Embed Size (px)

Citation preview

Voice of the American Shareholder Voice of the American Shareholder Quarterly Poll – Wave 5Quarterly Poll – Wave 5

Prepared for:Prepared for:

National Association of National Association of

Investors Corporation (NAIC)Investors Corporation (NAIC)

Final ReportFinal Report

March 18, 2005March 18, 2005

2

Table of Contents

Study Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Overview of Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Detailed Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

What Does A Typical Shareholder Look Like, and How do they Behave?. . . . . . . . . . . . . . . . . . . 20

How Do Shareholders Feel about the Economy and Stock Market? . . . . . . . . . . . . . . . . . . . . . . .28

What do Shareholders think about the Current Social Security System? . . . . . . . . . . . . . . . . . . . . 38

How do Shareholders feel about proposed changes to Social Security? . . . . . . . . . . . . . . . . . . . 55

How does the language used influence investors?. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

What do Shareholders think about Boards of Directors and Sarbanes-Oxley?. . . . . . . . . . . . . . . 75

Demographics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Detailed Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

3

Study Objectives

The National Association of Investors Corporation (NAIC) commissioned Harris Interactive to conduct a series of research studies to better understand the attitudes and behaviors of American investors. This study represents the fifth wave of research conducted for NAIC. The previous waves were conducted in September 2003, January 2004, May 2004, and November 2004.

By regularly reporting on these findings, NAIC expects to capture the voice of the American shareholder.

The survey questions are designed to measure a few key trends in shareholders’ portfolios and investing behavior as well as to understand shareholders’ attitudes and views toward current issues. Specifically, this wave of research focused on the following topics:

Investment profile, goals, strategy, and future plans;

Views toward the stock market;

Perception of the current Social Security system, views toward proposed changes, and impact of these changes on investors; and

Views toward corporate governance issues

4

Overview of Methodology

Sample includes 1,175 shareholders defined as U.S. adults aged 18 or older who currently own individual stocks or stock mutual funds.

A subset of questions about perceptions of the current Social Security system were also asked of non-shareholders, 2,847 U.S. adults aged 18 or older who do not own individual stocks or stock mutual funds.

Questions about proposed changes to Social Security were asked in two ways. About half of respondents were asked about private accounts and roughly half were asked about personal accounts.

To be consistent with President Bush’s use of “personal accounts,” the term personal will be used throughout this report.

Interviewing was conducted between February 15 and 25, 2005.

The interview averaged 10 minutes in length.

All interviewing was conducted online using the Harris Poll Online (HPOL) database consisting of several million members who have agreed to participate in survey research.

5

Executive SummaryExecutive Summary

6

Executive SummaryExecutive Summary

The general public, and specifically shareholders, believe that our current Social Security system is very much or somewhat in a state of crisis and that fundamental changes are needed. They recognize the problem and are not unwilling to sacrifice in order to strengthen the future of the system; however many are not optimistic about the availability of benefits for future generations. And most disagree with President Bush about the best course of action to follow.

Nearly two-thirds believe the current system is very much or somewhat in a state of crisis, and more than half believe that while there are some good things in the current system, fundamental changes are needed.

The top problems cited with the current system are that there will be too few workers in the future to support the number of retirees and that some people who do not need benefits are receiving them.

Specifically, more than half of shareholders cite too few workers in the future as the top problem with the system.

A majority of shareholders think it is somewhat or not at all likely that their children or grandchildren will receive their Social Security benefits.

The proposal with the greatest level of support from shareholders (69%) is that the income level subject to Social Security tax should be increased, a finding which holds true even among those with incomes of $75,000 or more. Furthermore, shareholders feel that increasing the income level would be among the most effective changes to make to guarantee that current and future generations receive their benefits.

Many shareholders oppose and fully one-third strongly oppose President Bush’s proposal to reform Social Security.

While language itself (private vs. personal) did not have a significant impact on shareholders’ views, party affiliation (Democrat vs. Republican) did, with Republicans being much more supportive than Democrats of the overall idea of personal or private accounts.

7

Executive SummaryExecutive Summary

Despite such strong disapproval of the President’s plan, shareholders recognize that there may be positive impacts as a result of the creation of personal accounts. Paradoxically, many are not ready to commit their own money. To reap those potential benefits, education would be necessary for those not familiar or comfortable with investing.

Many people are in favor of the idea that people should have the choice to decide how some of their Social Security payroll tax is invested.

Three-quarters of shareholders agree that most people are not knowledgeable enough about investing to benefit from these accounts, however, an even higher proportion (82%) think that if personal accounts are created, the government should provide education about how to invest.

Similar proportions agree that personal accounts would make the stock market accessible to those who would not otherwise have access and over half agree that these accounts will increase the amount of money available to retirees.

Overall, fully one in five shareholders would not invest anything in personal accounts and more than one-third (36%) would choose to invest less than the 33% currently proposed by President Bush.

8

Executive SummaryExecutive Summary

Shareholders would want a variety of investment options of a moderately aggressive nature.

On average, shareholders would want the investment options available in personal accounts to be moderately aggressive (3.5 on a scale where 1 is very conservative and 7 is very aggressive) and over half indicate that they would invest their Social Security money as aggressively (i.e. somewhat conservatively) as their other investments.

However, they want a variety of investment choices, including large majorities who want access to stock mutual funds and money market funds.

After five waves of data, we are beginning to build a clearer profile of the typical American investor and the data suggests that investors are somewhat cautious, in it for the long term and recognize that stocks can yield the greatest returns.

In each wave of data, the majority of investors indicate that they plan to make no changes to their portfolios in the near future (the next six months).

The average risk level of investor’s portfolios is steady at about 4 on a 7 point scale where 1 is not at all risky and 7 is very risky.

When asked, how they would invest either $10,000 or $100,000, over half indicate that they would put that money in either individual stocks or stock mutual funds.

9

Executive SummaryExecutive Summary

However, investors’ overall level of confidence in the economy and stock market are not as strong as in previous waves of research.

The NAIC Investor Confidence Index has declined again to it’s lowest level at +7.8 from a high of +19.3 in January 2004.

There is a great deal of fluctuation in the components that make up the Index and the data shows that investors are increasingly thinking that it’s a good time to move into safer investments, and decreasingly thinking that most stocks are a better bargain now than one year ago.

Belief that the overall direction of the US economy is going in the right direction is comparable to November 2004, with just over half thinking the economy is headed in the right direction, still down considerably from a high of 71% in January 2004.

These data also suggest that men are becoming slightly more cautious and are now more similar to women in their overall attitudes and beliefs, as compared to previous waves.

Men’s views of the economy are consistent since November 2004 while women’s show a slight increase.

Half of men now feel that it’s a good time for new investors to get involved in the stock market, compared with 66% in January 2004. In comparison, the proportion of female shareholders who feel this way has increased since November (50% vs. 45%).

The proportion of men who feel that it’s a good time to move into safer investments has steadily increased from a low of 29% in January 2004 to 40% in February 2005. Women, on the other hand, have remained fairly steady in their belief (range: 40% - 44%) about moving into safer investments.

10

Profile of the typical American ShareholderProfile of the typical American Shareholder

In general, the typical American shareholders’ behaviors and investment portfolio has remained virtually unchanged since January 2004.

Shareholders hold a variety of investments in addition to individual stocks and stock mutual funds, mostly including individual retirement accounts that they control or through their employers.

Shareholders continue to characterize most of their investments as moderately risky.

4 in 10 male shareholders characterize their investments as risky (40%) while less than 3 in 10 female shareholders (27%) do the same.

The majority of shareholders plan to make no changes to their investments in individual stocks (64%) or stock mutual funds (68%) over the next six months.

If they had $10,000 or $100,000 to invest, shareholders would continue to invest nearly half of this money in individual stocks or stock mutual funds. This allocation has remained virtually the same since January 2004.

11

Views toward the economy and stock marketViews toward the economy and stock market

Shareholders’ confidence in the direction of the U.S. economy remains virtually unchanged since November 2004, when confidence declined to its lowest levels in this series of research.

When asked about confidence in the United States economy, 55% of shareholders indicate that they have “a fair amount” or “a great deal” of confidence that it is moving in the right direction – down from 60% in May 2004.

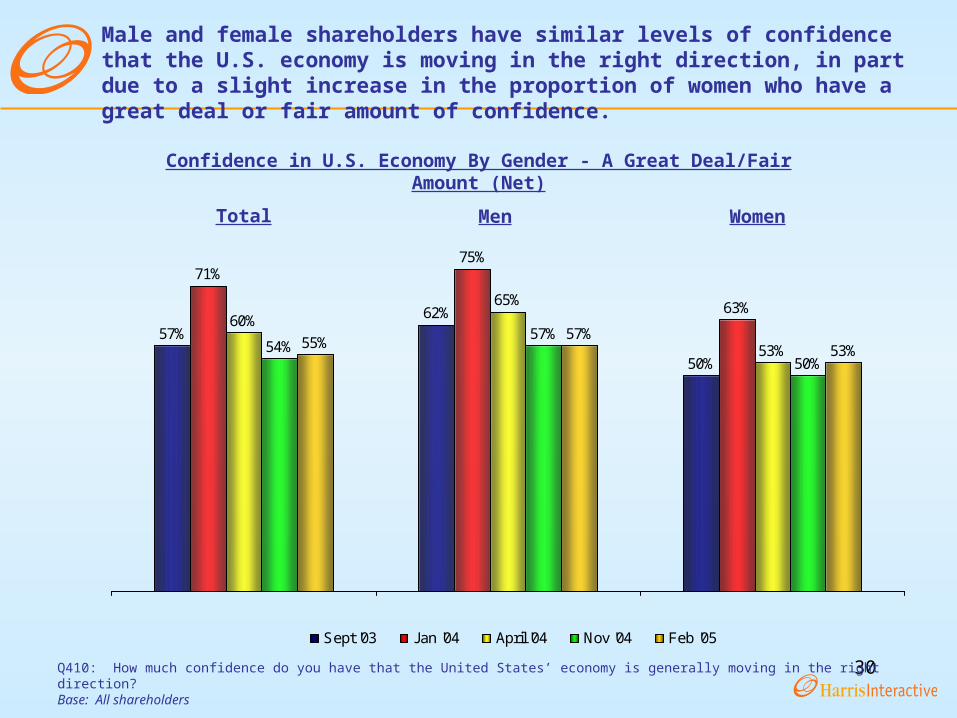

Women (53%) have slightly less confidence than do men (57% a great deal/fair amount)

The NAIC Shareholder Confidence Index has dropped slightly from +9.3 in November 2004 to +7.8 in February 2005.

Currently the NAIC Index is +7.8, down from +19.3 in January 2004. On a scale from -100 to +100 (where zero indicates a neutral attitude towards the stock market), an Index of +7.8 shows trace levels of optimism tempered by concern about the direction of the economy.

Compared to November 2004, there were large fluctuations in the components for confidence in the U.S. economy, -2.5 now down from 6.5 in November, and most stocks being a better bargain now than they were a year ago, 9.2 in November to -0.2 now.

12

Views toward the economy and stock marketViews toward the economy and stock market

As in November 2004, half of shareholders (50%) believe it’s a good time for new investors to get involved in the stock market.

Once again, there has been a decline in the proportion of shareholders who think that most stocks are a better bargain now than they were a year ago (29% now versus 35% then).

Since January 2004, this level of agreement has decreased from nearly 4 in 10 shareholders (43%) to less than 3 in 10 (29%).

Consistent with the previous finding, shareholders continue to agree that it’s a good time to move money into safer, lower risk investments from higher return/higher risk investments, with 42% who now hold this view.

While in January 2004, male and female shareholders disagreed on this point, with 29% of men agreeing versus 40% of females, now they are both at similar levels of agreement (40% of males versus 44% of females).

The proportion who agree that it’s a good time to move money into less risky investments has steadily increased since January 2004.

