Embed Size (px)

Citation preview

Confidential and Proprietary

DECODING ACA: IRS REPORTING AND SUBSIDY MANAGEMENT

1

Presented by Equifax Workforce Solutions

© 2015

, Equ

ifax

Confidential and Proprietary

2

Housekeeping

Slides will be emailed to you after the presentation All phones have been placed on mute Please submit questions using via the GotoWebinar console Participation in polling questions and follow-up survey is appreciated!

© 2015

, Equ

ifax

Confidential and Proprietary

Introductions

Kristin Lewis David Seifert

© 2015

, Equ

ifax

Confidential and Proprietary

4

Setting the Stage: ACA and IRS Reporting 101 Reporting & Compliance Deep-Dive Data Collection and Management Form Preparation and Distribution Subsidy Notifications and Appeals

Tackling IRS Reporting Q&A

Session Agenda

© 2015

, Equ

ifax

Confidential and Proprietary

SETTING THE STAGE ACA and IRS Reporting 101

© 2015

, Equ

ifax

Confidential and Proprietary

6

I would rate my organization’s current readiness for ACA compliance and reporting as…

a) Beginner b) Intermediate c) Expert d) Not sure e) I plead the 5th

Polling Question

© 2015

, Equ

ifax

Confidential and Proprietary

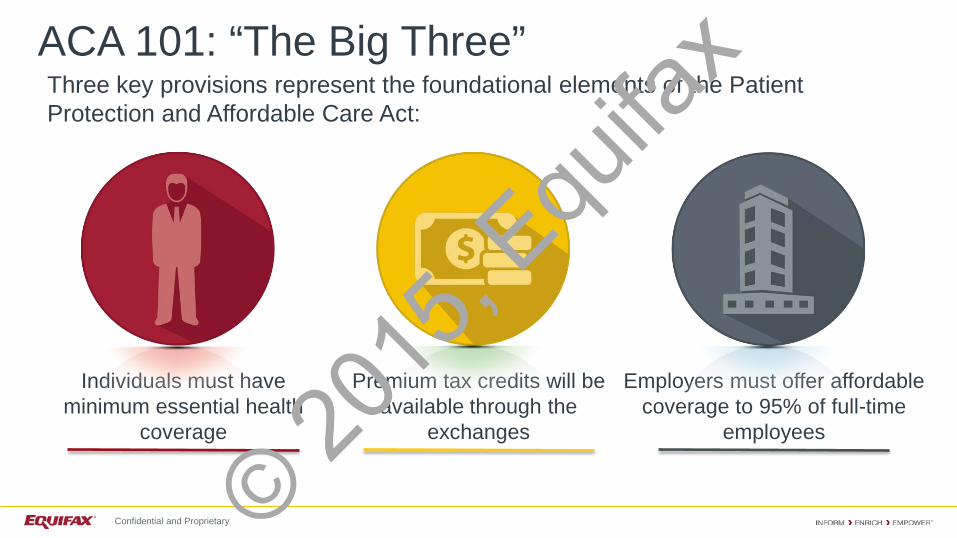

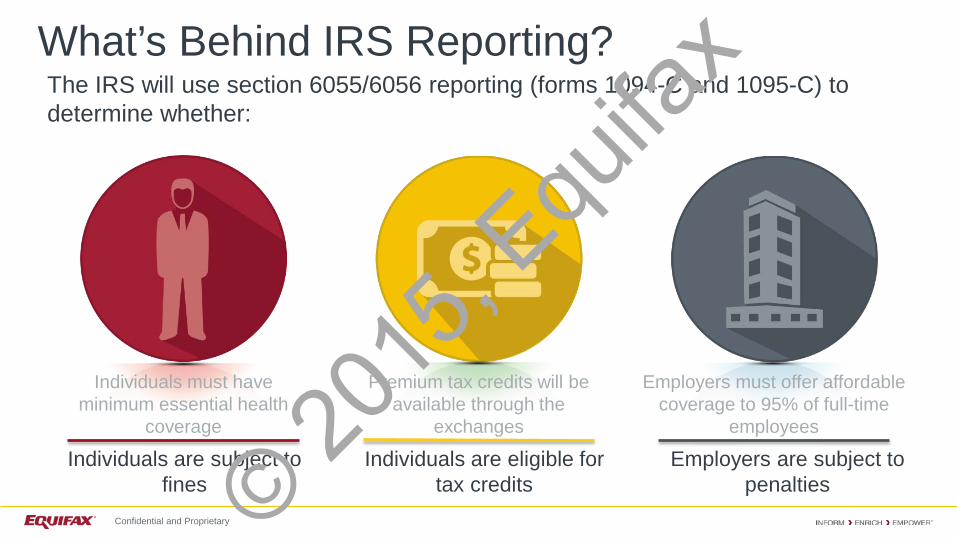

Individuals must have minimum essential health

coverage

Premium tax credits will be available through the

exchanges

Employers must offer affordable coverage to 95% of full-time

employees

ACA 101: “The Big Three” Three key provisions represent the foundational elements of the Patient Protection and Affordable Care Act:

© 2015

, Equ

ifax

Confidential and Proprietary

Individuals must have minimum essential health

coverage

Premium tax credits will be available through the

exchanges

Employers must offer affordable coverage to 95% of full-time

employees

What’s Behind IRS Reporting?

Individuals are subject to fines

Individuals are eligible for tax credits

Employers are subject to penalties

The IRS will use section 6055/6056 reporting (forms 1094-C and 1095-C) to determine whether:

© 2015

, Equ

ifax

Confidential and Proprietary

9

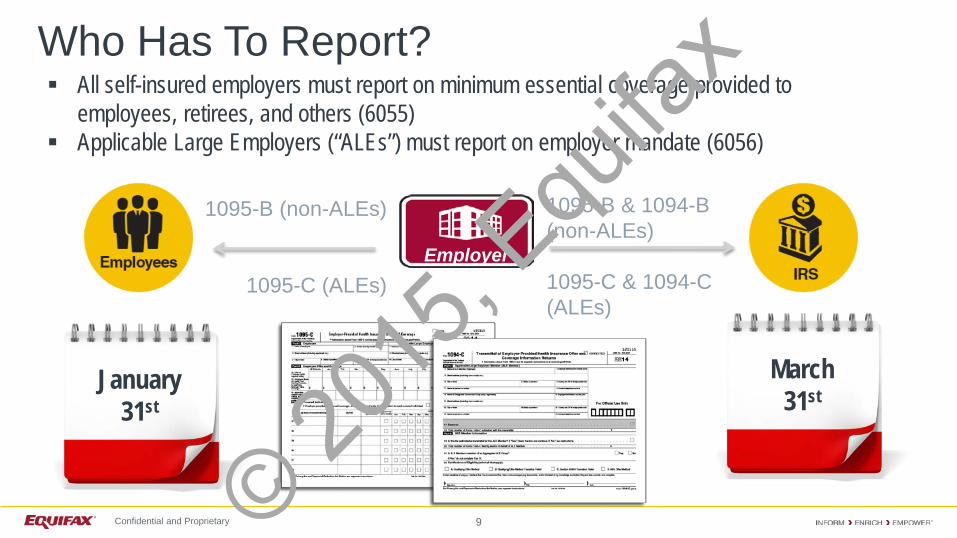

Who Has To Report?

Employer

1095-B (non-ALEs)

1095-C (ALEs)

1095-B & 1094-B (non-ALEs) 1095-C & 1094-C (ALEs)

All self-insured employers must report on minimum essential coverage provided to employees, retirees, and others (6055)

Applicable Large Employers (“ALEs”) must report on employer mandate (6056)

