Embed Size (px)

Citation preview

1

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

ACKNOWLEDGEMENTS

The journey to complete my thesis was both trying and fulfilling, I would not have

made it this far without the love and support from my family, lecturers and friends.

First and foremost, I would like to express my immense gratitude to my supervisor,

Professor Dominic Gasbarro. His tireless guidance, constructive suggestions and advice had

inspired me to strive for the best. Without his inexhaustible patience and guidance, this thesis

would not have been possible to accomplish. Under his abounding guidance, I have also

acquired new skills and insights, not only in academic studies but vigour in life.

Next, this valuable opportunity I have today, I owe to Professor Andrew Taggart. I am

very grateful to be awarded the Vice Chancellor’s SG50 Honours Scholarship. This award

has granted me a valuable opportunity to further my education abroad.

In addition, I would like to sincerely thank Mr Stephen Klomp for his hospitality and

kind guidance during my stay in Perth. I would also like to thank my lecturers, Dr Amy

Huang, Miss Thanesvary Subraamanniam and Miss Michelle Gander for their patience and

guidance throughout my units.

Last but not least, to my cherished family, I am deeply thankful and appreciative of

their boundless love, unwavering support and encouragement throughout this journey.

2

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

ABSTRACT

Past research primarily focus on evaluating market timing abilities using the returns

and stockholdings of mutual funds. We examine the market timing abilities of fund managers

using the trade proportions of mutual funds. These are statistically significant trade

proportions that encompass beta, sentiment beta and momentum. Trade proportions provide

insights on the direction that the fund manager was pursuing. Market and systemic risk

indicators are important for our study as they reflect the overall performance of the market

and the economy. We compare between the values of these indicators and the values of our

statistically significant trade proportions to evaluate if these values are highly correlated

during various market cycles. Using correlation and regression analysis, we examine the

relation between the trade proportions (dependent variable), the market and systemic risk

indicators (independent variables). We have also taken into consideration of certain

conditions that might affect the adjustments of these trade proportions and conducted some

preliminary and robust tests. In general, we expect that prior to a bull (bear) market, fund

managers will adjust their portfolios towards positive (negative) trade proportions.

Furthermore, majority of past studies had evaluated market timing abilities only during

recession periods therefore our study period between 1991 and 2012 has incorporated both

recession and boom periods to avoid biasness in results. However, similar to previous

findings, these trade proportions did not demonstrate superior market timing abilities.

Although no significant market timing abilities were exhibited, momentum trade proportions

displayed the most significant correlation and regression results. We observed an inverse

relationship between the positive momentum trade proportions and the momentum index.

This is consistent with fund managers having pursued a contrarian strategy.

