Embed Size (px)

Citation preview

1

Webinar with Chief Economist and

CIO, Saxo Bank, Steen Jakobsen

2

Housekeeping

This webinar will run for 40 minutes, inclusive of questions.

Please ask questions at any time. Where we can, we’ll answer them as we go.

This webinar will be recorded.

Please take the time at the end of the webinar to complete our feedback questionnaire.

This webinar contains general advice only and does not take into account your, or anybody else's, investment objectives, financial situation or needs. Please see the full disclaimer on our website www.rivkin.com.au.

3

About the presenter and host

Steen Jakobsen

Chief Economist and CIO, Saxo Bank

Oliver Gordon

Global Investment Director, Rivkin

Deflation: The Elephant in the room for the AUD housing boomAustralia, November 2015, Saxo Bank A/S

5

How bad is it?

6

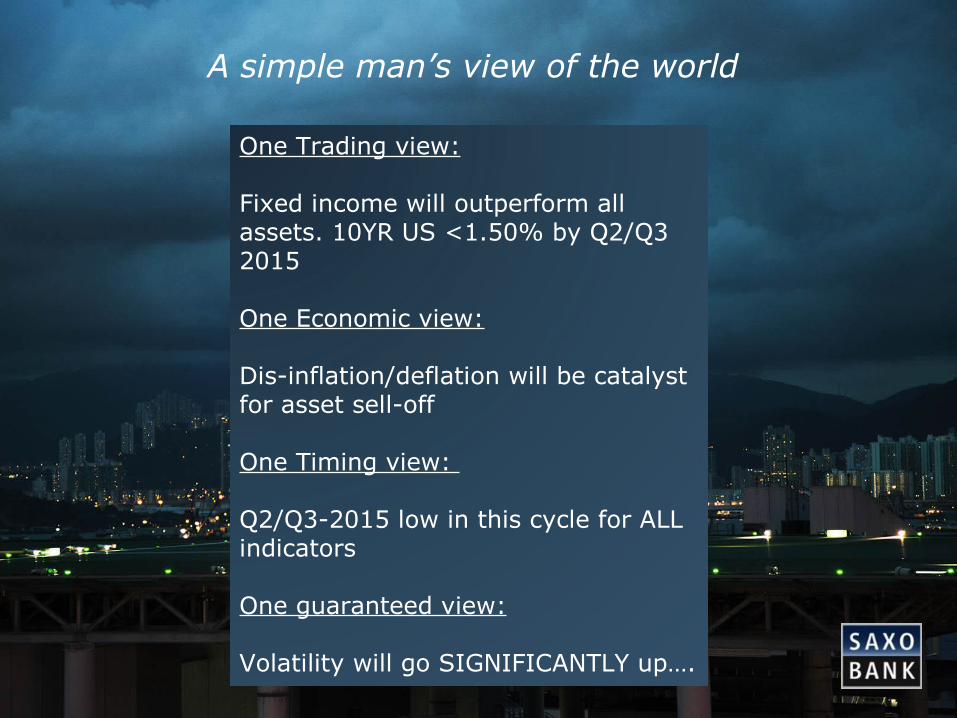

Macro core view

One Trading view:

Fixed income will outperform all assets. 10YR US <1.50% by Q2/Q3 2015

One Economic view:

Dis-inflation/deflation will be catalyst for asset sell-off

One Timing view:

Q2/Q3-2015 low in this cycle for ALL indicators

One guaranteed view:

Volatility will go SIGNIFICANTLY up….

A simple man’s view of the world

7

Our biggest call: Yields will go to new lows..

