Embed Size (px)

Citation preview

Morgan Stanley European Financials Conference 2017

BBVA- Delivering our Strategy

#BBVAFinance

MS European Financials Conference / 2

Delivering on our Strategy London, March 21st 2017

Carlos Torres Vila Chief Executive Officer

MS European Financials Conference / 3

01

02

Execution of our Transformation Journey

BBVA’s Strengths

03 Final Remarks

MS European Financials Conference / 4

01 Execution of Our Transformation Journey

MS European Financials Conference / 5

Clear Strategic Path

Our Purpose

New standard in

customer experience

A first class workforce

Drive digital sales

New business models

Optimal capital allocation

Unrivaled efficiency

Six Strategic Priorities

Creating Opportunities

To bring the age

of opportunity

to everyone

Industry Dynamics

Profitability of

financial

industry under

pressure

New disruptive

entrants

transforming each

vertical

Transformative

technologies and

use of data open up

unimaginable

opportunities

15.8%

-3.0%

5.6% 7.0% 2.7%

1.5% 1.7%

4.0% 4.4% 2.4%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Redefined value

proposition

Around positively

impacting financial

behavior of clients and

customers

Big Data Biometrics Cloud

A.I. (1) Blockchain

(1) Artificial Intelligence

MS European Financials Conference / 6

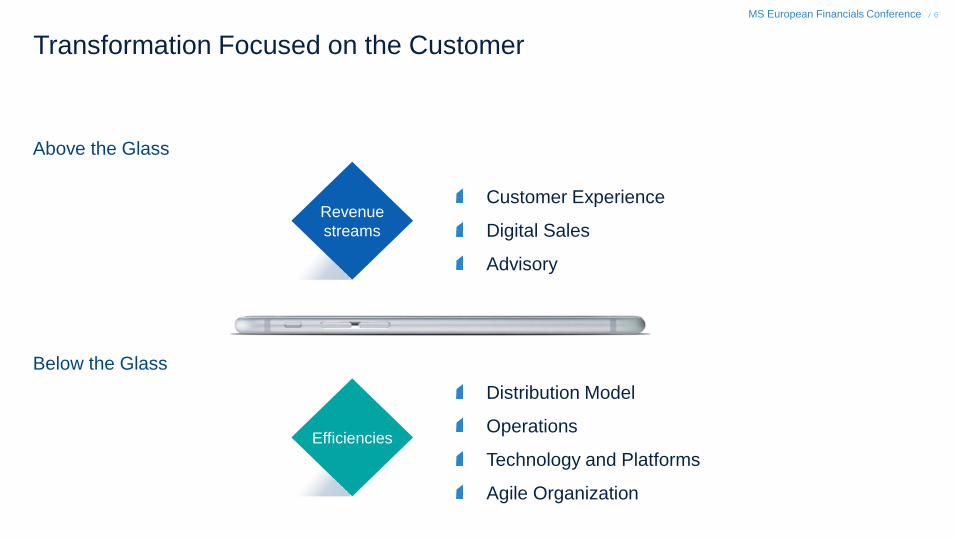

Transformation Focused on the Customer

Customer Experience

Digital Sales

Advisory

Distribution Model

Operations

Technology and Platforms

Agile Organization

Revenue

streams

Above the Glass

Below the Glass

Efficiencies

MS European Financials Conference / 7

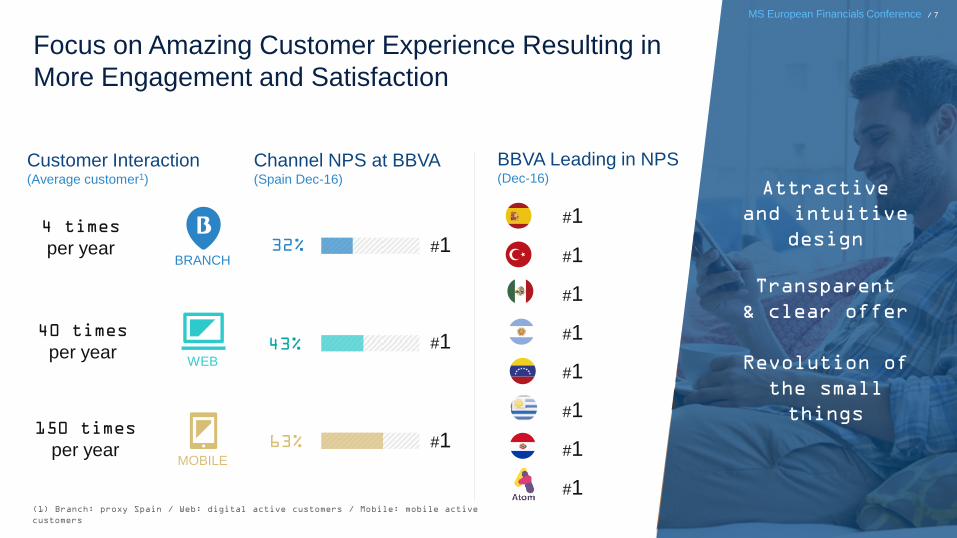

32%

43%

63%

#1

#1

#1

#1

#1

#1

#1

#1

BBVA Leading in NPS (Dec-16)

BRANCH

WEB

Focus on Amazing Customer Experience Resulting in

More Engagement and Satisfaction

Attractive

and intuitive

design

Transparent

& clear offer

Revolution of

the small

things

MOBILE

#1

150 times

per year

4 times

per year

40 times

per year

Customer Interaction (Average customer1)

