Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 1 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

A Synopsis on

Credit Risk Evaluation of

Micro, Small and Medium Scale

Enterprises using

Evolutionary Neuro Fuzzy Logic

by

Desai Karanam Sreekantha

submitted in fulfillment for requirements of the degree

DOCTOR OF PHILOSOPHY

in

FACULTY OF COMPUTER STUDIES

to

SYMBIOSIS INTERNATIONAL UNIVERSITY, PUNE

under the guidance of

Prof. Dr. R.V.Kulkarni Professor & Head

Chh. Shahu Institute of Business Education & Research

(SIBER), Kolhapur - 416 004.

April 2013

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 2 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Chapter Index

Chapter No. Title Page No.

1. 1.1

Introduction 1

Background of the problem 1

1.1.1 National status of MSME segment 1

1.1.2 International status of MSME segment 2

1.2 Statement of the problem 2

1.3 Purpose of the study 2

1.3.1 Advantages of credit risk assessment 2

1.3.2 Advantages of expert systems 2

1.4 Significance of the problem 3

1.5 Objectives of the study 3

1.6 Limitations of manual systems 3

2. Review of the literature 4

3. Research methodology and study design 7

3.1 Foundations for credit risk research 7

3.2 Scope of the study 7

3.3 Hybrid soft computing – evolutionary neuro fuzzy logic

7

3.4 Credit Lending Decision 8

4. Credit Rating Frameworks (CRF) design 9

4.1 4.1.1 Manufacturing industry CRF 10

4.1.2 Trading industry CRF 11

4.1.3 Service industry - healthcare - nursing home CRF 11

4.1.4 Service industry - hospitality – hotels CRF 12

5. Rulebase design 13

5.1 Manufacturing industry rulebase 13

5.2 Service industry rulebase 14

5.3 Trading industry rulebase 14

6. Expert system prototype development 15

6.1 Introduction to Expert System Builder(ESB)

software

15

6.2 Credit Risk Evaluation Expert System (CREES)

design

15

6.3 User interface design 16

6.4 Sample test reports 16-17

7. Result analysis 18

8. 8.1 Conclusions and Findings 19

8.2 Scope for further research 19

8.2 UGC MRP funding 19

8.3 Best paper of International Conference Award 19

9. Researcher publications and presentations 20-21

10. References 22-25

© SYMBIOSIS INTERNATIONAL UNIVERSITY, PUNE All Rights Reserved

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 3 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Chapter - 1 Introduction

Introduction chapter describes the credit risk evaluation of Micro, Small and

Medium scale Enterprises (MSME) research problem, its background and

significance. The national and international status of the MSME industry,

objectives of research, hypothesis formulated, definition of the basic terms,

assumptions are discussed. This chapter also covers the limitations and

outline of the study.

Introduction

MSME segment is one of the fastest growing industrial sectors and constitute

over 90% of total enterprises in most of the economies of the world. The

researchers estimate that about 60% of the MSME credit is provided by

commercial banks alone. Over the past few years the credit risk evaluation of

MSME by banks and financial institutions has been an active area of research

under the joint pressure of regulators and shareholders. The Credit Risk

Evaluation (CRE) involves evaluation of risk parameters such as financial,

business, industry and management etc. A MSME client always has more

private information about the risk in his proposal, so that when a client comes

with a loan request, the banks have no way to judge its risk extent from the

facts in the loan documents. This is the direct reason leading to risk and crux

of the problem for banks. An incorrect decision endangers bank’s financial

capability ending up in steep decline in the margin of profits.

1.1 Background of the problem

1.1.1 National status of MSME segment

The quick results of 4th all India census of MSME (2006-07) reveals that the

sickness in MSME has increased from 13.98 percent in 2001-02 to 14.47

percent in 2006-07. One of the reasons for sickness is shortage of working

capital. Federation of Indian Export Organizations (FIEO) president Mr. A.

Sakthivel pointed out that "Interest rates in India are much above the

international benchmark”. This increased prime lending rates are a jolt to

MSME exporters.

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 4 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

1.1.2 International status of MSME segment

Manufacturing sector accounts for 30–50% of GDP and drives the economies

of Asian countries such as Thailand, Indonesia, Malaysia, Singapore, Hong

Kong, Taiwan, Philippines, Korea, and China. China’s manufacturing segment

is 50% of GDP, but India is lagging behind with 25% share of GDP. The

present conditions do not promote manufacturing in India.

1.2 Statement of the problem

MSME need financial assistance to establish and conduct their business,

trading and service activities. The effective management of credit risk is a

critical component of risk management and essential to the long-term success

of any banking organization. The banks are in need of a consistent and

integrated credit risk evaluation system to optimize their lending operations.

Researcher developed of an Expert System called Credit Risk Evaluation

Expert System (CREES) prototype to support in taking credit risk decisions in

banks and financial institutions by credit rating executives.

1.3 Purpose of the study

The recent tarnishing bankruptcies in US such as WorldCom, Enron,

HealthSouth, Tyco and many other high profile banks failures in Asia forced

many banks and financial institutions to realize the need for a viable credit risk

management. The early decades of this century have witnessed many

sensational incidents of accounting irregularities in which the executives have

been caught cooking the books.

