Embed Size (px)

Citation preview

KBC Bank financial solutions & models for Smart Cities

Lode Verstraeten, Senior Banker & Head of Public Sector, KBC Corporate Banking Center Region Agoria Smart Cities Award event , 26 January 2017

Agenda

I

II

KBC & Sustainability

KBC & Smart Cities : approach, services & financing

solutions

I) Sustainability@

KBC Group

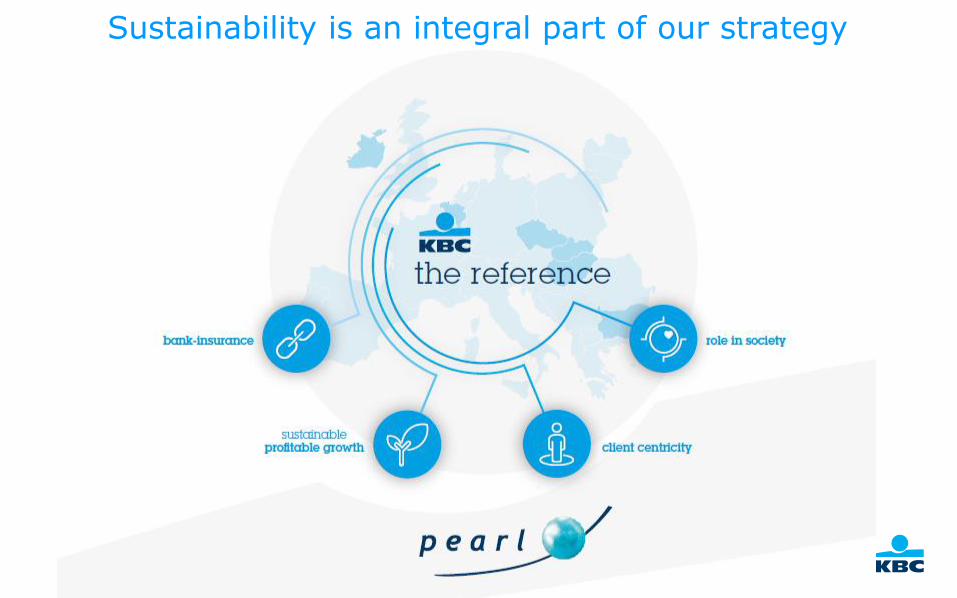

Sustainability is an integral part of our strategy

Increase our positive

impact on society

Responsible behaviour of all

staff

Limit our adverse

impact on society

• Focus on responsible behaviour and suitable advice, based on our corporate culture and Pearl- values

• Enhancing responsible behaviour via e.g. dilemma training

The core of our sustainability strategy

• Four focus domains close to our core business

Financial literacy Environmental responsibililty

Stimulating entrepreneurship Longevity or Health

• Strict policies for our activities regarding:

₋ Human Rights ₋ Environment ₋ Business ethics ₋ Socially sensitive issues

• Reducing our own footprint

₋ ISO 14001 certificate in all core countries

₋ Reduction targets greenhouse gases (GHG)

• A complete offer of SRI Funds

Agenda

I

II

KBC & Sustainability

KBC & Smart Cities : approach, services & financing

solutions

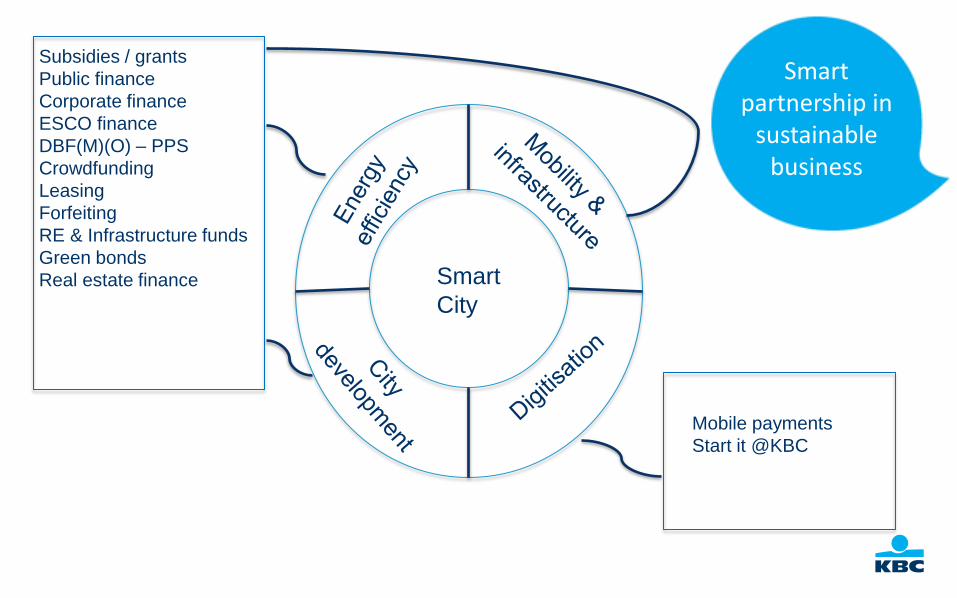

Smart

City

Subsidies / grants

Public finance

Corporate finance

ESCO finance

DBF(M)(O) – PPS

Crowdfunding

Leasing

Forfeiting

RE & Infrastructure funds

Green bonds

Real estate finance

Mobile payments

Start it @KBC

Smart partnership in

sustainable business

In addition to existing traditional (project) financing solutions, KBC has

developed new and innovative financing and service approaches relevant to

the Smart City theme, such as:

