Embed Size (px)

Citation preview

Non-Financial Performance Evaluation Parameters

Sheetal Wagh

Any quantitative measure of either an individual’s or an entity’s performance that is not expressed in monetary units.

This includes any ratio-based performance measure in that a non-financial performance measure that is ratio-based omits any monetary metric in either the numerator or denominator of that ratio.

Common examples include:

• measures of customer or employee satisfaction,

• quality, market share, and

• the number of new products.

Non-financial performance measures are sometimes considered to be leading indicators of future financial performance, while current financial performance measures such as earnings or return on assets are commonly considered to be trailing measures of performance.

• Non – Financial Performance Evaluation Parameters:

Two types:

1) Balance Scorecard

2) Malcolm Baldrige Framework

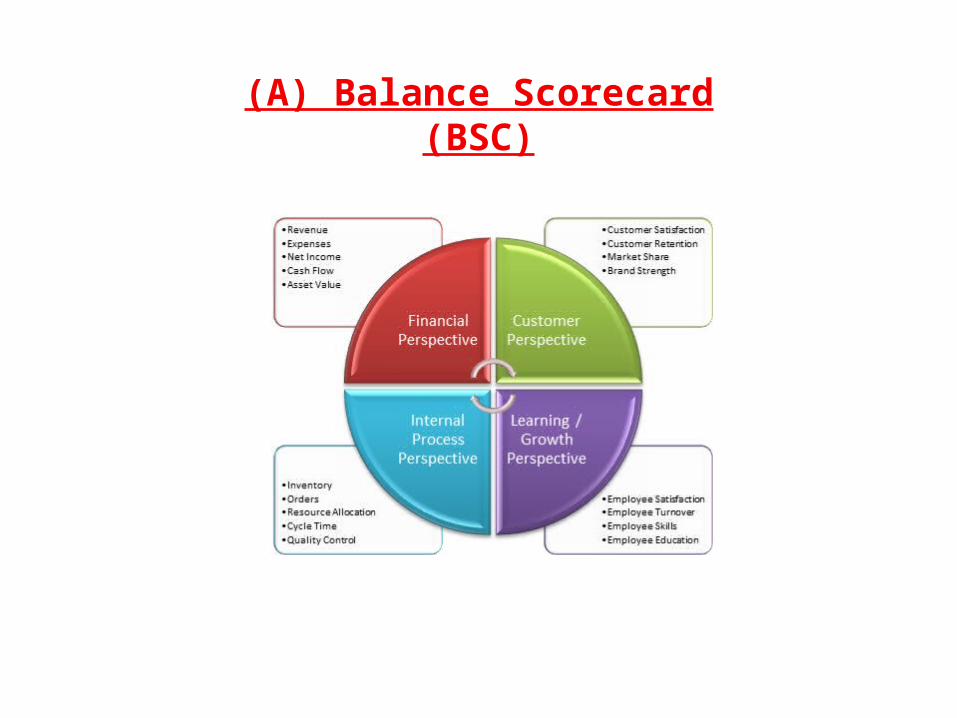

(A) Balance Scorecard (BSC)

The balanced scorecard is a strategic planning and management system that is used extensively in business and industry, government, and non-profit organizations worldwide to align business activities to the vision and strategy of the organization, improve internal and external communications, and monitor organization performance against strategic goals.

It was originated by Dr. Robert Kaplan (Harvard Business School) and Dr. David Norton as a performance measurement framework that added strategic non-financial performance measures to traditional financial metrics to give managers and executives a more 'balanced' view of organizational performance.

