Embed Size (px)

Citation preview

A report from the Economist Intelligence Unit

Sponsored by

From mobile aspirations to business results

Thenewretail:

© The Economist Intelligence Unit Limited 20141

The new retail: From mobile aspirations to business results

Preface 2

Executive summary 3

Introduction: A shopping mall in the palm of everyone’s hand 4

Consumers lead, retailers sluggishly follow 6

Easier said than done: Moving from theory to practice 7

Commitment and execution 8

Focus on customer value 10

Conclusion 13

Appendix: Survey results 14

Contents

1

2

3

4

5

© The Economist Intelligence Unit Limited 20142

The new retail: From mobile aspirations to business results

About this report

The new retail: From mobile aspirations to business results is an Economist Intelligence Unit research report, sponsored by AT&T. Our thanks go to all survey respondents and interviewees for their time and insight.

The report was written by Peter Moustakerski and edited by Christine Emba. The findings and views expressed in the report do not necessarily reflect the views of the sponsor.

March 2014

The survey, conducted in September and October 2013, reached 156 respondents in the retail sector: 30% from North America, 29% from Asia-Pacific, 27% from Western Europe, 6% from the Middle East and Africa, 5% from Latin America and 3% from Eastern Europe. Respondents filled a variety of functional roles—40% were in general

management, while 15% were in finance, 12% in strategy and business development, and 11% in marketing and sales, among others. Twenty-six percent of respondents were CEOs, presidents, or managing directors, 16% were SVPs, VPs or Directors in Merchandising, and 33% were SVP, VP or Director-level in other roles.

Who took the survey?

© The Economist Intelligence Unit Limited 20143

The new retail: From mobile aspirations to business results

A proliferation of powerful and functionality-laden mobile devices has transformed the way that people live and function. The ubiquity of mobile devices has had a particularly strong impact on the retail sector, as customers and employees increasingly use and depend on their mobile devices throughout their shopping experience. This mobile penetration is transforming shopping behaviours, as well as how retailers define success.

In order to determine how retailers are responding to the rise in mobile-empowered consumers, The Economist Intelligence Unit, on behalf of AT&T, conducted a survey of over 150 global executives from around the world.

Key findings include:

l The mobile transformation is solidly under way in retail, and consumers are leading the charge. As of January 2014, 91% of Americans owned a mobile phone, and 55% had a smartphone. According to our survey, 39% of respondents say that customers use mobile devices “extensively” or ”often” while shopping. Thirty percent of respondents have seen major behavioural shifts in customers attributable to mobile device usage, while 25% have observed similar shifts in their employees.

l Integrating mobile is crucial to delivering a quality omni-channel experience. Deploying mobile devices and fostering a culture of usage and innovation are seen by 84% of retailers as important to a strong omni-channel experience. To do so effectively, however, retailers must be able to integrate their theoretical ambitions with practical execution. In our survey, respondents who perceive their companies as “practical” leaders or early adopters—those who not only aspire to use but actually adopt mobile technologies and integrate them throughout their company—are more likely to report above-average success across the board.

l The most effective mobile tools for retailers focus on consumer value. Consumers respond more favourably to sophisticated, narrowly targeted and higher-value-add tools, such as mobile coupons (75% of retailers believe they have generated a positive response from customers), geo-targeted advertisements and promotions (74%) and product search apps (72%). Retailers’ next generation of mobile technologies will be designed to address specific customer needs and pain points, integrate the customer experience across sales channels and create previously unexplored sales opportunities.

Executive summary

© The Economist Intelligence Unit Limited 20144

The new retail: From mobile aspirations to business results

Shortly after taking over as head of marketing at Max Brenner—a chain of chocolate-themed cafés and candy boutiques—Stacey Paul took note of one particular metric: as many as half of all users were accessing the company’s website on their mobile devices. However, the newly redesigned site did not have key mobile features such as pinch-and-zoom or swiping between pages. “We had to rethink our strategy,” says Ms Paul. “The world is quicker and smaller, and your life is now on mobile. Retailers need to answer that call.” Hence one of

her first decisions as the company’s top marketing executive was to redraw the website and optimise it for smartphones and tablets using the latest in mobile Internet design and functionality.

The growing digital retail turnover is increasingly happening on the go. The significant penetration of mobile devices into the lives of everyday consumers is transforming shopping behaviours. As Ms Paul points out, consumers’ daily activities are increasingly reliant on mobile phones and tablets—how they shop is no exception. According to the

Introduction: A shopping mall in the palm of everyone’s hand1

Q

Source: Economist Intelligence Unit survey, October 2013.

