Disclaimer & Disclosures: This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

https://www.research.hsbc.com

Play interview withAnderson Chow

EQUITIESINDUSTRIALSNovember 2018

By: Anderson Chow

China InfrastructureOn the move again

We estimate an additional RMB2trn is required by the end of 2019e to bring infrastructure spending in line with growth in fixed asset investment

Central government financing could be the key funding source as local governments continue to deleverage

Buy ideas include CRCC, Gezhouba, Anhui Conch, and CRRC Corp

1

EQUITIES ● INDUSTRIALS

November 2018

THIS CONTENT MAY NOT BE DISTRIBUTED TO THE PEOPLE'S REPUBLIC OF CHINA (THE

"PRC") (EXCLUDING SPECIAL ADMINISTRATIVE REGIONS OF HONG KONG AND MACAO)

Why read this report?

Our analysis shows that China needs to increase

infrastructure investment by RMB2trn by the end

of 2019e to stabilise the growth rate of fixed

asset investment at around 5%.

We identify where the money is likely to be spent

and why the central government is likely to play a

major role in financing new projects through

several different channels.

We show which companies should benefit most

and why this current increase in infrastructure

investment should be more sustainable than

those in the past.

EQUITIES ● INDUSTRIALS

November 2018

2

Source: Wind, local governments, Ministry of Finance PPP Centre, HSBC

Financing China’s infrastructure

Local governments’ explicit debt as of July 2018 –

97% in the form of municipal bonds

BUY

CRCC (1186 HK)

Construction: A major

infrastructure contractor that

will benefit from increases in

infrastructure investment.

Strong balance sheet and

positive cash flow will help

increase asset turnover and

help gain market share in

Chinese construction

BUY

CRRC (1766 HK)

Machinery: Leveraged to

increasing locomotive and

freight wagon orders driven

by shift of freight transport

from highway to railway by

2020. Internal restructuring

should lower overhead costs

and enhance profitability

and ROE over the long term

BUY

BUY

Anhui Conch

(914 HK / 600585 CH)

Construction Materials:

Indisputable cost leader of

the industry. GP/ton

expansion driven by

supply-side control.

Attractive dividend yield of

around 6% for 2018e

BUY

Gezhouba (600068 CH)

Construction: Strong

earnings growth over 20%

p.a. with a 5-year order

backlog to revenue ratio.

Rapid expansion in

environmental division; focus

on recycling of solid waste

offers long term upside

Provincial municipal bonds and LGFV debt

outstanding as % of government income, 2017

Operating cash flows are expected to be positive in the coming years

Total gross output value of construction (RMBtrn)

China’s fixed asset investment growth

Worth of projects in the Ministry of Finance’s PPP

approved database at the end of June 2018

PPP projects by type of project as at 2Q18

RMB17.2trnRMB2trn RMB11.9trnIncrease in infrastructure investment is required to

stabilise fixed asset investment growth at +5%

We have Buy ratings on four industry leaders

RMB192bn2 provinces

30%-100%

RMB8.8trn10 provinces

100%-150%

RMB32.8trn19 provinces

100%-150%

RMB9trn Total fixed assets

y-o-y

RMB6trn

RMB3trn

Jan-18

21.4 22.5 23.7 25.0

Sep-18

0

15%

10%

5%

0%

+5%

31%

29%

13%

27%

Municipal

projects

Transport

infrastructure

Land

development

Others

2017

7%2020e

8%

The 3 major infrastructure

contractors combined would see

market share increase

2017 2018e 2019e 2020e

3

EQUITIES ● INDUSTRIALS

November 2018

Sizing up the investment 4

RMB2trn reasons for optimism 4

Where is the project funding

coming from? 5

Ranking of Chinese

construction companies 6

More sustainable growth 7

RMB2trn to stabilise infrastructure

investment by the end of 2019e 7

Funding infrastructure investment in

a deleveraging environment 9

PPP focus should shift towards

commercial projects 17

Chinese construction industry

consolidation 19

ESG matters for the Chinese

construction industry 22

Outlook for companies 25

Chinese construction companies 25

Capital goods – demand to

hold up in 2019 26

Disclosure appendix 53

Disclaimer 56

Contents

EQUITIES ● INDUSTRIALS

November 2018

4

RMB2trn reasons for optimism

In July 2018, the Chinese government announced its intention to increase infrastructure

investment to stabilise domestic demand in light of the challenging economic conditions caused

by trade tensions. This is clearly much-needed good news for construction companies, which

have suffered due to the rapid fall in infrastructure investment, as a result of China’s

deleveraging process. The fall in share prices over the past few quarters means that these

companies are trading at either close to or below levels last seen in 2014, another period of

crisis for the industry. However, investors are unsure about the magnitude and timing of the

increase, where the money is coming from, and who stands to benefit most. This report aims to

answer these questions.

Highlights

We estimate RMB2trn will be required by the end of 2019 for growth in total infrastructure

investment to recover to a rate similar to China’s overall fixed asset investment (FAI) growth

of 5.4%.

To put this in context, growth in Chinese infrastructure investment has been negative since

May 2018. RMB2trn would represent a hefty boost, given that total infrastructure investment

in 2017 was cRMB17trn.

The first green shoots are already visible – in September the broad measure of

infrastructure investment declined 2.6% y-o-y, an improvement on August’s fall of 5.4%.

We stress that the current policy initiative is different in nature from the huge stimulus

package of 2008-10 that was a response to the Global Financial Crisis. Back then, the pace

of construction and new project tenders soared immediately after the policy statement. We

think the current increase in investment is taking place in a more orderly fashion and is

focused on stabilising rather than stimulating domestic demand.

Our discussions with regulators, contractors, and government think tanks indicate that the

central government is likely to play an important role in providing project funding.

Sizing up the investment

Investors are unsure about the magnitude and timing of the increase

in China’s infrastructure investment, where the money is coming

from, and who stands to benefit most. We estimate that a further

RMB2trn is required by the end of 2019e to stabilise the growth rate

of fixed asset investment at around 5%. Increased funding from the

central government over the coming months should allay concerns

about the financing of existing and new projects. Meanwhile, we think

PPP financing should shift towards commercial projects in order to

attract private capital for infrastructure investment. Buy ideas include

CRCC, Gezhouba, Anhui Conch, and CRRC Corp.

Some much-needed good

news for construction

companies

5

EQUITIES ● INDUSTRIALS

November 2018

We think the first stage of the rise in infrastructure investment should benefit construction

company earnings in 2H18. The second stage should see an increase in new project

tenders in 2019.

Private involvement in infrastructure development would depend on public-private-

partnership (PPP) project financing shifting focus to more user-pay projects with reasonable

commercial returns. More transparent regulations on infrastructure returns can be expected

in the coming years, especially for toll roads and the railway sector.

Construction companies should benefit from faster project execution and more new projects

in 2019e. We think they are gradually gaining market share as small and medium sized

companies struggle to get financing.

Based on six key metrics, we prefer CRCC (1186 HK) and Gezhouba (600068 CH) among

the eight listed Chinese construction companies in the Hong Kong/China market under our

coverage.

Where is the project funding coming from?

Two major concerns among investors about the policy to increase infrastructure investment are:

(1) the current deleveraging process may hold back project funding availability; and (2) local

governments in China generally have a high level of financial leverage and would not be able to

provide funding. Our discussions with regulators, contractors, and government think tanks

indicate that the central government is likely to play an important role in providing project

funding.

We include research from HSBC’s China Fixed Income Research team on 31 provinces, 297

prefecture level cities, and 1,815 local government financing vehicles (LGFVs) in our

assessment of the local government debt issue. We think that while 35 cities out of the 297

prefecture level cities would be considered as having high financial leverage, a sharp rise in the

number of default is unlikely in China.

In this report we discuss ways in which the central government could increase funding support

to facilitate the increase in infrastructure investment. They include:

1. Increase transfer payments to local governments,

2. Increase the local government project-specific bond issuance programme, and

3. Increase the municipal bond swap quota.

The PPP financing model has been a major source of funding for a variety of public works since

2015. A major regulatory review of the PPP project database and financing structure was

completed in March 2018. Stricter equity financing for PPP projects and rigid monitoring of local

government repayment capability for PPP projects would benefit the major Chinese construction

companies. The Chinese construction industry has a total gross output value of c.RMB22trn per

annum and we expect potential industry consolidation will help major contractors gain market

share in the coming years.

We also think China’s PPP model should shift its focus to projects that generate commercial

returns. This would attract private capital to participate in either greenfield new infrastructure

development projects or invest in existing brownfield projects. This would help achieve the

government’s policy of encouraging private investment and also help local governments to

generate capital by selling their existing infrastructure assets to private enterprises. In our view,

more private involvement broadens the funding sources for local government while at the same

time improving the services provided by local government for residents.

