Embed Size (px)

Citation preview

RETAIL CLINIC SERVICES

Tacara 2008

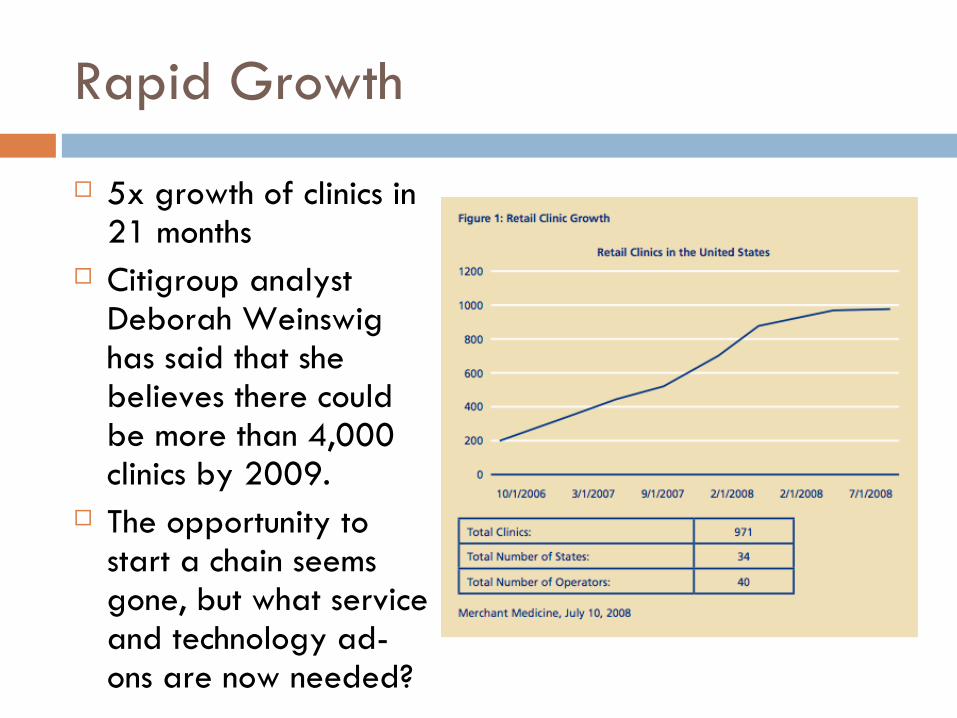

Rapid Growth

5x growth of clinics in 21 months

Citigroup analyst Deborah Weinswig has said that she believes there could be more than 4,000 clinics by 2009.

The opportunity to start a chain seems gone, but what service and technology ad-ons are now needed?

