Embed Size (px)

Citation preview

European Investment Bank Page 1

TBLI NORDIC June 2015 Conference

Peter MUNRO, Head of Investor Relations, EIB

© BEWAG

Green Bonds – market & energy transition

European Investment Bank Page 2

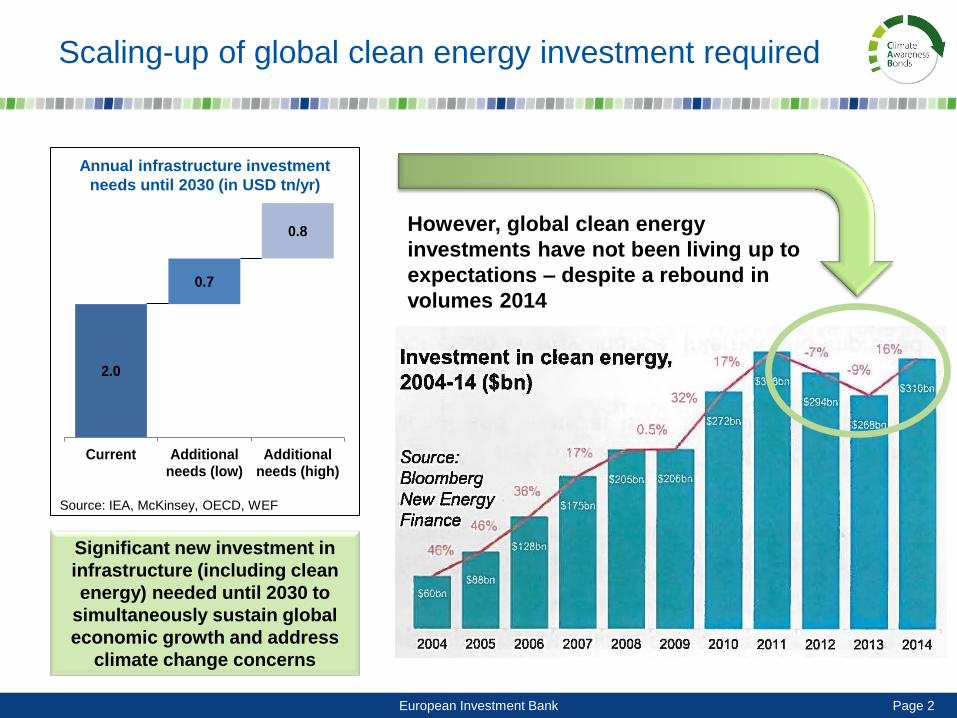

Scaling-up of global clean energy investment required

2.0

0.7

0.8

Current Additionalneeds (low)

Additionalneeds (high)

Source: IEA, McKinsey, OECD, WEF

Annual infrastructure investment

needs until 2030 (in USD tn/yr)

