EY Greater China Consumer Products and Retail Sector Journal

Dec 2017

Eric Chia

PartnerGreater China Consumer Products Sector Co-Leader

Arnold Sun

Partner

Greater China Consumer Products Sector Co-Leader

Dear Friends,

Greetings!

As many of us have already started thinking of yet another “New Year’s resolution”, it’s intriguing to notice that

so many have evolved in the world of Consumer and Retail. For one, consumption upgrade is clearly leading the

way across the year – and it really is happening. The market has just witnessed another record-setting 11-11,

and if we take a closer look at the category winners, it is obvious that many premium merchandises are speeding

up their pace and are already taking the lead as category killers. Another facet is relevant to a hypothetical yet

eminent “Big Bang in Consumerism” in the coming decade – who will emerge victorious among the incumbent big

names? Or may even replace them?

We have been able to share with you two very interesting perspectives in this current issue.

Firstly, Shutin Wah, Senior Manager, Corporate Finance Strategy, Ernst & Young (China) Advisory Limited has

presented a diagnostic of the Chinese restaurant market via his perspective of “Can restaurant investors and

operators still find growth in China?” The market reached RMB 4 trillion in 2016, yet is still growing in the single

digits, and the biggest issues that operators are facing are still scalability and profitability. Will there be room for

further growth, and what can operators do differently than they are currently? Drawing from his extensive

working experience in advising on the restaurant sector in China, Shutin has smoothly depicted a winning

framework: Location, Delivery, Customer Engagement and Innovation. Among the key elements of the

framework are also valuable insights on “where to grow” and a set of key success factors, just to name a few.

Most importantly, despite the not-very-favorable news in the sector starting a few years ago, “There are still

abundant opportunities for local and global operators to find growth, especially when compared to other major

markets globally”.

Secondly, in his article, “Smart Growth, Profitable Growth: Defining Issues for Today”, Ryan Zhou, Advisory

Services Director, Ernst & Young (China) Advisory Ltd has rightly pointed out that many are realizing the

difficulties in sustaining a reasonably favorable margin, as the market moves from “transactional” to

“transformational”, and fortunately there are multiple new alternatives to deal with these issues. Ryan has

articulated an innovative use of the combined approach – Managing Customer Profitability – that is built on

strategy and leverages an inter-related mechanism among process, system, governance and people to make

improved operational performance possible.

Finally, as the holiday season is approaching, I’d like to wish our dear readers a Merry Christmas and a Happy

New Year!

Enjoy reading – and looking forward to your comments.

2EY Greater China Consumer Products and Retail Sector Journal |

Can restaurant investors and operators still find growth in China?

Shutin Wah

Senior Manager, Corporate Finance Strategy

Ernst & Young (China) Advisory Limited

Synopsys: The dining and restaurant sector

is a huge market in China that continues to

grow, but operations have become more

difficult and compression of margins has

been a huge challenge for investors who lack

operational experience. Deep understanding

of target consumers and geographical

market nuances is essential for developing a

successful growth strategy. Four key success

factors include Location, Delivery, Customer

engagement and Innovation. Implementing a

successful strategy could drive growth and

operating margins that are at least 50%

higher than the market average, even for

established operators. This potential for

growth and improvement is critical for the

success or failure of deals in the industry.

4EY Greater China Consumer Products and Retail Sector Journal |

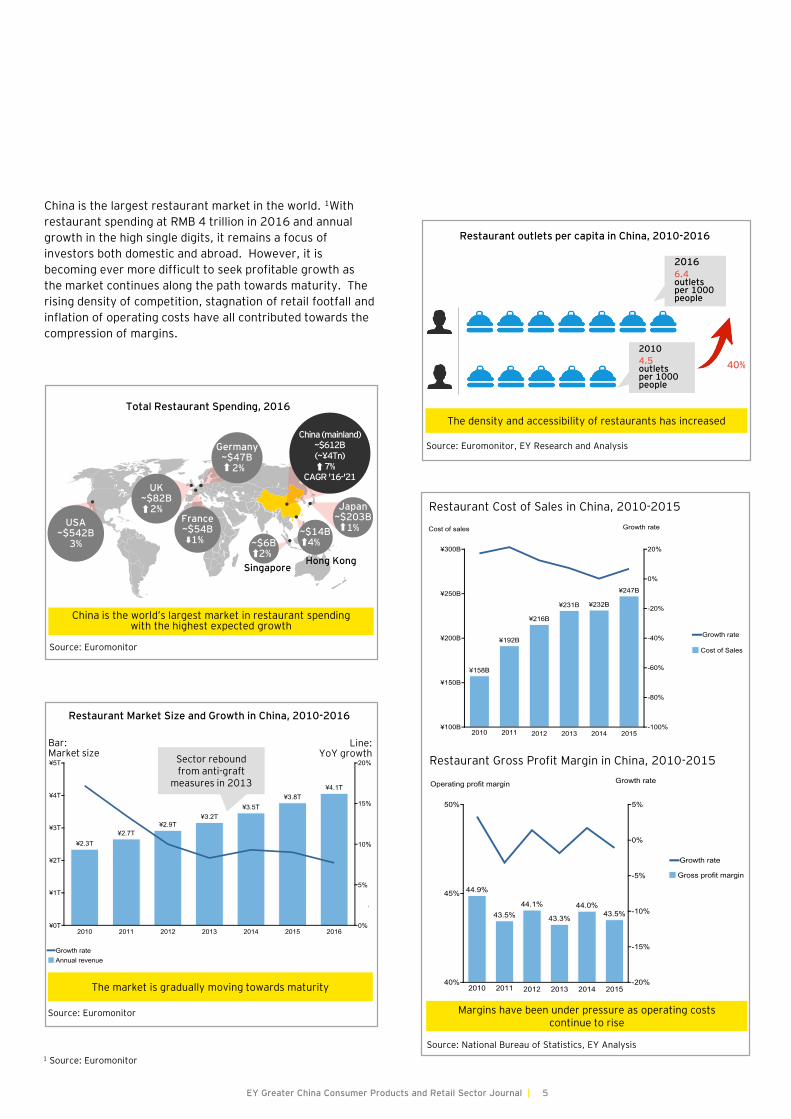

China is the largest restaurant market in the world. 1With

restaurant spending at RMB 4 trillion in 2016 and annual

growth in the high single digits, it remains a focus of

investors both domestic and abroad. However, it is

becoming ever more difficult to seek profitable growth as

the market continues along the path towards maturity. The

rising density of competition, stagnation of retail footfall and

inflation of operating costs have all contributed towards the

compression of margins.

5EY Greater China Consumer Products and Retail Sector Journal |

Source: Euromonitor

Sector rebound from anti-graft

measures in 2013

Restaurant Market Size and Growth in China, 2010-2016

Bar: Market size

Line: YoY growth

The market is gradually moving towards maturity

Source: Euromonitor, EY Research and Analysis

Restaurant outlets per capita in China, 2010-2016

40%

20166.4outlets per 1000 people

2010

4.5outlets per 1000 people

The density and accessibility of restaurants has increased

Source: National Bureau of Statistics, EY-Parthenon Analysis

Margins have been under pressure as operating costs continue to rise

Source: National Bureau of Statistics, EY Analysis

Restaurant Cost of Sales in China, 2010-2015

Restaurant Gross Profit Margin in China, 2010-2015

USA~$542B

3%

Japan~$203B

1%~$14B4%

Hong Kong

~$6B2%

Singapore

France~$54B

1%

UK~$82B

2%

Germany~$47B

2%

Source: Euromonitor

China is the world’s largest market in restaurant spending with the highest expected growth

Total Restaurant Spending, 2016

1 Source: Euromonitor

China (mainland)~$612B(~¥4Tn)

7% CAGR '16-'21

Investors are starting to appreciate the difficulty of running

successful restaurant businesses and have become more

cautious about investing in this sector. The number of deals

has shrunk from around 9 deals per year in 2012 and 2013

to around 5 per year in 2015 and 2016. There has also

been an observed shift from private equity investment

towards acquisitions from strategic buyers, who have the

advantage of operational experience for driving value

creation. This also includes the trend of franchise buy-backs

(particularly among global brands of cafe and fast food

chains) in an attempt to improve operations and brand

control in China.

