Embed Size (px)

Citation preview

Where is the end of the EU-rope

Richard Baldwin Graduate Institute, Geneva and University of Oxford

11 May 2013, Innsbruck

Plan of talk

• Misthinking globalisation

• What it means for future of Europe

– Membership

– Depth

Misthinking globalisation

• Conventional:

– Autarky to free trade, slowly.

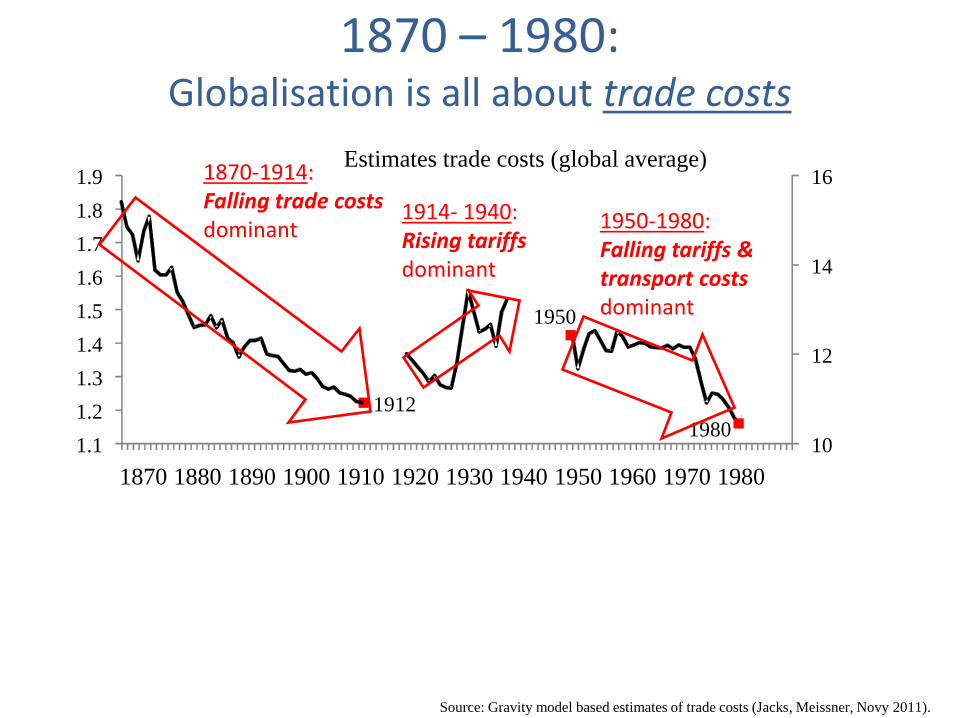

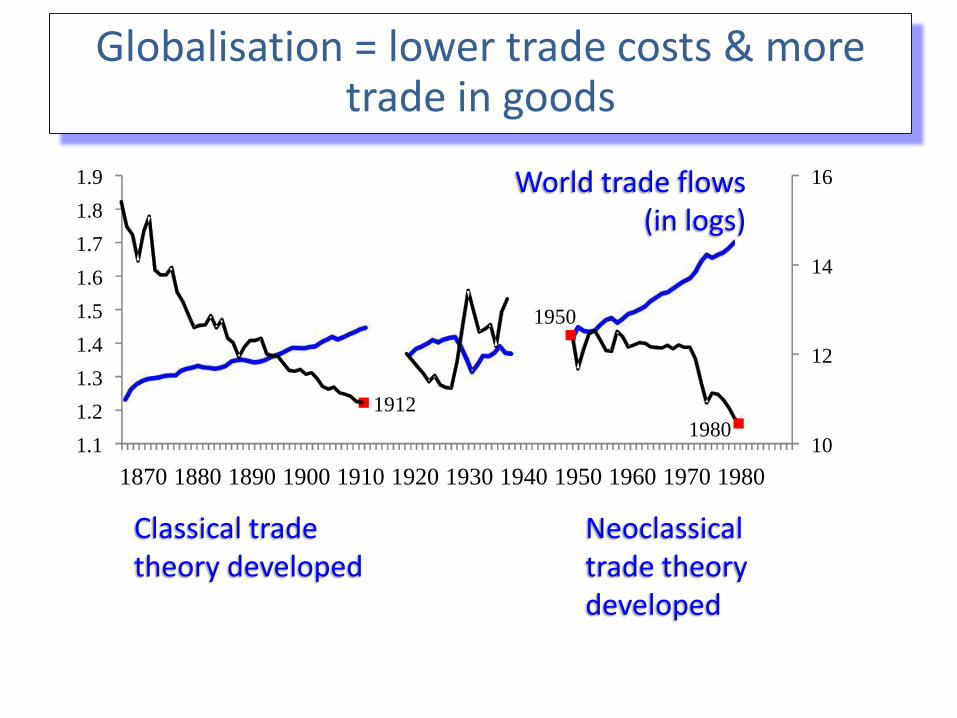

1870 – 1980: Globalisation is all about trade costs

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980

16

1.1 10

12

14

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

1912

1870-1914: Falling trade costs dominant

1914- 1940: Rising tariffs dominant

1950

1980

1950-1980: Falling tariffs & transport costs dominant

Source: Gravity model based estimates of trade costs (Jacks, Meissner, Novy 2011).

Estimates trade costs (global average)

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980

16

1.1 10

12

14

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

1912

1950

1980

World trade flows (in logs)

Classical trade theory developed

Neoclassical trade theory developed

Add trade flows Globalisation = lower trade costs & more trade in goods

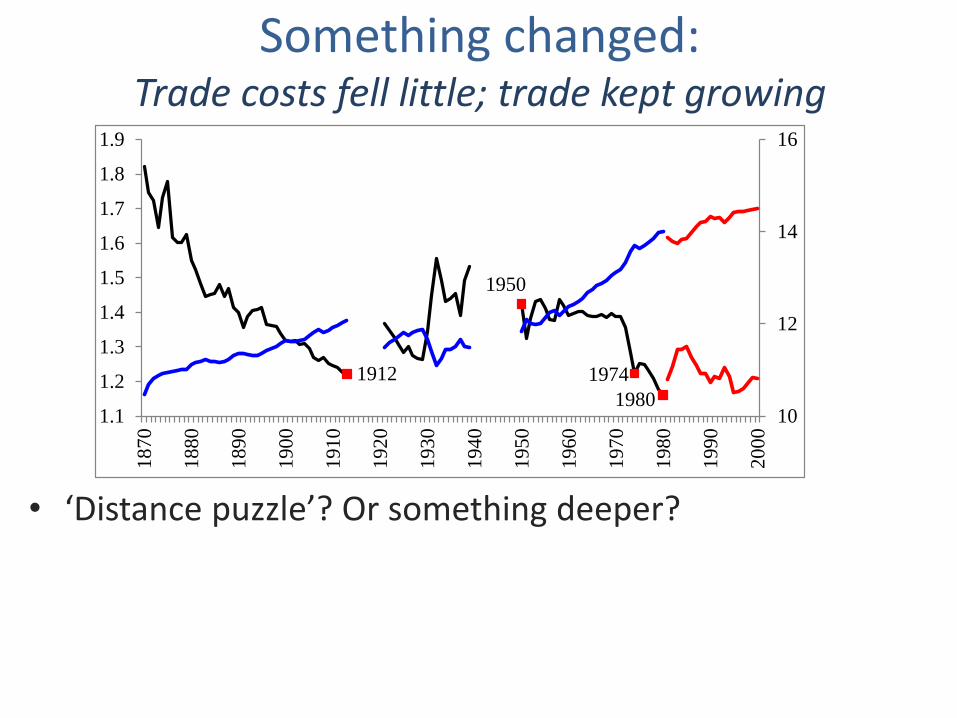

Something changed: Trade costs fell little; trade kept growing

• ‘Distance puzzle’? Or something deeper?

