Embed Size (px)

Citation preview

The Mining Industry in Mexico: A Long Tradition, A Promising Future

2 The Mining Industry in Mexico: A Long Tradition, A Promising Future

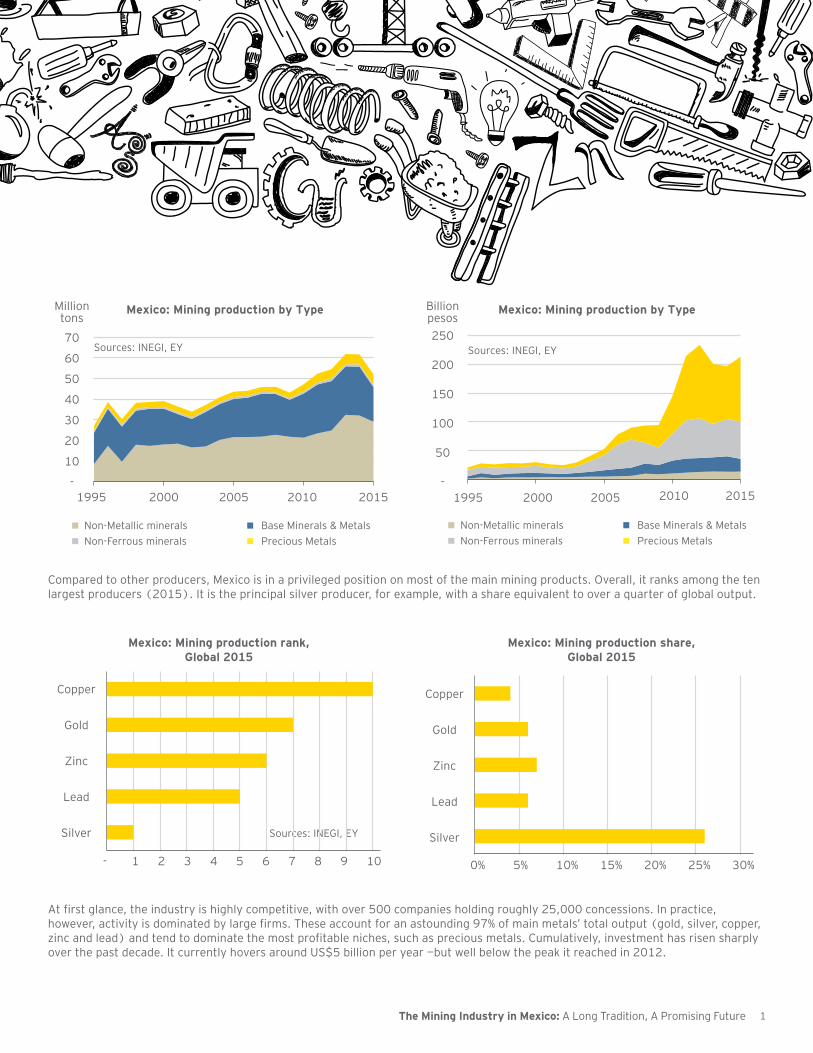

Mexico is one of the world’s largest producers of metals and minerals. Total output has risen sharply over the past two decades, reaching a peak of

over 60 million tons in 2014. The bulk of production is comprised by base metals and minerals, and non-metallic minerals. However, precious and non-ferrous metals are by far the most valuable, despite the recent volatility in international prices, representing over three-quarters of the country’s output’s value.

1The Mining Industry in Mexico: A Long Tradition, A Promising Future

Milliontons

Non-Metallic minerals Base Minerals & MetalsPrecious MetalsNon-Ferrous minerals

70

60

50

40

30

20

10

-1995 2000 2005 2010 2015

Mexico: Mining production by Type

Sources: INEGI, EY

Billion pesos

Non-Metallic minerals Base Minerals & MetalsPrecious MetalsNon-Ferrous minerals

1995 2000 2005 2010 2015

Mexico: Mining production by Type

Sources: INEGI, EY250

200

150

100

50

-

Compared to other producers, Mexico is in a privileged position on most of the main mining products. Overall, it ranks among the ten largest producers (2015). It is the principal silver producer, for example, with a share equivalent to over a quarter of global output.

At first glance, the industry is highly competitive, with over 500 companies holding roughly 25,000 concessions. In practice, however, activity is dominated by large firms. These account for an astounding 97% of main metals’ total output (gold, silver, copper, zinc and lead) and tend to dominate the most profitable niches, such as precious metals. Cumulatively, investment has risen sharply over the past decade. It currently hovers around US$5 billion per year —but well below the peak it reached in 2012.