3

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

CONTENTS

ACKNOWLEGDEMENTS 1

ABSTRACT 2

CONTENTS 3-7

FIGURES 8

GRAPHS 9

TABLES 10

1 INTRODUCTION 13-18

1.1 Introduction 13-18

2 LITERATURE REVIEW 19-60

2.1 Introduction 19

2.2 Overview of Literature 19-21

2.3 Characteristics of Mutual Funds 21-22

2.4 Mutual Fund Performance- Market Timing 22-23

2.4.1 Timing using Convex Relationship between Fund Returns and

Market Returns

23-25

2.4.2 Stationary Beta versus Non-Stationary Beta in Bull and Bear Markets 25-34

2.4.3 Evaluating Market Timing Abilities simultaneously with Security

Section Abilities

34-37

2.4.4 Free from Beta Estimates 37-39

2.4.5 Portfolio Performance Measures without Benchmarks 39-41

2.4.6 Volatility Timing 41-42

2.4.7 Downside of Returns Chasing Behaviour 43-44

2.4.8 Persistence in Fund Performance 44-46

2.4.9 Business Cycles and Predictability Skills 46-47

2.4.10 Stockholdings versus Trades 47-53

2.4.10.1 Market Timing Abilities 48-51

2.4.10.2 Stock Selection Abilities 51-54

2.4.11 Downside of Risk Shifting Behaviour 54-55

4

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

2.4.12 Successful Market Timing Abilities 56-57

2.5 Overview of Contrarian Strategies 57-58

2.5.1 Identifying Contrarian Strategies in Mutual Fund Trades 59

2.6 Conclusion of Literature Review and Motivation of Present Study 59-60

3 METHODOLOGY 61-79

3.1 Introduction 61

3.2 Overview of Methodology 61-63

3.3 Data Description 63

3.3.1 Bull and Bear Markets 63-64

3.3.2 Recession and Boom Periods 64-66

3.3.3 Four States of Bull and Bear Markets 66-68

3.4 Trades 68

3.4.1 Identifying Market Timing Trades 68

3.4.1.1 Formula for Identifying Market Timing Trades 68-69

3.4.2 Identifying Sentiment Beta Timing Trades 69

3.4.3 Identifying Momentum (Contrarian) Trades 69-70

3.5 Importance of Indices 70-71

3.5.1 Description of Indices 72-74

3.5.1.1 The S&P 500 Index 72

3.5.1.2 The Baker & Wurgler’s Sentiment Index 72

3.5.1.3 The S&P 500 Momentum Index 73

3.5.1.4 The S&P 500 Quality Index 73

3.5.1.5 The S&P 500 Growth Index 73-74

3.5.1.6 The S&P 500 Low Volatility Index 74

3.5.1.7 The S&P 500 High Beta Index 74

3.5.2 Systemic Risk Measures 74-77

3.5.2.1 Brief Description of Systemic Risk Measures (19 Elements) 75-77

3.6 Sources of Data and Availability 78

5

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

3.7 Trades’ Correlation with Indices 78-79

3.8 Conclusion of Methodology 79

4 RESULTS AND DISCUSSION 80-133

4.1 Introduction 80

4.2 Overview of Results and Discussion 80-83

4.2.1 Market Indicators 81

4.2.2 Systemic Risk Indicators 81-82

4.2.3 Overview of Analysis (Schematic Diagram) 82-83

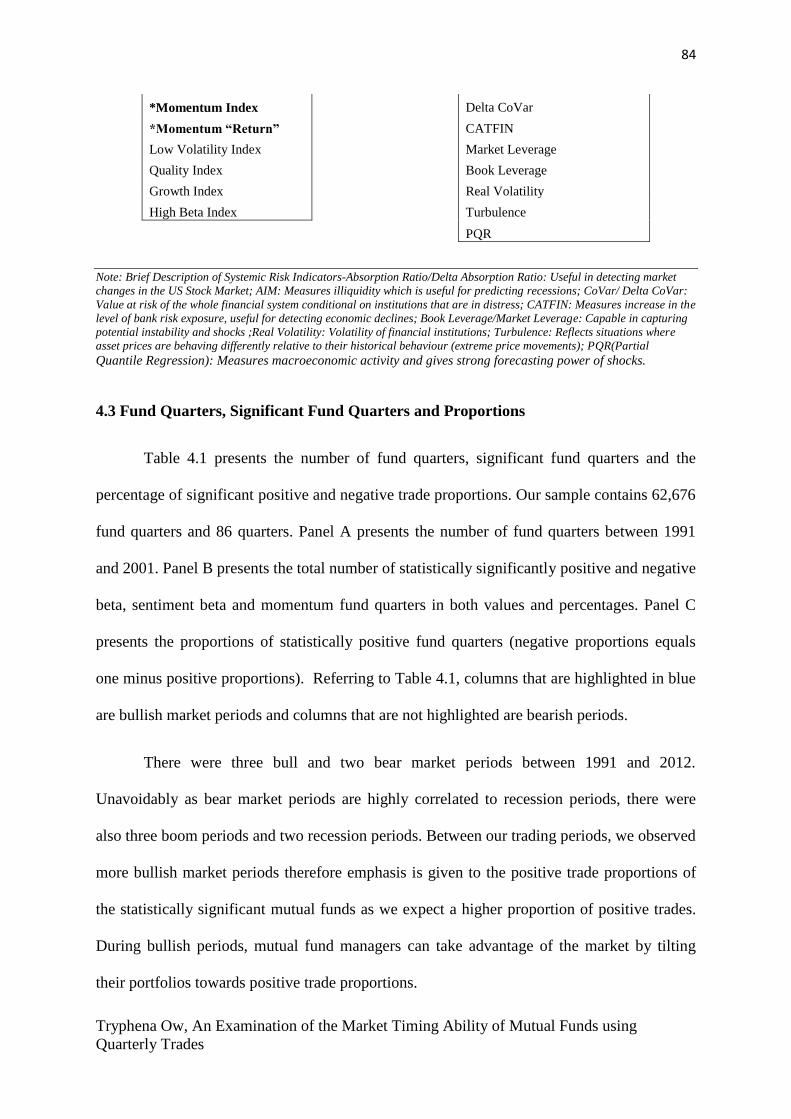

4.3 Fund Quarters, Significant Fund Quarters and Proportions 83-85

4.3.1 Descriptive Statistics of Significant Fund Quarters and Proportions 86-87

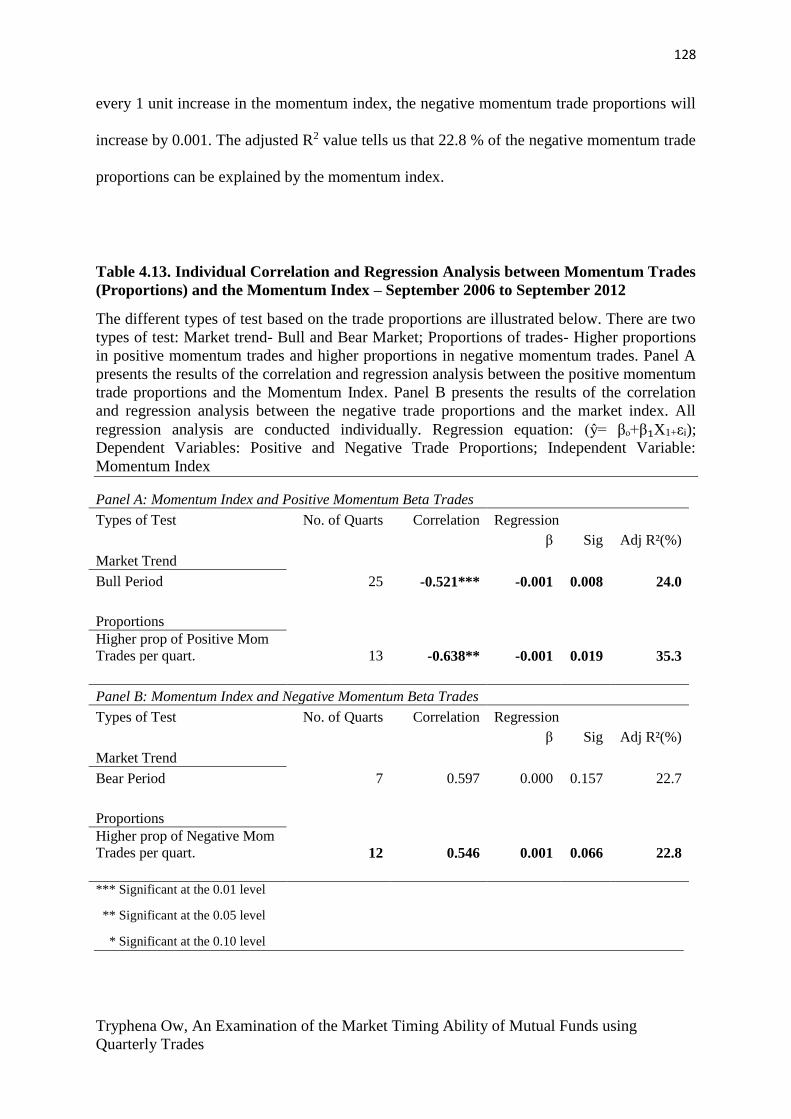

4.4 Descriptive Statistics of Market and Systemic Risk Indicators 87-91

4.4.1 Descriptive Statistics (In Months) 87-90

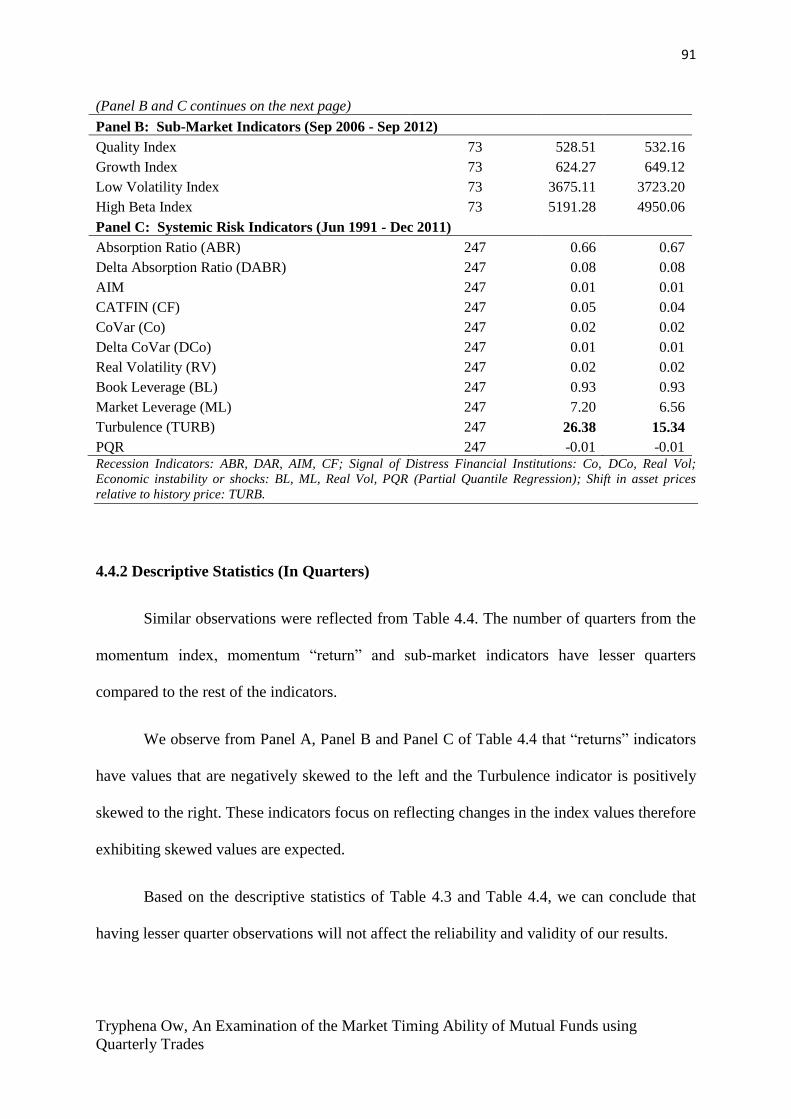

4.4.2 Descriptive Statistics (In Quarters) 90-91

4.5 Performance of Market Indicators 92-99

4.6 Correlation Testing 99

4.6.1 Correlation Testing between Market Indicators (Main Market

Indicators and Sub-Market Indicators)

100-102

4.6.2 Correlation Testing between Systemic Risk Indicators 102

4.6.2.1 Brief Description of the Selected Systemic Risk Indicators 102-107

4.7 Final Selection of Market and Systemic Risk Indicators 107-109

4.8 Correlation and Regression Analysis between Trade Proportions

(DV) and Indicators (IV)

