Embed Size (px)

Citation preview

Works of friction? Originator-sponsor affiliation and

losses on mortgage backed securities

Cem Demiroglu, Koc University

Christopher James, University of Florida

1

Transformation of banking from intermediation to brokerage

Assets Liabilities

Deposits

Capital

Cash

Loans

Competition from junk bond markets

Competition from money market mutual funds

When spreads narrow, it is no longer profitable to be a buy-and-hold intermediary. Banks respond by selling and/or securitizing loans, to

more effectively use their limited and expensive capital.

2

The securitization process

EquityMezzanine bonds

Assets Liabilities

Mortgages Senior bonds

SPV

Mortgage-backed securities (MBS)

Mortgage pool

ORIGINATOR: Decides to either retain or sell or securitize mortgages in return for fee income

SPONSOR: Purchases mortgages from originator(s) and transfers them in a bankruptcy remote trust

SERVICERCollects mortgage

payments and transfers them to MBS investors, foreclose homes etc. in return for fee income 3

INVESTORSFund the SPV by purchasing MBS

backed by cash flows on mortgages

MORTGAGORS: Take out a mortgages from the originator, promise to make principal and coupon payments

RATING AGENCIESProvides rating on

SPV’s bonds, works with the sponsor on

SPV’s capital structure

The Originate-to-Distribute Puzzle

Old-fashioned mortgage lending is like a marriage: both the bank and the borrower have an incentive to make things work. Securitization,

at least in this market, was more orgiastic, involving lots of participates in fleeting relationships.” The Economist, May 15, 2008.

• Vertical integration in the securitization process has reduced loan originators’ incentive to screen because originators now have “too little skin in the game”

• Lax screening results in greater defaults

• Do rating agencies and/or sponsors recognize this incentive problem?

4

Loss exposures of each agent

• Originator: Loans are sold into the pool without recourse thus the originator’s loss exposure is limited to

Warehousing risk Representations and warranties Reputational issues

• Sponsor: Retains residual tranches and claims on the XS/OC . Thus sponsors have first loss exposure

• Servicer: The value of servicing rights depend on default rates

So, as the degree of vertical integration decreases (i.e., originators also serve as sponsors and servicers), the total

loss exposure of the originator increases, resulting in greater screening incentives and presumably better screening.

5

Implications for pool performance

• Because better screening is likely to be associated with better performance, pools that include loans by originators that have greater incentives to screen are likely to perform better.

Deal typeExpected (relative)

performance

Originators are affiliated with the sponsor +

Originators retain servicing rights +

Originator concentration +

6

Implications for MBS design and pricing

• If investors recognize that some originators screen more carefully than others, investors will require higher yields and greater credit protection when investing in pools originated by lenders with weaker incentives to screen.

Deal type

Expected yield & credit enhancement

(relative)

Originators are affiliated with the sponsor -

Originators retain servicing rights -

Originator concentration -

7

Sample• 526 Alt-A residential MBS deals completed between 2003 and 2007.

• We exclude private placements, NIM deals, deals that include second-lien mortgages, as well as deals without information on originator identities.

• Information on mortgage characteristics as well as originator, sponsor, and servicer identities and shares from the prospectus

• Information on pool performance and deal structure (e.g., yields and credit protection) from ABSnet

• Information on geographic location of mortgages in the pool from Bloomberg

• Information on house price changes from the Federal Housing Finance Agency (OFHEO)

8

The degree of vertical integration varies among deals

• MBSs vary considerably in terms of the number of originators and whether the originator, sponsor and servicer are affiliated

– CWALT 2007-24: Subsidiaries of Countrywide Financial served as originator, servicer and sponsor of the MBS. We call this an “Affiliated” deal.

– CWALT 2006-OC8: Countrywide was the sponsor but one of several originators and servicers of mortgages in the pool. We call this a “Mixed” deal.

– Bear Sterns Alt-A Trust 2006-4: Bear Sterns is the sponsor with Countrywide and at least 5 other unaffiliated entities originating and servicing the mortgages. We call this an “Unaffiliated” deal.

9

Originator characteristics

10

Pool performance as of 8/2009

11

Univariate results: Affiliation

0 5 10 15Average loss rate (%)

Unaffiliated

Mixed

Affiliated

CUMLOSS FORCL

12

Univariate results: Servicing rights

0 5 10 15 20

Average loss rate (%)

Not Retained

Retained

CUMLOSS FORCL

* Affiliated deals are excluded from this analysis because originators retain servicing rights in all affiliated deals.

13

Univariate results: Concentration

* Affiliated deals are excluded from this analysis because all but one affiliated deals are sole originator deals.