1.3.1 Advantages of credit risk assessment

1. Facilitates informed credit decision consistent with bank’s risk appetite

2. Provides ability to price products on the basis of risk

3. Facilitates dynamic provisioning and minimizes impact of losses

4. Lending decisions can be taken within the minimum time, thus lending

business volume can increase substantially

1.3.2 Advantages of expert systems

Application of expert systems in financial management has grown

considerably in the last two decades and they have advantages like

1. Superior problem solving capability

2. Applying experience to problems

3. Reduced response time for complex problems and

4. Ability to look at problems from a variety of perspectives

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 5 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

1.4 Significance of the problem

1.5 Objectives of the study Fig-1 Bankruptcies

The researchers aimed at developing an expert system prototype for credit

risk evaluation of MSME segment with following objectives

1. Designing the credit rating framework to measure and quantify all

subjective and objective parameters of credit decision environment

2. The credit evaluation solution is based hybrid soft computing technique

called on evolutionary neuro fuzzy approach

3. Collecting real credit data from various banks in their region and test the

solution

4. Designing an expert system incorporating local conditions and

requirements

5. Designing the solution to meet the different business lines and Industries

6. Implementation of expert system using fuzzy and neural network tools

1.6 Limitations of manual systems

Research has shown that human brain is capable of evaluating only a small

number of factors at a time, but the credit risk analyst needs to analyze and

deal with large number of differently valued factors in short time. The lack of

rigor in professional judgment leads to the risk of misinterpretation,

misunderstanding, miscommunication, miscalculation and misuse of soft

information. The manual credit risk evaluation systems are quite expensive

due to high cost of training, maintaining the qualified and experienced

personnel.

In 2007 world economic crisis, 13 US based

companies reported $50 billion of losses and

$300 billion market capture losses shown in

Fig-1. In March 2005 American Insurance

Group admitted to improper accounting that

cut its net worth by more than $1.7 billion.

These tarnishing bankruptcies forced many

banks and financial institutions to realize the

importance of credit risk management.

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 6 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Chapter - 2 Review of literature

This chapter covers an exhaustive survey of literature (of about 300 most

relevant articles) on MSME and credit risk evaluation from reputed journals

such as IEEE Transactions on credit risk, machine intelligence, business

journals and proceedings of various international conference proceedings

since 1964 to today. Some selected articles from the survey are discussed by

way of illustration.

The surveyed literature can be classified in two major three categories as

casual methods, statistical methods and rulebased methods as shown in

Fig-2. There are hybrid methods which are adopting more than one technique

for credit risk evaluation

Fig-2 Survey of credit risk models

Paul F. Smith (1964) authored Measuring Risk on Consumer Installment

Credit paper and developed a relatively simple statistical method for

measuring risk on individual accounts that can also be used for measuring

and controlling portfolio quality and for estimating loss rates.

Peter Duchessi and Salvatore Belardo (1987) have designed knowledge

based system prototype to support commercial loan officers in credit risk

analysis. The knowledge based system was called Loan Analysis Support

System (LASS). This system provides a user interface to deal with variety of

data, analytical operations and models in a flexible manner.

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 7 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Rekha Jain (1989) paper entitled Expert Systems: A Management

Perspective highlights some of the expert system important features.

MARBLE (Managing and Recommending Business Loans Evaluations) expert

system is a loan evaluating expert system. MARBLE combines financial

projections with qualitative data. The loan granting decision is a combination

of factors related to an analysis of the firm's historical, financial information,

qualitative information about its product market, industry characteristics and

overall performance of the management. MARBLE system captures some of

these features by analyzing the economic characteristics (size, market share),

financial characteristics (profitability, liquidity and leverage), ability to repay

loans (cash flow analysis, security), value of collateral, competitive position in

industry, etc. Each of the relevant factors is given a certain weightage to

evaluate a credit risk score.

Sushmita Mitra and Yoichi Hayashi (2000) have conducted exhaustive survey

of neuro–fuzzy rule generation algorithms and presented Neuro–Fuzzy Rule

Generation: Survey in Soft Computing Framework paper. The neuro–fuzzy

approach, symbiotically combining the merits of connectionist and fuzzy

approaches constitutes a key component of soft computing at this stage.

Authors propose to bring these together under a unified soft computing

framework and included rule extraction and rule refinement in a broader

perspective of rule generation. Rules learned and generated for fuzzy

reasoning and fuzzy control are also considered from this wider view point.

This study also provided real life application to medical diagnosis.

Xuemei Zhu, Ping Wang (2008) in their paper, The credit risk assessment

method based on Dempster-Shafer combining evidence theory - Reasoning of

the methods evolved an expert methodology known as CAMPARI factor

analysis, which assesses the customer credit worthiness by applying seven

criterions. The word CAMPARI stands for C-Character, A-Ability, M-Margin, P-

Purpose, A-Amount, R-Repayment and I-Insurance. This method largely

depends on the ability of the expert in assessing the credit risk.

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 8 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Such an expert method can prove quite efficient in assessing the debtor credit

as it relies on the historic information of the debtor and the subjective

judgment of the experts. This method is usually applicable for qualitative

rather than quantitative analysis and hence lacks an objective appraisal.

Adel Lahsasna (2009) in his article Evaluation of credit risk using

evolutionary-fuzzy logic scheme discusses the transparency and the accuracy

of credit scoring model. The author investigates credit risk using two different

types of fuzzy models namely Takagi-Sugeno (TS) and Mamdani using

generic software called Evolutionary-Fuzzy-Neuro-System (EvoFNS). This

software is used for fuzzy identification, (generation and optimization)

prediction, classification and knowledge extraction.

Shaomei Yang and Junyan Zhao (2009) in their paper Study on commercial

banks credit risk based on CAMEL rating system identifies five areas such as

Capital adequacy, Asset quality, Management ability, Earnings and Liquidity.

The initials of five words form the term CAMEL and CAMEL rating system is

used for the assessment of commercial banks credit rating system.

Linda Delamaire (February 2012) proposed the implementation of credit risk

management system based on innovative scoring techniques. Their thesis

presents a credit scoring system which aims at setting credit lines and thus,

controlling credit risk. It includes three types of models: application

scorecards, early detection scorecards and behavioral scorecards. They have

been built on real and recent data coming from a German credit card

company. The models have been built with a training sample and validated

accordingly, using logistic regression. Information value and validation charts

have been used for comparing the models. Finally, the author presents

possible extensions to the research and hopes that the technique described in

this thesis can play some part in preventing future financial crisis.

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 9 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Chapter - 3 Research methodology and study design

This chapter deals with the foundation work done by earlier researchers and

scope of the present research. The hybrid soft computing technique called

Evolutionary Neuro fuzzy logic has been applied in the present work.

