Embed Size (px)

Citation preview

AN INDUSTRY ANALYSIS

OF THE REAL ESTATE

SECTORBy:

Arunav Nayak (11DM059)

Sanjeev Kumar (11DM017)

Sudeshna Sahu (11DM039)

Sulekha Routray (11DM104)

APPROACH

Analysis of the Real Estate Cycle and the

parameters affecting it

Current Scenario of Real Estate in India

Analysis of the segments of the Real Estate

Industry (i.e Residential, Commercial, Retail and

Hospitality)

Key Players in the Indian Real Estate

Sector Market Performance in NSE

Global Trends

Application of Porter’s 5 Forces Model

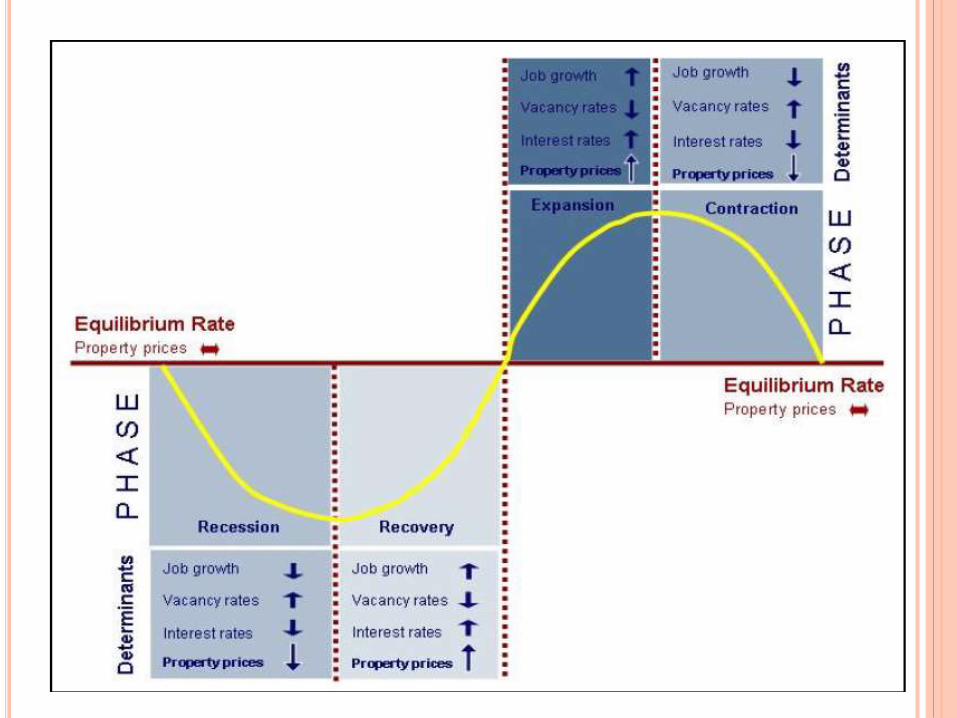

REAL ESTATE CYCLE

Real estate cycles are described as cyclic

movements of price in the real estate market which,

over a period of time, causes fluctuations in the

residential and commercial property market.

The real estate cycles involves periodic shifts of

rapid growth of output (recovery and

prosperity),alternating with relative stagnation or

decline (contraction or recession) over time.