1912

1950

1974

198010

12

14

16

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.91

87

0

1880

18

90

19

00

19

10

19

20

19

30

19

40

1950

19

60

19

70

19

80

19

90

20

00

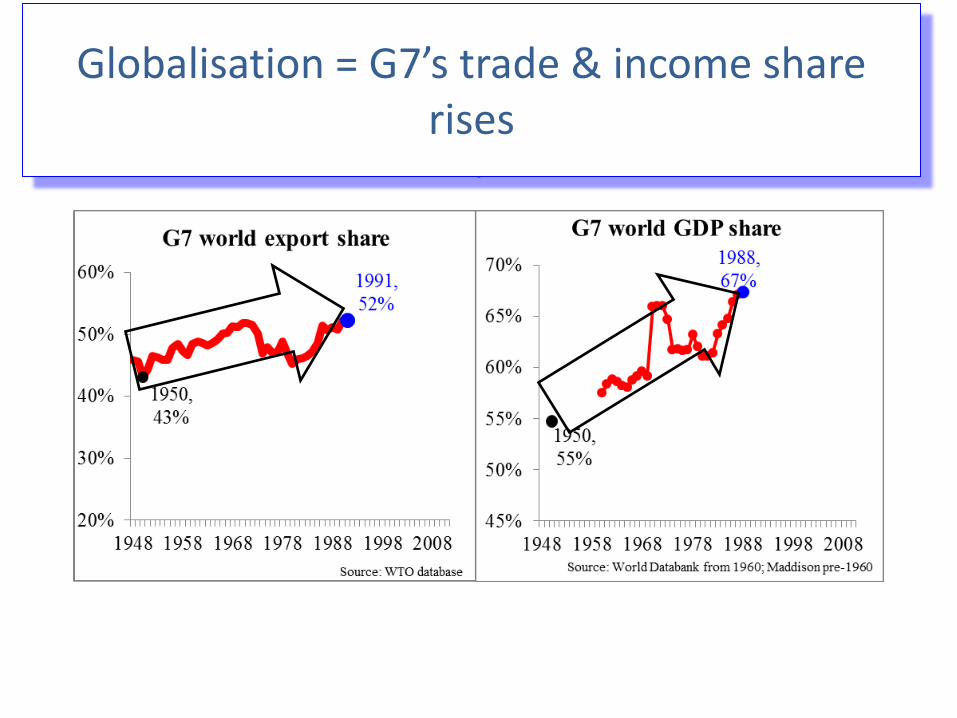

Big picture impact, 1870-1980s

• G7’s share of world exports & income

Globalisation = G7’s trade & income share rises

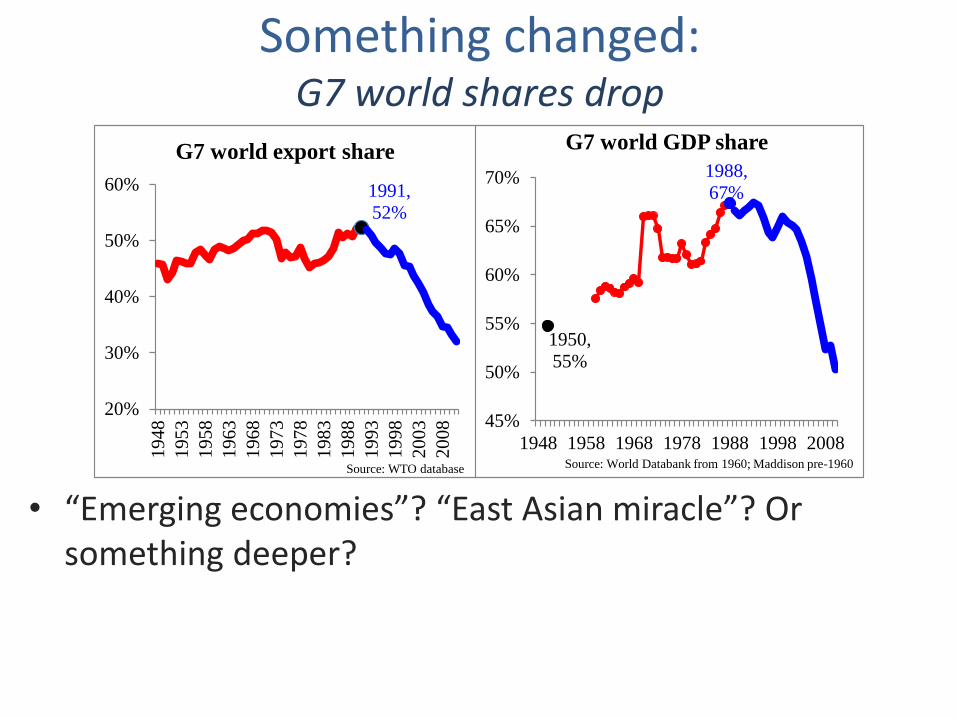

Something changed: G7 world shares drop

• “Emerging economies”? “East Asian miracle”? Or something deeper?

1991,

52%

20%

30%

40%

50%

60%

19

48

19

53

1958

19

63

19

68

19

73

19

78

19

83

19

88

19

93

19

98

20

03

20

08

Source: WTO database

G7 world export share

1950,

55%

1988,

67%

45%

50%

55%

60%

65%

70%

1948 1958 1968 1978 1988 1998 2008Source: World Databank from 1960; Maddison pre-1960

G7 world GDP share

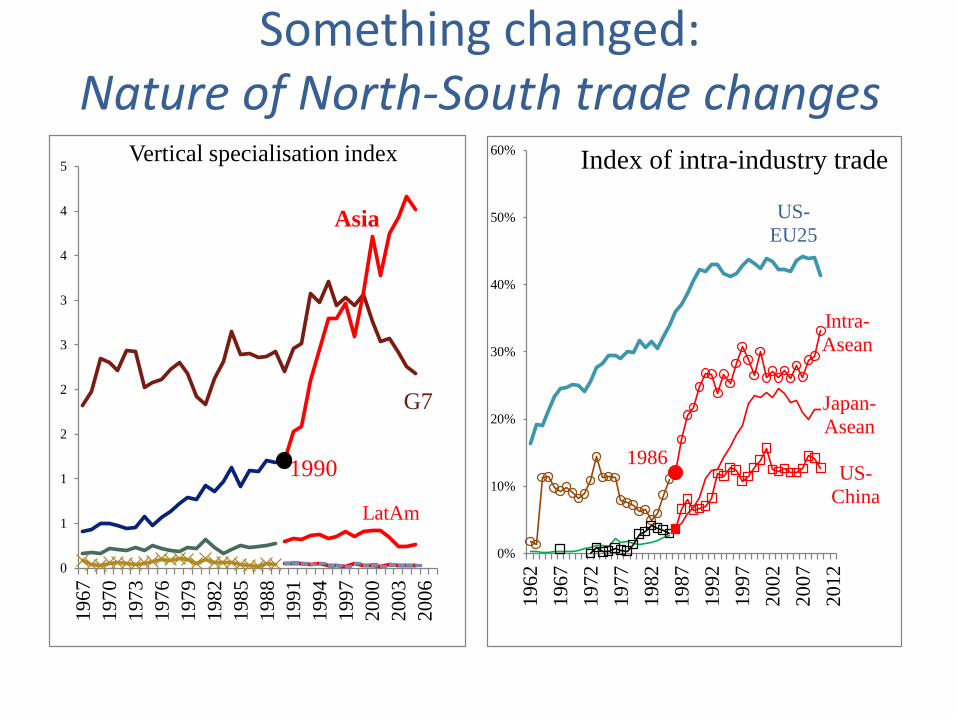

Something changed: Nature of North-South trade changes

US-

EU25

1986

Intra-

Asean

Japan-

Asean

US-

China

0%

10%

20%

30%

40%

50%

60%

1962

1967

1972

1977

1982

1987

1992

1997

2002

2007

2012

Index of intra-industry trade

G7

1990

Asia

LatAm

0

1

1

2

2

3

3

4

4

5

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

Vertical specialisation index

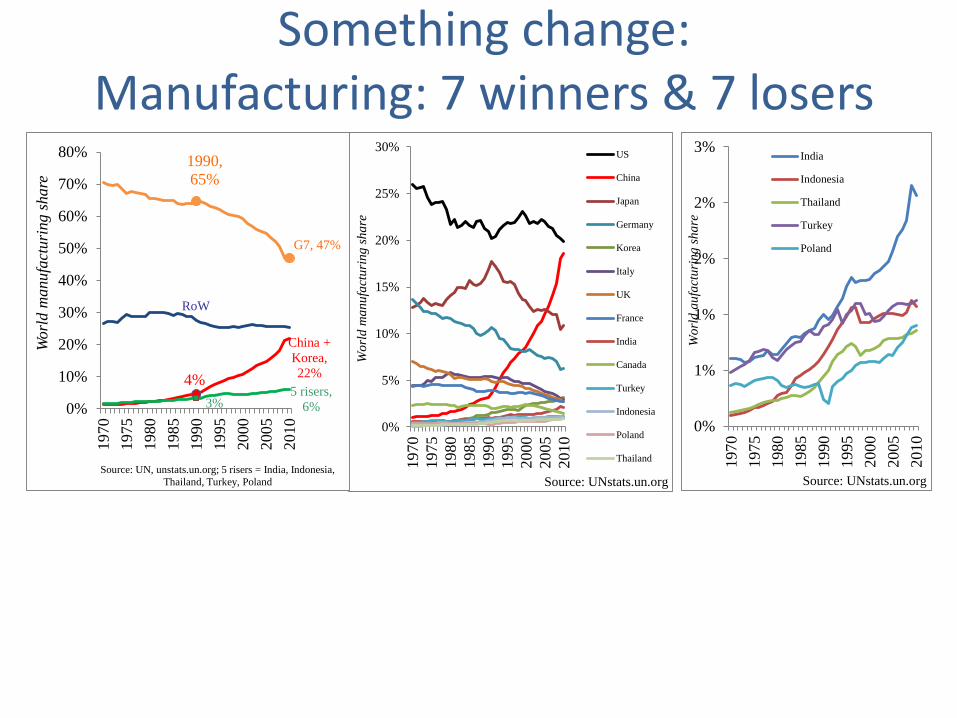

Something change: Manufacturing: 7 winners & 7 losers

0%

1%

1%

2%

2%

3%

1970

1975

1980

1985

1990

1995

2000

2005

2010

Wo

rld

au

fact

uri

ng

sh

are

Source: UNstats.un.org

India

Indonesia

Thailand

Turkey

Poland

0%

5%

10%

15%

20%

25%

30%

1970

1975

1980

1985

1990

1995

2000

2005

2010

Wo

rld

ma

nu

fact

uri

ng

sh

are

Source: UNstats.un.org

US

China

Japan

Germany

Korea

Italy

UK

France

India

Canada

Turkey

Indonesia

Poland

Thailand

1990,

65%

G7, 47%

4%

China +

Korea,

22%

3%5 risers,

6%

RoW

0%

10%

20%

30%

40%

50%

60%

70%

80%

1970

1975

1980

1985

1990

1995

2000

2005

2010

Worl

d m

anufa

cturi

ng s

hare

Source: UN, unstats.un.org; 5 risers = India, Indonesia,

Thailand, Turkey, Poland

Something changed: Developing nations unilateral cut tariffs

• Policy makers final listen to trade economists?

