Embed Size (px)

DESCRIPTION

In this issue of the Quarterly, we examine tax in its many forms, highlighting some of the tax concerns that drive the trusts & estates and business law industries. WealthCounsel Quarterly is published four times annually by WealthCounsel, LLC, P.O. Box 44403, Madison, WI 53744-4403. Comments and questions about WealthCounsel Quarterly may be addressed to the editor at [email protected].

Citation preview

TAXAT I ON

VOLUME 9 / NUMBER 3Q3 2015

WEALTHCOUNSEL

Q UA RT E R LY

PAGE 2

QUARTERLY

ContentsFrom The Editor... ..............................................................................................3

Effective Tax Planning For Partnerships: Understanding The IRC §754 Election ................................................... 4

How Pigs Get Slaughtered: Partnership Audit Proceedings Unwind Abusive Tax Shelters ...........................................10

Climbing The Tax-Efficiency Pyramid To Lower Taxes ..................... 14

Before You Pour: A Few Tax Considerations When Decanting… ..................................... 18

Today’s Investments In Loyalty Pay Dividends In The Future ....... 26

Getting Appreciated Real Estate Out Of C Corporations (Part II) ................................................................30

Alaska And Tennessee Community Property Trusts: Understanding These Basis Adjustment Tools And The Uncertainty They Carry ............................................................. 32

The Importance Of Basis: The New Era Of Estate Planning .............................................................. 37

To Multiscreen Or Not? ................................................................................42

IRC Section 280E: A Tax Thorn In The Side Of Marijuana Businesses ....................................................................45

Marital Planning In The Joint Trust: Balancing Income Tax, Transfer Tax, And Asset Protection Concerns ........... 47

Member Spotlight .......................................................................................... 52

Incomplete Gift, Non Grantor Trusts (aka DINGs, NINGs) ....................................................................................... 58

Education Calendar ....................................................................................... 63

WC QuarterlyMEMBER MAGAZINE

Volume 9, Number 2 • Q2 2015

STAFF

SENIOR EDITOR

Matthew T. McClintock, JD

EDITORS

Jennifer Villier, JD

Jeremiah Barlow, JD

PRODUCTION EDITOR

Caryl Ann Zimmerman

ART DIRECTOR

Ellen Bryant

CONTRIBUTING WRITERS

Elliot P. Smith, JD, MAcc, MS, CPA

Tim Voorhees, JD

Patrick Murphy, JD, LLM

Brenda L. Geiger, JD

Ed Morrow, JD, LLM, CFP

WealthCounsel Quarterly is published four times annually by WealthCounsel,

LLC, P.O. Box 44403, Madison, WI 53744-4403. Comments and questions

about WealthCounsel Quarterly may be addressed to the editor at

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 3

Share The WealthAt WealthCounsel, we want to celebrate a

match made just for you.

So now when you refer a new member, we’ll credit you and your referred colleague each one month of membership dues.

And, there is NO LIMIT to the number of people you can refer. Do the right thing, and refer a valued colleague to

WealthCounsel today. You’ll each get a free month of membership for simply growing our network and enjoying the

value of what your membership delivers.

For more information go to wealthcounsel.com/sharethewealth

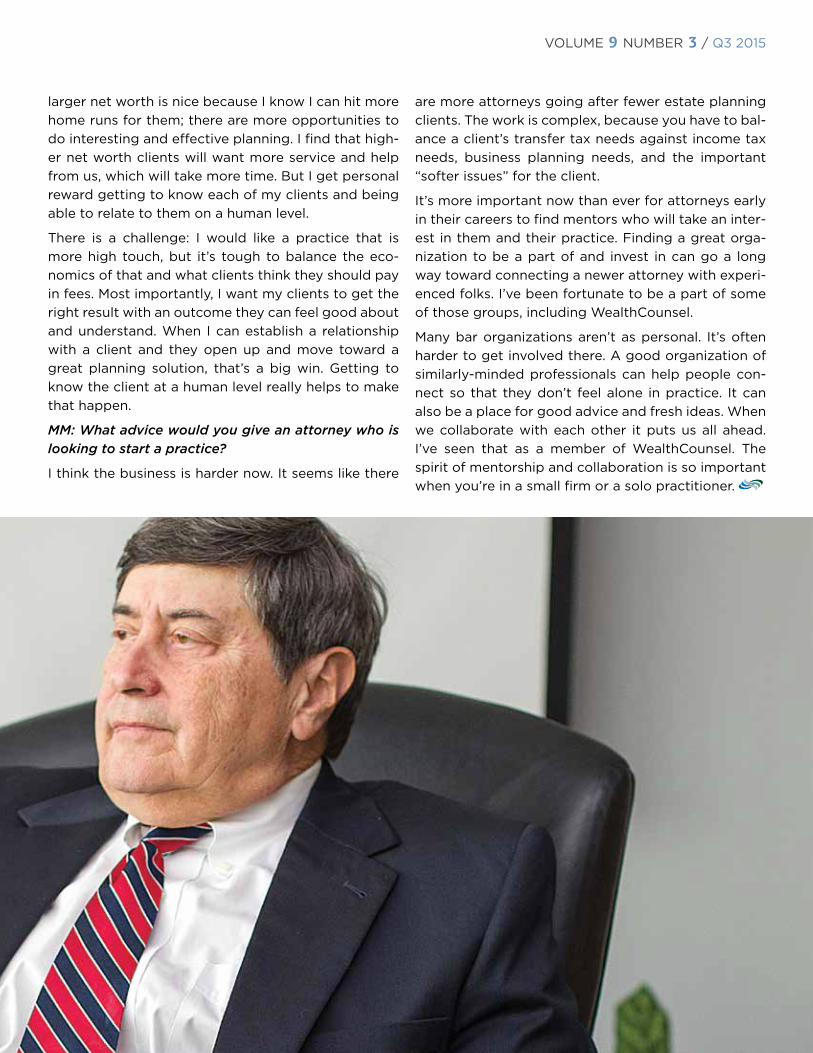

From the Editor...MATTHEW T. MCCLINTOCK, JD, VICE PRESIDENT OF EDUCATION, WEALTHCOUNSEL

“ ‘Tis impossible to be sure of any thing but Death and Taxes.”That quote, first spoken by the drunken cobbler Toby Guzzle in Christopher Bull-ock’s 1714 farce, The Cobler of Preston, and later coopted by Benjamin Franklin, largely describes the two great pri-

orities of our industry. Some 300 years later many of us spend our days helping families face the certainty of death and taxes and trying to minimize the adverse impact of both (admittedly with varying degrees of effectiveness). In this issue of the Quarterly, we exam-ine tax in its many forms, highlighting some of the tax concerns that drive the trusts & estates and business law industries.

It’s hard to overstate the impact that high, indexing, portable estate tax exemptions has had on the trusts & estates industry. Before ATRA, the uncertain status of the federal estate tax was still a motivator for many estate planning clients. But now that most clients are safely below the federal transfer tax threshold, many believe that capital gains tax and basis management have become “the new estate tax.”

In this issue we will look at the new tax environment and discuss many ways to address clients’ diverse tax planning needs. From a primer on basis to specific strategies for maximizing tax planning opportunities in estate plans, to understanding some of the special tax issues that business owners face, we hope that this issue will give you a few ideas for how you can best serve your clients in the modern trusts & estates and business practice.

One attorney has adapted well, and you’ll meet him in our WealthCounsel member spotlight. You’ll see how he has blended technical tax and sophisticated estate planning with the human element to build the satisfy-ing practice he enjoys today.

One more thing that Mr. Guzzle might agree is certain: uncertainty itself. The tax policies and other bodies of law that affect our clients are fluid. As political and economic realities change, so too does the law. That’s as certain as death and taxes.

“Sorry, I was hoping you’d ask me to join

WealthCounsel.”

PAGE 4

QUARTERLY

Effective Tax Planning For Partnerships:

UNDERSTANDING THE IRC §754 ELECTION

ELLIOT P. SMITH, JD, MACC, MS, CPA, WEALTHCOUNSEL MEMBER SINCE 2013

When used properly, an IRC §754 election can be an important tool for an estate planning or business planning

attorney. It can make a big difference in the tax burden of a company’s partners and should be given consider-

ation whenever there is a sale of a partnership interest, a death of a partner, or disproportionate distributions.

However, due to the binding nature of the election and its potential to affect future tax liability, the election

should only be made after a thorough evaluation of the pros and cons.

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 5

THE ELECTION

An election under Internal Revenue Code (“IRC”) §754 saves income taxes by increasing the tax basis of as-sets owned by a partnership. The election reduces the difference between a partner’s high tax basis in his or her partnership interest and the partnership’s low tax basis in his or her share of the partnership’s assets. Often this election can save a client significant money. It should never be overlooked when working with any entity that files IRS Form 1065.

Let’s start with the basics. Two great prongs of part-nership taxation are: 1) the “outside basis,” or the ad-justed basis of a partnership interest held by the part-ner; and 2), the “inside basis,” or the adjusted basis of the assets held by or “inside” the partnership.