109-111

4.9 Overall Test for Correlation and Regression Analysis 111-117

4.10 Preliminary Test 117-129

4.10.1 Market Beta Trade Proportions 118-121

4.10.1.1 Market Index 118-119

4.10.1.2 Market “Return” Indicator 119-121

4.10.2 Sentiment Beta Trade Proportions 121-124

4.10.2.1 Sentiment Index 121-122

6

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

4.10.2.2 Sentiment “Return” Indicator 122-124

4.10.3 Momentum Trade Proportions 125-128

4.10.3.1 Momentum Index 125-127

4.10.3.2 Momentum “Return” Indicator 127-129

4.11 Summary Table of Significant Results based on Overall Analysis

and Preliminary Tests

130

4.12 Conclusion of Results and Discussion 131-133

5 ROBUST TESTING 134-164

5.1 Introduction 134

5.2 Overview of Robust Testing 134-137

5.3 Beta Trade Proportions and the Market “Return” Indicator 137-140

5.3.1 Test (1): Magnitude of Change 137-138

5.3.2 Test (2): Changes in Standard Deviation 138-139

5.3.3 Test (3): Changes in Signs 139

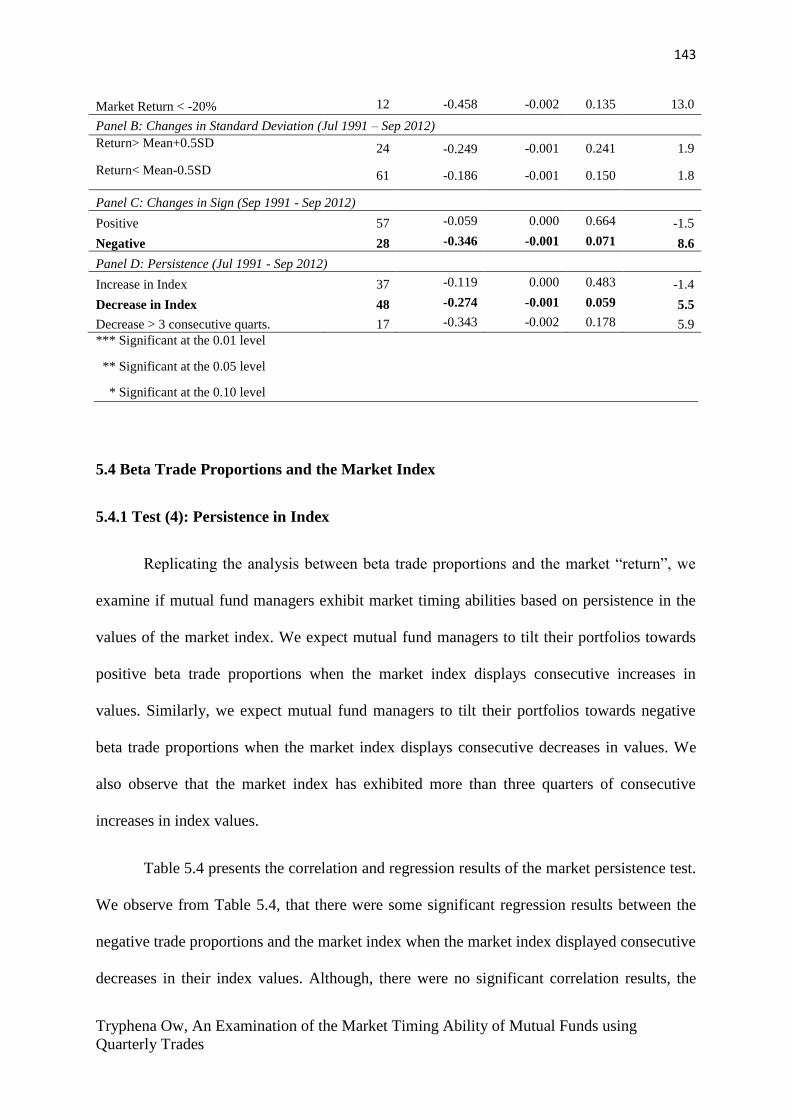

5.3.4 Test (4): Persistence in Index 139-140

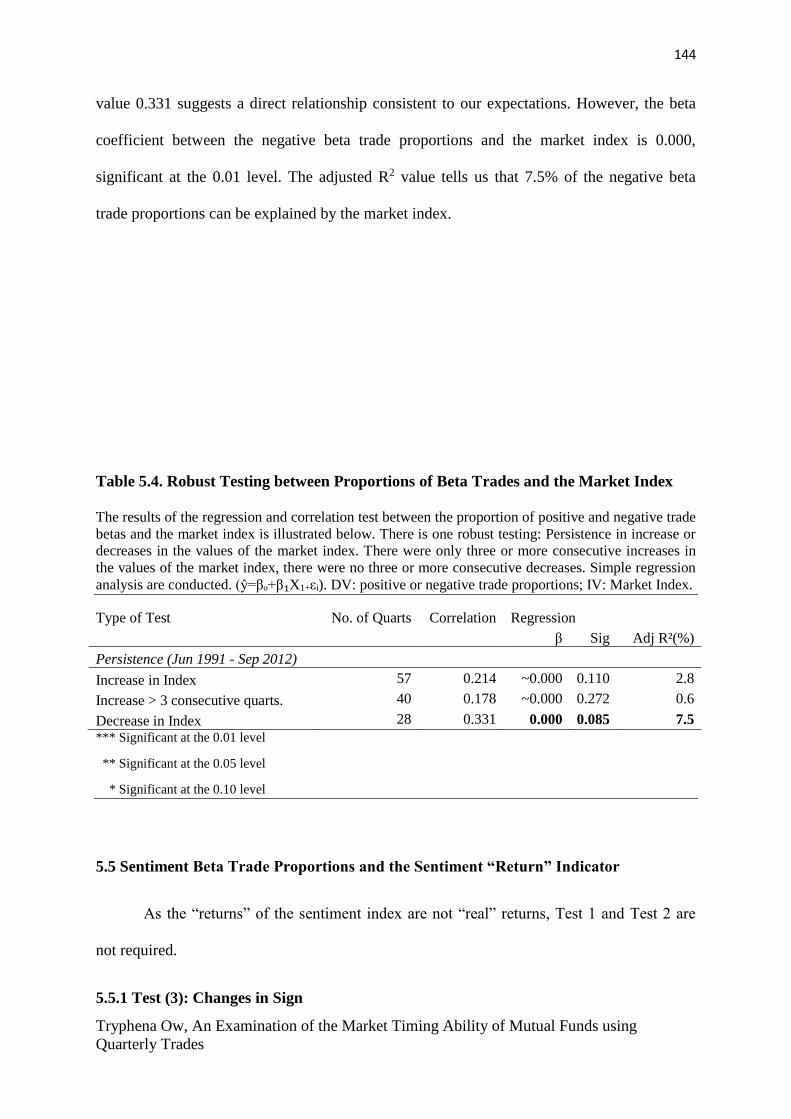

5.4 Beta Trade Proportions and the Market Index 142-143

5.4.2 Test (4): Persistence in Index 142

5.5 Sentiment Beta and the Sentiment “Return” Indicator 143-146

5.5.1 Test (3): Changes in Signs 143

5.5.2 Test (4): Persistence in Index 144

5.6 Sentiment Beta and the Sentiment Index 146-147

5.6.1 Test (3): Changes in Signs 145-146

5.6.2 Test (4): Persistence in Index 146

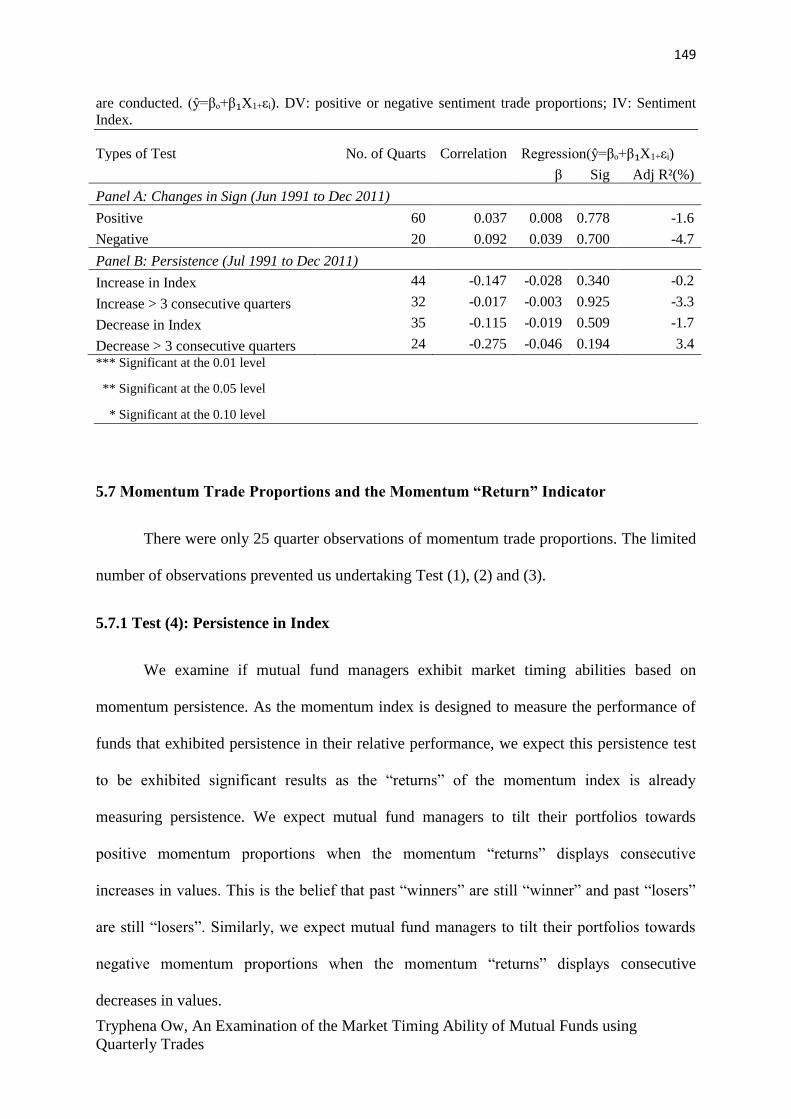

5.7 Momentum Trade Proportions and the Momentum “Return”

Indicator

148-149

5.7.1 Test (4): Persistence in Index 148

5.8 Momentum Trade Proportions and the Momentum Index 149-151

5.8.1 Test (4): Persistence in Index 149

5.9 Multiple Regression Analysis 151-160

7

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

5.9.1 Market Beta 151-54

5.9.1.1 Positive Market Beta Proportions with the Market “Return”

Indicator

151-153

5.9.1.2 Positive Market Beta Proportions with the Market Index 153-154

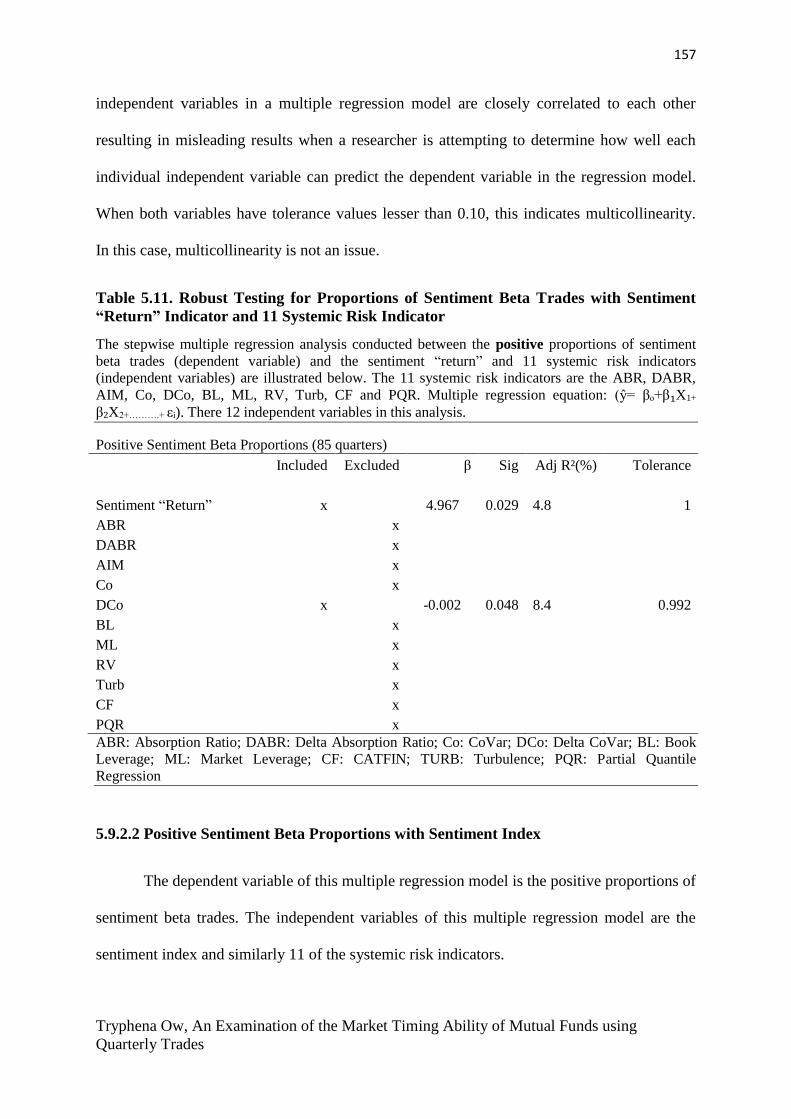

5.8.2 Sentiment Beta 154-157

5.9.2.1 Positive Sentiment Beta Proportions with the Sentiment “Return”

Indicator

154-156

5.9.2.2 Positive Sentiment Beta Proportions with the Sentiment Index

Indicator

156-157

5.9.3 Momentum Trades 157-160

5.9.3.1 Positive Momentum Proportions with the Momentum “Return”

Indicator

157-159

5.9.3.2 Positive Momentum Proportions with the Momentum Index 159-160

5.10 Summary Table of Significant Results based on Robust and

Multiple Regression Tests

161

5.11 Conclusion of Robust Testing 162-164

6 CONCLUSION 165-79

6.1 Introduction 165

6.2 Overview of Conclusion 165-167

6.3 Significant Research Findings 167-168

6.4 Limitations of the Research 168

6.6 Areas of Future Research 169-170

6.6 Summary of Study 170-171

REFERENCES 169-179

8

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

FIGURES

Figure 1.1: Schematic Diagram: Overview of Methodology 18

Figure 2.1: The Characteristic Line of a Fund that Outguess the Market (Treynor

and Mazuy, 1966)

23

Figure 3.1: Schematic Diagram: Overview of Methodology

62

Figure 4.1: Trades, Market Indicators and Systemic Risk Indicators

83

Figure 4.2: Final Selection of Indicators for Analysis

108

Figure 4.3: Statistically Significant Trades and their Respective Indicators

109

Figure 5.1: Types of Robust Test Conducted

136

9

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

GRAPHS

Graph 4.1: Price Fluctuations of the Market Index, June 1991 to September 2012 92

