Embed Size (px)

Citation preview

79

The European Journal of Management Studies is a publication of ISEG, Universidade de Lisboa. The mission of

EJMS is to significantly influence the domain of management studies by publishing innovative research articles.

EJMS aspires to provide a platform for thought leadership and outreach.

Editors-in-Chief:

Luís M. de Castro, PhD ISEG - Lisbon School of Economics and

Management, Universidade de Lisboa, Portugal

Gurpreet Dhillon, PhD Virginia Commonwealth University, USA

Tiago Cardão-Pito, PhD

ISEG - Lisbon School of Economics and Management, Universidade de Lisboa,

Portugal

Managing Editor:

Mark Crathorne, MA

ISEG - Lisbon School of Economics and Management, Universidade de Lisboa,

Portugal

ISSN: 2183-4172

Volume 21, Issue 2

www.european-jms.com

THE DETERMINANTS OF VALUE ADDED

TAX REVENUES IN THE EUROPEAN

UNION

Joaquim Sarmento

ISEG – Lisbon School of Economics and

Management, Universidade de Lisboa, Portugal

Abstract

In this paper we assess the critical factors of Value Added Tax

revenues in the European Union, by using a panel data of the

27 countries, between 1998 and 2011. Our findings show that

EU governments have been using tax rates increases to collect

more revenues, both at the normal and the minimum rate. It

was also found that an increase in the implicit rate increases

revenues as well. Tax administration efficiency and experience

is a critical factor for the capacity to collect VAT revenues. A

better legal and institutional environment is shown to be

related with higher revenues. Finally, countries in the

Eurozone are shown to have higher revenues, mainly due to

the fiscal rules that they are subject to. Higher income, as

measured by GDP per capita, increases revenues, on account

of the higher propensity for consumption.

Key words: Value Added Tax, Revenues, VAT revenues, Tax

system, European Union.

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

80

Introduction

Value Added Tax (VAT) can be defined as being “a broad-based business tax imposed at each stage

of the production and distribution process which, when applied nationally, is typically designed to

tax final household consumption” (Tait, Ebel, & Le, 2005, p. 461).

VAT has become more and more relevant in the tax systems around the world, and more than

140 countries using it to tax consumption, which represents over 20% of tax revenues (Keen,

2009). However, particularly in the European Union (EU), VAT is one of the main source of public

revenues. Looking at data from 2011, VAT revenues represented around 7% of GDP, both for the

European Union and the Eurozone, from a total taxation (including social security contributions)

of around 38% of GDP (Eurostat, 2013). According to the same source, total taxation, excluding

social security contributions, represents around 26% of GDP. This means that, in the EU, VAT

represents almost a third of all tax collection. As indirect taxes revenues represent around 13% of

GDP, VAT accounts for more than half of this. In the EU, only personal income taxes have a higher

value than VAT, representing 9% of GDP. Corporate taxes revenues represent just 2.5% of GDP.

Despite the relevance of VAT in tax revenues and the increased pressure of fiscal constraints in

increasing public revenues, little economic research has been carried out on VAT revenues,

particularly at the European level. As far as we know, no paper addresses the main determinants

of VAT revenues in Europe. Some literature exists with databases covering OECD and non-OECD

countries, measuring both the decision to adopt VAT, and the impact of VAT on revenues (Bogetic

& Hassan, 1993, for a panel data of OECD and non-OECD countries, with data for a single year:

1988; Legeida & Sologoub, 2003 for Ukraine; Keen & Lockwood, 2010 for a panel of 143 countries

for 25 years, focusing on the impact on adopting VAT rates and VAT revenues; Addison & Levin,

2011 for sub-Saharan Africa; Kaczyńska, 2015, for Poland). These studies found a positive impact

on revenues from VAT rates, VAT base, economic openness, and administration efficiency; and a

negative impact from the agriculture share of GDP, the use of several tax rates, and exemptions.

This paper addresses the issue regarding what are the main determinants of VAT revenues in the

European Union. For this purpose, we collected data on the VAT revenues in billions of Euros (and

then use the log function) and in percentage of GDP. We aim to assess the impact on VAT

revenues from tax administration efficiency and experience, from the level of VAT rates, from the

level of imports and services in the GDP, from the fiscal position and the participation in the

Eurozone, and also from the country’s legal environment. We divided the variables into four

groups: 1) VAT variables (VAT rate, minimum rate and implicit rate); 2) Economic variables

(imports, services and fiscal deficits as a percentage of GDP); 3) Tax administration efficiency

(measure by VAT C-efficiency, by the number of years of VAT application, and by Government

efficiency); 4) Legal and institutional environment (measure by the level of corruption and the rule

of law). We then added two control variables: whether the country is a member of the Eurozone,

and the log of GDP per capita.

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

81

We found a positive relationship between VAT rates and the amount of revenues, which shows

that, over the last years, countries have increased their tax rates in the face of fiscal constraints.

Tax administration efficiency also plays an important role in the capacity of governments to collect

revenues. A better legal and institutional environment tends to increase revenues. Countries in the

Eurozone are more likely to have higher revenues, which could be explained by the fact that they

are more subject to tight fiscal rules. A higher income, measured by GDP per capita, tends to

produce more VAT revenues, which could be explained by the marginal propensity for

consumption, particularly for goods and services subject to the normal rate.

This paper is novel with regards to previous literature in several aspects: first, it is the only study,

to our knowledge, that specifically addresses VAT revenues in the European Union and the

Eurozone context. Particularly important is the fact that we compared only European Union

countries, their VAT rates and tax administrations, and their economic, legal and institutional

environment. Second, with exception of the study by Keen & Lockwood (2010), all recent studies

have focused on a single country. Third, with regards to the study mentioned, we address different

questions. Whereas Keen & Lockwood (2010) study the impact on revenues from adopting VAT

and the impact of the VAT on the effectiveness of the tax system, we focus on what are the main

determinants of VAT revenues. We also innovate by considering new variables, such as corruption,

rule of law, and tax administration efficiency measures.

This paper is organized as follow: Chapter 2 presents a literature review on VAT revenues studies.

Data and methodology are presented in Chapter 3 and results in Chapter 4. Chapter 5 concludes.