The central government is

increasing leverage while

local governments continue

to deleverage

The PPP model should focus

on commercial returns in

order to attract private capital

EQUITIES ● INDUSTRIALS

November 2018

6

Ranking of Chinese construction companies

Our preferences within the Chinese construction sector is based on six key factors that we

consider to be most relevant for share price performance. From an operational perspective, we

think new contract growth, ROE, and 3-year EPS CAGR are the most important indicators.

From a valuation perspective, we think investors should focus on PBV, PER, and EV/EBITDA.

Based on this ranking exercise, we prefer CRCC (1186 HK) and Gezhouba (600068 CH) among

the eight listed Chinese construction companies in the Hong Kong/China market under our

coverage.

Figure 1: Construction company rankings based on six key factors

Ticker TP

(LC)

Rating FY19e new contract

growth

2019 ROE

3-year EPS

CAGR

FY18e PBV

FY18e

PE

FY18e

EV / EBITDA

Score Rank

CRCC 1186 HK HKD14.9 Buy 4 3 3 3 4 1 18 1 Gezhouba 600068 CH RMB10.5 Buy 1 1 1 6 3 6 18 2 CSCI 3311 HK HKD9.70 Buy 5 4 5 2 1 2 19 3 CSCEC RMB Buy 3 2 8 6 3 4 26 4 CRG 390 HK HKD8.6 Buy 6 5 4 4 5 3 27 5 CCCC 1800 HK HKD9.10 Buy 7 6 6 1 2 5 27 6 MCC RMB Buy 2 7 2 5 7 7 30 7 PCC RMB Buy 1 8 7 6 6 8 36 8

Source: HSBC estimates

Figure 2: Top Buy ideas – beneficiaries from rising infrastructure investment

Analyst Sector Stock Ticker Rating/TP /upside

Investment thesis

Anderson Chow* The Hong Kong and Shanghai Banking

Corporation Limited

Construction CRCC 1186 HK/ 601186 CH

Buy/Buy, HKD14.9/RMB13.3, +42.4%/+20.6%

A major infrastructure contractor that will benefit from increases in infrastructure investment.

Strong balance sheet and positive cash flow will help increase asset turnover and help gain market share in the Chinese construction industry.

Machinery CRRC 1766 HK Buy, HKD8.8 +23.0%

Leveraged to increasing locomotive and freight wagon orders driven by a shift in freight transport from highway to railway by 2020.

Internal restructuring would lower overhead costs and enhance profitability and ROE over the long term.

Howard Lau* The Hong Kong and Shanghai Banking

Corporation Limited

Construction Materials

Anhui Conch

914 HK/ 600585 CH

Buy/Buy, HKD58/RMB53, +35.8%/+55%

Indisputable cost leader of the industry.

GP/ton expansion driven by supply-side control.

Attractive dividend yield of around 6% for 2018e.

Corey Chan* HSBC Qianhai

Securities Limited

Construction Gezhouba 600068 CH Buy/RMB10.50/ +60.8%

Strong earnings growth over 20% p.a. with a 5-year order backlog to revenue ratio.

Rapid expansion in environmental division focus on recycling of solid waste offers long-term upside.

Note: Priced as of 7 November 2018.* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations. Source: HSBC estimates, HSBC Qianhai Securities estimates

Prefer CRCC and Gezhouba

7

EQUITIES ● INDUSTRIALS

November 2018

RMB2trn to stabilise infrastructure investment by the end of 2019e

On 23 July 2018, the Chinese government stated that it would use fiscal policy to support

domestic demand and monetary policy would ensure reasonable liquidity in the financial

system. The following is a summary of the key government policy statements to support the

initiative:

1. The People’s Daily, in an article published on 19 July 2018, it stated that the

deleveraging process had achieved initial results and that China was entering a phase

of stable leverage.

2. On 7 August 2018, China Railway Corporation (private, not rated) stated that it

intended to increase its railway infrastructure investment budget to RMB800bn for

2018, up from the initial budget of RMB732bn. Please see our report, China

Industrials, Rising tide lifts all boats, 7 August 2018.

3. The National Development and Reform Commission (NDRC), China’s key

macroeconomic planning body, announced on 19 September 2018 its intention to

speed up existing infrastructure project execution. The NDRC also stated that the

government will accelerate a batch of significant new project tenders to ensure the

sustainability of investment. This indicates the investment recovery could last well into

2019 and beyond. Please see our report, China Infrastructure, More new projects and

more sustainable investment, 19 September 2018.

4. The PBoC has reduced most of Chinese banks’ reserve requirement ratios (RRR) by

250bp in 2018 y-t-d to help liquidity.

5. The planned RMB1.35trn local government project-specific bond issuance programme

was completed in October 2018 to speed up existing project execution. Most of the

bond issuance happened between July and October as only c.RMB200-300bn was

issued in 1H18.

More sustainable growth

China plans to increase infrastructure investment to stabilise

domestic demand, while continuing to deleverage local governments

and state-owned companies

The seemingly contradictory nature of these policies may produce a

more sustainable investment growth rate than previous stimulus

programmes

We prefer contractors and building materials companies and selected

capital goods manufacturers

Using fiscal policy to

stabilise Chinese domestic

demand

EQUITIES ● INDUSTRIALS

November 2018

8

6. On 1 November 2018, The Ministry of Finance advanced its 2019 budget payment

amounting to RMB227bn to 33 provincial governments to help reduce their financial

burden.

The current policy stance is to stabilise domestic demand rather than to stimulate the economy

as was the case in 2008-10. There has been no official estimate of the meaning of

“stabilisation”. Growth in Chinese infrastructure investment (in a broad sense – transportation,

utilities, and other municipal works) has been negative since May 2018. We finally saw green

shoots emerging in September 2018 where the broad measure of infrastructure investment

declined 2.6% y-o-y, a smaller decline than the -5.4% in August.

Based on our estimate, we think about RMB2trn investment in infrastructure is required between

now and the end of 2019e in order to stabilise the growth rate of infrastructure investment at

around 5%, which is similar to the current FAI growth rate and consistent with HSBC China

Economist’s forecast of FAI growth of 5.4% in 2019e.

Figure 3: c.RMB2trn needed to stabilise infrastructure investment by the end of 2019e

(RMBm) Total infrastructure

investment

y-o-y

growth

Sept 2017 y-t-d infrastructure investment 12,167 Sept 2018 y-t-d infrastructure investment 12,260 0.8% 2017 total investment 16,980 Implied total infra investment (assuming +5.4% growth will be achieved in 2018e) 17,897 5.4% Total incremental infra investment required to achieve +5.4% growth for FY18e is 5,637 17.1%

less: planned investment in 4Q18 (assume similar to 4Q17) 4,800 Estimated increase for infrastructure investment in 4Q18 800 to 1000 Estimated increase in investment in 2019 to maintain +5.4% growth 966 Total increase in infrastructure investment by 2019 1,766 to 1,966

Source: HSBC estimates, Wind

Figure 4: China infrastructure investment trend – green shoots emerging

Source: WIND, HSBC calculations

The current policy is to

stabilise domestic demand

rather than stimulate the

economy as was the case in

2008-10

9

EQUITIES ● INDUSTRIALS

November 2018

Figure 5: China total FAI trend – hovering at around +5%

Source: CEIC, HSBC calculations

Funding infrastructure investment in a deleveraging environment

Many Chinese construction companies and capital goods manufacturers have outperformed the

Hong Kong/China equity market since late July 2018 as illustrated in Figure 6. Building material

suppliers, such as cement companies, have enjoyed strong share price performance since 2017

and some stocks may have seen profit taking in recent months. However, we believe the key

driver for cement stocks in this upcycle is pricing rather than a potential increase in demand. We

expect cement prices in China to rise c.5% in 2019e due to supply coordination among major

regional players. Thus, we think the recent weakness in share price could offer a good buying

opportunity.

At the same time we see more upside for Chinese infrastructure-related companies in the

coming quarters. The most common push back from investors is the concern about project

funding, especially at the local government level. It is not an easy task to finance infrastructure

investment when deleveraging remains in place.

Our recent trips to China included meetings with regulators, government think tanks,

contractors, and capital goods manufacturers. We think it is likely that project funding will come

in the form of greater contribution by the central government. This could be achieved through a

higher transfer of payments to local governments in 2019. These transfers have been one of the

major sources of funding for local governments historically and could play a pivotal role in the

near future. Moreover, an increase in local government project-specific bond issuance in 2019

is also a possibility. We have already seen a similar type of project-specific issuance

programme increased to RMB1.35trn in 2018 from RMB850bn in 2017.