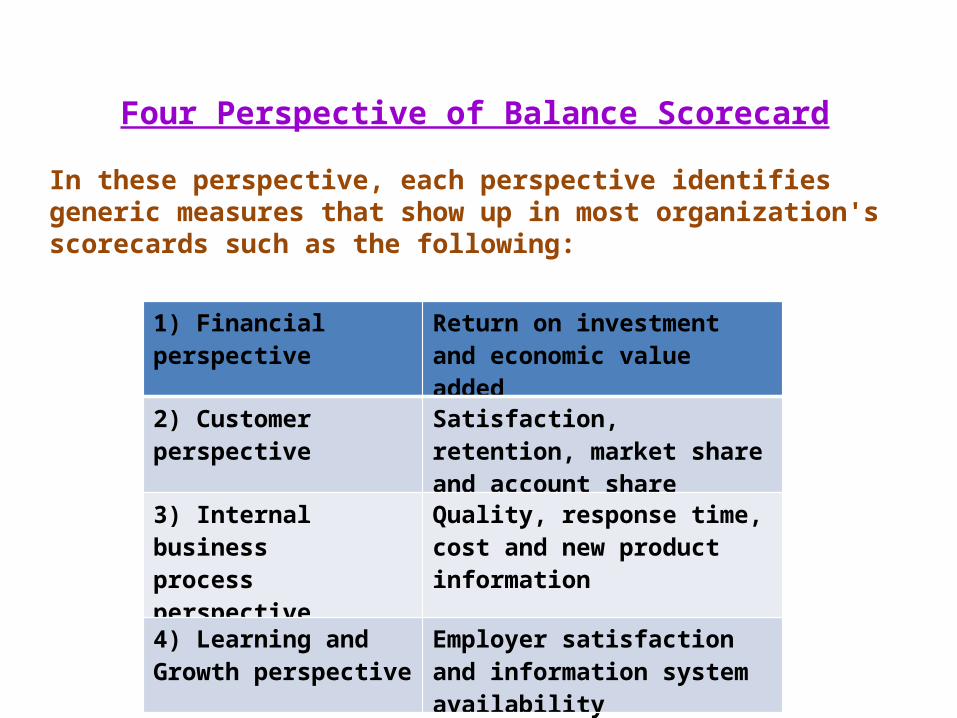

Four Perspective of Balance Scorecard

In these perspective, each perspective identifies generic measures that show up in most organization's scorecards such as the following:

1) Financial perspective Return on investment and economic value added

2) Customer perspective Satisfaction, retention, market share and account share

3) Internal business process perspective

Quality, response time, cost and new product information

4) Learning and Growth perspective

Employer satisfaction and information system availability

The Financial Perspective

Kaplan and Norton do not disregard the traditional need for financial data.

Timely and accurate funding data will always be a priority, and managers will do whatever necessary to provide it.

In fact, often there is more than enough handling and processing of financial data.

With the implementation of a corporate database, it is hoped that more of the processing can be centralized and automated.

But the point is that the current emphasis on financials leads to the "unbalanced" situation with regard to other perspectives.

There is perhaps a need to include additional financial-related data, such as risk assessment and cost-benefit data, in this category.

The Customer Perspective

Recent management philosophy has shown an increasing realization of the importance of customer focus and customer satisfaction in any business.

These are leading indicators: if customers are not satisfied, they will eventually find other suppliers that will meet their needs.

Poor performance from this perspective is thus a leading indicator of future decline, even though the current financial picture may look good.

In developing metrics for satisfaction, customers should be analysed in terms of kinds of customers and the kinds of processes for which we are providing a product or service to those customer groups.