13

Perceptions of the Current Social Security SystemPerceptions of the Current Social Security System

Overall, about one-quarter of the public is following the Social Security debate extremely or very closely. Shareholders are more likely than non-shareholders to be following the issue this closely.

In general, roughly equal proportions of male and female shareholders are following the issue closely.

Older shareholders, those aged 50 and older, are following it more closely than younger shareholders.

Nearly two-thirds of the public, shareholders and non-shareholders alike, believe that the current Social Security system is very much or somewhat in a state of crisis.

Male shareholders (59%) are less likely than females (66%) to believe that Social Security is in a state of crisis.

Younger shareholders, those aged 35 or less, are more likely to believe there is a crisis than older shareholders.

14

Perceptions of the Current Social Security SystemPerceptions of the Current Social Security System

The majority of shareholders believe that fundamental changes are needed to the Social Security system.

However, nearly 1 in 4 shareholders 35 or less (24%) think that the Social Security system needs to be completely rebuilt.

Shareholders think that the top problem with Social Security is that, in the future, there will be too few workers to support the number of people receiving benefits (56%).

However, albeit not a majority (45%), non-shareholders believe the top problem is that some people who don’t really need benefits are receiving them. This problem ranks as the second top concern for shareholders.

Majorities of the public, regardless of investor status, feel that it is somewhat or not at all likely that their children and grandchildren will receive their Social Security benefits.

Both shareholders and non-shareholders feel that it is unlikely that these Social Security benefits will be available to their children and to their grandchildren. Shareholders are more likely than non-shareholders to believe that they will be available to these two groups.

15

Perceptions of the current Social Security SystemPerceptions of the current Social Security System

The majority of the public, including shareholders (55%) and non-shareholders (63%) are opposed to President Bush’s Social Security plan, with roughly one-third indicating that they strongly oppose his proposal.

More than one third of both male and female shareholders strongly oppose the President’s plan.

Younger shareholders are more likely than older shareholders to support the plan although less than half do so.

16

Views toward changes to Social SecurityViews toward changes to Social Security

Nearly 70% of shareholders agree that the level of income subject to Social Security tax should be increased. Similarly, 70% also agree that people should have a choice as to how their Social Security tax is invested.

7 out of 10 shareholders favor increasing the level of income subject to Social Security tax, regardless of their own level of income. Moreover, half of shareholders agree this is the right move in order to guarantee benefits continue.

Men and women agree as to which types of changes should be made, citing an increase in the level of income subject to Social Security tax as the number one change. However, women are more likely than men to favor letting people decide how to invest their taxes while capping the annual or lifetime amount of money one could invest in a personal Social Security account.

Shareholders generally agree that the government should manage personal account investments and that private/personal accounts will increase the amount of money available to retirees in the long-run. However, shareholders also agree that managing a system of private/personal accounts will cost more than administering the current system.

Despite the notion that personal accounts will cost more than administering the current system, shareholders generally support the creation of personal accounts. Subsequently, shareholders are in agreement that the cost to manage such a personal account system should rest equally with the individual account owner as well as the government.

Large majorities (76%) feel that most people are not knowledgeable enough about how to invest to benefit from these accounts and even more (82%) feel that the government should provide education to the public concerning investment options, if personal accounts are created.

17

Impact of Proposed Changes on InvestorsImpact of Proposed Changes on Investors

The majority of shareholders would choose to invest less than the 33% of Social Security tax President Bush’s proposal would allow.

Shareholders generally agree that the portions of one’s Social Security tax that are to be invested in personal accounts should be invested in a rather conservative fashion. Men and women also agreed that personal investments should be made in a conservative manner.

Consistent with the findings that shareholder’s investments are moderately risky and would want somewhat more conservative choices, 60% of shareholders would invest their Social Security tax as aggressively as their other investments.

Nearly 70% of shareholders would like the option to choose from stock mutual funds in which their Social Security tax would be invested through a private/personal account. Further, nearly 60% would like the opportunity to invest their personal account holdings in money market funds.

18

Corporate GovernanceCorporate Governance

Nearly three-quarters of shareholders believe Boards of Directors are generally ineffective in overseeing companies they govern.

Further, as a consequence of recent corporate scandals, nearly 80% of shareholders believe directors will research companies more thoroughly before taking on the responsibility of joining a corporate board.

Just over 60% of shareholders believe that the financial and accounting regulations governing publicly held companies are too lenient.

Shareholders view Sarbanes-Oxley with mixed feelings, recognizing the necessary balance of protecting shareholder interests while allowing companies the freedom to run the business.

Most shareholders feel that the recent Sarbanes-Oxley legislation is in the best interest of investors as well as corporations yet half think too much regulation makes the cost of doing business too high.

However, for many shareholders Sarbanes-Oxley has not had its intended effect of increasing confidence in public statements. Nearly 92% of shareholders feel their confidence in public statements made by companies has stayed the same or decreased since the passage of Sarbanes-Oxley.

19

Detailed FindingsDetailed Findings

20

What Does the Typical American Shareholder Look What Does the Typical American Shareholder Look Like, and How Do They Behave?Like, and How Do They Behave?

21

Since November 2004, shareholders have increased the amount they have invested in both individual stocks and stock mutual funds.

Total Amount Invested in Individual Stocks and Stock Mutual Funds

Q1440: You mentioned that you have the following investments. About how much do you have invested in the following…?Base: All Shareholders

Individual Stocks (%) Stock Mutual Funds (%)

Jan ‘04 May ‘04 Nov ’04 Feb ‘05 Jan ‘04 May ‘04 Nov ‘04 Feb ‘05

Less than $5,000 41 41 36 42 30 32 25 30

$5,000 - $9,999 10 9 12 9 8 10 6 5

$10,000 - $49,999 20 28 20 25 29 31 25 32

$50,000 - $99,999 9 7 6 7 9 11 13 14

More than $100,000

19 15 13 17 24 16 15 18

MEAN $108,900 $64,200 $63,400 $156,200 $84,100 $56,300 $67,900 $94,400

MEDIAN $7,000 $8,350 $5,700 $8,700 $19,000 $14,640 $16,160 $17,400

22

Q430: Please indicate which types of investments or investment accounts you personally have. Do you currently have . . .?Base: All shareholders

Jan ‘04 May ‘04 Nov ‘04 Feb ‘05

% % % %

Individual stocks (not including stock options or restricted stocks from the company that I work for)

71 67 66 67

Stock mutual funds 67 70 69 72

Individual retirement account that I control (i.e., IRA, KEOGH, SEP)

56 51 52 59

Individual retirement accounts through my employer (i.e., 401(k) retirement savings plan or 403(b) retirement savings plan, or profit sharing plan)

52 52 50 51

Bonds or bond funds 33 35 35 37

Stock options or restricted stocks from the company that I work for

15 17 12 12

Other type of investment not mentioned 21 21 25 25

In addition to individual stocks and stock mutual funds, most shareholders also have various other types of investments.

Types of Investments Owned

23Q510: Again thinking about your investment portfolio, over the next six months, do you plan to increase, decrease or make no change in your investments in each of the following? Base: All shareholders

As in November 2004, the majority of shareholders plan to make no changes to their investments over the next six months.

Plans for Investments Over The Next Six Months

Increase (%) Make No Change (%) Decrease (%)

2004 2005 2004 2005 2004 2005

Jan May Nov Feb Jan May Nov Feb Jan May Nov Feb

Individual stocks 34 26 29 28 62 67 63 64 5 7 8 8

Stock mutual funds 31 24 24 28 64 71 69 68 5 5 7 4

Individual bonds 6 8 8 8 89 88 85 87 5 3 6 5

Bond mutual funds 10 11 11 11 84 84 83 85 5 5 6 3

Cash 39 38 38 35 52 54 52 55 9 8 10 10

Alternative investments

8 5 7 8 90 92 89 88 2 2 4 4

Other investments not mentioned

15 16 15 15 83 81 81 82 2 3 3 3

24Q510: Again thinking about your investment portfolio, over the next six months, do you plan to increase, decrease or make no change in your investments in each of the following? Base: All shareholders (n=1175; Male=674; Female=501)

Nearly one-third of male shareholders plan to increase their investments in stock mutual funds over the next six months, compared to just one-quarter of women.

Plan to Increase Investments Over The Next Six Months

Increase (%)

Total Male Female

Individual stocks 28 27 29

Stock mutual funds 28 31 24

Individual bonds 8 7 8

Bond mutual funds 11 12 10

Cash 35 35 35

Alternative investments (such as hedge funds, private equity and managed futures)

8 9 6

Other investments not mentioned

15 16 14

25

Whether they have $10,000 or $100,000 to invest, shareholders would continue to invest nearly half in stock mutual funds and individual stocks.

Percentage Allocated to Each Investment

Have $10,000 to Invest

Total (Mean)

Have $100,000 to Invest

Total (Mean)

Jan ‘04 May ‘04 Feb ‘05 Jan ‘04 May ‘04 Feb ‘05

Individual stocks 32 26 26 27 25 24

Stock mutual funds 26 27 27 27 27 28

Cash 14 16 14 13 15 14

Bond mutual funds 10 10 10 9 10 10

Individual bonds 6 5 6 6 6 7

Alternative investments 3 3 4 5 5 5

Other investments 7 11 12 13 13 12

Q515: If you had $10,000/$100,000 to invest, how much would you invest in each of the following? Base: All shareholdersNote: For this question, half of all respondents were asked to allocate $10,000 across the investments listed above and the other half were asked to allocate $100,000 across the investments listed above.

26

Q505: Investment risk is typically defined as a greater likelihood that your portfolio may lose value but is often associated with higher returns. On a scale from 1 to 7, in which “1” represents “not risky at all” and a “7” represents “very risky”, how would you characterize most of your investments?Base: All shareholders

Risk Level of Current Investments

36%

33%

38%

32%30%

35%

28%

37%

34%

31%

34%34%32%

34%

30%

Very Risky (5, 6, 7 Net) Moderately Risky (4) Not Risky (1, 2, 3 Net)

Sept '03 Jan '04 May '04 Nov '04 Feb '05

Sept ‘03 Jan ’04 May ’04 Nov ’04 Feb ‘05MEAN = 4.0 4.1 3.9 3.9 3.9

Shareholders continue to characterize their investments as moderately risky.

27Q505: How would you characterize most of your investments on a scale from “not risky at all” to “very risky”? Base: All shareholders

Sept ’03 Jan ’04 May ’04 Nov ‘04 Feb ‘05

% % % % %

Very Risky (5, 6, 7) (Net) 36 38 35 34 34

Men 42 45 41 43 40

Women 27 28 27 24 27

Moderately Risky (4) 30 32 28 31 32

Men 29 28 26 28 30

Women 31 38 32 35 35

Not Risky at All (1, 2, 3) (Net)

33 30 37 34 34

Men 28 27 33 29 30

Women 41 33 41 41 39

Mean 4.0 4.1 3.9 3.9 3.9

Men 4.2 4.2 4.0 4.2 4.1

Women 3.7 3.9 3.8 3.6 3.7

Risk Level of Current Investments By Gender

Four in ten male shareholders characterize their investments as risky while less than 3 in 10 female shareholders do the same.

28

How Do Shareholders Feel about the How Do Shareholders Feel about the Economy and Stock Market?Economy and Stock Market?

29

Confidence in the U.S. economy remains at similar levels as in November 2004.

Q410: How much confidence do you have that the United States’ economy is generally moving in the right direction?Base: All shareholders

57%

43%

71%

29%

60%

40%

54%

46%

55%

45%

A Great Deal/A Fair Amount (Net) Not Much/None At All (Net)

Sept '03 Jan '04 May '04 Nov '04 Feb '05

Confidence in the U.S. Economy

30

Male and female shareholders have similar levels of confidence that the U.S. economy is moving in the right direction, in part due to a slight increase in the proportion of women who have a great deal or fair amount of confidence.

