UNIVERSIDAD NACIONAL DE PIURA

FACULTAD DE ECONOMIA

DPTO. ACAD. DE ECONOMIA

SOLUCIÓN DEL EXAMEN PARCIAL DE ECONOMETRIA II

1º El investigador especifica el siguiente modelo:

���� � �� � ���� � ������� � � �� � ����� � ��

��� � �� � ����� � ���� � � �� � ���

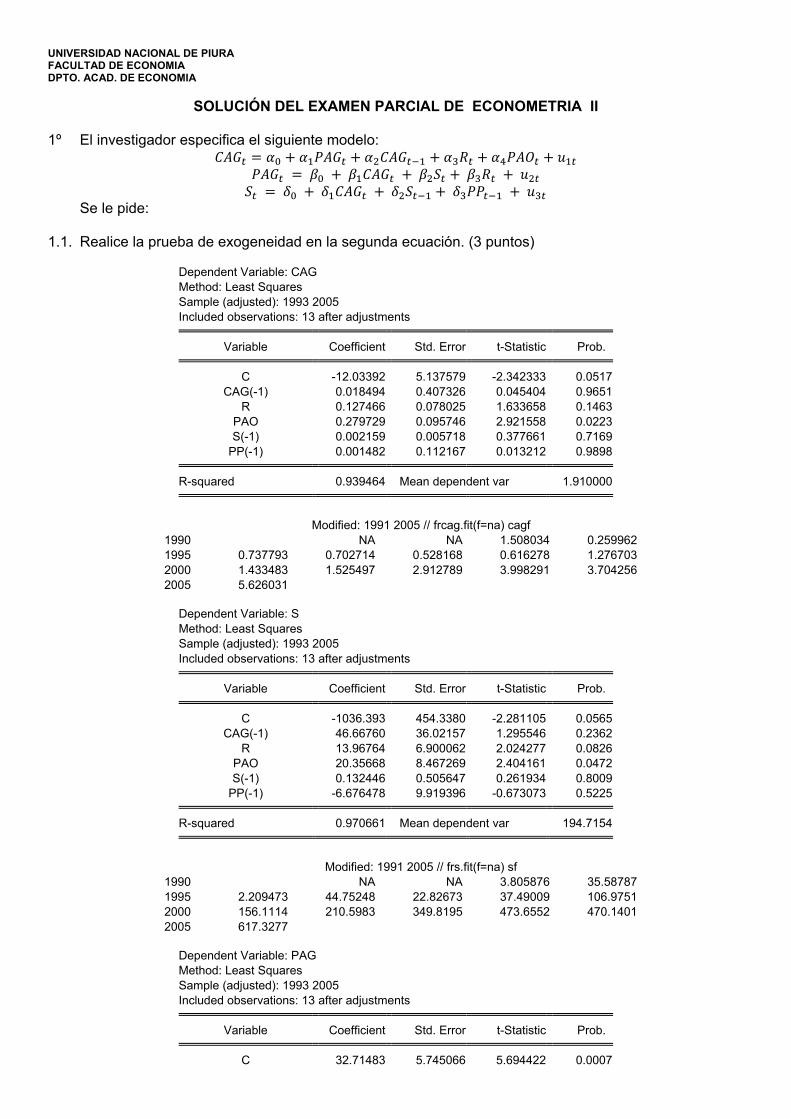

�� � �� � ����� � ����� � � �� � � � Se le pide: 1.1. Realice la prueba de exogeneidad en la segunda ecuación. (3 puntos)

Dependent Variable: CAG

Method: Least Squares

Sample (adjusted): 1993 2005

Included observations: 13 after adjustments Variable Coefficient Std. Error t-Statistic Prob. C -12.03392 5.137579 -2.342333 0.0517

CAG(-1) 0.018494 0.407326 0.045404 0.9651

R 0.127466 0.078025 1.633658 0.1463

PAO 0.279729 0.095746 2.921558 0.0223

S(-1) 0.002159 0.005718 0.377661 0.7169

PP(-1) 0.001482 0.112167 0.013212 0.9898 R-squared 0.939464 Mean dependent var 1.910000

Modified: 1991 2005 // frcag.fit(f=na) cagf

1990 NA NA 1.508034 0.259962

1995 0.737793 0.702714 0.528168 0.616278 1.276703

2000 1.433483 1.525497 2.912789 3.998291 3.704256

2005 5.626031

Dependent Variable: S

Method: Least Squares

Sample (adjusted): 1993 2005

Included observations: 13 after adjustments Variable Coefficient Std. Error t-Statistic Prob. C -1036.393 454.3380 -2.281105 0.0565

CAG(-1) 46.66760 36.02157 1.295546 0.2362

R 13.96764 6.900062 2.024277 0.0826

PAO 20.35668 8.467269 2.404161 0.0472

S(-1) 0.132446 0.505647 0.261934 0.8009

PP(-1) -6.676478 9.919396 -0.673073 0.5225 R-squared 0.970661 Mean dependent var 194.7154

