ADS Group Limited Salamanca Square 9 Albert Embankment London SE1 [email protected]

www.adsgroup.org.uk +44 (0) 20 7091 4500

UK DEFENCE OUTLOOK2015A

DS1

0246

–09/

15

Imag

e co

urte

sy o

f Fin

mec

cani

ca

FOREWORD

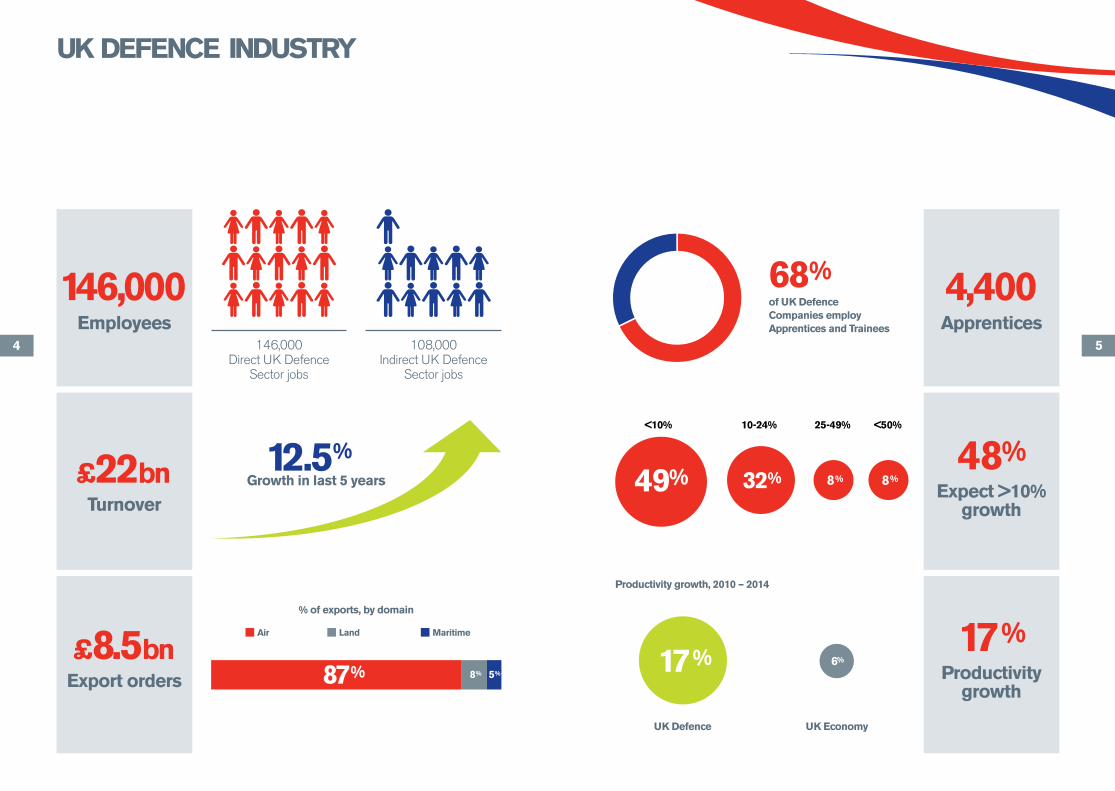

The defence industry is of strategic importance to the UK, generating £22bn in turnover during 2014 and making a direct and vital contribution to national security.

Productivity within the defence industry continues to outpace national levels, growing by 17 per cent over the past four years compared with just six per cent in the rest of the economy. The percentage of companies with a UK-based supply chain has also increased, up by ten per cent since last year.

The defence industry sustains 250,000 jobs across the UK economy. These are high value, long-term jobs with earnings around 40 per cent higher than the national average. Defence companies prioritise skills and are training 4,400 apprentices.

2014 was a challenging year for the defence industry, with many of the figures in this ADS Group Outlook Report showing slight decline. This has been a tough period for the industry with both the UK and many international customers operating within constrained public resources.

Looking ahead, the Government’s commitment to an above-inflation increase to the defence budget coupled with the commitment to meet the two per cent NATO target on defence spending has provided welcome certainty and stability.