Strong impact

Moderate impact

Weak impact

No impact Don’t know/ Not applicable

Pre-purchase: Discovery and awareness

Pre-purchase: Decision to purchase

Pre-purchase: Comparison and selection

Purchase: Decision to upgrade/increase purchase

Purchase: Shopping experience

Post-purchase: Fulfilment and delivery experience

Post-purchase: After-sales service and support experience

Post-purchase: Decision to repeat purchases/customer loyalty and advocacy

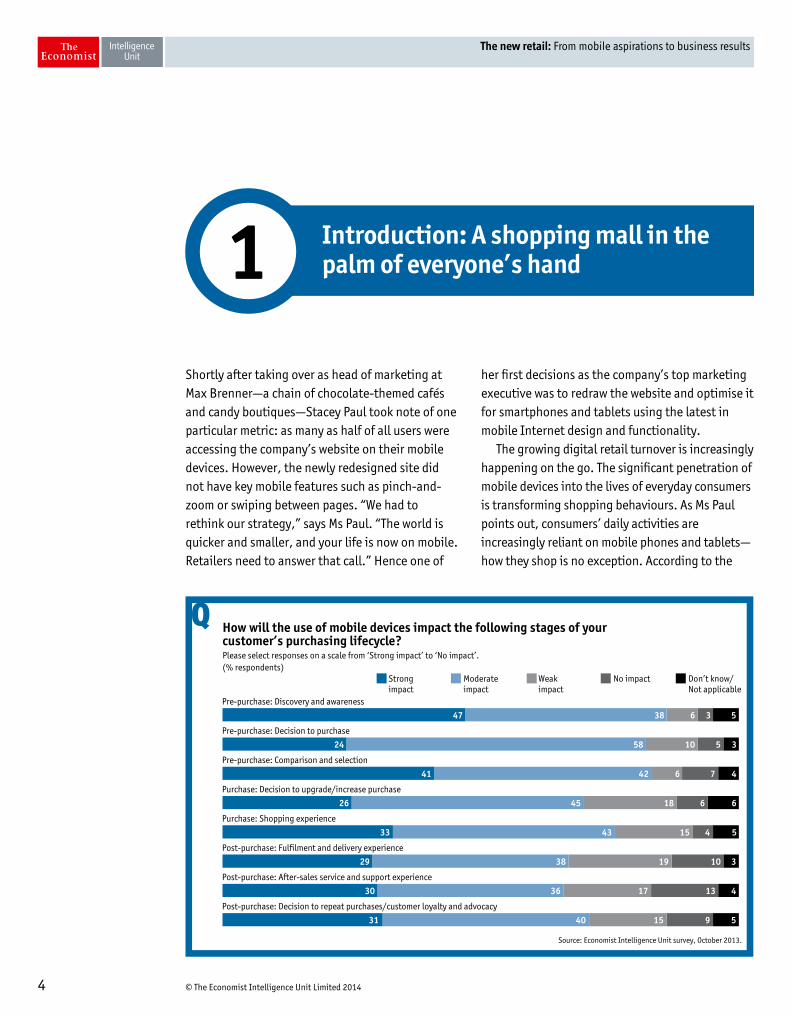

How will the use of mobile devices impact the following stages of your customer’s purchasing lifecycle? Please select responses on a scale from ‘Strong impact’ to ‘No impact’. (% respondents)

47 38 6 3 5

24 58 10 5 3

41 42 6 7 4

26 45 18 6 6

33 43 15 4 5

29 38 19 10 3

30 36 17 13 4

31 40 15 9 5

© The Economist Intelligence Unit Limited 20145

The new retail: From mobile aspirations to business results

Pew Research Center, a US think-tank, as of January 2014 91% of the US population carries a mobile phone, 55% have a smartphone and 42% own a tablet computer. Young people and wealthier, more-educated consumers are even more connected to their smart mobile devices—they do about one-quarter of their shopping online and one-third of them use their phones for online research when deciding whether to visit a brick-and-mortar store or a restaurant.

This mobile shopping trend is expected to accelerate—according to the 2014 Mobile 500 report published by Internet Retailer, mobile commerce in the US will grow 63% to reach US$34bn by the end of 2014, up from US$21bn in 2012. These trends are holding across retail industries, even in retail banking and brokerage.

“Today, 12% of our daily average revenue trades come through mobile,” says Paul Zettl, managing director of retail marketing and digital media at TD Ameritrade, a US online broker. Customers can use its mobile app from their smartphones or tablets to check balances, access investment research and place trade orders.

This rapid and on-going evolution has put large

amounts of information and powerful mobile-technology tools at the fingertips of ordinary people, resulting in the emergence of a culture that will forever transform how people plan and do their shopping. Results from an Economist Intelligence Unit (EIU) survey of more than 150 retail executives worldwide, conducted in October 2013, confirm that consumers are increasingly relying on their mobile devices during their shopping experiences—39% of respondents say that customers use them “extensively” or ”often” while shopping.

The growing prevalence of mobile devices is expected to affect every stage of retail shopping, though the awareness and comparison stages of a customer’s purchasing lifecycle should experience the greatest impact. Overall, mobile technologies will have a positive effect on customer engagement and key business metrics that matter to retailers’ business performance. Ultimately, mobile technologies are widely expected to benefit the two most important objectives for retail operators: profitability and customer experience. The trick for retail operators will be to transform their strategies to reap these benefits.

❛❛ The world is quicker and smaller, and your life is now on mobile. Retailers need to answer that call.❜❜Stacy Paul Head of marketing Max Brenner

© The Economist Intelligence Unit Limited 20146

The new retail: From mobile aspirations to business results

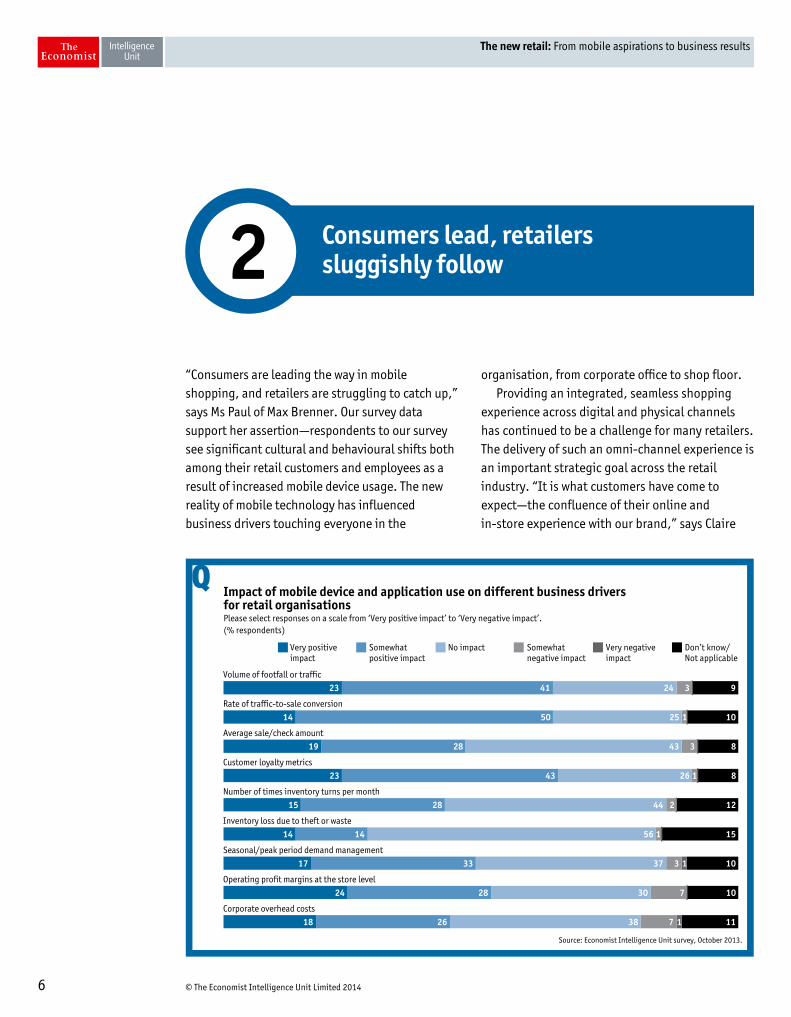

“Consumers are leading the way in mobile shopping, and retailers are struggling to catch up,” says Ms Paul of Max Brenner. Our survey data support her assertion—respondents to our survey see significant cultural and behavioural shifts both among their retail customers and employees as a result of increased mobile device usage. The new reality of mobile technology has influenced business drivers touching everyone in the

organisation, from corporate office to shop floor. Providing an integrated, seamless shopping

experience across digital and physical channels has continued to be a challenge for many retailers. The delivery of such an omni-channel experience is an important strategic goal across the retail industry. “It is what customers have come to expect—the confluence of their online and in-store experience with our brand,” says Claire

Consumers lead, retailers sluggishly follow2

Q

Source: Economist Intelligence Unit survey, October 2013.