Literature review

Despite the importance and popularity of VAT as a way of taxing consumption and of increasing

public revenues, there is little academic literature on the subject (Keen, 2009). VAT has been

adopted by all the European Union countries (VAT is mandatory, see for instance De La Feria et

al., 2010, Cnossen, 2011), and also in almost all African and Latin America countries (Tait, 1989;

Williams, 1996; Bird & Gendron, 2007; Keen, 2009). In the developing world, it has also been seen

as a source of change in tax and economic policy (Ebrill et al., 2001; Bird & Gendron, 2007; Keen,

2009, Keen & Lockwood, 2010). The introduction of VAT over the past few decades has been the

most visible tax reform undertaken by developing countries (Tanzi & Zee, 2000). There is some

evidence, particularly in the Third World, that those countries that have adopted VAT raise more

revenues (Keen & Lockwood, 2010).

The popularity of VAT comes from several sources, one being its potential scope for identifying

and taxing the economic contribution - or added value - made by any activity of a business or

commercial nature (Williams, 1996). The other issue regards its relative simplicity, with an invoice-

credit mechanism for collection (Mello, 2008, 2009). There is also the issue of it being economic

neutral, and the fact that it is a powerful tool for economic stabilisation (Lindholm, 1970). Finally,

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

82

several authors point out VAT’s efficiency and its high impact on collecting revenues. It is

sometimes referred to as a “cash machine” (Keen & Lockwood, 2006, 2010), but, as with any tax,

it is vulnerable to tax evasion, particularly “carrousel fraud” (Keen & Smith, 2006; van Brederode,

2008; Sergiou, 2012).

The Economic literature on taxation has been mainly focused on the optimal design of tax systems

and tax evasion (see Hanlon & Heitzman, 2010, for a review of tax research, Slemrod, 1990 for the

optimal tax system issue, and Dharmapala, 2014 for tax evasion). However, there is less literature

on the main determinants of tax revenues, and particularly on VAT revenues.

One of the first studies on the determinants of VAT revenues was carried out by Bogetic & Hassan

(1993). Using a sample of 34 countries, they found that the key variables influencing VAT revenue

performance were: tax rate, tax base (i.e, if VAT applies to all goods and service, or there is some

exceptions), and tax rate dispersion. The first two increase tax revenues, whereas the last tends

to reduce it. Bogetic & Hassan also found that countries with a single VAT rate tend to have more

revenues than countries with several rates. The positive impact of tax rates on VAT revenues was

also evidenced in Shoup et al. (1990). There is also evidence that VAT tax base has an impact on

VAT revenues (Kay & Davids, 1990). In the case of the negative impact of several tax rates, Bogetic

& Hassan (1993) confirms the previous results of Tait (1988). Similar results were latterly obtained

by Legeida (2003).

Godin & Hindriks (2015), using a database covering 203 countries with 40 tax items over the period

1980-2010, assess some of the main determinants of tax collection. The authors found a positive

effect on tax revenues from economic growth, government efficiency, and trade openness, along

with the size of tax rates. On the contrary, trade taxes and a higher share of agriculture in GDP

decreases the amount of tax revenues. Another study, by Keen and Lockwood (2010), used a panel

set of 143 countries over 26 years. The authors analysed what leads countries to adopt VAT, and

the impact of VAT on tax revenues. Their study concludes that, in the long run, VAT is associated

with an increase in tax revenues. They found several positive determinants of VAT revenues,

namely: income per capita, the openness of the economy, and the size of the younger population.

On the contrary, countries were agriculture has a higher share of GDP tend to have less revenues.

Keen (2009) also found evidence of the negative impact of exemptions and the use of reduced

rates on revenues. The fact that trade also has a positive impact on VAT revenues was also

concluded by Rodrick (1998) and Hines & Desai (2005). Similar results were found for sub-Saharan

Africa by Addison & Levin (2011).

Data and methodology

The objective of this paper is to assess the main determinants of VAT revenues. For this purpose,

we collected as our first dependent variable - annual VAT revenue in billions of Euros - for a panel

data of 27 EU countries, for a period between 1998 and 2011. For the Eurozone countries, data is

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

83

available directly from Eurostat (2013). For the non-Eurozone countries, we first collected from

Eurostat (2013) the value of VAT revenues as a percentage of GDP, and then multiplied that value

for the country’s GDP in billions of Euros. This last information is available at AMECO, the

European Commission’s online database. For the robustness check, we used a second dependent

variable - VAT revenue as a percentage of GDP, which is also available from Eurostat (2013).

We study VAT revenues by means of the following model (we run OLS with fixed effects, and also,

in the case of the second dependent variable, a GLM):

𝑌𝑖𝑡

= 𝛽0 + 𝛽1𝑉𝐴𝑇𝑟𝑎𝑡𝑒𝑖𝑡 + 𝛽2𝑚𝑖𝑛𝑟𝑎𝑡𝑒𝑖𝑡 + 𝛽3𝑖𝑚𝑝𝑙𝑖𝑐𝑖𝑡𝑟𝑎𝑡𝑒𝑖𝑡 + 𝛽4𝐼𝑚𝑝𝑜𝑟𝑡𝑠𝑖𝑡 + 𝛽5𝑆𝑒𝑟𝑣𝑖𝑐𝑒𝑖𝑡

+ 𝛽6𝐷𝑒𝑓𝑖𝑐𝑖𝑡𝑖𝑡 + 𝛽7𝐶𝑒𝑓𝑓𝑖𝑐𝑖𝑡 + 𝛽8𝑛𝑦𝑒𝑎𝑟𝑠𝑉𝐴𝑇𝑖𝑡 + 𝛽9𝐺𝑒𝑓𝑓𝑖𝑐𝑖𝑡 + 𝛽10𝐿𝑜𝑤𝐶𝑜𝑟𝑟𝑖𝑡 + 𝛽11𝑟𝑙𝑎𝑤𝑖𝑡 + 𝜇𝑖

Where:

Yit stands for our dependent variable (log of VAT revenues) or, for control of robustness of our

model, our second dependent variable - VAT revenue as a percentage of GDP. i and t are country

and time indicators respectively.

The main determinants were divided into the following categories: variables regarding Value Added

Tax, in order to assess how changes in VAT rates affect revenues; variables regarding the economic

environment, in order to analyse the impact of economic conditions in collecting revenues, and;

institutional variables. For the latter, we have variables regarding how tax administration efficiency

increases VAT revenues, and also variables concerning the impact of the legal and political

environment of each country on VAT revenues.

For the VAT variables, we expect normal statutory rate and implicit rate to increase tax revenues.

