Embed Size (px)

Citation preview

© 2015 Environmental Risk Communications, Inc.

Contact:

John Rosengard(415) 336-5085

www.erci.com

Fair Value Measurement of Environmental Liabilities

March 2015

© 2015 Environmental Risk Communications, Inc.

Outline for Today’s Webinar

Speaker’s Bio and Elevator Speech

Fair Value Measurement in GAAP

Why Transition to Fair Value Measurement

ERCI Observations

How to Document Fair Value Measurement

Q&A

© 2015 Environmental Risk Communications, Inc.

Speaker Background: John Rosengard

Wrote Defender™ liability forecasting software package

Environmental remediation liabilities (ASC 410-30) Asset retirement obligations (ASC 410-20) Due diligence on acquisitions and divestitures Watch list for future reserve increases (sites &

portfolios) Decision analysis on individual sites Pollution remediation obligations (GASB49) Counterparty (PRP) default tracking

We support Corporate remediation groups PRP groups Port authorities The engineering/consulting and legal partners Their internal and external auditors

MBA, Northwestern; BS, Georgetown

John RosengardPresident & CEO, [email protected], CA

© 2015 Environmental Risk Communications, Inc.

Elevator Speech: How/Why on FVM

What

“Market price”, since 2006, preferred basis for pricing liabilities, per GAAP.

Why

Common sense. Potentially validated by a counterparty, not a regulator.

And it might be free. Factor in deferred tax assets, full spectrum of cost recoveries, and avoidable escalation (lifecycle oversight, counterparty default, remedy failure)

How

Stop equating cleanup projects/budgets with environmental liabilities.

“Think like a counterparty” when we value an environmental liability. Understand why they would take on a liability; after all, this is how your company bought into the liabilities in the first place.

© 2015 Environmental Risk Communications, Inc.

Fair Value Volatility

six months

Fair value of environmental restoration cost

Fair value of operating asset

Fair value of environmental restoration cost

Fair value of operating asset

@ $100/barrel

@ $50/barrel

Takeaway: an asset that is operating profitably in 2013 can justify a small (present value) cost for restoration:-Indefinite “date of settlement”-Unknown future cleanup levels-Unknown future source (soil, GW)

Decommission or sell off an unprofitable asset in 2015, the environmental costs are:-Settled now-Based on current cleanup regulations-Based on today’s source knowledge

$5MM ($.5MM) $2MM ($3MM)

© 2015 Environmental Risk Communications, Inc.

Conceptual Framework

Source: FASB Statement of Financial Accounting Concepts No. 8, September 2010

Enhancing Qualitative

CharacteristicsFundamental Qualitative

Characteristics

Objective of Financial Reporting

Information

Useful to Decisions

Relevant

Predictive value

Confirmatory value

Faithful Representation

Complete

Neutral

Free from error

Elements of Financial

Statements

Comparability

Verifiability

Timeliness

Understandability

Recognition

Measurement

Presentation

Disclosure

Cost Constraint

Materiality Constraint

© 2015 Environmental Risk Communications, Inc.

GAAP Alignment Among Standard Owners

Standard owner FASB GASB IASBFor… US Corporations Govt Agencies Non-US Corp.

Environmental Obligations

ASC 410-30Oct1996

GASB 49Nov2006GASB 18Aug 1993

IAS 37Sep1998

ARO ASC 410-30Oct1996

ProjectOct2016 (est)

IFRIC 1Jul2004

Fair Value ASC 820 -Sep2006

GASB 72 –Feb 2015

IFRS 13 –May2011

Commitments ASC 440 Note in disclosures

IAS 16

Contingencies ASC 450 GASB 10 IAS 37Guarantees ASC 460 GASB 70 IAS 39Nonperformancerisk of counterparty default

ASC 820-10-35-17 and ASC 410-30-30-7

GASB 72, ¶62

IFRS 13:42

© 2015 Environmental Risk Communications, Inc.

What Are Environmental Liabilities (FASB)?