PHASES OF REAL ESTATE CYCLE

Recession

Recovery

Expansion

Contraction

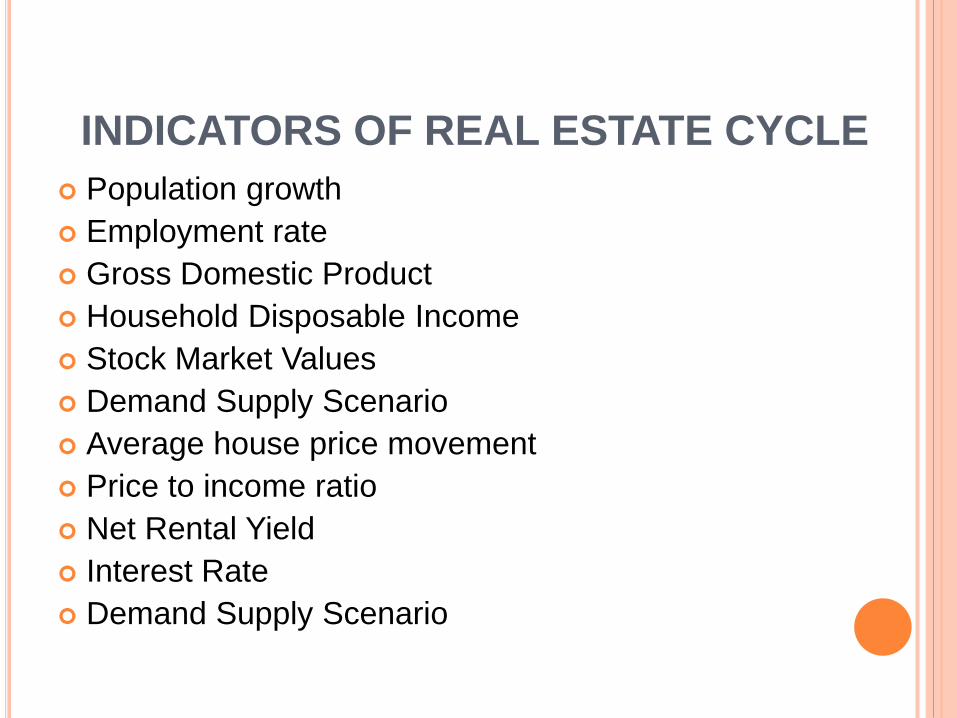

INDICATORS OF REAL ESTATE CYCLE

Population growth

Employment rate

Gross Domestic Product

Household Disposable Income

Stock Market Values

Demand Supply Scenario

Average house price movement

Price to income ratio

Net Rental Yield

Interest Rate

Demand Supply Scenario

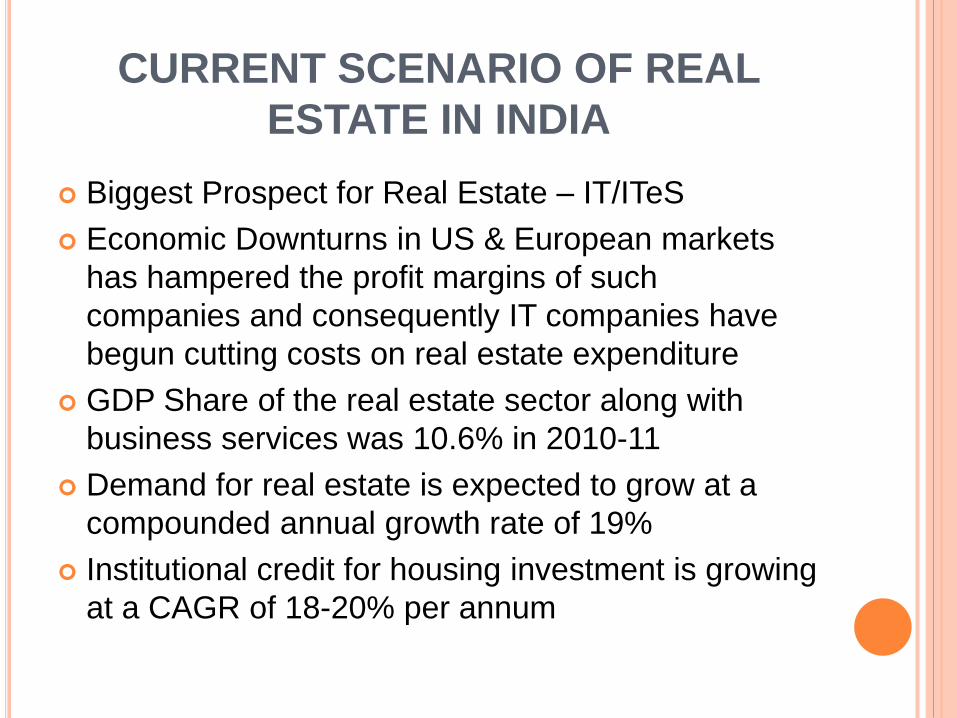

CURRENT SCENARIO OF REAL

ESTATE IN INDIA

Biggest Prospect for Real Estate – IT/ITeS

Economic Downturns in US & European markets

has hampered the profit margins of such

companies and consequently IT companies have

begun cutting costs on real estate expenditure

GDP Share of the real estate sector along with

business services was 10.6% in 2010-11