3.1 Foundations for credit risk research

The basic work on credit risk was discussed in the book entitled

Knowledgebase applications in Banking Sector by Prof. R.V.Kulkarni and

Prof. B. L. Desai. The present research may be viewed as a unique

contribution in this field, which uses hybrid soft computing - evolutionary

neuro-fuzzy technique.

MSME clients need finance to setup and conduct their operations, so they

approach banks/financial institutions for credit. The credit rating executives

gather information about the clients in order to take an informed decision

about his creditworthiness and the prospects of repayment.

3.2 Scope of the study

The effective management of credit risk is a critical component for long term

success of any banking organization. What is really needed is a consistent

and integrated risk management system. The quality of credit decision

depends on the ability of credit risk executive’s subjective judgment and

experience. The researchers have studied credit risk systems at State Bank of

India, Zonal Office, Hubli, State Bank of India Commercial Branch, Belgaum,

Canara Bank, Bagalkot, Karnataka State Finance Corporation branch office,

Bagalkot, BVVS Software Technology Entrepreneurs Park, Bagalkot and

BVVS Rural Development Foundation, Bagalkot.

3.3 Hybrid soft computing - Evolutionary Neuro fuzzy Logic

Authors have applied hybrid soft computing technique called evolutionary

neuro fuzzy logic for designing an expert system solution for credit risk

evaluation of MSME. Neural networks imitate functions of the human brain's

ability to sort out patterns and learning from trial and errors, discerning and

extracting the relationships that underlie the data with which it is presented.

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 10 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Neural networks are good at providing very fast and very close

approximations of the correct answer. Fuzzy computing can handle qualitative

values instead of quantitative values. It can define linguistic variables instead

of the classical numeric variable and perform computing with these variables,

using fuzzy rules, simulating in a certain way the human reasoning processes.

Evolutionary computation uses iterative progress, such as growth or

development in a population. This population is then selected in a guided

random search using parallel processing to achieve the desired end. The

principal constituents of soft computing are fuzzy logic, neuro computing, and

probabilistic reasoning, with the latter subsuming genetic algorithms, belief

networks, chaotic systems, and parts of learning theory.

3.4 The lending decision - participating institution model

Researchers have conducted interviews with credit rating executives and

evaluating documentation pertaining the underwriting process and identified

the key dimensions employed when assessing business loan applicants

Repayment capacity - accounts for 35 percent of the credit decision and

comprises the evaluation of financial parameters such as current, quick

and debt/service ratio; and an assessment of the borrower’s credit history

Financial position - accounts for 20 percent of the credit decision and

comprises the evaluation short and long term repayment capacity backed

by financial statements representative of an adequate financial condition

Character - accounts for 10 percent of the credit decision and comprises

personal factors of the borrower such as honesty, propensity to meet with

obligations, disposition, availability and cooperation with bank officials and

managerial experience

Business and industry conditions - accounts for 10 percent of the credit

decision and comprises the evaluation of physical conditions of the

business and industry conditions

Collateral - accounts for 25 percent of the credit decision and comprises the

evaluation of identifiable and accessible assets which net value covers the

loan principal, interests and escrow

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 11 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Chapter - 4 Credit rating frameworks design

This chapter deals with designing the framework called Credit Rating

Framework (CRF) for credit risk evaluation of MSME. CRF is designed to

measure all the objective and subjective risk parameters of credit decision

environment. The CRF organizes all the facts of the client in five levels

depending on their nature and criticality. These risk parameters are

organized in to five hierarchical levels. These risk parameters are transformed

in to the linguistic variables of fuzzy logic. Every risk parameter is assigned a

score based on its significance in credit decision-making. Each client’s actual

credit weight is computed on the basis of client’s credit worthiness. This

framework forms the basis for knowledge base and Expert System design.

This process resembles the credit risk executives thought process. The credit

risk evaluation process is depicted in Fig-3.

Fig-3 Credit Rating Framework Design Process

The credit decisions parameters for manufacturing, trading and service

industries are identified as shown in Fig-4. The technical feasibility is the

dominant risk parameter in manufacturing industry with score of 200 out of

total score 500 (40%) weightage. Finance risk is 40% of total risk in trading

industry. Management risk is the dominant risk parameter in service

industries like hotels and healthcare.

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 12 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Fig-4 Credit risk parameters in Manufacturing,Trading and Service Industries

Credit Rating Frameworks (CRF)

The Credit risk parameters for all there I dustries are shown in the following

Tables 1 to 3. Table-3 Service Industry risk parameters

Table -1 Manufacturing industry risk

20%

20%

15%

25%

20%

Management Risk

Property Risk

Operational Risk

H e a l t h C a r e C r e d i t R i s k

1 4 %

8 %

1 3 %

1 3 %1 3 %

8 %

1 0 %

1 3 %

8 %

1 P r o f i l e o f P r o m o t e r s 2 B a c k g r o u n d o f N u r s i n g H o m e

3 P r o p o s e d N u r s i n g H o m e 4 M a r k e t P o t e n t i a l

5 P r o j e c t C o s t 6 Im p l e m e n t a t i o n S c h e d u l e

7 S t a f f P r o f i l e 8 S o u r c e s o f F i n a n c e

9 R e p a y m e n t

Sl. No

Title Linguistic Values

Max Weight

1 Technical Feasibility

OK / Not OK 200

2 Management Commitment

Excellent/ Good/ OK/ Poor

100

3 Commercial Viability

OK /Not OK 75

4 Financial Analysis

Excellent/ Good/OK/Poor

75

5 Economic Analysis

Excellent/ Good/OK/ Poor

50

Total Weight 500

Sl. No

Risk Parameter Max. Score

Min. Score

1 Profile of Promoters 70 28

2 Background of Existing Nursing Home

70 28

3 Proposed Nursing Home Features

75 30

4 Market Potential 75 30

5 Project Cost 75 30

6 Schedule of Implementation

50 20

7 Staff Profile 75 30

8 Sources of Share Capital

60 24

9 Repayment Proposal

50 20

10 Total 600 240

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 13 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

The trading industry CRF is shown in table. The major risk parameters like

Management risk, Business risk and Finance risk, its sub parameters, fuzzy

linguistic variables are shown in the Table - 2 below and Table-4.

