Embed Size (px)

Citation preview

building on a

proven strategy

C O R P O R AT E U P D AT E

JULY 2015

Forward Looking Statements

This presentation contains “forward-looking statements”, within the meaning of the United States Private Securities Litigation Reform Act of 1995 and

applicable Canadian securities legislation, concerning the business, operations and financial performance and condition of Goldcorp Inc. (“Goldcorp or “The

Company”). Forward-looking statements include, but are not limited to, statements with respect to the future price of gold, silver, copper, lead and zinc, the

estimation of mineral reserves and resources, the realization of mineral reserve estimates, the timing and amount of estimated future production, costs of

production, capital expenditures, costs and timing of the development of new deposits, success of exploration activities, permitting time lines, hedging

practices, currency exchange rate fluctuations, requirements for additional capital, government regulation of mining operations, environmental risks,

unanticipated reclamation expenses, timing and possible outcome of pending litigation, title disputes or claims and limitations on insurance

coverage. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not

expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, “believes” or variations of such words

and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”. Forward-looking

statements are made based upon certain assumptions and other important factors that, if untrue, could cause the actual results, performances or

achievements of Goldcorp to be materially different from future results, performances or achievements expressed or implied by such statements. Such

statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which Goldcorp will

operate in the future, including the price of gold, anticipated costs and ability to achieve goals. Certain important factors that could cause actual results,

performances or achievements to differ materially from those in the forward-looking statements include, among others, gold price volatility, discrepancies

between actual and estimated production, mineral reserves and mineral resources and metallurgical recoveries, mining operational and development risks,

litigation risks, regulatory restrictions (including environmental regulatory restrictions and liability), activities by governmental authorities (including changes in

taxation), currency fluctuations, the speculative nature of gold exploration, the global economic climate, dilution, share price volatility, competition, loss of key

employees, additional funding requirements and defective title to mineral claims or property. Although Goldcorp believes its expectations are based upon

reasonable assumptions and has attempted to identify important factors that could cause actual actions, events or results to differ materially from those

described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended.

Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity,

performance or achievements of Goldcorp to be materially different from those expressed or implied by such forward-looking statements, including but not

limited to: risks related to the integration of acquisitions; risks related to international operations; risks related to joint venture operations; actual results of

current exploration activities; actual results of current reclamation activities; conclusions of economic evaluations; changes in project parameters as plans

continue to be refined; future prices of gold, silver, copper, lead and zinc; possible variations in ore reserves, grade or recovery rates; failure of plant,

equipment or processes to operate as anticipated; accidents, labour disputes; delays in obtaining governmental approvals or financing or in the completion of

development or construction activities and other risks of the mining industry, as well as those factors discussed in the section entitled “Description of the

Business – Risk Factors” in Goldcorp’s annual information form for the year ended December 31, 2014 available at www.sedar.com. Although Goldcorp has

attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be

other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as

actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on

forward-looking statements. Goldcorp does not undertake to update any forward-looking statements that are included in this document, except in accordance

with applicable securities laws.

All amounts are in U.S. dollars, unless otherwise stated.2

2015 DeliverablesP R O V E N S T R AT E G Y

Achieve zero fatalities

Grow gold production to between 3.3 and 3.6 million(1) ounces

Deliver free cash flow after dividends

Replace/grow gold mineral reserves Company-wide

Maintain investment grade balance sheet

Achieve successful ramp ups at Cerro Negro and Éléonore

Advance Concentrate Enrichment/Pyrite Leach feasibility study at Peñasquito

Realize benefits of $175 million from the Operating for Excellence program

Complete sale of Wharf; Probe acquisition

3

(1) See Appendix B for mine-by-mine guidance and Appendix E for non-GAAP disclosure

4

Goldcorp’s Key AttributesP R O V E N S T R AT E G Y

Growing Production

Declining AISC

Reduced Capital Spend

Reserve Growth Potential

Organic Growth Opportunities

Record of Portfolio Management Success

Free Cash Flow in 2015

Long Term Value

STRONG INVESTMENT GRADE(1) BALANCE SHEET

4

(1) Moody’s: Baa2; S&P: BBB-

5

Track Record of GrowthP R O V E N S T R AT E G Y

2012

2.4Moz

2013

2.7Moz

2014

2.87Moz

2015E(1)

3.3-3.6Moz

Start-up of new mines and strong production from cornerstone mines(1) See Appendix B for mine-by-mine guidance and Appendix E for non-GAAP disclosure

Growing RevenuesP R O V E N S T R AT E G Y

(1) Revenues on an attributable basis which include the Company’s share from Alumbrera and Pueblo Viejo and revenues associated with discontinued operations; net of TCRC’s

(2) See Appendix A for budget price assumptions

(3) Gold price – Capital IQ (January 1, 2012 – March 31, 2015)

2

1

2012

$5.4B 2013

$4.7B2014

$4.5B

2015E

$5.1B-

$5.5B

$1,000

$1,500

$2,000

Gold price3

US$/oz

6

P R O V E N S T R AT E G Y

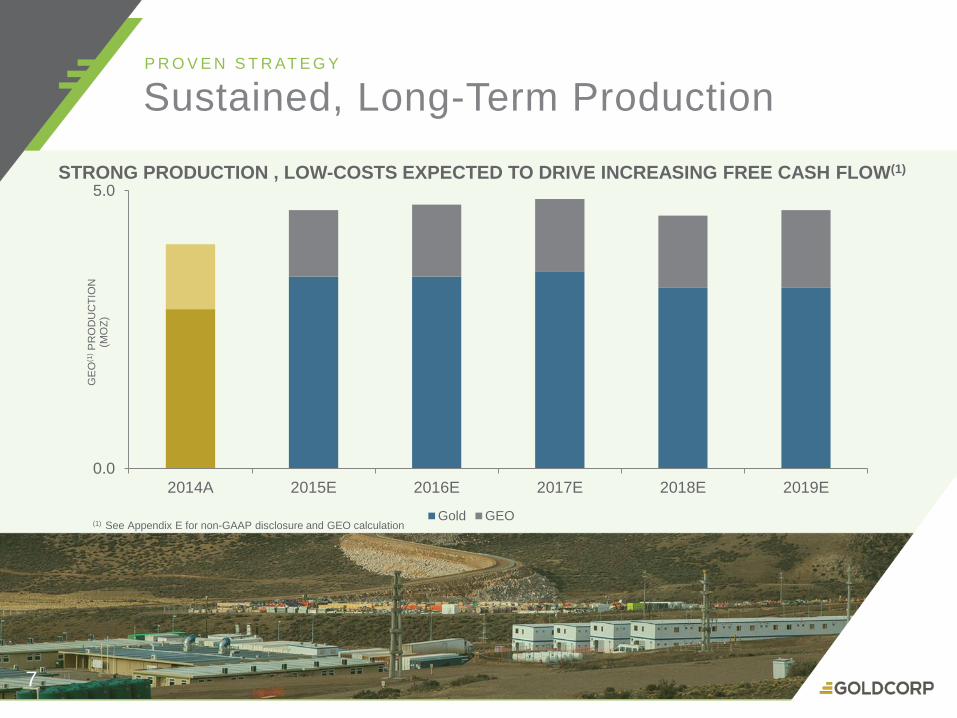

Sustained, Long-Term Production

STRONG PRODUCTION , LOW-COSTS EXPECTED TO DRIVE INCREASING FREE CASH FLOW(1)

0.0

5.0

2014A 2015E 2016E 2017E 2018E 2019E

GE

O(1

)P

RO

DU

CT

ION

(MO

Z)

Gold GEO(1) See Appendix E for non-GAAP disclosure and GEO calculation

7

P R O V E N S T R AT E G Y

2012

$884/oz

2013

$1,031/oz 2014

$949/oz

Focus on Cost Control Drives Declining Costs1

8

2015E

$875-

950/oz

New mines, Operating for Excellence program drive cost savings(1) Costs are all-in sustaining cost per gold ounce; see Appendix E for non-GAAP disclosure

Major Capital Spend CompletedP R O V E N S T R AT E G Y

2012

$2.6B

Capital spending decreases with completion of two new high quality mines

2013

$2.4B2014

$2.2B

2015E

$1.2-1.4B(Sustaining capex:

$875M-$1.025B)(1)