Channel NPS at BBVA (Spain Dec-16)

#1

#1

MS European Financials Conference / 7

(1) Branch: proxy Spain / Web: digital active customers / Mobile: mobile active

customers

MS European Financials Conference / 8

15.4 18.4

Digital Customers and Sales Grow Exponentially

as we Broaden our Digital Offer

8.4 17.1

Dec.15 Dec. 16

6.2 11.9

Dec.15 Dec. 16

SPAIN MEXICO

9.3 19.9

Dec.15 Dec. 16

USA

9.0 15.2

Dec.15 Dec. 16

SOUTH AMERICA

23.4 26.1

Dec.15 Dec. 16

TURKEY

Digital Sales (% of total sales YtD, # of transactions)

Digital Customers BBVA Group (Million, % penetration)

Mobile Customers BBVA Group (Million, % penetration)

Digital

onboarding

Still room

for growth

Increasing

DIY(1)

availability

Dec.1

5

Dec.16

+20%

+38%

MS European Financials Conference / 8

Penetration 33% 38%

Penetration 19% 25%

9.0 12.4

Dec.1

5

Dec.16

(1) DIY: Do-It-Yourself

MS European Financials Conference / 9

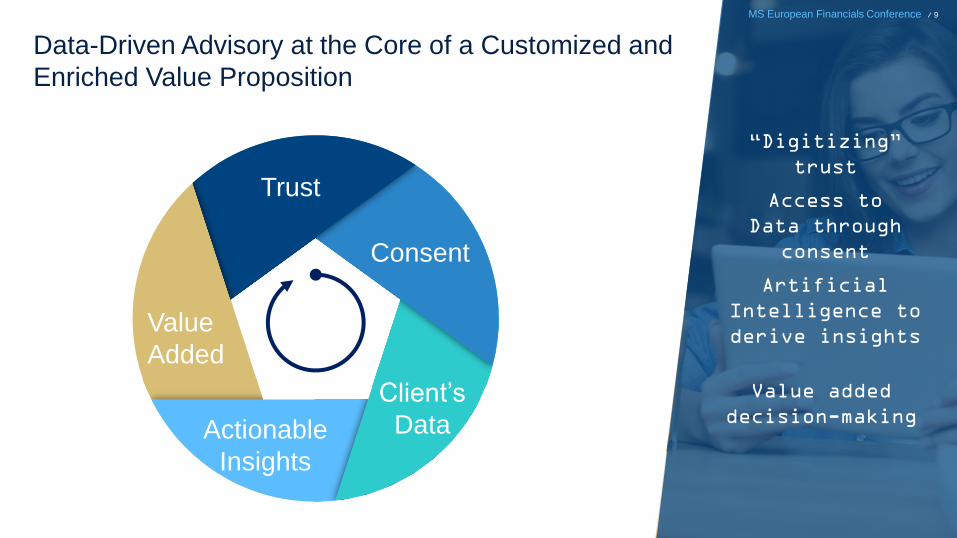

Trust

Consent

Client’s

Data Actionable

Insights

Value

Added

Data-Driven Advisory at the Core of a Customized and

Enriched Value Proposition

Access to

Data through

consent

Value added

decision-making

Artificial

Intelligence to

derive insights

MS European Financials Conference / 9

“Digitizing”

trust

MS European Financials Conference / 10

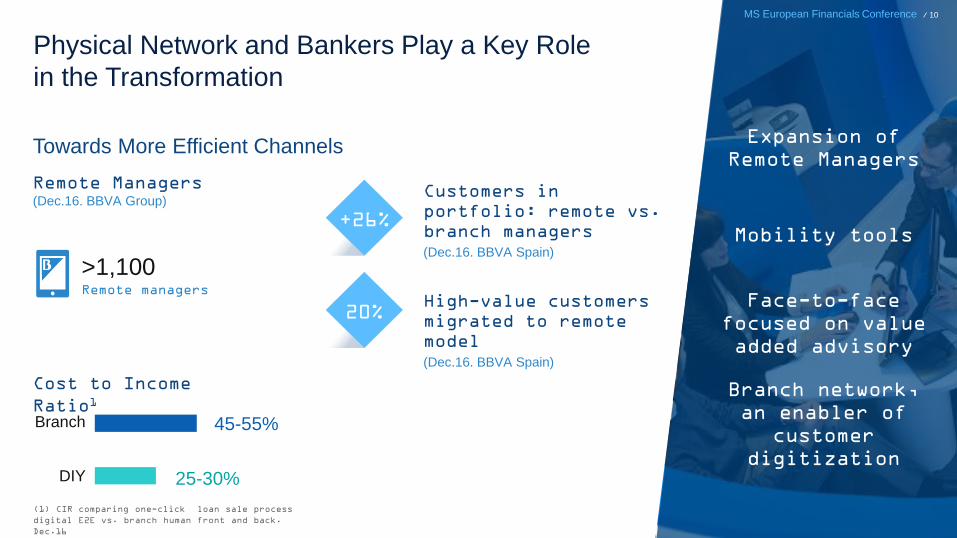

Physical Network and Bankers Play a Key Role

in the Transformation

Cost to Income

Ratio1

Remote Managers (Dec.16. BBVA Group)

>1,100 Remote managers

Customers in

portfolio: remote vs.

branch managers

(Dec.16. BBVA Spain)

Expansion of

Remote Managers

Branch network,

an enabler of

customer

digitization

Face-to-face

focused on value

added advisory

Mobility tools

Towards More Efficient Channels

MS European Financials Conference / 10

+26%

45-55%

25-30%

20% High-value customers

migrated to remote

model

(Dec.16. BBVA Spain)

(1) CIR comparing one-click loan sale process

digital E2E vs. branch human front and back.

