Embed Size (px)

Citation preview

FI$CAL ₹EFORMS

Presenting by-Trisha Sinha Roy(8629)Sanchari Mohanta(8631)

What is a Reform?

By Reform we mean making any change to the current condition for the soul purpose of improvement or in

Economic terms-to get ‘better off’

“Fiscal policy deals with the taxation and expenditure

decisions of the government. These include, tax policy,

expenditure policy, investment or disinvestment strategies

and debt or surplus management.”

- Kaushik Basu ( Former Chief Economic Adviser )

• Fisc : A French word means ‘Treasure of Government’• Fiscal policy refers to the overall effect of the

budget outcome on economic activity• The idea of using fiscal policy to combat recessions

was introduced by John Maynard Keynes in the 1930s • Fiscal Policy = Revenue + Expenditure Policy by the

Government of India• Related to ‘Development Policy’ of the Nation

Fiscal Policy

What is the need of Fiscal Policy?

Where Monetary Meets Fiscal Policy

Three Possible Budgetary Positions

A Neutral position applies when the budget outcome has neutral effect on the level of economic activity where the govt. spending is fully funded by the revenue collected from the tax. Where, G = T

An Expansionary position is when there is a higher budget deficit where the govt. spending is higher than the revenue collected from the tax. Where, G > T

An Contractionary position is when there is a lower budget deficit where the govt. spending is lower than the revenue collected from the tax. Where, G < T

G-Govt. SpendingT-Tax Revenue

Methods of Funding

This expenditure can be funded in a number of different ways:

Taxation Revenue Seigniorage Borrowing money Consumption of fiscal reserves Sale of fixed assets (e.g., land)

Types of Fiscal Policies

Discretionary policy Automatic stabilisation

1991- BOP Crisis• Gulf crisis of 1990--- increase in oil import bill• Exports were down significantly due to breakdown of Soviet

Union• Deterioration in the Exchange Rate of Rupee• Growing deficit on capital account

Actions Taken• Acquisition of Foreign Currency• Devaluation of Indian Rupee• Encouragement to Inflow of Funds from Abroad• Compression of Imports

Source: https://www.quora.com

Few Noteworthy Fiscal Reforms• 1934:Customs Duty• 1944:Excise Duty• 1953:Taxation Enquiry Commission • 1957-58:Wealth Tax, Expenditure Tax, Gift Tax• 1960-70 : Marginal Income Tax Rates• 1960-80 :Tax Revenue to GDP Ratio Improved from 6.3 % to

16.1 %• 1993-94: Reduction of the difference between the interest

rate on market borrowings & other internal liabilities• 1994-95: Inclusion of loans in conversion of maturing treasury

bills & zero coupon bondsSource: shodhganga.inflibnet.ac.in

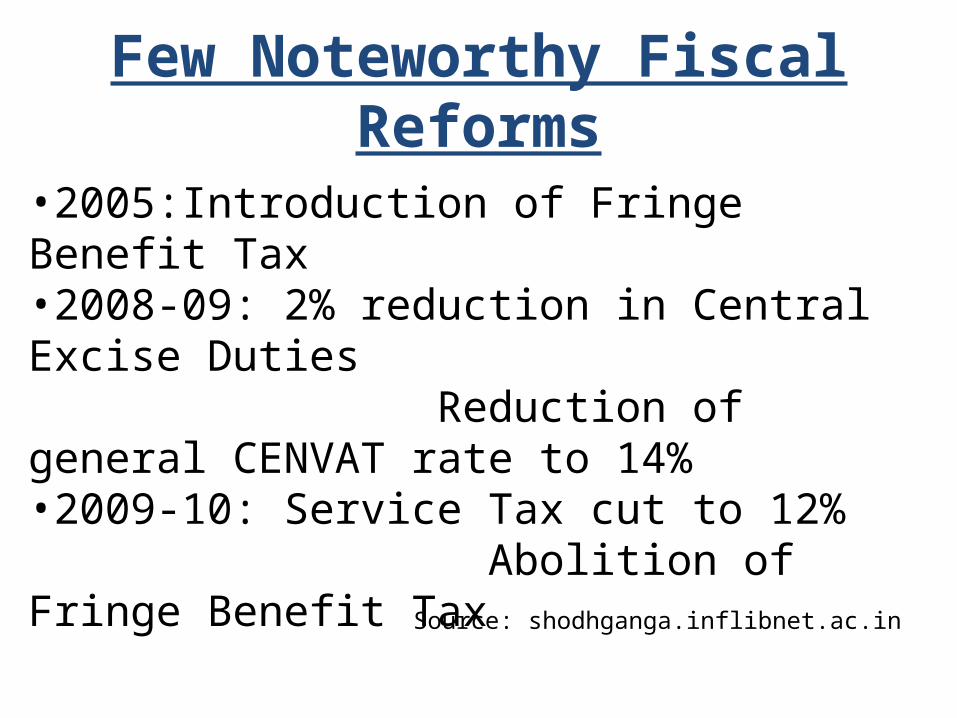

Few Noteworthy Fiscal Reforms

•2005:Introduction of Fringe Benefit Tax•2008-09: 2% reduction in Central Excise Duties Reduction of general CENVAT rate to 14% •2009-10: Service Tax cut to 12% Abolition of Fringe Benefit Tax