However, global clean energy

investments have not been living up to

expectations – despite a rebound in

volumes 2014

Significant new investment in

infrastructure (including clean

energy) needed until 2030 to

simultaneously sustain global

economic growth and address

climate change concerns

European Investment Bank Page 3

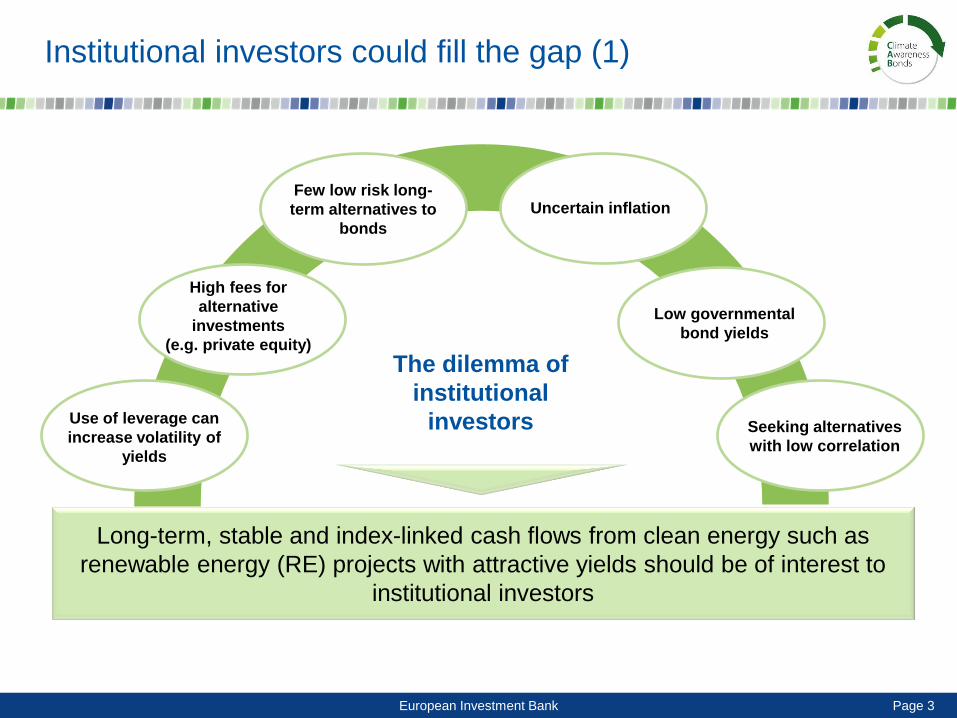

Institutional investors could fill the gap (1)

3

Few low risk long-

term alternatives to

bonds

High fees for

alternative

investments

(e.g. private equity)

The dilemma of

institutional

investors

Uncertain inflation

Low governmental

bond yields

Use of leverage can

increase volatility of

yields

Seeking alternatives

with low correlation

Long-term, stable and index-linked cash flows from clean energy such as

renewable energy (RE) projects with attractive yields should be of interest to

institutional investors

European Investment Bank Page 4

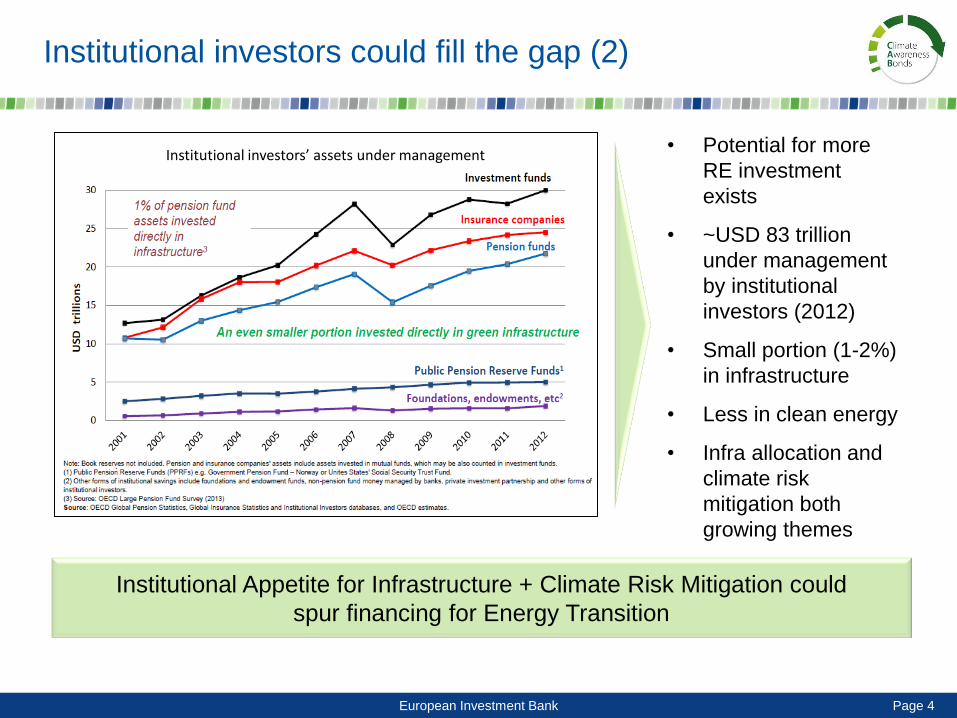

Institutional investors could fill the gap (2)

4

Institutional Appetite for Infrastructure + Climate Risk Mitigation could

spur financing for Energy Transition

Institutional investors’ assets under management • Potential for more

RE investment

exists

• ~USD 83 trillion

under management

by institutional

investors (2012)