Very positive impact

Somewhat positive impact

No impact Somewhat negative impact

Very negative impact

Don’t know/ Not applicable

Volume of footfall or traffic

Rate of traffic-to-sale conversion

Average sale/check amount

Customer loyalty metrics

Number of times inventory turns per month

Inventory loss due to theft or waste

Seasonal/peak period demand management

Operating profit margins at the store level

Corporate overhead costs

Impact of mobile device and application use on different business drivers for retail organisations Please select responses on a scale from ‘Very positive impact’ to ‘Very negative impact’. (% respondents)

23 41 24 3 9

14 50 25 1 10

19 28 43 3 8

23 43 26 1 8

15 28 44 2 12

14 14 56 1 15

17 33 37 3 1 10

24 28 30 7 10

18 26 38 7 1 11

© The Economist Intelligence Unit Limited 20147

The new retail: From mobile aspirations to business results

Chambers, founder and CEO of Journelle, an upscale lingerie retailer in the US.

Yet many retailers still struggle with the challenge of co-ordinating customer experiences across channels, and many haven’t been completely successful. Twenty-four percent of EIU survey respondents rate their company’s success in

creating an omni-channel experience as “somewhat” or “well below average” compared with that of their peers.

Why are many retailers failing to realise their omni-channel goals or even catch up with the rest of the field? What separates the organisations that succeed from the rest of the pack?

In our survey, we analysed two levels at which companies embrace mobile technology: “theoretical”, which reflects the leadership’s stance and the company’s stated position with regard to using mobile technology to achieve its strategic goals, and “practical”, which reflects the organisation’s actual use of mobile devices and apps to serve customers.

Our data show a strong connection between a retailer being either a theoretical or a practical leader in embracing mobile technologies and successfully implementing an omni-channel strategy—respondents who see their companies as frontrunners in the mobile space (either in theory or practice) are much more likely to report that

they are enjoying above-average success creating a high-quality omni-channel experience.

More than one-third of our survey respondents believe that their company is a theoretical leader—that is, their company and its leadership team have a positive, encouraging attitude towards the use of mobile devices to engage customers and drive business results. At the same time, however, actual use of these technologies tends to lag behind the operators’ theoretical aspirations.

This gap between theory and practice highlights both the challenge and the opportunity for retailers as they transform themselves into omni-channel players, and underlines the need for the strategies that we describe below.

Easier said than done: Moving from theory to practice

Source: Economist Intelligence Unit survey, October 2013.

Success by “practical” and “theoretical” mobile technology leaders in creating an omni-channel experience, compared with that of industry peers (% respondents)

Well above average

Somewhat above average

Average/On par with peers

Somewhat below average

Well below average

We do not focus on the development of an omni-channel experience

“Theoretical” leaders and early adopters “Practical” leaders and early adopters

36 34

36 39

27 27

00

00

20

© The Economist Intelligence Unit Limited 20148

The new retail: From mobile aspirations to business results

Commitment and execution3

Market leaders excel at motivating and mobilising their workforce to create an in-house app culture of their own.

For many retailers, in-store sales still dominate their revenues; thus, investing in the development of new digital channels may seem less urgent. Such thinking leads to a lack of top-down leadership commitment to new mobile channels, which in turn affects the buy-in of the rest of the organisation. In addition, mobile channels still account for a relatively small portion of revenues, and the cost of developing and maintaining a high-quality omni-channel experience can be significant.

“Merging the information from different databases is a real challenge,” says Ms Chambers of Journelle. “Customers expect to walk into your store and pick up merchandise that they placed in their online cart the day before. But we can’t see what’s in their online cart, and sometimes don’t even stock the same merchandise in our stores.”

If retailers are to succeed as omni-channel players, they must meet two challenges. First, they

have to develop the leadership commitment—the theoretical aspiration—to use mobile technologies across sales channels to achieve their strategic goals.

Second, they need to find the focus and stamina—the practical execution capabilities—to follow through on their commitment and complete the complex tasks required to transform themselves into omni-channel operators. These tasks include integrating information from multiple systems and databases, co-ordinating marketing content across customer touch-points and revamping operations to support product merchandising and fulfilment across different channels.

In our survey, respondents who perceive their companies as “practical” leaders or early adopters—those who not only aspire to adopt but also actually go forward to adopt mobile technologies and apps—are more likely to report above-average success across the board.

Q

Source: Economist Intelligence Unit survey, October 2013.

To what extent has the use of mobile devices and applications led to a cultural and behavioural shift at your organisation in the past 3 years? (% respondents)