1. Location

► Many restaurants have focused on opening new stores

to scale-up and drive top-line growth. However, this is

often at the expense of margins, especially when there

is a distraction from simultaneously driving same-store

sales growth

► With the rapid urbanization and expansion of

commercial real estate across all city tiers, the dilution

of customer traffic supports the rationale for a larger

number of smaller-sized outlets. Operators may run the

risk of building overly large stores if they fail to adjust

their expansion plans to include a rigorous analysis of

site traffic potential

► There are also considerable differences in the scale and

nature of market opportunities across geographies.

Operators need to be aware of macro-and behavioral

trends that are distinctive across geographic segments.

For example, a comparison between South, North and

East China:

► South China has a faster-growing and younger

population

► There is also a higher density of restaurants in the

South, which implies more competition, and is more

conducive for food delivery

► There are differences in dining preferences (flavor,

taste, cuisine type and price range). The South has

had greater preference for non-western and fine

dining, while the East has favored western casual

dining. The North shows generally slower growth,

with niche concepts and boutique restaurants faring

well.

► In addition to city selection, the optimization of store

network by location also needs to be reviewed from a

new lens. Some traditional hubs such as hypermarkets

and department stores are no longer generating traffic

like before, while theme-based locations (such as malls

that offer a full range of entertainment options, or

those with child and family themes) are gaining

popularity as consumers seek more purpose to their day

out. The prevalence of online shopping and food

delivery has already altered the needs, expectations and

behaviors for how consumers spend their time beyond

basic shopping and dining

6EY Greater China Consumer Products and Retail Sector Journal |

Source: Merger market, EY Research and Analysis

By investor type By cuisine concept

Trends in restaurant sector deals, China(2012/2013 vs. 2015/2016)

Restaurant operators have become more active in

making investments, while PEs have been shying away

Investors have become more interested in non-Chinese casual dining

concepts

Through our work advising restaurant operators in China and

around the world, we have observed four key drivers of

success that can make the difference for profitable growth:

location, delivery, customer engagement and innovation.

2. Delivery

► The rise of Third-Party Delivery Platforms (3PPs) since

2014 has disrupted consumers’ dining habits, as they

now have access to a much wider range of cuisines from

the comfort of their home or workplace. 3PPs have also

been welcomed by many restaurants as they help bring

incremental orders and drive up revenue without the

need for significant capital investment.

► Furthermore, 3PPs have evolved to become a major

marketing channel for restaurants to build localized

brand awareness.

► While this has led to quick growth for restaurants and has

been a key driver of revenue growth in the past 3 years,

the profitability of such delivery orders via 3PPs has

deteriorated as the platforms have started to adjust their

pricing models. Gross margins on delivery orders could

be over 10% points lower than that for dine-in. It has

become more important than ever for operators to

further analyze the overall economics and strategic value

of engaging 3PPs.

► The economic advantage of engaging a 3PP generally

diminishes with the number of orders, and many delivery-

focused restaurants have chosen to build an in-house

delivery team, especially in that it also enables them to

have better control of delivery time and quality. At an

average cost of between RMB 5 and RMB 10 charged by

3PPs per order, restaurant outlets that deliver over 30 to

50 orders per day should investigate the economics of

building an in-house team.

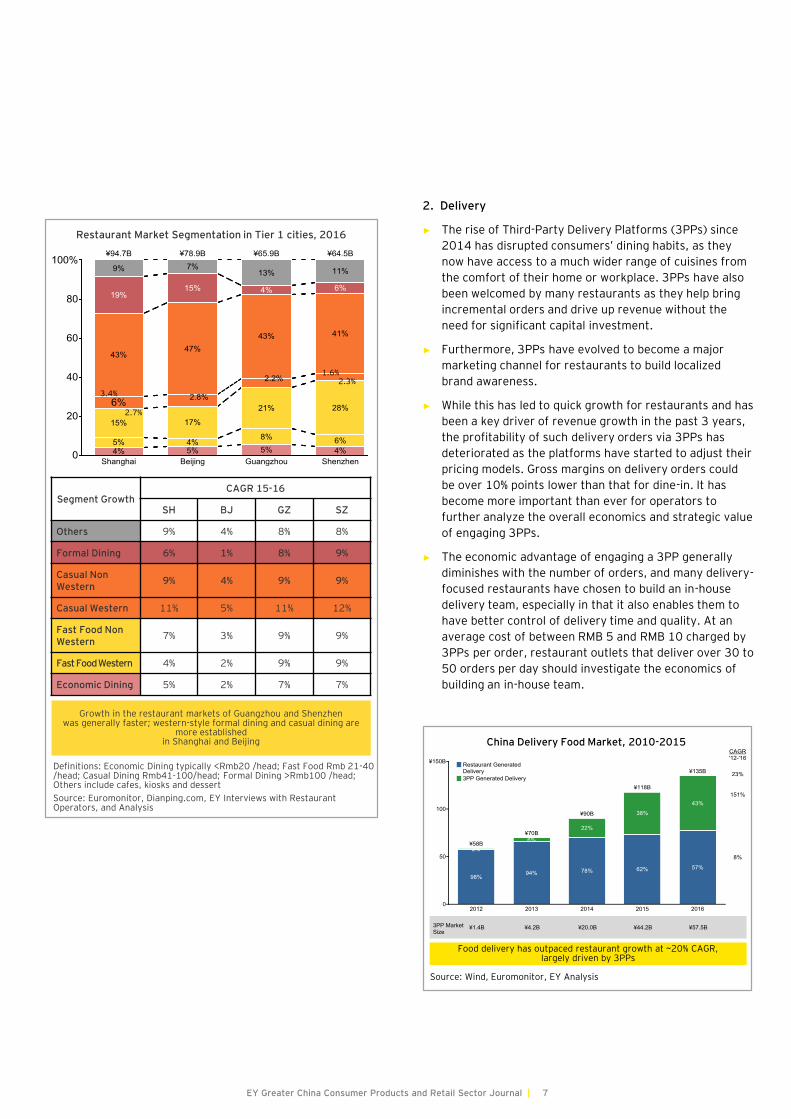

7EY Greater China Consumer Products and Retail Sector Journal |

Definitions: Economic Dining typically <Rmb20 /head; Fast Food Rmb 21-40 /head; Casual Dining Rmb41-100/head; Formal Dining >Rmb100 /head; Others include cafes, kiosks and dessert

Source: Euromonitor, Dianping.com, EY Interviews with Restaurant Operators, and Analysis