8

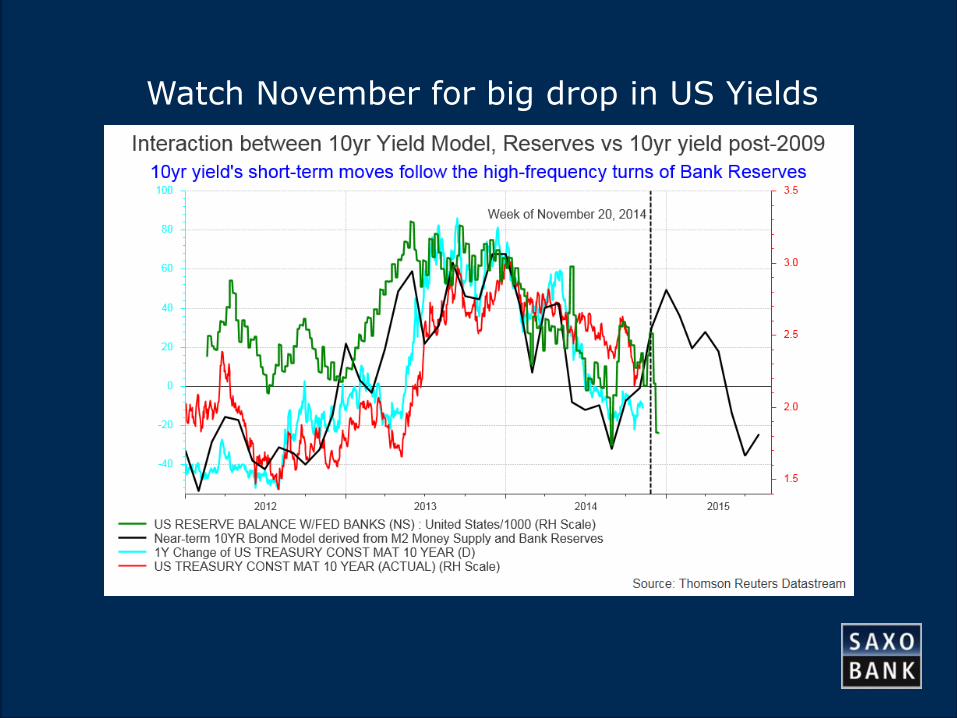

Watch November for big drop in US Yields

9

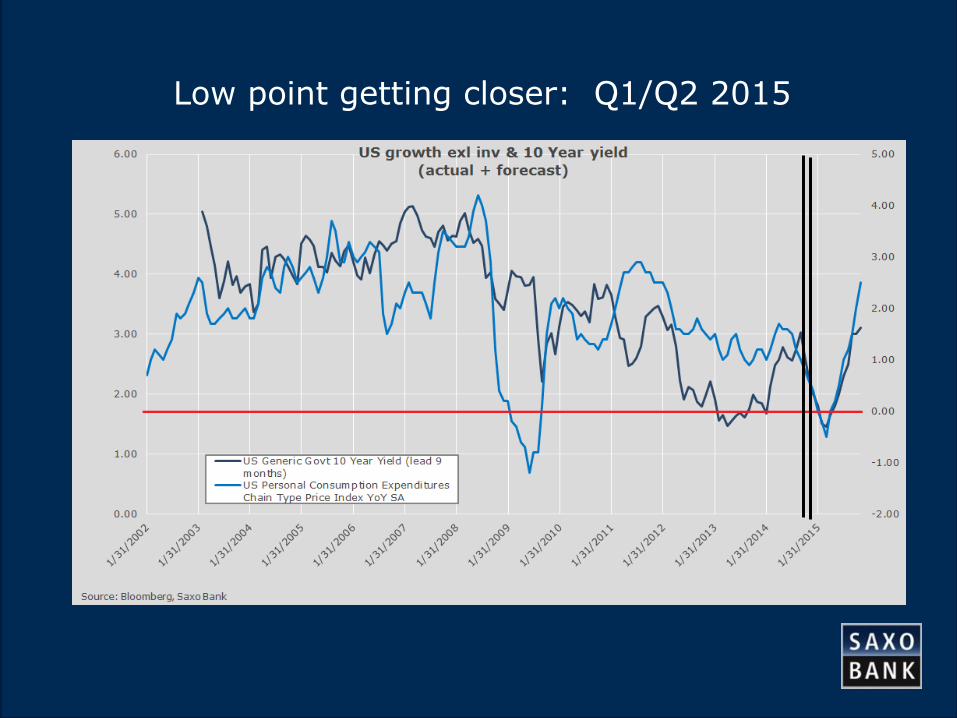

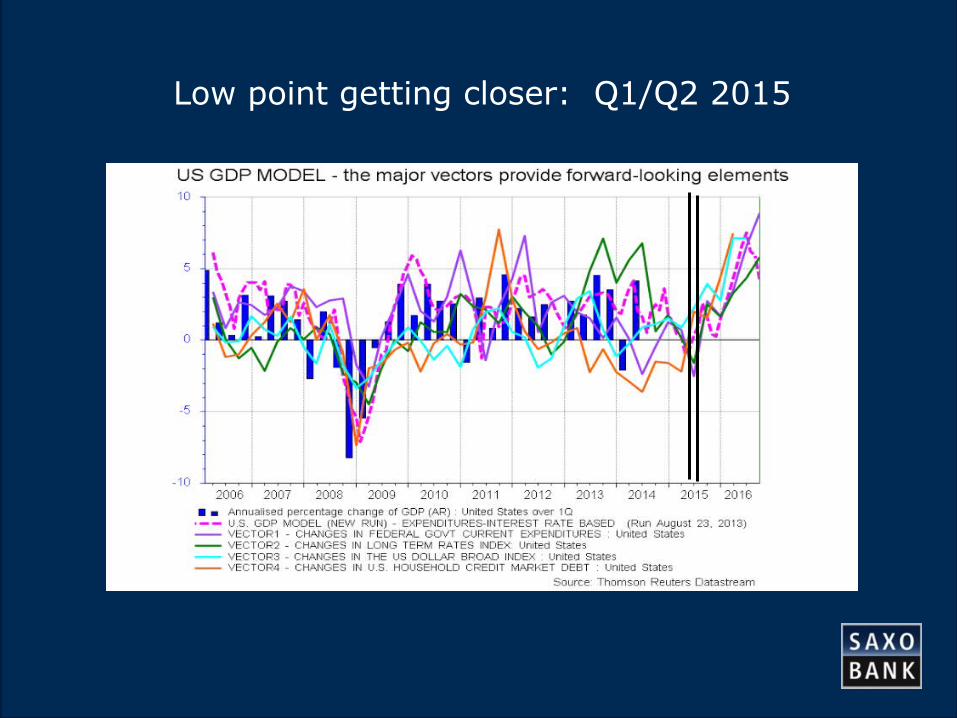

Low point getting closer: Q1/Q2 2015

10

Low point getting closer: Q1/Q2 2015

11

The Economic Bermuda Triangle

Steen Jakobsen’s Economic Theory – Where is my Nobel Prize?

12

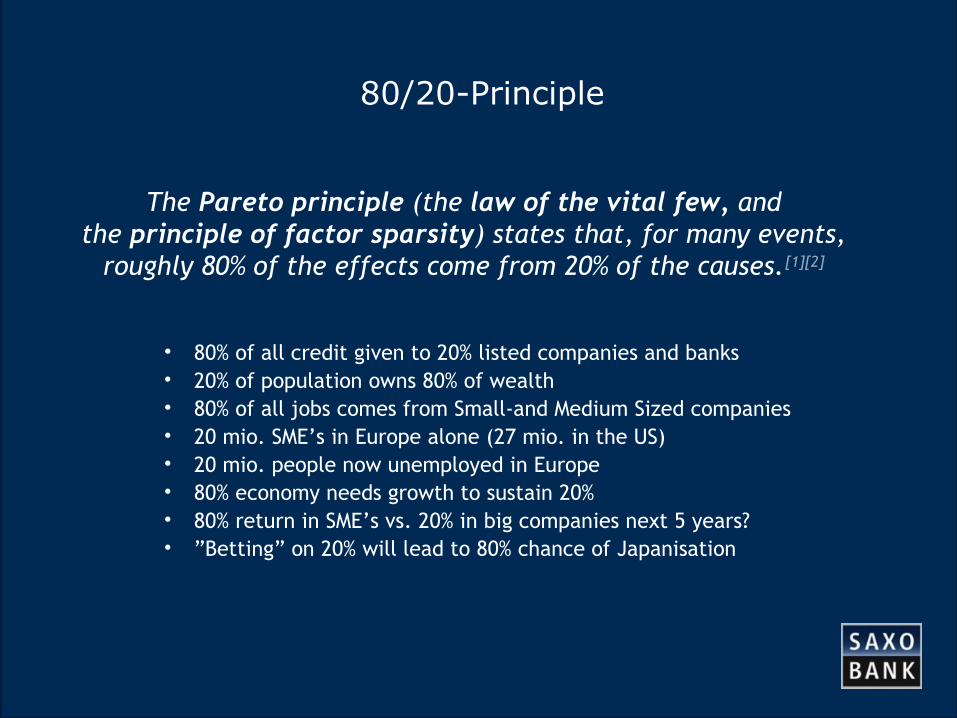

80/20-Principle

The Pareto principle (the law of the vital few, and the principle of factor sparsity) states that, for many events,

roughly 80% of the effects come from 20% of the causes.[1][2]

• 80% of all credit given to 20% listed companies and banks• 20% of population owns 80% of wealth• 80% of all jobs comes from Small-and Medium Sized companies• 20 mio. SME’s in Europe alone (27 mio. in the US)• 20 mio. people now unemployed in Europe • 80% economy needs growth to sustain 20% • 80% return in SME’s vs. 20% in big companies next 5 years?• ”Betting” on 20% will lead to 80% chance of Japanisation

Where does growth go from here?

14

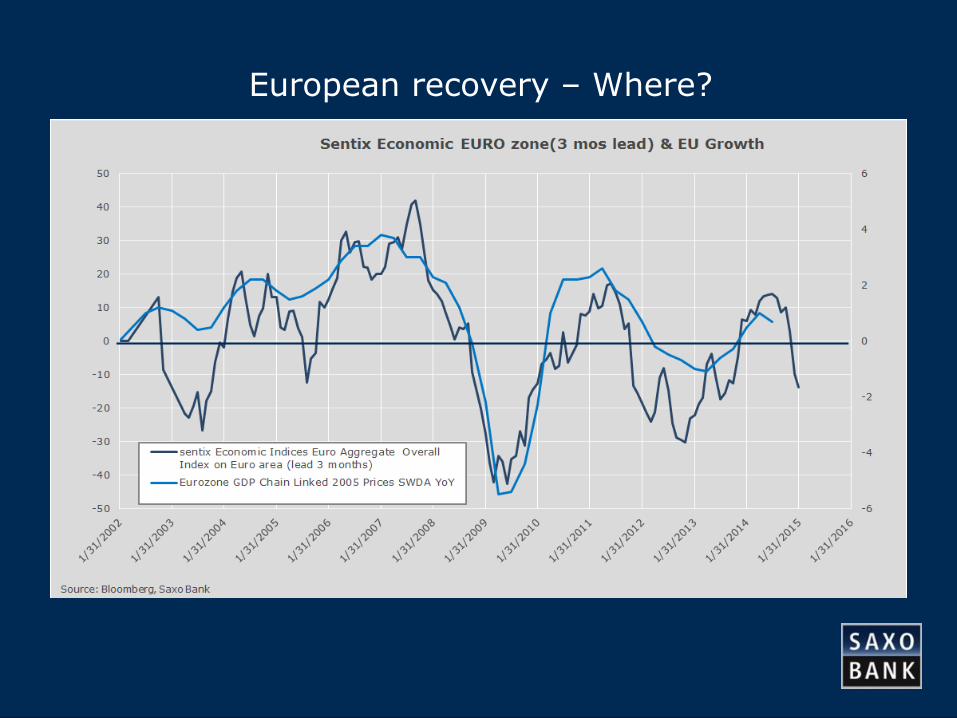

European recovery – Where?

