Embed Size (px)

Citation preview

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

1/22

05.03.2009

Table of Contents

I. Executive Summery 1

1. Introduction 2

2. Part A) Financial Analysis of M&S plc in regard to Hermes Principles 3

2.1 Principle 1 3

2.2 Principle 2 5

2.3 Principle 3 7

2.4 Principle 4 7

2.5 Principle 5 9

2.6 Principle 6 10

2.7 Principle 7 12

2.8 Principle 8 13

2.9 Principle 9 13

2.10 Principle 10 14

3. Part B) 15

3.1 Limitations and criticism on the 10 Hermes principles 15

3.1.1 Competition within the industry 15

3.1.2 Measures 15

3.1.3 Statically Aspects 15

3.1.4 Market, economy and population developments 16

3.1.5 Innovation 16

3.1.6 International Investments 17

3.1.7 Other Aspects 17

3.2 Usefulness for investors and level to apply these principles to companies

listed on the London Stock Exchange 17

3.2.1 Comprehensibility 17

3.2.2 Compactness 17

3.2.4 Generality 18

3.2.3 Easiness to apply 18

II. Conclusion 19

III. References 20

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

2/22

05.03.2009

I. Executive Summary

The following report is a financial analysis of the Marks and Spencer plc. For the

identification of key areas for a financial analysis the 10 Hermes principles are used, which

leaves a few parts of a total financial analysis aside. The 10 principles are divided into one

communicational, five financial, two strategic and two social, ethical and environmental

principles, which should prove whether a company is a suitable investment or not. Among

these principles the evaluation of financial management policies and practises were made.

Marks and Spencer fulfil most principles totally and some partially.

The communication of M&S has improved in the recent years, since IFRS were introduced in

2006. In general, the overall communication is very detailed, because plans, goals, process

and numbers of importance are outlined. The requirements of the first principle are met by

M&S.

The financial principles are considering financial measures and systems, which M&S surely

has, but M&S has not published every measure postulated by Hermes, e.g. the WACC.

Therefore a discussion between gearing ratio, CAPEX, retained profits and purchase of own

shares is lead, to give a statement, that concerns the capital structure and the WACC. The

capital structure was calmed down after a peak in 2005 by financial management using these

(CAPEX, retained profits and purchase of own shares). The other financial principles concern

incentive systems, opportunities for growth and investment plans, which are outlined

accurately to give a fair statement whether M&S follows these principles, which they do, but

sometimes only partially.

The strategic principles, to develop coherent strategies for each business unit and to be the

best parent, can also be agreed to be fulfilled by M&S. The Plan A of M&S suits the 7th

principle and the fulfilment of the 8th principle is e.g. the selling of M&S Money, as there

should be divested at subsidiaries, where the company is not the best parent.

The socio, ethical and environmental principles are fully met by M&S, as they won awards

concerning this topic.

Referring to the Hermes principles the investor should invest into M&S because all

requirements are met up to a very high level.

The second part of this report outlines limitations and criticism on the 10 Hermes principles,

usefulness for investors and level to apply these principles to companies listed on the

London Stock Exchange.

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

3/22

05.03.2009

1. Introduction

Dear Neil,

I hope you and your family are well off? I will analyse the financial policies and practises of

Marks and Spencer plc as an example for a company listed on the LSE by using the 10

Hermes principles you have sent to me.

You as a financial management expert should have no problems with the terms used, such

as abbreviations used. Furthermore the style will be held professional and impersonal,

because one of us, you or me might show this report to someone else. Furthermore, I will not

spent much time on explaining simple financial terms, effects, advantages and disadvantage

of every financial tool to keep this report short. In the last part I will outline some points for

improvement of the Hermes principles.

Yours sincerely

Hagen Ziemer

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

4/22

05.03.2009

2. Part A)

Critically evaluate the Financial Management policies and practices of Marks and

Spencer plc over the last five years. You should use the Hermes principles to help you

identify areas for investigation.

2.1 Principle 1

“Companies should seek an honest, open and ongoing dialogue with shareholders. They

should clearly communicate the plans they are pursuing and the likely financial and wider

consequences for those plans. Ideally goals, plans and progress should be discussed in the

annual report and accounts.”

The annual reports concerning communication improved constantly during the last five years.

Every annual report starts with a Chairman’s message, later renamed to foreword, and a

Chief Executive’s review, later changed to Chief Executive’s business review. The message

and the review have goals, plans and progress inherent. Taking a look at the financial review

of 2003, hereby having the lowest level of communication in quality and quantity of the past

five years, the chairman states the goal: “We are on a journey of continuous improvement

and our aspiration is always to do better.” (Financial Report 2003 pg. 1) In the next stage the

reader/shareholder receives information how this will be done, therefore the report

continuous with plans, specifically it was said, that they will shape the store locations and

products to the needs of the customers. To achieve this goal, M&S will further built on social

responsibility; thereby the ongoing progress is mentioned as well. The information is given,

that they are ranked among the 24 companies with the highest business responsibility index.

