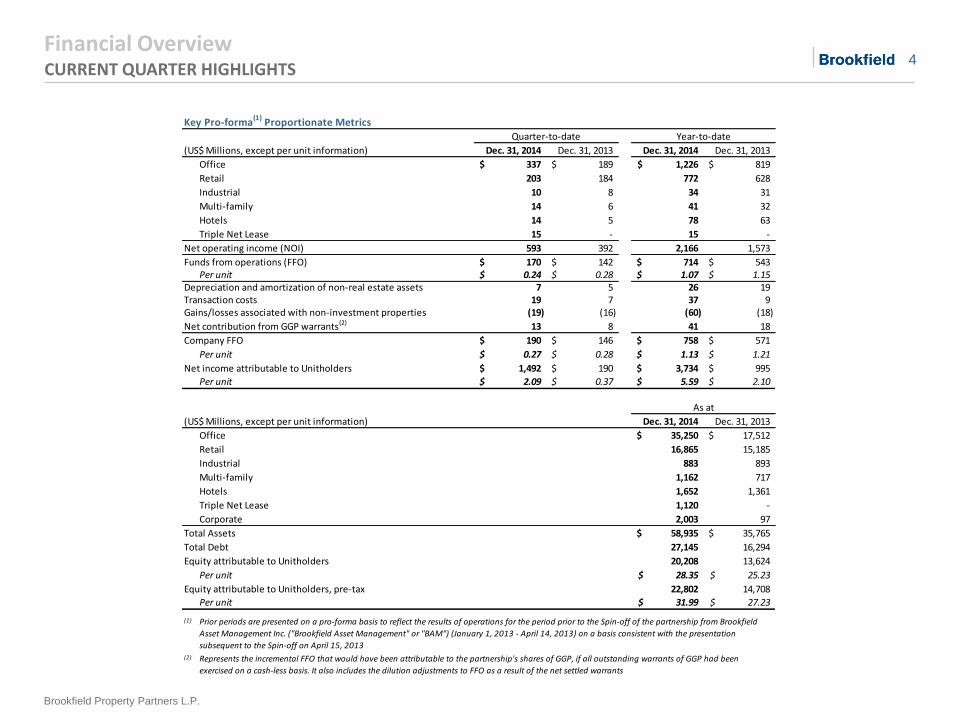

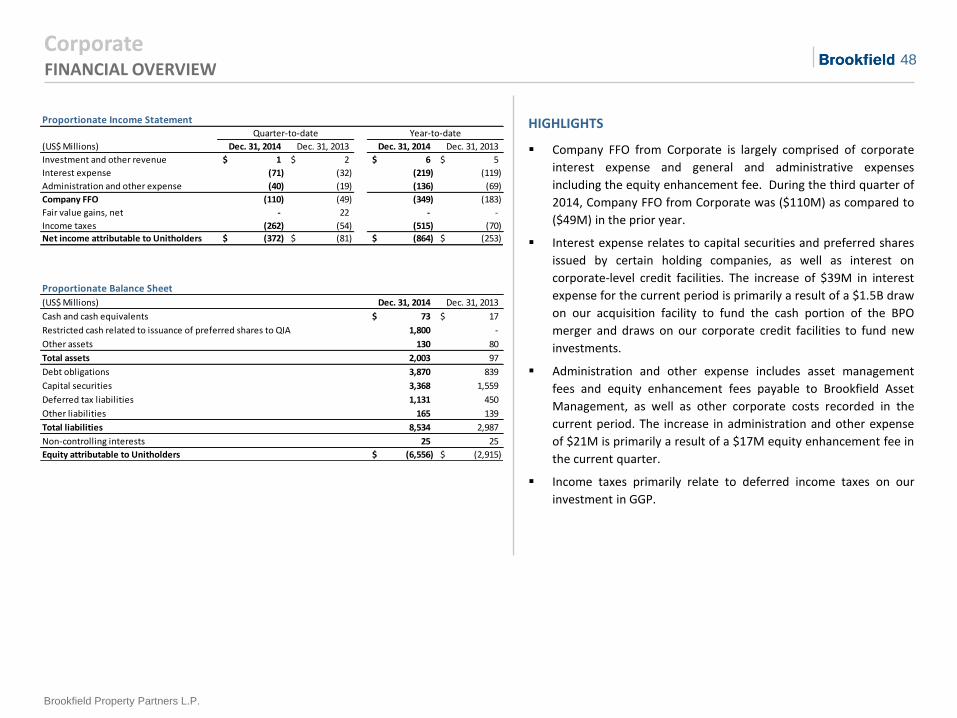

Financial Overview CURRENT QUARTER HIGHLIGHTS

Key Pro-forma(1)

Proportionate Metrics

(US$ Millions, except per unit information) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

Office 337$ 189$ 1,226$ 819$

Retail 203 184 772 628

Industrial 10 8 34 31

Multi-family 14 6 41 32

Hotels 14 5 78 63

Triple Net Lease 15 - 15 -

Net operating income (NOI) 593 392 2,166 1,573

Funds from operations (FFO) 170$ 142$ 714$ 543$ Per unit 0.24$ 0.28$ 1.07$ 1.15$

Depreciation and amortization of non-real estate assets 7 5 26 19 Transaction costs 19 7 37 9 Gains/losses associated with non-investment properties (19) (16) (60) (18)

Net contribution from GGP warrants(2) 13 8 41 18

Company FFO 190$ 146$ 758$ 571$

Per unit 0.27$ 0.28$ 1.13$ 1.21$

Net income attributable to Unitholders 1,492$ 190$ 3,734$ 995$

Per unit 2.09$ 0.37$ 5.59$ 2.10$

(US$ Millions, except per unit information) Dec. 31, 2014 Dec. 31, 2013

Office 35,250$ 17,512$

Retail 16,865 15,185

Industrial 883 893

Multi-family 1,162 717

Hotels 1,652 1,361

Triple Net Lease 1,120 -

Corporate 2,003 97

Total Assets 58,935$ 35,765$

Total Debt 27,145 16,294

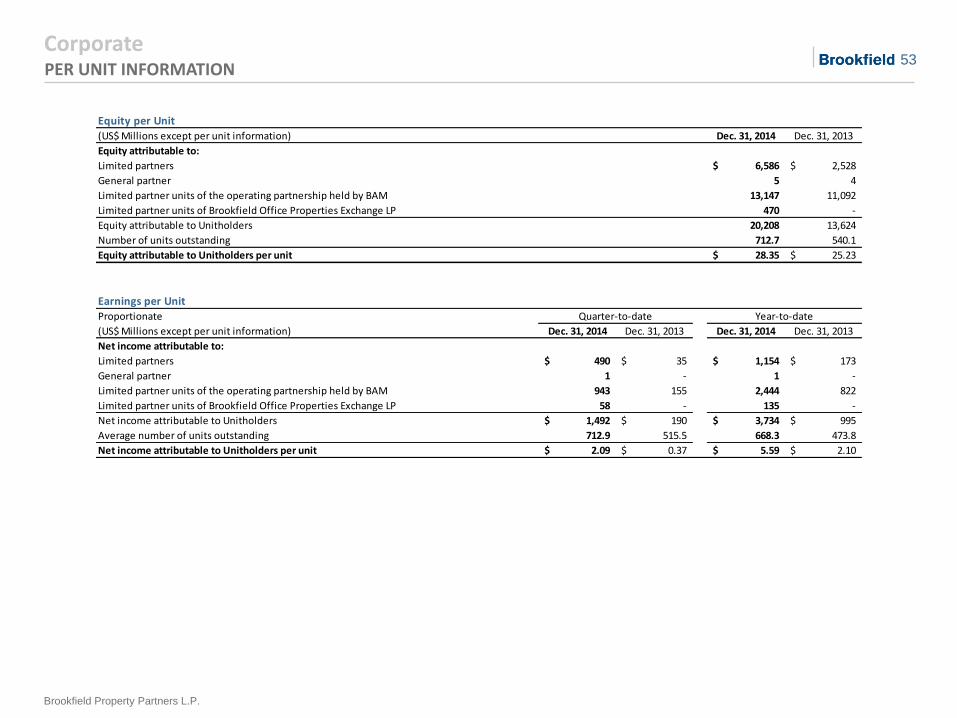

Equity attributable to Unitholders 20,208 13,624

Per unit 28.35$ 25.23$

Equity attributable to Unitholders, pre-tax 22,802 14,708

Per unit 31.99$ 27.23$

(1)

(2)

Year-to-dateQuarter-to-date

As at

Represents the incremental FFO that would have been attributable to the partnership's shares of GGP, if all outstanding warrants of GGP had been

exercised on a cash-less basis. It also includes the dilution adjustments to FFO as a result of the net settled warrants

Prior periods are presented on a pro-forma basis to reflect the results of operations for the period prior to the Spin-off of the partnership from Brookfield

Asset Management Inc. ("Brookfield Asset Management" or "BAM") (January 1, 2013 - April 14, 2013) on a basis consistent with the presentation

subsequent to the Spin-off on April 15, 2013

5

Brookfield Property Partners L.P.

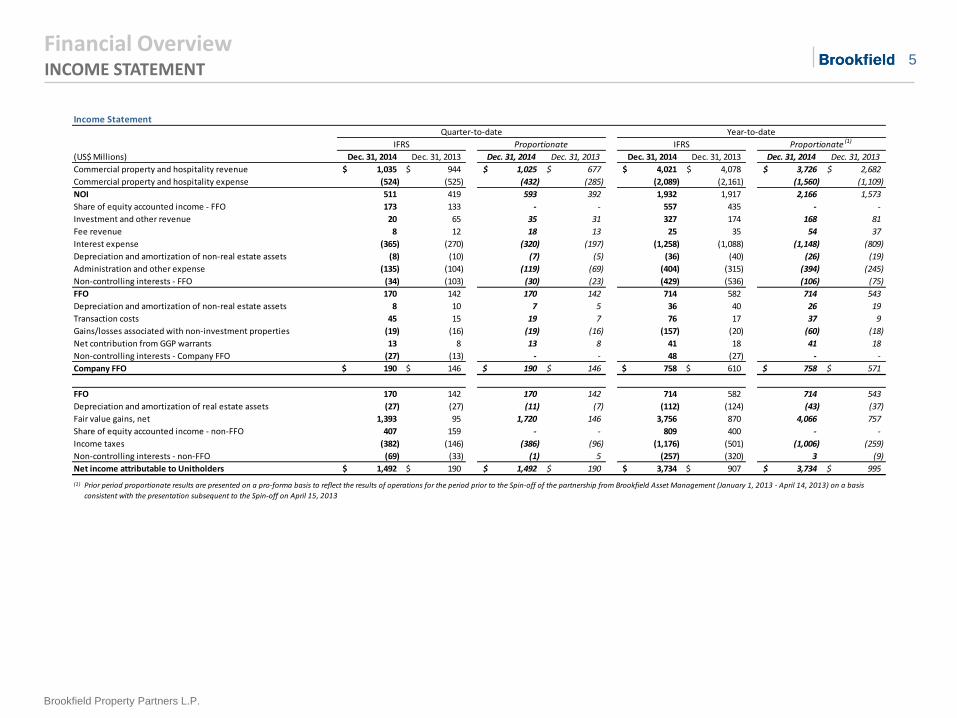

Financial Overview INCOME STATEMENT

Income Statement

(US$ Millions) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

Commercial property and hospitality revenue 1,035$ 944$ 1,025$ 677$ 4,021$ 4,078$ 3,726$ 2,682$

Commercial property and hospitality expense (524) (525) (432) (285) (2,089) (2,161) (1,560) (1,109)

NOI 511 419 593 392 1,932 1,917 2,166 1,573

Share of equity accounted income - FFO 173 133 - - 557 435 - -

Investment and other revenue 20 65 35 31 327 174 168 81

Fee revenue 8 12 18 13 25 35 54 37

Interest expense (365) (270) (320) (197) (1,258) (1,088) (1,148) (809)

Depreciation and amortization of non-real estate assets (8) (10) (7) (5) (36) (40) (26) (19)

Administration and other expense (135) (104) (119) (69) (404) (315) (394) (245)

Non-controlling interests - FFO (34) (103) (30) (23) (429) (536) (106) (75)

FFO 170 142 170 142 714 582 714 543

Depreciation and amortization of non-real estate assets 8 10 7 5 36 40 26 19

Transaction costs 45 15 19 7 76 17 37 9

Gains/losses associated with non-investment properties (19) (16) (19) (16) (157) (20) (60) (18)

Net contribution from GGP warrants 13 8 13 8 41 18 41 18

Non-controlling interests - Company FFO (27) (13) - - 48 (27) - -

Company FFO 190$ 146$ 190$ 146$ 758$ 610$ 758$ 571$

FFO 170 142 170 142 714 582 714 543

Depreciation and amortization of real estate assets (27) (27) (11) (7) (112) (124) (43) (37)

Fair value gains, net 1,393 95 1,720 146 3,756 870 4,066 757

Share of equity accounted income - non-FFO 407 159 - - 809 400 - -

Income taxes (382) (146) (386) (96) (1,176) (501) (1,006) (259)

Non-controlling interests - non-FFO (69) (33) (1) 5 (257) (320) 3 (9)

Net income attributable to Unitholders 1,492$ 190$ 1,492$ 190$ 3,734$ 907$ 3,734$ 995$

(1)

Quarter-to-date Year-to-date

IFRS Proportionate IFRS Proportionate (1)

Prior period proportionate results are presented on a pro-forma basis to reflect the results of operations for the period prior to the Spin-off of the partnership from Brookfield Asset Management (January 1, 2013 - April 14, 2013) on a basis

consistent with the presentation subsequent to the Spin-off on April 15, 2013

6

Brookfield Property Partners L.P.

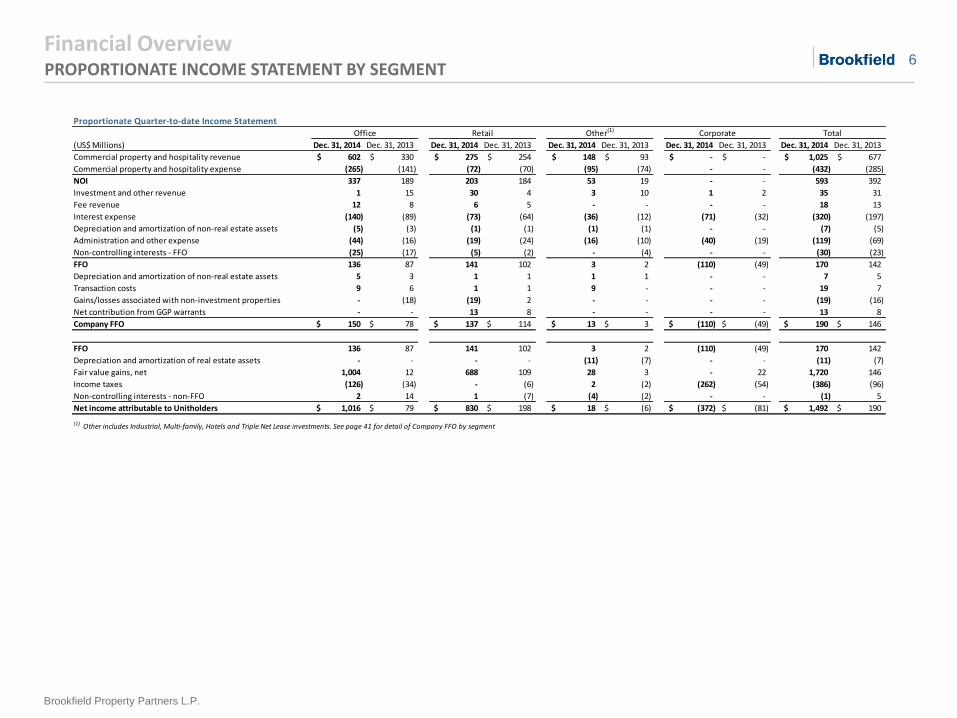

Financial Overview PROPORTIONATE INCOME STATEMENT BY SEGMENT

Proportionate Quarter-to-date Income Statement

(US$ Millions) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

Commercial property and hospitality revenue 602$ 330$ 275$ 254$ 148$ 93$ -$ -$ 1,025$ 677$

Commercial property and hospitality expense (265) (141) (72) (70) (95) (74) - - (432) (285)

NOI 337 189 203 184 53 19 - - 593 392

Investment and other revenue 1 15 30 4 3 10 1 2 35 31

Fee revenue 12 8 6 5 - - - - 18 13

Interest expense (140) (89) (73) (64) (36) (12) (71) (32) (320) (197)

Depreciation and amortization of non-real estate assets (5) (3) (1) (1) (1) (1) - - (7) (5)

Administration and other expense (44) (16) (19) (24) (16) (10) (40) (19) (119) (69)

Non-controlling interests - FFO (25) (17) (5) (2) - (4) - - (30) (23)

FFO 136 87 141 102 3 2 (110) (49) 170 142

Depreciation and amortization of non-real estate assets 5 3 1 1 1 1 - - 7 5

Transaction costs 9 6 1 1 9 - - - 19 7

Gains/losses associated with non-investment properties - (18) (19) 2 - - - - (19) (16)

Net contribution from GGP warrants - - 13 8 - - - - 13 8

Company FFO 150$ 78$ 137$ 114$ 13$ 3$ (110)$ (49)$ 190$ 146$

FFO 136 87 141 102 3 2 (110) (49) 170 142

Depreciation and amortization of real estate assets - - - - (11) (7) - - (11) (7)

Fair value gains, net 1,004 12 688 109 28 3 - 22 1,720 146

Income taxes (126) (34) - (6) 2 (2) (262) (54) (386) (96)

2 14 1 (7) (4) (2) - - (1) 5

Net income attributable to Unitholders 1,016$ 79$ 830$ 198$ 18$ (6)$ (372)$ (81)$ 1,492$ 190$

(1) Other includes Industrial, Multi-family, Hotels and Triple Net Lease investments. See page 41 for detail of Company FFO by segment

Office

Non-controlling interests - non-FFO

TotalOther(1) CorporateRetail

7

Brookfield Property Partners L.P.

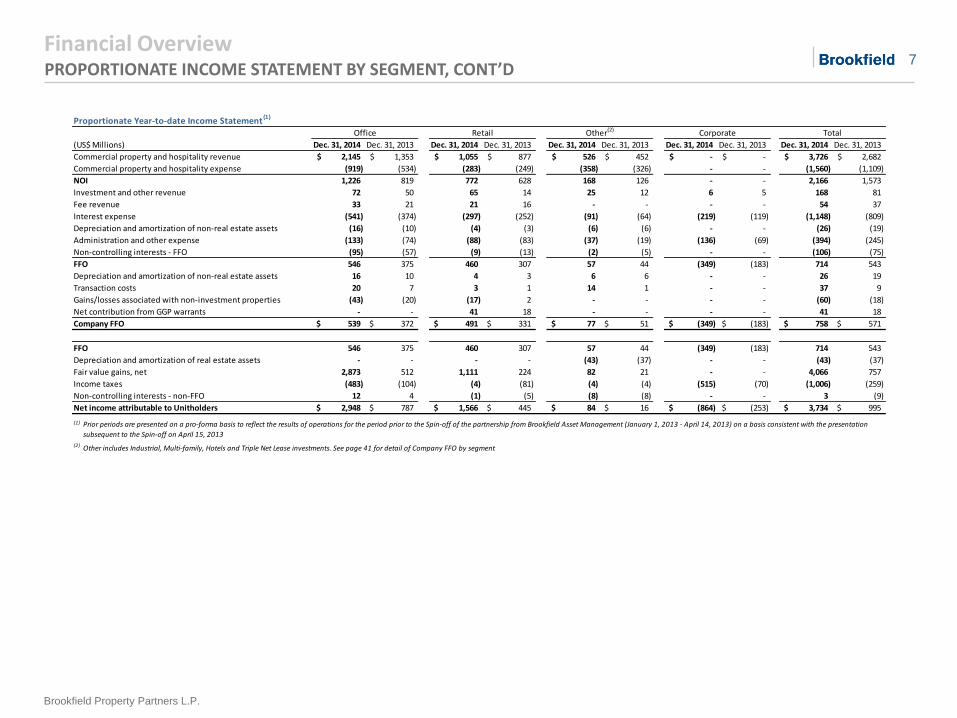

Financial Overview PROPORTIONATE INCOME STATEMENT BY SEGMENT, CONT’D

Proportionate Year-to-date Income Statement (1)

(US$ Millions) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

Commercial property and hospitality revenue 2,145$ 1,353$ 1,055$ 877$ 526$ 452$ -$ -$ 3,726$ 2,682$

Commercial property and hospitality expense (919) (534) (283) (249) (358) (326) - - (1,560) (1,109)

NOI 1,226 819 772 628 168 126 - - 2,166 1,573

Investment and other revenue 72 50 65 14 25 12 6 5 168 81

Fee revenue 33 21 21 16 - - - - 54 37

Interest expense (541) (374) (297) (252) (91) (64) (219) (119) (1,148) (809)

Depreciation and amortization of non-real estate assets (16) (10) (4) (3) (6) (6) - - (26) (19)

Administration and other expense (133) (74) (88) (83) (37) (19) (136) (69) (394) (245)

Non-controlling interests - FFO (95) (57) (9) (13) (2) (5) - - (106) (75)

FFO 546 375 460 307 57 44 (349) (183) 714 543

Depreciation and amortization of non-real estate assets 16 10 4 3 6 6 - - 26 19

Transaction costs 20 7 3 1 14 1 - - 37 9

Gains/losses associated with non-investment properties (43) (20) (17) 2 - - - - (60) (18)

Net contribution from GGP warrants - - 41 18 - - - - 41 18

Company FFO 539$ 372$ 491$ 331$ 77$ 51$ (349)$ (183)$ 758$ 571$

FFO 546 375 460 307 57 44 (349) (183) 714 543

Depreciation and amortization of real estate assets - - - - (43) (37) - - (43) (37)

Fair value gains, net 2,873 512 1,111 224 82 21 - - 4,066 757

Income taxes (483) (104) (4) (81) (4) (4) (515) (70) (1,006) (259)

12 4 (1) (5) (8) (8) - - 3 (9)

Net income attributable to Unitholders 2,948$ 787$ 1,566$ 445$ 84$ 16$ (864)$ (253)$ 3,734$ 995$

(1)

(2) Other includes Industrial, Multi-family, Hotels and Triple Net Lease investments. See page 41 for detail of Company FFO by segment

Corporate TotalOffice Retail

Prior periods are presented on a pro-forma basis to reflect the results of operations for the period prior to the Spin-off of the partnership from Brookfield Asset Management (January 1, 2013 - April 14, 2013) on a basis consistent with the presentation

subsequent to the Spin-off on April 15, 2013

Other(2)

Non-controlling interests - non-FFO

8

Brookfield Property Partners L.P.