Demand for real estate is expected to grow at a

compounded annual growth rate of 19%

Institutional credit for housing investment is growing

at a CAGR of 18-20% per annum

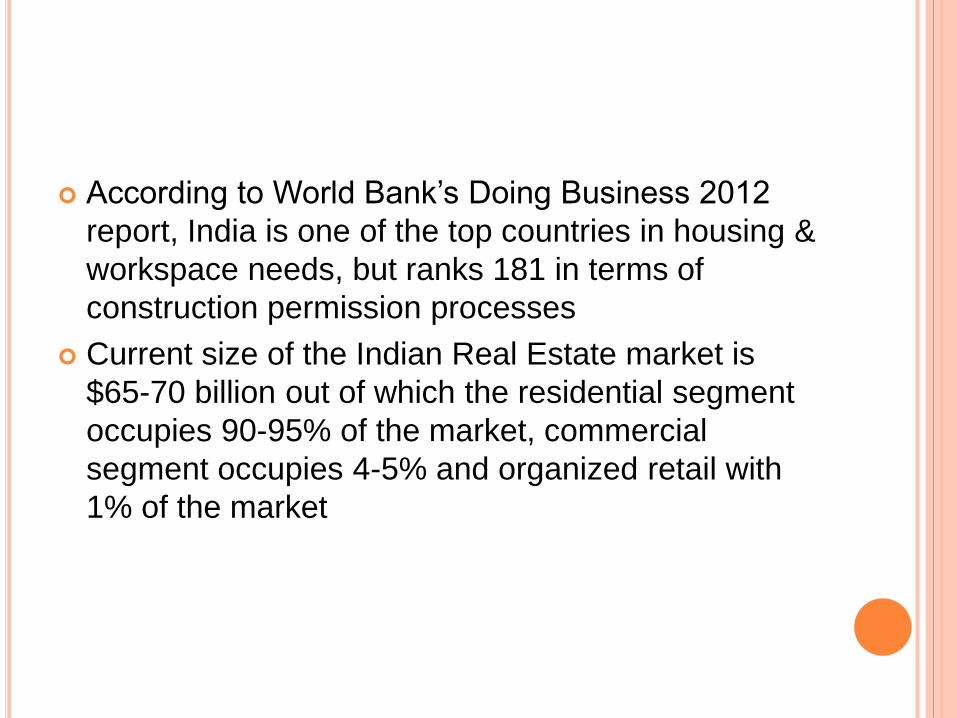

According to World Bank’s Doing Business 2012

report, India is one of the top countries in housing &

workspace needs, but ranks 181 in terms of

construction permission processes

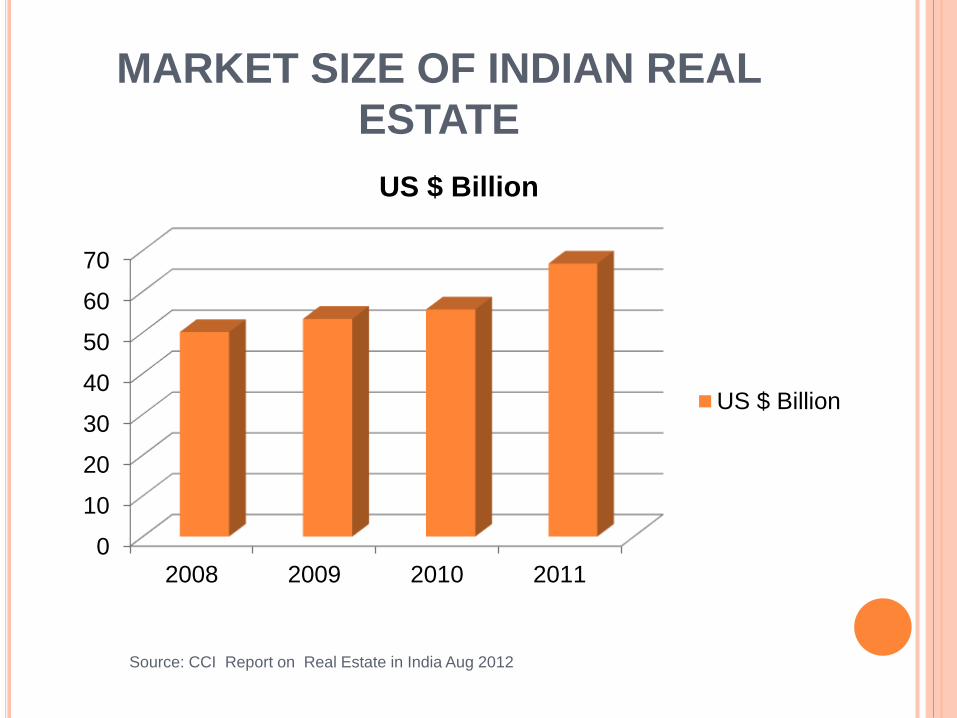

Current size of the Indian Real Estate market is

$65-70 billion out of which the residential segment

occupies 90-95% of the market, commercial

segment occupies 4-5% and organized retail with

1% of the market

GROWTH DRIVERS OF INDIAN REAL

ESTATE

Rapid urbanization

Significant rise in consumerism

Policy and Regulatory reforms (100% FDI

relaxation)