The Defence Growth Partnership (DGP) continues to provide a collaborative environment for the collective effort of Industry and Government to boost global competitiveness and grow exports, delivering a number of key initiatives including the UK Defence Solutions Centre (DSC). Working with a strengthened UKTI DSO, the UK DSC represents a step change in the sector’s ability to address global defence markets, bringing the very best that the UK has to meet the needs of the MoD and international customers.

The outcome of the Government’s Strategic Defence and Security Review is expected later this year. ADS has been able to provide significant industry input and to highlight the importance of investment in research and development. As well as boosting productivity levels, it generates the leading-edge capabilities that enable the UK to compete successfully for international market opportunities.

PAUL EVERITT Chief Executive, ADS Group

CONTENTS

Foreword 3

Summary 4

Achieving Growth 6

Investing in Productivity 10

Supporting High-Skill Jobs 12

About ADS 14

About the Data 15

4 5

UK DEFENCE INDUSTRY

£22bn 48%

146,000 4,400

12.5%

£8.5bn 17%

TurnoverExpect >10%

growth

Growth in last 5 years

% of exports, by domain

Air Land Maritime

of UK Defence Companies employ Apprentices and Trainees

Productivity growth, 2010 – 2014

UK Defence UK Economy

Employees Apprentices146,000

Direct UK Defence Sector jobs

108,000Indirect UK Defence

Sector jobs

Export orders Productivity growth

87% 8% 5%

68%

49% 32% 8 8% %

17% 6%

<10% 10-24% 25-49% <50%

76

UK DEFENCE INDUSTRY

48% OF FIRMS EXPECT GROWTH OF AT LEAST 10%

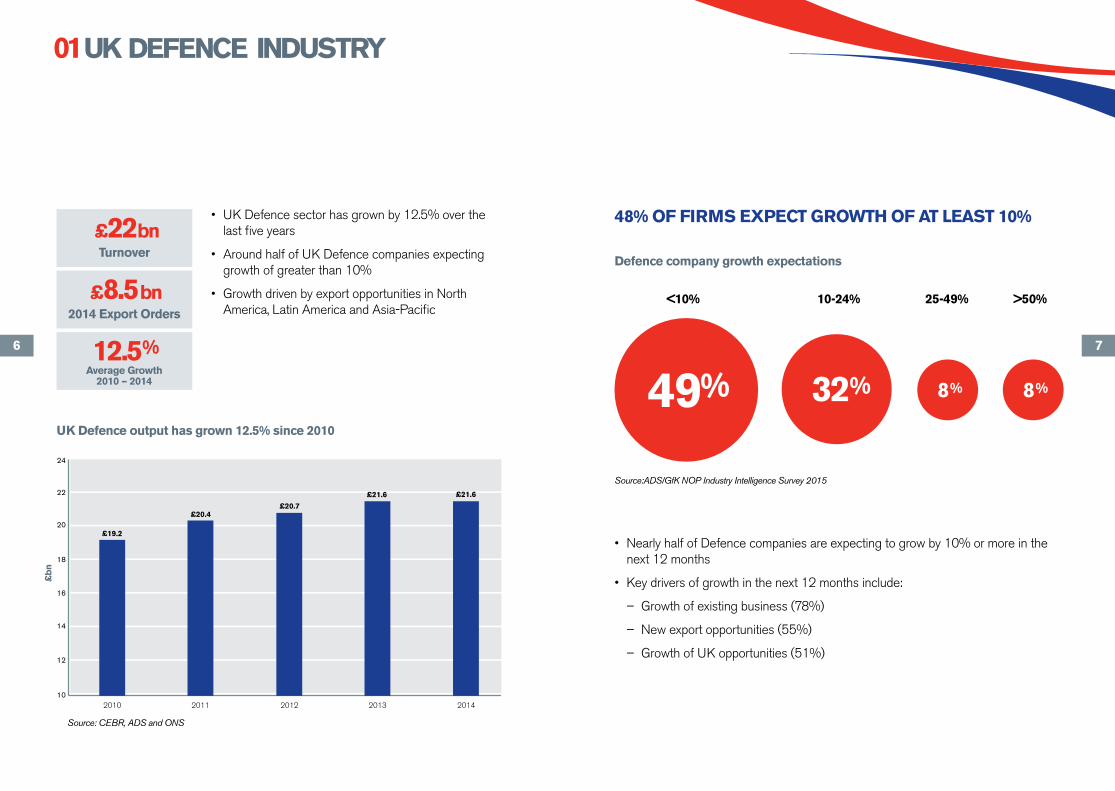

01

£22bn

£8.5bn

12.5%

Turnover

2014 Export Orders

Average Growth 2010 – 2014

UK Defence output has grown 12.5% since 2010