TAX BASIS OF PARTNERSHIP INTEREST (“OUTSIDE BASIS”)

Outside basis is roughly comparable to a sharehold-er’s tax basis in corporate stock. However, it’s not that simple because a corporation is a tax-paying entity and a partnership is a pass-through entity: Partners incur the tax liability instead of the partnership. Dif-ferences include increasing a partner’s outside basis for contributions plus his or her share of income and decreasing his or her outside basis for distributions and losses.

For example, suppose Partner A contributes $20 to a new partnership and during the first year of opera-tion he is allocated $5 of taxable income. The $5 of taxable income is reported to him on a Schedule K-1 and ends up on his personal Form 1040. For simplic-ity, also assume that the partnership has no debt and no contributions or distributions were made by or to Partner A during the tax year. Partner A’s outside ba-sis would increase from $20 to $25 because of the $5 of taxable income. If Partner A subsequently sells his partnership interest for $25, he would recognize zero gain because his outside basis would equal the sales price. This increase in outside basis prevents a part-ner from suffering the pain of double taxation – which would occur with a C-corporation paying taxes on its income followed by the shareholder paying taxes on his $5 stock sale.

TAX BASIS OF PARTNERSHIP ASSETS (“INSIDE BASIS”)

Inside basis is a partner’s share of the tax basis of the partnership’s assets. Examples include inventory, ac-counts receivable, machinery, and goodwill. Generally, fixed assets such as furniture and machinery are de-preciated over a period of years providing significant tax deductions. Purchased intangibles such as good-will can also provide amortization deductions. How-ever, these depreciation and amortization deductions can only be taken if the inside assets have a tax basis. Once the tax basis is exhausted, no further deduc-tions can come from that particular asset. And, upon the sale of a partnership asset with a high inside ba-sis, less gain or additional loss passes through to the partners.

RELATIONSHIP BETWEEN INSIDE AND OUTSIDE BASIS

Due to adjustments to a partner’s outside basis based on income, expense, contributions and distributions, the tax basis of assets inside the partnership often equals the partners’ aggregate outside bases. In the previous example, the partnership realized $5 of in-come; simultaneously we observed an increase in Partner A’s outside basis. The result is that both A’s outside basis and A’s share of the inside basis equal $25 prior to the sale of Partner A’s partnership in-terest. Several events, however, can cause a dispar-ity between inside and outside basis: (1) the sale of a partnership interest, (2) certain distributions from the partnership, and (3) the death of a partner. The IRC §754 election works to reduce these disparities so that a partner’s outside basis comes closer to match-ing her share of the inside basis of the partnership as-sets. On a slightly deeper level, an IRC §754 election also causes the tax equity account on a tax balance sheet to equal a partner’s outside basis when added to the partner’s share of liabilities.

SECTION 754 AND THE SALE OF PARTNERSHIP INTEREST

The sale of a partnership interest is frequently the reason for making an IRC §754 election. Often, a pur-

PAGE 6

QUARTERLY

chaser seeks to obtain the same tax benefit that he would receive if assets were purchased outright rather than indirectly as part of a partnership interest. If no election is in effect, nothing happens at the partner-ship level and the purchaser does not get the benefit of the depreciation, amortization, and/or decreased gain which (in all fairness) should have been his. How-ever, with an IRC §754 election in place, the tax basis of the assets inside the partnership are adjusted ac-cording to IRC §743(b) so the aggregate inside basis of the purchaser’s share of assets generally equals the purchase price for the partnership interest.

One of the most important assets to consider when evaluating whether to make an IRC §754 election is goodwill. According to IRC §197, goodwill only has an amortizable tax basis if it has been purchased. Other-wise the tax basis of goodwill is zero. However, if an IRC §754 election is in effect at the time of purchase there is often a significant increase in the tax basis of the goodwill, which could then be amortized over a 15-year period.

Also, an IRC §754 election only impacts the partner who paid real money to the old partner for her inter-est in the partnership. Any corresponding deprecia-tion, amortization, or other benefit (or detriment) will be included in the new partner’s distributive share of income or loss. That is, any adjustment made to the inside basis of partnership assets under IRC §743(b) due to a sale of partnership interest makes no differ-ence for the other partners in the partnership.

SECTION 754 AND PARTNERSHIP DISTRIBUTIONS

An IRC §754 election also affects the tax basis of the assets inside the partnership when certain distribu-tions from a partnership occur. And, in marked con-trast with the solitary impact on the one partner who buys her partnership interest, distribution-based ad-justments affect all of the partners who remain in the partnership.

However, not all distributions from a partnership cause a tax basis adjustment under the election. Ac-cording to IRC §734(b), in order for a distribution to cause inside basis to be adjusted as a result of the IRC §754 election, a distribution from a partnership must either (i) cause the partner receiving the asset

to recognize gain or loss from the distribution, or (ii) change the basis of a distributed asset.

Generally, under IRC §732, when an asset is distrib-uted from a partnership, the partner’s outside basis is decreased by the tax basis of the distributed asset. For example, if the partner’s outside basis is $50 and machinery with a tax basis of $12 is distributed, the partner’s outside basis would decrease by $12 to $38. The partner would then hold the machinery outside the partnership with a $12 tax basis. Sometimes, how-ever, a partner does not have sufficient outside basis to absorb the tax basis of an asset being distributed. If cash and marketable securities were distributed in excess of the partner’s outside basis a gain would re-sult equaling the excess amount. If an IRC §754 elec-tion has been made the resulting gain would cause an increase of the tax basis of the remaining assets inside the partnership.

In a similar situation where assets other than cash and marketable securities are also distributed from a part-nership, a partner’s outside basis is first decreased by the cash distributed, and then any remaining outside basis is allocated to the non-cash assets based on their relative market values. If cash and other prop-erty is distributed together and the cash exceeds the partner’s outside basis a gain would result and there would be zero basis to allocate to the other property. The consequence of such distribution is that the dis-tributed assets end up with a new basis less than they had inside the partnership. This situation would cause an adjustment under IRC §734(b) if an IRC §754 elec-tion was in effect so that the tax basis of assets inside the partnership would be increased – for the benefit of all partners – by the same amount the distributed asset basis was decreased.

A distribution could also cause an increase in the ba-sis of distributed assets. This could occur only upon a liquidating distribution when a partner’s outside ba-sis is greater than the tax basis of the assets being distributed. In this situation, the distributed assets as-sume the entire amount of the partner’s outside ba-sis. If an IRC §754 election is in effect, the tax basis of assets remaining inside the partnership would be reduced by an amount equal to the excess of the part-ner’s outside basis over the inside basis of the assets immediately prior to the distribution.

But what happens when a partner recognizes loss on a distribution? A loss could only occur upon a liq-

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 7

uidating distribution when a partner fully exits the partnership, and when the departing partner gets cash and marketable securities (and no other assets) which equal less than the partner’s outside basis. The result of the loss if an IRC §754 election is in effect is an increase in the tax basis of the assets inside the partnership.

SECTION 754 AND DEATH OF A PARTNER

If an IRC §754 election is in effect for the year of a partner’s death, a proportionate share of inside basis would also be adjusted in tandem with any tax ba-sis adjustment under IRC §1014(a). Similar to sales or exchanges, the adjustment of inside basis following the death of a partner is governed by IRC §734(b) and benefits only the successor partner who inherits the partnership interest. The IRC §754 election can

be an important estate planning tool because it can be made after the death of a partner so long as an election statement is filed along with a timely filed partnership tax return in the subsequent year.

SECTION 755 ALLOCATION OF ADJUSTMENT TO SPECIFIC ASSETS

IRC §755 and the corresponding regulations govern the allocation of the tax basis adjustments which re-sult under IRC §743(b) and IRC §734(b) if an IRC §754 election is in effect. However, the process is slightly dif-ferent depending on whether the adjustment is due to a sale or exchange or transfer on death or whether the adjustment is as a result of a distribution.

Adjustments that result under IRC §743(b) from the sale or exchange or from a transfer of a deceased

PAGE 8

QUARTERLY

partner’s interest are treated similarly. First, the ad-justment is divided into two different buckets: (i) ordinary income producing property such as inven-tory and accounts receivable and (ii) capital gain plus IRC §1231 property (real estate or depreciable prop-erty used in a trade or business for more than one year). Generally, an amount equal to the built-in net gain or loss is first allocated to the ordinary income producing property (up to its market value), with any remainder allocated to the capital gain and IRC §1231 property. This method of separation into the two dif-ferent groups causes any discount or premium on the purchase of the partnership interest to be allocated to the capital gain bucket rather than the bucket of or-dinary income producing assets. Once the allocation between the two different asset buckets occurs, al-location within the two different buckets takes place based on the amount of gain or loss that would occur if the assets were sold for market value.