Segment GrowthCAGR 15-16

SH BJ GZ SZ

Others 9% 4% 8% 8%

Formal Dining 6% 1% 8% 9%

Casual NonWestern

9% 4% 9% 9%

Casual Western 11% 5% 11% 12%

Fast Food NonWestern

7% 3% 9% 9%

FastFood Western 4% 2% 9% 9%

Economic Dining 5% 2% 7% 7%

Restaurant Market Segmentation in Tier 1 cities, 2016

3.4%

2.7%

1.6%2.3%

Growth in the restaurant markets of Guangzhou and Shenzhen was generally faster; western-style formal dining and casual dining are

more established in Shanghai and Beijing

Source: Wind, Euromonitor, EY Analysis

China Delivery Food Market, 2010-2015

Food delivery has outpaced restaurant growth at ~20% CAGR, largely driven by 3PPs

Hotpot chainChinese dining

groupChinese dining

group

2013

Revenue RMB 19 Billion RMB 14 Billion RMB 9 Billion

Operating margin

9.8% 0.4% 5.5%

2016

Revenue (& 13-16 CAGR)

RMB 28 Billion ( 13% CAGR)

RMB 20 Billion ( 13% CAGR)

RMB 12 Billion ( 11% CAGR)

Operatingmargin (& 13-16 increment)

17.2% ( 7.4% increment)

3.0%( 2.6% increment)

12.2%( 6.7% increment)

Location

Delivery

Customer engagement

Innovation

Highlights

1. Continued aggressive store expansion while maintaining a fast / casual positioning

2. Built in-house delivery team in 2015; redesigned delivery menu and proposition (leveraging store network)

3. Refined store decor in 2016

1. Embarked on turn-around strategy since 2013, including rationalization of stores

2. Created new concepts and menu for casualdining and with family friendly themes

3. Introduced productized items for home-cooking

1. Refocused on the casual dining segment to diversify customer base and brought in new concepts from overseas

2. Cautiously expanded store network for only concepts with proven success

3. Collaborated with 3PPs to drive delivery revenue

3. Customer engagement

► Understanding consumers and capturing market trends is

critical to staying relevant. Key trends observed in China

include:

► A generation of consumers that are urban, pressed

for time and digitally savvy

► The pursuit of healthy food and lifestyles

► Valuing authentic flavors, origins and brand stories

► Family themes fare well as children are the center of

Chinese families; and

► Consumer appreciation of personalized services and

willingness to pay for experiences

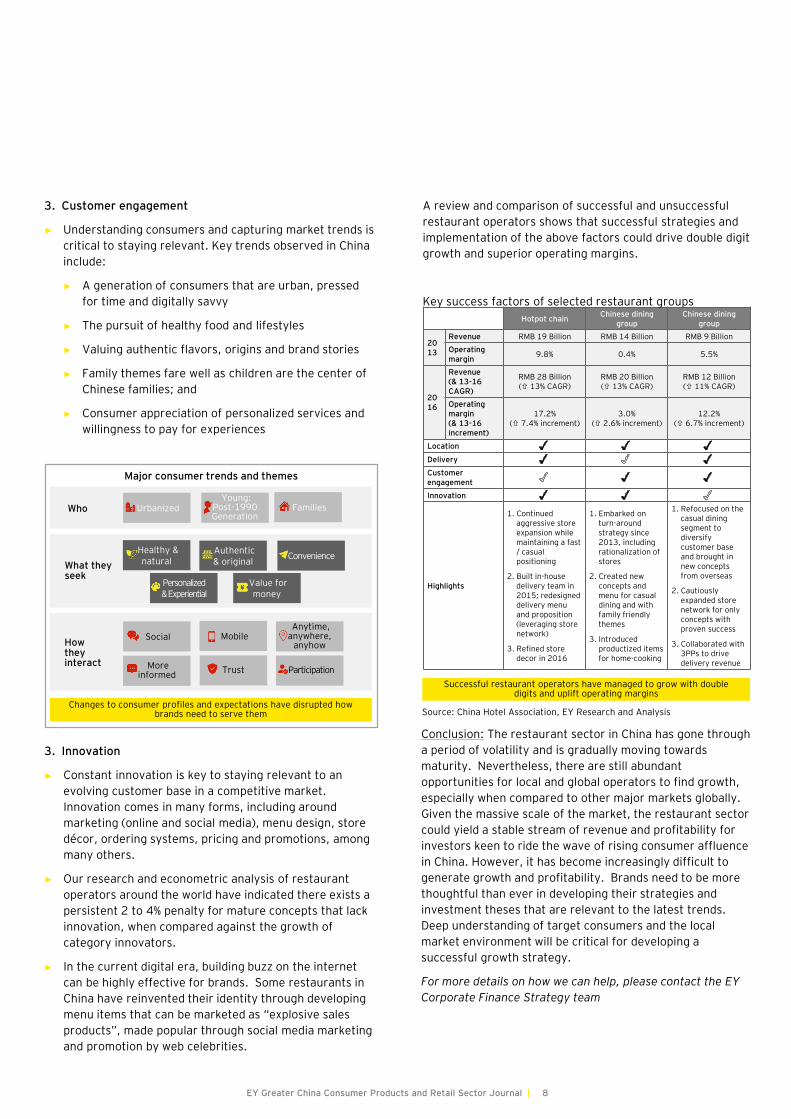

A review and comparison of successful and unsuccessful

restaurant operators shows that successful strategies and

implementation of the above factors could drive double digit

growth and superior operating margins.

Key success factors of selected restaurant groups

8EY Greater China Consumer Products and Retail Sector Journal |

Who

What they seek

How they interact

Major consumer trends and themes

Changes to consumer profiles and expectations have disrupted how brands need to serve them

UrbanizedYoung:

Post-1990 Generation

Families

Social MobileAnytime,

anywhere, anyhow

More informed

Trust Participation

Healthy & natural

Authentic & original

Convenience

Personalized & Experiential

Value for money

3. Innovation

► Constant innovation is key to staying relevant to an

evolving customer base in a competitive market.

Innovation comes in many forms, including around

marketing (online and social media), menu design, store

dé cor, ordering systems, pricing and promotions, among

many others.

► Our research and econometric analysis of restaurant

operators around the world have indicated there exists a

persistent 2 to 4% penalty for mature concepts that lack

innovation, when compared against the growth of

category innovators.

► In the current digital era, building buzz on the internet

can be highly effective for brands. Some restaurants in

China have reinvented their identity through developing

menu items that can be marketed as “explosive sales

products”, made popular through social media marketing

and promotion by web celebrities.

Conclusion: The restaurant sector in China has gone through

a period of volatility and is gradually moving towards

maturity. Nevertheless, there are still abundant

opportunities for local and global operators to find growth,

especially when compared to other major markets globally.

Given the massive scale of the market, the restaurant sector

could yield a stable stream of revenue and profitability for

investors keen to ride the wave of rising consumer affluence

in China. However, it has become increasingly difficult to

generate growth and profitability. Brands need to be more

thoughtful than ever in developing their strategies and

investment theses that are relevant to the latest trends.

Deep understanding of target consumers and the local

market environment will be critical for developing a

successful growth strategy.

