Embed Size (px)

Citation preview

Dubai Real Estate MarketREVIEW: SECOND QUARTER 2015

www.valustrat.com

1 | ValuStrat - Real Estate Research Report - Quarter 2, 2015 www.valustrat.com | 2

ValuStrat in the Media

- Dubai’s residential values retreat to 2014 levelsDubai’s residential property values have shed most of the premium they had put on at the peak of the upturn in June 2014, with average prices now hovering to what they were during January last year. This is according to the newly created ValuStrat Price Index, which also found that the correction was most pronounced at JBR and Downtown. The Palm also saw some of this, the ValuStrat report adds.

- Lower prices, higher yields: Right time to invest in Dubai property?Local consultancies such as ValuStrat have revealed that time is right for renters in the emirate to become homeowners as equated monthly instalments fall below their monthly rental outgo. However, one thing has to be remembered that it is now mandatory for a purchaser to put 25 per cent as down payment for completed properties.

- Marginal decline in Dubai rents give advantage to Sharjah tenants “ There are no master-planned developments in Sharjah. However, some of the towers are very well-built with quality fit-out and generous floor areas. Negatives include the lack of parking and on-site amenities such as gyms and swimming pools,” says Declan King, Director and Group Head — Real Estate, ValuStrat.

- Dubai Metro boosts

home valuesIn April, a ValuStrat study said properties within a 10-minute walk of new Dubai Metro stations proposed on the Red Line extension are likely to see an uplift in value even before the line becomes operational. Once operational, prices could rise by up to 15 percent compared to similar homes located further from the metro stations, the research intelligence firm said.

- Properties near Dubai

metro cost a premiumValuStrat’s research showed that studio apartments near a metro station in JLT are difficult to find and can command a price of around Dh750,000 to Dh900,000, a far cry from the studios in Jumeirah Village Circle or Dubai Silicon Oasis which are being offered for a little over Dh400,000.”Prices for studio apartments within five to ten minutes walking distance commanded a premium of up to 20 per cent. You can expect to pay an extra Dh150,000 for the privilege,” said ValuStrat research manager Haider Tuaima.

18 June 2015 17 June 2015

17 June 2015 10 June 2015

3 June 2015 19 May 2015

- Alternative Real Estate Asset ClassesMany real estate investors in the UAE

automatically think of residential villas or

apartments when they consider buying

property. However, both at home and

abroad, there are a number of

alternative sub-classes within the real

estate sector that a buyer can consider

strategic.

27 May 2015

- The Big PictureReal Estate strategist ValuStrat recently

compiled a report highlighting the

“substantial opportunity for investment in

affordable stock”, particularly family

apartments. Declan King, Director and

Group Head of Real Estate at ValuStrat, says

affordable housing presents a

“considerable investment opportunity” for

developers and investors due current

shortfall.

3 | ValuStrat - Real Estate Research Report - Quarter 2, 2015 www.valustrat.com | 4