Or something deeper?

AR

BO

BR

CH

COEC

MX

PE

PE

UY

VE

0

10

20

30

40

50

60

70

80

90

19

85

19

87

19

89

19

91

1993

19

95

19

97

19

99

20

01

20

03

20

05

Average MFN applied tariff

(%)ARBOBRCHCOECMXPEPYUYVE

South

Asia

Sub-

Saharan

Africa

Middle

East &

North

Africa

East

Asia &

Pacific0

5

10

15

20

25

30

35

40

45

50

1988

19

90

19

92

19

94

19

96

1998

20

00

20

02

20

04

20

06

2008

Developing nation applied tariffs

1986 1988

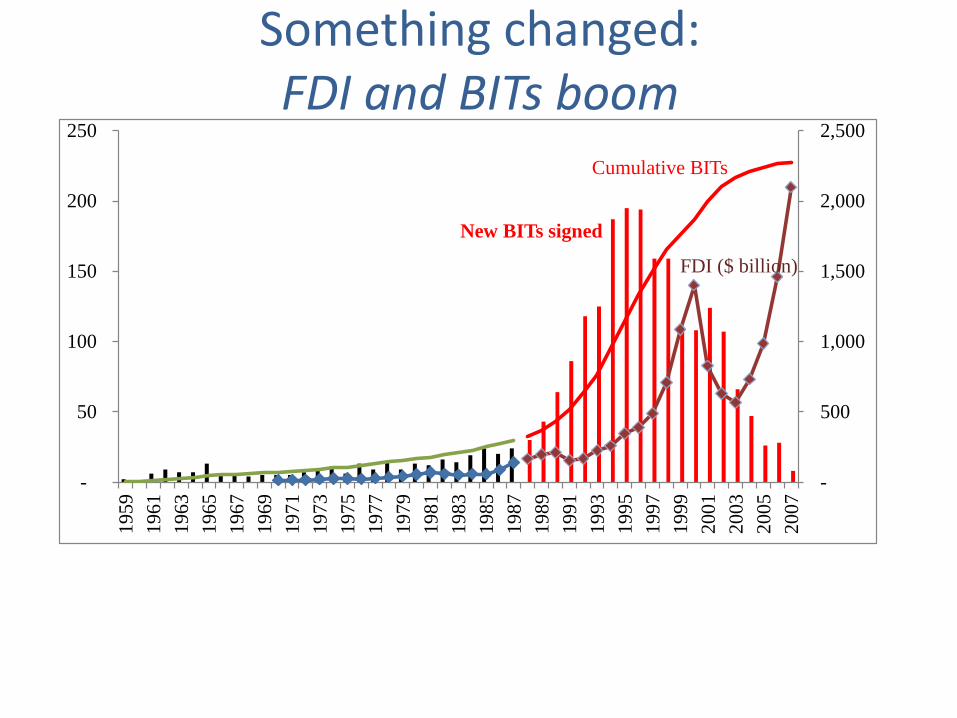

Something changed: FDI and BITs boom

New BITs signed

Cumulative BITs

FDI ($ billion)

-

500

1,000

1,500

2,000

2,500

-

50

100

150

200

2501959

19

61

19

63

19

65

19

67

19

69

19

71

19

73

19

75

19

77

19

79

1981

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

2001

20

03

20

05

20

07

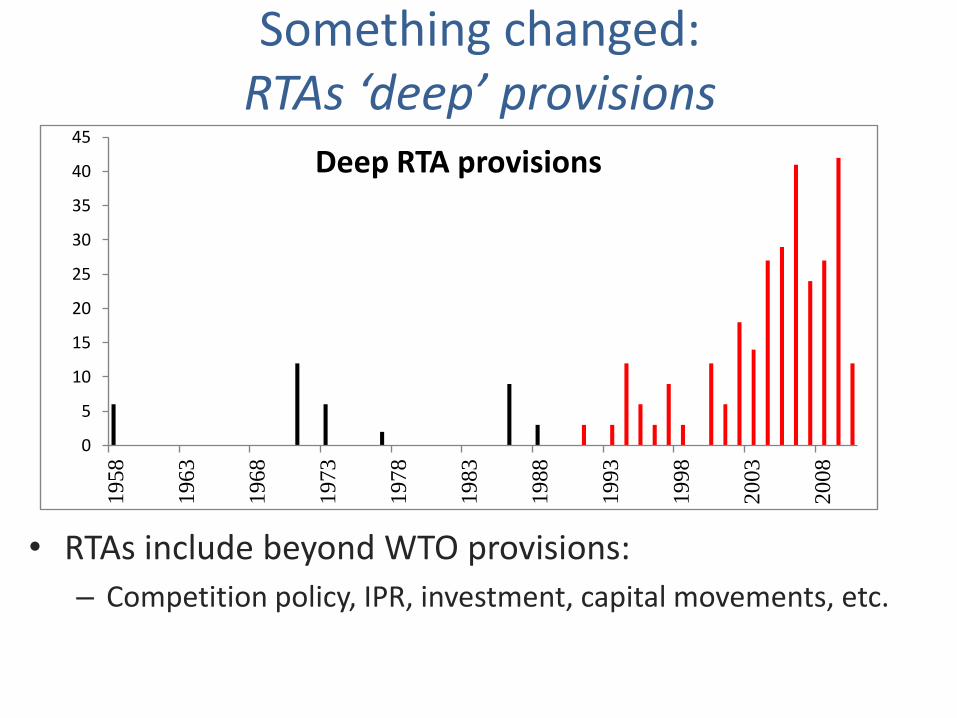

Something changed: RTAs ‘deep’ provisions

• RTAs include beyond WTO provisions:

– Competition policy, IPR, investment, capital movements, etc.

0

5

10

15

20

25

30

35

40

451958

1963

1968

1973

1978

1983

1988

1993

1998

2003

2008

Deep RTA provisions

What changed?

Stage B Stage A

Stage C

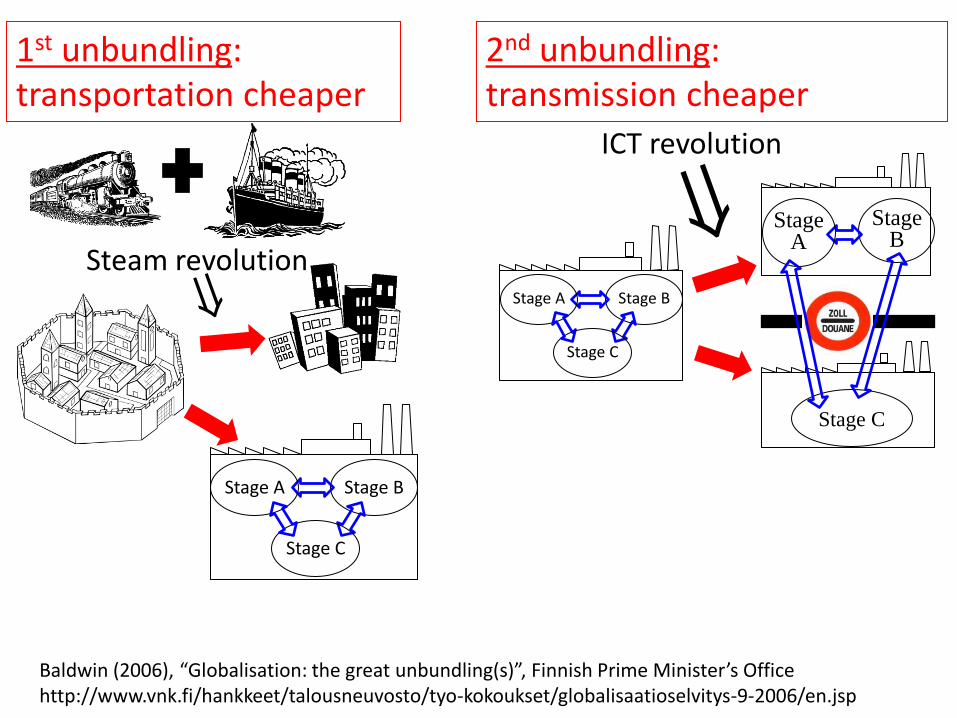

Steam revolution

1st unbundling: transportation cheaper

Baldwin (2006), “Globalisation: the great unbundling(s)”, Finnish Prime Minister’s Office http://www.vnk.fi/hankkeet/talousneuvosto/tyo-kokoukset/globalisaatioselvitys-9-2006/en.jsp

ICT revolution

2nd unbundling: transmission cheaper

Stage B

Stage A

Stage C

Stage B Stage A

Stage C

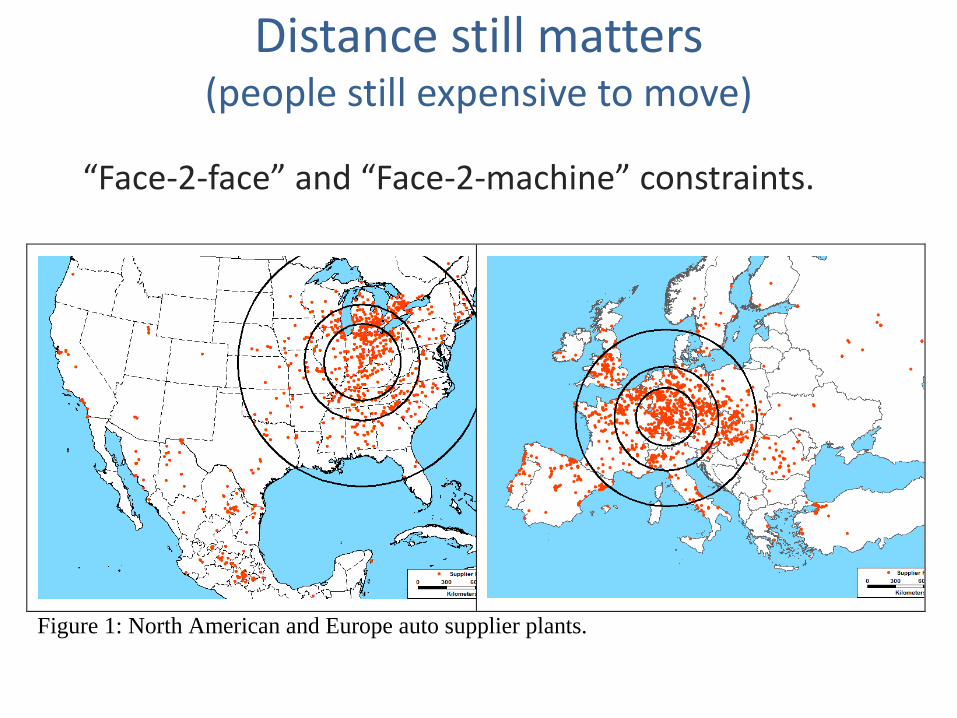

Distance still matters (people still expensive to move)

“Face-2-face” and “Face-2-machine” constraints.

