Embed Size (px)

Citation preview

SUSTAINABLE RETAILING OF TECHNOLOGIES TO THE POOR: IDENTIFICATION OF A HIGH VALUE COMMODITY BASE AND THE KEY TECHNOLOGICAL

CONSTRAINT TO ITS MASS MARKETING.

Guru Naik March 2001

International Development Enterprises

C5/43, Safdarjung Development Area

New Delhi - 110016

India

TABLE OF CONTENTS ABSTRACT………………………………………………………………………………………..2 1.0 INTRODUCTION ........................................................................................................................... 3

1.1 Background to the Project Rationale......................................................................................... 3 1.2 Background to Project Location ................................................................................................ 4 1.3 The Beneficiary Segment............................................................................................................ 6 1.4 The Cropping Pattern................................................................................................................... 6

2.0 METHODOLOGY .......................................................................................................................... 9 2.1 Identification of Key Produce and Technological Constraint Facing Farmers Entering

High Value Markets ...................................................................................................................... 9 2.1.1 Stakeholder Discussions...................................................................................................... 9 2.1.2 Predominance of Fruit and Vegetables in Cultivation .................................................. 13 2.1.3 Analysis of Vegetable Crops, by Value and Perishable Status.................................... 13 2.1.4 Understanding the Key Pathways for the Flow of Goods ............................................ 13

3.0 RESULTS AND DISCUSSION .................................................................................................. 15 3.1 Identification of Key Produce and Technological Constraint Facing Farmers Entering

High Value Markets .................................................................................................................... 15 3.1.1 Stakeholder Discussions.................................................................................................... 15 3.1.2 Predominance of Fruit and Vegetables in Cultivation .................................................. 17 3.1.3 Analysis of Vegetable Crops, by Value and Perishable Status.................................... 19 3.1.4 Identification of Key Technological Constraint to Accessing High Value Markets 20

3.2 Understanding the Key Pathways for the Flow of Goods .................................................... 24 3.2.1 Farm Produce to Consumer .............................................................................................. 24 3.2.2 Technology Pathways........................................................................................................ 27 3.2.3 Information Pathways........................................................................................................ 29

4.0 CONCLUSION AND RECOMMENDATIONS ...................................................................... 30

TABLES Table 1.1: Distribution of operational holdings and area in different size classes ............................. 6 Table 2.1: Market Survey ......................................................................................................................... 11 Table 3.1.2: Livelihoods Related Information Categorized by Capital Asset................................... 16 Table 3.1.3: Total area under cultivation by crop during the 1993-94 and 1998-99 growing seasons.......... 18 Table 3.1.4: Cost benefit analysis for five preferred crops .................................................................. 19 Table 3.1.5: Storage life of selected crops held without refrigeration .............................................. 20 Table 3.2.1: Flow of goods and the various marketing chains ............................................................ 28 Table 3.2.2: Flow of information to farmers.......................................................................................... 29 PLATES PLATE 1: Map Of Himachal Pradesh Showing The Study Locations ........................................................... 5 PLATE 2: A Typical Village In Himachal Pradesh........................................................................................ 8 PLATE 3: The Cropping Pattern .................................................................................................................... 8 PLATE 4: Tomato Crops in Himachal Pradesh.............................................................................................. 8 PLATE 5: Village Meeting at Panchad......................................................................................................... 14 PLATE 6: Farmers at Bhuntar Wholesale Market ........................................................................................ 14 PLATE 7: Sawmill at Solan Making Wooden Boxes for Packaging Vegetables ......................................... 14 PLATE 8: Tomatoes Being Transported in a Kilta....................................................................................... 22 PLATE 9: Tomatoes Packaged for Sale in Bamboo Baskets........................................................................ 22 PLATE 10: Wooden Boxes Being Constructed by Box Makers .................................................................. 23 PLATE 11: Tomatoes Packaged in Plastic Crates ........................................................................................ 23 PLATE 12: Farmers Bringing Tomatoes to Market (N.B. Tomatoes are Sold Loose) ................................. 26 PLATE 13: Local Mandi (N.B. the tomatoes packed in large plastic crates) ............................................... 26 PLATE 14: Major Mandi Showing the Scale of Produce Being Loaded onto Vehicles............................... 26

ABSTRACT This report provides a summary of the research methodology and findings of a needs assessment exercise undertaken for the CPHP project DFID R7551, Sustainable retailing of post-harvest technology to the poor: alternative institutional mechanisms for developing and transferring technology. The data gathered in this exercise was used to inform the selection of a key perishable produce that has high-value market potential and the key technological constraint facing farmers accessing these markets. These will form vehicles for research into the potential for forming commercial linkages as a means of transferring technology to the poor. Of the eleven off-season vegetables grown in the study locations, tomatoes were found to have the greatest marketing and income generating potential. Access to high-value tomato markets is reliant upon good quality packaging. Wooden crates are currently used but availability of timber is diminishing due to changes in government regulations on timber harvesting. Alternative appropriate and affordable packaging systems are not yet available, thereby threatening the high-value tomato trade. The research vehicles of choice are therefore tomatoes and packaging systems. Technology and information flow channels were studied. The hardware channel and the packaging box supply channel have potential as channels to deliver the proposed packaging systems to the small farmer. Of the information channels, the auction agents appear to be the most respected and to exert the greatest direct influence on the farmers.

2

1.0 INTRODUCTION This report provides a summary of the research methodology and findings of the needs assessment exercise undertaken for the CPHP project DFID R7551, Sustainable retailing of post-harvest technology to the poor: alternative institutional mechanisms for developing and transferring technology. The data gathered in this exercise has informed the selection of the key perishable produce and the technological constraint to accessing higher value markets that will form the vehicles for research into forming commercial linkages for technology transfer to the poor. The analysis of the data collected is presented and recommendations given as to the institutional linkages that should be considered in the commercialization process. 1.1 Background to the Project Rationale Agriculture is a primary source of livelihood security for the rural poor across the developing world and offers significant opportunities for poverty impact. However, post-harvest losses between 30 and 50% of the total agricultural output are common, having a significant effect on income and livelihood security (FAO, 1995). Many of these losses can be attributed to inadequate post-harvest practices, arising from a lack of knowledge of best practices and limitations in the kinds of technologies employed. Historically, and in common with many other developing countries, post-harvest research and dissemination in India has remained the monopoly of Government-run institutes and agencies. Although technological solutions are developed, their uptake by the target population of resource poor farmers is generally very low. A number of reasons have been suggested for this phenomenon: the technologies are not appropriate for the needs of poor farmers; the technologies are not affordable by poor farmers; dissemination is dependent upon the involvement of intermediary institutions (NGOs, Government Extension Departments etc.) who withdraw support, for financial or other reasons, after a limited period; the profit margins are insufficient for the private sector to become involved. Furthermore, where uptake does occur, it is rarely seen to expand beyond the immediate communities who were recipients of the extension programme. This raises questions about the existing institutional arrangements for developing and delivering the required technologies. It appears that alternative institutional mechanisms need to be explored (Hall et al., 1998a; Hall et al., 1998b). Across the world, the financially secure access and transfer technologies via the commercial market place, however, this route invariably excludes the cash poor and those unable to access credit. Market forces drive the process with profit margins dictating the level of commercial interest. Consumers make purchasing decisions based on the applicability of the technology for their needs and cost. Within the developing world, commerce does not recognize the resource poor as a viable market. However, this supposition is not strictly true. Providing technologies are developed that meet the needs of the poor at a price they can afford, they are no less a viable market than the wealthy (Polak et al.1997; World Bank Report, 1998). However, most technologies fail to meet the particular needs of poor people and are rarely affordable. Poverty does not preclude people from making informed decisions about their needs, but it does prohibit the purchase of many technological solutions to these needs. If technologies can be developed in collaboration with resource poor end-users, their applicability can be assured and the level of need determined. The technologies

3

can then be developed to a cost specification that allows for profit margins in their retail (IDE policy report, 1997). The aim of this research is to explore the potential for commercializing the process of technology development and delivery by building institutional linkages between the user level and the technology manufacturer/supplier level. Making use of free-market principles, whereby successful marketing relies upon products meeting user demands, the approach may facilitate long-term sustainability of the technology transfer process. 1.2 Background to Project Location The study is being conducted in the Indian State of Himachal Pradesh. The entire territory of Himachal is mountainous with altitude varying between 350m to 7000 m above the mean sea level. Topographically Himachal territory from south to north can be divided into 4 agro climatic zones (see map at Plate 1):