Modified: 1991 2005 // frs.fit(f=na) sf

1990 NA NA 3.805876 35.58787

1995 2.209473 44.75248 22.82673 37.49009 106.9751

2000 156.1114 210.5983 349.8195 473.6552 470.1401

2005 617.3277

Dependent Variable: PAG

Method: Least Squares

Sample (adjusted): 1993 2005

Included observations: 13 after adjustments Variable Coefficient Std. Error t-Statistic Prob. C 32.71483 5.745066 5.694422 0.0007

2

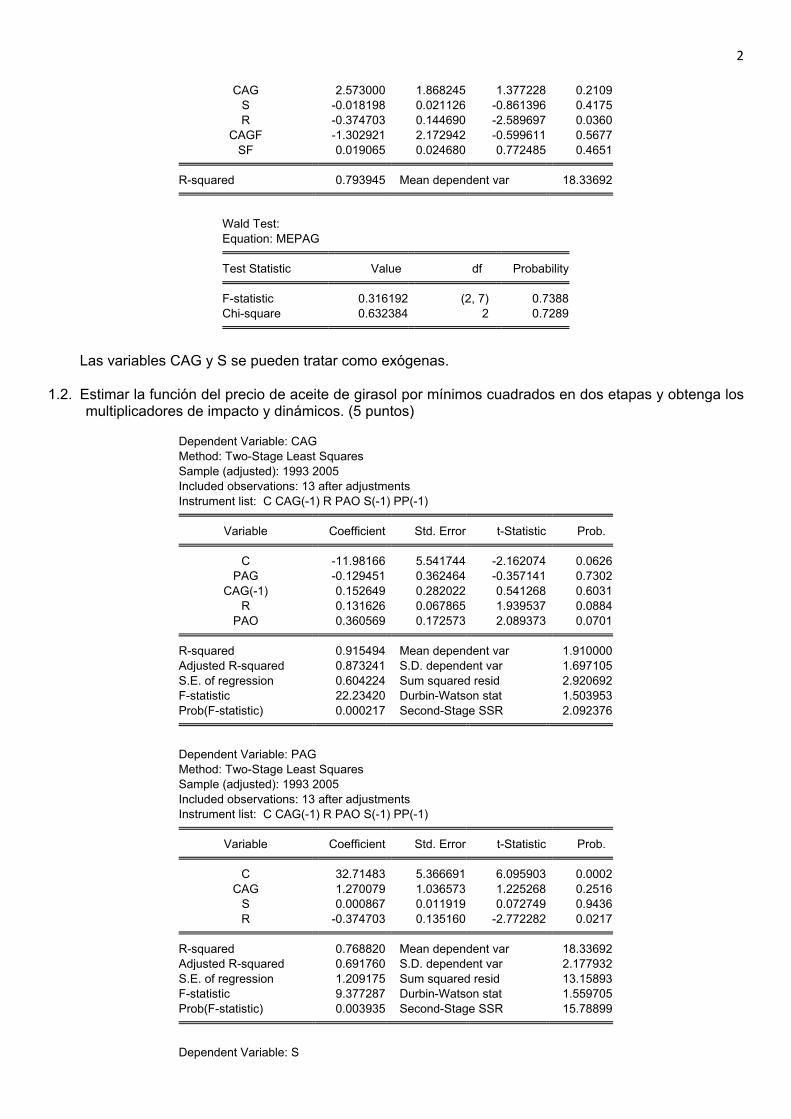

CAG 2.573000 1.868245 1.377228 0.2109

S -0.018198 0.021126 -0.861396 0.4175

R -0.374703 0.144690 -2.589697 0.0360

CAGF -1.302921 2.172942 -0.599611 0.5677

SF 0.019065 0.024680 0.772485 0.4651 R-squared 0.793945 Mean dependent var 18.33692

Wald Test:

Equation: MEPAG Test Statistic Value df Probability F-statistic 0.316192 (2, 7) 0.7388

Chi-square 0.632384 2 0.7289

Las variables CAG y S se pueden tratar como exógenas. 1.2. Estimar la función del precio de aceite de girasol por mínimos cuadrados en dos etapas y obtenga los

multiplicadores de impacto y dinámicos. (5 puntos)

Dependent Variable: CAG

Method: Two-Stage Least Squares

Sample (adjusted): 1993 2005

Included observations: 13 after adjustments

Instrument list: C CAG(-1) R PAO S(-1) PP(-1) Variable Coefficient Std. Error t-Statistic Prob. C -11.98166 5.541744 -2.162074 0.0626