Source: shodhganga.inflibnet.ac.in

Tax Reforms

• Expansion of Tax Base and not Tax Rates• Imposition of User Charges on all Non-Merit

goods• Imposition of Tax on Services• Widespread and bold programme on

Disinvestment

• Reducing the corporate tax rate• Rationalization of capital gains tax and dividend tax and

excise duties• Progressive reduction in the peak rate of customs duty on

non-agricultural products• Value Added Tax (VAT)• Total tax revenues of the centre were 9.7 % of GDP in

1990-91 which declined to only 8.8 % in 2000-01• As a part of the subsequent direct tax reforms, the

personal income tax brackets were reduced to three with rates of 20, 30 and 40 percent in 1992-93

Post 1991 Tax Reforms

Post 1991 Tax Reforms

• Tax concessions were also given to non-residents to encourage flow of foreign exchange remittances

• Lowering the maximum marginal rate on personal income tax

• Widening of the tax base by including :o Introduction of presumptive taxeso Adoption of a set of six (one-by-six) economic criteria for

identification of potential tax payers in urban areaso Taxation of services

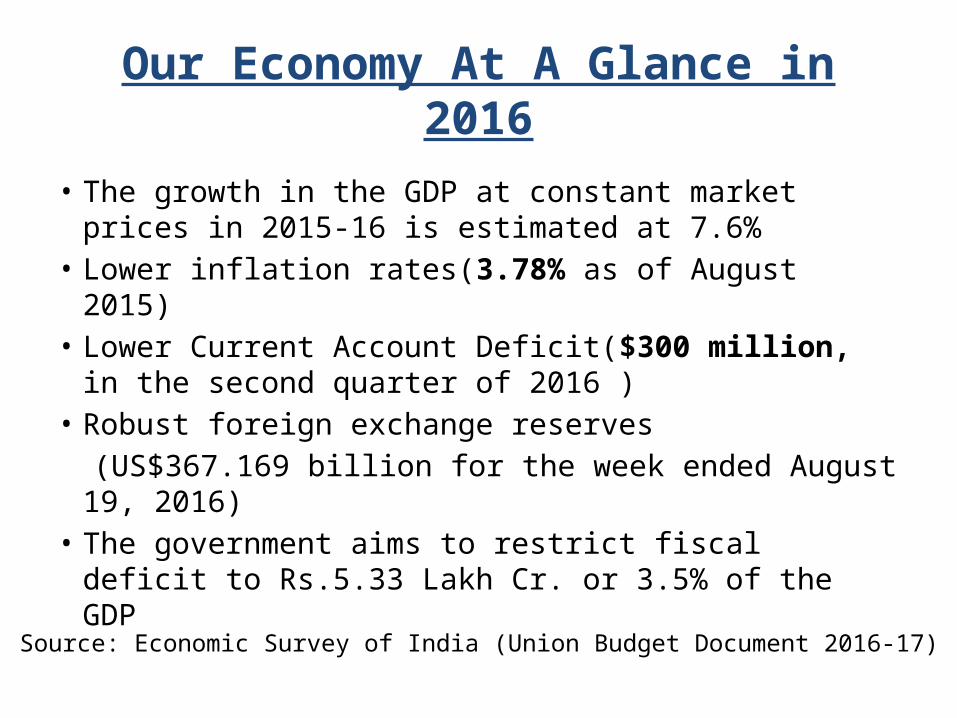

Our Economy At A Glance in 2016• The growth in the GDP at constant market prices in

2015-16 is estimated at 7.6%• Lower inflation rates(3.78% as of August 2015)• Lower Current Account Deficit($300 million, in the

second quarter of 2016 )• Robust foreign exchange reserves (US$367.169 billion for the week ended August 19, 2016)• The government aims to restrict fiscal deficit to Rs.5.33

Lakh Cr. or 3.5% of the GDP

Source: Economic Survey of India (Union Budget Document 2016-17)

Macroeconomic Policy in 2015-16The policy aimed at –• Promoting growth• Revival & Stability in macroeconomic environmentThe reforms initiated in 2014-15 included measures taken towards• De-bottlenecking the economy• Removing structural constraints• Promoting industry and enterprise• Enhancing foreign investment inflows• A host of attendant measures were also taken to improve the ease

of doing business, improve programme delivery performance through expansion of direct benefit transfers coverage and deepening the financial inclusion initiatives