Clinic Operators Acquired by Big Boys

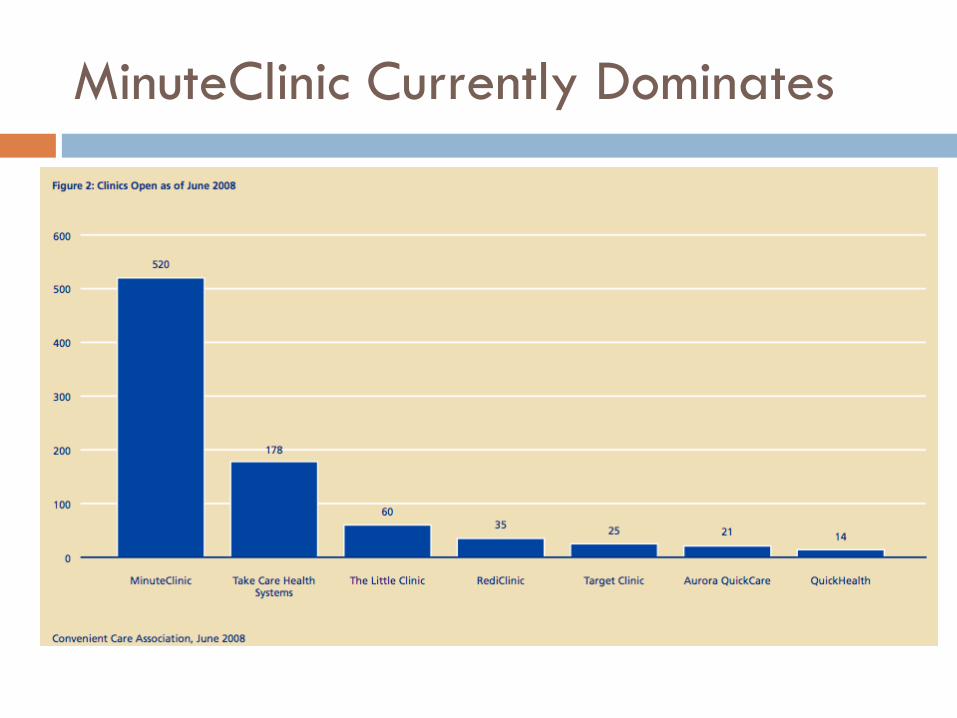

In July 2006, CVS/Caremark acquired MinuteClinic and its 83 clinics. As of June 2008, MinuteClinic had 512 to 520 clinics,1 and the company’s long-term

forecasts are calling for 2,500. Walgreen acquired Take Care Health Systems in May 2007, and doubled

operations in the fourth quarter of the same year: From October to December, Take Care grew from 60 clinics to 130; it had 178 total clinics as of June 2008 and has plans to open in excess of 200 additional clinics in 2008.2

The growth of retail clinics illustrates how important it is for clinic operators to establish alliances with a retail “host”. Synergies & foot traffic are big benefits of these acquisitions.

Wal-Mart has partnered with RediClinic. Overall, the retail clinic market is beginning to show signs of maturity, with the

largest operator slowing growth and smaller operators exiting the market. MinuteClinic has lowered growth expectations for 2008: It now expects to open only 100 new clinics in 2008 instead of its previously forecasted 200.

A number of smaller operators have exited the market as well, including the earlier-noted SmartCare Health Clinics as well as Corner Care Clinic and Checkups USA.

MinuteClinic Currently Dominates

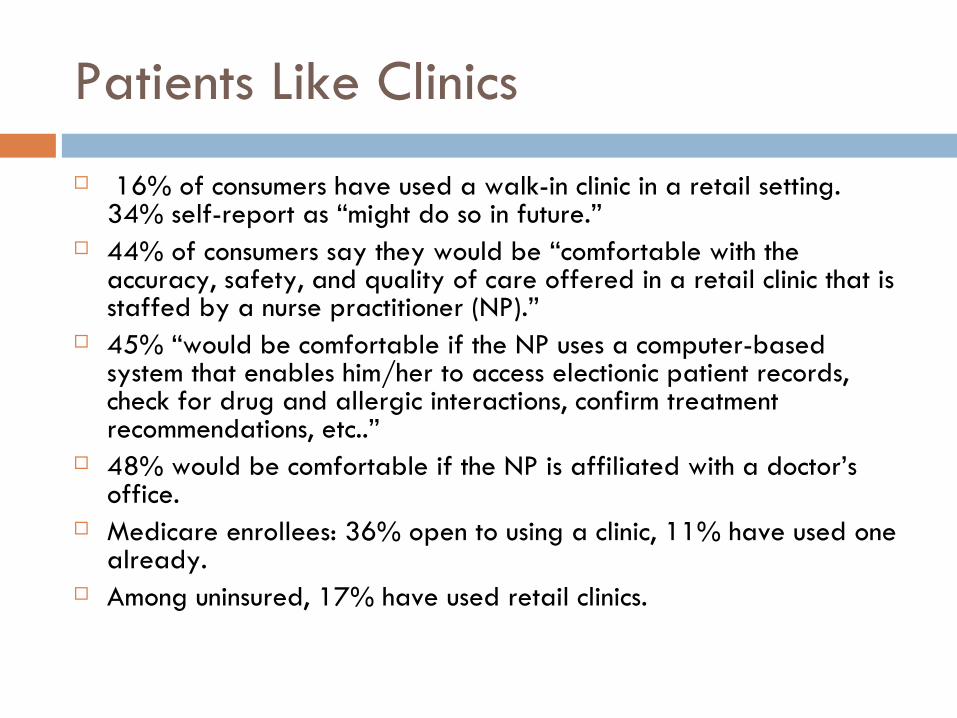

Patients Like Clinics

16% of consumers have used a walk-in clinic in a retail setting. 34% self-report as “might do so in future.”

44% of consumers say they would be “comfortable with the accuracy, safety, and quality of care offered in a retail clinic that is staffed by a nurse practitioner (NP).”