1. Energy efficiency financing solutions &

Environmental efficiency working group within Corporate Banking

focusing on Renewable Energy

2. KBC Mobility programme – examples: Velodroom & Traject Mobility

Management

3. Coaching start-ups via Start it @KBC

4. Focus on digitisation and mobile banking solutions

II) KBC & Smart Cities – approach, services & financing solutions

1 Energy efficiency financing

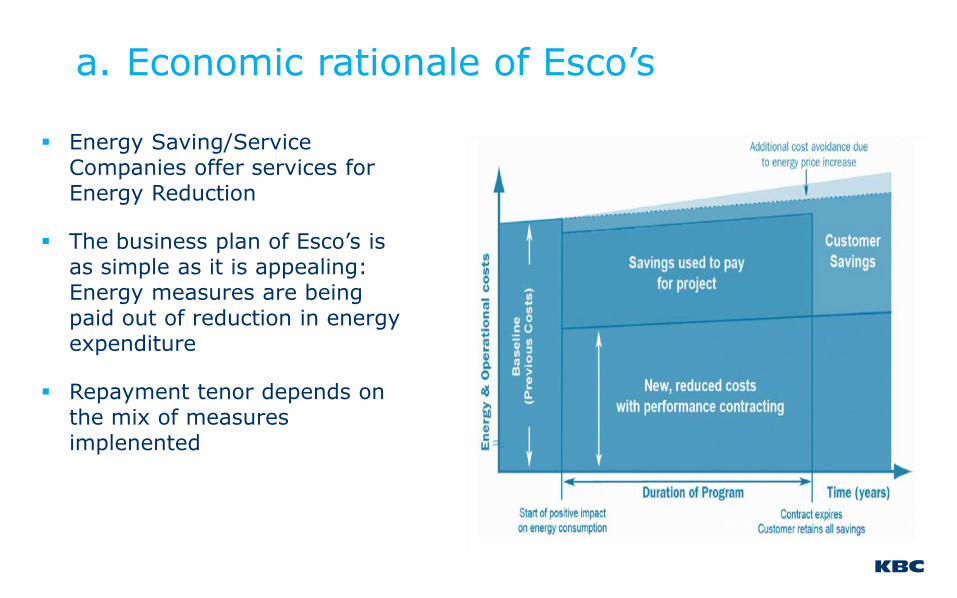

Economic rationale of Esco’s a.

Energy Saving/Service

Companies offer services for Energy Reduction

The business plan of Esco’s is as simple as it is appealing: Energy measures are being paid out of reduction in energy expenditure

Repayment tenor depends on the mix of measures implenented

Esco covers a variety of business models b.

Scope of services offered varies: in case of full scope “Esco” services include:

- Screening of potential energy efficiency measures (€ and kWh)

- Implementation of energy efficiency measures

- Monitoring and finetuning + Maintenance (preventive and corrective)

- Financing of investments

KBC is partner in finding tailor made solutions

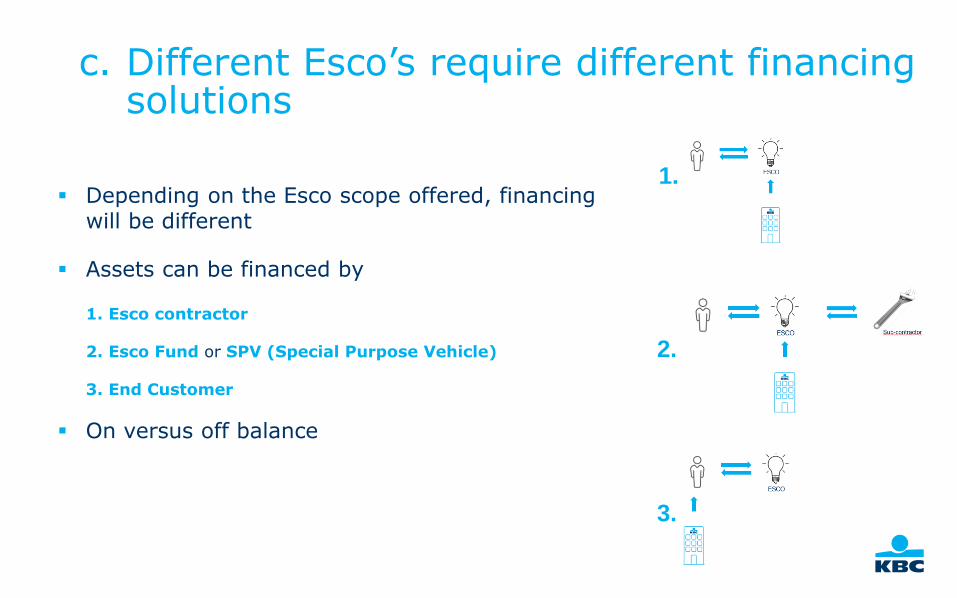

Different Esco’s require different financing solutions

c.

Depending on the Esco scope offered, financing will be different

Assets can be financed by

1. Esco contractor

2. Esco Fund or SPV (Special Purpose Vehicle)

3. End Customer

On versus off balance

1.

2.

3.