• Small portion (1-2%)

in infrastructure

• Less in clean energy

• Infra allocation and

climate risk

mitigation both

growing themes

European Investment Bank Page 5

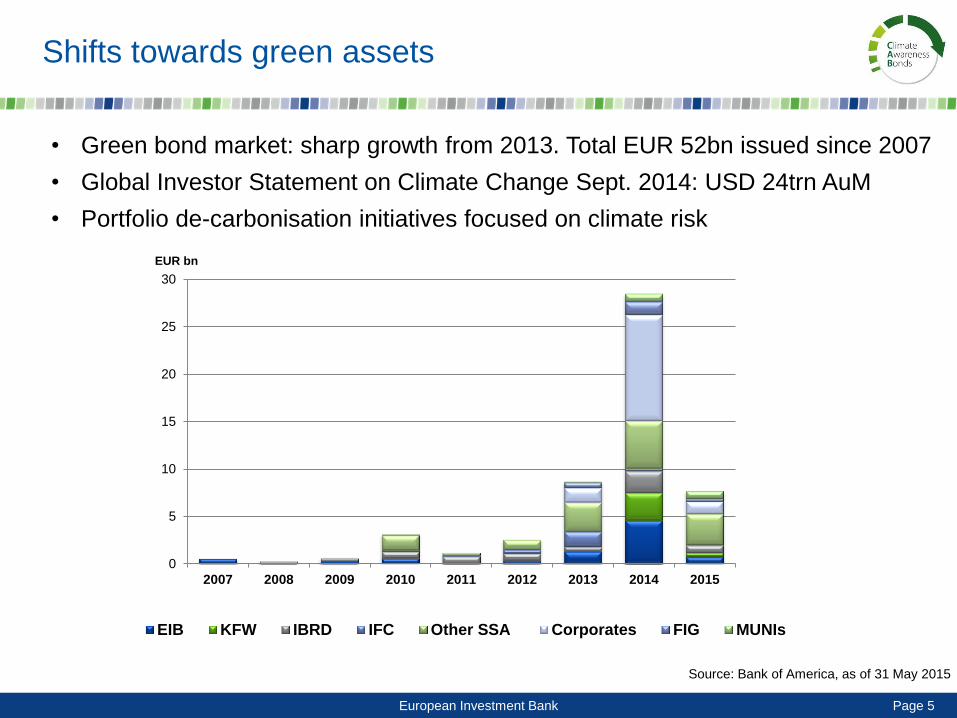

Shifts towards green assets

• Green bond market: sharp growth from 2013. Total EUR 52bn issued since 2007

• Global Investor Statement on Climate Change Sept. 2014: USD 24trn AuM

• Portfolio de-carbonisation initiatives focused on climate risk

Source: Bank of America, as of 31 May 2015

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014 2015

EIB KFW IBRD IFC Other SSA Corporates FIG MUNIs

EUR bn

European Investment Bank Page 6

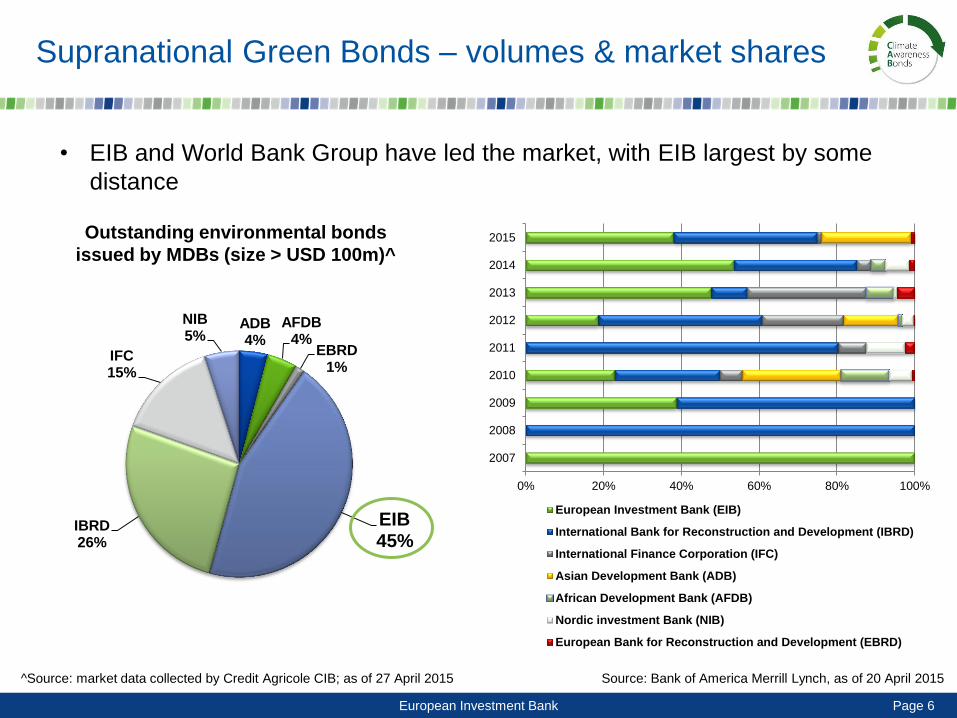

0% 20% 40% 60% 80% 100%

2007

2008

2009

2010

2011

2012

2013

2014

2015

European Investment Bank (EIB)

