Embed Size (px)

Citation preview

Transforming Enterprise Communications

Analyst Briefing

June 2010

Helping Customers Find the Value in Advanced Technologies

Elka Popova, Program DirectorMelanie Turek, Principal Analyst

2

Agenda

Key Customer Pain Points and Channel Concerns

From IP Telephony to UC: Where the Value Lies

Hosted UC and SIP Trunking: Cloud Nirvana?

Conclusions and Recommendations

About Frost & Sullivan

3

Key Customer Pain Points and Channel

Concerns

4

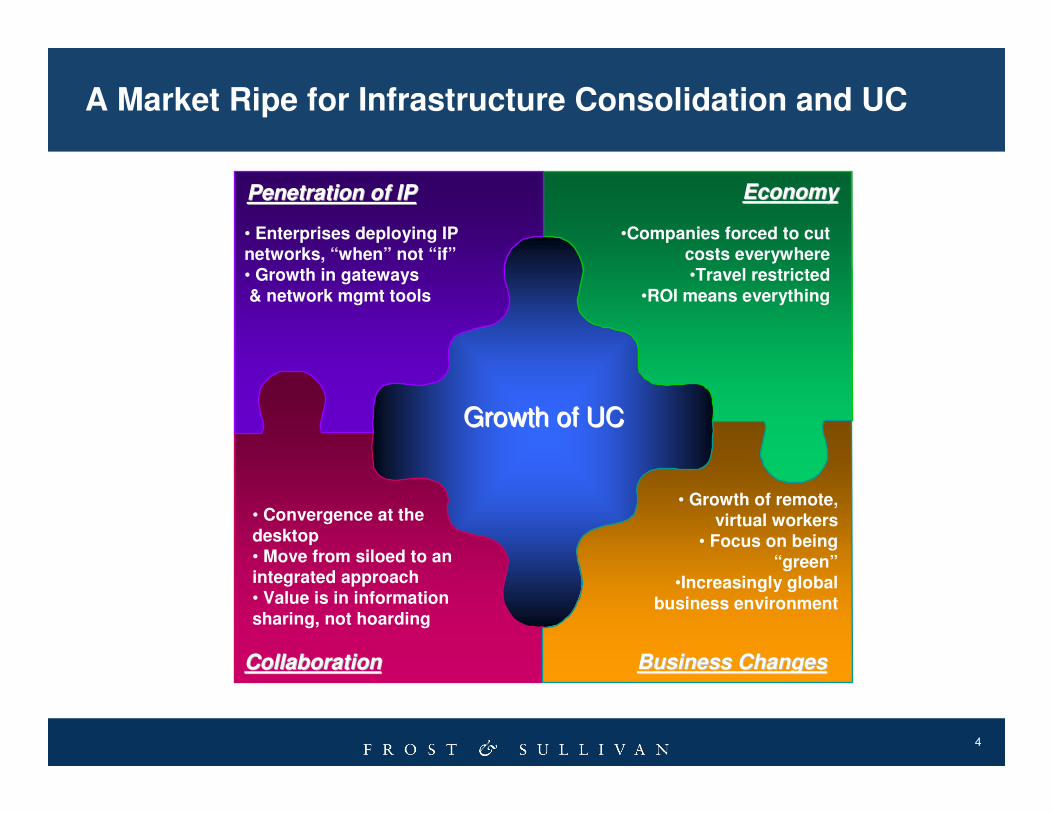

A Market Ripe for Infrastructure Consolidation and UC

Growth of UCGrowth of UC

CollaborationCollaboration

EconomyEconomy

Business ChangesBusiness Changes

Penetration of IPPenetration of IP

• Enterprises deploying IP networks, “when” not “if”• Growth in gateways

& network mgmt tools

• Growth of remote, virtual workers

• Focus on being “green”

•Increasingly global

business environment

• Convergence at the

desktop• Move from siloed to an integrated approach• Value is in information

sharing, not hoarding

•Companies forced to cut costs everywhere•Travel restricted

•ROI means everything

5

Top Customer Pain Points

Return on Investment

Training

Supporting Employee-Driven Next-Gen Technology

Mobile Device Support

Change Management

6

•Customers now including UC capabilities on their RFPs; in many cases, businesses are only upgrading a certain piece of their communications infrastructure (e.g. telephony).

•The challenges related to the integration process currently seem to outweigh the perceived benefits of UC, limiting proactive demand for multi-vendor solutions.

•Many businesses also continue to question the benefits of certain basic UC applications, including IM and videoconferencing.

•Over the next 5 to 6 years, UC will penetrate the market mostly by vendors’ “push”strategies, and less so due to customer “pull.” Free UC clients, attractive bundling and low-cost or no-cost pilot programs will help users experience UC and its benefits.

•UC adoption may remain limited to specific user groups (e.g. knowledge workers, marketing and sales people) for the next few years, until business models make it compelling for the average communications user to own a UC solution even if they are not using all of its capabilities and not benefiting as much as the early adopters.