Conversely, under IRC §734(b), any adjustment oc-curring as a result of gain or loss recognized as a re-sult of a distribution is only allocated to capital gain bucket. Once in the capital gain bucket, the adjust-ment is further allocated based on the relative value of each of the assets. Any adjustment occurring as a result of a change in the tax basis of the distributed assets is allocated between the two different buckets based on the type of asset distributed. For example, if inventory is distributed and assumes a smaller tax basis outside the partnership, only the tax basis of the partnership’s ordinary assets, such as inventory and accounts receivable inside the partnership, would be adjusted.

A DOUBLE-EDGED SWORD

Although an IRC §754 election can provide a positive tax benefit, it can also have a detrimental effect if the value of the partnership decreases in the future. If time passes after a partnership makes an IRC §754 election and the value of the partnership is lower than the tax basis of the assets inside the partnership, any sale or exchange, distribution, or transfer upon the death of a partner could cause the tax basis of assets inside the partnership to decrease. Due to the often hazy nature of future values, making an IRC §754 election should be done with caution.

ADMINISTRATIVE CONCERNS

For partnerships that have significant partner turn-over, the IRC §754 election can cause significant bur-den and expense due to the fact that the partnership must maintain separate tax basis records for each partner. That’s because the partnership must main-tain separate tax basis records for each partner. These additional records often cause complexity, increased risk for error on the tax return and must be balanced against any tax savings from making the election.

TECHNICAL TERMINATION

IRC §708(b) is also a valuable statute that can be used in conjunction with an IRC §754 election when 50 percent or more of the total interest in partner-ship capital and profits is sold or exchanged within a 12-month period. This is because the sale of such interest causes a partnership to terminate for tax pur-poses and a new partnership is deemed to be formed. Under IRC §708(b) the old partnership is treated as contributing all of its assets and liabilities to a new partnership in exchange for the new partnership inter-est. The old partnership is then deemed to liquidate and distribute its only asset, which is the new partner-ship interest, to the new partners. This is important because the old partnership files a final tax return and none of the elections of the old partnership are appli-cable to the new partnership. If an IRC §754 election is made on the old partnership final return the assets inside the partnership could be stepped up to reflect the purchase price without having future uncertainty. The new partnership would simply take the assets with the increased basis and have no IRC §754 elec-tion in place to cause future unwanted results.

MAKING AND REVOKING THE ELECTION

An IRC §754 election is made by attaching a state-ment to the IRS Form 1065 that is filed for the taxable year in which the election first applies. The election is a partnership election and not a partner election. This distinction is important because the election affects all the partners in a partnership and a partnership can only revoke the election by receiving special approval from the IRS, which is only granted under special cir-cumstances.

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 9

Cool headline would go here.

Uptasincta culparum nis voluptatur sam

ut providem et asped qui tem volectas et

quist, vendit am, coreniet pratus et estrum

et ilit harcimo l debis eatur, que sundus,

imi, nem que estios simin rem que nobit.

I heard about WealthCounselfrom a trusted collea� e.

I joined, because he was right.

Darrin K. JohnsMember since 2015

Deacon HaymondMember since 2012

When you invite a fellow

attorney to WealthCounsel,

you’re introducing a world of

opportunity to them. Our legal

drafting solutions will bring

effi ciency and professionalism

to their practice, while our

educational programs are

proven to grow and lengthen

careers. And we don’t have

to tell you how personally

and professionally rewarding

our member network can be.

This is where connections are

made, relationships are built,

and confi dence is found.

Why not invite someone new

to WealthCounsel today?

You’ll help a colleague and

enrich your own network

along the way.

NOW GET 1 MONTH FREE MEMBERSHIP for you and for

your referral when they join.

wealthcounsel.com/sharethewealth

PAGE 10

QUARTERLY

How Pigs Get Slaughtered:

PARTNERSHIP AUDIT PROCEEDINGS UNWIND ABUSIVE TAX SHELTERS

JENNIFER L. VILLIER, JD, WEALTHCOUSEL LEGAL EDUCATION FACULTY

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 11

Partnership taxation is the default federal tax classi-fication for multi-member LLCs. Most LLCs are taxed as partnerships because of the flexibility and pass-through taxation available to partnerships, which is not characteristic of the corporate form. As a result of the flexibility afforded partnership tax structures, they run the risk of abuse in the form of federally pro-hibited tax shelters. A number of recent cases, includ-ing a U.S. Supreme Court case that is the focus of this article, remind us that tax shelter litigation is still very much a part of many court dockets today.1 In review-ing partnership tax filings, the Internal Revenue Ser-vice (“IRS”) may identify red flags that trigger an au-dit, such as when an abusive tax shelter arrangement or sham partnership structure is suspected.

This article (i) provides a brief overview of federal partnership tax audit proceedings under the Tax Eq-uity and Fiscal Responsibility Act of 1982 (“TEFRA”),2 (ii) discusses U.S. v. Woods, a 2013 U.S. Supreme Court case involving a federal partnership audit where an abusive tax shelter was in place, and (iii) concludes that attorneys should be aware of the characteristics of abusive tax shelters and refrain from assisting in their formation or operation.

FEDERAL PARTNERSHIP TAX AUDIT PROCEEDINGS

Although a partnership3 is not a tax-paying entity, it must file a Form 1065 information return to report its income, gains, losses, deductions, and credits. Those tax items pass through the partnership, appear on each partner’s Schedule K-1, and are reported on each partner’s individual tax return. Prior to the enactment of TEFRA, there were no unified audit proceedings for partnerships. Instead, if the IRS identified an er-ror on the partnership’s information return, then it would have to bring a separate deficiency proceed-ing against each partner, which resulted in duplica-tive, sometimes inconsistent, proceedings. Pursuant to TEFRA, many partnerships are subject to unified federal tax audit proceedings, which are designed to facilitate partnership tax audits by determining ad-justments at the partnership level rather than requir-ing the IRS to audit each individual partner. Any part-nership subject to the comprehensive unified audit proceedings is required to have a tax matters partner.

The tax matters partner must be a “general partner,” and must either be (i) designated as tax matters part-ner by the partnership or, if no designation has been made, (ii) the partner with the largest profits interest.4

The unified federal tax audit proceedings generally consist of two stages: a partnership-level proceeding followed by partner-level proceedings. A partnership-level proceeding involves the partnership as a whole and is typically held after the IRS has identified an is-sue with the partnership’s information return. In a part-nership-level proceeding, “partnership items” may be adjusted. Once the partnership-level proceeding has taken place, the IRS issues a Notice of Final Partnership Administrative Adjustment (“FPAA”), which is subject to judicial review in the Tax Court, the Court of Federal Claims, or federal district court.5 The reviewing court has jurisdiction over all partnership items, including al-location of partnership items among the partners and determination of the applicability of penalties or ad-ditional tax relating to an adjustment of a partnership item.6 Following judicial review, the IRS’s partnership item adjustments become final, and the IRS may initi-ate partner-level proceedings to make related adjust-ments to each individual partner’s tax liability.7

A “small partnership” is exempt from the unified audit rules. A partnership is considered to be a “small part-nership” if it has ten or fewer partners, each of which is an individual (other than a non-resident alien), a C corporation, or the estate of a deceased partner. Any partnership having a disregarded entity as a partner cannot be a “small partnership,” regardless of its total number of partners. A husband and wife are treated as one partner for purposes of determining whether a partnership is a “small partnership.” Although exempt from the unified audit rules, a “small partnership” can elect to be subject to them.

U.S. V. WOODS8

In a series of recent cases, the unified partnership au-dit proceedings were utilized in situations involving abusive tax shelters. Two of those cases, Tigers Eye Trading9 and Petaluma,10 were resolved based upon the U.S. Supreme Court’s holding in U.S. v. Woods, and all three have remarkably similar fact patterns.11

The taxpayers in Woods were involved in an offset-ting-option tax shelter, a structure intended to create

PAGE 12

QUARTERLY

large paper losses that a taxpayer could use to reduce taxable income. By giving the taxpayer an artificially high basis in a partnership interest, the tax shelter en-abled the taxpayer to claim a substantial tax loss upon disposition of the partnership interest. The taxpayers in Woods, Gary Woods (the tax matters partner) and Billy Joe McCombs, participated in the tax shelter by engaging in the following series of transactions:

They created two general partnerships, one intended to produce ordinary losses (Tesoro Drive Partners) and the other intended to produce capital losses (SA Tesoro Investment Partners).

Acting through their respective wholly owned LLCs, each purchased five 30-day currency-option spreads and contributed them to the newly formed partner-ships, along with $900,000 in cash. The option spreads consisted of a long option (entitling them to a sum of money if a currency exchange rate exceeded a certain amount on a given date) and a short option (requiring them to pay the bank a sum of money if the exchange rate for the currency on the given date exceeded a cer-tain amount). The noteworthy feature of the long and short options was that the trigger amounts for each were so close that it was likely that both options would be triggered (or not triggered) on the specified date.

Using the cash, the partnerships purchased Canadian dollars for the partnership created to produce ordi-nary losses, and Sun Microsystems stock for the part-nership created to produce capital losses.