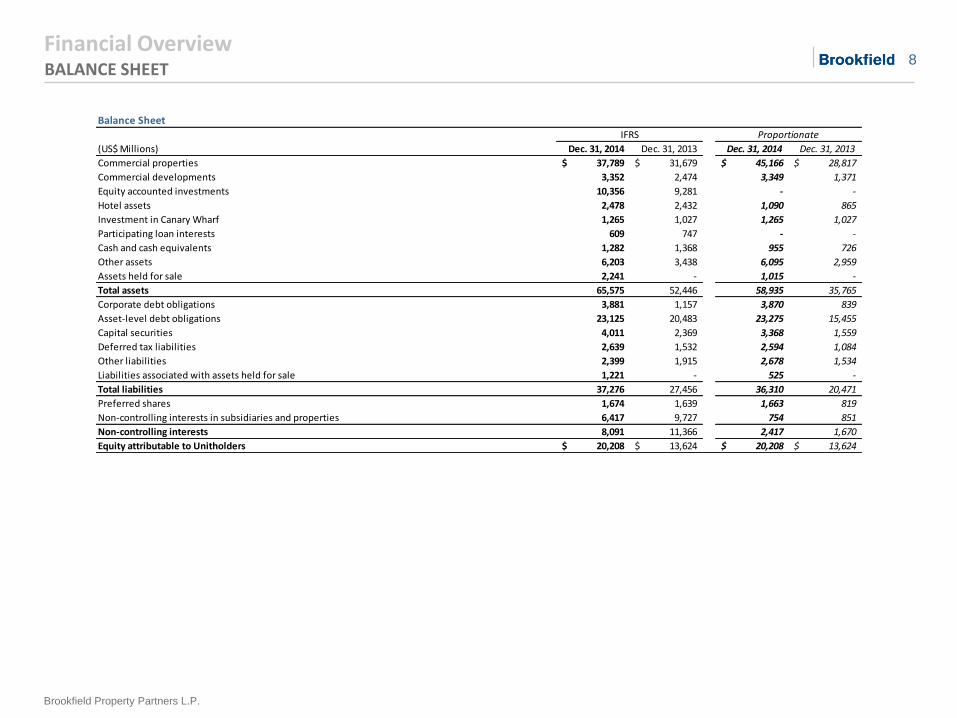

Financial Overview BALANCE SHEET

Balance Sheet

(US$ Millions) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

Commercial properties 37,789$ 31,679$ 45,166$ 28,817$

Commercial developments 3,352 2,474 3,349 1,371

Equity accounted investments 10,356 9,281 - -

Hotel assets 2,478 2,432 1,090 865

Investment in Canary Wharf 1,265 1,027 1,265 1,027

Participating loan interests 609 747 - -

Cash and cash equivalents 1,282 1,368 955 726

Other assets 6,203 3,438 6,095 2,959

Assets held for sale 2,241 - 1,015 -

Total assets 65,575 52,446 58,935 35,765

Corporate debt obligations 3,881 1,157 3,870 839

Asset-level debt obligations 23,125 20,483 23,275 15,455

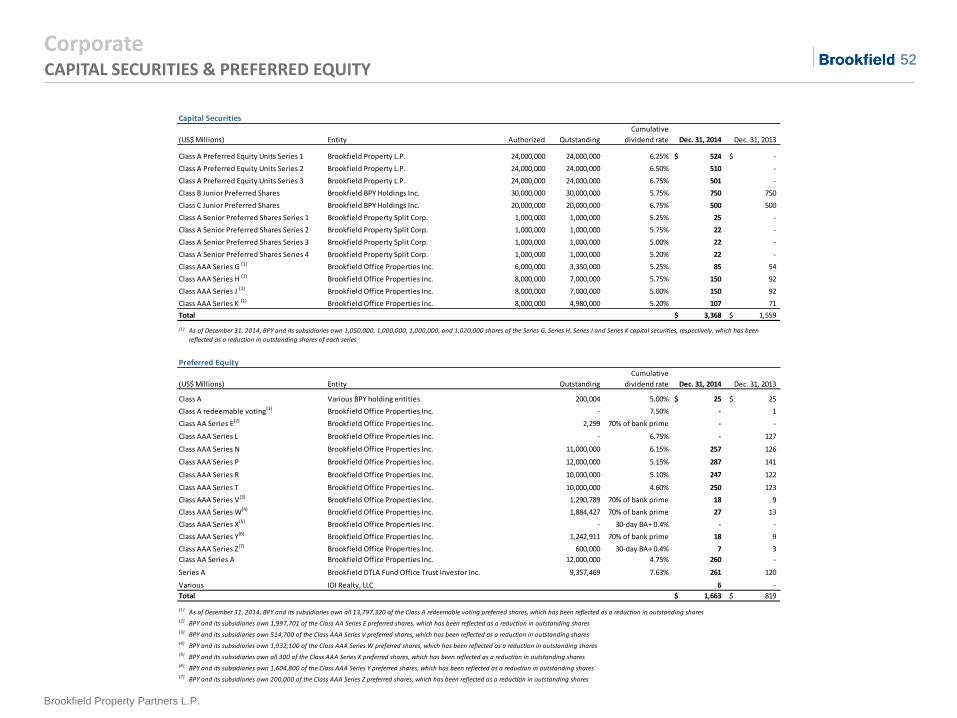

Capital securities 4,011 2,369 3,368 1,559

Deferred tax liabilities 2,639 1,532 2,594 1,084

Other liabilities 2,399 1,915 2,678 1,534

Liabilities associated with assets held for sale 1,221 - 525 -

Total liabilities 37,276 27,456 36,310 20,471

Preferred shares 1,674 1,639 1,663 819

Non-controlling interests in subsidiaries and properties 6,417 9,727 754 851

Non-controlling interests 8,091 11,366 2,417 1,670

Equity attributable to Unitholders 20,208$ 13,624$ 20,208$ 13,624$

ProportionateIFRS

9

Brookfield Property Partners L.P.

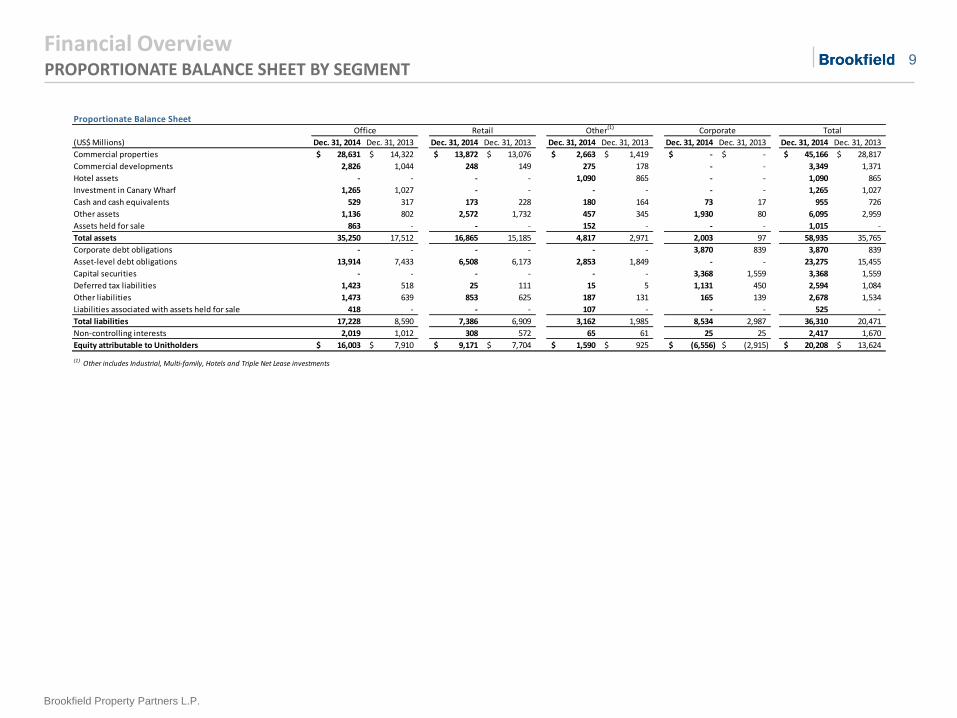

Financial Overview PROPORTIONATE BALANCE SHEET BY SEGMENT

Proportionate Balance Sheet

(US$ Millions) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

Commercial properties 28,631$ 14,322$ 13,872$ 13,076$ 2,663$ 1,419$ -$ -$ 45,166$ 28,817$

Commercial developments 2,826 1,044 248 149 275 178 - - 3,349 1,371

Hotel assets - - - - 1,090 865 - - 1,090 865

Investment in Canary Wharf 1,265 1,027 - - - - - - 1,265 1,027

Cash and cash equivalents 529 317 173 228 180 164 73 17 955 726

Other assets 1,136 802 2,572 1,732 457 345 1,930 80 6,095 2,959

Assets held for sale 863 - - - 152 - - - 1,015 -

Total assets 35,250 17,512 16,865 15,185 4,817 2,971 2,003 97 58,935 35,765

Corporate debt obligations - - - - - - 3,870 839 3,870 839

Asset-level debt obligations 13,914 7,433 6,508 6,173 2,853 1,849 - - 23,275 15,455

Capital securities - - - - - - 3,368 1,559 3,368 1,559

Deferred tax liabilities 1,423 518 25 111 15 5 1,131 450 2,594 1,084

Other liabilities 1,473 639 853 625 187 131 165 139 2,678 1,534

Liabilities associated with assets held for sale 418 - - - 107 - - - 525 -

Total liabilities 17,228 8,590 7,386 6,909 3,162 1,985 8,534 2,987 36,310 20,471

Non-controlling interests 2,019 1,012 308 572 65 61 25 25 2,417 1,670

Equity attributable to Unitholders 16,003$ 7,910$ 9,171$ 7,704$ 1,590$ 925$ (6,556)$ (2,915)$ 20,208$ 13,624$

(1) Other includes Industrial, Multi-family, Hotels and Triple Net Lease investments

TotalRetailOffice CorporateOther(1)

10

Brookfield Property Partners L.P.

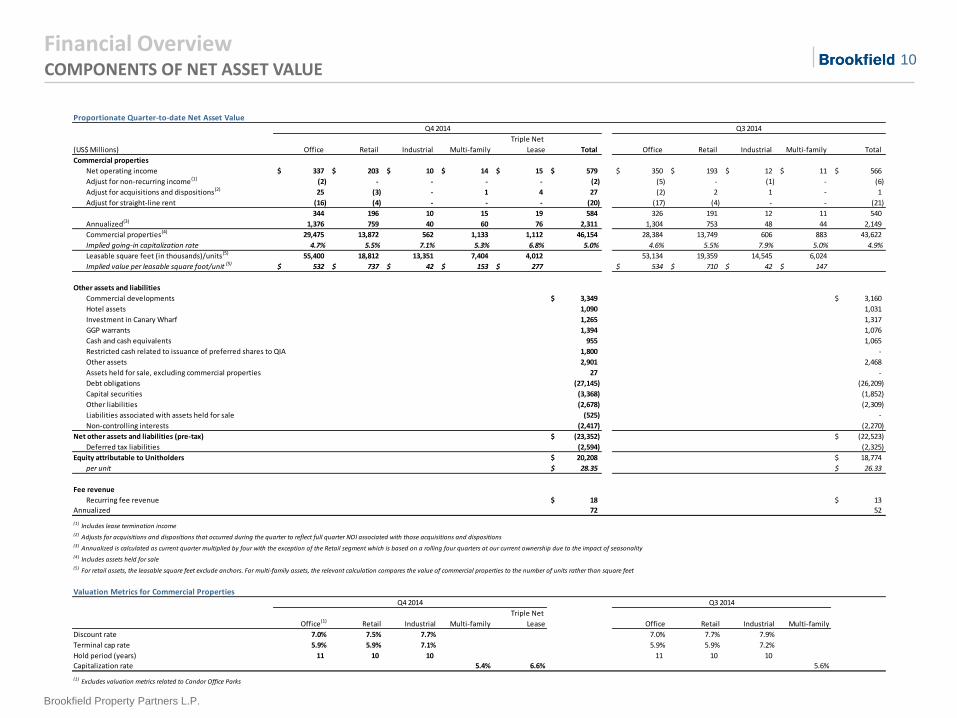

Financial Overview COMPONENTS OF NET ASSET VALUE

Proportionate Quarter-to-date Net Asset Value

(US$ Millions) Office Retail Industrial Multi-family

Triple Net

Lease Total Office Retail Industrial Multi-family Total

Commercial properties

Net operating income 337$ 203$ 10$ 14$ 15$ 579$ 350$ 193$ 12$ 11$ 566$

Adjust for non-recurring income (1) (2) - - - - (2) (5) - (1) - (6)

Adjust for acquisitions and dispositions(2) 25 (3) - 1 4 27 (2) 2 1 - 1

Adjust for straight-line rent (16) (4) - - - (20) (17) (4) - - (21)

344 196 10 15 19 584 326 191 12 11 540

Annualized(3) 1,376 759 40 60 76 2,311 1,304 753 48 44 2,149

Commercial properties(4) 29,475 13,872 562 1,133 1,112 46,154 28,384 13,749 606 883 43,622

Implied going-in capitalization rate 4.7% 5.5% 7.1% 5.3% 6.8% 5.0% 4.6% 5.5% 7.9% 5.0% 4.9%

Leasable square feet (in thousands)/units(5) 55,400 18,812 13,351 7,404 4,012 53,134 19,359 14,545 6,024

Implied value per leasable square foot/unit (5) 532$ 737$ 42$ 153$ 277$ 534$ 710$ 42$ 147$

Other assets and liabilities

Commercial developments 2,826$ 248$ 205$ 70$ -$ 3,349$ 3,160$

Hotel assets 1,090 1,031

Investment in Canary Wharf 1,265 1,317

GGP warrants 1,394 1,076

Cash and cash equivalents 955 1,065

Restricted cash related to issuance of preferred shares to QIA 1,800 -

Other assets 2,901 2,468

Assets held for sale, excluding commercial properties 27 -

Debt obligations (27,145) (26,209)

Capital securities (3,368) (1,852)

Other liabilities (2,678) (2,309)

Liabilities associated with assets held for sale (525) -

Non-controlling interests (2,417) (2,270)

Net other assets and liabilities (pre-tax) (23,352)$ (22,523)$

Deferred tax liabilities (2,594) (2,325)

Equity attributable to Unitholders 20,208$ 18,774$

per unit 28.35$ 26.33$

Fee revenue

Recurring fee revenue 12$ 6$ -$ -$ -$ 18$ 13$

Annualized 72 52

(1) Includes lease termination income(2) Adjusts for acquisitions and dispositions that occurred during the quarter to reflect full quarter NOI associated with those acquisitions and dispositions(3) Annualized is calculated as current quarter multiplied by four with the exception of the Retail segment which is based on a rolling four quarters at our current ownership due to the impact of seasonality(4) Includes assets held for sale(5) For retail assets, the leasable square feet exclude anchors. For multi-family assets, the relevant calculation compares the value of commercial properties to the number of units rather than square feet

Valuation Metrics for Commercial Properties

Office(1) Retail Industrial Multi-family

Triple Net

Lease Office Retail Industrial Multi-family

Discount rate 7.0% 7.5% 7.7% 7.0% 7.7% 7.9%

Terminal cap rate 5.9% 5.9% 7.1% 5.9% 5.9% 7.2%

Hold period (years) 11 10 10 11 10 10

Capitalization rate 5.4% 6.6% 5.6%

(1) Excludes valuation metrics related to Candor Office Parks

Q3 2014Q4 2014

Q3 2014Q4 2014

11

Brookfield Property Partners L.P.