Demand Analysis

7

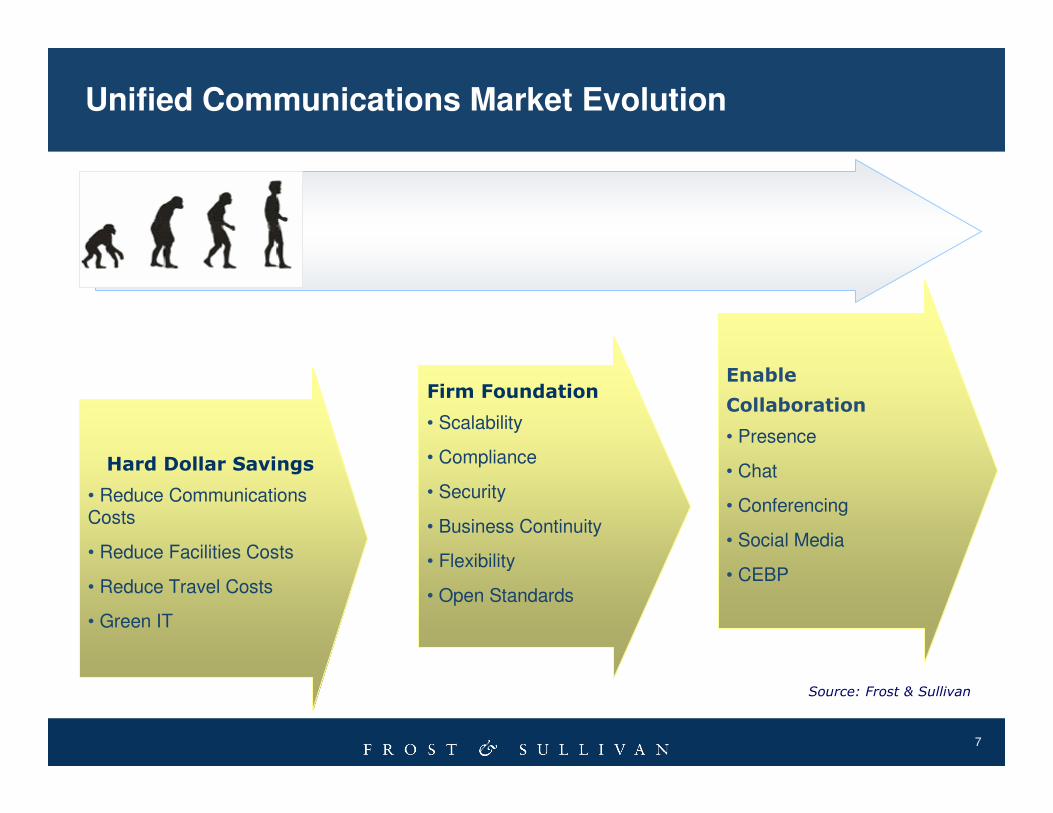

Enable

Collaboration

• Presence

• Chat

• Conferencing

• Social Media

• CEBP

Firm Foundation

• Scalability

• Compliance

• Security

• Business Continuity

• Flexibility

• Open Standards

Hard Dollar Savings

• Reduce Communications Costs

• Reduce Facilities Costs

• Reduce Travel Costs

• Green IT

Unified Communications Market Evolution

Source: Frost & Sullivan

8

The Channel Plays a Key Role

• The complexity of UC implementations,

especially in multi-vendor environments,

requires a significant vendor or channel partner

implementation and integration expertise.

• Intensifying competition and consolidation in

maturing communications markets are also

driving an increasing importance on the channel.

• The nature of channel partnerships is changing

as IT and telecom continue to converge with the

shift to software-centric solutions, and with

businesses increasingly virtualizing their data

centers and, going forward, their

communications infrastructures.

• To succeed, VARs and SIs must be able to

successfully deploy and manage converged

technologies—and that requires new skill sets,

education and training.