Table-4 Trading CRF

Sl. No

Parameter Score Wei ght. in%

1 Management risk

40 27

2 Business risk 50 33

3 Finance risk 60 40

Total 150 100

Code Parameter Score Sub Score

Relative Weight

in %

Best Good Avg. *

Poor

1.0 Management Risk 60 40 60 52 34 19

1.1 Management Quality 10 10 8 4 2

1.2 Financials and MIS 10 10 8 4 1

1.3 Account Behavior 20 20 18 13 8

1.4 Technical Qualification 20 20 18 13 8

2.0 Business Risk 50 33 50 36 26 13

2.1 Competition 10 10 8 6 3

2.2 Locational Advantage 5 5 3 2 1

2.3 Commodities Traded 5 5 3 2 1

2.4 Market Perception 10 10 8 6 3

2.5 Industry Profile 5 5 3 2 1

2.6 Product Characteristics 10 10 8 6 3

2.7 Marketing 5 5 3 2 1

3.0 Financial Risk 40 27 40 32 20 8

3.1 Earnings/Growth Trends 6 6 5 3 1

3.2 Tol/TNW 6 6 5 3 1

3.3 Inventories to Debtors/ Sales

4 4 3 2 1

3.4 Sundry Creditors to Purchases

4 4 3 2 1

3.5 Net Profit /Sales 6 6 5 3 1

3.6 Bank borrowing to sales 4 4 3 2 1

3.7 Current Ratio 6 6 5 3 1

3.8 Stock holding to Sales 4 4 3 2 1

Total 150 100 150 120 80 40

Credit Rate

Risk Level Weight Weight in%

AAA Highest Safety

WAAA >=95<100

AA High Safety WAA >=85< 95

A Adequate Safety

WA >=80< 85

BBB Moderate Safety

WBBB >=70< 80

BB Inadequate Safety

WBB >=60< 70

B Significant Risk

WB >=55< 60

C High Risk WC >=50< 55

D Default WD < 50

Table-5 Credit Ratings, Risk levels and Weights percentage

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 14 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

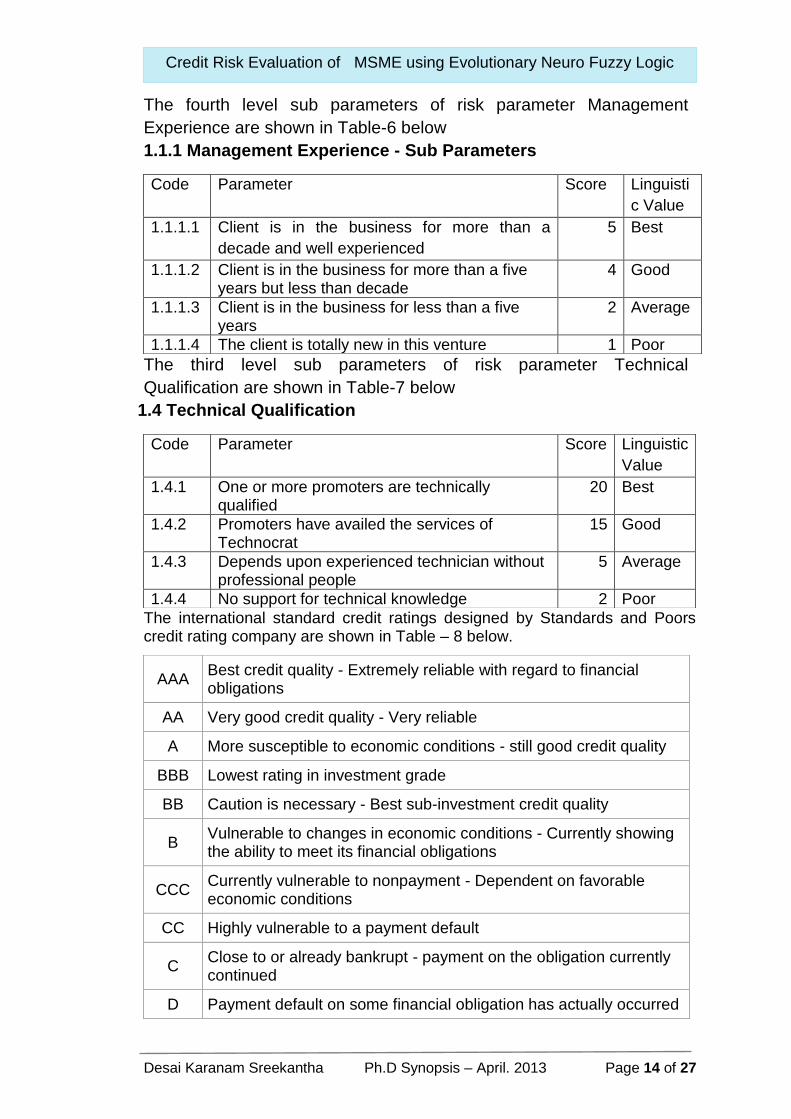

The fourth level sub parameters of risk parameter Management

Experience are shown in Table-6 below

1.1.1 Management Experience - Sub Parameters

The third level sub parameters of risk parameter Technical

Qualification are shown in Table-7 below

1.4 Technical Qualification

The international standard credit ratings designed by Standards and Poors credit rating company are shown in Table – 8 below.

