Embed Size (px)

Citation preview

CONNECTED TIMES UA

RESULTS 2014

CONTENTS 1. Today’s connected consumer

2. Digital market overview

3. Trends

4. Channels evolution:

1. Display & ivideo

2. Search

3. Paid social

4. Mobile

5. Technology overlook

CONNECTED CONSUMER

Connected population

18,8 mio of regular users

Source: Gemius Audience 11/2014

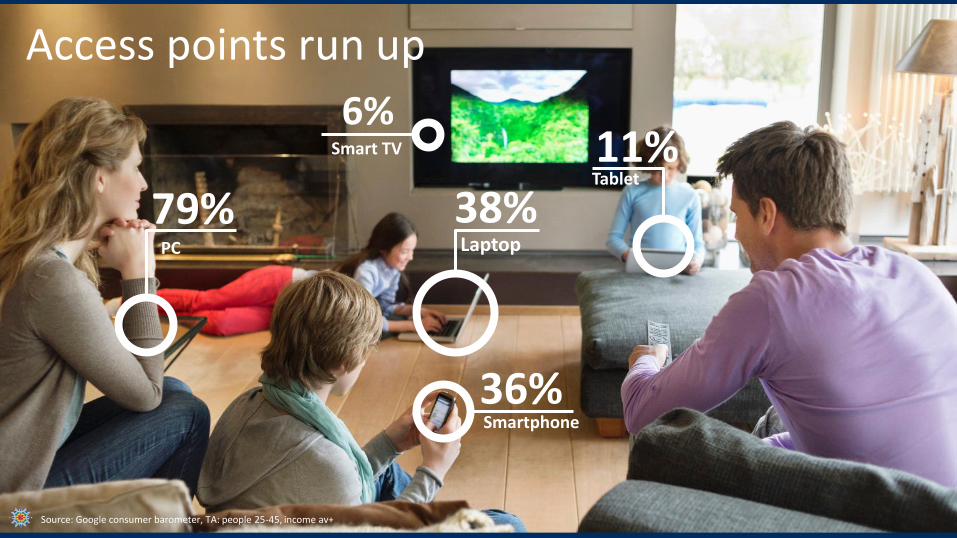

Access points run up

Source: Google consumer barometer, TA: people 25-45, income av+

38%

11%

Laptop