There are various examples which explain long-term goals and strategies in this report,

because some investments start functioning at a later time-point. The balance sheet, as a

snap shot, then shows its disadvantages.

Lastly, the report outlines reasons and consequences of the financial management and other

areas for management, even though the consequences were negative, e.g. it was stated that

“property, repair and renewal costs of £335m have increased by 8.0%, largely as a result of

the sale and leaseback transaction entered into last year, which added £15m to rental costs

this year” (Financial Report 2003 pg. 6). Leaseback can also be seen as a short-term source

of finance, which has changes in rights, but less taxation.

The Hermes principles are use to evaluate whether a company is a suitable investment. The

principle one at its wider explanation states an interesting point: “If a company’s share price

is to low, it probably reflects fundamental doubts about its prospects. Where this is the case,

and management is confident that the business is worth more, it is quite appropriate that they

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

5/22

05.03.2009

should respond by reappraising the capital structure and, if appropriate, buying back their

own shares.” (Principle 1 Hermes Principles)

First of all this must be seen in an international context, because not every “law on stock

companies” allows to purchase own shares, e.g. the German AktG., where there are only a

very few individual cases. (Leven and Helm 2006)

There had been an enormous purchase of own shares in the financial report 2005. As

“owned company shares” do not receive dividend payments M&S could reduce the total

amount of money available to shareholder and pay more dividends. This will optimise the

capital structure, but this discussion will be led later in this report.

However the key point of this part of the principle is that the company believes that the future

share price will increase, because their actual prospect is undervalued. M&S will then sell the

shares at a higher share price level to (financially literarily spoken), following Modigliani and

Miller, pay themselves their own dividend. (Handbook pg. 293 -315) The investor, who is

following “only” this approach, will buy shares on this hidden expectation. This discussion will

also be continued later at principle six.

The financial reports from 2003 to 2005 have the UK GAAP standard inherent, while 2006

and 2007 are reported in IFRS. In an overall comparison, there is more information available

in the years of IFRS. Nevertheless, for “non-English-speaking-natives” it is hard to

differentiate between the terms used, when the same operational number is meant.

Sometimes important numbers of the financial report are hidden or hard to identify. In

comparison to Tesco a similar retailer there is the same appearance, e.g. “Cash return on

investment (CROI) is measured as earnings before interest, tax, depreciation and

amortisation, expressed as a percentage of net invested capital” (Financial Report Tesco

2007). The net invested capital is not given in the report, nor is the EBITDA. For a clear

comparison it is necessary to compare numbers of same data content, but in many cases

there has been a different terminology, which makes the investor unsure, if same data

content can be compared.

In conclusion to the communication it can be said, that the “…overall package supports the

Company’s strategy and its commitment to continuous and sustainable enhancement of

shareholder value.” (Financial Report 2007 pg. 44) Which was postulated by Hermes in the

first principle for a suitable investment.

Up to this point we came across various aspects that are of main importance for the other

principles, but in the communication only partially outlined.

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

6/22

05.03.2009

2.2 Principle 2

“Companies should have appropriate measures and systems in place to ensure that they

know which activities contribute most to maximising shareholder value.”

The first measure postulated by Hermes is the WACC. M&S do not display this measure in

their annual reports and it is difficult to identify this number. Surely M&S is operating with this

measure, but they do not want to publish it. However, the investor can assume that M&S

decreases this measure in long-terms, as outlined above. The purchase of shares decreased

the cost of equity capital in both ways, reducing the total dividends to be paid and up to a

certain level of gearing equity capital will be more expensive then debt capital, in either way

of the capital structure debate (the traditional view, the first or the second generation of MM’s

theory). The alternative, “the peaking order theory”, makes future investments in regard to

the sources of finance easy, but it can not change the capital structure reversely. (Handbook

pg. 293 - 314)

To give a deeper analysis of the WACC consideration at Hermes, the level of gearing should

be analysed. Important in this perspective returning to the Hermes principle two is long-term

issue.

Balance

sheet

2007 2006 2005 2004 2003

Net assets

(incl pension

deficit)

1,648.2

1,155.3 909.2 2,454.0 2,108.3

Net debt 1,949.5 1,729.3 2,147.7 1,994.7 1,831.4

Capital

expenditure

792.4 326.8 218.5 433.5 311.0

There are various measures for the gearing ratios. The gearing ration here will be simplified

by dividing the net debt by the net assets (including the pension deficit).

Year 2007 2006 2005 2004 2003

Gearing ratio 118.28%

149.86% 236.22% 81.28% 86.86%

There is a huge variance between the gearing rations. M&S undertook many shifts within the

gearing. Taking the gearing ratio of 2005, we can see that the increased capital expenditure

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

7/22

05.03.2009

decreased to gearing ratio. CAPEX are long-term investments and add value to assets,

which decreases the level of gearing. This will increase the ROI in future therefore. The more

ROI, the more profit, the more profits that can be retained to make future investments with

the lowest source of finance. The shareholders equity increases, which should increase the

WACC, because equity finance is more expensive then debt finance. The WACC as a static

figure can therefore be misleading in the financial management. M&S do not display the

WACC figure in their annual report and therefore do not fulfil the 2nd principle, viewed from

this perspective. Nevertheless, this figure could be in the recent year, compared to the years

before, misleading, if the assumptions set above are correct. Furthermore M&S did not go on

the so called CAPEX holidays to increase short-term profits. M&S increased the CAPEX

sharply for their long-term orientation, which is in accordance with this Hermes principle.

