Embed Size (px)

Citation preview

Understanding Government Budgets

(aka - Annual Financial Statement)

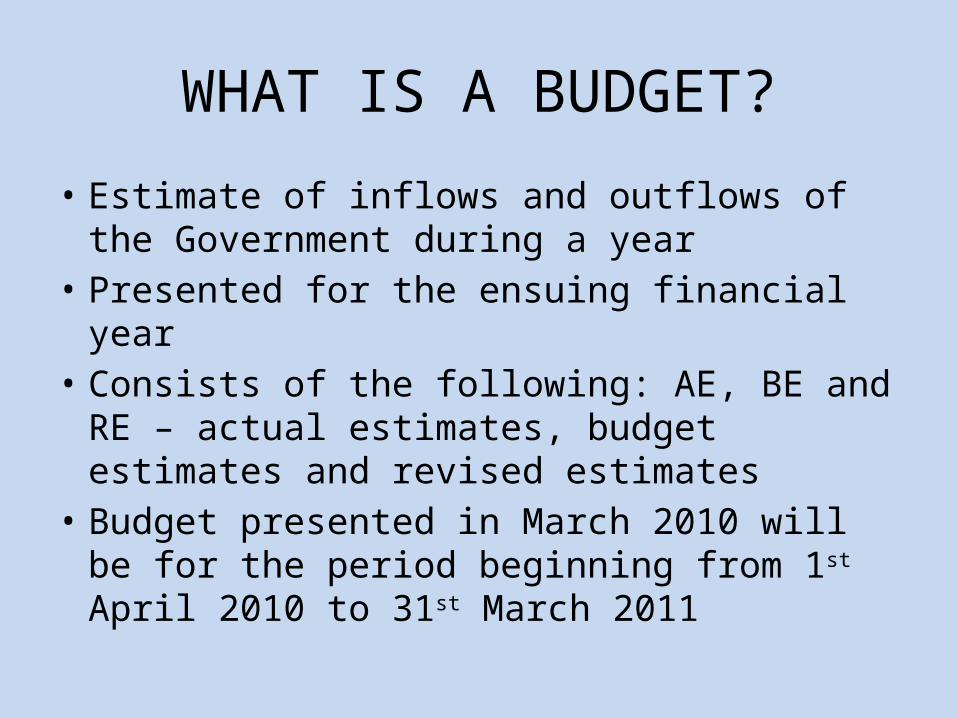

WHAT IS A BUDGET?

• Estimate of inflows and outflows of the Government during a year

• Presented for the ensuing financial year• Consists of the following: AE, BE and RE –

actual estimates, budget estimates and revised estimates

• Budget presented in March 2010 will be for the period beginning from 1st April 2010 to 31st March 2011

UNION BUDGET

• Timetable drawn up by the BAC – Business Advisory Committee of Parliament.

• Has a fixed period of discussion with each Ministry

• Budget division in the Finance Ministry has responsibility for the Budget

• Considers proposals from all Departments and Ministries subject to availability of funds

…UNION BUDGET

• Four organs of Govt involved: Finance Ministry, Administrative Ministries, Planning Commission and Comptroller and Auditor General

• Further, different lobbies, unions, economists• Final approval rests with Parliament

Government accounts (Union level)

• Divided between the Consolidated Fund of India, Contingency Fund of India and the Public Account

• Consolidated Fund of India: Credits all revenue received and all loans raised by issue of government debt and money received in repayment of loans

• Contingency Fund of India: For unforeseen expenditure pending subsequent authorisation by Parliament

• Public Account: Includes trust funds and where all transactions relating to Debt, Deposits, Advances and remittances are made

Government accounts (Union level)

• Budget is also divided up into Revenue Budget and Capital budget

• Revenue Budget – Expenditures and receipts of annually recurrent nature

• Capital Budget – Investment expenditure related – items are of a longer term duration; Results in the acquisition or construction of a fixed asset (land, building, vehicle, furniture or equipment) or enhancement of an existing fixed asset.

Rev vs capital expenditure

• CAP EXP: Acquisition/Creation of assets such as land, building and machinery, and also investments in shares, etc. Other items that also fall under this category include, loans and advances sanctioned by the Centre to State governments, union territories and public sector undertakings.

• REV EXP: Does not result in the creation of assets. This refers to the money spent on the normal functioning of the government departments and various other services such as interest charges on debt incurred by the government.