Outperformance by Chinese

contractors and capital

goods companies to continue

EQUITIES ● INDUSTRIALS

November 2018

10

Figure 6: Chinese industrial companies relative price performance vs. HSCEI Index

Company Ticker Relative performance since

19 July 2018

Capital Goods Zhuzhou CRRC Times 3898.HK 2.8% CRRC Corp 1766.HK 17.5% CRRC Corporation-A 601766.SS 17.2% Zoomlion Heavy Industry 1157.HK -8.6% Zoomlion Heavy Industry-A 000157.SZ -11.1% Lonking Holdings 3339.HK -40.6% Weichai Power-A 000338.SZ -7.2% Weichai Power 2338.HK -11.7% Sinotruk 3808.HK -9.5% China Yuchai CYD.N -21.7% Construction CRCC 1186.HK 33.4% CRCC-A 601186.SS 28.9% CCCC 1800.HK 4.2% CCCC-A 601800.SS 12.3% CRG 0390.HK 29.9% CRG-A 601390.SS 6.8% CSCI 3311.HK -29.2% Building Materials Anhui Conch 0914.HK -2.5% Anhui Conch-A 600585.SS 0.1% BBMG 2009.HK -17.6% BBMG Corp-A 601992.SS -1.8% CNBM 3323.HK -16.5% CR Cement 1313.HK 0.8% Asia Cement China 0743.HK 28.4% Taiwan Cement 1101.TW 51.0% Asia Cement 1102.TW -41.7% China Conch Venture 0586.HK -10.6%

Note: Priced as of 7 November 2018. Source: Refinitiv Datastream, HSBC

Figure 7: Breakdown of local government financing source for FY17

Source: Wind, HSBC

41%

29%

29%

1%

General public income

Transfer payment from central govt.

Govt funding income

Income from SOE ownership

11

EQUITIES ● INDUSTRIALS

November 2018

A summary of Chinese local government debt situation

HSBC China Fixed Income Analyst, Helen Huang, published a detailed report, China Onshore

Insights Local Government Debt: the knowns and unknowns, looking at the local government debt

situation, including the financial position of 1,815 LGFVs. While we think there are default risks for

some LGFVs, this should not cause a sharp rise in the default rate. If we combine government and

LGFV debt, we think that 35 cities out of the 297 prefecture level cities would be considered as

having high financial leverage. The conclusion is that the total explicit and implicit debt from local

government amounts to around RMB47trn. The following is an extract from her report that provides

background information on the Chinese local government debt situation.

Managing the debt of local governments and their related entities is one of the most important factors

determining China’s financial stability. Ideally, the market would like to be able to differentiate

between weak and strong local governments in order to manage exposure to the sector. However,

given the limited amount of information available, it is very difficult to do this effectively.

The reason is ‘implicit debt’ – borrowing mainly by LGFVs as opposed to ‘explicit’ debt in the

form of municipal bonds incurred by the local governments themselves. We have discussed this

developing theme in earlier reports (LGFV: Market-driven default mechanism is unrealistic,

China Onshore Insights, 5 July 2018; LGFV bond stand-off: It’s time to reach a compromise,

China Onshore Insights, 19 October 2017).

In a nutshell, an LGFV is a shell company created by a local government for the purpose of

borrowing money from the market and then investing in local infrastructure projects. They were

originally formed because the issuance quota of municipal bonds was very limited and strictly

controlled. LGFVs’ borrowing is booked on their balance sheets, not those of the local

governments. In other words, LGFVs help to enlarge China’s fiscal expansion without inflating

the government deficit, at least not visibly. And the reason why LGFVs can keep borrowing from

the market is that local governments still provide them with what many investors regard as an

implicit guarantee.

This report seeks to narrow the information gap in terms of what is known about the debt levels

of different local governments. We have sifted through debt and revenue data for 31 provinces,

297 prefecture-level cities, and 1,815 LGFVs contained in hundreds of local budget reports and

databases. When necessary, we have also made our own educated guesses. As in previous

reports, we use a Q&A format. A full list of data is provided at the end of the report.

1. How much explicit debt do local governments have?

As of July 2018, local governments’ explicit debt amounted to RMB17.2trn, 97% in the form of

municipal bonds. As Figure 8 shows, the share of municipal bonds in local debt has increased

significantly over the past four years. Some RMB12.7trn of municipal bonds have been issued

between 2015 and 2018 to refinance various other forms of local debt. By doing this, the

government was hoping to thoroughly clean up its implicit debt.

35 out of 297 prefecture cities

have high levels of financial

leverage

The market would like to be

able to differentiate between

weak and strong local

governments

Local government explicit

debt totals RMB17.2trn…

EQUITIES ● INDUSTRIALS

November 2018

12

Figure 8: Local government explicit debt outstanding

Source: Wind, HSBC estimates

This local explicit debt amount is not big – just 20.5% of China’s estimated nominal GDP in

2018e and 76.2% of local governments’ estimated income in 2018e. And the percentage has

dropped significantly over the past four years as the municipal bond swap programme has

progressed, as illustrated in Figures 9 and 10.

Note that there are four parts to local government income (Figure 11): general public income

(mainly from taxes and fees), government fund income (mainly land sales), transfer payments

from central government (Beijing redistributes fiscal or tax revenue among local governments),

and income from local SOEs.

Figure 9: Local government explicit debt as % of GDP

Figure 10: Local government explicit debt as % of local government income

Source: Wind, HSBC estimates Source: Wind, HSBC estimates

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2013E 2014 2015 2016 2017 2018E

RM

Bbn

Municipal bonds Other forms

19%

20%

21%

22%

23%

24%

25%

2013E 2014 2015 2016 2017 2018E

Local gov debt / GDP

74%

76%

78%

80%

82%

84%

86%

88%

2013E 2014 2015 2016 2017 2018E

Local gov debt / local gov income

13

EQUITIES ● INDUSTRIALS

November 2018

Figure 11: Local government income, broken down by source of income

Source: Wind, HSBC estimates

When we break down the outstanding amount of municipal bonds by province and municipality,

the result is not too alarming either. There are two thresholds of sustainable government debt

referred to by such organisations as the IMF and widely quoted in the China onshore market by

researchers and officials: they are 60% of GDP and 150% of government income. As Figures 5

and 6 illustrate, only Guizhou exceeds both. Many provinces are not even close.

Figure 12: Municipal bonds outstanding as % of GDP (2017)

Source: Wind, Local governments, HSBC

-

5,000

10,000

15,000

20,000

25,000

30,000

2012 2013 2014 2015 2016 2017 2018E

RM

Bbn

General public income Gov fund income Transfer payment from central gov Income from SOE ownership

0%

10%

20%

30%

40%

50%

60%

70%

Gui

zhou

Liao

ning

Inne

r M

ongo

lia

Yun

nan

Hun

an

Sha

anxi

Hai

nan

Nin

gxia

Fuj

ian

Tia

njin

Jilin

Qin

ghai

Sic

huan

Hei

long

jiang

Xin

jiang

Gua

ngxi

Sha

ndon

g

Jian

gsu

Anh

ui

Zhe

jiang

Heb

ei

Hub

ei

Cho

ngqi

ng

Hen

an

Jian

gxi

Gan

su

Sha

nxi

Gua

ngdo

ng

Sha

ngha

i

Bei

jing

Tib

et

Threshold

EQUITIES ● INDUSTRIALS

November 2018

14

Figure 13: Provincial municipal bonds outstanding as % of government income (2017)

Source: Wind, Local governments, HSBC

2. What, then, should the market worry about?

The answer is implicit debt. Local governments have repeatedly said that all LGFVs should now

become standalone SOEs. They have also stated that they will no longer provide implicit

guarantees for LGFVs, but their actions suggest otherwise.

A recent case provides some evidence for this. In August, a bond default by a local SOE in

Xinjiang Province was fixed in just two days. The company in question, Xinjiang Production and

Construction Corps Sixth State-owned Assets Management, is not even strictly speaking an

LGFV – it is an SOE whose operations are closely connected with local governments. It is more

understandable when support is given to an entity that is widely recognised as an LGFV, as

happened when Tianjin Municipal Construction and Development’s missed payment of a

RMB500m trust loan in April 2018 was made in full in less than a month.

The trouble for the market, however, is knowing how much implicit debt there is. Local

governments’ assertion of zero tolerance since 2015 on the one hand and the obvious

contradiction in their actual bailout behaviour on the other simply raises market concerns that

the implicit debt is formidable. So, to address this concern, what we did is this: we dug deep into

the data to track all the LGFV debt we could identify and added it to local governments’ explicit

debt to see how bad it might actually be.

LGFV debt has grown fast to around RMB30trn in 2017. The opposite was meant to happen

through the municipal bond swap programme, which started in 2015.