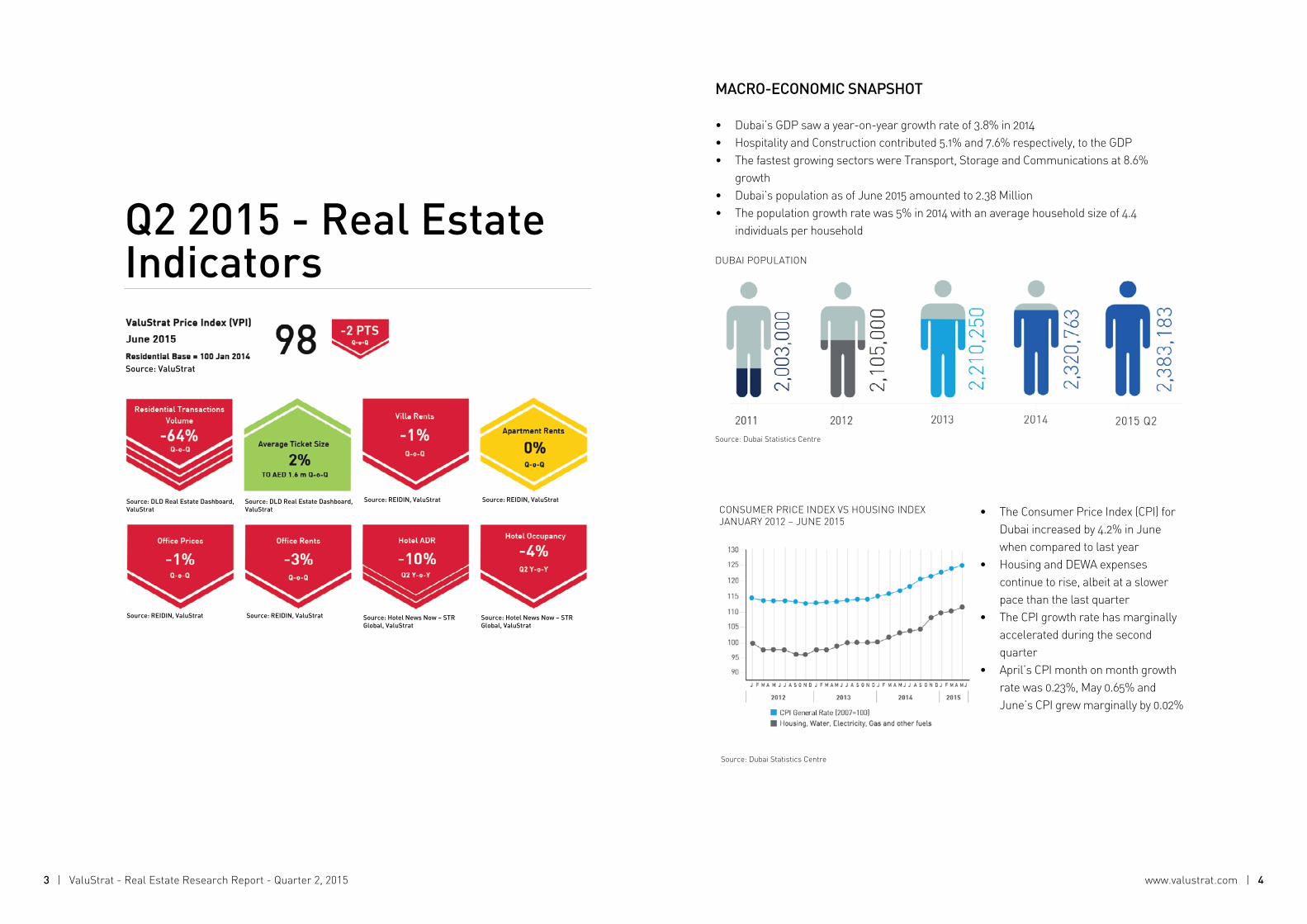

Q2 2015 - Real Estate Indicators

MACRO-ECONOMIC SNAPSHOT

• Dubai’s GDP saw a year-on-year growth rate of 3.8% in 2014• Hospitality and Construction contributed 5.1% and 7.6% respectively, to the GDP• The fastest growing sectors were Transport, Storage and Communications at 8.6%

growth• Dubai’s population as of June 2015 amounted to 2.38 Million• The population growth rate was 5% in 2014 with an average household size of 4.4

individuals per household

• The Consumer Price Index (CPI) for Dubai increased by 4.2% in June when compared to last year

• Housing and DEWA expenses continue to rise, albeit at a slower pace than the last quarter

• The CPI growth rate has marginally accelerated during the second quarter

• April’s CPI month on month growth rate was 0.23%, May 0.65% and June’s CPI grew marginally by 0.02%

Source: Dubai Statistics Centre

Source: Dubai Statistics Centre

Source: DLD Real Estate Dashboard, ValuStrat

Source: REIDIN, ValuStrat Source: REIDIN, ValuStrat

Source: REIDIN, ValuStrat Source: REIDIN, ValuStratSource: DLD Real Estate Dashboard, ValuStrat

Source: Hotel News Now – STR Global, ValuStrat

Source: Hotel News Now – STR Global, ValuStrat

DUBAI POPULATION

CONSUMER PRICE INDEX VS HOUSING INDEX JANUARY 2012 – JUNE 2015

Source: ValuStrat

5 | ValuStrat - Real Estate Research Report - Quarter 2, 2015 www.valustrat.com | 6

ValuStrat Price Index - Residential

Residential

• After an 11% YoY decline, residential price declines are expected to decelerate over the remainder of 2015

• Dubai apartment and villa markets saw values decline by 2.5% and 2.1% QoQ respectively

• The median value for apartments in June was AED 14,250 per sq m (AED 1,324 per sq ft) and for villas was AED 14,725 per sq m (AED 1,368 per sq ft)

• Compared to Q1, apartments in Business Bay saw an average value decline of 6%, followed by a 4% decline in International City, Dubai Sports City and Discovery Gardens

• Villas in Arabian Ranches, Jumeirah Park and Al Furjan saw an average value decline of 3% when compared to the last quarter

By tracking the values of a fixed basket of properties in 26 locations around Dubai, the ValuStrat Price Index (VPI) has shown a steady decline in property values since the peak during the second quarter last year. However, the rate of decline is easing and is expected to continue to decelerate over the remainder of the year. April’s VPI registered 99.5 points, almost on par with January 2014, while May and June registered 98.9 and 98.4 points respectively.