For more details on how we can help, please contact the EY

Corporate Finance Strategy team

Source: China Hotel Association, EY Research and Analysis

Successful restaurant operators have managed to grow with double digits and uplift operating margins

Smart growth, profitable

growth: defining issues for

today

Ryan Zhou

Director, Advisory Services

Ernst & Young (China) Advisory Limited

Overview

The consumer product and retail market is

experiencing a transformational era. A

recent EY survey of consumer products

executives globally found:

1) 75% believe it is now much more difficult

to sustain profitable growth

2) 75% believe traditional methods of value

creation are increasingly being disrupted;

and

3) 68% believe fueling growth requires

significant changes to business

operations and differentiated strategies

and capabilities

10EY Greater China Consumer Products and Retail Sector Journal |

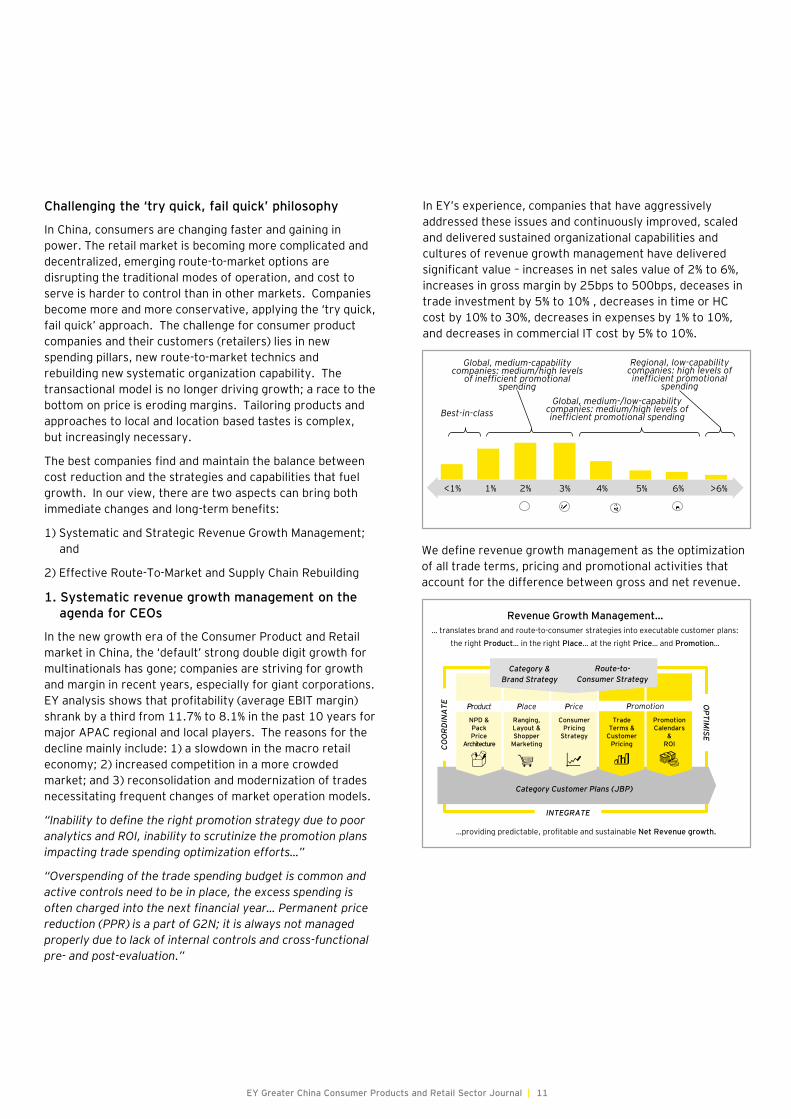

Challenging the ‘try quick, fail quick’ philosophy

In China, consumers are changing faster and gaining in

power. The retail market is becoming more complicated and

decentralized, emerging route-to-market options are

disrupting the traditional modes of operation, and cost to

serve is harder to control than in other markets. Companies

become more and more conservative, applying the ‘try quick,

fail quick’ approach. The challenge for consumer product

companies and their customers (retailers) lies in new

spending pillars, new route-to-market technics and

rebuilding new systematic organization capability. The

transactional model is no longer driving growth; a race to the

bottom on price is eroding margins. Tailoring products and

approaches to local and location based tastes is complex,

but increasingly necessary.

The best companies find and maintain the balance between

cost reduction and the strategies and capabilities that fuel

growth. In our view, there are two aspects can bring both

immediate changes and long-term benefits:

1) Systematic and Strategic Revenue Growth Management;

and

2) Effective Route-To-Market and Supply Chain Rebuilding

1. Systematic revenue growth management on the agenda for CEOs

In the new growth era of the Consumer Product and Retail

market in China, the ‘default’ strong double digit growth for

multinationals has gone; companies are striving for growth

and margin in recent years, especially for giant corporations.

EY analysis shows that profitability (average EBIT margin)

shrank by a third from 11.7% to 8.1% in the past 10 years for

major APAC regional and local players. The reasons for the

decline mainly include: 1) a slowdown in the macro retail

economy; 2) increased competition in a more crowded

market; and 3) reconsolidation and modernization of trades

necessitating frequent changes of market operation models.

“Inability to define the right promotion strategy due to poor

analytics and ROI, inability to scrutinize the promotion plans

impacting trade spending optimization efforts…”

“Overspending of the trade spending budget is common and

active controls need to be in place, the excess spending is

often charged into the next financial year… Permanent price

reduction (PPR) is a part of G2N; it is always not managed

properly due to lack of internal controls and cross-functional

pre- and post-evaluation.”

In EY’s experience, companies that have aggressively

addressed these issues and continuously improved, scaled

and delivered sustained organizational capabilities and

cultures of revenue growth management have delivered

significant value – increases in net sales value of 2% to 6%,

increases in gross margin by 25bps to 500bps, deceases in

trade investment by 5% to 10% , decreases in time or HC

cost by 10% to 30%, decreases in expenses by 1% to 10%,

and decreases in commercial IT cost by 5% to 10%.

We define revenue growth management as the optimization

of all trade terms, pricing and promotional activities that

account for the difference between gross and net revenue.

11EY Greater China Consumer Products and Retail Sector Journal |

INTEGRATE

Ranging, Layout & Shopper

Marketing

Trade Terms &

Customer Pricing

Promotion Calendars

&ROI

Category Customer Plans (JBP)

Consumer Pricing

Strategy

NPD & PackPrice

Architecture

Category &

Brand Strategy

Route-to-

Consumer Strategy

the right Product… in the right Place… at the right Price… and Promotion…

…providing predictable, profitable and sustainable Net Revenue growth.

… translates brand and route-to-consumer strategies into executable customer plans:

Revenue Growth Management…

Product Place Price Promotion

OP

TIM

ISE

CO

OR

DIN

AT

E

6%4%3%1% 2% 5% >6%<1%

Regional, low-capability companies: high levels of inefficient promotional

spending

Global, medium-/low-capability companies: medium/high levels of inefficient promotional spending