March 31st

January 31st

© 2015

, Equ

ifax

Confidential and Proprietary

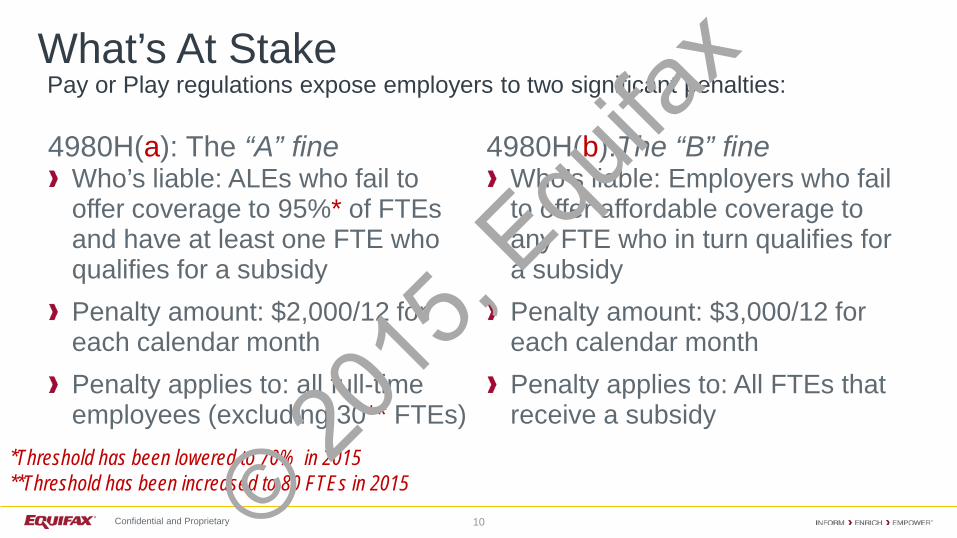

4980H(a): The “A” fine Who’s liable: ALEs who fail to offer coverage to 95%* of FTEs and have at least one FTE who qualifies for a subsidy Penalty amount: $2,000/12 for each calendar month Penalty applies to: all full-time employees (excluding 30** FTEs)

4980H(b):The “B” fine Who’s liable: Employers who fail to offer affordable coverage to any FTE who in turn qualifies for a subsidy Penalty amount: $3,000/12 for each calendar month Penalty applies to: All FTEs that receive a subsidy

10

What’s At Stake

*Threshold has been lowered to 70% in 2015 **Threshold has been increased to 80 FTEs in 2015

Pay or Play regulations expose employers to two significant penalties:

© 2015

, Equ

ifax

Confidential and Proprietary

11

ACA Is More Than Just Reporting Employers are at the epicenter of a challenging and complex compliance ecosystem.

© 2015

, Equ

ifax

Confidential and Proprietary

REPORTING AND COMPLIANCE DEEP-DIVE

Data Collection and Management Form Preparation and Distribution Subsidy Notifications and Appeals

© 2015

, Equ

ifax

Confidential and Proprietary

13

Which of the following data sources is not required to properly prepare forms 1094-C and 1095-C?

Payroll HRIS Benefits Absence Management Time and Attendance

Compliance Readiness Question #1

© 2015

, Equ

ifax

Confidential and Proprietary

14

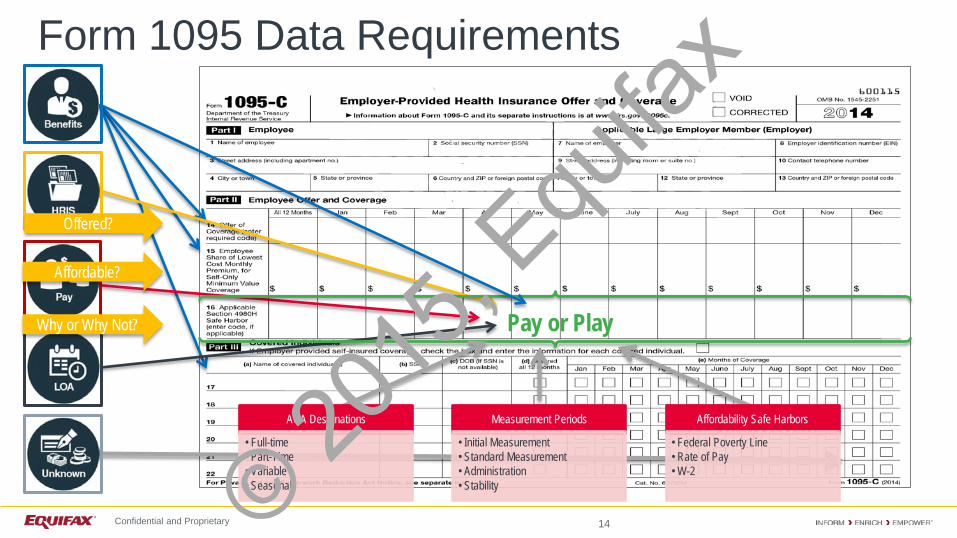

Form 1095 Data Requirements

Pay or Play

ACA Designations

• Full-time • Part-Time • Variable • Seasonal

Measurement Periods

• Initial Measurement • Standard Measurement • Administration • Stability

Affordability Safe Harbors

• Federal Poverty Line • Rate of Pay • W-2

Affordable?

Offered?

Why or Why Not?

