Embed Size (px)

DESCRIPTION

Citation preview

MACROECONOMICSUNEPLOYMENT OR INFLATION

REAL ALTERNATIVE?

UNEMPLOYMENT Definition – unemployment is an economic phenomenon that

people who want to work and are able to work cannot work because of the shortage of work (job places)

Unemployment rate = rate of the unemployed to the total labor force (U)

Labor force: the employed + the unemployed (LF)The key issue is how to count the unemployed Registered unemployed – those who are registered at labor

offices or in the other way officially The unemployed – based on survey of economic activities of

population: those of the adult population who did not work even single day in the proceedeng month

The unemployment rate depends on the definition of the unemployed

Manipulations with unemployment rate We can increase the base (labor force) by adding certain groups

to the labor force ( M. Tatcher, adding entrepreneurs to the base) We can demotivate people to register (distant labor office, lot of

formalities) We can decrease unemployment benefits to demotivate people to

register for benefits We can make people ashamed to tell the survey officers that they

had not earned any money in the last month Conclusion – the unemeployment rate can be maniputaled but the

real problem remains : there are people who cannot really find jobs accordingly to their residence location and qualifications

Employment rate - percentage of the employed to the population aged 18-64 in EU (it differs from country to country)

Labor Force Survey LFS (LFS), which covers persons aged 15 and more, members of households in

dwellings selected on a random basis. The survey is conducted by the continuous observation method, i.e., economic activity of the population is observed in each week during the whole quarter. Since the I quarter of 2003, data of the LFS have been generalized on the basis of the balance of population compiled with the use of the results of the Population and Housing Census 2002. Data presented by age groups have been calculated on the basis of the exact date of birth, until the I quarter of 2006 — with the exception of persons aged 15 — they were presented according to the year of birth.

The main criterion in dividing the population into economically active (employed and unemployed persons) and inactive is work, i.e., performing, holding or looking for work.

Employed persons are persons who during the reference week: — performed, for at least 1 hour any work providing earnings or income, or assisted

(without wages or salaries) in maintaining a family-owned farm in agriculture or conducting a family-owned business outside agriculture,

— formally had work but did not perform it (e.g., due to illness, vacation, a break in company activity, bad weather); if the break in work exceeded 3 months, since 2006 the additional criterion in case of paid employees (employees hired on the basis of an employment contract and outworkers) was the fact of receiving at least 50% of the hitherto remuneration.

LFS cont.Unemployed persons are persons aged 15—74, who

simultaneously fulfil three conditions:— within the reference week were not employed,— actively sought work, i.e., within a 4-week period

undertaken any real action (the last week being the reference week) to find work,

— were available for work within a fortnight period following the reference week.

The unemployed also include persons who have found work and were waiting to begin it within a 3-month period, as well as persons who were available for that work.

Economically inactive persons are persons who are not classified either as employed or unemployed.

Employment rates in EuropeSource: Eurostat

Unemployment rates in EuropeSource: Eurostat

Hours of work weekly Source: Eurostat

TYPES OF UNEMPLOYMENT Frictional Unemployment:

- is caused by imperfect information and frictions in the economy

- employers are not aware of all available workers and their qualifications, and,

- available workers are not fully aware of all the jobs being offered by employers.

- some people change jobs and are temporary unemployedStructural Unemployment:

- caused by an imperfect match of employee skills to skill requirements of the available jobs.

Cyclical Unemployment (Keynesian):- caused by changes in economy due to the business cycle

conditions- in the recession cyclical unemployment increases.