The partnerships terminated the five option spreads and received a lump-sum payment from the bank.

Near the tax-year end, the taxpayers each transferred their partnership interests to two S corporations (one S corporation received both partners’ interests in Tes-oro Drive Partners and the other received both part-ners’ interests in SA Tesoro Investment Partners).

The partnerships, each now having a single partner (the S corporation), were liquidated by operation of law and their assets were deemed distributed to the S corporations.

The S corporations sold the assets for a gain of $2,000 on the Canadian dollars and $57,000 on the stock.

Rather than reporting the gains, the S corporations reported an ordinary loss of $13 million on the sale of the Canadian dollars and a capital loss of $32 million on the sale of the stock. The losses were allocated be-

tween the taxpayers as the S corporations’ co-owners.

The taxpayers were able to claim such enormous losses because their outside tax basis was greatly inflated.12 The taxpayers had contributed $3.2 million in option spreads and cash to acquire their partnership interests, but, because they omitted the “short” option in their basis computation on the theory that it was “too con-tingent,” their total outside basis was over $48 million. Under Code §732(b), the basis of property distributed to a partner in a liquidating distribution is equal to the adjusted basis of the partner’s interest in the partner-ship (reduced by any cash distributed with the prop-erty). Therefore, the taxpayers’ inflated outside basis figures were carried over to the S corporations’ basis in the Canadian dollars and the stock, resulting in the taxpayers’ huge losses when the assets were sold.

The partnerships’ information returns triggered an audit, after which the IRS issued each partnership an FPAA. The IRS determined that the partnerships (i) had been formed and used solely for purposes of tax avoid-ance, (ii) had no business purpose other than tax avoid-ance, (iii) lacked economic substance, and (iv) were shams.13 Furthermore, the IRS subjected the taxpayers to a 40% penalty for gross valuation misstatements as a result of inflating the tax basis of their interests in a partnership that, for tax purposes, did not exist.

Woods sought judicial review of the FPAAs. The District Court held that the partnerships were properly disre-garded as shams but that the valuation misstatement penalty did not apply. As to the latter determination, the IRS appealed. While the appeal was pending, the Fifth Circuit held in a similar case that the valuation misstate-ment penalty does not apply when the partnership is disregarded as a sham.14 The U.S. Supreme Court grant-ed certiorari to resolve a Circuit split on this issue.

Under Code §6226(f), a court in a partnership-level proceeding has jurisdiction to determine the applica-bility of a penalty that “relates to” an adjustment to a partnership item. Thus, the issue was whether the val-uation misstatement penalty “relates to” the determi-nation that the taxpayers’ partnerships were shams. In resolving the dispute, the Court examined the struc-ture of TEFRA and concluded that, while penalties must be imposed at the partner level, their applicabil-ity may be determined at the partnership level. In oth-er words, a penalty can “relate to” a partnership-item adjustment even if the penalty cannot be imposed

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 13

without additional, partner-level determinations.15

Next, the Court considered the applicability of the valuation misstatement penalty. Generally, a 20% penalty applies to any underpayment of tax attribut-able to any substantial valuation misstatement. The penalty increases to 40%, however, when a taxpayer’s adjusted basis exceeds the correct amount by at least 400%.16 The Woods Court determined that because “the partnerships were deemed not to exist for tax purposes, no partner could legitimately claim an out-side basis greater than zero.”17 Since the partners used an outside basis greater than zero to claim losses that caused the partners to underpay their taxes, the re-sulting underpayment is “attributable” to the inflated adjusted basis amount. Thus, the Court held that (i) the District Court had jurisdiction in the partnership-level proceeding to determine the applicability of the valuation misstatement penalty, and (ii) the penalty is applicable to tax underpayments resulting from the partners’ participation in the tax shelter.

TAKEAWAYS

While the case law made no mention of the attorneys’ roles or liability in any of the three fact patterns (other than to point out that the tax shelter in Woods was de-veloped by the “now-defunct” law firm Jenkens & Gil-christ, P.C.), it goes without saying that, as professionals, we should steer clear of any involvement with abusive tax shelters.18 Model Rule of Professional Conduct Rule 1.16 instructs that attorneys should avoid counseling clients on matters involving illegal conduct or transac-tions. Attorneys representing clients in connection with abusive tax shelters risk stiff penalties as well as expen-sive and time-consuming malpractice litigation.

When Jenkens & Gilchrist closed its doors following its role in the marketing and promotion of fraudulent tax shelters, the IRS announced, “this should be a lesson to all tax professionals that they must not aid or abet tax evasion by clients or promote potentially abusive or illegal tax shelters, or ignore their responsibilities to register or disclose tax shelters.”19 Thus, attorneys rep-resenting partnership clients should consider whether a client’s proposed or existing structure has economic substance, and counsel clients regarding the lengthy audit proceedings and potential for penalties should the IRS suspect the partnership is merely a sham

formed with the purpose of evading federal taxes.

ENDNOTES

1 See U.S. v. Woods, 134 S.Ct. 557(2013); Logan Trust & Tigers Eye Trading, LLC v. Comm’r, No. 12-1148 (D.C. Cir. 2015); Petaluma FX Partners, LLC v. Comm’r, No. 12-1364 (D.C. Cir. 2015); Basr Partner-ship v. U.S., No. 2014-5037 (Fed. Cir. 2015)

2 26 U.S.C. §§6221, et seq.

3 Note that all references in this article to a “partnership” include any LLC taxed as a partnership, and all references to a “partner” include a member of an LLC that is taxed as a partnership.

4 When preparing an LLC operating agreement in Business Docx, you will be prompted to select a tax matters member. You have the option to either name a specific member in the Operating Agree-ment, or indicate that the manager will appoint a tax matters mem-ber at a later time.

5 26 U.S.C. §6226(a)

6 Id. §6226(f)

7 Id. §§6230(a)(1)-(2), (c), 6231(a)(6)

8 134 S.Ct. 557 (2013)

9 Logan Trust & Tigers Eye Trading, LLC v. Comm’r, No. 12-1148 (D.C. Cir. 2015)

10 Petaluma FX Partners, LLC v. Comm’r, No. 12-1364 (D.C. Cir. 2015)

11 Both Tigers Eye Trading and Petaluma involved taxpayers hold-ing interests in LLCs taxed as partnerships. Each such partner-ship was created to establish a Son of BOSS tax shelter pursuant to which each taxpayer artificially inflated his basis resulting in substantial “losses” that the taxpayers were able to use to offset against income and gains on their personal tax returns. The scheme artificially reduced their taxable income, as discovered by the IRS upon audit. Both cases were held in abeyance pending the Supreme Court’s decision in Woods, as the issue in all three cases was the same: whether courts in partnership-level proceedings have ju-risdiction to determine the applicability of accuracy-related pen-alties related to the partners’ underpayment of income tax. Both cases were ultimately decided on June 26, 2015, consistent with the Woods’ holding.

12 Tax basis is generally the cost of an asset and it is used to deter-mine the owner’s gain or loss for tax purposes upon sale.

13 Id. at 562

14 See Bemont Invs., LLC v. U.S., 679 F.3d 339, 347-48 (2012)

15 Id. at 564

16 Id. at 565; Code §6662(h)

17 Woods, at 565-66

18 For another recent case involving a partnership tax shelter and describing the attorneys’ role in marketing the scheme, please see Basr Partnership v. U.S., No. 2014-5037 (Fed. Cir. 2015).

19 See I.R.S. News Release IR-2007-71 (Mar. 29, 2007); Soled, Jay A. “Tax Shelter Malpractice Cases and their Implications for Tax Compliance,” American University Law Review 58, no. 2 (December 2008).

PAGE 14

QUARTERLY

Climbing the Tax-Efficiency Pyramid to Lower Taxes

TIM VOORHEES, JD, WEALTHCOUNSEL MEMBER SINCE 2013

Opportunities for attorneys in-creased dramatically in early 2013 when the President signed the American Tax Relief Act of 2012 into law. While the demand for estate planning shrank when the estate and gift tax exemption in-creased from $1million per person to the new “permanent” exemp-tion of more than $5 million per individual, the need for income tax planning grew substantially when the top marginal rates increased for most taxpayers. Many clients will now have top tax rates of more than 35 percent on capital gains and more than 50 percent on ordi-nary income unless financial plan-ners provide solutions.

The impact of the new higher tax rates is evident when projecting retirement savings growth over 20 years. For example, a business own-er funding a retirement plan with $500,000 over the next few years can expect the plan to generate more than $1,760,000 of tax-free

income (if money grows at 6.5 per-cent and there are no taxes on con-tributions or withdrawals). If, how-ever, the executive is married with income of more than $450,000, then marginal tax rates may be 39.6 percent at the federal level and 10.23 percent at the state level. Together, these taxes reduce mon-ey going into Roth IRAs, retirement annuities, and related retirement investments by almost 50 percent. If the executive keeps the money in annuities or stock investments, there will likely be additional tax-es when the funds are withdrawn. Even if withdrawals are taxed at capital gains rates instead of or-dinary income rates, the Federal capital gains rate of 20 percent is often increased by the 3.8 per-cent surtax for couples earning more than $250,000, and further increased by state tax rates that approach or exceed 10% in major states like California and New York. It is therefore common to see capi-

tal gains taxes that consume more than one-third of gains. In the larg-est state (California), capital gains rates can exceed 38%.