© 2015

, Equ

ifax

Confidential and Proprietary

15

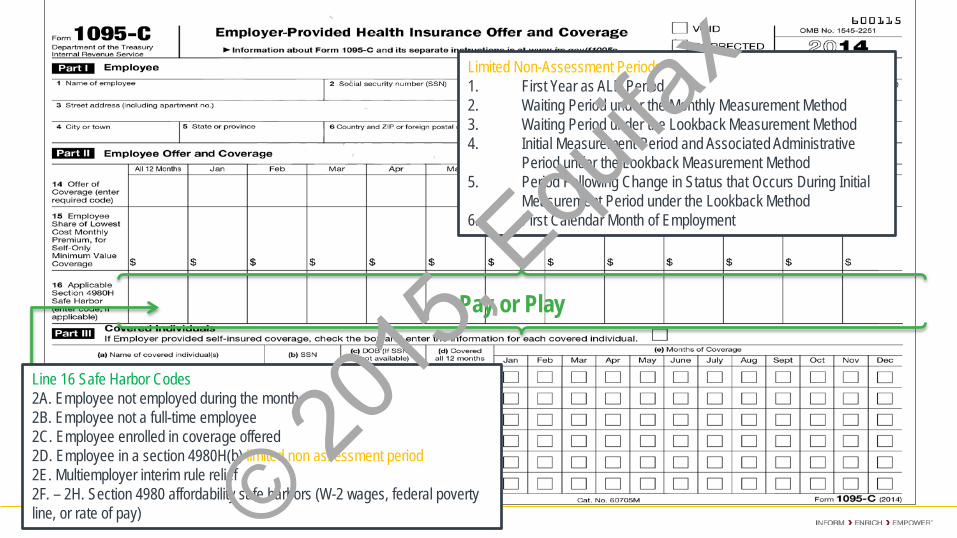

Limited Non-Assessment Periods 1. First Year as ALE Period 2. Waiting Period under the Monthly Measurement Method 3. Waiting Period under the Lookback Measurement Method 4. Initial Measurement Period and Associated Administrative

Period under the Lookback Measurement Method 5. Period Following Change in Status that Occurs During Initial

Measurement Period under the Lookback Method 6. First Calendar Month of Employment

Pay or Play

Line 16 Safe Harbor Codes 2A. Employee not employed during the month 2B. Employee not a full-time employee 2C. Employee enrolled in coverage offered 2D. Employee in a section 4980H(b) limited non assessment period 2E. Multiemployer interim rule relief 2F. – 2H. Section 4980 affordability safe harbors (W-2 wages, federal poverty line, or rate of pay) © 20

15, E

quifa

x

Confidential and Proprietary

16

Don’t wait! Your data is not getting cleaner on its own…don’t let data quality issues

stop you from getting started Identifying important factors such as special unpaid leave or

reclassifications will be difficult to incorporate retroactively

Establish clear ownership and accountability Internal resources processes, and systems External vendors/solutions

The devil is in the details Start date, overlapping pay periods, breaks in service, permissible

categories

Best Practices for Data Management

© 2015

, Equ

ifax

Confidential and Proprietary

REPORTING AND COMPLIANCE DEEP-DIVE

Data Collection and Management Form Preparation and Distribution Subsidy Notifications and Appeals

© 2015

, Equ

ifax

Confidential and Proprietary

18

A self-insured ALE is not responsible for providing form 1095-C to:

Employees that were full-time for at least one

calendar month Employees that enrolled in coverage for at

least one calendar month Retirees COBRA participants Dependents

Compliance Readiness Question #2

© 2015

, Equ

ifax

Confidential and Proprietary

19

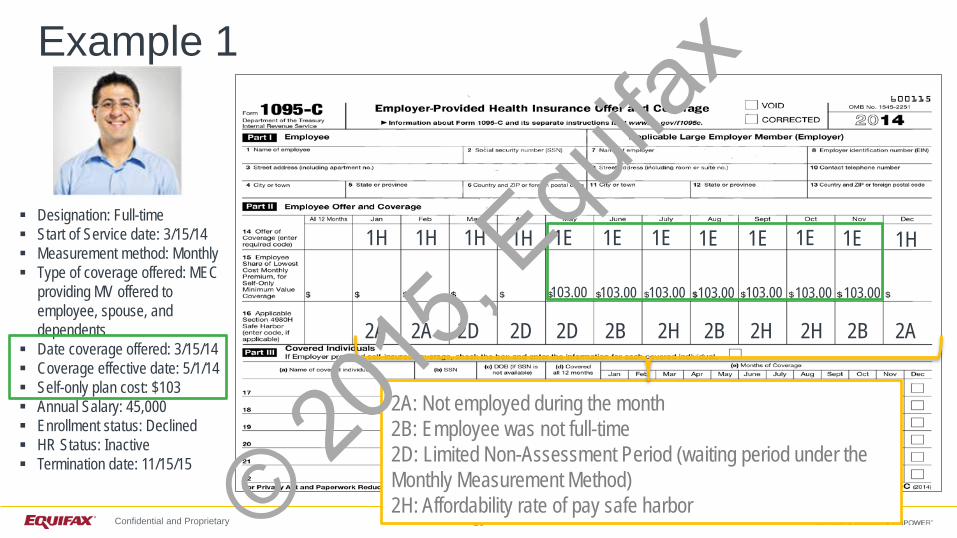

Designation: Full-time Start of Service date: 3/15/14 Measurement method: Monthly Type of coverage offered: MEC

providing MV offered to employee, spouse, and dependents

Date coverage offered: 3/15/14 Coverage effective date: 5/1/14 Self-only plan cost: $103 Annual Salary: 45,000 Enrollment status: Declined HR Status: Inactive Termination date: 11/15/15