Low hills (up to 900 m): Yellow Mid Hills (900 to 1600 m): Green High Hills (1600 to 2400 m): Red Cold desert (above 2400 m): Blue

The climate of Himachal varies at different altitude from semitropical to semi arctic. The low hills face high temperature in summer of up to 350c. The mid hills experience snowfall in winter and the cold desert has year round snow capped mountains. The total area of Himachal Pradesh is 55,673 sq. kms and the total population is 5,170,877 people. Himachal Pradesh is a completely mountainous state making life quite difficult for people to live there. The population density of Himachal Pradesh is 93 people per sq. km. against the national average of 273. The total cropped area in the state is 956,965 ha. In addition 832,347 ha are covered under forests. 80% of the state's agriculture is done in the low and mid hills, where the cultivation is primarily done in the terraces. A significant percentage of the population (91.32%) lives in the rural areas and is dependent on agriculture for their livelihood. However, an area of only 17.3% of the total cropped area is irrigated. Administratively the state is divided into 12 districts, 69 blocks and 2597 panchayats. The fieldwork of the study is being conducted in Solan and Kullu districts of Himachal Pradesh. The villages of Solan district are located in the low and mid hills, whilst the villages of Kullu district are located in the mid and high hills. Most of the villages of Solan district are mountainous and a large portion of Kullu district is a valley of river Beas. Chandigarh is the nearest major consumer market of the plains for both Solan and Kullu. However, Solan is only 70 kms from Chandigarh and Kullu is 300 kms away. Because of this distance Solan is much more accessible to Chandigarh and Delhi.

4

PLATE 1: Map Of Himachal Pradesh Showing The Study Locations

5

1.3 The Beneficiary Segment In India, farmers are classified under five categories depending on their operational land holding. In Himachal Pradesh, the land holding is further sub-divided to give a total of ten categories. Table 1.1 beneath provides details of the landholding classification of Himachal Pradesh farmers.

Table 1.1: Distribution of operational holdings and area in different size classes

Number Area

Total number

Percentage Total area (ha)

Percentage Size

Classification by Govt. of

India

Land Holding

(ha)

Simple Cumulative

Simple Cumulative

Marginal Below 0.5 3,49,803 41.95 41.95 83,035 8.22 8.22 0.5 – 1.0 1,82,331 21.87 63.82 1,31,684 13.04 21.26

Small 1.0 – 2.0 1,66,410 19.96 83.78 2,35,144 23.29 44.55 Semi-medium 2.0 – 3.0 64,090 7.69 91.47 1,55,624 15.41 59.96

3.0 – 4.0 29,826 3.58 95.04 1,01,992 10.10 70.06 Medium 4.0 – 5.0 15,216 1.82 96.87 67,803 6.71 76.78

5.0 – 7.5 15,221 1.83 98.69 91,377 9.05 85.83 7.5 – 10.0 5,374 0.64 99.34 46,019 4.56 90.39

Large 10.0 – 20.0 4,481 0.54 99.88 58,596 5.80 96.19 20.0 & above 1,041 0.12 100.00 38,492 3.81 100.00

Total 8,33,793 100 10,09,766 100 The total number of families in Himachal Pradesh is just 8,33,793 and a large percentage (83.78%) of these farmers belong to the small and marginal farmer category owning less than 2 ha of land, and farming 44% of the total land under cultivation. Less than 1% farmers are large farmers owning more than 10 ha land and less than 5% farmers are medium and large owning more than 4 ha land. Concentrating on marginal farmers, the project outputs should benefit almost 64% of farming families. 1.4 The Cropping Pattern Agriculture is the largest and the most important sector in the economic life of Himachal Pradesh. The hilly state of Himachal Pradesh, with abundant rainfall and rich forests, has not been able to keep pace with the development in the plains because of its inherent problems of topography, terrain and climatic condition. Cultivable fields here are mostly carved out on the sloping hillsides, and hence exposed to large-scale erosion of the top fertile soil. Unlike the other parts of India, Himachal Pradesh also has three climatic seasons i.e. Rainy, Winter and Summer season. However the length of cold days during the winter season vary drastically across different altitudes, affecting the agriculture activities in the state. The low hills normally have the perfect three seasons. But the mid and high hills

6

only have two agriculture seasons because of a prolonged winter. Agriculture is practically absent in the cold desert region. Perennial orchards are the primary crops in the high hills and seasonal crops are mostly grown in the low and mid hills. The crops that are grown in different seasons in Himachal Pradesh are:

Low hills Mid hills High hills

Rainy season

Paddy, Maize

Maize, Ginger, Beans Seed potato

Winter season

Wheat

Pea

Pea

Summer season

Off season vegetables

Off season vegetables

Perennial orchards

Lemon

Plum, Peach, Pomegranate

Apple, Apricot, Almond

In the last 30 years the area under cultivation with vegetables has increased by more than three fold and vegetable production has increased by more than five fold. There is a prolonged winter and a short summer season in the low and mid hills, during which time the vast plains of India face severe summer. During this time the climate of the low and mid hills region is highly conducive for the cultivation of fruit and vegetables. The harvest provides fruit and vegetables that are out-of-season to the remainder of India and so can command a very high price in the plains where demand is nearly unlimited. The availability of an infinite, high-value market is encouraging more and more of the farmers in Himachal Pradesh to risk a move in to fruit and vegetable production.

7

THE STUDY STATE PLATE 2: A Typical Village In Himachal Pradesh PLATE 3: The Cropping Pattern PLATE 4: Tomato Crops in Himachal Pradesh

8

2.0 METHODOLOGY 2.1 Identification of Key Produce and Technological Constraint Facing Farmers

Entering High Value Markets 2.1.1 Stakeholder Discussions Using PRA methods in interviews with all relevant stakeholders, knowledge on the livelihood systems in place and the farming practices followed was generated. Data was then gathered to inform the selection of: (i) the communities and households with whom to work; (ii) a perishable fruit or vegetable that forms a key component of their livelihood security; (iii) a significant storage or packaging constraint to entering high value markets for which a technological solution can be found. The selection process was supported by a secondary data survey of available literature along with local knowledge wherever possible. Various groups were identified as being primary stakeholders in the research. Interviews were undertaken with representatives of each group as follows: Marginal and Small-scale farmers Meetings with farmers were undertaken to develop an understanding of their livelihood systems and any issues relating to storage, packaging and marketing of their agriculture produce. Four villages from each of the Districts of Solan and Kullu were selected for these meetings. These Districts are within the operational areas of IDE and as such have good working relations with IDE. Discussion meetings were initially held in group format and then followed up with one-to-one meetings with a small number of farmers to ensure that information provided was representative of the whole. Farmers representing each of the official wealth categories were involved in the discussions. In order to facilitate the building of trust between farmers and IDE, and thus encourage the accurate exchange of information, meetings were initiated by, and undertaken in conjunction with, intermediary parties acting as linkages between IDE and the farmer segment. The intermediary linkage in Solan district was Ruchi, a grassroots NGO, whilst in Kullu area an agricultural input dealer, Laxmi Seeds, acted as an intermediary. Village meetings were open to all families of the village, regardless of wealth rank. Data Collection in Solan District Ruchi is the largest NGO operating in Solan and Sirmour districts of Himachal Pradesh. It has also been instrumental in developing water resources in many villages, which has been the key to the development of vegetable cultivation in those districts. In Solan the collaboration with Ruchi, will afford accurate collection of information from the farmers and subsequent implementation of the program in its project area. Four villages were selected from Ruchi’s operational villages. Ruchi already had a rainwater conservation program in these villages and had very good rapport with the villagers there. Ruchi’s field staff organized the meetings in these villages.