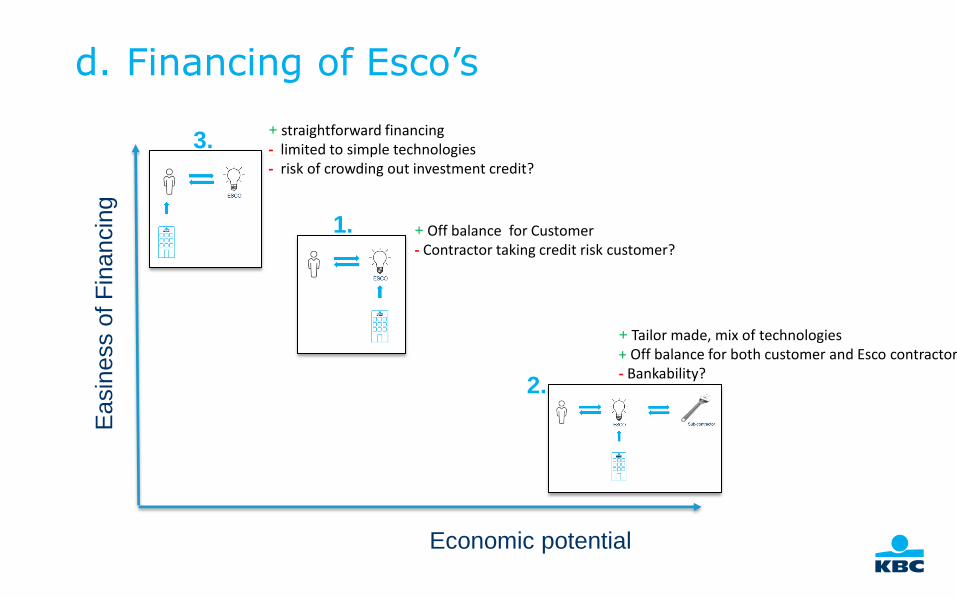

Financing of Esco’s d.

1.

2.

3.

Economic potential

Easin

ess o

f F

ina

ncin

g

+ straightforward financing - limited to simple technologies - risk of crowding out investment credit?

+ Off balance for Customer - Contractor taking credit risk customer?

+ Tailor made, mix of technologies + Off balance for both customer and Esco contractor - Bankability?

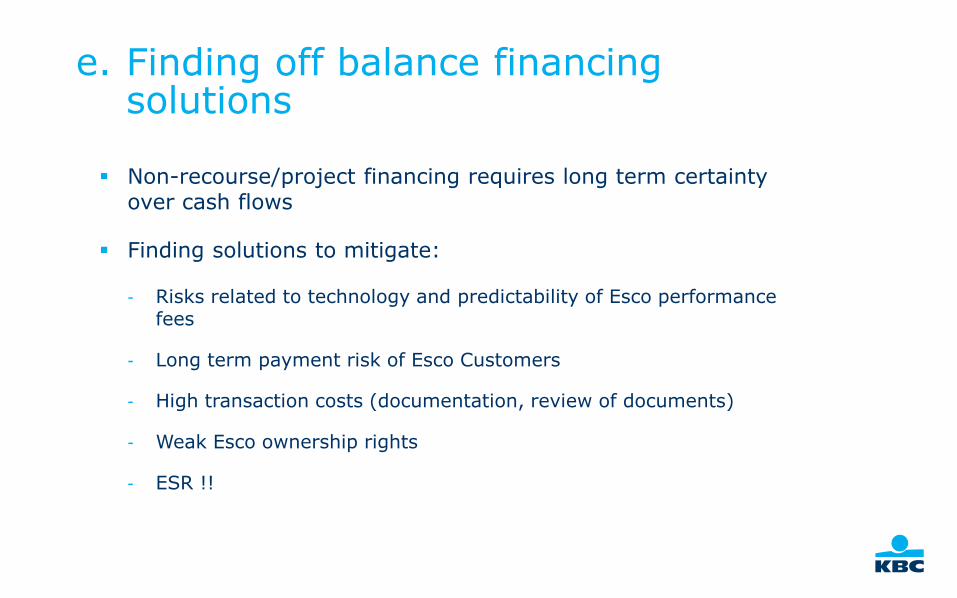

Finding off balance financing solutions

e.

Non-recourse/project financing requires long term certainty over cash flows

Finding solutions to mitigate:

- Risks related to technology and predictability of Esco performance fees

- Long term payment risk of Esco Customers

- High transaction costs (documentation, review of documents)

- Weak Esco ownership rights

- ESR !!

Innovative financing :

Green Bonds

15

KBC Securities │16

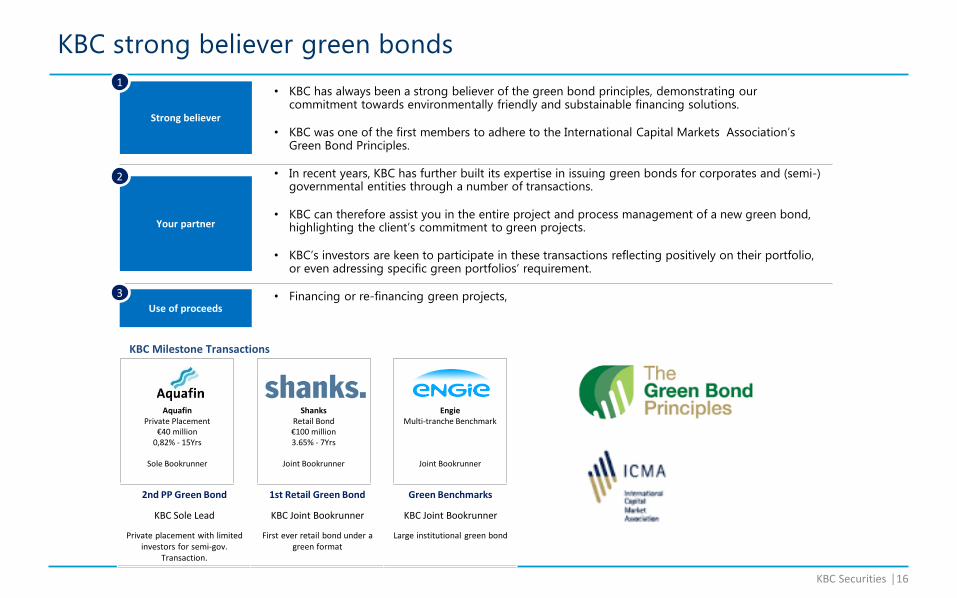

KBC strong believer green bonds

• KBC has always been a strong believer of the green bond principles, demonstrating our commitment towards environmentally friendly and substainable financing solutions.