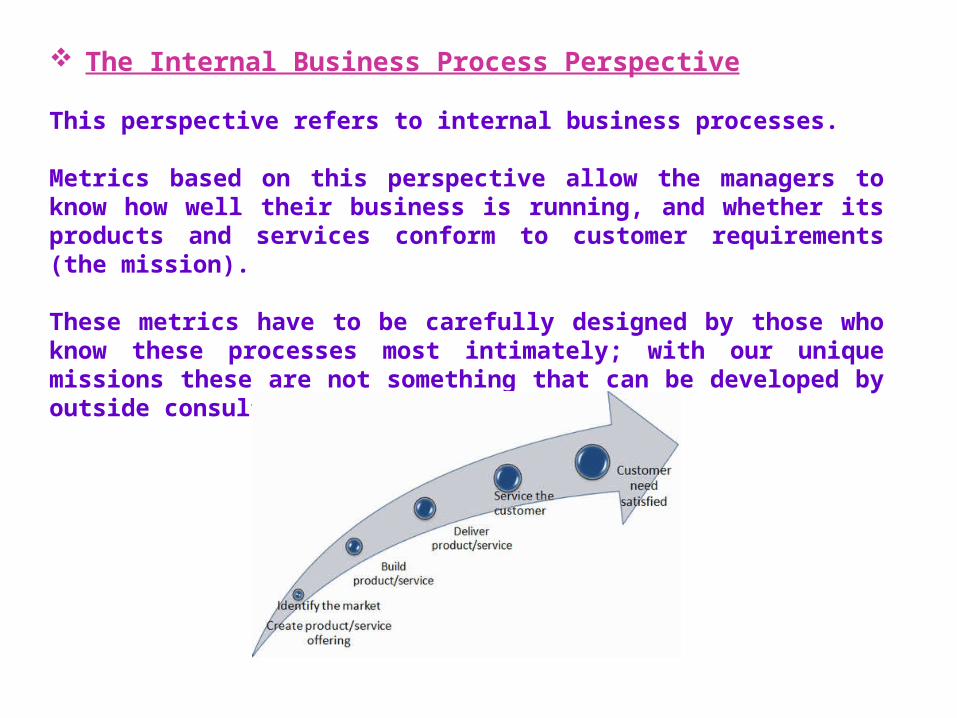

The Internal Business Process Perspective

This perspective refers to internal business processes.

Metrics based on this perspective allow the managers to know how well their business is running, and whether its products and services conform to customer requirements (the mission).

These metrics have to be carefully designed by those who know these processes most intimately; with our unique missions these are not something that can be developed by outside consultants.

The Learning & Growth Perspective

This perspective includes employee training and corporate cultural attitudes related to both individual and corporate self-improvement.

In a knowledge-worker organization, people -- the only repository of knowledge -- are the main resource. In the current climate of rapid technological change, it is becoming necessary for knowledge workers to be in a continuous learning mode.

Metrics can be put into place to guide managers in focusing training funds where they can help the most.

In any case, learning and growth constitute the essential foundation for success of any knowledge-worker organization.

Kaplan and Norton emphasize that 'learning' is more than 'training'; it also includes things like mentors and tutors within the organization, as well as that ease of communication among workers that allows them to readily get help on a problem when it is needed.

It also includes technological tools; what the Baldrige criteria call "high performance work systems."

Advantages of Balance Scorecard:

1) Balanced Scorecard presents organizational goals in a single page chart broken down into relatable areas.

2) Balanced Scorecard allows companies to bridge the gap between mission statement or over-arching goals and how day to day activities support the company's mission or objectives. A BSC goal of pleasing the customer can be tied to improving technical support performance according to the Service Level Agreement or exceeding the SLA.

3) BSC raises innovation and process improvement methods such as six sigma and lean manufacturing to a corporate goal. It also ensures that voice of the customer is equally important.

4) Balanced Scorecard does not exclude other methods of business reporting or process improvement. Six sigma projects naturally fall under the "learn and innovate" section. Financial standards like Sarbanes Oxley are simply used by the financial department when meeting financial scorecard goals or implemented by the financial department to meet a financial scorecard goal.

5) Balanced Scorecards can provide a visual means of demonstrating how different goals are related. Increased sales improve the profit or sales goals under the financial section. Improved customer service meets the “voice of the customer” goal.

6) Balanced Scorecards are straightforward enough to be used by many managers after gaining familiarity with the concept. Advanced training isn’t required to implement a simple version of BSC.