PAG -0.129451 0.362464 -0.357141 0.7302

CAG(-1) 0.152649 0.282022 0.541268 0.6031

R 0.131626 0.067865 1.939537 0.0884

PAO 0.360569 0.172573 2.089373 0.0701 R-squared 0.915494 Mean dependent var 1.910000

Adjusted R-squared 0.873241 S.D. dependent var 1.697105

S.E. of regression 0.604224 Sum squared resid 2.920692

F-statistic 22.23420 Durbin-Watson stat 1.503953

Prob(F-statistic) 0.000217 Second-Stage SSR 2.092376

Dependent Variable: PAG

Method: Two-Stage Least Squares

Sample (adjusted): 1993 2005

Included observations: 13 after adjustments

Instrument list: C CAG(-1) R PAO S(-1) PP(-1) Variable Coefficient Std. Error t-Statistic Prob. C 32.71483 5.366691 6.095903 0.0002

CAG 1.270079 1.036573 1.225268 0.2516

S 0.000867 0.011919 0.072749 0.9436

R -0.374703 0.135160 -2.772282 0.0217 R-squared 0.768820 Mean dependent var 18.33692

Adjusted R-squared 0.691760 S.D. dependent var 2.177932

S.E. of regression 1.209175 Sum squared resid 13.15893

F-statistic 9.377287 Durbin-Watson stat 1.559705

Prob(F-statistic) 0.003935 Second-Stage SSR 15.78899

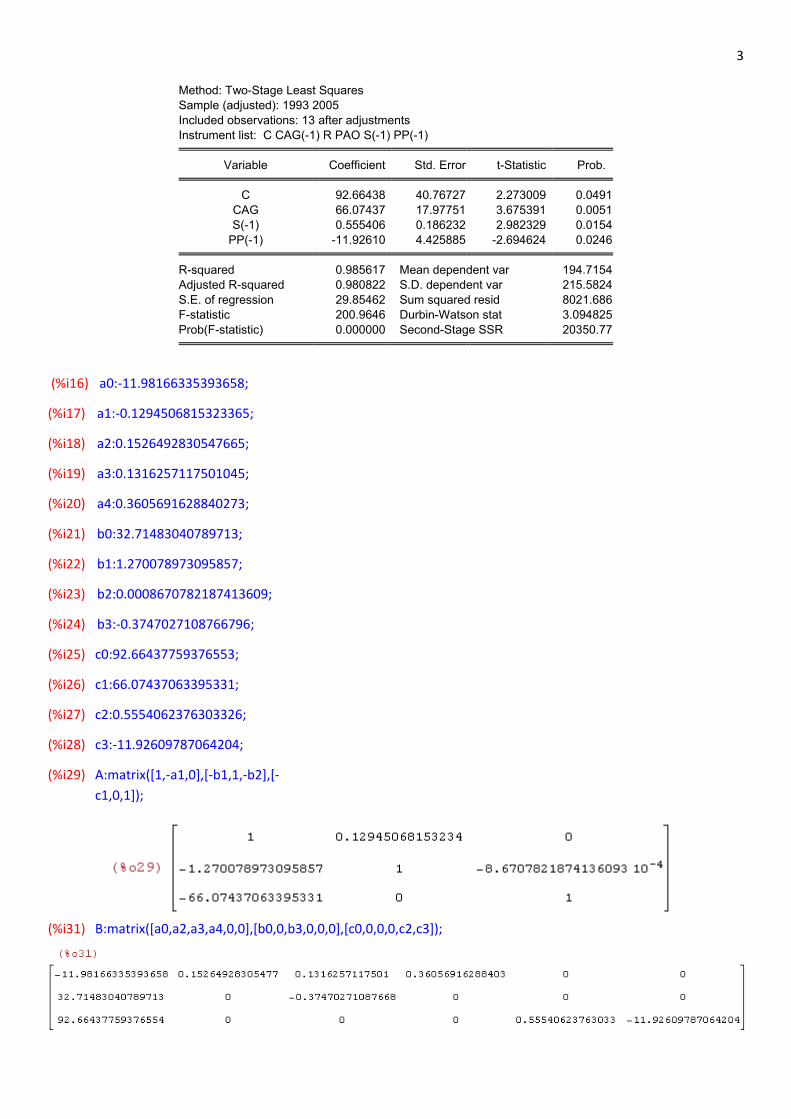

Dependent Variable: S

3

Method: Two-Stage Least Squares

Sample (adjusted): 1993 2005

Included observations: 13 after adjustments

Instrument list: C CAG(-1) R PAO S(-1) PP(-1) Variable Coefficient Std. Error t-Statistic Prob. C 92.66438 40.76727 2.273009 0.0491

CAG 66.07437 17.97751 3.675391 0.0051

S(-1) 0.555406 0.186232 2.982329 0.0154

PP(-1) -11.92610 4.425885 -2.694624 0.0246 R-squared 0.985617 Mean dependent var 194.7154