ObligationsASC 410

CommitmentsASC 440

ContingenciesASC 450

GuaranteesASC 460

Liabilities

Consent order to study and remediate a site

Promise to study and/or buy back a site if

contamination is found

Settlement to share past costs at a closed

landfill

Financial assurance instrument (LOC) to

regulator for performance of RCRA

monitoring

Asset retirement obligations

© 2015 Environmental Risk Communications, Inc.

Fair Value Measurement

Defined in FAS 157, now ASC 820 (Sep 2006)

For public agencies, GASB 72 (Feb 2015)

Presume an arm’s length, third party transfer in an orderly market

Three approaches

Market

Cost – best for environmental liabilities

Income

Counterparty risk included (a PRP fails and their liability defaults back to you)

Hierarchy of Inputs (next page)

© 2015 Environmental Risk Communications, Inc.

Fair Value Hierarchy (ASC 820, GASB 72)

Level 1 (preferred): quoted price, active market, identical liabilities

Example: Excavated soil will be “Class C” waste and trucked to landfill for a drive-off cost of $84.50/ton

Level 2: some observable inputs, less-active market, similar liabilities

Example: Operating a 20-gallon/minute groundwater extraction system has an annual utility cost of $8K to $10K

Level 3: unobservable inputs, little (if any) market, unique liabilities

Regulatory approval of the remediation plan may take four years; during that delay, the groundwater plume may expand 0%-25%, depending on rainfall

© 2015 Environmental Risk Communications, Inc.

Outline for Today’s Webinar

Speaker’s Bio and High-Level View

Fair Value Measurement in GAAP

Why Transition to Fair Value Measurement

ERCI Observations

How to Document Fair Value Measurement

Q&A

√

© 2015 Environmental Risk Communications, Inc.

Useful to decisions and decision makers

Eliminates surprises

GAAP Compliant: “relevant”, “faithful representation”

GAAP Compliant: comparable, verifiable, timely, understandable

Focuses spending on liability reduction (not deferral or remedy)

Helps manage knowledge loss

Improves execution on acquisitions and divestitures

Identifies portions of portfolio with long-term recoveries at risk- cost recovery mechanisms in customer contracts, which may be time limited- counterparties in danger of defaulting

Why Transition to Fair Value Measurement

© 2015 Environmental Risk Communications, Inc.

Where Do Liability Disclosures Fit In?

Source: FASB Statement of Financial Accounting Concepts No. 8, September 2010

Enhancing Qualitative

CharacteristicsFundamental Qualitative

Characteristics

Objective of Financial Reporting

Information

Useful to Decisions

Relevant

Predictive value

Confirmatory value

Faithful Representation

Complete

Neutral

Free from error

Elements of Financial

Statements

Comparability

Verifiability

Timeliness

Understandability

Recognition

Measurement

Presentation

Disclosure

Cost Constraint

Materiality Constraint

GAAP Conceptual Framework

© 2015 Environmental Risk Communications, Inc.

Legacy Behaviors: Liabilities not at Fair Value

Date Event12-31-2008 GM environmental reserve: $297 million6-01-2009 GM files Chapter 116-30-2009 GM updates their reserve to $536 million10-20-2010 $773 million for first six settlements12-14-2010 +$25.0 million settlement = $798.0 million3-3-2011 +$28.2 million settlement = $826.2 million3-7-2011 +$50.6 million settlement = $876.8 million3-29-2012 +$23.8 million settlement = $900.6 million6-29-2012 +$39.2 million settlement = $939.8 million

11 settlements = 3.2x reserve, three years$297 million >>> $940 million

Source: USEPA press releases

© 2015 Environmental Risk Communications, Inc.