Q410: How much confidence do you have that the United States’ economy is generally moving in the right direction?Base: All shareholders

Confidence in U.S. Economy By Gender - A Great Deal/Fair Amount (Net)

Men Women

57%62%

50%

71%75%

63%60%

65%

53%57%

50%55%

57%53%54%

Sept '03 Jan '04 April '04 Nov '04 Feb '05

Total

31

Feb 2005NAIC INDEX

+7.8

The NAIC Index of Investor Confidence has consistently declined since January 2004, reaching a low of +7.8.

February 2005Component Scores for Each Item

Included in NAIC Index

Note: The NAIC Index was calculated based on 7 components that reflect shareholder confidence in the economy and stock market and is rated on a scale from -100 to +100 where 0 is the midpoint. A more detailed explanation of the Index is found in the Detailed Methodology.

19.310.9 9.3 7.8

-100

-80

-60

-40

-20

0

20

40

60

80

100

Jan'04

May'04

Nov'04

Feb'05

Question Positive Neutral NegativeComponent

Scores

Q410 9.7 78.1 12.2 -2.5

Q511a1 27.5 64.4 8.0 19.5

Q511a2 27.9 67.6 4.4 23.5

Q505 34.2 31.8 34.0 0.2

Q502a1 25.9 32.3 41.8 -16.0

Q502a2 29.3 41.3 29.4 -0.2

Q502a3 50.1 29.9 20.0 30.1

= 54.6

NAIC

Index = +7.8

32

The NAIC Index of Investor Confidence has declined steadily for men since January 2004, reaching 8.6 in February 2005. The Index for women reached its lowest point of 3.4 in November 2004 and increased to 6.9 in February 2005.

Note: The NAIC Index was calculated based on 7 components that reflect shareholder confidence in the economy and stock market and is rated on a scale from -100 to +100 where 0 is the midpoint. A more detailed explanation of the Index is found in the Detailed Methodology.

24.319.8

13.98.6

-100

-80

-60

-40

-20

0

20

40

60

80

100

Jan '04 May'04

Nov'04

Feb'05

13.47.3 3.4 6.9

-100

-80

-60

-40

-20

0

20

40

60

80

100

Jan'04

May'04

Nov'04

Feb'05

FemaleMale

33

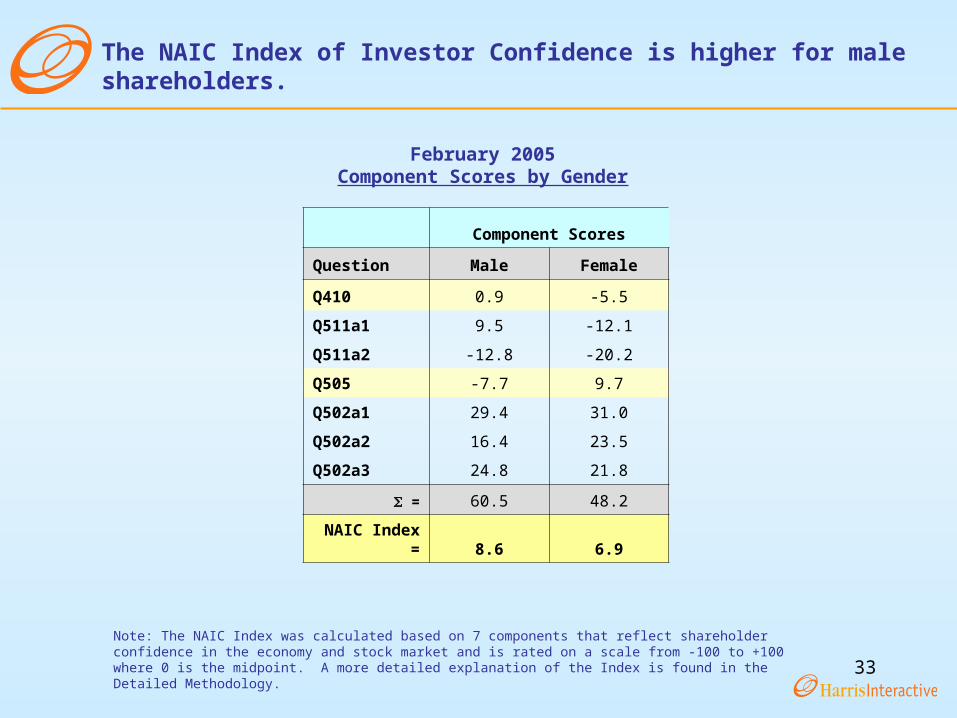

Note: The NAIC Index was calculated based on 7 components that reflect shareholder confidence in the economy and stock market and is rated on a scale from -100 to +100 where 0 is the midpoint. A more detailed explanation of the Index is found in the Detailed Methodology.

Component Scores

Question Male Female

Q410 0.9 -5.5

Q511a1 9.5 -12.1

Q511a2 -12.8 -20.2

Q505 -7.7 9.7

Q502a1 29.4 31.0

Q502a2 16.4 23.5

Q502a3 24.8 21.8

= 60.5 48.2

NAIC Index = 8.6 6.9

February 2005Component Scores by Gender

The NAIC Index of Investor Confidence is higher for male shareholders.

34

Note: The NAIC Index was calculated based on 7 components that reflect shareholder confidence in the economy and stock market and is rated on a scale from -100 to +100 where 0 is the midpoint. A more detailed explanation of the Index is found in the Detailed Methodology.

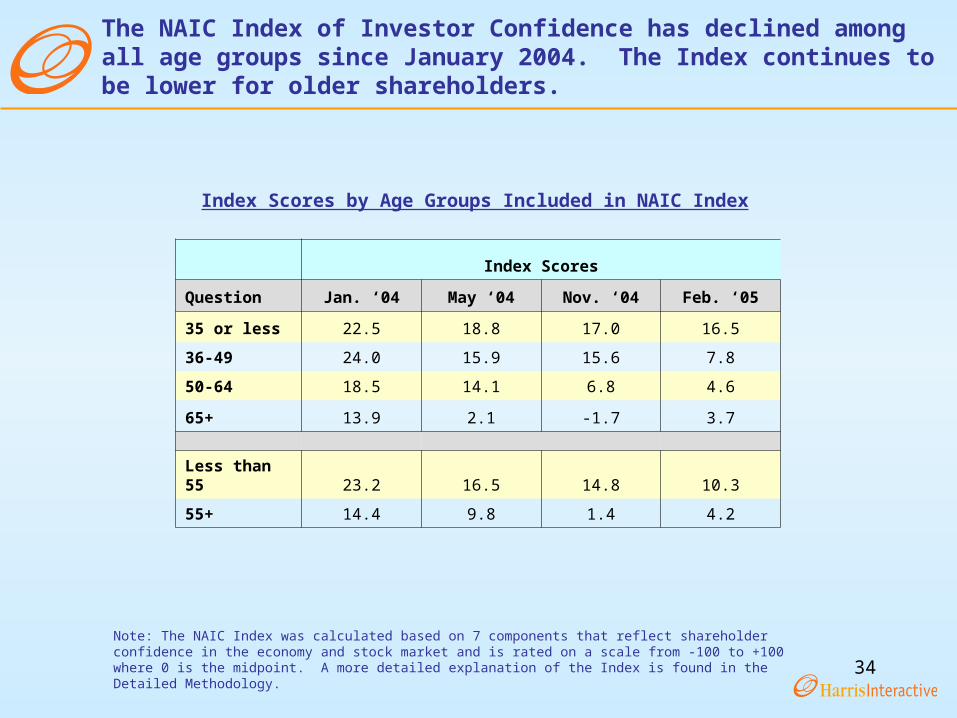

Index Scores

Question Jan. ‘04 May ‘04 Nov. ‘04 Feb. ‘05

35 or less 22.5 18.8 17.0 16.5

36-49 24.0 15.9 15.6 7.8

50-64 18.5 14.1 6.8 4.6

65+ 13.9 2.1 -1.7 3.7

Less than 55 23.2 16.5 14.8 10.3

55+ 14.4 9.8 1.4 4.2

Index Scores by Age Groups Included in NAIC Index

The NAIC Index of Investor Confidence has declined among all age groups since January 2004. The Index continues to be lower for older shareholders.

35

Note: The NAIC Index was calculated based on 7 components that reflect shareholder confidence in the economy and stock market and is rated on a scale from -100 to +100 where 0 is the midpoint. A more detailed explanation of the Index is found in the Detailed Methodology.

Component Scores

Question 35 or less 36-49 50-64 65+ Less than 55 55+

Q410 -3.4 -7.1 -0.5 4.6 -4.7 2.8

Q511a1 16.1 13.1 -8.2 -21.2 10.5 -15.5

Q511a2 -4.2 -14.3 -23.3 -20.7 -11.2 -23.1

Q505 -4.0 -9.8 1.2 13.9 -6.5 9.5

Q502a1 49.1 25.3 25.0 24.0 32.4 26.7

Q502a2 29.2 19.6 16.4 13.7 22.9 14.4

Q502a3 32.8 28.2 21.5 11.4 29.1 15.1

= 115.6 54.9 32.1 25.6 72.4 29.7

NAIC Index = 16.5 7.8 4.6 3.7 10.3 4.2

February 2005Component Scores by Age Groups Included in NAIC Index

The NAIC Index of Investor Confidence declines with age.

36Q501: How strongly do you agree or disagree with each of the following statements? Base: All shareholders

Half of shareholders agree that it’s a good time for new investors to get involved in the stock market.

62%

24%

15%

51%

25% 23%

50%

27% 24%

50%

30%

20%

Strongly/ Somewhat Agree Neither agree nor disagree Strongly/ Somewhat Disagree

Jan. '04 May '04 Nov '04 Feb '05

“It’s a good time for new investors to get involved in the stock market.”

37

For the first time, women are as likely as men to think it is a good time for new investors to get involved in the stock market.

Q502: How strongly do you agree or disagree with each of the following statements?Base: All shareholders

62%66%

56%51%

56%

44%

54%

45%50% 50% 50%50%

Total Men Women

Jan. '04 April '04 Nov '04 Feb '05

% Strongly/Somewhat Agree:“It’s a good time for new investors to get involved in the stock market.”

38

Since January 2004, fewer shareholders agree that most stocks are a better bargain now than they were a year ago.

43%

26%31%

41%

26%33%35% 38%

26%29%

41%

29%

Strongly/ Somewhat Agree Neither agree nor disagree Strongly/ Somewhat Disagree

Jan. '04 May '04 Nov '04 Feb' 05

“Most stocks are a better bargain now than they were one year ago.”

Q502: How strongly do you agree or disagree with each of the following statements?Base: All shareholders

39

Slightly more female shareholders agree that stocks are a better bargain now than they were a year ago.

43%

26%31%

41%

26%33%35% 38%

26%29% 26%33%

Total Men Women

Jan. '04 May '04 Nov '04 Feb' 05

%Strongly/Somewhat Agree:“Most stocks are a better bargain now than they were one year ago.”

Q502: How strongly do you agree or disagree with each of the following statements?Base: All shareholders

40Q501: How strongly do you agree or disagree with each of the following statements? Base: All shareholders

Since January 2004, the proportion of shareholders who agree that it’s a good time to move money into safer investments has steadily increased, with 42% of shareholders now holding this belief.

34% 32%35%37%

32% 30%

40%36%

24%

42%

32%26%

Strongly/ Somewhat Agree Neither agree nor disagree Strongly/ Somewhat Disagree

Jan. '04 May '04 Nov '04 Feb '05

“It’s a good time to move money into safer, lower risk investments from higher return/higher risk investments.”

41

While about 4 in 10 female shareholders have agreed since January 2004 that it’s a good time to move money into lower risk investments, the proportion of men who feel this way has steadily increased.