We use the following variables:

VATrate represents the normal statutory VAT rate for each year, in each country. Data was

collected from Eurostat (2015). Naturally, increases in VAT rate are expected to increase revenues

(see several studies regarding the impact of VAT rates on revenues: Engel et al., 2001; Pagan et al.,

2001 and regarding the impact of the standard VAT rate in revenues: Ebrill et al., 2001; Matthews,

2003; Bikas & Rashkauskas, 2011). Therefore, we expect this variable to be positively related with

VAT revenues.

minrate referees to the minimum statutory rate used in each country for the designed period. VAT

directives allow countries to choose which services and products (usually related with social issues)

have a lower VAT rate than the normal rate. Data was collected from Eurostat (2015). The

literature tends to consider that a minimum rate tends to increase the consumption of the

abovementioned products, creating a positive price-elasticity (see for instance Zee, 1995; Creedy

et al., 2004; Booters et al, 2010). We expect minimum rate to have a negative impact on VAT

revenue, as it represents an erosion of the tax base.

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

84

Implicitrate represents the implicit VAT rate of each country, in each year of our sample. This is the

effective VAT rate, measured according to Eurostat (2013) as the total VAT revenues divided by

the tax base (in this case consumption). It could be argued that this is the value of a single VAT tax

rate that would provide the same revenue as the current VAT rates in each country. Furthermore,

Eurostat (2013) refers that implicit rates are computed as being the ratio of total tax revenues of

the category (either consumption, labour, or capital taxes) to a proxy of the potential tax base,

defined using the production and income accounts of the national accounts. A higher tax is

associated with higher revenues, despite the negative impact that it can have on private

consumption (Alm et al., 2013).

Regarding the economic variables, we expect good economic times to have, naturally, a positive

impact on VAT revenues. We used the following variables:

Imports represents the imports of the country as a percentage of GDP. Data was collected from

AMECO. Imports are associated with more revenues, as VAT is charged by Customs. However,

in this case, for most of the countries, the majority of the imports are from inside the European

Union, and therefore, we do not anticipate a clear signal from this variable.

Services represents the proportion of services in the GDP (as a percentage). Data was collected

from AMECO, and it has a higher component of added value, and is expected to increase revenues.

Deficit represents the government fiscal deficit, in the national accounts. Data was collected from

AMECO. We do not have a predefined signal for this variable. Higher deficits can be the result of

lower tax revenues, but they can also cause an increase in tax rates, leading to higher revenues.

We also expect tax administration efficiency to have a positive impact on revenues. To measure

this efficiency, we used the following:

Ceffic stands for the C-efficiency of VAT for each country, for each year of the sample. C-efficiency

is a wider and broadly used efficiency measure for VAT. C-efficiency is an indicator of the departure

of VAT from a perfectly enforced tax, which is levied at a uniform rate on all consumption (Keen,

2013). C-efficiency is calculated by VAT revenues divided by the value of the consumption, which

is divided again by the normal VAT rate. The data used to calculate C-efficiency was collected from

Eurostat (2013) for VAT revenues, and from AMECO for consumption values, and Eurostat (2015)

for normal rate VAT. This indicator has been used in the literature to understand the determinants

of VAT compliance (Gebauer et al., 2007; Aizenman & Jinjarak, 2008; De Mello, 2009), and to

analyse and compare the level of VAT evasion across countries (Jack, 1996; Bird & Gendron, 2007;

OECD, 2008), and also in several countries, across time (Hybka, 2009). Using a sample of several

European countries, Keen (2013), found that changes in VAT revenues have been driven much less

by changes in standard rates, than by changes in ‘C-efficiency’. A higher value in C-efficiency means

a more efficient tax administration for collecting revenues and for fighting tax evasion. It is also

important to stress that VAT tends to lead to less tax evasion than other taxes, mainly due to the

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

85

invoice-credit mechanism used for its collection (Allingham & Sandmo, 1972; Slemrod & Itzhaki,

2002; Mello, 2009). There is some agreement in the literature, that indirect taxes are easier to

administrate (Piccolino et al., 2014). Increasing tax administration efficiency and enforcement

spending have a positive impact in reducing tax evasion (Engel et al., 2001). Therefore, we expect

this variable to have a positive coefficient, as a higher efficiency in collecting taxes is associated with

lower tax evasion, and naturally, with higher revenues.

nyearsVAT represents the number of years since VAT was introduced in each country. Data was

collected from Eurostat (2015) and it was found that more experience is related with better tax

compliance, and thus with greater efficiency and lower tax evasion (Agha & Haughton, 1996; Ebrill

et al., 2001; Aizenman & Jinjarak, 2008). Thus, we expect this variable to have a positive coefficient.

Geffic is an indicator of government efficiency. This is a dynamic variable, which ranges from 0 to

10 (with 10 being the highest level of efficiency in the government), and it was collected from the

World Bank. However, for each country and year, we used the quartile positions of each country

in the index. Godin & Hindriks (2015) found evidence of a positive relationship between better

government and transparency and the overall performance of government tax collection. We used

this variable as a proxy for tax administration efficiency. As mentioned by Tanzi & Zee (2000) and

Cnossen (2015), a complex tax system, in terms of tax rates, brackets, exemptions and deductions,

is generally less efficient. We expect more efficient governments to be more able to reduce tax

evasion and to collect revenues. Therefore, we expect this variable to be positive.

To measure a country’s legal and institutional quality (we expect this to have a positive impact on

the collection of tax revenues), we used the following variables:

LowCorr represents the corruption level of each country, for each year, measured by the World

Bank. The index is a dynamic variable ranging from 0 to 10 (with 10 being the lowest corruption).

Once again, we used the quartile positions of each country in the index. Corruption should

decrease tax revenues, either by increasing the size of the shadow economy (Bird, 2008;

Braşoveanu et al., 2009; Sokolovska, 2015), or by reducing the efficiency of tax administration.

Therefore, as this index increases when corruption is reduced, we expect a positive coefficient

(i.e.: an increase in the index means less corruption, and therefore more revenues).

Rlaw represents the level of the rule of law. The index is a dynamic variable, ranging from 0 to 10

(with 10 being the highest level of rule of law), collected from the World Bank. Once again, we

used the quartile positions of each country in the index. This represents the quality and strength

of the legal system, and it shows the judicial limits of government to realize their policy programme

through the legislative arm of government. Better enforcement is expected to increase revenues.

For control purpose, we add the following independent variables:

Euro is a dummy that equals 0 if the country did not belong to the Eurozone in that year, and 1 if

it did belong to it. As Eurozone countries have been subject to more fiscal constraints, mainly from

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

86

the Stability and Growth Pact (Buti, 1998, 2003, 2005, 2007; Dworak et al., 2002; Heipertz, 2004;

Afonso, 2010, Hernández et al., 2013), we expect an increase in tax revenues.