9

(1) Refer to Appendix E for non-GAAP disclosure

10

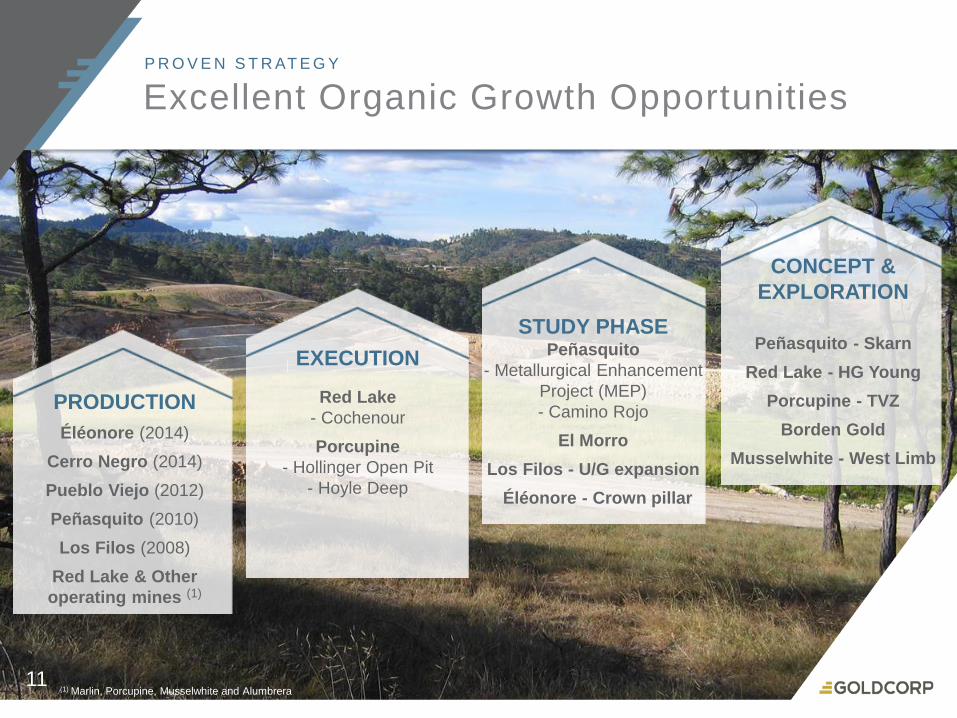

Potential for Reserve GrowthP R O V E N S T R AT E G Y

CERRO

NEGROÉLÉONORE PEÑASQUITO COCHENOUR BORDEN

GOLD

Re-started

drilling in

Q4 2014

Deep drilling

underway

Metallurgical

Enhancement

Project

Initial resources

and reserves

expected in 2015

Acquired

Q1 2015

PROVEN AND PROBABLE MINERAL RESERVES(1)

49,580,000 gold ounces

(1) Year ended December 31, 2014, refer to Appendix F for further information

11

PRODUCTION

Éléonore (2014)

Cerro Negro (2014)

Pueblo Viejo (2012)

Peñasquito (2010)

Los Filos (2008)

Red Lake & Other

operating mines (1)

STUDY PHASEPeñasquito

- Metallurgical Enhancement

Project (MEP)

- Camino Rojo

El Morro

Los Filos - U/G expansion

Éléonore - Crown pillar

CONCEPT &

EXPLORATION

Peñasquito - Skarn

Red Lake - HG Young

Porcupine - TVZ

Borden Gold

Musselwhite - West Limb

EXECUTION

Red Lake

- Cochenour

Porcupine

- Hollinger Open Pit

- Hoyle Deep

(1) Marlin, Porcupine, Musselwhite and Alumbrera,

Excellent Organic Growth OpportunitiesP R O V E N S T R AT E G Y

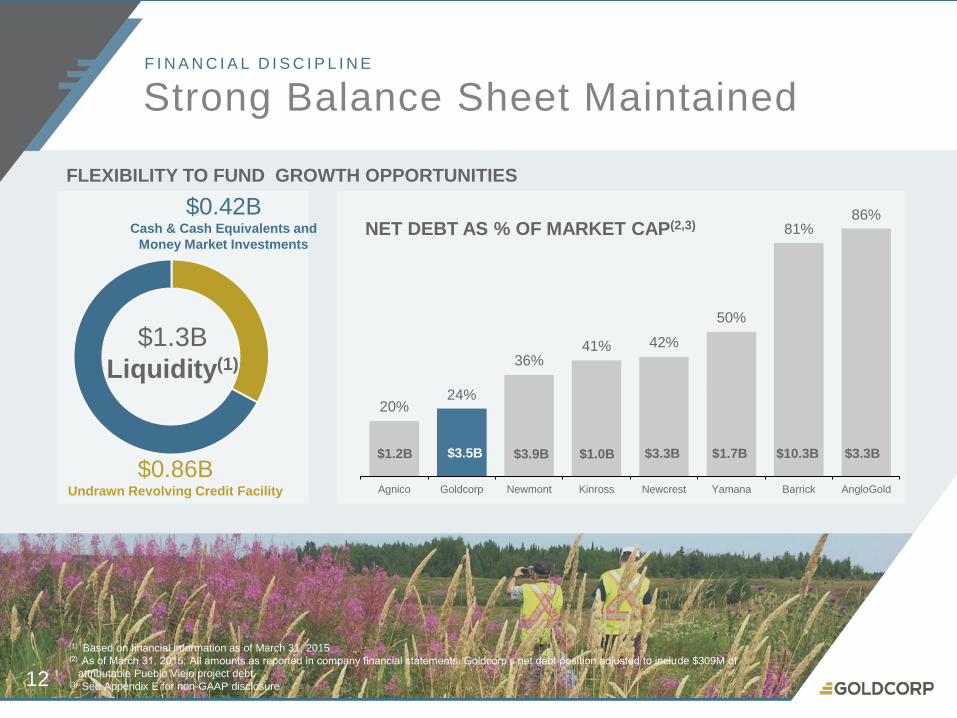

Strong Balance Sheet MaintainedF I N A N C I A L D I S C I P L I N E

$1.3B

Liquidity(1)

$0.42BCash & Cash Equivalents and

Money Market Investments

$0.86BUndrawn Revolving Credit Facility

NET DEBT AS % OF MARKET CAP(2,3)

FLEXIBILITY TO FUND GROWTH OPPORTUNITIES

(1) Based on financial information as of March 31, 2015(2) As of March 31, 2015; All amounts as reported in company financial statements. Goldcorp’s net debt position adjusted to include $309M of

attributable Pueblo Viejo project debt. (3) See Appendix E for non-GAAP disclosure12