Code Parameter Score Linguisti

c Value

1.1.1.1 Client is in the business for more than a

decade and well experienced

5 Best

1.1.1.2 Client is in the business for more than a five years but less than decade

4 Good

1.1.1.3 Client is in the business for less than a five years

2 Average

1.1.1.4 The client is totally new in this venture 1 Poor

Code Parameter Score Linguistic

Value

1.4.1 One or more promoters are technically qualified

20 Best

1.4.2 Promoters have availed the services of Technocrat

15 Good

1.4.3 Depends upon experienced technician without professional people

5 Average

1.4.4 No support for technical knowledge 2 Poor

AAA Best credit quality - Extremely reliable with regard to financial obligations

AA Very good credit quality - Very reliable

A More susceptible to economic conditions - still good credit quality

BBB Lowest rating in investment grade

BB Caution is necessary - Best sub-investment credit quality

B Vulnerable to changes in economic conditions - Currently showing the ability to meet its financial obligations

CCC Currently vulnerable to nonpayment - Dependent on favorable economic conditions

CC Highly vulnerable to a payment default

C Close to or already bankrupt - payment on the obligation currently continued

D Payment default on some financial obligation has actually occurred

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 15 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Chapter - 5 Rulebase design The set of guiding rules in taking the credit risk decision by credit rating

executives in banks are captured and encoded in to a rulebase. A separate

fuzzy rule base is developed for every industry and every major risk such as

management risk, business risk and finance risk in the credit rating framework,

to facilitate change of rules easily. These rulebases are used by expert system

in credit risk evaluation from the client’s credit data. The Mamdani inference

approach i.e. first infer-then-aggregate (FITA) is used to implement the fuzzy

logic rule base. These rulebases consists of about 300 rules to evaluate the

credit worthiness of the client. Some of the sample rules are listed below.

Manufacturing industry risk assessment rulebase

Rule No

Antecedent IF

Consequent Then

1. Technical Feasibility is Excellent AND Management Commitment is Excellent AND Commercial Viability is Excellent AND Financial Analysis is Excellent AND Economic Analysis is Excellent

Client Rating is Excellent

2. Integrity is excellent AND Involvement is excellent AND Financial Resources are excellent AND Competence is excellent AND Leadership is excellent AND Organization Structure is excellent

Management Commitment is excellent

Healthcare service industry risk assessment rulebase

3. Profile of Promoters is Excellent AND Background of Existing Nursing Home is Excellent AND Proposed Nursing Home Features are Excellent AND Market Potential is Excellent AND Project Cost is Excellent AND Staff profile is Excellent AND Schedule of Implementation is Excellent AND Sources of Capital are Excellent AND Repayment Proposal is Excellent

Promoters Rating is the Excellent, Credit Risk is Negligible

4. Infrastructure is Excellent AND Consultancy profile is Excellent AND Diagnosis facilities are Excellent AND Ambulance Facilities are Excellent AND Surgical Facilities is Excellent

Proposed Nursing Home Features are Excellent

5. Repayment of Interest is Excellent AND No Transgressions AND Compliance of Sanction terms is Excellent AND Turnover in the Account is Excellent AND Cheque /Bill Return is Excellent AND Operation in the Account is Excellent

Account behavior and Track Record is Excellent

6. Management Quality is the Best AND MIS & Financials is the Best AND Account Behavior & Track Record is the Best AND Technical Qualification is the Best

Management is the Best Management Risk is Negligible

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 16 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

7.

Property Risk Rating is Highest Safety AND Management Risk Rating is Highest Safety AND Operational Risk Rating is Highest Safety AND Financial Risk Rating is Highest Safety AND Market Risk Rating is Highest Safety

Hotel credit proposal is Excellent, Credit Risk Rating is Highest Safety, Rating is AAA

Hotel industry risk rulebase

8. Location & Visibility Rating AND Property Characteristics Rating AND Construction cost per room AND Access to Road Rail AND Parking Availability Rating AND Catchment Area Rating

Property Risk is Highest Safety Property Risk Rating is AAA

9. Management Quality is the Best AND MIS & Financials is the Best AND Account Behavior & Track Record is the Best AND Technical Qualification is the Best

Management is the Best, Management Risk is Negligible

Trading industry risk rulebase

Rule No

Antecedent IF

Consequent Then

10. Management is the Best AND Business is the Best AND Financial is the Best

Client Rating is the Best ,Client Risk is Negligible

11. Competition is the Best AND Locational Advantage is the Best AND Commodities Traded is the Best AND Industry Profile is the Best AND Market Perception is the Best

Business is the Best Business Risk is Negligible

12. Earnings/Growth Trends is The Best AND Tol/TNW is The Best AND Inventories +Debtors/Sales is The Best AND Sundry Creditors to Purchases is The Best AND Net Profit /Sales is The Best AND Bank borrowing to sales is The Best AND Current Ratio is The Best AND Stock holding to Sales

Financials is the Best Finance Risk is Negligible

13 Repayment of Interest is Excellent AND No Transgressions AND Compliance of Sanction terms is Excellent AND Turnover in the Account is Excellent AND Cheque/Bill Return is Excellent AND Operation in the Account is Excellent

Account behavior and Track Record is Excellent

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 17 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Chapter - 6 Expert system prototype design

6. Expert system prototype design This chapter discusses the methodology of developing the prototype for Credit

Risk Evaluation Expert System (CREES). The software development process

of CREES and tools used is explained. Menu structures and screen layouts

for capturing the client data and risk evaluation process are discussed.

Researchers have designed an expert system model and called Credit Risk

Evaluation Expert System (CREES) and tested the system with test data

select representative sample size of 500.

6.1 CREES design The CREES user/language interface frontend shown in Fig-3 is developed

using Dream viewer tool.

MySql server is used for implementing the backend database design.

Apache Tomcat 5.5 web server has been used in web interface development.

Fuzzy Jess tools are plugged in to eclipse environment.