Disadvantages of Balance Scorecard:

1) Balanced Scorecard performance is subjective. Unlike quality levels, it cannot be quantified except by surveys or management opinion. Mandating a specific number of training hours per year to meet an “learn and innovate” doesn’t necessarily mean all employees take courses that help them in their jobs or that attending classes to fill in the quota is better than working on the assembly line. Demanding high employee morale can hurt managers, since morale is not always a manager’s purview. Setting a goal of high morale along with lay offs to save money is counter-productive.

2) Balanced Scorecard does not include direct financial analysis of economic value or risk management. Goal selection under Balanced Scorecard does not automatically include opportunity cost calculations.

3) Because Balanced Scorecard can add a new type of reporting without necessarily improving quality or financial numbers, it can seem to be an additional set of non-value-added reporting or, worse, a distraction from achieving actual goals.

4) Overly abstract Balanced Scorecard goals are easy to reach but hard to quantify.

5) When a company is failing to meet its Balanced Scorecard goals, the goals may be re-interpreted to the current state of affairs to meet success or avoid failure. Altering the acceptance criteria for a good balanced scorecard is easier than altering the acceptance criteria for mechanical parts and hence the reject rate

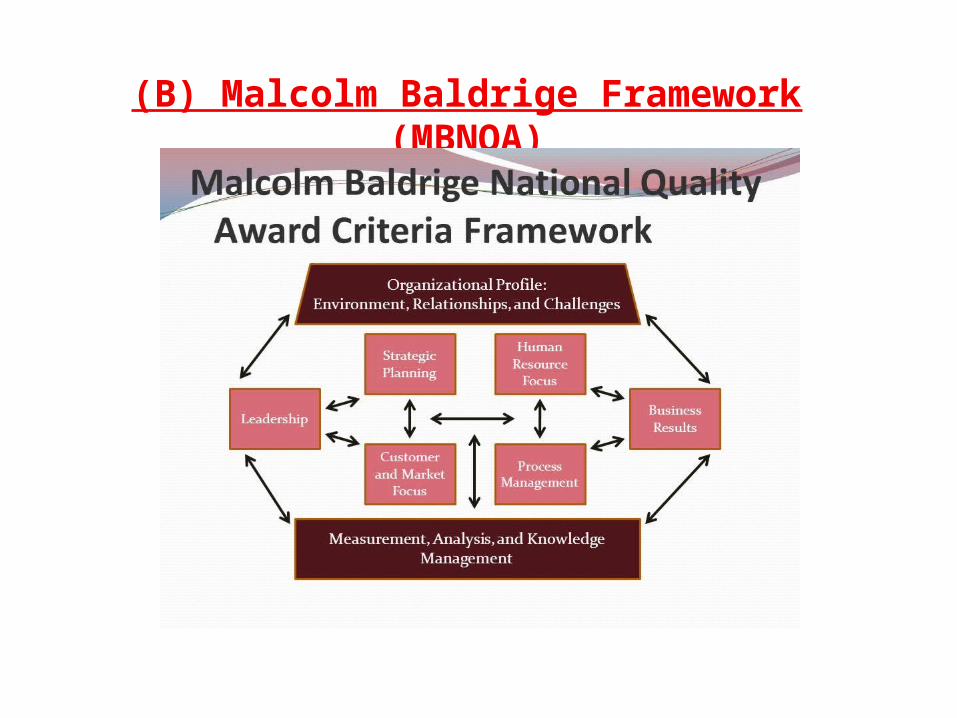

(B) Malcolm Baldrige Framework (MBNQA)