Major change

Moderate change

Minor change

No change

“Practical” leaders and early adopters Followers

52 16

41 47

5 29

2 6

© The Economist Intelligence Unit Limited 20149

The new retail: From mobile aspirations to business results

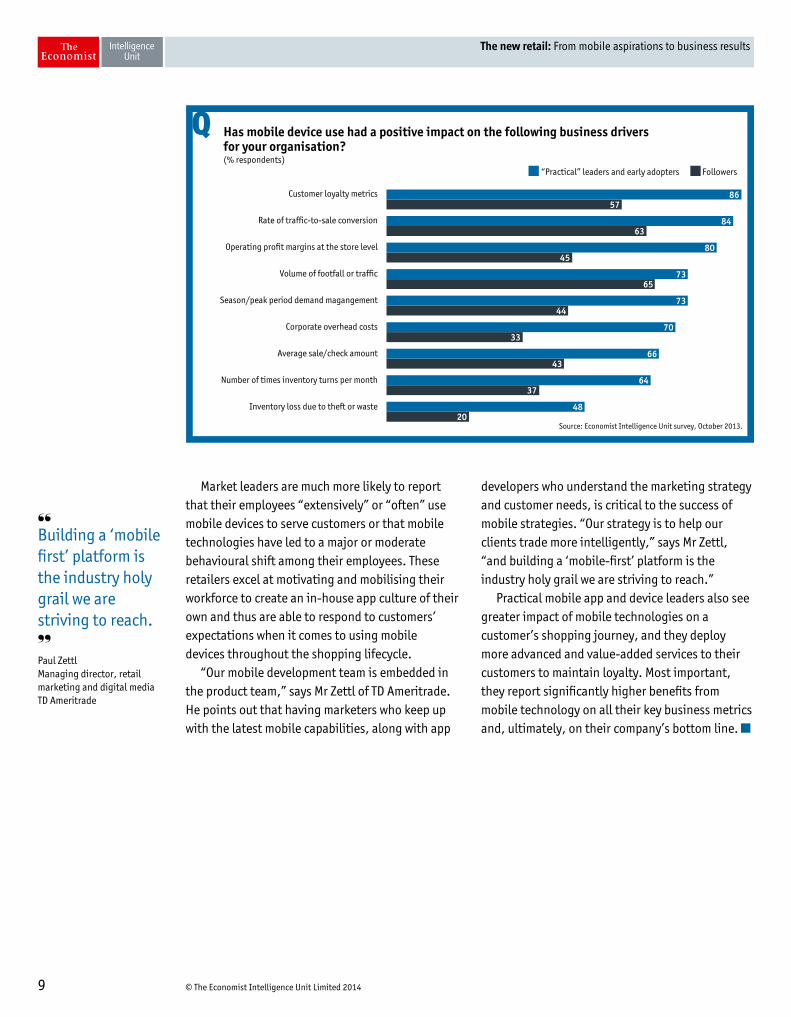

Market leaders are much more likely to report that their employees “extensively” or “often” use mobile devices to serve customers or that mobile technologies have led to a major or moderate behavioural shift among their employees. These retailers excel at motivating and mobilising their workforce to create an in-house app culture of their own and thus are able to respond to customers’ expectations when it comes to using mobile devices throughout the shopping lifecycle.

“Our mobile development team is embedded in the product team,” says Mr Zettl of TD Ameritrade. He points out that having marketers who keep up with the latest mobile capabilities, along with app

developers who understand the marketing strategy and customer needs, is critical to the success of mobile strategies. “Our strategy is to help our clients trade more intelligently,” says Mr Zettl, “and building a ‘mobile-first’ platform is the industry holy grail we are striving to reach.”

Practical mobile app and device leaders also see greater impact of mobile technologies on a customer’s shopping journey, and they deploy more advanced and value-added services to their customers to maintain loyalty. Most important, they report significantly higher benefits from mobile technology on all their key business metrics and, ultimately, on their company’s bottom line.

Q

Source: Economist Intelligence Unit survey, October 2013.

Has mobile device use had a positive impact on the following business drivers for your organisation? (% respondents)

Customer loyalty metrics

Rate of traffic-to-sale conversion

Operating profit margins at the store level

Volume of footfall or traffic

Season/peak period demand magangement

Corporate overhead costs

Average sale/check amount

Number of times inventory turns per month

Inventory loss due to theft or waste

“Practical” leaders and early adopters Followers

86 57

84 63

80 45

73 65

73 44

70 33

66 43

64 37

48 20

❛❛ Building a ‘mobile first’ platform is the industry holy grail we are striving to reach.❜❜Paul Zettl Managing director, retail marketing and digital media TD Ameritrade

© The Economist Intelligence Unit Limited 201410

The new retail: From mobile aspirations to business results

The second dimension that underpins the omni-channel success of leaders goes beyond whether they have the commitment and capabilities to adopt and use the latest mobile technology tools. Rather it matters what they do with these technologies and how well they deploy them to solve pressing customer problems.

The widespread penetration of mobile devices and the proliferation of free or low-cost mobile applications have presented consumers with a plethora of tools designed to address their slightest need. The realm of consumer retail

shopping in particular has been flooded with tools and applications that target every step of the purchasing process. Most, if not all, are aimed at making parting with cash anytime and anywhere as easy—and even fun— as possible for consumers.

The mobile tools most widely deployed by retailers today tend to focus on one primary sales channel rather than functioning across channels. The most common tools include a company-branded mobile website or app (used by 65% of total survey respondents.) and social media software (53%).

The next generation of mobile tools will be

Focus on customer value4

Q

Source: Economist Intelligence Unit survey, October 2013.

Which of the following mobile device technologies and applications are currently used by your company to serve your customers? (% respondents)

Company-branded mobile app/website

Customer WiFi

Social media software (eg, monitoring, engagement and analytics)

Big data analytics (eg, WiFi/Cellular)

Mobile point-of-sale/payment

Click & reserve functionality

Digital signage and in-store communications

Customer collaboration solutions (eg, customer profile, live chat/support)

Self-serve kiosks

“Practical” leaders and early adopters Followers

82 66

80 54

52 56

68 51

61 40

73 27

55 29

50 28

50 24

© The Economist Intelligence Unit Limited 201411

The new retail: From mobile aspirations to business results

designed to address specific customer needs and pain points, integrate the customer experience across sales channels and create previously unexplored sales opportunities. The Nieman Marcus mobile app, for example, combines customer service and collaboration with store staff. The luxury retailer’s app allows customers to bookmark certain items and then connect by e-mail, text or phone with sales staff in a nearby store.

“Mobile customers behave differently from shoppers who are online or in a physical store,” says Ms Paul. “They have less time and are acting with a specific purpose in mind.” Thus customers expect mobile apps to be simple, easy to navigate and geared towards achieving a specific, relevant objective.

Industry leaders and early adopters listen to pressing customer needs and respond with simple, user-friendly and useful apps and services. US retailer Wal-Mart, for example, realised that some of its recession-hit customers had smartphones and wanted to shop online, but did not have credit cards with which to place orders. To allow these customers to use their preferred channel, Wal-Mart began to let customers place orders online and

then come into a bricks-and-mortar outlet to make payment in cash.

“Following the customers to where they want to go is key,” says Ms Chambers of Journelle, “and giving them a valuable service, such as pulling up their past purchasing history or the ability to pick up or return in the store goods they purchased online.”

This distinction between mobile leaders and followers is evident in our survey results—leaders are much more likely to offer their customers click-and-reserve capabilities or use mobile point-of-sale payment systems.

For instance, US supermarket chain ShopRite is testing a mobile app that allows customers to scan items on their smartphones as they place them in their shopping carts and then use their phone to check out, thereby bypassing crowded checkout lanes.

Among mobile marketing tools, the most common are e-mail communication, social media integration and text messaging. Yet these traditional digital methods are not necessarily the most effective way to reach new customers or cement existing relationships. When asked about consumers’ response to different mobile marketing

Q

Source: Economist Intelligence Unit survey, October 2013.

Which of the following mobile marketing tools and strategies do you currently utilise to engage your customers? (% respondents)

Email communication

Social media integration

Text messaging/SMS

Store locator apps

Product search apps

Geo-targeted advertisement and promotions

QR codes

Mobile coupons

Mobile shopping card/payment apps

Mobile video advertisements

“Practical” leaders and early adopters Followers

82 81

70 64

80 57

77 49

75 45

66 41

70 38

68 32

48 16

41 15

❛❛ Following the customers to where they want to go is key.❜❜Claire Chambers Founder and CEO Journelle

© The Economist Intelligence Unit Limited 201412

The new retail: From mobile aspirations to business results

tools, EIU survey participants rate e-mail and text messaging as least appealing.