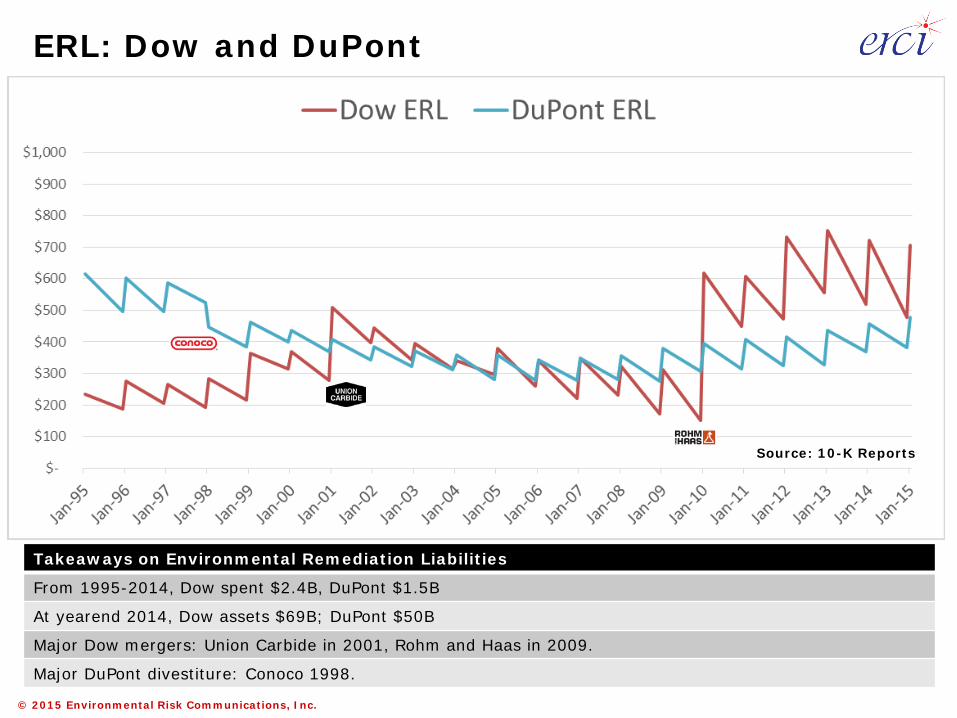

Source: 10-K Reports

ERL: Dow and DuPont

Takeaways on Environmental Remediation Liabilities

From 1995-2014, Dow spent $2.4B, DuPont $1.5B

At yearend 2014, Dow assets $69B; DuPont $50B

Major Dow mergers: Union Carbide in 2001, Rohm and Haas in 2009.

Major DuPont divestiture: Conoco 1998.

© 2015 Environmental Risk Communications, Inc.

If the ERLs were $439M annuities paying $79.6M/yr, they would be yielding 18% (!).

Use a lower discount rate instead, the liability shifts up:

Takeaway: “probably and reasonably estimable” liability balances are not consistent with PV of historical spend

Takeaway: adjust for inflation, distortion worsens

Are Reserve Balances Too Low?

Discount rate justification Discount rate Liability Value“probable and reasonably estimable”

$79.6M/$439M= 18.13%

$439M

NYSE – Price/Earnings Multiplier of 19 (March 2015)

5.27% $1,511M

DuPont pension plan (2014) 4.55% $1,749MDuPont’s cost of LT debt (2015) 2.43% $3,276M

DuPont 2010-2014 1995-2014ERL Spending/year $79.6M $75.4MERL Balance (avg) $439M $422MShelf life (years) =439/79.6 = 5.5 =422/75.4 = 5.6

© 2015 Environmental Risk Communications, Inc.

ERCI’s FAQ on Fair Value Measurement

Quote ERCI’s ReplyFVM applies to valuing assets, like our pension plan investments

FVM applies to liabilities, too. And not just financial instruments.

Our reserve policy generally treats Environmental Liabilities (ASC 410-30) as Contingencies (ASC 450)

FVM applies to Contingencies, too.

Our environmental reserves pass audit every year

Common outcome, but what are the root causes of recent reserve increases? What do we know nowthat we didn’t know before?

Auditors never ask for this; our reserves are immaterial

A statement like “all Obligations, Commitments, Contingencies and Guarantees are at/near market value” needs reliable evidence.

Some answers are privileged and confidential

Balance compartmentalization, privilege with business needs.

© 2015 Environmental Risk Communications, Inc.