34%29%

40%37%

33%

44%40% 39% 41%42% 40%

44%

Total Men Women

Jan. '04 April '04 Nov '04 Feb '05

% Strongly/Somewhat Agree:“It’s a good time to move money into safer, lower risk investments

from higher return/higher risk investments.”

Q502: How strongly do you agree or disagree with each of the following statements?Base: All shareholders

42

What do Shareholders think aboutWhat do Shareholders think about the Current Social Security System?the Current Social Security System?

43Q600: How closely would you say you have been following the Social Security Issue in the news?Base: All Adults

Shareholders are following the Social Security issue more closely than non-shareholders yet fully 4 out of 10 investors are following it only somewhat closely.

9%

17% 19%

41%

15%14%20% 20%

38%

8%7%

16% 18%

43%

17%

Extremely closely Very closely Closely Somewhatclosely

Not at all closely

Total (n=4077) Shareholders (n=1175) Non-Shareholders (n=2847)

How Closely Follow Social Security Issue

Total Shareholders Non-ShareholdersExtremely/Very closely 26 34 22Somewhat/Not at all closely 56 46 60

44Q600: How closely would you say you have been following the Social Security Issue in the news?Base: All Shareholders

One-third of both male and female shareholders are following the Social Security issue extremely or very closely.

14%20% 20%

38%

8%12%

22% 23%

36%

6%

16% 17% 17%

40%

11%

Extremely closely Very closely Closely Somewhat closely Not at all closely

Total (n=1175) Male (n=674) Female (n=501)

How Closely Follow Social Security Issue By Gender

Total Male FemaleExtremely/Very closely 34 34 33Somewhat/Not at all closely 46 42 51

45Q600: How closely would you say you have been following the Social Security Issue in the news?Base: All Shareholders

How Closely Follow Social Security Issue By Age

Older shareholders are following the Social Security issue more closely than younger shareholders.

14%20%

38%

8%8%

17%

43%

13%9%

19%18%22%

5% 3%

20%19%

12%

40%

20%

34%

20%

33%

20% 23%21%

Extremely closely Very closely Closely Somewhat closely Not at all closely

Total (n=1175) 35 or less (n= 136) 36-49 (n= 251) 50-64 (n= 429) 65+ (n= 359)

Total 35 or less 36-49 50-64 65+Extremely/Very closely 34 25 28 41 41Somewhat/Not at all closely 46 56 52 39 36

46Q601: To what degree do you believe that the Social Security system, as we know it, is in a state of crisis?Base: All Adults

More than 6 in 10 shareholders believe that the Social Security system is very much or somewhat in a state of crisis.

32% 32%24%

12%

33% 33%

23%

11%14%

24%32%

29%

Very much Somewhat A little Not at all

Total (n=4077) Shareholders (n=1175) Non-Shareholders (n=2847)

Belief That Social Security is in a State of Crisis

Total Shareholders Non-ShareholdersVery much/Somewhat 65 62 66A little/Not at all 35 38 34

47Q601: To what degree do you believe that the Social Security system, as we know it, is in a state of crisis?Base: All Shareholders

Male shareholders are less likely than female shareholders to believe that the Social Security system is in a state of crisis.

29%32%

24%

14%

28% 31%24%

17%

31%35%

25%

10%

Very much Somewhat A little Not at all

Total (n=1175) Male (n=674) Female (n=501)

Belief that Social Security is in a State of Crisis By Gender

Total Male FemaleVery much/Somewhat 62 59 66A little/Not at all 38 41 34

48Q601: To what degree do you believe that the Social Security system, as we know it, is in a state of crisis?Base: All shareholders

A belief that Social Security is in a state of crisis declines with age, which is possibly related to one’s belief about the availability of their benefits.

29%32%

24%

14%

37%34%

19%

10%

33% 33%

21%

13%

27%32%

27%

13%

20%

31% 30%

19%

Very much Somewhat A little Not at all

Total (n=1175) 35 or less (n= 136) 36-49 (n= 251) 50-64 (n= 429) 65+ (n= 359)

Total 35 or less 36-49 50-64 65+Very much/Somewhat 62 71 66 59 51A little/Not at all 38 29 34 41 49

Belief That Social Security is in a State of Crisis By Age

49Q603: Thinking of what you have read and heard about the President’s Social Security plan, how much do you support or oppose his plan for social security reform?Base: All Adults

The majority of shareholders and non-shareholders oppose President Bush’s Social Security plan including roughly one-third of each group who strongly opposes his plan.

Support for President Bush’s Social Security Plan

10%

30% 28%33%

14%

31%

22%

34%

8%

29% 31% 32%

Strongly Support Somewhat Support Somewhat Oppose Strongly Oppose

Total (n=4077) Shareholders (n=1175) Non-Shareholders (n=2847)

Total Shareholders Non-ShareholdersStrongly/Somewhat Support 39 45 37Strongly/Somewhat Oppose 61 55 63

50Q603: Thinking of what you have read and heard about the President’s Social Security plan, how much do you support or oppose his plan for social security reform?Base: All Shareholders

Male and female shareholders feel similarly about President Bush’s Social Security plan with roughly one-third strongly opposing it.

Support for President Bush’s Social Security Plan

14%

31%

22%

34%

15%

31%

21%

33%

13%

30%23%

35%

Strongly Support Somewhat Support Somewhat Oppose Strongly Oppose

Total (n=1175) Male (n=674) Female (n=501)

Total Male FemaleStrongly/Somewhat Support 45 46 42Strongly/Somewhat Oppose 55 54 58

51

14%

31%

22%

34%37%

27%

12%13%

35%

19%

44%

13%

23%

34%30%

24%

31%

21%

13%

25%

Strongly support Somewhat Support Somewhat oppose Strongly oppose

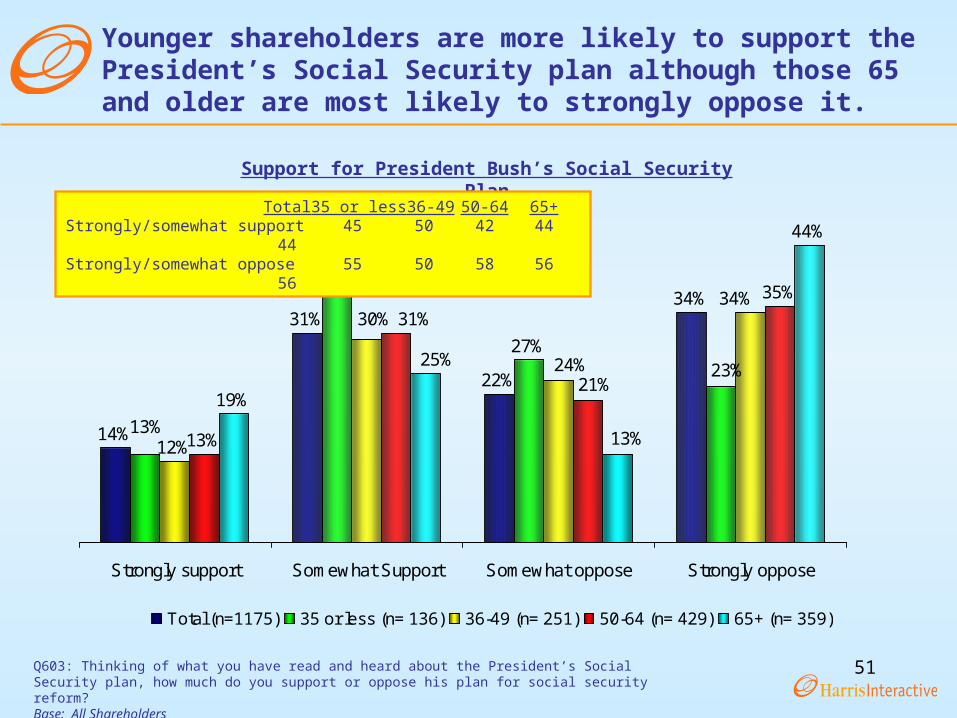

Total (n=1175) 35 or less (n= 136) 36-49 (n= 251) 50-64 (n= 429) 65+ (n= 359)

Support for President Bush’s Social Security Plan

Q603: Thinking of what you have read and heard about the President’s Social Security plan, how much do you support or oppose his plan for social security reform?Base: All Shareholders

Younger shareholders are more likely to support the President’s Social Security plan although those 65 and older are most likely to strongly oppose it.

Total 35 or less 36-49 50-64 65+Strongly/somewhat support 45 50 42 44 44Strongly/somewhat oppose 55 50 58 56 56

52

The majority of shareholders and non-shareholders feel that some fundamental changes to the Social Security system are needed.

Overall View of Social Security System

14%

30%

12%

34%

54%

14%

58%

57%

28%

The Social Securitysystem has so muchwrong with it that weneed to completely

rebuild it

Social Security workspretty well and only minorchanges are necessaryto make it work better

There are some goodthings in our social

security system but somefundamental changes are

needed

Total (n=4077) Shareholders (n=1175) Non-Shareholders (n=2847)

Q605: Which of the following comes closest to expressing your overall view of the Social Security system?Base: All Adults (n=4077)

53

12%

34%

24%

15%

60%

12%

57%

8%

42%

51%

4%

48%

54%

31%

48%

The Social Securitysystem has so muchwrong with it that weneed to completely

rebuild it

Social Security workspretty well and onlyminor changes are

necessary to make itwork better

There are some goodthings in our socialsecurity system butsome fundamental

changes are needed

Total (n= 1175) 35 or less (n= 136) 36-49 (n= 251) 50-64 (n= 429) 65+ (n= 359)

Overall View of Social Security System

Q605: Which of the following comes closest to expressing your overall view of the Social Security system?Base: All Shareholders

About 1 in 4 shareholders 35 or less believe the Social Security system has so much wrong with it that it needs to be completely rebuilt.

54Q610: Which of the following do you think are the top two problems with the Social Security system?Base: Total (n=4077) Shareholders (n=1175); Non-Shareholders (n=2847)

More than half of shareholders think that in the future, there will be too few workers to support the number of people receiving benefits.

Top Problems with the Social Security System

Total ShareholdersNon-

Shareholders

% % %

In the future, there will be too few workers to support the number of people receiving benefits

45 56 41

Some people who don’t really need benefits are receiving them

42 37 45

There is not enough money collected in taxes to pay future benefits/retirees

38 40 36

People are receiving more in benefits than they contributed because they are living longer

33 38 30

There is not enough money collected in taxes to pay current benefits/retirees

9 8 10

55

Mean Percentage of Retirement Income From Various Sources

Social

Security

Individual

Retirement Plan Provided By

Employer

Other

Retirement

Plan

Individual

Account

That I

Control

Earnings

From

Continued

Employment

Other

Income or

Investments

% % % % % %

Total 31 17 14 11 15 12

Shareholders 24 18 15 16 11 17

Non-Shareholders

35 17 13 9 17 10

Q615: Approximately what percent of your retirement income does or do you expect each of the following to provide?Base: All shareholders (n=1175)

Shareholders and non-shareholders have similar ideas as to what percent of their retirement income various plans do or will provide although non-shareholders expect more to come from Social Security.

56Q621: How likely do you think it is that Social Security benefits will be available to the following groups?Base: All Adults (n=4077); All Shareholders (n= 1175); All Non-shareholders (n= 2847)

While half of shareholders and nearly 4 in 10 non-shareholders think they will receive Social Security benefits, both investors and non-investors think it is less likely that their children and grandchildren will receive them.

Likelihood of Groups Receiving Benefits % Extremely/Very Likely

42%

52%

38%

17%

23%

14%

9%

11%

8%

Total

Shareholders

Non-Shareholders

Me My Children My Grandchildren

57

A large majority of shareholders and non-shareholders do not think it is likely that their children and grandchildren will receive benefits.

