Embed Size (px)

Citation preview

1| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

FOUNDATION IN NATURAL AND BUILT ENVIRONMENT

BASIC ACCOUNTING ACC 30205

ASSINGMENT 1 FINANCIAL REPORT

GROUP MEMBERS:

1. Yong Sing Yew 0318766

2. Kong Zhen Chung 0319528

3. Welson Lum Wei Jiunn 0319514

COMPANY: Nike’s Company

LECTURER: Mr. Chang Jau Ho

SUBMISSION DATE: 16 January 2015

2| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

TABLE CONTENTS

1.

HISTORY AND BACKGROUND

3

2.

RECENT DEVELOPMENT OF NIKE COMPANY

4

3.

PROFITABILITY RATIOS

5 - 6

4.

STABILITY RATIOS

7 - 8

5.

PRICE / EARNING RATIOS

9

6.

INVESTMENT RECOMMENDATION

10

7.

APPENDIX

11 - 15

8.

REFERENCES

16

3| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

History & Background of Nike

Nike is the world leader in athletic shoes. The company rose quickly from small-time sales at

track meets to a major publicly-traded Fortune 500 company. Throughout its history and

background, Nike has utilized strong advertising campaigns to separate itself from its

competition. Two of the most memorable marketing campaigns, "Just Do It" and the Air Jordan

brand, cemented Nike as one of the most popular shoe brands in the world.

Nike began its history as Blue Ribbon Sports in 1964 at the University of Oregon. Track star

Philip Knight and his coach Bill Bowerman distributed Japanese Onitsuka Tiger shoes at track

meets. The first retail location for the company opened in 1966 in Santa Monica, California. As

the relationship between Blue Ribbon Sports and Onitsuka Tiger ended in 1971, the company

launched its own line known simply as "Nike."

Nike successfully garnered 50 percent of the market share within the United States by 1980, the

same year the company went public. The advertising firm in charge of Nike, Wieden+Kennedy,

coined one of the most famous phrases in marketing history in 1988. The "Just Do It" was named

one of the top five slogans of all time by a 1999 article in "Advertising Age."

In 1984, Nike's sales were in decline. In response, the company hired rookie basketball player

Michael Jordan to be the company spokesman. The $2.5 million deal for five years resulted in

the creation of one of the most popular lines of shoes ever made.

4| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

RECENT DEVELOPMENT OF NIKE

Nike’s company has been 51 years since 1964 as a Blue Ribbons Sports. It already

expanding its franchise around the world. After Nike entering the International market, it starting

to sell different sports equipment likes soccer, basketball, running, golf, combat sports, tennis,

baseball, cycling, volleyball, auto racing, aquatic activities and recreational uses. Currently,

Nike’s company has 756 retail stores throughout the entire world. Nike also pay top athletes

which from different sports to use their products as a way to promote their equipment’s

technology and design. The example of top athletes that sponsor by Nike are Cristiano Ronaldo,

Wayne Rooney and Neymar who professional in soccer and Michael Jordan, Kobe Bryant and

Lebron James who professional in basketball. The most interesting part about Nike is it has run a

program which is NikeID. NikeID is a service provided to allow the customers to personalize or

design their own Nike merchandise. Nike + also one of the Nike’s successful business product.

Nike + is an activity tracker device that attached to the Nike’s shoes that can communicates with

the Nike +sport band, iPod and iPhone. The purpose of Nike + is help to identify the time of

workout, the distance traveled, calories burned and heartbeat rate.

5| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

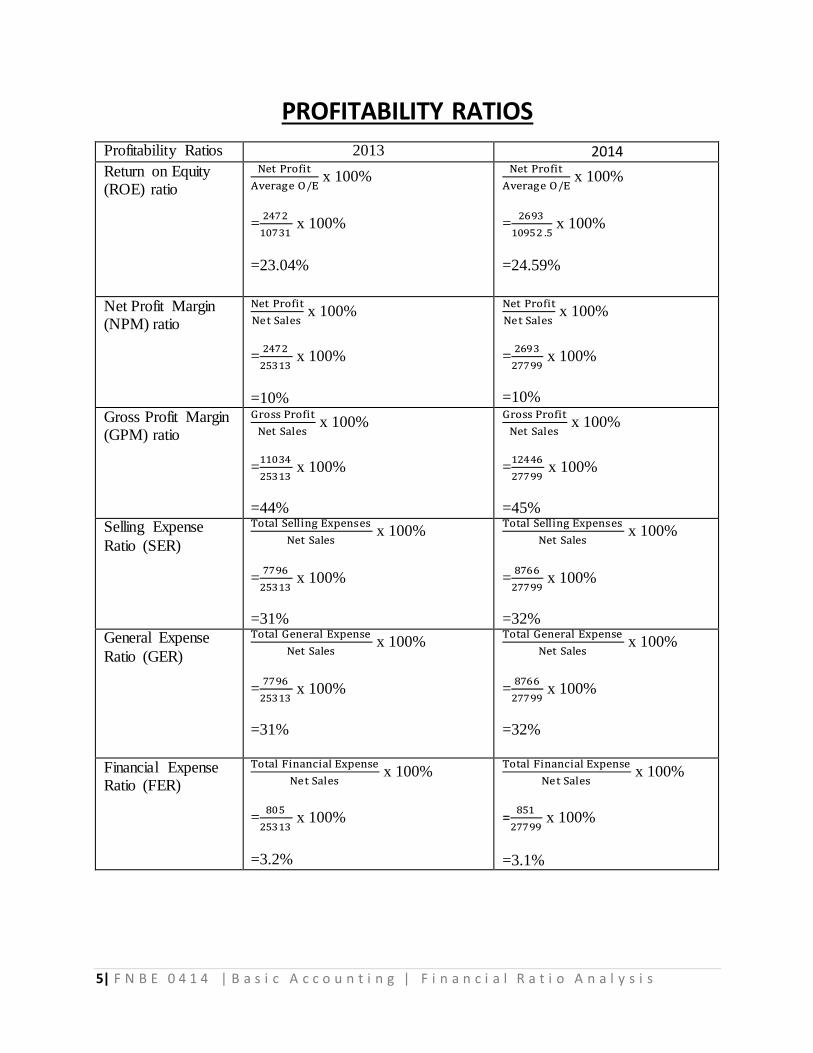

PROFITABILITY RATIOS

Profitability Ratios 2013 2014

Return on Equity (ROE) ratio

Net Profit

Average O/E x 100%

=2472

10731 x 100%

=23.04%

Net Profit

Average O/E x 100%

=2693

10952 .5 x 100%

=24.59%

Net Profit Margin (NPM) ratio

Net Profit

Net Sales x 100%

=2472

25313 x 100%

=10%

Net Profit

Net Sales x 100%

=2693

27799 x 100%

=10%

Gross Profit Margin (GPM) ratio

Gross Profit

Net Sales x 100%

=11034

25313 x 100%

=44%

Gross Profit

Net Sales x 100%

=12446

27799 x 100%

=45%

Selling Expense

Ratio (SER)

Total Selling Expenses

Net Sales x 100%

=7796

25313 x 100%

=31%

Total Selling Expenses

Net Sales x 100%

=8766

27799 x 100%

=32%

General Expense

Ratio (GER)

Total General Expense

Net Sales x 100%

=7796

25313 x 100%

=31%

Total General Expense

Net Sales x 100%

=8766

27799 x 100%

=32%

Financial Expense Ratio (FER)

Total Financial Expense

Net Sales x 100%

=805

25313 x 100%

=3.2%

Total Financial Expense

Net Sales x 100%

=851

27799 x 100%

=3.1%

6| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

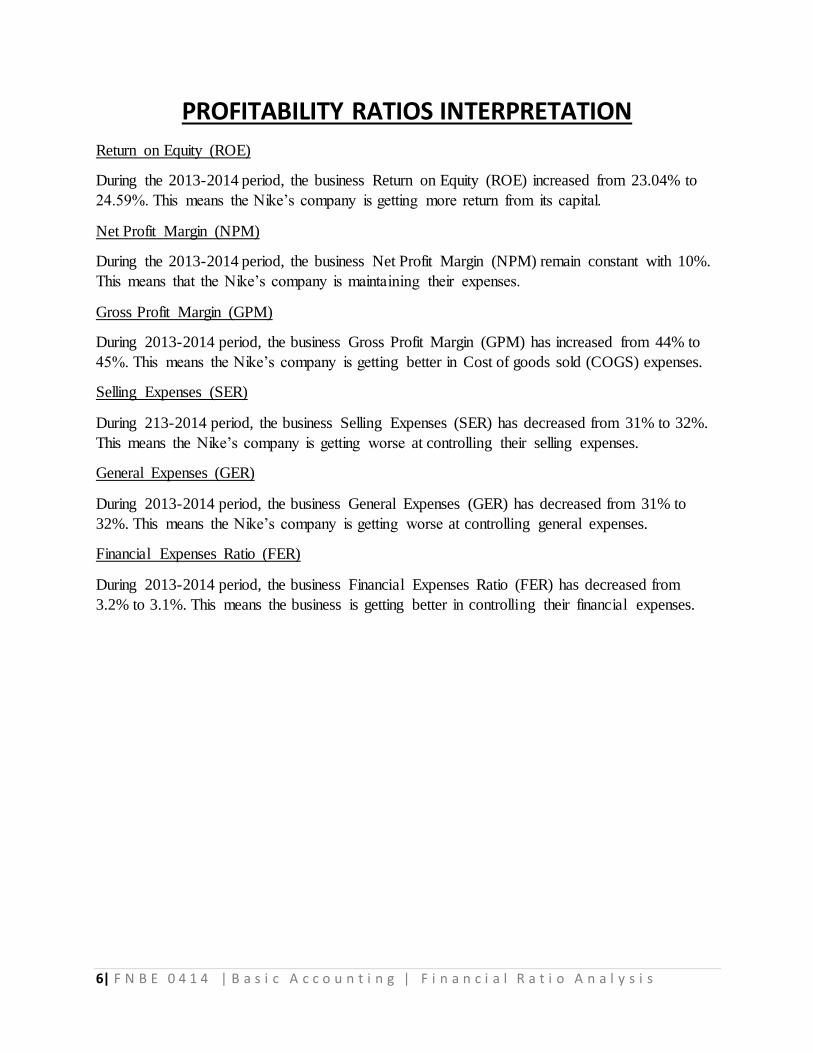

PROFITABILITY RATIOS INTERPRETATION

Return on Equity (ROE)

During the 2013-2014 period, the business Return on Equity (ROE) increased from 23.04% to

24.59%. This means the Nike’s company is getting more return from its capital.