Example 1

1E 1E 1E 1E 1E 1E 1E

103.00 103.00 103.00 103.00 103.00 103.00 103.00

2A 2A 2D 2D 2D 2B

1H 1H 1H 1H

2H 2B 2H 2H 2B 2A

1H

2A: Not employed during the month 2B: Employee was not full-time 2D: Limited Non-Assessment Period (waiting period under the Monthly Measurement Method) 2H: Affordability rate of pay safe harbor © 2015

, Equ

ifax

Confidential and Proprietary

20

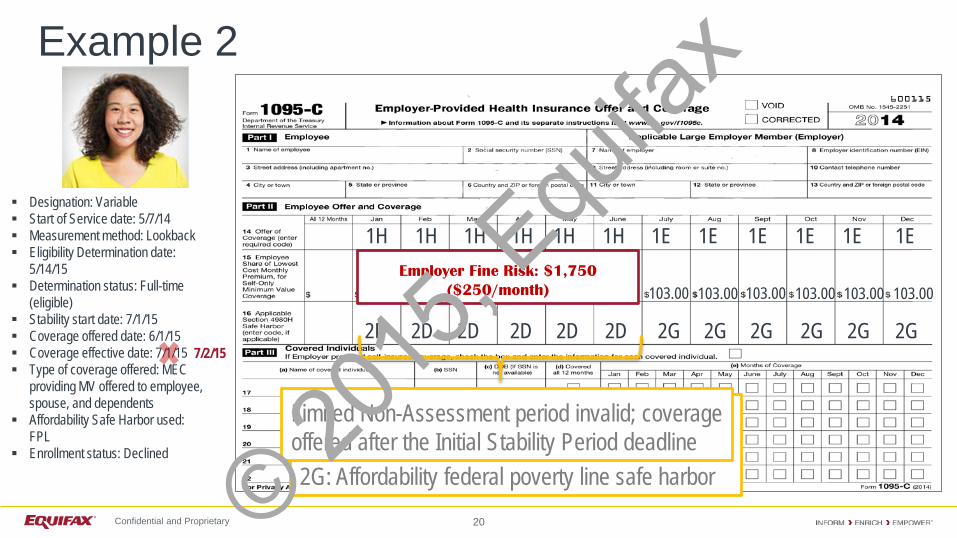

Designation: Variable Start of Service date: 5/7/14 Measurement method: Lookback Eligibility Determination date:

5/14/15 Determination status: Full-time

(eligible) Stability start date: 7/1/15 Coverage offered date: 6/1/15 Coverage effective date: 7/1/15 Type of coverage offered: MEC

providing MV offered to employee, spouse, and dependents

Affordability Safe Harbor used: FPL

Enrollment status: Declined

Example 2

1H 1H 1E 1E 1E 1E 1E

103.00 103.00 103.00 103.00 103.00

2D 2D 2D 2D 2D 2D

1H 1H 1H 1H

2G 2G 2G 2G 2G 2G

1E

103.00

2D: Limited Non-Assessment Period (Initial Measurement Period) 2G: Affordability federal poverty line safe harbor

Employer Fine Risk: $1,750 ($250/month)

7/2/15

Limited Non-Assessment period invalid; coverage offered after the Initial Stability Period deadline

