Embed Size (px)

Citation preview

Seminar in International Economics:

Dealing with Economic Crises

JProf. Dr. Konstantin M. Wacker

Chair of International Economics

Gutenberg School of Management and Economics

Johannes Gutenberg University Mainz

Summer term 2015

Seminar Thesis

The European financial crisis The role of capital flows and the distressed banking system

Submitted by:

Name

Student ID: 1234567

Major: Master in International Economics and Public Policy

Street

City

Email: [email protected]

Inhaltsverzeichnis I.Introduction..................................................................................................................................1

II.Literature......................................................................................................................................2

II.1Currencycrises...................................................................................................................................2II.2Suddenstopsandbalance-of-paymentcrises..........................................................................3II.3Foreignanddomesticdebtcrises................................................................................................4II.4Bankingcrises.....................................................................................................................................5

III.TheClassificationoftheEuropeanfinancialcrisis.......................................................6

III.1Currencycrisis..................................................................................................................................7III.2Balance-of-paymentscrisis...........................................................................................................8III.3Sovereigndebtcrisis.....................................................................................................................10III.4Bankingcrisis..................................................................................................................................11

IV.Theroleofprivateandofficialcapitalflows.................................................................13

IV.1Thestory(stories)behindtheprecrisisconvergenceofinterestrates......................14IV.2Targetbalances:Emergenceduringthecrisisandpolicyimplications......................15

V.Conclusion..................................................................................................................................18

List of figures Figure 1.1: Annual percentage growth rate of nominal GDP

Figure 3.1: Exchange rate of the Euro and purchasing power parity (PPP)

Figure 3.2: Current account balance (% of GDP)

Figure 3.3: Sudden stop episodes in southern euro-area countries

Figure 3.4: Ratio of gross public debt to GDP (per cent)

Figure 3.5: Bank nonperforming loans to total gross loans (%)

Figure 4.1: Current account balances in the Eurozone 2007 (% of GDP)

Figure 4.2: The evolution of 10-year government bond yield spreads (percentage points)

List of abbreviations ECB European Central Bank

EFSF European Financial Stability Facility

EFSM European Financial Stabilisation Mechanism

GDP Gross Domestic Product

IMF International Monetary Fund

NCB National Central Bank

NPL Nonperforming loans

OECD Organization of Economic Co-operation and Development

Target Trans-European Automated Real-Time Gross Settlement

Express Transfer

1

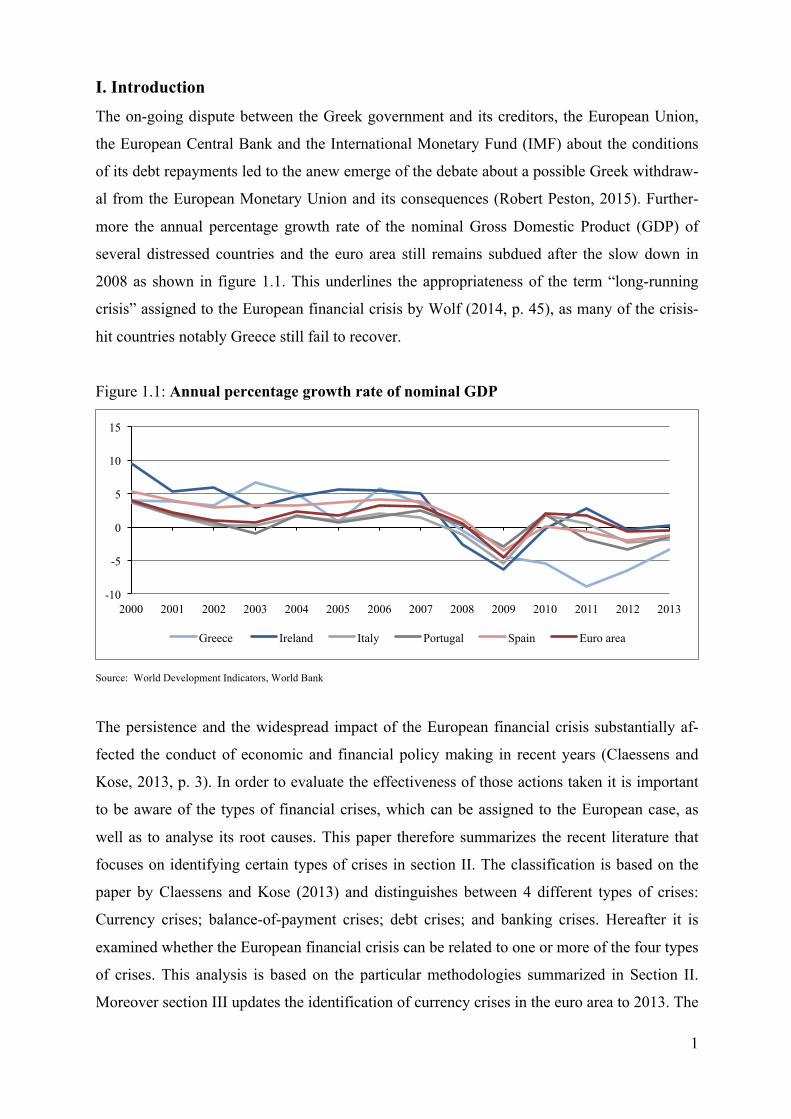

I. Introduction

The on-going dispute between the Greek government and its creditors, the European Union,

the European Central Bank and the International Monetary Fund (IMF) about the conditions

of its debt repayments led to the anew emerge of the debate about a possible Greek withdraw-

al from the European Monetary Union and its consequences (Robert Peston, 2015). Further-

more the annual percentage growth rate of the nominal Gross Domestic Product (GDP) of

several distressed countries and the euro area still remains subdued after the slow down in

2008 as shown in figure 1.1. This underlines the appropriateness of the term “long-running

crisis” assigned to the European financial crisis by Wolf (2014, p. 45), as many of the crisis-

hit countries notably Greece still fail to recover.

Figure 1.1: Annual percentage growth rate of nominal GDP

Source: World Development Indicators, World Bank

The persistence and the widespread impact of the European financial crisis substantially af-

fected the conduct of economic and financial policy making in recent years (Claessens and

Kose, 2013, p. 3). In order to evaluate the effectiveness of those actions taken it is important

to be aware of the types of financial crises, which can be assigned to the European case, as

well as to analyse its root causes. This paper therefore summarizes the recent literature that

focuses on identifying certain types of crises in section II. The classification is based on the

paper by Claessens and Kose (2013) and distinguishes between 4 different types of crises:

Currency crises; balance-of-payment crises; debt crises; and banking crises. Hereafter it is

examined whether the European financial crisis can be related to one or more of the four types

of crises. This analysis is based on the particular methodologies summarized in Section II.

Moreover section III updates the identification of currency crises in the euro area to 2013. The

-10

-5

0

5

10

15

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Greece Ireland Italy Portugal Spain Euro area

2

identification of the remaining types of crises covers time periods until 2011 and 2012, re-

spectively and provides the need for an update in further studies. The goal of this paper is to

analyse whether one or more of the aforesaid types of crises can classify the European finan-

cial crisis. Section IV examines the build up of pre-crisis current account deficits in the crisis-

hit countries of the euro area and the role of official capital flows after the outbreak of the

crisis, in particular the role of the Target system, in more detail.

While only one episode of a sovereign debt crisis can be identified in the respective period,

the European financial crisis can be characterised by several episodes of sudden stops and

banking crises. Capital exports to crisis-hit countries prior to the crisis tended to be excessive,

which caused large current account deficits in those countries and was a major factor of the

European financial crisis. The prevailing post crisis current account deficits in the crisis-hit

countries of the euro area can be attributed to official capital inflows, which counterbalanced

private capital outflows and thus mitigated the effects of the sudden stop episodes. The wid-

ening of Target balances, an example of public capital flows, reflects capital exports from the

core to the European periphery and in particular the crowding out of refinancing credits in the

former group of countries and increasing refinancing credits to the distressed banking sector

in the latter. While Target imbalances can be addressed by adopting the rules of the American

payment system, policy actions should focus on the persistent current account deficits and the

distressed banking system in the crisis-hit countries.

II. Literature

The methods used to identify and classify crises are various and often based on methodologies

derived from theories explaining these crises (Claessens and Kose, 2013, p. 22). It is im-

portant to distinguish between the identification of different types of crises. Whereas currency

crises and sudden stops can be objectively classified, the dating of debt and banking crises

involves qualitative and judgmental analyses (Claessens and Kose, 2013, p. 22). The subjec-

tive approach of the latter and variations in methodologies, notably in threshold values of cer-

tain indicators, explain the diversity of identification methods and their results (Claessens and

Kose, 2013).