• KBC was one of the first members to adhere to the International Capital Markets Association’s Green Bond Principles.

• In recent years, KBC has further built its expertise in issuing green bonds for corporates and (semi-) governmental entities through a number of transactions.

• KBC can therefore assist you in the entire project and process management of a new green bond, highlighting the client’s commitment to green projects.

• KBC’s investors are keen to participate in these transactions reflecting positively on their portfolio, or even adressing specific green portfolios’ requirement.

• Financing or re-financing green projects,

Strong believer

Your partner

1

2

Aquafin Private Placement

€40 million 0,82% - 15Yrs

Sole Bookrunner

Shanks Retail Bond €100 million 3.65% - 7Yrs

Joint Bookrunner

Engie Multi-tranche Benchmark

Joint Bookrunner

2nd PP Green Bond 1st Retail Green Bond Green Benchmarks

KBC Sole Lead KBC Joint Bookrunner KBC Joint Bookrunner

Private placement with limited investors for semi-gov.

Transaction.

First ever retail bond under a green format

Large institutional green bond

Use of proceeds

3

KBC Milestone Transactions

KBC Securities │17

Green Bonds • Green Bonds raise funds for new and existing projects with environmentally sustainable benefits. The Green Bond Principles

(GBP) are voluntary process guidelines that recommend transparency and disclosure, and promote integrity in the development of the Green Bond market. They are intended for broad use by the variety of actors participating in the market and are designed to provide the information needed to increase capital allocation to environmentally sustainable purposes without any single arbiter

• The Green Bond Principles (GBP) are voluntary process guidelines that recommend transparency and disclosure and promote integrity in the development of the Green Bond market by clarifying the approach for issuance of a Green Bond.

• The GBP have four core components:

• 1. Use of Proceeds : The cornerstone of a Green Bond is the utilization of the proceeds of the bond for Green Projects which should be appropriately described in the legal documentation for the security. All designated Green Project categories should provide clear environmental benefits, which will be assessed and, where feasible, quantified by the issuer.

• 2. Process for Project Evaluation and Selection : The issuer of a Green Bond should outline:

• a process to determine how the projects fit within the eligible Green Projects categories identified above;

• the related eligibility criteria; and

• the environmental sustainability objectives.

• 3. Management of Proceeds : The net proceeds of Green Bonds should be credited to a sub-account, moved to a sub-portfolio or otherwise tracked by the issuer in an appropriate manner and attested to by a formal internal process linked to the issuer’s lending and investment operations for Green Projects. So long as the Green Bonds are outstanding, the balance of the tracked proceeds should be periodically adjusted to match allocations to eligible Green Projects made during that period.

• 4. Reporting : Issuers should make, and keep, readily available up to date information on the use of proceeds to be renewed annually until full allocation, and as necessary thereafter in the event of new developments. This should include a list of the projects to which Green Bond proceeds have been allocated, as well as a brief description of the projects and the amounts allocated, and their expected impact. Where confidentiality agreements, competitive considerations, or a large number of underlying projects limit the amount of detail that can be made available, the GBP recommend that information is presented in generic terms or on an aggregated portfolio basis (e.g. percentage allocated to certain project categories).

Definition (ICMA)

Green Bond Principles

1

2

KBC Securities │18

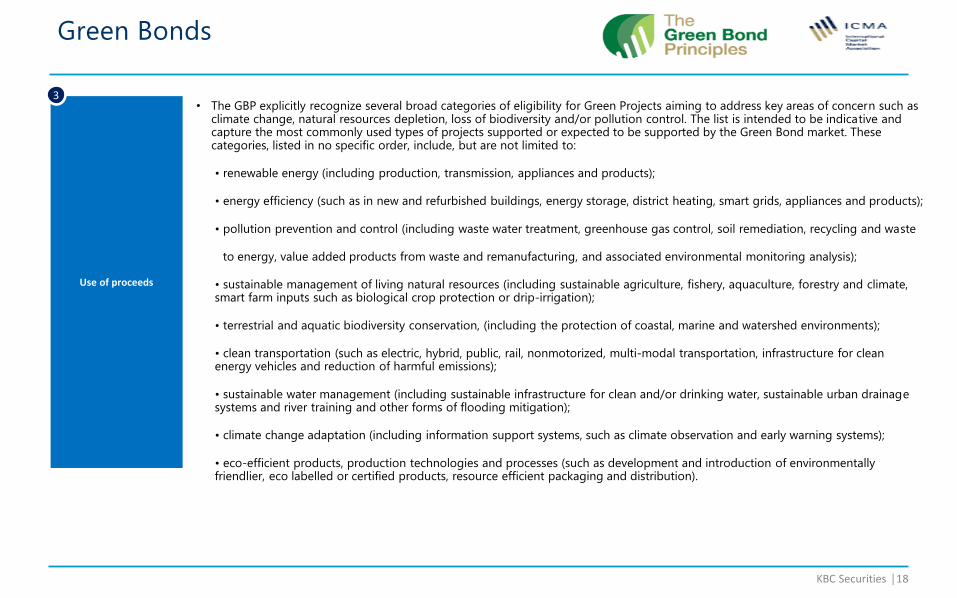

Green Bonds

• The GBP explicitly recognize several broad categories of eligibility for Green Projects aiming to address key areas of concern such as climate change, natural resources depletion, loss of biodiversity and/or pollution control. The list is intended to be indicative and capture the most commonly used types of projects supported or expected to be supported by the Green Bond market. These categories, listed in no specific order, include, but are not limited to:

• renewable energy (including production, transmission, appliances and products);

