Embed Size (px)

Citation preview

Document of The World Bank

FOR OFFICE USE ONLY

Report No: PAD738

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED CREDIT

IN THE AMOUNT OF SDR 3.6 MILLION (US$5.5 MILLION EQUIVALENT)

TO THE

KINGDOM OF LESOTHO

FOR THE

PUBLIC FINANCIAL MANAGEMENT REFORM SUPPORT PROJECT

January 10, 2014 Financial Management Core Operations Services Africa Region

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

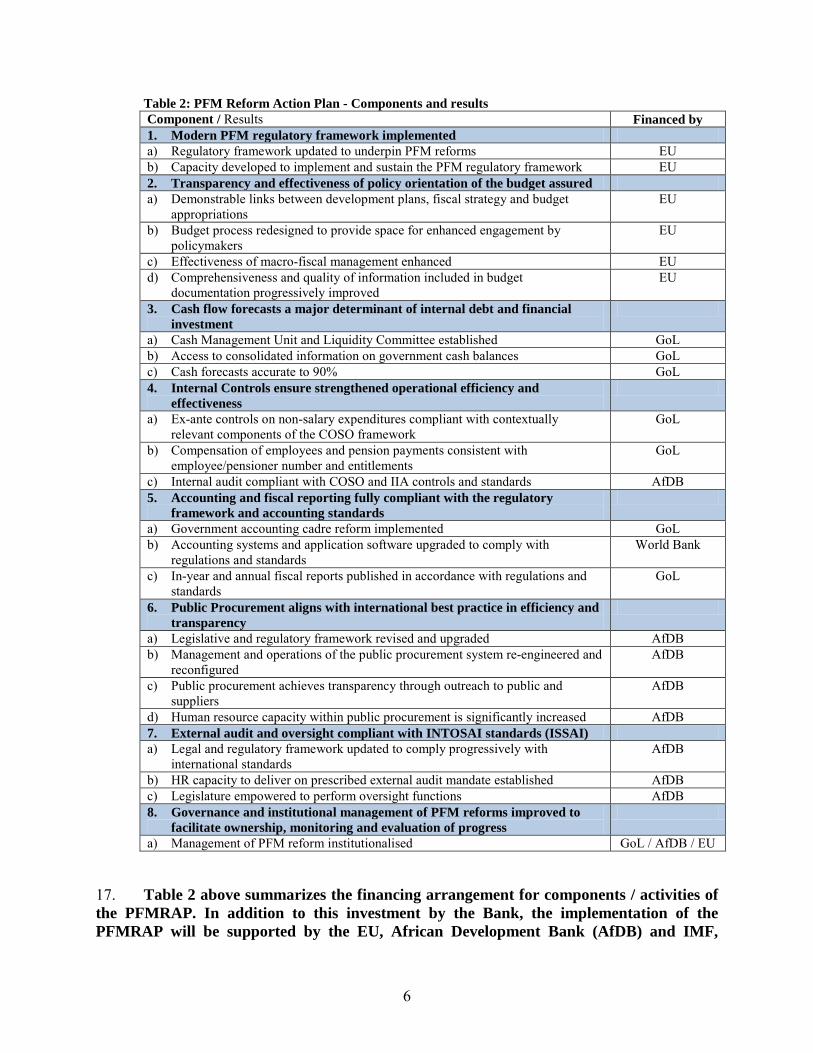

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ii

CURRENCY EQUIVALENTS

(Exchange Rate Effective 30 November, 2013)

Currency Unit = Maloti (LSL) US$1 = 10.49 US$1 = SDR 0.6545

FISCAL YEAR

April 1 – March 31

ABBREVIATIONS AND ACRONYMS AfDB African Development Bank

AIDS

ART

Acquired Immune Deficiency Syndrome

Anti-Retroviral Treatment

BLNS Botswana, Lesotho, Namibia and Swaziland

BoS Bureau of Statistics

CAS

CBEP

CBL

CIPFA

CIPS

CLs

CMA

COSO

CQS

CPAF

Country Assistance Strategy

Capacity Building in Economic Planning

Central Bank of Lesotho

Chartered Institute of Public Finance and Accountancy, UK

Chartered Institute of Purchasing and Supply, UK

Component Leaders

Common Monetary Area

Committee of Sponsoring Organizations of the Treadway Commission

Consultants Qualifications (CQS)

Common Performance Assessment Framework

DFID Department of International Development from United Kingdom

DPO Development Policy Operation

ECF

EFT

Extended Credit Facility

Electronic Funds Transfer

EU European Union

FDI Foreign Direct Investment

FIRST

GBS

Financial Sector Reform and Strengthening Initiative

General Budget Support

iii

GDP Gross Domestic Product

GNI Gross National Income

GoL Government of Lesotho

HBS

HIES

Household Budget Survey

Household Income and Expenditure Survey

HIV Human Immunodeficiency Virus

HMIS Health Management Information Systems

IBRD

ICB

International Bank for Reconstruction and Development

International Competitive Bidding

ICT Information and Communication Technologies

IDA

IDF

International Development Association

Institutional Development Fund of the World Bank

IFMIS Integrated Financial Management Information System

IMF

IPF

IRSC

LCAS

International Monetary Fund

Investment Project Finance

PFM Integrated Reform Steering Committee

Lesotho Centre for Accounting Studies

LDHS Labour and Demographic Health Survey

LNDC Lesotho National Development Corporation

LRA

MDAs

Lesotho Revenue Authority

Ministries, Departments and Agencies

MDGs Millennium Development Goals

M&E Monitoring and Evaluation

MDP Ministry of Development Planning

MoF Ministry of Finance

MoH Ministry of Health

MoSD Ministry of Social Development

MTEF

NCB

Medium-Term Expenditure Framework

National Competitive Bidding

NSDP National Strategic Development Plan

PAF Performance Assessment Framework

PEFA Public Expenditure and Financial Accountability

PPAD Procurement Policy and Advice Division

PFMRAP Public Finance Management Reform Action Plan

iv

PFM Public Finance Management

PRS

PRSP

PSIRP

QBS

QCBS

RTC

Poverty Reduction Strategy

Poverty Reduction Strategy Paper

Public Service Improvement and Reform Program

Quality-based Selection

Quality and Cost-Based Selection

Reform Technical Committee

SACU Southern African Customs Union

SADC Southern African Development Community

SME

SOE

SSS

TA

UPS

WAN

Small and Medium Size Enterprises

Statement of Expenditure

Single Source Selection

Technical Assistance

Uninterrupted power supply

Wide-Area Network

Regional Vice President: Makhtar Diop Country Director: Asad Alam

Sector Director: Edward Olowo-Okere Sector Manager: Patricia Mc Kenzie

Task Team Leader: Gert van der Linde

v

KINGDOM OF LESOTHO

PUBLIC FINANCIAL MANAGEMENT REFORM SUPPORT PROJECT (P143197)

TABLE OF CONTENTS

I. STRATEGIC CONTEXT .................................................................................................1

A: Country Context ............................................................................................................. 1

B: Sectoral and Institutional Context .................................................................................. 3

C: Higher Level Objectives to which the Project Contributes ............................................ 7

II. PROJECT DEVELOPMENT OBJECTIVE ..................................................................8

A: Project Development Objective ..................................................................................... 8

B: Project Beneficiaries ...................................................................................................... 8

C: PDO Level Results Indicators ........................................................................................ 9

III. PROJECT DESCRIPTION ..............................................................................................9

A: Project Components ....................................................................................................... 9

B: Project Financing ......................................................................................................... 15

C: Lessons Learned and Reflected in the Project Design ................................................. 16

IV. IMPLEMENTATION .....................................................................................................17

A: Institutional and Implementation Arrangements ......................................................... 17

B: Results Monitoring and Evaluation .............................................................................. 18

C: Sustainability ................................................................................................................ 18

V. KEY RISKS AND MITIGATION MEASURES ..........................................................19

A: Risk Ratings Summary Table ...................................................................................... 19

B: Overall Risk Rating Explanation ................................................................................. 19

C: Key Mitigation Measures ............................................................................................. 20

VI. APPRAISAL SUMMARY ..............................................................................................20

A: Economic and Financial Analysis ................................................................................ 20

B: Technical ...................................................................................................................... 21

C: Financial Management ................................................................................................. 22

vi

D: Procurement ................................................................................................................. 23

Annex 1: Results Framework and Monitoring .........................................................................24

Annex 2: Detailed Project Description .......................................................................................28

Annex 3: Implementation Arrangements ..................................................................................42

A: PFMRAP Institutional and Implementation Arrangements ......................................... 42

B: IFMIS Project implementation arrangements .............................................................. 47

C: Financial Management, Disbursements and Procurement ........................................... 50

C: Procurement ................................................................................................................. 56

D: Results Monitoring & Evaluation ................................................................................ 62

Annex 4: Operational Risk Assessment Framework (ORAF) .................................................63

Annex 5: Implementation Support Plan ....................................................................................69