II.1 Currency crises

Currency crises emerge in the event of a speculative attack on the currency. Possible out-

comes range from a devaluation, a sharp depreciation of the domestic currency, a sudden drop

in international reserves, to sharply increasing interest rates, depending on the degree of inter-

3

vention by the authorities (Claessens and Kose, 2013, p.12). Different dating approaches have

been evolved, which are based on the various outcomes of currency crises. Laeven and Va-

lencia (2013, p. 250) define a currency crisis as a nominal depreciation of the domestic cur-

rency vis-à-vis the US-Dollar of at least 30 per cent. The dataset of their study covers the pe-

riod from 1970 to 2011 and contains every country of the euro area, except Malta and Cyprus.

Furthermore, the rate of depreciation must be at least 10 percentage points higher than the rate

of depreciation of the previous year. This approach is based on Frankel and Rose’s (1996, p.

353) definition of a currency crisis. However, the latter use a threshold depreciation of 25 per

cent. The reason behind the second criterion is to avoid identifying independent currency cri-

ses every year, in countries with high inflation rates and thus high-expected rates of deprecia-

tion (Frankel and Rose, 1996, p. 353). As mentioned above monetary authorities have certain

instruments at their hands to defend the domestic currency in case of a speculative attack.

Hence, the previous approach may fail to identify a currency crisis, if an outflow of interna-

tional reserves or the adjustment in interest rates cushions exchange rate movements

(Claessens and Kose, 2013, p. 23). Glick and Hutchison (1999, p. 7) identify currency crises

on the basis of changes in an index of currency pressure, thus using the broader definition of

currency crises that includes unsuccessful attacks. The index is defined as a weighted average

of monthly per cent reserve outflows and monthly real exchange rate changes (Glick and

Hutchison, 1999, p. 7). The weights are inversely related to the variance of each component

of the index for each country, to equalize the influence of these components on the index

(Claessens and Kose, 2013, p. 23). Changes exceeding the mean by twice the country specific

standard deviation identify a currency crisis (Glick and Hutchison, 1999, p. 7). Kaminsky and

Reinhart (1999, p. 498) apply the same index. However, they use a change of three standard

deviations to catalogue a currency crisis. The differing threshold values may lead to differ-

ences in start and end dates of crises (Claessens and Kose, 2013, p. 22). Assessing these, yet

noteworthy, is beyond the scope of this paper.

II.2 Sudden stops and balance-of-payment crises

A sudden stop is characterised by a large and largely unexpected drop in international capital

inflows or a significant reversal in aggregate international capital flows to a country

(Claessens and Kose, 2013, p. 12). Disruptions in the supply of external financing affecting

the private and the public sector are classified as a sudden stop or a balance-of-payment crisis

(Merler and Pisani-Ferry, 2012, p. 8). Following the previous definition the literature focuses

on international capital flows to identify episodes of balance-of-payment crises. The method-

4

ology of Calvo, Izquierdo and Mejía (2004, p. 14) identifies a sudden stop, if at least one ob-

servation contains a year-on-year drop in capital flows that is two standard deviations below

the mean. The end of a sudden stop is determined by the first time the year-on-year change of

capital flows exceeds one standard deviation below its mean to incorporate the persistence

essential to many sudden stop episodes (Calvo, Izquierdo and Mejía, 2004, p. 14). A balance-

of-payment crises, once identified, starts when the year-on-year change in capital flows falls

one standard deviation below its mean. The latter threshold is set for symmetry reasons (Cal-

vo, Izquierdo and Mejía, 2004, p. 14). The determination of a valid proxy for international

capital flows is crucial. Since international reserves can be used to absorb disruptions in the

supply of external financing, episodes of sudden stops do not necessarily coincide with epi-

sodes of current account reversals (Edwards, 2004, p. 15). Thus, Calvo, Izquierdo and Mejía

(2004, p. 42) use the trade balance net of changes in international reserves in their empirical

study. Accordingly, their proxy incorporates private and public capital flows, mirroring the

evolution of the current account.1 However, according to Merler and Pisani-Ferry (2012, p. 3),

identifying balance-of-payment crises on the sole basis of the evolution of the current account

is a flawed approach, if the financial account includes official capital flows. Official capital

flows come along with net private capital flows, in case a stand-alone country is under an

International Monetary Fund programme or in a monetary union. Merler and Pisani-Ferry

(2012, p. 4), otherwise applying the approach of Calvo, Izquierdo and Mejía (2004), obtain

private capital inflows, by deducting official capital inflows from the current account balance.

The dataset of their study covers the period from 2002 to 2011 and contains every country of

southern Europe (Merler and Pisani-Ferry, 2012, p. 3). Sections III and IV cover the role of

official capital flows on the basis of the European financial crises more extensively.

II.3 Foreign and domestic debt crises

A foreign debt crisis occurs when a country is not able to, or purposely refuses to service its

foreign debt. The result can take the form of a sovereign and/or private debt crisis (Claessens

and Kose, 2013, p. 12). A domestic debt crisis in contrast is characterised by an explicit or

implicit default of domestic sovereign debt. The implicit default is realized either by inflating

the currency or by employing other forms of financial repression (Claessens and Kose, 2013,

p. 12). Since this paper focuses on foreign debt crises, in particular sovereign debt crises, only

the literature concerned with their identification is introduced below. External sovereign debt 1 Neglecting the primary income account and the secondary income account the evolution of the current account

is by definition equal to the evolution of the trade balance.

5

crises involve a specific year of default on payments, which facilitates the identification of

such crises (Claessens and Kose, 2013, p. 24). The start dates of defaults are obtained from

classifications of rating agencies or from international financial institutions. Laeven and Va-

lencia (2013, p. 250) rely on various databases to identify sovereign debt crises and to deter-

mine their start dates.2 Their methodology consists of an extension of the aforesaid definition

of sovereign debt crises. Besides episodes of sovereign debt default, the authors also identify

episodes of debt restructuring (Laeven and Valencia, 2013, p. 250). Das, Papaioannou and

Trebesch (2012, p. 8) point out that, while sovereign defaults and debt restructurings are

closely linked, they do not coincide, as both can occur independently. Furthermore, the empir-

ical study by Laeven and Valencia (2013, p. 250) considers defaults on private claims. Since

the authors are mainly interested in the identification of the crises themselves, rather than

their exact dating, they only provide start dates. This approach is sufficient for the purpose of

this paper, which is the classification of the European financial crisis. Therefore, the issue of

identifying the end date of sovereign debt crises summarized by Claessens and Kose (2013, p.

24) can be neglected and its description is beyond the scope of this paper. Lastly it is notewor-

thy, that other methodologies trying to identify sovereign debt crises focus on the surge in

spreads in sovereign bonds, which suggests an increasing probability of default (Claessens

and Kose, 2013, p. 24).

II.4 Banking crises

By providing maturity transformation a bank can raise social welfare, because it insures de-

positors against liquidity shocks (Diamond and Dybvig, 1983, p. 403). However, the resulting

maturity mismatch between its asset and liability side makes a bank vulnerable to coordina-

tion problems (Claessens and Kose, 2013, p. 18). Bank runs, a manifestation of such coordi-

nation problems, and failures can induce banks to suspend the convertibility of their liabilities

or cause government actions, like extending liquidity and capital assistance, and thus lead to a

banking crisis (Claessens and Kose, 2013, p. 12). Banking crises are mainly identified by us-

ing a qualitative approach, based on the combination of events. Those events can be bank

specific, like bank runs, or include government interaction, like forced closures or mergers,

government takeover or the extension of government assistance to one or more financial insti-

tutions (Claessens and Kose, 2013, p. 25). The advantage of the approach of using events to

2 The databases comprise of information from Beim and Calomiris (2001), World Bank (2002), Sturzenegger

and Zettelmeyer (2006), IMF staff reports, and reports from rating agencies (Laeven and Valencia, 2013, p.

250).

6

identify banking crises is its flexibility, which makes it possible to address the various mani-

festations of banking crises (Laeven and Valencia, 2013, p. 228). Some banking crises incur a

collapse of a significant fraction of the banking system, while in other cases bank closures can

be prevented by government intervention and regulatory forbearance, respectively (Laeven

and Valencia, 2013, p. 227). Furthermore, some banking crises can be related to a decrease in

aggregate demand shocks, while others are caused by idiosyncratic shocks (Laeven and Va-

lencia, 2013, p. 227). The methodology, developed by Laeven and Valencia (2013, p. 228),

identifies a systemic banking crisis in case significant sign of financial distress in the banking

system and significant banking policy intervention measures can be observed. The start date

of a systemic banking crisis is defined as the date, when both criteria are met.3 The first crite-

rion is indicated by significant bank runs, losses in the banking system and bank liquidations

(Laeven and Valencia, 2013, p. 228). The second criterion incorporates deposit freezes and

bank holidays, significant bank nationalizations, bank restructuring gross cost of at least 3 per

cent of GDP, extensive liquidity support, significant guarantees put in place and significant

asset purchases. If at least three of the latter criteria are met, a systemic banking crisis is iden-

tified (Laeven and Valencia, 2013, p. 229). In some cases however government interventions

are implemented on a large scale, but consist of less than three measures. In these cases

Laeven and Valencia (2013, p. 229-230) apply a new sufficient condition for a crisis episode,

which replaces the initial one: A banking crisis is classified as systemic, when either (i) non-

performing loans exceed 20 per cent or bank closures are above 20 per cent of banking system

assets or (ii) fiscal restructuring costs of the banking sector exceed five per cent of GDP. The

end date of a systemic banking crisis is defined, as the year before real credit growth and real

GDP growth are positive for two successive years (Laeven and Valencia, 2013, p. 245).