Sources: INEGI, EY

Mexico: Mining production rank, Global 2015

Copper

Gold

Zinc

Lead

Silver

- 1 2 3 4 5 6 7 8 9 10

Mexico: Mining production share, Global 2015

Copper

Gold

Zinc

Lead

Silver

0% 5% 10% 15% 20% 25% 30%

2 The Mining Industry in Mexico: A Long Tradition, A Promising Future

1,000

27.0

26.5

26.0

25.5

25.0

Area

32

30

28

26

24

222012 2013 2014 2015

Mexico: Mining companies by size, 2014

Total

Small

Medium

LargeSources: CGM, EY

0 200 400 600

2014 2009Number Million hectare

Mexico: Mining concessions

Sources: CAMIMEX, EY

Mexico: Mining production share by company size, 2015

Medium & small

0% 20% 40% 60% 80% 100%

Large

Sources: CGM, EY

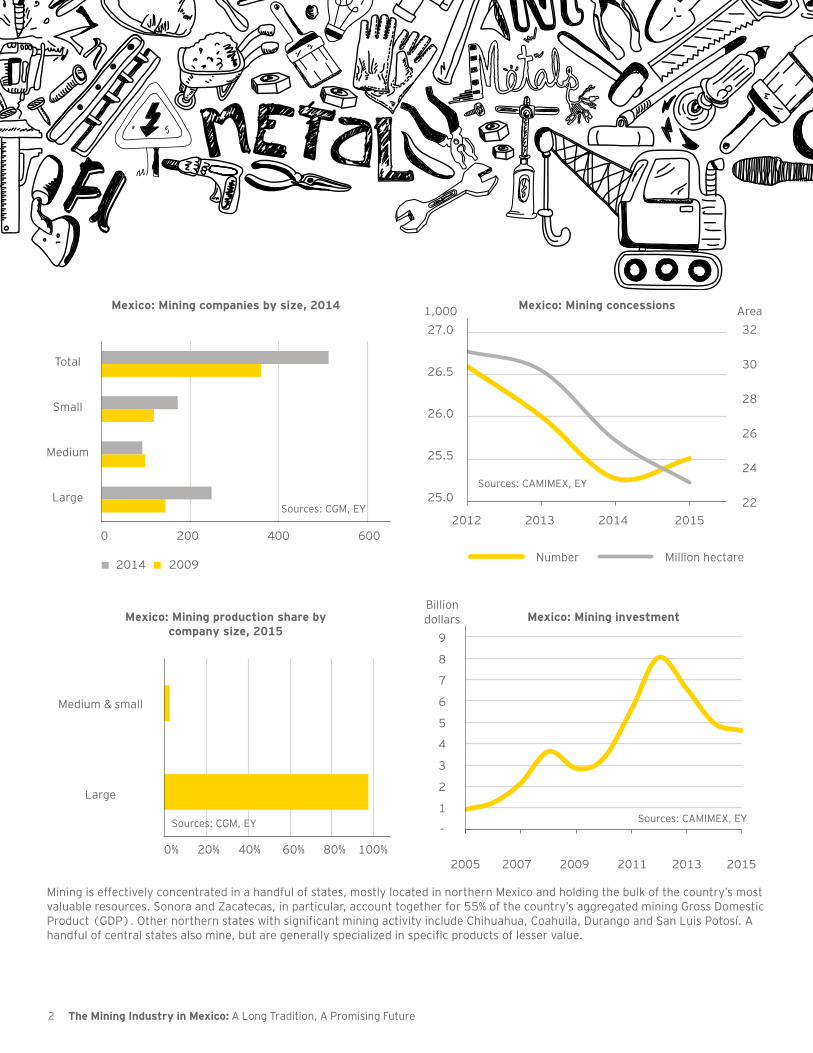

Mining is effectively concentrated in a handful of states, mostly located in northern Mexico and holding the bulk of the country’s most valuable resources. Sonora and Zacatecas, in particular, account together for 55% of the country’s aggregated mining Gross Domestic Product (GDP). Other northern states with significant mining activity include Chihuahua, Coahuila, Durango and San Luis Potosí. A handful of central states also mine, but are generally specialized in specific products of lesser value.