9

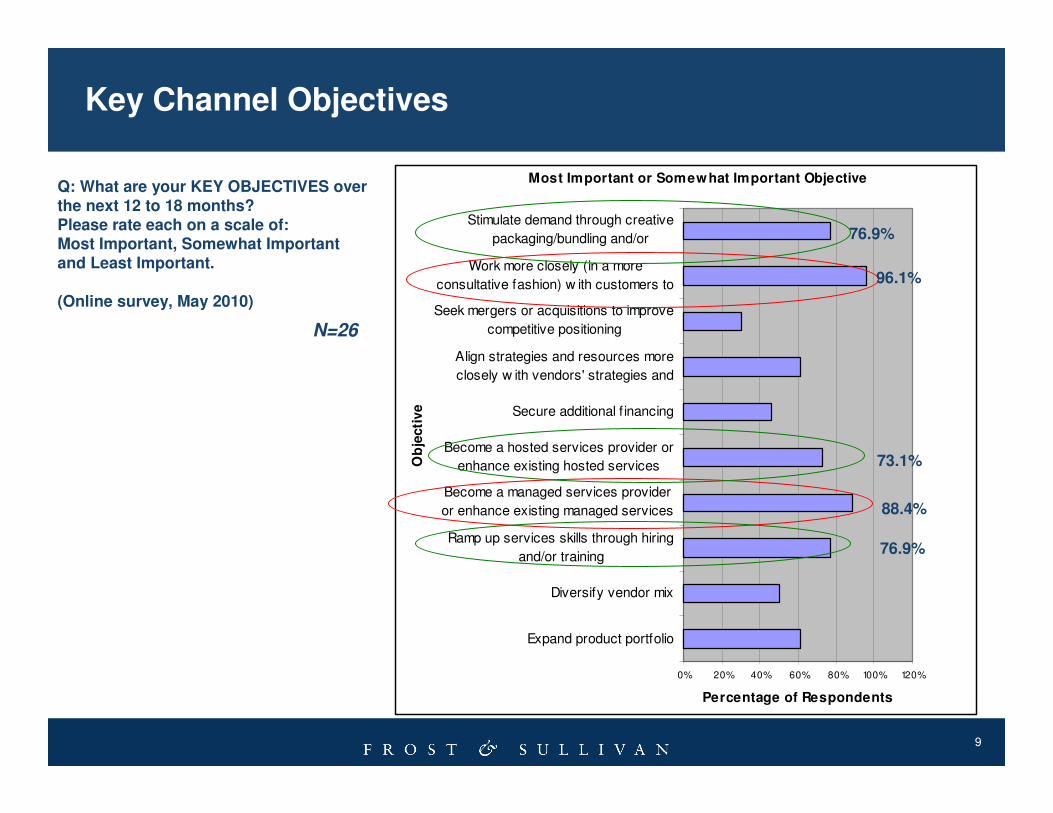

Key Channel Objectives

Most Important or Somewhat Important Objective

0% 20% 40% 60% 80% 100% 120%

Expand product portfolio

Diversify vendor mix

Ramp up services skills through hiring

and/or training

Become a managed services provider

or enhance existing managed services

Become a hosted services provider or

enhance existing hosted services

Secure additional f inancing

Align strategies and resources more

closely w ith vendors' strategies and

Seek mergers or acquisitions to improve

competitive positioning

Work more closely (in a more

consultative fashion) w ith customers to

Stimulate demand through creative

packaging/bundling and/or

Ob

jecti

ve

Percentage of Respondents

76.9%

88.4%

73.1%

96.1%

76.9%

N=26

Q: What are your KEY OBJECTIVES over the next 12 to 18 months? Please rate each on a scale of: Most Important, Somewhat Importantand Least Important.

(Online survey, May 2010)