© 2015

, Equ

ifax

Confidential and Proprietary

21

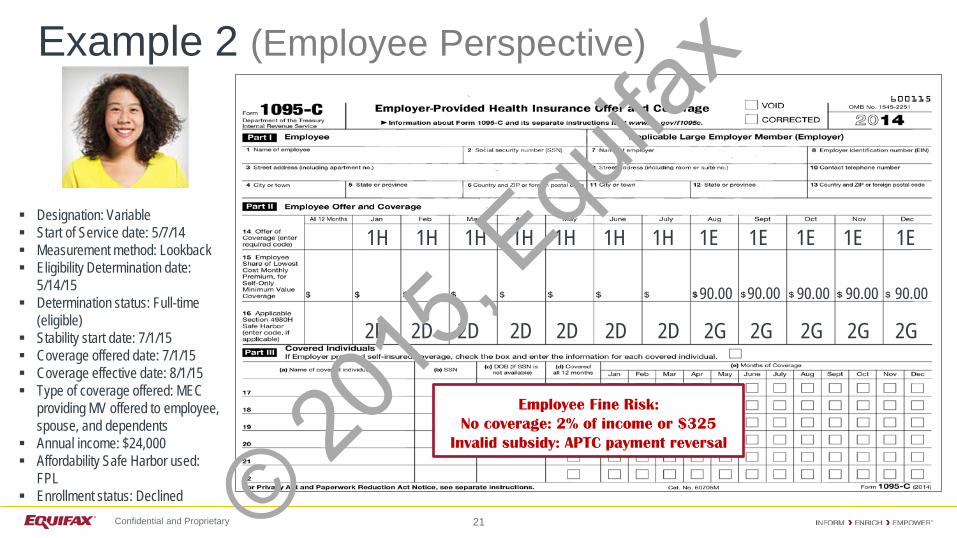

Example 2 (Employee Perspective)

1H 1H 1H 1E 1E 1E 1E

90.00 90.00 90.00 90.00

2D 2D 2D 2D 2D 2D

1H 1H 1H 1H

2D 2G 2G 2G 2G 2G

1E

90.00

Designation: Variable Start of Service date: 5/7/14 Measurement method: Lookback Eligibility Determination date:

5/14/15 Determination status: Full-time

(eligible) Stability start date: 7/1/15 Coverage offered date: 7/1/15 Coverage effective date: 8/1/15 Type of coverage offered: MEC

providing MV offered to employee, spouse, and dependents

Annual income: $24,000 Affordability Safe Harbor used:

FPL Enrollment status: Declined

Employee Fine Risk: No coverage: 2% of income or $325

Invalid subsidy: APTC payment reversal

© 2015

, Equ

ifax

Confidential and Proprietary

22

Why did my subsidy get appealed?

What is form 1095 and why is

my tax return asking for it?

Why am I getting penalized for not

having coverage?

Am I eligible now? Why not?

When will I become eligible?

Why didn’t I get a 1095 form?

What am I supposed to put

on my 1040?

Prepare for Employee Inquiries

© 2015

, Equ

ifax

Confidential and Proprietary

23

Education is key Start early Repeat often

Consider integrated distribution with W-2s Postage savings Employee experience

Electronic consent strategy New hire onboarding Benefits enrollment

Best Practices for Form 1095 Distribution

© 2015

, Equ

ifax

Confidential and Proprietary

24

Jennifer is hired by Employer A on March 15th, 2015 as a salaried, full-time employee. Employer A utilizes the Monthly Measurement Method to determine FT/PT status of their salaried employees. Jennifer is offered affordable coverage on April 1st, 2015 and works 40 hours/week every month for the rest of the year. Based on this information, what is the first month that Jennifer should be included in the total FTE count that Employer A reports on form 1094-C?

March April May June July

Compliance Readiness Question #3

© 2015

, Equ

ifax

Confidential and Proprietary

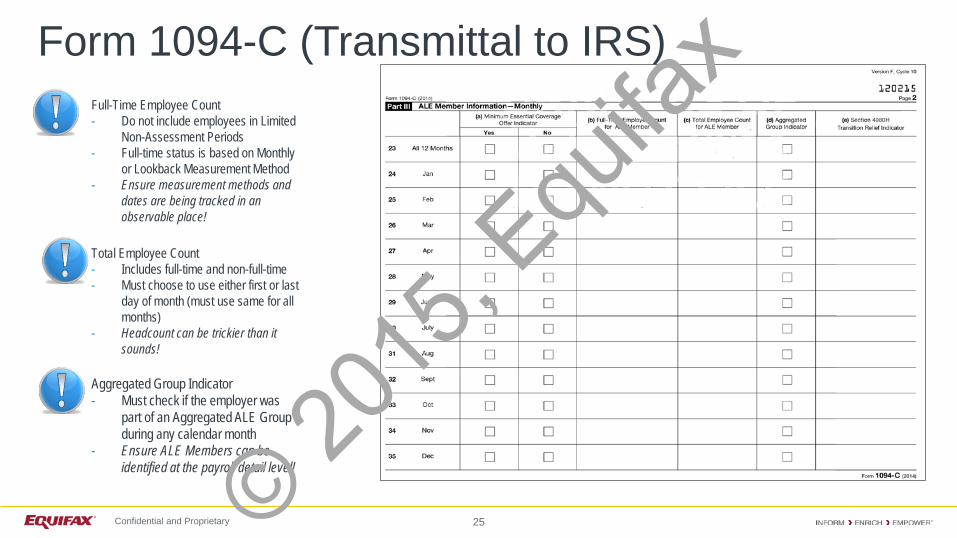

25

Form 1094-C (Transmittal to IRS) Full-Time Employee Count - Do not include employees in Limited

Non-Assessment Periods - Full-time status is based on Monthly

or Lookback Measurement Method - Ensure measurement methods and

dates are being tracked in an observable place!