20% 24%

36% 41% 42%

50%

81% 86%

Agnico Goldcorp Newmont Kinross Newcrest Yamana Barrick AngloGold

$3.3B$10.3B$1.7B$3.3B$1.0B$3.9B$3.5B$1.2B

13

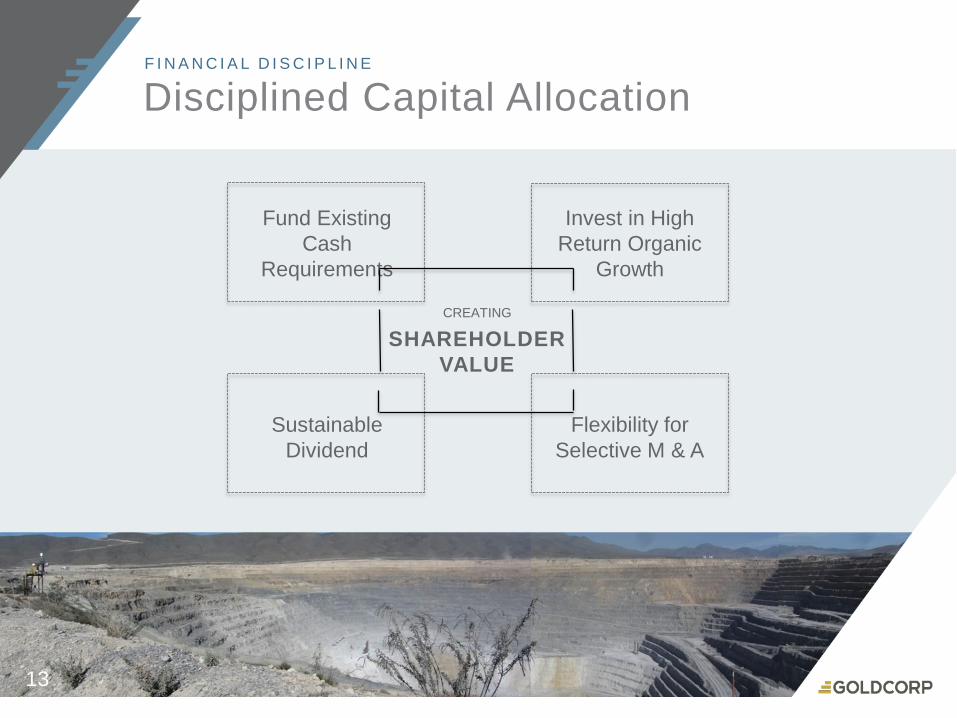

Disciplined Capital AllocationF I N A N C I A L D I S C I P L I N E

CREATING

SHAREHOLDER

VALUE

Fund Existing

Cash

Requirements

Invest in High

Return Organic

Growth

Sustainable

Dividend

Flexibility for

Selective M & A

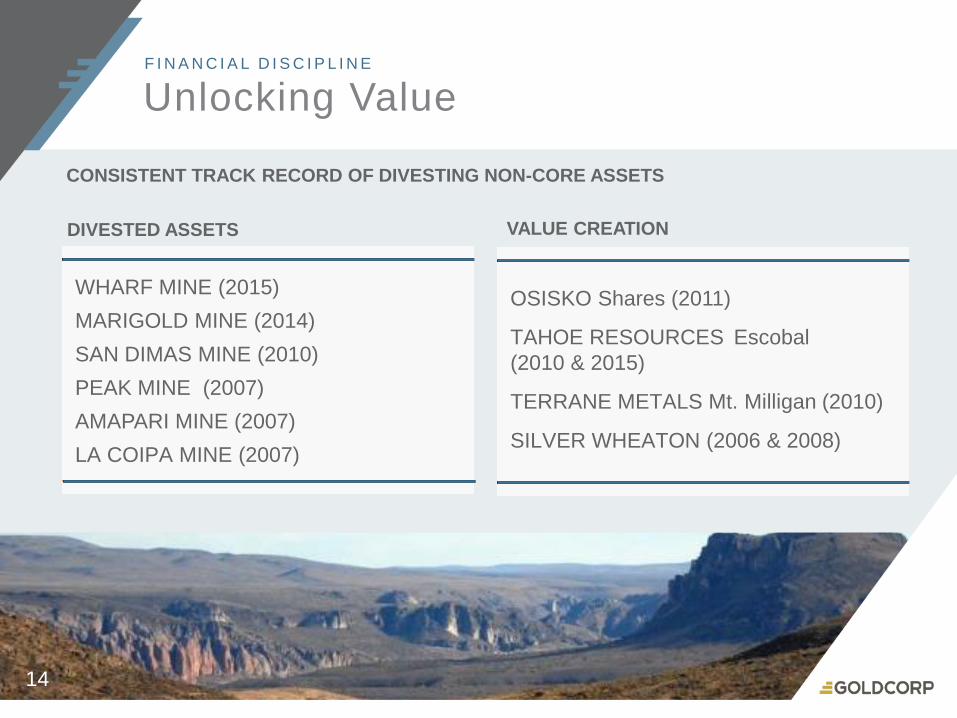

Unlocking ValueF I N A N C I A L D I S C I P L I N E

14

WHARF MINE (2015)

MARIGOLD MINE (2014)

SAN DIMAS MINE (2010)

PEAK MINE (2007)

AMAPARI MINE (2007)

LA COIPA MINE (2007)

OSISKO Shares (2011)

TAHOE RESOURCES Escobal

(2010 & 2015)

TERRANE METALS Mt. Milligan (2010)

SILVER WHEATON (2006 & 2008)

DIVESTED ASSETS VALUE CREATION

CONSISTENT TRACK RECORD OF DIVESTING NON-CORE ASSETS

Operating mines

Development projects

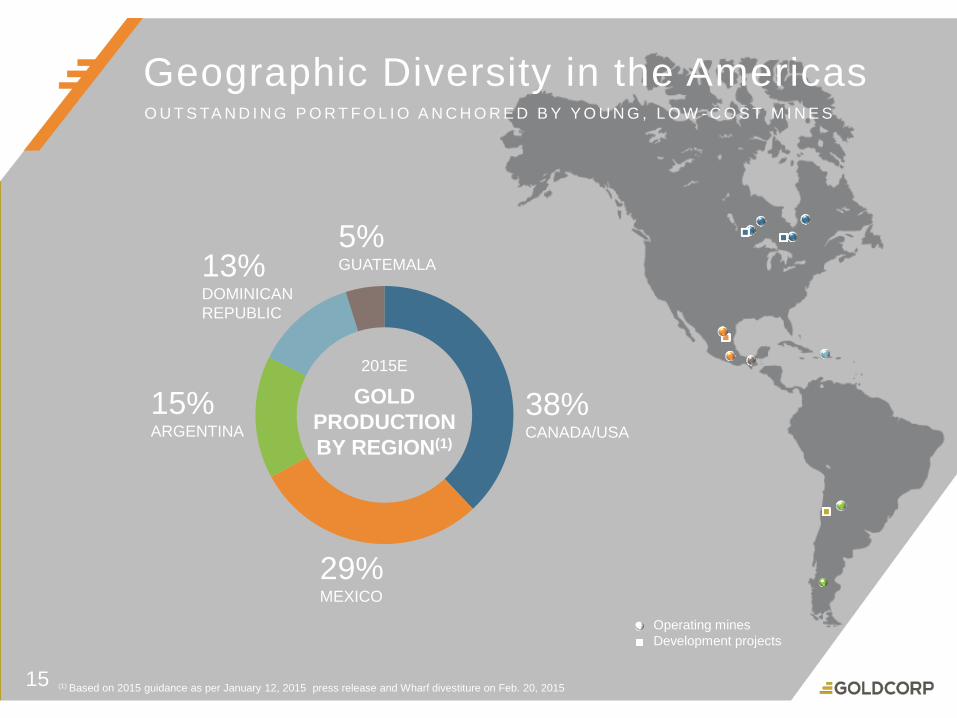

15 (1) Based on 2015 guidance as per January 12, 2015 press release and Wharf divestiture on Feb. 20, 2015

2015E

GOLD

PRODUCTION

BY REGION(1)

38%CANADA/USA

Geographic Diversity in the AmericasO U T S TA N D I N G P O R T F O L I O A N C H O R E D B Y Y O U N G , L O W - C O S T M I N E S

29%MEXICO

13%DOMINICAN

REPUBLIC

15%ARGENTINA

5%GUATEMALA

Cerro NegroN E W G R O W T H D R I V E R

COMMERCIAL PRODUCTION ACHIEVED

JAN. 1, 2015

- 2014A: 152,100ozs

- 2015E: 425,000 - 475,000ozs

MINE PRODUCTION RATES INCREASING

- Additional u/g mobile equipment on-site

- Training program ongoing

STRONG RAMP-UP CONTINUES

OUTSTANDING RESERVE GROWTH

POTENTIAL

- Resource confirmation drilling underway

- Reserve and resources(1)

- P&P gold reserves: 5.26Mozs

- M&I gold resources: 0.65Mozs

- Inferred gold resources: 0.32Mozs

16 (1) Year ended December 31, 2014, refer to Appendix F for further information

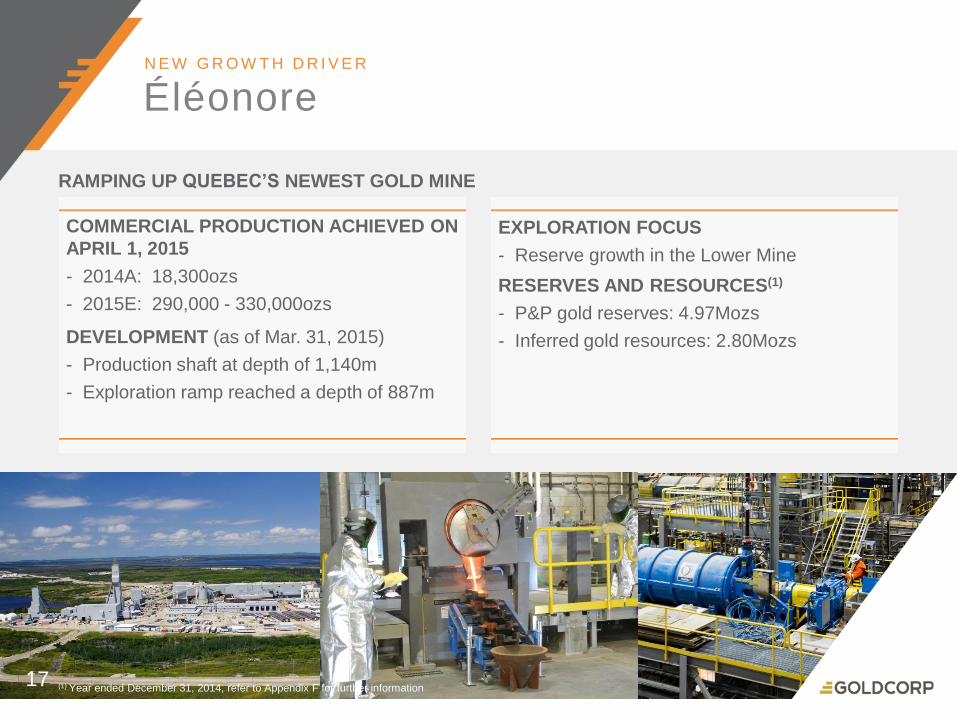

Éléonore N E W G R O W T H D R I V E R

COMMERCIAL PRODUCTION ACHIEVED ON

APRIL 1, 2015

- 2014A: 18,300ozs

- 2015E: 290,000 - 330,000ozs

DEVELOPMENT (as of Mar. 31, 2015)

- Production shaft at depth of 1,140m

- Exploration ramp reached a depth of 887m

RAMPING UP QUEBEC’S NEWEST GOLD MINE

EXPLORATION FOCUS

- Reserve growth in the Lower Mine

RESERVES AND RESOURCES(1)