6.2 User interface design

Credit Portfolio Knowledgebase

e

Credit Processing

Credit Models

Credit Reporting

Language I n t e r f a c e

Client Credit History

Database

Current Client Database

Fuzzyfication

Defuzzyfication Fuzzy Inference

Knowledge Acquisition

Neural Networks

Credit Experts Knowledgebase

Evaluate Alternatives

Explanation Knowledgebase

Knowledgebase Inference Engine Explanation

Fig-5 Prototype for Credit Risk Evaluation Expert System (CREES)

Fig-6 Desktop of Credit Risk Evaluation Expert System (CREES)

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 18 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Fig-7 System users information

6.3 Sample test reports The sample test reports are shown in the following test cases

Test Case : 1

Credit Risk Evaluation using Expert System- Manufacturing Sector Client Id : C000000001 Application Id : A000000001 Client Name : ABC Cement Industries Ltd 1. Technical Feasibility Rating is - OK 2. Management Commitment Rating is - OK 3. Commercial Viability Rating is - OK 4. Financial Analysis Rating is - OK 5. Economic Analysis Rating is - OK Credit Risk Rating of the client is Significant Safety

Test Case : 2

Client Id : C000000001 Application Id : A000000001 Client Name : ABC Cement Industries Ltd 1. Loan Details Rating is - Very Good 2. Net Present Value Rating is - Very Good 3. Business Ratios Rating is - Very Good 4. Project Cost Rating is - Very Good 5. Liquidity Rating is - Very Good 6. Profitability Rating is - Very Good 7. Current Business Assets Rating is - Very Good 8. Balance Sheet Status Rating is - Very Good Economic Analysis Risk Rating is Excellent Risk Rating High Safety-AA

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 19 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Test Case : 3 Management Client Integrity Risk Rating Client Id : C000000001 Application Id : A000000001 Client Name : ABC Cement Industries Bagalkot Credit Risk Code : 010301 1. Willingness Rating is - Good 2. Informated Rating is - Good 3. Enthusiasm Rating is - Good Risk Score vs Max Score 8.0/15.0 Risk Rating Moderate Safety-A

Test Case : 4

Credit Risk Evaluation using Expert System Trading Sector Client Credit Risk Assessment Client Id : C000000002 Application Id : A000000002 Client Name : ABC Pharma Industries Hubli Trading Sector Standard Credit Risk Rating Scores Soft Computed Trading Sector Credit Score is: Excellent :148.40 Out of Standard Score : 150.0 Credit Risk Rating Highest Safety - AAA Management Risk Rating is - Excellent Business Risk Rating is - Excellent Finance Risk Rating is - Excellent

Test Case : 5

Service Sector Credit Rating Assessment Client Id : C000000007 Application Id : A000000007 Client Name : Sanjeevini Nursing Home, Bagalkot 1. Promoters Risk Rating is - Default 2. Existing NursingHome Risk Rating is - Default 3. Proposed NursingHome Risk Rating is - Default 4. Market Potential Risk Rating is - Default 5. Project Costing Risk Rating is - Default 6. Staff Risk Rating is - Default 7. Implementation Risk Rating is - Default 8. Capital Risk Rating is - Default 9. Repayment Risk Rating is - Default Credit Risk Advice The Client Risk Rating is Default, Client Risk Rating is Highest Risk and Client Risk Grade is D

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 20 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Chapter – 7 Result analysis 7.1 Result analysis Researchers have collected the real data (Hiding the Client’s Identity) and

also simulated the about 500 client’s data. These samples are representing

the Manufacturing, Trading and Service sectors. They have tested CREES

system. The results are compared with that of manual system as shown in

Table-9. The Percentage of clients misjudged by the fuzzy tool is

(21/500)*100 = 4.2%. The credit risk decisions taken manually and CREES

system are agreeing to great extent about 95.8% accuracy. Fig-9 shows

graph of comparison of results.

Table – 9 Results of CREES are compared with that of manual system

Fig-9 Graph of comparison of results.

Sl. No Client Risk Level

Manual Decisions

CREES Decisions

Relative Error %

No. of Clients Mis Classified

1 Highest Safety 78 83 6.0 6

2 High Safety 70 73 4.1 3

3 Significant Safety 90 87 -3.4 3

4 Low Risk 91 93 2.1 2

5 High Risk 85 82 -3.6 3

Highest Risk 86 82 -4.8 4 Total 500 500 0.4 21

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 21 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Chapter - 8. Conclusions and Findings

8.1 Conclusions and Findings • Significance of the Credit Risk is realized and given high priority by

regulators and banking , finance and insurance sectors

• There is immense need for Expert System (CREES), as on now all credit

risk decisions of MSME are carried out manually and causes lot of delay

• The methodology Evolutionary Neurofuzzy logic captures the knowledge

of human experts in their domain languages

• CREES Expert system is friendly to Credit Rating Executives and MSME

Users

8.2 Scope for further research 1. Development of Data warehouse of the industry-wise, business-wise

knowledgebase of credit rating frameworks

2. Data mining techniques are needed to explore the hidden knowledge

patterns in the data sets.

3. Testing CREES with international Credit Data sets

8.3 UGC MRP Approval, Funding and Recognition of work Researcher’s had applied for Minor Research Project proposal based on

present research work to University Grant Commission (UGC), New Delhi.