Defence company growth expectations

<10% 10-24% 25-49% >50%

• UKDefencesectorhasgrownby12.5%overthelast five years

• AroundhalfofUKDefencecompaniesexpectinggrowthofgreaterthan10%

• GrowthdrivenbyexportopportunitiesinNorthAmerica, Latin America and Asia-Pacific

10

12

14

16

18

20

22

24

2010 2011 2012 2013 2014

£19.2

£20.4£20.7

£21.6 £21.6

Source: CEBR, ADS and ONS

Source:ADS/GfK NOP Industry Intelligence Survey 2015

49% 32% 8% 8%

• NearlyhalfofDefencecompaniesareexpectingtogrowby10%ormoreinthenext 12 months

• Keydriversofgrowthinthenext12monthsinclude:

– Growthofexistingbusiness(78%)

– Newexportopportunities(55%)

– GrowthofUKopportunities(51%)

£b

n

98

55% SAY GROWTH IS DRIVEN BY NEW EXPORTS UK CENTRAL TO SUPPLY CHAIN & INVESTMENT

% exporting to location / % entering new market % of supply chain in location / % investing in location

74/8 13/29

N AmericaN America

L America L America

Europe Europe

UK

ChinaChinaAfrica

Africa

Middle East Middle EastAsia (excl China)

Rest of Asia

89/9

14/27

69/93

49/161/14

22/62/8

55/13

3/17

22/120/6

23/160/7

Source:ADS/GfK NOP Industry Intelligence Survey 2015 Source:ADS/GfK NOP Industry Intelligence Survey 2015

• 26%ofDefenceturnoverisgeneratedbyexports

• LocationswherecompanieshavecitedgrowingexportlevelsincludeNorthAmerica, Middle East and Asia (excl China)

• ThepercentageofcompaniesexportingtoNorthAmericahasincreasedbymorethan10%sincethepreviousADSsurvey

• UK,EuropeandNorthAmericaremainthefocalpointforglobaldefencesupplychain investment

• MinimalsupplychainpresenceinLatinAmerica,MiddleEast,AfricaandAsiaoffers opportunities for growth from new export opportunities

• ThepercentageofdefencecompanieswithaUK-basedsupplychainhasincreasedbyover10%sincethe2014ADSsurvey