• energy efficiency (such as in new and refurbished buildings, energy storage, district heating, smart grids, appliances and products);

• pollution prevention and control (including waste water treatment, greenhouse gas control, soil remediation, recycling and waste

to energy, value added products from waste and remanufacturing, and associated environmental monitoring analysis);

• sustainable management of living natural resources (including sustainable agriculture, fishery, aquaculture, forestry and climate, smart farm inputs such as biological crop protection or drip-irrigation);

• terrestrial and aquatic biodiversity conservation, (including the protection of coastal, marine and watershed environments);

• clean transportation (such as electric, hybrid, public, rail, nonmotorized, multi-modal transportation, infrastructure for clean energy vehicles and reduction of harmful emissions);

• sustainable water management (including sustainable infrastructure for clean and/or drinking water, sustainable urban drainage systems and river training and other forms of flooding mitigation);

• climate change adaptation (including information support systems, such as climate observation and early warning systems);

• eco-efficient products, production technologies and processes (such as development and introduction of environmentally friendlier, eco labelled or certified products, resource efficient packaging and distribution).

Use of proceeds

3

Renovation Loan for Owners'

Associations

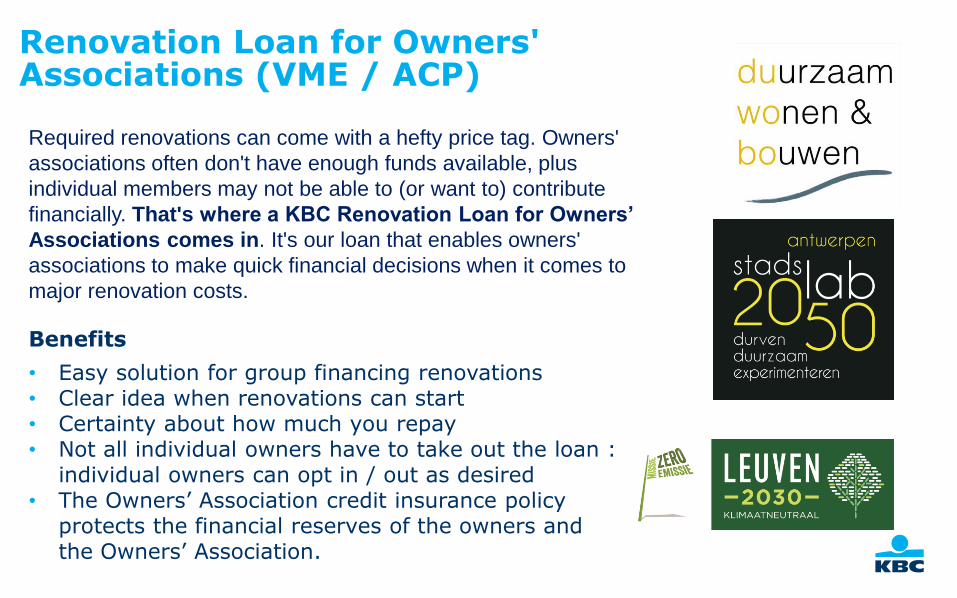

Renovation Loan for Owners' Associations (VME / ACP)

Required renovations can come with a hefty price tag. Owners'

associations often don't have enough funds available, plus

individual members may not be able to (or want to) contribute

financially. That's where a KBC Renovation Loan for Owners’

Associations comes in. It's our loan that enables owners'

associations to make quick financial decisions when it comes to

major renovation costs.

Benefits

• Easy solution for group financing renovations • Clear idea when renovations can start • Certainty about how much you repay • Not all individual owners have to take out the loan :

individual owners can opt in / out as desired • The Owners’ Association credit insurance policy

protects the financial reserves of the owners and the Owners’ Association.

2 KBC Mobility Programme

KBC Mobility focuses on sustainable and high-quality mobility solutions in Belgium

Mobility gets everyone moving – companies, governments, private individuals

KBC mobility wants to respond specifically to solutions for mobility issues:

- Chain mobility and mobility budget supported by ICT applications

- Sharing economy, pay per use, from ownership to usage

- Smart mobility – monitoring driving habits, smart to autonomous vehicles

- Sustainability – stricter fuel economy and emissions standards

- Health and safety – flexible working conditions, prevention, route monitoring

- Smart cities – chain mobility, ppp, etc.

https://ww33c.com/system/files/doc/n

ewsroom/pressreleases/2016/201604

20_KBC_Mobility_en.pdf

KBC Mobility “Velodroom”

From car to bike in 3 steps

‘VELODROOM’

Create a burning platform

The car model is under pressure from regulations introduced by cities and municipalities. These days, it's bikes not cars that determine how ‘cool’ a city really is.

Traffic congestion and time lost travelling to work are a daily source of frustration.

Employees can no longer ignore the urge to live a more active and healthier life.