Source: Economic Survey of India (Union Budget Document 2016-17)

Revenue Receipts

• Revenue Receipts= Tax Revenue + Non-Tax Revenue• Neither creates a liability nor reduces nor reduces

any assets• Tax Revenue: Tax Revenue forms part of the Receipt

Budget, which in turn is a part of the Annual Financial Statement of the Union Budget

• Non-Tax Revenue: Non-Tax Revenue is the recurring income earned by the government from sources other than taxes

Capital Receipts

• Capital Receipts = Recoveries of Loans + Other Receipts + Borrowings and other liabilities

• It is the amount received from the sale of assets, shares and debentures

CHANGE IN ESTIMATED REVENUE AND CAPITAL RECEIPTS (in Crores of Rupees)

2012-13 2013-14 2014-15 2015-16 2016-170

500000

1000000

1500000

2000000

2500000

REVENUE RECEIPTSCAPITAL RECEIPTSTOTAL RECEOPTS

Source: Economic Survey of India

Types of Taxes

Direct Taxes• Income tax• Wealth tax• Corporation taxIndirect Taxes• Service tax• Excise Duty• VAT• Customs duty• GST

Government Expenditure

• Plan Expenditure-This is essentially the budget support to the Central Plan and the Central assistance to State and Union Territory plans. Like all budget heads, this is also split into revenue and capital components.

• Non-Plan Expenditure-This is largely the revenue expenditure of the government, although it also includes capital expenditure. It covers all expenditure not included in the Plan Expenditure.

Fiscal Deficit Over Last Five Years

2011-12 2012-13 2013-14 2014-150

1

2

3

4

5

6

7

Source: Economic Survey of India

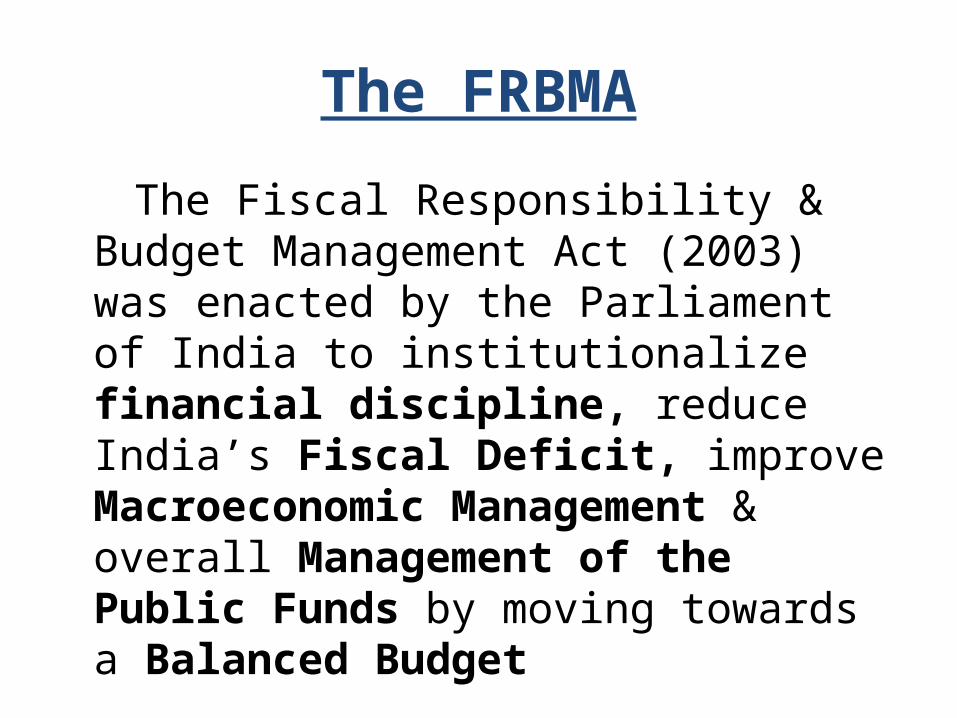

The FRBMA

The Fiscal Responsibility & Budget Management Act (2003) was enacted by the Parliament of India to institutionalize financial discipline, reduce India’s Fiscal Deficit, improve Macroeconomic Management & overall Management of the Public Funds by moving towards a Balanced Budget

Objectives of FRBMA

• Ensure inter-generational equity• Long term Macroeconomic Stability• Complementing the RBI’s Monetary Policy

Kelkar Committee Report• Released on 28 December 2015 by The Union Ministry of Finance• Revisiting and Revitalising Public Private Partnership (PPP) Model• Nine-member committee was headed by former Finance