A next part of this principle lays the emphasis again on long-term shareholder value, which is

measured best in cash flow returns. The investor can find key performance measures on

page 96 in the financial report 2007. M&S shows a variety of measures, e.g. return on equity

and retail gearing. Furthermore, they outline in this report the EBITDA the first time and give

an overview of the net cash generated, whereby the EBITDA has a value of 1,329.2m

pounds and the net cash generated amounts 231.1m pounds, which is heavily influenced by

the net capital expenditure (Financial Report 2007 pg. 30). It can be assumed that net capital

expenditure will be lower in the report of 2008. Taking this assumption it can be said that the

net cash generated will increase. The principle from this perspective can be agreed.

The second principle is partially in conflict with the financial reports of M&S, but can generally

be accepted, even though the financial reports for 2003 to 2005 do not have such specific

performance measures in detail. The more important years (2006 and 2007) included these

measures.

The last issue of concern are wider economical factors, e.g. the USA subprime crisis in

summer 2007, which, according to Amerman 2008, increases the interest rates and the

foreign currency portfolio. In this case benchmarks are useful to analyse the true situation.

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

8/22

05.03.2009

2.3 Principle 3

“Companies should ensure that all investment plans have been honestly and critically tested

in terms of their ability to deliver long term shareholder value.”

This principle can only be assumed to be fulfilled. One investment plan is the store

refurbishment programme, which is a long-term investment. As Sir Stuart Alan Ransom Rose,

Chief Executive of M&S, states in respond to the recent crisis at Marks and Spencer “…we

are not in it for just a 12 month game, we are planning here for what happens in 2012.”

(Times Online 2008)

M&S will stick to this investment, as the progress is at 70%, and maintain market share also

by continuing “…to keep its pricing competitive.” (Jameson 2008)

Speculative, investors can assume, that at least this example shows an investment plan,

which was critically and honestly evaluated, otherwise this situation might have the outcome

to stop store refurbishment programme. Following the thought this principle can suits M&S.

The annual report has also a corporate governance statement inherent. Thereafter the Chief

Executive is responsible for “…all aspects of the management of the Group and its business,

which includes developing the appropriate business strategies for Board approval and

achieving timely and effective implementation. He ensures that, within the strategies agreed

by the Board, appropriate objectives and policies are adopted for each area of the business,

that appropriate budgets are set and that their performance is effectively managed in keeping

with the Group’s values and business principles.” (Financial Report 2007 pg. 35)

M&S seeks to ensure critical and honest investment plans by setting a manager of high level

in place. The long-term aspects are not named directly, but they are in the business

principles of M&S. For more information, investors may analyse background information of

Stuart Rose.

This principle can partially be agreed. The investor can use historical facts for his

consideration; therefore compare the strategy set, the progress, the sustainability and the

long-term usefulness. Other information is given by the corporate governance statement,

which shows reporting channels, tasks and principles for investment plans in an overview.

2.4 Principle 4

“Companies should allocate capital for investment by seeking fully and creatively to exploit

opportunities for growth within their core businesses rather than seeking unrelated

diversification. This is particularly true when considering acquisitive growth.”

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

9/22

05.03.2009

M&S has the following departments and therefore they had invested in those: “women, Per

Una, Lingerie, entertainment, men, kids, travel (hereby luggage, travel money and travel

insurance), for the home, technology, E-catalogues, flowers & gifts, food and wine and M&S

Money (e.g. loans, insurance)” (Marks and Spencer Homepage). Usually M&S can be

summed up to be a retailer, whereby M&S money can be seen as unrelated diversification.

However in the financial report 2005 M&S stated that they “…closed Lifestore, acquired per

una, returned £2.3bn to shareholders and sold M&S Money, our Financial Services business,

to HSBC.” (Financial Report 2005 pg. 2) Nevertheless, the business M&S Money, “…which

will continue to operate under the M&S Money brand, will be developed by the respective

efforts of HSBC and Marks & Spencer.” (HSBC 2004)

To focus on core competencies M&S sold M&S Money, therefore the unrelated diversification

was abolished, on the other hand M&S made acquisitive growth by buying per una. Per una

can be seen as an expansion of the range of woman’s wear.

As outlined M&S has a range of related diversification to spread their risks. The risk

reduction by selling M&S money might have influence their rating or rating agency and

therefore reduced their cost of debt finance.