15

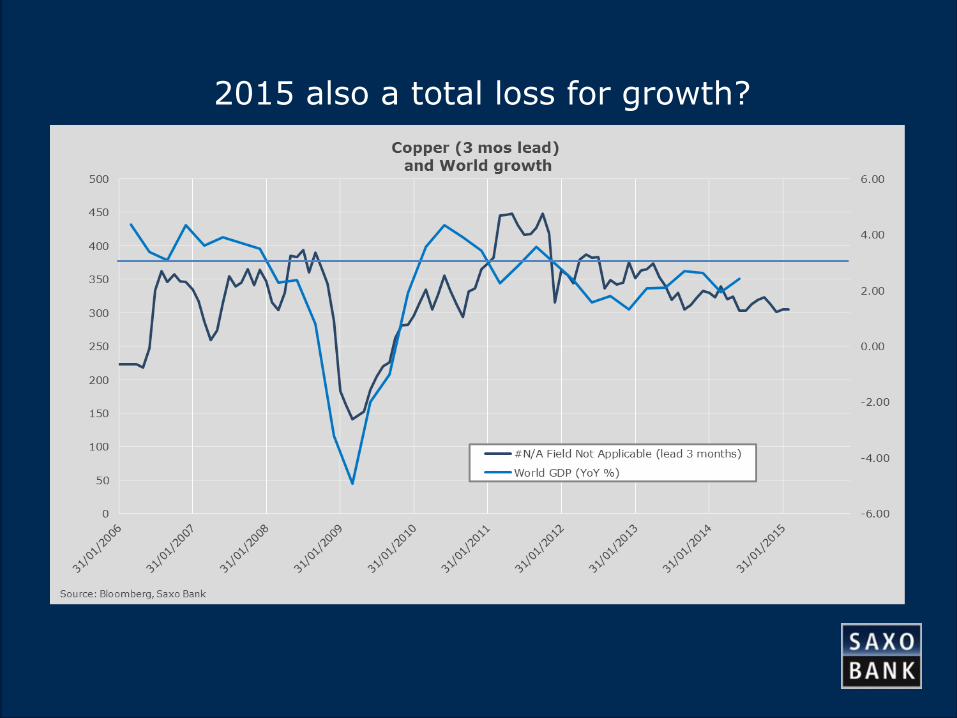

2015 also a total loss for growth?

16

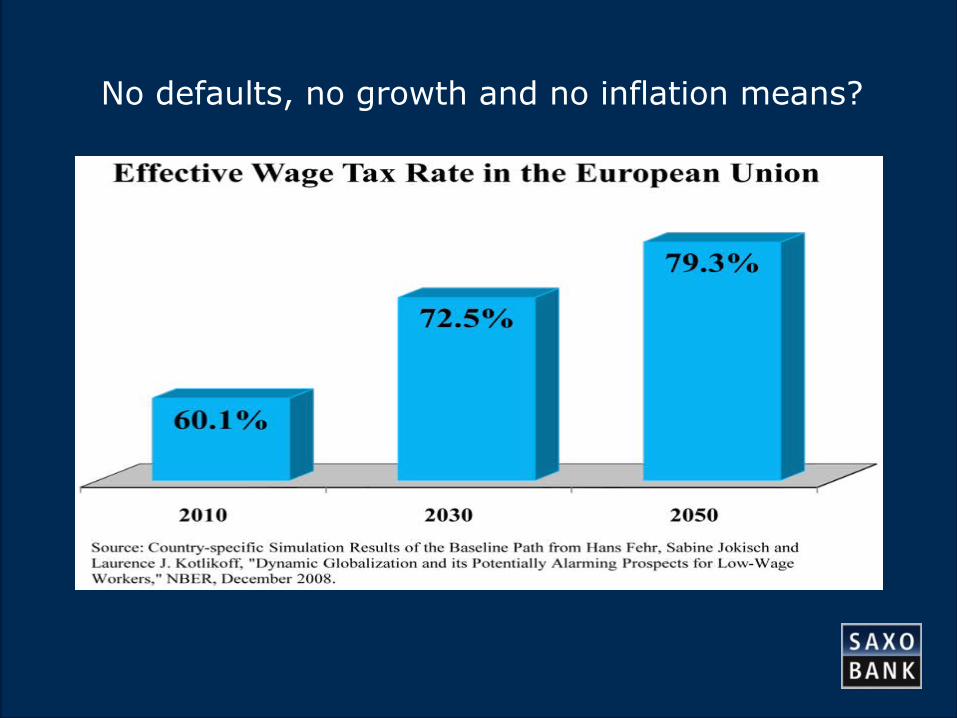

No defaults, no growth and no inflation means?