III. The Classification of the European financial crisis

This section is concerned with the analysis of the recent European financial crisis. In particu-

lar it is examined, whether the aforesaid crisis can be related to one or more of the four previ-

ously described types of crises. The analysis is mainly based on the identification methodolo-

gies applied in the study of Laeven and Valencia (2013) and Merler and Pisani-Ferry (2012),

respectively. Their methods are introduced in the previous section. While this selection suf-

fers from a lack of completeness, it contains recent data about the European financial crisis.

3 As opposed to the identification of sovereign debt crises and currency crises, which only incorporates the start

dates of the crises, as explained previously, the dating of banking crises by Laeven and Valencia (2013, p. 228)

considers the start as well as the end dates.

7

By increasing the amount of studies, further research can broaden the scope of the analysis

and thus ensure a complete assessment.

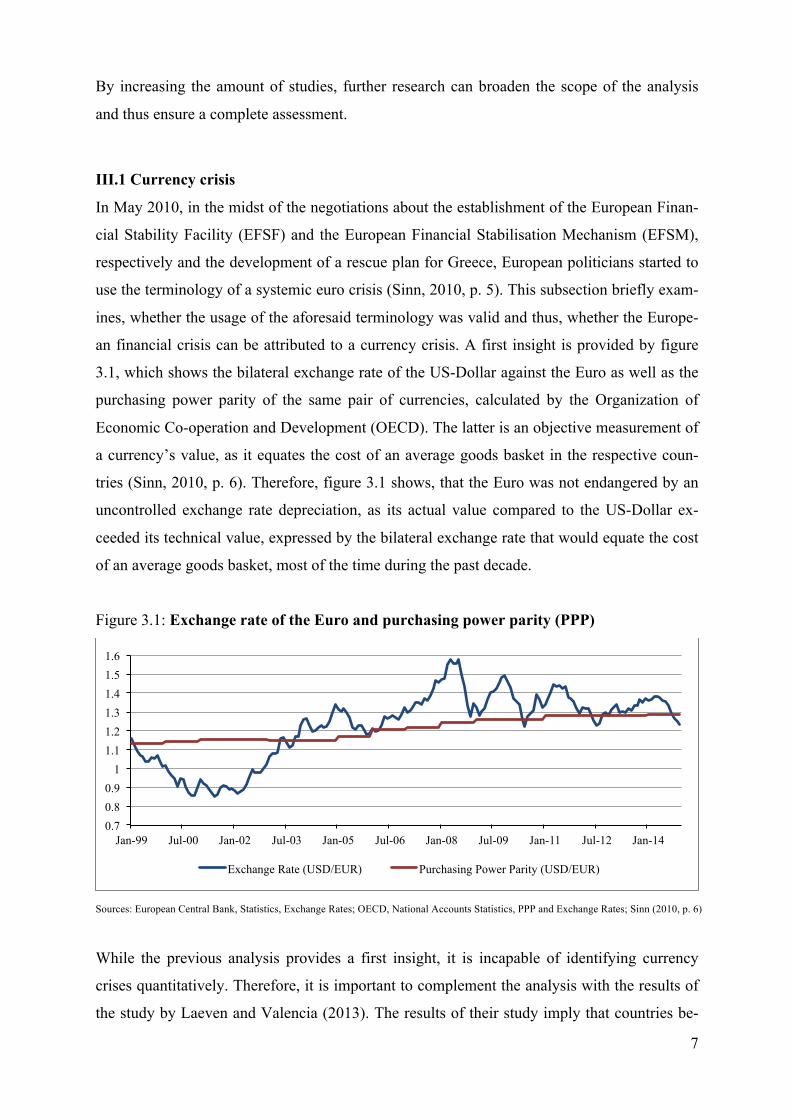

III.1 Currency crisis

In May 2010, in the midst of the negotiations about the establishment of the European Finan-

cial Stability Facility (EFSF) and the European Financial Stabilisation Mechanism (EFSM),

respectively and the development of a rescue plan for Greece, European politicians started to

use the terminology of a systemic euro crisis (Sinn, 2010, p. 5). This subsection briefly exam-

ines, whether the usage of the aforesaid terminology was valid and thus, whether the Europe-

an financial crisis can be attributed to a currency crisis. A first insight is provided by figure

3.1, which shows the bilateral exchange rate of the US-Dollar against the Euro as well as the

purchasing power parity of the same pair of currencies, calculated by the Organization of

Economic Co-operation and Development (OECD). The latter is an objective measurement of

a currency’s value, as it equates the cost of an average goods basket in the respective coun-

tries (Sinn, 2010, p. 6). Therefore, figure 3.1 shows, that the Euro was not endangered by an

uncontrolled exchange rate depreciation, as its actual value compared to the US-Dollar ex-

ceeded its technical value, expressed by the bilateral exchange rate that would equate the cost

of an average goods basket, most of the time during the past decade.

Figure 3.1: Exchange rate of the Euro and purchasing power parity (PPP)

Sources: European Central Bank, Statistics, Exchange Rates; OECD, National Accounts Statistics, PPP and Exchange Rates; Sinn (2010, p. 6)

While the previous analysis provides a first insight, it is incapable of identifying currency

crises quantitatively. Therefore, it is important to complement the analysis with the results of

the study by Laeven and Valencia (2013). The results of their study imply that countries be-

0.7 0.8 0.9

1 1.1 1.2 1.3 1.4 1.5 1.6

Jan-99 Jul-00 Jan-02 Jul-03 Jan-05 Jul-06 Jan-08 Jul-09 Jan-11 Jul-12 Jan-14

Exchange Rate (USD/EUR) Purchasing Power Parity (USD/EUR)

8

longing to the euro area and included in the sample did not experience a currency crisis, be-

tween the years 2007 and 2011 (Laeven and Valencia, 2013). This suggests, that the recent

European financial crisis cannot be classified as a currency crisis. To make the analysis more

complete, this paper updates the database of Laeven and Valencia (2013) for all relevant

countries4 until 2013, using the previously described thresholds and methodology of their

study. The calculated exchange rate depreciation of the sample countries in the years 2012

and 2013 is based on the period average of the official nominal bilateral US-dollar exchange

rate from the World Economic Indicators database of the World Bank. Thus, the data source

and concept used in this paper differs from the one used in the study by Laeven and Valencia

(2013, p. 250), as the latter authors based their analysis on the end-of-period nominal bilateral

US-dollar exchange rate from the World Economic Outlook database of the International

Monetary Fund. In spite of the different data sources and concepts used, it is noteworthy, that

the update does not reveal any currency crises in the countries of the sample in 2012 and 2013.

This confirms the previously mentioned insight that the recent European financial crisis can-

not be classified as a currency crisis.

III.2 Balance-of-payments crisis

In an early contribution on the European monetary union, Ingram (1973, p. 10) states that in

the short run financial markets can finance payment imbalances between member countries of

a monetary union. The resulting intra-community transfer among countries with adverse and

favourable clearing balances, respectively replaces interventions in the foreign exchange mar-

ket by monetary authorities (Ingram, 1973, p. 12). However, Wolf (2014, p. 59) notes that the

recent crisis revealed the importance of the balance-of-payments within the euro area. This

subsection examines the validity of both views and whether the European financial crisis can

be classified as a balance-of-payment crisis.