The threat of Hermes at a conglomerate takeover, which “…occurs when the predator and

the target companies are in industrial sectors that have no connection” (Handbook pg. 324),

is, that while the company seeks to reduce their risk by doing so, they actually buy’s a new

factor of risk. The lack of core competencies and the reduction to focus the core business

might lead to disorientation and a loss in both businesses. At reconstruction by a horizontal

or vertical takeover the company could gain advantages, such as synergies, gaining market

share, an increased know-how, more efficient utilisation of assets or economies of scale,

which are maximizing profit and reducing costs and are therefore financial related.

(Handbook 321 - 351).

However, M&S shows a well balanced and broadly product portfolio as a leading retailer in

UK with many franchisers in many different countries, whereby no business is absorbing

cash, while being supported by others, as stated to be the wrong strategy by this Hermes

principle.

Nevertheless there could be a more fully and creatively exploration to seek opportunities for

growth, on the other hand their current investments, the store refurbishment programme, is

necessary to maintain and regain market share. The store refurbishment programme is too

expensive to allocate capital for other larger investments.

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

10/22

05.03.2009

2.5 Principle 5

„Companies should have performance evaluation and incentive systems designed cost

effectively to incentivise managers to deliver long-term shareholder value. “

This main issue of concern is, that Hermes wants to ensure against is the egocentricity profit

maximisation of managers, in management literature titled agency theory. In general “the

agency problem is said to occur when managers make decisions that are not consistent with

the objective of the shareholder wealth maximisation.” (Watson and Head 2005 pg. 11) The

inconsistency could arise by managers realising their aspirations, ”…these could include a

simple desire for power, or to increase their personal status and wealth”. (Handbook pg. 331)

M&S has a system, which is postulated by Hermes, to give protection against the agency

problem. At M&S “there are two key components of variable pay: an Annual Bonus Scheme

(incorporating a deferred share element) and a Performance Share Plan. Their incentive

system delivers long-term shareholder.” (Financial Report 2007 pg. 44)

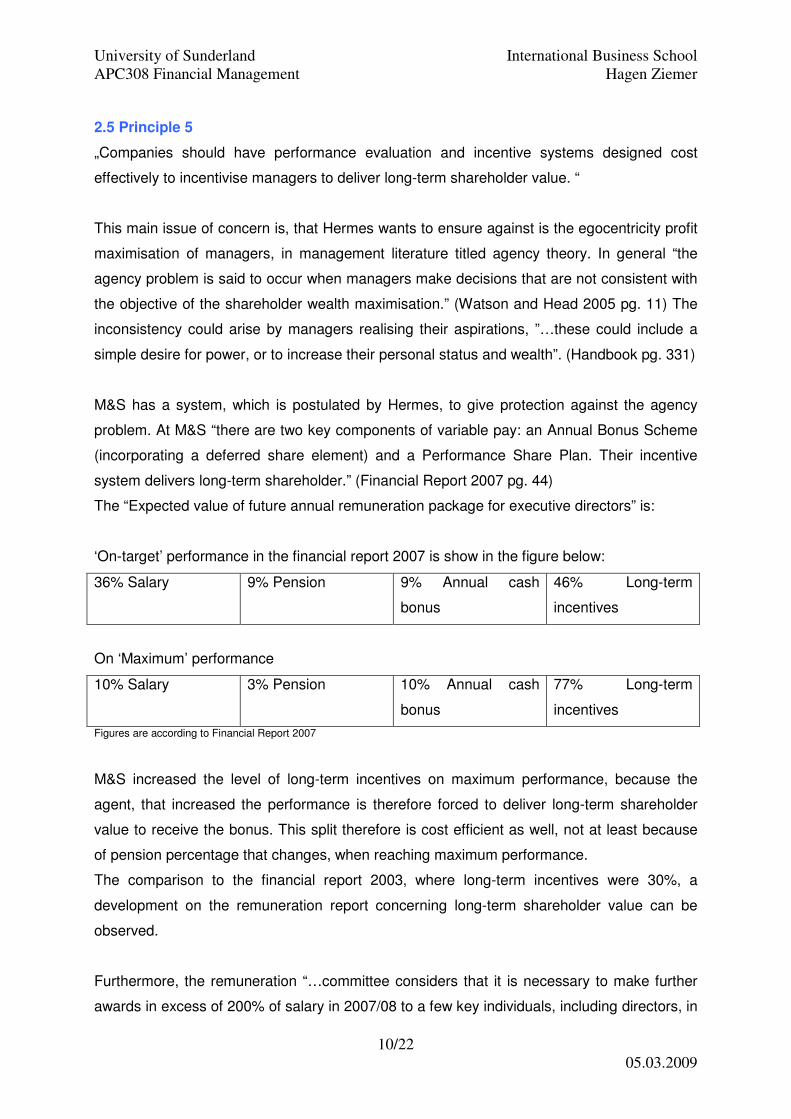

The “Expected value of future annual remuneration package for executive directors” is:

‘On-target’ performance in the financial report 2007 is show in the figure below:

36% Salary 9% Pension 9% Annual cash

bonus

46% Long-term

incentives

On ‘Maximum’ performance

10% Salary 3% Pension 10% Annual cash

bonus

77% Long-term

incentives

Figures are according to Financial Report 2007

M&S increased the level of long-term incentives on maximum performance, because the

agent, that increased the performance is therefore forced to deliver long-term shareholder

value to receive the bonus. This split therefore is cost efficient as well, not at least because

of pension percentage that changes, when reaching maximum performance.