Cyclists bridge in Antwerp

Pedestrian areas without cars in cities

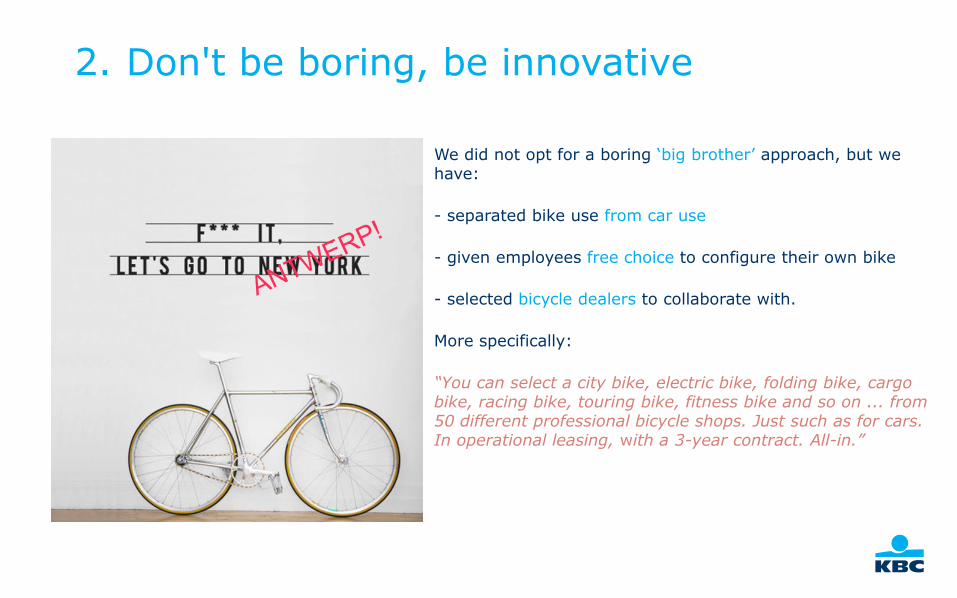

Don't be boring, be innovative

We did not opt for a boring ‘big brother’ approach, but we have:

- separated bike use from car use

- given employees free choice to configure their own bike

- selected bicycle dealers to collaborate with.

More specifically:

“You can select a city bike, electric bike, folding bike, cargo bike, racing bike, touring bike, fitness bike and so on ... from 50 different professional bicycle shops. Just such as for cars. In operational leasing, with a 3-year contract. All-in.”

2.

Ensure ‘instant happiness’

We do this by enabling employees to:

1) Redeem salary, … for lease payments:

e.g. redeem € 50 gross salary = € 70 euro lease budget per month e.g. redeem € 70 gross salary = € 100 euro lease budget per month

2) This is for EVERYONE (not just for administrative staff or company car users)

3) So you get more bike for the salary redeemed

We did not opt for:

1) Less car use (doesn't work)

2) Fewer options (doesn't work)

3.

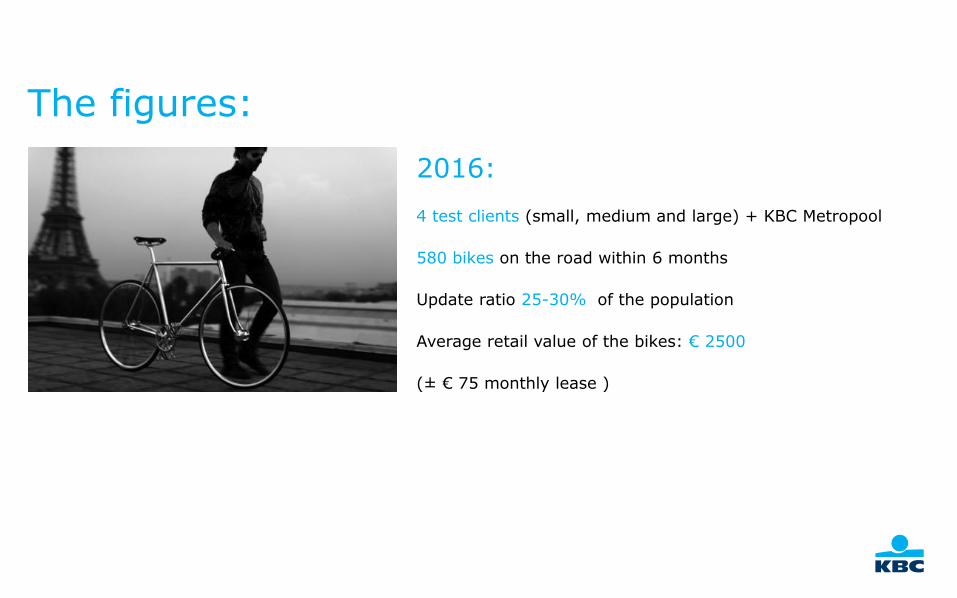

The figures:

2016:

4 test clients (small, medium and large) + KBC Metropool

580 bikes on the road within 6 months

Update ratio 25-30% of the population

Average retail value of the bikes: € 2500

(± € 75 monthly lease )

KBC Mobility:

Traject mobility

management

Traject mobility management presentation

January 2017

31

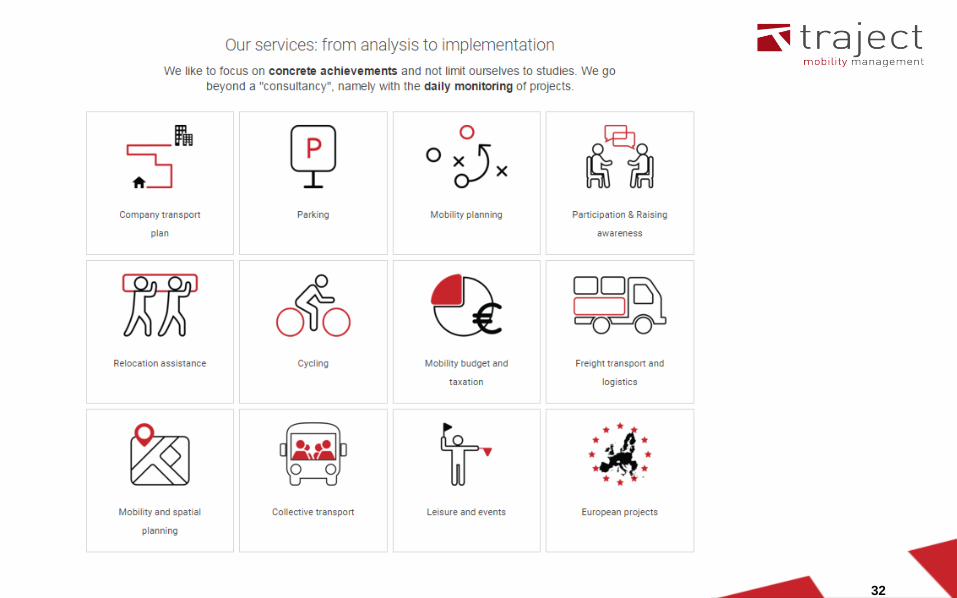

Our expertise

►Traffic & Mobility: consultancy – planning – management

►Respons to economical, social and sustainable criteria

►Change Management next to theoretical studies

►Corporate mobility plans, in house consulting, sustainable urban

mobility plans, parking studies, incidence studies…

►18 consultants, offices Brussels and Ghent

32

33

3 Coaching start-ups / Crowdfunding

Supporting

startups via Start

it @ KBC

Een paar cijfertjes… Start it is

momenteel de grootste incubator in

België, en waarschijnlijk één van de

grootste in Europa. Waar we ons de

komende tijd op willen focussen is net

dat Europees verhaal: met om te

beginnen sterke contacten in Berlijn,

Londen, Amsterdam, Parijs, Bulgarije,

Hongarije en in de Scandinavische

landen.

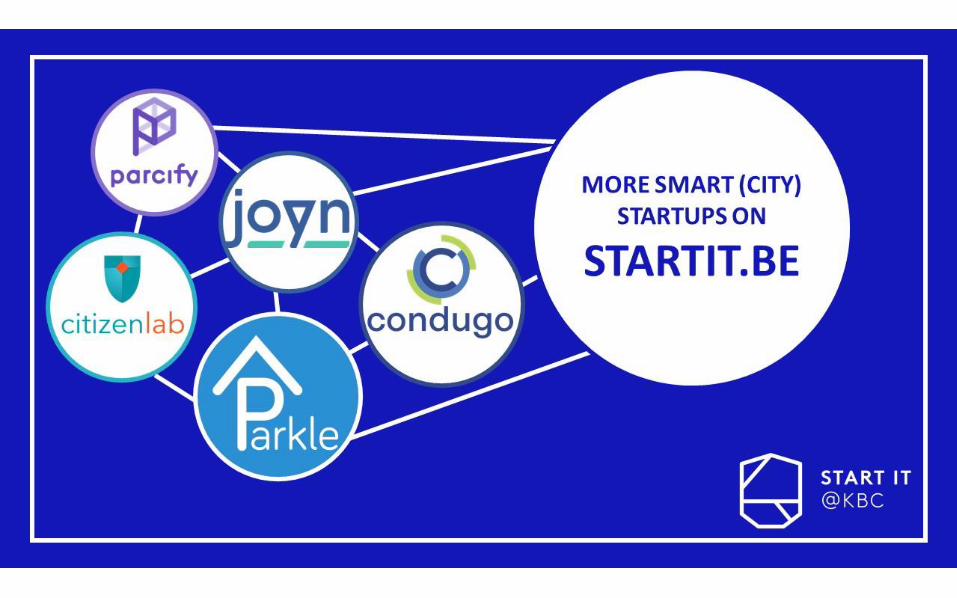

And many more smart city startups (energy, mobility, living and digital) on www.startit.be

zetapulse

Innovative financing :

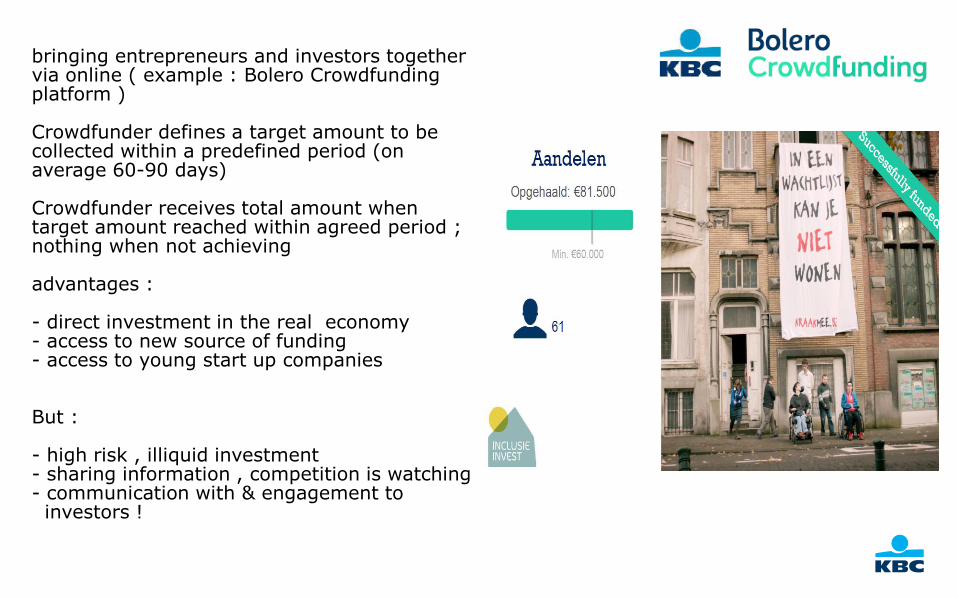

Crowdfunding

bringing entrepreneurs and investors together via online ( example : Bolero Crowdfunding platform ) Crowdfunder defines a target amount to be collected within a predefined period (on average 60-90 days) Crowdfunder receives total amount when target amount reached within agreed period ; nothing when not achieving advantages : - direct investment in the real economy - access to new source of funding - access to young start up companies But : - high risk , illiquid investment - sharing information , competition is watching - communication with & engagement to investors !