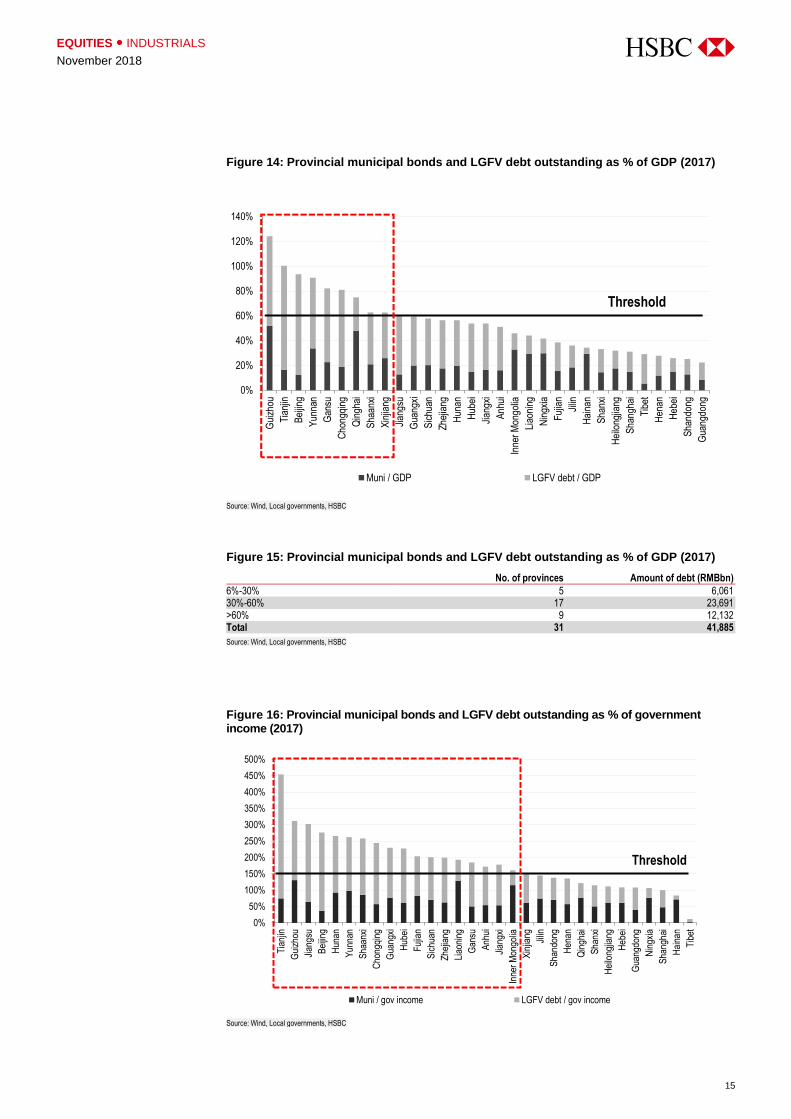

Figures 14 and 15 show that once the LGFV debt is added, the debt to GDP ratio in nine of the

31 provinces exceeds the 60% threshold. Figures 16 and 17 show that debt to government

income in 19 of the 31 provinces exceeds the 150% threshold. And Figure 18 shows that eight

provinces breached both thresholds. Among them, Tianjin and Guizhou Province have

particularly high leverage levels, both having debt to GDP ratios above 100% and debt to

government income ratios above 300%.

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Gui

zhou

Liao

ning

Inne

r M

ongo

lia

Yun

nan

Hun

an

Sha

anxi

Hai

nan

Nin

gxia

Fuj

ian

Tia

njin

Jilin

Qin

ghai

Sic

huan

Hei

long

jiang

Xin

jiang

Gua

ngxi

Sha

ndon

g

Jian

gsu

Anh

ui

Zhe

jiang

Heb

ei

Hub

ei

Cho

ngqi

ng

Hen

an

Jian

gxi

Gan

su

Sha

nxi

Gua

ngdo

ng

Sha

ngha

i

Bei

jing

Tib

et

Threshold

LGFV debt increased rapidly

to RMB30trn by 2017

15

EQUITIES ● INDUSTRIALS

November 2018

Figure 14: Provincial municipal bonds and LGFV debt outstanding as % of GDP (2017)

Source: Wind, Local governments, HSBC

Figure 15: Provincial municipal bonds and LGFV debt outstanding as % of GDP (2017)

No. of provinces Amount of debt (RMBbn)

6%-30% 5 6,061 30%-60% 17 23,691 >60% 9 12,132 Total 31 41,885 Source: Wind, Local governments, HSBC

Figure 16: Provincial municipal bonds and LGFV debt outstanding as % of government income (2017)

Source: Wind, Local governments, HSBC

0%

20%

40%

60%

80%

100%

120%

140%

Gui

zhou

Tia

njin

Bei

jing

Yun

nan

Gan

su

Cho

ngqi

ng

Qin

ghai

Sha

anxi

Xin

jiang

Jian

gsu

Gua

ngxi

Sic

huan

Zhe

jiang

Hun

an

Hub

ei

Jian

gxi

Anh

ui

Inne

r M

ongo

lia

Liao

ning

Nin

gxia

Fuj

ian

Jilin

Hai

nan

Sha

nxi

Hei

long

jiang

Sha

ngha

i

Tib

et

Hen

an

Heb

ei

Sha

ndon

g

Gua

ngdo

ng

Muni / GDP LGFV debt / GDP

Threshold

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

500%

Tia

njin

Gui

zhou

Jian

gsu

Bei

jing

Hun

an

Yun

nan

Sha

anxi

Cho

ngqi

ng

Gua

ngxi

Hub

ei

Fuj

ian

Sic

huan

Zhe

jiang

Liao

ning

Gan

su

Anh

ui

Jian

gxi

Inne

r M

ongo

lia

Xin

jiang

Jilin

Sha

ndon

g

Hen

an

Qin

ghai

Sha

nxi

Hei

long

jiang

Heb

ei

Gua

ngdo

ng

Nin

gxia

Sha

ngha

i

Hai

nan

Tib

et

Muni / gov income LGFV debt / gov income

Threshold

EQUITIES ● INDUSTRIALS

November 2018

16

Figure 17: Provincial municipal bonds and LGFV debt outstanding as % of government income (2017)

No. of provinces Amount of debt (RMBbn)

30%-100% 2 192 100%-150% 10 8,867 >150% 19 32,826 Total 31 41,885

Source: Wind, Local governments, HSBC

Figure 18: Provincial government debt level (2017)

Source: Wind, Local governments, HSBC

Current government debt policies essentially rely on a limited explicit debt swap quota and various

government bailouts to maintain both an artificially low explicit debt level and a low default rate.

However, there is no free lunch. In our view, one consequence of this strategy is that the

government will gradually move towards fiscal austerity, i.e. using cash flow to pay back debt.

This year, government income (central plus local, including both general public and government

fund income) grew 14% y-o-y as of August, when nominal GDP grew 10% y-o-y as of the first

half (Figure 19).

An official from the PBoC wrote an article in July this year criticising slow fiscal spending and an

over-dependence on monetary policy to support economic growth (source: Fiscal policy has

much bigger room/当前形势下财政政策大有可为, Xu Zhong, Head of Research Department,

PBoC, 13 July 2018). We believe it is a fair criticism, but local governments have to preserve

more cash to prepare for future debt repayment obligations. Also, LGFVs, rather than local

treasuries, are the main drivers of infrastructure investment. Figure 20 shows that the 1,815

Tianjin

GuizhouJiangsu

BeijingHunanYunnanShaanxi

ChongqingGuangxi

Hubei

FujianSichuan

Zhejiang

Liaoning Gansu

AnhuiJiangxi

Inner Mongolia XinjiangJilinShandong Henan

QinghaiShanxi

HeilongjiangHebei

Guangdong Ningxia

ShanghaiHainan

Tibet0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

500%

0% 20% 40% 60% 80% 100% 120% 140%

(Gov + LGFV debt) / GDP, 2017

(Go

v +

LGF

V d

ebt)

/ Go

v in

com

e, 2

017

Most leveraged:8 provinces

Least leveraged:11 provinces

17

EQUITIES ● INDUSTRIALS

November 2018

LGFVs invested around RMB3trn per year between 2015 and 2017, much more than the net

municipal project bond issuance quota, which officially is the main funding channel for local

fiscal investment in infrastructures. Now these LGFVs are supposed to wind down, according to

current government policies – so no wonder local infrastructure investment is slowing down.

Figure 19: Nominal GDP and government income, growth y-o-y

Source: Wind, HSBC

Figure 20: Explicit and implicit fiscal spending budget in local infrastructure

Source: Wind, Central government, HSBC

PPP focus should shift towards commercial projects

Public-private partnerships (PPPs) have been an important source of Chinese infrastructure

project funding since 2014. During 2017, the government embarked on a major review of project

structure, financing arrangements, and local government fiscal capability to ensure PPP project

financing would be sustainable over the long term. The review of the PPP project database at

the Ministry of Finance was completed in March 2018; however, reviews or restructuring of

existing PPP projects appears to be ongoing at the local government level.

At the end of June 2018, Ministry of Finance’s PPP project database had RMB11.9trn worth of

projects in the approved database (i.e. under active management process, 管理库) and about

RMB5.4trn worth of projects in the reserves database (i.e. awaiting formal approval,储备库).

-10%

-5%

0%

5%

10%

15%

20%

Mar2013

Jul2013

Nov2013

Mar2014

Jul2014

Nov2014

Mar2015

Jul2015

Nov2015

Mar2016

Jul2016

Nov2016

Mar2017

Jul2017

Nov2017

Mar2018

Jul2018

Growth YoY, nominal GDP Growth YoY, Gov income (general public income + gov fund income)

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2015 2016 2017 2018

RM

Bb

n

LGFV investing cash flow Muni net issuance quota, project bonds

EQUITIES ● INDUSTRIALS

November 2018

18

The small decline in March and April 2018 in the database was a result of the project database

review.