Rev vs capital receipts

• REV REC: Consist of tax collected by the government and other receipts consisting of interest and dividend on investments made by government, fees and other receipts for services rendered by government

• CAP REC: Are loans raised by the Government from the public (often referred to as market loans); borrowings by the Government from the Reserve Bank of India (RBI) and other parties through sale of Treasury Bills; loans received from foreign governments and bodies; and recoveries of loans granted by the Union Government to State governments, Union Territories and other parties. It can also include the proceeds from divestment of government equity in public enterprises.

Government Accounts

• Money given from the government’s account for the Central Plan is called Plan Expenditure. It consists of both Revenue Expenditure and Capital Expenditure, Central Assistance to States and Union Territories.

• Planning commission also involved – hence you find the terms “Plan expenditure” (current schemes/freshly intro in current FYP period) – “Non-plan expenditure” (carried forward schemes from earlier FYP periods) as well.

• The emphasis of the Commission is on maximising the output by using limited resources optimally. Effort is to look for increases in the efficiency of utilisation of the allocations being made.

5 stages• I. Presentation of budget with Finance

Minister’s Speech• II. General Discussion• III. Voting on demand for grants – which each

Ministry has - A statement of expenditure estimate from the Consolidated Fund that requires the approval of the Lok Sabha.

• IV. Passing of appropriation bills - A Bill that enables withdrawal of money from the Consolidated Fund to pay off expenses. These are instruments that Parliament clears after the demand for grants has been voted by the Lok Sabha.

• V. Passing of Finance Bill - Government’s plans for imposing new taxes, modifying of the existing tax structure or continuing the existing tax structure beyond the period approved by the Parliament.

Budget in general

• Railways takes out their own budget• State Government takes out its own budget in

consultation with the Central Government

State Government Budgets

Procedure

• Annual Financial Statement presented• No demand for grant shall be made w/o consent of

the Governor• Each demand shall contain first a statement of the

total grant proposed, and then a statement of the detailed estimate under each grant divided into items.

• Subject to these rules, the Budget shall be presented in such form as the Finance Minister may, after considering the suggestions, if any, of the Estimates Committee consider best.

… Procedure• The Budget shall be dealt with by the Assembly in two stages, namely:-

• a general discussion, and • the voting on demands for grants.

• Subject to sub-rules the demands for grants shall be presented in such order as the leader of the House, in consultation with the Leader of the Opposition, may determine.

• On the days allotted under sub-rule, no other business except the questions shall be taken up without the consent of the Speaker.

• Motion may be moved at this stage to reduce any demand for grant or to omit any item thereof but not to increase or alter the destination of, a demand for grant.

• No amendment to motions to reduce any demand for grant shall be permissible.• When several motions relating to the same demand are made they shall be discussed

in the order in which the heads to which they relate appear in the Budget.

Revenue receipts

• Revenue receipts divided up into tax revenue (70%) and non-tax revenue (30%)

• Tax revenue: Sales tax (VAT format), state excise duties and stamps and registration; Electricity duties; Taxes on goods and passengers; entertainment tax

• Non Tax revenue: Grants from centre and interest receipts, dividends, profits

Revenue expenditure

• 3 parts: – Developmental expenditure (54%)• Social and community services (63%) – education,

health, etc• Economic services (37%) – agriculture, irrigation,

industry, forests, land conservation, etc

– Non developmental expenditure (43%) (interest payments, admin services, pensions)

– Assignments and contributions to local bodies (3%)

Capital receipts

• Loans from Central Government (52%)– Plan scheme loans– Central schemes– Centrally sponsored programmes– Non plan loans: States’ share of collection of small

savings• Market loans and Debt (43%) • Loans and Advances from the Centre (9%)• Reserve Funds (15%)