RESIDENTIAL SUPPLY

• An expected supply of 26,100 apartments and 2,400 villas in 2015 will bring the total number of residential units in Dubai to almost half a million

• Residential projects with approximately 3,000 units initially scheduled for completion this year are delayed and due for handover during 2016

• 5,400 units were completed during the first half of 2015

• A further 26,200 apartments and 2,300 villas to be completed in 2016

• 18 off-plan residential projects were launched in Q2 adding 5,000 units to the residential pipeline by 2019

RESIDENTIAL PRICES

• According to the DLD Real Estate Dashboard, residential transaction volume plummeted by 64% when compared to Q1 2015, with a marginally higher average ticket size of AED 1.6 Million

• Average residential transaction prices witnessed negative trend year on year, declining by 12.7%

• When compared to the previous quarter, average residential prices dropped by 5.5%

• The median transacted apartment price stands at AED 11,560 per sq m (AED 1,074 per sq ft)

• The median transacted villa price stands at AED 13,024 per sq m (AED 1,210 per sq ft)

Source: REIDIN, Lookup, ValuStrat

Source: REIDIN, ValuStrat

Source: ValuStrat

VALUSTRAT PRICE INDEX – DUBAI RESIDENTIAL SECTOR [BASE: JAN 2014=100]

DUBAI AVERAGE RESIDENTIAL PRICE PERFORMANCE

DUBAI RESIDENTIAL SUPPLY 2013-2016(‘000 UNITS)

OfficeOFFICE SUPPLY

• 2015 began with an estimated 7.88 Million square meters (84.8 Million sq ft) of office Gross Leasable Area (GLA)

• 580,000 sq m (6.2 Million sq ft) GLA is expected to be delivered during 2015 and 550,000 sq m (5.9 Million sq ft) during 2016

• One key completion this quarter was The Binary by Omniyat, delivering 45,150 sq m (486,000 sq ft) of GLA in Business Bay

OFFICE PRICES

• Office prices dipped by a marginal 0.3% year on year

• Negative growth of 1% seen during this quarter when compared to the previous quarter

• Average prices of shell and core office space in Downtown Dubai ranged from AED 20,450 – 25,830 per sq m (AED 1,900 – 2,400 per sq ft)

• Average prices in Business Bay ranged from AED 9,700 – 15,000 per sq m (AED 900 – 1,400 per sq ft)

• TECOM & JLT average office prices remained similar to last quarter

OFFICE RENTS

• YoY asking rents continue to see double digit increase, currently standing at 11.8%

• Quarter on quarter asking rents are down by 3%

• The median asking rent for office space is AED 1,184 per sq m (AED 110 per sq ft)

• DIFC saw the highest asking rents of AED 2,500 per sq m (AED 232 per sq ft)

Source: REIDIN, ValuStrat Source: REIDIN, ValuStrat

Source: REIDIN, ValuStrat

7 | ValuStrat - Real Estate Research Report - Quarter 2, 2015 www.valustrat.com | 8

RESIDENTIAL RENTS

• Residential asking rents dipped by 2.1% when compared to the same period last year

• Overall residential asking rents remained stable since the start of 2015

• Apartment asking rents saw a 2% decrease since last year

• On average, apartment rents saw no change during H1 2015

• Villa asking rents dipped by 3% YoY and 1% QoQ

DUBAI AVERAGE RESIDENTIAL ASKING RENT PERFORMANCE

Source: REIDIN, Lookup, ValuStrat

DUBAI OFFICE SUPPLY 2012-2016(MILLION SQ M GLA)

DUBAI AVERAGE OFFICE PRICE PERFORMANCE

DUBAI AVERAGE OFFICE ASKING RENT PERFORMANCE

RETAIL SUPPLY

• Downtown Dubai represents 15% of the total retail mall GLA in Dubai, this figure will grow due to expansion work for Dubai Mall and the announced extension within Emaar’s recently announced Downtown Views