We think there will be further potential amendments to the PPP regulations over the next 6 to 12

months. These potential changes could impact new PPP projects and private participation. We

think two potential changes may be more impactful from equity investors’ perspective:

1. Linking the local government debt level to the 10% fiscal account threshold in

determining whether a local government could propose additional new PPP projects.

Currently no local government can allocate more than 10% of their annual fiscal

revenue to finance PPP projects (including initial investment in PPP projects,

repayment or government subsidies of PPP projects). In order to ensure local

government debt remains under control, we think the Ministry of Finance is likely to

impose restrictions on the balance sheet of all local governments along with the

existing threshold on government revenue. This should lower credit risk of PPP

projects, however, it could slow down new PPP project inflows.

2. Private participation in PPP projects remains low and the NDRC has been stressing

the importance of getting the private sector involved in infrastructure investment.

Currently only c.9% of PPP projects are using the user-pay system to generate

repayment or project returns. Almost 63% of PPP projects rely on a mix of government

subsidies and user pay. We think a shift towards more user-pay systems for PPP

projects could encourage private sector participation. This should also include putting

up existing or brownfield assets or services as PPP projects to attract private sector

investment. Other regulatory changes may be required to improve the transparency on

project returns, such as the pending revision to Expressway Management Ordinance.

Figure 22: PPP by payment method (2Q18) Figure 23: PPP by type of project (2Q18)

Source: Ministry of Finance PPP Center Source: Ministry of Finance PPP Center

User pay9%

Government subsidy and user …

Goverment pay29%

Municipal projects

31%

Transport infra29%

Land development

13%

Others27%

Figure 21: Total MOF PPP approved project database

(RMBbn) Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18

Total 10,760 11,350 11,960 11,560 11,390 11,880 11,900

Project in 准备阶段 preparatory stage 2,860 2,730 2,880 2,650 2,470 2,650 2,570

Project in 采购阶段 procurement stage 3,300 3,720 3,710 3,400 3,260 3,360 3,330

Project in 执行阶段 execution stage 4,600 4,900 5,370 5,510 5,660 5,870 6,000

Proportion of projects under execution 42.8% 43.2% 44.9% 47.7% 49.7% 49.4% 50.4%

Source: Ministry of Finance PPP Center

19

EQUITIES ● INDUSTRIALS

November 2018

Chinese construction industry consolidation

As at the end of 2017, there were 88,059 construction companies in China. It has always been

a fragmented industry with a total gross output value of RMB21.4trn in 2017. The three major

Chinese infrastructure contractors listed in Hong Kong (CRCC, CRG, and CCCC) only had

about a combined 7% market share in 2017. This compares to a 10.8% market share back in

2010.

Major contractors lost market share after the 2008-10 fiscal stimulus. Small and medium-sized

contractors, either private or controlled by local government and LGFVs, gained market share

as investment-related projects became more important than cash construction projects. Also,

shadow banking products were helping project financing for many smaller players. The de-

leveraging process and tightening of PPP regulations meant the small and medium-sized

contractors found it increasingly difficult to secure financing. Since April 2018 wealth

management and trust products have not been allowed to participate in PPP project equity

funding. We believe this was a key negative for the smaller players.

Based on our current revenue forecast, we expect the major infrastructure contractors to

gradually increase their market share up to 2020. Their financial position has improved in recent

years, with lower financial leverage and operating cash flows expected to be positive in the

coming years. The three major infrastructure contractors combined should see market share

increase from 7% in 2017 to 8% in 2020e.

Not only would revenue growth from the major contractors outpace industry growth (i.e.

infrastructure investment growth), we think more rational competition for projects could also help

profitability for the construction sector in general.

Figure 24: Construction companies' market share to increase going forward

Source: CEIC, Company data, HSBC estimates

Major Chinese contractors in much better financial positions than 2011

Financial leverage ratios for the construction companies under our coverage are under control.

Net debt to equity reached a low point for CRCC, CRG, and CCCC at the end of 2017

compared to 2011, the year after the fiscal stimulus was completed. Seasonality in 1H18 and

initial investment into PPP projects led to increasing leverage for construction companies in

2.6%3.1%

2.7%

3.1%

1.6% 1.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018e 2019e 2020e

Construction companies market share (%)

Total gross output value of construction (Rmb m)

Total Gross Output Value of Construction 1186.HK 390.HK 1800.HK 601668.SS

The three major

infrastructure contractors

should see market share

increase from 7% in 2017 to

8% in 2020e

EQUITIES ● INDUSTRIALS

November 2018

20

1H18. However, we expect financial leverage at the end of 2018 to be similar or an

improvement on 2017’s. This should be driven by project repayments in 2H18 and faster project

execution from improvements in funding. A stronger balance sheet is important in this capital

intensive sector. It would also facilitate project execution and bidding for new contracts. This

supports our view that major contractors will gain market share from non-listed contractors.

Figure 25: Healthy net debt/equity ratios for all companies

Source: Company data, HSBC estimates

Big enough backlog and execution improving

The construction companies’ order backlog has grown over the past few years as new contract

growth was strong and execution could not keep up with the new order inflow. For example, the

Chinese construction sector over the past two years has seen very strong 20-30% new contract

growth, while revenue growth was only in single digits.

Figure 26: Order backlog/revenue ratio

Company 2008a 2009a 2010a 2011a 2012a 2013a 2014a 2015a 2016a 2017a 2018e 2019e 2020e

CRCC 2.1x 2.0x 2.1x 2.6x 3.1x 3.0x 3.0x 3.0x 3.1x 3.5x 4.3x 4.7x 5.0x CRG 1.9x 2.1x 2.2x 2.6x 3.2x 3.6x 3.3x 3.2x 3.5x 4.0x 4.9x 5.5x 6.0x CSCI 2.0x 2.3x 2.7x 3.1x 2.9x 3.1x 2.9x 3.3x 3.3x 3.7x 4.5x 4.7x 4.7x CCCC 1.9x 1.9x 1.9x 2.0x 2.4x 2.2x 2.2x 2.1x 2.7x 3.0x 3.3x 3.5x 3.6x

Source: Company data, HSBC estimates

We see this backlog build up as a double-edged sword. We would prefer to see the ratio go

down to the historical levels of between 2x and 3x from the current 3-4x. Having said that, we

continue to believe that the order books of these construction companies are healthy. We think

sector revenue and earnings growth will soon start to be in sync with new contract growth. This

will be due to a combination of improvement in project execution and a deceleration in the new

contract growth rate to low single digits or flat growth in 2019e and 2020e.

Valuation yet to build in a positive scenario

The massive de-rating that we have seen in construction companies over the past few quarters

means that the companies are trading at either close to or even below their 2011 levels. Back

then, most railway construction projects were suspended and the number of new contracts

shrank after the fatal accident on the Yongtaiwen high-speed-rail line in July 2011.

We think the current situation today is very different and believe current projects under

construction and those with confirmed project funding will continue to move forward. We believe

the construction companies in our coverage trade at attractive valuations based on a number of

different metrics – forward PE, forward EV/EBITDA, and EV/order backlog.

9%

44%

5%

93%

54%

25%

87%

102%

68%

8%

62%

41%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

2011A 2012A 2013A 2014A 2015A 2016A 2017A 1H18 2018E

CRCC CRG CCCC CSCI

21

EQUITIES ● INDUSTRIALS

November 2018

Figure 27: EV/order backlog

Source: Company data, Refinitiv Datastream, HSBC estimates

Improving profitability trend

Profitability has improved over the past three years (especially net profit margins) as the construction

companies have benefited from operating leverage, a higher proportion of PPP projects and, most

importantly, diversifying away to non-infrastructure businesses such as real estate.

Figure 28: Construction company profitability improvement to continue

FY15a FY16a FY17a FY18e FY19e FY20e

CRCC (1186 HK) GP 11.5% 9.2% 9.2% 9.1% 9.0% 8.9% EBIT 3.6% 3.4% 3.5% 3.8% 4.3% 4.2% NPAT 2.2% 2.4% 2.5% 2.7% 3.1% 3.0% CRG (390 HK) GP 8.1% 7.9% 9.1% 9.7% 9.7% 9.6% EBIT 3.3% 3.4% 3.2% 4.4% 4.7% 4.9% NPAT 2.0% 2.0% 2.1% 2.7% 2.9% 3.1% CCCC (1800 HK) GP 12.3% 13.4% 13.1% 13.3% 13.5% 13.6% EBIT 6.4% 7.2% 6.9% 6.8% 7.0% 7.2% NPAT 3.9% 4.4% 4.7% 4.0% 4.1% 4.5% CSCI (3311 HK) GP 13.5% 12.9% 15.2% 14.6% 14.5% 14.4% EBIT 13.3% 13.0% 13.5% 12.9% 12.8% 12.9% NPAT 11.4% 11.2% 10.9% 9.8% 9.9% 10.1%

Source: Company data, HSBC estimates

For CRCC, the infrastructure construction business used to contribute the bulk of both revenue

and operating profit (c.90% of FY09 revenues and 63% of FY09 PBT). However, over the years

higher-margin and fast-growing businesses like real estate have accounted for an increasing

share of profitability. As a result, while infrastructure construction still generates the bulk of

revenues (c.82% in FY17), it accounts for only 49.3% of the FY17 PBT.