LogofGDPpercapita is the log-function of GDP per capita. Higher GDP per capita should increase

revenues. This increase is due to the propensity to consumption of wealthier people, particularly

in goods and services subject to the normal tax rate. Several authors have showed that higher GDP

per capita (using the log values) is associated with higher VAT efficiency and VAT revenues (Ebrill

et al., 2001; Cizek et al., 2012; Alm et al., 2013; Zidkova, 2014 and Godin & Hindricks, 2015).

Table 1 exhibits their descriptive statistics. The correlation matrix and the VIF test shows

multicollinearity between the three variables from the World Bank (corruption, rule of law, and

government efficiency), which we used separated in each model. There is also multi-collinearity

between the normal VAT rate and the implicit rate (as expected). The Breusch–Pagan test for

heteroskedasticity rejects the null hypothesis. The Jarque-Bera test on variables’ normality is

statistically significant, and thus we can safely consider that the data have a normal distribution. The

Ramsey test did not show any omitted variable. There is some evidence of dependent variable

normality of data in Figures 1 and 2. Data for each country in the sample is presented in Table 2.

Variable Obs Mean Std. Dev. Min Max

Dependent variables

Log VATrev 365 2.20 1.70 -1.88 5.25

VATrevGDP 365 7.48 1.17 4.14 10.9

Explanatory variables

VAT variables

VAT rate 365 19.66 2.96 8 25

Minrate 365 5.78 3.24 0 17

Implicitrate 365 21.2 4.34 11.1 34.2

Economic variables

ImportsGDP 365 54.2 27.2 21.1 158.6

ServicesGDP 365 50.1 25.9 0.19 10.5.7

Deficit 365 3.09 3.53 -6.83 15.4

Tax administration efficiency

Ceffic 365 50.3 9.36 30.8 86.7

nyearsVAT 365 22.7 11.8 1 45

GovefficQ 365 82.9 13.5 28.3 100

Institutional and legal variables

LowCorruptionQ 365 80.1 15.4 30.2 100

RuleofLawQ 365 82.1 14.7 37.3 100

Control variables

Euro 365 0.50 0.5 0 1

LogGDPcapita 365 3.39 1.39 0.50 7.94

Source: The Author

Table 1 – Descriptive statistics

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

87

Mean Sd Min Max Median Mean Sd Min Max Median

Belgium 20.9 3.37 15.4 25.98 20.74 6.98 0.13 6.74 7.18 7

Bulgaria 2.24 1.03 0.96 3.86 2.19 9.12 1.12 7.31 10.9 8.87

Czech Republic 6.91 2.72 3.36 10.94 6.82 6.49 0.41 5.87 7.04 6.36

Denmark 20.06 3.20 15.18 23.87 20.06 9.9 0.26 9.57 10.39 9.82

Germany 152.75 21.09 128.37 191.19 139.91 6.77 0.41 6.26 7.48 6.73

Estonia 0.91 0.38 0.41 1.42 0.86 8.39 0.44 7.68 9.07 8.41

Ireland 10.13 2.68 5.59 14.4 10.08 7.05 0.48 6.15 7.77 7.08

Greece 15.8 0.96 14.91 17.02 15.67 7.15 0.36 6.45 7.44 7.25

Spain 49.14 10.70 30.86 64.35 49.37 5.81 0.62 4.14 6.53 5.97

France 121.89 13.81 101.21 140.84 123.42 7.27 0.24 6.91 7.75 7.25

Italy 84.4 10.33 66.16 98.6 83.42 6.08 0.21 5.69 6.47 6.1

Cyprus 1.1 0.50 0.39 1.82 1.15 7.83 2.07 4.48 10.59 8.4

Latvia 0.98 0.41 0.48 1.73 0.9 7.19 0.71 5.99 8.59 7.04

Lithuania 1.9 0.55 1.11 2.59 1.96 7.46 0.60 6.44 8.11 7.57

Luxembourg 1.78 0.56 0.96 2.63 1.76 5.94 0.37 5.37 6.71 5.8

Hungary 6.45 1.81 3.3 8.44 7.05 8.25 0.43 7.6 8.86 8.18

Malta 0.35 0.11 0.15 0.53 0.37 6.81 1.16 4.35 8.05 7.34

Netherlands 35.97 6.16 24.31 43.22 36.38 7.15 0.21 6.76 7.5 7.22

Austria 19.36 2.49 15.58 23.33 19 7.96 0.21 7.62 8.37 7.95

Poland 19.28 6.83 10.92 29.94 16.95 7.52 0.49 6.77 8.34 7.46

Portugal 11.79 2.16 7.98 14.42 11.77 7.85 0.49 7.1 8.56 7.73

Romania 6.08 3.46 2.04 11.41 5.26 7.2 0.85 6.05 8.69 7.14

Slovenia 2.44 0.53 1.67 3.17 2.39 8.51 0.10 8.27 8.61 8.52

Slovakia 2.88 1.22 1.31 4.7 2.83 7.12 0.44 6.35 7.87 6.98

Finland 13.18 2.25 9.64 16.84 13.3 8.45 0.25 7.98 8.93 8.44

Sweden 26.81 4.87 19.86 36.41 26.21 9.02 0.35 8.6 9.67 8.9

United Kingdom 113.15 15.28 84.48 135.97 113.8 6.58 0.34 5.7 7.34 6.58

VAT Revenue Rate in Bill ion €

Country

VAT Revenues as % GDP

This table presents the descriptive statistics of the dependent and independent variables used in this study.

Source: The Author

Table 2 – Country data

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

88

Source: The Author

Figure 1 – Histogram of VAT revenue as % of GDP

Source: The Author

Figure 2 – Histogram of the variable Log of VAT RevenueVAT revenue as % of GDP

Results and discussion

For a comparative to assess and evaluate the main determinants of VAT revenues, we estimate an

OLS with fixed effects (due to the Hausmann test), using the log of the VAT revenues as a dependent

variable. Results are shown in Table 3. A robustness check was performed, adding a variable Euro

to the model and a variable log of GDP per capita. Results of this new model are shown in Table 4.

Later, we run these models with our second dependent variable (VAT revenue as a % of GDP), as a

robustness for our results. Table 5 presents the first model, and Table 6 shows the model with the

two control variables already mentioned. This subsection addresses conclusions from all models.