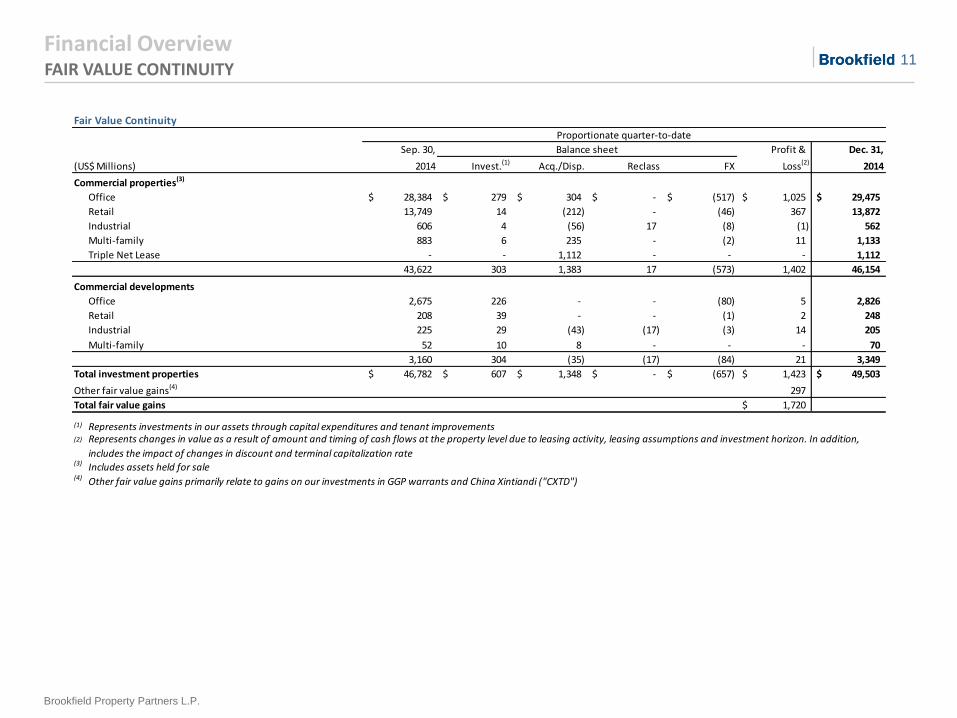

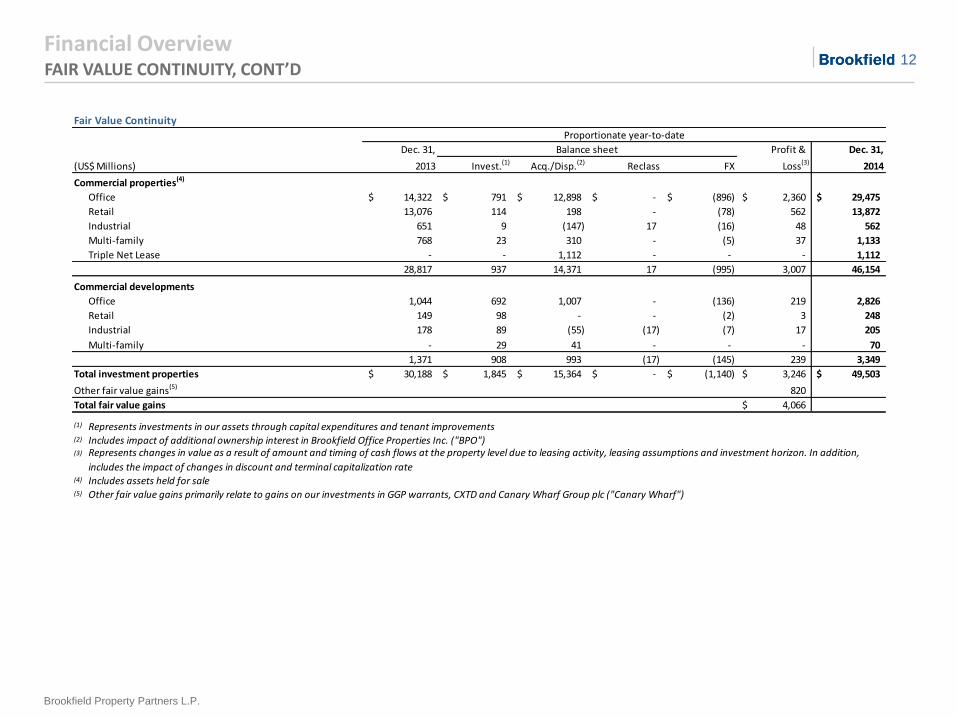

Financial Overview FAIR VALUE CONTINUITY

Fair Value Continuity

Sep. 30, Profit & Dec. 31,

(US$ Millions) 2014 Invest.(1) Acq./Disp. Reclass FX Loss(2) 2014

Commercial properties(3)

Office 28,384$ 279$ 304$ -$ (517)$ 1,025$ 29,475$

Retail 13,749 14 (212) - (46) 367 13,872

Industrial 606 4 (56) 17 (8) (1) 562

Multi-family 883 6 235 - (2) 11 1,133

Triple Net Lease - - 1,112 - - - 1,112

43,622 303 1,383 17 (573) 1,402 46,154

Commercial developments

Office 2,675 226 - - (80) 5 2,826

Retail 208 39 - - (1) 2 248

Industrial 225 29 (43) (17) (3) 14 205

Multi-family 52 10 8 - - - 70

3,160 304 (35) (17) (84) 21 3,349

Total investment properties 46,782$ 607$ 1,348$ -$ (657)$ 1,423$ 49,503$

Other fair value gains(4) 297

Total fair value gains 1,720$

(1) Represents investments in our assets through capital expenditures and tenant improvements(2)

(3) Includes assets held for sale(4) Other fair value gains primarily relate to gains on our investments in GGP warrants and China Xintiandi ("CXTD")

Proportionate quarter-to-date

Balance sheet

Represents changes in value as a result of amount and timing of cash flows at the property level due to leasing activity, leasing assumptions and investment horizon. In addition,

includes the impact of changes in discount and terminal capitalization rate

12

Brookfield Property Partners L.P.

Financial Overview FAIR VALUE CONTINUITY, CONT’D

Fair Value Continuity

Dec. 31, Profit & Dec. 31,

(US$ Millions) 2013 Invest.(1) Acq./Disp.(2) Reclass FX Loss(3) 2014

Commercial properties(4)

Office 14,322$ 791$ 12,898$ -$ (896)$ 2,360$ 29,475$

Retail 13,076 114 198 - (78) 562 13,872

Industrial 651 9 (147) 17 (16) 48 562

Multi-family 768 23 310 - (5) 37 1,133

Triple Net Lease - - 1,112 - - - 1,112

28,817 937 14,371 17 (995) 3,007 46,154

Commercial developments

Office 1,044 692 1,007 - (136) 219 2,826

Retail 149 98 - - (2) 3 248

Industrial 178 89 (55) (17) (7) 17 205

Multi-family - 29 41 - - - 70

1,371 908 993 (17) (145) 239 3,349

Total investment properties 30,188$ 1,845$ 15,364$ -$ (1,140)$ 3,246$ 49,503$

Other fair value gains(5) 820

Total fair value gains 4,066$

(1) Represents investments in our assets through capital expenditures and tenant improvements(2) Includes impact of additional ownership interest in Brookfield Office Properties Inc. ("BPO")(3)

(4) Includes assets held for sale(5) Other fair value gains primarily relate to gains on our investments in GGP warrants, CXTD and Canary Wharf Group plc ("Canary Wharf")

Proportionate year-to-date

Balance sheet

Represents changes in value as a result of amount and timing of cash flows at the property level due to leasing activity, leasing assumptions and investment horizon. In addition,

includes the impact of changes in discount and terminal capitalization rate

13

Brookfield Property Partners L.P.

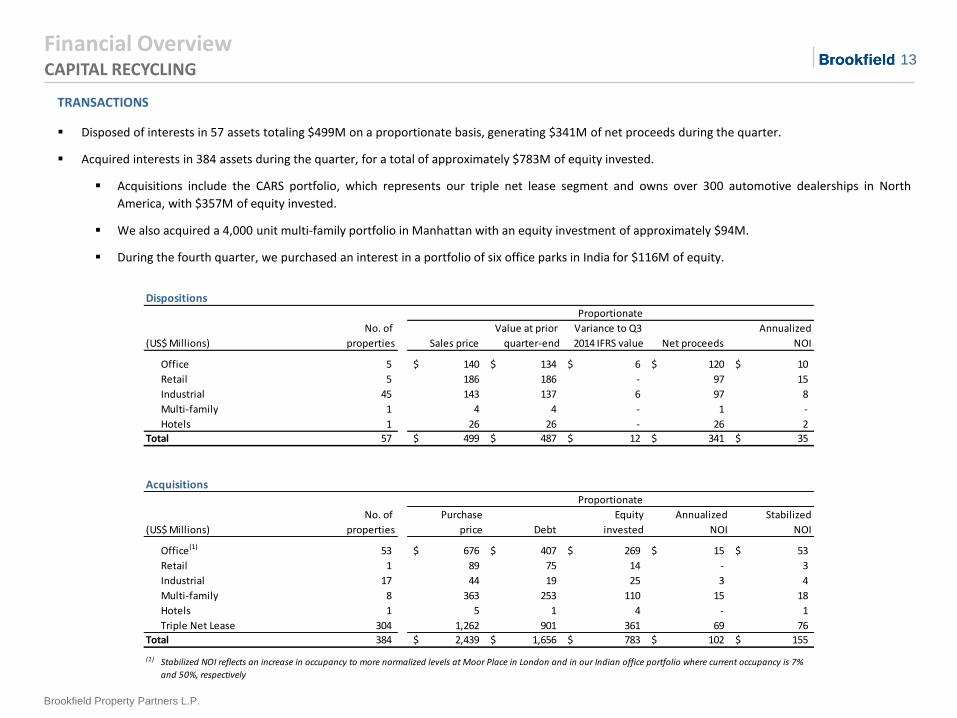

Financial Overview CAPITAL RECYCLING

TRANSACTIONS

Disposed of interests in 57 assets totaling $499M on a proportionate basis, generating $341M of net proceeds during the quarter.

Acquired interests in 384 assets during the quarter, for a total of approximately $783M of equity invested.

Acquisitions include the CARS portfolio, which represents our triple net lease segment and owns over 300 automotive dealerships in North

America, with $357M of equity invested.

We also acquired a 4,000 unit multi-family portfolio in Manhattan with an equity investment of approximately $94M.

During the fourth quarter, we purchased an interest in a portfolio of six office parks in India for $116M of equity.

Dispositions

(US$ Millions) Sales price

Value at prior

quarter-end

Variance to Q3

2014 IFRS value Net proceeds

Annualized

NOI

Office 5 140$ 134$ 6$ 120$ 10$

Retail 5 186 186 - 97 15

Industrial 45 143 137 6 97 8

Multi-family 1 4 4 - 1 -

Hotels 1 26 26 - 26 2

Total 57 499$ 487$ 12$ 341$ 35$

Acquisitions

(US$ Millions)

Purchase

price Debt

Equity

invested

Annualized

NOI

Stabilized

NOI

Office(1) 53 676$ 407$ 269$ 15$ 53$

Retail 1 89 75 14 - 3

Industrial 17 44 19 25 3 4

Multi-family 8 363 253 110 15 18

Hotels 1 5 1 4 - 1

Triple Net Lease 304 1,262 901 361 69 76

Total 384 2,439$ 1,656$ 783$ 102$ 155$

(1) Stabilized NOI reflects an increase in occupancy to more normalized levels at Moor Place in London and in our Indian office portfolio where current occupancy is 7%

and 50%, respectively

Proportionate

Proportionate

No. of

properties

No. of

properties

14

Brookfield Property Partners L.P.

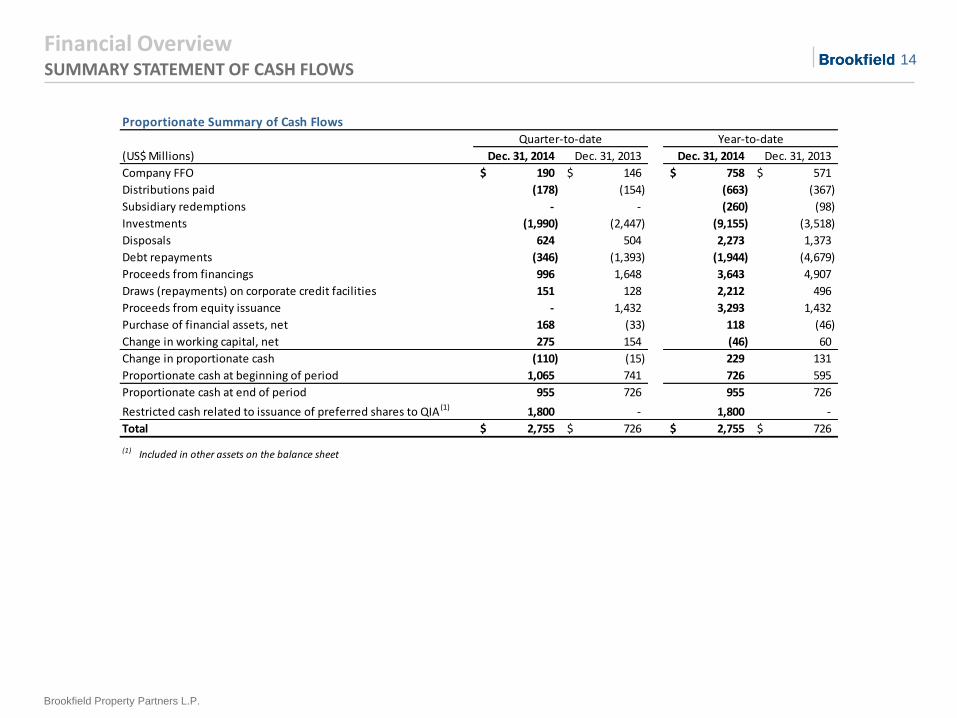

Financial Overview SUMMARY STATEMENT OF CASH FLOWS

Proportionate Summary of Cash Flows

(US$ Millions) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

Company FFO 190$ 146$ 758$ 571$

Distributions paid (178) (154) (663) (367)

Subsidiary redemptions - - (260) (98)

Investments (1,990) (2,447) (9,155) (3,518)

Disposals 624 504 2,273 1,373

Debt repayments (346) (1,393) (1,944) (4,679)

Proceeds from financings 996 1,648 3,643 4,907

Draws (repayments) on corporate credit facilities 151 128 2,212 496

Proceeds from equity issuance - 1,432 3,293 1,432

Purchase of financial assets, net 168 (33) 118 (46)

Change in working capital, net 275 154 (46) 60

Change in proportionate cash (110) (15) 229 131

Proportionate cash at beginning of period 1,065 741 726 595

Proportionate cash at end of period 955 726 955 726

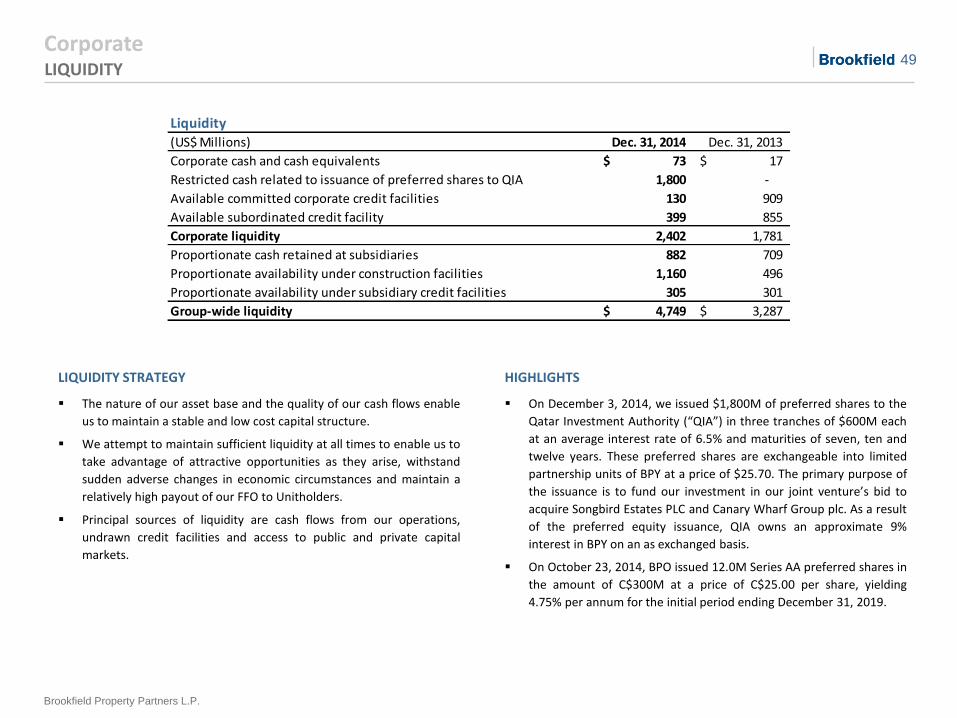

Restricted cash related to issuance of preferred shares to QIA (1) 1,800 - 1,800 -

Total 2,755$ 726$ 2,755$ 726$

(1) Included in other assets on the balance sheet

Quarter-to-date Year-to-date

Office Segment

16

Brookfield Property Partners L.P.

Office Segment

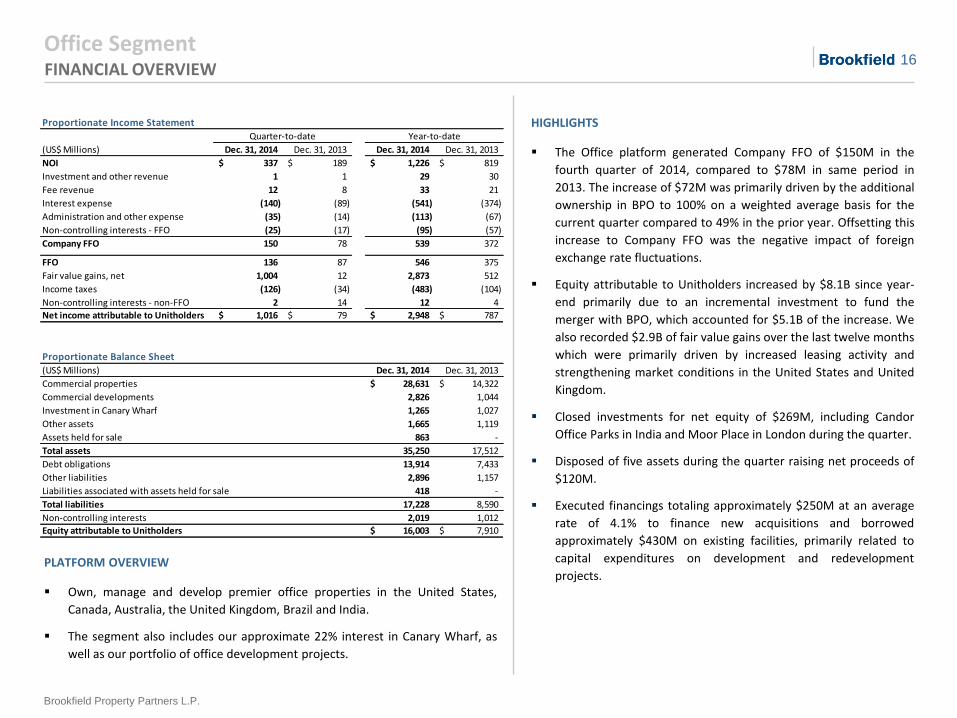

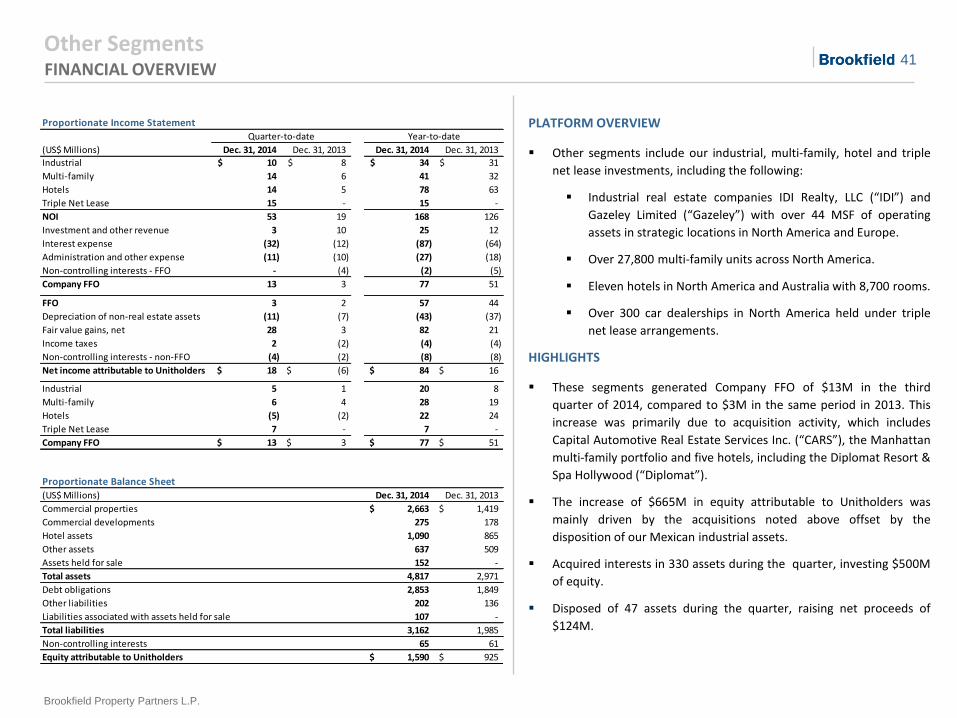

HIGHLIGHTS

The Office platform generated Company FFO of $150M in the

fourth quarter of 2014, compared to $78M in same period in

2013. The increase of $72M was primarily driven by the additional

ownership in BPO to 100% on a weighted average basis for the

current quarter compared to 49% in the prior year. Offsetting this

increase to Company FFO was the negative impact of foreign

exchange rate fluctuations.

Equity attributable to Unitholders increased by $8.1B since year-

end primarily due to an incremental investment to fund the

merger with BPO, which accounted for $5.1B of the increase. We

also recorded $2.9B of fair value gains over the last twelve months

which were primarily driven by increased leasing activity and

strengthening market conditions in the United States and United

Kingdom.

Closed investments for net equity of $269M, including Candor

Office Parks in India and Moor Place in London during the quarter.

Disposed of five assets during the quarter raising net proceeds of

$120M.

Executed financings totaling approximately $250M at an average

rate of 4.1% to finance new acquisitions and borrowed

approximately $430M on existing facilities, primarily related to

capital expenditures on development and redevelopment

projects.

FINANCIAL OVERVIEW

PLATFORM OVERVIEW

Own, manage and develop premier office properties in the United States,

Canada, Australia, the United Kingdom, Brazil and India.

The segment also includes our approximate 22% interest in Canary Wharf, as

well as our portfolio of office development projects.