Net Profit Margin (NPM)

During the 2013-2014 period, the business Net Profit Margin (NPM) remain constant with 10%.

This means that the Nike’s company is maintaining their expenses.

Gross Profit Margin (GPM)

During 2013-2014 period, the business Gross Profit Margin (GPM) has increased from 44% to

45%. This means the Nike’s company is getting better in Cost of goods sold (COGS) expenses.

Selling Expenses (SER)

During 213-2014 period, the business Selling Expenses (SER) has decreased from 31% to 32%.

This means the Nike’s company is getting worse at controlling their selling expenses.

General Expenses (GER)

During 2013-2014 period, the business General Expenses (GER) has decreased from 31% to

32%. This means the Nike’s company is getting worse at controlling general expenses.

Financial Expenses Ratio (FER)

During 2013-2014 period, the business Financial Expenses Ratio (FER) has decreased from

3.2% to 3.1%. This means the business is getting better in controlling their financial expenses.

7| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

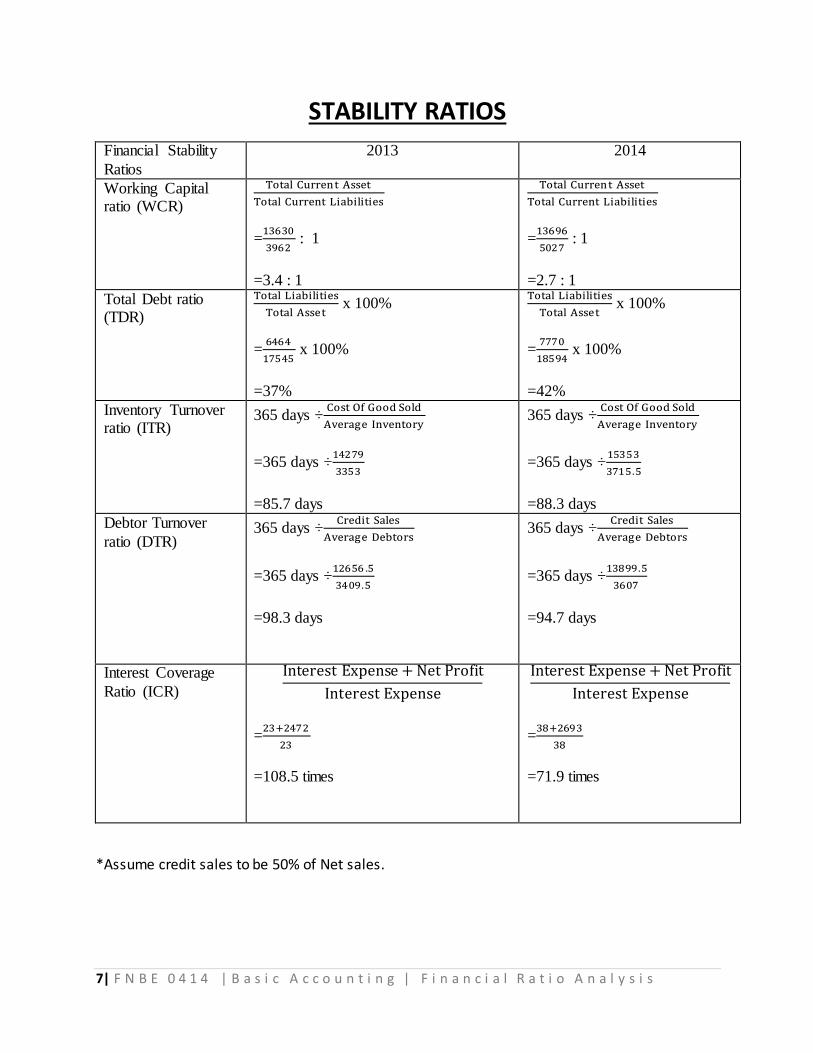

STABILITY RATIOS

Financial Stability

Ratios

2013 2014

Working Capital ratio (WCR)

Total Current Asset

Total Current Liabilities

=13630

3962 : 1

=3.4 : 1

Total Current Asset

Total Current Liabilities

=13696

5027 : 1

=2.7 : 1

Total Debt ratio (TDR)

Total Liabilities

Total Asset x 100%

=6464

17545 x 100%

=37%

Total Liabilities

Total Asset x 100%

=7770

18594 x 100%

=42%

Inventory Turnover ratio (ITR)