10

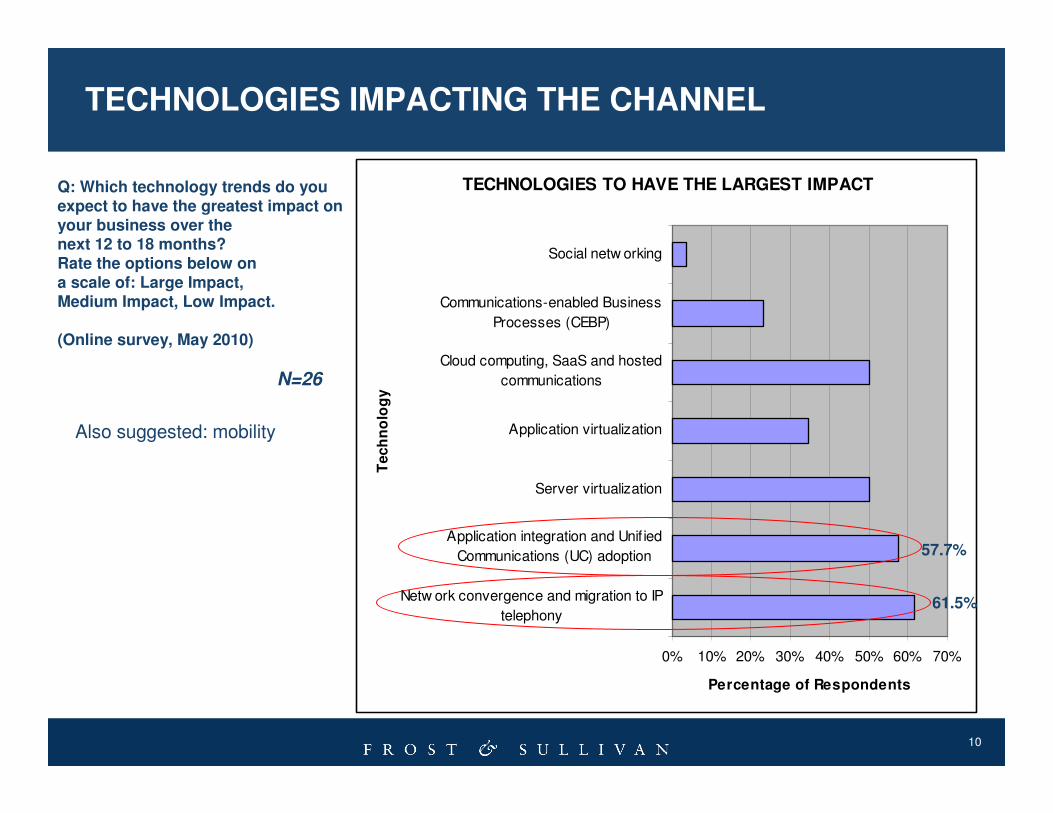

TECHNOLOGIES IMPACTING THE CHANNEL

TECHNOLOGIES TO HAVE THE LARGEST IMPACT

0% 10% 20% 30% 40% 50% 60% 70%

Netw ork convergence and migration to IP

telephony

Application integration and Unif ied

Communications (UC) adoption

Server virtualization

Application virtualization

Cloud computing, SaaS and hosted

communications

Communications-enabled Business

Processes (CEBP)

Social netw orking

Tech

no

log

y

Percentage of Respondents

61.5%

57.7%

Q: Which technology trends do you expect to have the greatest impact onyour business over the next 12 to 18 months? Rate the options below on a scale of: Large Impact,Medium Impact, Low Impact.

(Online survey, May 2010)

N=26

Also suggested: mobility

11

From IP Telephony to UC: Where the Value Lies

12

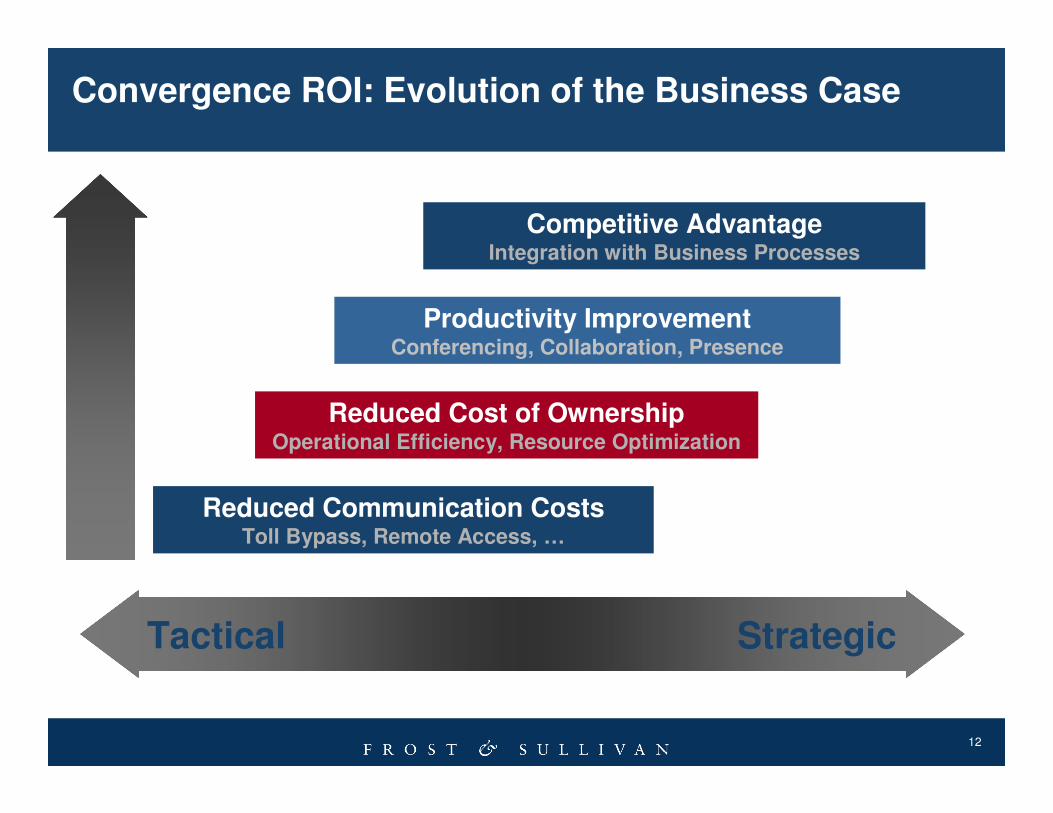

Convergence ROI: Evolution of the Business Case

Reduced Communication CostsToll Bypass, Remote Access, …

Reduced Cost of OwnershipOperational Efficiency, Resource Optimization

Productivity ImprovementConferencing, Collaboration, Presence

Competitive AdvantageIntegration with Business Processes

“H

AR

D”

“S

OF

T”