This MRP was approved and funded Rs 1,20,000/- by UGC in Nov.2012

and the work is in progress

8.4 Best Paper of the International Conference Award

The paper presented Expert System Design for MSME Credit Risk Rating

International Conference on Management of MSME - MSMECON-2010 at

Institute of Management Technology (IMT) in Nagpur has been awarded as

Best Paper of Conference with Cash prize of Rs. 10,000/-

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 22 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

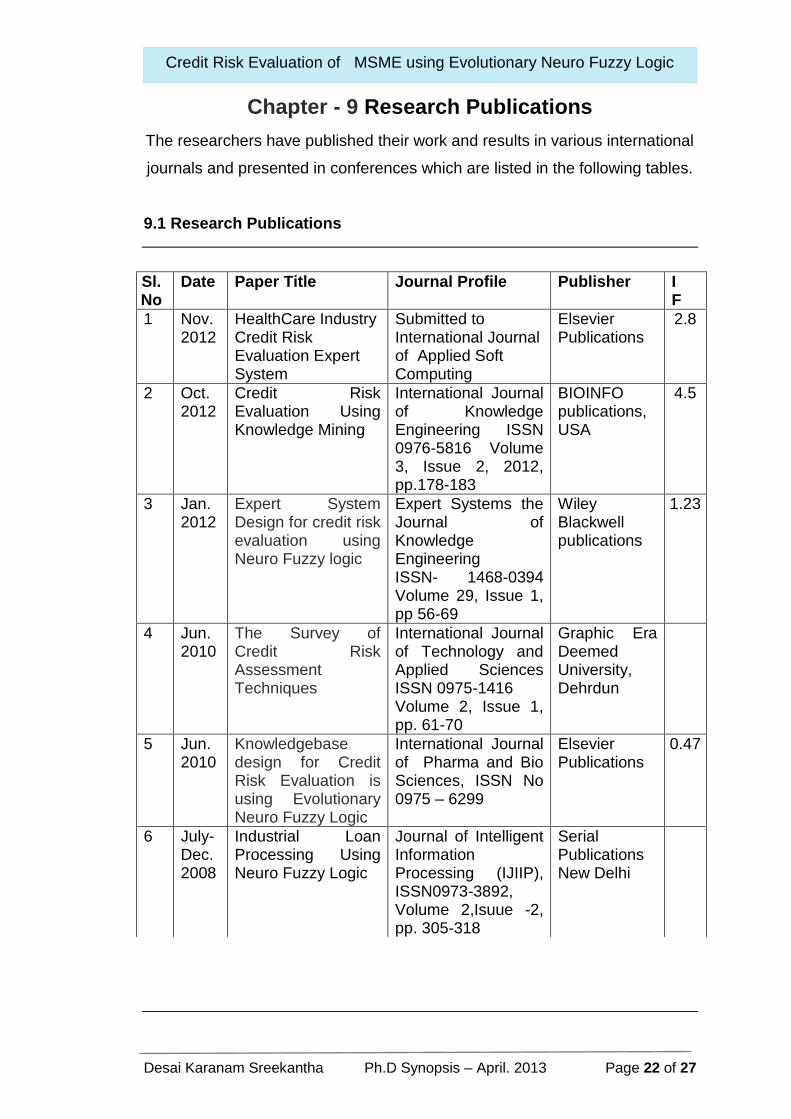

Chapter - 9 Research Publications

The researchers have published their work and results in various international

journals and presented in conferences which are listed in the following tables.

9.1 Research Publications

Sl. No

Date

Paper Title Journal Profile Publisher IF

1 Nov. 2012

HealthCare Industry Credit Risk Evaluation Expert System

Submitted to International Journal of Applied Soft Computing

Elsevier Publications

2.8

2 Oct. 2012

Credit Risk Evaluation Using Knowledge Mining

International Journal of Knowledge Engineering ISSN 0976-5816 Volume 3, Issue 2, 2012, pp.178-183

BIOINFO publications, USA

4.5

3 Jan. 2012

Expert System Design for credit risk evaluation using Neuro Fuzzy logic

Expert Systems the Journal of Knowledge Engineering ISSN- 1468-0394 Volume 29, Issue 1, pp 56-69

Wiley Blackwell publications

1.23

4 Jun. 2010

The Survey of Credit Risk Assessment Techniques

International Journal of Technology and Applied Sciences ISSN 0975-1416 Volume 2, Issue 1, pp. 61-70

Graphic Era Deemed University, Dehrdun

5 Jun. 2010

Knowledgebase design for Credit Risk Evaluation is using Evolutionary Neuro Fuzzy Logic

International Journal of Pharma and Bio Sciences, ISSN No 0975 – 6299

Elsevier Publications

0.47

6 July- Dec. 2008

Industrial Loan Processing Using Neuro Fuzzy Logic

Journal of Intelligent Information Processing (IJIIP), ISSN0973-3892, Volume 2,Isuue -2, pp. 305-318

Serial Publications New Delhi

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 23 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

9.2 Paper presentations in International and National conferences

Sl. No

Period Title of the Paper Presented

Conference Hosted by

1 Jan. 2013

Accepted the paper for presentation Hospitality Industry Credit Risk Evaluation

National Conference on Risk Management in Banking and Insurance and Financial Services

Institute of Public Enterprise, Hyderabad

2 17-18th Feb. 2012

Innovative Credit Risk Management

National Conference on Innovative Management Practices

Banarasdas Chandiwala Institute of Professional Studies, New Delhi

3 10 to 12th March 2011

Knowledgebase design for Credit Risk Evaluation is using Evolutionary Neuro Fuzzy Logic

National Conference in Computational Neuro Science

SIBACA, Lonavala., Maharastra.

4 17th - 18th Sep. 2010.

Expert System Design for MSME Credit Risk Rating

International Conference on Management of MSME-MSMECON-2010

Institute of Management Technology (IMT), in Nagpur

5 2nd – 3rd March 2008

Knowledgebase System Design for Credit Risk Evaluation using Neuro Fuzzy Logic

National Conference on Knowledge Mining

Annamalai University, Chidambaram, Tamilnadu

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 24 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

Chapter - 10 References

10.1 Bibliography

This research work comprises an exhaustive survey of credit risk literature of

text books, websites, credit policy documents, interactions with experts and

study of about 300 most relevant articles on credit risk evaluation from

reputed journals such as IEEE transactions, machine intelligence, business

journals and proceedings of various symposiums some selected articles from

the survey are discussed by way of illustration.

10.2 Text books and documents studied

R.V.Kulkarni and B.L. Desai, Knowledgebased Applications in Banking

Sector, New Delhi, New Century Publications, 2004.