365 days ÷Cost Of Good Sold

Average Inventory

=365 days ÷14279

3353

=85.7 days

365 days ÷Cost Of Good Sold

Average Inventory

=365 days ÷15353

3715.5

=88.3 days

Debtor Turnover

ratio (DTR) 365 days ÷

Credit Sales

Average Debtors

=365 days ÷12656 .5

3409.5

=98.3 days

365 days ÷Credit Sales

Average Debtors

=365 days ÷13899.5

3607

=94.7 days

Interest Coverage

Ratio (ICR)

Interest Expense + Net Profit

Interest Expense

=23+2472

23

=108.5 times

Interest Expense + Net Profit

Interest Expense

=38+2693

38

=71.9 times

*Assume credit sales to be 50% of Net sales.

8| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

FINANCIAL STABILIT RATIOS INTERPRETATION

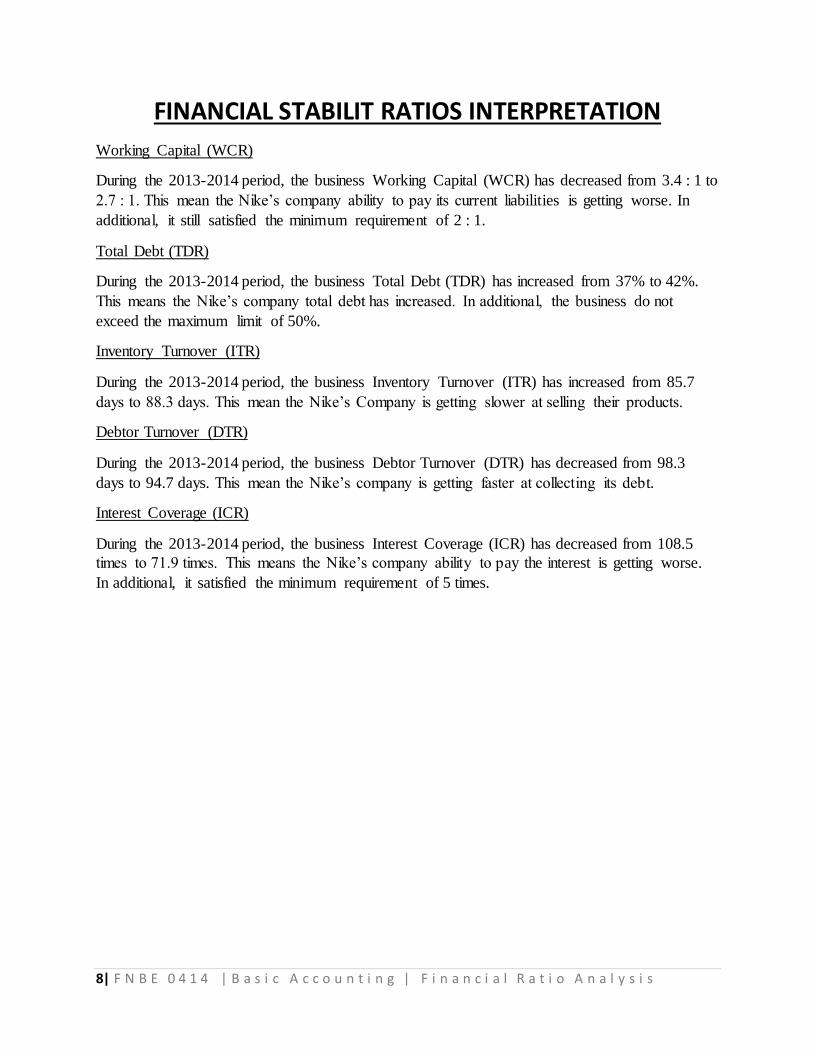

Working Capital (WCR)

During the 2013-2014 period, the business Working Capital (WCR) has decreased from 3.4 : 1 to

2.7 : 1. This mean the Nike’s company ability to pay its current liabilities is getting worse. In

additional, it still satisfied the minimum requirement of 2 : 1.

Total Debt (TDR)

During the 2013-2014 period, the business Total Debt (TDR) has increased from 37% to 42%.

This means the Nike’s company total debt has increased. In additional, the business do not

exceed the maximum limit of 50%.

Inventory Turnover (ITR)

During the 2013-2014 period, the business Inventory Turnover (ITR) has increased from 85.7

days to 88.3 days. This mean the Nike’s Company is getting slower at selling their products.

Debtor Turnover (DTR)

During the 2013-2014 period, the business Debtor Turnover (DTR) has decreased from 98.3

days to 94.7 days. This mean the Nike’s company is getting faster at collecting its debt.

Interest Coverage (ICR)

During the 2013-2014 period, the business Interest Coverage (ICR) has decreased from 108.5

times to 71.9 times. This means the Nike’s company ability to pay the interest is getting worse.

In additional, it satisfied the minimum requirement of 5 times.

9| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

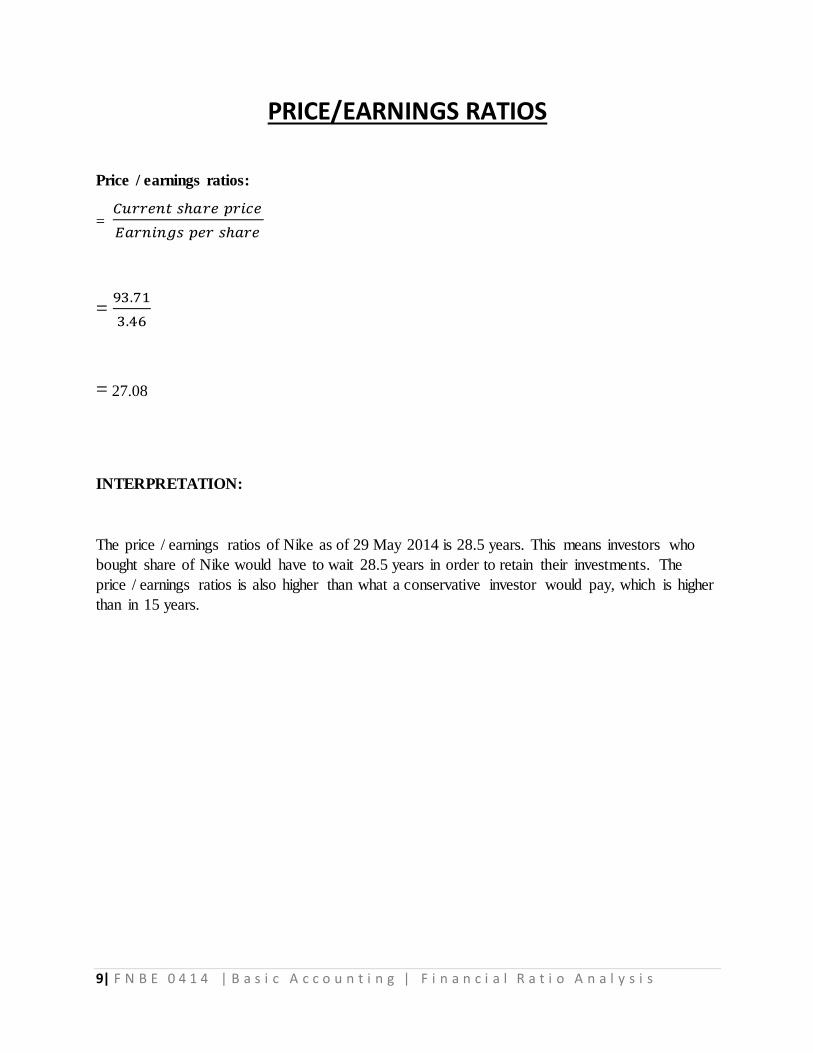

PRICE/EARNINGS RATIOS

Price / earnings ratios:

= 𝐶𝑢𝑟𝑟𝑒𝑛𝑡 𝑠ℎ𝑎𝑟𝑒 𝑝𝑟𝑖𝑐𝑒

𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠 𝑝𝑒𝑟 𝑠ℎ𝑎𝑟𝑒

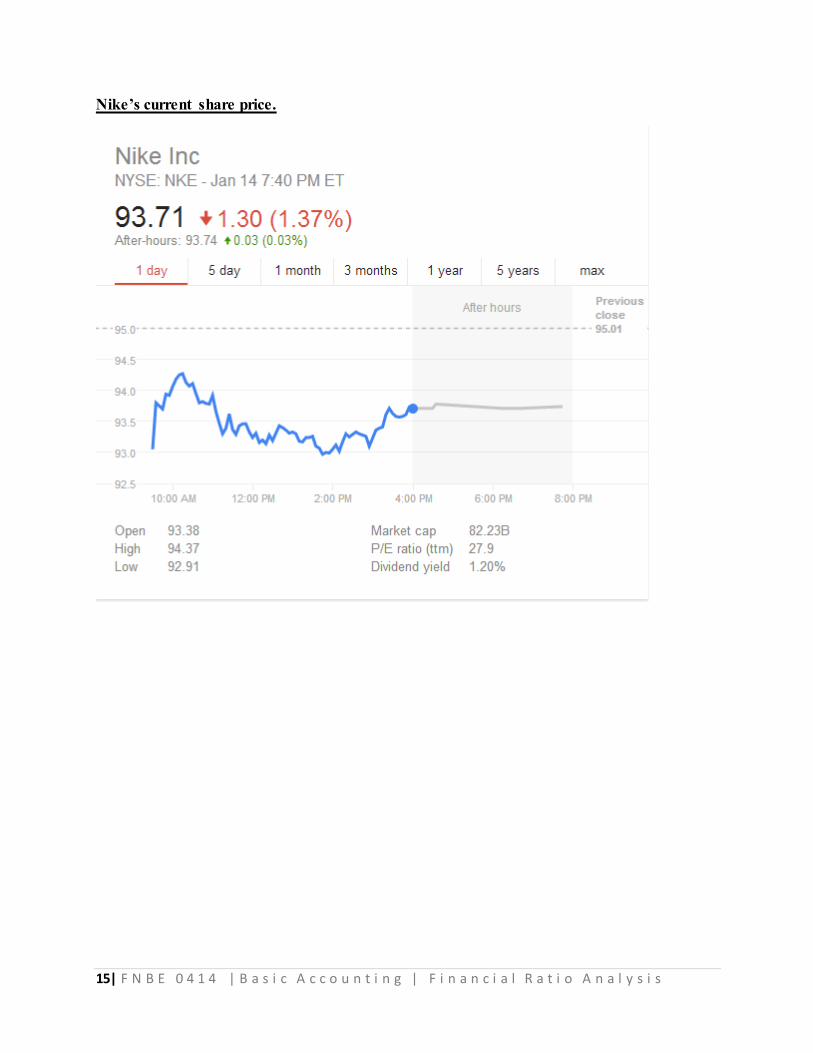

= 93.71

3.46

= 27.08

INTERPRETATION:

The price / earnings ratios of Nike as of 29 May 2014 is 28.5 years. This means investors who

bought share of Nike would have to wait 28.5 years in order to retain their investments. The

price / earnings ratios is also higher than what a conservative investor would pay, which is higher

than in 15 years.

10| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

INVESTMENT RECOMMENDATION

For our recommendation through the analysis, NIKE would not be a company worth to

invest on.

From the profitability ratio, the return of equity has increased 23.04% to 24.59% which

mean they are getting more return from its capital. NIKE’s Gross Profit Margin also showed that

the company is getting better in Cost of Goods Sold. Other than that, NIKE Company’s Selling

Expenses Ratio and General Expenses Ratio showed that the company was getting worst at

controlling it. For Net Profit Margin, it’s showed that NIKE Company was maintaining their

expenses.

As for stability ratio, the working capital of NIKE Company has decreased its mean the

ability for them to pay current liabilities is getting worst, but it’s still satisfied the minimum

requirement of 2:1. For Total Debt, although it’s has increased but it still does not exceed the

maximum limit of 50%. In additional, NIKE Company are getting slower at selling their

products as shown in the Inventory Turnover. The NIKE Company also getting faster at

collecting its debt as shown in the Debtor Turnover. Last, the NIKE Company’s Interest

Coverage has decreased. This mean the ability of them to pay the interest is getting worst and it

satisfied the minimum requirement of 5 times.

The price per earning of NIKE is higher than what a conservative investor would pay

which is higher than 15 years. The investor can only get their investment back after 27.08 years.

As a conclusion, even though NIKE’s net profit is getting better and they are earning

more. But the Price/Earnings ratio make us think that NIKE would not be a company worth

investing on if you wanted to earn money quickly.

11| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

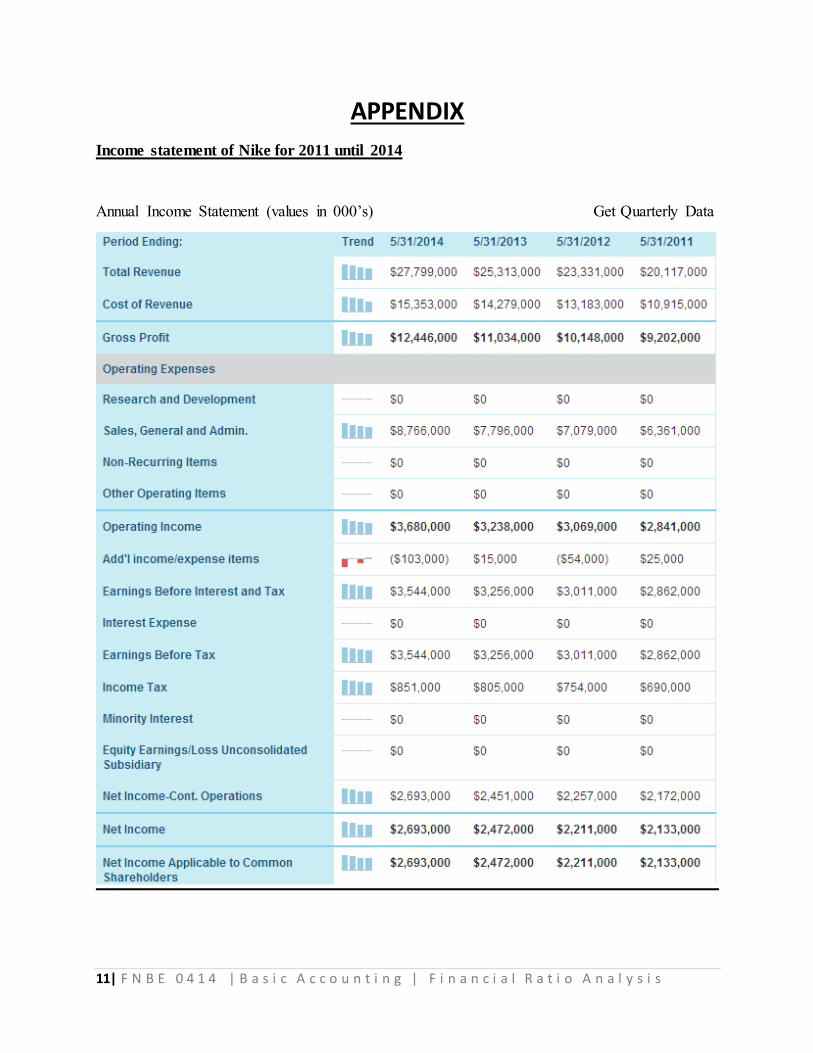

APPENDIX

Income statement of Nike for 2011 until 2014

Annual Income Statement (values in 000’s) Get Quarterly Data

12| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

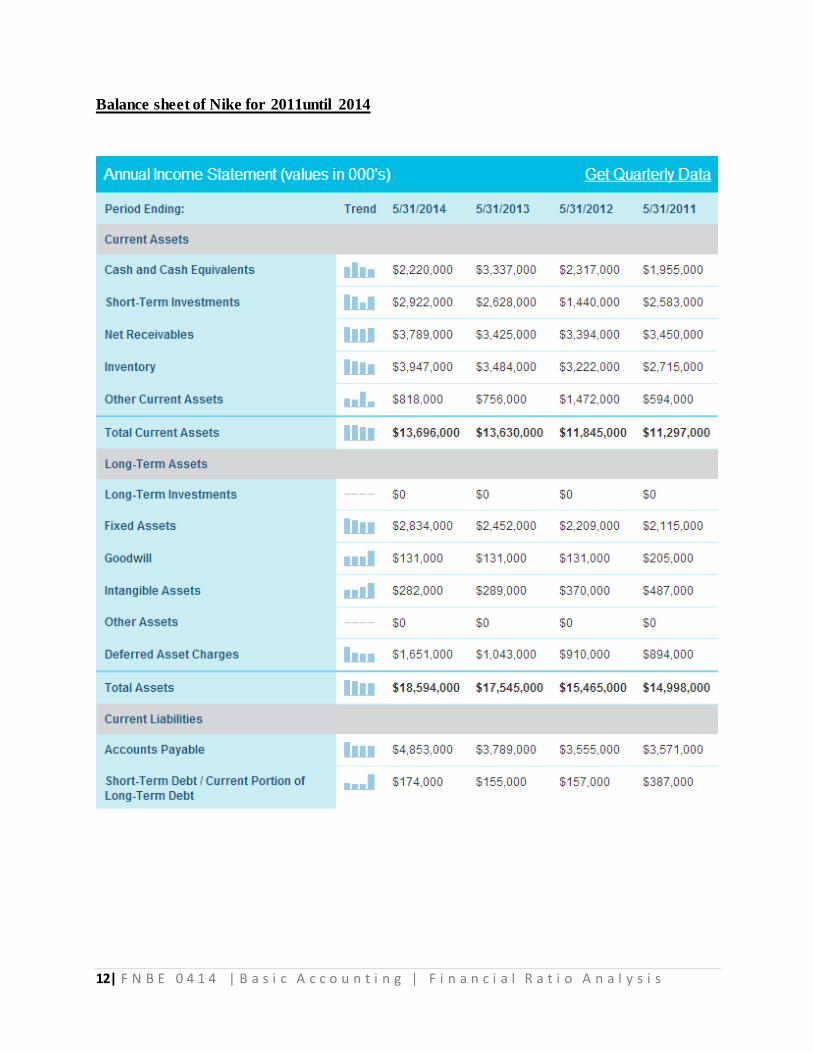

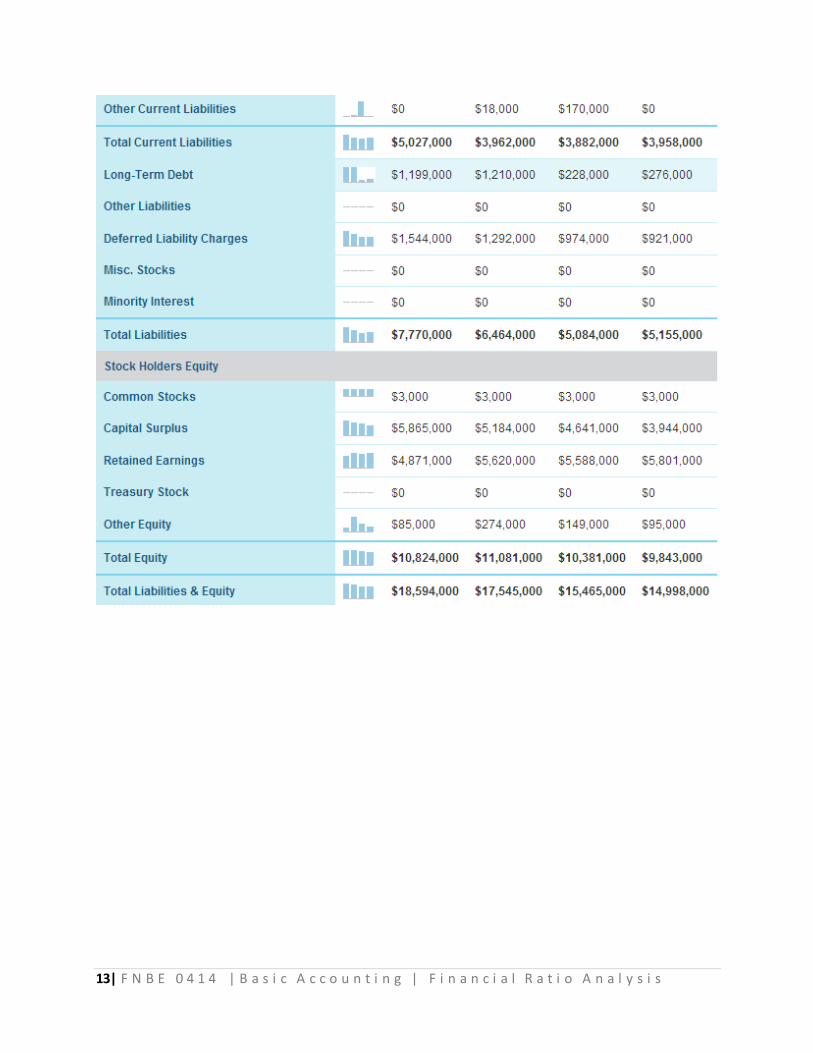

Balance sheet of Nike for 2011until 2014

13| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

14| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

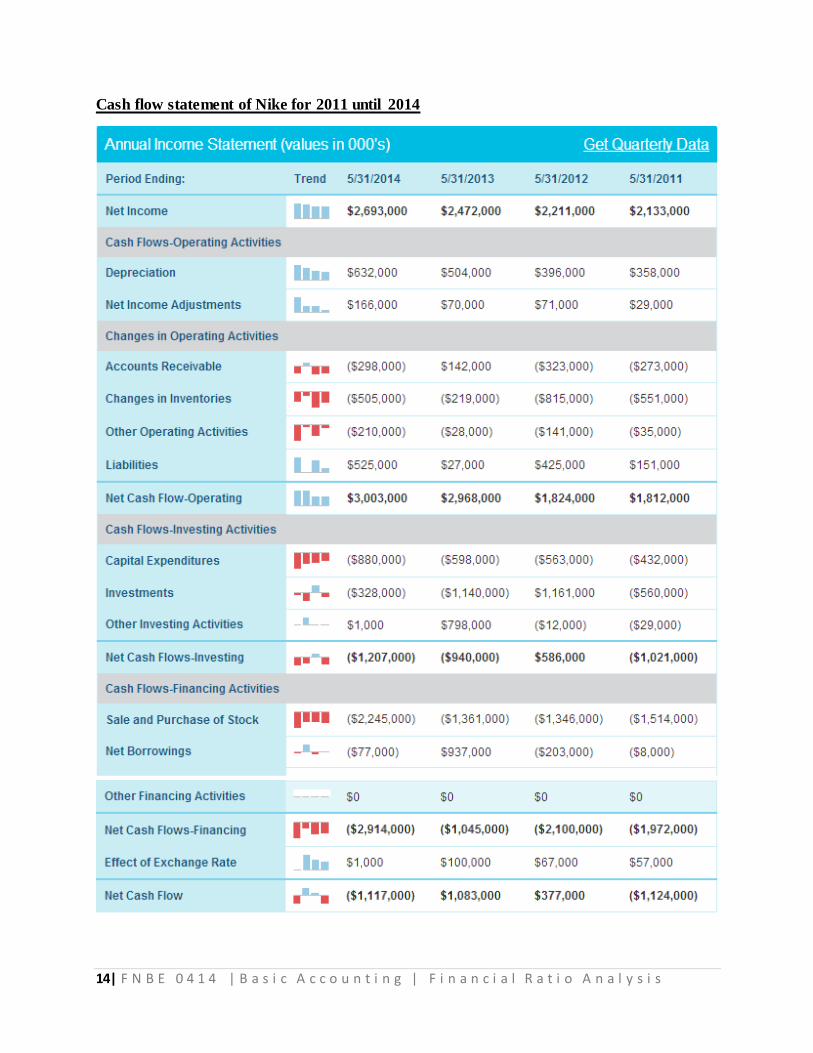

Cash flow statement of Nike for 2011 until 2014

15| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

Nike’s current share price.

16| F N B E 0 4 1 4 | B a s i c A c c o u n t i n g | F i n a n c i a l R a t i o A n a l y s i s

REFERENCES

1. NKE Company Financials. (2015, January 14). Retrieved from

http://www.nasdaq.com/symbol/nke/financials?query=ratios

2. Nike, Inc. (NKE). (2015, January 14). Retrieved from

https://finance.yahoo.com/q/is?s=NKE Income Statement&annual

3. Wiley, J. (2000) Accounting Standard: Statements of Financial Accounting Concepts.

N.Y.

4. Jones, M. (2006) Financial Accounting. Chichester, England.

5. Walter, T.H. & Charles, T.H. (2001) Financial Accounting. Upper Saddle River, N.J.