Figure 1: North American and Europe auto supplier plants.

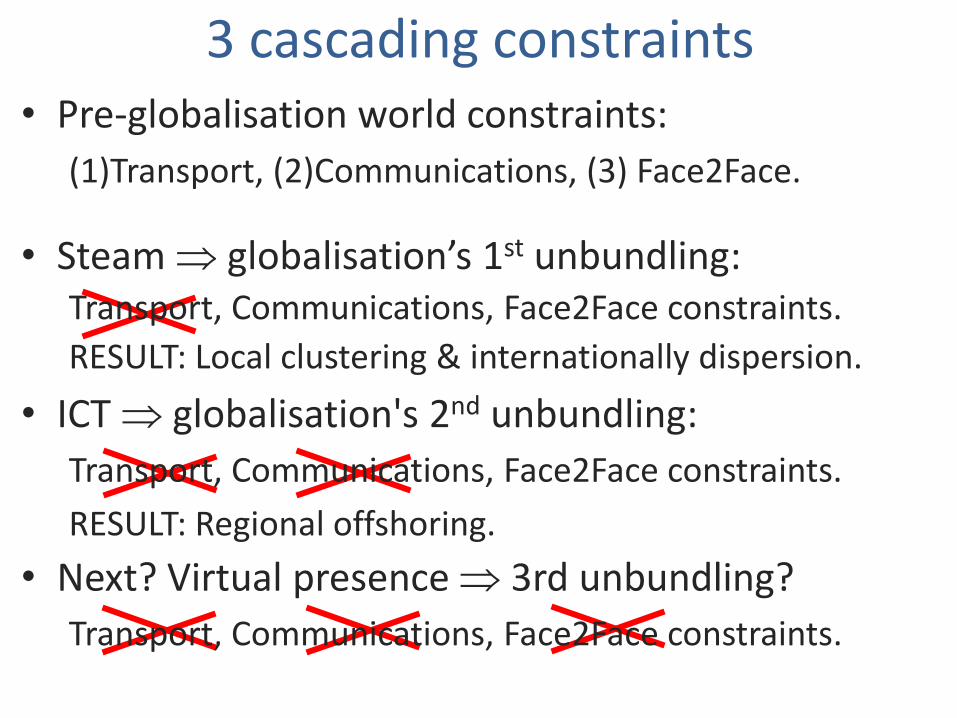

3 cascading constraints • Pre-globalisation world constraints:

(1)Transport, (2)Communications, (3) Face2Face.

• Next? Virtual presence 3rd unbundling?

Transport, Communications, Face2Face constraints.

• Steam globalisation’s 1st unbundling: Transport, Communications, Face2Face constraints.

RESULT: Local clustering & internationally dispersion.

• ICT globalisation's 2nd unbundling:

Transport, Communications, Face2Face constraints.

RESULT: Regional offshoring.

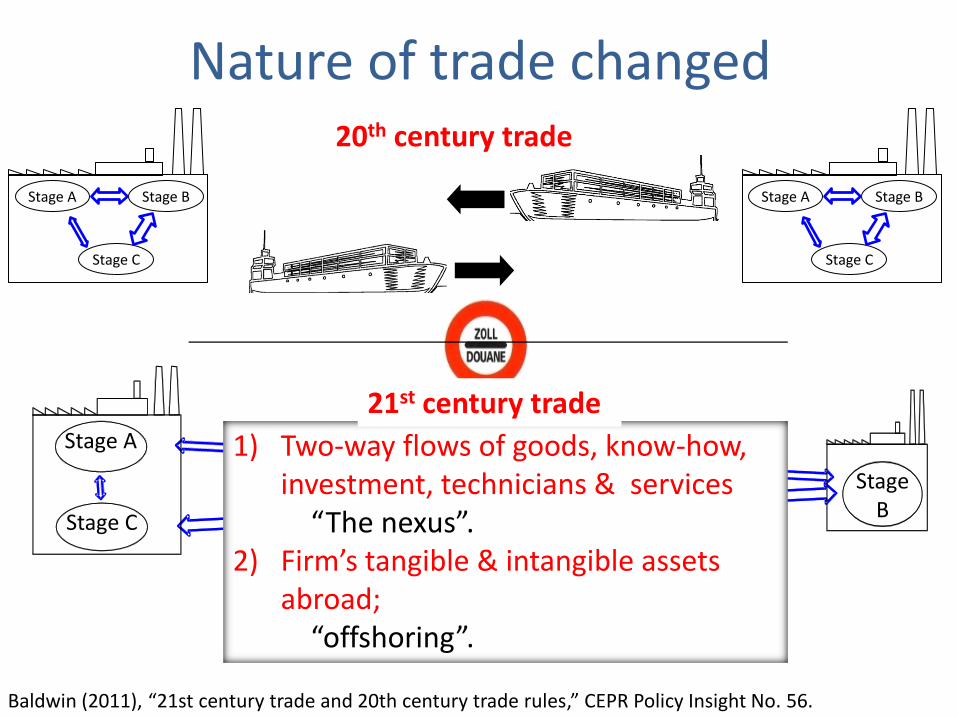

Nature of trade changed 20th century trade

Baldwin (2011), “21st century trade and 20th century trade rules,” CEPR Policy Insight No. 56.

Stage B

Stage A

Stage C

1) Two-way flows of goods, know-how, investment, technicians & services

“The nexus”. 2) Firm’s tangible & intangible assets

abroad; “offshoring”.

21st century trade

Stage B Stage A

Stage C

Stage B Stage A

Stage C

Elephant = Know-how easier to move.

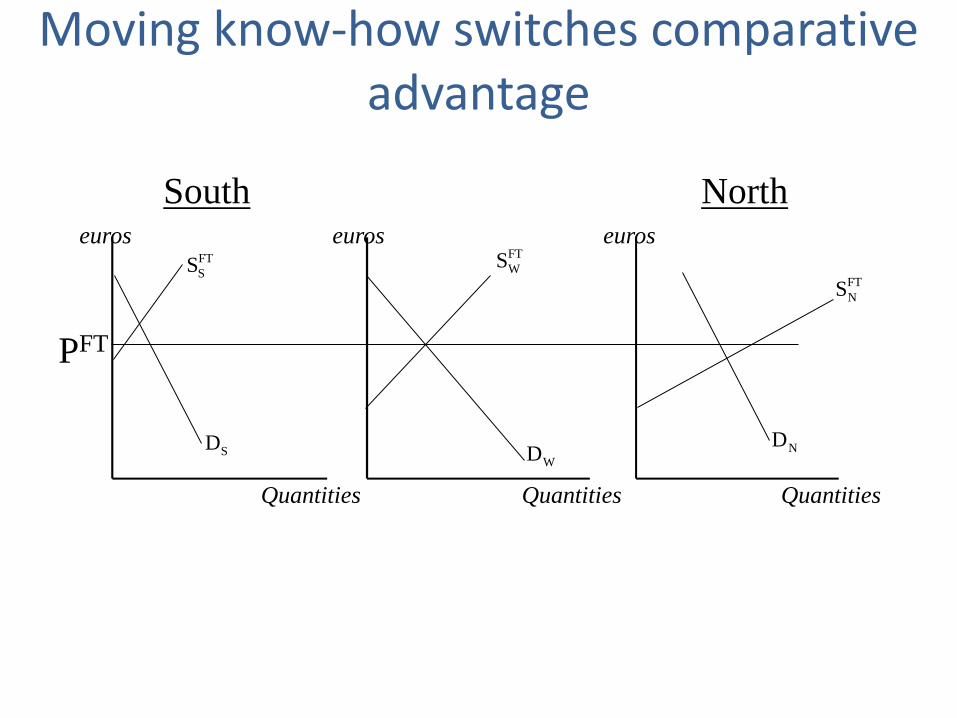

Basic economic difference

• 1st unbundling globalisation:

– Better exploit comparative advantage by exporting more.

– Trade driven by incipient cost differences.

• 2nd unbundling globalisation:

– Better exploit firm-specific know-how by moving the sources of comparative advantage internationally.

• North high-tech + South low-wages: Labour to tech, or tech to labour

– Trade driven by know-how mobility.