Total Employee Count - Includes full-time and non-full-time - Must choose to use either first or last

day of month (must use same for all months)

- Headcount can be trickier than it sounds!

Aggregated Group Indicator - Must check if the employer was

part of an Aggregated ALE Group during any calendar month

- Ensure ALE Members can be identified at the payroll detail level!

© 20

15, E

quifa

x

Confidential and Proprietary

REPORTING AND COMPLIANCE DEEP-DIVE

Data Collection and Management Form Preparation and Distribution Subsidy Notifications and Appeals

© 2015

, Equ

ifax

Confidential and Proprietary

27

An employer cannot be fined under either 4980H(a) or 4980H(b) unless…

The employer fails to offer coverage to

all employees An employee receives a subsidy An employer offers coverage that

doesn’t meet affordability requirements

Compliance Readiness Question #4

© 2015

, Equ

ifax

Confidential and Proprietary

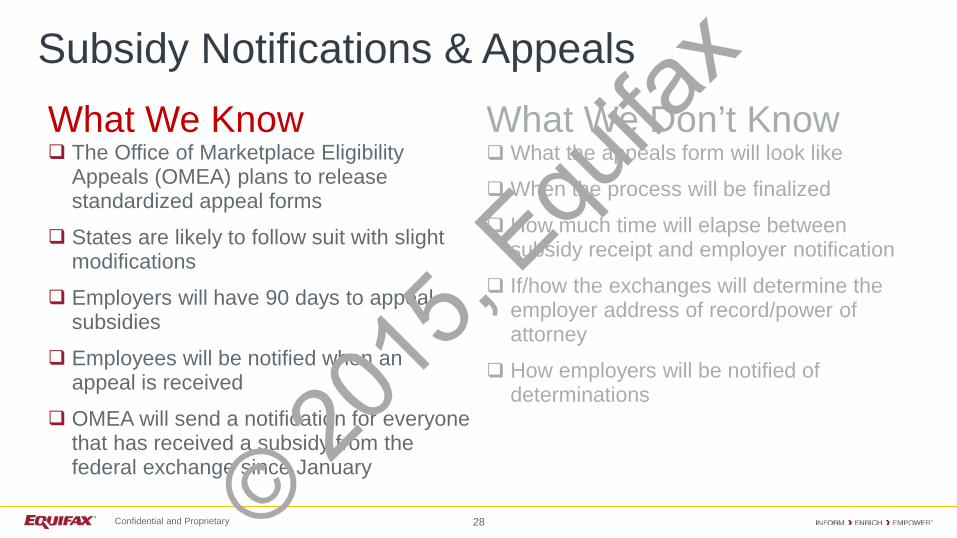

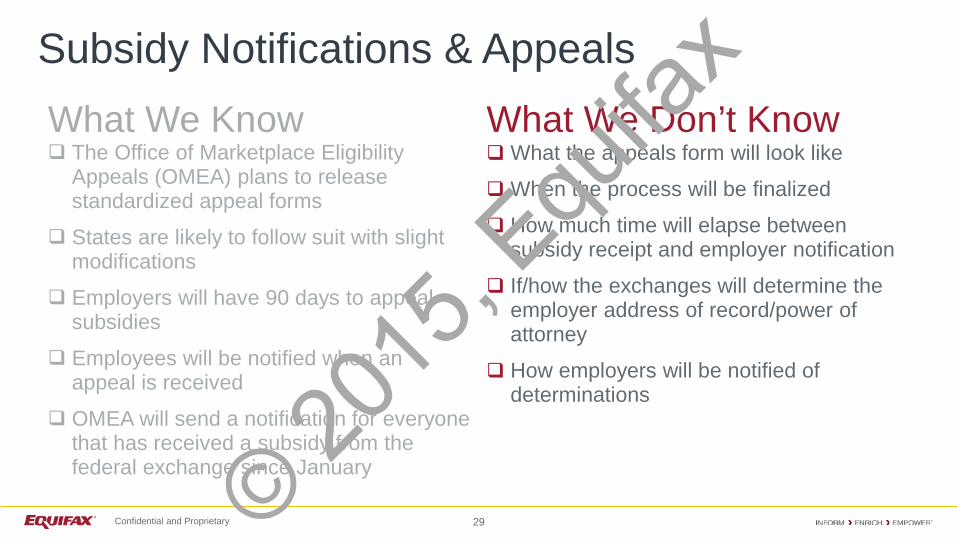

What We Know The Office of Marketplace Eligibility

Appeals (OMEA) plans to release standardized appeal forms

States are likely to follow suit with slight modifications

Employers will have 90 days to appeal subsidies

Employees will be notified when an appeal is received

OMEA will send a notification for everyone that has received a subsidy from the federal exchange since January

What We Don’t Know What the appeals form will look like

When the process will be finalized

How much time will elapse between subsidy receipt and employer notification

If/how the exchanges will determine the employer address of record/power of attorney

How employers will be notified of determinations

28

Subsidy Notifications & Appeals

© 2015

, Equ

ifax

Confidential and Proprietary

What We Know The Office of Marketplace Eligibility

Appeals (OMEA) plans to release standardized appeal forms