Adjusted R-squared 0.980822 S.D. dependent var 215.5824

S.E. of regression 29.85462 Sum squared resid 8021.686

F-statistic 200.9646 Durbin-Watson stat 3.094825

Prob(F-statistic) 0.000000 Second-Stage SSR 20350.77

(%i16) a0:-11.98166335393658;

(%i17) a1:-0.1294506815323365;

(%i18) a2:0.1526492830547665;

(%i19) a3:0.1316257117501045;

(%i20) a4:0.3605691628840273;

(%i21) b0:32.71483040789713;

(%i22) b1:1.270078973095857;

(%i23) b2:0.0008670782187413609;

(%i24) b3:-0.3747027108766796;

(%i25) c0:92.66437759376553;

(%i26) c1:66.07437063395331;

(%i27) c2:0.5554062376303326;

(%i28) c3:-11.92609787064204;

(%i29) A:matrix([1,-a1,0],[-b1,1,-b2],[-

c1,0,1]);

(%i31) B:matrix([a0,a2,a3,a4,0,0],[b0,0,b3,0,0,0],[c0,0,0,0,c2,c3]);

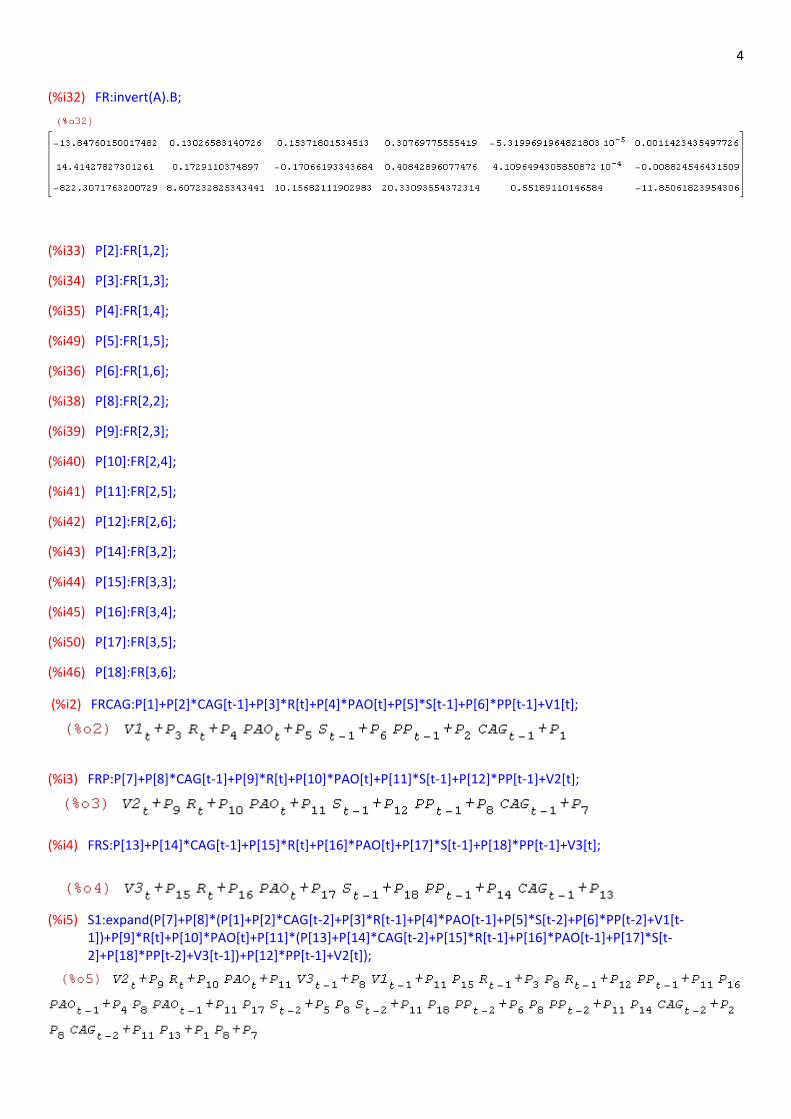

4

(%i32) FR:invert(A).B;

(%i33) P[2]:FR[1,2];

(%i34) P[3]:FR[1,3];

(%i35) P[4]:FR[1,4];

(%i49) P[5]:FR[1,5];

(%i36) P[6]:FR[1,6];

(%i38) P[8]:FR[2,2];

(%i39) P[9]:FR[2,3];

(%i40) P[10]:FR[2,4];

(%i41) P[11]:FR[2,5];

(%i42) P[12]:FR[2,6];

(%i43) P[14]:FR[3,2];

(%i44) P[15]:FR[3,3];

(%i45) P[16]:FR[3,4];

(%i50) P[17]:FR[3,5];

(%i46) P[18]:FR[3,6];