9

Data Collection In Kullu Area In Kullu area IDE has already established a network of over 20 private sector dealers who are selling micro irrigation kits. These dealers also sell agriculture inputs such as seeds, pesticides and fertilizers. The dealers have played an important role in the development of vegetable cultivation in the area. In Kullu the collaboration with an agriculture input dealer was entered into as the target sector farmers know the dealers and a level of trust has been developed over a number of years. A partnership was developed with Laxmi Seeds, a dealership located in Hurla village, and owned by Mr. N. D. Mahant. Four villages were selected from those where Laxmi Seeds has good business links. Mr. Mahant organized the village meetings and was also present at all the meetings. Visits to Wholesale Vegetable Markets As the total level of vegetable production in Himachal Pradesh far exceeds the local demand, much of the production is intended for sale outside of Himachal Pradesh. Data arising from 3.1.1 showed that farmers are mainly selling their vegetables in wholesale markets, both inside and outside Himachal Pradesh. Three markets inside Himachal Pradesh and two markets outside Himachal Pradesh were therefore studied. Each of these markets has similarities in terms of the kind of actors involved, as detailed below:

Farmers: In each market a large number of farmers are seen to be bringing their vegetable to the market on their back, by donkey or in hired tractors / trucks.

•

Traders: The buyers in these markets are normally traders, who purchase the vegetables, transport them to distant markets, and sell to retailers, who ultimately sell to the consumers.

•

Commission Agents: This is a new class of entrepreneurs, who facilitate auctioning of vegetables, which is the main system of sale in these markets. These agents charge the farmers a fixed percentage of the value of the sale as their commission for the service.

•

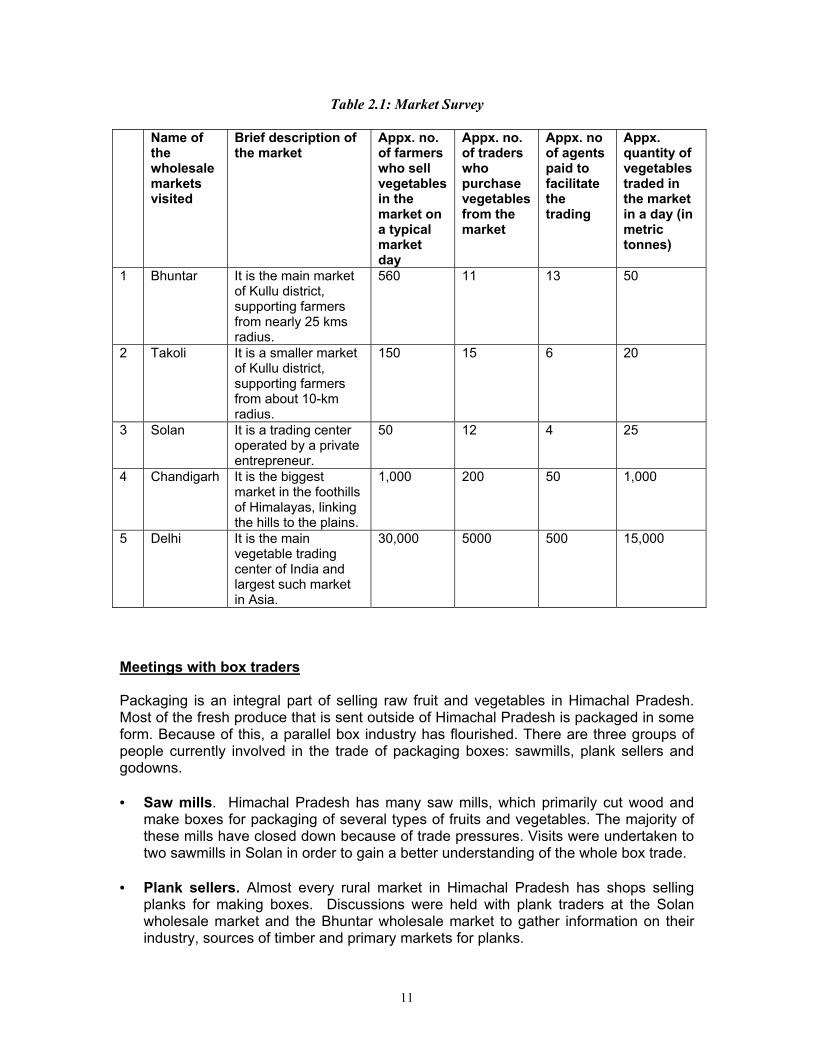

Discussions were held with representatives of each of these actors to gain a better understanding of the marketing systems in place, and to ascertain what are considered to be important post-harvest and marketing constraints. A summary of the wholesale markets surveyed is given in Table 2.1.

10

Table 2.1: Market Survey Name of

the wholesale markets visited

Brief description of the market

Appx. no. of farmers who sell vegetables in the market on a typical market day

Appx. no. of traders who purchase vegetables from the market

Appx. no of agents paid to facilitate the trading

Appx. quantity of vegetables traded in the market in a day (in metric tonnes)

1 Bhuntar It is the main market of Kullu district, supporting farmers from nearly 25 kms radius.

560 11 13 50

2 Takoli It is a smaller market of Kullu district, supporting farmers from about 10-km radius.

150 15 6 20

3 Solan It is a trading center operated by a private entrepreneur.

50 12 4 25

4 Chandigarh It is the biggest market in the foothills of Himalayas, linking the hills to the plains.

1,000 200 50 1,000

5 Delhi It is the main vegetable trading center of India and largest such market in Asia.

30,000 5000 500 15,000

Meetings with box traders Packaging is an integral part of selling raw fruit and vegetables in Himachal Pradesh. Most of the fresh produce that is sent outside of Himachal Pradesh is packaged in some form. Because of this, a parallel box industry has flourished. There are three groups of people currently involved in the trade of packaging boxes: sawmills, plank sellers and godowns.

Saw mills. Himachal Pradesh has many saw mills, which primarily cut wood and make boxes for packaging of several types of fruits and vegetables. The majority of these mills have closed down because of trade pressures. Visits were undertaken to two sawmills in Solan in order to gain a better understanding of the whole box trade.

•

•

Plank sellers. Almost every rural market in Himachal Pradesh has shops selling planks for making boxes. Discussions were held with plank traders at the Solan wholesale market and the Bhuntar wholesale market to gather information on their industry, sources of timber and primary markets for planks.

11

Godowns (warehouses) of planks. Kalka is the border town between Himachal Pradesh and Punjab where huge godowns of packaging planks are located. Four of these godowns were visited to gather information on their industry, where the timber originates and who constitutes their primary market.

•

Meeting with transporters Near the Azadpur Mandi is located a transport nagar (a town or suburb wholly committed to trucking and transportation), that is one of the largest centers of fleet owners in India. The commission agents of Delhi, who procure vegetables from Himachal Pradesh, normally hire trucks from this nagar. Discussions were undertaken with one fleet owner, "Five star transport agency" in Delhi, to gain an insight into this trade and the problems associated with the transport of perishable fruit and vegetables. Further discussions were held with the transport union of Bhuntar, Himachal Pradesh. Meetings with Agriculture Departments Officially, the State Department of Agriculture is responsible for the promotion of new varieties of fruit and vegetables in Himachal Pradesh. This department is also responsible for maintaining statistical information about the agricultural area and the production under various crops. Discussions were undertaken with the "Subject Matter Specialist - Vegetables" in the Directorate of Agriculture to ascertain the history and status of vegetable production in Himachal Pradesh. Further discussions were held with Mr. J. R. Thakur, Assistant Director of the Horticulture Research Station, Bajora. Meetings with the Horticulture University Solan has the only University of Horticulture in Himachal Pradesh. This university has also been involved in research and development into new varieties of fruits and vegetables. Discussions were held with the Director, Extension Department, of the University, and with Mr. D. S. Thakur, Director of Agriculture Research Station, Bajora, to gain a better understanding of the development of vegetable cultivation in Himachal Pradesh. Meeting with NGOs A number of NGOs operate in Himachal Pradesh. One of the largest of these is Ruchi with whom IDE linked to undertake the farmer discussion meetings. Discussions were held with Mr. Dharamvir Singh (Ruchi), Mr. Walia (Society for Technology Development) and Mr. Rajendra Thakur (Serve India) to understand the village dynamics and the vulnerability context of the study villages. Meetings with Agriculture input dealers Both Solan and Kullu have a large number of retail shops selling seeds and pesticides. Many of these dealers sell the micro irrigation kits developed and promoted by IDE and so a very good rapport has evolved over the years with these dealers. Interviews were undertaken with16 of the dealers to gain further knowledge on the business of vegetable cultivation in the study districts. One of these dealers facilitated a linkage between IDE and the target farmers during the farmer discussion meetings in Kullu.