1110

INVESTING IN PRODUCTIVITY02

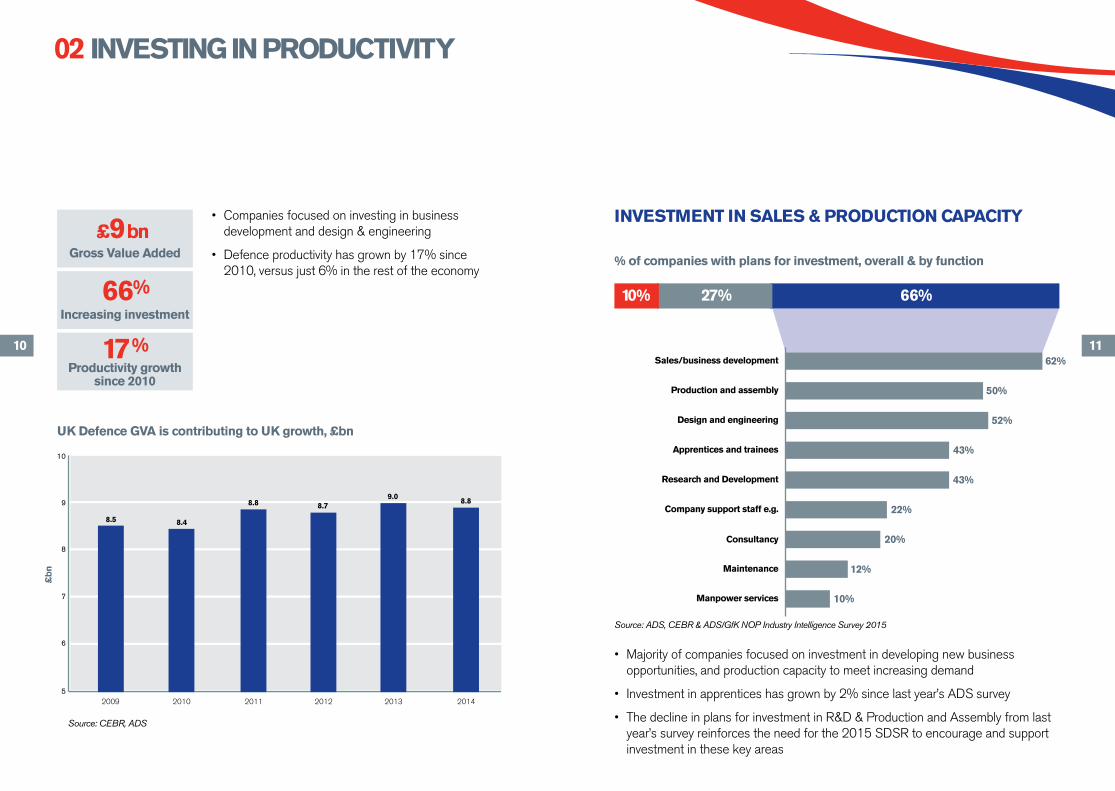

£9bn

66%

17%

Gross Value Added

Increasing investment

Productivity growth since 2010

UK Defence GVA is contributing to UK growth, £bn

• Companiesfocusedoninvestinginbusinessdevelopment and design & engineering

• Defenceproductivityhasgrownby17%since2010,versusjust6%intherestoftheeconomy

Source: CEBR, ADS

5

6

7

8

9

10

2009 2010 2011 2012 2013 2014

8.5 8.4

8.8 8.79.0 8.8

INVESTMENT IN SALES & PRODUCTION CAPACITY

% of companies with plans for investment, overall & by function

Source: ADS, CEBR & ADS/GfK NOP Industry Intelligence Survey 2015

• Majorityofcompaniesfocusedoninvestmentindevelopingnewbusinessopportunities, and production capacity to meet increasing demand

• Investmentinapprenticeshasgrownby2%sincelastyear’sADSsurvey

• ThedeclineinplansforinvestmentinR&D&ProductionandAssemblyfromlastyear’s survey reinforces the need for the 2015 SDSR to encourage and support investment in these key areas

10% 27% 66%

62%Sales/business development

Production and assembly

Design and engineering

Apprentices and trainees

Research and Development

Company support staff e.g.