International Bank for Reconstruction and Development (IBRD)

International Finance Corporation (IFC)

Asian Development Bank (ADB)

African Development Bank (AFDB)

Nordic investment Bank (NIB)

European Bank for Reconstruction and Development (EBRD)

Source: Bank of America Merrill Lynch, as of 20 April 2015

Supranational Green Bonds – volumes & market shares

ADB 4%

AFDB 4%

EBRD 1%

EIB 45%

IBRD 26%

IFC 15%

NIB 5%

Outstanding environmental bonds

issued by MDBs (size > USD 100m)^

^Source: market data collected by Credit Agricole CIB; as of 27 April 2015

• EIB and World Bank Group have led the market, with EIB largest by some

distance

European Investment Bank Page 7

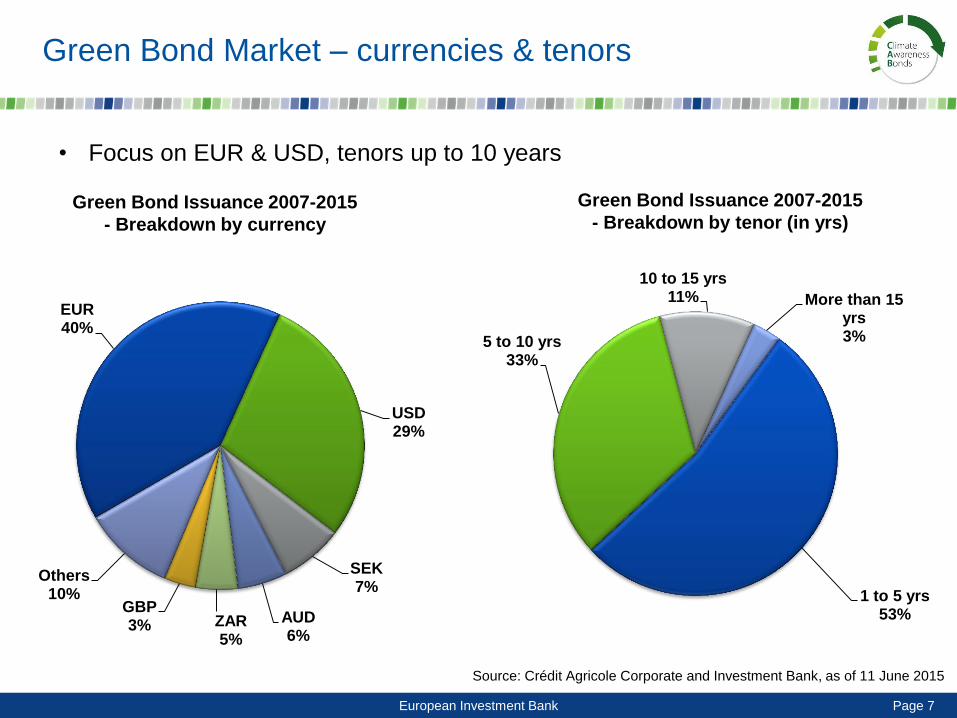

Green Bond Issuance 2007-2015

- Breakdown by currency

Source: Crédit Agricole Corporate and Investment Bank, as of 11 June 2015

Green Bond Issuance 2007-2015

- Breakdown by tenor (in yrs)