FT

WS

WD

Quantities

euros

FT

NS

Quantities

euros FT

SS

PFT

Quantities

euros

NDSD

Moving know-how switches comparative advantage

North South

FT

WS

WD

Quantities

euros

FT

NS

Quantities

euros FT

SS

PFT

Quantities

euros

NDSD

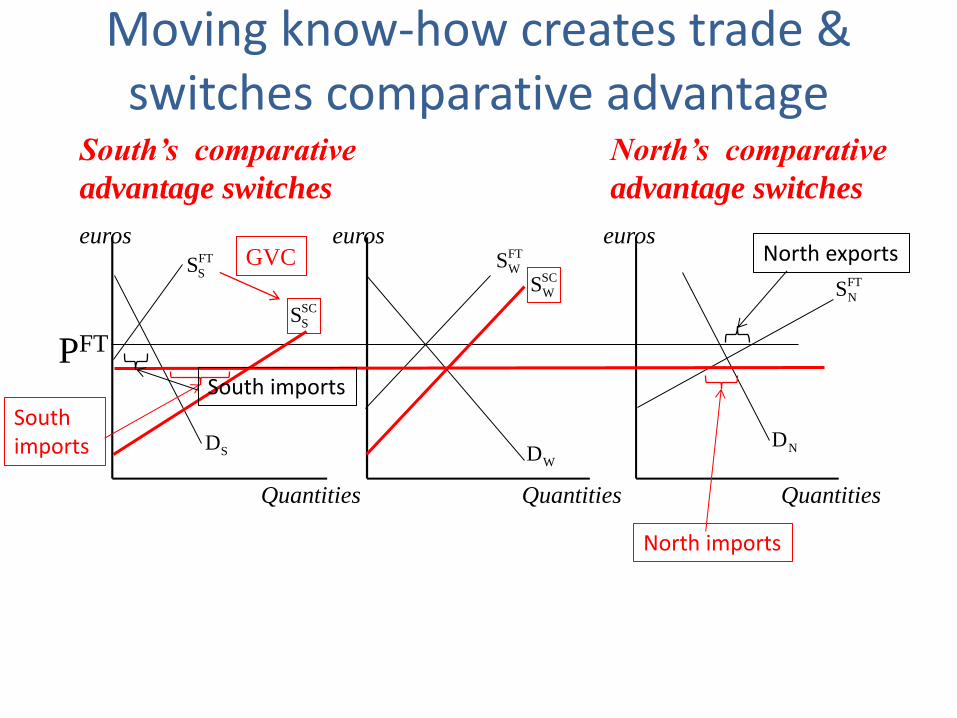

Moving know-how creates trade & switches comparative advantage

North South

South’s comparative

advantage switches

North’s comparative

advantage switches

SC

WSSC

SS

GVC

South imports

North imports

North exports

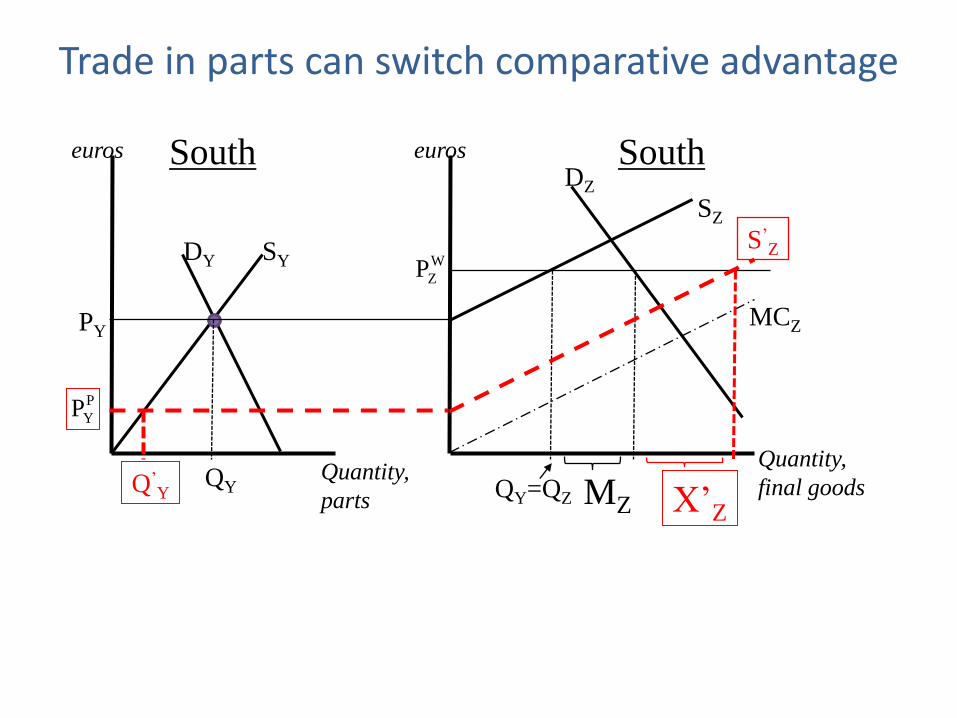

South imports

Quantity,

parts

DY

SZ

DZ

euros euros

MCZ

Quantity,

final goods QY=QZ

SY W

ZP

PY

MZ

Trade in parts can switch comparative advantage

QY

South South

S’Z

P

YP

X’Z

Q’Y

GVC revolution gets data

• Gary Gereffi working on GVC for years.

– http://www.globalvaluechains.org/concepts.html

– Theory in 1960s, 1970s, 1980s, 1990s, 2000s.

• New data changes everything:

– WIOD.org dataset

• Timmer et al. papers

– TiVA dataset

– GTAP dataset work

• Johnson & Noguera paper

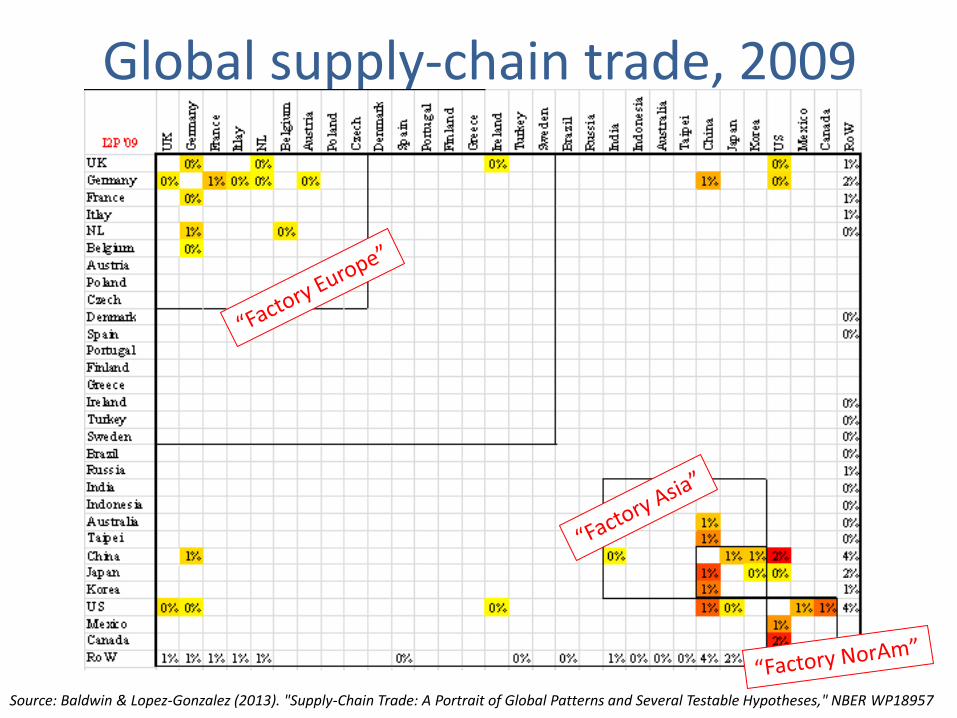

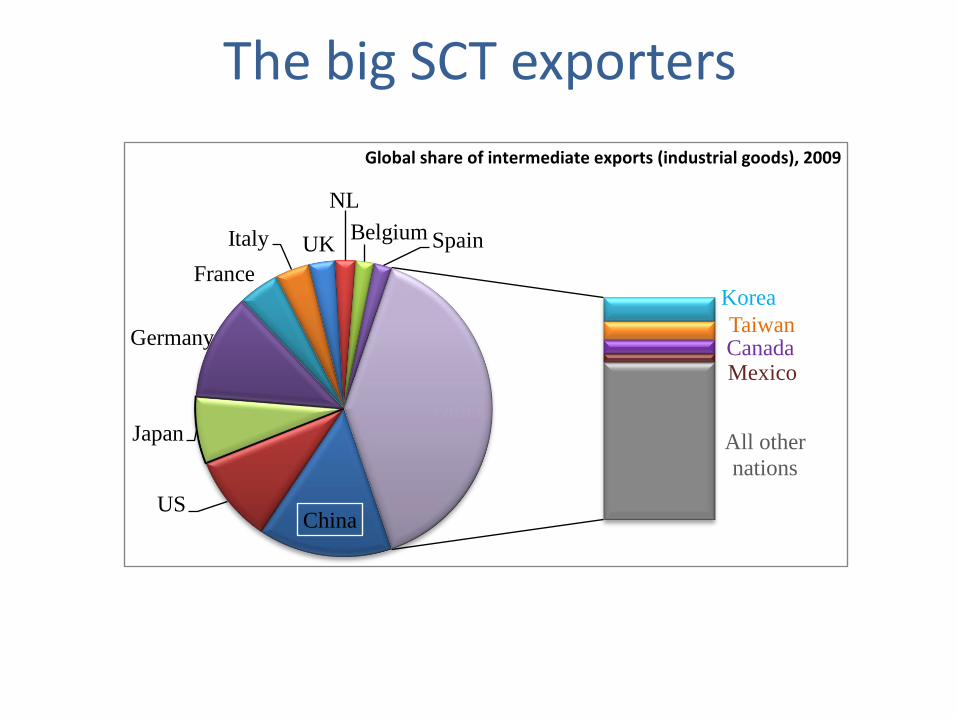

Global supply-chain trade, 2009

Source: Baldwin & Lopez-Gonzalez (2013). "Supply-Chain Trade: A Portrait of Global Patterns and Several Testable Hypotheses," NBER WP18957