17

Minsky moment

18

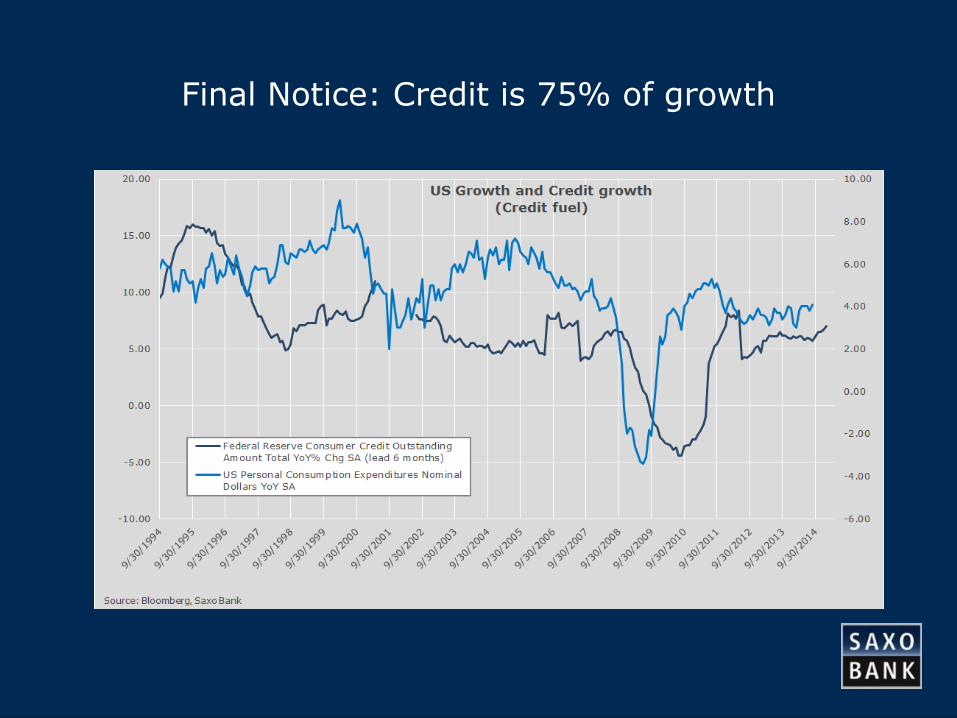

Final Notice: Credit is 75% of growth

19

Deflation: The death of status quo

20

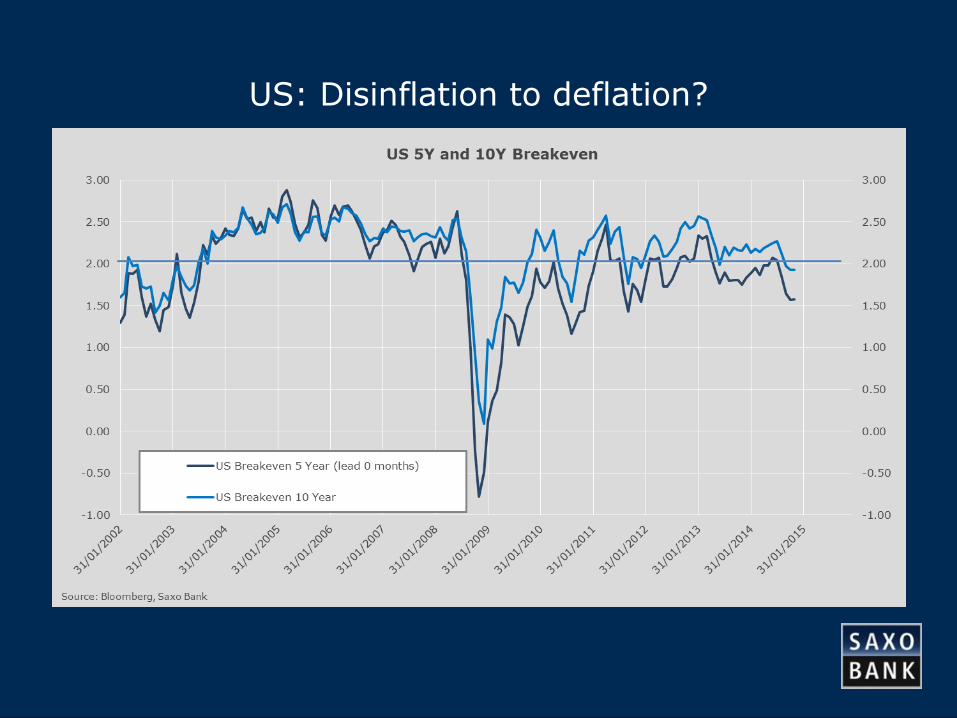

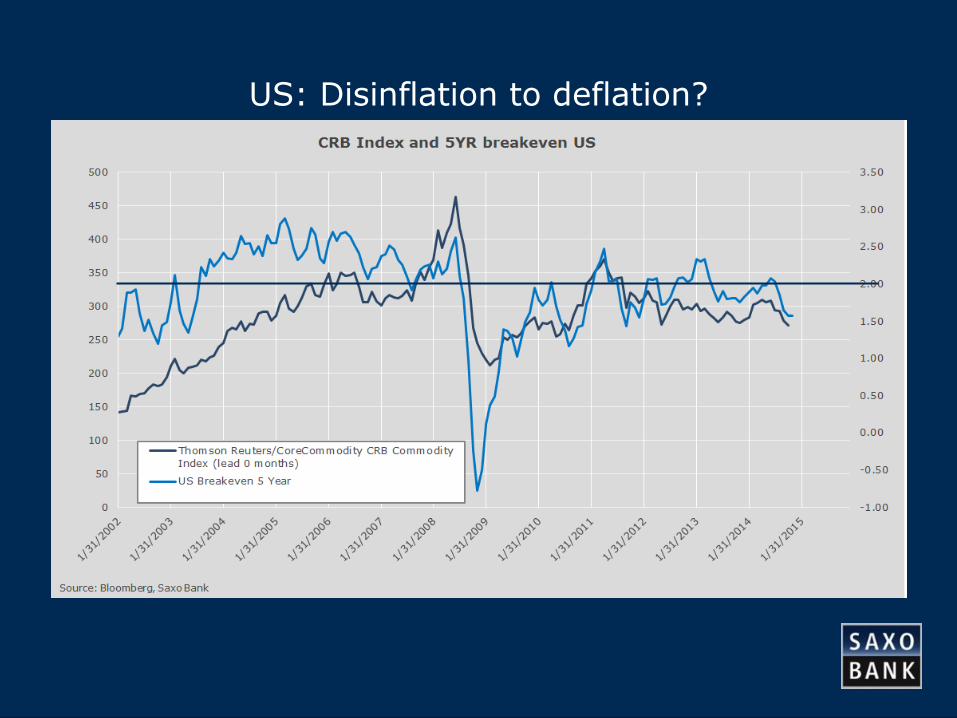

US: Disinflation to deflation?

21

US: Disinflation to deflation?

22

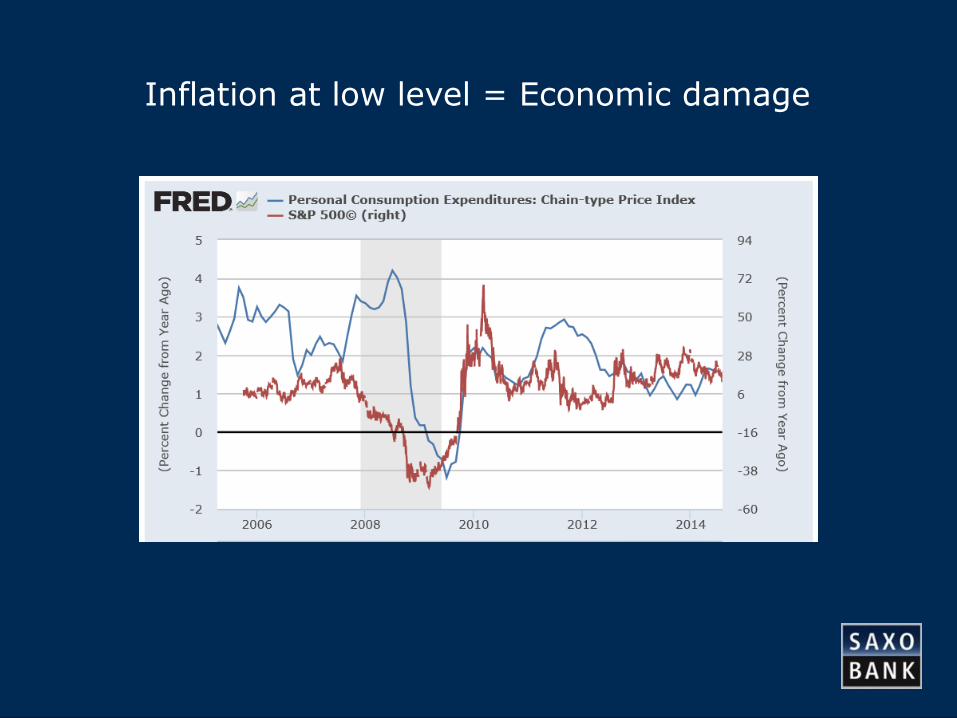

Inflation at low level = Economic damage

23

ECB – final round with Draghi and easy money?