Green Bond Market – currencies & tenors

• Focus on EUR & USD, tenors up to 10 years

EUR 40%

USD 29%

SEK 7%

AUD 6%

ZAR 5%

GBP 3%

Others 10% 1 to 5 yrs

53%

5 to 10 yrs 33%

10 to 15 yrs 11% More than 15

yrs 3%

European Investment Bank Page 8

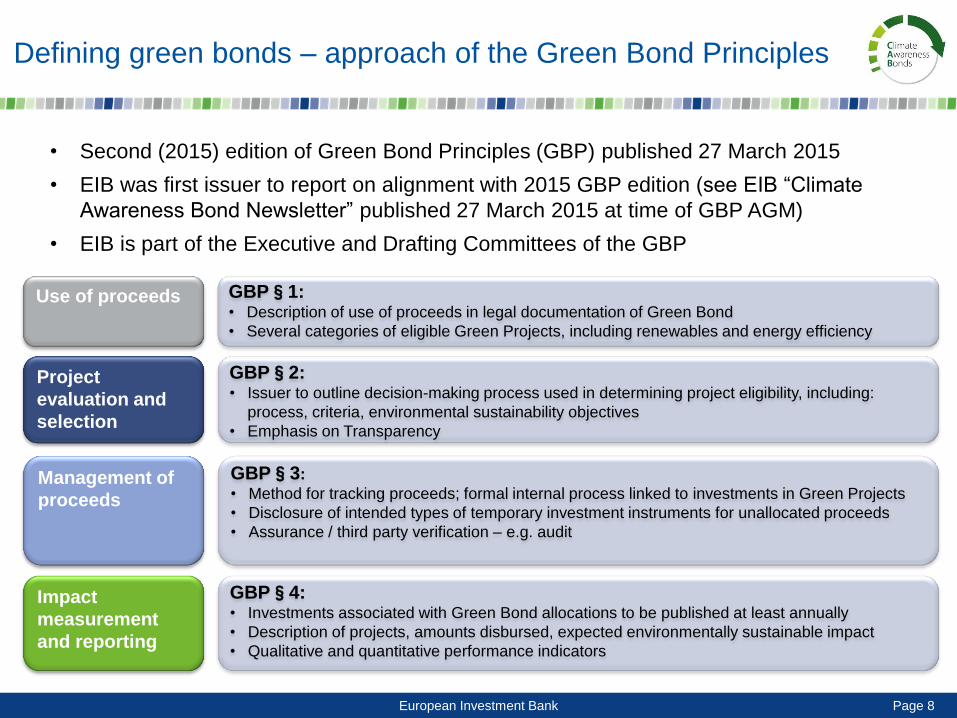

Defining green bonds – approach of the Green Bond Principles

Project evaluation

and selection

Management of

proceeds

• Second (2015) edition of Green Bond Principles (GBP) published 27 March 2015

• EIB was first issuer to report on alignment with 2015 GBP edition (see EIB “Climate

Awareness Bond Newsletter” published 27 March 2015 at time of GBP AGM)

• EIB is part of the Executive and Drafting Committees of the GBP

GBP§1: • Description of use of proceeds in legal documentation of Green Bond

• Several categories of eligible Green Projects, including renewables and energy efficiency

GBP§2: • Issuer to outline decision-making process used in determining project eligibility, including:

process, criteria, environmental sustainability objectives

• Emphasis on Transparency

GBP§3:

• Method for tracking proceeds; formal internal process linked to investments in Green Projects

• Disclosure of intended types of temporary investment instruments for unallocated proceeds

• Assurance / third party verification – e.g. audit

GBP§4: • Investments associated with Green Bond allocations to be published at least annually

• Description of projects, amounts disbursed, expected environmentally sustainable impact