To illustrate the impact of taxes, it is useful to look at how taxes re-duce returns across time. Con-sider a client who has $500,000 of excess income (e.g., income not used for lifestyle expenses) this year or over the next few years. If the 50 percent rate on contri-butions applies along with the 38 percent rate on withdrawals, the $500,000 is worth only $662,287 in 30 years. On the other hand, if the client invests the $500,000 in vehicles that generate current tax deductions and avoid taxes on investment income and distri-butions, the $500,000 can grow across 30 years to be worth more than $5,000,000. Would a client rather have a half million of extra taxable income grow to $662,000 or $5,000,000?

VOLUME 9 NUMBER 3 / Q3 2015

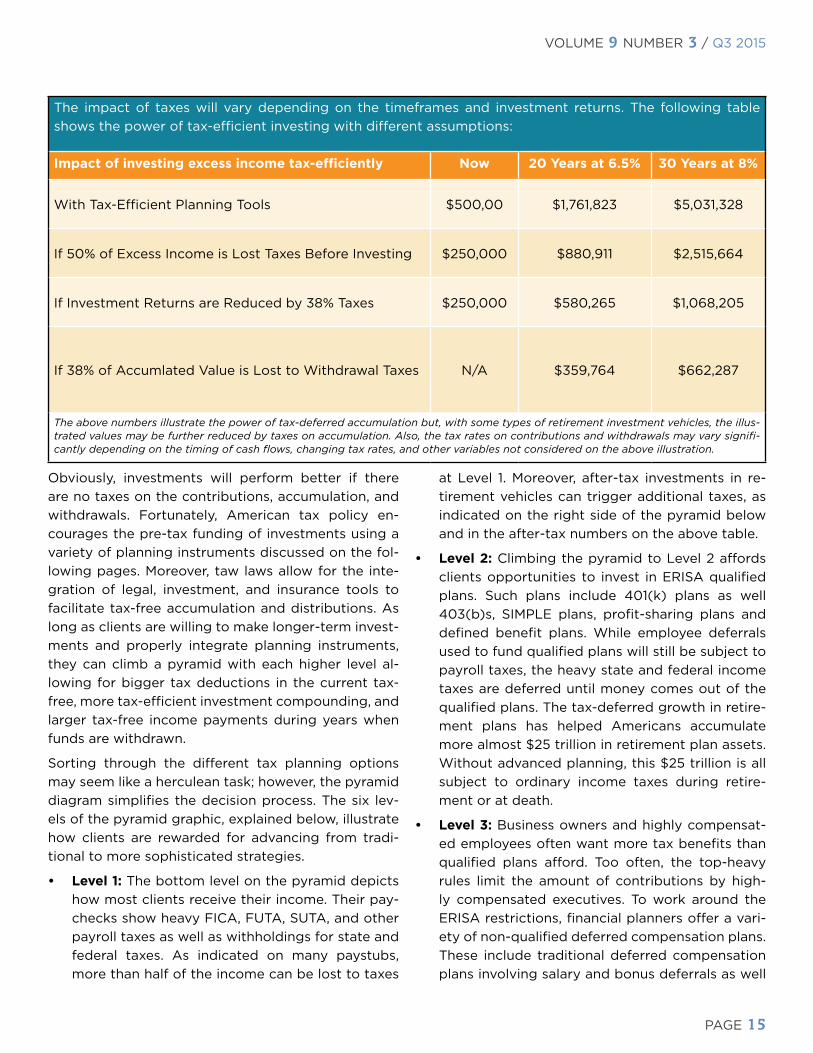

PAGE 15

The impact of taxes will vary depending on the timeframes and investment returns. The following table shows the power of tax-efficient investing with different assumptions:

Impact of investing excess income tax-efficiently Now 20 Years at 6.5% 30 Years at 8%

With Tax-Efficient Planning Tools $500,00 $1,761,823 $5,031,328

If 50% of Excess Income is Lost Taxes Before Investing $250,000 $880,911 $2,515,664

If Investment Returns are Reduced by 38% Taxes $250,000 $580,265 $1,068,205

If 38% of Accumlated Value is Lost to Withdrawal Taxes N/A $359,764 $662,287

The above numbers illustrate the power of tax-deferred accumulation but, with some types of retirement investment vehicles, the illus-trated values may be further reduced by taxes on accumulation. Also, the tax rates on contributions and withdrawals may vary signifi-cantly depending on the timing of cash flows, changing tax rates, and other variables not considered on the above illustration.

Obviously, investments will perform better if there are no taxes on the contributions, accumulation, and withdrawals. Fortunately, American tax policy en-courages the pre-tax funding of investments using a variety of planning instruments discussed on the fol-lowing pages. Moreover, taw laws allow for the inte-gration of legal, investment, and insurance tools to facilitate tax-free accumulation and distributions. As long as clients are willing to make longer-term invest-ments and properly integrate planning instruments, they can climb a pyramid with each higher level al-lowing for bigger tax deductions in the current tax-free, more tax-efficient investment compounding, and larger tax-free income payments during years when funds are withdrawn.

Sorting through the different tax planning options may seem like a herculean task; however, the pyramid diagram simplifies the decision process. The six lev-els of the pyramid graphic, explained below, illustrate how clients are rewarded for advancing from tradi-tional to more sophisticated strategies.

• Level 1: The bottom level on the pyramid depicts how most clients receive their income. Their pay-checks show heavy FICA, FUTA, SUTA, and other payroll taxes as well as withholdings for state and federal taxes. As indicated on many paystubs, more than half of the income can be lost to taxes

at Level 1. Moreover, after-tax investments in re-tirement vehicles can trigger additional taxes, as indicated on the right side of the pyramid below and in the after-tax numbers on the above table.

• Level 2: Climbing the pyramid to Level 2 affords clients opportunities to invest in ERISA qualified plans. Such plans include 401(k) plans as well 403(b)s, SIMPLE plans, profit-sharing plans and defined benefit plans. While employee deferrals used to fund qualified plans will still be subject to payroll taxes, the heavy state and federal income taxes are deferred until money comes out of the qualified plans. The tax-deferred growth in retire-ment plans has helped Americans accumulate more almost $25 trillion in retirement plan assets. Without advanced planning, this $25 trillion is all subject to ordinary income taxes during retire-ment or at death.

• Level 3: Business owners and highly compensat-ed employees often want more tax benefits than qualified plans afford. Too often, the top-heavy rules limit the amount of contributions by high-ly compensated executives. To work around the ERISA restrictions, financial planners offer a vari-ety of non-qualified deferred compensation plans. These include traditional deferred compensation plans involving salary and bonus deferrals as well

PAGE 16

QUARTERLY

as more sophisticated plans covered by 409(A) rules on deferred compensation. With the com-mon Supplemental Employee Retirement Plan (“SERP”) arrangements, the employer must wait to receive the deduction until the employee re-ceives the benefit.

Since 2004, the 409(A) regulations have in-creased the risk of current taxes applying to non-qualified deferred compensation plans, including restricted stock, phantom stock and performance

share plans, as well as stock appreciation rights and long-term bonus or commission programs. Many executives have used these plans to ac-cumulate substantial balances without realizing the full extent of the likely withdrawal taxes. Now these executives face much higher than expected taxes on their withdrawals because of the higher marginal rates in 2015. This is spurring growing in-terest in Levels 4 through 6 of the pyramid.

• Level 4: The Level 4 solutions include a vari-

CLIMBING THE PYRAMID ENHANCES TAX-EFFICIENCYTAXES ON

CONTRIBUTIONSTAXES ON

EMPLOYEE WITHDRAWAL

Minimal Tax on Contributions

LEVEL 6 Advanced Tax-Efficient Lifetime Income Solutions

ChESOP Capital Split Dollar

Charitable LLC Captive Preferred LLC

Retirement Rescue

Minimal Withdrawal Taxes

Moderate Tax on Contributions

LEVEL 5 Specialized Plans with Tax-Efficient Funding and Tax Free

Withdrawals Super CLAT

Section 79 Plan Section 162 Plan

Moderate Withdrawal Taxes

Moderate Tax on Contributions

LEVEL 4 Speicialized Plans with Pre-Tax Funding Partially Withdrawals

Charitable Reminder Trust Gift Annuities

Pooled Income Fund

Moderate Withdrawal Taxes

Moderate Tax on Contributions

LEVEL 3 Non-Qualified Deferred Comp

SERPS 409(A) Plans

Traditional Deferred Comp

Heavy Withdrawal Taxes

Heavy FICA, FUTA, SUTA Taxes

LEVEL 2 Qualified Plans

Profit Sharing Defined Benefit

401(K)

Heavy Withdrawal Taxes

Heavy FICA, FUTA, SUTA Taxes

LEVEL 1 Traditional Compensation

Heavily taxed with payroll taxes going in and ordinary income out

Heavy Withdrawal Taxes

THE TAX EFFICIENCY PYRAMID

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 17

ety of charitable planning instruments that al-low for large income tax deductions when they are funded as well as tax-deferred growth on the plan balances. Moreover, the distributions may have only moderate withdrawal taxes. For example, charitable remainder trusts (CRTs) can distribute tax-free or capital gains income. Gift annuities can pay out partially tax-free in-come by returning the initial investment capital as part of each payment. These charitable tools can be custom-designed for each individual to start retirement income when income is most needed or tax rates are lowest. For these reasons, the charitable tools at Level 4 can provide bet-ter bottom line benefits than those generated at levels 1-3.