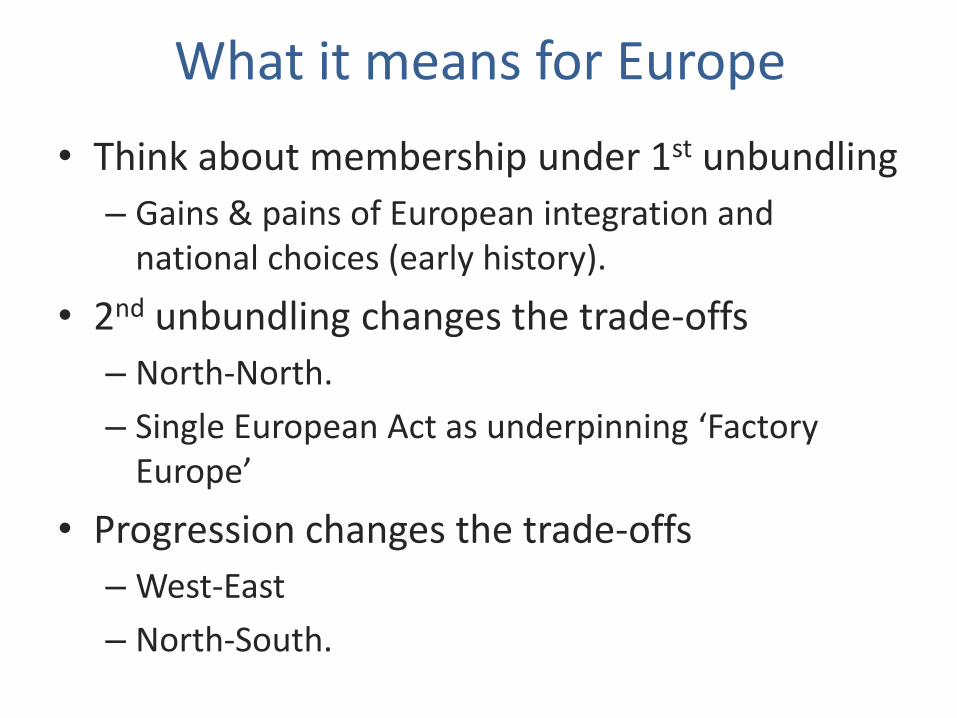

What it means for Europe

• Think about membership under 1st unbundling

– Gains & pains of European integration and national choices (early history).

• 2nd unbundling changes the trade-offs

– North-North.

– Single European Act as underpinning ‘Factory Europe’

• Progression changes the trade-offs

– West-East

– North-South.

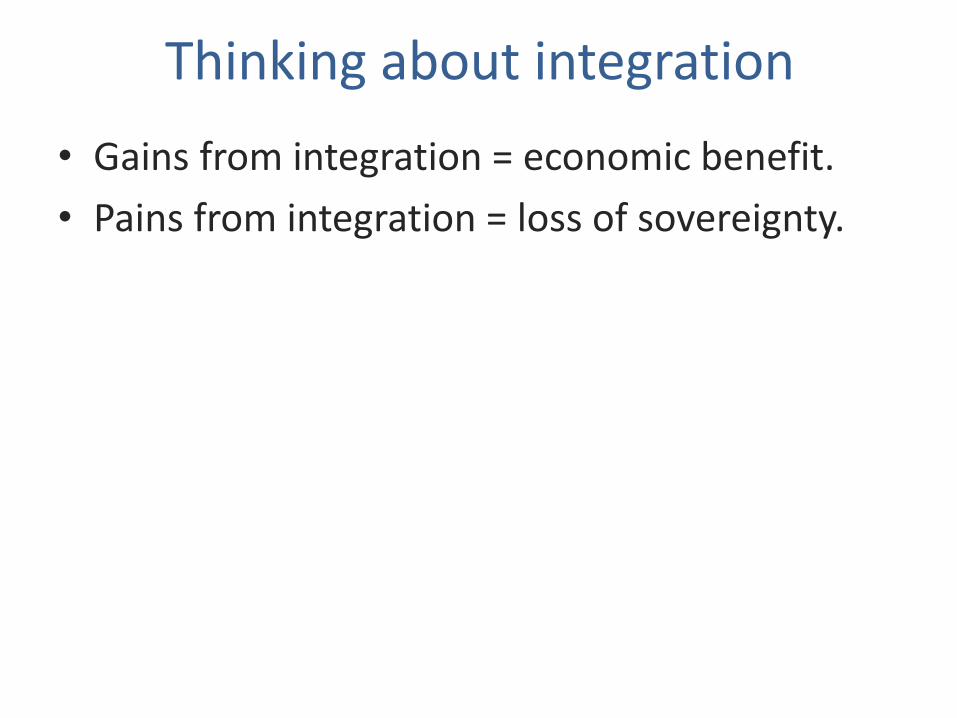

Thinking about integration

• Gains from integration = economic benefit.

• Pains from integration = loss of sovereignty.