• Qualitative and quantitative performance indicators

Use of proceeds

Project

evaluation and

selection

Management of

proceeds

Impact

measurement

and reporting

European Investment Bank Page 9

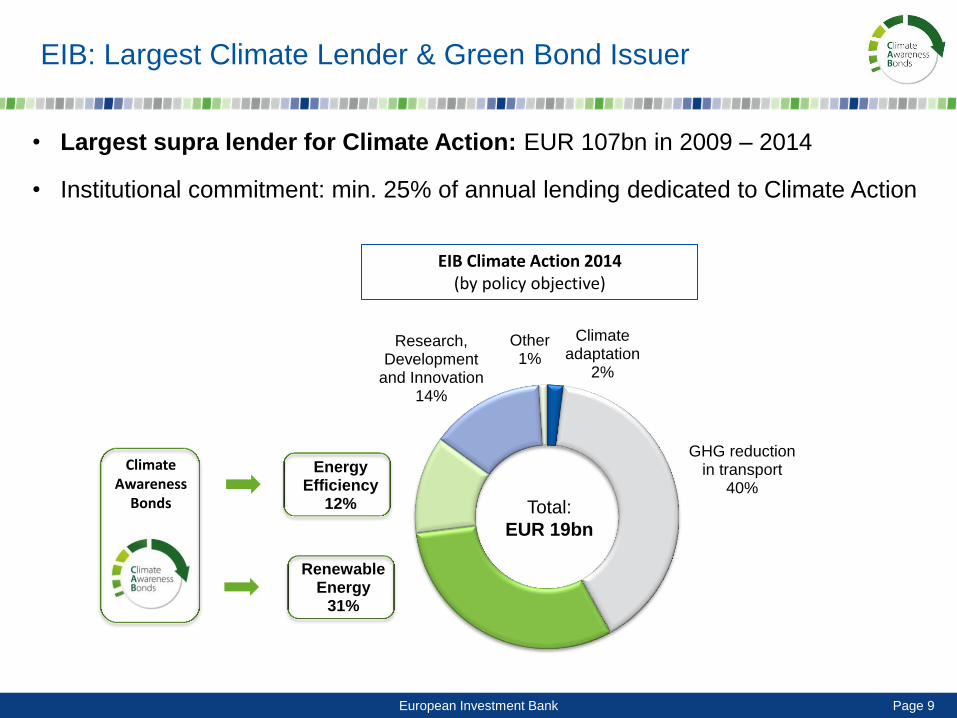

• Largest supra lender for Climate Action: EUR 107bn in 2009 – 2014

• Institutional commitment: min. 25% of annual lending dedicated to Climate Action

EIB: Largest Climate Lender & Green Bond Issuer

Climate Awareness

Bonds

EIB Climate Action 2014 (by policy objective)

Climate adaptation

2%

GHG reduction in transport

40%

Renewable Energy

31%

Energy Efficiency

12%

Research, Development

and Innovation 14%

Other 1%

Total:

EUR 19bn

European Investment Bank Page 10

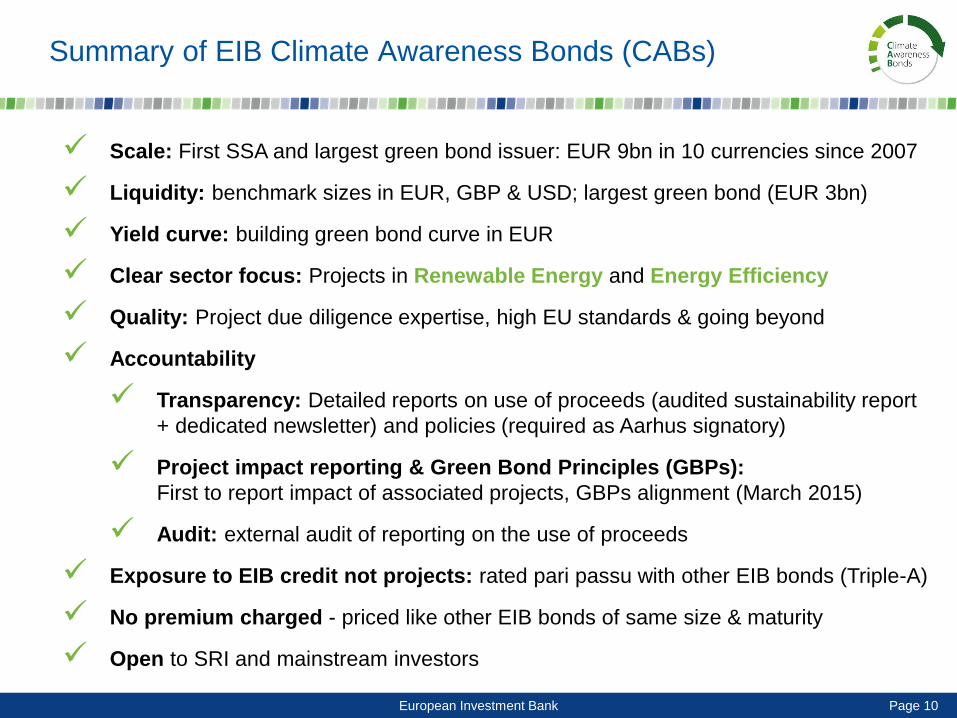

Summary of EIB Climate Awareness Bonds (CABs)

Scale: First SSA and largest green bond issuer: EUR 9bn in 10 currencies since 2007

Liquidity: benchmark sizes in EUR, GBP & USD; largest green bond (EUR 3bn)

Yield curve: building green bond curve in EUR

Clear sector focus: Projects in Renewable Energy and Energy Efficiency

Quality: Project due diligence expertise, high EU standards & going beyond

Accountability

Transparency: Detailed reports on use of proceeds (audited sustainability report

+ dedicated newsletter) and policies (required as Aarhus signatory)

Project impact reporting & Green Bond Principles (GBPs):