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

89

(1) (2) (3) (4)

VARIABLES logVATrev logVATrev logVATrev logVATrev

VAT variables

VAT rate 0.0355*** 0.0352*** 0.0351***

(0.0056) (0.0056) (0.0052)

Minrate 0.0331*** 0.0332*** 0.0252*** 0.0330***

(0.0038) (0.0038) (0.0036) (0.0039)

implicitrate 0.0250***

(0.0056)

Economic variables

Imports%GDP -0.0043*** -0.0046*** -0.0034*** -0.0043***

(0.0011) (0.0011) (0.0010) (0.0011)

Services%GDP 0.0063*** 0.0061*** 0.0052*** 0.0050***

(0.0016) (0.0016) (0.0015) (0.0016)

Deficit -0.0037* -0.0034 -0.0055*** -0.0041*

(0.0022) (0.0022) (0.0020) (0.0022)

Tax administration efficiency

Ceffic 0.0308*** 0.0313*** 0.0280*** 0.0229***

(0.0017) (0.0017) (0.0016) (0.0020)

nyearsVAT 0.0566*** 0.0565*** 0.0550*** 0.0580***

(0.0021) (0.0021) (0.0019) (0.0021)

GovefficQ 0.0042**

(0.0018)

Institutional and legal variables Low CorruptionQ 0.0051***

(0.0019)

RuleoflawQ 0.0159***

(0.0020)

Constant -2.0074*** -1.9369*** -2.6619*** -1.0048***

(0.2350) (0.2307) (0.2104) (0.1320)

Observations 365 365 365 365

R-squared 0.8855 0.8849 0.9019 0.8762

Number of Country 27 27 27 27

This table presents the results of an OLS with fixed effects (due to the Hausmann test results).

The dependent variable is the logarithm of VAT revenues in millions of Euros (for non-Eurozone

countries, values in national currencies were converted to Euros), for 1998 to 2011. Country

effects were used, but were omitted. Variables CorruptionQ, GovefficQ, RuleoflawQ and

implictrate were used separated, due to multicollinearity.

Robust standard errors in parentheses. *** stands for p<0.01, ** stands for p<0.05, and * for

p<0.1.

Source: The Author

Table 3 – Regression results with dependent variable LogVATrevenues

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

90

(1) (2) (3) (4)

VARIABLES logVATrev logVATrev logVATrev logVATrev

VAT variables VAT rate 0.0430*** 0.0426*** 0.0417***

(0.0034) (0.0035) (0.0033)

Minrate 0.0085*** 0.0086*** 0.0064** 0.0056**

(0.0025) (0.0026) (0.0025) (0.0027)

implicitrate 0.0363***

(0.0035)

Economic variables Imports%GDP -0.0039*** -0.0038*** -0.0034*** -0.0034***

(0.0007) (0.0007) (0.0006) (0.0007)

Services%GDP 0.0130*** 0.0131*** 0.0124*** 0.0127***

(0.0010) (0.0011) (0.0010) (0.0011)

Deficit -0.0035*** -0.0037*** -0.0046*** -0.0045***

(0.0013) (0.0013) (0.0013) (0.0014)

Tax Administration efficiency

Ceffic 0.0249*** 0.0246*** 0.0237*** 0.0128***

(0.0011) (0.0011) (0.0011) (0.0014)

nyearsVAT 0.0217*** 0.0231*** 0.0251*** 0.0246***

(0.0020) (0.0019) (0.0019) (0.0020)

GovefficQ -0.0004

(0.0011)

Institutional and legal variables Low CorruptionQ 0.0031**

(0.0012)

RuleoflawQ 0.0066***

(0.0014)

Control variables Euro 0.1048*** 0.1117*** 0.1080*** 0.1101***

(0.0245) (0.0247) (0.0238) (0.0259)

logGDPpercapita 0.6162*** 0.5962*** 0.5541*** 0.6091***

(0.0272) (0.0264) (0.0266) (0.0276)

Constant -2.7618*** -2.9407*** -3.3138*** -2.3694***

(0.1472) (0.1494) (0.1393) (0.1026)

Observations 365 365 365 365

R-squared 0.9574 0.9566 0.9595 0.9520

Number of Country 27 27 27 27

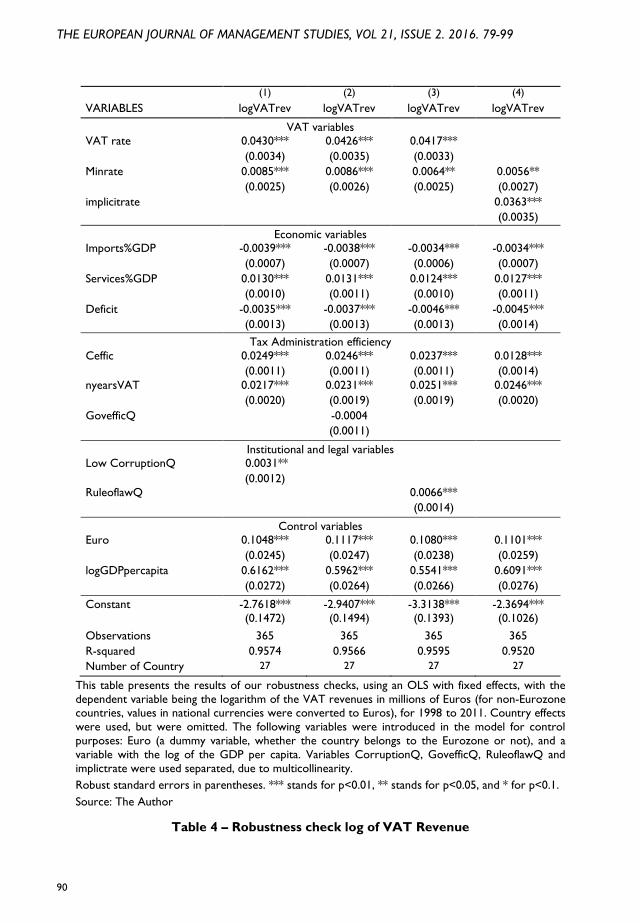

This table presents the results of our robustness checks, using an OLS with fixed effects, with the

dependent variable being the logarithm of the VAT revenues in millions of Euros (for non-Eurozone countries, values in national currencies were converted to Euros), for 1998 to 2011. Country effects

were used, but were omitted. The following variables were introduced in the model for control

purposes: Euro (a dummy variable, whether the country belongs to the Eurozone or not), and a

variable with the log of the GDP per capita. Variables CorruptionQ, GovefficQ, RuleoflawQ and

implictrate were used separated, due to multicollinearity.

Robust standard errors in parentheses. *** stands for p<0.01, ** stands for p<0.05, and * for p<0.1.