Sources: CAMIMEX, EY

Billion dollars

9

8

7

6

5

4

3

2

1

-

Mexico: Mining investment

2005 2007 2009 2011 2013 2015

3The Mining Industry in Mexico: A Long Tradition, A Promising Future

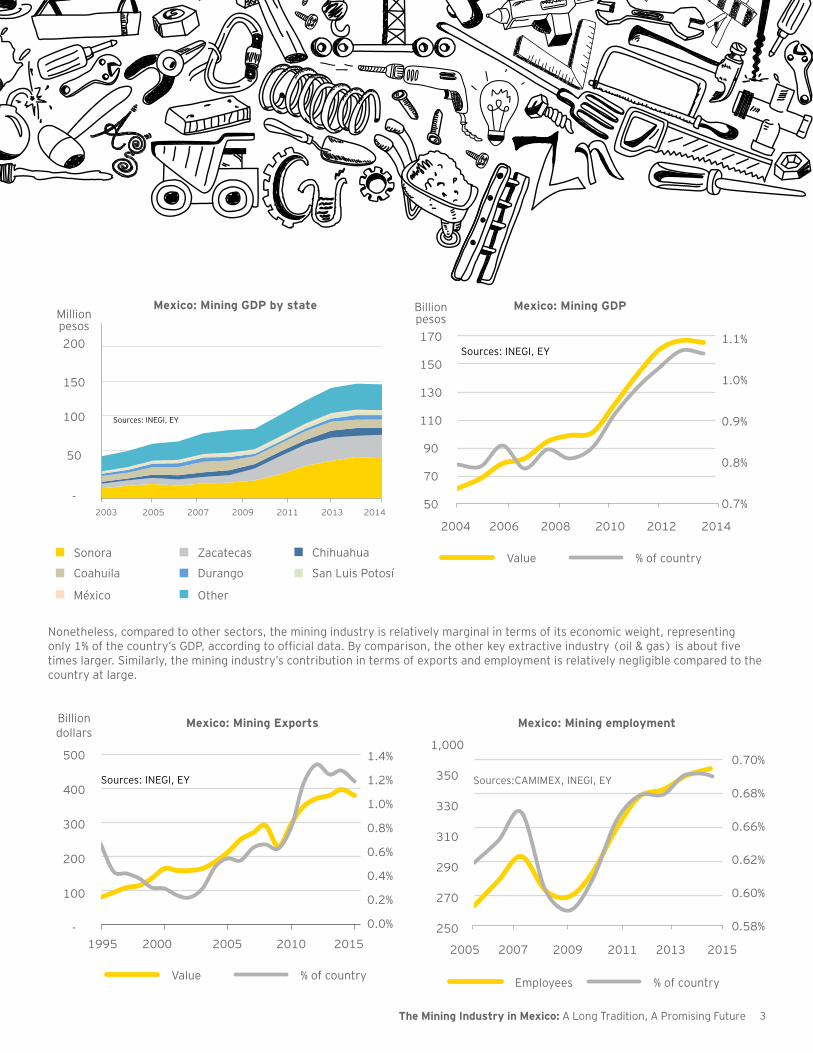

Nonetheless, compared to other sectors, the mining industry is relatively marginal in terms of its economic weight, representing only 1% of the country’s GDP, according to official data. By comparison, the other key extractive industry (oil & gas) is about five times larger. Similarly, the mining industry’s contribution in terms of exports and employment is relatively negligible compared to the country at large.

Mexico: Mining GDP by state

Millionpesos200

150

100

50

-

Sources: INEGI, EY

2003 2005 2007 2009 2011 2013 2014

San Luis Potosí

ChihuahuaZacatecas

Durango

Other

Sonora

Coahuila

México

2004 2006 2008 2010 2012 2014

Mexico: Mining GDP

Billion pesos170

150

130

110

90

70

50

Sources: INEGI, EY1.1%

1.0%

0.9%

0.8%

0.7%

Value % of country

1995 2000 2005 2010 2015

Mexico: Mining Exports

1.4%

1.2%

1.0%

0.8%

0.6%

0.4%

0.2%

0.0%

Value % of country

Sources: INEGI, EY

Billion dollars

500

400

300

200

100

-

2005 2007 2009 2011 2013 2015

Mexico: Mining employment

0.70%

0.68%

0.66%

0.62%

0.60%

0.58%

Employees % of country

1,000

350

330

310

290

270

250

Sources:CAMIMEX, INEGI, EY

4 The Mining Industry in Mexico: A Long Tradition, A Promising Future

The sector is governed by the Mining Law, first enacted in 1992 and amended several times since then. The law establishes the notions of concessions and a corresponding national registry where these are recorded. Tax matters pertain to other legislation.

Concessions can be granted either to private individuals, companies, villages and indigenous communities, or to the Mexican Geological Service. The former encompass both exploration and production for 50 years, and may be renewed. The latter only apply to exploration, last only 6 years and cannot be extended. The purpose is to identify prospective areas that may attract the interest of private investors.