First to report impact of associated projects, GBPs alignment (March 2015)

Audit: external audit of reporting on the use of proceeds

Exposure to EIB credit not projects: rated pari passu with other EIB bonds (Triple-A)

No premium charged - priced like other EIB bonds of same size & maturity

Open to SRI and mainstream investors

European Investment Bank Page 11

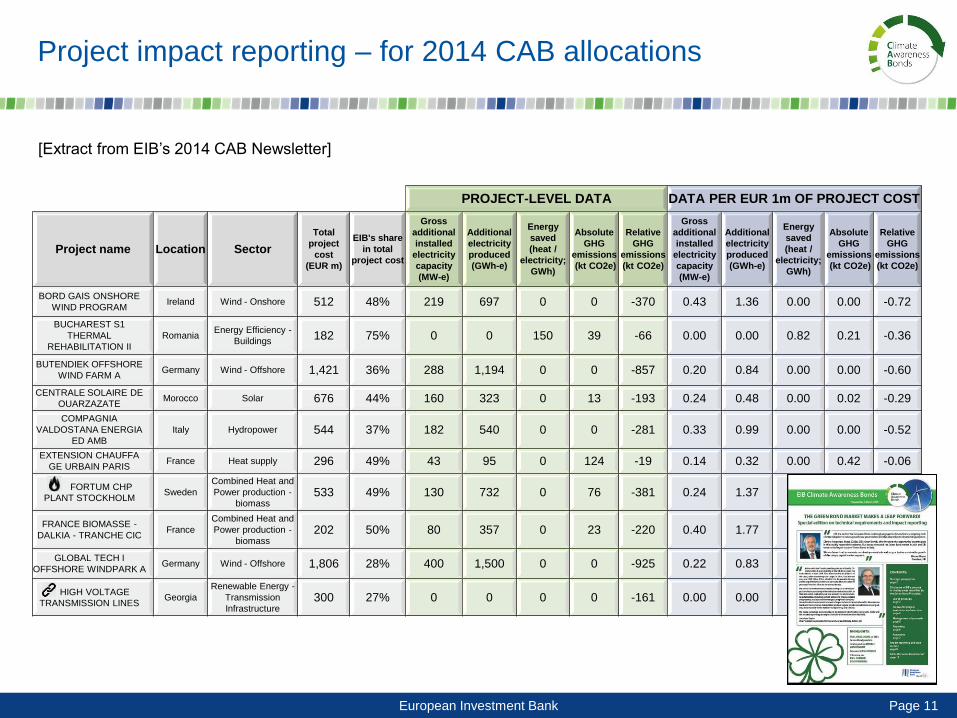

Project impact reporting – for 2014 CAB allocations

PROJECT-LEVEL DATA DATA PER EUR 1m OF PROJECT COST

Project name Location Sector

Total

project

cost

(EUR m)

EIB's share

in total

project cost

Gross

additional

installed

electricity

capacity

(MW-e)

Additional

electricity

produced

(GWh-e)

Energy

saved

(heat /

electricity;

GWh)

Absolute

GHG

emissions

(kt CO2e)

Relative

GHG

emissions

(kt CO2e)

Gross

additional

installed

electricity

capacity

(MW-e)

Additional

electricity

produced

(GWh-e)

Energy

saved

(heat /

electricity;

GWh)

Absolute

GHG

emissions

(kt CO2e)

Relative

GHG

emissions

(kt CO2e)

BORD GAIS ONSHORE

WIND PROGRAM Ireland Wind - Onshore 512 48% 219 697 0 0 -370 0.43 1.36 0.00 0.00 -0.72

BUCHAREST S1

THERMAL

REHABILITATION II

Romania Energy Efficiency -

Buildings 182 75% 0 0 150 39 -66 0.00 0.00 0.82 0.21 -0.36

BUTENDIEK OFFSHORE

WIND FARM A Germany Wind - Offshore 1,421 36% 288 1,194 0 0 -857 0.20 0.84 0.00 0.00 -0.60

CENTRALE SOLAIRE DE

OUARZAZATE Morocco Solar 676 44% 160 323 0 13 -193 0.24 0.48 0.00 0.02 -0.29

COMPAGNIA

VALDOSTANA ENERGIA

ED AMB

Italy Hydropower 544 37% 182 540 0 0 -281 0.33 0.99 0.00 0.00 -0.52

EXTENSION CHAUFFA

GE URBAIN PARIS France Heat supply 296 49% 43 95 0 124 -19 0.14 0.32 0.00 0.42 -0.06