Surge in Industrial and Business Activities

Increasing demand for newer avenues for

entertainment, leisure and shopping

MARKET SIZE OF INDIAN REAL

ESTATE

0

10

20

30

40

50

60

70

2008 2009 2010 2011

US $ Billion

US $ Billion

Source: CCI Report on Real Estate in India Aug 2012

SEGMENTS OF REAL ESTATE

SECTOR IN INDIA

Residential

Commercial

Retail

Hospitality

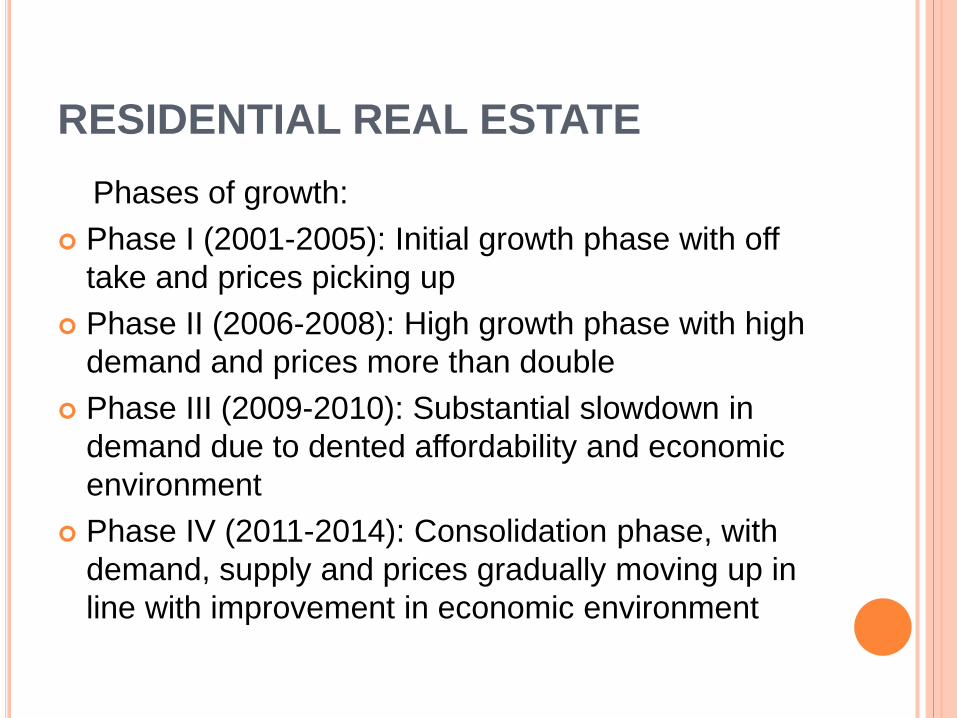

RESIDENTIAL REAL ESTATE

Phases of growth:

Phase I (2001-2005): Initial growth phase with off

take and prices picking up

Phase II (2006-2008): High growth phase with high

demand and prices more than double

Phase III (2009-2010): Substantial slowdown in

demand due to dented affordability and economic

environment

Phase IV (2011-2014): Consolidation phase, with

demand, supply and prices gradually moving up in

line with improvement in economic environment

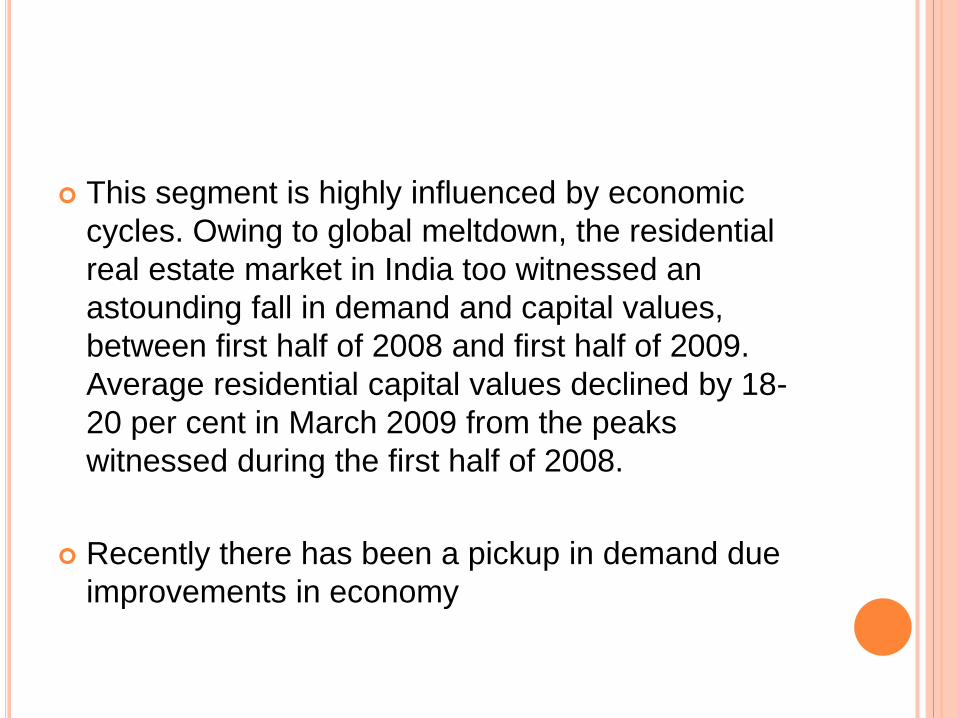

This segment is highly influenced by economic

cycles. Owing to global meltdown, the residential

real estate market in India too witnessed an

astounding fall in demand and capital values,

between first half of 2008 and first half of 2009.

Average residential capital values declined by 18-

20 per cent in March 2009 from the peaks

witnessed during the first half of 2008.

Recently there has been a pickup in demand due

improvements in economy

COMMERCIAL REAL ESTATE

The commercial real estate has been driven largely by the growth in service sectors, especially IT/ITeSand with this began movement from CBD’s (Central Business Districts) towards city suburbs.

Tax sops on the profits of IT-ITeS companies also led to massive development of IT Parks and SEZs (Special Economic Zones)

Demand for office space is directly linked to addition in number of employees, which in turn is dependent on economic growth. When economy slows down, companies hold their expansion plans leading to lower demand for office space.