Bart Kosko, Neural Networks and Fuzzy Systems, Prentice Hall of India

Pvt. Ltd, New Delhi Eastern Economy Edition 2000

Stamatios V.Kartalopoulos, Understanding Neural Networks and Fuzzy

Logic, IEEE Press Eastern Economy Edition, 2003

Lending Policy Karnataka State Financial Corporation 2005-2006

C.R.Kothari Research Methodology Methods and Techniques, New Age

International Publishers, 2008.

Programme on Risk Management Canara Bank Staff Training College.

Bangalore.

10.3 Research journal articles

1. Peter, Duchessi and Salvatore Belardo. (July/August 1987). Lending

Analysis Support System (LASS) an application of knowledge based

system to support commercial loan analysis margin credit evaluation

system, IEEE Transactions systems, man on Cybernetics, 17 (4), pp.

608-616.

2. Lyn C.Thomas. (2000). A survey of credit and behavioral scoring:

forecasting financial risk of lending to consumers, International Journal of

Forecasting 16, pp. 149-172, www.elsevier.com/locate/ijforecast.

3. Pang Sulin, Liu Yongqing and Li Rongzhou. (June 28-July 2,2000). The

Optimal Design on The Decision Mechanism of Credit Risk for Banks

With Imperfect Information, Proceedings of The 3 World Congress on

Intelligent Control and Automation, Hefei, P.R. China.

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 25 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

4. Sushmita Mitra and Yoichi Hayashi (2000) Neuro–Fuzzy Rule

Generation: Survey in Soft Computing Framework.

5. Markus Kern / Bernd Rudolph. (January 2001). Comparative Analysis of

Alternative Credit Risk Models – an Application on German Middle

Market- Loan Portfolios, Center for Financial Studies, an der Johann

Wolfgang Goethe-University aunusanlage, 6 D-60329.

6. Frankfurt am Main. Rong Zhouli, Su-Lin Pang, Jian Min Xu. (Nov. 2002).

Neural networks credit risk evaluation model based on back propagation,

Conference on Machine Learning and Cybernatics Beijing.

7. Uwe Schmock Ernst Young. (2003). Performance of Modern Techniques

for Rating Model Design, Master Thesis Master of Advanced Studies in

Finance.

8. Adel Lahsasna. (June 2004). Evaluation of Credit Risk Using

Evolutionary-Fuzzy Logic Scheme No 16, ECB Publications Occasional

paper series.

9. Chorng-Shyong Ong, Jih-JengHuang, Gwo-Hshiung Tzeng. (2005).

Building credit scoring models using genetic programming, Expert

Systems with Applications, pp. 1-7.

10. B.K.Kim and Ram R. Bishu. (2006). Uncertainty of Human error and

Fuzzy approach to Human Reliability Analysis, International journal of

Uncertainty Fuzziness and Knowledge System, 14(1) World Scientific

Publishing Company, pp. 111-129.

11. Yuan Hua, Chen Xiaohong. (2007). Credit Risk Assessment Revisited

Methodological Issues and Practical Implications, working group on risk

assessment, 1-4244-1312-5/07/$25.00.

12. Jozef Zurada. (2007). Rule Induction Methods for Credit Scoring Review

of Business Information Systems, Second Quarter, 11(2) E-mail:

[email protected]), University of Louisville, pp. 11- 22.

13. Viresh Moonasar. (31 May, 2007). Credit Risk Analysis using Artificial

Intelligence: Evidence from a Leading South African Banking Institution

Research Report: Mbl3 presented to the Graduate School of Business

Leadership University of South Africa.

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 26 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

14. Yuansheng Huang, Chengfang Tian. (2008). Research On Credit Risk

Assessment Model of Commercial Banks Based on Fuzzy Probabilistic

Neural Network, The International Conference On Risk Management &

Engineering Management 978-0-7695-3402-2/08 $25.00 © 2008 Ieee,

Doi 0.1109/Icrmem.2008.33.

15. A.Lahsasna, R.N.Ainon, Teh Ying Wah. (May, 2008). Intelligent Credit

Scoring Model using Soft Computing Approach, Proceedings of the

International Conference on Computer and Communication Engineering,

Kuala Lumpur, Malaysia.

16. Wai Chuen Wong, Yao Xiao, Le Lei and Xinjiang Guo. (September,

2008). Research on Credit Risk Evaluation Model Based on LVQ Neural

Network. Proceedings of the IEEE International Conference on

Automation and Logistics Qingdao, China, 978-1-4244-2503-7/08/2008

IEEE.

17. R.V.Kulkarni and Prof.B.L.Desai. Knowledgebase Applications in

Banking.

18. Shorouq Fathi Eletter, Saad Ghaleb Yaseen and Ghaleb Awad Elrefae.

(2010). Neuro-Based Artificial Intelligence Model for Loan Decisions,

American Journal of Economics and Business Administration 2(1), ISSN

1945-5488 © 2010 Science Publications , pp. 27-34.

Desai Karanam Sreekantha Ph.D Synopsis – April. 2013 Page 27 of 27

Credit Risk Evaluation of MSME using Evolutionary Neuro Fuzzy Logic

19. Adel Lahsasna, Raja Noor Ainon and Teh Ying Wah. (April, 2010).

Credit Scoring Models using Soft Computing Methods, The International

Arab Journal of Information technology, 7(2), pp. 115-123.

20. Shaomei Yang. Study on Commercial Banks Credit Risk Based on AGA

and Camel Rating System, Second International Workshop on

Knowledge Discovery and Data Mining.

21. Linda Delamaire. (February 2012). Implementing a credit risk

management system based on innovative scoring techniques, Linda

Delamaire University of commerce and social science department of

economics the University of Birmingham.

22. CreditWeek Special Report. (January 25, 2012). The Global Authority On

Credit Quality Leveraged Debt in 2012, The Markets Are Open, But

Credit Risk Remains Special Report.

(Desai Karanam Sreekantha) (Prof. (Dr.) R.V. Kulkarni)

Date : Professor & Head

SIBER, Kolhapur

Recommended