% Somewhat/Not at all LikelyLikelihood of Receiving Benefits

33%

26%

35%

61%

54%

65%

77%

71%

79%

Total

Shareholders

Non-Shareholders

Me My Children My Grandchildren

Q621: How likely do you think it is that Social Security benefits will be available to the following groups?Base: All Adults (n=4077); All Shareholders (n= 1175); All Non-shareholders (n= 2847)

58

Most shareholders and non-shareholders anticipate retiring and drawing on Social Security benefits in their 60s.

Total ShareholdersNon-

Shareholders

% % %

18-49 4 3 4

50-59 16 19 14

60-69 64 62 65

70-79 14 14 14

80+ 2 2 3

Mean 63.1 62.8 63.3

Q625: At what age do you plan to retire?Q630: At what age do you plan to start drawing on your Social Security benefits?Base: Total (n= 4077); All Shareholders (n=1175); All Non-Shareholders (n= 2847)

Likely Age of Retirement

Total ShareholdersNon-

Shareholders

% % %

18-49 3 1 4

50-59 5 2 5

60-69 79 85 77

70-79 12 10 12

80+ 2 2 2

Mean 64.2 63.9 65.0

Likely Age to Start Drawing on Social Security Benefits

59

How do Shareholders Feel About How do Shareholders Feel About Proposed Changes to Social Security?Proposed Changes to Social Security?

60Q701: There have been several changes suggested to the current Social Security program. Please indicate the degree to whichyou favor or oppose each of the following.Base: All Shareholders (n=1,175)

Level of Support for Proposed Changes to Social Security

Strongly/Somewhat

Favor

Strongly Favor

Somewhat Favor

Strongly/Somewhat

Oppose

Somewhat Oppose

Strongly Oppose

Increase the income level subject to Social Security tax

% 69 29 41 31 19 12

Change the way benefits are calculated using consumer prices rather than average wages

% 60 9 51 40 27 14

Allow individuals to invest a portion of their tax in the stock market

% 52 20 32 48 20 28

Base current and future benefits on need

% 51 10 41 49 28 21

Increase the age at which benefits can be received

% 40 6 33 60 33 27

Increase payroll tax rates % 37 4 33 63 33 30

Decrease benefits for future retirees

% 11 1 10 89 42 46

Decrease benefits for current retirees

% 8 2 7 92 25 67

Nearly 7 in 10 shareholders would strongly or somewhat favor increasing the income level subject to Social Security tax. There is little support for reducing benefits for current or future retirees.

61Q701: There have been several changes suggested to the current Social Security program. Please indicate the degree to whichyou favor or oppose each of the following.Base: All Shareholders (n=1,175)

Level of Support for Proposed Changes to Social Security by Income

Total Shareholders

Less than $50K

$50K-$75K

More than $75K

Increase the income level subject to Social Security tax

% 69 74 68 66

Change the way benefits are calculated using consumer prices rather than average wages

% 60 58 59 61

Allow individuals to invest a portion of their tax in the stock market

% 52 51 53 55

Base current and future benefits on need

% 51 54 52 47

Increase the age at which benefits can be received

% 40 42 44 36

Increase payroll tax rates % 37 39 32 38

Decrease benefits for future retirees % 11 10 15 12

Decrease benefits for current retirees % 8 6 10 8

Those with lower incomes are most likely to agree with increasing the income level subject to Social Security tax though even those with the highest incomes show a good deal of support for this.

62

Q705: Regardless of your position on each of these proposed changes, which two do you think would be most effective in guaranteeing that current and future generations would receive their full benefits?Base: All Shareholders (n-1175)

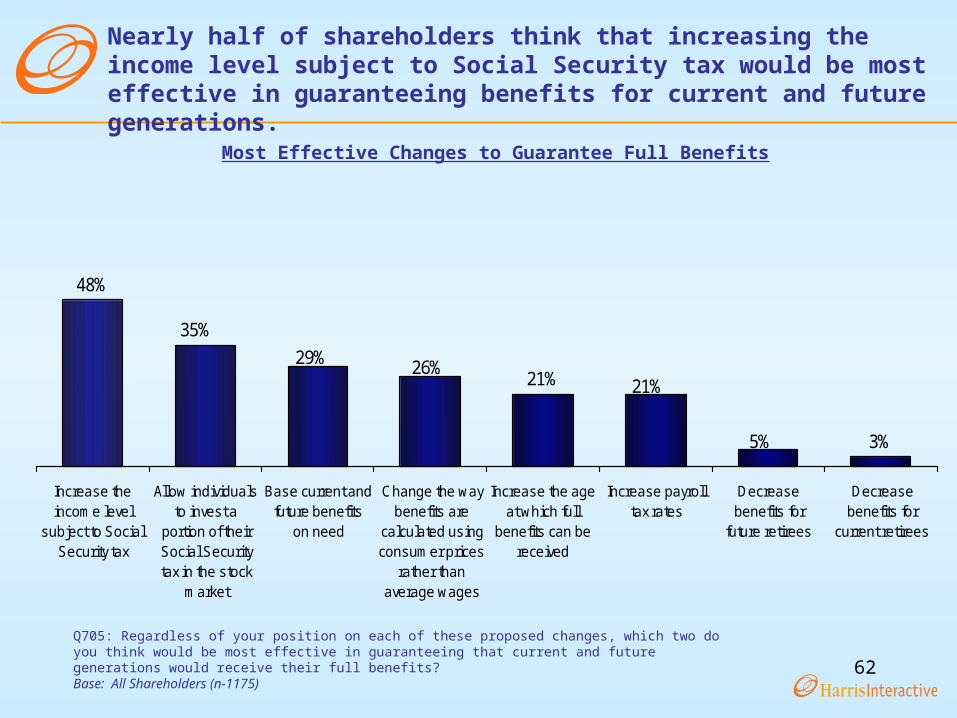

Nearly half of shareholders think that increasing the income level subject to Social Security tax would be most effective in guaranteeing benefits for current and future generations.

48%

21%

3%

29% 26%21%

5%

35%

Increase theincome level

subject to SocialSecurity tax

Allow individualsto invest a

portion of theirSocial Securitytax in the stock

market

Base current andfuture benefits

on need

Change the waybenefits are

calculated usingconsumer prices

rather thanaverage wages

Increase the ageat which full

benefits can bereceived

Increase payrolltax rates

Decreasebenefits for

future retirees

Decreasebenefits for

current retirees

Most Effective Changes to Guarantee Full Benefits

63Q705: Regardless of your position on each of these proposed changes, which two do you think would be most effective inguaranteeing that current and future generations would receive their full benefits?Base: All Shareholders (n=1,175) Male (n=674); Female (n=501)

Total Male Female

% % %

Increase the income level subject to Social Security tax

48 48 49

Allow individuals to invest a portion of their Social Security tax in the stock market

35 35 35

Base current and future benefits on need 29 28 30

Change the way benefits are calculated using consumer prices rather than average wages

26 23 31

Increase the age at which full benefits can be received

21 19 24

Increase payroll tax rates 21 21 21

Decrease benefits for future retirees 5 7 2

Decrease benefits for current retirees 3 4 1

Most Effective Changes to Guarantee Full Benefits By Gender

Male and female shareholders agree on which proposed changes would be most effective in guaranteeing benefits.

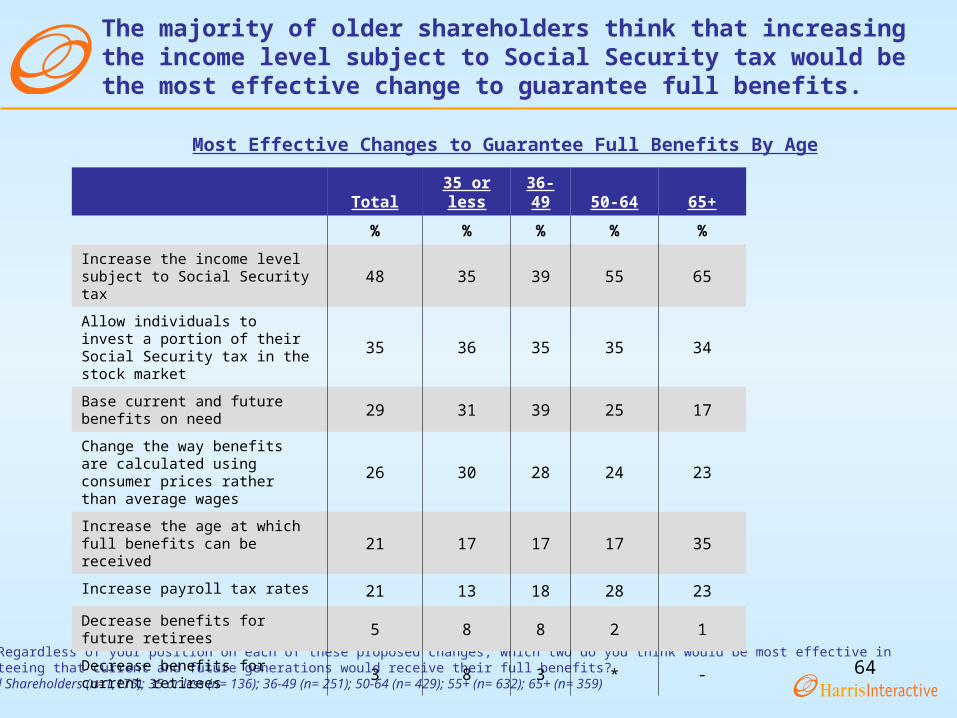

64Q705: Regardless of your position on each of these proposed changes, which two do you think would be most effective inguaranteeing that current and future generations would receive their full benefits?Base: All Shareholders (n=1,175); 35 or less (n= 136); 36-49 (n= 251); 50-64 (n= 429); 55+ (n= 632); 65+ (n= 359)

Total35 or less

36-49 50-64 65+

% % % % %

Increase the income level subject to Social Security tax

48 35 39 55 65

Allow individuals to invest a portion of their Social Security tax in the stock market

35 36 35 35 34

Base current and future benefits on need

29 31 39 25 17

Change the way benefits are calculated using consumer prices rather than average wages

26 30 28 24 23

Increase the age at which full benefits can be received

21 17 17 17 35

Increase payroll tax rates 21 13 18 28 23

Decrease benefits for future retirees 5 8 8 2 1

Decrease benefits for current retirees

3 8 3 * -

Most Effective Changes to Guarantee Full Benefits By Age

The majority of older shareholders think that increasing the income level subject to Social Security tax would be the most effective change to guarantee full benefits.

65

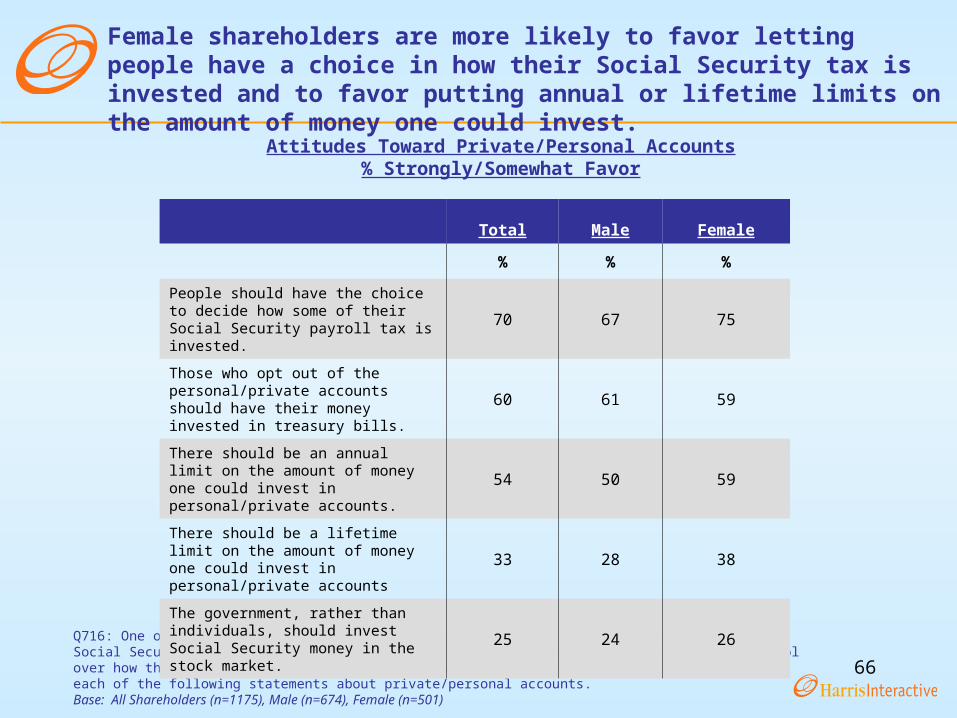

Q716: Please indicate the degree to which you favor or oppose each of the following statements about private/personal accounts.Base: All shareholders (n=1175)

7 out of 10 shareholders believe that people should have a choice in deciding how their Social Security payroll tax is invested.