Proportionate Income Statement

(US$ Millions) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

NOI 337$ 189$ 1,226$ 819$

Investment and other revenue 1 1 29 30

Fee revenue 12 8 33 21

Interest expense (140) (89) (541) (374)

Administration and other expense (35) (14) (113) (67)

Non-controlling interests - FFO (25) (17) (95) (57)

Company FFO 150 78 539 372

FFO 136 87 546 375

Fair value gains, net 1,004 12 2,873 512

Income taxes (126) (34) (483) (104)

Non-controlling interests - non-FFO 2 14 12 4

Net income attributable to Unitholders 1,016$ 79$ 2,948$ 787$

Proportionate Balance Sheet(US$ Millions) Dec. 31, 2014 Dec. 31, 2013

Commercial properties 28,631$ 14,322$

Commercial developments 2,826 1,044

Investment in Canary Wharf 1,265 1,027

Other assets 1,665 1,119

Assets held for sale 863 -

Total assets 35,250 17,512

Debt obligations 13,914 7,433

Other liabilities 2,896 1,157

Liabilities associated with assets held for sale 418 -

Total liabilities 17,228 8,590

Non-controlling interests 2,019 1,012

Equity attributable to Unitholders 16,003$ 7,910$

Quarter-to-date Year-to-date

17

Brookfield Property Partners L.P.

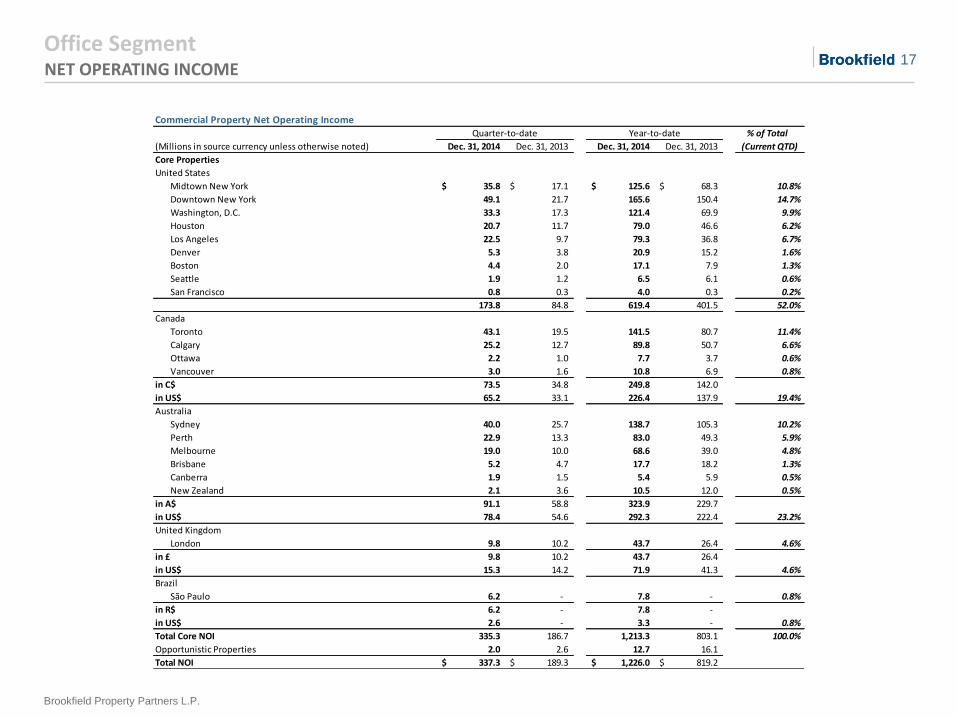

Office Segment NET OPERATING INCOME

Commercial Property Net Operating Income% of Total

Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013 (Current QTD)

Core Properties

United States

Midtown New York 35.8$ 17.1$ 125.6$ 68.3$ 10.8%

Downtown New York 49.1 21.7 165.6 150.4 14.7%

Washington, D.C. 33.3 17.3 121.4 69.9 9.9%

Houston 20.7 11.7 79.0 46.6 6.2%

Los Angeles 22.5 9.7 79.3 36.8 6.7%

Denver 5.3 3.8 20.9 15.2 1.6%

Boston 4.4 2.0 17.1 7.9 1.3%

Seattle 1.9 1.2 6.5 6.1 0.6%

San Francisco 0.8 0.3 4.0 0.3 0.2%

173.8 84.8 619.4 401.5 52.0%

Canada

Toronto 43.1 19.5 141.5 80.7 11.4%

Calgary 25.2 12.7 89.8 50.7 6.6%

Ottawa 2.2 1.0 7.7 3.7 0.6%

Vancouver 3.0 1.6 10.8 6.9 0.8%

in C$ 73.5 34.8 249.8 142.0

in US$ 65.2 33.1 226.4 137.9 19.4%

Australia

Sydney 40.0 25.7 138.7 105.3 10.2%

Perth 22.9 13.3 83.0 49.3 5.9%

Melbourne 19.0 10.0 68.6 39.0 4.8%

Brisbane 5.2 4.7 17.7 18.2 1.3%

Canberra 1.9 1.5 5.4 5.9 0.5%

New Zealand 2.1 3.6 10.5 12.0 0.5%

in A$ 91.1 58.8 323.9 229.7

in US$ 78.4 54.6 292.3 222.4 23.2%

United Kingdom

London 9.8 10.2 43.7 26.4 4.6%

in £ 9.8 10.2 43.7 26.4

in US$ 15.3 14.2 71.9 41.3 4.6%

Brazil

São Paulo 6.2 - 7.8 - 0.8%

in R$ 6.2 - 7.8 -

in US$ 2.6 - 3.3 - 0.8%

Total Core NOI 335.3 186.7 1,213.3 803.1 100.0%

Opportunistic Properties 2.0 2.6 12.7 16.1

Total NOI 337.3$ 189.3$ 1,226.0$ 819.2$

Quarter-to-date Year-to-date

(Millions in source currency unless otherwise noted)

18

Brookfield Property Partners L.P.

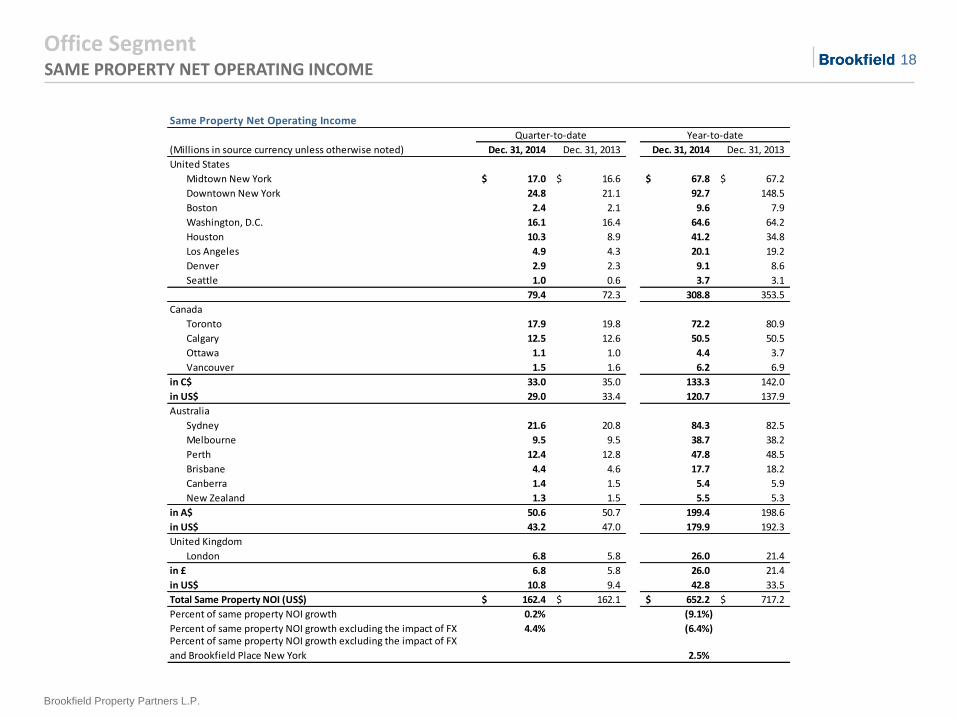

Office Segment SAME PROPERTY NET OPERATING INCOME

Same Property Net Operating Income

Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

United States

Midtown New York 17.0$ 16.6$ 67.8$ 67.2$

Downtown New York 24.8 21.1 92.7 148.5

Boston 2.4 2.1 9.6 7.9

Washington, D.C. 16.1 16.4 64.6 64.2

Houston 10.3 8.9 41.2 34.8

Los Angeles 4.9 4.3 20.1 19.2

Denver 2.9 2.3 9.1 8.6

Seattle 1.0 0.6 3.7 3.1

79.4 72.3 308.8 353.5

Canada

Toronto 17.9 19.8 72.2 80.9

Calgary 12.5 12.6 50.5 50.5

Ottawa 1.1 1.0 4.4 3.7

Vancouver 1.5 1.6 6.2 6.9

in C$ 33.0 35.0 133.3 142.0

in US$ 29.0 33.4 120.7 137.9

Australia

Sydney 21.6 20.8 84.3 82.5

Melbourne 9.5 9.5 38.7 38.2

Perth 12.4 12.8 47.8 48.5

Brisbane 4.4 4.6 17.7 18.2

Canberra 1.4 1.5 5.4 5.9

New Zealand 1.3 1.5 5.5 5.3

in A$ 50.6 50.7 199.4 198.6

in US$ 43.2 47.0 179.9 192.3

United Kingdom

London 6.8 5.8 26.0 21.4

in £ 6.8 5.8 26.0 21.4

in US$ 10.8 9.4 42.8 33.5

Total Same Property NOI (US$) 162.4$ 162.1$ 652.2$ 717.2$

Percent of same property NOI growth 0.2% (9.1%)

Percent of same property NOI growth excluding the impact of FX 4.4% (6.4%)

2.5%

(Millions in source currency unless otherwise noted)

Quarter-to-date Year-to-date

Percent of same property NOI growth excluding the impact of FX

and Brookfield Place New York

19

Brookfield Property Partners L.P.

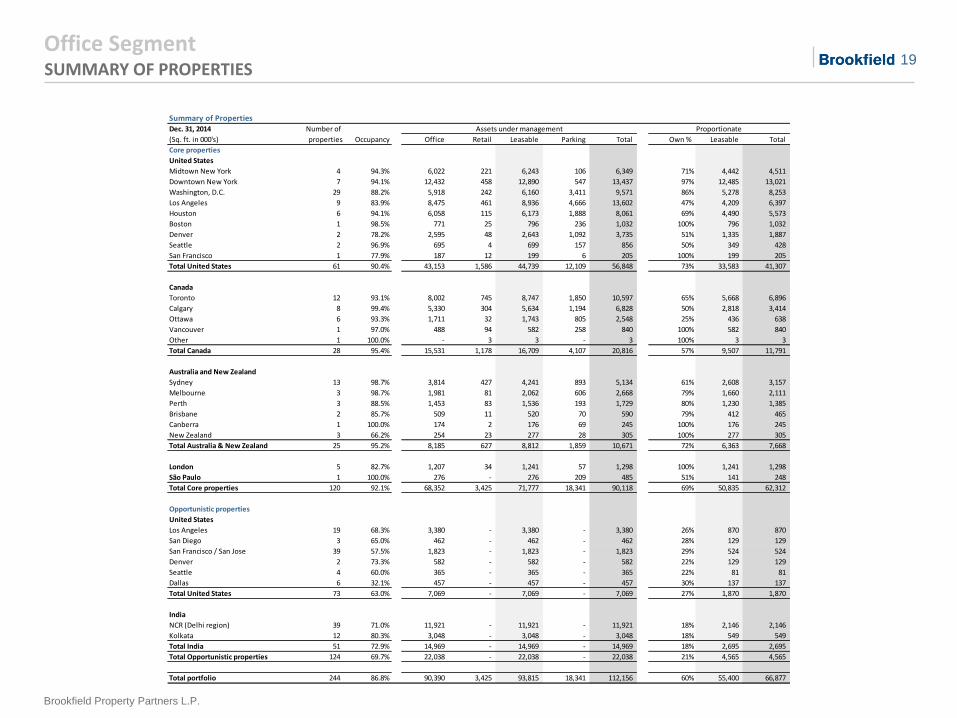

Office Segment SUMMARY OF PROPERTIES

Summary of Properties

Dec. 31, 2014

(Sq. ft. in 000's) Occupancy Office Retail Leasable Parking Total Own % Leasable Total

Core properties

United States

Midtown New York 4 94.3% 6,022 221 6,243 106 6,349 71% 4,442 4,511

Downtown New York 7 94.1% 12,432 458 12,890 547 13,437 97% 12,485 13,021

Washington, D.C. 29 88.2% 5,918 242 6,160 3,411 9,571 86% 5,278 8,253

Los Angeles 9 83.9% 8,475 461 8,936 4,666 13,602 47% 4,209 6,397

Houston 6 94.1% 6,058 115 6,173 1,888 8,061 69% 4,490 5,573

Boston 1 98.5% 771 25 796 236 1,032 100% 796 1,032

Denver 2 78.2% 2,595 48 2,643 1,092 3,735 51% 1,335 1,887

Seattle 2 96.9% 695 4 699 157 856 50% 349 428

San Francisco 1 77.9% 187 12 199 6 205 100% 199 205

Total United States 61 90.4% 43,153 1,586 44,739 12,109 56,848 73% 33,583 41,307

Canada

Toronto 12 93.1% 8,002 745 8,747 1,850 10,597 65% 5,668 6,896

Calgary 8 99.4% 5,330 304 5,634 1,194 6,828 50% 2,818 3,414

Ottawa 6 93.3% 1,711 32 1,743 805 2,548 25% 436 638

Vancouver 1 97.0% 488 94 582 258 840 100% 582 840

Other 1 100.0% - 3 3 - 3 100% 3 3

Total Canada 28 95.4% 15,531 1,178 16,709 4,107 20,816 57% 9,507 11,791

Australia and New Zealand

Sydney 13 98.7% 3,814 427 4,241 893 5,134 61% 2,608 3,157

Melbourne 3 98.7% 1,981 81 2,062 606 2,668 79% 1,660 2,111

Perth 3 88.5% 1,453 83 1,536 193 1,729 80% 1,230 1,385

Brisbane 2 85.7% 509 11 520 70 590 79% 412 465

Canberra 1 100.0% 174 2 176 69 245 100% 176 245

New Zealand 3 66.2% 254 23 277 28 305 100% 277 305

Total Australia & New Zealand 25 95.2% 8,185 627 8,812 1,859 10,671 72% 6,363 7,668

London 5 82.7% 1,207 34 1,241 57 1,298 100% 1,241 1,298

São Paulo 1 100.0% 276 - 276 209 485 51% 141 248

Total Core properties 120 92.1% 68,352 3,425 71,777 18,341 90,118 69% 50,835 62,312

Opportunistic properties

United States

Los Angeles 19 68.3% 3,380 - 3,380 - 3,380 26% 870 870

San Diego 3 65.0% 462 - 462 - 462 28% 129 129

San Francisco / San Jose 39 57.5% 1,823 - 1,823 - 1,823 29% 524 524

Denver 2 73.3% 582 - 582 - 582 22% 129 129

Seattle 4 60.0% 365 - 365 - 365 22% 81 81

Dallas 6 32.1% 457 - 457 - 457 30% 137 137

Total United States 73 63.0% 7,069 - 7,069 - 7,069 27% 1,870 1,870

India

NCR (Delhi region) 39 71.0% 11,921 - 11,921 - 11,921 18% 2,146 2,146

Kolkata 12 80.3% 3,048 - 3,048 - 3,048 18% 549 549

Total India 51 72.9% 14,969 - 14,969 - 14,969 18% 2,695 2,695

Total Opportunistic properties 124 69.7% 22,038 - 22,038 - 22,038 21% 4,565 4,565

Total portfolio 244 86.8% 90,390 3,425 93,815 18,341 112,156 60% 55,400 66,877

Proportionate Number of

properties

Assets under management

20

Brookfield Property Partners L.P.

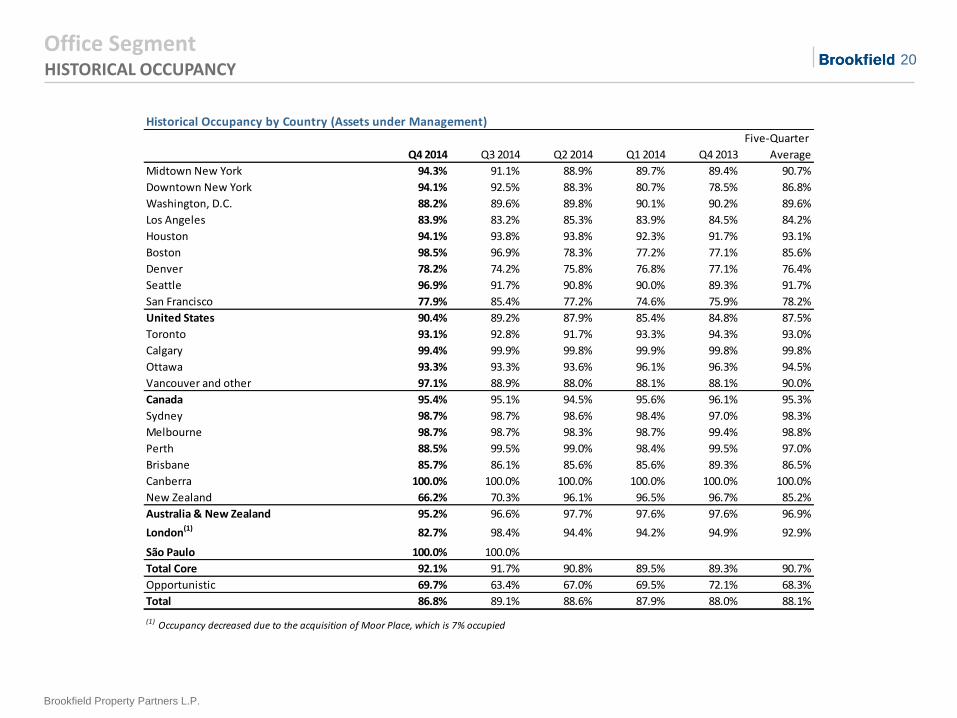

Office Segment HISTORICAL OCCUPANCY

Historical Occupancy by Country (Assets under Management)

Q4 2014 Q3 2014 Q2 2014 Q1 2014 Q4 2013

Five-Quarter

Average

Midtown New York 94.3% 91.1% 88.9% 89.7% 89.4% 90.7%

Downtown New York 94.1% 92.5% 88.3% 80.7% 78.5% 86.8%

Washington, D.C. 88.2% 89.6% 89.8% 90.1% 90.2% 89.6%

Los Angeles 83.9% 83.2% 85.3% 83.9% 84.5% 84.2%

Houston 94.1% 93.8% 93.8% 92.3% 91.7% 93.1%

Boston 98.5% 96.9% 78.3% 77.2% 77.1% 85.6%

Denver 78.2% 74.2% 75.8% 76.8% 77.1% 76.4%

Seattle 96.9% 91.7% 90.8% 90.0% 89.3% 91.7%

San Francisco 77.9% 85.4% 77.2% 74.6% 75.9% 78.2%

United States 90.4% 89.2% 87.9% 85.4% 84.8% 87.5%

Toronto 93.1% 92.8% 91.7% 93.3% 94.3% 93.0%

Calgary 99.4% 99.9% 99.8% 99.9% 99.8% 99.8%

Ottawa 93.3% 93.3% 93.6% 96.1% 96.3% 94.5%

Vancouver and other 97.1% 88.9% 88.0% 88.1% 88.1% 90.0%

Canada 95.4% 95.1% 94.5% 95.6% 96.1% 95.3%

Sydney 98.7% 98.7% 98.6% 98.4% 97.0% 98.3%

Melbourne 98.7% 98.7% 98.3% 98.7% 99.4% 98.8%

Perth 88.5% 99.5% 99.0% 98.4% 99.5% 97.0%

Brisbane 85.7% 86.1% 85.6% 85.6% 89.3% 86.5%

Canberra 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

New Zealand 66.2% 70.3% 96.1% 96.5% 96.7% 85.2%

Australia & New Zealand 95.2% 96.6% 97.7% 97.6% 97.6% 96.9%

London(1) 82.7% 98.4% 94.4% 94.2% 94.9% 92.9%

São Paulo 100.0% 100.0%

Total Core 92.1% 91.7% 90.8% 89.5% 89.3% 90.7%

Opportunistic 69.7% 63.4% 67.0% 69.5% 72.1% 68.3%

Total 86.8% 89.1% 88.6% 87.9% 88.0% 88.1%

(1) Occupancy decreased due to the acquisition of Moor Place, which is 7% occupied

21

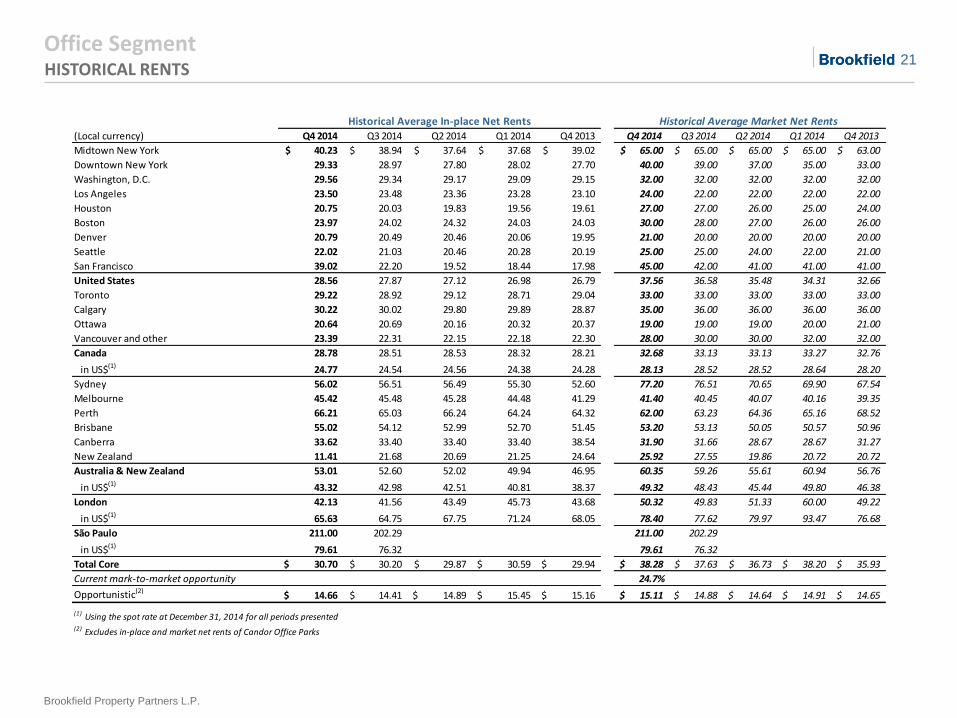

Brookfield Property Partners L.P.