45% “would be comfortable if the NP uses a computer-based system that enables him/her to access electionic patient records, check for drug and allergic interactions, confirm treatment recommendations, etc..”

48% would be comfortable if the NP is affiliated with a doctor’s office.

Medicare enrollees: 36% open to using a clinic, 11% have used one already.

Among uninsured, 17% have used retail clinics.

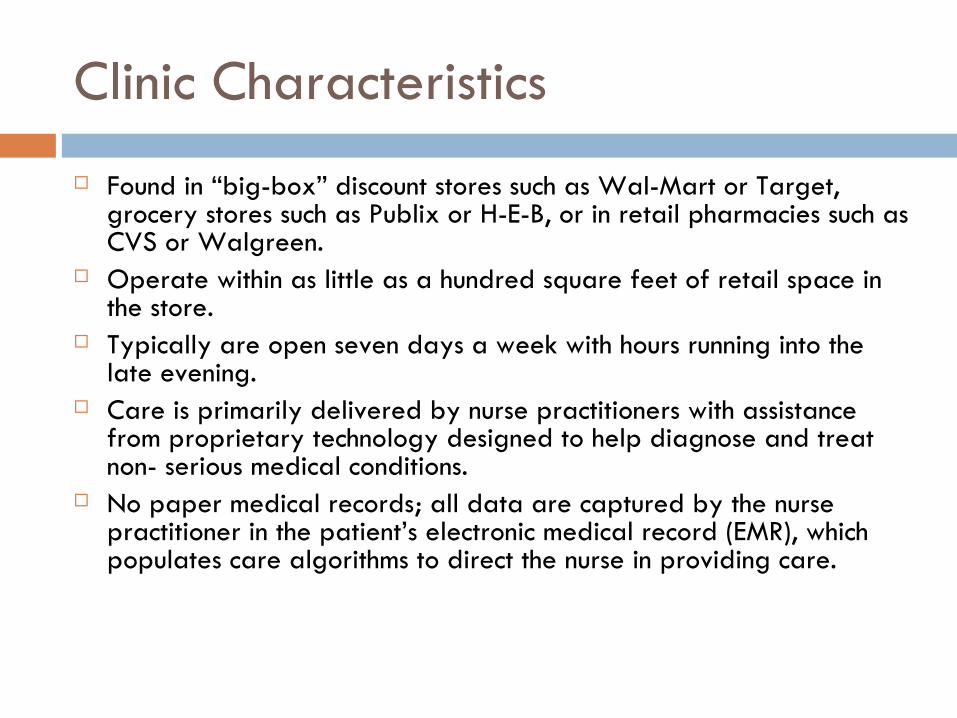

Clinic Characteristics

Found in “big-box” discount stores such as Wal-Mart or Target, grocery stores such as Publix or H-E-B, or in retail pharmacies such as CVS or Walgreen.

Operate within as little as a hundred square feet of retail space in the store.

Typically are open seven days a week with hours running into the late evening.

Care is primarily delivered by nurse practitioners with assistance from proprietary technology designed to help diagnose and treat non- serious medical conditions.

No paper medical records; all data are captured by the nurse practitioner in the patient’s electronic medical record (EMR), which populates care algorithms to direct the nurse in providing care.