Tablet

36% Smartphone

79% PC

6% Smart TV

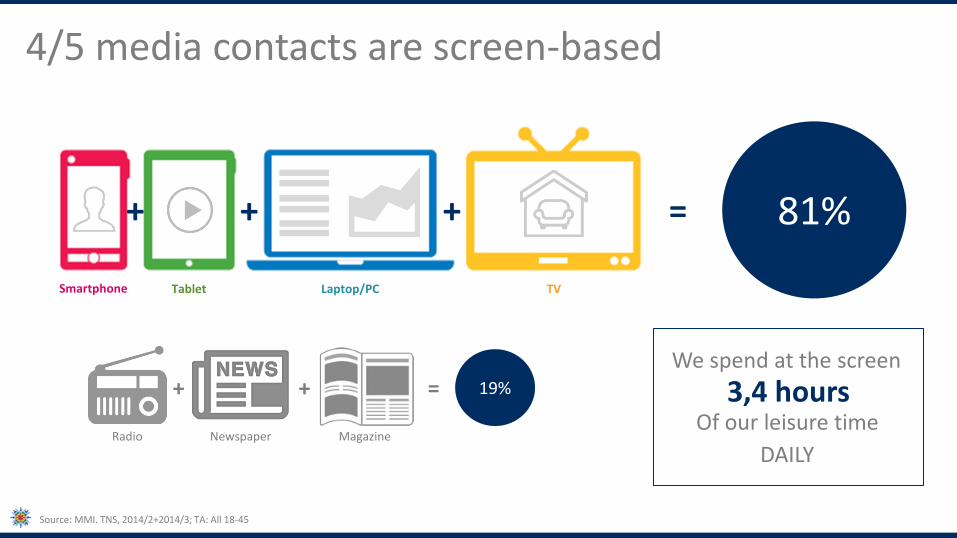

4/5 media contacts are screen-based

81%

19%

Source: MMI. TNS, 2014/2+2014/3; TA: All 18-45

Smartphone Tablet Laptop/PC TV

+ + + =

Radio Newspaper Magazine

+ + = 3,4 hours We spend at the screen

Of our leisure time

DAILY

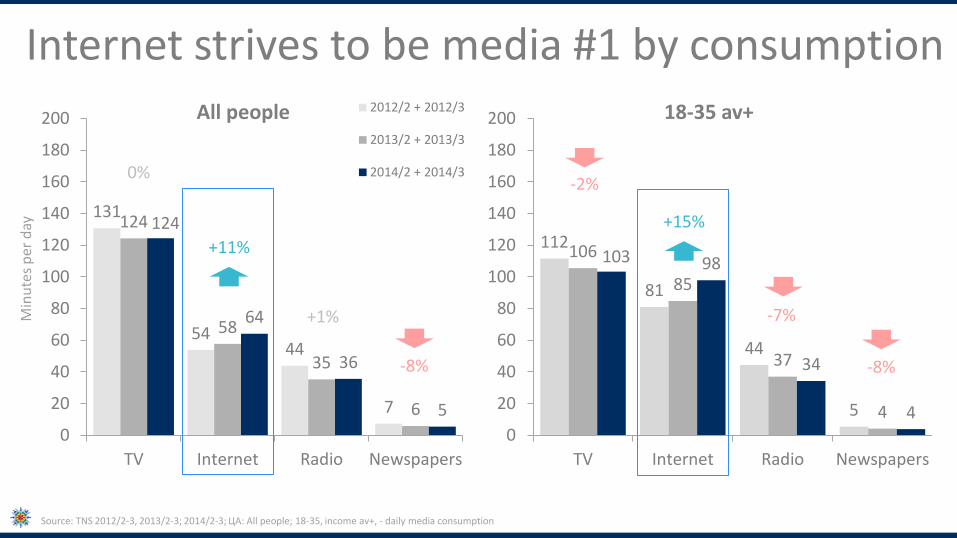

Internet strives to be media #1 by consumption

Source: TNS 2012/2-3, 2013/2-3; 2014/2-3; ЦА: All people; 18-35, income av+, - daily media consumption