Dec.16

Branch

DIY

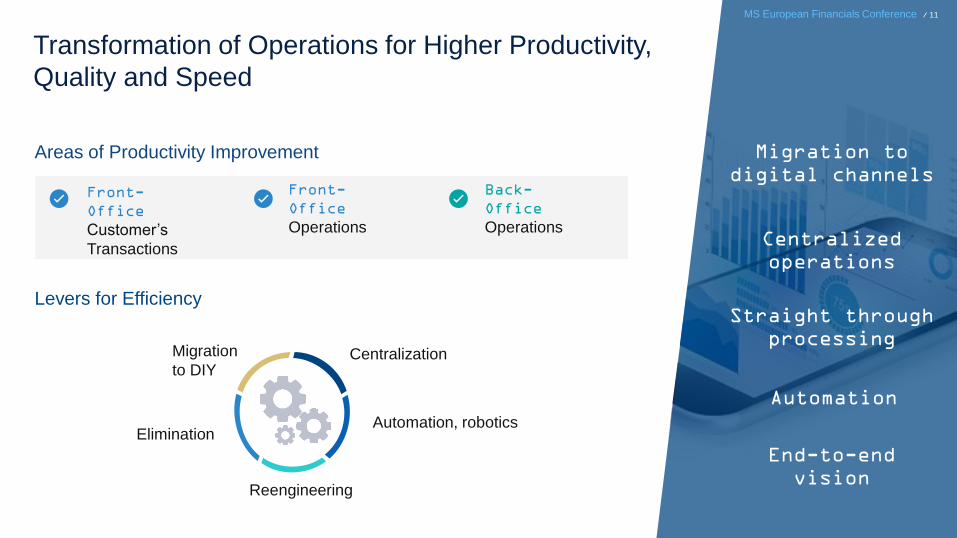

MS European Financials Conference / 11

Levers for Efficiency

Automation, robotics

Transformation of Operations for Higher Productivity,

Quality and Speed

Migration to

digital channels

End-to-end

vision

Straight through

processing

Centralized

operations

Areas of Productivity Improvement

Front-

Office

Customer’s

Transactions

Front-

Office

Operations

Back-

Office

Operations

MS European Financials Conference / 11

Centralization Migration

to DIY

Elimination

Reengineering

Automation

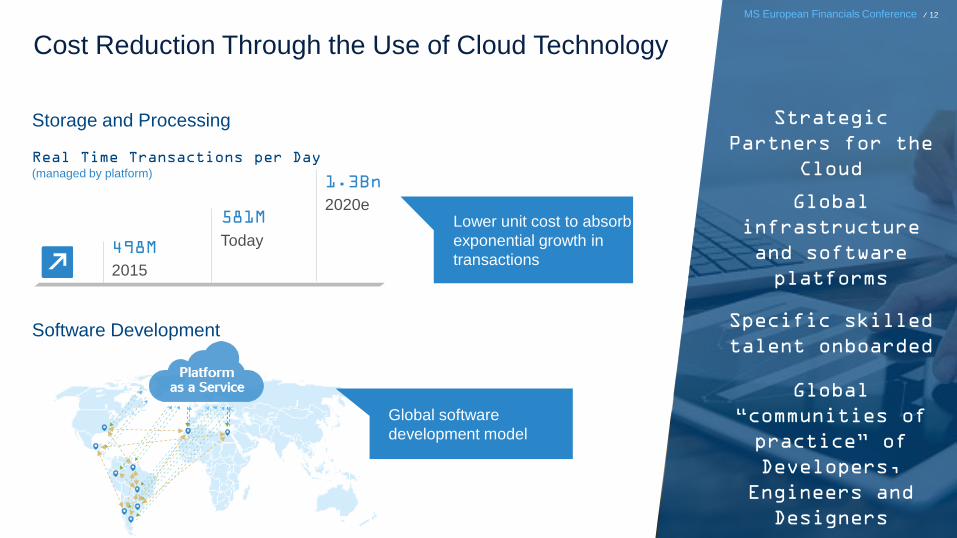

MS European Financials Conference / 12

Lower unit cost to absorb

exponential growth in

transactions

Storage and Processing

Software Development

Real Time Transactions per Day (managed by platform)