24

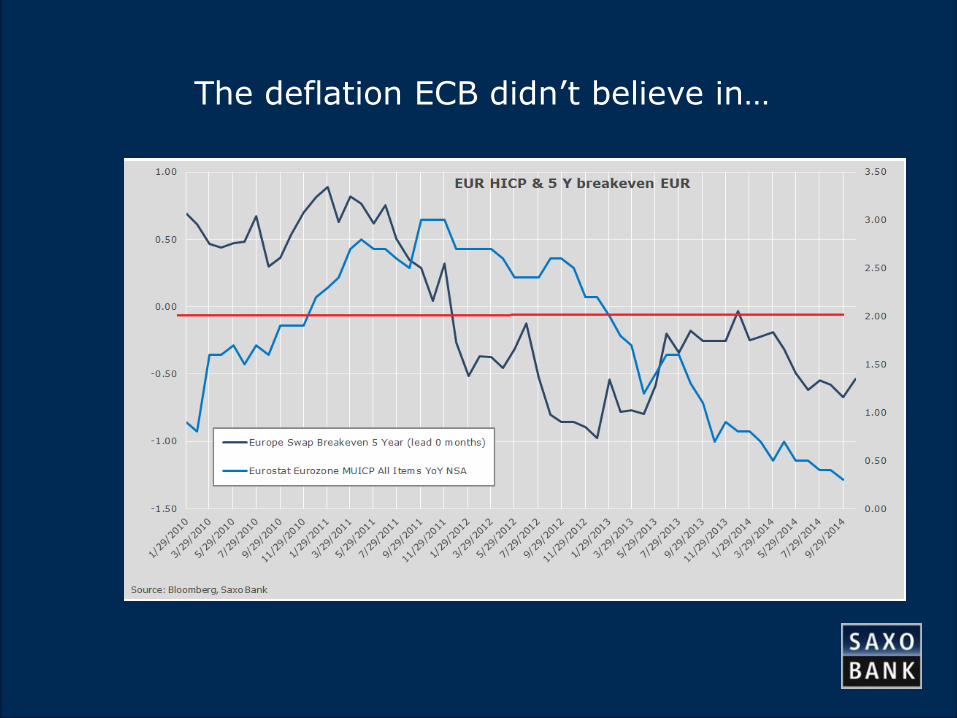

The deflation ECB didn’t believe in…

25

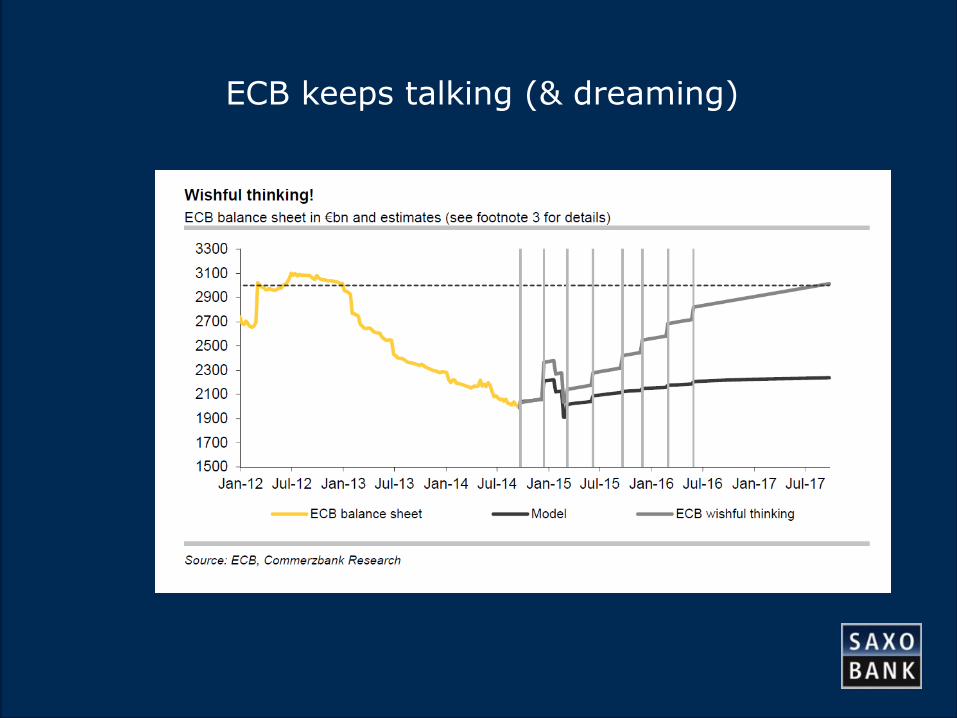

ECB keeps talking (& dreaming)

26

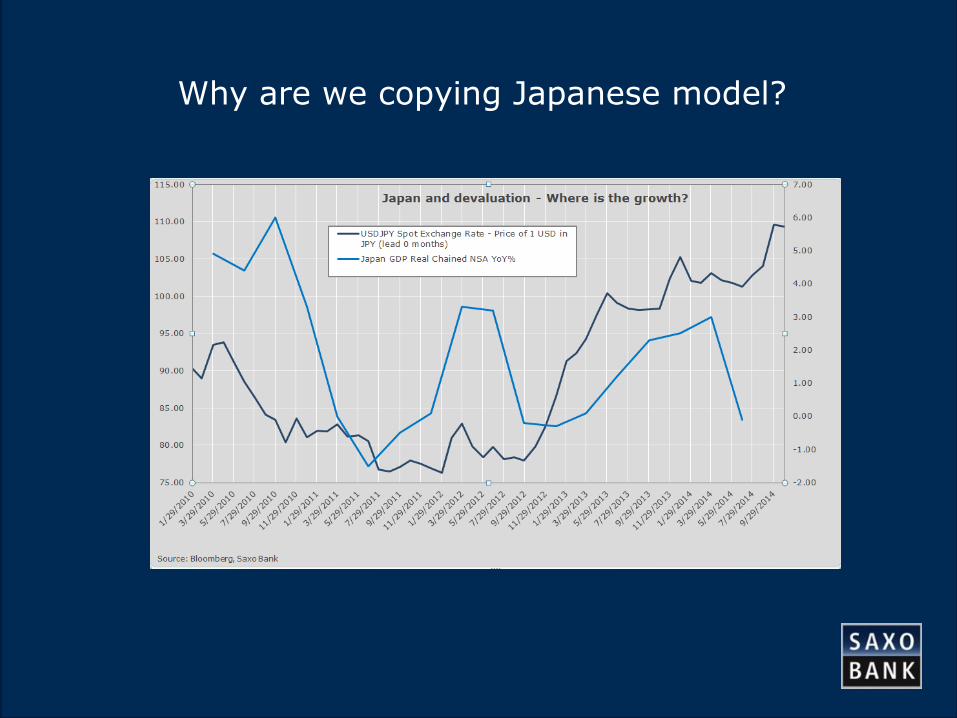

Why are we copying Japanese model?

27

Australia:A one trick economy

with outsized risk

28

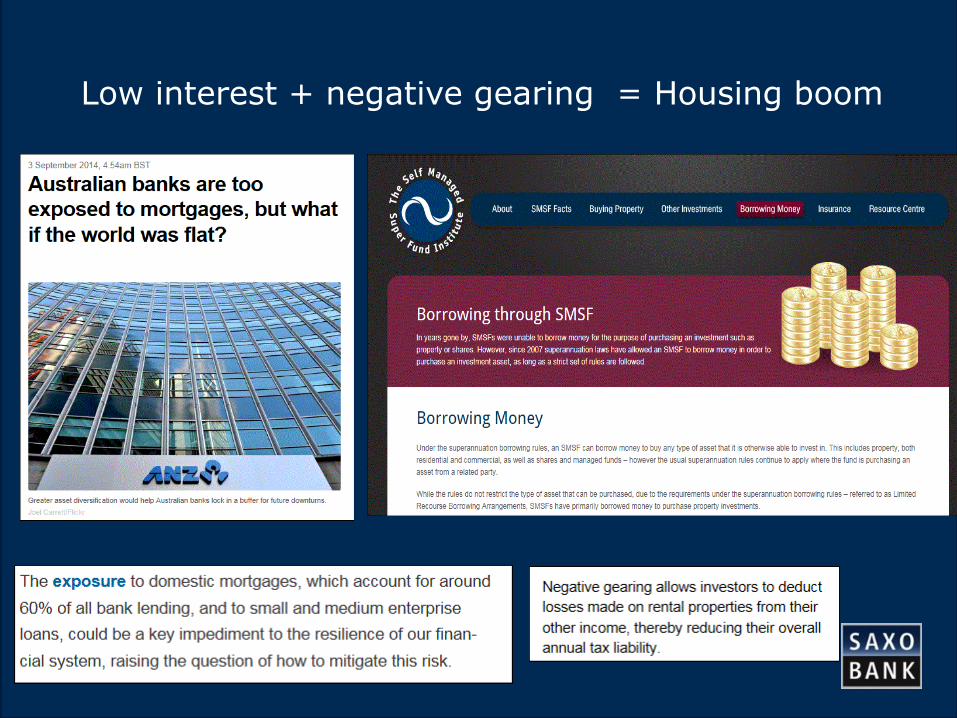

Low interest + negative gearing = Housing boom

29

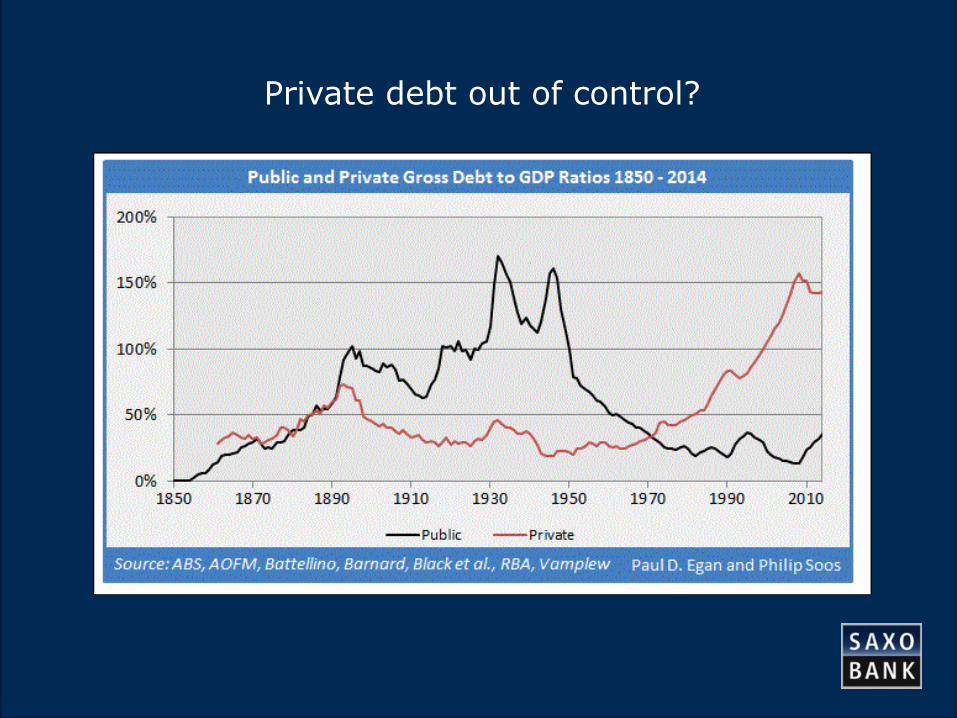

Private debt out of control?