Source: The Author

Table 4 – Robustness check log of VAT Revenue

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

91

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

92

(1) (2) (3) (4)

VARIABLES VATrevGDP VATrevGDP VATrevGDP VATrevGDP

VAT variables

VAT rate 0.3513*** 0.3490*** 0.3495***

(0.0143) (0.0143) (0.0143)

Minrate -0.0075 -0.0083 -0.0088 -0.0270*

(0.0106) (0.0106) (0.0108) (0.0141)

implicitrate 0.2629***

(0.0184)

Economic variables

Imports%GDP -0.0156*** -0.0157*** -0.0152*** -0.0136***

(0.0027) (0.0028) (0.0028) (0.0037)

Services%GDP 0.0006 0.0013 0.0005 -0.0033

(0.0043) (0.0043) (0.0044) (0.0057)

Deficit -0.0098* -0.0104* -0.0109* -0.0175**

(0.0055) (0.0055) (0.0056) (0.0073)

VAT Administration efficiency Ceffic 0.1278*** 0.1271*** 0.1265*** 0.0378***

(0.0045) (0.0045) (0.0046) (0.0071)

nyearsVAT 0.0271*** 0.0334*** 0.0327*** 0.0480***

(0.0082) (0.0080) (0.0080) (0.0102)

GovefficQ 0.0052

(0.0047)

Institutional and legal variables

Low CorruptionQ 0.0087*

(0.0052)

RuleoflawQ 0.0044

(0.0058)

Control variables

Euro 0.2761*** 0.2834*** 0.2914*** 0.2865**

(0.1022) (0.1023) (0.1021) (0.1344)

logGDPpercapita -0.0614 -0.1388 -0.1477 -0.0445

(0.1133) (0.1092) (0.1140) (0.1433)

Constant -4.8251*** -5.7820*** -5.6284*** 0.0055

(0.6139) (0.6186) (0.5973) (0.5333)

Observations 365 365 365 365

R-squared 0.8208 0.8200 0.8196 0.6863

Number of Country 27 27 27 27

This table presents the results of ours robustness checks, using an OLS with fixed effects with the dependent variable being the logarithm of VAT revenues in millions of Euros (for non-Eurozone

countries, other values were converted to Euros), for 1998 to 2011. The following variables were

introduced for control purposes: Euro (a dummy, whether the country belongs to the Eurozone or

not), and the log of the GDP per capita. Variables CorruptionQ, GovefficQ, RuleoflawQ and

implictrate were used separated, due to multicollinearity.

Robust standard errors in parentheses. *** stands for p<0.01, ** stands for p<0.05, and * for p<0.1.

Source: the Author

Table 6 - Robustness check VAT Revenue as percentage of GDP

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

93

As expected, we found evidence of a positive impact in revenues from increasing the normal

statutory rate. In average, an increase in 1 p.p. in the statutory rate increased VAT revenues by 0.4

p.p. of GDP. An increase in the implicit rate represents, on average, an increase of 0.2 p.p. in

revenues as a percentage of GDP.

Up until the financial crisis of 2008, we found that normal rate had increased by an average of 0.4

p.p., from an average of 18.9% in 1998, to an average of 19.3% in 2007. After 2008, the fiscal

constraints and the need of most European countries to reduce their deficits, led most countries

to use VAT as one of their measures to increase revenues. In many cases, countries opted not only

to increase the tax base, but also to increase tax rates. After the crisis, normal rates have increased,

in average by 2.2 p.p.., from an average of 19.3% in 2007, to an average of 21.5% in 2014 (see Bozio

et al., 2015 for an overall perspective of the European responses to the crisis, and Marti et al.

(2015) for the Spanish response to the crisis, Figari et al. (2015) for the Italian case, and Keane

(2015) for Ireland, with all finding that VAT was one of the main tools for increasing revenues). For

instance, in the countries that had a bail-out, we found that, after 2008, Hungry increased the

normal rate by 7 p.p., Spain increased it by 5 p.p., Greece by 4 p.p., and Portugal and Ireland, both

increased it by 2 p.p. Therefore, we also found evidence of a positive impact of the implicit VAT rate

on revenues. What was less expected however, was the positive impact of minimum rate. This could

be explained by the significant increases in minimum rates over the last years. Minimum rates

increased, on average by 1 p.p. from 2008 to 2012 (from an average of 5.7% in 2007, to an average

of 6.7% in 2014). However, this represents an average growth of 15%, which compares with 11%

for the case of the normal rate. For all the three variables, there is some evidence that there is still

some space in Europe to increase VAT revenues by increasing tax rates.

Economic environment also has an impact on VAT revenues. We found, a negative impact on the

variable Imports. On the contrary, countries whose GDP has a higher percentage of services are

related with higher VAT revenues. This is explained by the higher added value of services when

compared with industry or agriculture. With regards to the fiscal position of each country, we

found that higher deficits have a negative impact on VAT revenues.

Tax administration efficiency is a relevant issue regarding the collection of VAT revenues. All the

three variables used are positive and statistically significant. Not only does C-efficiency, but also a

higher number of years also increases revenues. There is some evidence that more experience in

the administration of this tax (which is measured here by the number of years since VAT was

introduced) increases the potential for higher revenues. It appears that tax administrations are

subject to a learning curve in becoming more efficient. Furthermore, a more efficient government

impacts positively on tax revenues.

A better legal and institutional environment is also related with a higher capacity for a country to

collect VAT revenues. Lowering corruption and a higher value in the variable rule of law tends to

increase revenues. In the case of rule of law, this could be attributed to the fact that conflicts

between the tax administration and taxpayers can be resolved in court if the legal system is fast,

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

94

reliable, and fair. A strong rule of law appears to have the effect of making taxpayers more compliant,

thus increasing tax revenues.

Finally, our control variables do not change the results from our previous models. Additionally, we

can see that belonging to the Eurozone tends to increase VAT revenues. This could be explained

by the tighter fiscal rules present in the Eurozone, which make countries more willing to increase

revenues. A higher GDP per capita (measured by the log function) also increases VAT revenues.

Table 7 summarises the signals for each variable.

Independent

variable

Dependent variable:

VAT revenues

Dependent Variable:

VAT revenues as % GDP

VAT rate Positive Positive

Minimum rate Positive n.s.

Implicit rate Positive Positive

Imports Negative Negative

Services Positive Positive

Deficit Negative Negative

C-Efficiency Positive Positive

Nº years Positive Positive

Gov. efficiency Positive Positive

Low Corruption Positive Positive

Rule of Law Positive Positive

Euro Positive Positive

GDP per capita Positive n.s.