• Level 5: Clients focused on retirement security and income may reject level 4 solutions because “char-ity begins at home.” Fortunately, there are chari-table solutions, such as a Super CLAT designed with the current low 7520 rate that can increase what goes to the donor throughout retirement. For substantial benefits from non-charitable tools, employers will often take deductions for a Section 162 plan or a Section 79 plan. For example, a com-pany can make pre-tax contributions of $500,000 to a Section 79 plan so that an employee can re-ceive tax-free income of nearly $1.1 million while also funding a tax-free death benefit for his or her heirs that may be more than $1 million.

• Level 6: Creative planners continue to find syner-gistic combinations of planning instruments that can provide benefits that exceed those illustrated in Level 5. For example, the Family Retirement Ac-count™ (“FRA”) leverages the benefits of universal life insurance using loans and a dynasty trust in order to convert taxable retirement income into tax-free cash flow and/or wealth transfers. Capital Split Dollar (“CSD”) helps employers take income tax deductions for funding tax-free retirement and death benefits for key executives. An Em-

ployee Stock Ownership Plan (“ESOP”) can pro-vide tax-free build-up of assets. When the ESOP is combined with a charitable trust, the resulting “ChESOP” can produce both tax deductions in the early years and tax-free income in later years.

For clients with more charitable intent, a popular Lev-el 6 strategy is the charitable LLC. $500,000 contrib-uted can produce more than $2 million for family and charity. The family benefits can exceed those of the Section 79 plan while also giving clients the satisfac-tion of redirecting tax money to their favorite chari-ties.

While qualified attorneys opine that the above Lev-el 6 strategies are within the letter and spirit of the tax code, the techniques may be too complicated for some clients. Moreover, attorneys must consider a long list of legal, tax, and financial issues when in-tegrating the components of the advanced planning tools. Failure to implement and monitor strategies correctly can create unnecessary audit risks. If the cli-ent has concerns about the ability of his or her team to maintain a Level 6 strategy across time, then sim-pler strategies at Levels 2 to 5 may be better.

CONCLUSION

New tax laws, such as the 409(A) rules passed sev-eral years ago and the American Tax Relief Act signed in 2013, have curtailed many popular planning strate-gies. Wise planners, like Hercules, find that each time a head is cut off the hydra, two new heads grow. The decline in the demand for estate tax planning is small compared to the big increase in the demand for in-come planning and retirement planning. Attorneys have immense opportunities to serve the tens of mil-lions of present and prospective clients who are stuck at Level 1 or Level 2 of the tax efficiency pyramid. As indicated above, there are compelling reasons and great financial rewards for the clients who advance to Levels 3, 4, 5 and 6 in the tax efficient lifetime income planning process.

ABOUT THE AUTHOR

Tim is the Principal Partner at Matsen Voorhees Mintz, LLP and President of Voorhees Family Office Services. He has 37 year of experience providing wealth, estate, and charitable planning for multi-million dollar estates through national wealth planning organizations and financial service companies. Tim regularly publishes ar-ticles in leading publications and speaks at conferences for many national organizations.

PAGE 18

QUARTERLY

Before you pour…

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 19

The uncertainty of the transfer tax system in place be-fore ATRA1 motivated many clients to establish vari-ous irrevocable trusts as part of their estate planning process. In addition to the ILITs, IDGTs, and other ir-revocable trust-driven lifetime wealth transfer strate-gies that wealthier clients implemented, most married couples who completed their planning before 2013 relied on mandatory marital deduction funding meth-ods in their wills and revocable trusts.

Those common marital deduction strategies often forced the establishment of a bypass or “credit shel-ter” trust to set assets aside for the surviving spouse and other beneficiaries in an estate tax-sheltered en-vironment. When the surviving spouse later died, the assets in that bypass trust would be excluded from his or her gross estate, passing to the remainder benefi-ciaries free of transfer tax.

With ATRA came the combination of permanent, $5 million inflation-indexing estate tax exemptions and DSUE Amount portability for surviving spouses, ob-viating estate tax-driven strategies for all but a min-iscule percentage of the U.S. population. In fact, ac-cording to a 2015 report from the Congressional Joint Committee on Taxation, only 0.2% (roughly two in 1,000) of Americans will die owing federal estate tax liability.2

But higher marginal income tax rates, a higher capi-tal gains tax rate, and certain income surtaxes that washed in with the Affordable Care Act have put in-come tax-driven strategies closer to the top of the list for most clients. Moreover, while the pain of transfer tax was on a distant horizon, the pain of income tax is acute and immediate as clients see that their income and wealth doesn’t stretch as far as it used to. With trusts reaching the highest 39.6% marginal income tax bracket with only $12,300 in income (for the 2015 tax year), finding ways to minimize the amount of income trapped inside trusts and maximizing basis adjust-ment on appreciated assets have become among the most critical planning issues attorneys must consider when planning and administering clients’ estates.

IMPACT OF SHIFTED FOCUS ON CLIENT PLANNING INCOME TAX

The shifted focus from transfer tax to income tax can be particularly vexing in the context of a client’s ex-isting irrevocable trust strategy. Whether the trusts were initially designed as irrevocable, or whether the trust has become irrevocable because of the settlor’s death, when circumstances change that impose new adverse consequences, or when new opportunities

Before you pour…A FEW TAX CONSIDERATIONS WHEN DECANTING

MATTHEW T. MCCLINTOCK, JD, VICE PRESIDENT, WEALTHCOUNSEL EDUCATION

PAGE 20

QUARTERLY

emerge that can benefit the client and her family, cli-ents and their advisors need solutions to restructure irrevocable trusts for maximum benefit.

For many grantors, opportunities to modify a trust to trigger estate inclusion will mean a step up in basis when the grantor dies, allowing unrecognized capital gains to get wiped away as remainder beneficiaries receive a new basis under IRC §1014. For nongrant-or beneficiaries of irrevocable trusts, modifications might strategically add general powers of appoint-ment over trust corpus, allowing the value of those assets to be included in the beneficiary’s estate at death, again triggering a basis adjustment.

In other circumstances, modifications may be neces-sary to allow a trustee to update key administrative provisions to account for revisions to the governing trust code, or to change the situs and governing law of the trust to a jurisdiction with more favorable trust and tax laws.

Modifications might also allow the trustee to strategi-cally allocate capital gains to income, or modify the trustee’s discretion in making distributions that carry

out the trust’s Distributable Net Income to shift in-come trapped in the trust to beneficiaries in lower tax brackets. Trust modifications may also allow adjust-ments to grantor trust provisions, expanding, con-tracting, or shifting the identity of the taxpayer to strategically direct the trust’s income tax liability.

ASSET PROTECTION

To paraphrase the cynic: so long as there are law-yers, there will be litigants. While many lawsuits are meritorious, others may stem from dubious claims, are brought as nuisance actions, or arise from simple malice by aggrieved parties.

Recognizing that many professions carry a higher level of litigation risk than others, clients often ex-press concern about asset protection opportunities to strengthen their bargaining position in contested matters and improve the possibility for reasonable settlements with claimants.

Clients often turn to trust & estate and business at-torneys to design and implement a series of strate-

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 21

gies that mitigate exposure from creditors. But what happens when clients are beneficiaries of existing irrevocable trusts established by someone else, or when they have preexisting irrevocable trusts in place that offer suboptimal protection? Steps may be taken through trust modification techniques to change an existing irrevocable trust strategy for the better inter-ests of the client.

For instance, in some jurisdictions a trustee may de-cant trusts that contain distribution or demand rights at certain ages into longer term discretionary trusts. Also, modification may allow a trust subject to an “as-certainable standard”3 to be converted to a purely discretionary trust served by an independent trustee. Many practitioners agree that converting the trustee’s power to a standard that is not “ascertainable” will better insulate the beneficiary’s interest in the trust, so long as the trustee is not related or subordinate4 to the beneficiary or the grantor.