Employee compliance with reserve policy is paramount From divestitures: FVM discounts are last-minute surprises From acquisitions: FVM discounts sometimes go unreserved;

field observations never get resolved Purchase accounting window closes after an acquisition

Multiyear budget ≈ reserve, which defaults to ≈ liability Incumbent vendors pricing “their” reserves @ “their” sites Reserve is not current market value of liability

“Don’t know what accounting does with our numbers” “Heave it over the transom” “I can’t explain the number in our SEC 10-K (20-F) report”

“Our auditor is not asking us for this; no one is….” Acceptance of the above

ERCI Observations on FVM

© 2015 Environmental Risk Communications, Inc.

Fair Value Reserve Calculation Example

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

VendorQuote

RemedyFailure

ProjectManagement

CounterpartyDefault

Fair Value

Vendor QuoteGroundwater P&T System$2M install, $3 M O&MLess 50% in cost sharing= $2.5M

Remedy Failure80% status quo OK20% expand remedy (+$4M, less 50%)= [(80% x 0) +(20% x $2M)] = $0.4M

Project Mgmt10% add-on= $0.3M

Counterparty60% no defaults25% one PRP default, +$1M15% two PRP defaults, +$2M= [(60% x 0) + (25% x $1M) + (15% x $2M)] = $0.6M

$2.5

$3.8

+$0.4+$0.3

+$0.6

© 2015 Environmental Risk Communications, Inc.

How to transition to FVM @ lowest cost

Term Sheet for Each Liability Lifecycle cost projection

Contingencies for changes to scope, schedule and vendor

Premium for full/partial strategy failure

Premium for project management

Premium/discount for counterparty risk

Premium/discount for your company’s own ability to pay

Insurance covering cost escalation, reopener, NRDA risk

Income for brownfield redevelopment

Recovery of current and future spending Asserted and unasserted claims

Income for sunk cost recovery Asserted and unasserted claims

Consequences of deferred tax assets

© 2015 Environmental Risk Communications, Inc.

Fair Value Term Sheet (Reserve = A through F)

Variable Level 1/2/3 inputs: site-specific conditions, KPIs, unit costs

FVM Level

Income Impact

A. Lifecycle cost projection 12 years pump & treat, 10 gpm from 5 wells, three pore volumes of 19 acres

2 -$5.5 million

B. Contingencies for changes to scope, schedule and vendor

25% cost increase for fourth pore volume, doubling well count (to 10) in years 8-12

2 -$1.2 million

C. Premium for full/partial strategy failure

Additional ten years pump & treat for fifth and sixth pore volume

3 -$3.8 million

D. Premium for project management

12 years oversight, legal, contracting, cost recovery work

2 -$2.8 million

E. Premium/discount for counterparty risk

Successor owner has diesel generator onsite; credit rating 620

1 -$1.5 million

F. Premium/discount for your company’s own ability to pay

Fortune 200, credit rating 1085 1 +$0.5 million

G. Insurance for cost cap, etc Self-insuring all cost escalation, reopeners 3 +$0.0 million

H. Income for brownfield Ground lease $500K/yr to 2025 2 +$5.0 million

I. Recovery - current/future costsAsserted and unasserted claims

50% recoverable under Federal contract20% recoverable from legacy owner

2 +$7.4 million+$3.0 million

J. Recovery – sunk costsAsserted and unasserted claims

50% recoverable under Federal contract20% recoverable from legacy owner

1 +$0.5 million+$3.0 million

K. Value of deferred tax assets 30% of items A through F 1 +$4.3 million

Fair Value Components Total OutflowsInflows

Net

-$14.8 million+$23.7 million+$8.9 million

© 2015 Environmental Risk Communications, Inc.

How to Efficiently Transition to FVM

Objective: comply with the duty to display the obligation to management, and possibly to disclose

Build consensus for a Pilot Project Environmental project team Legal department Audit (internal and external) Treasury/Risk Management Board of Directors

© 2015 Environmental Risk Communications, Inc.

How to Efficiently Transition to FVM

Conduct a Pilot FVM Evaluation Project Opportunity Question: what can an acquirer find out/pay out by

2025?