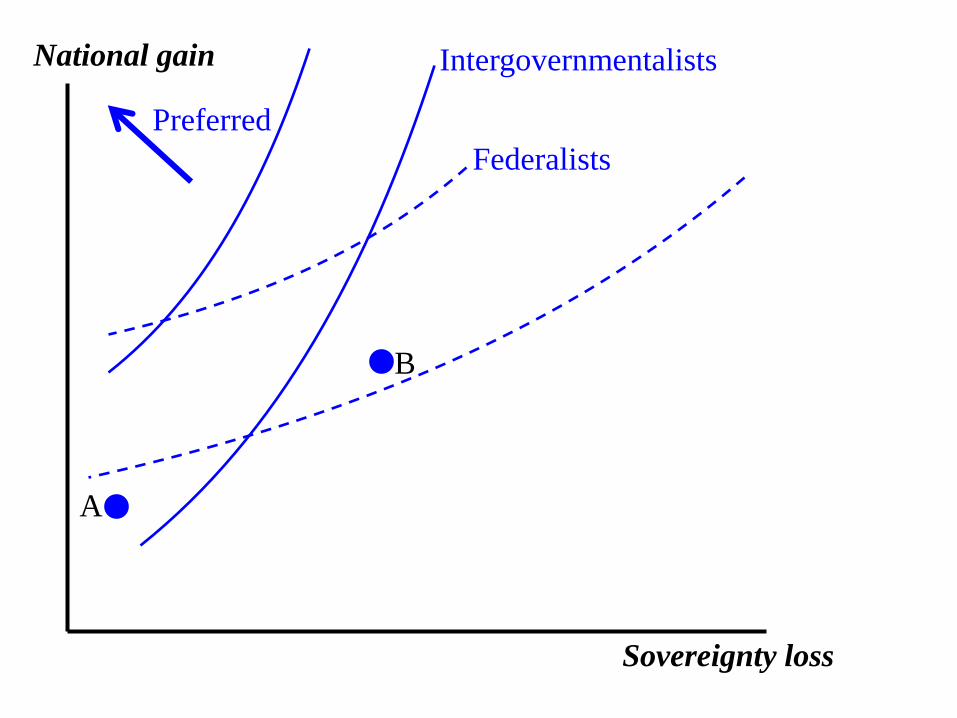

National gain

Sovereignty loss

A

B

Preferred

Federalists

Intergovernmentalists

National gain

Sovereignty loss

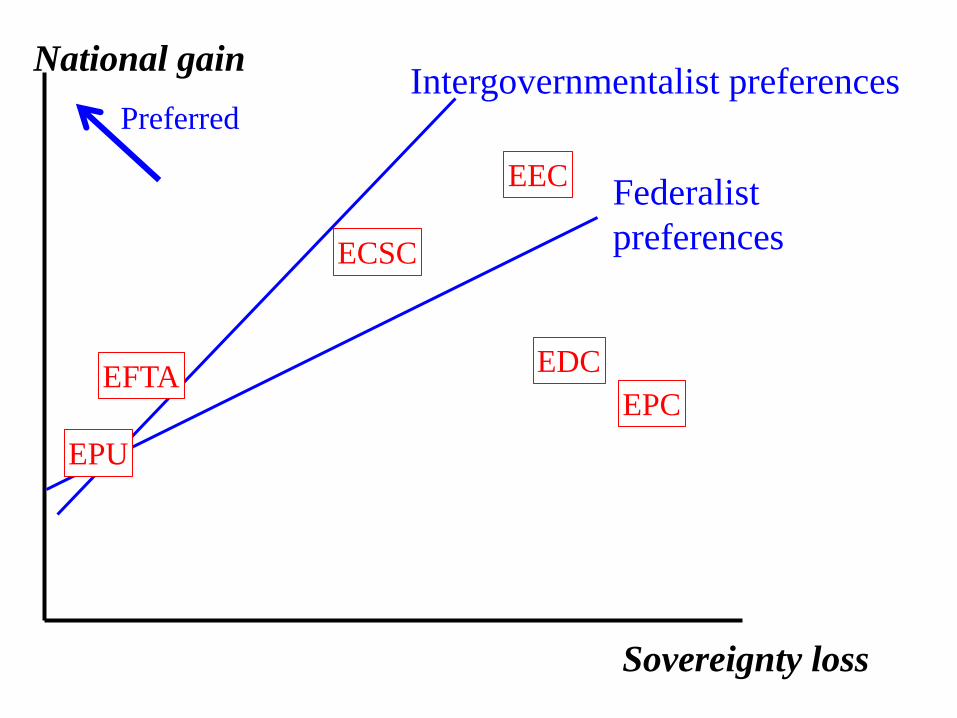

Intergovernmentalist preferences

Federalist

preferences

EPU

EDC

ECSC

EPC

EEC

EFTA

Preferred

National gain

Sovereignty loss

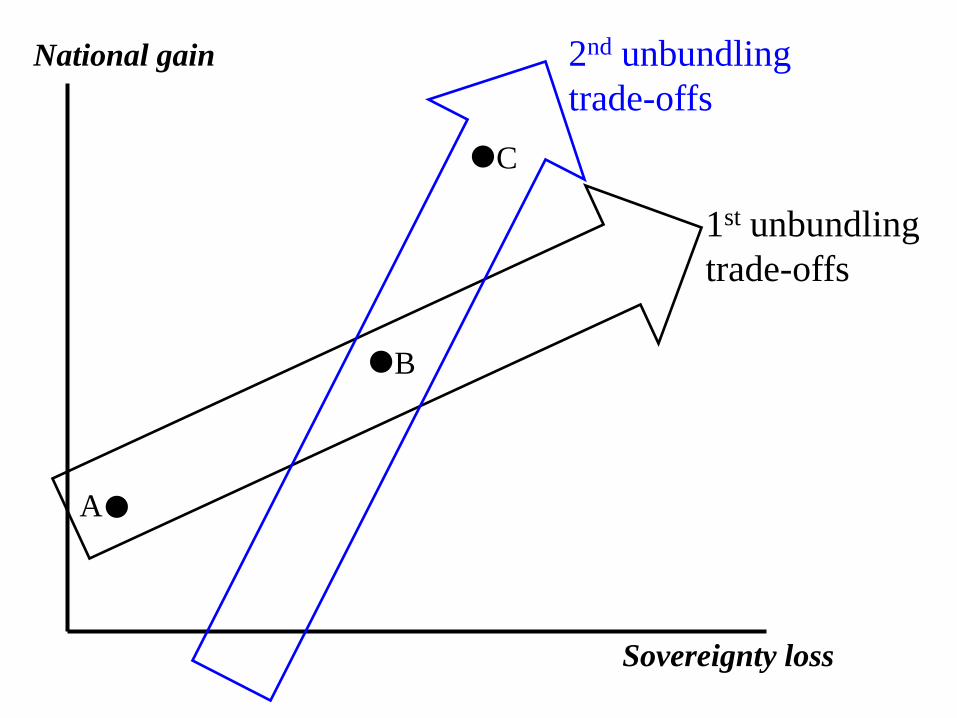

A

1st unbundling

trade-offs

B

2nd unbundling

trade-offs

C

National gain

Sovereignty loss

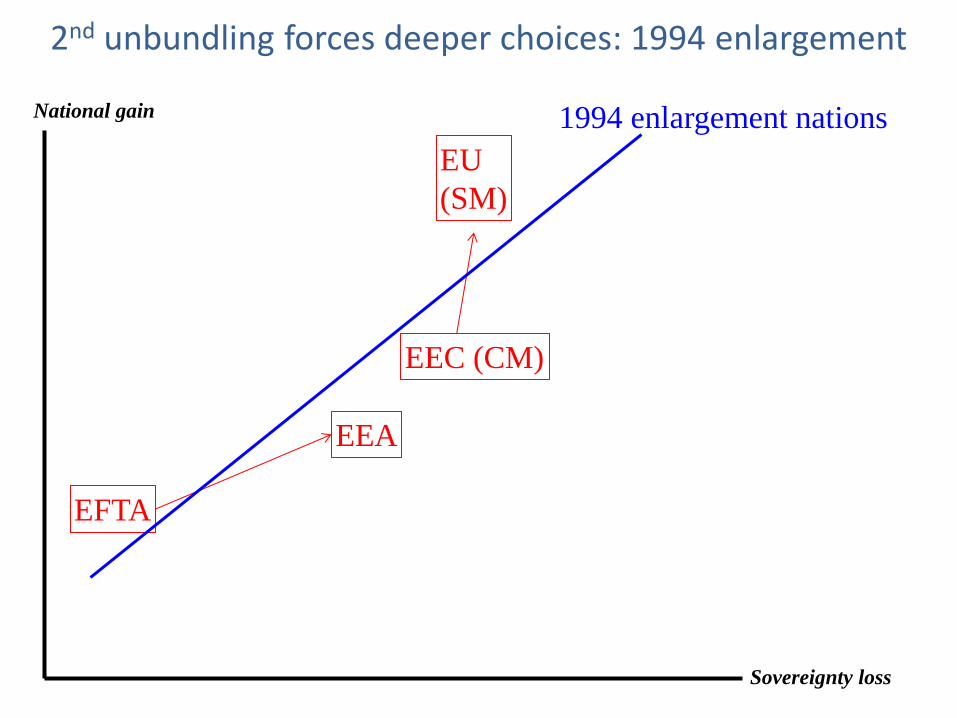

EEC (CM)

EFTA

EU

(SM)

EEA

1994 enlargement nations

2nd unbundling forces deeper choices: 1994 enlargement

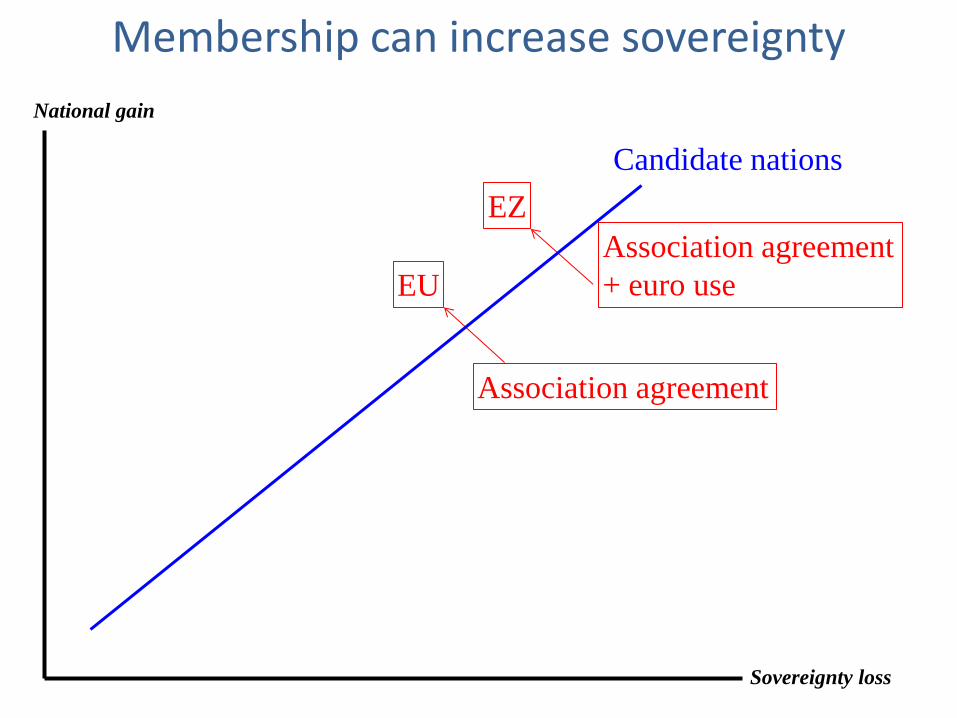

Candidate nations

EU

EZ

Association agreement

Association agreement

+ euro use

National gain

Sovereignty loss

Membership can increase sovereignty

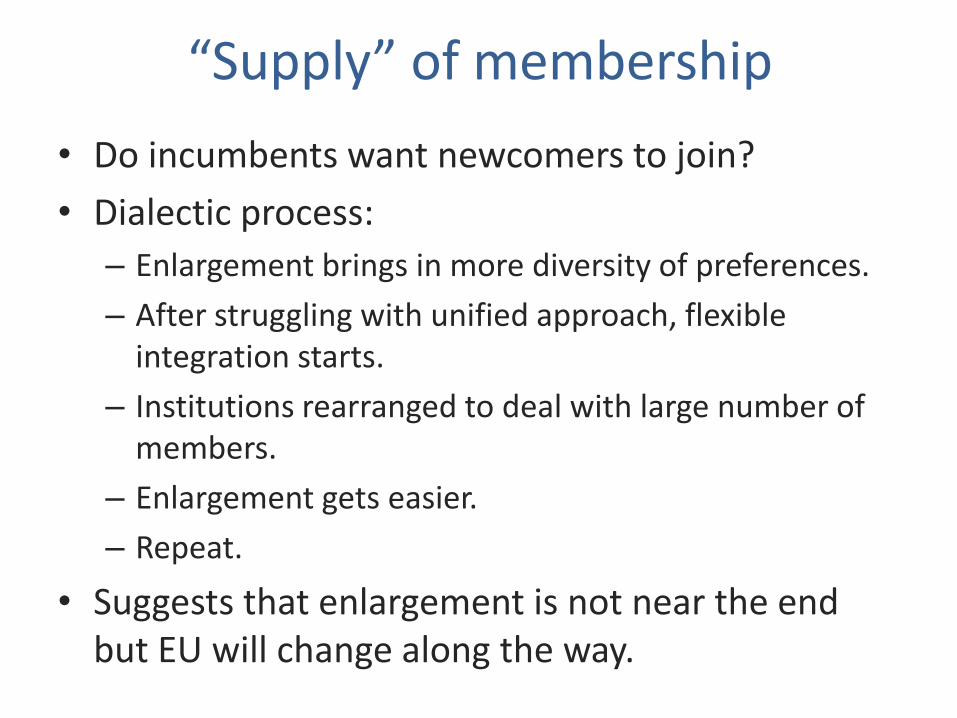

“Supply” of membership

• Do incumbents want newcomers to join?