CRCC wants to continue to focus on its high-margin real estate property development business

– 6% of FY17 revenues but c.16% of FY17 PBT – and grow the share of revenue to between

10% and 15% in FY18e. Company management wants to continue to focus on tier 2 and tier 3

cities as these offer fast asset turnover opportunities as opposed to tier 1 cities where

developers are often required to operate rental property.

0.05 0.05

0.12 0.06

0.25 0.20

0.42

0.32

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

2011A 2012A 2013A 2014A 2015A 2016A 2017A 2018E

CRCC CRG CCCC CSCI

EQUITIES ● INDUSTRIALS

November 2018

22

ESG matters for the Chinese construction industry

Carbon dioxide reduction of Chinese construction companies

Chinese construction companies under our coverage – CRCC, CCCC, CRG, and CSCI –

consume c87,575 million Kwh per annum. Figure 29 shows the energy consumption trend in

2016 and 2017. Apart from CRCC, which maintained its energy intensity, the other three

contractors have reduced their energy consumption.

Figure 29: Construction companies energy usage (in million Kwh)

Source: Company data, HSBC

All four companies have a CO2 reduction policy and reduced their combined energy usage in

2017 by 4.2% over 2016. Similarly, CRG, CCCC, and CSCI have collectively reduced their

combined GHG emissions by about 10.3% in 2017 to 18,422 million KG.

Figure 30: GHG emission (in million KG)

Source: Company data, HSBC

Increase pre-fabrication to enhance precision and save on building materials

The Chinese government is encouraging companies to change their method of construction

from labour intensive to prefabrication. The target is for c30% of all construction projects to use

pre-fabrication in 10 years compared with around 5% in 2017. This could reduce building

material waste and increase construction efficiency (i.e. higher precision rate and less repetitive

work done by humans).

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

CRCC CCCC CRG CSCI

2016 2017

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

CCCC CRG CSCI

2016 2017

Construction companies

have been reducing energy

consumption

Greenhouse gas emissions

are also falling

Increase pre-fabrication from

5% in 2017 to 30% in 10 years

23

EQUITIES ● INDUSTRIALS

November 2018

Pre-fabrication is commonly used in developed countries. Factories manufacture standardised

building parts, such as window frames, kitchens and toilets, on a modular basis with a high level

of precision. Rising labour cost is a key reason behind the increased use of prefabrication in

overseas markets. A similar trend in China in recent years is likely to increase the use of

prefabrication in more affluent cities. The government will focus on the Pearl River Delta,

Yangtze River Delta, and Beijing-Tianjin-Hebei Economic zone, and also cities with populations

over 3 million. The increased use of prefabrication should save construction costs through lower

wage bills and better management of building materials.

Other long-term ESG trends – smart buildings

The NDRC and Ministry of Housing and Urban Renewal and Development announced a Green

Building Action Plan in 2013 to improve the energy efficiency of existing and new buildings.

Green building initiatives could reduce the power consumption required for climate control of

buildings. Increasing wages and a decreasing payback period for the adoption of automation

and robots, especially in manufacturing, has the potential to replace humans on a major scale.

We see smart buildings with a higher technology content as a global trend and China is moving

in a similar direction.

According to Edward Perry, Michael Hagmann, and Puneet Garg in their report Building

Technology – Smart Buildings The Key to Future Growth, 2 October 2018, a wide range of

industries could benefit from smart buildings. They range from cement admixtures to high-rise

elevators, where building technology companies design and manufacture products which

enhance the performance of buildings.

Building automation: Rapid growth in the Internet of Things and cloud computing has led

to the delivery of intelligent systems at a lower cost to traditional platforms. Whilst older

systems were previously too expensive for small/medium-sized buildings, which constitute

c.90% of total building stock, new technology has made building automation an economic

reality for almost all buildings.

Schneider Electric (SU FP, Buy, EUR64.82, TP EUR88) estimates that buildings currently

represent 40% of global energy demand, and that 30% of energy used in buildings is

wasted due to inefficient management systems. Greater environmental awareness and

policy are also driving investment in smarter buildings, which – as a result of being more

energy efficient – are almost always greener buildings. Smarter buildings using less energy

are highlighted as a policy option for making cities more efficient.

Smart buildings are the

future trend in China and

globally

EQUITIES ● INDUSTRIALS

November 2018

24

Key definitions for smart buildings

Building technology: Ranging from cement adhesives to high-rise elevators, building

technology companies design and manufacture products that enhance the performance of

buildings. Within building technology, we cover the sub-segments of elevators, low-voltage

equipment, building products, engineering software, and access controls. We also cover the

system integrators, or rather those who sell entire automation systems, which include companies

with diversified portfolios such as Siemens and Schneider. Building technology companies are

typically high-margin and have relatively low capital requirements, leading to strong returns on

investment. Barriers to entry are often high, growth is solid, and pricing power is significant. For

these reasons, the segment often trades at a significant premium to the broader capital goods

sector.

Smart buildings: Smart buildings connect systems and components across areas

including access control, lighting and heating to reduce energy consumption and optimise

building performance. Smart buildings are becoming an increasingly important theme within

the sector, and a fundamental driver of top-line growth. For more detail on the development,

mechanics, and economics of smart buildings please see our sector thematic Smart

Buildings and the IoT 27 March 2018. Smart buildings and improved building energy

efficiency are a key component of smart cities, which we cover in greater depth in the

thematic report The future of cities, 19 September 2018.

25

EQUITIES ● INDUSTRIALS

November 2018

Chinese construction companies

Earnings and cash flow improvement in 2018

The RMB1.35trn project-specific bonds issued by local governments so far in FY18 will mostly

be used to speed up existing projects. Operating cash flows for construction companies will

improve in 2H18 leading to a move into positive territory for FY18 for most contractors.

However, the bulk of these repayments will experience a lag after the recent liquidity

improvement and they will likely come in 4Q18, so 3Q18 operating cash flows might remain

subdued. Faster execution of existing projects would support both economic growth and

increase asset turnover for the companies, resulting in better return ratios.

Figure 31: 1H18 results summary and forecasts

(RMBm) 1H18a 2H18e FY18e FY19e FY20e

CRCC

Rev 308,981 431,203 740,184 817,140 893,456 GP 29,956 37,418 67,374 73,725 79,519 EBIT 13,352 15,098 28,451 35,130 37,888 NPAT 8,009 10,924 18,933 23,682 25,160

y-o-y growth 22.8% 14.6% 17.9% 25.1% 6.2%

CRG

Rev 316,102 434,335 750,437 827,898 891,331 GP 31,132 41,773 72,905 80,067 86,010 EBIT 13,999 19,275 33,274 38,826 43,629 NPAT 9,552 10,081 19,633 23,301 26,287

y-o-y growth 23.9% 20.6% 22.2% 18.7% 12.8%

CCCC

Rev 207,586 306,808 514,394 556,277 605,112 GP 27,859 40,548 68,407 74,936 82,471 EBIT 15,041 20,004 35,045 38,736 43,435 NPAT 7,389 11,332 18,721 21,124 25,125

y-o-y growth 5.6% 25.5% 10.8% 12.8% 18.9%

CSCI

Rev 27,106 30,322 57,428 67,265 77,805 GP 4,105 4,262 8,367 9,725 11,242 EBIT 3,653 3,736 7,388 8,629 10,040 NPAT 2,522 3,104 5,626 6,635 7,831

y-o-y growth 20.6% 5.1% 11.5% 17.9% 18.0%

Source: Company data, HSBC estimates

Outlook for companies

Better project execution should help earnings in 2018, while new

contract growth should improve in 2019

Upstream demand to hold up for construction machinery and building

materials; emission upgrade will also help machinery sales

Plan to increase railway freight will benefit rail equipment demand

more than an increase in investment over the next 12 months

Operating cash flows for

construction companies will

improve in 2H18

EQUITIES ● INDUSTRIALS

November 2018

26

Potential upside for new contract growth in 2019

We think the current policy to increase infrastructure investment is different from the stimulus we

saw back in 2008-10 or 2014-15. New projects are still proceeding in an orderly fashion. The

requirement to complete survey and design, project approval, and financing arrangement

means we may only start to see a positive impact on new contract flows in 1H19. Following the

review of the PPP project database and likely further refinements in PPP regulations, all major

contractors have slowed down the intake of new PPP projects during 2018. Most prefer to focus

on traditional engineering-procurement-construction contracts instead of PPP or investment

projects.