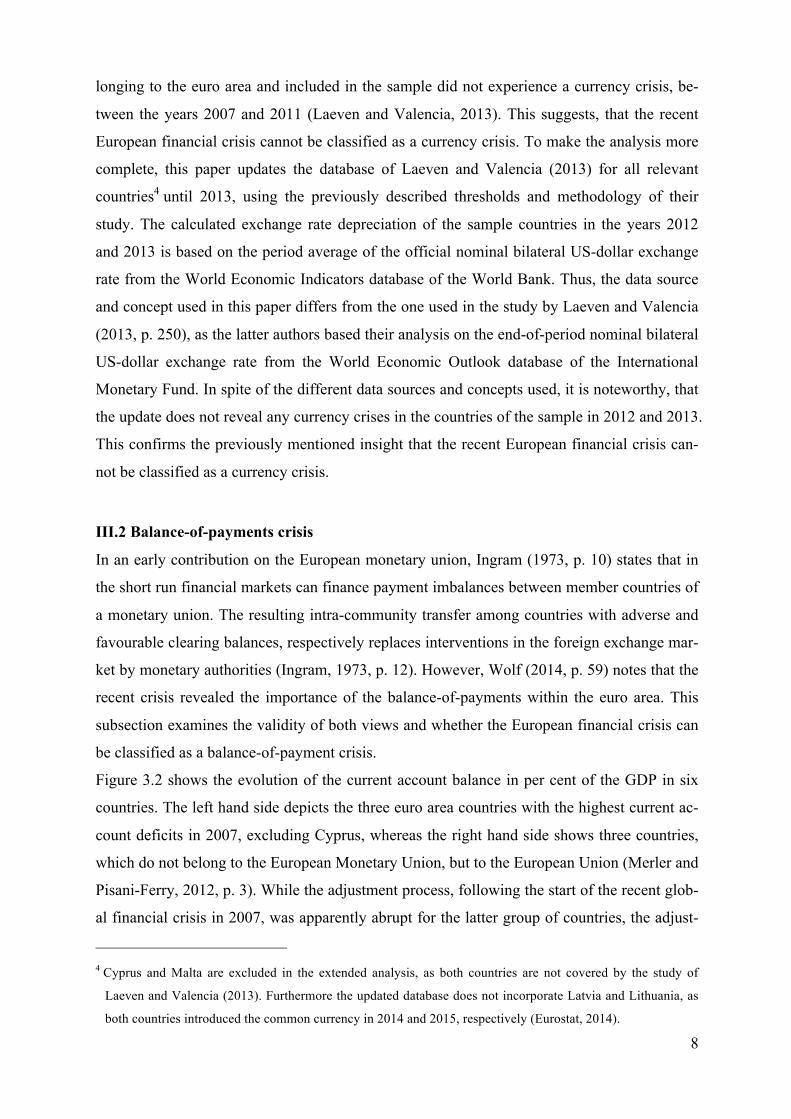

Figure 3.2 shows the evolution of the current account balance in per cent of the GDP in six

countries. The left hand side depicts the three euro area countries with the highest current ac-

count deficits in 2007, excluding Cyprus, whereas the right hand side shows three countries,

which do not belong to the European Monetary Union, but to the European Union (Merler and

Pisani-Ferry, 2012, p. 3). While the adjustment process, following the start of the recent glob-

al financial crisis in 2007, was apparently abrupt for the latter group of countries, the adjust-

4 Cyprus and Malta are excluded in the extended analysis, as both countries are not covered by the study of

Laeven and Valencia (2013). Furthermore the updated database does not incorporate Latvia and Lithuania, as

both countries introduced the common currency in 2014 and 2015, respectively (Eurostat, 2014).

9

ment process of the former group was rather smooth and slow (Merler and Pisani-Ferry, 2012,

p. 3).

Figure 3.2: Current account balance (% of GDP)

Sources: World Bank, World Development Indicators; Merler and Pisani-Ferry (2012, p. 3)

Supporting the first view, noted by Ingram (1973), the previous analysis based on figure 3.2

suggests absence of a balance-of-payment crisis in the euro area in the relevant time period,

starting in 2007. According to Merler and Pisani-Ferry (2012, p. 3) an analysis of sudden

stops on the sole basis of the evolution of the current account is however misleading. This is

due to the fact that in stand-alone countries under an IMF programme or countries belonging

to a monetary union, the financial account consists not only of private capital flows, but also

official ones (Merler and Pisani-Ferry, 2012, p. 3). In these cases the current account is not a

valid mirror of private capital flows. Official capital flows in the euro area comprise Eurosys-

tem financing through the Target system, financing through official IMF and European assis-

tance and European Central Bank purchases of sovereign bonds (Merler and Pisani-Ferry,

2012, p. 3). A private capital outflow can be outweighed by the aforesaid components of offi-

cial capital flows. By applying the previously described methodology, the study by Merler

and Pisani-Ferry (2012, p. 7) identifies nine episodes of sudden stops between 2007 and 2011

in the crisis-hit countries. By examining, whether capital outflows solely result from the dis-

posal by non-residents of their portfolios of sovereign bonds, or if private agents are also af-

fected by capital outflows, Merler and Pisani-Ferry (2012, p. 8) confirm that their identified

episodes of sudden stops were not confounded with episodes of sovereign debt crises.

Figure 3.3 shows the evolution of the sudden stops in the euro area. The emerging distress in

the interbank market and the rise in risk aversion led to a significant private capital outflow in

2008 and 2009 in Greece and Ireland. The sudden stop episode in Portugal reflects the intensi-

-30

-25

-20

-15

-10

-5

0

5

10

2007 2008 2009 2010 2011 2012 2013

Bulgaria Latvia Lithuania

-30

-25

-20

-15

-10

-5

0

5

10

2007 2008 2009 2010 2011 2012 2013

Greece Portugal Spain

10

fying of the financial crisis and completed the first period of sudden stop episodes (Merler

and Pisani-Ferry, 2012, p. 7). The second period of sudden stops, which is characterised by

significant private capital outflows in Greece and Portugal, coincides with the agreement of

the IMF/EU programmes (Merler and Pisani-Ferry, 2012, p. 7). The last period of sudden stop

episodes involved, besides Portugal, also Spain and Italy, which both got under scrutiny and

pressure of the sovereign bond market (Merler and Pisani-Ferry, 2012, p. 7).

Figure 3.3: Sudden stop episodes in southern euro-area countries

Source: Merler and Pisani-Ferry (2012, p. 7)

The result supports the view of the importance of the balance-of-payments in the euro area

and indicates that the European financial crises can be classified as a balance-of-payments

crisis. Because of the severe consequences of sudden turnarounds in private capital flows in a

monetary union, highlighted by Wolf (2014, p. 60) and the previous results, Section IV exam-

ines the build-up of current account deficits prior to the crisis in the crisis-hit countries of the

euro area and the role of official capital flows, in particular the role of the Target system after

the outbreak of the European financial crisis, in more detail.

III.3 Sovereign debt crisis

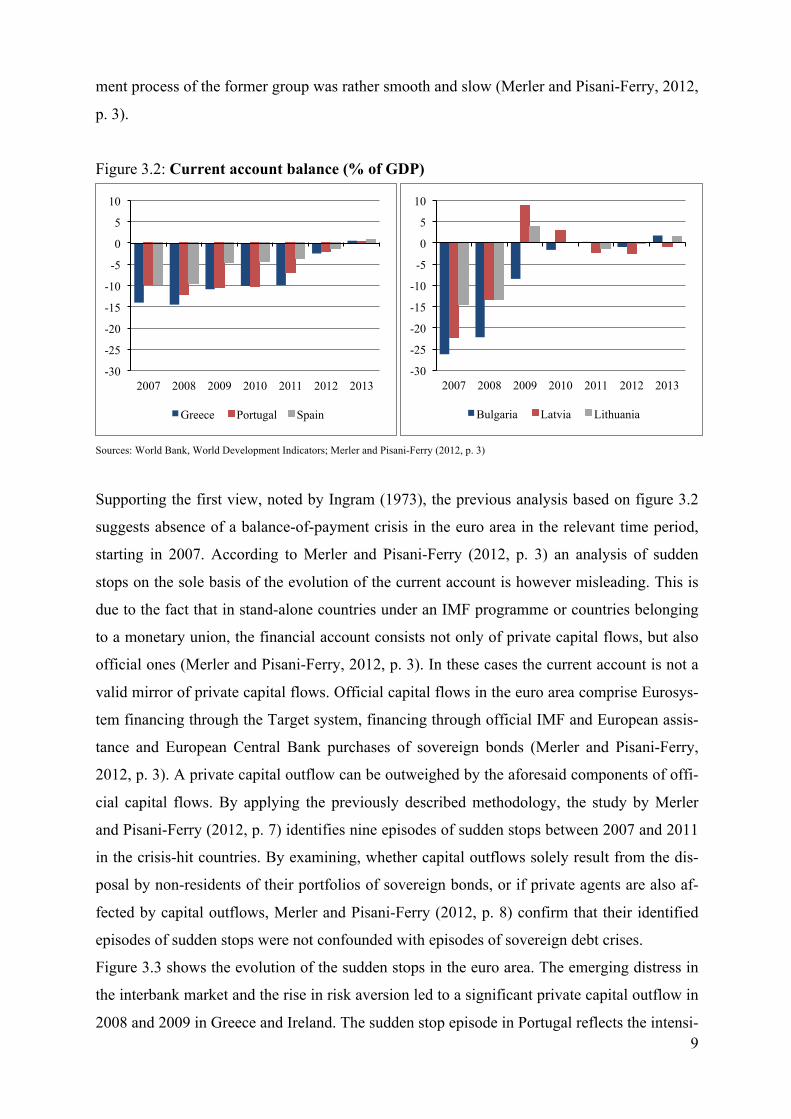

Two views prevail about the contribution of excessive government spending to the crisis. The

first view is hold by Wolfgang Schäuble (2011), the German finance minister, who stresses

that excessive state spending caused unsustainable debt levels that were a major factor of the

European financial crisis. Wolf (2014, p. 75) however notes, that crisis-hit countries had very

divergent ratios of gross public debt to GDP in the run-up to the crisis, shown by figure 3.4.