More sophisticated mobile marketing tools such as geo-targeted promotions (used by 45% of survey respondents) and mobile coupons (39%) are also gaining ground and tend to generate greater customer engagement.

The Hijack app by Guatemalan footwear retailer Meatpack uses GPS technology to detect when users are in competitors’ stores. Customers receive a message with a discount that starts at 99% and drops by 1% every second, meaning that the faster customers arrive at a Meatpack retail store, the higher a discount they will receive. In addition to generating significant marketing buzz, the app reportedly “hijacked” 600 customers in a single week.

Consumers respond more favourably to such

sophisticated, narrowly targeted and higher-value-add tools. According to participants in our survey, mobile coupons are most welcome, followed by geo-targeted advertisements and promotions, and product search-and-compare apps.

And when it comes to marketing tools, industry leaders in mobile deployment are much more adept at using high-value-add tools such as store locator apps, QR codes and geo-targeted ads and promotions.

“Targeting is key,” says Ms Paul. “Your marketing message can’t be broad anymore, which is why geo-targeting is a must—it’s expected.” Best-in-class mobile tools provide both the speed and convenience mobile consumers crave, as well as content and interactions that are specifically targeted to their preferences and thus relevant to their needs.

❛❛ Targeting is key. Your message can’t be broad anymore. ❜❜Stacey Paul Head of Marketing Max Brenner

© The Economist Intelligence Unit Limited 201413

The new retail: From mobile aspirations to business results

Mobile technology will continue to play an increasing role in improving the consumer retail experience and unlocking new revenue opportunities for retailers. For the foreseeable future, consumers will likely set the speed, direction and expectations of the app culture revolution and retailers will do their best to keep pace and realise the business benefits.

Accordingly, retailers will need to rethink their strategies to incorporate and prioritise the new mobile channels. They will need to communicate these new attitudes both internally and externally, and mobilise their leadership and rank-and-file employees to execute the transformational initiatives that will lay the groundwork for their

omni-channel success. In-store employees will be especially critical to this transformation. Companies should enable those on the front lines with the necessary tools and training to develop a supply-side culture that meets the new needs of an increasingly mobile-savvy consumer.

Finally, retailers will need to become far better listeners to their customers. Rather than taking a one-size-fits-all approach, they must navigate the clutter of apps and tools now available and prioritise those that address specific needs and problems—such as convenience, speed of transaction, individually tailored offerings and promotions—if they are to remain fresh, relevant and indispensable in the minds and hearts of consumers.

Conclusion5

© The Economist Intelligence Unit Limited 201414

The new retail: From mobile aspirations to business results

Appendix: Survey results

Percentages may not add to 100% owing to rounding or the ability of respondents to choose multiple responses.

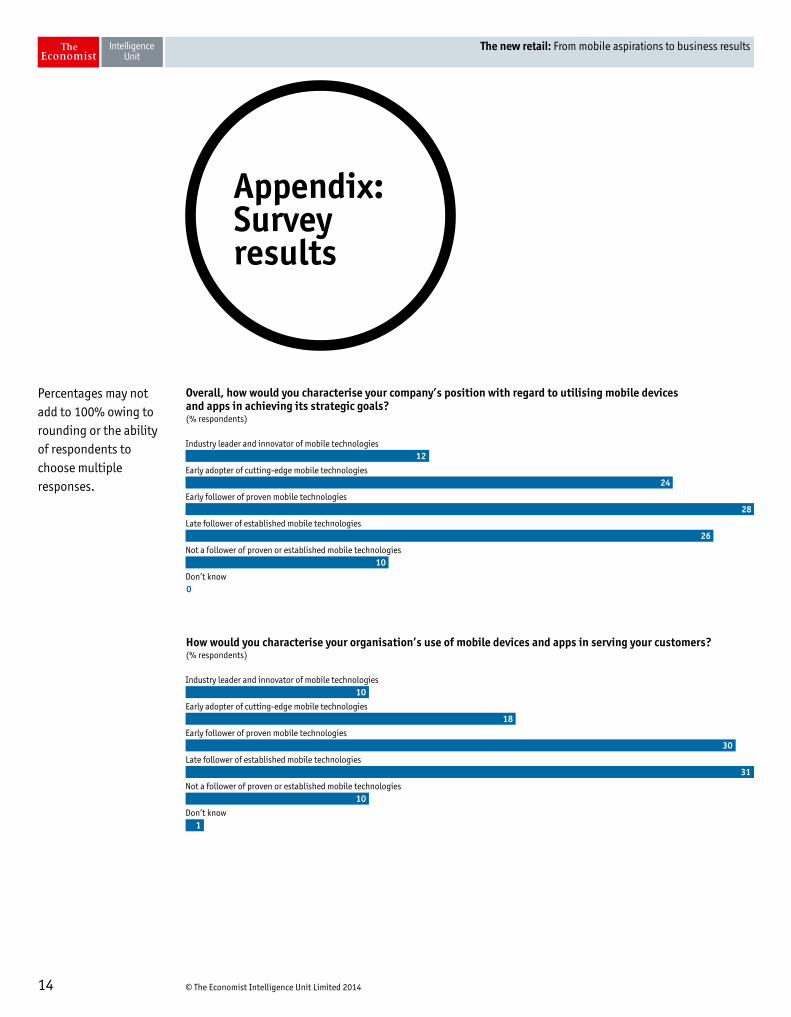

Overall, how would you characterise your company’s position with regard to utilising mobile devices and apps in achieving its strategic goals? (% respondents)

Industry leader and innovator of mobile technologies

Early adopter of cutting-edge mobile technologies

Early follower of proven mobile technologies

Late follower of established mobile technologies

Not a follower of proven or established mobile technologies

Don’t know

12

24

28

26

10

0

How would you characterise your organisation’s use of mobile devices and apps in serving your customers? (% respondents)

Industry leader and innovator of mobile technologies

Early adopter of cutting-edge mobile technologies

Early follower of proven mobile technologies

Late follower of established mobile technologies

Not a follower of proven or established mobile technologies

Don’t know

10

18

30

31

10

1

© The Economist Intelligence Unit Limited 201415

The new retail: From mobile aspirations to business results

To what extent are your employees using mobile devices and apps to serve their customers throughout their shopping journey? (% respondents)