The comparison to the financial report 2003, where long-term incentives were 30%, a

development on the remuneration report concerning long-term shareholder value can be

observed.

Furthermore, the remuneration “…committee considers that it is necessary to make further

awards in excess of 200% of salary in 2007/08 to a few key individuals, including directors, in

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

11/22

05.03.2009

order to ensure that the incentives provided by the Company are sufficient to retain them

over the coming years and to reward them appropriately for achieving excellent results.”

(Financial Report 2007 pg. 44)

These few individuals are part of the policy at M&S and agree further point of this Hermes

principle, to retain appropriate staff, which is essential for long-term performance of a

company. M&S therefore has the fulfilled this principle.

2.6 Principle 6

„Companies should have an efficient capital structure which minimises long-term cost of

capital. “

There has already been a detailed WACC and capital structure discussion of M&S in

principle two of this report. This section will give a wider content of deliberations met by M&S

concerning the efficient capital structure. At principle one the purchase of own shares has

already been outlined. This section will give a deeper discussion of this topic as well.

Year 2003 2004 2005 2006 2007

Profit for the

year

attributable

to

shareholders

480.5 552.3 587.0 586.2 523.1

Dividend

payments in

total

(246.0) (263.2 (203.3) (239.7) (204.1)

Single

dividends in

total

10.5p 11.5 12.1 14 pence 18.3 pence

Figures from 2003 – 2006 taken from five year review

Figures from 2007 taken from the Financial Report 2007

The “profit for the year attributable to shareholders” of the years displayed in the table does

not vary in extensively, with a maximum variance of 18.14% (between 2003 and 2005).

Nevertheless the value of “dividend payments in total” balances the “single dividends in total”

with the outcome that the “single dividend in total” increases slightly, but constantly. This can

be seen as their dividend policy, which follows the traditional view in the dividend decision.

Dividends are relevant to shareholder wealth. “Investors prefer dividends to capital gains on

their shares” (Handbook pg. 297), because dividends carry certainty while retaining the

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

12/22

05.03.2009

“profit attributable” to shareholders will be reinvested and therefore carry uncertainty. The

reinvestment could fail so the wealth of shareholders would decrease. Furthermore, “the

announcement of the payment of a dividend has effect of positive publicity, inspiring investor

confidence in the company” (Handbook pg. 297). Marks and Spencer plc does provide

confidence among shareholders by increasing dividend payments constantly. This

confidence decreases the expected risk of shareholders and therefore the expected

dividends. Furthermore their retaining profits ensure future dividend payments at an ongoing

increasing level and minimization of the weighted average cost of capital (WACC), which

should provide an efficient capital structure. The WACC decreases on both sides, since

retained profits are the cheapest source of finance, the cost of equity and the cost of debt

finance. Reducing the debt level or the level of gearing bears less risk of payback to creditors

and therefore the interest rate such as the total amount of interest to be paid.

In 2007 the “dividend payments in total” are less the in 2006 even though the “single

dividends in total” increased by 4.3 pence. The financial management of M&S purchased

own shares at the high value of 2,300.0m pounds (Financial Report 2005 pg. 52) to reduce

equity costs, because there are no dividend payments on “company owned shares”.

Therefore it was possible to maintain an increase of dividend payment, while reducing

“dividend payments in total”. The cost for equity capital is reduced through both, the

purchase of shares and the retained profit. The retained profit reduces the cost of debt

financing as well.

Own funds or retained profits are needed for financing fixed assets, which have increased

from 218.5m pound to 792.4m pound. According to Heyd 2001, an international valid rule of

thumb says, that fixed assets should preferably be financed by equity. The main problem for

the company was therefore of how to increase equity. It was carefully arranged by

repurchasing own shares in the market, amounting 2.3bn pounds. This was sufficient to

finance 573.9m pounds within two years and to reconstruction the capital structure.

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

13/22

05.03.2009

2.7 Principle 7

“Companies should have and continue to develop coherent strategies for each business unit.

These should ideally be expressed in terms of market prospects and of competitive

advantages the business has in exploiting these prospects. The company should understand

the factors which drive market growth, and the particular strengths which underpin its

competitive position.”

The Chief Executive of M&S states in every financial report strategic plans for the whole

organization usually in five year terms. Examples of this for the report 2003 have already

been outlined in the communication principle.

The financial report 2007 shows deeper explanations of their major goals and strategies.

These major goals or strategies are developed in long terms. The development of each

strategy is shown, the future goal of the strategy, such as methods to achieve this, e.g. the

major strategy was to increase service and their method is mystery shopping.

An other example is the global expenditure strategy, whereby M&S strategy is “…to focus on

markets where there’s a strong demand for our products from a growing middle class.”