A: Strategy and Approach for Implementation Support ................................................... 69

Annex 6: Summary of the 2012 PEFA PFM Performance Assessment ..................................71

A: Context of this assessment ........................................................................................... 71

B: Integrated Assessment of PFM Performance ............................................................... 71 Table 1: Selected Social Indicators ………………………………………………………….….2 Table 2: PFM Reform Action Plan - Components and results ....................................................... 6 Table 3: Project cost and financing ............................................................................................... 15 Table 4: Project cost and financing ............................................................................................... 39 Table 5: IFMIS Chart of Accounts ............................................................................................... 51 Table 6: Financial Management Risk Assessment and Mitigation ............................................... 52 Table 7: FM implementation support plan.................................................................................... 55 Table 8: Procurement Risk Assessment and Mitigation ............................................................... 57 Table 9: Prior Review Threshold: Good, works and non-consulting services ............................. 60 Table 10: Procurement Packages - Supply and Installation Contracts and Non-Consulting Services ......................................................................................................................................... 61 Table 11: Prior Review Threshold: Consultants ........................................................................... 61 Table 12: Procurement Packages - Consultancy Assignments ..................................................... 62 Figure 1: Current IFMIS and TSA architecture ............................................................................ 36 Figure 2: Future IFMIS and TSA Architecture............................................................................. 37 Figure 3: Estimated project disbursements ................................................................................... 40 Figure 4: Project timeline .............................................................................................................. 41 Figure 5: PFMRAP Implementation Arrangements ..................................................................... 46

vii

PAD DATA SHEET Lesotho

LS-PFM Reform Support Project (P143197) PROJECT APPRAISAL DOCUMENT

.

AFRICA AFTME

Report No.: PAD738 .

Basic Information Project ID EA Category Team Leader P143197 C - Not Required Gert Johannes Alwyn Van Der

Linde Lending Instrument Fragile and/or Capacity Constraints [ ] Investment Project Financing Financial Intermediaries [ ]

Series of Projects [ ]

Project Implementation Start Date Project Implementation End Date 06-Feb-2014 03-Mar-2017 Expected Effectiveness Date Expected Closing Date 03-Mar-2014 03-Jul-2017

Joint IFC No Sector Manager Sector Director Country Director Regional Vice President Patricia Mc Kenzie Edward Olowo-Okere Asad Alam Makhtar Diop .

Borrower: Ministry of Finance and Development Planning

Responsible Agency: Ministry of Finance and Development Planning Contact: Title: Telephone No.:

(266) 2232-3703 Email: [email protected]

.

Project Financing Data(in US$ Million) [ ] Loan [ ] Grant [ ] Guarantee [ X ] Credit [ ] IDA Grant [ ] Other Total Project Cost: 6.09 Total Bank Financing: 5.50 Financing Gap: 0.00 .

Financing Source Amount(US$ Million)

viii

BORROWER/RECIPIENT 0.59 International Development Association (IDA) 5.50 Total 6.09 .

Expected Disbursements (in US$ Million) Fiscal Year 2014 2015 2016 2017 2018 Annual 3.27 1.90 0.32 0.01 0.00 Cumulative 3.27 5.17 5.49 5.50 5.50 .

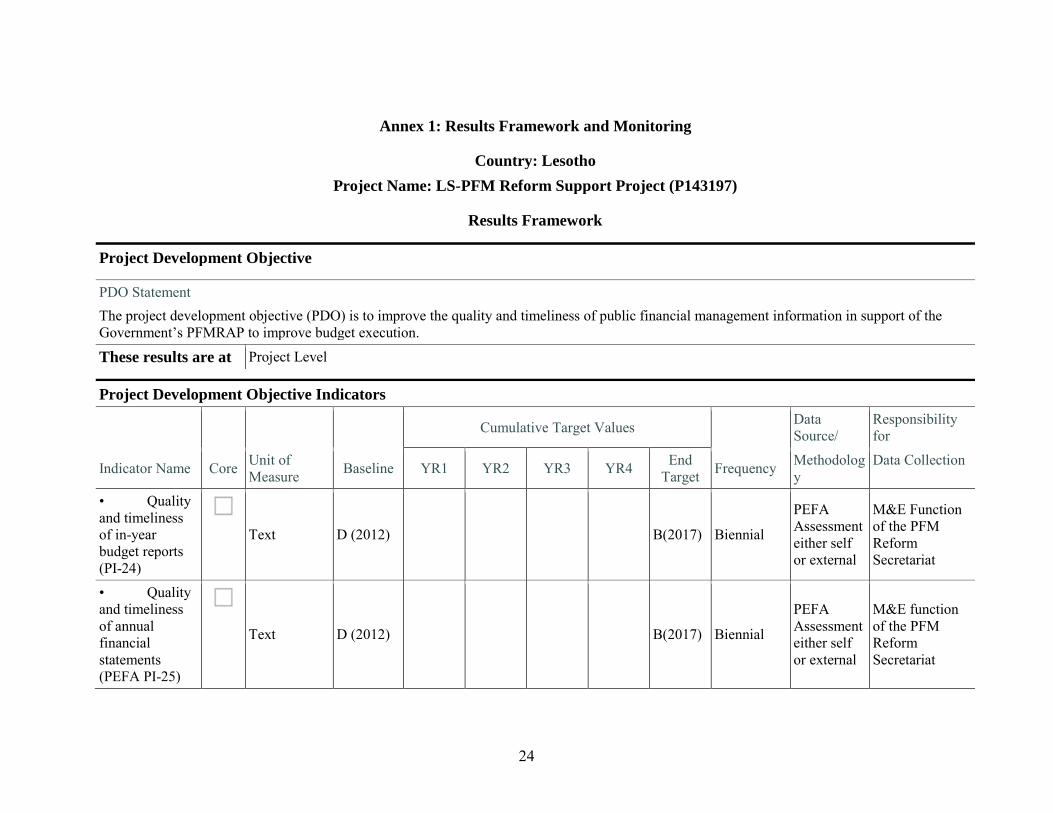

Proposed Development Objective The project development objective (PDO) is to improve the quality and timeliness of public financial management information in support of the Government’s PFMRAP to improve budget execution. .

Components

Component Name Cost (US$ Millions) Support for improving the stability and reliability of existing IFMIS

0.75

Support for expansion and modernization of IFMIS platform 3.91

Support for change management, training and project management

0.83

.

Institutional Data Sector Board Financial Management .

Sectors / Climate Change Sector (Maximum 5 and total % must equal 100) Major Sector Sector % Adaptation

Co-benefits % Mitigation Co-benefits %

Public Administration, Law, and Justice

Central government administration

100

Total 100

I certify that there is no Adaptation and Mitigation Climate Change Co-benefits information applicable to this project. .

Themes Theme (Maximum 5 and total % must equal 100) Major theme Theme % Public sector governance Public expenditure, financial

management and procurement 100

Total 100

ix

.

Compliance Policy Does the project depart from the CAS in content or in other significant respects?

Yes [ ] No [ X ]

.

Does the project require any waivers of Bank policies? Yes [ ] No [ X ] Have these been approved by Bank management? Yes [ ] No [] Is approval for any policy waiver sought from the Board? Yes [ ] No [ X ] Does the project meet the Regional criteria for readiness for implementation? Yes [ X ] No [ ] .

Safeguard Policies Triggered by the Project Yes No Environmental Assessment OP/BP 4.01 X

Natural Habitats OP/BP 4.04 X

Forests OP/BP 4.36 X

Pest Management OP 4.09 X

Physical Cultural Resources OP/BP 4.11 X

Indigenous Peoples OP/BP 4.10 X

Involuntary Resettlement OP/BP 4.12 X

Safety of Dams OP/BP 4.37 X

Projects on International Waterways OP/BP 7.50 X

Projects in Disputed Areas OP/BP 7.60 X .

Legal Covenants Name Recurrent Due Date Frequency Counterpart Funding 31-Mar-2015 Description of Covenant The Recipient shall provide in its FY 14/15 budget, adequate funds to carry out specific activities as contained in Schedule 2 Section IV (C) of the Financing Agreement .

Team Composition Bank Staff Name Title Specialization Unit Zoe Kolovou Lead Counsel Lead Counsel LEGAM

Marie J. Bolou Senior Program Assistant

Program Assistant AFTME

Mabel Nomsa Mkhize Program Assistant Team Assistant AFCS1

Jose C. Janeiro Senior Finance Officer Senior Finance Officer CTRLA

x

Gert Johannes Alwyn Van Der Linde

Lead Financial Management Specialist

Team Lead AFTME

Ismaila B. Ceesay Lead Financial Management Specialist

Lead Financial Management Specialist

AFTMW

Cem Dener Sr Public Sector Spec. Sr Public Sector Spec. PRMPS

Ikechi B. Okorie Senior Operations Officer

Senior Operations Officer

AFTME

Chitambala John Sikazwe

Procurement Specialist Procurement Specialist AFTPE

Tandile Gugu Zizile Msiwa

Financial Management Specialist

Financial Management Specialist

AFTME

1

I. STRATEGIC CONTEXT

A: COUNTRY CONTEXT

1. Lesotho is a lower middle-income country with per capita gross national income of US$1,380.1 It is a small country, mostly mountainous and largely rural with about 2 million people and completely surrounded by South Africa. Lesotho has an open economy traditionally centered on trade. Its main exports are textiles, water, and diamonds. Lesotho’s main trading partners are the United States and South Africa. It is a member of the Southern African Customs Union (SACU) and the Southern African Development Community (SADC) and, as a member of the Common Monetary Area (CMA); its currency is pegged to the South African rand.