Graph 4.2: Price Fluctuations of Market “Return” Indicator, July 1991 to

September 2012 93

Graph 4.3: Changes in the Sentiment Index Values, June 1991 to March 2011 95

Graph 4.4: Changes in the Values of the Sentiment “Return” Indicator, July 1991

to March 2011 96

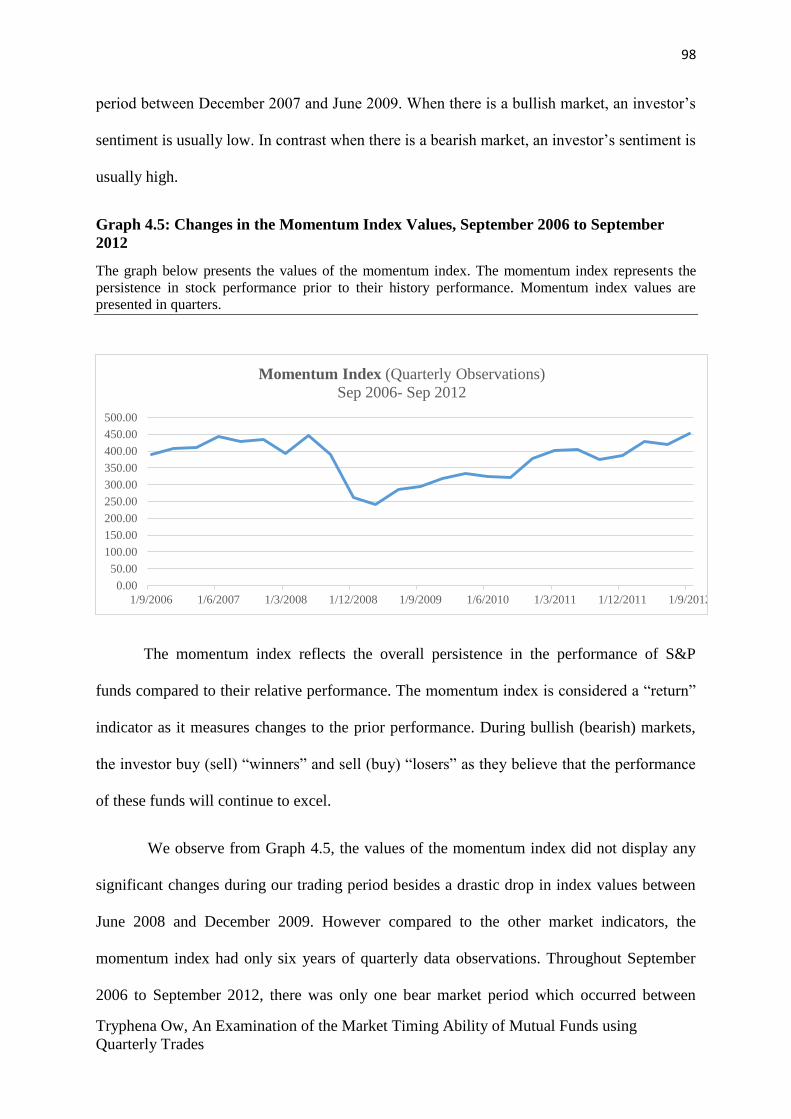

Graph 4.5: Changes in the Momentum Index Values, September 2006 to

September 2012 97

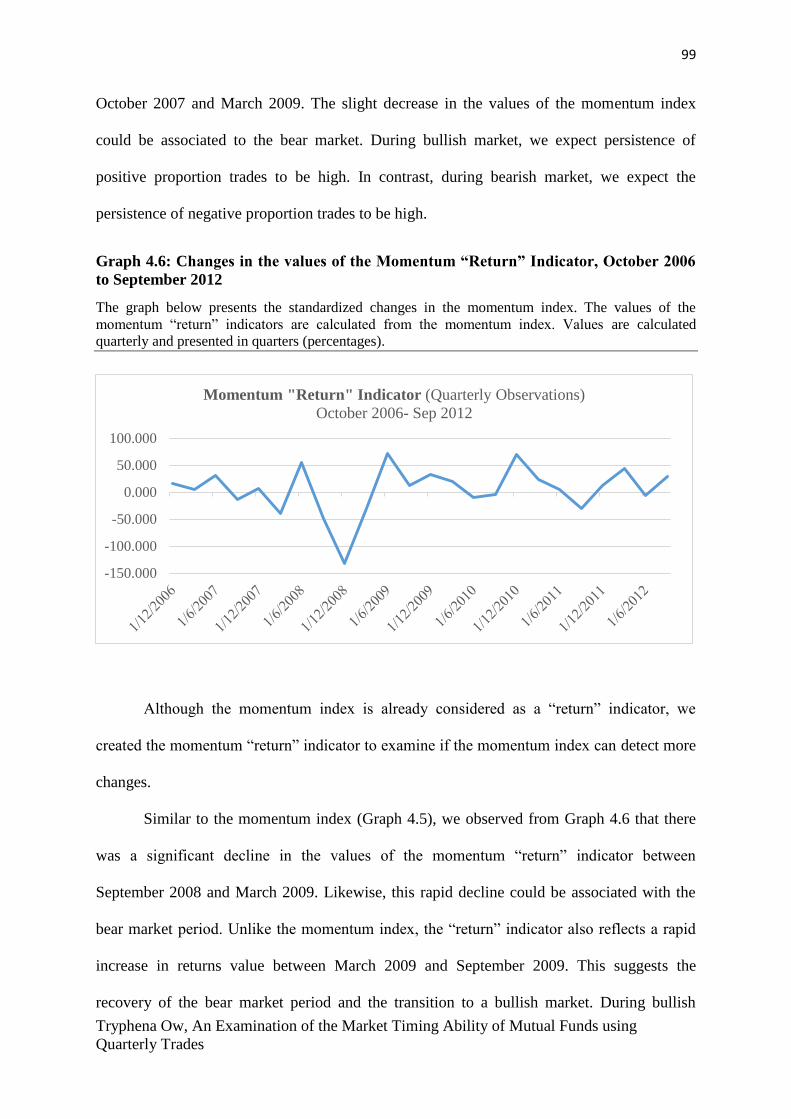

Graph 4.6: Changes in the Values of the Momentum “Return” Indicator, October

2006 to September 2012

98

10

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

TABLES

Table 3.1: Bull and Bear Market Durations throughout the Trading Period

between July 1991 and October 2012

63

Table 3.2: Recession and Boom Durations throughout the Trading Period

between July 1991 and October 2012

65

Table 3.3: Data Sources, Availability and Types of Data

78

Table 4.1: Trades- Number of Fund Quarters, Significant Fund Quarters and

Proportions

85

Table 4.2: Descriptive Statistics of Statistically Significant Fund Quarters and

Proportions

86-87

Table 4.3: Descriptive Statistics of Market and Systemic Risk Indicators

(Presented in Months)

89-90

Table 4.4: Descriptive Statistics of Market and Systemic Risk Indicators

(Presented in Quarters)

91

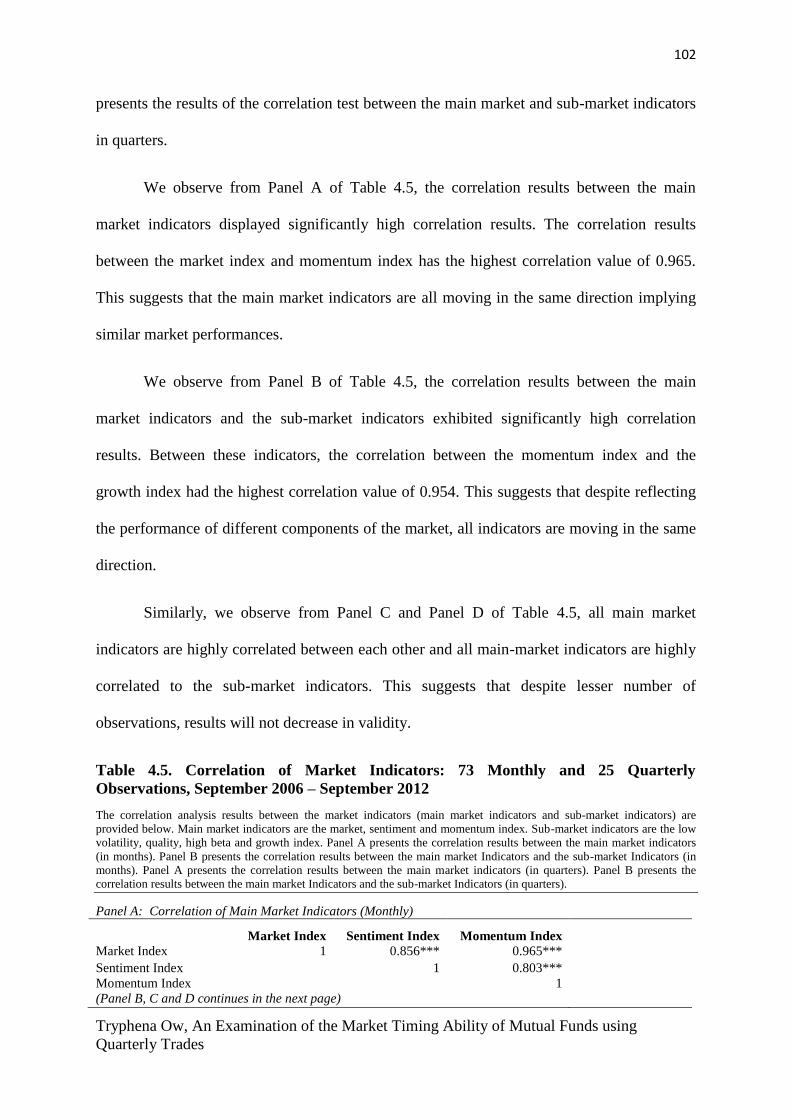

Table 4.5: Correlation of Market Indicators: 73 Monthly and 25 Quarterly

Observations, September 2006 – September 2012

101-102

Table 4.6: Correlation between Systemic Risk Indicators: 247 Monthly

Observations and 83 Quarterly Observations, June 1991 to

December 2011

104-105

Table 4.7: Significant (at 0.01 Level) Results of Positive and Negative

Correlations between the Selected Systemic Risk Indicators: 83

Quarterly Observations, June 1991 to December 2011

106-107

Table 4.8: Overall Correlation and Regression between Trade Proportions and

Indicators

115-117

Table 4.9: Individual Correlation and Regression Analysis between Market

Beta Trades (Proportions) and the Market Index – June 1991 to

September 2012

118-119

Table 4.10: Individual Correlation and Regression Analysis between Market

Beta Trades (Proportions) and the Market “Return” Indicator – July

1991 to September 2012

120-121

Table 4.11: Individual Correlation and Regression Analysis between Sentiment

Beta Trades (Proportions) and the Sentiment Index– June 1991 to

March 2011

122

11

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

Table 4.12: Individual Correlation and Regression Analysis between Sentiment

Beta Trades (Proportions) and the Sentiment “Return” Indicator–

July 1991 to March 2011

124

Table 4.13: Individual Correlation and Regression Analysis between

Momentum Trades (Proportions) and the Momentum Index –

September 2006 to September 2012

127

Table 4.14: Individual Correlation and Regression Analysis between

Momentum Trades (Proportions) and the Momentum “Return”

Indicator – October 2006 to September 2012

129

Table 4.15: Significant Results based on Overall Analysis and Preliminary Tests

130

Table 5.1: Number of Quarters in relation to Market “Returns”- July 1991 to

September 2012

138

Table 5.2: Empirical Rule for Normally Distributed Data

139

Table 5.3: Robust Testing between Proportions of Beta Trades based and the

Market “Return” Indicator

141

Table 5.4: Robust Testing between Proportions of Beta Trades and the Market

Index

143

Table 5.5: Robust Testing between Proportions of Sentiment Beta Trades and

the Sentiment “Return” Indicator

145-146

Table 5.6: Robust Testing between Proportions of Sentiment Beta Trades and

Sentiment Index

147

Table 5.7: Robust Testing between Proportions of Momentum Trades and the

Momentum “Return” Indicator

149

Table 5.8: Robust Testing between Proportions of Momentum Trades and the

Momentum Index

150

Table 5.9: Robust Testing for Proportions of Beta Trades with the Market

“Return” Indicator and 11 Systemic Risk Indicator

152-153

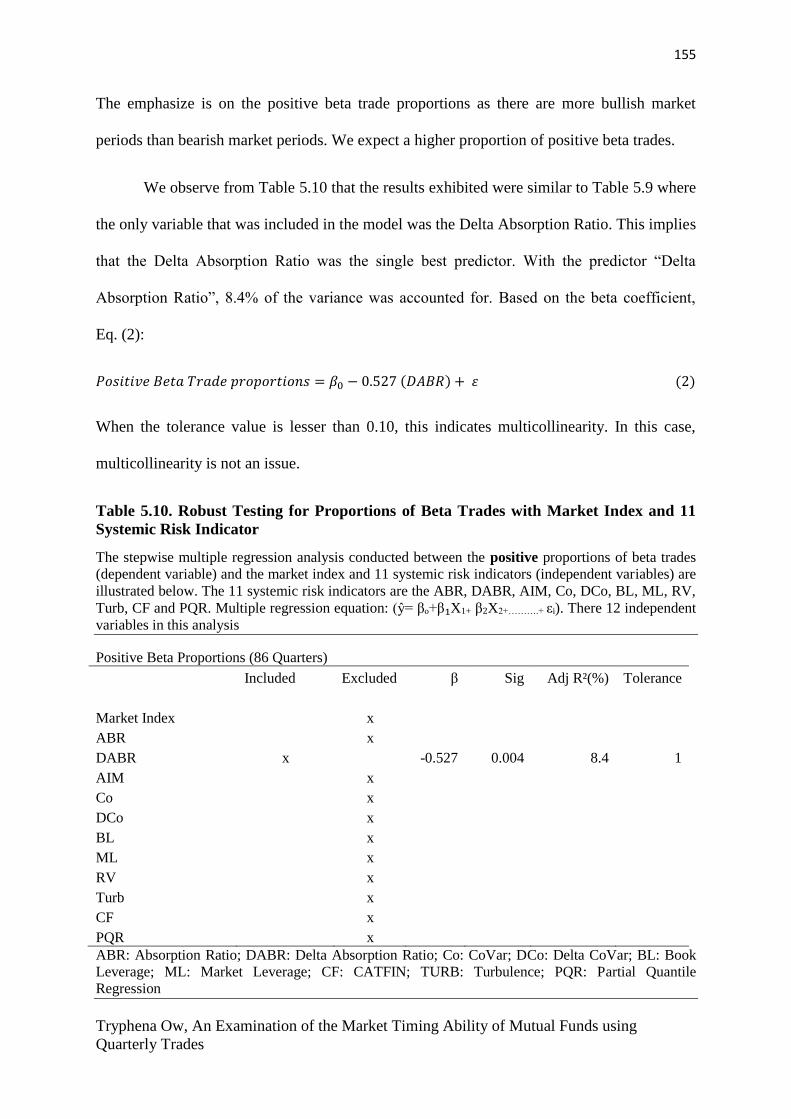

Table 5.10: Robust Testing for Proportions of Beta Trades with the Market

Index and 11 Systemic Risk Indicator

154

Table 5.11: Robust Testing for Proportions of Sentiment Beta Trades with the

Sentiment “Return” Indicator and 11 Systemic Risk Indicator

155-156

12

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

Table 5.12: Robust Testing for Proportions of Sentiment Beta Trades with the

Sentiment Index and 11 Systemic Risk Indicator

157

Table 5.13: Robust Testing for Proportions of Momentum Trades with the

Momentum “Return” Indicator and 11 Systemic Risk Indicator

158-159

Table 5.14: Robust Testing for Proportions of Momentum Trades with the

Sentiment Index and 11 Systemic Risk Indicator

160

Table 5.15: Significant Results based on Robust and Multiple Regression Tests

161

13

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

CHAPTER 1

INTRODUCTION

1.1 Introduction

The performance measures for market timing abilities of fund managers has been a

predominant topic. Market timing is the ability of fund managers to tilt their portfolios in

accordance to the anticipated market trends to exploit returns. Common market trends are the

bullish and bearish markets. During bullish markets, fund managers can take advantage of the

market by buying high beta stocks and selling low beta stocks. In contrast, during bearish

markets, fund managers can take advantage of the market by buying low beta stocks and

selling high beta stocks.