(Financial Report 2007 pg. 24)

However, they do not outline estimated future cash flows, even though plans have already

been clear: “we will open another store in Tallaght later in the year.” (Financial Report 2007

pg. 24)

Nevertheless, improvement of employees and the global marketing strategy can not be

related to particular business units, because they carry overall character.

The “Plan A” of M&S is a very detailed prospect within their “How we do business report”,

also outlining: What has to be done? Who with? and When? Whereby the investor can

separate this core plan into different business units. The Plan A is their “…five-year, £200m,

100-point ‘eco plan’. It will touch every part of M&S, transforming the way…” (How we do

business report 2007 pg. 7) M&S does business, which relates to their competitive

advantage. One of their competitive advantages, which they also built on with Plan A is their

excellence in food, which they won a award for in 2006 (Financial Report 2007 pg. 20).

Therefore M&S fulfils the requests of this Hermes principle.

Referring to the BCG matrix future investments will be made were market growth meets

market share of the company. The new green segment relates to the premium products, with

high profit margins. Higher profit margins and the competitive advantage provide more

confidence to debtors and shareholder (e.g. such as Hermes), which could result a lower

WACC.

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

14/22

05.03.2009

The bottom line is that M&S assess their competitive advantage, give goals, develop core

strategies, review those, such as particular strategies, in exception they outline the methods,

which can be related to the different business units.

2.8 Principle 8

“Companies should be able to explain why they are “best parent” of the businesses they run.

Where they are not best parent they should be developing plans to resolve the issue.”

In principle 4 was already mentioned the case of divesting M&S Money, which has not been

their one of their core competencies. This followed the postulation of this principle to divest a

business, when it “…would generate greater value if it were independent or managed by

another corporate body…” (Hermes Principle 8).

Per Una has already been mentioned as well as a subsidiary of Marks & Spencer, which was

bought. Communicating to be the “best parent” is at a take-over an important price factor. A

bad communication by the predator, in terms of not stating the advantages of the takeover or

the explanation why the predator is the “best parent”, could be huge price driver.

It can only be assumed that they communicate to their subsidiaries why they are the “best

parent” and since they divest subsidiaries it can also be assumed that they do so.

In the financial report it can be found, that they are communicating the success of their

subsidiaries, which can be seen as a part of showing to be the “best parent”, e.g. “‘Per una’

continued to grow strongly in the year, with sales of £423.5m, as it celebrated its fifth birthday

with strong ranges from ‘Collezione Italia’ fashion flair to stylish eveningwear and a

relaunched jeans collection.” (Financial Report pg. 13) This principle at this set of

assumptions fulfils this principle.

2.9 Principle 9

“Companies should manage effectively relationships with their employees, suppliers and

customers and with other who have legitimate interest in the company’s activities.

Companies should behave ethically and have regarded the environment and society as a

whole.”

Good stakeholder relations are necessary to provide long-term sustainability of a company.

Pension funds which must have long-term stabilized returns are therefore interested in good

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

15/22

05.03.2009

stakeholder relationships. These relations can be used for marketing campaigns to provide

consumers confidence, which should generate long-term cash inflows. Cash inflows are most

important for survival of companies. M&S is engaged in various programmes stated in their

CSR (corporate social responsibility) report, which published on the M&S website. In

England the corporate social responsibility of M&S should be common knowledge, as they

won several awards in this area, e.g. in regard to environment M&S reduced their CO2

emissions from 404,000 tonnes to 296,000 tonnes within one year. (Financial Report 2007

pg. 2). According to the financial report 2007, an independent research shown that M&S is

the most trusted retailer in the UK. (Financial Report 2007 pg. 19)

2.10 Principle 10

“Companies should support voluntary and statutory measures which minimise the

externalisation of cost to the detriment of society at large.”

The reduction of CO2 emission expressed in tonnes can be seen as a voluntary reduction of

costs, whereby the measure is the number of tonnes. The EU commission bounded the CO2

emission at a maximum volume of 1.72bn tonnes for the whole EU. (Becker 2008) The

European Union members would otherwise have to stabilise the M&S voluntary reduced

amount of 108,000 tonnes. M&S paid for their voluntary reduction of CO2, but they might be

able to set down the budget for advertising, because the media might communicates this to

society. This would increase customer satisfaction and increase sales. M&S might have set

measures to evaluate the “real costs” for actions that carry voluntarism, but these measures

are not published.

Word count for part A

Total number of words Words cited (incl. headings,

references and tables)

Net words

4341 1175 3166

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

16/22

05.03.2009

3. Part B)

You should critically evaluate how useful you found the Hermes principles when

carring out your evaluation, and what changes you think might improve these

principles.

3.1 Limitations and criticism on the 10 Hermes principles

For a critical evaluation of improvement of the ten Hermes principles a set of criteria is

needed. The following points can be criticised respectively carry no consideration at all by

the Hermes principles: competition within the industry, measures outlined with deeper

explanations of meaning, statically aspects, market, economical and population

developments, and lastly an international investment perspective.