Select a division, plant, asset type; <15% of company 90-day effort; use an FVM term sheet template; document what

contingencies do/don’t cover; learn if the remedy can fail and if so…what is the backup plan and probability

Produce a term sheet for each liability, listing key assumptions Numerical: soil and groundwater volume, cleanup goal(s), unit costs

Regulatory: contaminants of concern, driving regulations, future land use

Counterparties: identity, tentative allocation, current credit rating

Timeline: deadlines, constraints Scorecard: Level 3 answers moved to Level 2; Level 2 to Level 1

Perform “market testing” on select site(s) Ask a vendor to validate a market price to take over a liability

Compare terms and lifecycle costs

© 2015 Environmental Risk Communications, Inc.

How to Efficiently Transition to FVM

Conduct Post-Pilot Evaluation Develop business case for analyzing full portfolio Confirm cost/benefit for level 3, 2 and 1 answers Determine governance and frequency of deep-dive updates

Niche valuation experts or internal staff Three to five year cycles to bridge staff turnover, knowledge loss issues

Develop key performance indicators, phase-in schedule

Make final decision Implement, refine transition plan

Review 20%-33% of portfolio annually (3-5 year cycles) Rebuild forecasts, especially after major transactions Confirm type and approach for each liability (GAAP terms are obligation,

commitment, contingency, guarantee) Reclassify funding type as needed (ARO, OPEX, CAPEX, reserves)

Rebuild exit strategies Reduce the liabilities (“work it down”) Evaluate captive insurance (“fund it, isolate it”)

© 2015 Environmental Risk Communications, Inc.

Best Practices in FVM

Train everyone to use ASC 820 FVM Project managers Key external consultants Corporate leadership, asset managers, property managers Auditors Counsel

Use your spending data to justify -30%/+50% accuracy; reassure cost engineers (“never shoot the messenger”) that uncertainty is expected

Document pro/con of projects and current strategies (“what has to go right” “what can go wrong”)

Factor in strategy failure (starting over), in-kind services

Include sites that are “done”, “new”, “sold”, “never studied”

Include counterparty risk (% allocation grows)

© 2015 Environmental Risk Communications, Inc.

Best Practices: Site Estimates

Common work breakdown structure for all sites in the portfolio

Study, remedial design, remediation, OM&M, legal, project management

For costs >$100K, pinpoint Level 1 and 2 inputs “Four years OM&M after excavation concludes”

“Groundwater P&T system based on two pore volumes; five-year term, single flood event to reach 50gpm design requirement”

“25,000 cubic yards of soil, bulking factor of 1.25 due to high sand ratio, 83 miles to approved disposal facility”

Justification for revising the scenario weighting “Completed decision analysis exercise in June 2016”

“Reweighted the three scenarios after the community advisory board meeting in August and email exchange with regulator in September 2016”

“Operating plant asked that closure construction be synchronized with turnaround project X, now scheduled for Q4-2017”

© 2015 Environmental Risk Communications, Inc.

Outline for Today’s Webinar

Speaker’s Bio and High-Level View

Fair Value Measurement in GAAP

Why to Document Fair Value Measurement

ERCI Observations

How to Document Fair Value Measurement

Q&A √

© 2015 Environmental Risk Communications, Inc.

Resources to Read

ASC 410 – current FASB GAAP on environmental obligations

ASC 820 – current FASB on fair value measurement

GASB 49 – Pollution Remediation Obligations

GASB 72 – Fair Value Measurement and Application

28

© 2015 Environmental Risk Communications, Inc.

Next Steps

Website: www.erci.com

LinkedIn Group – webinar announcements

YouTube page – select webinar recordings

Email [email protected] or call me at (415) 336-5085 PDF of this presentation (original PPTX format on request)

March 2015 webinars on Managing Nonperformance Risk of Environmental Counterparties Obstacles to Recognizing and Measuring Environmental Liabilities

April 2015 webinars on Estimating and Disclosing Environmental Liabilities Auditor’s Tough Questions on Environmental Liabilities Calculating Counterparty Risk on Environmental Liabilities

29