In relation to predictability skills, fund managers can monitor the performance of the

market with the assistance of market indicators as they reflect the market movements. If the

index level of the S&P 500 market index consistently increases (decreases), we can anticipate

a bullish (bearish) market. However, market timing can also be a form of risk as the cost of

adjusting a portfolio may not be justified for the gains in return. Furthermore, portfolio tiling

may not necessarily suggest that fund managers are taking advantage of fluctuating

investment opportunities but a signal of ill motivated trades from mediocre abilities of fund

managers or agency issues (Huang, Sialm and Zhang, 2011). There is also a possibility of

mistiming which exposes funds to underperformance by selling (buying) stocks with high

(low) betas before a bullish (bearish) market period.

Early studies identified market timing abilities by evaluating the returns of mutual

funds. Treynor and Mazuy (1966) studied the returns of mutual funds on their historical

success of forecasting variations in the stock market. They reported that the fund returns and

the market returns had a convex relationship. Successful market timers would increase their

14

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

exposure to the market during bullish markets and decrease their exposure during bearish

markets. However, they did not consider how the systematic risk which is measured by beta

could vary in bullish and bearish markets. Subsequently, researchers incorporated the use of a

non-stationarity beta to evaluate market timing abilities of fund managers (Fabozzi and

Francis, 1979; Kim and Zumwalt, 1979; Miller and Gressis, 1980; Chen, 1982). A non-

stationary beta gives allowance for the increase in risk exposure. However, there were still no

significant evidence of market timing abilities.

Attention has been shifted to the evaluation of the performance of stockholdings and

trades to examine the predictive abilities of fund managers. Jiang, Yao and Yu (2007) found

positive market timing abilities when quarterly portfolio holdings were applied to a single

index model. However, Elton Gruber and Blake (2012) re-examined their study and argued

that using quarterly portfolio holdings may have resulted in an inaccurate conclusion of

market timing abilities as a vast number of trades were not captured in their analysis. In

addition, when monthly portfolio holdings were applied to a two index model, market timing

abilities were non-existence.

Comparing the use between stockholdings and trades, Chen, Jegadeesh and Wermers

(2000) reported that active stock trades represents a stronger opinion of a manager as

compared to a “passive” stockholding. Although no evidence of predictive abilities, Chen,

Jegadeesh and Wermers (2000) and Baker, Litov, Wachter and Wurgler (2010) found that

trade buys outperformed the trades they sell.

Using a different approach, researchers have also evaluated market timing abilities

simultaneously with stock selection abilities. Similar studies by Chang and Lewellen (1984)

and Chen and Stockum (1986) evaluated market timing and stock selection skills at the same

time using mutual fund returns. Chang and Lewellen (1984) proposed that there is a

15

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

possibility that fund managers might exploit returns by engaging in effective “macro” market

timing activities as well as careful “micro” security selection efforts. However, there were no

evidence of market timing abilities. Following the same method, Kacperczyk, Niewerburgh

and Veldkamp (2014) also evaluated market timing and stock selection abilities

simultaneously. However they took into consideration of the changing economic trends like

the boom and recession periods. They conditioned the state of the economy and developed a

new method where more weightage is given to a fund manager’s market timing success

during recession periods and stock picking success during boom periods. Studying mutual

fund holdings, they found market timing abilities in both recession and boom periods.

We contribute to the literature in several ways. First, we examine the market timing

abilities of fund managers by evaluating their statistically significant trade proportions that

encompass beta, sentiment beta and momentum. Second, we investigate if fund manager

adjust their portfolios between positive and negative trade proportions in accordance to the

various market cycles. Unlike past researchers, we study the proportions of these trades as

they provide insights on the direction that a fund manager was pursuing. We expect a higher

proportion of positive trades when the market is bullish or in an expansion phase. In contrast,

we expect a higher proportion of negative trades when the market is bearish or undergoing a

recession period. Third, we show that although momentum trade proportions had the least

number of quarter observations, they exhibited the most significant results from our

correlation and regression analyses. We observed that positive momentum trade proportions

exhibited an inverse relationship with the momentum index during bullish market periods.

Although results were inconsistent to our expectations, an inverse relationship suggests that

the fund manager may have pursed a contrarian strategy.

To identify trades that are engaged in market timing in any calendar quarter, we

conducted correlation and regression analyses between the trade proportions and their related

16

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

market indicators. We apply these measures to mutual fund trade proportions from 1991 to

2012. We conduct an overall correlation and regression test between the trade proportions

and their respective indicators to appreciate the general direction of their relationship. Next,

we consider how bullish and bearish markets will affect the adjustments of trade proportions.

We expect that during bullish market periods, the positive trade proportions would exhibit a

direct relationship with the market indicators. Similarly, during bearish market periods, we

expect negative trade proportions to exhibit a direct relationship with the market indicators.

Finally, various robust tests were also conducted to investigate if fund managers were

selective with the adjustments of their portfolio proportions based on market persistence,

turning points of the market and we study how big and small changes in the market returns

will affect their portfolio adjustment decisions.

We observe the following results from the correlation and regression analyses. Based

on the results of overall correlation and regression analysis, we observe that the positive

sentiment and positive momentum trade proportions exhibited significant results. However,

both trade proportions had an inverse relationship with their respective indicators. There were

no significant results from the beta trade proportions. Second, when bullish and bearish

market conditions are considered, the most number of significant results were exhibited from

the sentiment and momentum trade proportions. We observe an inverse relationship between

these trade proportions and their respective indicators. Third, based on the results from the

robust tests, the most number of significant results were also from the sentiment and

momentum trade proportions. Likewise, inverse relationships were exhibited between these

trade proportions and their respective indicators. Overall, despite momentum trade

proportions having the least number of quarter observations, they displayed the most number

of significant relationships. It is plausible that these fund managers have adopted a contrarian

strategy. Similar to previous findings, there we no evidence of market timing abilities.

17

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

We consider some limitations of the study. Although the use of quarterly data

observations provides more time allowance for fund managers to form market expectations

and make right decisions in portfolio adjustments, these observations may not be able to

capture sufficient information of fund managers with higher trading frequencies. It is also

possible that the total number of quarter observations might have affected our results.

Therefore, we suggest some areas of future research. We consider evaluating a longer time

period that incorporates all four recession periods in future studies as research have shown

that predictability skills are best displayed during recession periods. We also suggest

evaluating market timing and stock selection skills simultaneously with regards to the

changes in the economic conditions using the trade proportions of mutual funds.

This paper is organized in the following manner. In Section 2.0, we discuss the

literature review. In Section 3.0, we discuss the data and provide an overview of the

methodology. In Section 4.0, we discuss and present our findings. In Section 5.0, we conduct

various robust tests. In Section 6.0, we conclude our study. An overview of our study’s

methodology is provided (Refer to Figure 1.1).

18

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

Figure 1.1 Schematic Diagram: Overview of Methodology

The figure below illustrates the overview of our methodology. Trade betas that encompass beta,

sentiment beta and momentum are provided by Cullen et al. (2015). Quarterly data observations of

trade proportions are used for the analysis.

Indices

Trade Betas

(Proportions)

(1991-2012)

Trades associated with

Market Beta

Trades associated with

Sentiment Beta

Trades associated with

Momentum

S&P500 Market Index

Baker & Wurgler’s Sentiment Index

S&P 500 Momentum Index

S&P 500 Quality Index

S&P 500 Growth Index

S&P 500 Low Volatility Index

S&P 500 High Beta Index

Systemic risk

measures

Market Trends

-Bull and Bear Markets

-Recession and Boom Periods

-Further break down of Bull and Bear Markets

with the consideration of Volatility

Quarterly

Convert Data

Correlated

Check with

Daily

Monthly

Quarterly

19

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

CHAPTER 2

LITERATURE REVIEW

2.1 Introduction

This chapter describes the background and presents the literature review for this

study. In section 2.2, we discuss the background of our study and review the literature on the

key areas which are the market timing abilities of mutual funds managers, the evolution

performance measures which involves the use of stationarity and non-stationarity beta and the

examination of stockholdings and trades of mutual funds. We also identify the purpose of our

research and provide an overview of our methodology. Our sample comprises mainly of

statistically significant trade betas that encompass beta, sentiment beta and momentum of US

equity mutual funds over the period 1991 to 2012 and the data are provided by Cullen et al.

(2015).

2.2 Overview of Literature

Millions of people have invested in a once obscure financial instrument, the mutual

fund. Investors have constantly compared the advantages between active trading and passive

trading strategies of mutual funds. Over the years, the evaluation of mutual fund

performance has been vital to ensure optimal investment allocation as well as the

development of a mutual fund manager’s reward structure. Nevertheless, performance

measures have been consistently challenged and subsequently refined. Measures of a mutual

fund’s performance includes stock selection, market and industry timing abilities. Stock

selection and market timing abilities are the most popular measures of performance where

stock selection is the ability to select undervalued securities and market timing is the ability

to adjust security holdings to anticipate the movements of the market.

20

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

Determining the market timing abilities of mutual fund managers have been the focal

point of research. Managers with market timing abilities can attempt to exploit returns using

two common strategies. They can either move in and out of the market or conduct a tactical

asset allocation between low and high beta stocks using predictive methods by monitoring the

performance of indicators like the S&P 500 Market Index to detect any changes in the market

trends. The early stages of determining market timing abilities was derived using a quadratic

term in the capital asset pricing model (CAPM). Subsequently, researchers had focused on

the stationarity and non-stationarity of beta in the bull and bear market. The increase

(decrease) of a non-stationarity fund’s beta allows the fund’s equity holdings to rebalance in

the anticipation of the expected bull (bear) market.

In order to avoid these benchmark issues, recent studies have concentrated on mutual

fund holdings and mutual fund trades. The intuition is that a fund with successful market

timing skills will hold more stocks that possess high beta in bull markets and conversely hold

predominately lower beta in bear markets. Similarly, a fund will purchase high beta stocks

and sell low beta stocks when the market is expected to rise and purchase low beta stocks and

sell high beta stocks when the market is expected to fall.

We contribute to the literature in several ways. First, we examine market timing

abilities of fund managers by evaluating the statistically significant trades that encompass

beta, sentiment beta and momentum. Trade proportions are used as they provide insights on

the direction that the fund manager is pursuing. Second, we consider both upmarket and

downmarket periods in our study. Third, using a new approach, we investigate if fund

managers make technical adjustments to their portfolios according to different market trends

based on market indices. During the bullish periods, we expect a higher proportions of

positive trades in a fund’s portfolio. On the other hand, during bearish markets, we expect a

higher proportions of negative trades in a fund’s portfolio. Market timing is significant when

21

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

we observe a positive significant relationship between the market indices and the statistically

significant trade proportions.

This paper is organized in the following manner: in Section 2.0, we discuss the

literature of our research. Section 3.0, we provide and discuss the data and overview of the

methodology. In Section 4.0 we discuss the results of our research. Section 5.0, we conduct

various robust test. Finally in Section 5, we conclude the study and discuss about the

limitations of our study and suggest areas of future research.