498M

581M

1.3Bn

Cost Reduction Through the Use of Cloud Technology

Strategic

Partners for the

Cloud

Specific skilled

talent onboarded

Global

infrastructure

and software

platforms

MS European Financials Conference / 12

2015

Today

2020e

Global software

development model

Global

“communities of

practice” of

Developers,

Engineers and

Designers

MS European Financials Conference / 13

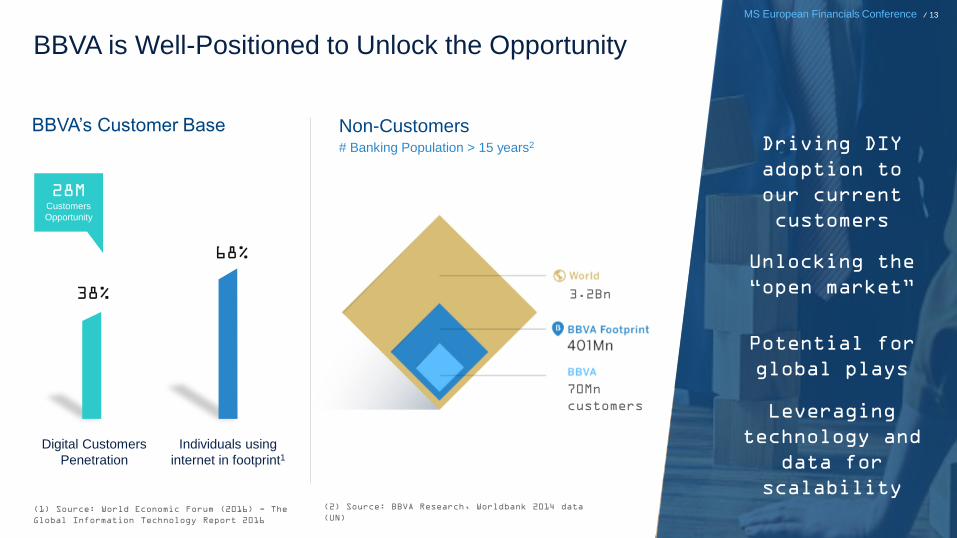

68%

38%

(1) Source: World Economic Forum (2016) - The

Global Information Technology Report 2016

# Banking Population > 15 years2

3.2Bn

BBVA is Well-Positioned to Unlock the Opportunity

Driving DIY

adoption to

our current

customers

Leveraging

technology and

data for

scalability

Potential for

global plays

MS European Financials Conference / 13

BBVA’s Customer Base Non-Customers

Digital Customers

Penetration

Individuals using

internet in footprint1

28M Customers

Opportunity

70Mn

customers

(2) Source: BBVA Research, Worldbank 2014 data

(UN)

Unlocking the

“open market”

MS European Financials Conference / 14

02 BBVA’s Strengths

MS European Financials Conference / 15

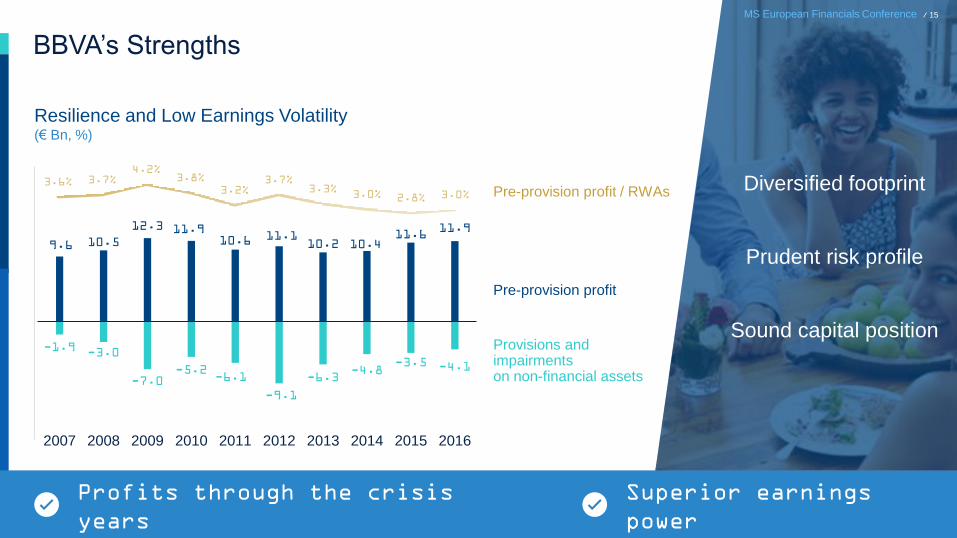

9.6 10.5

12.3 11.9 10.6 11.1

10.2 10.4 11.6

11.9

-1.9 -3.0

-7.0 -5.2

-6.1

-9.1

-6.3 -4.8

-3.5 -4.1

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

BBVA’s Strengths

Profits through the crisis

years

Superior earnings

power

Resilience and Low Earnings Volatility (€ Bn, %)