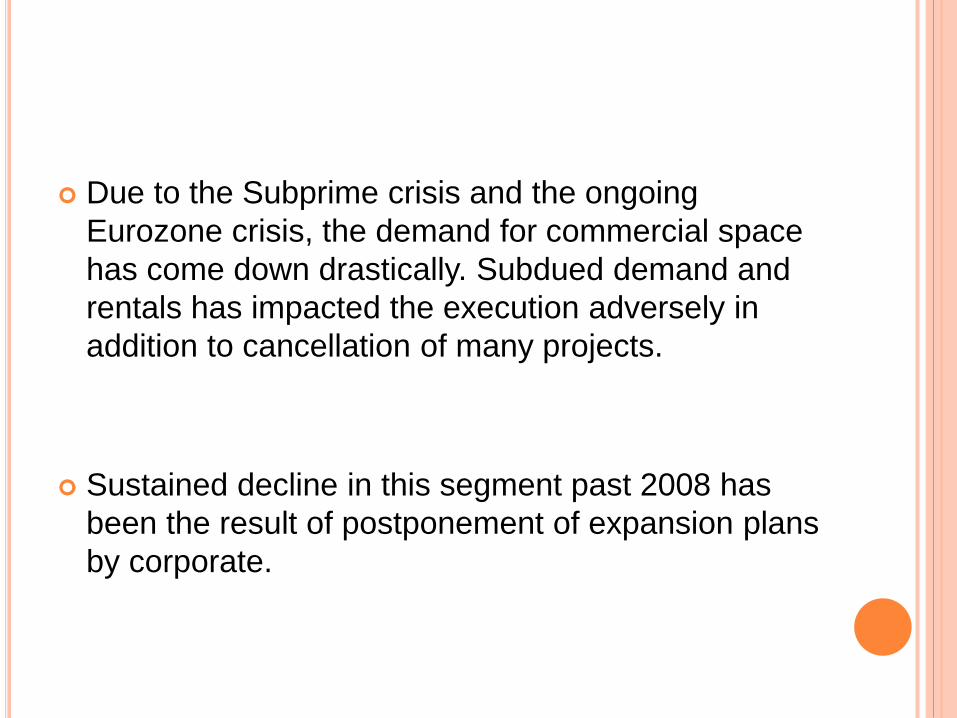

Due to the Subprime crisis and the ongoing

Eurozone crisis, the demand for commercial space

has come down drastically. Subdued demand and

rentals has impacted the execution adversely in

addition to cancellation of many projects.

Sustained decline in this segment past 2008 has

been the result of postponement of expansion plans

by corporate.

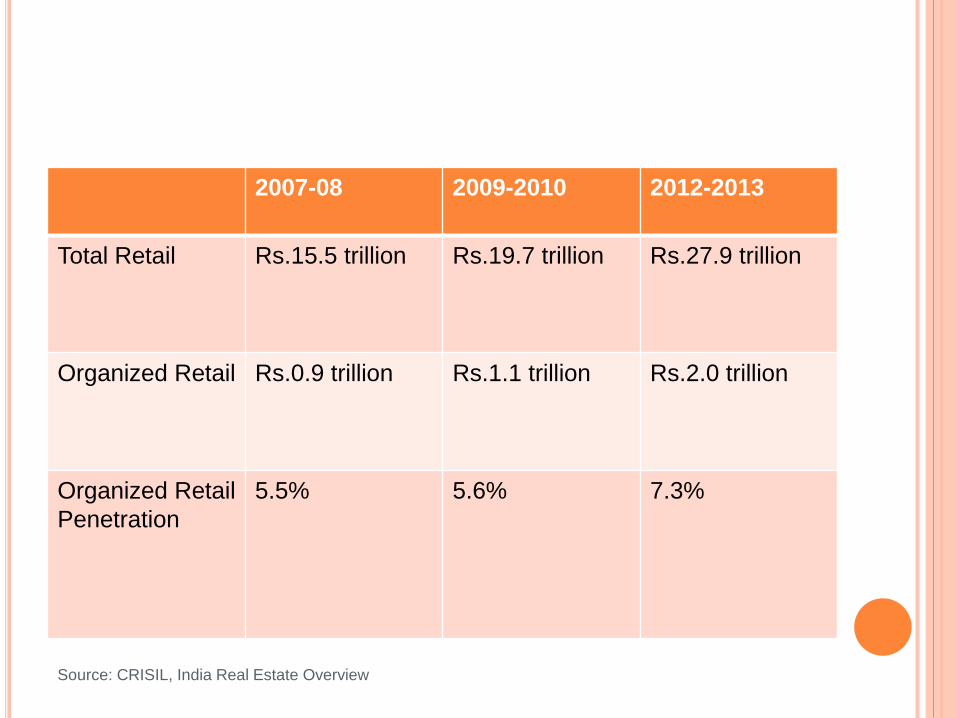

ORGANIZED RETAIL REAL ESTATE

The retail industry in India is in slowdown despite

attaining peaks of CAGR at 28% in the 2005-08

period. The industry is expected to increase at a

CAGR of 14% in the short term and 19% over the

next 5 years.

Organised retail penetration has grown to about

5.6% in 2009-10, which is further expected to

increase to about 7.3% by 2012-13.

Key driving factors for growth of this sector includes

lavish lifestyles, high disposable incomes and a

propensity to spend.

2007-08 2009-2010 2012-2013

Total Retail Rs.15.5 trillion Rs.19.7 trillion Rs.27.9 trillion

Organized Retail Rs.0.9 trillion Rs.1.1 trillion Rs.2.0 trillion

Organized Retail

Penetration

5.5% 5.6% 7.3%

Source: CRISIL, India Real Estate Overview

HOSPITALITY SECTOR REAL

ESTATE

Rising incomes, higher weekend trips and increased access to travel-related information over the Internet have propelled growth in hospitality.