2.3 Characteristics of Mutual Funds

Generally, in comparison to larger investment companies, individual investors lack of

substantial wealth to invest in large variety of stocks, bonds and securities. Consequently,

these individual investors turned into risk averse investors. Russell (2007) explained that

individual investors usually lack of professional knowledge and experience to make the best

decisions for their portfolios. Also, due to time management issues and complicated

paperwork, investors often struggle to keep up to their portfolios.

By offering diversification and simplicity for individual investors, mutual funds are a

good solution to these problems as they are a collection form of investments (Russell, 2007).

These funds are open-end investment companies and they pool funds of individual investors

offering them professional management by investing in a variety of securities or other assets

(Russell (2007); Bodie, Kane and Marcus (2014)). Instead of owning individual stocks or

bonds, mutual fund investors owns a portion of shares in a mutual fund and these shares

represent a portion of the holdings of the funds (Investopedia, 2016). The common types of

mutual funds are the money market funds, equity funds, bond funds, hedge funds and index

funds (Bodie, Kane and Marcus, 2014).

22

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

Commonly used by sophisticated investors due to their numerous advantages, mutual

funds are also well known for their professional management of money (Investopedia, 2016).

As investors may lack time or expertise to manage their own portfolio, these funds offer

convenience and cost efficiency as they allow investors to have an inexpensive way to make

and monitor their investments (Investopedia, 2016). Bodie, Kane and Marcus (2004)

explained that as mutual funds includes a wide range of securities, this reduces portfolio risk

as any loss in a particular security can be minimised by the gains of others (Investopedia,

2016).

Mutual funds also offer lower transaction costs as they are usually purchased and sold

in large volumes of securities in bulk (Bodie, Kane and Marcus, 2004). Compared to

individual investors, these large scale investors are usually given a discounted trading cost.

Additionally, mutual funds are valuable for their liquidity advantages. Although they are a

collective form of investments, they allow shares to be converted into cash at any point of

time of request like an individual stock (Bodie, Kane and Marcus, 2004).

2.4 Mutual Fund Performance – Market Timing

In our study, market timing is the ability of a fund manager to adjust his or her

portfolio composition between high volatile stock and low volatile stocks based on using

predictive methods such as technical indicators like the market index. The market index

reflects the overall performance of the market and suggesting periods of bullish or bearish

market trends.

Fund managers that possess market timing abilities can generate superior returns by

adjusting their portfolios in accordance to the anticipated market trend. During bullish

(bearish) market periods, fund manager can adjust their portfolios towards high (low) volatile

23

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

stocks. In other words, during bullish (bearish) periods, fund manager can exploit returns by

buying high (low) beta stocks and selling low (high) beta stocks.

2.4.1 Timing using Convex Relationship between Fund Returns and Market Returns

There has been an ongoing debate on the best performance measure for market timing

abilities of fund managers. Traditional performance measures like the Capital Asset Pricing

Model (CAPM) have reported that the relationship between the fund returns and market

returns are linear. Conversely, the study by Treynor and Mazuy (1966) showed that the

relationship between the fund returns and market returns are actually convex. Treynor and

Mazuy (1966) evaluated market timing abilities of mutual funds based on their historical

success in predicting major fluctuations in the stock market. They concluded that successful

market timers would increase their exposure to the market when a bullish period is

anticipated and reduce exposure to the market when a bearish period is anticipated. This

action causes the characteristic line of the portfolio to surpass the market as the portfolio

asset structure can be constantly adjusted (Figure 2.1).

Figure 2.1: The Characteristic Line of a Fund that Outguess the Market (Treynor and Mazuy,

1966)

Volatility

Volatility

Fund Returns

Market Returns

Characteristic Line

24

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

Using the basis of the CAPM, Eq. (1), Treynor and Mazuy (1966) developed a least

square regression technique performance focusing on the squared relation between fund

returns and market returns. A curvature line was identified by fitting in the characteristic line

data of 57 open-end mutual funds using their yearly data observations of returns during the

period between 1953 and 1963, Eq. (2):

𝑅𝑖𝑡 = 𝑅𝑓 + 𝛽𝑖(𝑅𝑚𝑡 − 𝑅𝑓𝑡) (1)

𝑅𝑖𝑡 − 𝑅𝑓𝑡 = 𝑎𝑖 + 𝛽𝑖(𝑅𝑚𝑡 − 𝑅𝑓𝑡) + 𝛾𝑖(𝑅𝑚 − 𝑅𝑓𝑡)2

+ ℯ𝑖𝑡 , (2)

where, 𝑅𝑖𝑡 denotes return on assets of the selected fund at time t, 𝑅𝑓𝑡 denotes risk free return

rate at time t, 𝑅𝑚𝑡 is the return on the market at time t, 𝑎𝑖 denotes a selectivity ability,

𝛾𝑖 denotes the parameter measuring the market timing performance, if 𝛾𝑖 > 0, it implies the

existence of a timing ability. The difference between the equation of the CAPM model and

the Treynor and Mazuy model is the addition of 𝛾𝑖(𝑅𝑚 − 𝑅𝑓𝑡)2 as this changes the linear

relationship between the fund returns and market returns into a quadratic equation.

Treynor and Mazuy used yearly data observations of returns as they believed that

even for smaller funds, the frequency of portfolio changes which will alter their fund’s

volatility will not happen more than once a year. However, only one out of 57 funds exhibited

a curve characteristic line. This suggest that on average, mutual funds were not successful at

outguessing the market. Treynor and Mazuy (1966) concluded that any excess returns

generated were not from the success of timing abilities but from the abilities of fund

managers in identifying under-priced industries and companies.

Supporting the study of Treynor and Mazuy (1966), Williamson (1972) stated that the

relationship between the fund returns and the market returns would be convex instead of

linear. Based on the characteristic line graph, when the line is curved upwards at the upper

25

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

right and lower left end, this suggest that mutual funds had performed well in bearish markets

and performed even better during bullish markets.

Williamson (1972) attempted to identify market timing abilities by reviewing the

available published data of 180 mutual funds during the period between 1961 and 1970.

However, similar to Treynor and Mazuy (1966), on average, no mutual funds were able to

outperform the market. Moreover, four out of 180 funds displayed significant unsuccessful

forecasting. Against expectations, these funds were more volatile during bearish market and

less volatile during bullish markets.

2.4.2 Stationary Beta versus Non-Stationary Beta in Bull and Bear Markets

Jensen (1968) believed that the performance of risky investment portfolios is the

ability of a portfolio manager to earn superior returns through successful predictions of future

security prices. These returns should be higher than the returns expected by the portfolio

manager for the level of risk associated with their portfolios. This belief is based on the

concept that on average, the riskier the asset is, the higher the returns will be. Portfolio

managers will be compensated for taking on additional risk. If the asset’s actual returns are

above the expected returns of the asset, a positive alpha is established.

On the contrary to earlier studies that evaluated forecasting abilities of portfolio

managers using relative performance measures, Jensen (1968) has provided an absolute

measure of performance. Absolute performance measure is a measure that is compared

against a certain standard. The Jensen’s equation determines the superior returns obtained

when deviated from the benchmark, Eq. (3):

𝛼𝑖 = [𝑒(𝑟𝑖𝑡) − 𝑟𝐹𝑡] − 𝛽𝑖(𝑒(𝑟𝑚𝑡) − 𝑟𝑓𝑡), (3)

26

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

where, 𝑟𝑖𝑡 denotes the return of fund 𝑖 at time t, 𝛼𝑖 denotes the abnormal returns of the fund

(an idea of forecasting abilities), 𝛽𝑖 denotes the systematic risk of the fund 𝑖, 𝑟𝑚𝑡 denotes the

return of the market at time t and 𝑟𝑓𝑡 denotes the risk free rate at time t. The value of alpha

could either positive or negative. Having a positive alpha would imply superior forecasting

abilities and in contrast, having a negative alpha would imply either poor selection choices or

the existence of high expenses.

Given that the predictability skills of a portfolio manager not only involves the skills

to predict price movements of individual securities and the general behaviour of future

security prices, the Jensen (1968) model also considers the abilities of a fund manager to

forecast the market behaviour. Henceforth, the Jensen (1968) model not only evaluates the

portfolio manager’s ability to predict how much a security or portfolio is expected to earn

given the level of systemic risk (measured by beta) but also measures the ability of a portfolio

manager to forecast the market’s behaviour. However, this is based on the assumption that

the portfolio manager tries to maintain the given level of risk in his or her portfolio.

Jensen (1968) investigated the existence of predictability skills by analysing 115 open

ended mutual funds using their yearly data observation of returns during the period between

1945 and 1964. Based on the results, on average, mutual funds were not able to predict

security prices to outguess the market henceforth underperforming buy and hold strategies.

They were also unsuccessful in their trading activities to recoup brokerage expenses. We

consider some limitations of this study. The assumption that the portfolio manager attempts

to maintain the same level of risk may have caused inaccurate results. As mutual funds are

being actively managed, it is reasonable to expect changes in the level of risk due to the

buying and selling decisions of portfolio managers.

27

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

Subsequently, there has been attention drawn to the stability of the systematic risk

measured by beta in bull and bear market conditions. The systematic risk of mutual funds in

different market conditions is an important factor in evaluating the market timing abilities of

a fund manager. If there is different beta for different market conditions, using a stationary

beta for the entire period can result in different conclusion of a fund manager’s abilities.

During market changes, when a stationary beta is used for the entire time period there is no

consideration for the additional risk exposure. If a fund manager correctly adjusts the fund’s

beta in an anticipation of a bull market, the beta in a bull market would be greater than the

estimation of beta for both bull and bear market period. One of the limitations from Jensen

(1968) study was the use a stationary beta for the entire period of the study as the fund

managers attempted to on average, maintain the given level of risk in their portfolio.

Taking into consideration a non-stationary beta, Fabozzi and Francis (1979)

investigated if the beta of mutual funds varies in bullish and bearish markets. A statistical

model was developed by Fabozzi and Francis (1979) to examine if the systemic risk of

mutual funds was altered during different market conditions. The monthly data observations

of returns of 85 mutual funds were tested between the period from 1965 and 1971. In order to

examine if the systematic risk (beta) are different in various market conditions, this equation

has taken into consideration of beta shifting, Eq. (3):

𝑅𝑖 = 𝐴1𝑖 + 𝐴2𝑖𝐷𝑡 + 𝛽1𝑖𝑅𝑚𝑡 + 𝛽2𝑖𝐷𝑡𝑅𝑚𝑡 + ℯ𝑖𝑡, (4)

where, 𝑅𝑖 denotes the excess returns of fund i, 𝑅𝑚𝑡 denotes the excess returns on the market

𝐷𝑡 denotes a dummy variable which is unity if the tth period is a bull market and zero

otherwise, The coefficients of the dummy variable, 𝐴2𝑖 and 𝐵2𝑖, measure the differential

effects of bull market conditions on the alpha, 𝐴1𝑖 and beta, 𝐵1𝑖 respectively and ℯ𝑖𝑡 is the

28

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

random error term. This equation allows the shifting of alpha and beta and is designed to

determine if the regression coefficients are significantly different in bull and bear markets.

Fabozzi and Francis (1979) reported that there were three definitions of bull and bear

markets for this study. First, defined by a well-established textbook (Cohen, Zingbarg and

Zeikel, 1973), certain months were designated as bull and bear markets in accordance to

market trends. Second, when market returns positive, the market is known to be bullish.

When market returns are negative, the market is known to be bearish. Third, without the

consideration of market trends, months with market returns higher (lower) than one half of

the standard deviation of market returns over the sample period are designated as bull (bear)

markets.