2. Lesotho has undergone political and economic changes over the last two decades. The political system has evolved towards open and competitive elections. The economy has grown at an annual rate of 3 percent in per capita terms, which, though modest for its income level, compares well with the rest of the SACU region and the African continent as well as other small states.2 The economy has been able to adapt itself to new realities and has taken advantage of new growth opportunities. The changes have involved shifts from subsistence agriculture and remittances toward mining, water exports, manufacturing exports, and services. 3. The country now finds itself at a crossroads, requiring new growth engines, a more streamlined role for the state, and the need for a dynamic private sector to seize opportunities in the Southern African market. Public spending grew from 45 percent of GDP in FY2004/05 to about 62 percent in FY2011/12, one of the highest ratios in the world. This level is unsustainable, and public spending can no longer be relied upon to drive growth.3 The effectiveness of public spending has also been low, weakening its effect on growth and social outcomes.4 The fiscal consolidation needed to strengthen fiscal and external sustainability would weigh on future growth, especially if not matched by greater effectiveness of spending and service delivery institutions. 4. Economic growth has not been adequately inclusive, resulting in high concentration of poverty in rural areas, persistent high levels of inequality, and widespread unemployment. Unemployment stood at 24 percent in 2008, among the highest in the world. Only 230,000 of the 608,000 employed people engage in formal wage employment. The rest are informal activities, and they are often paid in-kind. Preliminary Government’s estimates based on the 2010/11 Household Budget survey show that the national poverty head count rate stood at 57.1 percent and the Gini Coefficient based on consumption stood at about 0.53 (Table 1). Both these figures are virtually the same as those obtained in the 2002/2003 Household Budget survey. However, in comparison with the 2010/11 figures, poverty decreased in urban areas while increasing in rural areas (see Table 1). Given that about three quarters of the population live in the rural areas, addressing this poverty incidence will require greater inclusiveness of

1 2012 Atlas GNI per capita. 2 Small states are defined as sovereign countries with a population of 2 million or less. Favaro, Edgardo M., (2008), Small States, Smart Solutions, World Bank Press, Washington D.C. 3Lesotho Public Expenditure Review 2012 (Report No. 71973-LS). 4Lesotho Public Expenditure Review 2012 (Report No. 71973-LS).

2

growth, a sustainable and effective public sector, and access to quality service delivery. At the heart of this development agenda, is job creation, particularly in low-skilled sectors. Table 1: Selected Social Indicators

1995

2000

2010 (or latest

available)

National headcount poverty ratio (% of population)

56.6* 57.1** National headcount poverty ratio- urban (% of population) 39* 36.6** National headcount poverty ratio- rural (% of population) 60.9* 61.8** Gini coefficient 0.51* 0.53** Primary school enrolment (% net) 68 76 73.4 Secondary school enrolment (% gross) 30 30 46 Life expectancy at birth (years) 56.9 47.6 46.7 Under-5 mortality rate (per 1,000 live births) 99.4 126.8 85 Maternal mortality rate ( modeled per 100,000 live births) 340 470 530 Prevalence of HIV (% of population ages 15-49) 14.3 24.5 23.6 *Information from 2002/03 HIES **Preliminary Government estimate based on the 2010/11 HIES Source: World Bank World Development Indicators

5. Much of the expansion of Government spending over the past decade has been directed toward the social sectors, but social outcomes have not improved significantly. Lesotho spends close to 30 percent of GDP, or more than half the Government’s budget, in three social sectors: education, health, and social protection. The country's health systems have been overwhelmed by HIV/AIDS, with the adult prevalence rate climbing to the world’s third highest at 23.6 percent. However, overall coverage of key HIV/AIDS interventions has improved, including Prevention of Mother to Child Transmission (PMTCT) and Anti-Retroviral Treatment (ART).5 Maternal mortality is among the highest in Sub-Saharan Africa. In the education sector, learning outcomes and coverage have improved, but quality remains low at the primary level. In terms of social protection, Lesotho spends close to 9 percent of GDP on social transfers and most of them do not target the poor. 6. Deep-rooted inefficiencies in Public Financial Management (PFM) have minimized the effectiveness of public spending, especially in the social sector. Since as far back as 2000 the Government does not have timely and reliable in-year and annual financial information to support budget execution, monitoring and oversight. An investment is therefore required in order to provide Government the necessary financial information that is required to help improve the effectiveness of its public spending. Improving the effectiveness of public spending in Lesotho, especially to improve social outcomes, will directly support the Bank’s twin goals of poverty reduction and shared prosperity.

5 Through the HIV and AIDS Technical Assistance Project (P107375), the Bank has continued to support the Government’s efforts to build the capacity of ministries, departments, and agencies (MDAs) and civil society organizations (CSOs) to implement the Second HIV/AIDS National Strategic Plan in a coordinated manner.

3

7. Lesotho’s National Strategic Development Plan (NSDP) FY2012/13-FY2016/17 serves as the Poverty Reduction Strategy Paper (PRSP) and is the second PRSP that the Government has produced. With the central objective of faster growth and poverty elimination, the Government has set out its approach towards a stable democracy, a united and prosperous nation at peace with itself and its neighbours by 2020. The strategy is based on the (i) pursuit of shared and job-creating economic growth; (ii) development of priority infrastructure; (iii) enhancement of the country’s skills base, technology adoption, and foundations for innovation; (iv) improvement in health outcomes including combating HIV/AIDS and reducing (social) vulnerability; (v) reversal in environmental degradation and adaptation to climate change; and (vi) promotion of peace and democratic governance and build effective institutions. This governance pillar includes a focus on enhancing the public sector’s effectiveness and efficiency in delivering services, improving public financial management, and maintaining the rule of law. In view of the importance of PFM to the effective implementation of the NSDP, to minimize inefficiencies in government spending; and provide a platform for budget support assistance from development partners (DPs), the effective functioning of PFM institutions and systems at central and local levels of government in Lesotho has been identified as a high priority.

B: SECTORAL AND INSTITUTIONAL CONTEXT

8. Lesotho’s initiated a Public Service Improvement and Reform Program (PSIRP) in 2003/04 of which the first (of three) component was aimed at improving government financial management (the other two addressed decentralization and government management). Under the auspices of this program DFID undertook research into the state of government financial management and determined that it was heavily dysfunctional, concluding that it operated to a ‘cultural norm of fiscal indiscipline’. Due in part to these findings, DFID was nominated by development partners to lead the assistance to the Government of Lesotho (GoL) in addressing the challenges in the sector. As a consequence, the ‘DFID Foundation Programme’ was launched in 20046 9. The DFID Foundation Programme and the two CBEP projects were intended to address a wide range of PFM reforms covering the following main areas -

a) planning and budgeting – including MTEF, improved macroeconomic forecasting, data collection and tax policy;

b) accounting and reporting – including implementing a new integrated financial management information system (IFMIS), strengthening internal and financial controls and internal audit, improved technical and professional training;

c) audit and oversight – including addressing the backlog of financial reports, strengthening the capacity of the Office of the Auditor General;

6 The program was originally scheduled to run from 2004 to 2008 but it was extended to 2010 to allow more time for some of the activities to be completed. It ended in 2010 when DFID largely withdrew from Lesotho. The EU was also active in the then Ministry of Finance and Development Planning (MFDP) with its Capacity Building in Economic Planning (CBEP – now succeeded by CBEPII project) with Irish Aid also providing assistance to the wider sector.