From 2003-04 to 2010-11,the market size of the hotel sector has more than doubled from Rs 77.13 billion in 2003-04 to more than Rs 200 billion in 2008-09, registering an impressive CAGR of more than 15%

In 2008-09, the market size decreased by around 4 per cent due to decline in revenues. The hotel industry faced a fall in room demand due to the global financial crisis and the 26/11 terror attacks in Mumbai.

Demand is expected to increase at a CAGR of 15

per cent while room availability is expected to

record a CAGR of 9 per cent across premium

segments. Business destinations are poised to see

higher growth in room inventory compared to

leisure destinations.

KEY PLAYERS IN THE INDIAN REAL

ESTATE

DLF Ltd

1. Presence across 30 cities in India

2. Residential, townships, commercial complexes, IT

parks, hotels etc pan its project coverage

3. It is the only real estate company to be listed in

BSE Sensex, NSE Nifty, MSCI India Index and

MSCI Emerging Markets Asia Index

UNITECH

1. First developer to be certified ISO 9001

2. Offers diversified projects across residential,

commercial and IT parks, retail, hotels etc.

3. First real estate company to be listed in NSE Nifty

4. Has ventured into infrastructure business as

UNITECH Infra

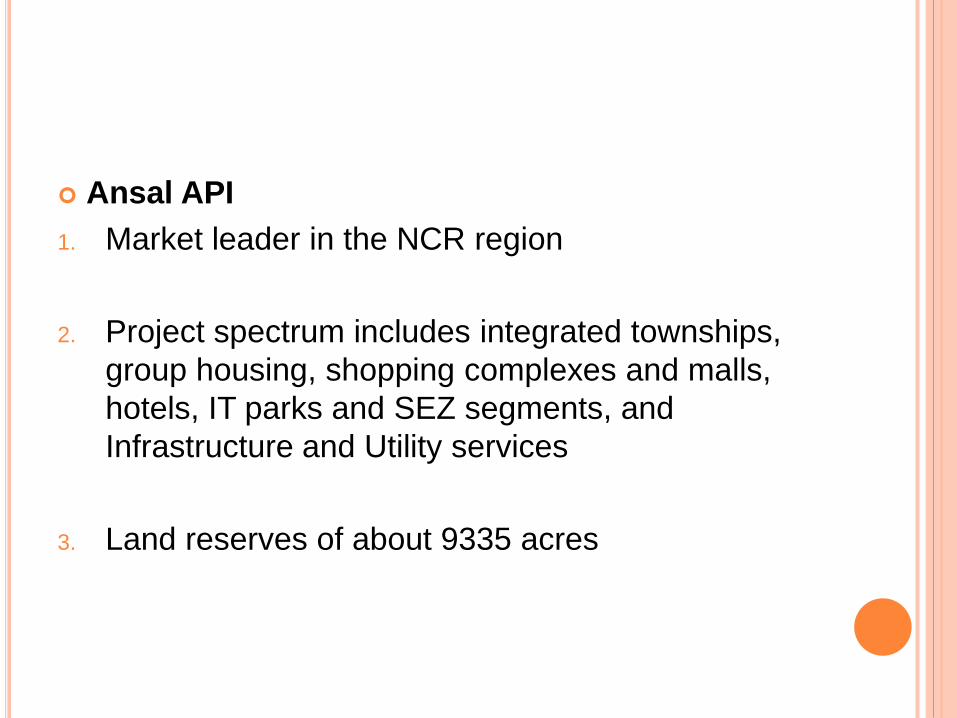

Ansal API

1. Market leader in the NCR region

2. Project spectrum includes integrated townships,

group housing, shopping complexes and malls,

hotels, IT parks and SEZ segments, and

Infrastructure and Utility services

3. Land reserves of about 9335 acres

SECTOR MARKET PERFORMANCE

(NSE)