Global, medium-capability companies: medium/high levels

of inefficient promotional spending

Best-in-class

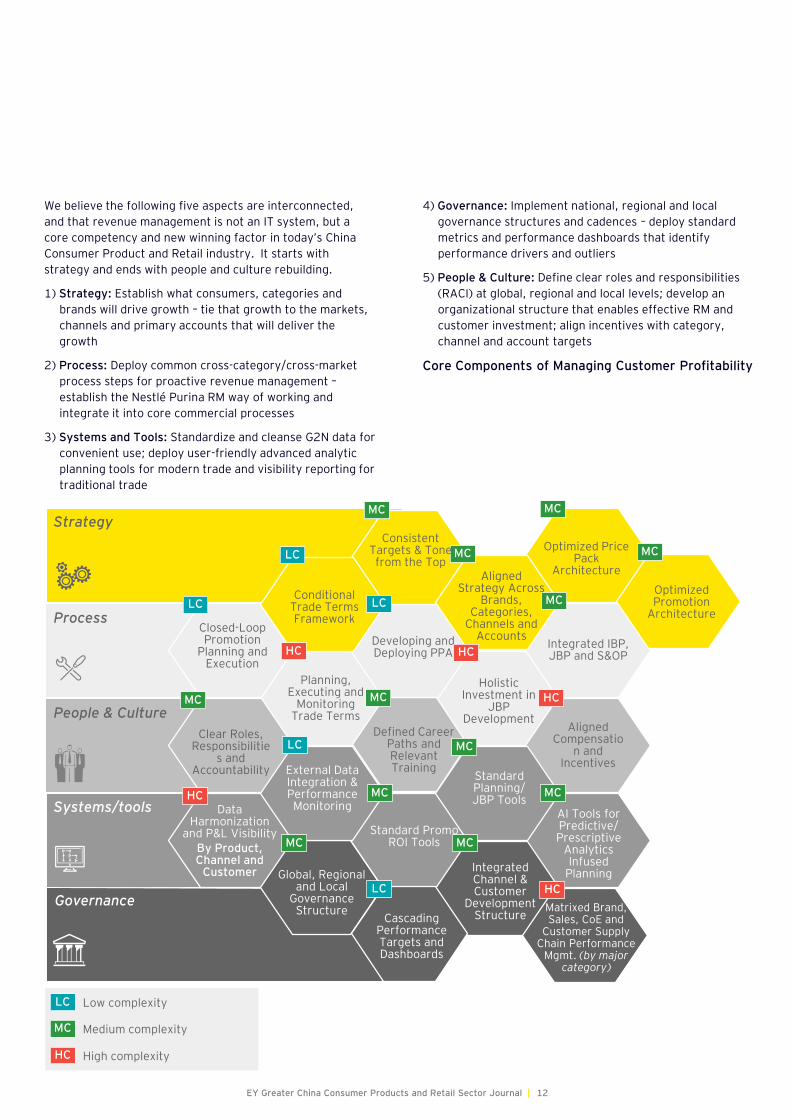

We believe the following five aspects are interconnected,

and that revenue management is not an IT system, but a

core competency and new winning factor in today’s China

Consumer Product and Retail industry. It starts with

strategy and ends with people and culture rebuilding.

1) Strategy: Establish what consumers, categories and

brands will drive growth – tie that growth to the markets,

channels and primary accounts that will deliver the

growth

2) Process: Deploy common cross-category/cross-market

process steps for proactive revenue management –

establish the Nestlé Purina RM way of working and

integrate it into core commercial processes

3) Systems and Tools: Standardize and cleanse G2N data for

convenient use; deploy user-friendly advanced analytic

planning tools for modern trade and visibility reporting for

traditional trade

4) Governance: Implement national, regional and local

governance structures and cadences – deploy standard

metrics and performance dashboards that identify

performance drivers and outliers

5) People & Culture: Define clear roles and responsibilities

(RACI) at global, regional and local levels; develop an

organizational structure that enables effective RM and

customer investment; align incentives with category,

channel and account targets

Core Components of Managing Customer Profitability

Aligned Compensatio

n and Incentives

Integrated IBP, JBP and S&OP

Low complexityLC

MC

HC High complexity

Medium complexity

Process

People & Culture

Strategy

Systems/tools

Governance

Data Harmonization

and P&L VisibilityBy Product, Channel and

Customer

Closed-LoopPromotion

Planning and Execution

Developing and Deploying PPA

Standard Planning/JBP Tools

Standard Promo ROI Tools

AI Tools forPredictive/Prescriptive

Analytics Infused

PlanningIntegratedChannel & Customer

DevelopmentStructure Cascading

Performance Targets and Dashboards

Matrixed Brand, Sales, CoE and

Customer Supply Chain Performance

Mgmt. (by major category)

Planning, Executing and

MonitoringTrade Terms

AlignedStrategy Across

Brands, Categories,

Channels and Accounts

LC

LC LC

LC

LC

MC

MC

MC

MC

MC

MC

MC

MC

MC

MC

MC

MC

HC

HC

HC

HC

HC

Conditional Trade Terms Framework

Clear Roles, Responsibilitie

s and Accountability External Data

Integration & Performance Monitoring

Global, Regional and Local

Governance Structure

Consistent Targets & Tone from the Top

Defined Career Paths and RelevantTraining

Holistic Investment in

JBP Development

Optimized Price Pack

Architecture

OptimizedPromotion

Architecture

12EY Greater China Consumer Products and Retail Sector Journal |

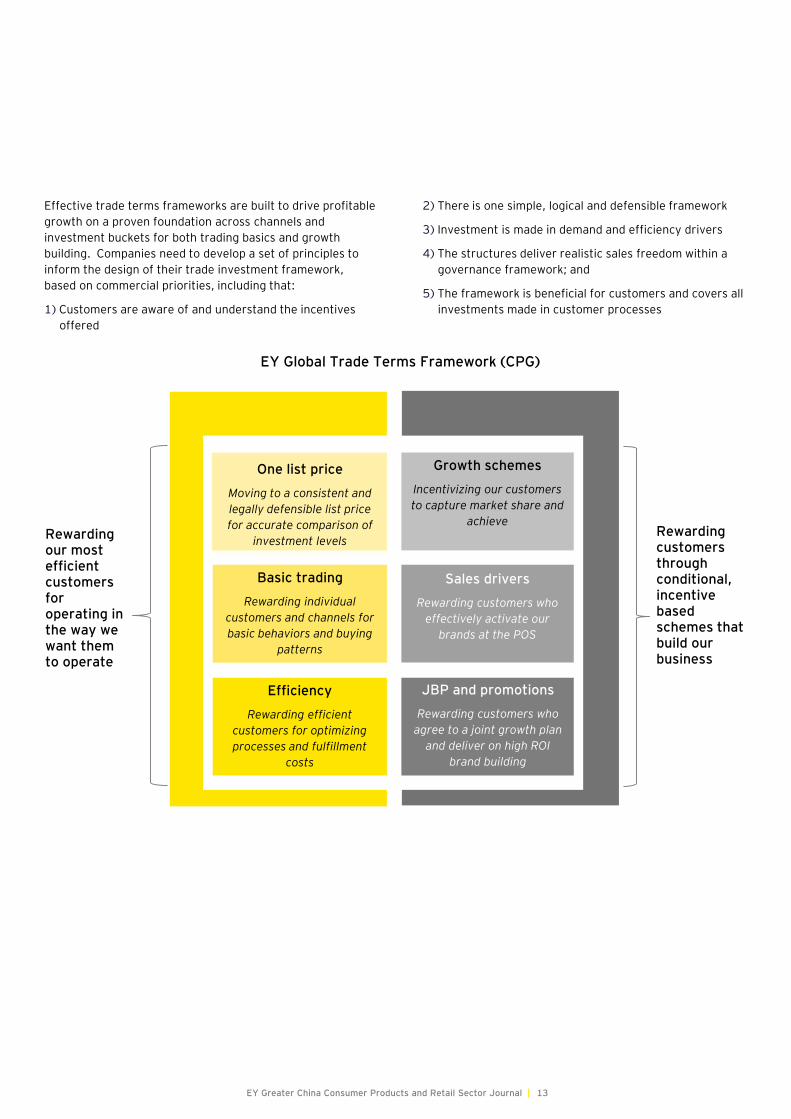

Effective trade terms frameworks are built to drive profitable

growth on a proven foundation across channels and

investment buckets for both trading basics and growth

building. Companies need to develop a set of principles to

inform the design of their trade investment framework,

based on commercial priorities, including that:

1) Customers are aware of and understand the incentives

offered

2) There is one simple, logical and defensible framework

3) Investment is made in demand and efficiency drivers

4) The structures deliver realistic sales freedom within a

governance framework; and

5) The framework is beneficial for customers and covers all

investments made in customer processes

Efficiency

Rewarding efficient

customers for optimizing

processes and fulfillment

costs

Growth schemes

Incentivizing our customers

to capture market share and

achieve

EY Global Trade Terms Framework (CPG)