Secretary Vijay Kelkar• Was constituted on 26 May 2015 • To improve capacity building in Government for their effective

implementation• Recognized the PPP Model in infrastructure as a valuable

instrument to speed up infrastructure development in India• Needs to focus more on service delivery instead of fiscal benefits

alone

Significance of the Committee

• Speeding up of the PPP model is urgently required for India to grow rapidly and generate a demographic dividend for itself and also to tap into the large pool of pension and institutional funds from aging populations in the developed countries• India’s success in deploying PPPs as an important instrument for creating infrastructure will depend on a change in attitude of all authorities dealing with PPPs-public agencies, government departments supervising and auditing and legislative institutions

Key recommendations of the Committee• The Government may take early action to amend the Prevention of

Corruption Act, 1988• the need to further strengthen the three key pillars of PPP

frameworks namely Governance, Institutions and Capacity• Independent regulators should be set up in different infrastructure sub

sectors to ensure harmonized performance by the regulators• advised against adopting PPP structures for very small projects• Unsolicited Proposals (“Swiss Challenge”) may be actively discouraged• state owned entities SoEs/PSUs should not be allowed to bid for PPP

projects• to notify comprehensive guidelines on the applicability and scope

of access to, under RTI and Art 12 of the Constitution, and auditing of financial related matters in order to avoid any delays in public asset provision

• Banks and financial institution should be encouraged to issue Deep Discount Bonds or Zero Coupon Bonds (ZCB) to mobilise long term capital at low cost

Existing Indirect Tax Structure

Entry Tax & Octroi

Entertainment Tax

Electricity Duty

Luxury Tax

VAT

State Levies

Customs Duty

Central Sales Tax

Service Tax

Excise Duty

Central Levies

Goods & Services TaxTo Trade To Consumers

Reduction in multiplicity of taxes Simpler Tax system

Mitigation of cascading/ double taxation Reduction in prices of goods & services due to elimination of cascading of taxes

More efficient neutralization of taxes especially for exports

Uniform prices throughout the country

Development of common national market Transparency in taxation system

Simpler tax regime:•Fewer rates & exemptions •Distinction between Goods & Services no longer required

Increase in employment opportunities

Source: http://www.cbec.gov.in

33

• Can be a powerful tool for accelerating growth • Total government expenditure as proportion of

GDP needs to be maintained, and raised at the State level

• Adherence to fiscal legislation• Fiscal empowerment• The approach to Fiscal Federalism

Suggestions on Fiscal Policy

References• http://www.economywatch.com/indianecono

my/fiscal-sector-reforms.html• https://www.google.co.in/webhp?sourceid=ch

rome-instant&ion=1&espv=2&ie=UTF-8#q=fiscal+deficit+india+2016

• https://www.google.co.in/webhp?sourceid=chrome-instant&ion=1&espv=2&ie=UTF-8#q=foreign%20exchange%20reserves%20of%20india

• https://www.google.co.in/webhp?sourceid=chrome-instant&ion=1&espv=2&ie=UTF-8#q=current+account+deficit+in+india

• https://www.google.co.in/webhp?sourceid=chrome-instant&ion=1&espv=2&ie=UTF-8#q=inflation+rate+in+india

• http://www.economywatch.com/indianeconomy/fiscal-sector-reforms.html

• http://indiabudget.nic.in/ub2016-17/frbm/frbm3.pdf

• http://economictimes.indiatimes.com/• http://www.indianeconomy.net/splclassroom/

223/what-is-fiscal-responsibility-and-budget-management-frbm-act-what-are-the-amendments-to-it/#sthash.TmeRgkXs.dpuf (FRBM)

References• http://www.jagranjosh.com/current-affairs/report-of-vijay-kelkar-commi

ttee-on-revisiting-revitalizing-ppp-model-released-1451371983-1 (Kelkar Committee Report)

• https://www.bankbazaar.com/tax/direct-tax.html (Direct Taxes)

• http://www.cbec.gov.in/resources//htdocs-cbec/deptt_offcr/gst-dgtps-12092016.pdf (GST)

• https://www.google.co.in/webhp?sourceid=chrome-instant&ion=1&espv=2&ie=UTF-8#q=discretionary%20fiscal%20policy

• https://www.google.co.in/webhp?sourceid=chrome-instant&ion=1&espv=2&ie=UTF-8#q=automatic%20fiscal%20policy

• https://shodhganga.inflibnet.ac.in• https://

www.quora.com/What-exactly-happened-to-the-Indian-economy-in-1991-in-laymans-terms (1991 Crisis)

Thank You

![Economic Reforms India[1]](https://img.pdfslide.net/doc/110x75/577d20011a28ab4e1e91c5b2/economic-reforms-india1.jpg)