Office Segment HISTORICAL RENTS

(Local currency) Q4 2014 Q3 2014 Q2 2014 Q1 2014 Q4 2013 Q4 2014 Q3 2014 Q2 2014 Q1 2014 Q4 2013

Midtown New York 40.23$ 38.94$ 37.64$ 37.68$ 39.02$ 65.00$ 65.00$ 65.00$ 65.00$ 63.00$

Downtown New York 29.33 28.97 27.80 28.02 27.70 40.00 39.00 37.00 35.00 33.00

Washington, D.C. 29.56 29.34 29.17 29.09 29.15 32.00 32.00 32.00 32.00 32.00

Los Angeles 23.50 23.48 23.36 23.28 23.10 24.00 22.00 22.00 22.00 22.00

Houston 20.75 20.03 19.83 19.56 19.61 27.00 27.00 26.00 25.00 24.00

Boston 23.97 24.02 24.32 24.03 24.03 30.00 28.00 27.00 26.00 26.00

Denver 20.79 20.49 20.46 20.06 19.95 21.00 20.00 20.00 20.00 20.00

Seattle 22.02 21.03 20.46 20.28 20.19 25.00 25.00 24.00 22.00 21.00

San Francisco 39.02 22.20 19.52 18.44 17.98 45.00 42.00 41.00 41.00 41.00

United States 28.56 27.87 27.12 26.98 26.79 37.56 36.58 35.48 34.31 32.66

Toronto 29.22 28.92 29.12 28.71 29.04 33.00 33.00 33.00 33.00 33.00

Calgary 30.22 30.02 29.80 29.89 28.87 35.00 36.00 36.00 36.00 36.00

Ottawa 20.64 20.69 20.16 20.32 20.37 19.00 19.00 19.00 20.00 21.00

Vancouver and other 23.39 22.31 22.15 22.18 22.30 28.00 30.00 30.00 32.00 32.00

Canada 28.78 28.51 28.53 28.32 28.21 32.68 33.13 33.13 33.27 32.76

in US$(1) 24.77 24.54 24.56 24.38 24.28 28.13 28.52 28.52 28.64 28.20

Sydney 56.02 56.51 56.49 55.30 52.60 77.20 76.51 70.65 69.90 67.54

Melbourne 45.42 45.48 45.28 44.48 41.29 41.40 40.45 40.07 40.16 39.35

Perth 66.21 65.03 66.24 64.24 64.32 62.00 63.23 64.36 65.16 68.52

Brisbane 55.02 54.12 52.99 52.70 51.45 53.20 53.13 50.05 50.57 50.96

Canberra 33.62 33.40 33.40 33.40 38.54 31.90 31.66 28.67 28.67 31.27

New Zealand 11.41 21.68 20.69 21.25 24.64 25.92 27.55 19.86 20.72 20.72

Australia & New Zealand 53.01 52.60 52.02 49.94 46.95 60.35 59.26 55.61 60.94 56.76

in US$(1) 43.32 42.98 42.51 40.81 38.37 49.32 48.43 45.44 49.80 46.38

London 42.13 41.56 43.49 45.73 43.68 50.32 49.83 51.33 60.00 49.22

in US$(1) 65.63 64.75 67.75 71.24 68.05 78.40 77.62 79.97 93.47 76.68

São Paulo 211.00 202.29 211.00 202.29

in US$(1) 79.61 76.32 79.61 76.32

Total Core 30.70$ 30.20$ 29.87$ 30.59$ 29.94$ 38.28$ 37.63$ 36.73$ 38.20$ 35.93$

Current mark-to-market opportunity 24.7%

Opportunistic(2)14.66$ 14.41$ 14.89$ 15.45$ 15.16$ 15.11$ 14.88$ 14.64$ 14.91$ 14.65$

(1) Using the spot rate at December 31, 2014 for all periods presented(2) Excludes in-place and market net rents of Candor Office Parks

Historical Average In-place Net Rents Historical Average Market Net Rents

22

Brookfield Property Partners L.P.

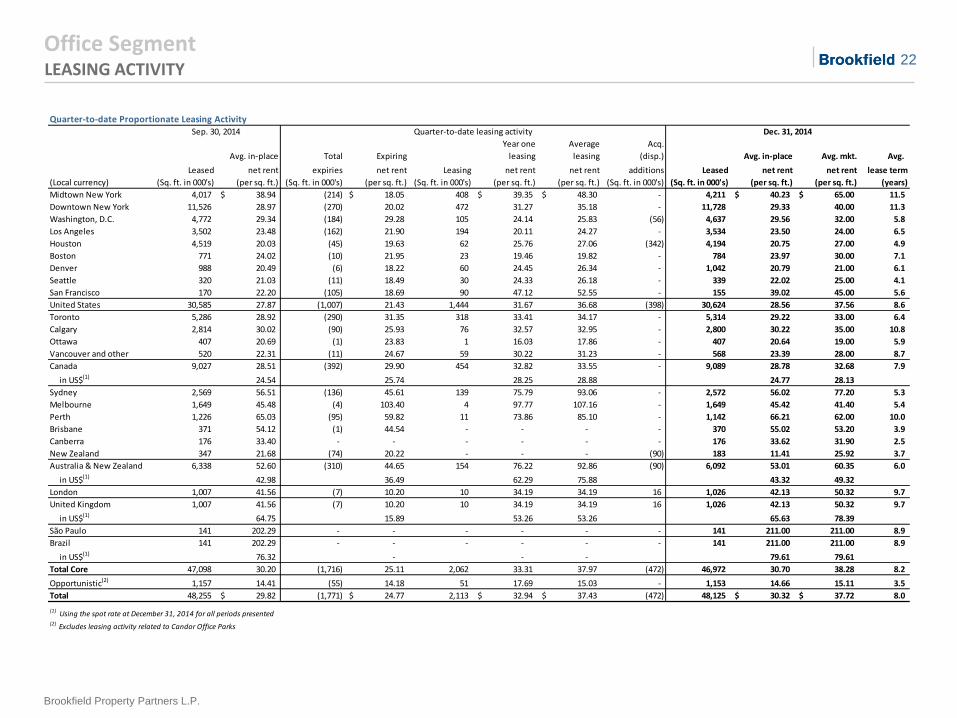

Office Segment LEASING ACTIVITY

Quarter-to-date Proportionate Leasing Activity

Year one Average Acq.

Avg. in-place Total Expiring leasing leasing (disp.) Avg. in-place Avg. mkt. Avg.

Leased net rent expiries net rent Leasing net rent net rent additions Leased net rent net rent lease term

(Local currency) (Sq. ft. in 000's) (per sq. ft.) (Sq. ft. in 000's) (per sq. ft.) (Sq. ft. in 000's) (per sq. ft.) (per sq. ft.) (Sq. ft. in 000's) (Sq. ft. in 000's) (per sq. ft.) (per sq. ft.) (years)

Midtown New York 4,017 38.94$ (214) 18.05$ 408 39.35$ 48.30$ - 4,211 40.23$ 65.00$ 11.5

Downtown New York 11,526 28.97 (270) 20.02 472 31.27 35.18 - 11,728 29.33 40.00 11.3

Washington, D.C. 4,772 29.34 (184) 29.28 105 24.14 25.83 (56) 4,637 29.56 32.00 5.8

Los Angeles 3,502 23.48 (162) 21.90 194 20.11 24.27 - 3,534 23.50 24.00 6.5

Houston 4,519 20.03 (45) 19.63 62 25.76 27.06 (342) 4,194 20.75 27.00 4.9

Boston 771 24.02 (10) 21.95 23 19.46 19.82 - 784 23.97 30.00 7.1

Denver 988 20.49 (6) 18.22 60 24.45 26.34 - 1,042 20.79 21.00 6.1

Seattle 320 21.03 (11) 18.49 30 24.33 26.18 - 339 22.02 25.00 4.1

San Francisco 170 22.20 (105) 18.69 90 47.12 52.55 - 155 39.02 45.00 5.6

United States 30,585 27.87 (1,007) 21.43 1,444 31.67 36.68 (398) 30,624 28.56 37.56 8.6

Toronto 5,286 28.92 (290) 31.35 318 33.41 34.17 - 5,314 29.22 33.00 6.4

Calgary 2,814 30.02 (90) 25.93 76 32.57 32.95 - 2,800 30.22 35.00 10.8

Ottawa 407 20.69 (1) 23.83 1 16.03 17.86 - 407 20.64 19.00 5.9

Vancouver and other 520 22.31 (11) 24.67 59 30.22 31.23 - 568 23.39 28.00 8.7

Canada 9,027 28.51 (392) 29.90 454 32.82 33.55 - 9,089 28.78 32.68 7.9

in US$(1) 24.54 25.74 28.25 28.88 24.77 28.13

Sydney 2,569 56.51 (136) 45.61 139 75.79 93.06 - 2,572 56.02 77.20 5.3

Melbourne 1,649 45.48 (4) 103.40 4 97.77 107.16 - 1,649 45.42 41.40 5.4

Perth 1,226 65.03 (95) 59.82 11 73.86 85.10 - 1,142 66.21 62.00 10.0

Brisbane 371 54.12 (1) 44.54 - - - - 370 55.02 53.20 3.9

Canberra 176 33.40 - - - - - - 176 33.62 31.90 2.5

New Zealand 347 21.68 (74) 20.22 - - - (90) 183 11.41 25.92 3.7

Australia & New Zealand 6,338 52.60 (310) 44.65 154 76.22 92.86 (90) 6,092 53.01 60.35 6.0

in US$(1) 42.98 36.49 62.29 75.88 43.32 49.32

London 1,007 41.56 (7) 10.20 10 34.19 34.19 16 1,026 42.13 50.32 9.7

United Kingdom 1,007 41.56 (7) 10.20 10 34.19 34.19 16 1,026 42.13 50.32 9.7

in US$(1) 64.75 15.89 53.26 53.26 65.63 78.39

São Paulo 141 202.29 - - - - - - 141 211.00 211.00 8.9

Brazil 141 202.29 - - - - - - 141 211.00 211.00 8.9

in US$(1) 76.32 - - - 79.61 79.61

Total Core 47,098 30.20 (1,716) 25.11 2,062 33.31 37.97 (472) 46,972 30.70 38.28 8.2

Opportunistic(2) 1,157 14.41 (55) 14.18 51 17.69 15.03 - 1,153 14.66 15.11 3.5

Total 48,255 29.82$ (1,771) 24.77$ 2,113 32.94$ 37.43$ (472) 48,125 30.32$ 37.72$ 8.0

(1) Restated for the impact of foreign exchangeUsing the spot rate at December 31, 2014 for all periods presented(2) Excludes leasing activity related to Candor Office Parks

Sep. 30, 2014 Quarter-to-date leasing activity Dec. 31, 2014

23

Brookfield Property Partners L.P.

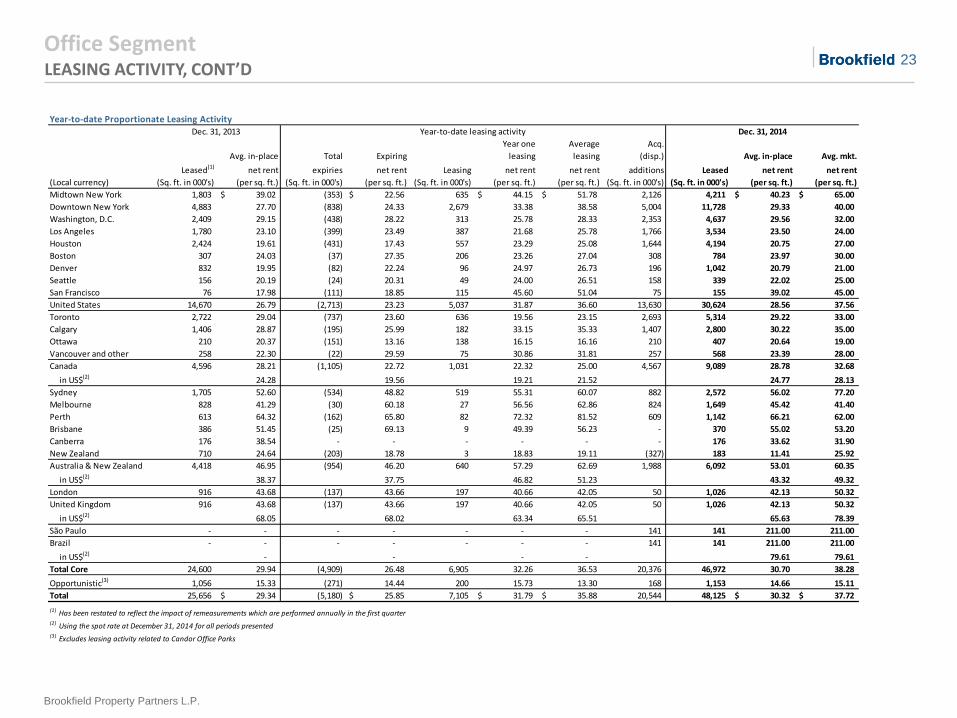

Office Segment LEASING ACTIVITY, CONT’D

Year-to-date Proportionate Leasing Activity

Year one Average Acq.

Avg. in-place Total Expiring leasing leasing (disp.) Avg. in-place Avg. mkt.

Leased(1) net rent expiries net rent Leasing net rent net rent additions Leased net rent net rent

(Local currency) (Sq. ft. in 000's) (per sq. ft.) (Sq. ft. in 000's) (per sq. ft.) (Sq. ft. in 000's) (per sq. ft.) (per sq. ft.) (Sq. ft. in 000's) (Sq. ft. in 000's) (per sq. ft.) (per sq. ft.)

Midtown New York 1,803 39.02$ (353) 22.56$ 635 44.15$ 51.78$ 2,126 4,211 40.23$ 65.00$

Downtown New York 4,883 27.70 (838) 24.33 2,679 33.38 38.58 5,004 11,728 29.33 40.00

Washington, D.C. 2,409 29.15 (438) 28.22 313 25.78 28.33 2,353 4,637 29.56 32.00

Los Angeles 1,780 23.10 (399) 23.49 387 21.68 25.78 1,766 3,534 23.50 24.00

Houston 2,424 19.61 (431) 17.43 557 23.29 25.08 1,644 4,194 20.75 27.00

Boston 307 24.03 (37) 27.35 206 23.26 27.04 308 784 23.97 30.00

Denver 832 19.95 (82) 22.24 96 24.97 26.73 196 1,042 20.79 21.00

Seattle 156 20.19 (24) 20.31 49 24.00 26.51 158 339 22.02 25.00

San Francisco 76 17.98 (111) 18.85 115 45.60 51.04 75 155 39.02 45.00

United States 14,670 26.79 (2,713) 23.23 5,037 31.87 36.60 13,630 30,624 28.56 37.56

Toronto 2,722 29.04 (737) 23.60 636 19.56 23.15 2,693 5,314 29.22 33.00

Calgary 1,406 28.87 (195) 25.99 182 33.15 35.33 1,407 2,800 30.22 35.00

Ottawa 210 20.37 (151) 13.16 138 16.15 16.16 210 407 20.64 19.00

Vancouver and other 258 22.30 (22) 29.59 75 30.86 31.81 257 568 23.39 28.00

Canada 4,596 28.21 (1,105) 22.72 1,031 22.32 25.00 4,567 9,089 28.78 32.68

in US$(2) 24.28 19.56 19.21 21.52 24.77 28.13

Sydney 1,705 52.60 (534) 48.82 519 55.31 60.07 882 2,572 56.02 77.20

Melbourne 828 41.29 (30) 60.18 27 56.56 62.86 824 1,649 45.42 41.40

Perth 613 64.32 (162) 65.80 82 72.32 81.52 609 1,142 66.21 62.00

Brisbane 386 51.45 (25) 69.13 9 49.39 56.23 - 370 55.02 53.20

Canberra 176 38.54 - - - - - - 176 33.62 31.90

New Zealand 710 24.64 (203) 18.78 3 18.83 19.11 (327) 183 11.41 25.92

Australia & New Zealand 4,418 46.95 (954) 46.20 640 57.29 62.69 1,988 6,092 53.01 60.35

in US$(2) 38.37 37.75 46.82 51.23 43.32 49.32

London 916 43.68 (137) 43.66 197 40.66 42.05 50 1,026 42.13 50.32

United Kingdom 916 43.68 (137) 43.66 197 40.66 42.05 50 1,026 42.13 50.32

in US$(2) 68.05 68.02 63.34 65.51 65.63 78.39

São Paulo - - - - - - - 141 141 211.00 211.00

Brazil - - - - - - - 141 141 211.00 211.00

in US$(2) - - - - 79.61 79.61

Total Core 24,600 29.94 (4,909) 26.48 6,905 32.26 36.53 20,376 46,972 30.70 38.28

Opportunistic(3) 1,056 15.33 (271) 14.44 200 15.73 13.30 168 1,153 14.66 15.11

Total 25,656 29.34$ (5,180) 25.85$ 7,105 31.79$ 35.88$ 20,544 48,125 30.32$ 37.72$

(1) Has been restated to reflect the impact of remeasurements which are performed annually in the first quarter(2) Using the spot rate at December 31, 2014 for all periods presented(3) Excludes leasing activity related to Candor Office Parks

Dec. 31, 2013 Year-to-date leasing activity Dec. 31, 2014

24

Brookfield Property Partners L.P.