Tactical Strategic

13

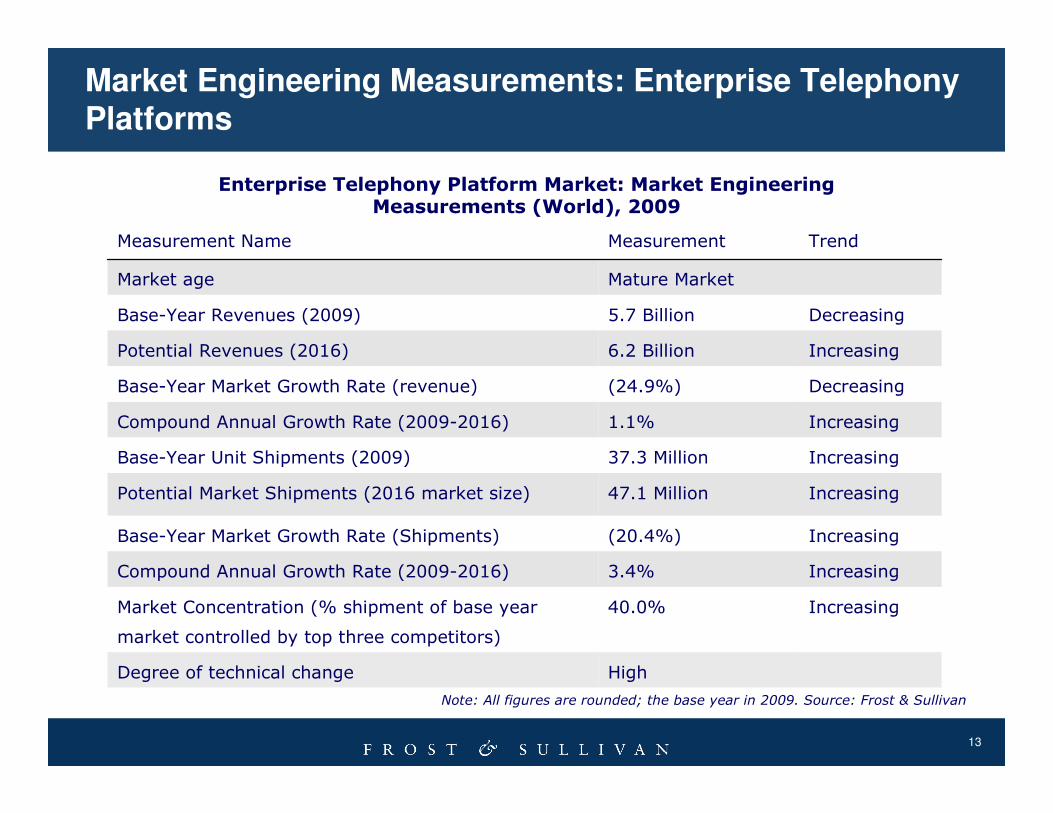

Market Engineering Measurements: Enterprise Telephony Platforms

Enterprise Telephony Platform Market: Market Engineering Measurements (World), 2009

Note: All figures are rounded; the base year in 2009. Source: Frost & Sullivan

Increasing40.0%Market Concentration (% shipment of base year

market controlled by top three competitors)

Increasing3.4%Compound Annual Growth Rate (2009-2016)

Decreasing(24.9%)Base-Year Market Growth Rate (revenue)

Increasing1.1%Compound Annual Growth Rate (2009-2016)

HighDegree of technical change

Increasing(20.4%)Base-Year Market Growth Rate (Shipments)

Increasing47.1 MillionPotential Market Shipments (2016 market size)

Increasing37.3 MillionBase-Year Unit Shipments (2009)

Increasing6.2 BillionPotential Revenues (2016)

Decreasing5.7 BillionBase-Year Revenues (2009)