The market trend in NSE for last 7, 15, 30 and 90

days can be obtained

In this presentation, there will be focus on top

gainers and losers over a period from 14th

September 2012 to 28th September 2012

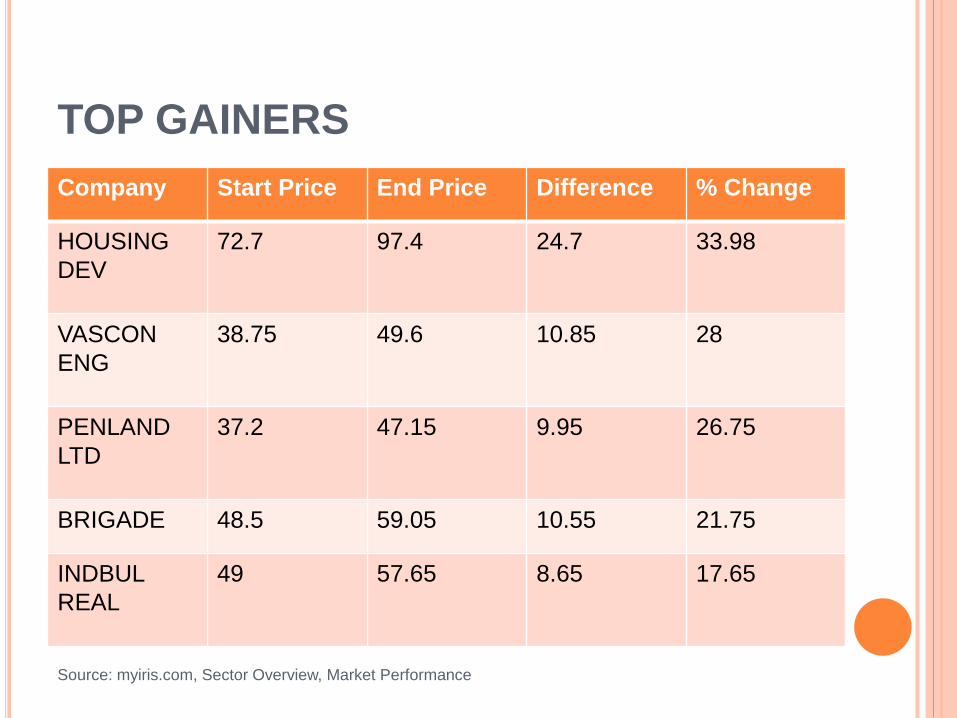

TOP GAINERS

Company Start Price End Price Difference % Change

HOUSING

DEV

72.7 97.4 24.7 33.98

VASCON

ENG

38.75 49.6 10.85 28

PENLAND

LTD

37.2 47.15 9.95 26.75

BRIGADE 48.5 59.05 10.55 21.75

INDBUL

REAL

49 57.65 8.65 17.65

Source: myiris.com, Sector Overview, Market Performance

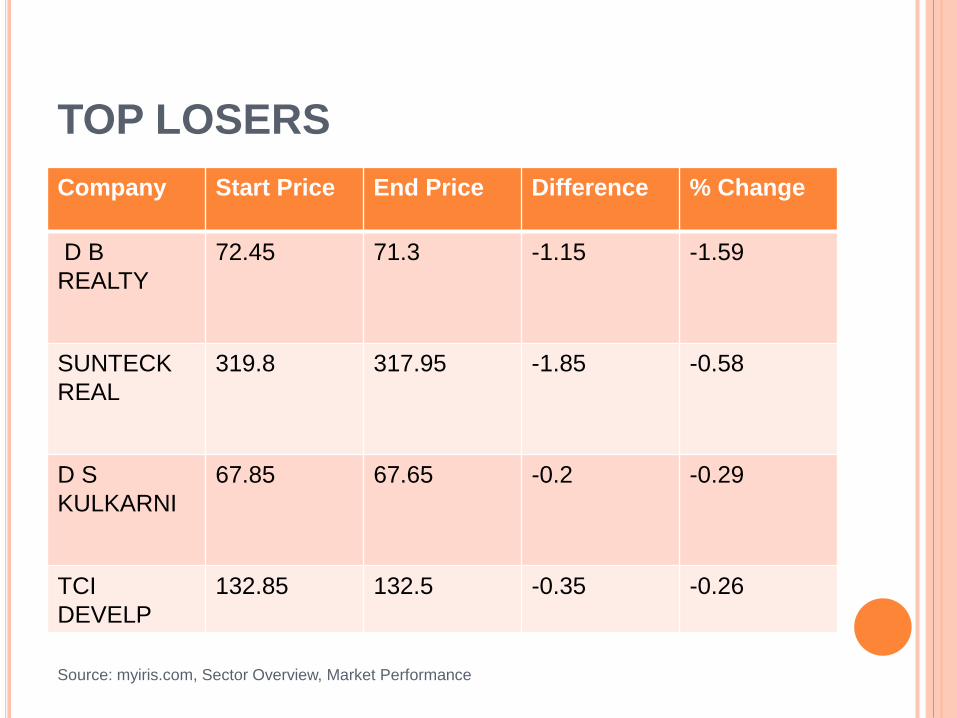

TOP LOSERS

Company Start Price End Price Difference % Change

D B

REALTY

72.45 71.3 -1.15 -1.59

SUNTECK

REAL

319.8 317.95 -1.85 -0.58

D S

KULKARNI

67.85 67.65 -0.2 -0.29

TCI

DEVELP

132.85 132.5 -0.35 -0.26

Source: myiris.com, Sector Overview, Market Performance

GLOBAL TRENDS

As per a report published by Scotiabank dated

September 14, 2012:

Among the international property markets tracked,

the number of countries reporting declining average

real prices on a year-over-year basis outnumbered

those reporting price increases by more than two to

one.

Weak consumer confidence, high unemployment

and tight credit conditions continue to weigh heavily

on housing demand and pricing.

Housing markets remain weakest in Europe, where

sharp fiscal austerity, rising unemployment and

financial sector strains are deepening recessionary

conditions.

In European countries that are financially sound,

there were some tentative signs of improvement.

The U.S. housing market is showing increasing

signs of recovery.

U.S. homeowner affordability, rising rental costs

and strengthening household formation are

contributing to the pickup in sales. Lower inventory

levels and a falling share of distressed property

sales also have contributed to the stabilization in

prices, though significant differences in local market

conditions persist.

An increasing number of cities in China are seeing

renewed home price appreciation. This is being

supported by an easing in monetary conditions .