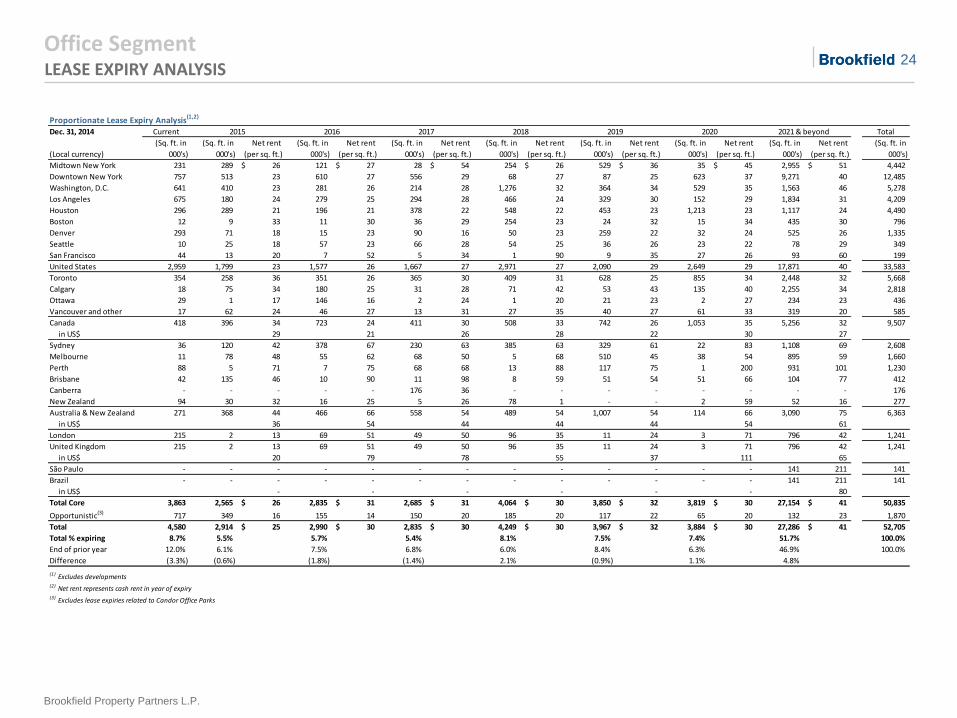

Office Segment LEASE EXPIRY ANALYSIS

Proportionate Lease Expiry Analysis(1,2)

Dec. 31, 2014 Current Total

(Sq. ft. in

000's)

(Sq. ft. in

000's)

Net rent

(per sq. ft.)

(Sq. ft. in

000's)

Net rent

(per sq. ft.)

(Sq. ft. in

000's)

Net rent

(per sq. ft.)

(Sq. ft. in

000's)

Net rent

(per sq. ft.)

(Sq. ft. in

000's)

Net rent

(per sq. ft.)

(Sq. ft. in

000's)

Net rent

(per sq. ft.)

(Sq. ft. in

000's)

Net rent

(per sq. ft.)

(Sq. ft. in

000's)

Midtown New York 231 289 26$ 121 27$ 28 54$ 254 26$ 529 36$ 35 45$ 2,955 51$ 4,442

Downtown New York 757 513 23 610 27 556 29 68 27 87 25 623 37 9,271 40 12,485

Washington, D.C. 641 410 23 281 26 214 28 1,276 32 364 34 529 35 1,563 46 5,278

Los Angeles 675 180 24 279 25 294 28 466 24 329 30 152 29 1,834 31 4,209

Houston 296 289 21 196 21 378 22 548 22 453 23 1,213 23 1,117 24 4,490

Boston 12 9 33 11 30 36 29 254 23 24 32 15 34 435 30 796

Denver 293 71 18 15 23 90 16 50 23 259 22 32 24 525 26 1,335

Seattle 10 25 18 57 23 66 28 54 25 36 26 23 22 78 29 349

San Francisco 44 13 20 7 52 5 34 1 90 9 35 27 26 93 60 199

United States 2,959 1,799 23 1,577 26 1,667 27 2,971 27 2,090 29 2,649 29 17,871 40 33,583

Toronto 354 258 36 351 26 365 30 409 31 628 25 855 34 2,448 32 5,668

Calgary 18 75 34 180 25 31 28 71 42 53 43 135 40 2,255 34 2,818

Ottawa 29 1 17 146 16 2 24 1 20 21 23 2 27 234 23 436

Vancouver and other 17 62 24 46 27 13 31 27 35 40 27 61 33 319 20 585

Canada 418 396 34 723 24 411 30 508 33 742 26 1,053 35 5,256 32 9,507

in US$ 29 21 26 28 22 30 27

Sydney 36 120 42 378 67 230 63 385 63 329 61 22 83 1,108 69 2,608

Melbourne 11 78 48 55 62 68 50 5 68 510 45 38 54 895 59 1,660

Perth 88 5 71 7 75 68 68 13 88 117 75 1 200 931 101 1,230

Brisbane 42 135 46 10 90 11 98 8 59 51 54 51 66 104 77 412

Canberra - - - - - 176 36 - - - - - - - - 176

New Zealand 94 30 32 16 25 5 26 78 1 - - 2 59 52 16 277

Australia & New Zealand 271 368 44 466 66 558 54 489 54 1,007 54 114 66 3,090 75 6,363

in US$ 36 54 44 44 44 54 61

London 215 2 13 69 51 49 50 96 35 11 24 3 71 796 42 1,241

United Kingdom 215 2 13 69 51 49 50 96 35 11 24 3 71 796 42 1,241

in US$ 20 79 78 55 37 111 65

São Paulo - - - - - - - - - - - - - 141 211 141

Brazil - - - - - - - - - - - - - 141 211 141

in US$ - - - - - - 80

Total Core 3,863 2,565 26$ 2,835 31$ 2,685 31$ 4,064 30$ 3,850 32$ 3,819 30$ 27,154 41$ 50,835

Opportunistic(3) 717 349 16 155 14 150 20 185 20 117 22 65 20 132 23 1,870

Total 4,580 2,914 25$ 2,990 30$ 2,835 30$ 4,249 30$ 3,967 32$ 3,884 30$ 27,286 41$ 52,705

Total % expiring 8.7% 5.5% 5.7% 5.4% 8.1% 7.5% 7.4% 51.7% 100.0%

End of prior year 12.0% 6.1% 7.5% 6.8% 6.0% 8.4% 6.3% 46.9% 100.0%

Difference (3.3%) (0.6%) (1.8%) (1.4%) 2.1% (0.9%) 1.1% 4.8%

(1) Excludes developments (2) Net rent represents cash rent in year of expiry(3) Excludes lease expiries related to Candor Office Parks

2020 2021 & beyond

(Local currency)

2015 2016 2017 2018 2019

25

Brookfield Property Partners L.P.

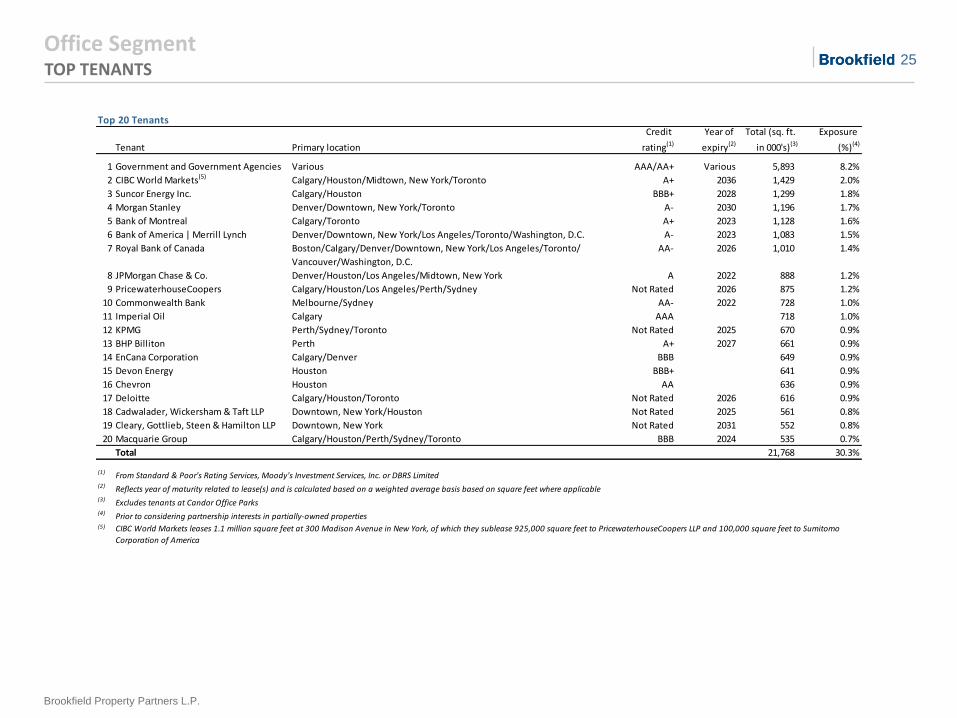

Office Segment TOP TENANTS

Top 20 Tenants

Tenant Primary location

Credit

rating(1)

Year of

expiry(2)

Total (sq. ft.

in 000's)(3)

Exposure

(%)(4)

1 Government and Government Agencies Various AAA/AA+ Various 5,893 8.2%

2 CIBC World Markets(5) Calgary/Houston/Midtown, New York/Toronto A+ 2036 1,429 2.0%

3 Suncor Energy Inc. Calgary/Houston BBB+ 2028 1,299 1.8%

4 Morgan Stanley Denver/Downtown, New York/Toronto A- 2030 1,196 1.7%

5 Bank of Montreal Calgary/Toronto A+ 2023 1,128 1.6%

6 Bank of America | Merrill Lynch Denver/Downtown, New York/Los Angeles/Toronto/Washington, D.C. A- 2023 1,083 1.5%

7 Royal Bank of Canada Boston/Calgary/Denver/Downtown, New York/Los Angeles/Toronto/

Vancouver/Washington, D.C.

AA- 2026 1,010 1.4%

8 JPMorgan Chase & Co. Denver/Houston/Los Angeles/Midtown, New York A 2022 888 1.2%

9 PricewaterhouseCoopers Calgary/Houston/Los Angeles/Perth/Sydney Not Rated 2026 875 1.2%

10 Commonwealth Bank Melbourne/Sydney AA- 2022 728 1.0%

11 Imperial Oil Calgary AAA 718 1.0%

12 KPMG Perth/Sydney/Toronto Not Rated 2025 670 0.9%

13 BHP Billiton Perth A+ 2027 661 0.9%

14 EnCana Corporation Calgary/Denver BBB 649 0.9%

15 Devon Energy Houston BBB+ 641 0.9%

16 Chevron Houston AA 636 0.9%

17 Deloitte Calgary/Houston/Toronto Not Rated 2026 616 0.9%

18 Cadwalader, Wickersham & Taft LLP Downtown, New York/Houston Not Rated 2025 561 0.8%

19 Cleary, Gottlieb, Steen & Hamilton LLP Downtown, New York Not Rated 2031 552 0.8%

20 Macquarie Group Calgary/Houston/Perth/Sydney/Toronto BBB 2024 535 0.7%

Total 21,768 30.3%

(1) From Standard & Poor's Rating Services, Moody's Investment Services, Inc. or DBRS Limited(2) Reflects year of maturity related to lease(s) and is calculated based on a weighted average basis based on square feet where applicable(3) Excludes tenants at Candor Office Parks(4) Prior to considering partnership interests in partially-owned properties(5) CIBC World Markets leases 1.1 million square feet at 300 Madison Avenue in New York, of which they sublease 925,000 square feet to PricewaterhouseCoopers LLP and 100,000 square feet to Sumitomo

Corporation of America

26

Brookfield Property Partners L.P.

Office Segment DEVELOPMENT SITES

Office Development Density

Dec. 31, 2014 Number of

(Sq. ft. in 000's) Location sites

Active developments(1) 7 5,139 4,887

Active planning

United States

Manhattan West New York City - 4,414 4,414

United Kingdom

100 Bishopsgate London 1 950 950

Principal Place Residential London 1 255 128

Active planning 2 5,619 5,492

Held for development

United States

1501 Tremont Place Denver 1 733 733

Block 173 Denver 1 600 600

Reston Crescent Washington 1 724 610

1500 Smith Street Houston 1 500 422

Five Allen Center Houston 1 1,100 927

Allen Center Clay Street Houston 1 600 506

755 Figueroa Los Angeles 1 792 375

Canada

Bay Adelaide North Toronto 1 825 825

Brookfield Place III Toronto 1 800 432

Bankers West Parkade Calgary 1 250 125

Brookfield Place West Tower Calgary 1 1,000 1,000

300 Queen Street Ottawa 1 577 144

Held for development 12 8,501 6,699

Total office developments 21 19,259 17,078

(1) Refer to table below

Active Developments

Dec. 31, 2014

(Local Currency Millions) Location (Sq. ft. in 000's) Total To-date

Manhattan West Platform(1) New York City 680$ 639$

Manhattan West Residential (2) New York City 586 Q4 2018 520$ 20$ 5%

Bay Adelaide East Toronto 980 Q2 2017 69% 463C$ 335C$ 7%

Brookfield Place East Tower Calgary 1,400 Q3 2018 71% 799C$ 204C$ 7%

Brookfield Place Tower 2 Perth 366 Q1 2016 52% 338A$ 184A$ 8%

London Wall Place London 505 Q3 2019 61% 192£ 65£ 8%

Principal Place Commercial London 621 Q4 2019 69% 379£ 89£ 8%

Giroflex São Paulo 681 Q1 2018 - 642R$ 530R$ 9%

Active developments 5,139

(1) Total cost representative of the cost of the platform upon which the five million square foot site will be constructed(2) Yield on cost calculation reflects allocation of a portion of Manhattan West platform costs

Assets under

Management Proportionate

Percent pre-

leased

Proportionate

Area currently

under

construction

Expected date

of cash

stabilization

Cost

Yield on cost

27

Brookfield Property Partners L.P.

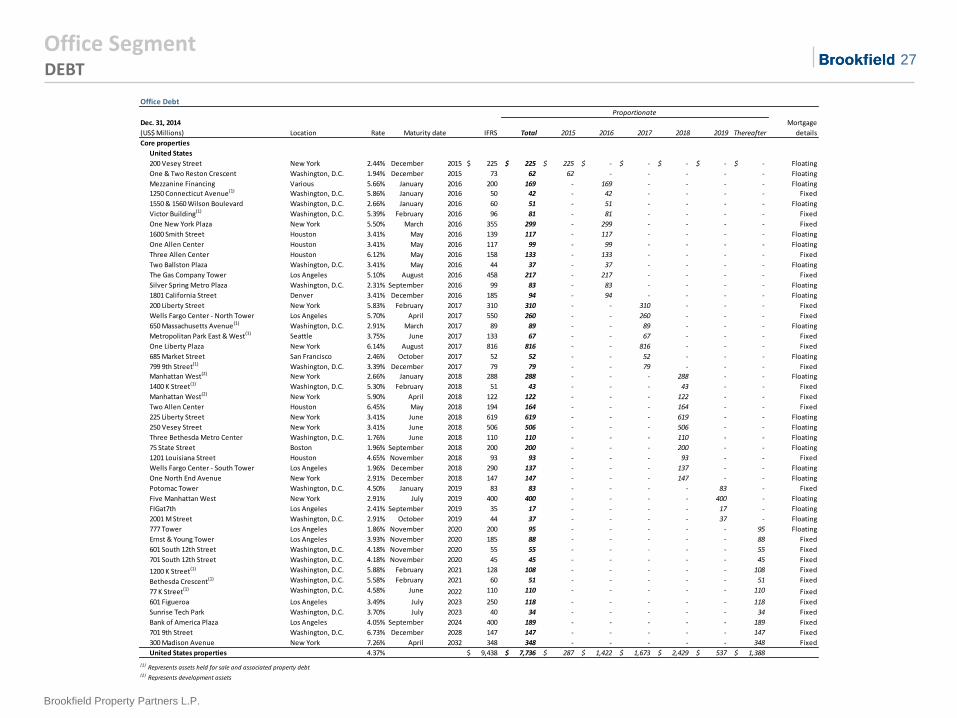

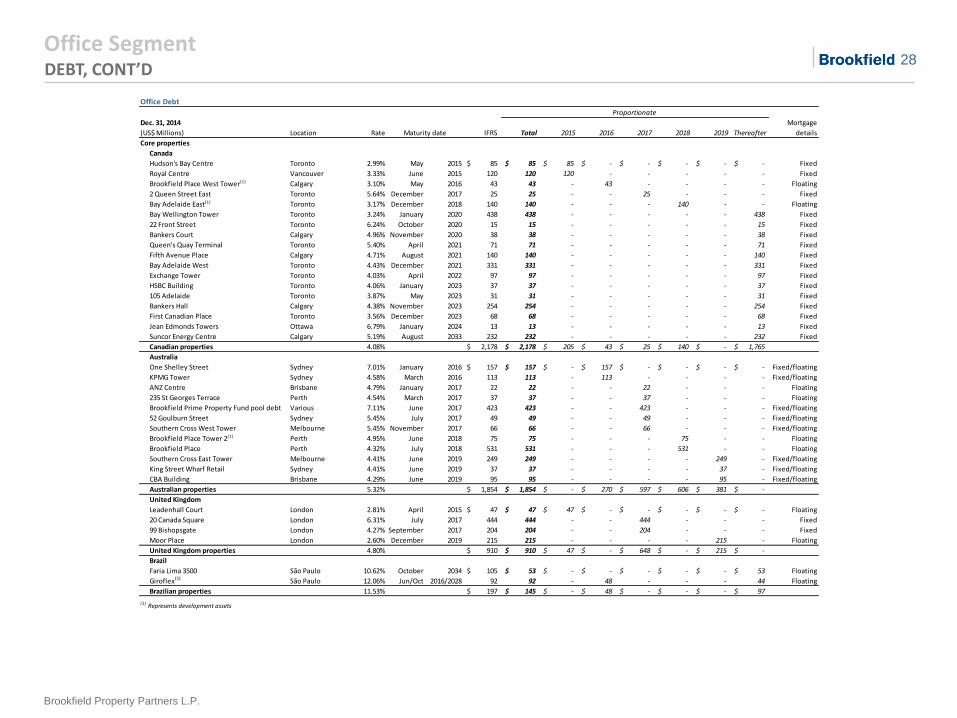

Office Segment DEBT

Office Debt

Location Rate IFRS Total 2015 2016 2017 2018 2019 Thereafter

Mortgage

details

Core properties

United States

200 Vesey Street: Lender1200 Vesey Street New York 2.44% December 2015 225$ 225$ 225$ -$ -$ -$ -$ -$ Floating

One Reston Crescent: Lender1One & Two Reston Crescent Washington, D.C. 1.94% December 2015 73 62 62 - - - - - Floating

Trizec Corporate 84%: Lender1Mezzanine Financing Various 5.66% January 2016 200 169 - 169 - - - - Floating

1250 Connecticut Ave: Lender11250 Connecticut Avenue(1) Washington, D.C. 5.86% January 2016 50 42 - 42 - - - - Fixed

1550 & 1560 Wilson Boulevard: Lender11550 & 1560 Wilson Boulevard Washington, D.C. 2.66% January 2016 60 51 - 51 - - - - Floating

Victor Building: Lender1Victor Building(1) Washington, D.C. 5.39% February 2016 96 81 - 81 - - - - Fixed

One New York Plaza: Lender1One New York Plaza New York 5.50% March 2016 355 299 - 299 - - - - Fixed

1600 Smith Street: Lender11600 Smith Street Houston 3.41% May 2016 139 117 - 117 - - - - Floating

One Allen Center: Lender1One Allen Center Houston 3.41% May 2016 117 99 - 99 - - - - Floating

Three Allen Center: Lender1Three Allen Center Houston 6.12% May 2016 158 133 - 133 - - - - Fixed

Two Ballston Plaza: Lender1Two Ballston Plaza Washington, D.C. 3.41% May 2016 44 37 - 37 - - - - Floating

The Gas Company Tower: Lender1The Gas Company Tower Los Angeles 5.10% August 2016 458 217 - 217 - - - - Fixed

Silver Spring Metro Plaza: Lender1Silver Spring Metro Plaza Washington, D.C. 2.31% September 2016 99 83 - 83 - - - - Floating

1801 California Street: Lender11801 California Street Denver 3.41% December 2016 185 94 - 94 - - - - Floating

200 Liberty Street: Lender1200 Liberty Street New York 5.83% February 2017 310 310 - - 310 - - - Fixed

Wells Fargo Center - North Tower: Lender1Wells Fargo Center - North Tower Los Angeles 5.70% April 2017 550 260 - - 260 - - - Fixed

650 Massachusetts Avenue: Lender1650 Massachusetts Avenue(1) Washington, D.C. 2.91% March 2017 89 89 - - 89 - - - Floating

Metropolitan Park East & West: Lender1Metropolitan Park East & West(1) Seattle 3.75% June 2017 133 67 - - 67 - - - Fixed

One Liberty Plaza: Lender1One Liberty Plaza New York 6.14% August 2017 816 816 - - 816 - - - Fixed

685 Market Street: Lender1685 Market Street San Francisco 2.46% October 2017 52 52 - - 52 - - - Floating

799 9th Street: Lender1799 9th Street(1) Washington, D.C. 3.39% December 2017 79 79 - - 79 - - - Fixed