We also think the de-leveraging process for local governments is likely to continue and central

government is likely to increase project funding directly for infrastructure development.

Figure 32: New contract summary table

(RMBm) Sep-18 FY18e FY19e FY20e

CRCC 891,657 1,603,182 1,630,883 1,655,115 y-o-y growth 5.3% 6.3% 1.7% 1.5%

CRG 951,300 1,629,868 1,631,056 1,635,901 y-o-y growth 5.9% 4.7% 0.1% 0.3%

CCCC 154,038 856,591 834,673 847,322 y-o-y growth -16.9% -4.8% -2.6% 1.5%

CSCI* 90,430 120,782 121,053 120,678 y-o-y growth 11.6% 17.1% 0.2% -0.3%

Source: Company data, HSBC estimates

Capital goods – demand to hold up in 2019

Strong infrastructure should offset property construction slow down: The property

construction market has been quite good during 2018. New starts and the land area purchased

by developers both grew 16% y-t-d to September. However, the best leading indicator is

property transaction volumes, which showed a 3% decline in September and property prices

appear to have weakened during 2H18. We think the property construction activity outlook in

2019 could face downward pressure. The pick-up in infrastructure investment should be able to

offset any weakness in property construction activity.

Chinese excavator usage hours remained stable during 2018 at above 130 hours per month.

This is in line with the last 5-year average of c.132 hours, according to the Komtrax data

provided by Komatsu (6301 JP, not rated). In theory, usage hours above 110 hours per month

should result in new demand for excavators or an expansion of the installed base, assuming no

change in the number of idle machines among the installed base.

27

EQUITIES ● INDUSTRIALS

November 2018

Figure 33: Chinese excavator usage hours remains steady during 2018

Source: Komatsu company filings

Industry OEM expectation by product

Excavator and wheel loader

The normal seasonal pattern – 1H sales being stronger than 2H sales – should continue in

2018. While China’s domestic unit sales growth in 2019 might be slower than the growth in

2018 for a wide array of construction equipment, companies generally expect to enjoy better

profitability than industry volume growth. This should be attained by a combination of price hikes

to offset cost pressures, market share gains in the global market, and operating cost

management through automation and mechanisation.

Manufacturers are more cautious in terms of industry growth outlook for excavators as 2018

total sales volume is likely to surpass the previous peak. This coincides with our minor reduction

to our sales volume forecast for 2019e by 1.2% y-o-y.

Figure 34: HSBC forecast for China’s construction machinery industry sales

2017 Sep-18 2018e 2019e 2020e

Wheel loaders 97,610 91,028 122,060 155,384 161,610 y-o-y growth 47.3% 24.2% 25.0% 27.3% 4.0%

Excavator 140,063 156,242 192,336 190,085 148,395 y-o-y growth 99.2% 53.6% 37.3% -1.2% -21.9%

Source: China Construction Machinery Association, HSBC estimates

We remain positive on the growth outlook for wheel loaders. We estimate 25% y-o-y growth in

industry unit sales in FY18e and 27% growth in FY19e. We think wheel loader sales are likely to

recover to the theoretical replacement demand in China (c.150,000 units per annum) in FY19e.

Chinese construction machinery manufacturers remain disciplined with their production capacity

as well as inventory management. This was a major issue during the down-cycle between 2012

and 2016. We see no plans by major manufacturers to expand capacity at the moment.

Product sales and credit terms remain prudent with limited financial leasing activity. The

customer base (mostly equipment leasing companies and machinery operators) has seen an

improvement in financial capability after consolidation during the industry downturn.

Concrete machinery

Concrete machinery demand recovery lagged the excavator and wheel loader recovery and

only started around mid-2017. Concrete pump sales volume remains at c.20-30% of peak level

in 2012 (c.11,000 units). Major players are optimistic about the demand rebound, driven by

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18

China Komtrax equipment usage (Hours / month) Average (since Jan 2013)

EQUITIES ● INDUSTRIALS

November 2018

28

replacement demand and emission standards upgrade. However, it is more likely to reach

around 70% of the peak level due to the historical over-supply situation.

Truck crane

Truck crane and crawler crane enjoyed strong sales rebound in 2017 and 2018. The sales

volume has returned to around 80% of the previous peak level and industry players expect

sales growth to slow in 2019, instead of seeing 50-100% sales volume growth during 2018.

Figure 35: ROE vs. PB for 2018e chart for China capital goods and construction companies

Note: Bubble sizes represents the ROE of the company. Source: HSBC estimates

Positive outlook for rail equipment demand

CRRC Corp (1766 HK)

Upcoming strong rail freight will drive equipment demand: CRCC is optimistic about the

policy to shift more transport from road to rail. It is not only China Railway Corporation’s or

CRC’s (private, not rated) target to increase freight volume by 30% over the next three years but

also part of the national strategy for a modern transportation upgrade over the long term. CRRC

Qiqihar is focusing on new product R&D including: (1) heavy loading for commodity goods and

(2) fast delivery and non-commodity transportation – e.g. cold-chain, container, and car

transportation. The commodity goods shift from road to rail will be key over the next three years

due to environmental concerns.

In the future, modern integrated transportation, including high speed rail delivery, rail+truck and

rail+ship models, should drive rail freight efficiency improvements. These models will also aid

non-commodity transport volume growth, although the process will be gradual as it takes time

for equipment upgrades and investment in network facilities. CRCC management believes the

next 3-5 years will be the golden period for rail freight and expects wagon (and locomotive)

tenders to hit a historical high.

No price cut on standard MU: CRCC reiterated that there is no price cut on standard MU

(multiple units, high speed passenger train) 350km/h unit due to an agreement with CRC last

year. If there is a price cut, CRRC will transfer the price pressure to component providers,

including external and internal providers. According to CRC, the MU demand in 2018-20 should

be 900 sets at least – 500 sets are 350km/h and 400 sets 250km/h. As CRC has tendered 372

sets of 350km/h MU in 2018, the upcoming tender may see more 250km/h sets. CRCC still

thinks there is potential demand for more than 900 MUs over the coming years and high-grade

MU maintenance demand may help revenue from the high-speed or MU business remain

stable.

Zoomlion

Zhuzhou CRRC

CRRC Corp

Lonking

Weichai PowerCSCI

CRCC

CCCC

CRG

Sinotruk

China Yuchai0.00

0.50

1.00

1.50

2.00

2.50

3.00

0 2 4 6 8 10 12 14 16 18 20 22 24

Chinese industrials PB/ROE chart

ROE(%)

P/B (x)

29

EQUITIES ● INDUSTRIALS

November 2018

Zhuzhou CRRC (3898 HK)

At the 2Q18 post-results briefing in August 2018, company management was cautiously

optimistic that new orders for locomotives would improve over the coming months as the

government encourages the shift of commodity transport from the highway to the railway in the

coming years.

Figure 35: Zhuzhou CRRC FY18e revenue breakdown

Source: HSBC estimates

Valuation and Risks

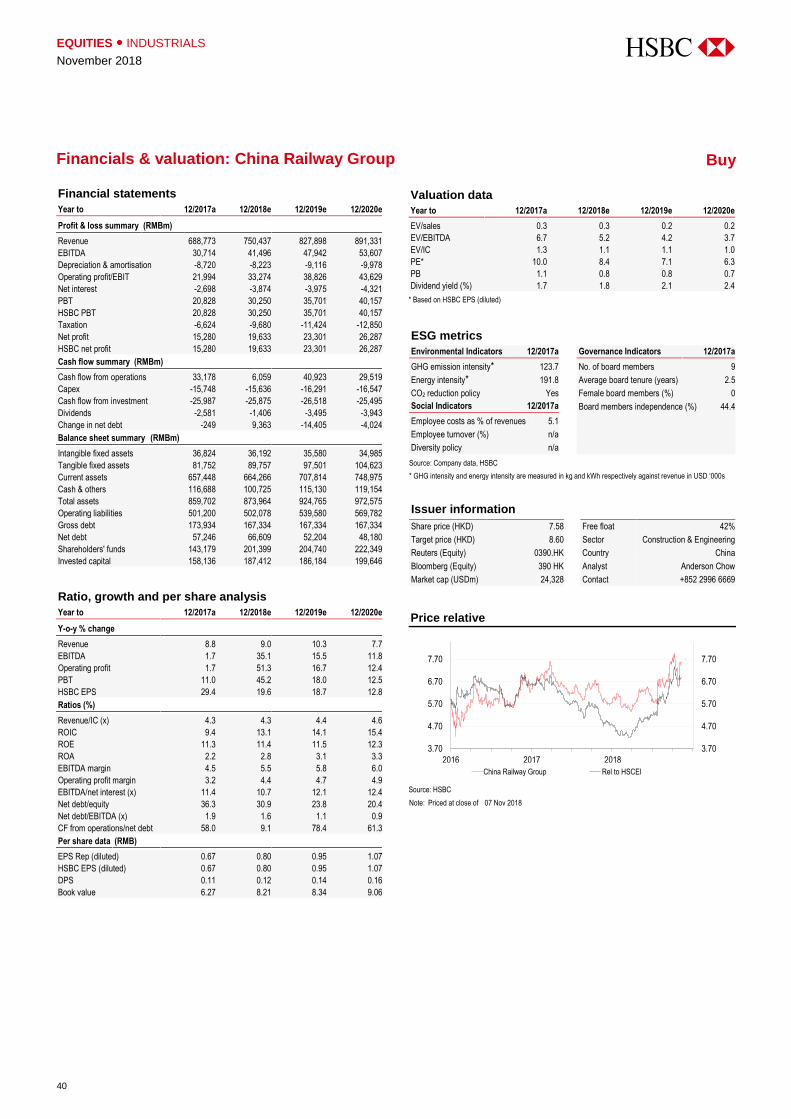

CRCC H-shares (1186 HK, HKD10.46, Buy, TP HKD14.90)