3.1.1 Competition within the industry

The growth and the strategies of competitors are left beside in the Hermes principles.

Hermes might include benchmarking with both, the strongest competitor and the industry as

a whole. Hermes could add reactive strategic management to competition. Therefore

benchmarking was left aside in this financial analysis.

3.1.2 Measures

Even though Hermes names a number of measures, these could be more and with further

explanations of a deeper context. As they state that shareholder value “...is best measured

in cash flow returns...” (Hermes principle 2) and as investors is benchmark the market growth

rate of two companies a refurbishment programme, e.g. currently at M&S, might influence

the cash inflow of the one company. Following this the investor might invests into the wrong

company in the long term. Another point of concern might be the transparency and

consistency of measures to compare same numbers in same years of one company or to

compare same numbers of two different companies. A company might take another, but a

similar measure of performance to beguile consistency or improvements.

3.1.3 Statically Aspects

There is to less emphasis on statically aspects. Even tough financial reports improved

concerning their dynamics, but they still reflect only snap shot of the company. This snap

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

17/22

05.03.2009

shot could be influenced by window dressing. The Hermes principles make whether

statements or give hints concerning window dressing areas, nor for a take-over requirements

of a due diligence, which might give a negative surprise.

As already outlined in the criticism of measures, factors must be analysed, which may affect

these measures in the long term, e.g. CAPEX. Deeper explanations in the Hermes principles

would be useful to show the limits of a balance sheet.

3.1.4 Market, economy and population developments

The Hermes principles do not concern market developments. As a market as a whole

decreases, as the market life-cycle reaches maturity, certain companies can still gain market

share. In long terms however, there will a decrease in sales and therefore a decrease of

shareholder value, in this case thinking of other branches Hermes might invest, e.g. the

automobile sector.

The time point for the investment is not mentioned at all, this could be when the economy is

considered to grow as a whole, after an overall recession. In the actual context the sub-prime

mortage crisis in the USA affects the economies in the world, especially their main trading

partners. This might be another driver an increased WACC.

Another issue which is disrespected is the development of a population. Since principles

carry overall character, all sectors are tackled by these Hermes principles. Currently the

population becomes older and less children are born, a toy manufacturer could experience a

downfall and a wine seller, assuming that an older population drinks more wine, will make

positive experiences. Changes in population are long-term developments.

Before analysing if a company is a good investment, it might be better to analyse if the sector

the company is in is a good investment.

These three factors are three limitations of a balance sheet and partially of a financial report.

3.1.5 Innovation

As innovations are a proven factor for growth, so innovation ratios might be analysed by

investors. Another aspect is the risk of innovations that might destroy a whole sector, e.g. the

actual development stages of “rapid manufacturing”, whereby it is said that this technology

could for example manufacture a T-shirt right next to the user’s computer. Hermes could

therefore ask for scenario planning to reduce this risk, which would further may be rated

positive by rating agencies and therefore decrease the cost of capital.

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

18/22

05.03.2009

3.1.6 International Investments

The Hermes principles give no hints for international investment. The law on stock

companies might differ in particular areas, e.g. the ability to purchase own shares as outlined

in principle one. Furthermore aspects of companies changing accounting standards are left

aside. There might be the postulate of Hermes that companies should publish the changes in

terminology.

3.1.7 Other Aspects

There are many other aspects, such as relevancy of properties and investment properties,

goodwill developments, scandals in history that might come back, the personalities and

backgrounds of leaders of a company and the actuality of financial reports, which could

partially be balanced by analysing press releases.

3.2 Usefulness for investors and level to apply these principles to companies listed on

the London Stock Exchange

The usefulness and the level to apply these principles on the London Stock exchange can be

divided into the following criteria: comprehensibility, compactness, easiness to apply and

generality.

3.2.1 Comprehensibility

The principles are easy to understand, well written and underpinned with further explanations

as well as supported by examples. The formulations are written in a professional style, but

investors will be aware of it. The further explanations ensure no doubts about how things are

meant and why these should be so.

3.2.2 Compactness

The 10 principles cover major criteria for long-term investments. Investors using these

principles have a very well package of criteria. The principles have more points inherent then

expected at first view. The further explanations go very deep into financial management by

giving particular hints, e.g. the purchase of own shares, when a company estimates to be

undervalued; even though this could be to prevent a takeover by a predator, but a takeover

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

19/22

05.03.2009

should be known of by investors. The aim of these principles is to identify companies that

give long-term shareholder value. Some principles, e.g. the 10th, measures which minimise

externalisation of cost, do not seem, from the beginning on, to have a relationship to

shareholder wealth and investors might not think in such a deep sense. Therefore it can be

stated that these principles are very compact.

3.2.3 Easiness to apply

Bearing in mind the complexity of the principles it can be said they are easy to apply,

because they are clear to understand, well described and focus on specific areas. The

investor can look up these specific areas in most cases in the financial report –since the

PDF-document search functions even much faster then ever.