- P&P gold reserves: 4.97Mozs

- Inferred gold resources: 2.80Mozs

17 (1) Year ended December 31, 2014, refer to Appendix F for further information

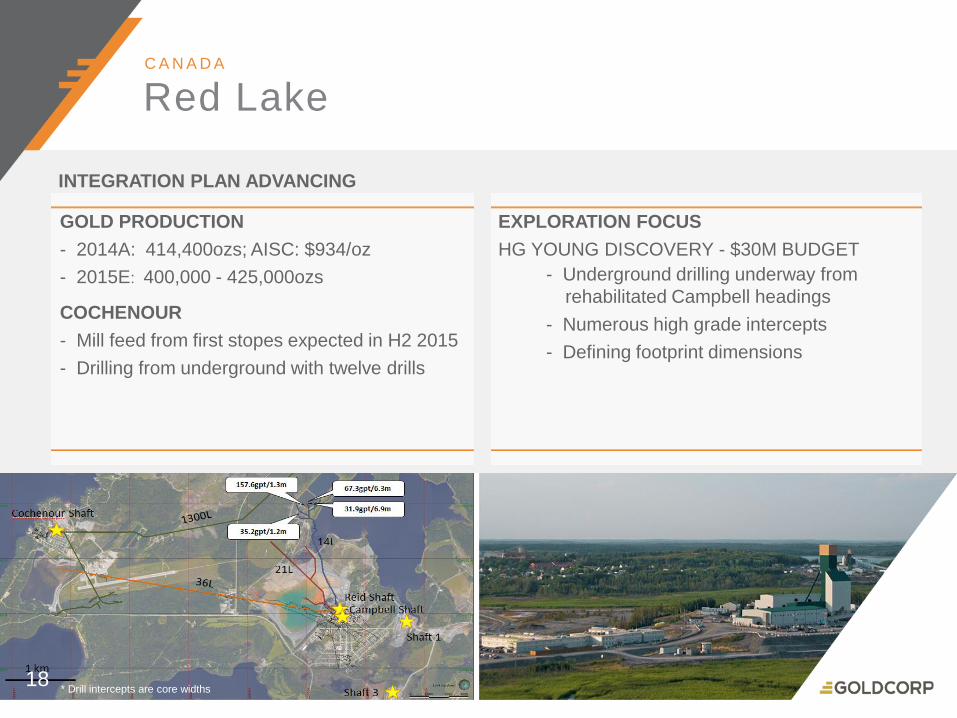

Red Lake C A N A D A

GOLD PRODUCTION

- 2014A: 414,400ozs; AISC: $934/oz

- 2015E: 400,000 - 425,000ozs

COCHENOUR

- Mill feed from first stopes expected in H2 2015

- Drilling from underground with twelve drills

INTEGRATION PLAN ADVANCING

EXPLORATION FOCUS

HG YOUNG DISCOVERY - $30M BUDGET

- Underground drilling underway from

rehabilitated Campbell headings

- Numerous high grade intercepts

- Defining footprint dimensions

18* Drill intercepts are core widths

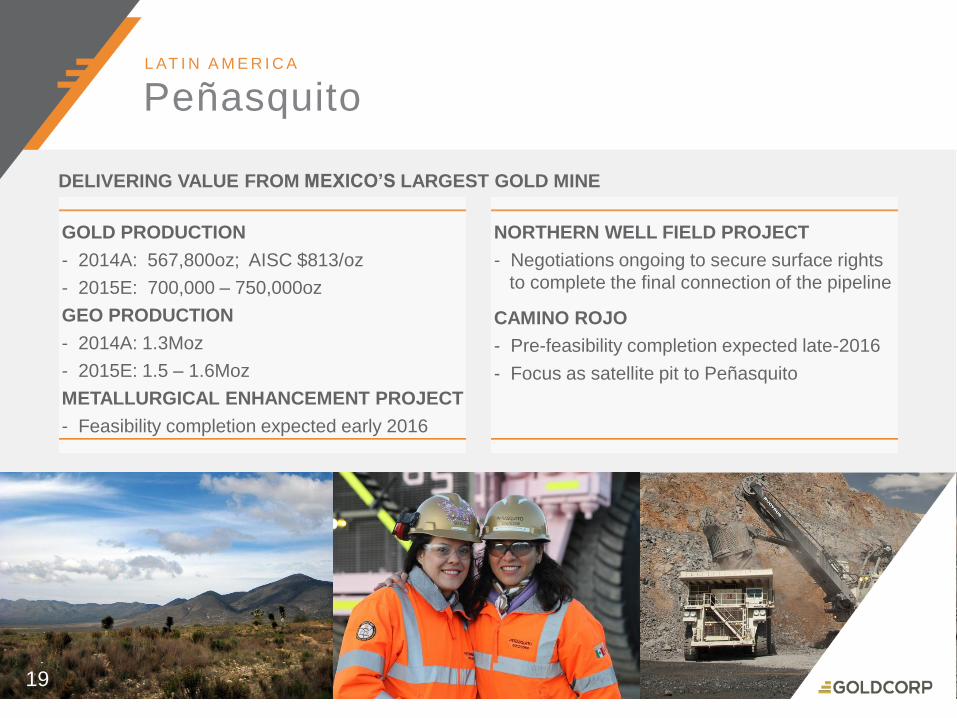

Peñasquito L AT I N A M E R I C A

DELIVERING VALUE FROM MEXICO’S LARGEST GOLD MINE

GOLD PRODUCTION

- 2014A: 567,800oz; AISC $813/oz

- 2015E: 700,000 – 750,000oz

GEO PRODUCTION

- 2014A: 1.3Moz

- 2015E: 1.5 – 1.6Moz

METALLURGICAL ENHANCEMENT PROJECT

- Feasibility completion expected early 2016

NORTHERN WELL FIELD PROJECT

- Negotiations ongoing to secure surface rights

to complete the final connection of the pipeline

CAMINO ROJO

- Pre-feasibility completion expected late-2016

- Focus as satellite pit to Peñasquito

19

Text line 1T E X T L I N E 2

20

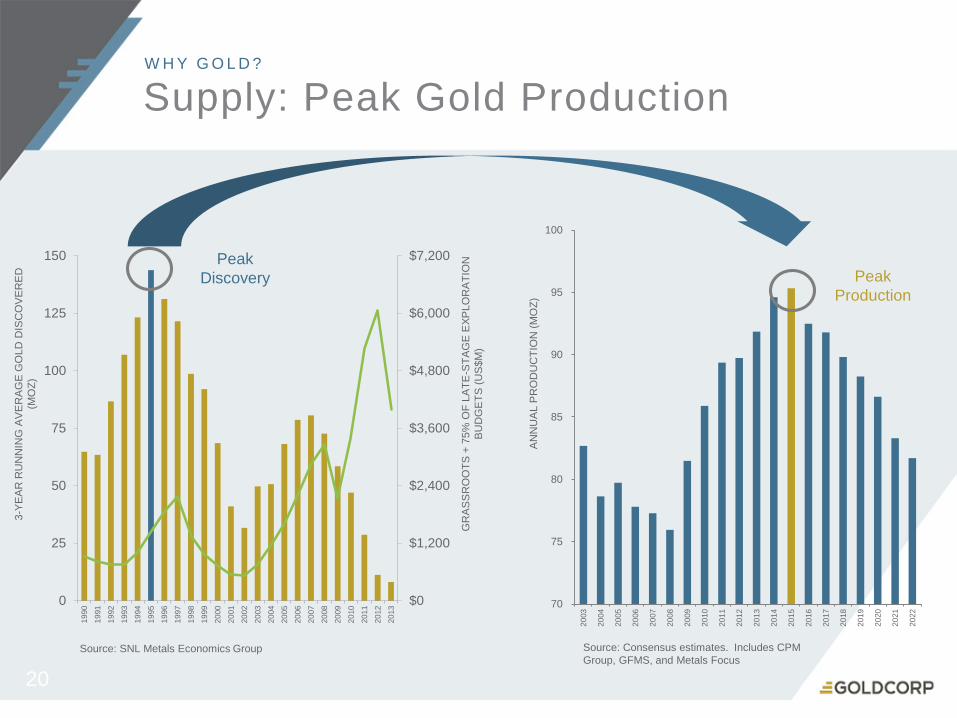

Supply: Peak Gold ProductionW H Y G O L D ?