4

d) administration – restructuring the MFDP, improving pension administration. 10. Another relevant (and ongoing) reform is related to the development of human resource capacity in accounting, auditing and procurement. At an early stage in the DFID Foundation Program, DFID and the GoL agreed that a major brake on raising standards in PFM was the lack of human resource capacity in accounting, audit and procurement. A study carried out by the UK Chartered Institute of Public Finance and Accountancy (CIPFA) in 2006 recommended the introduction of professional training programs aimed at government employees in these disciplines. This recommendation was accepted and the programs commenced in early 2007 with the accountancy and audit courses operated at the Lesotho Centre for Accounting Studies (with examinations for the CIPFA International Certificate and Diploma qualifications conducted joint by CIPFA and the Lesotho Institute of Accountants), and in procurement at the Institute for Development Management with students sitting for the external qualifications of the UK Chartered Institute of Purchasing and Supply (CIPS). Funding for this program from 2007 to 2012 was provided by MFDP using a grant from Irish Aid specifically for this purpose, though Irish Aid has recently indicated that this funding will no longer be available from 2013. Therefore, the CIPFA scheme for professional training in government will be replaced from 2014 by the new professional accountancy qualification scheme recently developed with the support of the Bank, through an IDF grant to the Lesotho Institute of Accountants, with different funding arrangements – currently the European Union (EU) is providing financial support of about EUR 1.2million for the implementation of the new arrangements. The CIPS scheme will be reviewed as part of this initiative. 11. Mixed results of this first phase of the reform program are evidenced in two PEFA PFM Performance Reports conducted in Lesotho in 2009 and 2012. Progress has been made on some fronts - most notably in budgeting and macroeconomic forecasting, the introduction of a new legal framework for PFM, the introduction of a new IFMIS on 1 April 2009 and completion of public accounts from 2005 to 2010 (which was just completed up to FY 2013 and submitted for auditing on 30 September 2013). But several long standing problems are yet to be resolved - a sufficient strategic overview of the allocation of resources is currently lacking, inadequate planning of services, insufficiently competitive procurement, weak cash management, the IFMIS is not yet effective in supporting good financial management and timely and reliable in-year and annual reporting, weak accounting processes and disciplines, weak payroll controls, ineffective internal and external auditing systems. Fuller details of the PEFA PFM Performance assessments are provided in Annex 6.

12. Most notably the IFMIS platform has only been partially utilized to support key budget execution functions of the Central Government since its introduction in April 2009. Due to a number of technical and adaptive challenges, the system does not support daily operations effectively, and the timely production of reliable in-year and annual financial information is not possible. Some of the core PFM functions (requisitions, orders, commitment control and payments) were initially not performed through the IFMIS - budgets that were not loaded, users that were not properly trained and system unavailability are all contributing factors. Frequent system unavailability still continues (up to two days a week) and causes bypassing of the IFMIS in order to continue operations with no controls to ensure timely capture of transactions created outside of the IFMIS. Other PFM functions (e.g. budget preparation & asset management) are still performed manually or through parallel systems in line ministries and

5

district sub-accountancies. Good practice accounting disciplines, such as month-end closures and bank reconciliations, are also not yet fully functional. These deficiencies severely limit revenue and expenditure control, budget execution, reliable and timely reporting, and ultimately financial accountability. 13. At an early stage in the history of PSIRP the stakeholders in the PFM component established - within the framework of PSIRP – a steering committee under the title of the PFM Improvement and Reform Steering Committee (PFM IRSC) with membership drawn from across all stakeholders (government, development partners and others) and chaired by the Principal Secretary of the then MFDP. This Committee continues in existence and provides a regular opportunity for interface between Government and other stakeholders, having met roughly every six weeks over the last year. Whilst the existence of IRSC has provided some stability to the management of the reform process, it has yet to deliver the level of program planning and coordination expected of it and, to a degree, since the end of the DFID Foundation Program has lost its sense of direction with no central program driving the reforms. 14. The Government and development partners have however committed to move to a new phase of the reforms founded on greater implementation of the new rules and regulations, tighter internal controls and greater attention to the benefits of PFM reforms for Ministries, Departments, Agencies (MDAs) and sectors. In preparation for this new phase, Government and development partners have been working together since late 2011, through the IRSC, on creating a future reform program. An initial program was approved in principle by the IRSC in May 2012, and then further refined and finalized with technical assistance from the International Monetary Fund (IMF) during the last quarter of calendar 2012. A final version of the Government Public Financial Management Reform Action Plan (PFMRAP) 2012-2017/18, with a foreword by the Minister of Finance, was approved by the IRSC in March 2013. A High Level PFM Workshop was also hosted by the Minister of Finance on 11 November, 2013 with representation from Parliament (specifically the chairperson of the Public Accounts Committee); several Ministers (including Finance, Development Planning, Health, Education and Social Development); Development Partners (DPs, including the IMF, EU, AfdB and UNDP); several Principal Secretaries, Component Leaders for the PFM Reform Action Plan (PFMRAP), and other key staff involved in its implementation. The GoL provided an overview of the PFMRAP, and the associated implementation arrangements, and the workshop concluded with overwhelming support for its implementation and appreciation to the DPs for their support. 15. The approved PFMRAP covers a number of strategic actions, that have been structured into 8 components and linked to key results (with reference to the associated PEFA performance indicators where possible). Key outputs have been defined for each of the components and are financed as reflected in Table 2 below:

16. This operation will support the GoL with the implementation of key result (b) of component 5 of its PFMRAP. Essentially this will entail stabilization and improving the effectiveness of the IFMIS platform.

6

Table 2: PFM Reform Action Plan - Components and results Component / Results Financed by 1. Modern PFM regulatory framework implemented a) Regulatory framework updated to underpin PFM reforms EU b) Capacity developed to implement and sustain the PFM regulatory framework EU 2. Transparency and effectiveness of policy orientation of the budget assured a) Demonstrable links between development plans, fiscal strategy and budget

appropriations EU

b) Budget process redesigned to provide space for enhanced engagement by policymakers

EU

c) Effectiveness of macro-fiscal management enhanced EU d) Comprehensiveness and quality of information included in budget

documentation progressively improved EU

3. Cash flow forecasts a major determinant of internal debt and financial investment

a) Cash Management Unit and Liquidity Committee established GoL b) Access to consolidated information on government cash balances GoL c) Cash forecasts accurate to 90% GoL 4. Internal Controls ensure strengthened operational efficiency and

effectiveness

a) Ex-ante controls on non-salary expenditures compliant with contextually relevant components of the COSO framework

GoL

b) Compensation of employees and pension payments consistent with employee/pensioner number and entitlements

GoL

c) Internal audit compliant with COSO and IIA controls and standards AfDB 5. Accounting and fiscal reporting fully compliant with the regulatory

framework and accounting standards

a) Government accounting cadre reform implemented GoL b) Accounting systems and application software upgraded to comply with

regulations and standards World Bank

c) In-year and annual fiscal reports published in accordance with regulations and standards

GoL

6. Public Procurement aligns with international best practice in efficiency and transparency

a) Legislative and regulatory framework revised and upgraded AfDB b) Management and operations of the public procurement system re-engineered and

reconfigured AfDB

c) Public procurement achieves transparency through outreach to public and suppliers

AfDB

d) Human resource capacity within public procurement is significantly increased AfDB 7. External audit and oversight compliant with INTOSAI standards (ISSAI) a) Legal and regulatory framework updated to comply progressively with

international standards AfDB

b) HR capacity to deliver on prescribed external audit mandate established AfDB c) Legislature empowered to perform oversight functions AfDB 8. Governance and institutional management of PFM reforms improved to

facilitate ownership, monitoring and evaluation of progress

a) Management of PFM reform institutionalised GoL / AfDB / EU

17. Table 2 above summarizes the financing arrangement for components / activities of the PFMRAP. In addition to this investment by the Bank, the implementation of the PFMRAP will be supported by the EU, African Development Bank (AfDB) and IMF,

7

under oversight and coordination from the IRSC. The AFDB7 will be providing financial support approximating US$ 3.9million primarily for activities related to procurement, internal audit and external audit. Its operation will also fund PEFA assessments envisaged for 2015 and 2017. The EU will be supporting components 1, 2 and 8 of the PFMRAP with financial support and technical assistance in total approximating EUR 10million8. IMF is in discussion with the EU to receive funding to provide such technical assistance, including on cash management and PFMRAP coordination.

18. Since the IFMIS has already been in operation since 1 April 2009, the planned interventions are quite distinct from other PFMRAP activities. However, IFMIS dependencies on and links to the regulatory framework, processes, controls, standards and data requirements will be coordinated through the PFM Reform Technical Committee (RTC), a sub-committee of the IRSC. This will be focused in particular on the activities related to the following key outputs – (i) Regulatory framework updated to underpin PFM reforms; (ii) Cash Management Unit; (iii) Access to consolidated information on government cash balances; (iv) Ex-ante controls on non-salary expenditures compliant with contextually relevant components of the Committee of Sponsoring Organizations of the Treadway Commission (COSO) framework; (v) In-year and annual fiscal reports published in accordance with regulations and standards; and (vi) Management and operations of the public procurement system re-engineered and reconfigured. 19. This project’s deliverables are directly complementary to the PFM policy actions of the current series of World Bank development policy operations. The Development Policy Operation (DPO) series have a focus on the following key areas of reform embedded in the PFMRAP – (i) introducing a medium term budget policy statement and a medium term fiscal framework approved by Cabinet; (ii) eliminating the backlog of audited public accounts; (iii) improving the quality and timeliness of public financial management information, to support better budget execution and financial accountability (to which this project directly links); (iv) strengthening the transparency in public procurement; (v) further strengthening of the legal framework through the finalization of new PFM regulations; and (vi) improving responsiveness of key ministries to audit findings, in order to help improve the control environment. A General Budget Support Group (GBS – currently chaired by the EU) is in operation, which has joint annual reviews and an agreed Common Performance Assessment Framework (CPAF). The last joint review was in February 2013.