12

2.1.2 Predominance of Fruit and Vegetables in Cultivation Using data gathered from the stakeholder discussion meetings, along with observations made in the field, a list was drawn up of the predominant fruit and vegetables cultivated in the project locations and the acreage allocated to each. 2.1.3 Analysis of Vegetable Crops, by Value and Perishable Status Using data gathered from the stakeholder discussion meetings, along with technical knowledge, an analysis of the value to the farmer and the perishable status of the key crops was calculated. 2.1.4 Understanding the Key Pathways for the Flow of Goods Discussions were held with the stakeholder groups outlined above to ascertain the key pathways for the flow of goods. Information gathered from these discussions was supported by observations made by field staff at farms, markets and retail outlets. The principle pathways studied were

• Farms - markets – consumers • Technology Manufacturer– Distributor - Farmer • Information – Dissemination source - Farmer

13

STAKEHOLDER DISCUSSIONS PLATE 5: Village Meeting at Panchad PLATE 6: Farmers at Bhuntar Wholesale Market PLATE 7: Sawmill at Solan Making Wooden Boxes for Packaging Vegetables

14

3.0 RESULTS AND DISCUSSION 3.1 Identification of Key Produce and Technological Constraint Facing Farmers

Entering High Value Markets 3.1.1 Stakeholder Discussions The stakeholder discussion meetings held with farmers took place over the course of one month. The number of villagers participating in the meetings in each location is given in Table 3.1.1.

Table 3.1.1: Summary of PRA discussion meetings with micro and small-scale farmers

Date of

meeting Meeting organized by

Name of the village where meetings were held

Name of the IDE field office to which the village belongs

No. of households in the village (as stated by villagers)

Total population of the village (as stated by villagers)

No. of villagers participated in the meeting

1 18.5.2000 Ruchi, NGO Panchad Solan 54 324 29 2 19.5.2000 Ruchi, NGO Shargaon Solan 75 400 31 3 21.5.2000 Ruchi, NGO Sanora Solan 53 333 30 4 20.5.2000 Ruchi, NGO Kolan Solan 87 325 30 5 6.6.2000 Laxmi Seeds Bhadyali Kullu 29 153 18 6 21.6.2000 Laxmi Seeds Jarad Kullu 40 250 50 7 7.6.2000 Laxmi Seeds Dhalasni Kullu 85 541 18 8 20.6.2000 Laxmi Seeds Ghurdoor Kullu 50 250 22 Information generated through the farmer discussion meetings was analysed using the Sustainable Livelihoods Framework. The intention of this analysis was to provide some initial understanding of the livelihood patterns existing in the selected villages, an in-depth socio-economic appraisal has been carried out independently of this needs identification study (report to follow). The livelihood issues arising out of the stakeholder discussions are summarized in Table 3.1.2 below. From Table 3.1.2, it can be seen that the mode land holding in the study locations is very small, often less than one hectare, which relates to a wealth ranking beneath the poverty level. The land is exposed to extreme weather conditions that increase the vulnerability of the farmers. Discussions revealed that following a climatic disaster farmers may react by reducing the area of land they allocate to high-risk crops, such as tomatoes, and grow more low risk, low-value crops in their place. This pattern is then reversed as the farmer becomes more willing to increase his risk in order to increase his income. This decision is unlikely to be solely based on climatic factors but will include other factors that impact upon vulnerability such as market fluctuations, transport problems etc. Changes in cropping patterns will only impact upon the project if outputs of the selected produce fall to a level where supplying high-value markets is no longer viable. This is unlikely to happen as cropping decisions will be made at a local level and so will vary between villages.

15

Table 3.1.2: Livelihoods Related Information Categorized by Capital Asset

Vulnerability context

Human capital Natural capital Social capital Financial capital

Ghu

ddur

Frequent hail storms cause severe damage to crops

88% men and 62% women of this village are literate.

Average land holding is 0.3 ha, streams irrigate 60% of the agriculture land.

People of this village are united. There are two women's groups in the village.

10% of farmers take a loan from the bank; others secure loan from family links.

Dha

lasn

i

30% farmers lose their tomato crop every year because of pest attack and poor seed quality.

36% farmers of this village belong to backward community. But 97% men and 95% women are literate.

30% farmers have less than 0.2 ha, 50% between 0.2 to 0.4 ha and 20% more than 1 ha land.

The village is more united than surrounding villages and has one women's group.

There is no formal credit institution in the vicinity of the village.

Jara

d

Heavy hailstorm and prolonged rain occurring each year damage the crops.

There is a primary school in the village. 93% men and 55% women are literate.

25% of farmers have less than 1 ha, 65% between 1 to 2 ha, 10% more than 2 ha land.

People of this village are united. There is one women's group in the village.

The farmers have access to banks at Bhuntar. Seed dealers also offer credit.

Bha

dyau

li Cloud burst in the nearby village erodes soil and houses.

25% of farmers of this village belong to backward community. But 95% men and 89% women are literate.

Average land holding is 0.5 ha. There is no irrigation facility in the village.

People of this village are united. There is one women's group in this village.

There is no formal credit institution in the vicinity of the village.

Kol

an

Uncertain rains cause damage to crops and increase pest attack.

There is a school at Khour, most of the young generation have studied up to 10th class.

Average land holding is 0.5 ha. Low yielding streams are used for irrigation.

People of this village are united. There is one women's group in this village.

There are two banks at 10 km distance. Internally within the village farmers manage loan up to Rs.2000.

Sano

ra

Landslide occurs every year during rainy season damaging tomato crop.

There is a middle school in the nearby village. People from this village are also employed outside the village.

Average land holding is 0.8 ha. Farming is done in terraces.

People of this village are united. One women's club and one farmer's club are recently formed.

No loan from the banks due to lengthy procedures. Traders provide seasonal credit.

Sarg

aon

Land slide and hail storm occur causing damage to crops and blocking roads.

School at Shargaon up to 10th class. Most of the younger generation goes to schools.

Average land holding is 0.4 ha. RUCHI NGO has constructed a tank for life saving irrigation.

People of this village are united. There is one farmer's club in this village.

No loan from the banks due to lengthy procedures. Traders provide seasonal credit.

Panc

had

Cloud burst and land slide occur regularly damaging tomato and potato crops.

Education level is good. People from this village are also employed outside the village.

Average land holding is 0.4 ha. RUCHI NGO has constructed a tank for life saving irrigation.

People of this village are united. There are one farmer's club, one watershed committee and one women's club in this village.

There is a bank at Habban, but no loans are taken from the bank. People take small loans from the women's group.

16

The high level of literacy within the study locations is representative of the State average. This enables the community to make informed decisions about their farming practices and cropping choices. This will be beneficial to the project as farmers will be in a better position to become fully involved in technology development and selection discussions and in making appropriate technology purchasing choices. Size of land holding and presence of irrigation impact upon the volume of high value crops planted. Typically, the high-value crops require good irrigation if they are to crop well. Without the irrigation the chance of success is much smaller and so farmers plant a proportionately smaller area of their holding with these crops. Similarly, the less land a farmer holds, the less risk they are prepared to take as land holding and wealth rank are interlinked. The level of unity displayed in each of the study locations is quite typical of mountain communities. This often means that information is disseminated quickly to all members of the community and acceptance of any technological change is more dependant on group uptake than on individual choice. Access to credit through formal institutions is limited and so alternative credit mechanisms have developed in each of the study locations. Often this involves the farmer entering into a credit agreement with traders. The terms of these agreements were not specified but will be investigated further when the project considers the technology retail phase. Information arising from discussions with other stakeholders has been collated and is incorporated into the remaining sections. 3.1.2 Predominance of Fruit and Vegetables in Cultivation Following the survey of farmers and government and independent institutions the following list of out-of-season fruits and vegetables being grown in Himachal Pradesh was drawn up. The predominant fruits grown by the target farmers are mango, lemon, apple, almond, plum and pears. However, in discussions farmers specified that vegetables were more important to them in terms of potential cash returns and exposed them to a lower level of risk for this return. The remainder of the data collection exercise therefore focused on vegetable production. Eleven off-season vegetables were found to be popularly grown in Himachal Pradesh: 1. Green pea 2. Tomato* 3. Beans 4. Garlic 5. Cabbage 6. Cauliflower 7. Raddish 8. Okra 9. Cucumber 10. Capsicum 11. Brinjal (Egg plant or aubergine)