Attitudes Toward Private/Personal Accounts% Strongly/Somewhat Favor

Strongly/Somewhat

Favor

Strongly Favor

SomewhatFavor

Strongly/Somewhat

Oppose

SomewhatOppose

Strongly Oppose

% % % % % %

People should have the choice to decide how some of their Social Security payroll tax is invested.

70 30 40 30 14 15

Those who opt out of the personal/private accounts should have their money invested in treasury bills.

60 9 51 40 25 15

There should be an annual limit on the amount of money one could invest in personal/private accounts.

54 20 34 46 24 22

There should be a lifetime limit on the amount of money one could invest in personal/private accounts

33 10 23 67 34 33

The government, rather than individuals, should invest Social Security money in the stock market.

25 6 19 75 30 45

66

Q716: One of the proposals being made is to allow workers to invest a portion of their Social Security tax in private/personal accounts through which they would have some control over how that money is invested. Please indicate the degree to which you favor or oppose each of the following statements about private/personal accounts.Base: All Shareholders (n=1175), Male (n=674), Female (n=501)

Female shareholders are more likely to favor letting people have a choice in how their Social Security tax is invested and to favor putting annual or lifetime limits on the amount of money one could invest.

Attitudes Toward Private/Personal Accounts% Strongly/Somewhat Favor

Total Male Female

% % %

People should have the choice to decide how some of their Social Security payroll tax is invested.

70 67 75

Those who opt out of the personal/private accounts should have their money invested in treasury bills.

60 61 59

There should be an annual limit on the amount of money one could invest in personal/private accounts.

54 50 59

There should be a lifetime limit on the amount of money one could invest in personal/private accounts

33 28 38

The government, rather than individuals, should invest Social Security money in the stock market.

25 24 26

67

How Does the Language Used Influence How Does the Language Used Influence Investors?Investors?

68Q716: Please indicate the degree to which you favor or oppose each of the following statements about private/personal accounts.Base: All Shareholders (n=1175), Private accounts (n=614), Personal accounts (n=561)

The language used to describe the accounts did not impact shareholders’ level of support for various proposals under consideration.

Level of Support for Proposed Changes By Type of AccountStrongly/Somewhat Favor

Total Private Personal

% % %

People should have the choice to decide how some of their Social Security payroll tax is invested.

70 71 70

Those who opt out of the personal/private accounts should have their money invested in treasury bills.

60 61 59

There should be an annual limit on the amount of money one could invest in personal/private accounts.

54 55 53

There should be a lifetime limit on the amount of money one could invest in personal/private accounts

33 33 32

The government, rather than individuals, should invest Social Security money in the stock market.

25 28 21

69

Q716: Please indicate the degree to which you favor or oppose each of the following statements about private/personal accounts.Base: All Qualified Respondents (n=1175), Total Republican (n= 470); Total Democrat (n= 368)Private accounts (n=614), Personal accounts (n=561); Democrat Private (n=184); Democrat Personal (n= 184); Republican Private (n= 243); Republican Personal (n= 227)

Level of Support for Proposed Changes By Party Affiliation and Type of Account% Strongly/Somewhat Favor

Democrat Republican

Total Private Personal Total Private Personal

% % % % % %

People should have the choice to decide how some of their Social Security payroll tax is invested.

54 54 53 85 86 85

Those who opt out of the personal/private accounts should have their money invested in treasury bills.

55 54 56 65 68 63

There should be an annual limit on the amount of money one could invest in personal/private accounts.

56 58 54 54 57 52

There should be a lifetime limit on the amount of money one could invest in personal/private accounts

40 43 38 28 28 27

The government, rather than individuals, should invest Social Security money in the stock market.

27 30 24 25 27 23

Republicans are much more likely to agree that people should have the choice to decide how some of their Social Security payroll tax is invested.

70Q721: Please indicate the degree to which you agree or disagree with the following statements.Base: All Shareholders (n=1,175); Private accounts (614); Personal account (561)

Total Private Personal

% % %

If private/personal accounts are created, the government should provide education about how to invest to the American people

82 81 83

Private/personal accounts will give some people access to the stock market who wouldn't otherwise have access

78 76 80

Most people are not knowledgeable enough about how to invest to benefit from private/personal accounts

76 75 78

Tracking private/personal accounts will cost more than administering the current system and reduce the amount of earnings from equity investments

62 61 63

Private/personal accounts may help make more money available to retirees but cost to cover difference in benefits is expected to be so great, the government will go deeper into debt

58 55 61

Private/personal accounts will increase the amount of money available to retirees

55 55 54

Attitudes Toward Private/Personal Accounts By Type of Account% Strongly/Somewhat Agree

The vast majority of shareholders believe that government should provide education to the public if private/personal accounts are created.

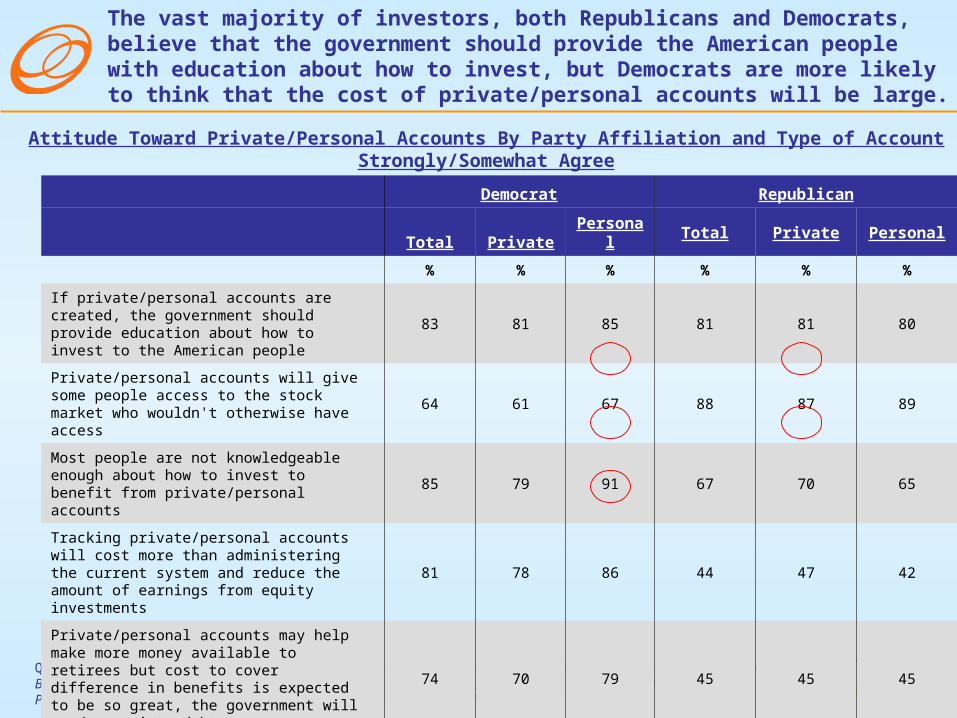

71Q721: Please indicate the degree to which you agree or disagree with the following statements.Base: All Shareholders (n=1,175); Democrats (n= 368); Republicans (n= 470); Democrat Private (n= 184); Democrat Personal (n= 184) Republican Private (n= 243); Republican Personal (n= 227)

Democrat Republican

Total Private Personal Total Private Personal

% % % % % %

If private/personal accounts are created, the government should provide education about how to invest to the American people

83 81 85 81 81 80

Private/personal accounts will give some people access to the stock market who wouldn't otherwise have access

64 61 67 88 87 89

Most people are not knowledgeable enough about how to invest to benefit from private/personal accounts

85 79 91 67 70 65

Tracking private/personal accounts will cost more than administering the current system and reduce the amount of earnings from equity investments

81 78 86 44 47 42

Private/personal accounts may help make more money available to retirees but cost to cover difference in benefits is expected to be so great, the government will go deeper into debt

74 70 79 45 45 45

Private/personal accounts will increase the amount of money available to retirees

29 30 28 81 81 80

Attitude Toward Private/Personal Accounts By Party Affiliation and Type of AccountStrongly/Somewhat Agree

The vast majority of investors, both Republicans and Democrats, believe that the government should provide the American people with education about how to invest, but Democrats are more likely to think that the cost of private/personal accounts will be large.

72

23%

34%

43%

22%

35%

44%

24%

33%

43%

Government Individual Taxpayers Both

Total Private Personal

Who Should Pay Mutual Fund Fees

Q726: Who do you think should pay for the following in a system that includes private/personal accounts?Base: All Shareholders (n=1,175); Private accounts (n= 614); Personal accounts (n= 561)

The plurality of shareholders think that the cost of mutual fund fees should be shared between the government and taxpayers.

73

31%

24%

44%

27% 27%

45%

21%

43%

35%

Government Individual Taxpayers Both

Total Private Personal

Who Should Pay Fees Necessary to Track Accounts

Q726: Who do you think should pay for the following in a system that includes private/personal accounts?Base: All Shareholders (n=1,175); Private accounts (n= 614); Personal accounts (n= 561)

Similarly, shareholders think that both the government and individual taxpayers should pay the fees necessary to track accounts.

74

Q800: One proposal would allow workers to invest 33% of their Social Security tax into a private/personal account. Regardless of what the proposal may call for, what percentage of your Social Security taxes, if any, would you be willing to contribute to a private/personal account?Base: All Shareholders (n=1,175); Democrats (n= 368); Republicans (n= 470); Democrat Private (n= 184); Democrat Personal (n= 184) Republican Private (n= 243); Republican Personal (n= 227)

Percent of Social Security Taxes Willing to Contribute to Private/Personal Account

Democrat Republican

Total Private Personal Total Private Personal

% % % % % %

0 38 34 41 8 9 7

1-32% 37 42 32 38 37 38

33% 9 10 7 15 16 13

34% or more 16 14 20 40 37 42

Mean 19 18 21 37 37 37

Median 10 10 10 33 33 33

Democratic shareholders are willing to contribute much less to private/personal accounts than Republican shareholders.

75

Total Private Personal

% % %

Very Aggressive (5, 6, 7) (Net)

25 22 29

Moderately Aggressive (4) 32 34 29

Very Conservative (1, 2, 3) (Net)

43 44 41

MEAN 3.5 3.4 3.7

Risk Level of Investments

Shareholders think that investment options that would be available in a Social Security system with private/personal accounts should be conservative.