This table summarizes the results of this paper. n.s. stands for ‘not significant’.

Source: the Author

Table 7 – Variables results

Conclusions

In this paper we assess the critical determinants of VAT revenues in the European Union. By means

of a panel data of the 27 EU countries, from 1998 to 2011, we test VAT revenues in millions of

Euros, and VAT revenues as a percentage of GDP. We divided our explanatory variables into

groups for different categories: 1) VAT rates, using normal rate, minimum rate, and implicit rate;

2) economic variables, using imports as a percentage of GDP, share of services in GDP, and fiscal

deficit as a percentage of GDP; 3) Tax administration efficiency, using the C-efficiency ratio, number

of years since VAT was introduced, and the government efficiency ratio, and; 4) the legal and

institutional environment, using level of corruption, and the rule of law. Two control variables were

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

95

used to test the robustness of our results, namely: whether the country belongs to the Eurozone,

and the log of the GDP per capita.

Results bring to light important issues regarding collecting VAT revenues in the EU, namely that

tax rates are very relevant, as they increase significantly revenues, even the minimum tax rate.

Governments have used VAT as a main source of increasing revenues, particularly over the last

years, due to fiscal consolidation. Another important issue regards tax administration, where

greater efficiency is a critical determinant for increasing revenues. There is also evidence that tax

administrations with more years of using VAT tend to have higher revenues. This could represent

a learning process for the public sector in dealing with this tax. Finally, a lower level of corruption,

higher compliance, and a better legal and judicial system tend to impact positively on VAT revenues.

As VAT is increasingly being used by governments in Europe to increase revenues, concern about

the efficiency of collecting these revenues has grown. This paper address a very relevant topic -

what determines the collection of VAT revenues? However, the literature is still scarce on this

aspect, mainly focusing on developing countries, and not Europe. Nonetheless, VAT has been a key

public policy for all of Europe. This paper should be useful for both academics and practitioners

alike, and it should help increase our understanding of VAT revenues and their determinants.

However, further research is still required before concrete conclusions can be reached. Additional

research on VAT revenues is still needed, using comprehensive data, especially concerning the

possible relationship between economic shocks and political cycles, along with tax administration

efficiency and the legal and institutional environment. Thus, it is clear that research on VAT

revenues is still at an early stage.

References

Addison, T., & Levin, J. (2011). The determinants of tax revenue in sub-Saharan Africa. Journal of

International Development.

Afonso, A. (2010). Expansionary fiscal consolidations in Europe: new evidence. Applied Economics

Letters, 17(2), 105-109.

Agha, A. & Haughton, J. (1996). Designing VAT Systems: Some Efficiency Considerations. The

Review of Economics and Statistics 78 (2), 303-308.

Aizenman, J., & Jinjarak, Y. (2008). The Collection Efficiency of the Value Added Tax: Theory and

International Evidence. Journal of International Trade and Economics, 391-410.

Allingham, M. & A. Sandmo, (1972), “Income Tax Evasion: A Theoretical Analysis”, Journal of Public

Economics, Vol. 1, pp. 323-38.

Alm, J. & El-Ganainy, A. (2013). Value-Added Taxation and Consumption. International Tax and

Public Finance 20 (1), 105-128.

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

96

Bikas, E. & Rashkauskas, J. (2011). Value Added Tax Dimension: The Case of Lithuania. Ekonomika

90 (1), 22-38.

Bird, R., & Gendron, P. (2007). The VAT in Developing and Transitional Countries. Cambridge

University Press.

Bird, R., Martinez-Vazquez, J., & Torgler, B. (2008). Tax effort in developing countries and high

income countries: The impact of corruption, voice and accountability. Economic Analysis and

Policy, 38(1), 55-71.

Boeters, S., Böhringer, C., Büttner, T., & Kraus, M. (2010). Economic effects of VAT reforms in

Germany. Applied Economics, 42(17), 2165-2182.

Bogetic, Z., & Hassan, F. (1993). Determinants of Value-Added Tax Revenues. World Bank Policy

Research Working Paper, (1203).

Bozio, A., Emmerson, C., Peichl, A., & Tetlow, G. (2015). European Public Finances and the Great

Recession: France, Germany, Ireland, Italy, Spain and the United Kingdom Compared. Fiscal Studies,

36(4), 405-430.

Braşoveanu, I., & Obreja Braşoveanu, L. (2009). „Correlation between Corruption and Tax

Revenues in EU 27”. Economic Computation and Economic Cybernetics Studies and Research,

43(4), 133-142.

Buti, M., D. Franco & H. Ongena (1998), “Fiscal Discipline and Flexibility in EMU: The

Implementation of the Stability and Growth Pact.” Oxford Economic Review 14, 3, pp 81-97

Buti, M., S. Eijffinger, & D. Franco, (2003), “Revisiting the Stability and Growth Pact: Grand Design

or Internal Adjustment?” European Economy Economics Papers, No. 180 (Brussels: European

Commission).

Buti, M., Eijffinger, S., & Franco, D. (2005). The stability Pact pains: a forward-looking assessment

of the reform debate.

Buti, M. (2007). Will the new Stability and Growth Pact succeed? An economic and political

perspective. The Stability and Growth Pact Experiences and Future Aspects, 155-181.

Čížek, P., Lei, J. & Ligthart, J. E. (2012). The Determinants of VAT Introduction: A Spatial Duration

Analysis. CentER Discussion Paper No. 2012-71.

Cnossen, S. (2015). Mobilizing VAT revenues in African countries. International Tax and Public

Finance, 22(6), 1077-1108.

Creedy, J., & Gemmell, N. (2004). The income elasticity of tax revenue: estimates for income and

consumption taxes in the United Kingdom. Fiscal Studies, 25(1), 55-77.

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

97

De La Feria, R. & Lockwood, B. (2010), Opting for Opting-In? An Evaluation of the European

Commission's Proposals for Reforming VAT on Financial Services. Fiscal Studies, 31: 171–202. doi:

10.1111/j.1475-5890.2010.00111

De Mello, L. (2008). The Brazilian “Tax War'' - The Case of Value-Added Tax Competition among

the States. Public Finance Review, 36(2), 169-193.

De Mello, L. (2009). Avoiding the Value Added Tax: Theory and Cross-Country Evidence. Public

Finance Review, 27-46.