17

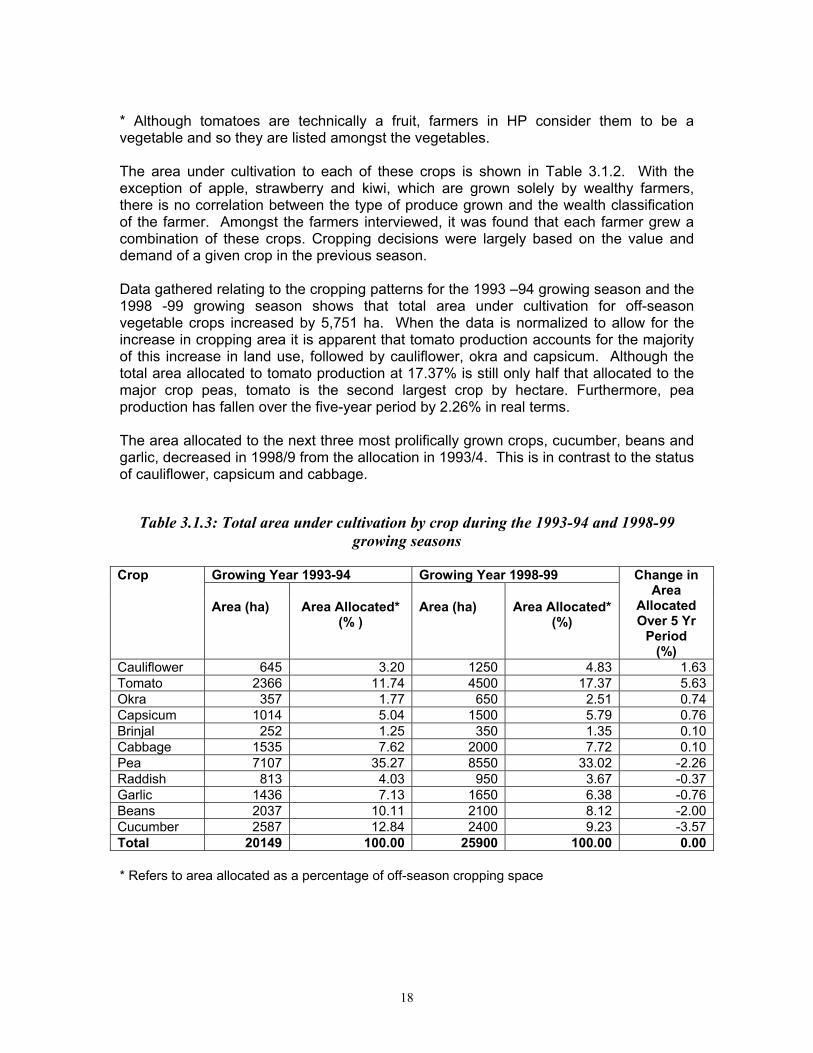

* Although tomatoes are technically a fruit, farmers in HP consider them to be a vegetable and so they are listed amongst the vegetables. The area under cultivation to each of these crops is shown in Table 3.1.2. With the exception of apple, strawberry and kiwi, which are grown solely by wealthy farmers, there is no correlation between the type of produce grown and the wealth classification of the farmer. Amongst the farmers interviewed, it was found that each farmer grew a combination of these crops. Cropping decisions were largely based on the value and demand of a given crop in the previous season. Data gathered relating to the cropping patterns for the 1993 –94 growing season and the 1998 -99 growing season shows that total area under cultivation for off-season vegetable crops increased by 5,751 ha. When the data is normalized to allow for the increase in cropping area it is apparent that tomato production accounts for the majority of this increase in land use, followed by cauliflower, okra and capsicum. Although the total area allocated to tomato production at 17.37% is still only half that allocated to the major crop peas, tomato is the second largest crop by hectare. Furthermore, pea production has fallen over the five-year period by 2.26% in real terms. The area allocated to the next three most prolifically grown crops, cucumber, beans and garlic, decreased in 1998/9 from the allocation in 1993/4. This is in contrast to the status of cauliflower, capsicum and cabbage.

Table 3.1.3: Total area under cultivation by crop during the 1993-94 and 1998-99 growing seasons

Growing Year 1993-94 Growing Year 1998-99

Crop

Area (ha) Area Allocated* (% )

Area (ha) Area Allocated* (%)

Change in Area

Allocated Over 5 Yr

Period (%)

Cauliflower 645 3.20 1250 4.83 1.63 Tomato 2366 11.74 4500 17.37 5.63 Okra 357 1.77 650 2.51 0.74 Capsicum 1014 5.04 1500 5.79 0.76 Brinjal 252 1.25 350 1.35 0.10 Cabbage 1535 7.62 2000 7.72 0.10 Pea 7107 35.27 8550 33.02 -2.26 Raddish 813 4.03 950 3.67 -0.37 Garlic 1436 7.13 1650 6.38 -0.76 Beans 2037 10.11 2100 8.12 -2.00 Cucumber 2587 12.84 2400 9.23 -3.57 Total 20149 100.00 25900 100.00 0.00 * Refers to area allocated as a percentage of off-season cropping space

18

Discussions with Farmers Without exception, all farmers involved in stakeholder discussion meetings identified tomatoes and plums as the crops that offer the greatest opportunity for increasing their incomes. Demand for these crops is currently greater than supply, and financial returns are high. Both crops are considered fairly high risk owing to their susceptibility to disease and pest attack. However, where markets are secure, farmers consider this risk is worth taking on at least part of their holdings. The risk is balanced by growing other low risk crops comprising varying percentages of their land allocation according to the level of risk they are prepared to take. 3.1.3 Analysis of Vegetable Crops, by Value and Perishable Status Using the data gathered above, five of the most important crops, in terms of area under cultivation, were analyzed on the basis of their value to the farmer's livelihood and their post-harvest perishability. Cost benefit analysis of the net income provided by tomatoes, peas, cabbage, cauliflower and capsicum is given in Table 3.1.3 Though an individual farmer grows these crops in a fraction of a hectare, the calculations have been done on a per hectare basis using the total hectarage under cultivation for each crop.

Table 3.1.4: Cost benefit analysis for five preferred crops

Crop Production (MT / ha)

Area under Cultivation

(ha)

Sale value (Rs) Input cost (Rs)

Net income (Rs)