Rewarding customers through conditional, incentive based schemes that build our business

Rewarding our most efficient customers for operating in the way we want them to operate

Basic trading

Rewarding individual

customers and channels for

basic behaviors and buying

patterns

One list price

Moving to a consistent and

legally defensible list price

for accurate comparison of

investment levels

Sales drivers

Rewarding customers who

effectively activate our

brands at the POS

JBP and promotions

Rewarding customers who

agree to a joint growth plan

and deliver on high ROI

brand building

13EY Greater China Consumer Products and Retail Sector Journal |

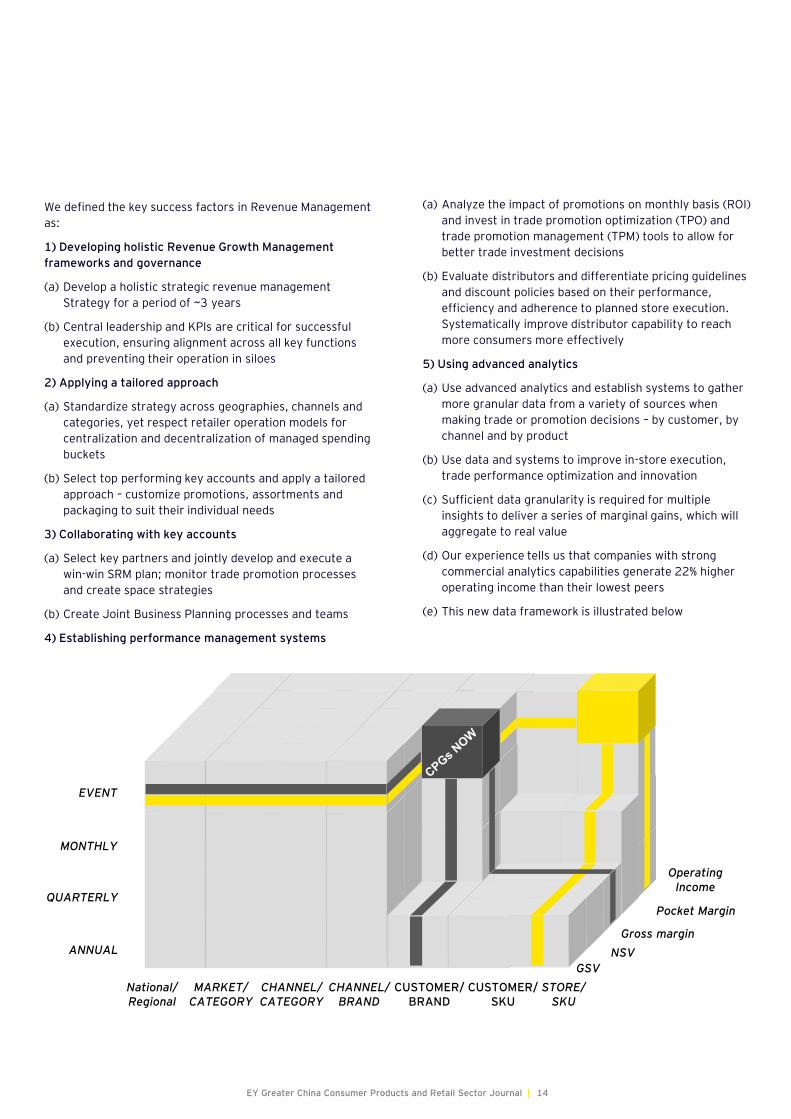

We defined the key success factors in Revenue Management

as:

1) Developing holistic Revenue Growth Management

frameworks and governance

(a) Develop a holistic strategic revenue management

Strategy for a period of ~3 years

(b) Central leadership and KPIs are critical for successful

execution, ensuring alignment across all key functions

and preventing their operation in siloes

2) Applying a tailored approach

(a) Standardize strategy across geographies, channels and

categories, yet respect retailer operation models for

centralization and decentralization of managed spending

buckets

(b) Select top performing key accounts and apply a tailored

approach – customize promotions, assortments and

packaging to suit their individual needs

3) Collaborating with key accounts

(a) Select key partners and jointly develop and execute a

win-win SRM plan; monitor trade promotion processes

and create space strategies

(b) Create Joint Business Planning processes and teams

4) Establishing performance management systems

(a) Analyze the impact of promotions on monthly basis (ROI)

and invest in trade promotion optimization (TPO) and

trade promotion management (TPM) tools to allow for

better trade investment decisions

(b) Evaluate distributors and differentiate pricing guidelines

and discount policies based on their performance,

efficiency and adherence to planned store execution.