30

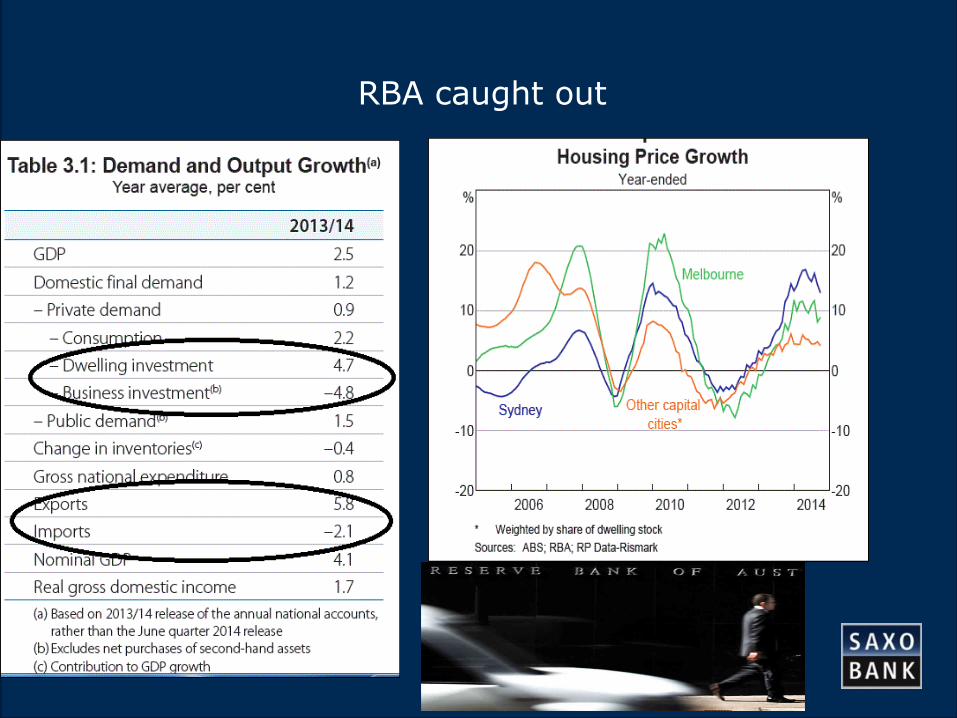

RBA caught out

31

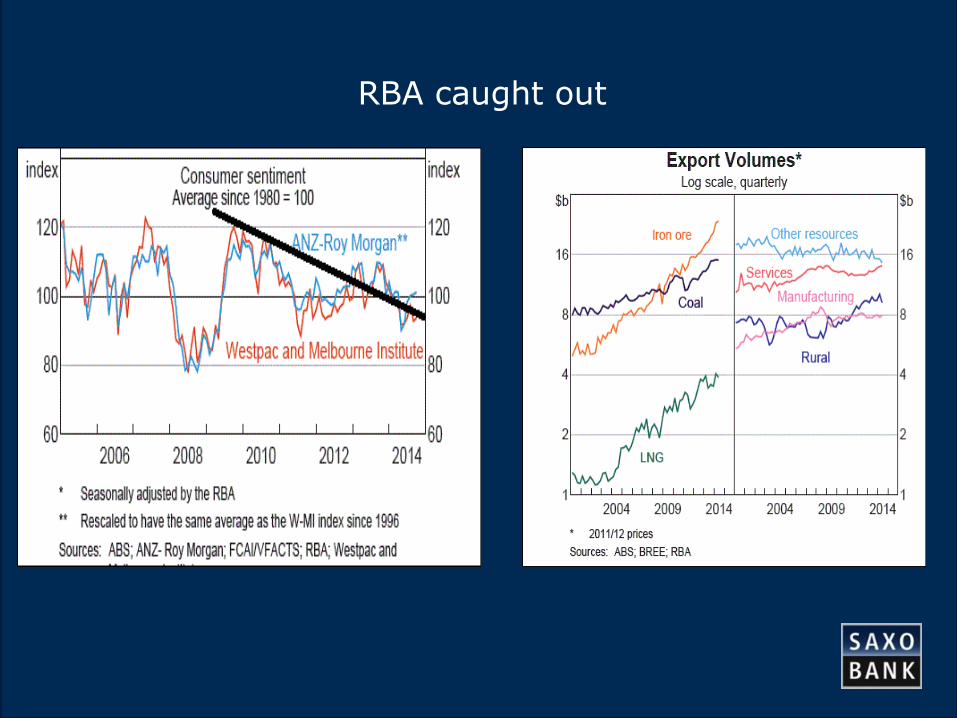

RBA caught out

32

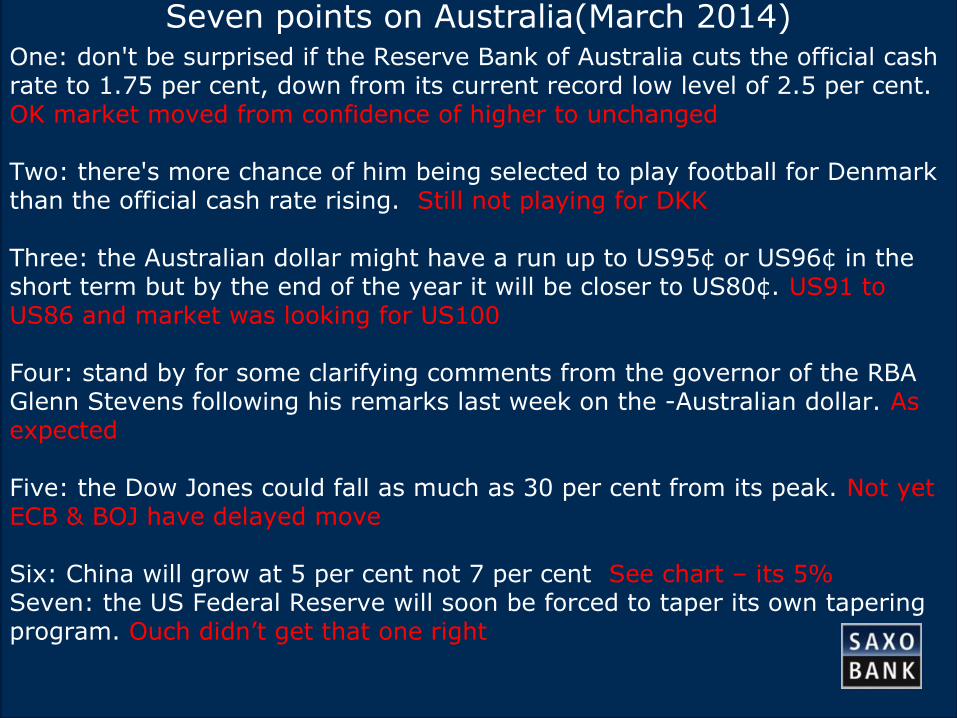

One: don't be surprised if the Reserve Bank of Australia cuts the official cash rate to 1.75 per cent, down from its current record low level of 2.5 per cent. OK market moved from confidence of higher to unchanged

Two: there's more chance of him being selected to play football for Denmark than the official cash rate rising. Still not playing for DKK

Three: the Australian dollar might have a run up to US95¢ or US96¢ in the short term but by the end of the year it will be closer to US80¢. US91 to US86 and market was looking for US100

Four: stand by for some clarifying comments from the governor of the RBA Glenn Stevens following his remarks last week on the Australian dollar. As expected

Five: the Dow Jones could fall as much as 30 per cent from its peak. Not yet ECB & BOJ have delayed move