States are likely to follow suit with slight modifications

Employers will have 90 days to appeal subsidies

Employees will be notified when an appeal is received

OMEA will send a notification for everyone that has received a subsidy from the federal exchange since January

What We Don’t Know What the appeals form will look like

When the process will be finalized

How much time will elapse between subsidy receipt and employer notification

If/how the exchanges will determine the employer address of record/power of attorney

How employers will be notified of determinations

29

Subsidy Notifications & Appeals

© 2015

, Equ

ifax

Confidential and Proprietary

30

Establish processes and systems for aggregating and storing notices, appeals, and determinations Key question: to appeal or not to appeal?

Best Practices for Appeals Management

Remember: the processes for appealing subsidies and tax penalties are wholly separate

© 2015

, Equ

ifax

Confidential and Proprietary

TACKLING IRS REPORTING Equifax Solution Overview

© 2015

, Equ

ifax

Confidential and Proprietary

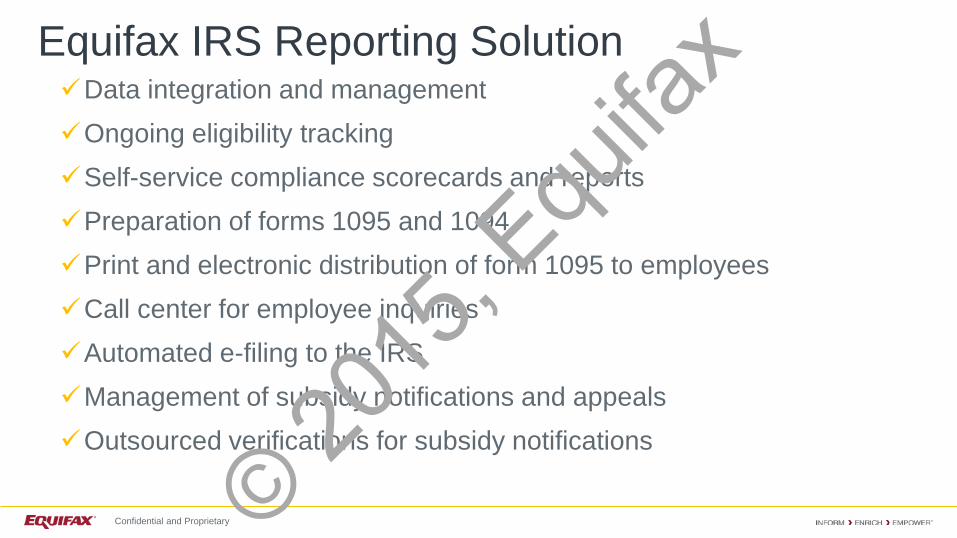

Data integration and management Ongoing eligibility tracking Self-service compliance scorecards and reports Preparation of forms 1095 and 1094 Print and electronic distribution of form 1095 to employees Call center for employee inquiries Automated e-filing to the IRS Management of subsidy notifications and appeals Outsourced verifications for subsidy notifications

Equifax IRS Reporting Solution

© 2015

, Equ

ifax

Confidential and Proprietary

QUESTIONS?

© 2015

, Equ

ifax

Confidential and Proprietary

David Seifert Equifax Workforce Solutions [email protected]

843-573-4142

Kristin Lewis Equifax Workforce Solutions [email protected]

843-573-4131

www.equifaxworkforce.com/academo

Thank you!

© 2015

, Equ

ifax