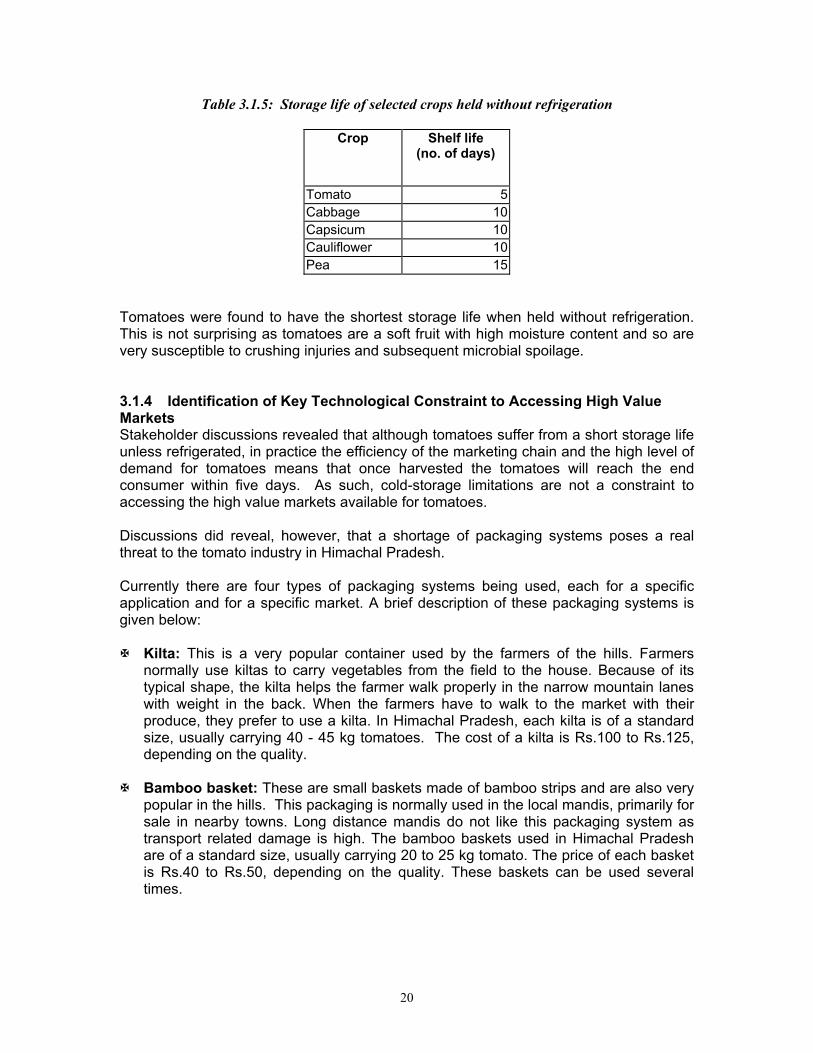

Tomato 36.0 4500 22,161,600,000 4,034,286,000 18,127,314,000 Cauliflower 27.5 8550 22,630,781,250 6,936,657,750 15,694,123,500 Cabbage 27.5 2000 4,537,500,000 1,536,095,000 3,001,405,000 Pea 12.5 1250 894,531,250 160,671,875 733,859,375 Capsicum 9.0 1500 830,196,000 206,955,000 623,241,000 From the above table it is clear that, in Himachal Pradesh, tomatoes generate the highest income per hectare for the farmers. Furthermore, tomato production contributes the most to total income generation of the crops analysed. These crops were then analyzed on the basis of their shelf life, which is expressed in terms of the number of days the produce can be stored without refrigeration in Himachal Pradesh. Table 3.1.4 shows the approximate storage life without refrigeration for the five crops being assessed:

19

Table 3.1.5: Storage life of selected crops held without refrigeration

Crop Shelf life (no. of days)

Tomato 5 Cabbage 10 Capsicum 10 Cauliflower 10 Pea 15

Tomatoes were found to have the shortest storage life when held without refrigeration. This is not surprising as tomatoes are a soft fruit with high moisture content and so are very susceptible to crushing injuries and subsequent microbial spoilage. 3.1.4 Identification of Key Technological Constraint to Accessing High Value Markets Stakeholder discussions revealed that although tomatoes suffer from a short storage life unless refrigerated, in practice the efficiency of the marketing chain and the high level of demand for tomatoes means that once harvested the tomatoes will reach the end consumer within five days. As such, cold-storage limitations are not a constraint to accessing the high value markets available for tomatoes. Discussions did reveal, however, that a shortage of packaging systems poses a real threat to the tomato industry in Himachal Pradesh. Currently there are four types of packaging systems being used, each for a specific application and for a specific market. A brief description of these packaging systems is given below:

Kilta: This is a very popular container used by the farmers of the hills. Farmers normally use kiltas to carry vegetables from the field to the house. Because of its typical shape, the kilta helps the farmer walk properly in the narrow mountain lanes with weight in the back. When the farmers have to walk to the market with their produce, they prefer to use a kilta. In Himachal Pradesh, each kilta is of a standard size, usually carrying 40 - 45 kg tomatoes. The cost of a kilta is Rs.100 to Rs.125, depending on the quality.

Bamboo basket: These are small baskets made of bamboo strips and are also very

popular in the hills. This packaging is normally used in the local mandis, primarily for sale in nearby towns. Long distance mandis do not like this packaging system as transport related damage is high. The bamboo baskets used in Himachal Pradesh are of a standard size, usually carrying 20 to 25 kg tomato. The price of each basket is Rs.40 to Rs.50, depending on the quality. These baskets can be used several times.

20

Wooden box: This is the most popular packaging technique used for packing fruits and vegetables in India. More than 70% of tomatoes grown in Himachal Pradesh are packed in wooden boxes for transport to markets. Indeed, this is the most commonly used packing material for long distance marketing of nearly all fruits and vegetables in India. Within Himachal Pradesh, apples, pears and peaches are routinely packed in wooden boxes and tomatoes from other tomato growing belts such as Nasik and Pune also utilize wooden boxes. The capacity of the standard tomato box of Himachal Pradesh is 15 kg and the cost is Rs. 15. These boxes are normally used once.

The Government, both Central and Regional in the hill states, is now challenging the extensive use of this packaging box as the volume of wood consumed in the fruit and vegetable packing industry is contributing significantly to deforestation in India. Data gathered in this study suggests that a rough estimate of nearly 100,000 trees must be cut down every year to support the tomato packaging industry in India. Though tomato production is a major source of livelihood security for over 50,000 small farmers in India, the associated packaging industry is creating a significant environmental problem. The findings from all relevant stakeholder discussions indicate that this is a recognized problem and one that farmers, markets and hauliers all wish to address.

Plastic crates: Plastic crates are just being introduced in Himachal Pradesh. Some

local / regional traders go to the local mandis with these crates. They normally purchase loose tomatoes and bring in their own crates. Later they sell the tomatoes on to retailers in the loose form. Each standard plastic crate costs Rs. 200 to Rs.250 and carries 20 kg tomatoes. These crates have a very long life, but are currently only used in local trade. It is possible that the use of these plastic re-usable crates will increase with the pressure to stop using wooden boxes for transporting vegetables and fruits. At the current prices farmers feel the plastic crates are too expensive, hence plastic crates have not replaced the wooden boxes. Disposability is a critical factor and reusable containers are not practical for long distance marketing as it is almost impossible to get them returned.

The findings from this study clearly indicate that the fruit and vegetable market in general, and the tomato market in particular, are very reliant on effective packaging systems. Currently, this need is being met in the main by the use of wooden crates. However, effective and affordable alternatives are urgently required to limit the environmental impact of this trade and to compensate for a likely reduction in availability of box planks following government imposed bans on timber harvesting.

21

PACKAGING SYSTEMS IN USE PLATE 7: Tomatoes Being Transported in a Kilta PLATE 8: Tomatoes Packaged for Sale in Bamboo Baskets

22

PLATE 9: Wooden Boxes Being Constructed by Box Makers PLATE 10: Tomatoes Packaged in Plastic Crates (N.B. the use of bamboo baskets as well showing dual/multiple packaging methods may be in use at one mandi.)