3.6% 3.7% 4.2%

3.8%

3.2% 3.7%

3.3% 3.0% 2.8% 3.0%

Provisions and impairments on non-financial assets

Pre-provision profit

Pre-provision profit / RWAs Diversified footprint

Prudent risk profile

Sound capital position

MS European Financials Conference / 15

MS European Financials Conference / 16

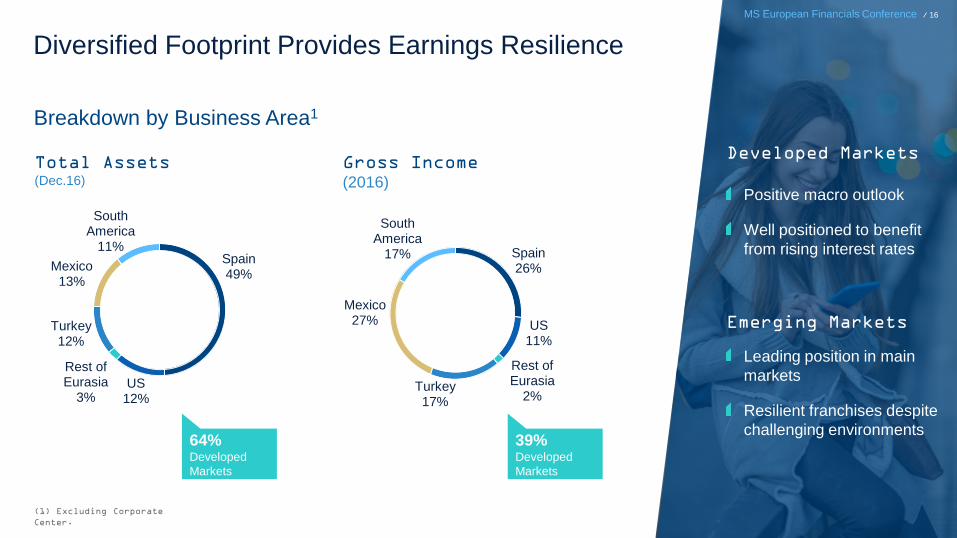

Diversified Footprint Provides Earnings Resilience

Breakdown by Business Area1

Spain 49%

US 12%

Rest of Eurasia

3%

Turkey 12%

Mexico 13%

South America

11% Spain 26%

US 11%

Rest of Eurasia

2% Turkey 17%

Mexico 27%

South America

17%

Total Assets (Dec.16)

Gross Income

(2016)

(1) Excluding Corporate

Center.

64% Developed

Markets

39% Developed

Markets

Leading position in main

markets

Resilient franchises despite

challenging environments

Positive macro outlook

Well positioned to benefit

from rising interest rates

Developed Markets

Emerging Markets

MS European Financials Conference / 16

MS European Financials Conference / 17

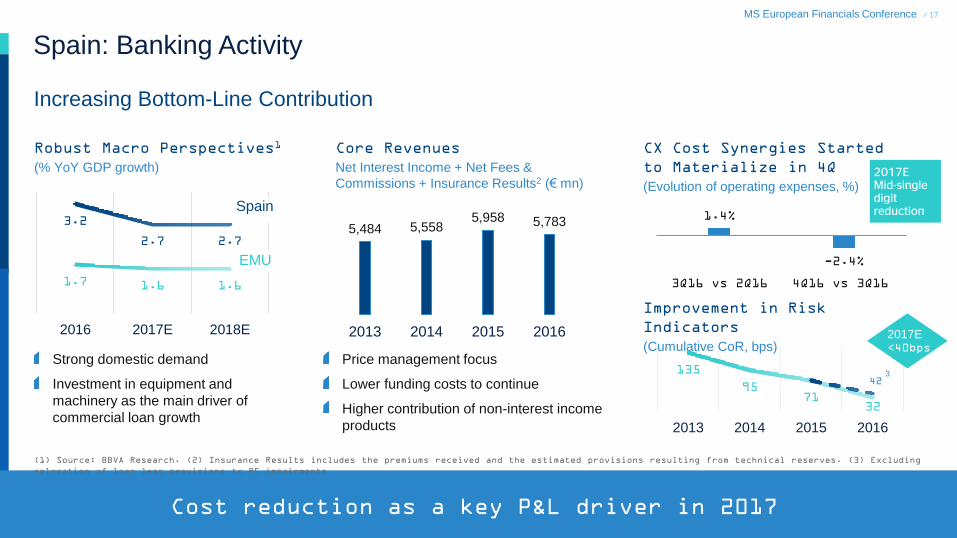

Spain: Banking Activity

Increasing Bottom-Line Contribution

Cost reduction as a key P&L driver in 2017

Robust Macro Perspectives1

(% YoY GDP growth)

Core Revenues

Net Interest Income + Net Fees &

Commissions + Insurance Results2 (€ mn)

CX Cost Synergies Started

to Materialize in 4Q

(Evolution of operating expenses, %)

3.2

2.7 2.7

1.7 1.6 1.6

2016 2017E 2018E

Strong domestic demand

Investment in equipment and

machinery as the main driver of

commercial loan growth

Price management focus

Lower funding costs to continue

Higher contribution of non-interest income

products

5,484 5,558 5,958 5,783

2013 2014 2015 2016

1.4%

-2.4%

3Q16 vs 2Q16 4Q16 vs 3Q16

Improvement in Risk

Indicators

(Cumulative CoR, bps)

135

95 71

32

42

2013 2014 2015 2016

3

2017E Mid-single digit reduction

(1) Source: BBVA Research. (2) Insurance Results includes the premiums received and the estimated provisions resulting from technical reserves. (3) Excluding

relocation of loan loss provisions to RE impairments

2017E <40bps

Spain

EMU

MS European Financials Conference / 18

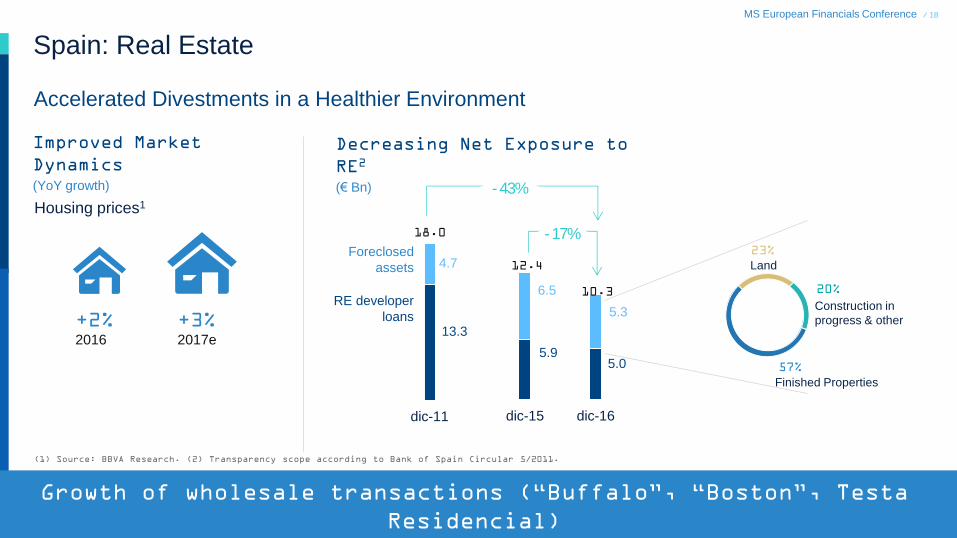

Accelerated Divestments in a Healthier Environment

Spain: Real Estate

Improved Market

Dynamics

(YoY growth)