$0

$1,200

$2,400

$3,600

$4,800

$6,000

$7,200

0

25

50

75

100

125

150

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13 70

75

80

85

90

95

100

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

AN

NU

AL P

RO

DU

CT

ION

(M

OZ

)

Source: Consensus estimates. Includes CPM

Group, GFMS, and Metals FocusSource: SNL Metals Economics Group

Peak

Discovery Peak

Production

3-Y

EA

R R

UN

NIN

G A

VE

RA

GE

GO

LD

DIS

CO

VE

RE

D

(MO

Z)

GR

AS

SR

OO

TS

+ 7

5%

OF

LA

TE

-ST

AG

E E

XP

LO

RA

TIO

N

BU

DG

ET

S (

US

$M

)

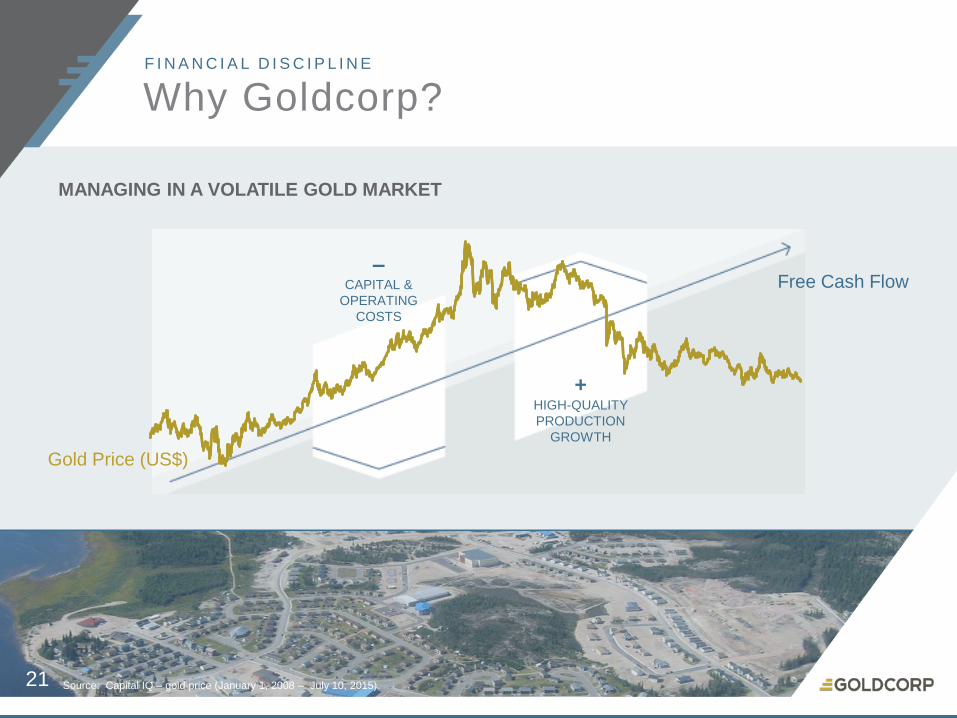

Why Goldcorp?F I N A N C I A L D I S C I P L I N E

MANAGING IN A VOLATILE GOLD MARKET

Gold Price (US$)

Free Cash Flow

21 Source: Capital IQ – gold price (January 1, 2008 – July 10, 2015)

+HIGH-QUALITY

PRODUCTION

GROWTH

–CAPITAL &

OPERATING

COSTS

Goldcorp Advantage

SUPERIOR INVESTMENT PROPOSITION

22

Quality

GrowthGold Focus

ResponsibleMining

Practices

Safe, Profitable

Production

Peer-Leading

Balance Sheet

Low Political

Risk

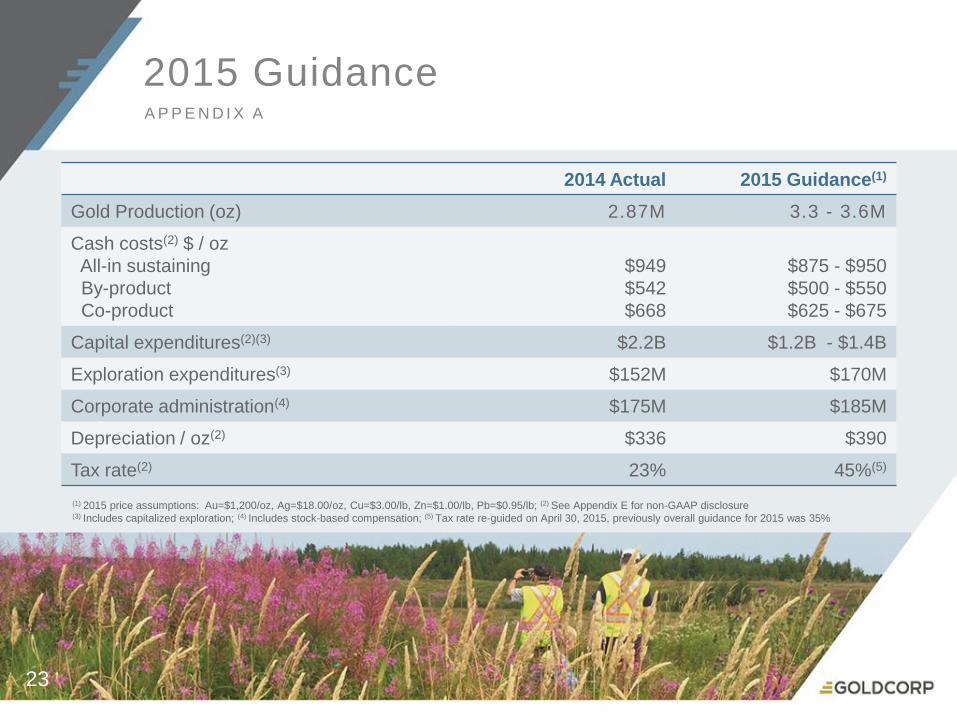

(1) 2015 price assumptions: Au=$1,200/oz, Ag=$18.00/oz, Cu=$3.00/lb, Zn=$1.00/lb, Pb=$0.95/lb; (2) See Appendix E for non-GAAP disclosure (3) Includes capitalized exploration; (4) Includes stock-based compensation; (5) Tax rate re-guided on April 30, 2015, previously overall guidance for 2015 was 35%

2014 Actual 2015 Guidance(1)

Gold Production (oz) 2.87M 3.3 - 3.6M

Cash costs(2) $ / oz

All-in sustaining

By-product

Co-product

$949

$542

$668

$875 - $950

$500 - $550

$625 - $675

Capital expenditures(2)(3) $2.2B $1.2B - $1.4B

Exploration expenditures(3) $152M $170M

Corporate administration(4) $175M $185M

Depreciation / oz(2) $336 $390

Tax rate(2) 23% 45%(5)

23

2015 GuidanceA P P E N D I X A

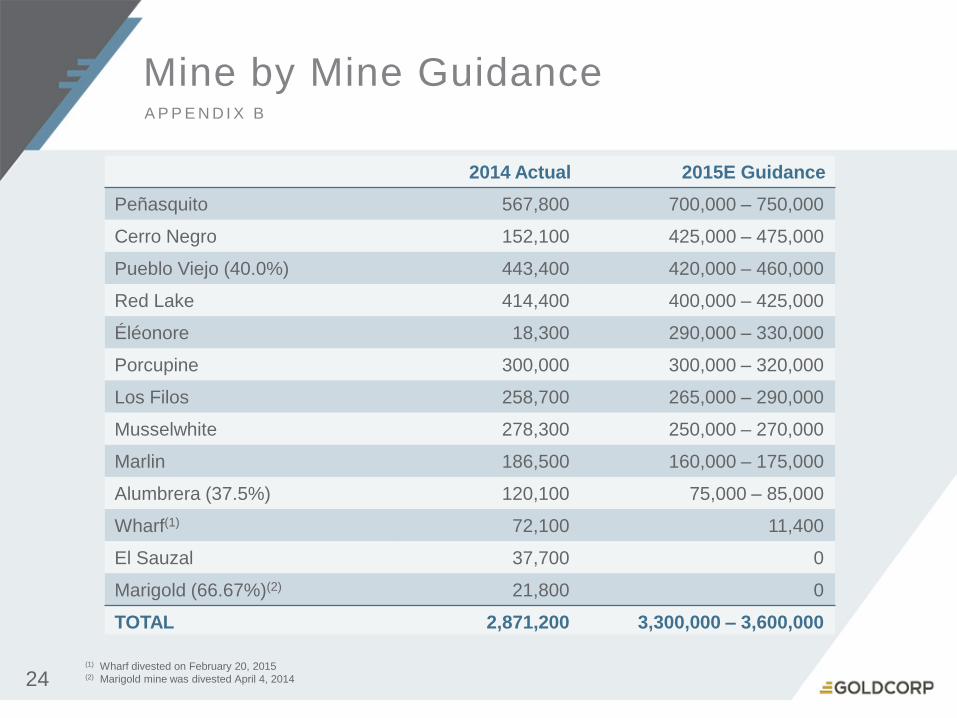

(1) Wharf divested on February 20, 2015(2) Marigold mine was divested April 4, 201424