C: HIGHER LEVEL OBJECTIVES TO WHICH THE PROJECT CONTRIBUTES

20. The rationale for the proposed PFM reform support project is consistent with, and aligned with Pillar 6 of the NSDP (2012-2016). The emphasis under this Pillar on PFM related

7 Institutional Support for the Enhancement of Public Financial Management (ISEP) Project Appraisal Report, African Development Bank, 14 October 2013 8 As reported in the speech by H.E. Ambassador Hans Duynhouwer at the GoL High Level PFM Workshop, 11 November 2013, as well as his speech at the 5th Annual Conference of the Lesotho Institute of Accountants, 23 October 2013

8

interventions is primarily focused on efficient delivery of quality, timely services in an accountable and transparent manner; and political governance, including decentralization and local government transformation. This pillar also recognizes the fact that a sound PFM is crucial to achieve the national development goals of promotion of peace, democratic governance and building effective institutions. 21. In this phase of the PFM reform agenda, the government seeks to improve its capacity to utilise public resources towards meeting the NSDP targets and ultimately those of Vision 2020 through the strengthening of human resource capacity; development of systems and procedures for effective financial management and reporting, strengthening an institutional framework that is transparent and ensures accountability in the public sector. To this end, the Project will support the Government’s efforts towards ensuring aggregate fiscal discipline, more strategic allocation of resources, and greater financial accountability. The achievement of these broader goals will not only be critical to a more efficient delivery of basic services but also serve as a major step towards the achievement of the NSDP goals of poverty reduction and shared prosperity through broad-based economic growth.

22. Strengthening of PFM systems to support the development of the public sector capacity and efficient service delivery is consistent with the foundational pillar of the World Bank’s Strategy for Africa: governance and public sector and aligned with the Bank’s twin objectives of poverty reduction and shared prosperity. The relevance of strengthening the PFM system cannot be overemphasized in a country like Lesotho if more 50 percent of the budget currently being spent in three social sectors - education, health, and social protection - is to be translated into greater human development and economic transformational outcomes. This project serves as a platform for resolving these challenges as it will support the rebuilding of institutions and the PFM systems and practices that provide timely and reliable financial information. Without such information the ability of GoL to improve service delivery in support of the goals for poverty reduction and shared prosperity will continue to be greatly impeded.

II. PROJECT DEVELOPMENT OBJECTIVE

A: PROJECT DEVELOPMENT OBJECTIVE

23. The project development objective (PDO) is to improve the quality and timeliness of public financial management information in support of the Government’s PFM Reform Action Plan (PFMRAP) to improve budget execution.

B: PROJECT BENEFICIARIES

24. The main beneficiaries of this project are – the core IFMIS team, PFM staff who depends on the IFMIS for the execution of their functions, Program Managers and Heads of Ministries, District Councils, the Auditor-General, Cabinet, the Public Accounts Committee, Parliament, the Central Bank, development partners and citizens and suppliers who transact with the Government.

9

25. Government hosted a High Level PFM Reform Workshop on 11 November 2013, to ensure broad stakeholder consultation and ownership for the PFMRAP. In particular the opportunity was also used to initiate a change process for the key IFMIS stakeholders, by clarifying the current situation, objectives, envisaged benefits, timeline, roles and responsibilities for project implementation. As part of project preparation several IFMIS specific consultations were also held with the financial controllers and other key staff of line ministries, including Local Government and Chieftainship, Health, and Education.

C: PDO LEVEL RESULTS INDICATORS

26. Achievement of the PDO will be assessed through its impact on relevant PEFA PFM performance indicators. PEFA assessments of central government were carried out in Lesotho in 2009 and 2012 (refer to Annex 6 for a summary of the results). The PEFA assessments have made an important contribution to the shaping and implementing of reforms and improvements to the PFM system, and the GoL has expressed strong interest in using the results of the 2012 PEFA assessment to help shape its future reform agenda and to track its progress. 27. The achievement of the project's overall development objective will be measured by regular focused assessments of the following key indicators of the PEFA PFM Performance Assessment Framework:

(i) Quality and timeliness of PFM Information • Quality and timeliness of in-year budget reports as measured by PI-24 • Quality and timeliness of annual financial statements as measured by PI-25.

(ii) Improved Budget Execution

• Stock and monitoring of expenditure payment arrears as measured by PI-4 • Predictability of the availability of funds for commitment of expenditures measured

by PI-16

III. PROJECT DESCRIPTION

A: PROJECT COMPONENTS

28. The Bank and donor partners’ PFM engagement in Lesotho across sectors, including through budget support operations, focuses to a considerable extent on strengthening fiscal management institutions, accountability and oversight for improved service delivery. The ability to put in place adequate systems, policies and good practices in both revenue and expenditure management is a prerequisite for a sustainable path for good governance. While there are complementary support operations provided by development partners (the EU, the AfDB and the IMF) for the other components of the PFMRAP (refer Table 2), the activities to be financed under this project will avoid overlaps. Their implementation will be coordinated in a manner that ensures that project spending is directed to unfunded outcome areas.

10

29. The Project will be implemented through 3 distinct components, related sub-components and core activities as defined below: Component 1: Support for improving the stability and reliability of the existing IFMIS platform (US$ 0.883 million, of which IDA US$ 0.752million) 30. Objective: The objective of this component is to improve the stability, performance and reliability of the existing IFMIS platform. Government plans to go-live with an upgrade of its existing software on 1 April 2015, and the existing IFMIS platform will need to be operationally and technically sound through to the closing of FY15 (which could be as late as December 2015). 31. Current situation: Most of the operational issues experienced today stem from the rapid deployment of IFMIS in April 2009, coupled with a decision by the GoL to allow more than 700 untrained users access to the system whilst key staff to operate and maintain the system was not ready and / or departed shortly after go-live. The IFMIS implementation was initiated in November 2007, through a turn-key contract (EUR 7.3 million, including a 3-year warranty period - funded by the EU) with the authorized supplier of the selected software in Africa (see Annex 2 for the details). The system implementation was completed in a relatively short time (16 months), however, a number of contract management and system support challenges emerged afterwards. For instance, despite training of 16 Application, 16 Technical and 16 Help Desk support personnel, the numerous problems and frustrations after go-live and a weak retention strategy have resulted in almost all of these team members leaving within a short time after system go-live. 32. A recent evaluation of the IFMIS9 and World Bank staff assessment during project preparation confirm that several key problems with the configuration and operation of the IFMIS remain to be addressed. These include amongst others: (i) severe Wide Area Network (WAN) downtime; (ii) inadequate system performance; (iii) non-support of payment processing by an Electronic Funds Transfer (EFT) system; (iv) revenue receipting by cashiers of MDAs not performed on the IFMIS; (v) district spending units of MDAs are not connected to the IFMIS, but supported through Sub-accountancies connected to the IFMIS with cumbersome payment processes through commercial bank accounts; (vi) time-consuming bank reconciliation processes, which is the result of failure to originate some transactions directly in the IFMIS and data capture errors by the Central Bank of Lesotho (CBL); (vii) non-existent help desk function; (viii) lack of month-end closing procedures for the IFMIS resulting in inconsistency of financial information in reports; (ix) bypass of commitment controls in the IFMIS. The resolution of these problems, the details of which are contained in Annex 2 - have informed the design of the project components and sequencing of activities as further described below. 33. In addition, there are several adaptive challenges and policy decisions which require high level attention from the Government, to ensure the successful resolution of the current problems. For example, IFMIS roles and responsibilities must be clearly defined; the Office of 9 Evaluation of Public Financial Management – Integrated Financial Management Information System (FMIS), Pohl Consulting & Associates, European Union, May 2013

11

the Accountant-General and the broader Ministry of Finance (MoF) management do not routinely rely on IFMIS to support their core functions and decision making, and several others detailed further explained in Annex 2. In order to lay a proper foundation for a stable and effective IFMIS going forward these shortcomings should be addressed urgently and have been incorporated in the design of the project components and sequencing of activities as described below. 34. Activities: The project will support the implementation of the following key activities in order to address existing technical and operational challenges, and lay a solid foundation for the expansion and modernization of IFMIS platform through Component 2:

a) Activity 1.1 - Improvement of existing wide-area network connectivity: A joint effort by

the IFMIS Information and Communication Technology (ICT) team at the MoF and that of Ministry of Communications Science and Technology (MCST) has been initiated. However, further support is needed for the rapid resolution of existing network issues affecting the IFMIS operations;

b) Activity 1.2 - Improvement of primary and backup IFMIS data centers: This will include immediate server and UPS upgrades. The Ministry of Finance will contribute to this activity by undertaking other urgent ICT infrastructure improvements, including the electrical works, upgrade of generators and improvement of the cooling systems;

c) Activity 1.3 - Activation of the EFT interface with the CBL: This activity is expected to support activation of the IFMIS EFT interface with the CBL;

d) Activity 1.4 –Cleaning IFMIS databases and improving accounting controls: This activity will support the correction/cleaning of database records in the current IFMIS system and transfer of reliable opening balances to the upgraded version of the existing software. In addition, technical assistance will be provided to the Office of the Accountant-General to strengthen accounting controls such as reconciliations.