Housing prices1

Decreasing Net Exposure to

RE2

(€ Bn)

13.3

4.7

dic-11

18.0

Foreclosed

assets

RE developer

loans

5.9 5.0

6.5

5.3

dic-15 dic-16

12.4

10.3

- 17%

- 43%

57%

23%

20%

Finished Properties

Construction in

progress & other

Land

+2% 2016

+3% 2017e

Growth of wholesale transactions (“Buffalo”, “Boston”, Testa

Residencial)

(1) Source: BBVA Research. (2) Transparency scope according to Bank of Spain Circular 5/2011.

MS European Financials Conference / 19

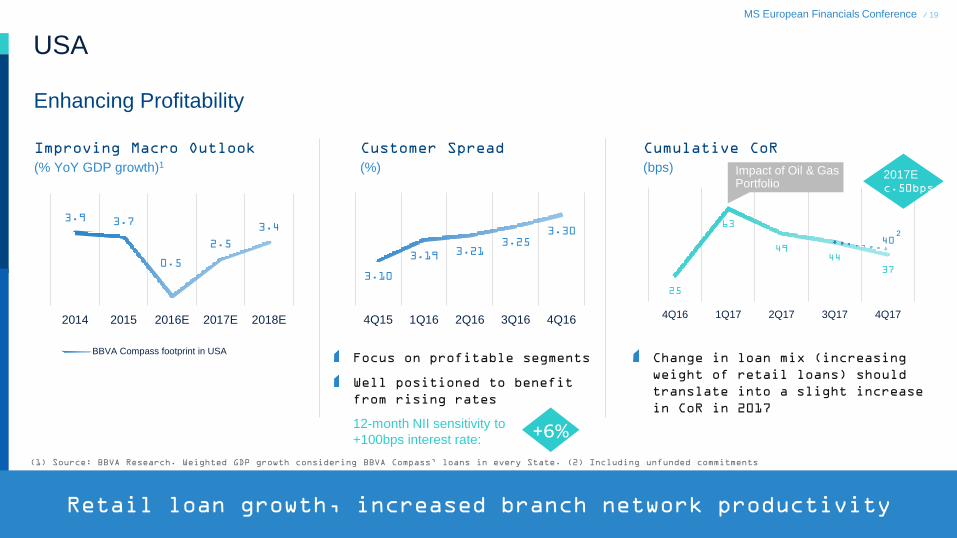

3.9 3.7

0.5

2.5

3.4

2014 2015 2016E 2017E 2018E

BBVA Compass footprint in USA

USA

Enhancing Profitability

Improving Macro Outlook

(% YoY GDP growth)1

Customer Spread

(%)

Cumulative CoR

(bps)

Retail loan growth, increased branch network productivity

Focus on profitable segments

Well positioned to benefit

from rising rates

Change in loan mix (increasing

weight of retail loans) should

translate into a slight increase

in CoR in 2017

3.10

3.19 3.21 3.25

3.30

4Q15 1Q16 2Q16 3Q16 4Q16

+6% 12-month NII sensitivity to

+100bps interest rate:

(1) Source: BBVA Research. Weighted GDP growth considering BBVA Compass’ loans in every State. (2) Including unfunded commitments

25

63

49 44

37

40

4Q16 1Q17 2Q17 3Q17 4Q17

2017E c.50bps

2

Impact of Oil & Gas Portfolio

MS European Financials Conference / 20

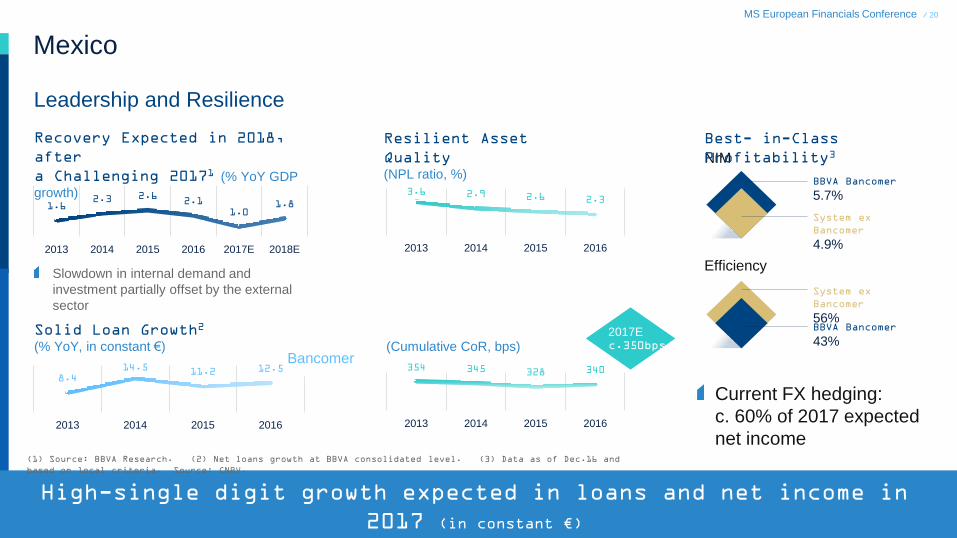

Mexico

Leadership and Resilience

Recovery Expected in 2018,

after

a Challenging 20171 (% YoY GDP

growth)

Resilient Asset

Quality (NPL ratio, %)

1.6 2.3 2.6

2.1

1.0 1.8

2013 2014 2015 2016 2017E 2018E

Slowdown in internal demand and

investment partially offset by the external

sector

(1) Source: BBVA Research. (2) Net loans growth at BBVA consolidated level. (3) Data as of Dec.16 and

based on local criteria. Source: CNBV.