Mature MarketMarket age

TrendMeasurementMeasurement Name

14

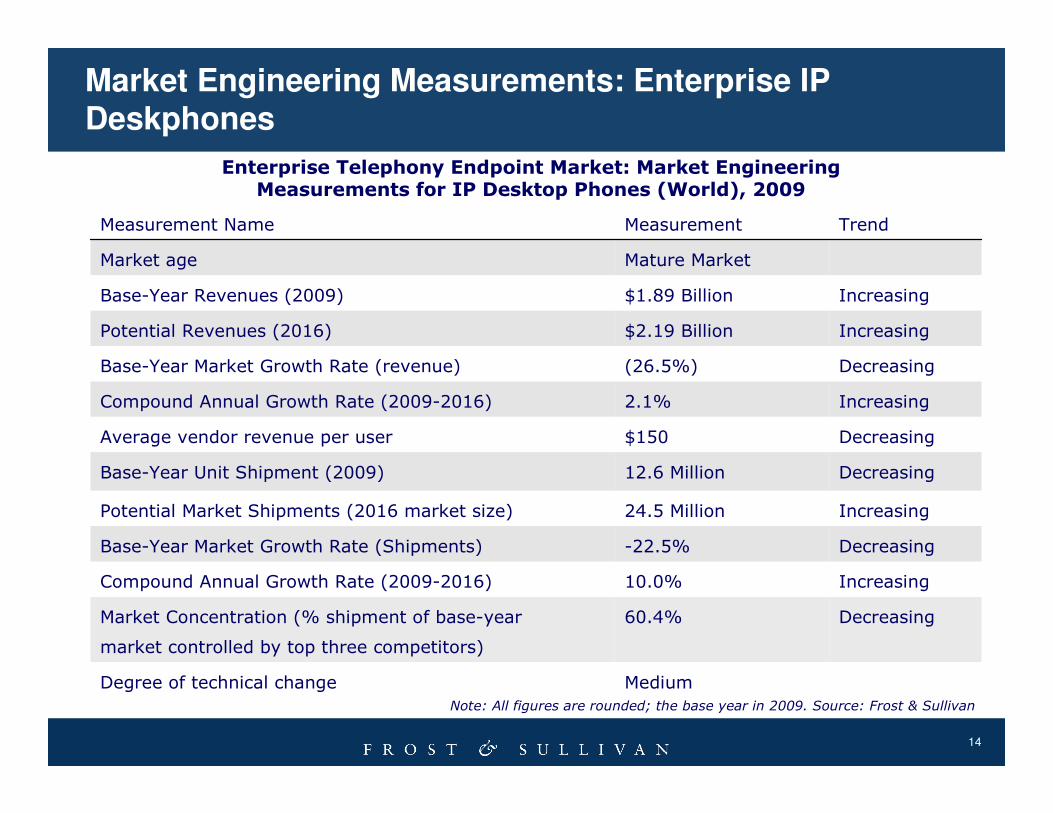

Market Engineering Measurements: Enterprise IP Deskphones

Enterprise Telephony Endpoint Market: Market Engineering Measurements for IP Desktop Phones (World), 2009

Note: All figures are rounded; the base year in 2009. Source: Frost & Sullivan

Decreasing60.4%Market Concentration (% shipment of base-year

market controlled by top three competitors)

Increasing10.0%Compound Annual Growth Rate (2009-2016)

Decreasing-22.5%Base-Year Market Growth Rate (Shipments)

Decreasing(26.5%)Base-Year Market Growth Rate (revenue)

Increasing2.1%Compound Annual Growth Rate (2009-2016)

MediumDegree of technical change

Increasing24.5 MillionPotential Market Shipments (2016 market size)

Decreasing12.6 MillionBase-Year Unit Shipment (2009)

Decreasing$150Average vendor revenue per user

Increasing$2.19 BillionPotential Revenues (2016)

Increasing$1.89 BillionBase-Year Revenues (2009)

Mature MarketMarket age

TrendMeasurementMeasurement Name

15

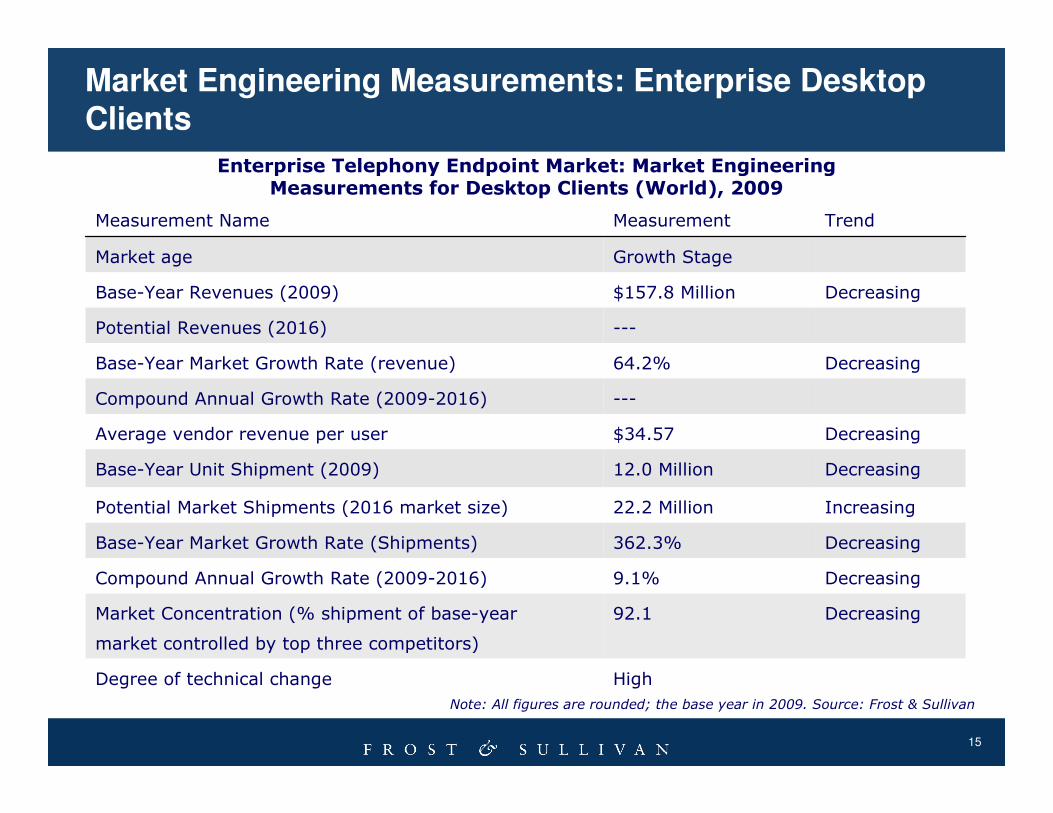

Market Engineering Measurements: Enterprise Desktop Clients

Enterprise Telephony Endpoint Market: Market Engineering Measurements for Desktop Clients (World), 2009