131

54 44

7

124

58

35

6

124

64

36

5

0

20

40

60

80

100

120

140

160

180

200

TV Internet Radio Newspapers

All people 2012/2 + 2012/3

2013/2 + 2013/3

2014/2 + 2014/3

Min

ute

s p

er d

ay

+11%

0%

+1%

-8%

112

81

44

5

106

85

37

4

103 98

34

4 0

20

40

60

80

100

120

140

160

180

200

TV Internet Radio Newspapers

18-35 av+

+15%

-2%

-7%

-8%

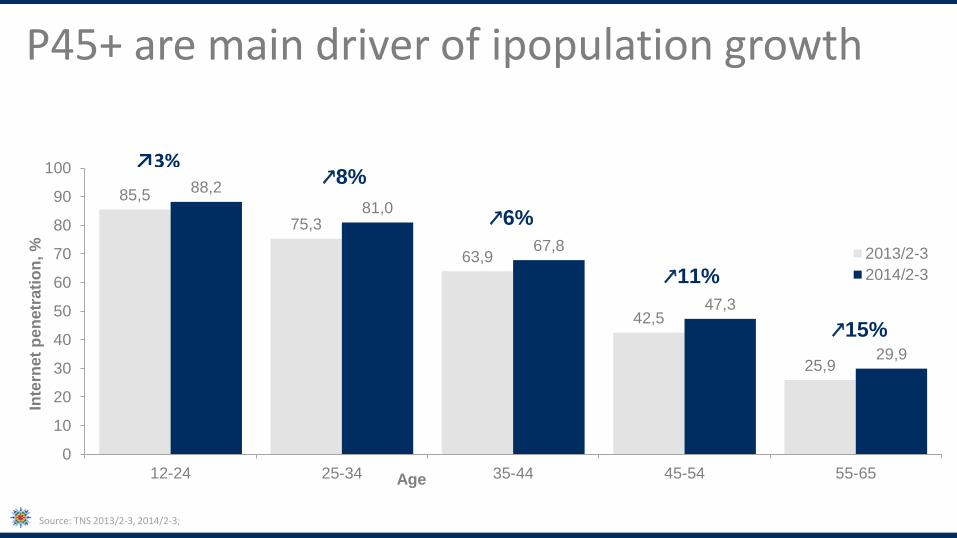

85,5

75,3

63,9

42,5

25,9

88,2

81,0

67,8

47,3

29,9

0

10

20

30

40

50

60

70

80

90

100

12-24 25-34 35-44 45-54 55-65

Inte

rnet

pen

etr

ati

on

, %

Age

2013/2-3

2014/2-3

↗3% ↗8%

↗6%

↗11%

↗15%

P45+ are main driver of ipopulation growth

Source: TNS 2013/2-3, 2014/2-3;

SUMMARY Internet breathing down TV’s neck in pursuit of the user's attention

P45+ is the most fast-growing age group among internet population

Number of connected devices is growing too

Screen-based media gradually finishing off print

MARKET

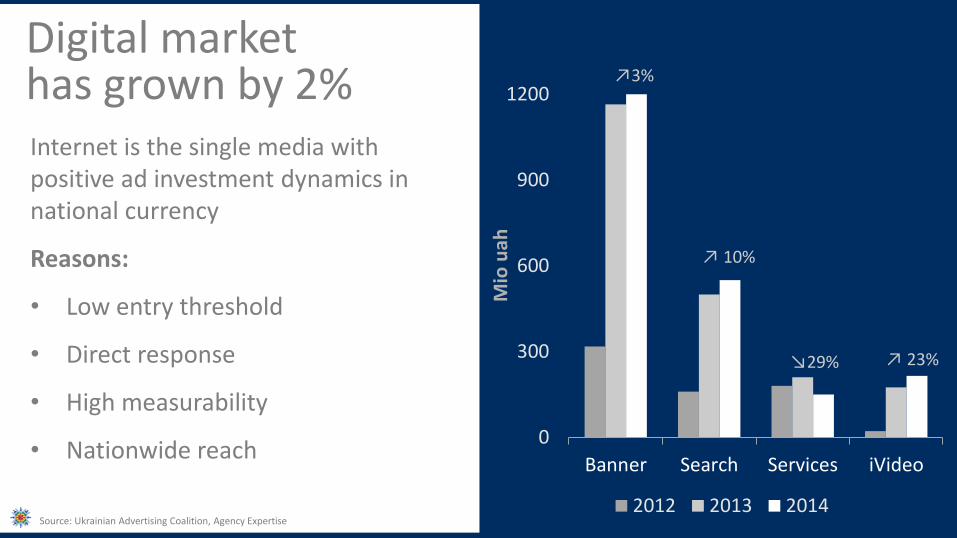

Digital market has grown by 2%

Source: Ukrainian Advertising Coalition, Agency Expertise

Internet is the single media with positive ad investment dynamics in national currency

Reasons:

• Low entry threshold

• Direct response

• High measurability

• Nationwide reach 0

300

600

900

1200

Banner Search Services iVideo

Mio

uah

2012 2013 2014

↗3%

↗ 10%

↘29% ↗ 23%

TRENDS

Individual message depending on socio-demographic, behavioral, purchase behavior, location, time of a day via:

• Programmatic buying with use of 2nd and 3rd party data (social networks, web-services, other not competing businesses)

• CRM-based campaigns on 1st party data

Personalization

CRMization

More opportunities for brands to build personal and consistent communication through multiple digital channels: e-mail, display, search, video, mobile

E-commerce

To increase CR and ROI

Tobacco, Alcohol, Beer?