(%i2) FRCAG:P[1]+P[2]*CAG[t-1]+P[3]*R[t]+P[4]*PAO[t]+P[5]*S[t-1]+P[6]*PP[t-1]+V1[t];

(%i3) FRP:P[7]+P[8]*CAG[t-1]+P[9]*R[t]+P[10]*PAO[t]+P[11]*S[t-1]+P[12]*PP[t-1]+V2[t];

(%i4) FRS:P[13]+P[14]*CAG[t-1]+P[15]*R[t]+P[16]*PAO[t]+P[17]*S[t-1]+P[18]*PP[t-1]+V3[t];

(%i5) S1:expand(P[7]+P[8]*(P[1]+P[2]*CAG[t-2]+P[3]*R[t-1]+P[4]*PAO[t-1]+P[5]*S[t-2]+P[6]*PP[t-2]+V1[t-

1])+P[9]*R[t]+P[10]*PAO[t]+P[11]*(P[13]+P[14]*CAG[t-2]+P[15]*R[t-1]+P[16]*PAO[t-1]+P[17]*S[t-

2]+P[18]*PP[t-2]+V3[t-1])+P[12]*PP[t-1]+V2[t]);

5

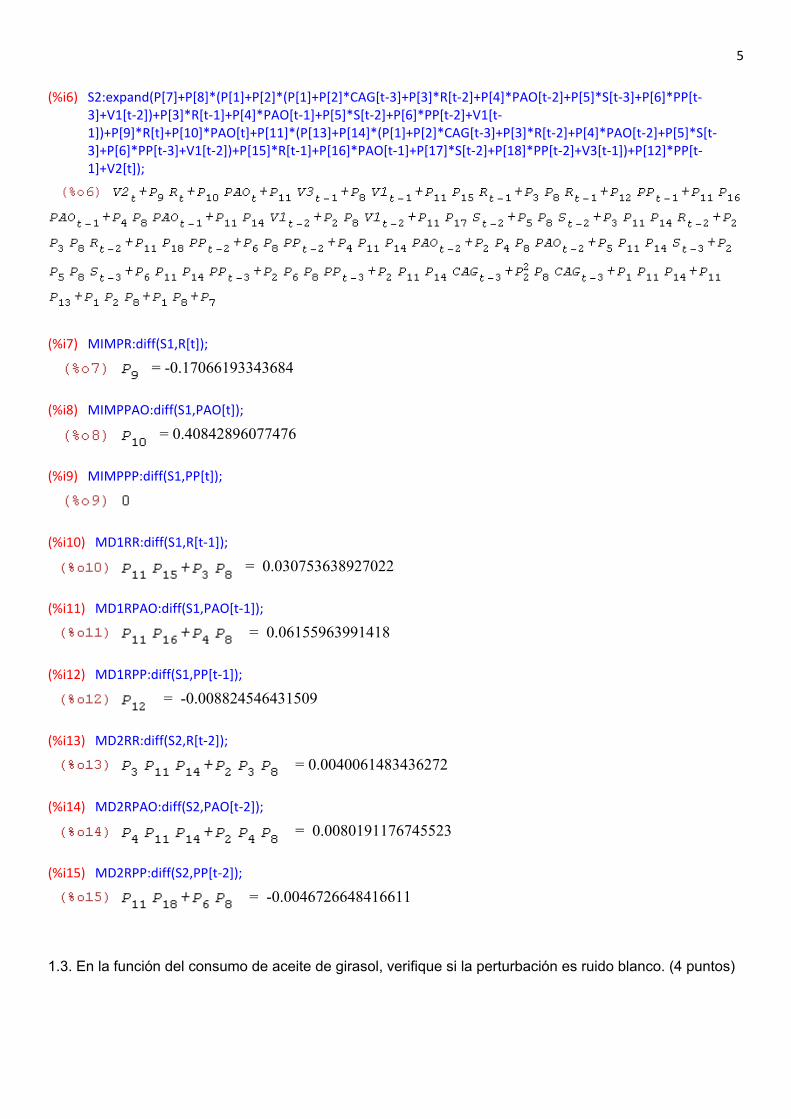

(%i6) S2:expand(P[7]+P[8]*(P[1]+P[2]*(P[1]+P[2]*CAG[t-3]+P[3]*R[t-2]+P[4]*PAO[t-2]+P[5]*S[t-3]+P[6]*PP[t-

3]+V1[t-2])+P[3]*R[t-1]+P[4]*PAO[t-1]+P[5]*S[t-2]+P[6]*PP[t-2]+V1[t-

1])+P[9]*R[t]+P[10]*PAO[t]+P[11]*(P[13]+P[14]*(P[1]+P[2]*CAG[t-3]+P[3]*R[t-2]+P[4]*PAO[t-2]+P[5]*S[t-