Manhattan West: Lender3Manhattan West(2) New York 2.66% January 2018 288 288 - - - 288 - - Floating

1400 K Street: Lender11400 K Street(1) Washington, D.C. 5.30% February 2018 51 43 - - - 43 - - Fixed

Manhattan West: Lender2Manhattan West(2) New York 5.90% April 2018 122 122 - - - 122 - - Fixed

Two Allen Center: Lender1Two Allen Center Houston 6.45% May 2018 194 164 - - - 164 - - Fixed

225 Liberty Street: Lender4225 Liberty Street New York 3.41% June 2018 619 619 - - - 619 - - Floating

250 Vesey Street: Lender3250 Vesey Street New York 3.41% June 2018 506 506 - - - 506 - - Floating

Three Bethesda Metro Center: Lender2Three Bethesda Metro Center Washington, D.C. 1.76% June 2018 110 110 - - - 110 - - Floating

75 State Street: Lender275 State Street Boston 1.96% September 2018 200 200 - - - 200 - - Floating

1201 Louisiana Street: Lender11201 Louisiana Street Houston 4.65% November 2018 93 93 - - - 93 - - Fixed

Wells Fargo Center - South Tower: Lender1Wells Fargo Center - South Tower Los Angeles 1.96% December 2018 290 137 - - - 137 - - Floating

One North End Avenue: Lender1One North End Avenue New York 2.91% December 2018 147 147 - - - 147 - - Floating

Potomac Tower: Lender1Potomac Tower Washington, D.C. 4.50% January 2019 83 83 - - - - 83 - Fixed

Five Manhattan West: Lender2Five Manhattan West New York 2.91% July 2019 400 400 - - - - 400 - Floating

FIGat7th: Lender1FIGat7th Los Angeles 2.41% September 2019 35 17 - - - - 17 - Floating

2001 M Street: Lender22001 M Street Washington, D.C. 2.91% October 2019 44 37 - - - - 37 - Floating

777 Tower: Lender1777 Tower Los Angeles 1.86% November 2020 200 95 - - - - - 95 Floating

Ernst & Young Tower DTLA: Lender1Ernst & Young Tower Los Angeles 3.93% November 2020 185 88 - - - - - 88 Fixed

601 and 701 South 12th Street: Lender3601 South 12th Street Washington, D.C. 4.18% November 2020 55 55 - - - - - 55 Fixed

601 and 701 South 12th Street: Lender4701 South 12th Street Washington, D.C. 4.18% November 2020 45 45 - - - - - 45 Fixed

1200 K Street: Lender11200 K Street(1) Washington, D.C. 5.88% February 2021 128 108 - - - - - 108 Fixed

Bethesda Crescent: Lender1Bethesda Crescent(1) Washington, D.C. 5.58% February 2021 60 51 - - - - - 51 Fixed

77 K Street: Lender277 K Street(1) Washington, D.C. 4.58% June 2022 110 110 - - - - - 110 Fixed

601 Figueroa DTLA: Lender1601 Figueroa Los Angeles 3.49% July 2023 250 118 - - - - - 118 Fixed

Sunrise Tech Park: Lender2Sunrise Tech Park Washington, D.C. 3.70% July 2023 40 34 - - - - - 34 Fixed

Bank of America plaza DTLA: Lender2Bank of America Plaza Los Angeles 4.05% September 2024 400 189 - - - - - 189 Fixed

701 9th Avenue: Lender1701 9th Street Washington, D.C. 6.73% December 2028 147 147 - - - - - 147 Fixed

300 Madison Avenue: Lender1300 Madison Avenue New York 7.26% April 2032 348 348 - - - - - 348 Fixed

United States properties 4.37% 9,438$ 7,736$ 287$ 1,422$ 1,673$ 2,429$ 537$ 1,388$

(1) Represents assets held for sale and associated property debt(2) Represents development assets

Dec. 31, 2014

(US$ Millions) Maturity date

Proportionate

28

Brookfield Property Partners L.P.

Office Segment DEBT, CONT’D

Office Debt

Location Rate IFRS Total 2015 2016 2017 2018 2019 Thereafter

Mortgage

details

Core properties

Canada

Hudson's Bay Centre: Lender1Hudson's Bay Centre Toronto 2.99% May 2015 85$ 85$ 85$ -$ -$ -$ -$ -$ Fixed

Royal Centre: Lender2Royal Centre Vancouver 3.33% June 2015 120 120 120 - - - - - Fixed

Brookfield Place Calgary West Tower: Lender1Brookfield Place West Tower(1) Calgary 3.10% May 2016 43 43 - 43 - - - - Floating

2 Queen Street East: Lender12 Queen Street East Toronto 5.64% December 2017 25 25 - - 25 - - - Fixed

Bay Adelaide East: Lender1Bay Adelaide East(1) Toronto 3.17% December 2018 140 140 - - - 140 - - Floating

Bay Wellington Tower: Lender3Bay Wellington Tower Toronto 3.24% January 2020 438 438 - - - - - 438 Fixed

22 Front Street: Lender122 Front Street Toronto 6.24% October 2020 15 15 - - - - - 15 Fixed

Bankers Court: Lender1Bankers Court Calgary 4.96% November 2020 38 38 - - - - - 38 Fixed

Queen's Quay Terminal: Lender1Queen's Quay Terminal Toronto 5.40% April 2021 71 71 - - - - - 71 Fixed

Fifth Avenue Place: Lender1Fifth Avenue Place Calgary 4.71% August 2021 140 140 - - - - - 140 Fixed

Bay Adelaide West: Lender1Bay Adelaide West Toronto 4.43% December 2021 331 331 - - - - - 331 Fixed

Exchange Tower: Lender2Exchange Tower Toronto 4.03% April 2022 97 97 - - - - - 97 Fixed

HSBC Building: Lender2HSBC Building Toronto 4.06% January 2023 37 37 - - - - - 37 Fixed

105 Adelaide: Lender2105 Adelaide Toronto 3.87% May 2023 31 31 - - - - - 31 Fixed

Bankers Hall: Lender3Bankers Hall Calgary 4.38% November 2023 254 254 - - - - - 254 Fixed

First Canadian Place: Lender3First Canadian Place Toronto 3.56% December 2023 68 68 - - - - - 68 Fixed

Jean Edmonds Towers: Lender1Jean Edmonds Towers Ottawa 6.79% January 2024 13 13 - - - - - 13 Fixed

SUNCOR Energy Centre: Lender3Suncor Energy Centre Calgary 5.19% August 2033 232 232 - - - - - 232 Fixed

Canadian properties 4.08% 2,178$ 2,178$ 205$ 43$ 25$ 140$ -$ 1,765$

Australia

One Shelley StreetOne Shelley Street Sydney 7.01% January 2016 157$ 157$ -$ 157$ -$ -$ -$ -$ Fixed/floating

KPMG TowerKPMG Tower Sydney 4.58% March 2016 113 113 - 113 - - - - Fixed/floating

ANZ CentreANZ Centre Brisbane 4.79% January 2017 22 22 - - 22 - - - Floating

235 St Georges Terrace: Lender4235 St Georges Terrace Perth 4.54% March 2017 37 37 - - 37 - - - Floating

Brookfield Prime Property FundBrookfield Prime Property Fund pool debt Various 7.11% June 2017 423 423 - - 423 - - - Fixed/floating

52 Goulburn Street52 Goulburn Street Sydney 5.45% July 2017 49 49 - - 49 - - - Fixed/floating

Southern Cross West TowerSouthern Cross West Tower Melbourne 5.45% November 2017 66 66 - - 66 - - - Fixed/floating

Brookfield Place Tower 2: Lender2Brookfield Place Tower 2(1) Perth 4.95% June 2018 75 75 - - - 75 - - Floating

Brookfield Place: Lender6Brookfield Place Perth 4.32% July 2018 531 531 - - - 531 - - Floating

Southern Cross East TowerSouthern Cross East Tower Melbourne 4.41% June 2019 249 249 - - - - 249 - Fixed/floating

King Street Wharf RetailKing Street Wharf Retail Sydney 4.41% June 2019 37 37 - - - - 37 - Fixed/floating

CBA Building CBA Building Brisbane 4.29% June 2019 95 95 - - - - 95 - Fixed/floating

Australian properties 5.32% 1,854$ 1,854$ -$ 270$ 597$ 606$ 381$ -$

United Kingdom

Leadenhall Court: Lender1Leadenhall Court London 2.81% April 2015 47$ 47$ 47$ -$ -$ -$ -$ -$ Floating

20 Canada Square 20 Canada Square London 6.31% July 2017 444 444 - - 444 - - - Fixed

99 Bishopsgate: Lender199 Bishopsgate London 4.27% September 2017 204 204 - - 204 - - - Fixed

Mooregate Exchange: Lender1Moor Place London 2.60% December 2019 215 215 - - - - 215 - Floating

United Kingdom properties 4.80% 910$ 910$ 47$ -$ 648$ -$ 215$ -$

Brazil

Faria Lima 3500Faria Lima 3500 São Paulo 10.62% October 2034 105$ 53$ -$ -$ -$ -$ -$ 53$ Floating

Giroflex(1) São Paulo 12.06% Jun/Oct 2016/2028 92 92 - 48 - - - 44 Floating

Brazilian properties 11.53% 197$ 145$ -$ 48$ -$ -$ -$ 97$

(1) Represents development assets

Dec. 31, 2014

(US$ Millions) Maturity date

Proportionate

29

Brookfield Property Partners L.P.

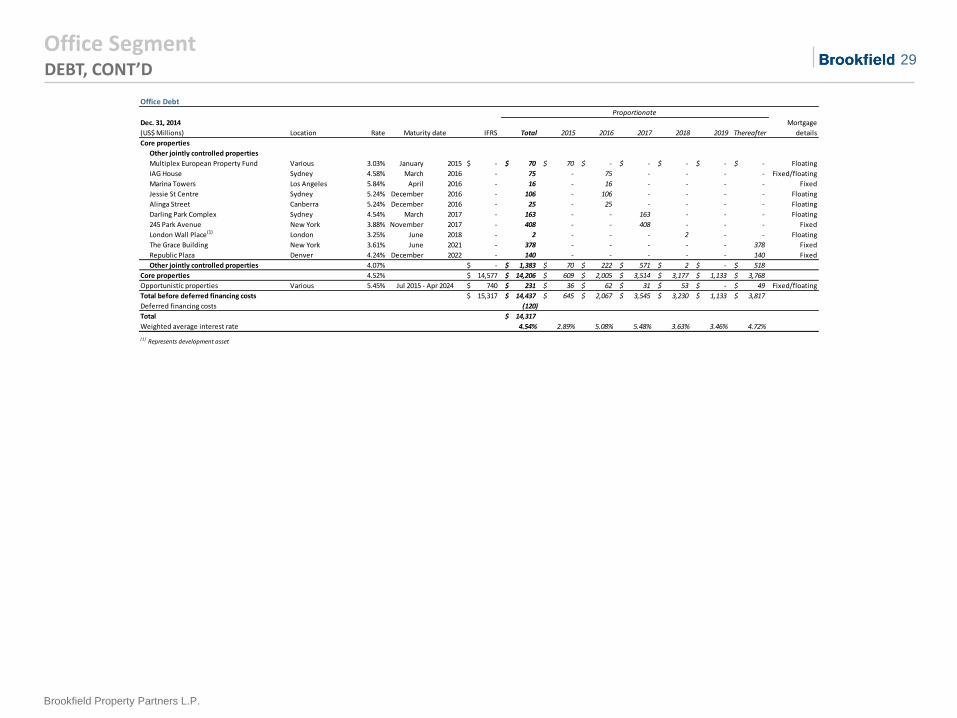

Office Segment DEBT, CONT’D

Office Debt

Location Rate IFRS Total 2015 2016 2017 2018 2019 Thereafter

Mortgage

details

Core properties

Other jointly controlled properties

MUEMultiplex European Property Fund Various 3.03% January 2015 -$ 70$ 70$ -$ -$ -$ -$ -$ Floating

IAG HouseIAG House Sydney 4.58% March 2016 - 75 - 75 - - - - Fixed/floating

Marina Towers: Lender1Marina Towers Los Angeles 5.84% April 2016 - 16 - 16 - - - - Fixed

Jessie St CentreJessie St Centre Sydney 5.24% December 2016 - 106 - 106 - - - - Floating

Alinga StreetAlinga Street Canberra 5.24% December 2016 - 25 - 25 - - - - Floating

Darling Park Complex: Lender4Darling Park Complex Sydney 4.54% March 2017 - 163 - - 163 - - - Floating

245 Park Avenue: Lender1245 Park Avenue New York 3.88% November 2017 - 408 - - 408 - - - Fixed

London Wall Place: Lender1London Wall Place(1) London 3.25% June 2018 - 2 - - - 2 - - Floating

The Grace BuildingThe Grace Building New York 3.61% June 2021 - 378 - - - - - 378 Fixed

Republic Plaza: Lender3Republic Plaza Denver 4.24% December 2022 - 140 - - - - - 140 Fixed

Other jointly controlled properties 4.07% -$ 1,383$ 70$ 222$ 571$ 2$ -$ 518$

Core properties 4.52% 14,577$ 14,206$ 609$ 2,005$ 3,514$ 3,177$ 1,133$ 3,768$

Opportunistic properties Various 5.45% 740$ 231$ 36$ 62$ 31$ 53$ -$ 49$ Fixed/floating

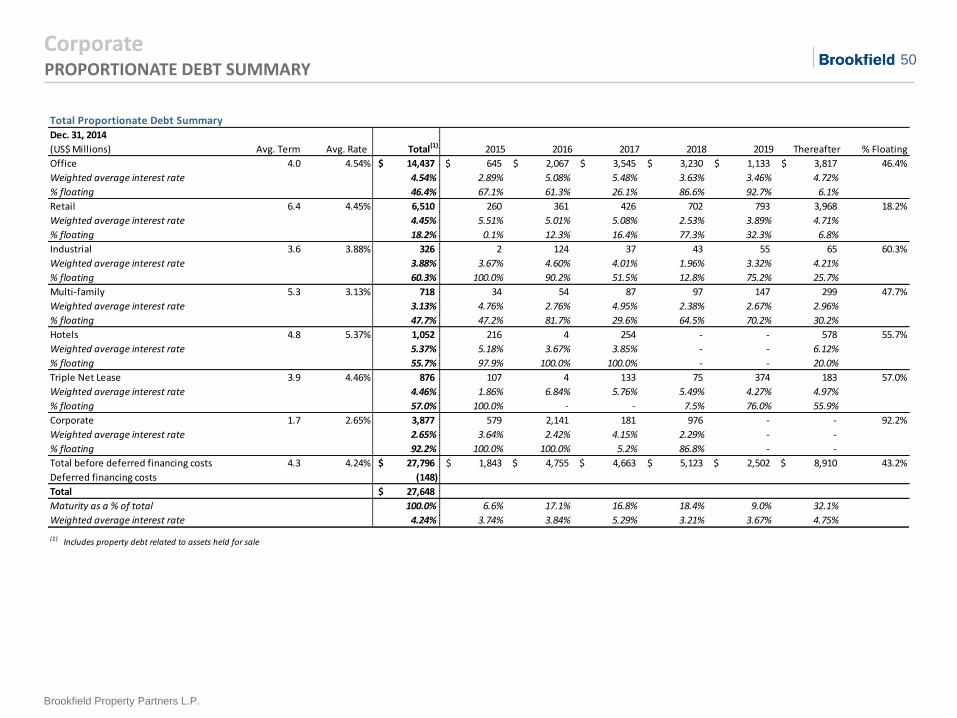

Total before deferred financing costs 15,317$ 14,437$ 645$ 2,067$ 3,545$ 3,230$ 1,133$ 3,817$

Deferred financing costs (120)

Total 14,317$

Weighted average interest rate 4.54% 2.89% 5.08% 5.48% 3.63% 3.46% 4.72%

(1) Represents development asset

Jul 2015 - Apr 2024

Dec. 31, 2014

(US$ Millions) Maturity date

Proportionate

30

Brookfield Property Partners L.P.

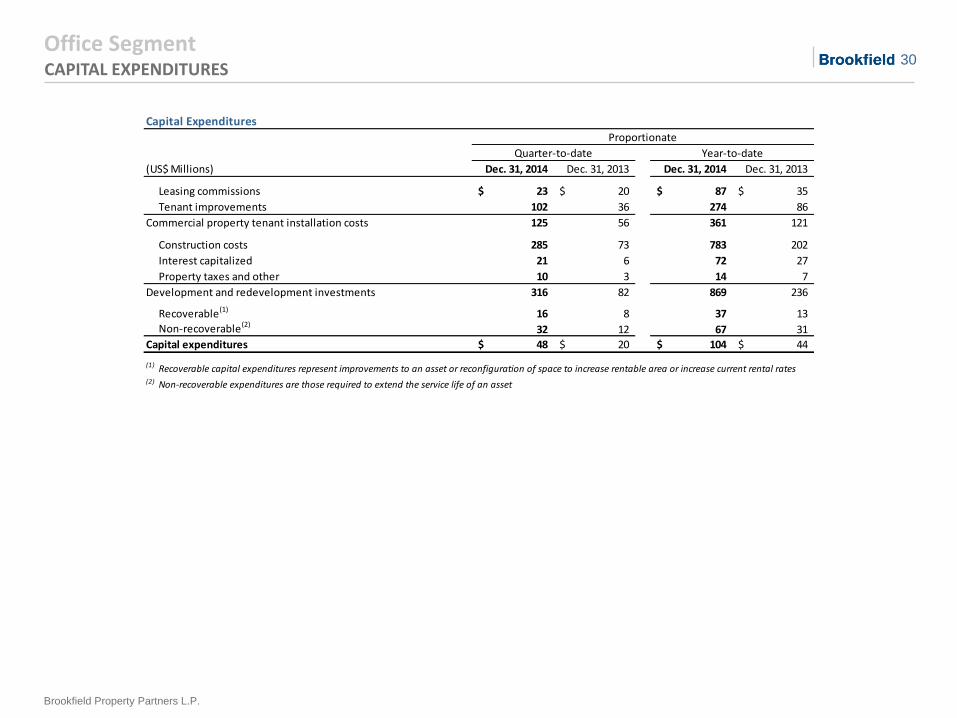

Office Segment CAPITAL EXPENDITURES

Capital Expenditures

(US$ Millions) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

Leasing commissions 23$ 20$ 87$ 35$

Tenant improvements 102 36 274 86

Commercial property tenant installation costs 125 56 361 121

Construction costs 285 73 783 202

Interest capitalized 21 6 72 27

Property taxes and other 10 3 14 7

Development and redevelopment investments 316 82 869 236

Recoverable(1) 16 8 37 13

Non-recoverable(2)32 12 67 31

Capital expenditures 48$ 20$ 104$ 44$

(1) Recoverable capital expenditures represent improvements to an asset or reconfiguration of space to increase rentable area or increase current rental rates(2) Non-recoverable expenditures are those required to extend the service life of an asset

Year-to-date

Proportionate

Quarter-to-date

Retail Segment

32

Brookfield Property Partners L.P.

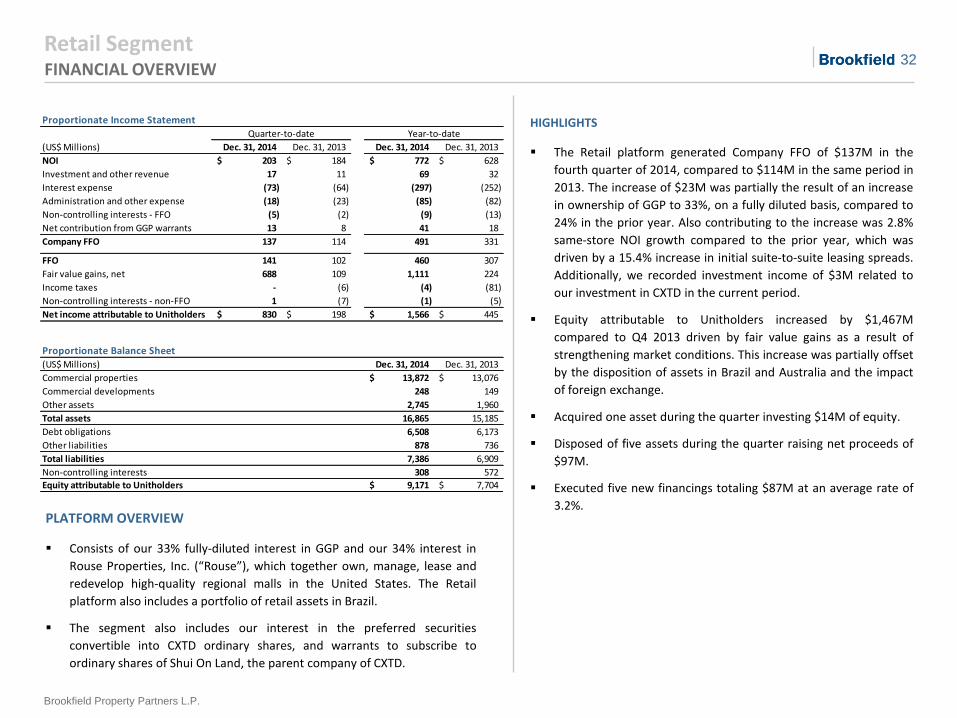

Retail Segment FINANCIAL OVERVIEW

PLATFORM OVERVIEW

Consists of our 33% fully-diluted interest in GGP and our 34% interest in

Rouse Properties, Inc. (“Rouse”), which together own, manage, lease and

redevelop high-quality regional malls in the United States. The Retail

platform also includes a portfolio of retail assets in Brazil.