Modifications may be desirable to change the struc-ture of trust management, such as adding one or more specialized trustees, changing the mechanisms for reviewing, removing, and replacing trustees, or changing the trust’s situs and governing law to a more favorable jurisdiction – such as a state that has more liberal decanting rules, lower (or no) state income tax, superior asset protection laws, more favorable trustee investment powers, etc.

And some strategies rely on a third party modifica-tion from the outset. For many years the Wealth Docx Standalone Retirement Trust (SRT) assembly has in-corporated an option to allow an independent party serving as a trust protector to convert any trust share originally established as a conduit share into an ac-cumulation trust share, affording superior asset pro-tection for beneficiaries receiving distributions under retirement accounts payable to the trust.5

Similarly, the “hybrid” DAPT strategy6 allows an inde-pendent trust protector to add the grantor as a dis-cretionary beneficiary under a third party DAPT the grantor establishes for other beneficiaries. The trust is arguably not a self-settled spendthrift trust at incep-tion, but if the trust protector decides – presumably independently – to add the grantor into the trust as a beneficiary, proponents of the strategy believe that the trust corpus will be insulated from claims by the grantor’s creditors.

DECANTING AS A MODIFICATION OPTION

Trust decanting ranks fairly high on the spectrum of trust modification options, and it’s the first level that affords real creativity and flexibility.7 Much has been written on the subject and states are increasingly en-acting decanting statutes. But few attorneys (let alone other professionals) have a firm understanding of the range of decanting options that exist, the mechanics of making it work, and the tax implications of decanting.

Trust decanting occurs when the trustee of an existing irrevocable trust8 (often referred to as the “originat-ing” or “inception” trust) exercises his or her discre-tion in making distributions for the benefit of a ben-eficiary and, rather than distribute the property from the trust outright, the trustee distributes property in further trust (the “new” trust).

The origins of decanting stem from the position that if the trustee may distribute property outright – as 1L property class taught us, in “fee simple absolute” – to a beneficiary, then the trustee may distribute prop-erty in less than fee simple, by creating a new trust to manage the distributed property for the benefit of the beneficiary of the property. The trustee’s power to decant may arise from a state’s case law, from statute, or within the governing trust instrument.

TAX IMPLICATIONS OF DECANTING

The IRS has not provided much guidance on the tax implications of decanting beyond highlighting a se-ries of decanting-related issues that may trigger tax liability.9 One of the most important tax-related issues to resolve is the nature and identity of the decanted trust for tax purposes. Wrapped inside that issue are many other questions. Limited space and knowledge does not permit us to address them all, but consider-ation of a few is worth our efforts here.

FOR EXAMPLE…

Is the new trust a new taxpayer, or is it an extension of the originating trust for income tax purposes?

We get some insight from the Treasury Regs, which indicate that, “If a trust makes a gratuitous transfer of property to another trust, the grantor of the trans-

PAGE 22

QUARTERLY

feror trust generally will be treated as the grantor of the transferee trust.”10 There is an exception where the transfer is directed by an individual who holds a general power of appointment over the property in the trust and that person directs the transfer. In that case, the individual exercising the power is treated as the transferor.11 In most trust decantings, the trustee exercising the power to decant will not have a general power of appointment over the trust. An even safer option is to require that any decanting be performed by an independent trustee who has no beneficial in-terest in the trust at all.12

Assuming that the identity of the grantor for income tax purposes remains the same before and after the decanting, it seems logical that the taxpayer identi-fication number (EIN) of the new trust is the same as that of the originating trust. While we don’t have clear guidance from the IRS on this point, PLRs sug-gest that this is the case.13 In the case of cascading subtrusts for individual beneficiaries after the death of the maker of an RLT, each subtrust would receive its own EIN at the time of funding. If the trustee later decants a subtrust into its own separate trust agree-ment, the new trust becomes an extension of that subtrust, and should receive the EIN obtained when the subtrust was established during administration.

To what extent do decanting transfers carry out DNI?

Generally, any distribution from a trust carries out Dis-tributable Net Income (DNI) to the extent of the lesser of the amount distributed or the amount of trust tax-able income for the year of distribution.14 Further, we know that trusts that are created under a decedent’s will (or will substitute, like an RLT) are considered for income tax purposes as a beneficiary of the decedent’s estate.15 And assuming that the originating trust and the new trust are treated as the same taxpayer, the dis-tribution of all the corpus should carry out all the tax attributes from the old trust into the new trust. As oth-er authors point out, even the distribution of less than the entire trust corpus – a partial decanting in further trust – should be treated as distribution to beneficiary, carrying out DNI subject to a few limitations.16

Do transfers of assets from an originating trust trig-ger the recognition of gain or loss?

If the act of decanting triggers a recognition event

causing the recognition of capital gains or losses on the assets, capital gains tax would be due and the ba-sis of the assets in the trust would be subject to ad-justment at the time of transfer.17

In considering this issue, many turn to the holding of Cottage Savings18 for guidance. There the U.S. Su-preme Court found that where there were material differences in the value and composition of assets that were exchanged in an asset swap, the taxpay-ers would recognize taxable gain or loss on the asset swap even if the assets were not distributed and the parties’ economic position hadn’t changed.19

But where the nature of the beneficial interests ad-ministered under an agreement are not materially different before and after a modification, Cottage Savings does not appear to apply and the decant-ing action should be a “non-recognition” event. Al-though the IRS is not yet providing public guidance on this issue, there are PLRs that help frame this po-sition.20

Does a beneficiary who consents – or acquiesces – to decanting make a taxable gift?

If the beneficiary affirmatively consents to a decant-ing, can the beneficiary be treated as a transferor for transfer tax (gift, estate, and GSTT) purposes? Although the Treasury’s position is unclear, we can make some reasonable conclusions to these and other questions. And to provide the lawyer’s answer, sometimes it depends on the nature of the decanting.

A beneficiary’s failure to exercise a legally enforce-able right that arises under state law may constitute a taxable transfer if that failure extinguishes some legal right of the beneficiary.21 Further, when a beneficiary has a vested, presently-exercisable right to property and that beneficiary affirmatively consents to the transfer of that interest to other beneficiaries, the beneficiary will likely be treated as having exercised a taxable power of appointment in favor of those other beneficiaries.22

The safer approach is to permit the trustee to exercise a decanting power without beneficiary involvement at all. This is especially true when acts of decanting alter the nature of beneficial rights or dispositive pro-visions, or modify powers of appointment.

Moreover, if the power to decant is indeed a power of

the trustee, the trustee should be permitted to exercise that power subject to the trustee’s fiduciary obligations. A beneficiary should be required to show that the act of decanting constituted a breach of the trustee’s fiduciary duties in order to object to or set aside the decanting transfer.

Does an interested trustee who decants make a taxable gift?

When the trustee has no interest in the trust, we believe that the trustee who decants in furtherance of his or her fiduciary duties has no transfer tax con-cerns. As stated in Treasury Reg. §25.2511-1(g)(1), “A transfer by a trustee of trust property in which he has no beneficial interest does not constitute a gift by the trustee…” Further, the Regs provide that even when the trustee does have an interest in the trust, if the trustee makes a transfer in furtherance of a fiduciary duty, and if that duty is limited by a fixed or ascertainable standard, then the trustee has not made a taxable transfer.23

Where the act of decanting is intended to strengthen the asset protection character of the trust to convert from an ascertainable standard trust to a discretionary standard trust (and where this is permitted by governing law), it is more effective to have an independent trustee effect the decanting. Where a beneficiary or other interested party is serving as trustee, that interested trustee may resign to make way for an independent trustee to perform the decanting. In the alternative, a special independent trustee may be appointed concurrently with the trustee (either under the terms of the document, as provided by Wealth Docx, or by petition and appointment by a court) to then exercise the power to decant the trust to a more protective structure.

Who is the grantor or transferor for gift, estate, and GSTT purposes?

Because decanting is an extension of an existing trust – and assuming that the decanting is performed by an inde-pendent trustee bound to fiduciary duties – there should be no change in transferor for transfer tax pur-poses. A trustee should only be at risk of being treated as a trans-feror where the trustee has a beneficial interest in the trust, or where the trustee exercises the decanting power in a man-ner that discharges a legal ob-ligation of the trustee.24

PAGE 24

QUARTERLY

HELP YOUR BUSINESS CLIENTS TAKE CARE OF BUSINESS.

Business Docx™ has the communication tools you need.

Small business clients need your help keeping track of their legal and tax priorities.

Business Docx™, from WealthCounsel, is the drafting system estate planners and

small business attorneys turn to for not only superior document drafting, but also a

comprehensive suite of client communication tools and guidance. Because the more

connected you are with your clients, the more engaged they are and the deeper your

relationship becomes. And that’s how smart practices grow.

Let our practice consultants give you a personal demonstration of what makes Business

Docx™ so powerful. Contact WealthCounsel today:

CALL (888) 659-4069 #819

EMAIL [email protected]

OR VISIT wealthcounsel.com

“ Business Docx™ does such a great job of educating that I can tell a client: here’s your document, here’s how it works, here’s why we did it this way and here’s why you’re going to enjoy working with me.”