Systematically improve distributor capability to reach

more consumers more effectively

5) Using advanced analytics

(a) Use advanced analytics and establish systems to gather

more granular data from a variety of sources when

making trade or promotion decisions – by customer, by

channel and by product

(b) Use data and systems to improve in-store execution,

trade performance optimization and innovation

(c) Sufficient data granularity is required for multiple

insights to deliver a series of marginal gains, which will

aggregate to real value

(d) Our experience tells us that companies with strong

commercial analytics capabilities generate 22% higher

operating income than their lowest peers

(e) This new data framework is illustrated below

14EY Greater China Consumer Products and Retail Sector Journal |

EVENT

MONTHLY

QUARTERLY

ANNUAL

National/ Regional

CHANNEL/CATEGORY

CHANNEL/BRAND

CUSTOMER/BRAND

MARKET/CATEGORY

CUSTOMER/SKU

STORE/SKU

NSV

Pocket Margin

Operating Income

GSV

Gross margin

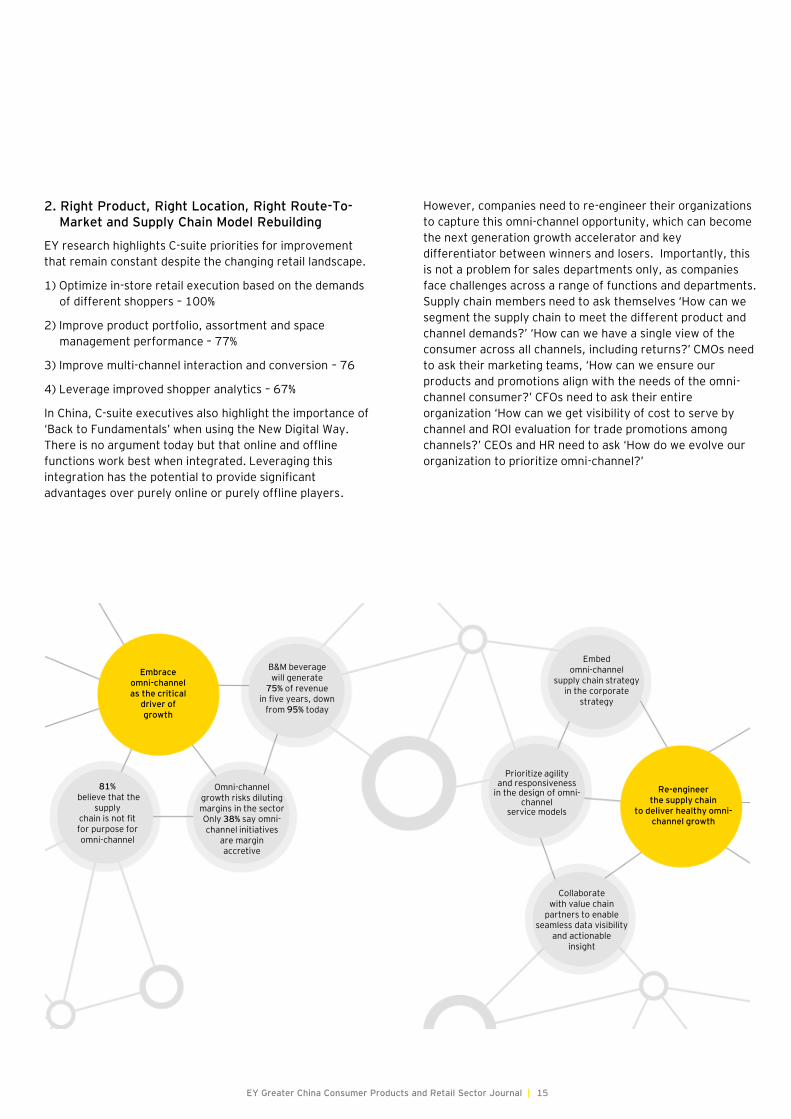

2. Right Product, Right Location, Right Route-To-Market and Supply Chain Model Rebuilding

EY research highlights C-suite priorities for improvement

that remain constant despite the changing retail landscape.

1) Optimize in-store retail execution based on the demands

of different shoppers – 100%

2) Improve product portfolio, assortment and space

management performance – 77%

3) Improve multi-channel interaction and conversion – 76

4) Leverage improved shopper analytics – 67%

In China, C-suite executives also highlight the importance of

‘Back to Fundamentals’ when using the New Digital Way.

There is no argument today but that online and offline

functions work best when integrated. Leveraging this

integration has the potential to provide significant

advantages over purely online or purely offline players.

However, companies need to re-engineer their organizations

to capture this omni-channel opportunity, which can become

the next generation growth accelerator and key

differentiator between winners and losers. Importantly, this

is not a problem for sales departments only, as companies

face challenges across a range of functions and departments.

Supply chain members need to ask themselves ‘How can we

segment the supply chain to meet the different product and

channel demands?’ ‘How can we have a single view of the

consumer across all channels, including returns?’ CMOs need

to ask their marketing teams, ‘How can we ensure our

products and promotions align with the needs of the omni-

channel consumer?’ CFOs need to ask their entire

organization ‘How can we get visibility of cost to serve by

channel and ROI evaluation for trade promotions among

channels?’ CEOs and HR need to ask ‘How do we evolve our

organization to prioritize omni-channel?’

EY Greater China Consumer Products and Retail Sector Journal |

Embrace omni-channel as the critical

driver of growth

B&M beveragewill generate

75% of revenue in five years, down

from 95% today

Omni-channel growth risks diluting margins in the sector Only 38% say omni-channel initiatives

are margin accretive

81%believe that the

supply chain is not fit for purpose for omni-channel

Re-engineer the supply chain

to deliver healthy omni-channel growth

Embed omni-channel

supply chain strategy in the corporate

strategy

Prioritize agility and responsiveness

in the design of omni-channel

service models

Collaborate with value chain

partners to enableseamless data visibility

and actionable insight

15

There are two key foundations needed to embrace an

omni-channel strategy – location based market and

consumer segmentation, and digital route to market

rebuilding. Due to the availability of big data in China, we

are more capable than ever of having a clear picture of who

our consumers are, what their habits are, what product

assortment is most suitable for them and what promotion

methods attract them. As a result, product portfolio,

EY Greater China Consumer Products and Retail Sector Journal |

► Age of residence

► Habits of residence

► Females 18-25

People Demographic

►Active traffic time

►Number of outlets

►Number of outlets is repeated

►Number of outlets

►Number of bus stations

►Number of outdoor billboards

►Number of outlets

► Express delivery

►Number of households with kids

High-end neighborhood

Mass-Medium Shopping Mall

Residence demographic

Point of interest of surrounding infrastructure

High-end Commercial BuildingPeople Demographic

School Zone

assortment and space management need to be connected

with consumers or shoppers according to specific

geographical locations, rather than the traditional way of

channel by market. The key challenge today is how to

rebuild organizations to make different functions work

seamlessly and collaboratively.

16

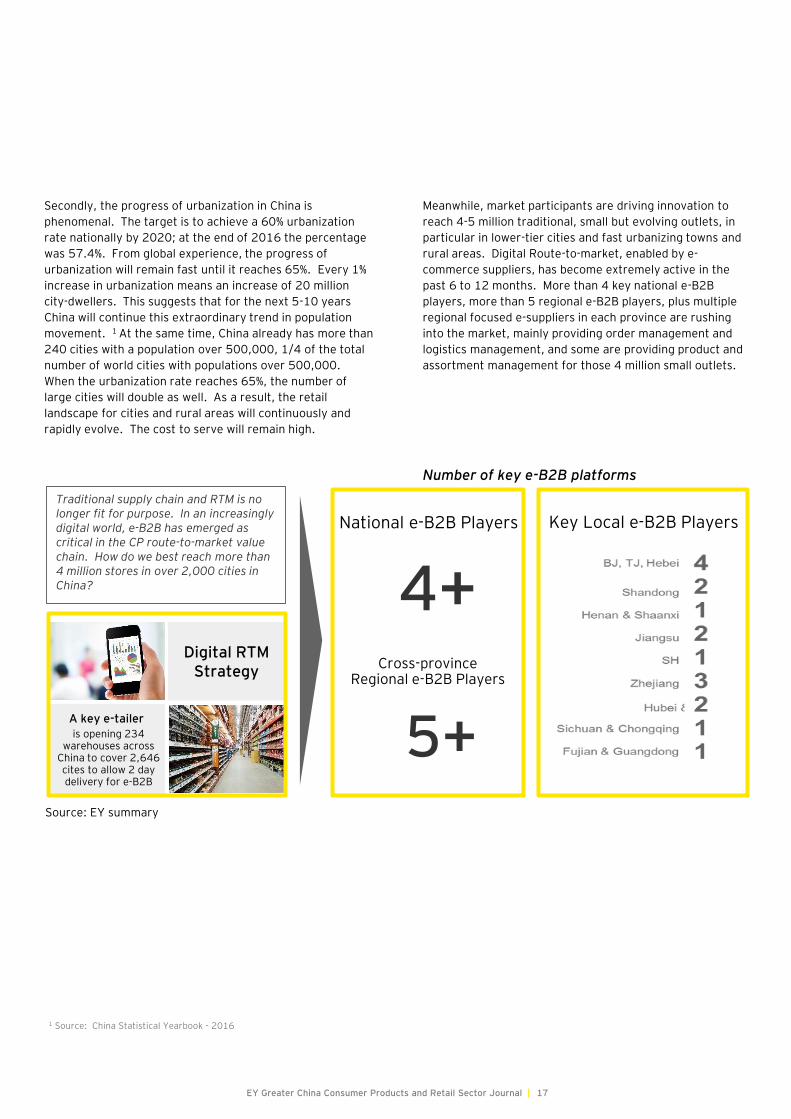

Secondly, the progress of urbanization in China is

phenomenal. The target is to achieve a 60% urbanization

rate nationally by 2020; at the end of 2016 the percentage

was 57.4%. From global experience, the progress of

urbanization will remain fast until it reaches 65%. Every 1%

increase in urbanization means an increase of 20 million

city-dwellers. This suggests that for the next 5-10 years

China will continue this extraordinary trend in population

movement. 1 At the same time, China already has more than

240 cities with a population over 500,000, 1/4 of the total

number of world cities with populations over 500,000.