In 2007 the ratio of gross government debt to GDP exceeded the Maastricht Treaty’s thresh-

0

1

2

3

4

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11

Greece Portugal Spain Italy Ireland

11

old of 60 % in Greece, Italy and Portugal, while it was below 60 % in Cyprus, Ireland and

Spain. Hence fiscal indiscipline is unlikely to be the root cause of the recent financial crisis.

However, rising government debt in the subsequent years, as shown by the blue bars, may

indicate sovereign debt crises in crisis-hit countries (Wolf, 2014, p. 80).

Figure 3.4: Ratio of gross public debt to GDP (per cent)

Sources: IMF, World Economic Outlook Database; Wolf (2014, p. 81)

It is therefore important to complement the analysis with the results of the study by Laeven

and Valencia (2013). By applying the previously described methodology the authors identify

one case of a sovereign debt crisis in 2012. According to Laeven and Valencia (2013, p. 250),

Greece restructured its sovereign debt in the first half of 2012. Thus, the European financial

crisis can be classified as a sovereign debt crisis. It is however noteworthy the amount of sud-

den stop episodes exceeds the number of episodes of sovereign debt crises by a factor of

nine.5 Other methodologies, which identify sovereign debt crises on the basis of spreads in

sovereign bonds, may identify more cases of sovereign debt crises, as the interest rates on the

debt of some Eurozone sovereigns rose significantly in the course of the European financial

crisis, which suggests an increasing probability of default (Wolf, 2014, p. 80).

III.4 Banking crisis

Severe losses after the recent global financial crisis incurred by many European banks and the

nexus between banks and financially ailing governments of their home countries indicate dis-

5 However, the quantitative outweighing of the occurrence of sudden stops and sovereign debt crises, respective-

ly, does not give information about which type of crises had severer economic consequences.

0 20 40 60 80

100 120 140 160 180 200

Cyprus Greece Ireland Italy Portugal Spain 2007 2013

12

tress of euro-area banking systems (Wolf, 2014).6 While bank portfolios consist of a high

share of domestic government bonds, as they can be used as collateral, sovereigns often en-

gage in bank rescue policies to protect domestic banks (Wolf, 2014, p. 56). The distress in the

euro-area banking system can be attributed to the increasing number of nonperforming loans

(NPL), which consist in part of real estate loans that went sour in the course of the recent

global financial crisis (Claessens and Kose, 2013, p. 20) and the interbank market collapse

triggered by the bankruptcy of Lehman Brothers (Sinn, 2010, p. 9). Additionally, doubts

about the creditworthiness of sovereigns, which manifested in a widening of spreads in gov-

ernment bonds during the European financial crisis, also contributed to increasing funding

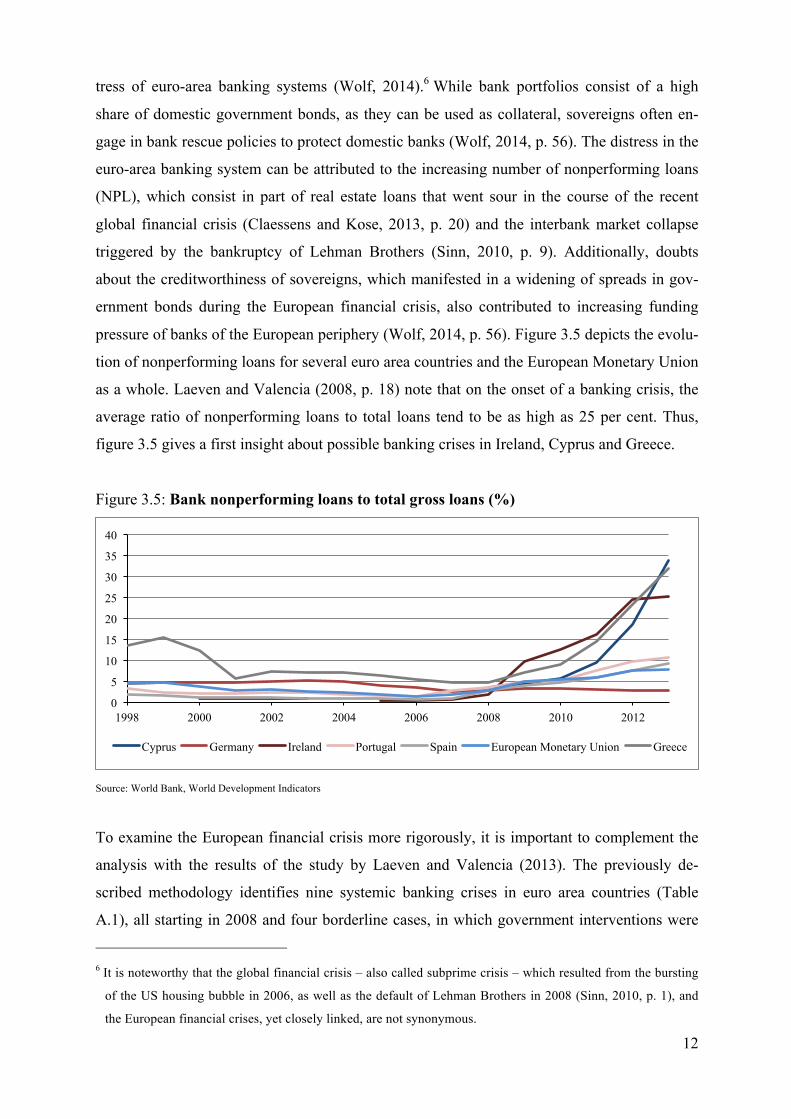

pressure of banks of the European periphery (Wolf, 2014, p. 56). Figure 3.5 depicts the evolu-

tion of nonperforming loans for several euro area countries and the European Monetary Union

as a whole. Laeven and Valencia (2008, p. 18) note that on the onset of a banking crisis, the

average ratio of nonperforming loans to total loans tend to be as high as 25 per cent. Thus,

figure 3.5 gives a first insight about possible banking crises in Ireland, Cyprus and Greece.

Figure 3.5: Bank nonperforming loans to total gross loans (%)

Source: World Bank, World Development Indicators

To examine the European financial crisis more rigorously, it is important to complement the

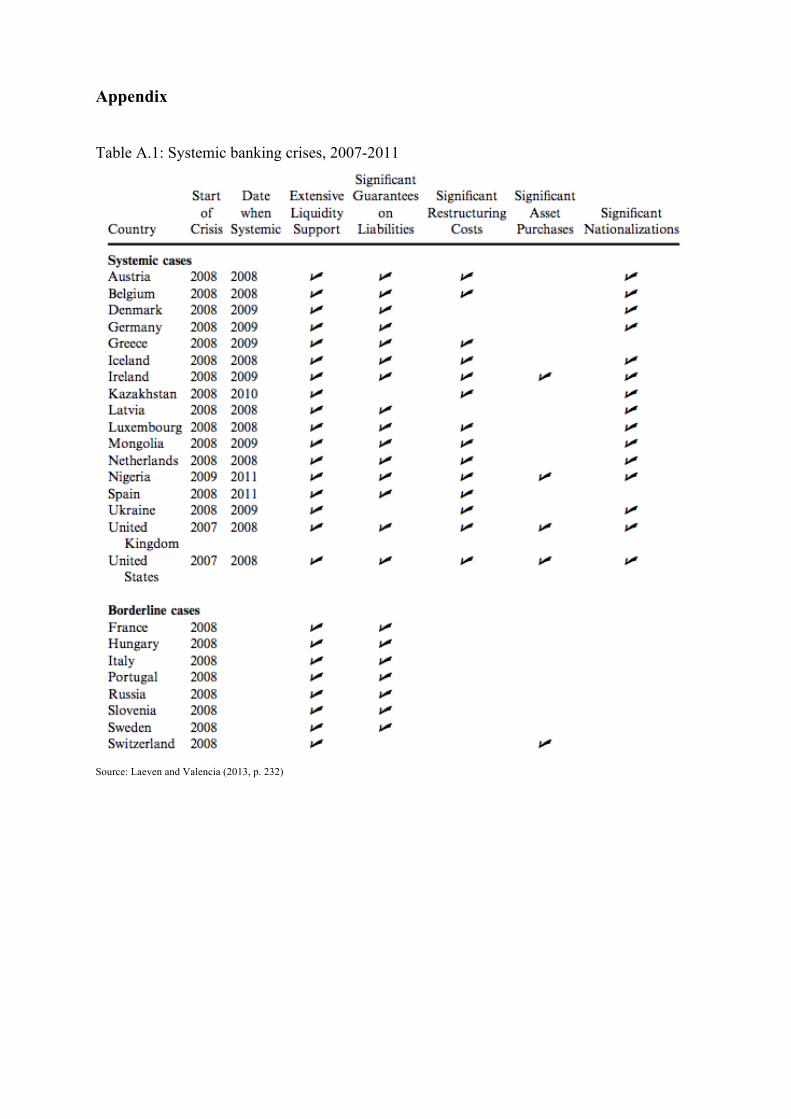

analysis with the results of the study by Laeven and Valencia (2013). The previously de-

scribed methodology identifies nine systemic banking crises in euro area countries (Table