Dharmapala, D. (2014), What Do We Know about Base Erosion and Profit Shifting? A Review of

the Empirical Literature. Fiscal Studies, 35: 421–448. doi: 10.1111/j.1475-5890.2014.12037

Dworak, M, Wirl, F., Prskawetz, A. & Feichtinger, G. (2002), "Optimal Long-Run Budgetary Policies

Subject to the Maastricht Criteria or a Stability Pact", Macroeconomic Dynamics, 6/5, 665-686

Hines J., & Desai, M. (2005). Value-Added Taxes and International Trades: The Evidence.

Unpublished Manuscript.

Ebrill, L., Keen, M., Bodin, J. & Summers, V. (2001). The Modern VAT. Washington: International

Monetary Fund.

Engel, E, Galetovic, A. & Raddatz, C. (2001). A Note on Enforcement Spending and VAT Revenues.

The Review of Economics and Statistics 83 (2), 384-387.

Eurostat (2013), “Taxation Trends 2013”.

Eurostat (2015), VAT rates across the European Union.

Figari, F., & Fiorio, C. (2015). Fiscal consolidation policies in the context of Italy's two recessions.

Fiscal Studies, 36(4), 499-526.

Gebauer, A. & Nam, C. (2007). Can Reform Models of Value Added Taxation Stop the VAT Evasion

and Revenue Shortfalls in the EU? Journal of Economic Policy Reform, 1-13.

Godin, M. & Hindriks, J. (2015). A Review of Critical Issues on Tax Design and Tax Administration

in a Global Economy and Developing Countries. Core Discussion Paper 28.

Hanlon, M., & Heitzman, S. (2010). A review of tax research. Journal of Accounting and Economics,

50(2), 127-178.

Heipertz, M., & Verdun, A. (2004). The dog that would never bite? What we can learn from the

origins of the Stability and Growth Pact. Journal of European Public Policy, 11(5), 765-780.

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

98

Hernández de Cos, P., & Moral‐Benito, E. (2013). Fiscal consolidations and economic growth. Fiscal

Studies, 34(4), 491-515.

Hybka, M. (2009). Vat Collection Efficiency in Poland before and after accession to the European

Union--A Comparative Analysis. Ekonomika/Economics, 85.

Jack, W. (1996). The efficiency of VAT implementation: A comparative study of Central and Eastern

European countries in transition. IMF working paper, WP/96/79.

Kay, J., & Davis, E. (1987). The VAT and services (No. 245). World Bank.

Keane, C. (2015). Irish public finances through the financial crisis. Fiscal Studies, 36(4), 475-497.

Keen, M. (2009). What Do (and Don't) We Know about the Value Added Tax? A Review of Richard

M. Bird and Pierre-Pascal Gendron's." The VAT in Developing and Transitional Countries". Journal

of Economic Literature, 159-170.

Keen, M., & Lockwood, B. (2006). Is the VAT a money machine? National Tax Journal, 905-928.

Keen, M., & Lockwood, B. (2010). The value added tax: Its causes and consequences. Journal of

Development Economics, 92(2), 138-151.

Keen, M., & Smith, S. (2006). VAT fraud and evasion: What do we know and what can be done?.

National Tax Journal, 861-887.

Legeida, N., & Sologoub, D. (2003). Modeling value added tax (VAT) revenues in a transition

economy: Case of Ukraine. Institute for economic research and policy consulting working paper,

(22), 1-21.

Lindholm, R. (1970). The Value Added Tax: A Short Review of the Literature. Journal of Economic

Literature, 8(4), 1178-1189.

Matthews, K. (2003). VAT Evasion and VAT Avoidance: Is there a European Laffer Curve for VAT?

International Review of Applied Economics 17 (1), 105-114.

Martí, F., & Pérez, J. J. (2015). Spanish public finances through the financial crisis. Fiscal Studies,

36(4), 527-554.

OECD. (2008). Consumption tax trends 2008: VAT/GST and excise rates, trends and

administration issues. Paris: OECD.

Pagán, J., Soydemir, G. & Tijerina-Guardado, J. (2001). The Evolution of VAT Rates and Government

Tax Revenue in Mexico. Contemporary Economic Policy 19 (4), 424-433.

THE EUROPEAN JOURNAL OF MANAGEMENT STUDIES, VOL 21, ISSUE 2. 2016. 79-99

99

Piccolino, G. (2014). A Democratic Rentier State? Taxation, Aid Dependency, and Political

Representation in Benin, available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2554285

Rodrik, D. (1998). Why do more open economies have bigger governments? Journal of Political

Economy, October.

Sergiou, L. (2012). Value added tax (VAT) carousel fraud in the European Union. The Journal of

Accounting and Management, 2(2).

Shoup, C., Gillis, M., Shoup, C. & Sicat, G. (1990). Value added taxation in developing countries.

Value added taxation in developing countries.

Slemrod, J. (1989). Optimal taxation and optimal tax systems (No. w3038). National Bureau of

Economic Research.

Slemrod, J., & Yitzhaki, S. (2002). Tax avoidance, evasion, and administration. Handbook of public

economics, 3, 1423-1470.

Sokolovska, O. & Sokolovskyi, D. (2015). VAT Efficiency in the Countries Worldwide. Research

Institute of Financial Law, State Fiscal Service of Ukraine.

Tait, M. (1988). Value added tax: International practice and problems. International Monetary Fund.

Tait, M., R. Ebel, & T. Minh Le. (2005). ‘‘Value-Added Tax, National.’’ In The Encyclopedia of

Taxation & Tax Policy. Eds. Joseph J. Cordes, Robert D. Ebel, and Jane G. Gravelle. Washington:

The Urban Institute Press.

Tanzi, V., & Zee, H. (2000). Tax policy for emerging markets: developing countries. National tax

journal, 299-322.

van Brederode, R. (2008). Third-Party Risks and Liabilities in Case of VAT Fraud in the EU. Int'l

Tax J., 34, 31.

Williams, D. (1996). Value-Added Tax. Tax Law Design and Drafting, Thuronyi,

V.(ed),(Washington: International Monetary Fund).

Zee, H. (1995). Theory of Optimal Commodity Taxation. Tax Policy Handbook. Washington, DC:

International Monetary Fund, 71-74.

Zídková, H. (2014). Determinants of VAT Gap in EU. Prague Economic Papers 2014 (4), 514-530.

![[XLS] · Web viewIncome Statement Summary Non-operating income Total Airport Revenues Operating aeronautical revenues Ground handling revenues Operating non-aeronautical revenues](https://img.pdfslide.net/doc/110x75/5acac1f37f8b9a7d548e1826/xls-viewincome-statement-summary-non-operating-income-total-airport-revenues-operating.jpg)