When the urbanization rate reaches 65%, the number of

large cities will double as well. As a result, the retail

landscape for cities and rural areas will continuously and

rapidly evolve. The cost to serve will remain high.

Meanwhile, market participants are driving innovation to

reach 4-5 million traditional, small but evolving outlets, in

particular in lower-tier cities and fast urbanizing towns and

rural areas. Digital Route-to-market, enabled by e-

commerce suppliers, has become extremely active in the

past 6 to 12 months. More than 4 key national e-B2B

players, more than 5 regional e-B2B players, plus multiple

regional focused e-suppliers in each province are rushing

into the market, mainly providing order management and

logistics management, and some are providing product and

assortment management for those 4 million small outlets.

is opening 234warehouses across

China to cover 2,646 cites to allow 2 day delivery for e-B2B

A key e-tailer

Digital RTM Strategy

Traditional supply chain and RTM is no longer fit for purpose. In an increasingly digital world, e-B2B has emerged as critical in the CP route-to-market value chain. How do we best reach more than 4 million stores in over 2,000 cities in China?

Key Local e-B2B PlayersNational e-B2B Players

4+

5+

Cross-province Regional e-B2B Players

Number of key e-B2B platforms

Source: EY summary

17EY Greater China Consumer Products and Retail Sector Journal |

1 Source: China Statistical Yearbook - 2016

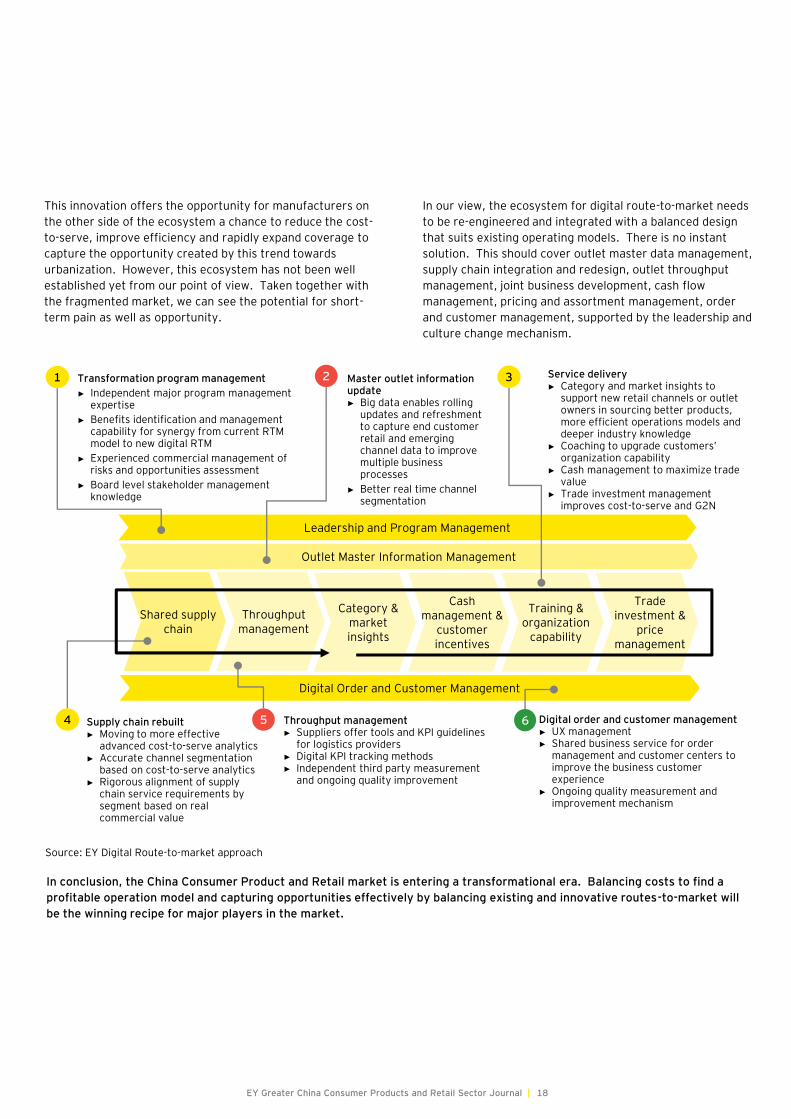

This innovation offers the opportunity for manufacturers on

the other side of the ecosystem a chance to reduce the cost-

to-serve, improve efficiency and rapidly expand coverage to

capture the opportunity created by this trend towards

urbanization. However, this ecosystem has not been well

established yet from our point of view. Taken together with

the fragmented market, we can see the potential for short-

term pain as well as opportunity.

In our view, the ecosystem for digital route-to-market needs

to be re-engineered and integrated with a balanced design

that suits existing operating models. There is no instant

solution. This should cover outlet master data management,

supply chain integration and redesign, outlet throughput

management, joint business development, cash flow

management, pricing and assortment management, order

and customer management, supported by the leadership and

culture change mechanism.

18EY Greater China Consumer Products and Retail Sector Journal |

Supply chain rebuilt ► Moving to more effective

advanced cost-to-serve analytics► Accurate channel segmentation

based on cost-to-serve analytics► Rigorous alignment of supply

chain service requirements by segment based on real commercial value

1 2

4 6

Leadership and Program Management

Throughput management

Shared supply chain

Category & market insights

Cash management &

customer incentives

Training & organization

capability

Trade investment &

price management

Digital Order and Customer Management

Outlet Master Information Management

Transformation program management

► Independent major program management expertise

► Benefits identification and management capability for synergy from current RTM model to new digital RTM

► Experienced commercial management of risks and opportunities assessment

► Board level stakeholder management knowledge

Master outlet information update ► Big data enables rolling

updates and refreshment to capture end customer retail and emerging channel data to improvemultiple business processes

► Better real time channel segmentation

Throughput management► Suppliers offer tools and KPI guidelines

for logistics providers ► Digital KPI tracking methods► Independent third party measurement

and ongoing quality improvement

5 Digital order and customer management ► UX management ► Shared business service for order

management and customer centers to improve the business customer experience

► Ongoing quality measurement and improvement mechanism

3 Service delivery► Category and market insights to

support new retail channels or outlet owners in sourcing better products, more efficient operations models and deeper industry knowledge

► Coaching to upgrade customers’ organization capability

► Cash management to maximize trade value

► Trade investment management improves cost-to-serve and G2N

Source: EY Digital Route-to-market approach

In conclusion, the China Consumer Product and Retail market is entering a transformational era. Balancing costs to find a

profitable operation model and capturing opportunities effectively by balancing existing and innovative routes-to-market will

be the winning recipe for major players in the market.

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2017 Ernst & Young (China) Advisory LimitedAll Rights Reserved.

APAC no. 03005854ED None.

This material has been prepared for general informational purposes only

and is not intended to be relied upon as accounting, tax or other

professional advice. Please refer to your advisors for specific advice.

ey.com/china

Follow us on WeChatScan the QR code and stay up to date with the latest EY news.

Contact us

Eric Chia

Partner

Advisory Services

Ernst & Young (China) Advisory Ltd

+ 86 21 2228 3388

Alfred Yin

Partner

Assurance Services

Ernst & Young Hua Ming LLP

+ 86 21 2228 2152

Arnold Sun

Partner

Transaction Services

Ernst & Young (China) Advisory Ltd

+ 86 21 2228 5235

Audrie Xia

Partner

Tax Services

Ernst & Young (China) Advisory Ltd

+ 86 21 2228 2886

Recommended