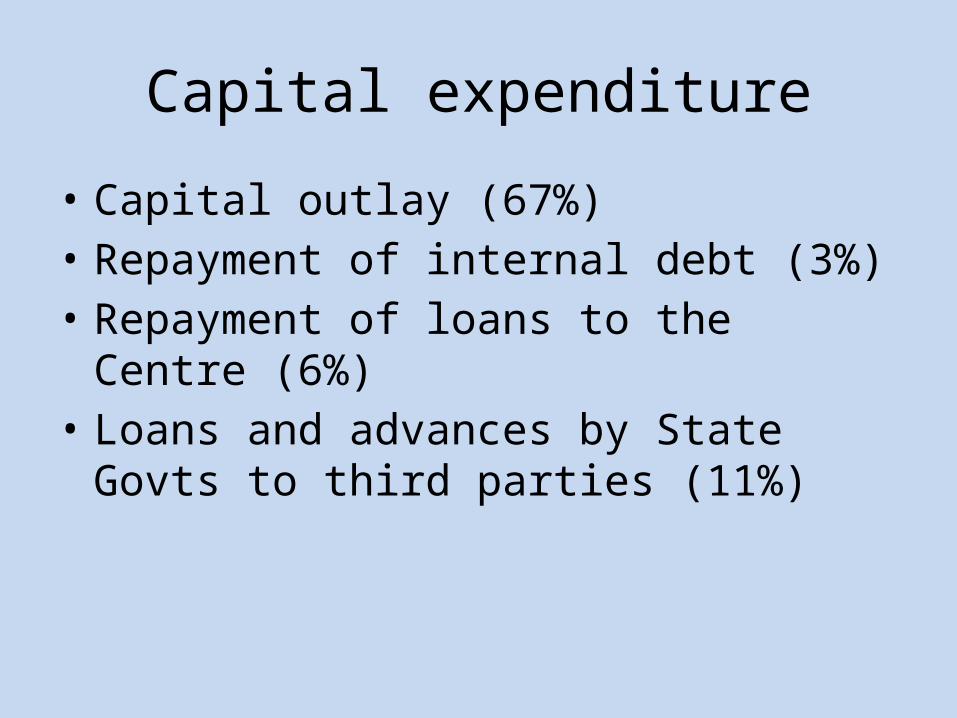

Capital expenditure

• Capital outlay (67%)• Repayment of internal debt (3%)• Repayment of loans to the Centre (6%)• Loans and advances by State Govts to third

parties (11%)

Aims of budget analysis

• Relate information obtained on the Government sector to similar information made available on other major sectors of the economy.

• It is designed to obtain the kinds of information on Government transactions, which are required for determining aggregates of state income and expenditure, and for tracing their inter-relationships with other major sectors of the state economy.

… Aims of budget analysis

Classification of Govt Expenditure• (i)ECONOMIC: The economic character of the expenditure

like current expenditure, capital expenditure, loans etc• (ii) PURPOSE: The purpose it is likely to serve, such as, health,

education, social security & welfare servicesEconomic-cum-Purpose Classification shows how expenditure for a particular purpose is divided between economic categories or how expenditure in a particular economic category is allocated to different purposes or types of public services.

State Government Budgets• As per the recommendations of the Committee on Regional

Accounts/National Accounts system, the following four accounts have been taken by the Delhi govt to analyse the budget:-ECONOMIC

• How does one interpret a budget?I. Income and outlay account of administrative departments

(current)

…State Government Budgets

II. Capital finance account of general govtIII. Production a/c of Departmental Commercial Undertakings –

irrigation and forestsIV. Production Accounts of Govt. Services –

• Comprised of (i) services produced for own use of administrative departments (which has already been defined under the final consumption expenditure of Income & Outlay Account) and (ii) sale of goods & services

• Gross input is inclusive of (i) Intermediate consumption (ii) Compensation of employees and (iii) Consumption of fixed capital.

Purpose classification

• The purposes of the government expenditure may be of two types (i) long term

• (ii) short term• Long-term expenditure - tackling the problem of

unemployment, economic development of the state, fundamental changes in the structure of the economy.

• The short-term expenditures relate to immediate objectives of expenditure incurred in regard to health, defense, education, social welfare, economic services, etc.

…Purpose classification… e.g.

• 1.1 General Admn., External Affairs, Public Order & Safety• 1.1.1 Public Order & Safety• 1.1.2 Planning & Statistical Activities• 1.1.3 General Admn.,External Affairs, Public Order & Safety

n.e.c.• 1 General Public• Services• 1.2 General Research• 2 Defence including Civil Defence

…Purpose classification.. e.g.• 3.1 Administration, Regulation and Research• 3.1.1 Primary Education• 3.1.2 Secondary Education• 3.1.3 Higher Education• 3.1.4 Other Educational Administration n.e.c.• 3.2 Educational Services• 3.2.1 Primary Education• 3.2.2 Secondary Education• 3.2.3 Higher Education• 3 Education• Affairs and• Services• 3.2.4 Educational Services n.e.c.