Six: China will grow at 5 per cent not 7 per cent See chart – its 5%Seven: the US Federal Reserve will soon be forced to taper its own tapering program. Ouch didn’t get that one right

Seven points on Australia(March 2014)

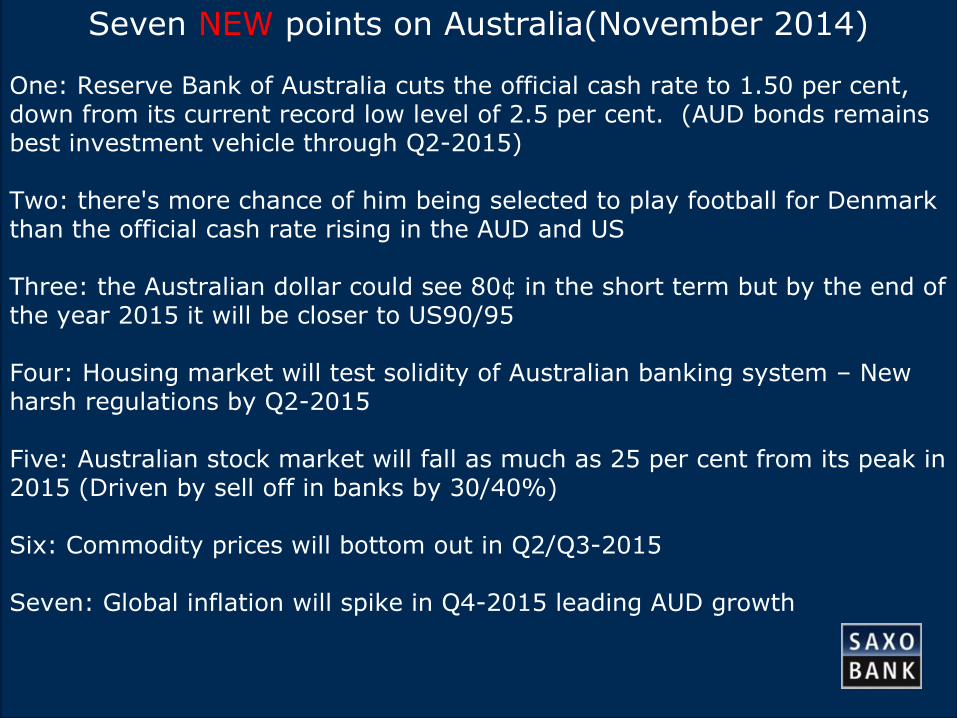

33

One: Reserve Bank of Australia cuts the official cash rate to 1.50 per cent, down from its current record low level of 2.5 per cent. (AUD bonds remains best investment vehicle through Q22015)

Two: there's more chance of him being selected to play football for Denmark than the official cash rate rising in the AUD and US

Three: the Australian dollar could see 80¢ in the short term but by the end of the year 2015 it will be closer to US90/95

Four: Housing market will test solidity of Australian banking system – New harsh regulations by Q22015

Five: Australian stock market will fall as much as 25 per cent from its peak in 2015 (Driven by sell off in banks by 30/40%)

Six: Commodity prices will bottom out in Q2/Q32015

Seven: Global inflation will spike in Q42015 leading AUD growth

Seven NEW points on Australia(November 2014)

34

China and JapanAt opposite ends?

35

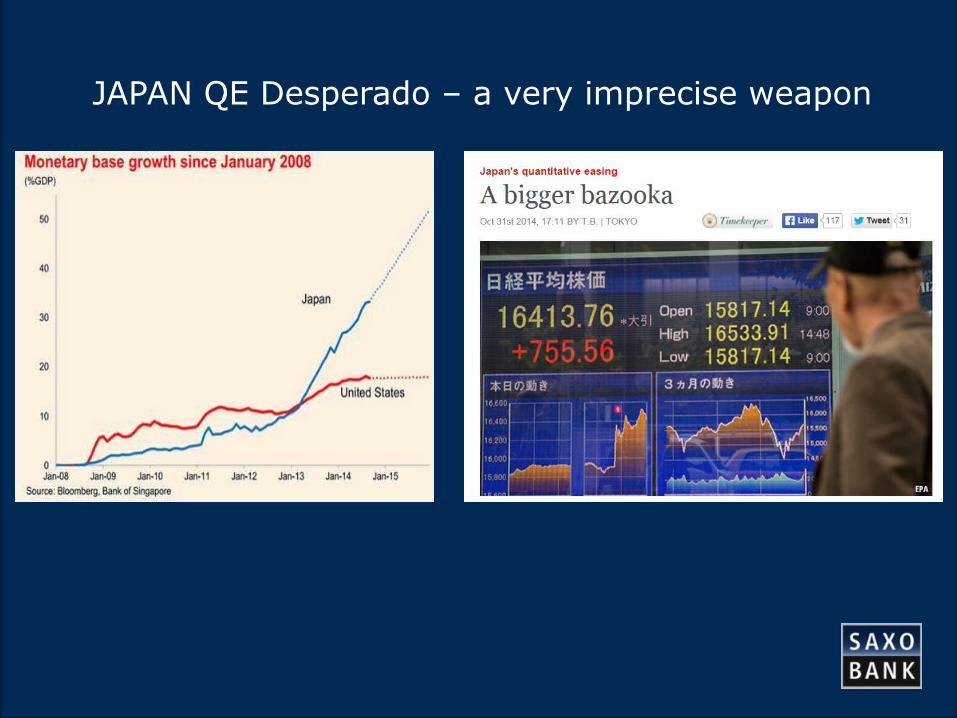

JAPAN QE Desperado – a very imprecise weapon

36

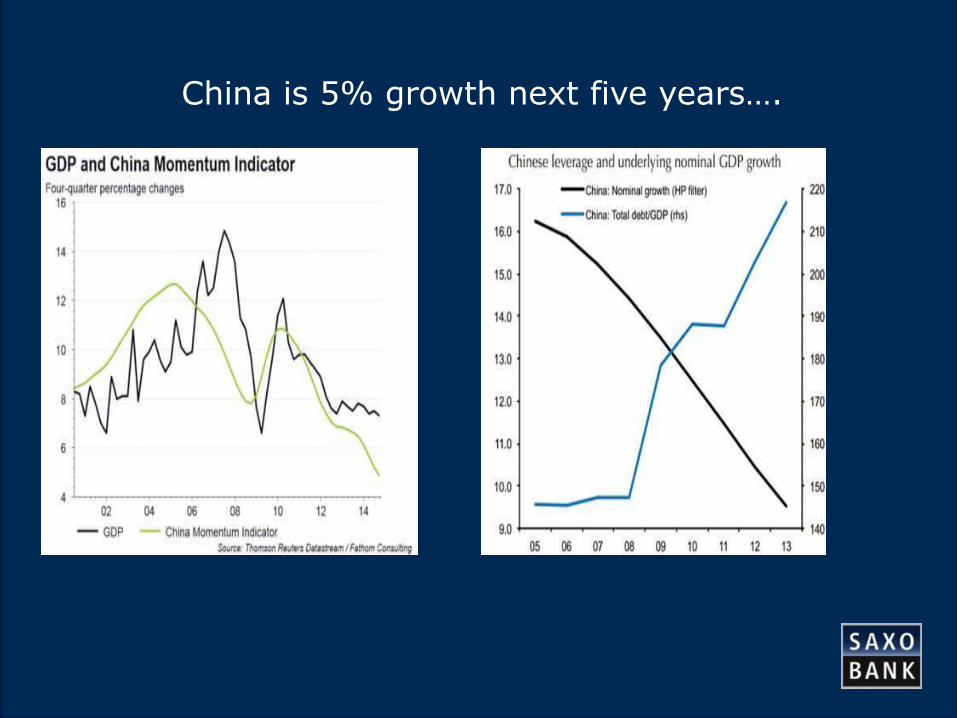

China is 5% growth next five years….

37

Markets and RISK

38

US Real economy leads S&P?