Solid Loan Growth2

(% YoY, in constant €)

8.4 14.5 11.2 12.5

2013 2014 2015 2016

3.6 2.9 2.6 2.3

2013 2014 2015 2016

354 345 328 340

2013 2014 2015 2016

(Cumulative CoR, bps)

NIM

Efficiency

BBVA Bancomer

5.7%

Best- in-Class

Profitability3

Current FX hedging:

c. 60% of 2017 expected

net income

System ex

Bancomer

4.9%

BBVA Bancomer

43%

System ex

Bancomer

56%

High-single digit growth expected in loans and net income in

2017 (in constant €)

2017E c.350bps

Bancomer

MS European Financials Conference / 21

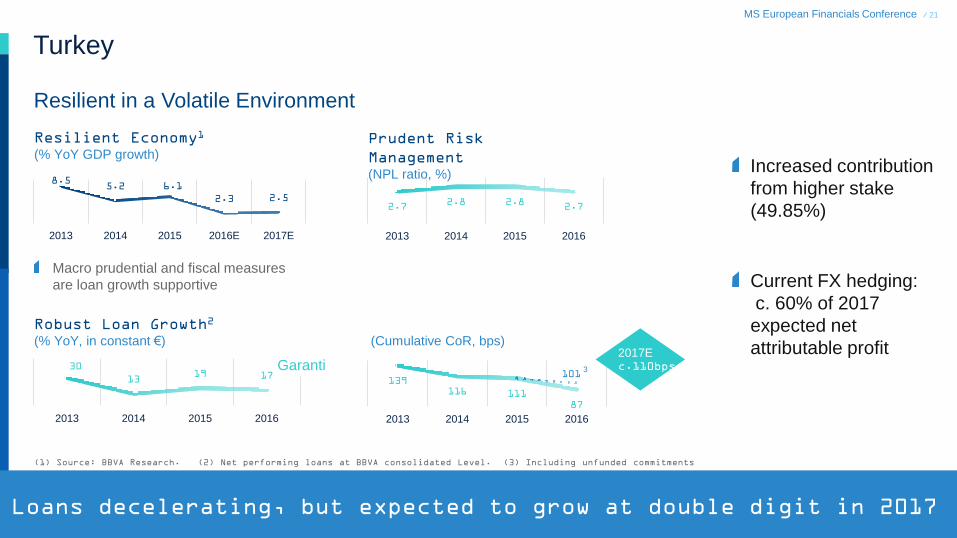

Turkey

Resilient in a Volatile Environment

Macro prudential and fiscal measures

are loan growth supportive

(1) Source: BBVA Research. (2) Net performing loans at BBVA consolidated Level. (3) Including unfunded commitments

Increased contribution

from higher stake

(49.85%)

Current FX hedging:

c. 60% of 2017

expected net

attributable profit

8.5 5.2 6.1

2.3 2.5

2013 2014 2015 2016E 2017E

2.7 2.8 2.8

2.7

2013 2014 2015 2016

30

13 19 17

2013 2014 2015 2016

139 116 111

87

101

2013 2014 2015 2016

3

Loans decelerating, but expected to grow at double digit in 2017

Resilient Economy1

(% YoY GDP growth) Prudent Risk

Management (NPL ratio, %)

Robust Loan Growth2

(% YoY, in constant €)

(Cumulative CoR, bps)

2017E c.110bps Garanti

MS European Financials Conference / 22

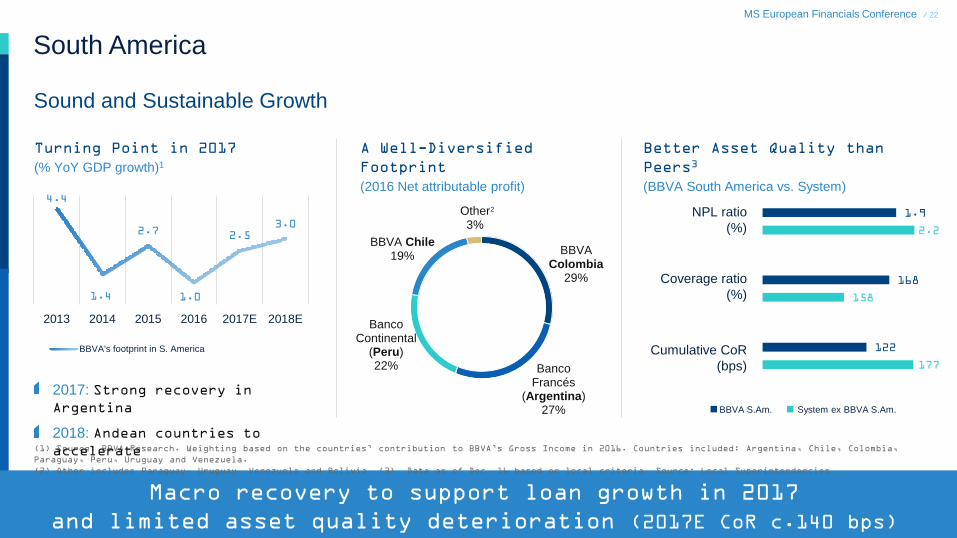

South America

Sound and Sustainable Growth

Turning Point in 2017

(% YoY GDP growth)1

A Well-Diversified

Footprint

(2016 Net attributable profit)