• Dialectic process:

– Enlargement brings in more diversity of preferences.

– After struggling with unified approach, flexible integration starts.

– Institutions rearranged to deal with large number of members.

– Enlargement gets easier.

– Repeat.

• Suggests that enlargement is not near the end but EU will change along the way.

Back to international supply chains

• To date, most of ‘Factory Europe’ is inside EU.

– Turkey, Tunisia, Morocco

• Factory Europe likely to spread:

– Maghreb & Egypt

– Kenya

– Ukraine

• Do Europeans want tech to go to workers, or workers to come to tech?

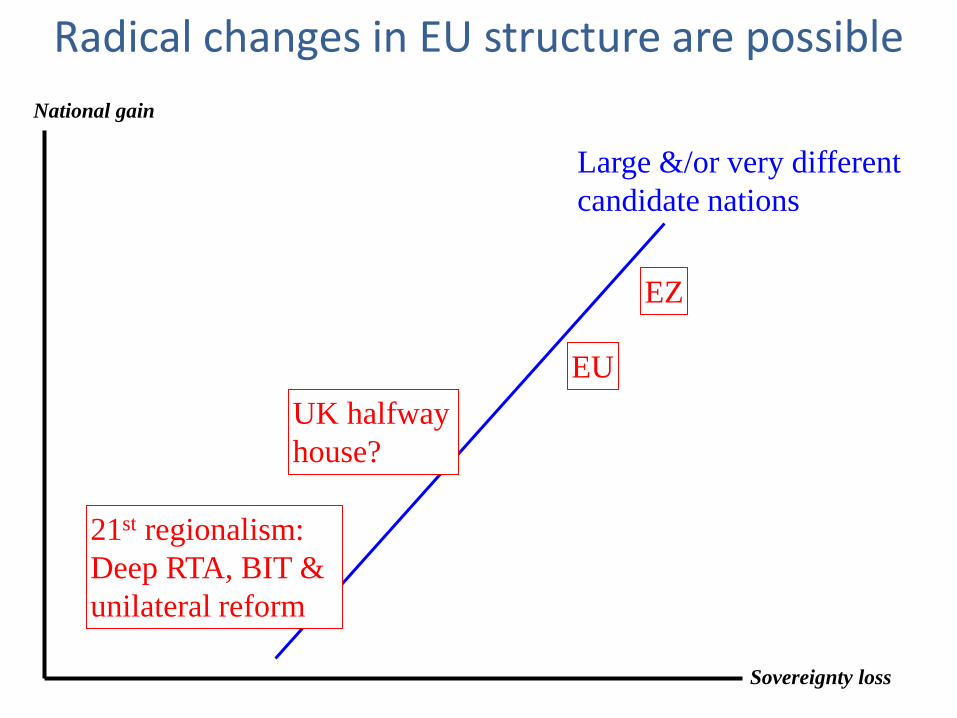

Large &/or very different

candidate nations

EU

EZ

21st regionalism:

Deep RTA, BIT &

unilateral reform

UK halfway

house?

National gain

Sovereignty loss

Radical changes in EU structure are possible

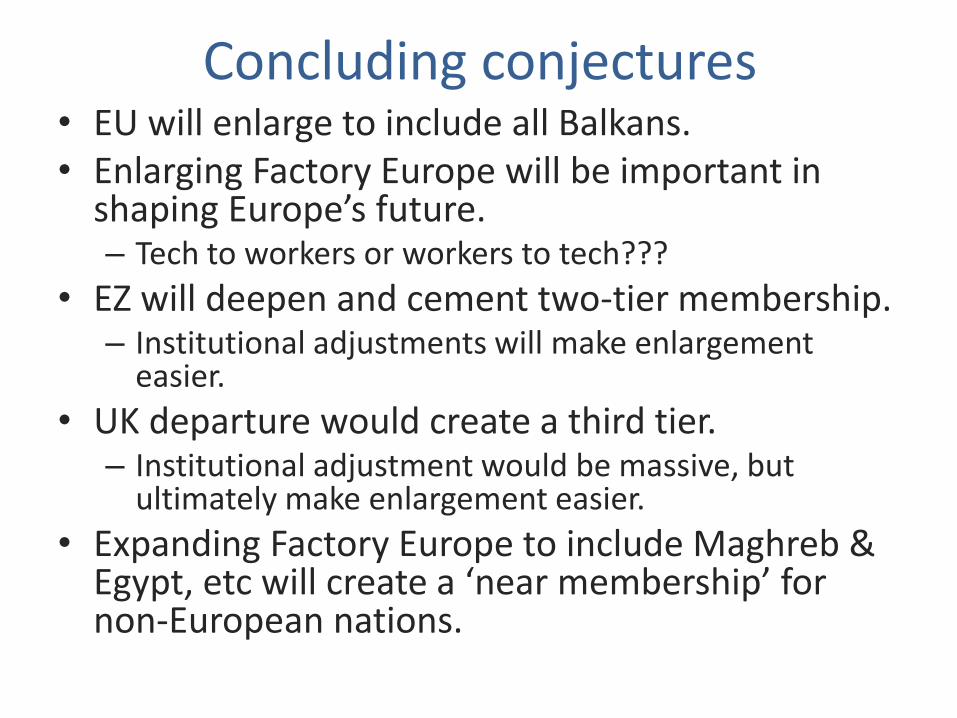

Concluding conjectures • EU will enlarge to include all Balkans. • Enlarging Factory Europe will be important in

shaping Europe’s future. – Tech to workers or workers to tech???

• EZ will deepen and cement two-tier membership. – Institutional adjustments will make enlargement

easier.

• UK departure would create a third tier. – Institutional adjustment would be massive, but

ultimately make enlargement easier.

• Expanding Factory Europe to include Maghreb & Egypt, etc will create a ‘near membership’ for non-European nations.

Thanks for listening

• Research-based policy analysis and commentary: VoxEU.org

http://www.voxeu.org/

The big SCT exporters

ChinaUS

Japan

Germany

France

Italy UK

NL

Belgium Spain

Korea

TaiwanCanadaMexico

All other

nations

Other

Global share of intermediate exports (industrial goods), 2009

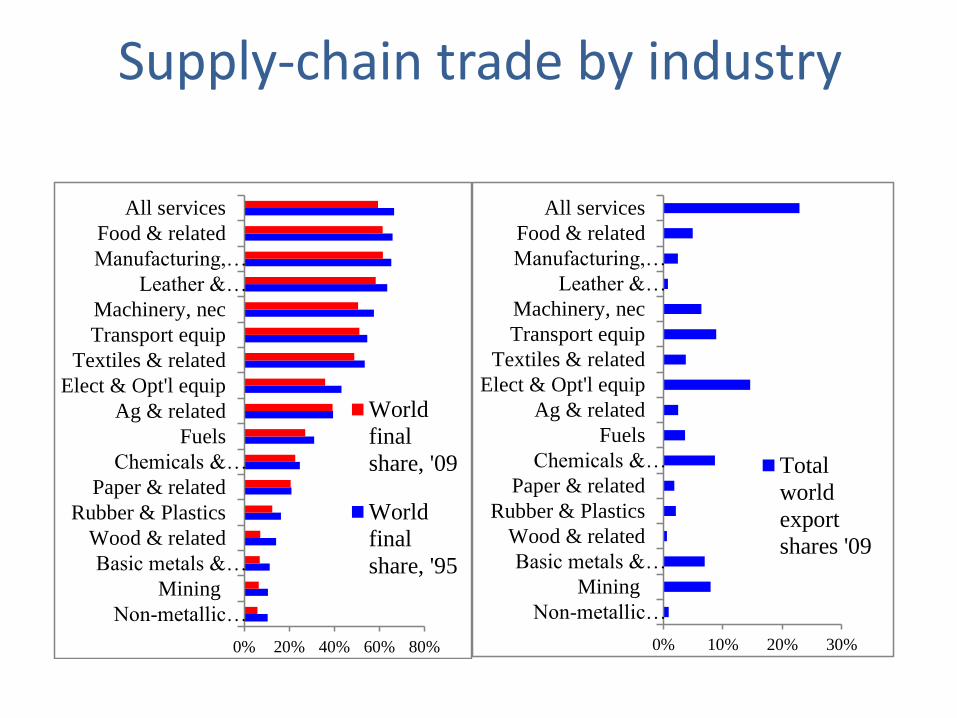

Supply-chain trade by industry

0% 10% 20% 30%

Non-metallic…

Mining

Basic metals &…

Wood & related

Rubber & Plastics

Paper & related

Chemicals &…

Fuels

Ag & related

Elect & Opt'l equip

Textiles & related

Transport equip

Machinery, nec

Leather &…

Manufacturing,…

Food & related

All services

Total

world

export

shares '09

0% 20% 40% 60% 80%

Non-metallic…

Mining

Basic metals &…

Wood & related

Rubber & Plastics

Paper & related

Chemicals &…

Fuels

Ag & related

Elect & Opt'l equip

Textiles & related

Transport equip

Machinery, nec

Leather &…

Manufacturing,…

Food & related

All services

World

final

share, '09

World

final

share, '95