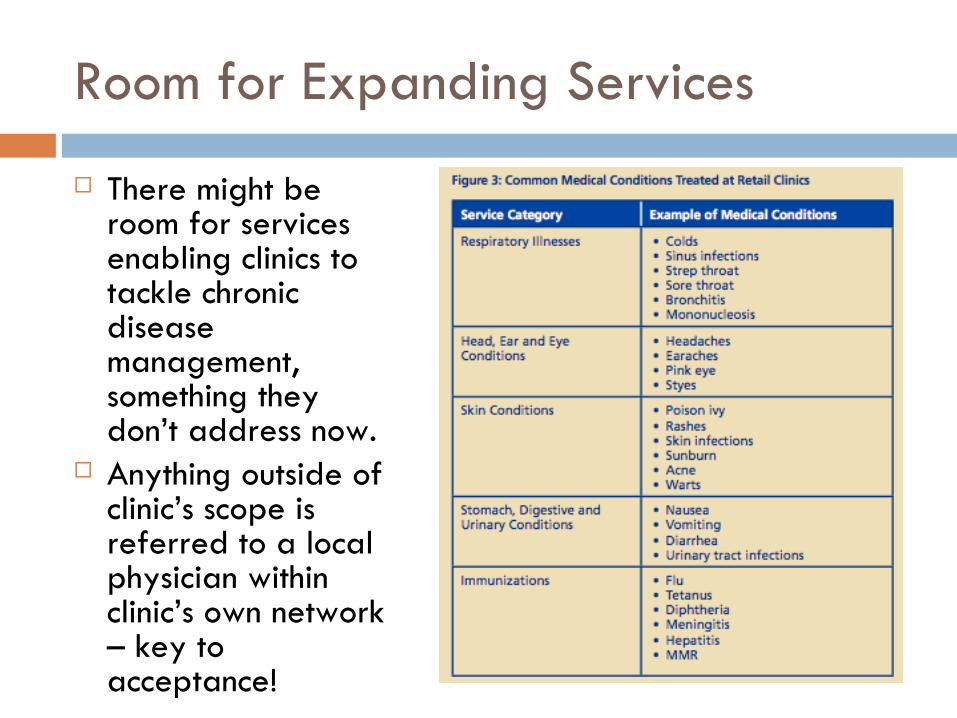

Room for Expanding Services

There might be room for services enabling clinics to tackle chronic disease management, something they don’t address now.

Anything outside of clinic’s scope is referred to a local physician within clinic’s own network – key to acceptance!

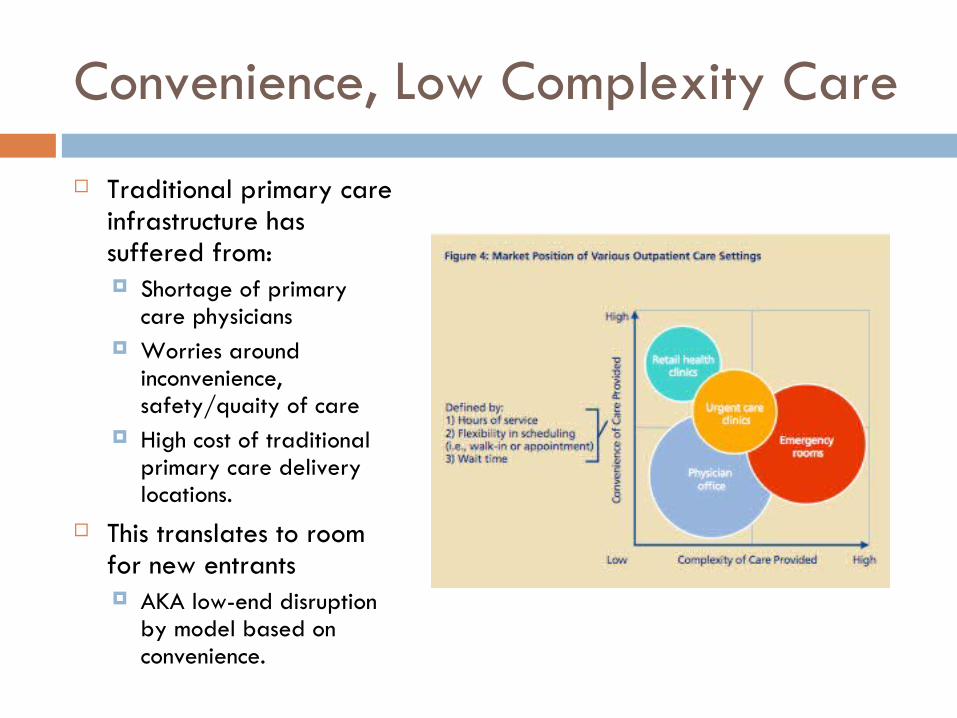

Convenience, Low Complexity Care

Traditional primary care infrastructure has suffered from: Shortage of primary

care physicians Worries around

inconvenience, safety/quaity of care

High cost of traditional primary care delivery locations.

This translates to room for new entrants AKA low-end disruption

by model based on convenience.