Note: All figures are rounded; the base year in 2009. Source: Frost & Sullivan

Decreasing92.1Market Concentration (% shipment of base-year

market controlled by top three competitors)

Decreasing9.1%Compound Annual Growth Rate (2009-2016)

Decreasing362.3%Base-Year Market Growth Rate (Shipments)

Decreasing64.2%Base-Year Market Growth Rate (revenue)

---Compound Annual Growth Rate (2009-2016)

HighDegree of technical change

Increasing22.2 MillionPotential Market Shipments (2016 market size)

Decreasing12.0 MillionBase-Year Unit Shipment (2009)

Decreasing$34.57Average vendor revenue per user

---Potential Revenues (2016)

Decreasing$157.8 MillionBase-Year Revenues (2009)

Growth StageMarket age

TrendMeasurementMeasurement Name

16

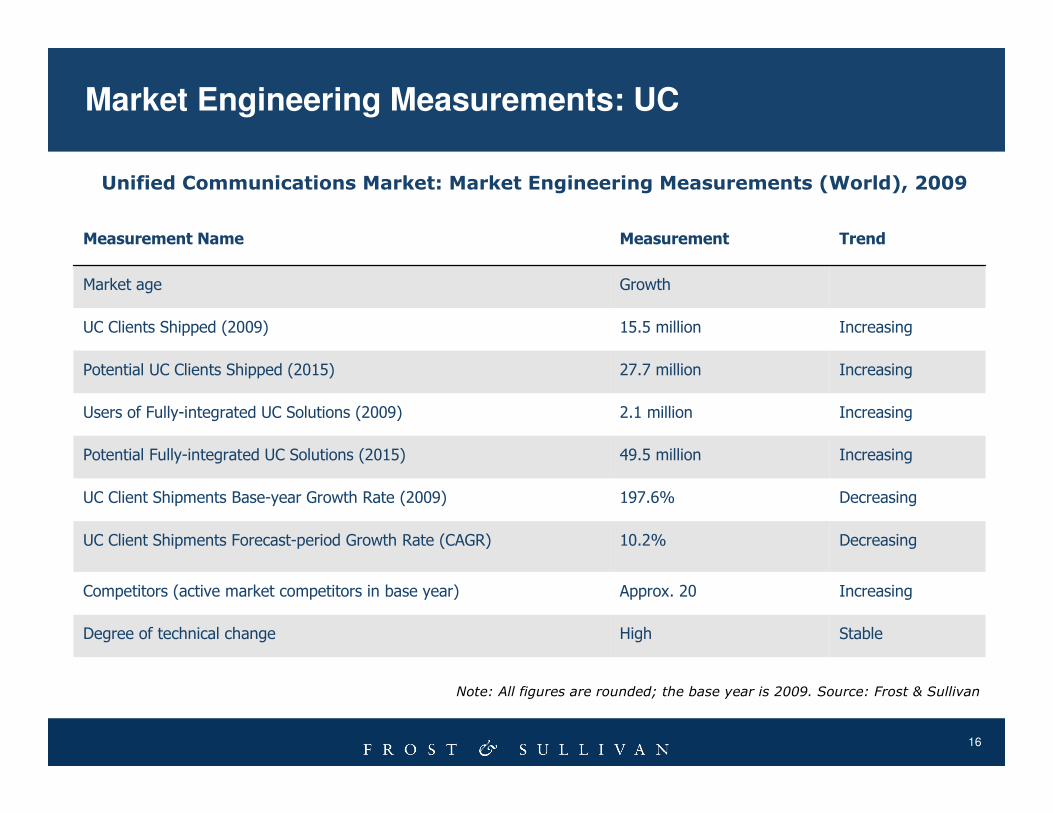

Market Engineering Measurements: UC

Unified Communications Market: Market Engineering Measurements (World), 2009

Note: All figures are rounded; the base year is 2009. Source: Frost & Sullivan

Increasing2.1 millionUsers of Fully-integrated UC Solutions (2009)

Increasing49.5 millionPotential Fully-integrated UC Solutions (2015)

StableHighDegree of technical change

IncreasingApprox. 20Competitors (active market competitors in base year)

Decreasing10.2%UC Client Shipments Forecast-period Growth Rate (CAGR)

Decreasing197.6%UC Client Shipments Base-year Growth Rate (2009)

Increasing27.7 millionPotential UC Clients Shipped (2015)

Increasing15.5 millionUC Clients Shipped (2009)

GrowthMarket age

TrendMeasurementMeasurement Name

17

Hosted UC and SIP Trunking: Cloud Nirvana?