3]+P[6]*PP[t-3]+V1[t-2])+P[15]*R[t-1]+P[16]*PAO[t-1]+P[17]*S[t-2]+P[18]*PP[t-2]+V3[t-1])+P[12]*PP[t-

1]+V2[t]);

(%i7) MIMPR:diff(S1,R[t]);

= -0.17066193343684

(%i8) MIMPPAO:diff(S1,PAO[t]);

= 0.40842896077476

(%i9) MIMPPP:diff(S1,PP[t]);

(%i10) MD1RR:diff(S1,R[t-1]);

= 0.030753638927022

(%i11) MD1RPAO:diff(S1,PAO[t-1]);

= 0.06155963991418

(%i12) MD1RPP:diff(S1,PP[t-1]);

= -0.008824546431509

(%i13) MD2RR:diff(S2,R[t-2]);

= 0.0040061483436272

(%i14) MD2RPAO:diff(S2,PAO[t-2]);

= 0.0080191176745523

(%i15) MD2RPP:diff(S2,PP[t-2]);

= -0.0046726648416611

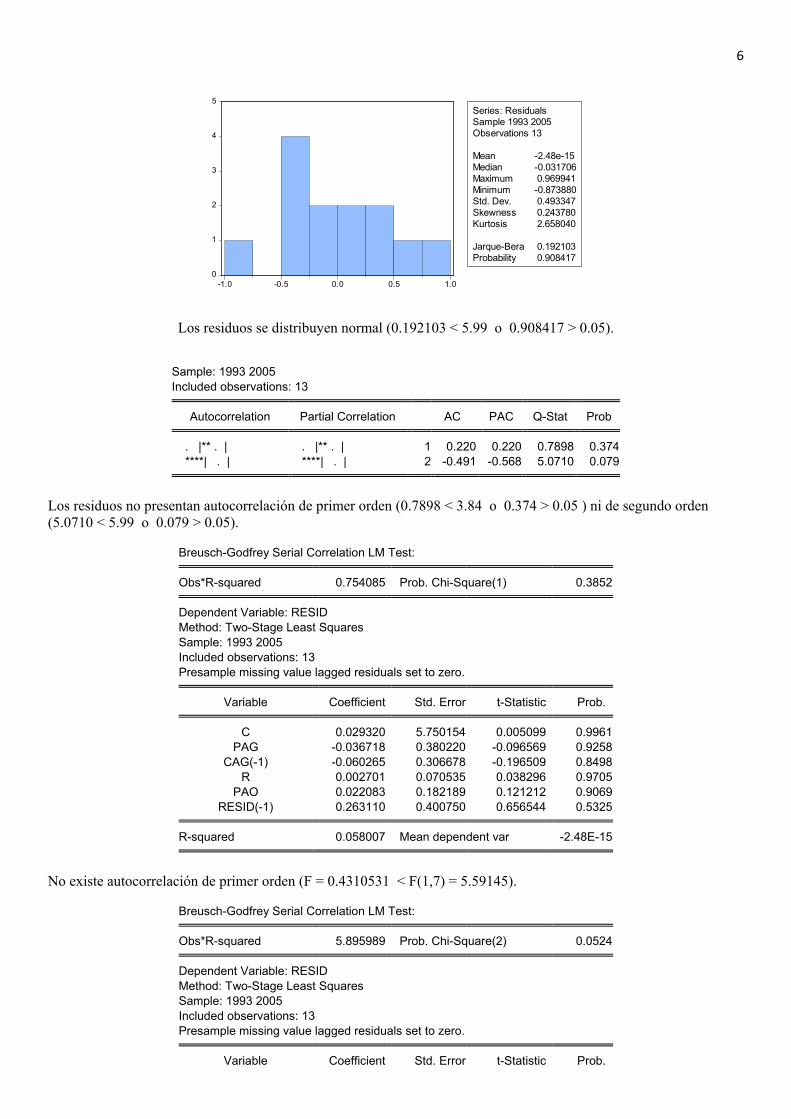

1.3. En la función del consumo de aceite de girasol, verifique si la perturbación es ruido blanco. (4 puntos)

6

0

1

2

3

4

5

-1.0 -0.5 0.0 0.5 1.0

Series: ResidualsSample 1993 2005

Observations 13

Mean -2.48e-15

Median -0.031706

Maximum 0.969941

Minimum -0.873880

Std. Dev. 0.493347

Skewness 0.243780

Kurtosis 2.658040

Jarque-Bera 0.192103

Probability 0.908417

Los residuos se distribuyen normal (0.192103 < 5.99 o 0.908417 > 0.05).

Sample: 1993 2005

Included observations: 13 Autocorrelation Partial Correlation AC PAC Q-Stat Prob . |** . | . |** . | 1 0.220 0.220 0.7898 0.374

****| . | ****| . | 2 -0.491 -0.568 5.0710 0.079

Los residuos no presentan autocorrelación de primer orden (0.7898 < 3.84 o 0.374 > 0.05 ) ni de segundo orden

(5.0710 < 5.99 o 0.079 > 0.05).