Extensively/always

Often

Sometimes

Rarely

Not at all

Don’t know/Not applicable

16

25

34

18

6

1

To what extent are your customers using mobile devices and apps to fulfil their shopping missions at your retail stores? (% respondents)

Extensively/always

Often

Sometimes

Rarely

Not at all

Don’t know/Not applicable

10

28

36

18

4

4

Major change

Moderate change

Minor change

No change Don’t know

Cultural shift among your employees

Cultural shift among your customers

Behavioural shift among your employees

Behavioural shift among your customers

In your opinion, to what extent has the use of mobile devices and applications led to a cultural and behavioural shift at your organisation in the past 3 years? Please select responses on a scale from ‘Major change’ to ‘No change’. (% respondents)

28 42 21 8 1

27 42 21 8 2

25 42 22 8 2

30 35 27 5 3

© The Economist Intelligence Unit Limited 201416

The new retail: From mobile aspirations to business results

Major change

Moderate change

Minor change

No change Don’t know

Cultural shift among your employees

Cultural shift among your customers

Behavioural shift among your employees

Behavioural shift among your customers

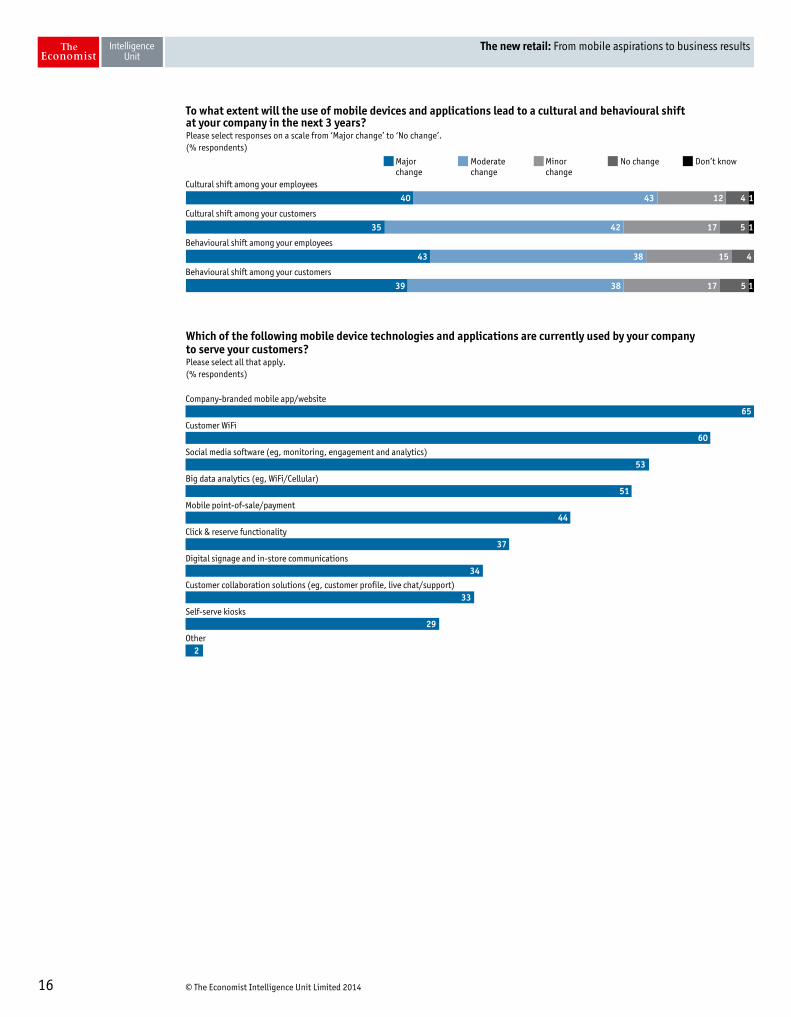

To what extent will the use of mobile devices and applications lead to a cultural and behavioural shift at your company in the next 3 years? Please select responses on a scale from ‘Major change’ to ‘No change’. (% respondents)

40 43 12 4 1

35 42 17 5 1

43 38 15 4

39 38 17 5 1

Which of the following mobile device technologies and applications are currently used by your company to serve your customers? Please select all that apply. (% respondents)

Company-branded mobile app/website

Customer WiFi

Social media software (eg, monitoring, engagement and analytics)

Big data analytics (eg, WiFi/Cellular)

Mobile point-of-sale/payment

Click & reserve functionality

Digital signage and in-store communications

Customer collaboration solutions (eg, customer profile, live chat/support)

Self-serve kiosks

Other

65

60

53

51

44

37

34

33

29

2

© The Economist Intelligence Unit Limited 201417

The new retail: From mobile aspirations to business results

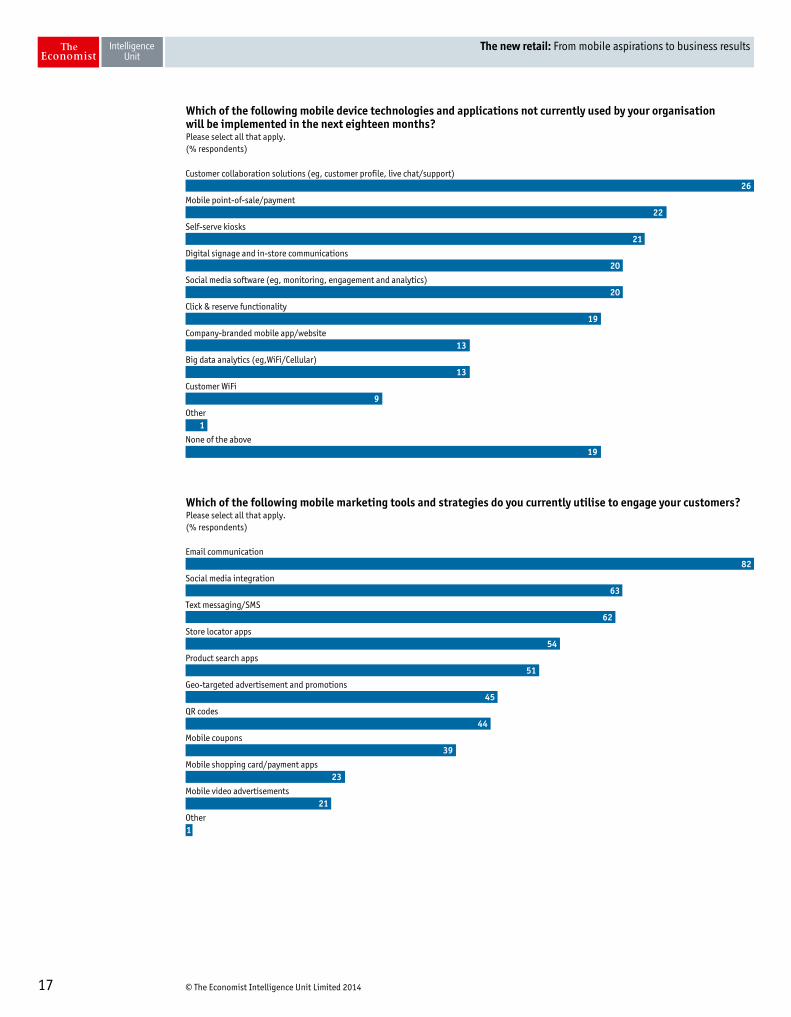

Which of the following mobile device technologies and applications not currently used by your organisation will be implemented in the next eighteen months? Please select all that apply. (% respondents)