39

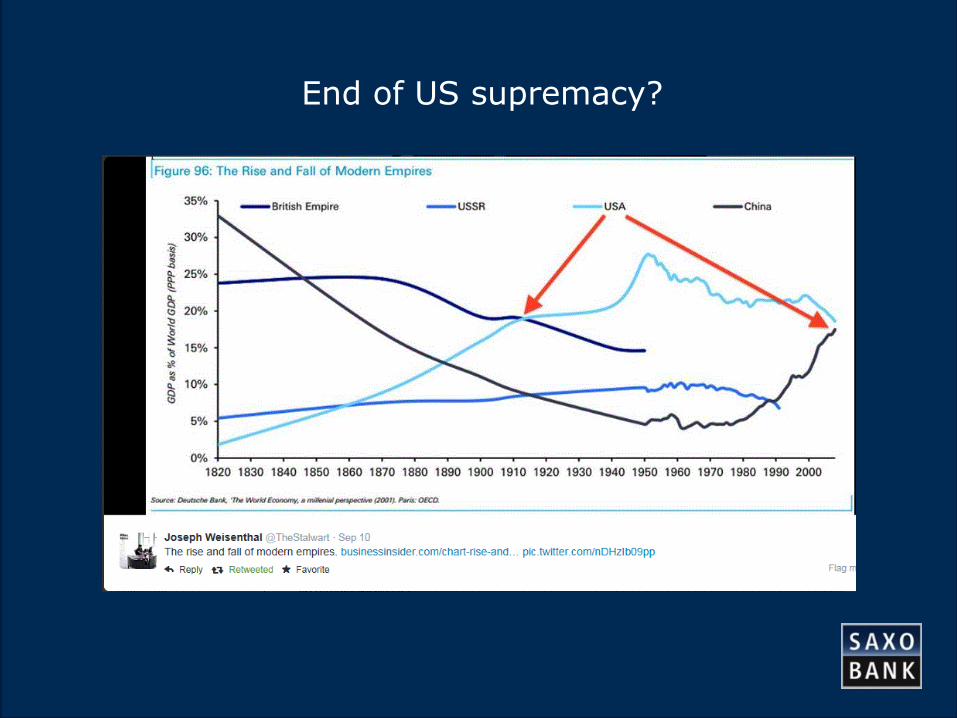

End of US supremacy?

40

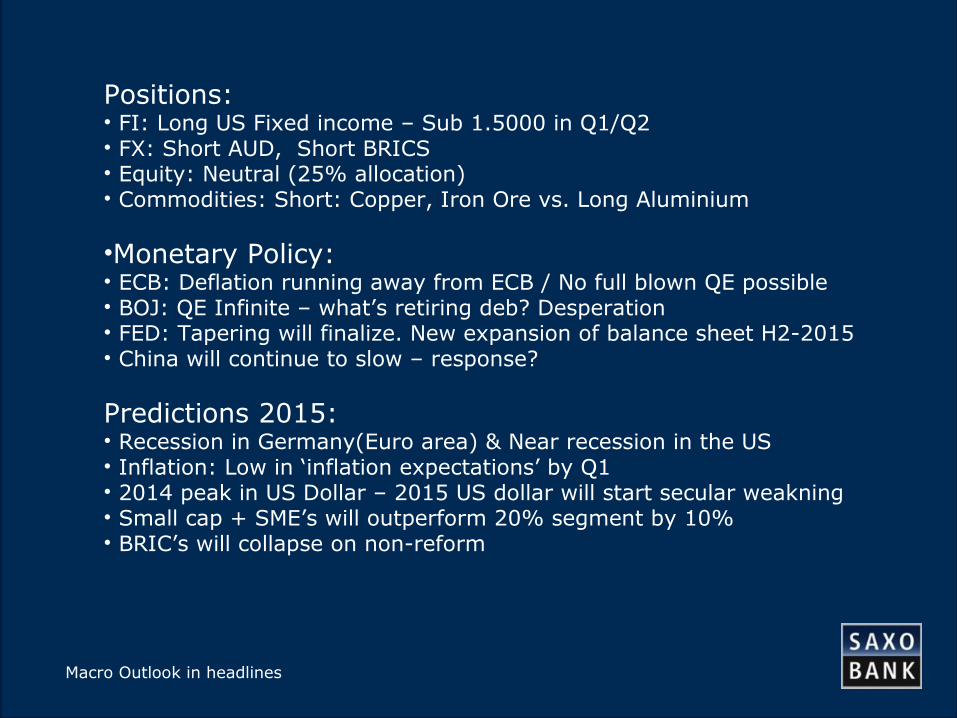

Positions:• FI: Long US Fixed income – Sub 1.5000 in Q1/Q2• FX: Short AUD, Short BRICS• Equity: Neutral (25% allocation)• Commodities: Short: Copper, Iron Ore vs. Long Aluminium

•Monetary Policy:• ECB: Deflation running away from ECB / No full blown QE possible• BOJ: QE Infinite – what’s retiring deb? Desperation• FED: Tapering will finalize. New expansion of balance sheet H2-2015• China will continue to slow – response?

Predictions 2015:• Recession in Germany(Euro area) & Near recession in the US• Inflation: Low in ‘inflation expectations’ by Q1• 2014 peak in US Dollar – 2015 US dollar will start secular weakning• Small cap + SME’s will outperform 20% segment by 10%• BRIC’s will collapse on non-reform

Macro Outlook in headlines

41

Outragous Predictions 2015

DRAFT

42

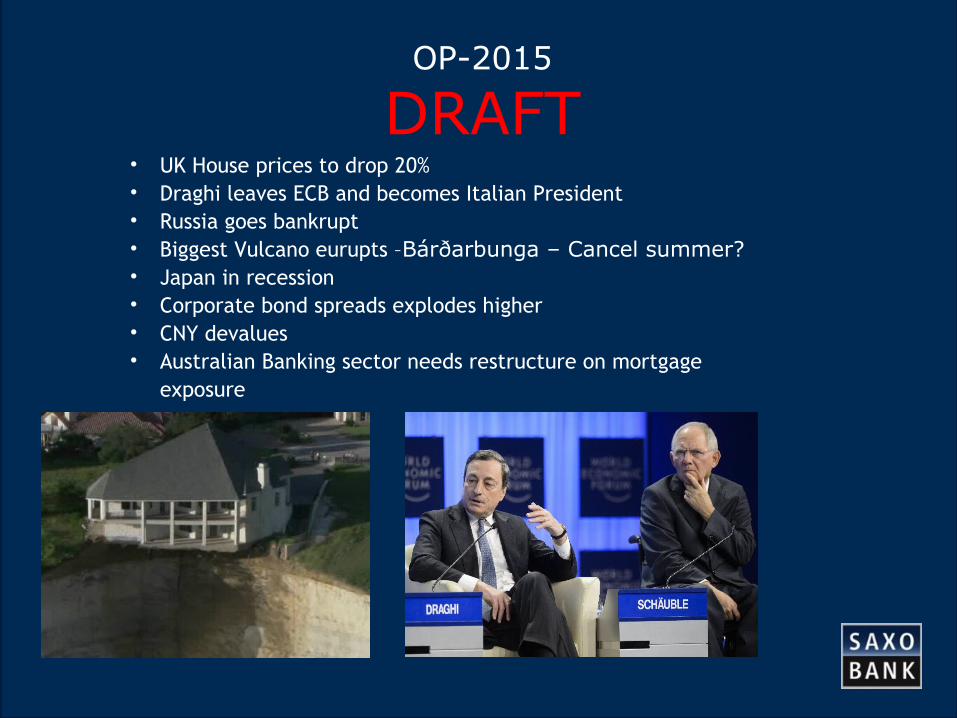

OP-2015

DRAFT• UK House prices to drop 20%• Draghi leaves ECB and becomes Italian President• Russia goes bankrupt• Biggest Vulcano eurupts –Bárðarbunga – Cancel summer?• Japan in recession• Corporate bond spreads explodes higher• CNY devalues• Australian Banking sector needs restructure on mortgage

exposure

43

Thank you

Thanks for attending our webinar! We trust you found it useful and enjoyable.

We hope to see you on another webinar again soon.

If you’re interested in learning more about trading Global markets, or Rivkin Global, please email

Or visit www.tradingfloor.com