Breusch-Godfrey Serial Correlation LM Test: Obs*R-squared 0.754085 Prob. Chi-Square(1) 0.3852 Dependent Variable: RESID

Method: Two-Stage Least Squares

Sample: 1993 2005

Included observations: 13

Presample missing value lagged residuals set to zero. Variable Coefficient Std. Error t-Statistic Prob. C 0.029320 5.750154 0.005099 0.9961

PAG -0.036718 0.380220 -0.096569 0.9258

CAG(-1) -0.060265 0.306678 -0.196509 0.8498

R 0.002701 0.070535 0.038296 0.9705

PAO 0.022083 0.182189 0.121212 0.9069

RESID(-1) 0.263110 0.400750 0.656544 0.5325 R-squared 0.058007 Mean dependent var -2.48E-15

No existe autocorrelación de primer orden (F = 0.4310531 < F(1,7) = 5.59145).

Breusch-Godfrey Serial Correlation LM Test: Obs*R-squared 5.895989 Prob. Chi-Square(2) 0.0524 Dependent Variable: RESID

Method: Two-Stage Least Squares

Sample: 1993 2005

Included observations: 13

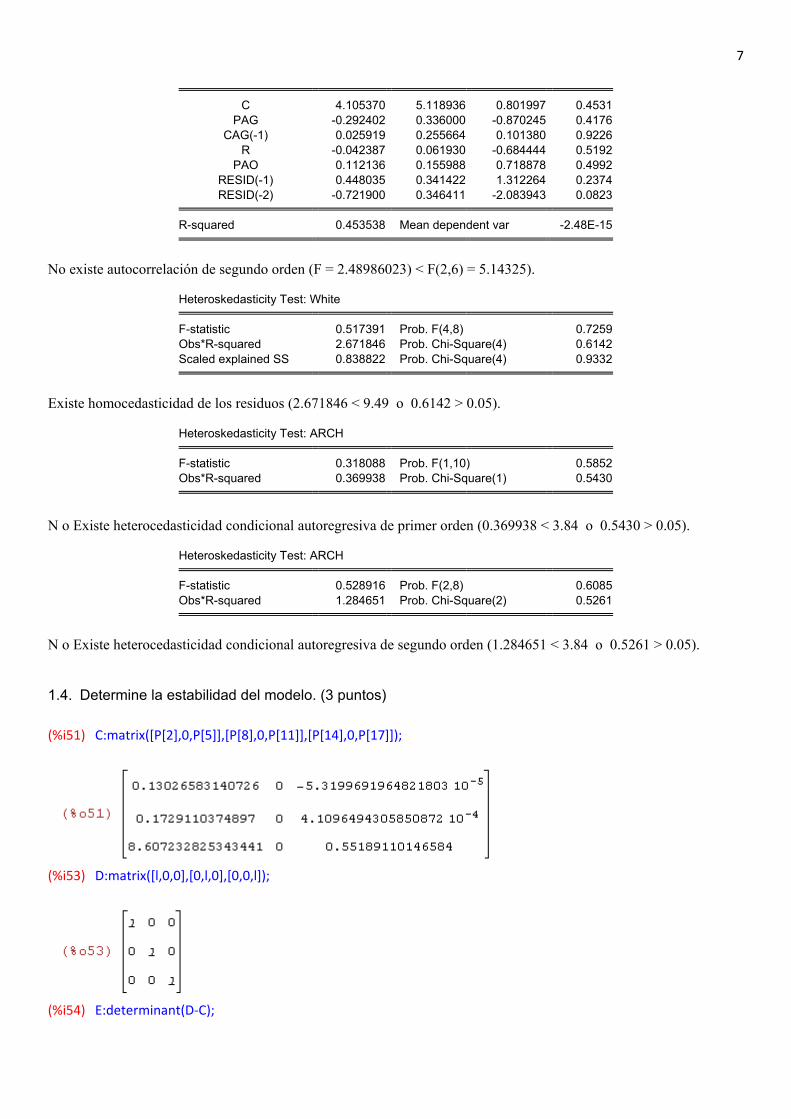

Presample missing value lagged residuals set to zero. Variable Coefficient Std. Error t-Statistic Prob.

7

C 4.105370 5.118936 0.801997 0.4531

PAG -0.292402 0.336000 -0.870245 0.4176

CAG(-1) 0.025919 0.255664 0.101380 0.9226

R -0.042387 0.061930 -0.684444 0.5192

PAO 0.112136 0.155988 0.718878 0.4992

RESID(-1) 0.448035 0.341422 1.312264 0.2374

RESID(-2) -0.721900 0.346411 -2.083943 0.0823 R-squared 0.453538 Mean dependent var -2.48E-15

No existe autocorrelación de segundo orden (F = 2.48986023) < F(2,6) = 5.14325).