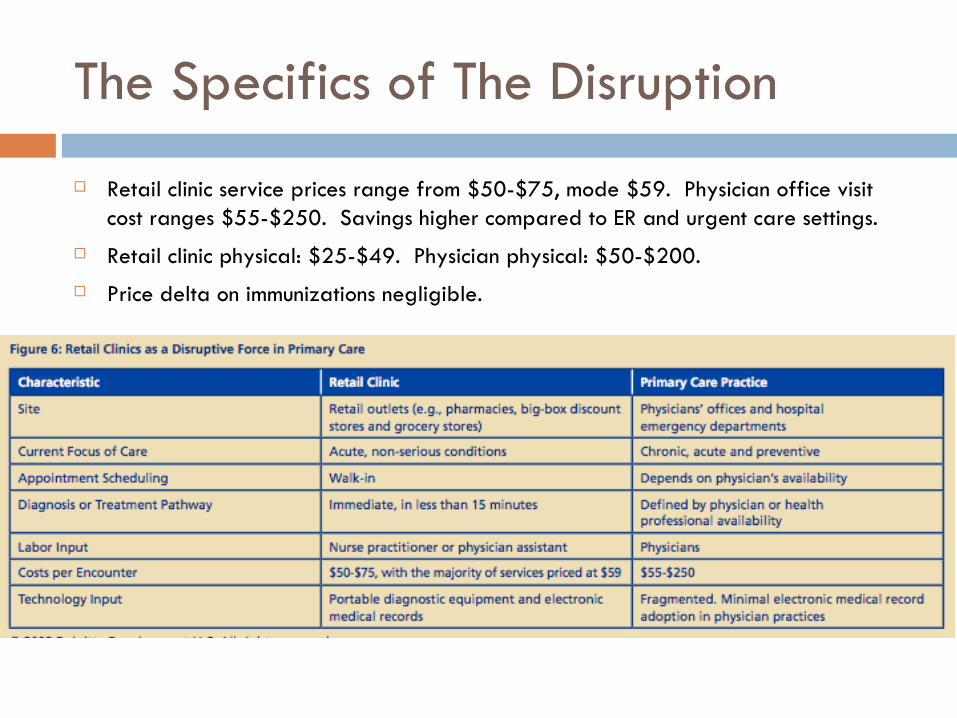

The Specifics of The Disruption

Retail clinic service prices range from $50-$75, mode $59. Physician office visit cost ranges $55-$250. Savings higher compared to ER and urgent care settings.

Retail clinic physical: $25-$49. Physician physical: $50-$200.

Price delta on immunizations negligible.