A.1), all starting in 2008 and four borderline cases, in which government interventions were

6 It is noteworthy that the global financial crisis – also called subprime crisis – which resulted from the bursting

of the US housing bubble in 2006, as well as the default of Lehman Brothers in 2008 (Sinn, 2010, p. 1), and

the European financial crises, yet closely linked, are not synonymous.

0

5

10

15

20

25

30

35

40

1998 2000 2002 2004 2006 2008 2010 2012

Cyprus Germany Ireland Portugal Spain European Monetary Union Greece

13

implemented on a large scale, but consisted of less than three measures (Laeven and Valencia,

2013, 229). Thus the European financial crisis can be classified as a systemic banking crisis.

IV. The role of private and official capital flows

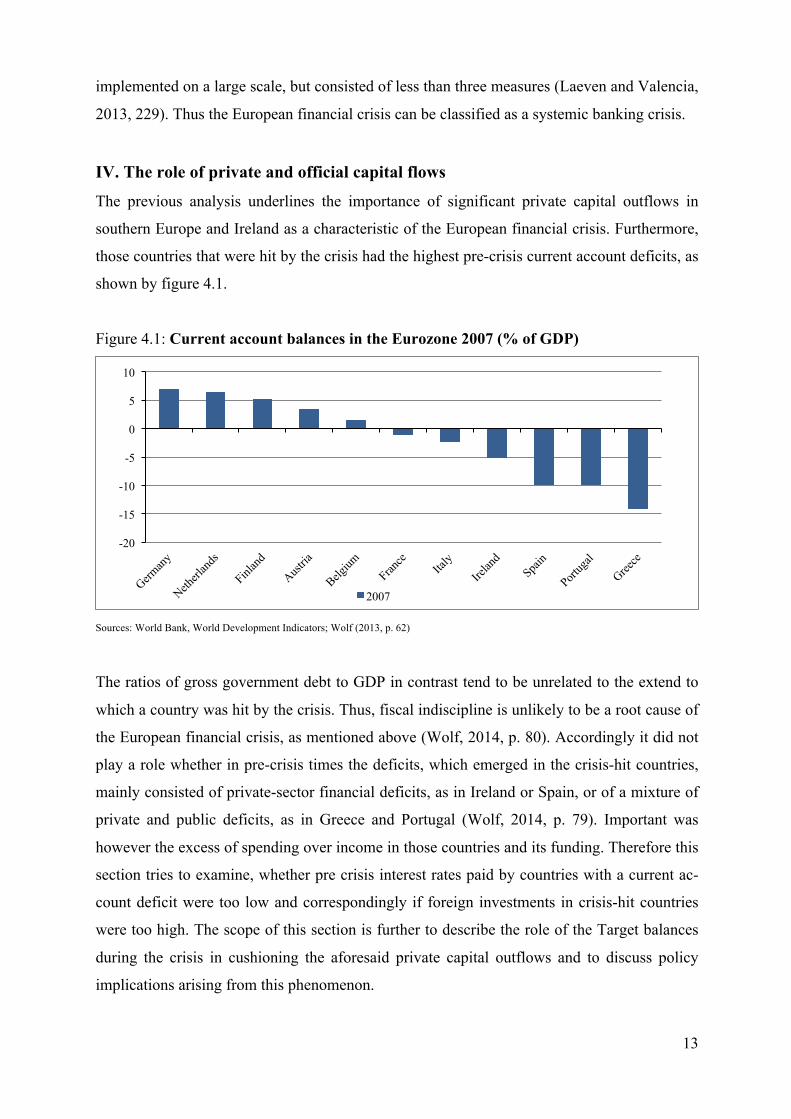

The previous analysis underlines the importance of significant private capital outflows in

southern Europe and Ireland as a characteristic of the European financial crisis. Furthermore,

those countries that were hit by the crisis had the highest pre-crisis current account deficits, as

shown by figure 4.1.

Figure 4.1: Current account balances in the Eurozone 2007 (% of GDP)

Sources: World Bank, World Development Indicators; Wolf (2013, p. 62)

The ratios of gross government debt to GDP in contrast tend to be unrelated to the extend to

which a country was hit by the crisis. Thus, fiscal indiscipline is unlikely to be a root cause of

the European financial crisis, as mentioned above (Wolf, 2014, p. 80). Accordingly it did not

play a role whether in pre-crisis times the deficits, which emerged in the crisis-hit countries,

mainly consisted of private-sector financial deficits, as in Ireland or Spain, or of a mixture of

private and public deficits, as in Greece and Portugal (Wolf, 2014, p. 79). Important was

however the excess of spending over income in those countries and its funding. Therefore this

section tries to examine, whether pre crisis interest rates paid by countries with a current ac-

count deficit were too low and correspondingly if foreign investments in crisis-hit countries

were too high. The scope of this section is further to describe the role of the Target balances

during the crisis in cushioning the aforesaid private capital outflows and to discuss policy

implications arising from this phenomenon.

-20

-15

-10

-5

0

5

10

2007

14

IV.1 The story(stories) behind the pre crisis convergence of interest rates

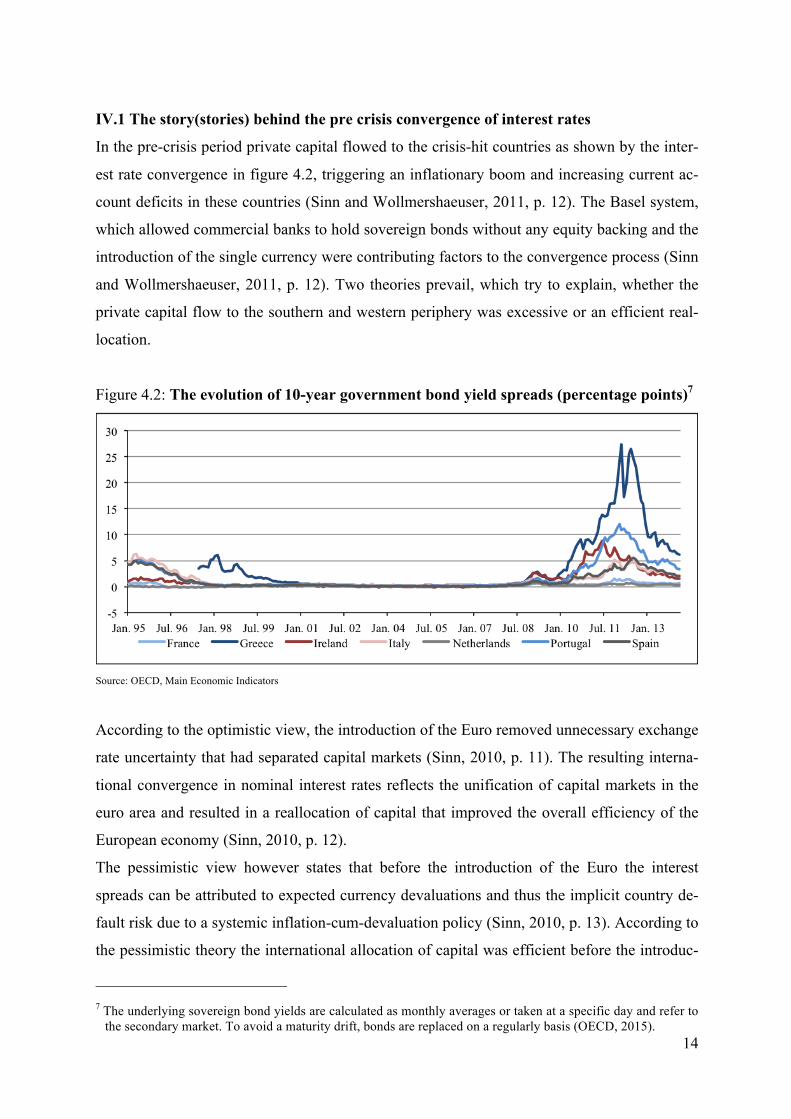

In the pre-crisis period private capital flowed to the crisis-hit countries as shown by the inter-

est rate convergence in figure 4.2, triggering an inflationary boom and increasing current ac-

count deficits in these countries (Sinn and Wollmershaeuser, 2011, p. 12). The Basel system,

which allowed commercial banks to hold sovereign bonds without any equity backing and the

introduction of the single currency were contributing factors to the convergence process (Sinn

and Wollmershaeuser, 2011, p. 12). Two theories prevail, which try to explain, whether the

private capital flow to the southern and western periphery was excessive or an efficient real-

location.