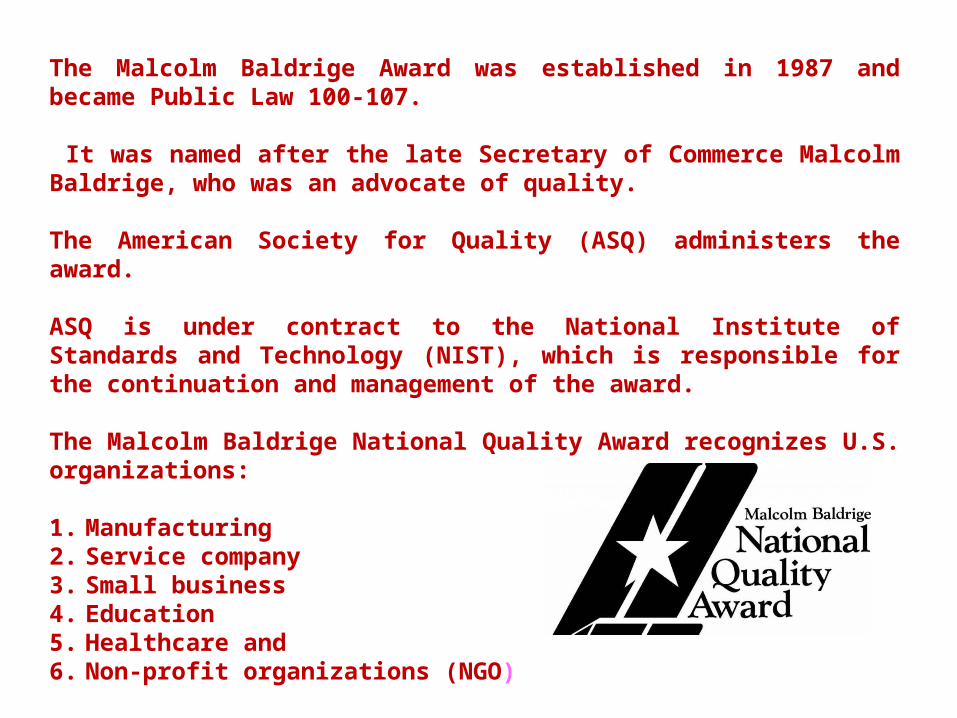

The Malcolm Baldrige Award was established in 1987 and became Public Law 100-107.

It was named after the late Secretary of Commerce Malcolm Baldrige, who was an advocate of quality.

The American Society for Quality (ASQ) administers the award.

ASQ is under contract to the National Institute of Standards and Technology (NIST), which is responsible for the continuation and management of the award.

The Malcolm Baldrige National Quality Award recognizes U.S. organizations:

1. Manufacturing2. Service company3. Small business4. Education5. Healthcare and6. Non-profit organizations (NGO)

Framework of MBNQA

Organizations that apply for the Baldrige Award are judged by an independent board of examiners.

Recipients are selected based on achievement and improvement in seven areas, known as the Baldrige Criteria for Performance Excellence:

1) Leadership: How upper management leads the organization, and how the organization leads within the community.

2) Strategic planning: How the organization establishes and plans to implement strategic directions.

3) Customer and market focus: How the organization builds and maintains strong, lasting relationships with customers.

4) Measurement, analysis, and knowledge management: How the organization uses data to support key processes and manage performance.

5) Human resource focus: How the organization empowers and involves its workforce.

6) Process management: How the organization designs, manages and improves key processes.

7) Business/organizational performance results: How the organization performs in terms of customer satisfaction, finances, human resources, supplier and partner performance, operations, governance and social responsibility, and how the organization compares to its competitors.

Advantages of MBNQA:

1) Helps in achieving sustainable results in today’s challenging environment.

2) Helps American companies to improve quality and productivity for the pride of recognition while obtaining a competitive edge through increased profits.

3) Helps organizations to think strategically.

4) Establishing guidelines and criteria that can be used by business, industrial, governmental and other enterprises in evaluating their own quality improvement efforts.

5) Recognizes the achievements of those companies that improve quality of their goods and services providing an example to others.

6) Helps companies align processes, people, resources and customer needs.

Disadvantages of MBNQA:

1) Incremental improvements

2) Narrow focus

3) Baldrige Award is Division-based and not Organization-wide

4) Over-Advertisement

5) Applying for the award is too expensive

6) Use the award’s assessment process and not the award

THANK YOU