While betas of individual securities may be stable despite changes in market trends

like the bull and bear markets, Fabozzi and Francis (1979) argued that there is a possibility

for a non-stationary beta to occur even if the fund manager did not attempt to adjust the

portfolio risk. They considered how the individual securities’ betas may be intertemporally

unstable. Also, changes in the relative market value weights of individual securities will alter

the portfolio’s beta, which is the weighted average beta regardless if the betas of individual

securities were not altered. Therefore, a benchmark is created to determine if the number of

funds that shifted in beta were a result of a planned changed in risk exposure. For comparison

purpose, 85 random portfolios were created as benchmarks. Each stock of the 85 random

portfolios were given equal weightage.

Despite considering a non-stationary beta, results suggest that regardless of different

market conditions, on average, mutual funds did not respond differently. Similar to previous

studies, mutual fund managers were not able to outguess the market to earn higher risk-

29

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

adjusted returns for shareholders. Fund managers did not alter their fund’s beta to benefit

from the different market conditions.

Fabozzi and Francis (1979) revealed three reasons why fund managers were not

observed to increase their funds’ beta during bearish to bullish market periods or decrease

their funds’ beta during bullish to bearish periods. One, there were random beta coefficients

from a significant number of New York Stock Exchange (NYSE) stocks and the portfolio

managers might have overvalued or undervalued the beta. Two, there is a possibility that the

portfolio manager was unable to foresee changes in market conditions hence was unable to

shift the fund’s beta during bullish markets. Three, although fund managers may have

correctly anticipated the right change in direction of the market, the cost of altering a fund’s

beta may not be justifiable for the gains in return.

An extension to the Fabozzi and Francis (1979) study, Kim and Zumwalt (1979)

investigated if there were variations of returns of securities and portfolios in up (bull) and

down (bear) markets. This process has the effect of separating the total variation of the

security or portfolio returns into two components, variations when the market is up and

variations when the market is down. Kim and Zumwalt (1979) pointed out that although the

beta of mutual funds are not significantly different in up and down market periods, the

variations of returns of mutual funds may be different. If investors are presumed to be risk-

averse, they would expect to receive a premium for bearing additional risk from the “down”

market and expected to pay a premium for the returns they would receive from the “up”

market.

For the development of the study, two assumptions were employed. The first

assumption was that each security may react differently in up and down markets. If securities

do respond differently, beta coefficients may be determined for both up and down markets

30

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

and investigated for statistically significant differences. There were three measures to

determine what establishes an “up” or “down” market. An “up” market are months with rate

of returns on the market portfolios that exceed the 1) average market return, 2) the risk free

rate or 3) zero. Otherwise, the market is defined as a “down” market. The single index model

was modified to examine both up and down betas, Eq. (5):

𝑅𝑖𝑡 =∝𝑖+ 𝛽𝑖+𝑅𝑚𝑡

+ + 𝛽𝑖−𝑅𝑚𝑡

− + ℯ𝑖𝑡, (5)

where, 𝑅𝑖𝑡 denotes the excess return of fund i , ∝𝑖 denotes the actual return of fund i minus

the expected return of fund i, 𝑅𝑚𝑡 denotes the excess return on the market, ℯ𝑖𝑡 is the random

error term, 𝛽𝑖+is determined from the months when the returns comes from the “up” market

and 𝛽𝑖− is determined when the returns come from the “down” market. As the number of

securities in the portfolio increases, the unsystematic risk also known as firm-specific risk

would be diversified away. The variance of portfolio equation would be written as, Eq. (6):

𝜎𝑝2 = (𝛽𝑝

+)2𝜎𝑝2

𝑝+ + (𝛽𝑝−)2𝜎𝑝

2𝑝− , (6)

where, 𝜎𝑝2 is the variance of the portfolio. The formula is separated into (𝛽𝑝

+)2𝜎𝑝2

𝑝+ being the

variations from the bull market and (𝛽𝑝−)2𝜎𝑝

2𝑝− being the variations from the bear market.

The second assumption was that investors had a preference for greater up side

variation of returns and a preference for a smaller downside variation of returns. This

suggests that an investor has a preference that is positively related to the upside variations

and negatively related to the downside variations. Kim and Zumwalt (1979) believed that

investors require a risk premium on the downside portion of variation and a negative risk

premium on the upside portion of the variation. Expressed in Eq. (7):

𝐸(𝑅𝑝) = 𝑅𝑓 + 𝜆1 𝛽𝑝+ + 𝜆2 𝛽𝑝

− (7)

31

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

where, 𝜆1 𝛽𝑝+ denotes the negative coefficient and 𝜆2 𝛽𝑝

− denotes the positive coefficient. The

two beta model of equation 7 was tested to determine if the expected negative value for 𝜆1

and positive value for 𝜆2 was confirmed.

Kim and Zumwalt (1979) developed the two beta model to incorporate the responses

of beta during “up” and “down” market periods. The variations of returns in both market

periods were investigated using the monthly data observations of returns from a sample of

322 securities between the periods from 1962 to 1976. This model allows the separation of

the total systemic risk into two components, risk from upside variations markets which are

considered to be favourable and risk from bearish markets which are considered to be

unfavourable.

Results reflected that out of 322 securities, 34 exhibited significantly different up and

down market betas. In comparison to the Fabozzi and Francis (1979) study, more securities

displayed statistically significant differences between “up” market and “down” market betas

than would occur randomly. The signs of the regression coefficients were also correct and

statistically significant, suggesting that investors do receive a risk premium for tolerating

downside risk. Consistent to Kim and Zumwalt’s expectations, the negative premium was

associated to the beta of the “up” market. This suggests that the measurement of downside

variation of returns is more appropriate when measured by the “down” market beta rather

than the conventional single beta in the market model.

Miller and Gressis (1980) created a new measure based on the traditional CAPM

which allows and statistically estimates the extent of non-stationarity in the relationships

between the fund returns and market returns. This measure allows a precise estimation of

alpha and beta in the presence of non-stationarity beta. Miller and Gressis (1980) revealed

that if non-stationarity is significant in a risk return relationship but is ignored, this can result

32

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

in misleading information as the estimates of alphas and betas are calculated based on a

stationary beta which is the weighted averages of the actual values. When mutual funds are

actively managed, the level of systemic risk would fluctuate as a result of the buying and

selling decisions of their managers. Hence beta, the measure of systematic risk should not be

ignored as this might result in biased results. It is also reasonable to expect non-stationary

risk return relationships in some mutual funds as well-managed funds would take advantage

of the market by altering their betas in accordance to the general market movements.

Miller and Gressis’s (1980) approach is based on the traditional CAPM which allows

and statistically gauge the extent of non-stationarity in relationships between the returns of

funds and the returns from the market. In order to obtain a more precise estimate of beta and

alpha, time can be segmented into intervals during which the betas are stationary. A

partitioning algorithm and partition selection procedure is conducted on the sample of 28

mutual funds using the weekly data observations of returns between the periods from 1973 to

1974. Unlike previous researchers that evaluated the performance of mutual funds using

yearly or monthly data observations of returns (Jensen, 1986; Fabozzi and Francis, 1979;

Kim and Zumwalt, 1979), Miller and Gressis (1980) used weekly data observations of returns

as they believed that it is a more appropriate measure in detecting shifts between the risk and

returns of mutual funds.

The presence of a non-stationary beta would suggest either changes in the distribution

of risk in the economy or changes in the mutual fund portfolio composition. Investors are

interested in such changes as they attempt to take advantage of these deviations to earn

superior returns. Based on the results, only one out of 28 funds exhibited stationary betas and

the rest had betas that varied over the periods. Based on correlation and regression analysis

results of the information gathered from the partition regression, a mixture of results were

exhibited between the betas and the market returns. There were some evidence of weak

33

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

positive relationships and some weak negative relationships between the betas and market

returns. Similarly, there were also weak negative relationships and weak positive

relationships between the alphas and betas. However, there were no statistically significant

relationships of either type.

Following up on the studies that incorporated the use of non-stationary beta, Chen

(1982) re-examined the relationship between the risk and returns of mutual funds in in bull

and bear market conditions. Chen (1982) evaluates the study of Kim and Zumwalt (1979) as

their procedure of valuing “up” and “down” market betas may have led to in inaccurate

results in the risk analysis of “up” and “down” markets.

Chen (1982) revealed that the study by Kim and Zumwalt (1979) gave inconsistent

results due to multicollinearity issues which resulted in large sampling variances of estimates

of the “up” and “down” market betas. Also, the model did not take into consideration that the

beta coefficient would change over time. Chen (1982) used a time-varying beta coefficient

approach to resolve these issues. It is revealed that the two beta model used for the test of the

trade-off between the risk and returns in “up” and “down” market is constant regardless of a

stable or non-stable beta coefficient. The two beta model from the Kim and Zumwalt’s study

was modified to be, Eq. (8):

𝐸(𝑅𝑝𝑡) = 𝑅𝑓 + 𝛽𝑝+𝐸(𝑅𝑚𝑡 − 𝑅𝑓)

++ 𝛽𝑝

−𝐸(𝑅𝑚𝑡 − 𝑅𝑓)−

+ ℯ𝑖𝑡 (8)

where, 𝐸(𝑅𝑝𝑡) denotes the expected return of the portfolio, 𝑅𝑓 denotes the risk free rate of

interest, 𝛽𝑝+ denotes the bull market beta, 𝛽𝑝

− denotes the bear market beta and ℯ𝑖𝑡 denotes the

random error term.

The sample of 360 mutual funds’ monthly data observations of returns were tested

between the periods from 1965 to 1977. Similar to Kim and Zumwalt’s (1979) results, Chen

34

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

(1982) concluded that investors do require a premium for taking on risk from the downside

market and investors pay a premium for the returns they receive from the “up” market. The

results of the time varying beta approach method have supported the Kim and Zumwalt’s

findings that the breakdown of total systemic risk into risk due to upside deviation of returns

and risk due to the response of a bear market still appeared to be correct even with a non-

stationary beta. Irrespective of a stationary or non-stationary beta, investors do request

compensation for undertaking the risk from the variation of returns from the bear market

which was viewed as unfavourable and pay a premium for the upside variation of returns

which was viewed as favourable.

Both studies by Chen (1982) and Kim and Zumwalt (1979) revealed that an

appropriate measure of downside risk (bear market) would be the “down” market beta instead

of a stationary beta. It is not appropriate to consider the use of a stationary beta as a

measurement of the market as the market cycle changes over time. A stationary beta does not

give any allowance for the increase in risk exposure.

2.4.3 Evaluating Market Timing Abilities simultaneously with Security Selection

Abilities

Past research have investigated the market timing abilities of fund managers

individually. Using a different approach, Chang and Lewellen (1984) evaluated market

timing abilities of fund managers simultaneously with security selection abilities. They

believed that portfolio managers might be able to exploit returns by engaging in effective

“macro” market timing activities as well as cautious “micro” security selection efforts. That

is the ability to modify the total risk composition of their portfolios in the anticipation of the

general movements of the market. This study considers the fact that a non-stationary beta

would be a more appropriate measure of mutual fund performance. Based on the studies by

35

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

Fabozzi and Francis (1979), Kim and Zumwalt (1979), Miller and Gressis (1980) and Chen

(1982), they found some evidence that mutual fund portfolios do not have a constant risk

position over time. They also concluded that skills of market timing may well be a

measurement of a fund manager’s decision process.

Chang and Lewellen (1984) conducted a parametric statistical procedure that allowed

a joint test for the presence of either security selection or superior market timing skills in

managed portfolio to investigate the performance of 67 mutual funds using their monthly data

observations of returns between the periods from 1971 to 1979. Majority of research have

evaluated the performance of mutual funds based on the single market model equation, Eq.