Q805: On a scale from “very conservative” to “very aggressive”, how aggressive should the investment options be that would be available in a Social Security system with private/personal accounts?Base: All shareholders (n=1,175); Private (n= 614); Personal (n= 561)

76

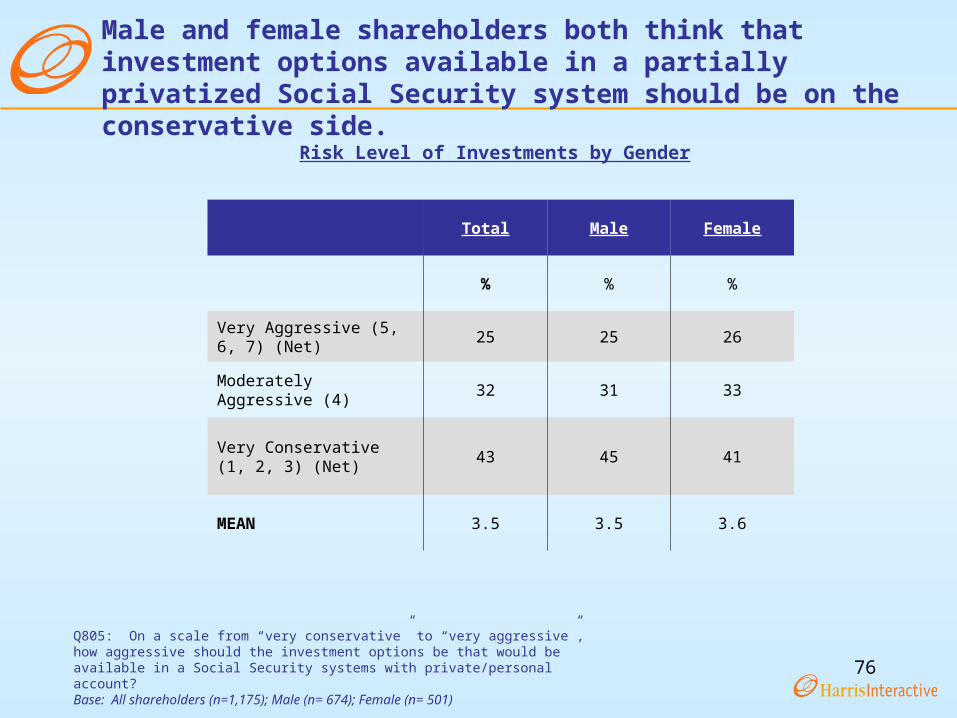

Total Male Female

% % %

Very Aggressive (5, 6, 7) (Net)

25 25 26

Moderately Aggressive (4) 32 31 33

Very Conservative (1, 2, 3) (Net)

43 45 41

MEAN 3.5 3.5 3.6

Risk Level of Investments by Gender

Male and female shareholders both think that investment options available in a partially privatized Social Security system should be on the conservative side.

Q805: On a scale from “very conservative” to “very aggressive”, how aggressive should the investment options be that would be available in a Social Security systems with private/personal account?Base: All shareholders (n=1,175); Male (n= 674); Female (n= 501)

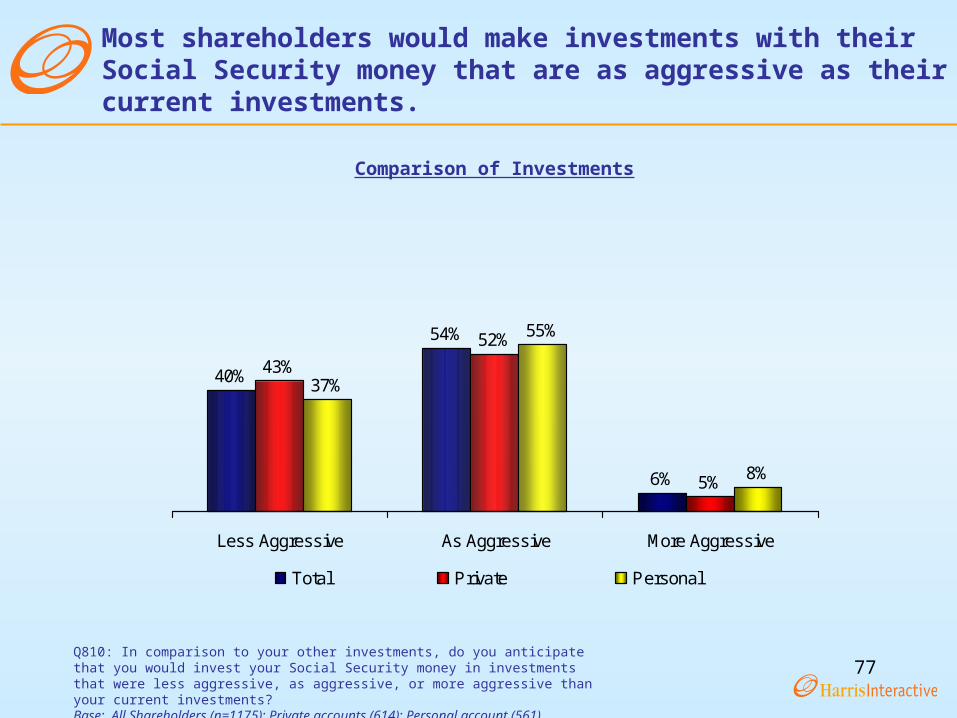

77Q810: In comparison to your other investments, do you anticipate that you would invest your Social Security money in investments that were less aggressive, as aggressive, or more aggressive than your current investments?Base: All Shareholders (n=1175); Private accounts (614); Personal account (561)

Most shareholders would make investments with their Social Security money that are as aggressive as their current investments.

40%

54%

6%

43%

52%

5%

37%

55%

8%

Less Aggressive As Aggressive More Aggressive

Total Private Personal

Comparison of Investments

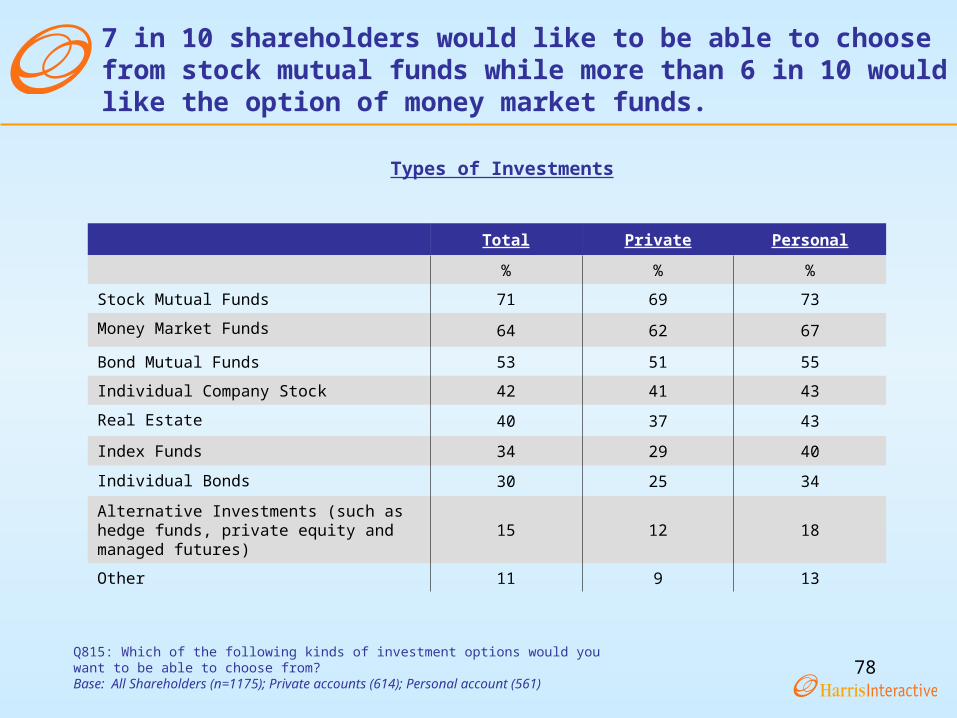

78Q815: Which of the following kinds of investment options would you want to be able to choose from?Base: All Shareholders (n=1175); Private accounts (614); Personal account (561)

7 in 10 shareholders would like to be able to choose from stock mutual funds while more than 6 in 10 would like the option of money market funds.

Total Private Personal

% % %

Stock Mutual Funds 71 69 73

Money Market Funds 64 62 67

Bond Mutual Funds 53 51 55

Individual Company Stock 42 41 43

Real Estate 40 37 43

Index Funds 34 29 40

Individual Bonds 30 25 34

Alternative Investments (such as hedge funds, private equity and managed futures)

15 12 18

Other 11 9 13

Types of Investments

79

What do Shareholders think about Boards What do Shareholders think about Boards of Directors and Sarbanes-Oxley?of Directors and Sarbanes-Oxley?

80Q905: How effective do you think Boards of Directors are in overseeing the companies they govern?Base: All Shareholders (n= 1175)

Three-quarters of shareholders think Boards of Directors are somewhat or not at all effective in overseeing the companies they govern.

Effectiveness of Board of Directors

1%7%

18%

54%

20%

Extremelyeffective

Very effective Effective Somewhateffective

Not at all effective

8%

74%

81Q911: How much do you agree or disagree with the following statements about how this case may influence other board members in the future?Base: All Shareholders (n= 1175)

Strongly/

Somewhat Agree

Strongly Agree

Somewhat Agree

Strongly/

Somewhat

Disagree

Somewhat

DisagreeStrongly Disagree

Potential directors will research the companies for which they might serve more carefully than in the past

% 80 23 57 20 14 6

Corporate board members will take their responsibilities more seriously than in the past

% 76 24 52 24 19 5

It will have no impact on the behavior of corporate board members

% 46 13 33 54 38 16

Qualified people will be discouraged from wanting to serve as a corporate board member

% 36 6 31 64 43 21

Influence of Worldcom Case on Board Members

In the wake of the WorldCom case, 8 in 10 shareholders think that directors will more carefully research companies for which they might serve and three-quarters think that board members will take their responsibility more seriously. However, majorities do not think this case will have much impact on board member’s behavior.

82Q915: Do you think that the financial and accounting regulations governing publicly held companies are too lenient, about right, or too strict?Base: All Shareholders (n= 1175)

63%

33%

3%

Too Lenient About Right Too Strict

Level of Financial and Accounting Regulation

Nearly two-thirds of shareholders think that the financial and accounting regulations governing publicly held companies are too lenient.

83

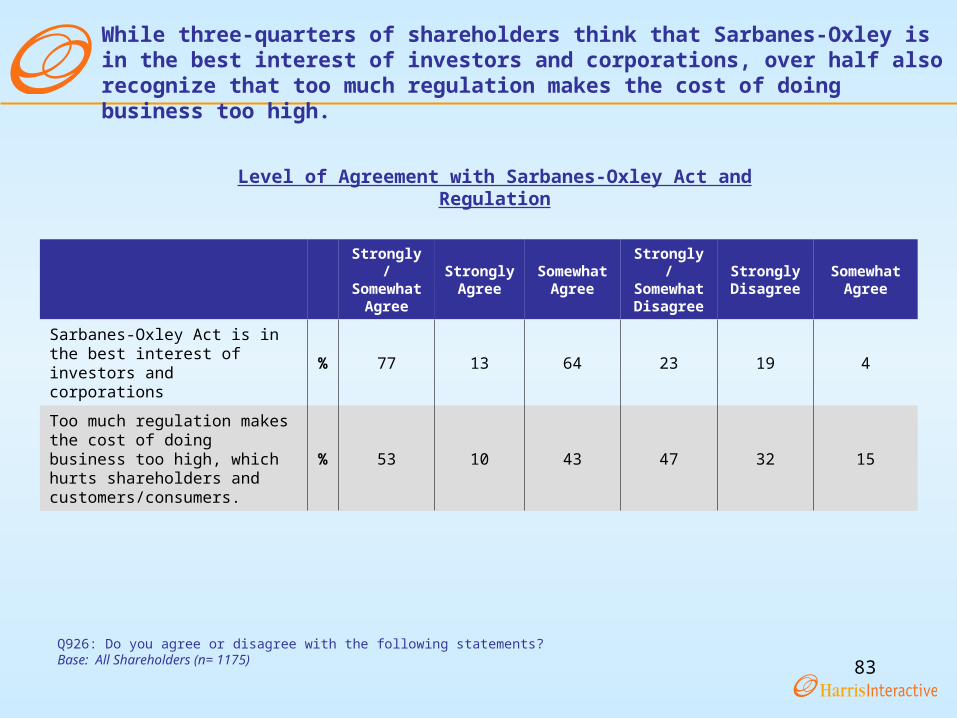

Strongly/Somewhat

Agree

StronglyAgree

SomewhatAgree

Strongly/SomewhatDisagree

StronglyDisagree

SomewhatAgree

Sarbanes-Oxley Act is in the best interest of investors and corporations

% 77 13 64 23 19 4

Too much regulation makes the cost of doing business too high, which hurts shareholders and customers/consumers.