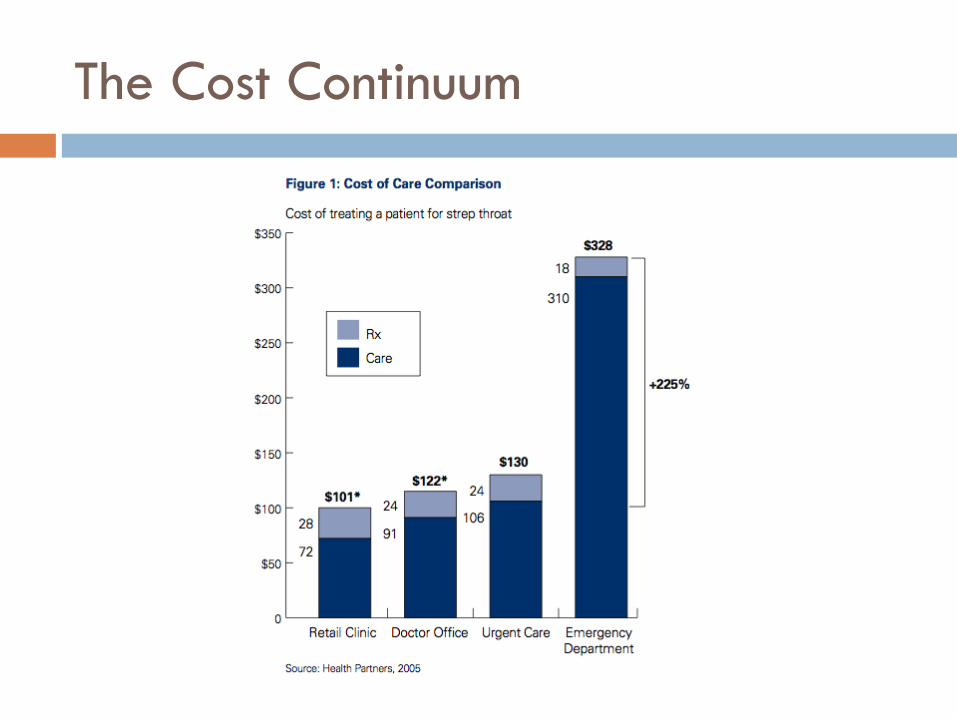

The Cost Continuum

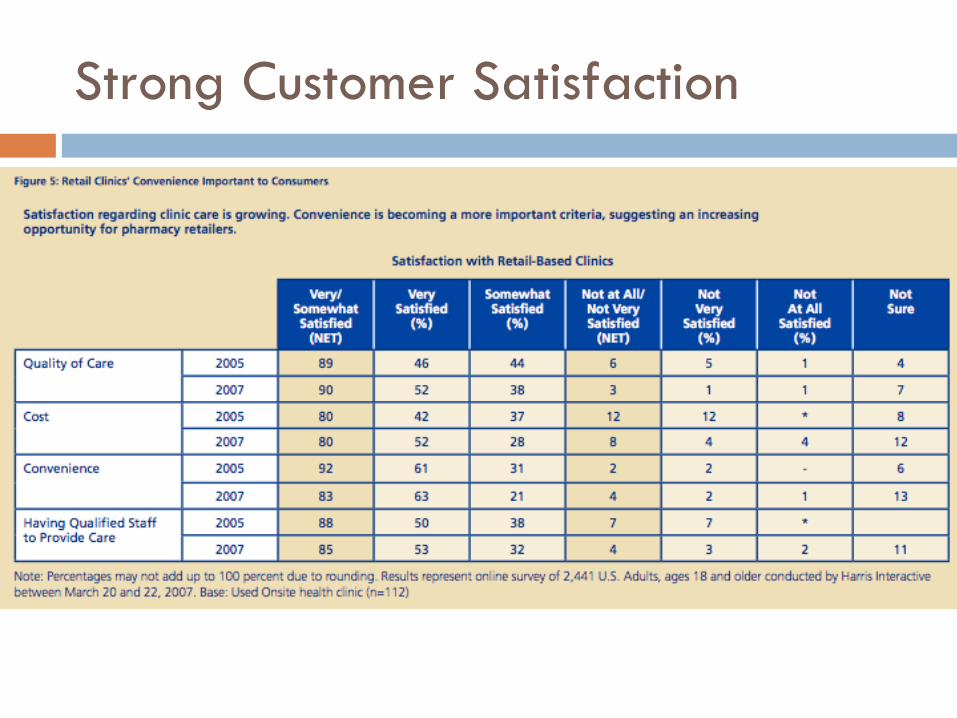

Strong Customer Satisfaction

Growth by Expanding Services

Current clinic service options limited Expansion into chronic and preventive care could

greatly expand market potential. Expanded offerings into these areas must be routine

care (that is, care that follows standard pathways) that RN’s can offer directly and cost-effectively

Confirming data points Effectiveness of chronic disease management dependent on

number and frequency of patient touch points Some health plans already using customer service reps to

manage chronic disease patients.

Synergies for Big Boys

MinuteClinic and Take Care are owned by pharmacy/pharma benefit management corporations (CVS and Walgreen’s)

Clinics could be used by parent corporations to drive pharmaceutical purchasing.

Or, parent companies could bundle care and pharma services and sell them to insurance companies or employers, disintermediating physicians. Purchasers would see lower expenses for care, clinic owners

would get steady volume with high prescription-drug attachment rates.