2014 Actual 2015E Guidance

Peñasquito 567,800 700,000 – 750,000

Cerro Negro 152,100 425,000 – 475,000

Pueblo Viejo (40.0%) 443,400 420,000 – 460,000

Red Lake 414,400 400,000 – 425,000

Éléonore 18,300 290,000 – 330,000

Porcupine 300,000 300,000 – 320,000

Los Filos 258,700 265,000 – 290,000

Musselwhite 278,300 250,000 – 270,000

Marlin 186,500 160,000 – 175,000

Alumbrera (37.5%) 120,100 75,000 – 85,000

Wharf(1) 72,100 11,400

El Sauzal 37,700 0

Marigold (66.67%)(2) 21,800 0

TOTAL 2,871,200 3,300,000 – 3,600,000

Mine by Mine GuidanceA P P E N D I X B

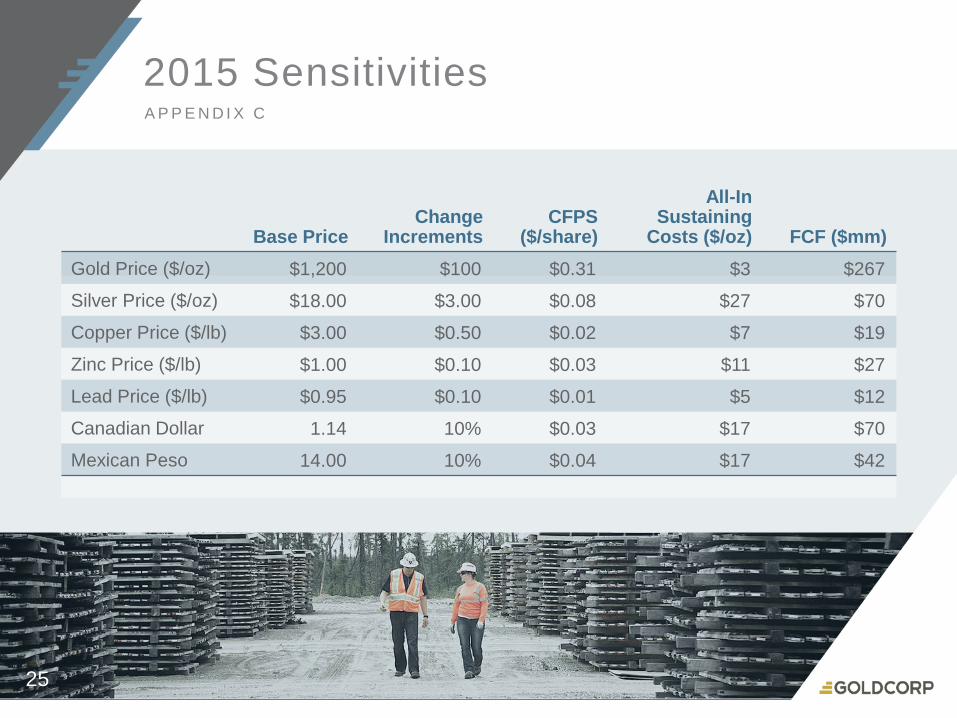

2015 SensitivitiesA P P E N D I X C

Base PriceChange

IncrementsCFPS

($/share)

All-In Sustaining

Costs ($/oz) FCF ($mm)

Gold Price ($/oz) $1,200 $100 $0.31 $3 $267

Silver Price ($/oz) $18.00 $3.00 $0.08 $27 $70

Copper Price ($/lb) $3.00 $0.50 $0.02 $7 $19

Zinc Price ($/lb) $1.00 $0.10 $0.03 $11 $27

Lead Price ($/lb) $0.95 $0.10 $0.01 $5 $12

Canadian Dollar 1.14 10% $0.03 $17 $70

Mexican Peso 14.00 10% $0.04 $17 $42

25

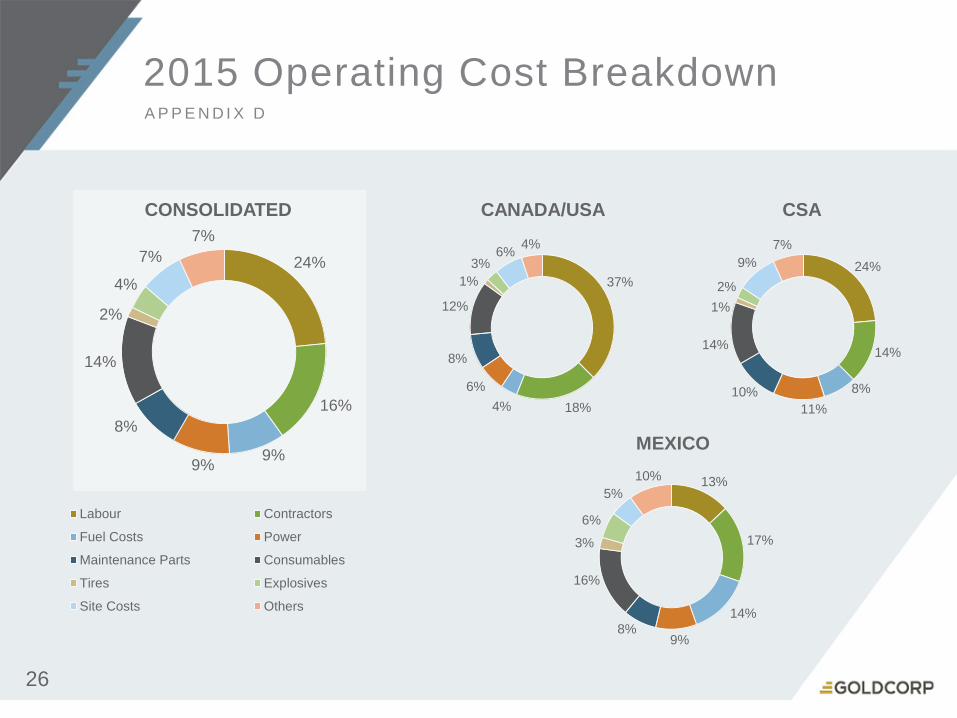

24%

16%

9%9%

8%

14%

2%

4%

7%

7%

Labour Contractors

Fuel Costs Power

Maintenance Parts Consumables

Tires Explosives

Site Costs Others

2015 Operating Cost BreakdownA P P E N D I X D

CONSOLIDATED CANADA/USA CSA

MEXICO

26

37%

18%4%

6%

8%

12%

1%

3%6%

4%

13%

17%

14%

9%8%

16%

3%

6%

5%

10%

24%

14%

8%

11%

10%

14%

1%

2%

9%

7%

Notes

Note 1: The Company has included non-GAAP performance measures on an attributable (or Goldcorp’s share) basis throughout this presentation. Attributable performance

measures include the Company’s mining operations, including its discontinued operation, and projects, and the Company’s share of Alumbrera and Pueblo Viejo. The

Company believes that disclosing certain performance measures on an attributable basis is a more relevant measurement of the Company’s operating and economic

performance, and reflects the Company’s view of its core mining operations. The Company believes that, in addition to conventional measures prepared in accordance with

GAAP, the Company and certain investors use this information to evaluate the Company’s performance and ability to generate cash flow; however, these performance

measures do not have any standardized meaning. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a substitute for

measures of performance prepared in accordance with GAAP.

Note 2: The Company has included non-GAAP performance measures – total cash costs, by-product and co-product, per gold ounce, throughout this presentation. In the

gold mining industry, total cash costs is a common performance measure but does not have any standardized meaning. The Company follows the recommendations of the

Gold Institute Production Cost Standard. The Gold Institute, which ceased operations in 2002, was a non-regulatory body and represented a global group of suppliers of gold

and gold products. The production cost standard developed by the Gold Institute remains the generally accepted standard of reporting cash costs of production by gold mining

companies. In addition to conventional measures prepared in accordance with GAAP, the Company assesses this measure in a manner that isolates the impacts of gold

production volumes, the by-product credits, and operating costs fluctuations such that the non-controllable and controllable variability is independently addressed. The

Company uses total cash costs, by-product and co-product, per gold ounce, to monitor its operating performance internally, including operating cash costs, as well as in its

assessment of potential development projects and acquisition targets. The Company believes these measures provide investors and analysts with useful information about

the Company’s underlying cash costs of operations and the impact of by-product credits on the Company’s cost structure and is a relevant metric used to understand the

Company’s operating profitability and ability to generate cash flow. When deriving the production cash costs associated with an ounce of gold, the Company includes by-

product credits as the Company considers that the cost to produce the gold is reduced as a result of the by-product sales incidental to the gold production process, thereby

allowing the Company’s management and other stakeholders to assess the net costs of gold production. The Company and certain investors use this information to evaluate

the Company’s performance and ability to generate cash flow. Accordingly, it is intended to provide additional information and should not be considered in isolation or as a

substitute for measures of performance prepared in accordance with GAAP. Total cash costs on a by-product basis are calculated by deducting Goldcorp’s share of by-

product silver, copper, lead and zinc sales revenues from Goldcorp’s share of production costs. Refer to page 36 of the Q1 2015 MD&A for a reconciliation of total cash costs

(by-product) per ounce for Q1 2015 to the unaudited condensed interim consolidated financial statements.