In general, however, it must be said, that information which is not directly given by M&S has

to be identified or estimated by the investor. This may courses a lot of effort. The investor

needs to think about how to estimate these requirements of the principle which are not

directly communicated by the company. The investor in this task is partially supported by the

examples given in the further information of the principle. The level to apply these principles

can be stated to be low for the complexity they give.

3.2.4 Generality

The example outlined (M&S) has shown that these principles can be applied to the company.

Furthermore these principles seem to have overall validity, excepted by the limitations as

outlined above. At the London Stock Exchange all companies report in IFRS and the Hermes

Principles can therefore be applied with a minimum of effort, whether a company is a suitable

long-term investment or not.

Word count for part B

Total number of words Words cited (incl. headings,

references and tables)

Net words

1251 81 1170

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

20/22

05.03.2009

II. Conclusion

Marks and Spencer plc has been financially analysed, by the ten principles postulated by

Hermes. M&S fulfils all principles to an acceptable point, so Hermes investors should invest

in M&S, if they have not already.

The ten principles are a useful guideline to make long-term investments. They can be seen

as a compacted package, but they have certain limitations. These limitations are wider

factors of economy, statically aspects, comparisons with competitors and issues of the

companies.

The last two principles will gain importance in future, because humans become more and

more psychologically sensitive. Plan A is a major strategy of M&S, recognising the last two

issues, and can been seen as a future development.

Financial management, however, is more then discounting cash flow, assessing risk and to

optimise the capital structure etc. Financial management is interrelated with all areas of a

company. The contemporary developments give financial management a more and more

dynamic character. Investors need to understand that balance sheets are a snap shot, a

static picture, which can be influenced by companies, e.g. by window dressing, at least to the

time point where companies have to publish balance sheets every day.

The current crisis on financial markets keeps on going. Banks try with tenders to prevent the

worst case. The financial economy is faster then the rest of the economy, therefore this gives

interesting time points for investments, e.g. an investment in Marks and Spencer plc.

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

21/22

05.03.2009

III. References

Becker, S. (2008). EU-Kommission beschränkt CO2-Emissionen 2020 auf 1,72 Mrd t.

Aailable at: http://www.finanznachrichten.de/nachrichten-2008-01/artikel-9939934.asp

Heyd, R. (2001). Die Kunst Bilanzen zu lesen. Anleitung zur treffsicheren Bilanzbeurteilung.

7. überarbeitet Auflage.

HSBC Webpage 2004. [online]. available at: http://www.hsbc.com/1/2/newsroom/news/news-

archive-2004/hsbc-and-marks-and-spencer-complete-the-sale-of-mands-money-

Jameson, A. (2008). Marks & Spencer shares plunge on first sales drop in two years. [online].

Available at:

http://business.timesonline.co.uk/tol/business/industry_sectors/retailing/article3157745.ece?t

oken=null&offset=12

Leven, F. and Helm, L. (1996). Der Erwerb eigener Aktien - Ein notwendiges Instrument

der Unternehmensfinanzierung. BVH-News & Aktienkultur. [online]. Available at:

http://www.dai.de/internet/dai/dai-2-

0.nsf/0/41256A99002BDD55C12569A4003EB10A?OpenDocument

Marks & Spencer (2003). Annual Report 2003. [online]. available at:

http://www.marksandspencer.com/gp/node/n/57101031/202-0888916-

5797444?ie=UTF8&mnSBrand=core

Marks & Spencer (2004). Annual Report 2004. [online]. available at:

http://www.marksandspencer.com/gp/node/n/57101031/202-0888916-

5797444?ie=UTF8&mnSBrand=core

Marks & Spencer (2005). Annual Report 2005. [online]. available at:

http://www.marksandspencer.com/gp/node/n/57101031/202-0888916-

5797444?ie=UTF8&mnSBrand=core

Marks & Spencer (2006). Annual Report 2006. [online]. available at:

http://www.marksandspencer.com/gp/node/n/57101031/202-0888916-

5797444?ie=UTF8&mnSBrand=core

University of Sunderland International Business School

APC308 Financial Management Hagen Ziemer

22/22

05.03.2009

III. References

Marks & Spencer (2007). Annual Report 2007. [online]. available at:

http://www.marksandspencer.com/gp/node/n/57101031/202-0888916-

5797444?ie=UTF8&mnSBrand=core

Marks and Spencer (2008). Homepage. [online].Accessed on 29.03.2008. Available at:

http://www.marksandspencer.com/gp/node/n/42966030/202-0888916-

5797444?ie=UTF8&mnSBrand=core

Marks and Spencer (2008). How we do Business. [online]. Available at:

https://images-na.ssl-images-amazon.com/images/G/02/00/00/00/32/17/82/32178202.pdf

Tesco (2007). Annual Report 2007. [online]. Available at:

http://www.tescocorporate.com/page.aspx?pointerid=40B6E68B255B44ECADF894ACA012

D4FF

University of Sunderland BA (Honours) Business Management, Financial Management.

Version 7.0, Prentice Hall.

Watson, D. and Head, A. (2007). Corporate Finance Principles & Practice. 4th edition. New

York, Prentice Hall.