35. The following priority actions are recommended to facilitate more effective use of IFMIS for daily operations and reporting:

a) Ensure daily recording of all revenue in IFMIS by connecting cashiers of line ministries

to the existing IFMIS. b) Enforce monthly closing of IFMIS (for example, 15 days after month-end) for data

capture, monitor data quality, provide training support and enforce basic accounting disciplines.

c) Enforce year-end closing of IFMS for data capture (for example, 30 days after year-end). d) Re-affirm the directive to highlight the requirements for using IFMIS on a daily basis in

all line ministries and sub-accountancies. e) Strengthen the MoF Application Support team with additional staff, training, equipment

and office space. f) Activate the issue tracking portal of the software supplier to record all IFMIS technical

and functional issues and record the solutions promptly. g) Complete the reorganization of the MoF ICT Department and define the roles and

responsibilities of all technical specialists.

12

Component 2: Support for expansion and modernization of IFMIS platform (US$ 4.375 million, of which IDA US$ 3.913million) 36. Objective: The objective of this component is to upgrade, configure and deploy the latest version of the existing IFMIS Software to support a simplified business architecture from a stable and well performing technology platform. 37. Current situation: The MoF is of the view that the existing IFMIS software is sound and relevant to the perceived needs of Lesotho. An upgrade of its existing IFMIS software, including to a web-based architecture, is required as the current version will no longer be maintained. This upgrade will assist to resolve some of the configuration issues such as separate databases, budget preparation, commitment control, cash management, and support for Treasury Single Account (TSA) operations. In addition, the implementation of the current IFMIS is bedeviled by an overly complex architecture and process design, capacity weakness in the management of the Treasury function, control weaknesses and a general lack of clarity of and compliance with rules and regulations governing financial management practices (including timeliness of data collection and fiscal reporting). 38. Activities: In order to address these challenges, the project will finance the following activities:

a) Activity 2.1 - IT Audit of the IFMIS platform: A technical and operational assessment (IT Audit) of existing IFMIS software and data centers will be completed through this activity, before any system upgrade or modernization effort. The IT Audit is also expected to assist the GoL to update the necessary system design documentation and provide the necessary justification for the hardware to be procured.

b) Activity 2.2 - PFM business process re-engineering: Apart from the process and architecture issues already identified and addressed in Component 1, a more detailed business process review needs to be completed rapidly in order to clarify and implement possible further improvements and simplifications before the IFMIS upgrade / modernization;

c) Activity 2.3 - Expansion and modernization of the IFMIS platform: This activity is expected to enhance the functional support by the IFMIS software (e.g., improved commitment management and budget execution, TSA operations, better cash management, etc.), modernize the technical architecture (transition to web-based application through an upgrade of the existing software), enhance the relevant ICT infrastructure and extend the IFMIS to all Ministry offices in Districts and District Councils (estimated at 122 offices) with the necessary capacity building. The Ministry of Finance will contribute to this activity by procuring the necessary servers to support the upgraded version of the existing software.

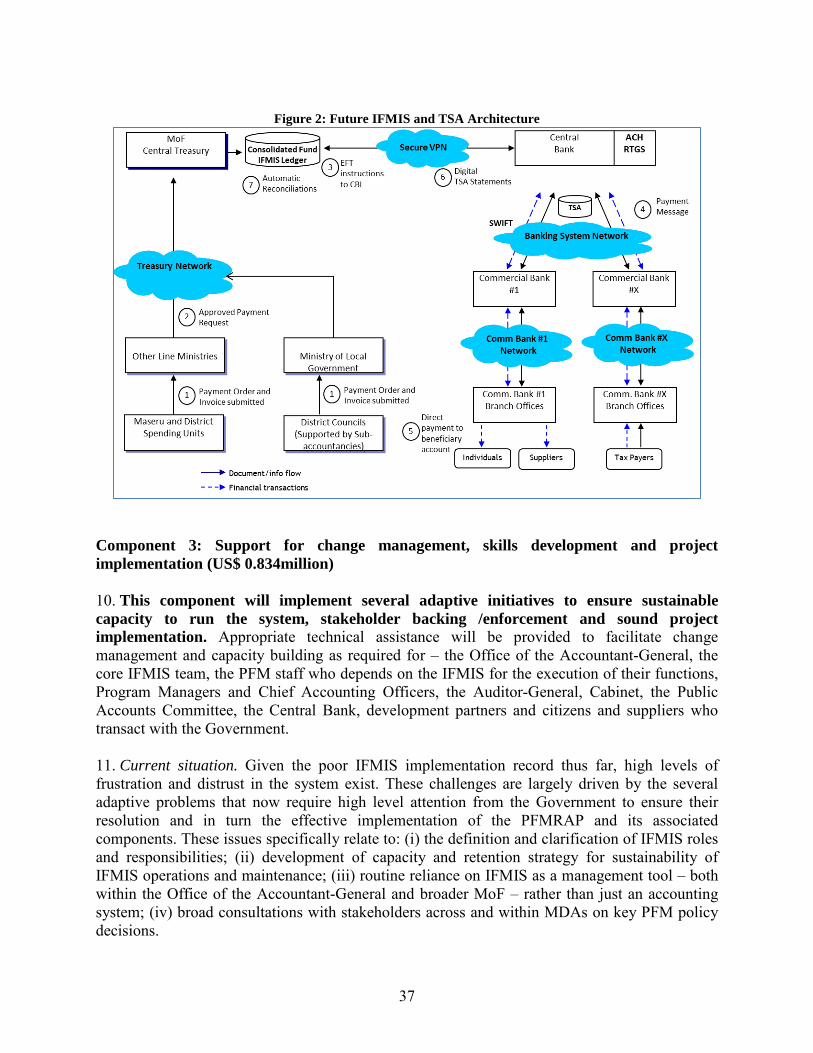

39. In addition, the project will support MoF to introduce the following policy and architecture changes before or during the expansion and modernization of IFMIS to simplify processing and prevent operational IFMIS problems. The key changes to the IFMIS and TSA architectures are presented graphically in Figure 1 and Figure 2 in Annex 2 -

13

a) Several key policy decisions should be made in consultation with relevant stakeholders on: (i) transition to centralized TSA operation benefiting from an interface with the CBL systems for electronic payments and reconciliation of accounts (which will require all staff, suppliers and beneficiaries transacting with government to open bank accounts); (ii) supporting the operations of District Councils (DCs) through IFMIS web portal extensions; (iii) supporting the operations of district spending units of line ministries, and cashier’s functions through IFMIS web portal extensions; and (iv) initiating the establishment of digital signature infrastructure (benefiting from ongoing e-Government initiatives of the MCST).

b) One general ledger should be created for the Consolidated Fund and all line ministries operating against the TSA. This will also require district spending units of line ministries to be connected to the central IFMIS, operating against the TSA (using EFTs) and no longer through commercial bank accounts managed by the sub-accountancies. This will also require a review of the Chart of Accounts.

c) Only one District Council (Maseru) currently uses a commercial accounting package for financial control, accounting and reporting. The other nine run manual systems, and a recent diagnostic assessment10 of decentralization in Lesotho found that “Only limited audits of local Authorities have been undertaken since 2005. The Auditor General explained that only 3 district councils namely Botha Bothe, Mafeteng and Mohale Hoek have had their accounts audited over the period. In all cases, the accounts returned qualified opinions pointing to significant weaknesses in their financial management systems”. A key challenge therefore is the absence of reliable and timely financial statements. To support their obligations under the Public Financial Management and Accountability Act, 2011, District Councils urgently require access to the IFMIS to bring this situation under control. From the dimensions of cash flow management, capacity, cost effectiveness and maintaining data integrity, they are to be connected to the central IFMIS, preferably as cost centers under the Ministry of Local Government and Chieftainship (MLGC) and also operating against the TSA. It is also proposed that the current sub-accountancies in districts are utilized to support the DCs, to support their financial management functions.

d) The Budget Department must be equipped to use the Active Planner module for the FY16 budget preparation process. This will eliminate additional work and controls to ensure reliable transfer to and maintenance of the budget in the IMFIS.

Component 3: Support for change management, training and project implementation (US$ 0.834million) 40. Objective: The objective of this component is to facilitate the provision of technical assistance in support of change management and capacity building requirements of the Office of the Accountant-General, the core IFMIS team, the PFM staff of selected Line Ministries, , the Cabinet, the Public Accounts Committee, the Central Bank, development partners, and other stakeholders.