To overcome some legal limitations

FMCG

To increase loyalty, buying frequency and average bill

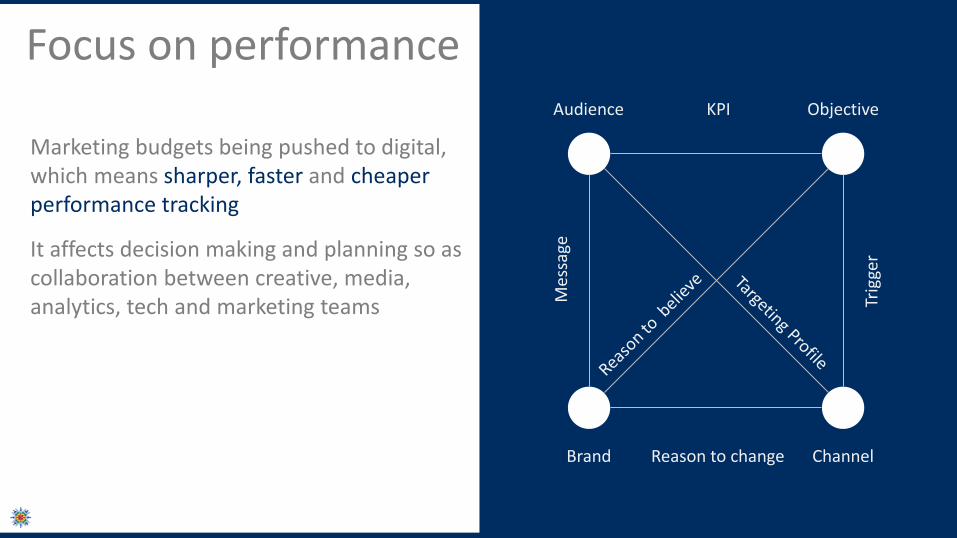

Focus on performance

Marketing budgets being pushed to digital, which means sharper, faster and cheaper performance tracking

It affects decision making and planning so as collaboration between creative, media, analytics, tech and marketing teams

Audience Objective

Channel Brand

Mes

sage

Trig

ger

KPI

Reason to change

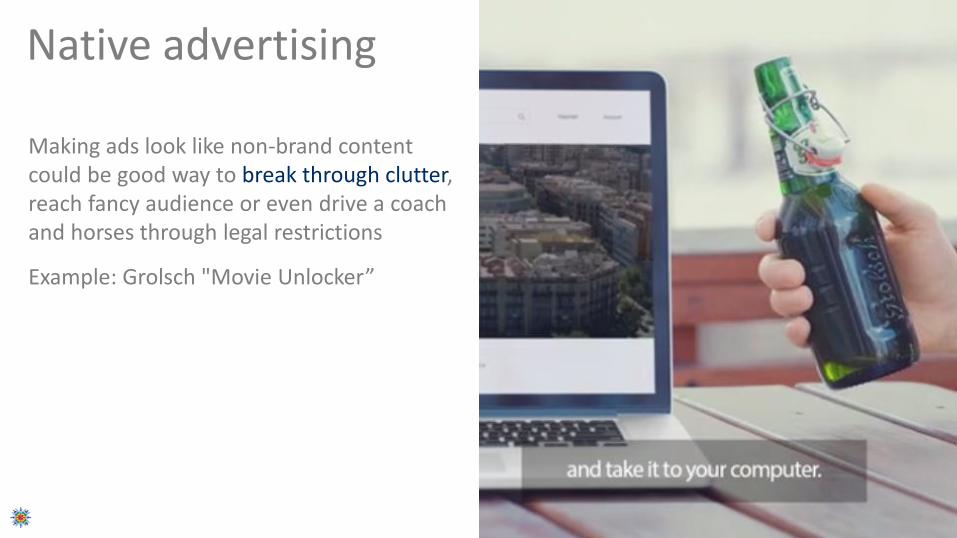

Making ads look like non-brand content could be good way to break through clutter, reach fancy audience or even drive a coach and horses through legal restrictions