0 5 10 15

Average loss rate (%)

Multiple originators

Sole originator

CUMLOSS FORCL

14

Control variables used in multivariate regressions

• Deal level, loan size-weighted average…– Coupon rate on mortgages – Borrower FICO score– Loan-to-value ratio – Documentation type (% limited or no-doc) – % of mortgages that are adjustable rate or hybrid– Whether the mortgages have negative amortization feature – Occupancy status of mortgages – Ownership type – State-level % change in house prices from loan date to August 2009– Vintage fixed effects – Sponsor fixed effects

15

Multivariate results: Affiliation & CUMLOSS (%)

16

Multivariate results: Affiliation & FORCL (%)

17

Does the impact of affiliation on performance increase as uncertainties

regarding loan quality increase?

18

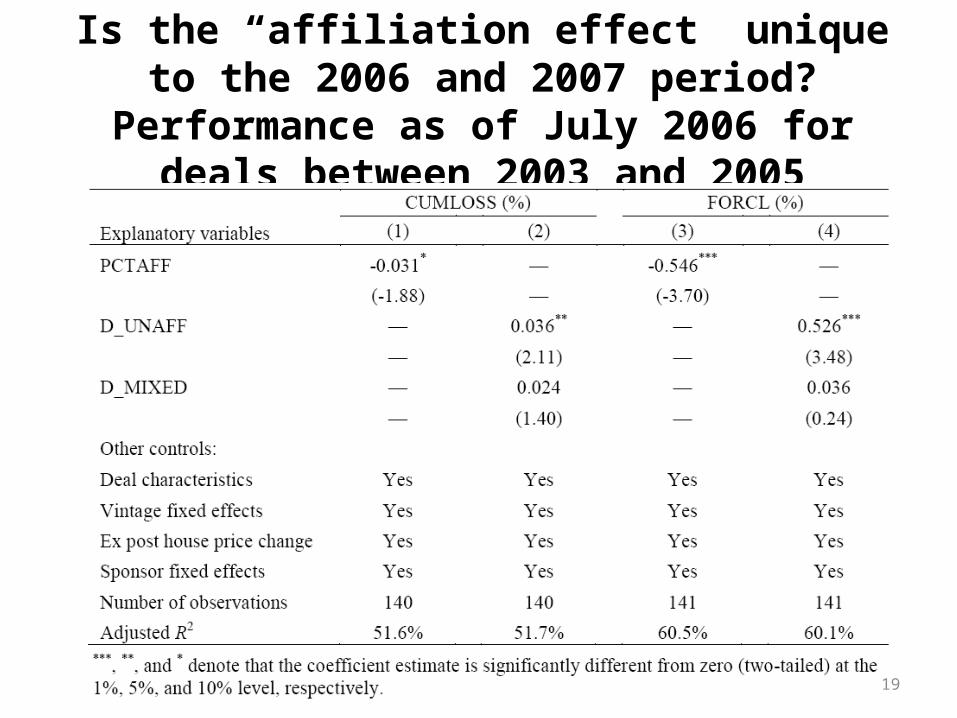

Is the “affiliation effect” unique to the 2006 and 2007 period? Performance as of July

2006 for deals between 2003 and 2005

19

Is affiliation a proxy for depository originators with specialized

screening abilities?

20

Originator concentration, originator-servicer affiliation, and deal performance

for unaffiliated and mixed deals

21

Evidence so far

• Deals perform relatively better ex post if the originator’s distance from loss is shorter. This is particularly true when there is greater uncertainty regarding the borrowers’ creditworthiness (where screening is more important).

• The evidence points to the importance of originators’ screening incentives on deal performance.

• The evidence also suggests that originator screening incentives were related to deal performance before the economy-wide decline in house prices and the credit crisis, but the incentive effect was largely masked by credit expansion and house price increases.

22

Do investors and/or rating agencies recognize the variability

in originators’ screening incentives?

• It’s been argued that the originate-to-distribute model of lending (i.e., securitization) is flawed because it reduces lenders’ incentive to screen.

• However, as Gorton (2009) points out, the other part of the argument that securitization promoted lax lending has to be that pool sponsors and ultimately investors systematically misunderstood or ignored how securitization affects the incentives of originators and ultimately the risk of the underlying mortgages.

• Therefore, we next examine whether investors require higher yields and greater credit protection in deals with greater originator moral hazard.

23

Deal structure variables

24

Deal structure regressions

25

Conclusions

• Originators with greater distance from default are less likely to screen the loans that they originate. Consequently, these loans perform relatively poorly.

• Investors recognize this incentive problem on behalf of mortgage originators and request higher yields and greater credit protection in deals in which the moral hazard problem is likely to be more severe. It is not clear, however, whether the problem is correctly reflected into prices.

• Recent policy proposals to force originators to hold bigger stakes in the securitized pools and disclose the full extent of their exposure to the pool’s losses are likely to be useful.

26

![Koc Katimi [PowerPoint]](https://img.pdfslide.net/doc/110x75/548517a0b47959140d8b4de2/koc-katimi-powerpoint.jpg)