The size of concessions is not specified, nor does the law distinguish between the various types of metals and minerals or between onshore and offshore locations. Concessions are granted upon demand on a first-come, first-served basis, but may be subject to bidding if deemed necessary by the authorities. All concessions are recorded in the Public Mining Registry in order to ensure transparency, together with the Mining Map. It should be noted, though, that the law does not mandate nor impede the publication of a concession’s real beneficiaries. However, as Mexico intends to join the Extraction Industries Transparency Initiative (EITI), it is anticipated that such information will be eventually required from all concession holders.

Contrary to the other extractive industry -oil & gas- mining in Mexico is not overseen by a ministry, but by the General Mining Coordination, which in turn depends on the Ministry of Economy. Despite its long history, mining has been overshadowed by oil & gas over the past century, both in terms of symbolism and economic weight. However, the government is taking steps to grant the industry more visibility within the cabinet, as well as to foster more transparency. The Mining Registry, for example, will soon become available online.

With regards to tax matters, in general terms the framework applicable to the mining industry is federal. Mining companies are indeed subject to similar taxes as other industries (e.g., income tax, VAT, import duties, etc.), in addition to a set of specific royalties or “mining fees”. The latter were established in 2014, and largely feed a Mining Fund intended to finance infrastructure in mining communities.

Legal & Tax Considerations

5The Mining Industry in Mexico: A Long Tradition, A Promising Future

The collapse of commodity prices from mid-2014 delivered a devastating blow to the mining industry, and Mexico was no exception, with production plunging by a fifth in 2015. Yet the country remains an attractive option for mining investors.

Indeed, Mexico has a number of attributes that make it stand apart when compared to other countries, in Latin America and elsewhere. As noted, the country’s resources are significant and diverse, offering opportunities for many types of companies. By the same token, Mexico has a strong mining tradition, going back centuries. As a result, qualified staff is abundant, and in most regions local inhabitants are accustomed to mining activities, which helps reduce potential conflicts (which nowadays tend to occur mostly in “new” areas with no previous exposure to mining). In practice, some of the largest companies finance social and environmental projects in the areas where they operate. These initiatives help to build trust and prevent conflicts, particularly in regions with an important presence of indigenous peoples.

Another advantage is the relative legal and tax stability. The current system of concessions, for example, is over two decades old, and has functioned well so far. On the tax side, even if royalties were hiked two years ago, most players were expecting such changes, as duties were hitherto too low compared to many other countries. The fact that Mexico is part of the North American Free Trade Agreement (NAFTA) has also helped

channel financial resources. The Toronto Stock Exchange has emerged as a key source of funds for mining projects in Mexico, given the presence of numerous Canadian mining companies, which represent about two thirds of all the foreign firms operating in the country.

As in any other country, however, there are risks. Some are intrinsic to the industry: global prices, financing, strategic focus, cost control, project execution, productivity gains, access to energy, etc. Other challenges are local: land tenure, social responsibility and security issues, to name but a few. Access to land is a particularly convoluted problem, notably in self-proclaimed indigenous communities, given the regime of communal ownership that still prevails in large portions of Mexico. Companies must generally engage in delicate negotiations when launching a project. Similarly, security can be an issue, particularly in remote areas.

Last, but not least, the Mexican tax authorities (SAT) have begun to realize that the mining industry is less marginal in economic—and tax—terms than previously thought. This does not mean that royalties will be increased once again, but merely that the SAT will excercise greater oversight beyond large companies, particularly with regards to transfer prices, in order to ensure industry participants are properly taxed. New entrants will thus require extensive fiscal advice to navigate the country’s complex rules governing the mining industry.

Business Opportunities & Risks

EY | Assurance | Tax | Transactions | Advisory About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

How EY’s Global Mining & Metals Network can help your business

With a volatile outlook for mining and metals, the global mining and metals sector is focused on margin and productivity improvements, while poised for value-based growth opportunities as they arise. The sector also faces the increased challenges of maintaining its social license to operate, balancing its talent requirements, effectively managing its capital projects and engaging with government around revenue expectations.

EY’s Global Mining & Metals Network is where people and ideas come together to help mining and metals companies meet the issues of today and anticipate those of tomorrow by developing solutions to meet these challenges. It brings together a worldwide team of professionals to help you succeed a team with deep technical experience in providing assurance, tax, transactions and advisory services to the mining and metals sector. Ultimately it enables us to help you meet your goals and compete more effectively.

Contact us:Alfredo Álvarez

Mario [email protected]

José [email protected]

José Luis [email protected]

Koen van ‘t [email protected]