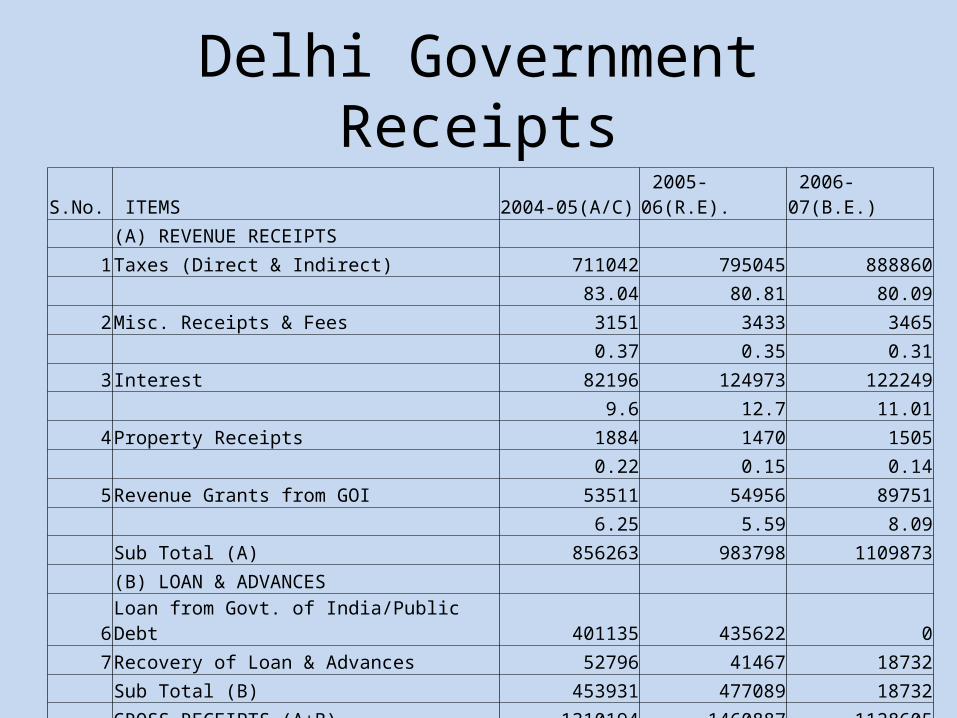

Delhi Government ReceiptsS.No. ITEMS 2004-05(A/C) 2005-06(R.E). 2006-07(B.E.)

(A) REVENUE RECEIPTS

1Taxes (Direct & Indirect) 711042 795045 888860

83.04 80.81 80.09

2Misc. Receipts & Fees 3151 3433 3465

0.37 0.35 0.31

3Interest 82196 124973 122249

9.6 12.7 11.01

4Property Receipts 1884 1470 1505

0.22 0.15 0.14

5Revenue Grants from GOI 53511 54956 89751

6.25 5.59 8.09

Sub Total (A) 856263 983798 1109873

(B) LOAN & ADVANCES

6Loan from Govt. of India/Public Debt 401135 435622 0

7Recovery of Loan & Advances 52796 41467 18732

Sub Total (B) 453931 477089 18732

GROSS RECEIPTS (A+B) 1310194 1460887 1128605

S.No. ITEMS 2004-05(A/C) 2005-06(R.E). 2006-07(B.E.) (A) EXPENDITURE (Rs lakh) (Rs lakh) (Rs lakh)

1Compensation of Employees 144978 163921 184920 11.26 11.71 13.86

2Purchase of Goods & Services including maint

60643 102701 84025 4.71 7.34 6.3

3Current transfers i/cg subsidy 153227 184928 177002 11.9 13.21 13.26

4New Construction 107830 134517 157729 8.38 9.61 11.82

5Machinery & Equipments i/c transport and software 20005 22247 37872 1.55 1.59 2.84

6Cultivated assets 370 516 589 0.03 0.04 0.04

7Financial Assets 33690 34769 32103 2.62 2.48 2.41

8Other Assets 14197 23307 19992 1.1 1.65 1.5

9Capital Transfers 33350 45889 47428 2.59 3.28 3.55

10Interest paid 156855 170082 213007 12.18 12.15 15.96

11Advances to Local Bodies’ and others 332077 288651 281453 25.79 20.62 21.09

12Repayment of Loan to Central Govt 230165 228167 97898 17.88 16.3 7.33 TOTAL OUTLAY 1287542 1400000 1334548

State Government Budgets

• How does one interpret a budget?OUTCOME BUDGETGENDER BUDGETING/SOCIAL BUDGETING - Calls for

separate budgetory allocations for women/specific social groups in the national budget.