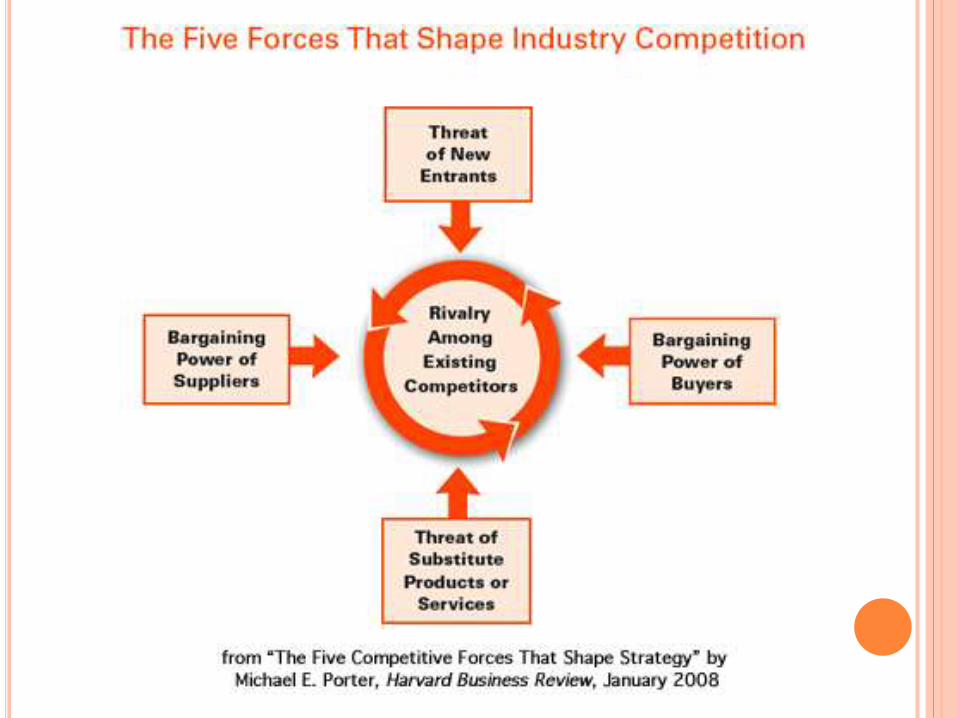

APPLICATION OF PORTER’S 5

FORCES MODEL TO INDIAN REAL

ESTATE

The analysis of 5 Forces model has been done to

determine whether the Indian Real Estate sector will

remain profitable in the years to come

It is important to consider the impact of the

Eurozone Crisis as well as the Subprime Crisis

THREAT OF NEW ENTRANTS

There will be decrease in profitability due to

increase in the number of entrants.

As a result of the economic downturn around the

globe, it has been difficult for the new entrants to

get a hold because of cost reduction in expansion

plans by corporates in real estate, little scope in

commercial construction, and strong rivalry

between existing firms.

Result: Relatively weak threat of new entrants

BARGAINING POWER OF BUYERS

Powerful customers are able to exert pressure to

drive down prices, or increase the required quality

for the same price, and therefore reduce profits in

an industry.

Customers significantly influence the business

operations in real estate.

Customers do possess a threat of integrating

backwards.

Consequently, the bargaining power of the buyers

is strong.

BARGAINING POWER OF SUPPLIERS

An important category of suppliers is the bank.

They have the power to decide whether to fund a

venture or not and at what rate.

Banks have now become highly conservative

especially after the economic downturn.

Are significantly affected by the monetary

regulations like the Repo rate & CRR formulated by

the Central Bank of the country. This is in turn

affects the real estate sector.

Consequently the bargaining power of suppliers is

very strong

THREAT OF SUBSTITUTE

PRODUCTS AND SERVICES

In real estate business, substitute might be some

type of totally new retail space, some new location

for office space or rehabilitation instead of new

construction.

The threat of substitute in real estate business and

its impact on profitability of the industry is quite

ambiguous and difficult to establish given the

economic downturns and the recovery mode of the

real estate business cycle.

RIVALRY AMONG EXISTING

COMPETITORS

Rivalry is strong due to the large no. of real estate

firms operating in India (65 in total) and the difficulty

to differentiate

The services offered by real estate companies

cannot be differentiated because these firms don’t

offer a product, other than the facilities they lease

and this itself is very difficult to quantify.

In the current economic crisis, there is minimal

profitability and only companies with large cash

reserves are likely to survive.

ANALYSIS

Considering all the 5 forces, it can be said that the

real estate industry is not very profitable at this

stage as it was before the subprime crisis of US in

2008

But considering the fact that the real estate cycle is

in the recovery stage right now and given that the

demand for real estate is growing at a CAGR of

19%, it can be said that there are still bright

prospects ahead in a country like India.

REFERENCES

(August 2012). Real Estate Sector in India. New Delhi: Competition Corporation of India (CCI)http://www.cci.in/pdf/surveys_reports/real-estate-sector-india.pdf

Warren, A. (September 14,2012). Global Real Estate Trends. Toronto: Scotia Bank http://www.gbm.scotiabank.com/English/bns_econ/retrends.pdf

Porter, M. E. (June 2002). Competitive Strategy and Real Estate Development. Harvard Business School , 9. http://www.isc.hbs.edu/Porter_Strategy_Real_Estate1.pdf

Dr.V.Chandrasekhar, G. S. (2011). Indicators of

Real Estate Cycle - Implication for India. ICREI, ISB

, 20.

THANK YOU