23

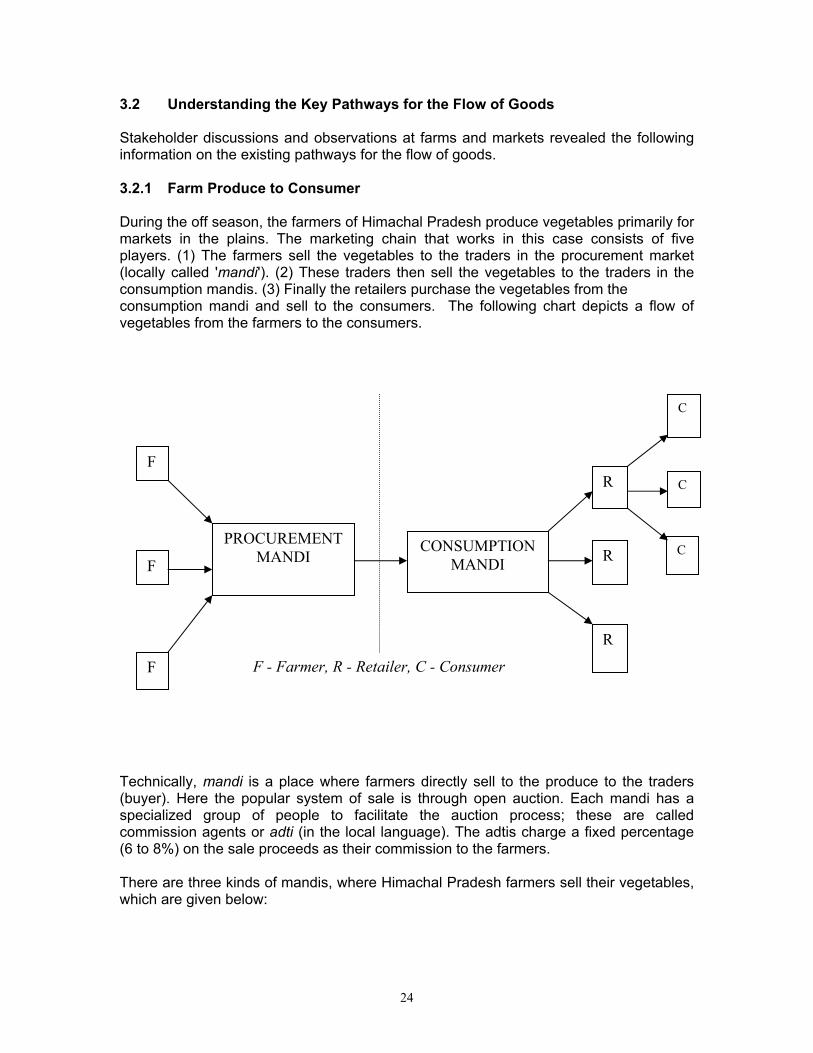

3.2 Understanding the Key Pathways for the Flow of Goods Stakeholder discussions and observations at farms and markets revealed the following information on the existing pathways for the flow of goods. 3.2.1 Farm Produce to Consumer During the off season, the farmers of Himachal Pradesh produce vegetables primarily for markets in the plains. The marketing chain that works in this case consists of five players. (1) The farmers sell the vegetables to the traders in the procurement market (locally called 'mandi'). (2) These traders then sell the vegetables to the traders in the consumption mandis. (3) Finally the retailers purchase the vegetables from the consumption mandi and sell to the consumers. The following chart depicts a flow of vegetables from the farmers to the consumers.

F - Farmer, R - Retailer, C - Consumer

R

R

R

CONSUMPTION MANDI

PROCUREMENT MANDI

F

F

F

C

C

C

Technically, mandi is a place where farmers directly sell to the produce to the traders (buyer). Here the popular system of sale is through open auction. Each mandi has a specialized group of people to facilitate the auction process; these are called commission agents or adti (in the local language). The adtis charge a fixed percentage (6 to 8%) on the sale proceeds as their commission to the farmers. There are three kinds of mandis, where Himachal Pradesh farmers sell their vegetables, which are given below:

24

Local Mandi: These are mandis, which are located inside Himachal Pradesh and within 25km of the villages. Examples of these mandis are the mandis of Solan, Bhuntar and Takoli. Mostly traders from consumer mandis of the nearby states of Punjab and Haryana come to purchase vegetables from these mandis. Sometimes even small retailers from the nearby markets will come to purchase vegetables. Farmers bring their vegetables loose (unpacked) to these markets. Normally in these markets skilled labour is available to pack the vegetables. If the trader needs to pack some vegetables, he pays these skilled laborers to do it. The biggest advantage of these markets is that the auction happens in the presence of the farmer, so he knows the exact price at which the vegetables were sold. Farmers also get paid immediately after the auction is over. The disadvantage is that, these mandis are normally smaller than the other mandis and the total volume of produce that can be sold is less than the other mandis.

•

Regional mandis: These are mandis, which are located in the foot hills of the Himalayas, in states adjacent to Himachal Pradesh. Examples of such mandis are, Chandigarh, Jallandhar, Amritsar etc. These places are big cities in the periphery of the Himalayas having a large customer base of their own and of nearby small towns. Usually some traders purchase vegetables from the above-mentioned local mandis and sell in these regional mandis. At times, some farmers will also directly sell vegetables in these mandis. The vegetable uptake of these mandis is much higher than the local mandis, but the auction rate more or less remains the same.

•

Major mandis: These are mandis that are located in big metropolitan cities like Delhi, Bombay, Calcutta, Madras, Banglore and Guwahati. These mandis cater to the markets of surrounding states. They are very large and so their uptake capacity is correspondingly large. The advantage of these mandis is that almost any quantity of vegetables can be sold in these markets, though the price might vary with the fluctuating volume. Nearly 70% of the tomatoes produced in Himachal Pradesh are sold in the Azadpur (New Delhi) mandi. Normally in the beginning of the tomato season the adtis from Azadpur mandi visit the farmers in Himachal Pradesh and negotiate with the farmers to sell tomatoes through them. During the season the adtis send the trucks daily from Delhi and procure tomatoes from the farmers. These tomatoes are then auctioned in the Azadpur mandi. The farmers are informed by the adtis of the price obtained the following day when the procurement truck arrives again. Azadpur gets tomatoes from various tomato-growing belts of India depending on their growing season, as shown below:

•

Period of the year Procurement belts June - August Himachal Pradesh July - September Pune (Maharastra) September - January Nasik (Maharastra) December - March Abu (Rajasthan) February - April Jaipur (Rajasthan)

25

MARKETING SYSTEM PLATE 11: Farmers Bringing Tomatoes to Market (N.B. Tomatoes are Sold Loose) PLATE 12: Local Mandi (N.B. the tomatoes packed in large plastic crates) PLATE 13: Major Mandi Showing the Scale of Produce Being Loaded onto Vehicles

26

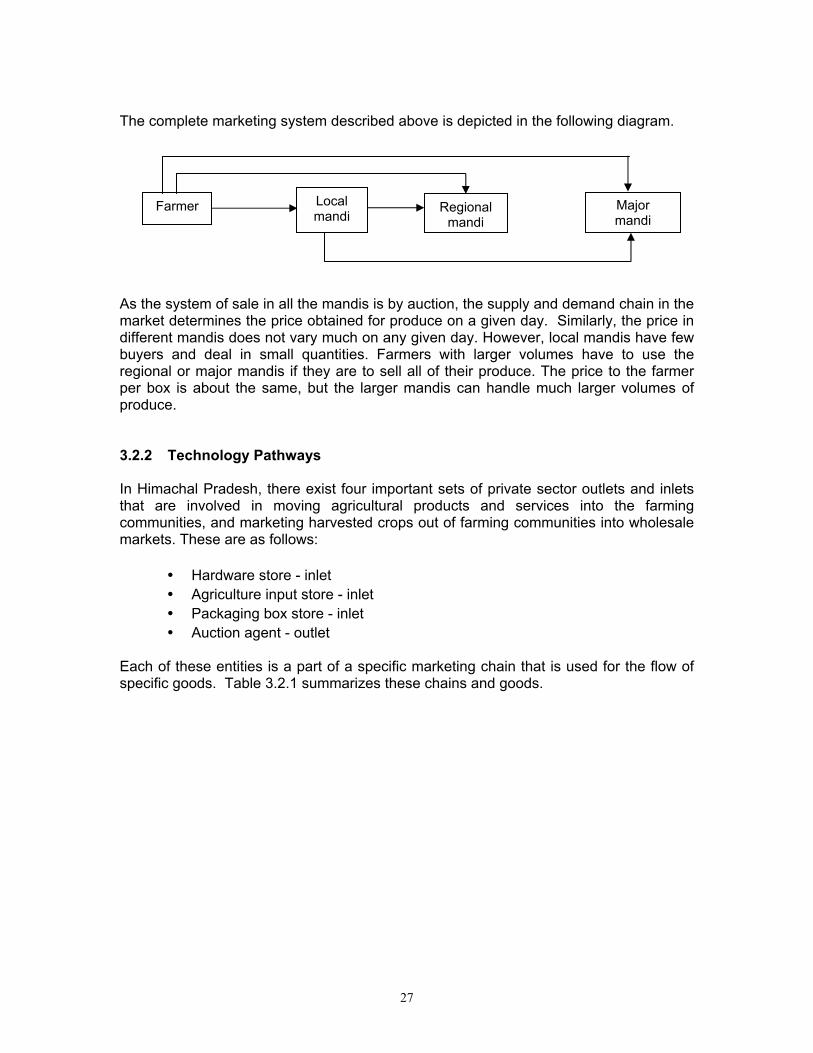

The complete marketing system described above is depicted in the following diagram.