Customer collaboration solutions (eg, customer profile, live chat/support)

Mobile point-of-sale/payment

Self-serve kiosks

Digital signage and in-store communications

Social media software (eg, monitoring, engagement and analytics)

Click & reserve functionality

Company-branded mobile app/website

Big data analytics (eg,WiFi/Cellular)

Customer WiFi

Other

None of the above

26

22

21

20

20

19

13

13

9

1

19

Which of the following mobile marketing tools and strategies do you currently utilise to engage your customers? Please select all that apply. (% respondents)

Email communication

Social media integration

Text messaging/SMS

Store locator apps

Product search apps

Geo-targeted advertisement and promotions

QR codes

Mobile coupons

Mobile shopping card/payment apps

Mobile video advertisements

Other

82

63

62

54

51

45

44

39

23

21

1

© The Economist Intelligence Unit Limited 201418

The new retail: From mobile aspirations to business results

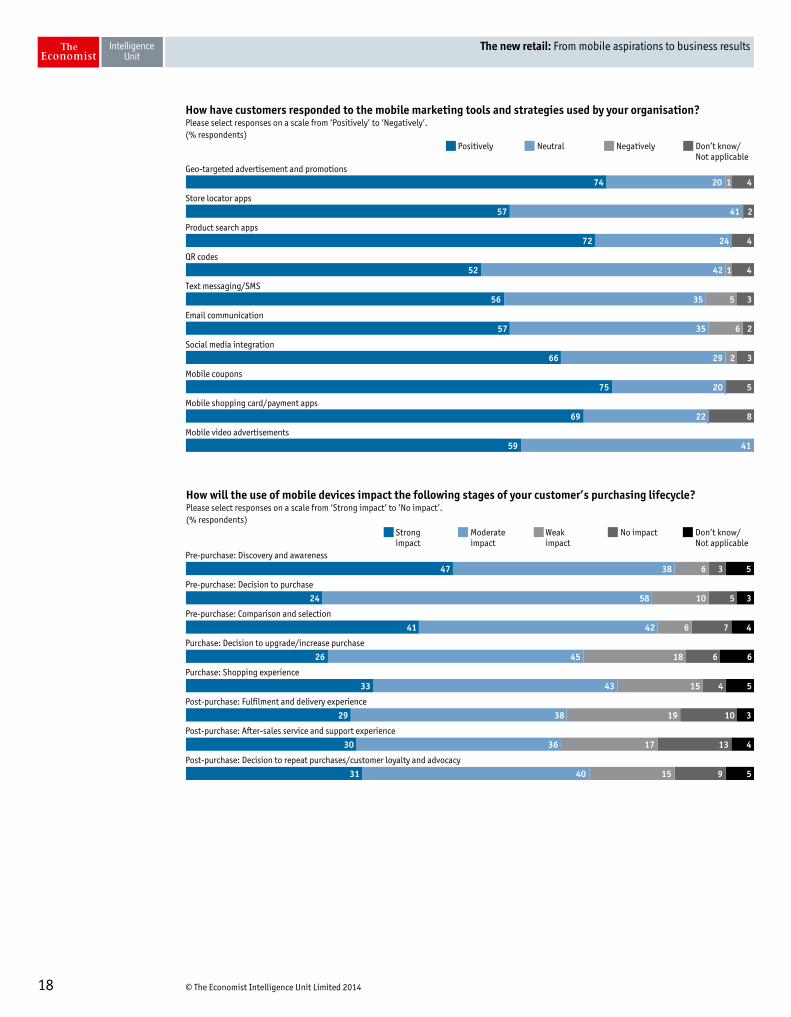

Positively Neutral Negatively Don’t know/ Not applicable

Geo-targeted advertisement and promotions

Store locator apps

Product search apps

QR codes

Text messaging/SMS

Email communication

Social media integration

Mobile coupons

Mobile shopping card/payment apps

Mobile video advertisements

How have customers responded to the mobile marketing tools and strategies used by your organisation? Please select responses on a scale from ‘Positively’ to ‘Negatively’. (% respondents)

74 20 1 4

57 41 2

72 24 4

52 42 1 4

56 35 5 3

57 35 6 2

66 29 2 3

75 20 5

69 22 8

59 41

Strong impact

Moderate impact

Weak impact

No impact Don’t know/ Not applicable

Pre-purchase: Discovery and awareness

Pre-purchase: Decision to purchase

Pre-purchase: Comparison and selection

Purchase: Decision to upgrade/increase purchase

Purchase: Shopping experience

Post-purchase: Fulfilment and delivery experience

Post-purchase: After-sales service and support experience

Post-purchase: Decision to repeat purchases/customer loyalty and advocacy

How will the use of mobile devices impact the following stages of your customer’s purchasing lifecycle? Please select responses on a scale from ‘Strong impact’ to ‘No impact’. (% respondents)

47 38 6 3 5

24 58 10 5 3

41 42 6 7 4

26 45 18 6 6

33 43 15 4 5

29 38 19 10 3

30 36 17 13 4

31 40 15 9 5

© The Economist Intelligence Unit Limited 201419

The new retail: From mobile aspirations to business results

How would you rate your company’s success in creating an omni-channel experience compared with that of your industry peers? (% respondents)

Well above average

Somewhat above average

Average/On par with peers

Somewhat below average

Well below average

We do not focus on the development of an omni-channel experience

14

29

28

19

5

6

In your opinion, how important is the deployment of mobile devices and apps to the creation of an omni-channel experience? (% respondents)

Highly important

Moderately important

Minimally important

Not important at all

Don’t know

47

37

10

1

4

Very positive impact

Somewhat positive impact

No impact Somewhat negative impact

Very negative impact

Don’t know/ Not applicable

Volume of footfall or traffic

Rate of traffic-to-sale conversion

Average sale/check amount

Customer loyalty metrics

Number of times inventory turns per month

Inventory loss due to theft or waste

Seasonal/peak period demand management

Operating profit margins at the store level

Corporate overhead costs

What impact has the use of mobile devices and apps had on the following business drivers for your organisation? Please select responses on a scale from ‘Very positive impact’ to ‘Very negative impact’. (% respondents)