Total cash costs on a co-product basis are calculated by allocating Goldcorp’s share of production costs to each co-product based on the ratio of actual sales volumes

multiplied by budget metal prices, as compared to realized sales prices. The Company uses budget prices to eliminate price volatility and improve co-product cash cost

reporting comparability between periods. The budget metal prices used in the calculation of co-product total cash costs were as follows:

2015 2014 2013

Gold $ 1,200 $ 1,200 $ 1,600

Silver 18 20 30

Copper 3.00 3.00 3.50

Lead 0.95 1.00 0.90

Zinc 1.00 0.90 0.90

A P P E N D I X E

27

NotesA P P E N D I X E ( C O N T ’ D )

If silver, lead and zinc for Peñasquito, silver for Marlin, Cerro Negro and Pueblo Viejo, and copper for Alumbrera were treated as co-products, Goldcorp's share of total co-

product cash costs, including discontinued operations, for the three months ended March 31, 2015, would be $670 per ounce of gold, $9.79 per ounce of silver, $2.36 per

pound of copper, $0.80 per pound of zinc, and $0.81 per pound of lead (March 31, 2014 – $673 per ounce of gold, $10.58 per ounce of silver, $2.26 per pound of copper,

$0.73 per pound of zinc and $0.85 per pound of lead). Using actual realized sales prices, co-product total cash costs, including discontinued operations, would be $683 per

gold ounce for the three months ended March 31, 2015 (March 31, 2014 – $683). Refer to page 35 of the Q1 2015 MD&A for a reconciliation of total cash costs to reported

production costs.

Note 3: All-in sustaining costs and all-in costs are non-GAAP performance measures that the Company believes more fully define the total costs associated with producing

gold; however, these performance measures have no standardized meaning. Accordingly, it is intended to provide (in United States dollars, tabular amounts in millions,

except where noted) additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with

GAAP. The Company reports these measures on a gold ounces sold basis. The Company's all-in sustaining and all-in cost definitions conform to the guidance note

released by the World Gold Council, which became effective January 1, 2014. The World Gold Council is a non-regulatory market development organization for the gold

industry whose members comprise global senior gold mining companies. Refer to page 36 of the Q1 MD&A for a reconciliation of all-in sustaining costs, page 57 of the

2014 Annual Report and page 57 of the 2013 Annual Report.

Note 4: Free cash flows is a non-GAAP performance measure which the Company believes, in addition to conventional measures prepared in accordance with GAAP, the

Company and certain investors use to evaluate the Company's ability to generate cash flows. Accordingly, it is intended to provide additional information and should not be

considered in isolation or as a substitute for measures of performance prepared in accordance with GAAP and it has no standardized meaning. Free cash flows are

calculated by deducting from net cash provided by operating activities, Goldcorp's share of expenditures on mining interests, deposits on mining interest expenditures and

capitalized interest paid, and adding Goldcorp's share of net cash provided by operating activities from Alumbrera and Pueblo Viejo.

Note 5: Net Debt/Market capitalization is a non-GAAP performance measure which the Company believes, in addition to conventional measures prepared in accordance

with GAAP, the Company and certain investors use to evaluate the Company's debt levels relative to its peers. Accordingly, it is intended to provide additional information

and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with GAAP and it has no standardized meaning. Net debt

is calculated, on an attributable basis to include the Company’s share of Alumbrera and Pueblo Viejo, by adding short term and long term debt less cash and cash

equivalents. Market capitalization is information retrieved from Capital IQ and uses the outstanding number of shares of a company multiplied by its share price as at a

certain time period. To reconcile Net Debt to a GAAP measure the debt of $309M from Pueblo Viejo is deducted.

Note 6: Sustaining capital expenditures are defined as those expenditures which do not increase annual gold ounce production at a mine site and excludes all

expenditures at the Company’s projects and certain expenditures at the Company’s operating sites which are deemed expansionary in nature.

Note 7: Gold equivalent ounces are calculated using the following assumptions: $1300 per ounce of gold and by-product metal prices of $22.00 per ounce of silver, $3.00

per pound of copper, $0.90 per pound of lead and $0.90 per pound of zinc . By-product metals are converted to gold equivalent ounces by multiplying by-product metal

production with the associated by-product metal price and dividing it by the gold price.