Example: Grolsch "Movie Unlocker”

Native advertising

Integrated buying

Expansion of Open RTB seem to be technological way to integrated buying and analytics with single entry point to search, display, video, paid social and mobile

But technology is not the main stumbling-stone on local market, there are lots of legal, organizational and cultural issues

SUMMARY Technology gives brands a chance to go broad and deep: reach nationwide keeping it personal and relevant across multiple channels

In crisis conditions some brands can reconsider and repurpose owned media

Blurry KPIs of “image campaigns” gradually give way to what-you-measure-is-what-you-got approach

DISPLAY ADS

Programmatic ecosystem evolves RTB infrastructure growth is being heavily depressed by exchange rates on Dollar and Euro to national currency

Yet number of international players entered Ukrainian market: RTBHouse, Doubleclick, Adform

Moreover, we have seen releases of local solutions, that offer SSP and DSP services: Admixer, C8 (cQube), DSPRate, RB Mail

Ad viewability issue

Google talks a lot about billions of ad impressions, that haven’t been seen by users, and lobbying its viewability control technology

Apparently target audience for this product are non-ecommerce advertisers, who build brand awareness online

But in terms of indirect effect it’s quite difficult task to measure, how “viewable” campaigns boost result

Expecting some proof cases from Google to come soon

Sold out of licensed inventory becomes a rule. As a solution new in-page formats and additional in-stream ad blocks being introduced by publishers

Targeting on Smart TV and Mobile become available and meaningful due to non-desktop video consumption growth

Initially Google’s CPV buying model unofficially practiced by other publishers

ivideo

0

2

4

6

8

10

DiGi Media Youtube.com Admixer Video Megogo.net Ex.ua Fs.to Rutube.ru

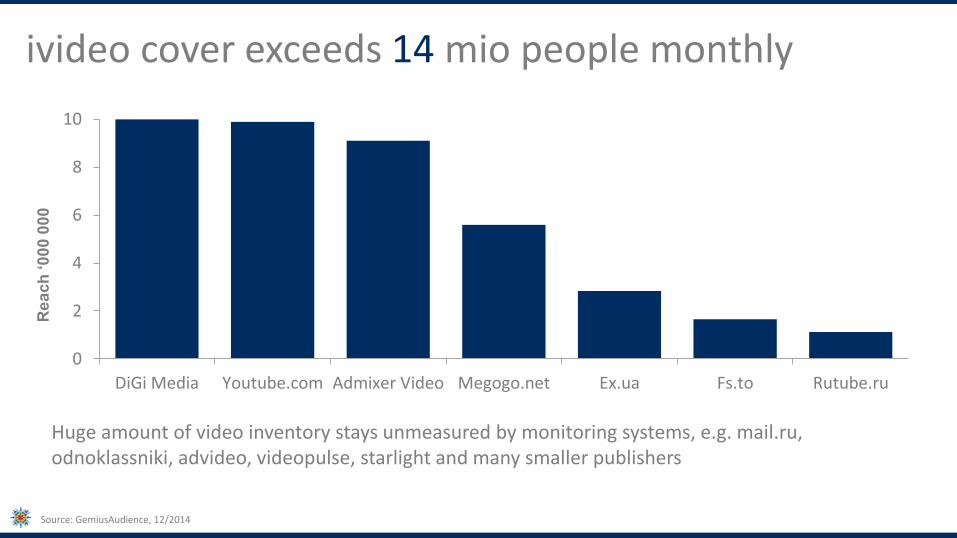

ivideo cover exceeds 14 mio people monthly R

ea

ch

‘0

00

00

0

Source: GemiusAudience, 12/2014

Huge amount of video inventory stays unmeasured by monitoring systems, e.g. mail.ru, odnoklassniki, advideo, videopulse, starlight and many smaller publishers