23 41 24 3 9

14 50 25 1 10

19 28 43 3 8

23 43 26 1 8

15 28 44 2 12

14 14 56 1 15

17 33 37 3 1 10

24 28 30 7 10

18 26 38 7 1 11

© The Economist Intelligence Unit Limited 201420

The new retail: From mobile aspirations to business results

Positive effect

No effect Negative effect

Don’t know/ Not applicable

Your company’s bottom line

Your customers’ shopping experience

In your opinion, over the next 3 years, will the use of mobile devices and apps have a positive or negative effect on your company’s bottom line and your customer’s experience? Please select responses on a scale from ‘Positive effect’ to ‘Negative effect’. (% respondents)

75 18 3 5

82 14 1 3

Please select the retail sub-sector your company belongs to. Select the one response that best reflects the classification of your company. (% respondents)

General merchandiser

Department store

Supermarket

Superstore/discounter

Convenience store

Specialty retailer: footwear and apparel

Specialty retailer: personal care or health and beauty merchandise

Specialty retailer: household goods

Specialty retailer: home improvement merchandise

Specialty retailer: consumer electronics

Other specialty retailer

Catalogue or online retailer

Other retailer

8

8

8

1

3

17

8

6

5

5

13

7

9

In which country are you personally located? (% respondents)

United States of America

United Kingdom

Singapore

Australia, China, India, Japan, South Korea

Brazil, Germany, Italy, Romania, Spain

Canada, France, Saudi Arabia, United Arab Emirates

Argentina, Denmark, Hong Kong, Switzerland, Austria, Belgium, Finland, Ghana, Ireland, Israel, Kenya, Latvia, Lithuania, Malaysia, Mexico, Poland, Portugal, South Africa, Sweden, Taiwan, Turkey

28

8

5

4

3

2

1

North America

Asia-Pacific

Western Europe

Middle East and Africa

Latin America

Eastern Europe

In which region are you personally located?(% respondents)

30

29

27

6

5

3

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your organisation’s global annual revenues in US dollars?(% respondents)

52

15

17

6

10

© The Economist Intelligence Unit Limited 201421

The new retail: From mobile aspirations to business results

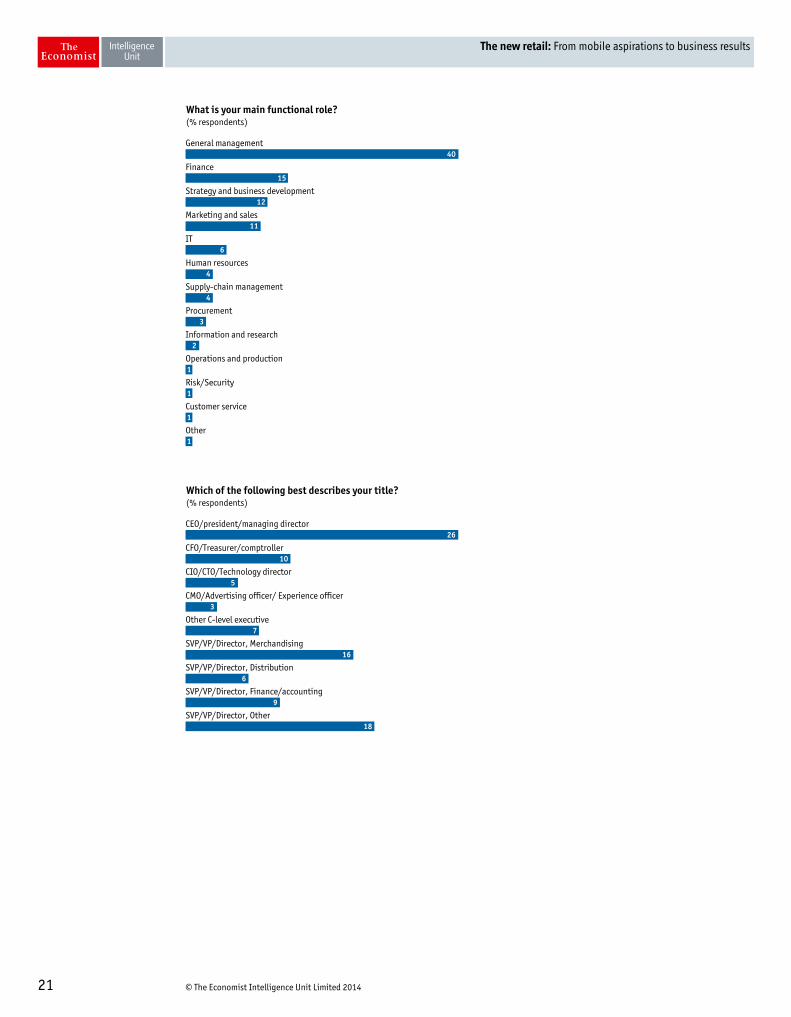

General management

Finance

Strategy and business development

Marketing and sales

IT

Human resources

Supply-chain management

Procurement

Information and research

Operations and production

Risk/Security

Customer service

Other

What is your main functional role?(% respondents)

40

15

12

11

6

4

4

3

2

1

1

1

1

CEO/president/managing director

CFO/Treasurer/comptroller

CIO/CTO/Technology director

CMO/Advertising officer/ Experience officer

Other C-level executive

SVP/VP/Director, Merchandising

SVP/VP/Director, Distribution

SVP/VP/Director, Finance/accounting

SVP/VP/Director, Other

Which of the following best describes your title?(% respondents)

26

10

5

3

7

16

6

9

18

© The Economist Intelligence Unit Limited 201422

The new retail: From mobile aspirations to business results

Whilst every effort has been taken to verify the accuracy of this

information, neither The Economist Intelligence Unit Ltd. nor the

sponsor of this report can accept any responsibility or liability

for reliance by any person on this white paper or any of the

information, opinions or conclusions set out in the white paper.

Cove

r: S

hutt

erst

ock

London20 Cabot SquareLondon E14 4QWUnited KingdomTel: (44.20) 7576 8000Fax: (44.20) 7576 8476E-mail: [email protected]

New York750 Third Avenue5th FloorNew York, NY 10017United StatesTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

Hong Kong6001, Central Plaza18 Harbour RoadWanchai Hong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

GenevaBoulevard des Tranchées 161206 GenevaSwitzerlandTel: (41) 22 566 2470Fax: (41) 22 346 93 47E-mail: [email protected]