Figure 4.2: The evolution of 10-year government bond yield spreads (percentage points)7

Source: OECD, Main Economic Indicators

According to the optimistic view, the introduction of the Euro removed unnecessary exchange

rate uncertainty that had separated capital markets (Sinn, 2010, p. 11). The resulting interna-

tional convergence in nominal interest rates reflects the unification of capital markets in the

euro area and resulted in a reallocation of capital that improved the overall efficiency of the

European economy (Sinn, 2010, p. 12).

The pessimistic view however states that before the introduction of the Euro the interest

spreads can be attributed to expected currency devaluations and thus the implicit country de-

fault risk due to a systemic inflation-cum-devaluation policy (Sinn, 2010, p. 13). According to

the pessimistic theory the international allocation of capital was efficient before the introduc-

7 The underlying sovereign bond yields are calculated as monthly averages or taken at a specific day and refer to

the secondary market. To avoid a maturity drift, bonds are replaced on a regularly basis (OECD, 2015).

15

tion of the Euro (Sinn, 2010, p. 13). Since investors overlooked the explicit default risk,

which replaced the implicit one after the introduction of the single currency, the convergence

of the nominal interest rates indicates an excessive capital export from the core to the coun-

tries of the periphery (Sinn, 2010, p. 14). According to Sinn (2010, p. 14) elements of both

theories were operative in the Eurozone. While the creation of a common European capital

market and the resulting private capital export from the core to the periphery benefited the

European economy initially, private capital movements turned out to be excessive and thus

led to the crisis (Sinn, 2010, p. 14). These cross border flows financed large current account

deficits, as depicted in figure 4.1, and correspondingly large excesses of spending over in-

come in those countries (Wolf, 2014, p. 60).

IV.2 Target balances: Emergence during the crisis and policy implications

This subsection examines one reason behind the deceleration of the adjustment process of the

aforesaid large current account deficits. Target balances – the acronym Target stands for

Trans-European Automated Real-Time Gross Settlement Express Transfer – are claims and

liabilities of the national central banks (NCB) of the Eurozone vis-à-vis the European central

bank system, that arise from different types of transactions (Sinn and Wollmershaeuser, 2012,

p. 8). These transactions involve cross-border payments resulting from inter alia asset and

trade flows (Sinn and Wollmershaeuser, 2011, p. 8). Thus, the Target system is the Eurosys-

tem’s transaction settlement system through which national central banks provide payment

and settlement services for commercial banks of member countries (Merler and Pisani-Ferry,

2012, p. 4). The interest rate on Target claims and liabilities equals the main refinancing rate

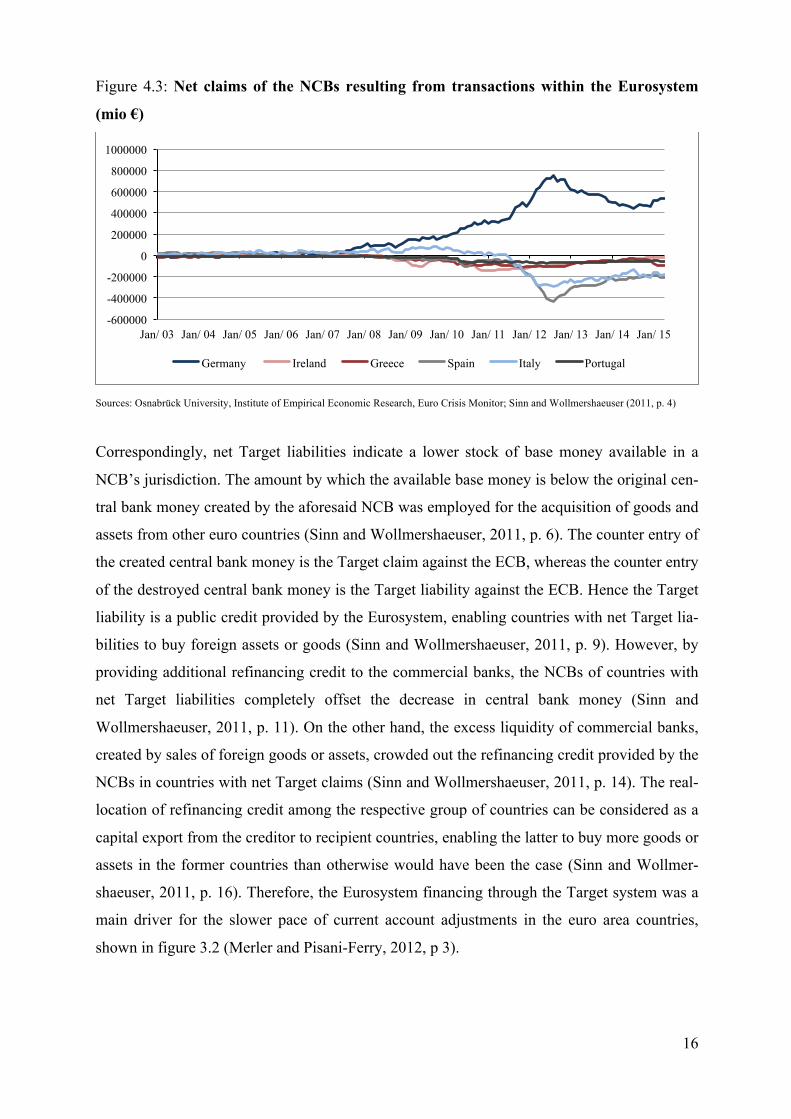

of the European Central Bank (ECB) (Sinn and Wollmershaeuser, 2011, p. 2). Figure 4.3 de-

picts the Target balances for several euro area countries. Whereas before mid-2007 imbalanc-

es were close to zero, they started to grow hereafter, as the first distress in the European inter-

bank market emerged (Sinn and Wollmershaeuser, 2011, p. 3).

In the first period, the payments between the countries netted out, as transactions resulting

from goods imports (exports) were counterbalanced by transactions resulting from the sale

(purchase) of assets (Sinn and Wollmershaeuser, 2011, p. 7). In this case, the normal case,

private capital flows financed the trade flows. In the latter period in contrast, trade and asset

flows did not counterbalance each other (Sinn and Wollmershaeuser, 2011, p. 7). In this case,

the crisis case, the stock of central bank money, flowing in via the Target accounts, accumu-

lated in the countries with net Target claims (Sinn and Wollmershaeuser, 2011, p. 7).

16

Figure 4.3: Net claims of the NCBs resulting from transactions within the Eurosystem

(mio €)

Sources: Osnabrück University, Institute of Empirical Economic Research, Euro Crisis Monitor; Sinn and Wollmershaeuser (2011, p. 4)

Correspondingly, net Target liabilities indicate a lower stock of base money available in a

NCB’s jurisdiction. The amount by which the available base money is below the original cen-

tral bank money created by the aforesaid NCB was employed for the acquisition of goods and

assets from other euro countries (Sinn and Wollmershaeuser, 2011, p. 6). The counter entry of

the created central bank money is the Target claim against the ECB, whereas the counter entry

of the destroyed central bank money is the Target liability against the ECB. Hence the Target

liability is a public credit provided by the Eurosystem, enabling countries with net Target lia-

bilities to buy foreign assets or goods (Sinn and Wollmershaeuser, 2011, p. 9). However, by

providing additional refinancing credit to the commercial banks, the NCBs of countries with

net Target liabilities completely offset the decrease in central bank money (Sinn and

Wollmershaeuser, 2011, p. 11). On the other hand, the excess liquidity of commercial banks,

created by sales of foreign goods or assets, crowded out the refinancing credit provided by the

NCBs in countries with net Target claims (Sinn and Wollmershaeuser, 2011, p. 14). The real-

location of refinancing credit among the respective group of countries can be considered as a

capital export from the creditor to recipient countries, enabling the latter to buy more goods or

assets in the former countries than otherwise would have been the case (Sinn and Wollmer-

shaeuser, 2011, p. 16). Therefore, the Eurosystem financing through the Target system was a

main driver for the slower pace of current account adjustments in the euro area countries,

shown in figure 3.2 (Merler and Pisani-Ferry, 2012, p 3).