Member of the KBC group

4 KBC & Digital solutions for Smart

Cities

46

KBC considers local involvement to be vitally important.

Solidarity between retailers, consumers, government bodies ... between

everyone who lives and contributes to the local community.

This community is increasingly confronted with growing digitisation, online

business and communication

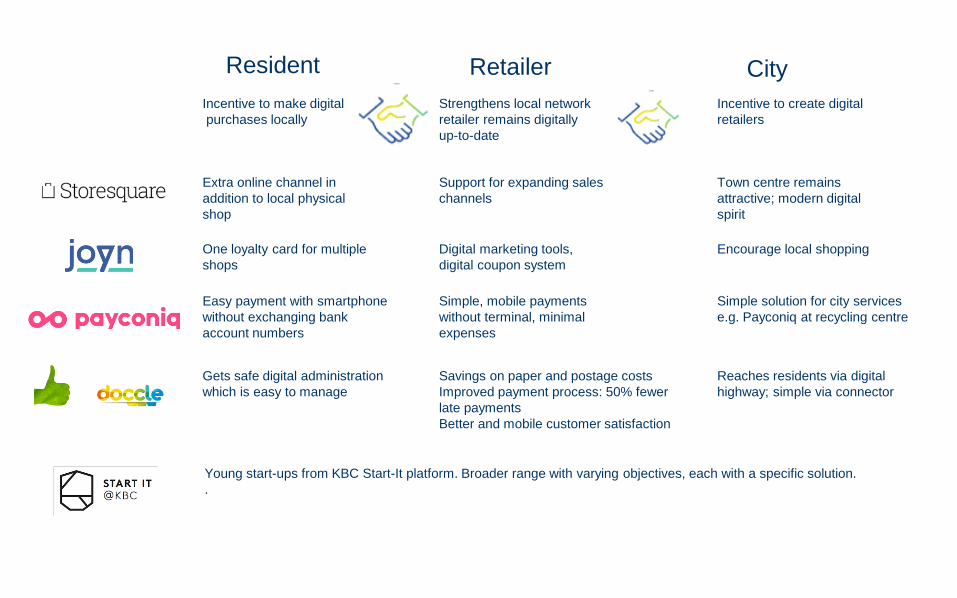

Resident Retailer City

Incentive to create digital

retailers

Strengthens local network

retailer remains digitally

up-to-date

Incentive to make digital

purchases locally

One loyalty card for multiple

shops

Digital marketing tools,

digital coupon system

Extra online channel in

addition to local physical

shop

Support for expanding sales

channels

Town centre remains

attractive; modern digital

spirit

Encourage local shopping

Easy payment with smartphone

without exchanging bank

account numbers

Simple, mobile payments

without terminal, minimal

expenses

Simple solution for city services

e.g. Payconiq at recycling centre

Gets safe digital administration

which is easy to manage

Reaches residents via digital

highway; simple via connector

Young start-ups from KBC Start-It platform. Broader range with varying objectives, each with a specific solution.

.

Savings on paper and postage costs

Improved payment process: 50% fewer

late payments

Better and mobile customer satisfaction

48

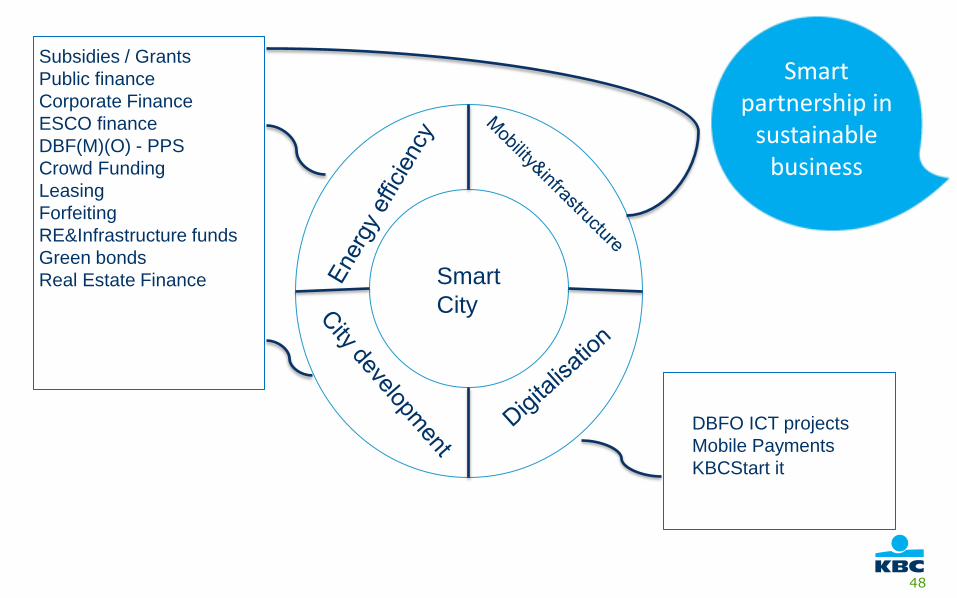

Smart

City

Subsidies / Grants

Public finance

Corporate Finance

ESCO finance

DBF(M)(O) - PPS

Crowd Funding

Leasing

Forfeiting

RE&Infrastructure funds

Green bonds

Real Estate Finance

DBFO ICT projects

Mobile Payments

KBCStart it

Smart partnership in

sustainable business

We go for smart

partnership in sustainable

business

49

Company 50

Contact: Wim Leemen, General Manager Corporate Banking Centre Region [email protected] T: 02.429.49.80 Havenlaan 6, 1080 Brussels Lode Verstraeten, Senior Banker & Head of Public Sector & Institutionals, Corporate Banking Centre Region [email protected] T: 02.429.52.23 Havenlaan 6, 1080 Brussels

Company 52