Google brand uplift survey

In terms of growing popularity of ivideo local release of Google brand uplift survey is expected. Service enables to measure YouTube trueview ad efficiency by tracking brand health metrics

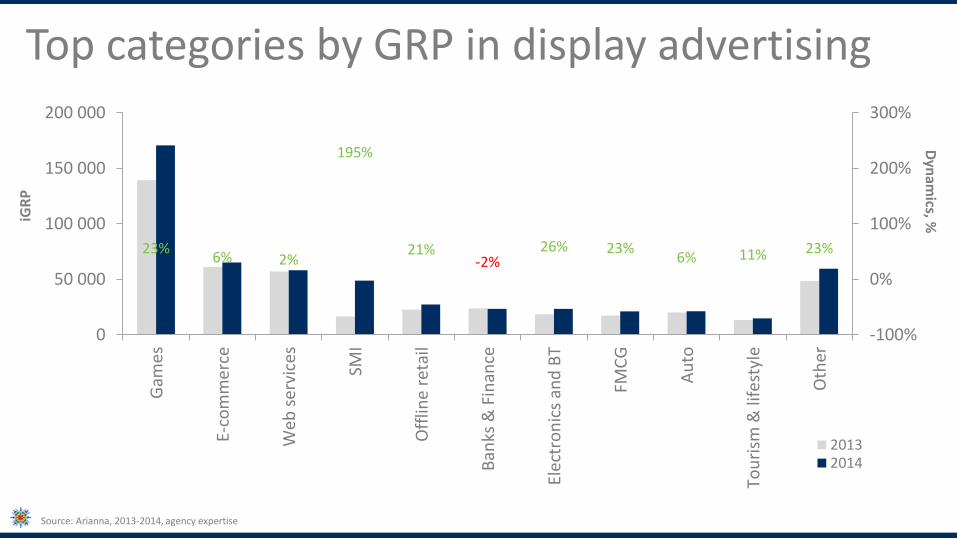

Top categories by GRP in display advertising

23% 6% 2%

195%

21% -2%

26% 23% 6% 11% 23%

-100%

0%

100%

200%

300%

0

50 000

100 000

150 000

200 000

Gam

es

E-co

mm

erce

Web

ser

vice

s

SMI

Off

line

reta

il

Ban

ks &

Fin

ance

Elec

tro

nic

s an

d B

T

FMC

G

Au

to

Tou

rism

& li

fest

yle

Oth

er

20132014Dynamics

iGR

P

Dyn

amics, %

Source: Arianna, 2013-2014, agency expertise

SUMMARY Ivideo is good complement and in some cases even substitution for TV

Topical issues of 2015:

• Effective cross-channel planning

• Single source ad measurement across media

• Brand image campaigns evaluation

• Quality control

SEARCH

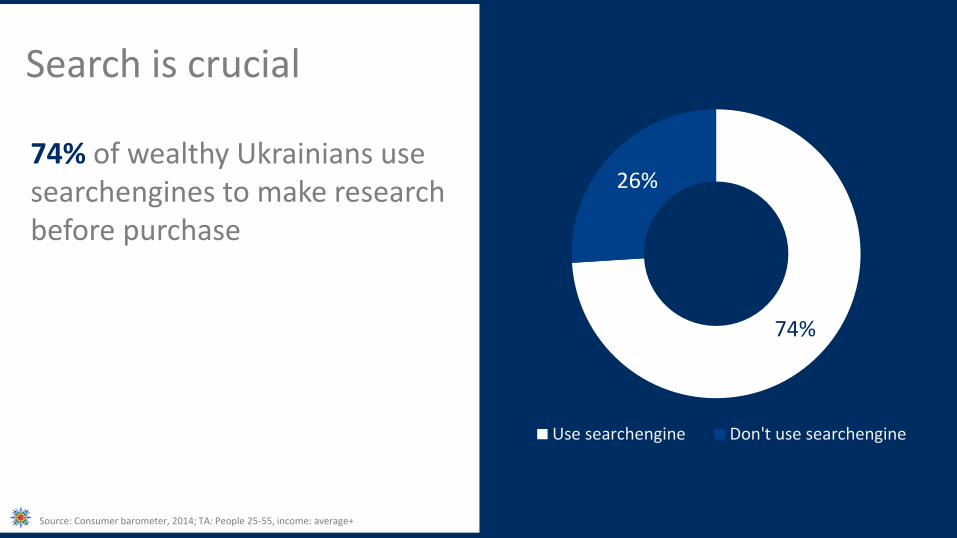

Search is crucial

74% of wealthy Ukrainians use searchengines to make research before purchase

Source: Consumer barometer, 2014; TA: People 25-55, income: average+

74%

26%

Use searchengine Don't use searchengine

Search! wherever you are

Source: Consumer barometer, 2014; TA: People 25-55, income: average+

Smart phone

17%

PC/laptop

93% Tablet

10%

Research being made across multiple connected devices, but very few online advertisers take it into account

7% used all devices

SUMMARY 3/4 of internet audience use searchengine during purchase making process

Search is still one of the main drivers of online sales

Investment in search advertising in 2014 has grown by 83%

PAID SOCIAL

In August Twitter made available promoted posts with targeting on Ukrainian audience

So far Twitter has been used mostly by media companies and publishers

Twitter launched ads in Ukraine

Source: Twitter Advertising Blog

In Ukraine

• Ad image size got bigger

• Less ad slots in block

• New reporting dashboard

Globally

• Hyperlocation targeting

• Image video campaigns

New on Facebook

SUMMARY For most verticals contribution of social networks in business results not proven yet

But wide audience reach in combination with huge amount of users’ data, aggregated in one place, make them promising channel

MOBILE

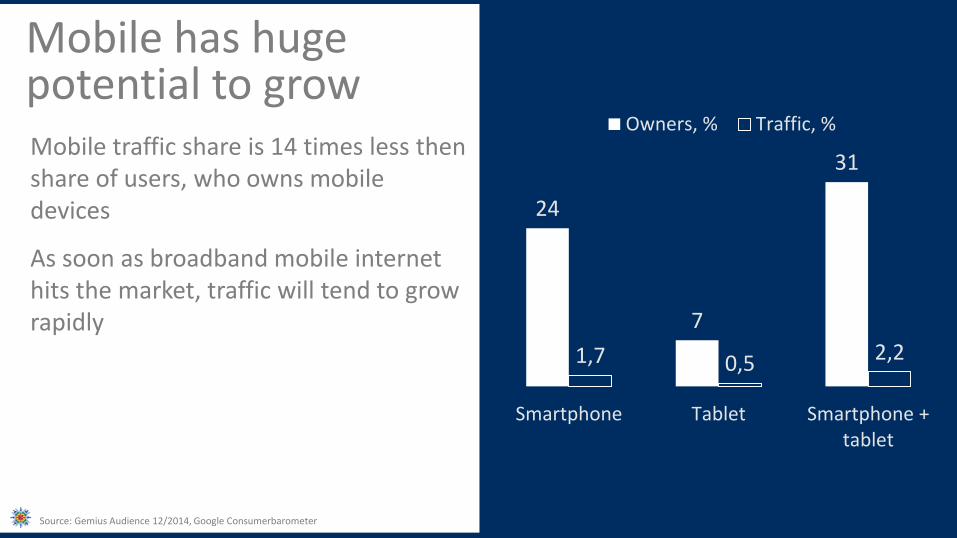

Mobile has huge potential to grow

Source: Gemius Audience 12/2014, Google Consumerbarometer

24

7

31

1,7 0,5 2,2

Smartphone Tablet Smartphone +tablet

Owners, % Traffic, %Mobile traffic share is 14 times less then share of users, who owns mobile devices