28

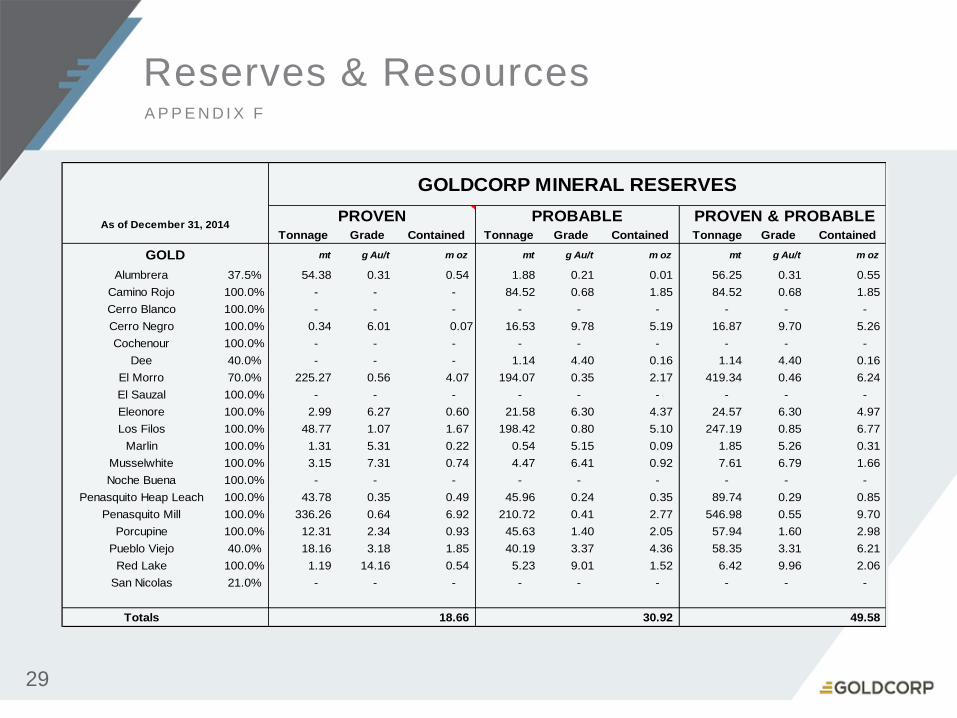

Reserves & Resources A P P E N D I X F

29

Tonnage Grade Contained Tonnage Grade Contained Tonnage Grade Contained

mt g Au/t m oz mt g Au/t m oz mt g Au/t m oz

Alumbrera 37.5% 54.38 0.31 0.54 1.88 0.21 0.01 56.25 0.31 0.55

Camino Rojo 100.0% - - - 84.52 0.68 1.85 84.52 0.68 1.85

Cerro Blanco 100.0% - - - - - - - - -

Cerro Negro 100.0% 0.34 6.01 0.07 16.53 9.78 5.19 16.87 9.70 5.26

Cochenour 100.0% - - - - - - - - -

Dee 40.0% - - - 1.14 4.40 0.16 1.14 4.40 0.16

El Morro 70.0% 225.27 0.56 4.07 194.07 0.35 2.17 419.34 0.46 6.24

El Sauzal 100.0% - - - - - - - - -

Eleonore 100.0% 2.99 6.27 0.60 21.58 6.30 4.37 24.57 6.30 4.97

Los Filos 100.0% 48.77 1.07 1.67 198.42 0.80 5.10 247.19 0.85 6.77

Marlin 100.0% 1.31 5.31 0.22 0.54 5.15 0.09 1.85 5.26 0.31

Musselwhite 100.0% 3.15 7.31 0.74 4.47 6.41 0.92 7.61 6.79 1.66

Noche Buena 100.0% - - - - - - - - -

Penasquito Heap Leach 100.0% 43.78 0.35 0.49 45.96 0.24 0.35 89.74 0.29 0.85

Penasquito Mill 100.0% 336.26 0.64 6.92 210.72 0.41 2.77 546.98 0.55 9.70

Porcupine 100.0% 12.31 2.34 0.93 45.63 1.40 2.05 57.94 1.60 2.98

Pueblo Viejo 40.0% 18.16 3.18 1.85 40.19 3.37 4.36 58.35 3.31 6.21

Red Lake 100.0% 1.19 14.16 0.54 5.23 9.01 1.52 6.42 9.96 2.06

San Nicolas 21.0% - - - - - - - - -

Totals 18.66 30.92 49.58

GOLDCORP MINERAL RESERVES

As of December 31, 2014PROVEN PROBABLE PROVEN & PROBABLE

GOLD

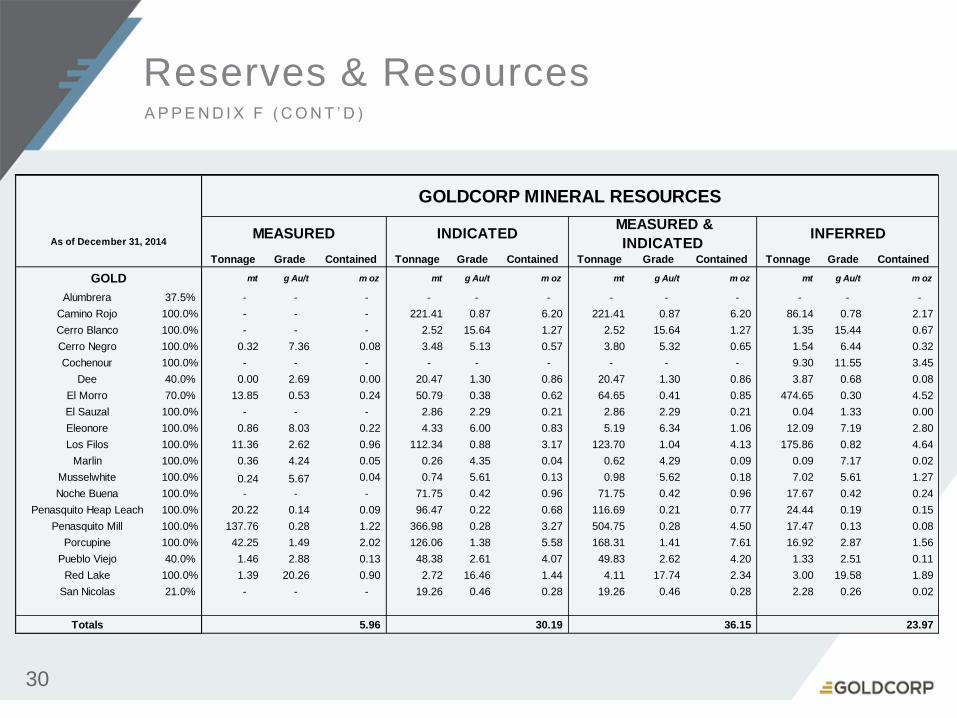

Reserves & ResourcesA P P E N D I X F ( C O N T ’ D )

30

Tonnage Grade Contained Tonnage Grade Contained Tonnage Grade Contained Tonnage Grade Contained

mt g Au/t m oz mt g Au/t m oz mt g Au/t m oz mt g Au/t m oz

Alumbrera 37.5% - - - - - - - - - - - -

Camino Rojo 100.0% - - - 221.41 0.87 6.20 221.41 0.87 6.20 86.14 0.78 2.17

Cerro Blanco 100.0% - - - 2.52 15.64 1.27 2.52 15.64 1.27 1.35 15.44 0.67

Cerro Negro 100.0% 0.32 7.36 0.08 3.48 5.13 0.57 3.80 5.32 0.65 1.54 6.44 0.32

Cochenour 100.0% - - - - - - - - - 9.30 11.55 3.45

Dee 40.0% 0.00 2.69 0.00 20.47 1.30 0.86 20.47 1.30 0.86 3.87 0.68 0.08

El Morro 70.0% 13.85 0.53 0.24 50.79 0.38 0.62 64.65 0.41 0.85 474.65 0.30 4.52

El Sauzal 100.0% - - - 2.86 2.29 0.21 2.86 2.29 0.21 0.04 1.33 0.00

Eleonore 100.0% 0.86 8.03 0.22 4.33 6.00 0.83 5.19 6.34 1.06 12.09 7.19 2.80

Los Filos 100.0% 11.36 2.62 0.96 112.34 0.88 3.17 123.70 1.04 4.13 175.86 0.82 4.64

Marlin 100.0% 0.36 4.24 0.05 0.26 4.35 0.04 0.62 4.29 0.09 0.09 7.17 0.02

Musselwhite 100.0% 0.24 5.67 0.04 0.74 5.61 0.13 0.98 5.62 0.18 7.02 5.61 1.27

Noche Buena 100.0% - - - 71.75 0.42 0.96 71.75 0.42 0.96 17.67 0.42 0.24

Penasquito Heap Leach 100.0% 20.22 0.14 0.09 96.47 0.22 0.68 116.69 0.21 0.77 24.44 0.19 0.15

Penasquito Mill 100.0% 137.76 0.28 1.22 366.98 0.28 3.27 504.75 0.28 4.50 17.47 0.13 0.08

Porcupine 100.0% 42.25 1.49 2.02 126.06 1.38 5.58 168.31 1.41 7.61 16.92 2.87 1.56

Pueblo Viejo 40.0% 1.46 2.88 0.13 48.38 2.61 4.07 49.83 2.62 4.20 1.33 2.51 0.11

Red Lake 100.0% 1.39 20.26 0.90 2.72 16.46 1.44 4.11 17.74 2.34 3.00 19.58 1.89

San Nicolas 21.0% - - - 19.26 0.46 0.28 19.26 0.46 0.28 2.28 0.26 0.02

Totals 5.96 30.19 36.15 23.97

GOLDCORP MINERAL RESOURCES

As of December 31, 2014MEASURED INDICATED

MEASURED &

INDICATED INFERRED

GOLD

Scientific and technical information contained in this presentation was reviewed and approved by Gil Lawson, P.Eng., Vice-President, Geology and Mine

Planning for Goldcorp, and a “qualified person” as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”).

For additional information on the scientific and technical information contained herein, see Goldcorp’s annual information form dated March 13, 2015 filed

under Goldcorp’s profile on SEDAR at www.sedar.com

Goldcorp December 31, 2014 Mineral Reserve and Mineral Resource Reporting Notes:

1 All Mineral Reserves and Mineral Resources have been estimated in accordance with the standards of the Canadian Institute of Mining, Metallurgy

and Petroleum and NI 43-101, or the AusIMM JORC equivalent.

2 All Mineral Resources are reported exclusive of Mineral Reserves.

3 Mineral Reserves and Mineral Resources are reported as of December 31, 2014, with the following conditions or exceptions:

(i) Mineral Reserves and Mineral Resources for Pueblo Viejo are as per information provided by Barrick Gold Corporation.

(ii) Mineral Reserves and Mineral Resources for Dee are as per information provided by Barrick Gold Corporation.

(iii) Mineral Resources for San Nicolas are as per information provided by Teck Resources Limited (2012 Study).

5 Mineral Reserves are estimated using appropriate recovery rates and US$ commodity prices of $1,300 per ounce of gold, $22 per ounce of

silver, $3.00 per pound of copper, $0.90 per pound of lead, and $0.90 per pound of zinc, unless otherwise noted below:

(i) Alumbrera $1,332/oz gold and $3.17/lb copper

(ii) Pueblo Viejo, Dee $1,100/oz gold, $17/oz silver, $3.00/lb copper

6 Mineral Resources are estimated using US$ commodity prices of $1,500 per ounce of gold, $24 per ounce of silver, $3.50 per pound of copper,

$1.00 per pound of lead, and $1.00 per pound of zinc, unless otherwise noted below;

(i) Pueblo Viejo, Dee $1,400/oz gold, $19/oz silver, $3.50/lb copper

(ii) San Nicolas $1,275/oz gold, $22.50.00/oz silver, $2.75/lb copper, $1.00/lb zinc

(iii) Éléonore $1,300/oz gold

Reserves & ResourcesA P P E N D I X F ( C O N T ’ D )

31

Cautionary Note to United States Investors Concerning Estimates of Measured, Indicated and Inferred Resources:

These tables have been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of United

States securities laws and uses terms that are not recognized by the United States Securities and Exchange Commission (“SEC”). The terms “Mineral Reserve”,

“Proven Mineral Reserve” and “Probable Mineral Reserve” are Canadian mining terms as defined in accordance with the Canadian Institute of Mining, Metallurgy

and Petroleum (“CIM”) — Definition Standards adopted by CIM Council on May 10, 2014 (the “CIM Definition Standards”) which were incorporated by reference in

the Canadian Securities Administrators’ NI 43-101 . These definitions differ from the definitions in SEC Industry Guide 7 (“SEC Industry Guide 7”) under United

States securities laws. Under SEC Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves or cash flow analysis to

designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority.

In addition, the terms “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral Resource” are defined in and

required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and are normally not permitted to be used in

reports and registration statements filed with the SEC. United States investors are cautioned not to assume that any part or all of mineral deposits in these

categories will ever be converted into reserves. “Inferred Mineral Resources” have a great amount of uncertainty as to their existence, and great uncertainty as to

their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under

Canadian regulations, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. United States

investors are cautioned not to assume that all or any part of an Inferred Mineral Resource exists or is economically or legally mineable. Disclosure of “contained

ounces” in a resource is permitted disclosure under Canadian regulations if such disclosure includes the grade or quality and the quantity for each category of

Mineral Resource and Mineral Reserve; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC

standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this presentation containing descriptions of the Company’s mineral deposits may not be comparable to similar information

made public by United States companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and

regulations thereunder.

Reserves & ResourcesA P P E N D I X F ( C O N T ’ D )

32