- SARAH OSTAHOWSKI, JD

MEMBER SINCE 2011

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 25

As discussed above, if a beneficiary affirmatively consents to a decanting or requests a decanting in a manner that shifts the beneficiary’s interest in the trust to another beneficiary, the beneficiary may be considered to have made a taxable transfer. To avoid this result, decantings should be carried out by inde-pendent trustees without affirmative consent by the beneficiaries.

Many other questions about the tax implications of decanting remain, but unfortunately the IRS’s lips are sealed. After a few years of accepting comments on the tax consequences of trust modification action, the IRS imposed a moratorium on new decanting PLRs25 and appears to continue studying the issue internally. Until that bright day when Treasury fully colors in the lines for us, we should counsel trustees carefully and err on the conservative side when decanting unfavor-able trusts.

ENDNOTES

1 The American Taxpayer Relief Act of 2012, Pub. L. 112-240

2 Joint Committee on Taxation, “History, Present Law, and Analysis of the Federal Wealth Transfer Tax System,” March 16, 2015. Available online at https://www.jct.gov/publications.html?func=startdown&id=4744

3 An “ascertainable standard” trust is one that permits or directs the trustee to pay income and/or principal to the beneficiary for the beneficiary’s health, education, maintenance, or support. When a power is fixed or ascertainable, possession of that power by an interested trustee does not constitute a general power of appoint-ment for transfer tax purposes. (IRC §§2041(b)(1)(A), 2514(c)(1).) Critics of this drafting approach believe that when the beneficiary’s interest is ascertainable, it gives rise to a property interest to which a creditor may attach a claim. Vesting purely discretionary distri-bution power (over both income and principal) in an independent trustee is often far more advantageous from an asset protection perspective.

4 The Regs explain that the term “related or subordinate party” means a nonadverse party – that is, a party who does not have a personal interest in the trust – who is the grantor’s spouse (if liv-ing with the grantor), the grantor’s parent, descendant, sibling, or employee, or the employee of a corporation in which the grantor has substantial voting control or where the grantor is an executive. If a party is related or subordinate to the grantor as defined by the Regs, then the grantor must prove by a preponderance of the evi-dence that the individual is not subservient. Regs. §1.672(c)-1

5 This strategy, pioneered under PLR 200537044, is often inart-fully described as a “toggle” provision. More appropriately it’s a one-time switch – a detonator of sorts. Once converted, the trust cannot be converted back to a conduit trust. Further, the protector must exercise the power to convert a conduit trust to an accumula-tion trust within 9 months of the decedent’s death: the deadline for

identifying the beneficiaries under a qualified plan as required by Reg. §1.401(a)(9)-4, Q&A 5(b)(3). Attorneys must also bear in mind that PLRs cannot be relied on as precedent by any party other than the party who obtained it in their case. IRC §6110(k)(3).

6 For more information on this strategy please see LISI Asset Protection Newsletter #200, “Steve Oshins & the Hybrid Domestic Asset Protection Trust,” available online at http://www.oshins.com/images/Hybrid_DAPT.pdf,

7 Trust modification options fall into a spectrum ranging from ref-ormation (on the low end of flexibility) to modification, equitable deviation, decanting, and modification by protector. This article fo-cuses on the decanting option as it provides both a high level of flexibility and a high degree of legal acceptance among the states. At the time of this writing at least 33 states authorize trust modi-fication by beneficiaries and others without court involvement; 23 states have statutes authorizing decanting. A few other states allow decanting under the common law.

8 Remember that the trust may have been irrevocable from incep-tion, or it may have become irrevocable after the settlor died. A very common trust for which decanting might make sense would be the bypass or credit shelter trust established after the death of a settlor. When that bypass is no longer needed to shelter assets from estate tax inclusion, decanting may be a good option to trigger “defects” that will cause inclusion and a §1014 basis adjustment when the surviving spouse or other beneficiary dies.

9 See Internal Revenue Service Notice 2011-101

10 Regs. §1.671-2(e)(5)

11 Id.

12 This is the default approach under the Wealth Docx decanting option.

13 See PLRs 200607015 and 200736002

14 See IRC §§652, 663

15 See Regs. §1.643(c)-1

16 See Blattmachr, Horn, & Zeydel: Tax Effects of Decanting – Ob-taining and Preserving the Benefits, Journal of Taxation (WG&L) Vol. 111, No. 5, Nov. 2009 at 293; Regs. §1.643(a)-3(e) exs. 8-9

17 See IRC §1001

18 Cottage Savings Ass’n v. Commissioner, 499 U.S. 554 (1991)

19 Id. at 567

20 See, e.g., PLR 200736002 (division of trust on pro rata basis did not trigger gain or loss) and PLR 201516020 (division and modifi-cation of trust will not trigger realization of income, gain, or loss). For further reading on this topic, please see Jason Kleinman, Trust Decanting: A Sale Without Gain Realization, ABA Real Property, Probate, & Trust Journal Vol. 49, No. 3 (Winter 2015) 453, 455

21 See Rev. Rul. 81-264, 1981-2 CB 185

22 See PLR 9419007

23 Treas. Reg. §25.2511-1(g)(2)

24 Wealth Docx contains default safeguards to prevent this from occurring.

25 See Rev. Proc. 2015-3 §5.01 (14), (20), (21).

PAGE 26

QUARTERLY

TODAY’S INVESTMENTS IN

PAY DIVIDENDS IN THE FUTURE

KATELYN GRIFFIN, DIRECTOR, WEALTHCOUNSEL MEMBER SERVICES

Today’s rapid rate of technological advance and shifting expectations leaves the world of customer service in constant flux. Instantaneous information has become both an expectation and the norm thanks in large part to smart phones and ubiquitous mobile devices. Virtually everything we need to know and want to share can be accomplished with the click of a button.

If you think this change doesn’t affect your law business, think again. Your clients are comparing the service they receive from you and your staff with every other customer service interaction they have. If you aren’t measuring up, chances are their loyalty is waning. Follow me on a journey to learn how you can benefit from customer loyalty and how to improve your customer service experience.

VOLUME 9 NUMBER 3 / Q3 2015

PAGE 27

LOYALTY MATTERS

I often speak with solo and small firm practitioners who question their fees. Am I losing clients because of the price tag? Am I undervaluing my experience and product? Does this sound like you? While there is an obvious correlation between price and profit, con-sider for a moment that price isn’t where your com-petitive advantage exists. Perhaps your law business could be easily (and inexpensively) adapted to com-pete in another profitable area: customer loyalty.

Loyal customers aren’t focused on price alone. They understand the holistic value of what they’re receiv-ing – product and service. Loyal customers believe this value outweighs the monetary obligation.

A loyal customer is confident an error is the excep-tion, not the rule, because they have had multiple ex-periences with your practice. These customers are far more likely to overlook the “dropped ball.”

Loyal customers’ needs are satisfied. In other words, they aren’t likely to survey your competitors. Think of it like this: very few people search for take-out menus after indulging in Thanksgiving dinner. Your goal is to provide an experience worth indulging in… repeatedly.

Loyal customers are also more likely to refer you to their network. That means more clients for you and more opportunities to continue the customer loyalty (revenue generating) cycle.

Now that you understand the benefits, let’s discuss how to create a culture of loyalty.

LOYALTY TECHNIQUES

Focus on the experience, not the product.

Greeting clients with a warm welcome is common sense to most. Something that I hear many service providers overlook is the customer’s exit. When a cli-ent is leaving your office, what is the lasting impres-sion they will take with them throughout their day? Work to craft an equally personable and thorough exit experience. Never make a client feel like you or your staff’s attention has already shifted to the next person in line before they are even out the door. If there are action items or there is another step, be sure the client is fully prepared for what lies ahead. Answer any questions they ask. If possible, address questions

they might not realize they need to ask. Remember, they are not just looking to you for documents. They are looking to you for counseling and guidance.

Manage your client’s expectations.

If you have learned something new that will change the scope of your customer’s agreement, update them. Ensure they understand what has changed, any related implications, and why. Don’t save news that will affect their future or pocketbook for signing meetings or invoices. While it can be uncomfortable to share bad news, avoiding this pitfall will help you earn your customer’s trust.

Tailor communication to your niche audience and content.

High net worth families have different needs from a young entrepreneur or single mom. Baby Boomers have different preferences from a Gen X client. Deter-mine what communication channels are most conve-nient and effective for your niche, and adjust accord-ingly. If being accessible over the phone will provide a more valuable experience for your customers, work to create this culture. This may mean locating outside services, revising job responsibilities, documenting processes or providing staff incentives.

Alternatively, if email is a preferred method of commu-nication, dedicate time to provide timely responses. Consider what you are communicating. Some news is best delivered in person. Other updates should be shared quickly through a phone call or email. Set com-munication expectations in your first meeting. Many firms include details and contact direction in their en-gagement letter, too.