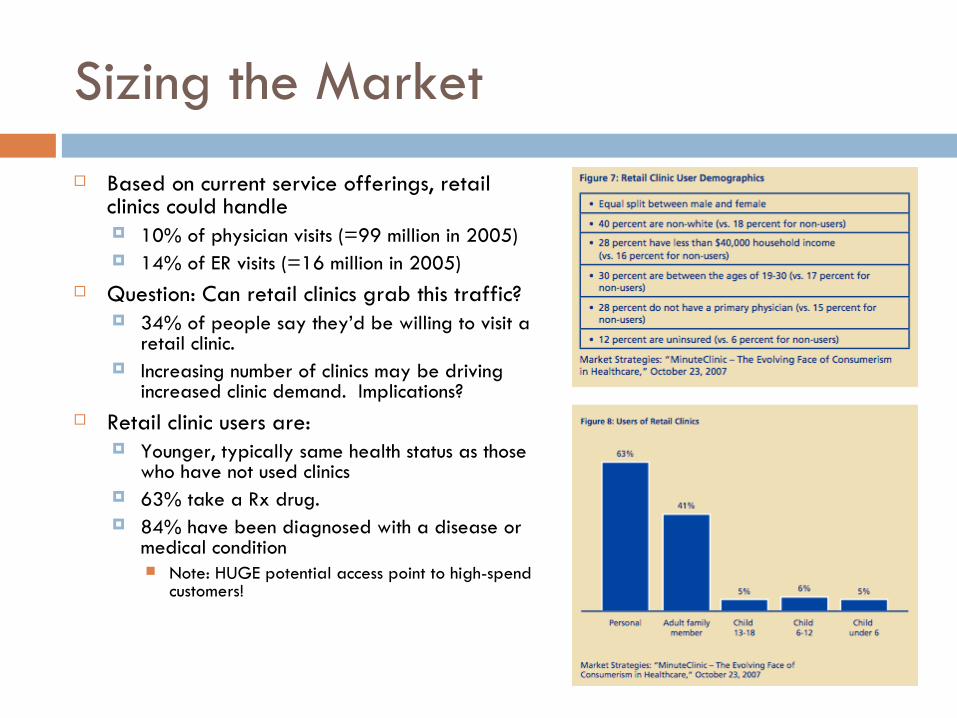

Sizing the Market

Based on current service offerings, retail clinics could handle 10% of physician visits (=99 million in 2005) 14% of ER visits (=16 million in 2005)

Question: Can retail clinics grab this traffic? 34% of people say they’d be willing to visit a

retail clinic. Increasing number of clinics may be driving

increased clinic demand. Implications? Retail clinic users are:

Younger, typically same health status as those who have not used clinics

63% take a Rx drug. 84% have been diagnosed with a disease or

medical condition Note: HUGE potential access point to high-spend

customers!

Non-Market Concerns: Opposition but Favorable Trends Overall AMA and state affiliates lobbying to increase regulation of retail clinics despite no

evidence of sub-par quality or problems In Massachusetts, clinic openings were delayed by an initial application rejection,

reform of the application process, and multiple hearings. Eventually, the Commonwealth allowed the opening of limited-service clinics but opposition still remains from the City of Boston itself.

In Georgia, increased supervision is required for clinic nurses writing prescriptions. In Florida, primary care physicians are barred from supervising more than five physician-staffed offices.

But, the FTC has found that strict limitations on supervision could be considered anti-competitive. FTC issued also comment on other aspects of regulation, including limitations on retail clinic advertising, differential cost-sharing, and co-location of retail clinics inside stores which sell alcohol and tobacco, factors which may influence quality of care. The FTC commented that strict limitation in these aspects could be considered anti-competitive, as well “The FTC’s comments are a significant win for the retail clinic industry and a blow to the AMA and its state-level affiliates.”

Insurance Outlook Favorable

All of the major clinic operators are now accepting insurance from the majority of large carriers, including UnitedHealthcare, Aetna, CIGNA, Humana and Medicare. Also have negotiated contracts with large regional carriers.

Early 2007 Harris poll showed that only 54 percent of insured individuals who visited a retail clinic had some or all of their costs covered by insurance, but that percentage is likely to increase as more partnerships are publicized.

Use of retail clinics also is likely to rise as consumers become more aware of reimbursement policies which require only small co-payments to visit the clinics.

Some insurers, such as Blue Cross Blue Shield of Minnesota, are waiving co-payments altogether to further drive demand because of cost savings.

AMA has lobbied to outlaw the practice of differential cost-sharing between retail clinics and traditional primary care settings, citing quality and conflict-of-interest concerns as the primary reasons. BUT the FTC’s opinion is that limiting an insurer’s ability to utilize differential cost- sharing could be considered anti-competitive.