As soon as broadband mobile internet hits the market, traffic will tend to grow rapidly

8% of Ukrainian consumers

compare the prices via smartphone before purchase

right now

And…

Source: Google consumer barometer, TA: people 25-45, income av+

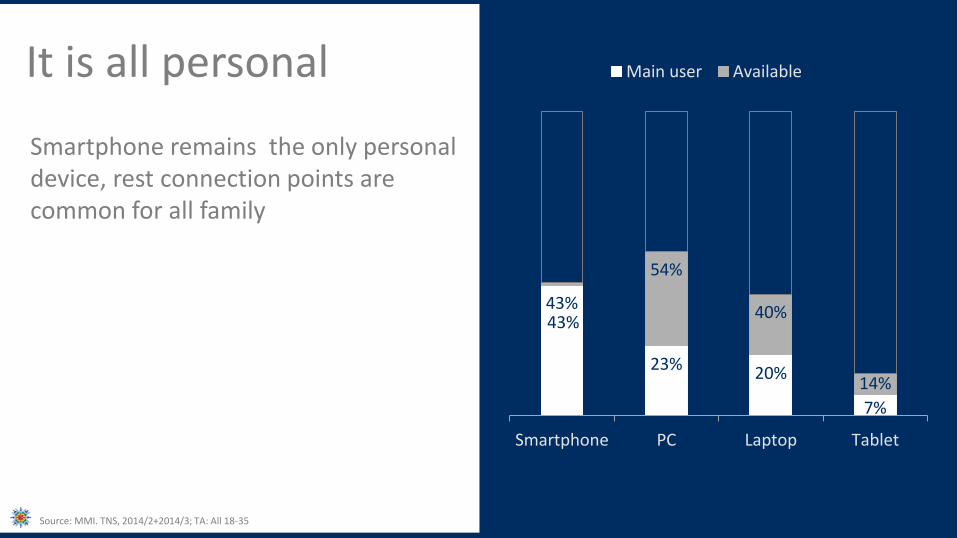

It is all personal

Source: MMI. TNS, 2014/2+2014/3; TA: All 18-35

Smartphone remains the only personal device, rest connection points are common for all family

43%

23% 20%

7%

43%

54%

40%

14%

Smartphone PC Laptop Tablet

Main user Available

Marketer’s must have mobile kit

Responsive web-site Mobile friendly ads App

• Decrease bounce rate • Increase CR • ROI boost

• Higher CTR • Better targeting • Richer UX • Click to call

• User’s data access • Mobile CRM • Free recurrent contact

SUMMARY One in three users access Internet via mobile devise

It is 6 000 000 of potential clients, who:

• have sophisticated requirements to brand’s site, quality and promptness of service

• live here and now, ready to pay for new experience

TECH that will change the way we interact

Mobile payment vanish the gap between decision and purchase

And looks like this trend is here to stay, since Apple considered to support it

Apple Pay

UHD Video – new opportunities and challenges

Chance to reach super premium audience on UHD TV

But ad video should be UHD ready to perform flawlessly

Reinvent TV as modern entertainment center:

• Multiplayer mobile games on big screen

• Exploring pictures and video from mobile devices

• Web-browsing

Affordable pricing ($35) of devise promises popularity

Brands can guide users through unique cross-screen experiences

Chromecast reincarnation of TV

Wearables

Who already use it to market their products:

• Healthcare

• Navigation and security services

• Sportswear (Nike+)

• Auto (Nissan Nismo Watch)

WELCOME TO CONNECT [email protected] GARMASHABLE