Heteroskedasticity Test: White F-statistic 0.517391 Prob. F(4,8) 0.7259

Obs*R-squared 2.671846 Prob. Chi-Square(4) 0.6142

Scaled explained SS 0.838822 Prob. Chi-Square(4) 0.9332

Existe homocedasticidad de los residuos (2.671846 < 9.49 o 0.6142 > 0.05).

Heteroskedasticity Test: ARCH F-statistic 0.318088 Prob. F(1,10) 0.5852

Obs*R-squared 0.369938 Prob. Chi-Square(1) 0.5430

N o Existe heterocedasticidad condicional autoregresiva de primer orden (0.369938 < 3.84 o 0.5430 > 0.05).

Heteroskedasticity Test: ARCH F-statistic 0.528916 Prob. F(2,8) 0.6085

Obs*R-squared 1.284651 Prob. Chi-Square(2) 0.5261

N o Existe heterocedasticidad condicional autoregresiva de segundo orden (1.284651 < 3.84 o 0.5261 > 0.05).

1.4. Determine la estabilidad del modelo. (3 puntos)

(%i51) C:matrix([P[2],0,P[5]],[P[8],0,P[11]],[P[14],0,P[17]]);

(%i53) D:matrix([l,0,0],[0,l,0],[0,0,l]);

(%i54) E:determinant(D-C);

8

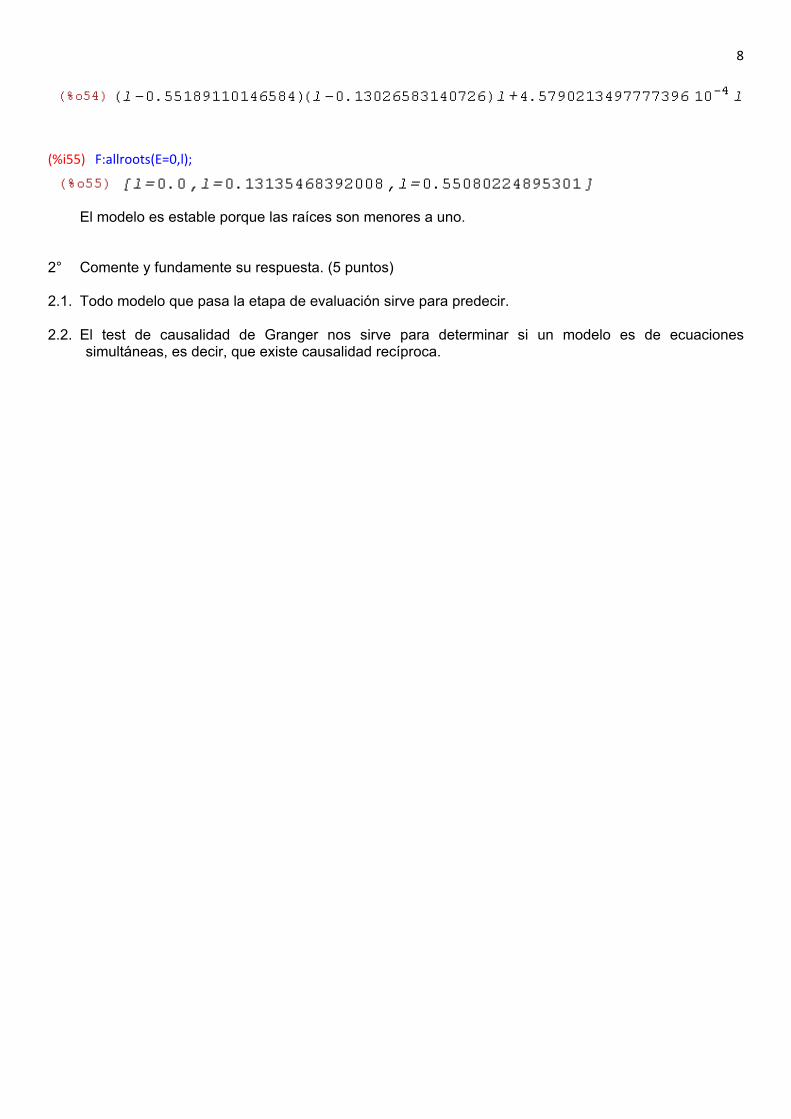

(%i55) F:allroots(E=0,l);

El modelo es estable porque las raíces son menores a uno. 2° Comente y fundamente su respuesta. (5 puntos) 2.1. Todo modelo que pasa la etapa de evaluación sirve para predecir. 2.2. El test de causalidad de Granger nos sirve para determinar si un modelo es de ecuaciones

simultáneas, es decir, que existe causalidad recíproca.

Recommended