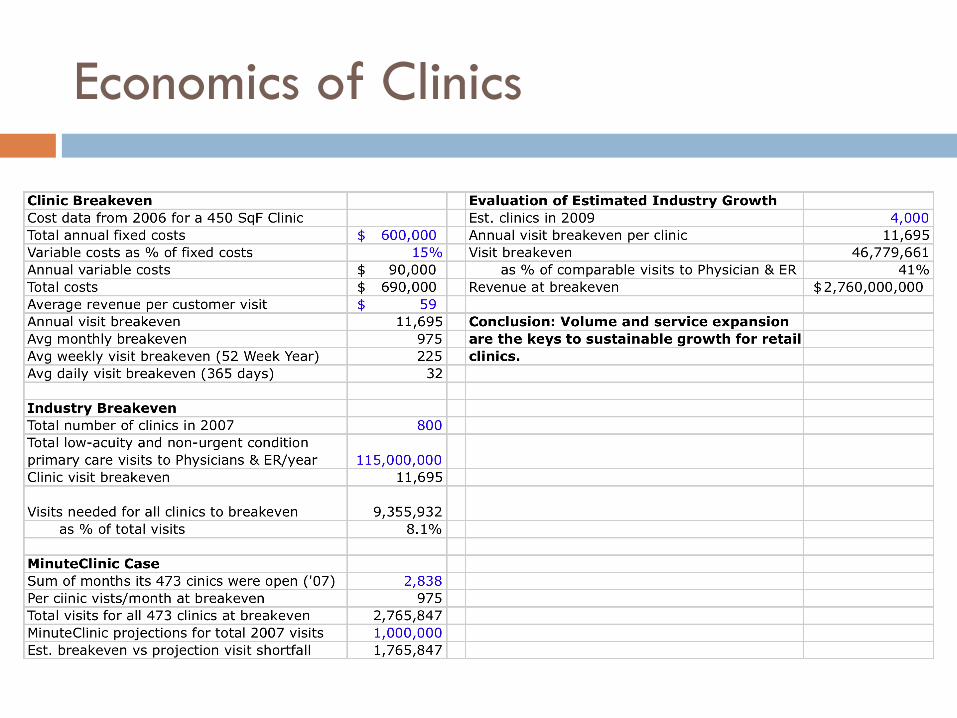

Economics of Clinics

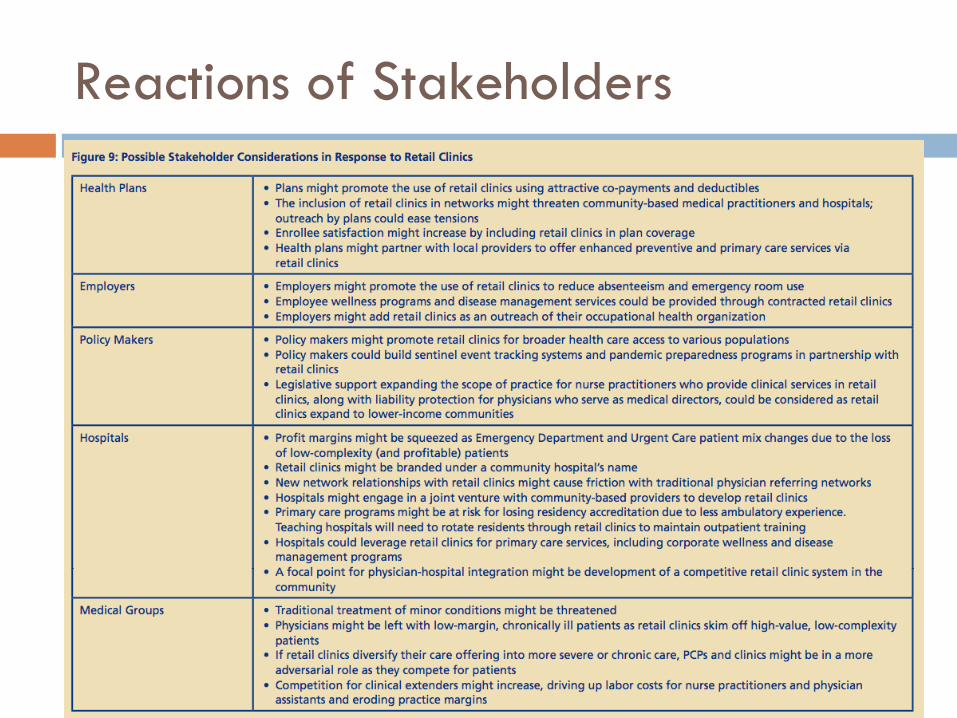

Reactions of Stakeholders