We value the stock using a PE method using the following formula:

Target PE = ROE - g/ROE * (Cost of Equity - g)

Where: FY18e ROE is 12.3%, g is 0%, and cost of equity is 10.5%. Our risk free rate is 3.0%

and equity risk premium is 5.0%, in line with our HSBC global strategy recommendations. Our

Equity Beta is 1.5 as we think CRCC’s business could remain volatile based on the policy

directives of China’s central government.

We derive a target PE of 9.5x, which we apply to our FY18e EPS estimate of RMB1.39

(unchanged) and use a 4Q18 RMB-HKD exchange rate of 1.12 to derive our target price of

HKD14.90. The H-share has traded at an average forward PE 10.7x since listing, which

continues to be at a premium to our fair value target multiple of 9.5x. We think the company

offers a healthy earnings growth outlook at 18% in 2018e and 17% CAGR from 2017-20e with a

dividend yield of c4%. Our H-share TP of HKD14.90 implies 42.4% upside from current levels;

accordingly, we rate the stock Buy.

Key downside risks: Potential slower-than-expected construction project progress; potential

lower-than-expected PPP project returns; volatility in profit margins; and overseas construction

project risks.

CRCC A-shares (601186 CH, RMB11.03, Buy, TP RMB13.30)

We value CRCC’s A-shares at the same target PE multiple of 9.5x as the H-shares as

described above. Applying this target multiple to our FY18e EPS forecast of RMB1.39 per

share, we derive a fair value target price of RMB13.30. Our A-share TP of RMB13.30 implies

20.6% upside from current levels. We maintain our Buy rating on the stock because the

18%

23%

17%4%

20%

18%

Locomotive

EMU

Metro

Safety

Maintenance

Eletrical component

EQUITIES ● INDUSTRIALS

November 2018

30

company is likely to continue to benefit from the pro-investment policy stance taken by the

government.

Key downside risks: Potential slower-than-expected construction project progress; potential

lower-than-expected PPP project returns; volatility in profit margins; and overseas construction

project risks.

CRG H-shares (390 HK, HKD7.58, Buy, TP HKD8.60)

We value the stock using a PE method using the following formula:

Target PE = ROE - g/ROE * (Cost of Equity - g)

Where: FY18e ROE is 11.4%, g is 0%, and cost of equity is 9.5%. Our risk-free rate is 3.0% and

equity risk premium is 5.0%, in line with our HSBC global strategy recommendations. Our equity

beta is 1.5 as we think CRG’s business could remain volatile based on the policy directives of

China’s central government.

We derive a target PE of 9.5x, which we apply to our FY18e EPS estimate of RMB0.80

(unchanged) and use an end-2018 RMB-HKD exchange rate forecast of 1.12 to derive our

target price of HKD8.60. Our fair value target multiple of 9.5x is in line with the average forward

PE of 9.7x at which the H-share has traded since listing. We think the company offers a healthy

earnings growth outlook at 19% in 2018e and a 17% EPS CAGR for 2017-20e with a dividend

yield of c2%.

Our H-share TP of HKD8.60 implies 13.5% upside from current levels. We maintain our Buy

rating on the stock as the company is likely to continue to benefit from the pro-investment policy

stance taken by the government.

Key downside risks: Slower-than-expected construction progress; a potential lower-than-

expected return from PPP projects; worsening property market conditions; and overseas project

risks.

CRG A-shares (601390 CH, RMB7.52, Hold, TP RMB7.60)

We value CRG’s A-shares at the same fair value target PE multiple of 9.5x as we do for its H-

shares. Applying this target multiple to our FY18e EPS forecast of RMB0.80, we derive a fair

value TP of RMB7.60. Our TP implies upside of 1.1%. We maintain our Hold rating on the A-

shares as we believe the company is likely to continue to benefit from the pro-investment policy

stance taken by the government.

Key upside risks: A potential increase in government funding to boost infrastructure

investment and a reduction in financial leverage through better management of operations.

Key downside risks: Slower-than-expected construction progress; a potential lower-than-

expected return from PPP projects; worsening property market conditions; and overseas project

risks.

CSCI (3311 HK, HKD5.67, Buy, TP HKD9.70)

We value the stock using a PE method using the following formula:

Target PE = ROE - g/ROE * (Cost of Equity - g)

Where: FY18e ROE is 13.7%, g is 0%, and cost of equity is 9.5%. Our risk free rate to 3.0% and

Equity risk premium is 5.0% based on HSBC Global strategist. Our Equity Beta is high at 1.7 as

we think CSCI’s business could remain volatile based on the policy directives of China’s central

government.

We derive a target PE of 8.7x. This is lower than the company’s long-term PE trading multiple of

9.8x.

31

EQUITIES ● INDUSTRIALS

November 2018

We apply our target multiple of 8.7x to our revised FY18e EPS estimate of HKD1.11 and derive

our target price of HKD9.70. Our target price implies 71.1% upside from current levels;

accordingly, we maintain our Buy rating on the stock.

CCCC H-shares (1800 HK, HKD7.56, Buy, TP HKD9.10)

We forecast 2018 new contract growth to be -4.8%. We think the company might continue to

trade in a PE range reflective of a down-cycle environment. During the last down-cycle in 2013,

the H-shares traded in a range of 5-8.3x one-year forward PE. We set our target 2018e PE at

7x, which is at the middle of the range (vs. 8.3x previously, which was at the upper end of the

range); 7x is also the average forward PE of the H-shares since 2011 and during 2013.

Using our FY18 EPS forecast of RMB1.16, we calculate our H-share fair value target price at

HKD9.10 based on HSBC FX team’s end-2018 RMB-HKD exchange rate forecast of 1.12. Our

target price implies 20.4% upside from current levels; accordingly, we rate CCCC H-shares Buy.

Downside risks: Higher-than-expected financial leverage, potential overseas acquisitions of

construction business and projects, project execution risk of overseas infrastructure projects,

potential operation risk for infrastructure operating assets.

CCCC A-shares (601800 CH, RMB12.43, Reduce, TP RMB8.10)

We value CCCC’s A-shares at the same target 2018e PE multiple of 7.0x as the H-shares as

described above. Applying this target multiple to our FY18e EPS forecast of RMB1.12 per

share, we derive a fair value target price of RMB8.10. Our target price implies 34.8% downside

from current levels. We maintain our Reduce rating on the A-shares as they are trading at a

c.80% premium to the H-shares.

Key upside risks: Faster-than-expected asset restructuring to strengthen the balance sheet

and potential A-share equity private placement; positive policy announcement on infrastructure

project funding; and potential new financing source or partners to develop the company’s BOT

portfolio in China.

CRRC (1766 HK, HKD7.16, Buy, TP HKD8.80) / (601766 CH, RMB8.62, Hold, TP RMB7.80)

We value CRRC Corp using a discounted cash flow model. We assume a WACC of 8.95%

based on our key assumptions of a risk-free rate of 3.0%, equity risk premium of 5.0%, long-

term target debt/(debt + equity) of 10%, equity beta of 1.27, and a terminal growth rate of 0.5%.

Our DCF-based fair value target price for the A-share is RMB7.80, which implies 9.5%

downside from current levels. We maintain our Hold rating on the A-share as the A-share trades

at a significant valuation premium to the H-share.

Our H-share target price of HKD8.80 implies 22.9% upside from current levels; hence, we

maintain our Buy rating on the stock.

Our TP of HKD8.80 implies a FY18e PE of 18.6x, which is slightly higher than the company’s

long-term trading PE of 17.1x since the listing of its H-shares in 2008. We think this slight

premium is justified as the restructuring initiatives at the company should yield benefits over the

long term.

We maintain our Hold rating on the A-share as it is trading at c.35% premium to the H-share

price, which looks stretched to us.

Key upside risks for A-shares: Stronger-than-expected new orders for China Railway

Corporation; rapid transit vehicle demand remaining high due to the restart of subway project

tenders; and higher profitability improvement from internal restructuring.

Key downside risks for A- and H-shares: Worse-than-expected cost control for production