Classical unemployment:- caused by too high level of working compesation above the level

of labor market equilibrium

CLASSICAL VS KEYNESIAN UNEMPLOYMENT Source: http://www.s-cool.co.uk/alevel/economics/unemployment-and-the-phillips-curve/unemployment--the-details.html

Natural rate of unemployment The Natural Rate of Unemployment is the rate of Unemployment when the Labour

market is in equilibrium. It is the difference between those who would like a job at the current wage rate and

those who are willing and able to take a job. The Natural Rate of Unemployment will therefore include:

frictional unemployment structural unemployment E.g. a worker who is not able to get a job because he doesn’t have the right skills

The natural rate of unemployment is unemployment caused by supply side factors rather than demand side factors

Monetarists argue that the Natural Rate of Unemployment occurs when the Long Run Phillips Curve crosses the x axis

The Natural Rate of Unemployment is sometimes known as the Non accelerating inflation rate of Unemployment NAIRUThis is because when unemployment is 4% there is no tendency for inflation to increase

In this example the Natural rate of unemployment is 4%. If the govt increased AD there may be a temporary fall in unemployment but in the Long Run it would return to the natural rate of 4%

Sometimes the natural rate is known as the full employment level of unemployment This is because even if the economy is operating at full capacity and there is no

demand deficient unemployment then there will still be some unemployment caused by supply side factors.

Source: http://www.economicshelp.org/macroeconomics/unemployment/natural_rate.html

Natural rate of unemployment Source: http://tutor2u.net/economics/content/topics/unemp/natural_rate.htm

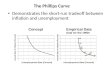

Original Phillips curve

Theoretical Phillips curve

NAIRUnon-accelerating inflation rate of unemployment

NAIRU The NAIRU concept maintains that when unemployment is at the

rate defined by the red line, inflation will be stable. However, in the short-run policymakers will face an inflation-unemployment rate tradeoff marked by the "Initial Short-Run Phillips Curve“. Policymakers can therefore reduce the unemployment rate temporarily, moving from point A to point B through expansionary policy. However, according to the NAIRU, exploiting this short-run tradeoff will raise inflation expectations, shifting the short-run curve rightward to the "New Short-Run Phillips Curve" and moving the point of equilibrium from B to C. Thus the reduction in unemployment below the "Natural Rate" will be temporary, and lead only to higher inflation in the long run.

The name "NAIRU" arises because with actual unemployment below it, inflation accelerates, while with unemployment above it, inflation decelerates. With the actual rate equal to it, inflation is stable, neither accelerating nor decelerating. One practical use of this model was to provide an explanation for stagflation, which confounded the traditional Phillips curve.

Inflation vs. Unemployment criticism Coincidence or cause-effect relationship Naive concept within the complex economic world Pretext to expand expenditures or money supply With context to the Long Run Phillips Curve was

the Short run only the coincidence? Do LPC really exist? Polish research in 90’ shows that the higher public

deficit the lower growth rate and higher U– it is totally opposite to theory

It seems that different factors influence inflation and unemployment

Costs of unemployment Social (margin, crime, etc.)Individual (psychological) Consumer pesimism (can cause the spiral of

stagflation) To GDP (Okun law – when U grows by 1%

over natural unemployment rate the GDP falls by 3 %)

Other costs Think: who benefits from unemployment

Costs of inflation Loses of cashholders Loses of institutional creditors Loses of bonds holders Loses of employees and entrepreneurs Loses of taxpayers Loses of pensionaires Think: who benefits from inflation?

Fisher lawMV = PQ where:M – money supply V – velocity of money P – price levelQ – the quantity of goods and services When V and Q are constant in the short run

then P depends on M

Fisher law conclusion The price level depends on the quantity of

money in circulation and money supply decides on inflatioon

This approach dominates in economics and influences the moderation in money supply

Doubts? Can the central bank influence the money supply

in the fixed exchange rates environment? Is money supply shaped by export surpluses of

certain countries and the central bank must exchange foreign curriencies into the domestic money on demand ?

Can shortterm employees’ transfers function in the similar way as export surpluses?

Can inflow or outflow of foreign investment will not influence the money supply instead of the central bank?

Conclusion: in the small open economy the central bank has a limited opportunity to control money supply.

Types of inflation Cost pushed Demand driven Structural