% 53 10 43 47 32 15

Q926: Do you agree or disagree with the following statements?Base: All Shareholders (n= 1175)

While three-quarters of shareholders think that Sarbanes-Oxley is in the best interest of investors and corporations, over half also recognize that too much regulation makes the cost of doing business too high.

Level of Agreement with Sarbanes-Oxley Act and Regulation

84

15%

8%

77%

Increased Decreased Stayed the Same

Effect of Sarbanes-Oxley on Confidence in Public Statements from Companies

Q930: Since Sarbanes-Oxley, has your level of confidence in public statements that companies make increased, decreased, or stayed the same?Base: All Shareholders (n= 1175)

The majority of shareholders feel that their confidence in the public statements that companies make has stayed the same since Sarbanes-Oxley.

85

DemographicsDemographics

86

Shareholder DemographicsShareholder Demographics

GenderTotal

%

Male 57

Female 43

GenderTotal

%

Male 57

Female 43

Age

Total

%

35 years old or less 2236-49 2950-64 2765+ 23

MEAN 49.6MEDIAN 49

Age

Total

%

35 years old or less 2236-49 2950-64 2765+ 23

MEAN 49.6MEDIAN 49

Marital Status

Total

%

Single, never married 20

Married 61Divorced 7Separated 2Widowed 5Living with partner 5

Marital Status

Total

%

Single, never married 20

Married 61Divorced 7Separated 2Widowed 5Living with partner 5Children in Household Under 18

Total

%

0 751 142 83+ 3MEAN 0.4

Children in Household Under 18

Total

%

0 751 142 83+ 3MEAN 0.4

Race/Ethnicity

Total

%White 81Black/African-American 6

Asian or Pacific Islander 2Native American or Alaskan Native *Mixed racial background *Other race *Hispanic 7Decline to answer 3

Race/Ethnicity

Total

%White 81Black/African-American 6

Asian or Pacific Islander 2Native American or Alaskan Native *Mixed racial background *Other race *Hispanic 7Decline to answer 3

87

Shareholder Demographics (Cont’d)Shareholder Demographics (Cont’d)

Education

Total%

High school graduate or less 33Some college 26College (e.g., B.A., B.S.) 30Graduate school (e.g., M.S., M.D., Ph.D.) 11

Education

Total%

High school graduate or less 33Some college 26College (e.g., B.A., B.S.) 30Graduate school (e.g., M.S., M.D., Ph.D.) 11

Party Identification

Total

%

Republican 38Democrat 33Independent 29

Party Identification

Total

%

Republican 38Democrat 33Independent 29

Political Philosophy

Total

%

Conservative 33Moderate 48Liberal 18

Political Philosophy

Total

%

Conservative 33Moderate 48Liberal 18

Employment

Total%

Employed (net) 63Employed full-time 43

Employed part-time 10Self-employed 12

Not employed, but looking for work 4Not employed and not looking for work 2Retired 27Student 7Homemaker 6

Employment

Total%

Employed (net) 63Employed full-time 43

Employed part-time 10Self-employed 12

Not employed, but looking for work 4Not employed and not looking for work 2Retired 27Student 7Homemaker 6

88

Shareholder Demographics (Cont’d)Shareholder Demographics (Cont’d)

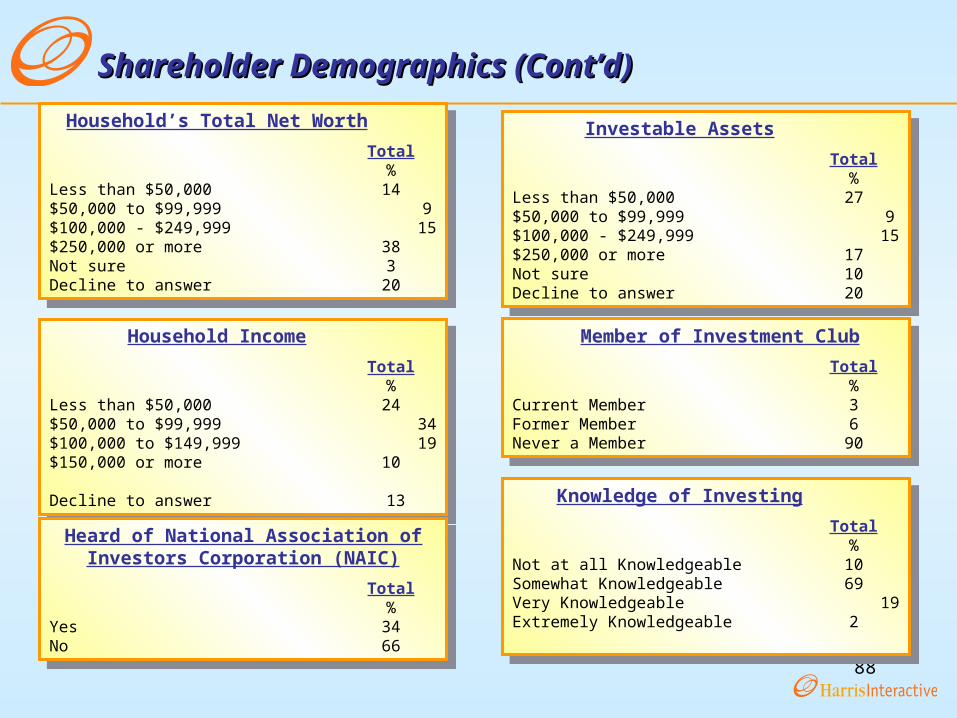

Household’s Total Net Worth

Total%

Less than $50,000 14$50,000 to $99,999 9$100,000 - $249,999 15$250,000 or more 38Not sure 3Decline to answer 20

Household’s Total Net Worth

Total%

Less than $50,000 14$50,000 to $99,999 9$100,000 - $249,999 15$250,000 or more 38Not sure 3Decline to answer 20

Investable Assets

Total%

Less than $50,000 27$50,000 to $99,999 9$100,000 - $249,999 15$250,000 or more 17Not sure 10Decline to answer 20

Investable Assets

Total%

Less than $50,000 27$50,000 to $99,999 9$100,000 - $249,999 15$250,000 or more 17Not sure 10Decline to answer 20

Household Income

Total%

Less than $50,000 24$50,000 to $99,999 34$100,000 to $149,999 19$150,000 or more 10

Decline to answer 13

Household Income

Total%

Less than $50,000 24$50,000 to $99,999 34$100,000 to $149,999 19$150,000 or more 10

Decline to answer 13

Member of Investment Club

Total%

Current Member 3Former Member 6Never a Member 90

Member of Investment Club

Total%

Current Member 3Former Member 6Never a Member 90

Heard of National Association of Investors Corporation (NAIC)

Total%

Yes 34No 66

Heard of National Association of Investors Corporation (NAIC)

Total%

Yes 34No 66

Knowledge of Investing

Total%

Not at all Knowledgeable 10Somewhat Knowledgeable 69Very Knowledgeable 19Extremely Knowledgeable 2

Knowledge of Investing

Total%

Not at all Knowledgeable 10Somewhat Knowledgeable 69Very Knowledgeable 19Extremely Knowledgeable 2

89

Shareholder Demographics (Cont’d)Shareholder Demographics (Cont’d)

Region

Total%

East 23Midwest 22South 31West 23

Region

Total%

East 23Midwest 22South 31West 23

Size of Place

Total

%Central counties of metro areas of 1 million or more 49Fringe counties of metro areas of 1 million or more 4Counties in metro areas of 250,000 to 1 million 25Counties in metro areas of fewer than 250,000 8Urban population of 20,000 or more, adjacent to metro area 3Urban population of 20,000 or more, not adjacent to metro area 2Urban population of 2,500-19,999, adjacent to metro area 4Urban population of 2,500-19,999, not adjacent to metro area 2Completely rural or less than 2,500 urban population, adjacent to metro area 1Completely rural or less than 2,500 urban population, not adjacent to metro area *NA 1

Size of Place

Total

%Central counties of metro areas of 1 million or more 49Fringe counties of metro areas of 1 million or more 4Counties in metro areas of 250,000 to 1 million 25Counties in metro areas of fewer than 250,000 8Urban population of 20,000 or more, adjacent to metro area 3Urban population of 20,000 or more, not adjacent to metro area 2Urban population of 2,500-19,999, adjacent to metro area 4Urban population of 2,500-19,999, not adjacent to metro area 2Completely rural or less than 2,500 urban population, adjacent to metro area 1Completely rural or less than 2,500 urban population, not adjacent to metro area *NA 1

90

Detailed MethodologyDetailed Methodology

91

Detailed Methodology

The Voice of the American Shareholder Quarterly Poll Wave 5 was conducted by Harris Interactive on behalf of the National Association of Investors Corporation (NAIC). Interviewing was conducted between February 15 and February 25, 2005 among a nationally representative sample of 1,175 U.S. adults aged 18 and older who currently have investments in individual stocks or stock mutual funds. The length of the questionnaire was 10 minutes in length, not including the demographics.

SAMPLE SELECTION

Harris Interactive maintains the Harris Poll Online database (HPOL) comprised of several million respondents who have agreed to participate in survey research. The HPOL database was used as the sample source for this study. E-mail addresses for respondents in the database have been obtained from over 100 sources, including the HPOL registration site, Yahoo!, HPOL banner advertisements, and MSN/Hotmail.

Qualified respondents for this study were U.S. adults age 18+ who identified themselves as currently having investments in individual stocks or stock mutual funds in response to the question “Please indicate which types of investments or investment accounts you personally have.”

ONLINE INTERVIEWING PROCEDURES

Interviews were conducted using a self-administered, online questionnaire, via proprietary, web-assisted interviewing software. The HPOL interviewing system permitted online data entry of interviews by the respondents. Questionnaires were programmed into the system with the following checks: 1. Question and response series2. Skip pattern3. Question rotation4. Range checks5. Mathematical checks6. Consistency checks7. Special edit procedures

92

Detailed Methodology (cont’d)

ONLINE INTERVIEWING PROCEDURES (cont’d)

To maintain the reliability and integrity in the sample, each invitation contained a password that is uniquely assigned to that e-mail address. A respondent was required to enter the password at the beginning of the survey to gain access into the survey. Password protection ensured that a respondent completed the survey only one time.

To increase the number of respondents in the survey and to improve overall response rates, up to two additional reminder invitations are typically mailed at 2-4 day intervals to those respondents who have not yet participated in the survey. For this study, one reminder was sent to potential respondents.

To increase the number of respondents in the survey and to improve overall response rates, respondents were provided with a summary of some of the survey responses. This too was done via the Internet. Respondents were sent an email that provided them access to a web site that contained the survey findings. As with the survey itself, this was a password protected site that was accessible for a limited period (1-2 weeks).

All data were then tabulated, checked for internal consistency and processed by computer. A series of computer-generated tables were produced for each of the key sample groups that showed the results of each survey question, both by the total number of respondents and by the key subgroups.

93

Detailed Methodology (cont’d)

WEIGHTING