-600000

-400000

-200000

0

200000

400000

600000

800000

1000000

Jan/ 03 Jan/ 04 Jan/ 05 Jan/ 06 Jan/ 07 Jan/ 08 Jan/ 09 Jan/ 10 Jan/ 11 Jan/ 12 Jan/ 13 Jan/ 14 Jan/ 15

Germany Ireland Greece Spain Italy Portugal

17

Equation i shows the accounting identity for countries within the euro area. It states that a

negative current account balance (CA) can be maintained, even if it exceeds the amount of

private capital inflows (PCI). This is the case, if the sum of official capital inflows, which

consists of Eurosystem financing through the Target system (T2F), financing through official

IMF and European assistance (PGM) and ECB purchases of government securities from resi-

dents (SMP), counterbalances the loss in private capital inflows (Merler and Pisani-Ferry,

2012, p 3).

(i) CA + PCI + T2F + PGM + SMP = 0

Private capital that preferred to finance domestic endeavours in countries with net Target

claims, instead of purchasing foreign assets and thus offsetting foreign trade transactions from

countries with net Target liabilities and further flight capital coming in from abroad were the

reasons for the abundance of capital supply in the former group of countries (Sinn and

Wollmershaeuser, 2011, p. 16). The reluctant private capital was however channelled abroad

by public actions in form of rescue credits incorporated by PGM (Sinn and Wollmershaeuser,

2011, p. 16). Thus, all of the previously described components of official capital flows went

contrary to market flows, i.e. private capital flows, decelerating the adjustment process of

goods-, labour-, and asset prices and correspondingly of the structural current account deficit

in the crisis-hit countries (Sinn and Wollmershaeuser, 2011, p. 17). Maintaining the unsus-

tainable vector of relative prices prevented the emergence of a new equilibrium in crisis-hit

countries, which would attract new capital coming from abroad and domestic capital to stay

(Sinn and Wollmershaeuser, 2011, p. 27). The excessive private capital export, described in

section IV.1, was just replaced by excessive public capital exports. Another problem of the

size of the post crisis Target balances emerges, if a country with net Target liabilities defaults,

causing a default of its NCB. The loss of the ECB’s claims against the country is divided

among the remaining NCBs according to their capital share, in case the Eurosystem as such

survives, while it is likely that countries with net Target claims have to write off their claims

individually, if the Eurosystem cease to exist in response to the default (Sinn and Wollmer-

shaeuser, 2011, p. 27).

According to Sinn and Wollmershaeuser (2011, p. 28) the problem of widening Target bal-

ances in the Eurozone can be solved by adopting the rules of the US Federal Reserve System,

whose Target analogue is called “Interdistrict Settlement Account”. By settling the deviation

from the average balance of the Interdistict Settlement Account of the past 12 months, in

April of each year with tangible asset, the District feds (counterparts of the euro area NCBs)

18

do not have an interest to extend central bank money, in order to satisfy their internal credit

demand (Sinn and Wollmershaeuser, 2011, p. 28). The crucial requirements for the tangible

assets are that they retain their value, even if the District Fed with net Interdistrict Settlement

Account liabilities goes bankrupt and that they earn the market rate of interest for their corre-

sponding risk category (Sinn and Wollmershaeuser, 2011, p. 28). In contrast Target liabilities

of a euro area NCB would lose their value if this particular NCB would default. However, the

implementation of the described system into the Eurosystem would need to be prolonged, as

the NCBs with net Target liabilities would have to pay large amounts of assets they do not

have to the remaining NCBs, due to the significant size of Target balances (Sinn and

Wollmershaeuser, 2011, p. 29).

V. Conclusion While the European financial crisis consists of several episodes of banking crises and sudden

stops, only one government restructured its debt, in particular Greece. The Euro was stable

throughout the past years, indicating that the European financial crisis cannot be attributed to

a currency crisis. Consequently, distress in the banking system and private capital outflows

are characteristics of the crisis. The latter were however offset by contrary official capital

flows, decelerating the adjustment process. Besides other forms of public capital inflows, Eu-

rosystem financing through the Target system helped the crisis-hit countries to maintain their

structural current account deficits. Hence, the excessive private capital export, which pre-

vailed previous to the crisis, was just replaced by excessive public capital exports. Therefore

policy actions should focus on reducing these excessive official capital exports to facilitate

the adjustment process and to continue reducing the current account deficits and maintaining

a sustainable current account balance, respectively in crisis-hit countries. Moreover, the scope

of policy intervention should focus on the distressed banking sector. Recent reforms, e.g. the

starting of the implementation of the banking union or the Macroeconomic Imbalance Proce-

dure provide a good basis. However, further effort is needed, to reduce imbalances in the Eu-

rozone and the distress in the banking system.

Bibliography Beim, David and Charles Calomiris (2001): Emerging Financial Markets. Appendix to chap-

ter 1, New York: McGraw-Hill/Irwin Publishers.

Calvo, Guillermo A., Alejandro Izquierdo and Luis-Fernando Mejía (2004): On the empirics

of sudden stops: The relevance of balance-sheet effects,” NBER Working Paper, 10520.

Claessens, Stijn and M. Ayhan Kose (2013): “Financial Crises: Explanations, Types, and Im-

plications,” IMF Working Paper, 13/28.

Das, Udaibir S., Michael G. Papaioannou and Christoph Trebesch (2012): “Sovereign Debt

Restructurings 1950-2010: Literature Survey, Data, Stylized Facts,” IMF Working Paper,

12/203.

Diamond, Douglas W. and Philip H. Dybvig (1983): “Bank Runs, Deposit Insurance, and

Liquidity,” Journal of Political Economics, Vol. 91, 401-419.

European Central Bank (2015), Statistics, June 2014.

Edwards, Sebastian (2004): “Thirty years of current account imbalances, current account re-

versals and sudden stops,” NBER Working Paper, 10276.

Eurostat (2014): “Glossary: Euro area enlargements”, http://ec.europa.eu/eurostat/statistics-

explained/index.php/Glossary:Euro_area_enlargements (checked on the 13th June 2015).

Frankel, Jeffrey A. and Andrew K. Rose (1996): “Currency crashes in emerging markets: An

empirical treatment,” Journal of International Economics, 351-366.

Glick, Reuven and Michael Hutchison (1999): “Banking and Currency Crises: How Common

are Twins,” Federal Reserve Bank of San Francisco Working Paper Series, PB99-07.

IMF (2015), World Economic Outlook Database, June 2015.

Ingram, James C. (1973): “The case for European monetary integration,” Essays in Interna-

tional Finance 98, Princeton University.

Kaminsky, Graciela L. and Carmen M. Reinhart (1999): “The Twin Crises: The Causes of

Banking and Balance-of-Payments Problems,” The American Economic Review, Vol. 89,

473-500.

Laeven, Luc and Fabián Valencia (2008): “Systemic Banking Crises: A New Database,” IMF

Working Paper, 08/224.

Laeven, Luc and Fabián Valencia (2013): “Systemic Banking Crises Database,” IMF Eco-

nomic Review, Vol. 61 No. 2, 225-270.

Merler, Silvia and Jean Pisani-Ferry (2012): “Sudden Stops in the Euro Area,” Bruegel Policy

Contribution, 2012/06.

OECD (2015), Main Economic Indicators, June 2015.

Osnabrück University Institute of Empirical Economic Research (2015), Euro Crisis Monitor,

June 2015.

Peston, Robert (2015): “Eurozone still in denial about Greece,” BBC News,

http://www.bbc.com/news/business-32989534 (checked on the 5th June 2015).

Schäuble, Wolfgang (2011): “Why austerity is only cure for Eurozone,” Financial Times,

http://www.ft.com/intl/cms/s/0/97b826e2-d7ab-11e0-a06b-

00144feabdc0.html#axzz3dDG6FECE (checked on the 16th June 2015).

Sinn, Hans-Werner (2010): “Rescuing Europe,” CESifo Forum 11 (Special Issue).

Sinn, Hans-Werner and Timo Wollmershaeuser (2011): “Target loans, current account bal-

ances and capital flows: The ECB’s rescue facility,” NBER Working Paper, 17626.

Sturzenegger, Federico and Jeromin Zettelmeyer (2006): Debt Defaults and Lessons from a

Decade of Crises. Cambridge: MIT Press.

Wolf, Martin (2014): The Shifts and the shocks: What we’ve learned – and have to learn –

from the financial crisis. New York: Penguin Press.

World Bank (2002): World Development Finance. Appendix on Commercial Debt Restructur-

ing, Washington, DC: World Bank.

World Bank (2015), World Development Indicators, June 2015.

Appendix

Table A.1: Systemic banking crises, 2007-2011

Source: Laeven and Valencia (2013, p. 232)