FORTUM CHP

PLANT STOCKHOLM Sweden

Combined Heat and

Power production -

biomass 533 49% 130 732 0 76 -381 0.24 1.37 0.00 0.14 -0.71

FRANCE BIOMASSE -

DALKIA - TRANCHE CIC France

Combined Heat and

Power production -

biomass 202 50% 80 357 0 23 -220 0.40 1.77 0.00 0.11 -1.09

GLOBAL TECH I

OFFSHORE WINDPARK A Germany Wind - Offshore 1,806 28% 400 1,500 0 0 -925 0.22 0.83 0.00 0.00 -0.51

HIGH VOLTAGE

TRANSMISSION LINES Georgia

Renewable Energy -

Transmission

Infrastructure 300 27% 0 0 0 0 -161 0.00 0.00 0.00 0.00 -0.54

[Extract from EIB’s 2014 CAB Newsletter]

European Investment Bank Page 12

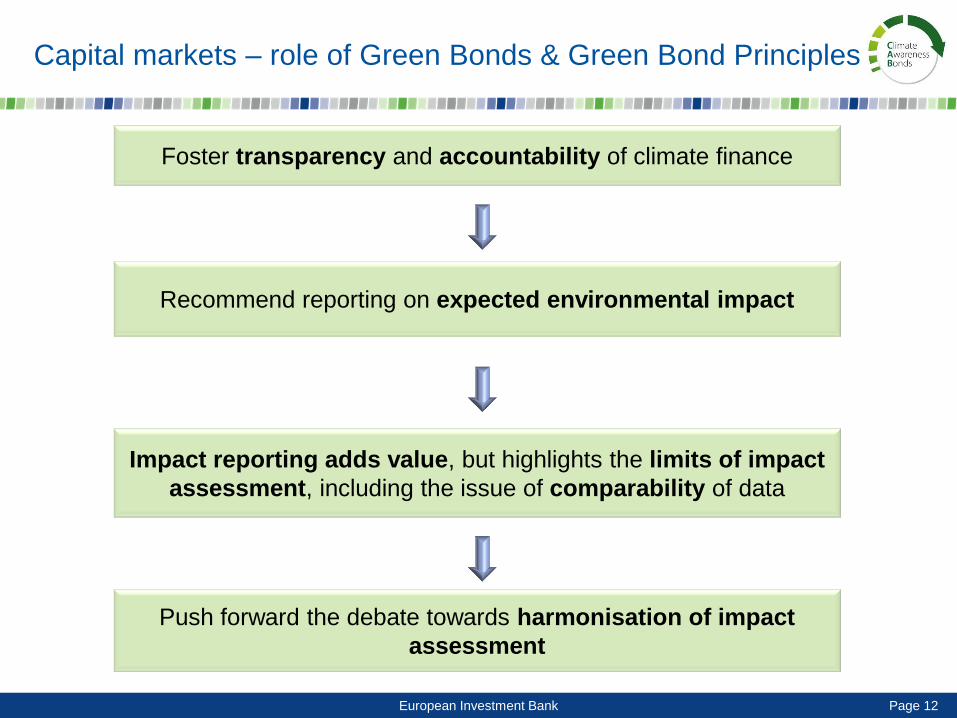

Capital markets – role of Green Bonds & Green Bond Principles

Foster transparency and accountability of climate finance

Recommend reporting on expected environmental impact

Impact reporting adds value, but highlights the limits of impact

assessment, including the issue of comparability of data

Push forward the debate towards harmonisation of impact

assessment

European Investment Bank Page 13

Green Bond market – challenges & opportunities

Governance and Product Quality:

Balance between flexibility and stringency => Green Bond Principles

Authoritative Indicators & Arbiters for Environmental Performance

Harmonisation of assessment and reporting

Drivers of market development:

Structural:

Policy: Global (G7, UNFCCC/COP21), Regional (e.g. EU) & National

Imperatives and ? Incentives

Demand from asset owners

Financial: learning from conventional bonds

Portfolio performance (risk mitigation, evidence of historical returns)

Supply: flow, benchmarks / liquidity, name and credit diversification

Pricing: fiduciary duty to optimise, potential of green yield curves

European Investment Bank Page 14

European Investment Bank

100, bd. Konrad Adenauer L-2950 Luxembourg

www.eib.org

Contacts

General enquiries on EIB bonds:

Peter Munro

Head of Investor Relations

Tel: +352 4379 88457