10 Diagnostic Assessment of Decentralization in Lesotho, UNDP, October 2013

14

41. Current situation: Given the poor IFMIS implementation record thus far, high levels of frustration and distrust in the system exist. These challenges are largely driven by the several adaptive problems that now require attention at the highest levels in Government to ensure their resolution and in turn, the effective implementation of the PFMRAP and its associated components. As detailed in paragraph 3 of Annex 2, these specifically relate to such issues as the: (i) definition and clarification of IFMIS roles and responsibilities; (ii) development of capacity and retention strategy for sustainability of IFMIS operations and maintenance; (iii) routine reliance on IFMIS as a management tool – both within the Office of the Accountant-General and broader MoF – rather than just an accounting system; (iv) broad consultations with stakeholders across and within MDAs on key PFM policy decisions; amongst others. 42. Activities: This component will implement several adaptive initiatives to ensure sustainable capacity to run the system, stakeholder backing /enforcement and sound project implementation. Key activities include the following:

a) Activity 3.1 - Support for change management and training. This will include – (i) Provision of IFMIS operations and maintenance training/capacity development to the core IFMIS team (IFMIS custodian, super users, administrators, application support team, ICT support team, training team, etc.). (ii) Support to the MoF in the development of the requisite capacity and skills amongst the IFMIS stakeholders; the assignment of IFMIS training function to the Lesotho Centre for Accounting Studies (CAS); and strengthening the capacity and training capability of the Application Support team to deliver the necessary accounting and systems training to end users on a sustainable basis, with the support from CAS as needed. (iii) User database clean-up to ensure that only valid users remain registered for access to the IFMIS software. A training program will be structured to deliver the right training at the right time. A core training team will be equipped in all respects to carry out training of end users and managers. (iv) Full PFM and relevant IFMIS training for management of Ministries and DCs, Cabinet and the Public Accounts Committee will also be delivered - this should include the full PFM cycle and how the IFMIS supports the objectives of fiscal discipline, strategic allocation of resources, efficient service delivery and financial accountability. (v) Technical Assistance to the Government for the development and implementation of a retention and succession plan for the core IFMIS team. In particular, assistance will be provided to develop the skill and competency profiles for all functions required to support the continued operation and maintenance of the IFMIS, together with a training plan for staff in post. Assistance will also be provided to explore options for GoL to appoint key IFMIS staff on performance contracts as a means to support better retention of staff in such positions.

b) Activity 3.2 - Support for project implementation. This activity will support the project implementation costs, including – (i) technical assistance to set-up and run the project in IFMIS, and financial management and procurement assistance; (ii) basic office and IT equipment for the core IFMIS team; (iii) technical assistance to supplement capacity gaps in the core IFMIS team; and (iv) monitoring and evaluation, and reporting progress on all components.

15

c) Activity 3.3 - Audit of project/financial activities. This activity will support the annual

audit and reporting of project activities.

B: PROJECT FINANCING

43. The lending instrument is Investment Project Financing (IPF). An IPF is selected as it is a flexible instrument that allows for the financing of different activities (consultants, equipment and works). Investment Project Financing supports projects with defined development objectives, activities, and results, and disburses the proceeds of Bank financing against specific eligible expenditures.

44. The total project cost is US$6.09 million, of which IDA will be financing 90% as summarized in Table 3 below:

Table 3: Project cost and financing

45. GoL will be executing and financing the following activities as their 10% contribution to the total project costs -

a) Component 1 - IFMIS data center electrical works - estimated at US$ 50,000 b) Component 1 - IFMIS data center upgrade of generators - estimated at US$ 40,000 c) Component 1 - IFMIS data center upgrade of cooling systems - estimated at

US$40,000 d) Component 2 - Upgrade of IFMIS primary and backup data center servers for

upgraded version of IFMIS Software - estimated at US$ 461,737

US$ US$ US$Total Project Cost GoL Financing IDA Financing

1 Support for improving the stability and reliability of existing IFMIS platform 882,101 130,000 752,101 85%

1.1 Improvement of existing wide-area network connectivity 200,000 0 200,0001.2 Improvement of primary & backup IFMS data centers 282,101 130,000 152,1011.3 Activation of the IFMIS EFT interface with the CBL 100,000 0 100,0001.4 Cleaning IFMIS databases & improving accounting controls 300,000 0 300,0002 Support for the expansion and modernization of IFMIS 4,375,164 461,737 3,913,427 89%

2.1 IT Audit of the IFMIS platform 100,000 0 100,0002.2 PFM business process re-eningineering 200,000 0 200,0002.3 Expansion and modernization of the IFMIS platform 4,075,164 461,737 3,613,427

3 Support for change management, training and project implementation 834,472 0 834,472 100%

3.1 Support for change management and training 572,735 0 572,7353.2 Support for project implementation (operating costs) 120,000 0 120,0003.3 Audit 50,000 0 50,0003.4 Unallocated 91,737 0 91,737

6,091,737 591,737Planned

Disbursement5,500,000 90%

Lesotho IFMIS stabilization and upgrade project % IDA financing

16

C: LESSONS LEARNED AND REFLECTED IN THE PROJECT DESIGN

46. The IFMIS system, although not entirely failed and limping along, display most of the classical failure factors that the Bank11 found in reviewing past IFMIS project supported:

a) Inadequate capacity / training of users: More than 700 untrained users were allowed access to the IFMIS upon its go-live date of 1 April 2009. No sustainable training function was established and the help desk was disbanded. A large core of untrained users still exists, which must be addressed. Component 3 will specifically address this.

b) Inadequate capacity / training and retention of the core IFMIS team: Transfer of the more advanced skills through formal and on-the-job training to the Application and IT Technical Team to fully participate in the configuration and operation of the existing IFMIS software was not properly managed. This has left the IFMIS system and core staff extremely vulnerable, especially in light of the sheer number of untrained users that were allowed access to the system and the original problems associated with go-live as well as the high level of system instability that has occurred since. Since the original go-live date most of the original Government IFMIS core team has also left. These matters are critical to resolve and Component 3 will specifically address the capacity building needs of the core IFMIS team. The Government also needs to consider a retention strategy for key IFMIS staff, possibly through performance contract appointments which could allow for market related remuneration.

c) Inadequate ICT infrastructure: A lack of investment in system maintenance and basic failures to maintain support agreements led to the infrastructure issues that crippled the IFMIS. The operation will invest to resolve current server, network and related issues. It will also invest in setting up the required infrastructure for the upgrade of the existing IFMIS software. In addition risks and costs of end-user equipment, and its future maintenance, will be lowered through the deployment of network computers, rather than full PCs. This will be supported through Component 2.

d) Institutional / organizational resistance: Resistance reared its head upon the failed go-live on 1 April 2009. The lack of investment in training, change management, support systems - such as the help desk and core IFMIS team - as well as in maintenance of the infrastructure, has further fuelled the resistance to near resentment. The basics have to be fixed in order to address the resistance. This project has at its core the resolution of the basic configuration and technical problems that have occurred, coupled with significant investment in capacity and change management. All components will assist to address this particular issue. In addition, change management will be proactively be provided to all stakeholders in order to clarify the benefits of the stable, upgraded and expanded IFMIS. Capacity building will be provided to the Office of the Accountant-General to monitor line ministries that continue to originate transactions outside of the IFMIS, in order to address such loopholes and provide the necessary capacity building and incentives to ensure as extensive use as possible of the IFMIS for financial control, accounting and reporting. Continued non-compliance will be sanctioned in terms of the regulatory framework. Incentives such as more flexible budget execution parameters will also be explored with GoL as part of the BPR activities.

11 Financial Management Information Systems - 25 Years of World Bank Experience on What Works and What Doesn’t, Cem Dener, Joanna Alexandra Watkins and William L Dorotinskty, World Bank, Washington DC, April 2011

17

e) Lack of business process reengineering to align with the IFMIS: Key business processes (especially for payment processing, receipting and reconciliations) were not simplified and aligned to the IFMIS functionalities. Other PFM functions (e.g. budget preparation & asset management) are still performed manually or through parallel systems in line ministries and district sub-accountancies. Good practice accounting disciplines, such as month-end closures and bank reconciliations, are also not yet fully functional. These are all addressed with technical design and implementation assistance through Component 1 and 2, and Component 3 will supply the necessary change management and training.

IV. IMPLEMENTATION

A: INSTITUTIONAL AND IMPLEMENTATION ARRANGEMENTS

47. The GoL implementation arrangements for the PFMRAP consist of two tiers, as follows - (i) an oversight/steering committee as the top tier (the IRSC); (ii) a reform technical committee (RTC) as the second tier, consisting of Component Leaders (CLs) and their support teams who will be involved in delivering the necessary outputs. A central PFM Reform Secretariat will provide overall monitoring, coordination and support for the implementation of the PFMRAP by the CLs. 48. The IRSC has been reconstituted12 under authority of the Minister of Finance as the oversight/steering committee for the implementation of the PFMRAP. Its membership include - PFM Development Partners; Chairperson of the Parliamentary Public Accounts Committee; Ministry of Public Service; Representatives from key Line Ministries, Departments and Agencies (Education, Health, Agriculture, Local Government, etc.); Component Leaders; and a PFM Reform Coordinator, who will serve as the IRSC Secretariat. It will meet under chairmanship of the Minister of Finance at least three times a year with the purpose to drive the reform process; inform the relevant partners and raise support for the reform; and decide on critical conceptual issues and recommendations related to the reform. 49. The day-to-day PFMRAP activities will be supported / coordinated by a PFM Reform Technical Committee (RTC), which comprise of all Component Leaders. It will be chaired by the Principal Secretary, Ministry of Finance, with the support of the PFM Reform Secretariat. 50. The MoF, through the Accountant-General as Component Leader, and the Deputy Accountant-General (Cash Management) as Sub-component leader, will be the executing agency for this operation. A new Accountant-General has been announced at the High Level PFM Workshop hosted by the Minister of Finance on 11 November, 2013. He is expected to assume position in January 2014. The core IFMIS team, under the leadership of the Deputy Accountant-General (Cash Management), will be responsible for implementation and coordinating of all project activities.