Farmer Regional mandi

Local mandi

Major mandi

As the system of sale in all the mandis is by auction, the supply and demand chain in the market determines the price obtained for produce on a given day. Similarly, the price in different mandis does not vary much on any given day. However, local mandis have few buyers and deal in small quantities. Farmers with larger volumes have to use the regional or major mandis if they are to sell all of their produce. The price to the farmer per box is about the same, but the larger mandis can handle much larger volumes of produce. 3.2.2 Technology Pathways In Himachal Pradesh, there exist four important sets of private sector outlets and inlets that are involved in moving agricultural products and services into the farming communities, and marketing harvested crops out of farming communities into wholesale markets. These are as follows:

• • • •

Hardware store - inlet Agriculture input store - inlet Packaging box store - inlet Auction agent - outlet

Each of these entities is a part of a specific marketing chain that is used for the flow of specific goods. Table 3.2.1 summarizes these chains and goods.

27

Table 3.2.1: Flow of goods and the various marketing chains

Ultimate inlet / outlet Specific goods moved

through the inlet / outlet Marketing chain

Hardware store (inlet) • • • •

Agriculture implements Pump sets PVC pipes HDPE tanks

Fabricators / manufacturers

Wholesalers

Hardware stores

Farmers Agriculture inputs retailer (inlet)

• • • •

Seeds Pesticides Fertilizers Small agriculture tools

Manufacturers

Distributors

Retailers

Farmers Packaging material retailer (inlet)

• Wooden planks for packaging

Saw mills

Warehouses

Retailers

Farmers Auction agent (outlet) • All fruits and vegetables Farmers

Auction agents (adti)

Vegetable traders

Consumers

28

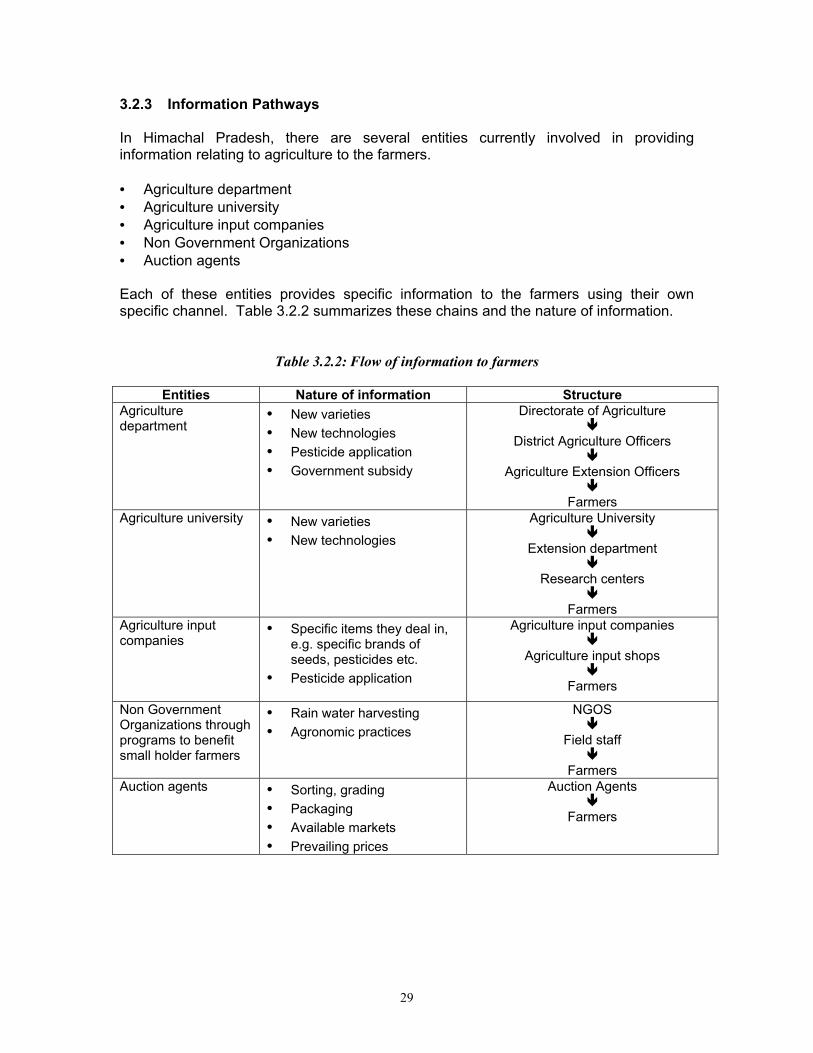

3.2.3 Information Pathways In Himachal Pradesh, there are several entities currently involved in providing information relating to agriculture to the farmers. • • • • •

Agriculture department Agriculture university Agriculture input companies Non Government Organizations Auction agents

Each of these entities provides specific information to the farmers using their own specific channel. Table 3.2.2 summarizes these chains and the nature of information.

Table 3.2.2: Flow of information to farmers

Entities Nature of information Structure Agriculture department

• • • •

New varieties New technologies Pesticide application Government subsidy

Directorate of Agriculture

District Agriculture Officers

Agriculture Extension Officers

Farmers Agriculture university •

• New varieties New technologies

Agriculture University

Extension department

Research centers

Farmers Agriculture input companies

•

•

Specific items they deal in, e.g. specific brands of seeds, pesticides etc. Pesticide application

Agriculture input companies

Agriculture input shops

Farmers

Non Government Organizations through programs to benefit small holder farmers

• •

Rain water harvesting Agronomic practices

NGOS

Field staff

Farmers Auction agents •

• • •

Sorting, grading Packaging Available markets Prevailing prices

Auction Agents

Farmers

29

4.0 CONCLUSION AND RECOMMENDATIONS Based on the information gathered and its analysis the following conclusions have been reached: 1. Of the eleven vegetables that are commonly grown by the smallholder farmers of

Himachal Pradesh, off-season tomatoes offer the greatest income generating potential to the small-holder farmers within Himachal Pradesh. They are, however, a high-risk crop to grow and are subject to a short storage life and high risk of injury and spoilage post-harvest.

2. Four packaging technologies that are currently being used to market tomato were

studied. A standard 15-20 kg wooden box was found to be the preferred packaging material to access the high value and high volume metropolitan wholesale vegetable markets. However, availability of wood is rapidly becoming a problem due to a new government ban on deforestation as well as increased awareness about the environment. Packaging is thus considered a key constraint to farmers accessing high value tomato markets and alternate packaging solutions are a necessity.

3. Four technology flow channels existing in Himachal Pradesh were studied. The

hardware channel and the packaging box supply channel tentatively appear appropriate as channels to provide the developed packaging systems to the small farmer. The project should field test the appropriateness of both of these channels during the second phase of the project.

4. Five information flow channels existing in Himachal Pradesh were studied. Of these,

the auction agent appears to be the most respected and to exert the greatest direct influence on the farmers packaging choices. The other channels, such as the government, universities, NGOs etc., can be used to influence farmers to accept the new packaging systems by advocating against the non-sustainable use of wood as a packaging material.

30

31

REFERENCES HALL, A.J., SIVAMOHAN, M.J.K., CLARK, N., TAYLOR, S. & BOCKETT, G. (1998a) A strategy for research on public and private sector horticulture R&D systems in India: A review of process, concepts, case studies and research needs. Report. Natural Resources Institute, Chatham. HALL, A.J., SIVAMOHAN, M.J.K., CLARK, N., TAYLOR, S. & BOCKETT, G. (1998b) Institutional developments in Indian agricultural R&D systems: The emerging patterns of public and private sector activity. Science, Technology and Development (In press). IDE “The Treadle Pump : Economic power to the landless” Internal report. POLAK, P., NANES, B. & ADHIKARI, D. (1997) A low cost drip irrigation system for small farmers in developing countries. Journal of the American Water Resources Association, 33 (1): 119-124. (Peer reviewed paper) WORLD BANK REPORT (1998) The potential contribution of low cost drip irrigation to the improvement of irrigation productivity in India. pp121-123. In:India – Water resources management sector review: Report on the irrigation sector. (Report Series)