(9):

𝑍𝑝(𝑡) − 𝑅(𝑡) = 𝑎𝑝 + 𝛽𝑝[𝑍𝑚(𝑡) − 𝑅(𝑡)] + 𝜖(𝑡), (9)

where, 𝑍𝑝(𝑡) denotes the observed rate of return on the portfolio p during the period, 𝑅(𝑡)

denotes the simultaneous rate of return on a riskless asset, 𝑍𝑚(𝑡) denotes the return on the

fully diversified “market” portfolio of all risky assets during t and 𝜖(𝑡) denotes the random

error term with it being a value of 0. 𝛽𝑝 is assumed to be stationary over time. When alpha

has a positive value, this indicates superior return performance based on security selection

efforts. However, this model only evaluates stock selection abilities and does not take into

consideration that the level of systemic risk (𝛽𝑝) might change over time.

The equation was later modified by Henriksson and Merton (1981) to a least square

regression which evaluates the stock selectivity and market timing abilities of mutual fund

abilities separately. It was also modified to capture an “up-market beta” and a “down-market

beta.” The modified equation was, Eq. (10):

𝑍𝑝(𝑡) − 𝑅(𝑡) = 𝛼∗ + 𝛽1∗𝑋1(𝑡) + 𝛽2

∗𝑋2(𝑡) + 𝜖𝑝∗ (𝑡), (10)

36

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

where, 𝑋1(𝑡) and 𝑋2(𝑡) =𝑍𝑚(𝑡) − 𝑅(𝑡), 𝛽1∗ denotes the “up-market beta” of a managed

portfolio and 𝛽2∗ denotes the “down market beta”. The contributions of returns have been

separated into two components, α represents the returns due to security selection ability and

𝛽 is used to measure the portfolio’s market-timing skill. When there is no existence of market

timing abilities, the value of beta would be zero.

While this was a joint test that considered both market timing and stock selection

abilities of fund managers, results suggest that on average, neither skilful market timing nor

clever security selection abilities were evident. Overall, mutual funds were unable to outguess

the market. It seemed that passive strategies still have an upper hand in mutual fund

investments.

Similar to Chang and Lewellen (1984), Chen and Stockum (986) also investigated the

market timing and stock selection abilities of fund managers simultaneously. Traditional

performance measures like the Sharpe ratio assumed that that the systematic risk level of a

fund is a fixed coefficient rather than a decision variable. However, this results in inaccurate

performance measures as the risk of the portfolio varies over time. Following which, studies

have incorporated the use of a non-stationary beta. However, they did not consider that the

mutual fund’s beta could also be non-stationary when fund managers are not engaged in

timing decisions (Fabozzi and Francis, 1979; Kim and Zumwalt, 1979; Miller and Gressis,

1980; Chen, 1982). Hence, the presence of a non-stationary beta does not necessary represent

the existence of market timing abilities.

Chen and Stockum (1986) presented a generalized varying parameter model to

examine the performance of mutual funds by allowing for both timing decisions of funds and

random behaviour of fund’s systematic risk levels. Although the generalized varying

37

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

parameter model is similar to the Treynor and Mazuy model, this model allows the beta of

mutual funds to be a decision variable instead of a fixed coefficient, Eq. (11):

𝑅𝑖𝑡 = 𝑎𝑖 + 𝑅𝑚𝛽− + 𝜆𝑖𝑅𝑚𝑖

2 + 𝜔𝑖𝑡 (11)

where, 𝜔𝑖𝑡 equals (𝜇𝑖𝑡 + 𝜖𝑖𝑡𝑅𝑚𝑡). 𝑅𝑖𝑡 denotes mutual fund i’s return at time t, 𝑅𝑚 denotes the

market return at time t, 𝜇𝑖𝑡 denotes random shock, β denotes target systemic risk, 𝑎𝑖 measures

the selectivity component and 𝜆𝑖𝑅𝑚𝑖2 measures changes due to market timing. A portfolio

beta might still be non-stationary even if fund managers are not actively managing their

portfolios by adjusting the portfolio beta in accordance to the market. This is because a

portfolio beta might respond differently to various market cycles.

Chen and Stockum (1986) examined 43 mutual funds using their quarterly data

observations of returns between the periods from 1975 to 1982. Unlike prior studies that used

monthly or yearly data observations of returns, Chen and Stockum (1986) stated that the use

of quarterly data observations gives fund managers an extended period of time to form

market expectations and adjust their portfolios accordingly. Throughout this sample period,

there were two bull and two bear market periods. By incorporating both cycles of the

markets, it will help to reduce biasness in this study.

Based on the results, 30% of funds showed selectivity, 19% were random betas and

14% showed significant but negative market timing performance. Although there were some

significant selectivity abilities, results suggest that similar to previous findings, mutual funds

did not reflect any market timing abilities regardless individually or as a group.

2.4.4 Free from Beta Estimates

On the contrary to prior research, Ferri, Oberhelman and Roenfeldt (1984) examined

the market timing abilities of mutual funds without the use of beta estimates. This method

38

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

focuses on the composition of assets in a fund’s portfolio and investigates alterations in the

composition prior to variations in the broad level of stock market prices. The main objective

of this method is to examine whether a fund manager’s decision to gradually increase or

decrease the fund’s commitment to common stocks. The expectations of fund managers are

reflected on the decisions that they made and simultaneously shifts the portfolio’s market-

related volatility.

A fund manager is successful at market timing when their decisions and expectations

are consistent with the later movements of the market. For instance, a fund manager who

anticipates a bearish market will lower the portfolio’s volatility by decreasing the percentage

of assets in a portfolio that are invested in stocks. Market timing skills are exhibited if the

later market is bearish. Likewise, successful market timing is exhibited when a fund manager

increases the portfolio assets invested in stocks in the expectations of an increase in market

prices and the later market is bullish.

Ferri, Oberhelman and Roenfeldt (1984) examined the quarterly changes in the

mutual fund’s stock holdings of 69 mutual funds between the periods from 1975 to 1980.

These types of mutual funds have aggressive management with a preference of being

completely invested by stocks. Therefore, any alterations in these funds are considered as an

attempt to forecast or time the market movements. Additionally, two subgroups of

stockholdings were also examined, those preceding extensive fluctuations in stock prices and

those when managerial reallocations of portfolios are not impacted by shareholder’s

contributions or withdrawal from funds.

Market timing abilities are evaluated by examining the increases and decreases in a

fund’s relative commitment to stocks measured by the ratio of net purchases or sales of

common stocks (NETPS) to total assets. If the NETPS has a positive value, the fund has

39

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

purchased more stock than it sold, increasing its exposure to market risk. A t test was

conducted to compare the mean levels of NETPS for a fund quarter before an increase in the

stock index with the mean NETPS for the fund quarter before a decrease in the stock index.

Ferri, Oberhelman and Roenfeldt (1984) hypothesized that the NETPS is classified as an

upmarket decision if the stock index increases during the subsequent months and the NETPS

is classified as downmarket decision if the stock index decreases during the subsequent

months. The null hypothesis is rejected if the average NETPS for the upmarket is

significantly larger than the average NETPS for the down market. However, the test of means

could be inaccurate as there is a possibility that a fund made merely a few large mistakes as

the test results are reliant on the extent of the deviations in stock holdings. Therefore, a

frequency test is also conducted as it only examines the direction of changes in stock

holdings prior to the movements in the stock index and eliminates the limitations of the test

of means. A correct decision can either be classified as a positive NETPS before a bullish

market or a negative NETPS before a bearish market.

Based on the results, although a few funds displayed some market timing abilities, on

average, there were no significant market timing abilities exhibited. In sum, although this

study offers an alternative way of examining market timing abilities which is a method that is

free from the estimates of beta, there were no new evidence that fund managers possess

market timing abilities.

2.4.5 Portfolio Performance Measures without Benchmarks

Past researchers have evaluated performance measures of mutual funds by comparing

the returns of managed portfolios to the returns of a benchmark portfolio. However, this

could be a bias measure of market timing abilities as results are dependent on the choice of

benchmark selected. Often, information regarding the portfolio composition of funds are not

40

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

utilised. Grinblatt and Titman (1993) believed that by making use of information about the

portfolio composition, the method of comparing returns to a benchmark portfolio can be

eliminated.

This method is adapted by the Event Study Measure where the performance of mutual

funds are evaluated by calculating the differences between the returns of assets during the

portfolio period known as “the event period” and returns of a later date known as “the

comparison period”. This is the belief that the assets held in a well-managed portfolio (event

period) would have higher returns compared to periods when assets are not included in any

portfolios (comparison period). This method uses later period returns compared to earlier

period returns as they have taken into account that some portfolio managers are likely to pick

their assets based on their past returns. However, this might be a bias assumption as it forces

the researcher to ignore assets that lacked returns in the comparison periods.

Grinblatt and Titman (1993) developed a new measure that is not subjected to

survivorship biases. It is based on the assumption that from the standpoint of uninformed

investors, the direction of expected asset returns is constant over time. This implies that the

portfolio holdings of an uninformed investor does not have any form of relationship with the

future returns. Unlike a well-informed manager who is able to predict when certain assets

will exhibit higher or lower than average returns, the direction of the expected asset returns

will vary over time. The manager can take advantage of these changing expected returns by

tilting his or her portfolio weights towards assets that have increased in expected returns and

tilt away from assets that have decreased in expected returns.

Grinblatt and Titman (1993) examined 155 mutual funds quarterly changes in

stockholdings from the period between 1974 and 1984. Concluding results showed that on

average, mutual fund portfolios exhibited positive abnormal investment performances and

41

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

that the strongest performance was computed from the aggressive growth category of funds

which earned significantly positive risk adjusted returns. In relation to the study by Ferri,

Oberhelman and Roenfeldt (1984), any movements in these funds are considered as an

attempt to forecast or time the market movements. Although no market timing abilities were

present, this article emphasized that superior performance can be predicted without the use of

a benchmark when portfolio holdings were examined.

2.4.6 Volatility Timing

Previous studies have examined the market timing abilities of mutual fund managers

exclusively by comparing the returns between their funds and the market (Treynor and

Mazuy, 1966; Jensen, 1968; Fabozzi and Francis, 1979; Kim and Zumwalt, 1979; Miller and

Gressis, 1980; Chen, 1982). The main theory behind these studies often investigate if fund

managers have taken advantage of superior information by adjusting their funds towards

more (less) volatile stocks in the anticipation of bull (bear).

Often, fund managers encounter difficulties in predicting market returns. Using a new

perspective, Busse (1999) investigated the funds’ ability to time market volatility. He

examined if funds change market exposure in relation to market volatility changes and

highlighted that volatility timing is a significant influence in the returns of mutual funds as it

leads to higher risk-adjusted returns.

Attention has been shifted to market volatility for two reason. First, unlike market

returns which are hard to predict, market volatility is predictable because it is persistent. High

volatility is usually followed by high volatility and low volatility is usually followed by low

volatility. Second, majority of performance measures are risk adjusted. These measures affect

the cash flows of funds and how funds manage risk has repercussions for manager

compensation. However, it is uncertain that a fund manager can increase risk adjusted

42

Tryphena Ow, An Examination of the Market Timing Ability of Mutual Funds using

Quarterly Trades

performance or investor utility by timing market volatility. Therefore, Busse (1999)

investigates if funds respond to changes in market volatility and how these strategies will

affect the performance of funds.

Busse (1999) motivated volatility timing in the perspective of a fund manager,

assuming that fund managers attempt to time market exposure in the best interest of the fund

shareholder. Busse (1999) analysed the daily data observation of returns of 230 domestic

equity funds between 1985 and 1995 with a daily single factor volatility timing model to

study how managers respond to publicly available information. This single factor volatility