12 High Level PFM Workshop, 11 November 2013

18

B: RESULTS MONITORING AND EVALUATION

51. The Monitoring and Evaluations (M&E) framework will be a key instrument for tracking progress towards the achievement of the project’s development objective and providing reports on performance including potential bottlenecks as they emerge. The M&E framework presented in Annex 1 captures the high and medium level results that are expected to be achieved during the life of the PFMRS project. A mid-term evaluation (informed by a PEFA PFM Performance Assessment to be funded by the AfDB13) will be carried out during 2015 to ensure that the project is on track. The evaluation will serve as a basis for examining progress on expected project outcomes and will recommend actions needed to address implementation challenges. A final PEFA evaluation of the project will be carried in 2017.

C: SUSTAINABILITY

52. Establishing an equitable balance between delivering tangible project outcomes and establishing sustainable capacity in a low capacity environment such as Lesotho, is a challenging exercise. Nevertheless, the underlying rationale deployed in the design of the project is consistent with the cardinal requirement for ensuring the presence of in-built sustainability of project outcomes with regard to the influence of local political economy considerations. The proposed project will further develop and nurture the basic capacity in financial management through a more rigorous implementation and strategic deployment of resources in priority areas. This approach will not only reinforce the requisite skills needed for a strong PFM foundation, but would also minimize roll-backs in the core PFM reform arena supported under the project. Systematic training of staff responsible for implementing the core financial management functions within Government, while ensuring the introduction of more robust and modern systems and tools, will provide a sound basis for ensuring that capacity is retained after the project closure. Equally, leveraging development policy operations to introduce policy and institutional actions that will create the political and executive environment necessary for the implementation of project actions will be a considered option during implementation. This will help to secure policy and institutional changes supportive of critical implementation successes impacting such areas as financial reporting and fiscal discipline.

53. The project envisages the use of technical assistance to support the development of on-the-job capacity of IFMIS beneficiaries. This will ensure that skills and competencies developed in the implementation of the IFMIS are sustainable. The implementation of the initial IFMIS, to some extent, has led to foundational skills and capacity especially in the areas of application support and database management. Therefore, skills development under this project is not expected to start from ground zero but will rather focus on deepening, expanding and enhancing. Complementary capacity building activities are supported by a number of development partners including the AfDB, EU, and the IMF.

13 Institutional Support for the Enhancement of Public Financial Management (ISEP) Project Appraisal Report, African Development Bank, 14 October 2013

19

54. The proposed project also makes provision for the establishment of a coherent maintenance and support organizational structure that caters to both the technical and functional aspects of systems maintenance and support during project implementation and after project closure. This is reflected in the site preparation and support, applications, and training team that constitute the backbone for the IFMIS implementation. These teams – as part of the functional and technical infrastructure - will ensure the sustainable maintenance and upkeep of the systems at participating MDA level.

55. In terms of the recurrent cost for implementation of the reforms, post project closure, the GoL is already funding, and will continue to fund the required infrastructure, software licenses and maintenance costs, staff to operate and support the IFMIS, and other related operations costs.

V. KEY RISKS AND MITIGATION MEASURES

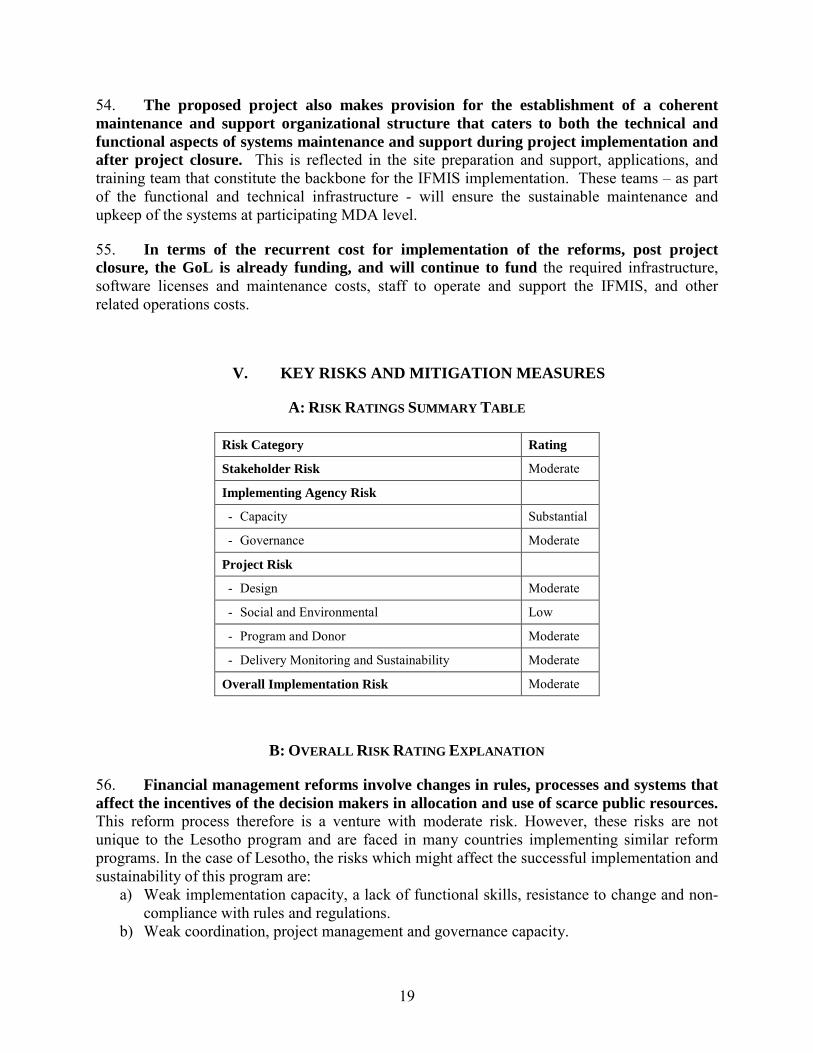

A: RISK RATINGS SUMMARY TABLE

Risk Category Rating

Stakeholder Risk Moderate

Implementing Agency Risk

- Capacity Substantial

- Governance Moderate

Project Risk

- Design Moderate

- Social and Environmental Low

- Program and Donor Moderate

- Delivery Monitoring and Sustainability Moderate

Overall Implementation Risk Moderate

B: OVERALL RISK RATING EXPLANATION

56. Financial management reforms involve changes in rules, processes and systems that affect the incentives of the decision makers in allocation and use of scarce public resources. This reform process therefore is a venture with moderate risk. However, these risks are not unique to the Lesotho program and are faced in many countries implementing similar reform programs. In the case of Lesotho, the risks which might affect the successful implementation and sustainability of this program are:

a) Weak implementation capacity, a lack of functional skills, resistance to change and non-compliance with rules and regulations.

b) Weak coordination, project management and governance capacity.

20

c) Weak ownership and resistance to implement the key architecture and process changes. d) Retention of trained staff.

C: KEY MITIGATION MEASURES

57. The project design addresses key technology, architecture and process issues that have severely constrained the effective running of the IFMIS, given the available skills and capacity. GoL is in agreement with the technology, architecture and process changes embedded in the project design. The design further includes extensive implementation support, and investment in training and change management. The project management and governance structures will further ensure adequate risk management. 58. A High Level PFM Workshop was hosted by the Minister of Finance on 11 November, 2013, with representation from members of Parliament (specifically the chairperson of the Public Accounts Committee); several Ministers (including Finance, Development Planning, Health, Education and Social Development); Development Partners (DPs, including the IMF, EU, AfdB and UNDP); several Principal Secretaries, Component Leaders for the PFM Reform Action Plan (PFMRAP), and other key staff involved in its implementation. The GoL provided an overview of the PFMRAP, and confirmed the implementation arrangements as detailed in Annex 3. The workshop concluded with overwhelming support for its implementation and appreciation to the DPs for their support.

59. As part of the PFMRAP the GoL also aims to implement an accounting cadre reform, which aims to address systemic issues related to attraction and retention of staff.

VI. APPRAISAL SUMMARY

A: ECONOMIC AND FINANCIAL ANALYSIS