(1) Source: BBVA Research. Weighting based on the countries’ contribution to BBVA’s Gross Income in 2016. Countries included: Argentina, Chile, Colombia,

Paraguay, Peru, Uruguay and Venezuela.

(2) Other includes Paraguay, Uruguay, Venezuela and Bolivia. (3) Data as of Dec. 16 based on local criteria. Source: Local Superintendencies.

Better Asset Quality than

Peers3

(BBVA South America vs. System) 4.4

1.4

2.7

1.0

2.5 3.0

2013 2014 2015 2016 2017E 2018E

BBVA's footprint in S. America

2017: Strong recovery in

Argentina

2018: Andean countries to

accelerate

1.9

2.2

168

158

122

177

NPL ratio

(%)

Coverage ratio

(%)

Cumulative CoR

(bps)

BBVA S.Am. System ex BBVA S.Am.

Macro recovery to support loan growth in 2017

and limited asset quality deterioration (2017E CoR c.140 bps)

BBVA Colombia

29%

Banco Francés

(Argentina) 27%

Banco Continental

(Peru) 22%

BBVA Chile 19%

Other 3%

2

MS European Financials Conference / 23

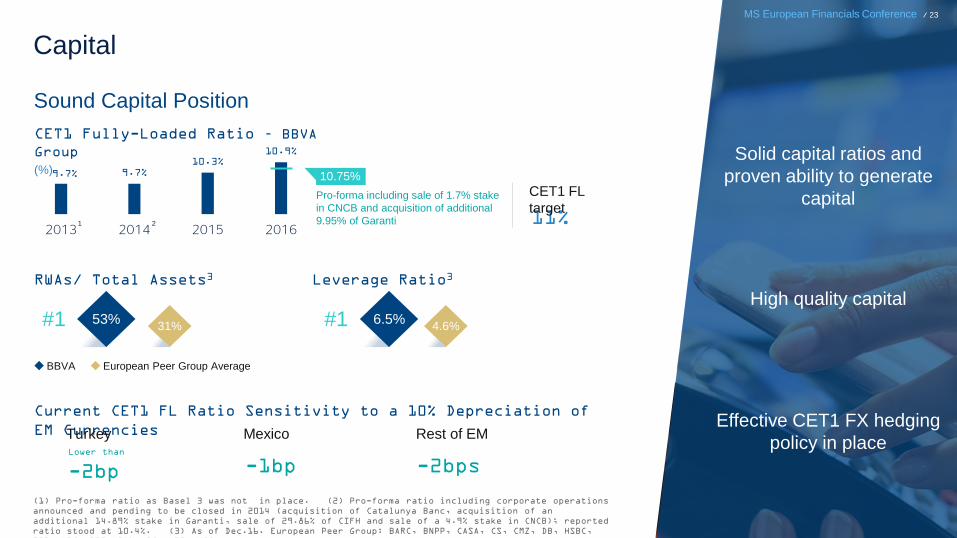

Capital

(1) Pro-forma ratio as Basel 3 was not in place. (2) Pro-forma ratio including corporate operations

announced and pending to be closed in 2014 (acquisition of Catalunya Banc, acquisition of an

additional 14.89% stake in Garanti, sale of 29.86% of CIFH and sale of a 4.9% stake in CNCB); reported

ratio stood at 10.4%. (3) As of Dec.16. European Peer Group: BARC, BNPP, CASA, CS, CMZ, DB, HSBC,

ISP, LBG, RBS, SAN, SG, UBS, UCG.

CET1 Fully-Loaded Ratio – BBVA

Group

(%) 9.7% 9.7%

10.3% 10.9%

2013 2014 2015 2016

Pro-forma including sale of 1.7% stake

in CNCB and acquisition of additional

9.95% of Garanti

10.75%

53% 31%

RWAs/ Total Assets3

6.5% 4.6%

Leverage Ratio3

European Peer Group Average BBVA

Current CET1 FL Ratio Sensitivity to a 10% Depreciation of

EM Currencies

#1 #1

Turkey Rest of EM Lower than

-2bp

Mexico

-1bp -2bps

Sound Capital Position

1 2 11%

CET1 FL

target

MS European Financials Conference / 23

Solid capital ratios and

proven ability to generate

capital

High quality capital

Effective CET1 FX hedging

policy in place

MS European Financials Conference / 24

03 Final Remarks

MS European Financials Conference / 25

Final Remarks

Strategy: A clear strategic path around our purpose

and six strategic priorities

Execution: Progressing on our transformation

journey leveraging data and technology to support our

clients and customers in their life and business

Earnings Power: Well positioned in this environment to

take advantage of the market opportunities

1

2

3

Diversified footprint

Prudent risk profile

Sound capital position

MS European Financials Conference / 25

MS European Financials Conference / 26

Delivering on our Strategy London, March 21st 2017

Carlos Torres Vila Chief Executive

Officer