Consultancy

Maintenance

Manpower services

50%

52%

43%

43%

22%

20%

12%

10%

£b

n

1312

SUPPORTING HIGH-SKILL JOBS03

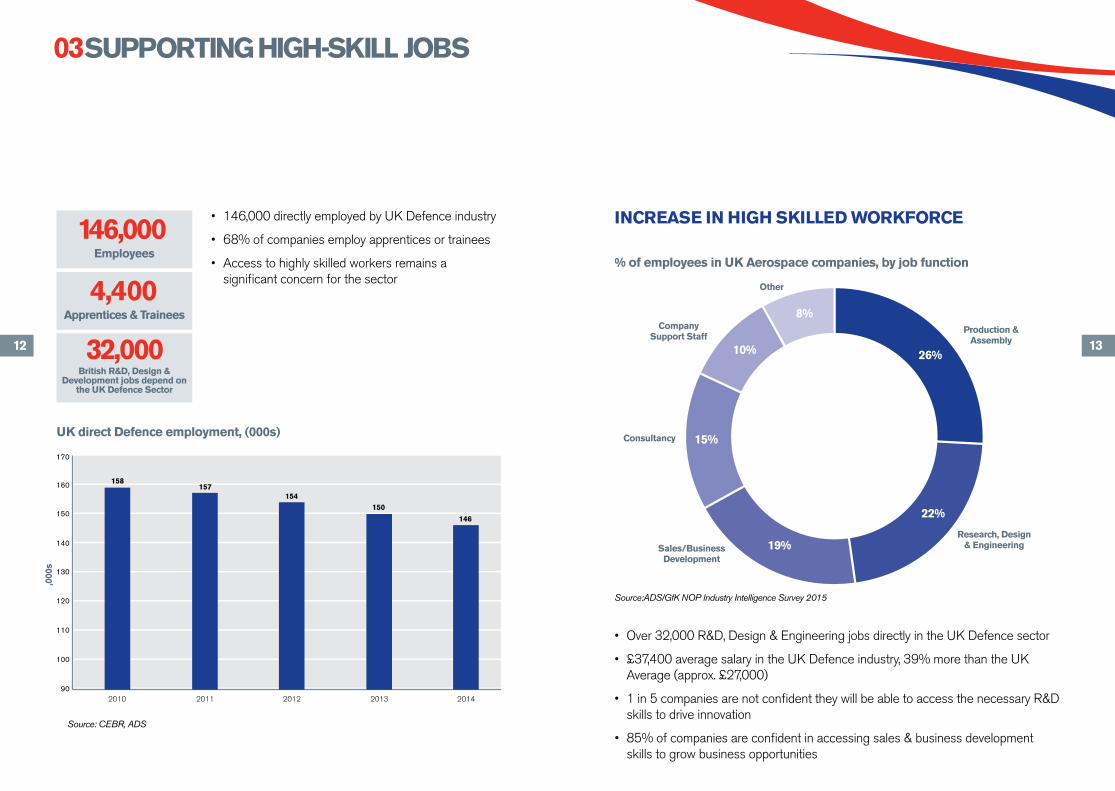

146,000

4,400

32,000

Employees

Apprentices & Trainees

British R&D, Design & Development jobs depend on

the UK Defence Sector

Company Support Staff

Sales/Business Development

Research, Design & Engineering

Production & Assembly

Consultancy

Other

UK direct Defence employment, (000s)

• 146,000directlyemployedbyUKDefenceindustry

• 68%ofcompaniesemployapprenticesortrainees

• Accesstohighlyskilledworkersremainsasignificant concern for the sector

Source: CEBR, ADS

90

100

110

120

130

140

150

160

170

2010 2011 2012 2013 2014

158157

154150

146

INCREASE IN HIGH SKILLED WORKFORCE

% of employees in UK Aerospace companies, by job function

Source:ADS/GfK NOP Industry Intelligence Survey 2015

• Over32,000R&D,Design&EngineeringjobsdirectlyintheUKDefencesector

• £37,400averagesalaryintheUKDefenceindustry,39%morethantheUKAverage (approx. £27,000)

• 1in5companiesarenotconfidenttheywillbeabletoaccessthenecessaryR&Dskills to drive innovation

• 85%ofcompaniesareconfidentinaccessingsales&businessdevelopmentskills to grow business opportunities

10%

15%

19%

22%

8%

26%

,000

s

1514

www.adsgroup.org.uk 0845 872 3231

ADS Group is the UK trade organisation representing the Aerospace, Defence, Security and Space sectors. ADS is focused on representing the interests of these valuable wealth producing industries in the UK and overseas to key stakeholders, government, and the media

ADS plays an instrumental role in bringing industry and government together, working closely and collaboratively to maintain and grow the UK’s world leading position in these industries. In doing so, these sectors will support and facilitate a sustainable UK economic recovery, securing future sector prosperity through a strong strategy and united approach.

Farnborough International Limited is a wholly owned subsidiary of ADS Group. The Farnborough International Airshow 2016 will run from 11-17 July 2016. In 2014, the Farnborough International Airshow saw over $200bn worth of confirmed orders.

In 2015, ADS Group commissioned two different research strands to assess the size, shape and priorities for the UK’s Aerospace, Defence, Security and Space sectors.

• ADS/GfKNOPSurvey. Between 06 March – 27 March 2015, GfK NOP conducted a web-based surveyed 900 ADS Members, asking 30 questions about employment, investment, export and growth trends. The Survey was web-based, with a 14% response rate.

• CentreforEconomics&BusinessResearch(CEBR).ADS commissioned CEBR to assess the turnover, employment and gross value added levels for each of ADS’s four sectors. Their research draws on data from Office National Statistics, Ministry of Defence, ADS Group and the ADS/GfK NOP Survey data.

ABOUT ADS ABOUT THE SURVEY

Recommended