The segment also includes our interest in the preferred securities

convertible into CXTD ordinary shares, and warrants to subscribe to

ordinary shares of Shui On Land, the parent company of CXTD.

HIGHLIGHTS

The Retail platform generated Company FFO of $137M in the

fourth quarter of 2014, compared to $114M in the same period in

2013. The increase of $23M was partially the result of an increase

in ownership of GGP to 33%, on a fully diluted basis, compared to

24% in the prior year. Also contributing to the increase was 2.8%

same-store NOI growth compared to the prior year, which was

driven by a 15.4% increase in initial suite-to-suite leasing spreads.

Additionally, we recorded investment income of $3M related to

our investment in CXTD in the current period.

Equity attributable to Unitholders increased by $1,467M

compared to Q4 2013 driven by fair value gains as a result of

strengthening market conditions. This increase was partially offset

by the disposition of assets in Brazil and Australia and the impact

of foreign exchange.

Acquired one asset during the quarter investing $14M of equity.

Disposed of five assets during the quarter raising net proceeds of

$97M.

Executed five new financings totaling $87M at an average rate of

3.2%.

Proportionate Income Statement

(US$ Millions) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

NOI 203$ 184$ 772$ 628$

Investment and other revenue 17 11 69 32

Interest expense (73) (64) (297) (252)

Administration and other expense (18) (23) (85) (82)

Non-controlling interests - FFO (5) (2) (9) (13)

Net contribution from GGP warrants 13 8 41 18

Company FFO 137 114 491 331

FFO 141 102 460 307

Fair value gains, net 688 109 1,111 224

Income taxes - (6) (4) (81)

Non-controlling interests - non-FFO 1 (7) (1) (5)

Net income attributable to Unitholders 830$ 198$ 1,566$ 445$

Proportionate Balance Sheet(US$ Millions) Dec. 31, 2014 Dec. 31, 2013

Commercial properties 13,872$ 13,076$

Commercial developments 248 149

Other assets 2,745 1,960

Total assets 16,865 15,185

Debt obligations 6,508 6,173

Other liabilities 878 736

Total liabilities 7,386 6,909

Non-controlling interests 308 572

Equity attributable to Unitholders 9,171$ 7,704$

Quarter-to-date Year-to-date

33

Brookfield Property Partners L.P.

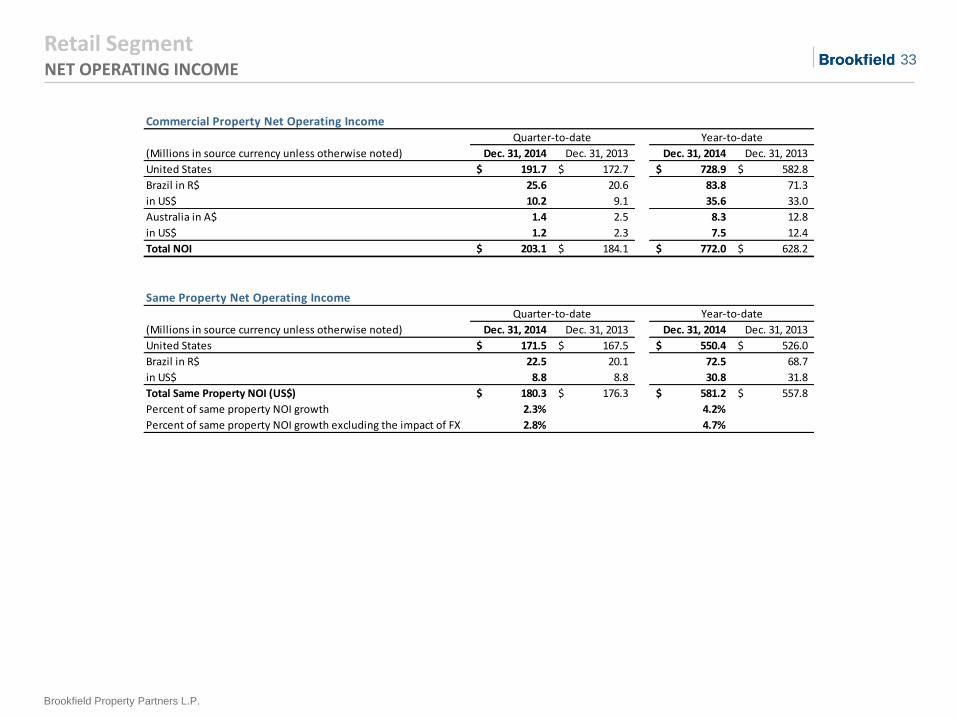

Retail Segment NET OPERATING INCOME

Commercial Property Net Operating Income

Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

United States 191.7$ 172.7$ 728.9$ 582.8$

Brazil in R$ 25.6 20.6 83.8 71.3

in US$ 10.2 9.1 35.6 33.0

Australia in A$ 1.4 2.5 8.3 12.8

in US$ 1.2 2.3 7.5 12.4

Total NOI 203.1$ 184.1$ 772.0$ 628.2$

Same Property Net Operating Income

Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

United States 171.5$ 167.5$ 550.4$ 526.0$

Brazil in R$ 22.5 20.1 72.5 68.7

in US$ 8.8 8.8 30.8 31.8

Total Same Property NOI (US$) 180.3$ 176.3$ 581.2$ 557.8$

Percent of same property NOI growth 2.3% 4.2%

Percent of same property NOI growth excluding the impact of FX 2.8% 4.7%

(Millions in source currency unless otherwise noted)

Quarter-to-date Year-to-date

(Millions in source currency unless otherwise noted)

Quarter-to-date Year-to-date

34

Brookfield Property Partners L.P.

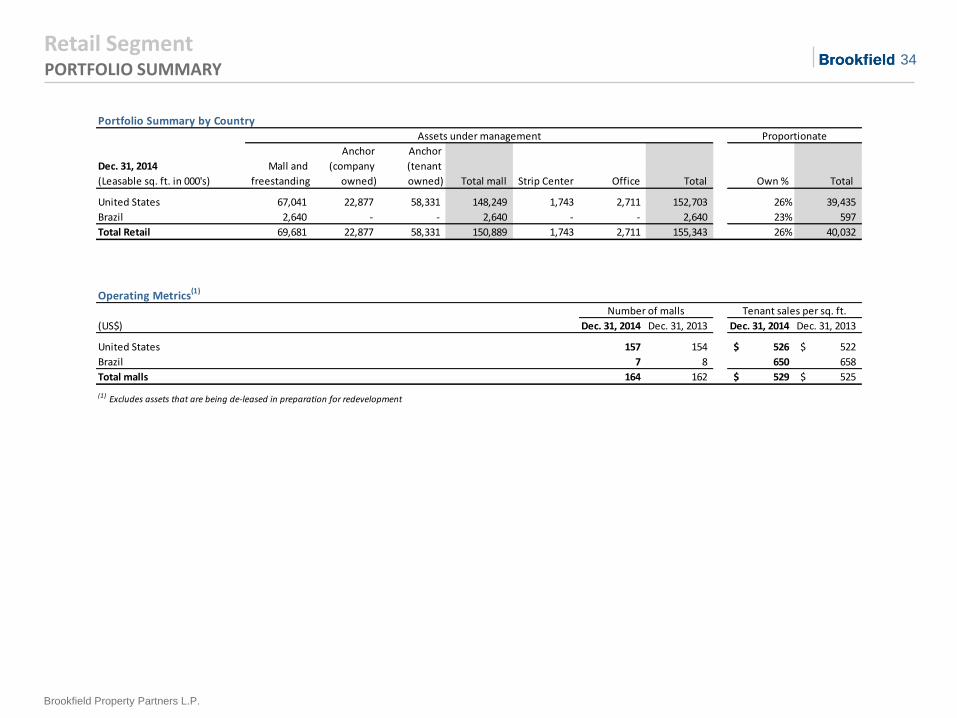

Retail Segment PORTFOLIO SUMMARY

Portfolio Summary by Country

(Leasable sq. ft. in 000's) Strip Center Office Total Own % Total

United States 67,041 22,877 58,331 148,249 1,743 2,711 152,703 26% 39,435

Brazil 2,640 - - 2,640 - - 2,640 23% 597

Total Retail 69,681 22,877 58,331 150,889 1,743 2,711 155,343 26% 40,032

Operating Metrics(1)

(US$) Dec. 31, 2014 Dec. 31, 2013 Dec. 31, 2014 Dec. 31, 2013

United States 157 154 526$ 522$

Brazil 7 8 650 658

Total malls 164 162 529$ 525$

(1) Excludes assets that are being de-leased in preparation for redevelopment

Dec. 31, 2014

Total mall

Assets under management Proportionate

Number of malls Tenant sales per sq. ft.

Mall and

freestanding

Anchor

(company

owned)

Anchor

(tenant

owned)

35

Brookfield Property Partners L.P.

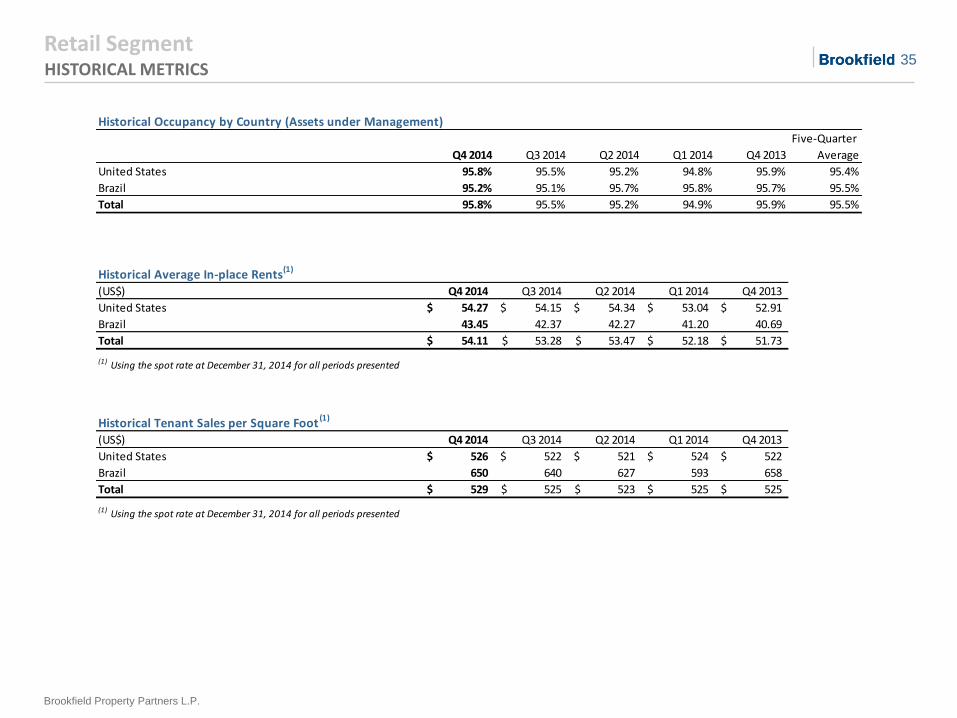

Retail Segment HISTORICAL METRICS

Historical Occupancy by Country (Assets under Management)

Q4 2014 Q3 2014 Q2 2014 Q1 2014 Q4 2013

Five-Quarter

Average

United States 95.8% 95.5% 95.2% 94.8% 95.9% 95.4%

Brazil 95.2% 95.1% 95.7% 95.8% 95.7% 95.5%

Total 95.8% 95.5% 95.2% 94.9% 95.9% 95.5%

Historical Average In-place Rents(1)

(US$) Q4 2014 Q3 2014 Q2 2014 Q1 2014 Q4 2013

United States 54.27$ 54.15$ 54.34$ 53.04$ 52.91$

Brazil 43.45 42.37 42.27 41.20 40.69

Total 54.11$ 53.28$ 53.47$ 52.18$ 51.73$

(1) Using the spot rate at December 31, 2014 for all periods presented

Historical Tenant Sales per Square Foot (1)

(US$) Q4 2014 Q3 2014 Q2 2014 Q1 2014 Q4 2013

United States 526$ 522$ 521$ 524$ 522$

Brazil 650 640 627 593 658

Total 529$ 525$ 523$ 525$ 525$

(1) Using the spot rate at December 31, 2014 for all periods presented

36

Brookfield Property Partners L.P.

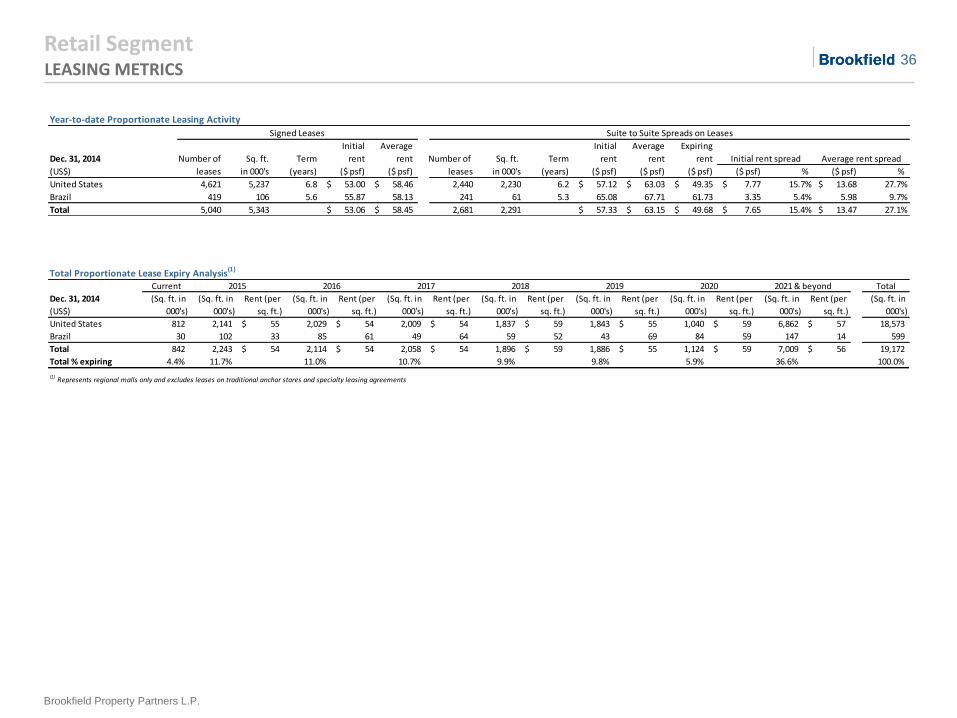

Retail Segment LEASING METRICS

Year-to-date Proportionate Leasing Activity

Initial Average Initial Average Expiring

Dec. 31, 2014 Number of Sq. ft. Term rent rent Number of Sq. ft. Term rent rent rent

(US$) leases in 000's (years) ($ psf) ($ psf) leases in 000's (years) ($ psf) ($ psf) ($ psf) ($ psf) % ($ psf) %

United States 4,621 5,237 6.8 53.00$ 58.46$ 2,440 2,230 6.2 57.12$ 63.03$ 49.35$ 7.77$ 15.7% 13.68$ 27.7%

Brazil 419 106 5.6 55.87 58.13 241 61 5.3 65.08 67.71 61.73 3.35 5.4% 5.98 9.7%

Total 5,040 5,343 53.06$ 58.45$ 2,681 2,291 57.33$ 63.15$ 49.68$ 7.65$ 15.4% 13.47$ 27.1%

Initial rent spread Average rent spread

Signed Leases Suite to Suite Spreads on Leases

Total Proportionate Lease Expiry Analysis(1)

Current Total

(Sq. ft. in

000's)

(Sq. ft. in

000's)

Rent (per

sq. ft.)

(Sq. ft. in

000's)

Rent (per

sq. ft.)

(Sq. ft. in

000's)

Rent (per

sq. ft.)

(Sq. ft. in

000's)

Rent (per

sq. ft.)

(Sq. ft. in

000's)

Rent (per

sq. ft.)

(Sq. ft. in

000's)

Rent (per

sq. ft.)

(Sq. ft. in

000's)

Rent (per

sq. ft.)

(Sq. ft. in

000's)

United States 812 2,141 55$ 2,029 54$ 2,009 54$ 1,837 59$ 1,843 55$ 1,040 59$ 6,862 57$ 18,573

Brazil 30 102 33 85 61 49 64 59 52 43 69 84 59 147 14 599

Total 842 2,243 54$ 2,114 54$ 2,058 54$ 1,896 59$ 1,886 55$ 1,124 59$ 7,009 56$ 19,172

Total % expiring 4.4% 11.7% 11.0% 10.7% 9.9% 9.8% 5.9% 36.6% 100.0%

(1) Represents regional malls only and excludes leases on traditional anchor stores and specialty leasing agreements

2020 2021 & beyond

Dec. 31, 2014

(US$)

2015 2016 2017 2018 2019

37

Brookfield Property Partners L.P.

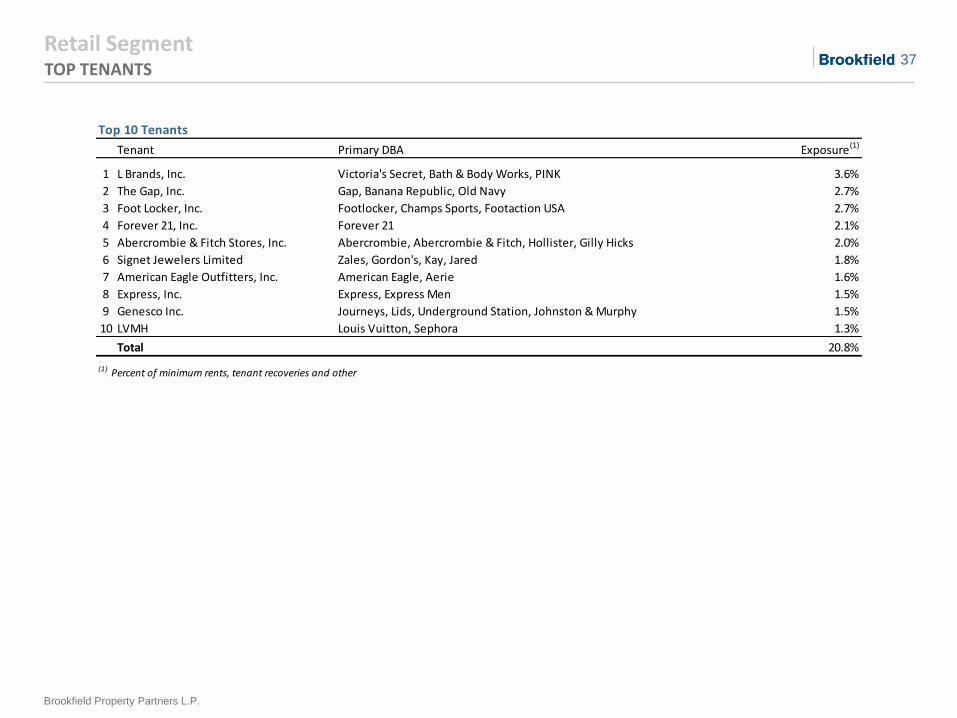

Retail Segment TOP TENANTS

Top 10 Tenants

Tenant Primary DBA Exposure(1)

1 L Brands, Inc. Victoria's Secret, Bath & Body Works, PINK 3.6%

2 The Gap, Inc. Gap, Banana Republic, Old Navy 2.7%

3 Foot Locker, Inc. Footlocker, Champs Sports, Footaction USA 2.7%