• 100 out of 145 outlets were leased at The Pointe by Nakheel

• 55% of The Nakheel Mall has been reported as leased

• Nakheel launched additional 71,000 sq m (766,000 sq ft) of retail space at Ibn Battuta Mall’s new extension

• Damac launched Vista Lux at Akoya Oxygen

• Construction has begun on Gate Village Building 11 at DIFC, adding 3,700 sq m (40,000 sq ft) of retail space

HOTEL SUPPLY

• The total number of hotel rooms and hotel apartments at the beginning of Q2 2015 stood at 94,217

• Before the end of the year, Dubai is expected to cross the 100,000 hotel room mark

• 1,557 hospitality units were added in Q2 • New hotel openings include Damac

Maison The Vogue and Pullman Dubai Jumeirah Lake Towers

• Twenty four new hotels were announced adding 7,220 keys to the pipeline in the next 4 years

• Notable hotel announcements included Four Seasons Hotel - DIFC, Studio M, Holiday Inn DWC and Rixos The WalkHOTEL PERFORMANCE

• The average occupancy in Q2 was 75% • April and May saw occupancy rates of 81.7% and 80% respectively, while in June the

occupancy rate fell to a record 63% low due to Ramadan• With increasing new hotel room supply, the average Daily Rate (ADR) for April slipped 7%

YoY, May dropped by 12% YoY and in June by 10% YoY • Further downward pressure on room rates is expected in the next quarter

RETAIL PERFORMANCE

• More global brands recently entered Dubai’s retail market such as Hollister, Cavalli Cafe and McQ Alexander McQueen

• Average prime mall rents for anchors and entertainment ranged between AED 970 – 1,400 per sq m (AED 90 – 130 per sq ft)

• Prime line shop rentals averaged AED 6,700 per sq m (AED 622 per sq ft)

Source: REIDIN, ValuStrat

9 | ValuStrat - Real Estate Research Report - Quarter 2, 2015 www.valustrat.com | 10

Retail Hospitality

Source: REIDIN, ValuStrat

Source: Hotel News Now – STR Global, ValuStrat

Source: Dubai Statistics Centre, ValuStrat

MALLS AND SHOPPING CENTRES IN DUBAI DUBAI HOTEL ROOM SUPPLY 2013 - 2015(‘000 KEYS)

DUBAI HOTEL PERFORMANCE PRIME RETAIL MALL RENTS

MethodologyEvery effort has been made to ensure the accuracy of this document. New supply data covers 38 defined areas in Dubai including non-freehold areas. Only completed and under construction projects are included. The new supply data does not include announced projects, and projects in design phase. The new supply database does not take into account most private building projects. Prices are calculated from actual transactions that have been carefully cleansed to exclude duplicates, bulk sales and outdated transactions. Rental data is derived from a carefully cleansed database of listings that don’t include duplicates, potential errors and outliers.

The ValuStrat Price Index (VPI) for Dubai’s residential sector is constructed to represent the monthly price change experienced by typical freehold residential units within Dubai. The VPI provides an up-to-date opinion of current pricing. The VPI is a comprehensive weighted sample of all property types across the city.

Copyright © ValuStrat Consulting FZCo. 2015This document is the property of ValuStrat Consulting FZCo and must not be reproduced or transmitted in any form or by any means, without the prior written consent of ValuStrat Consulting FZCo. We welcome your constructive feedback and any corrections that may need to be made to this document. ValuStrat Consulting FZCo does not accept any liability in negligence or otherwise for any damage suffered by any party resulting from reliance on this document.

ABOUT VALUSTRATValuStrat is a leading consulting firm headquartered in Dubai providing Advisory, Valuations, Research, Due Diligence and Divestment services across a diverse range of industry sectors since 1977. Offices in UAE, Saudi Arabia and Qatar serve over 750 corporate clients in the Middle East. Client base includes financial institutions, local corporates, multinationals, governments, SME’s, family businesses and start-ups. Some of the key sectors serviced by ValuStrat’s consulting team include real estate, hospitality, healthcare, education, manufacturing, retail, entertainment, transport and FMCG.

Declan King, MRICSDirector & Group Head of Real [email protected]

Haider TuaimaResearch [email protected]

Saad UmeraniChief Operating [email protected]

Vismer Mulenga, MRICSAssociate [email protected]

DUBAI +971 4 326 [email protected]

RIYADH+ 966 11 293 [email protected]

JEDDAH+ 966 12 [email protected]

DOHA+974 [email protected]

ValuStrat is a firm regulated by RICS