18

Driving Forces: A Dynamic IT Environment

Multiple market forces are coming together to produce a Multiple market forces are coming together to produce a communications market ripe for changecommunications market ripe for change

Rapid convergence of IT Rapid convergence of IT

and communicationsand communications

Emergence of cloud Emergence of cloud

computing helps to enable computing helps to enable

more compelling servicesmore compelling services

Growth in VoIP and Growth in VoIP and

other IPother IP--based based

communicationscommunications

Virtualization and other Virtualization and other

enabling technologies become enabling technologies become

part of value proposition part of value proposition

Inflection Point for Hosted Services is Here

Consolidation occurs as Consolidation occurs as

IP telephony maturesIP telephony matures

Source: Frost & Sullivan

19

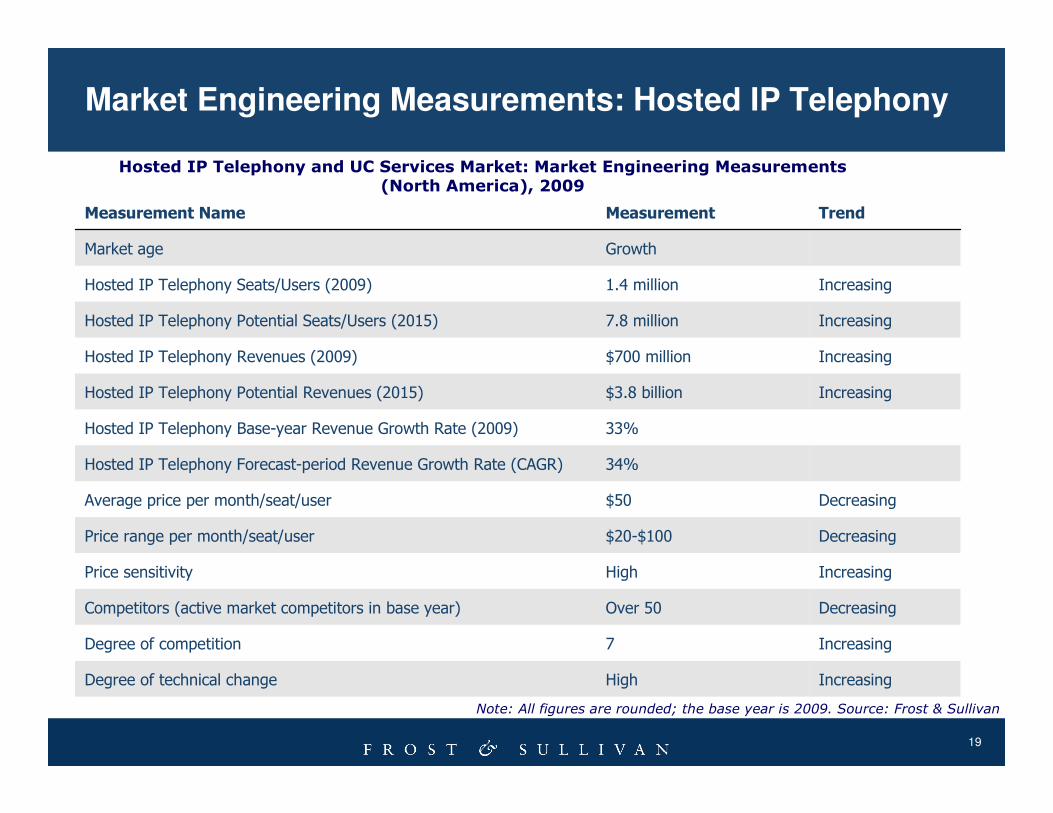

Note: All figures are rounded; the base year is 2009. Source: Frost & Sullivan

Increasing$700 millionHosted IP Telephony Revenues (2009)

Increasing$3.8 billionHosted IP Telephony Potential Revenues (2015)

IncreasingHighDegree of technical change

DecreasingOver 50Competitors (active market competitors in base year)

Increasing7Degree of competition

IncreasingHighPrice sensitivity

Decreasing$20-$100Price range per month/seat/user

Decreasing$50Average price per month/seat/user

34%Hosted IP Telephony Forecast-period Revenue Growth Rate (CAGR)

33%Hosted IP Telephony Base-year Revenue Growth Rate (2009)

Increasing7.8 millionHosted IP Telephony Potential Seats/Users (2015)

Increasing1.4 millionHosted IP Telephony Seats/Users (2009)

GrowthMarket age

TrendMeasurementMeasurement Name

Market Engineering Measurements: Hosted IP Telephony

Hosted IP Telephony and UC Services Market: Market Engineering Measurements (North America), 2009

20

Current State of the Hosted UC Market

Hosted UC is riding the wave

Up to 50,000 seats/users in 2009

A handful of service providers: Alteva, Apptix,

CallTower, Cypress Communications, Engage

Incorporated, LightEdge, USA.NET, Verizon

Two backgrounds:

• hosted/shared-tenant voice service providers

• hosted email/business application providers

Cisco, IBM, Microsoft, Siemens hosting or

planning to host some services in the cloud

themselves.

Two business models: fully hosted and hybrid

Also: private and public cloud

21

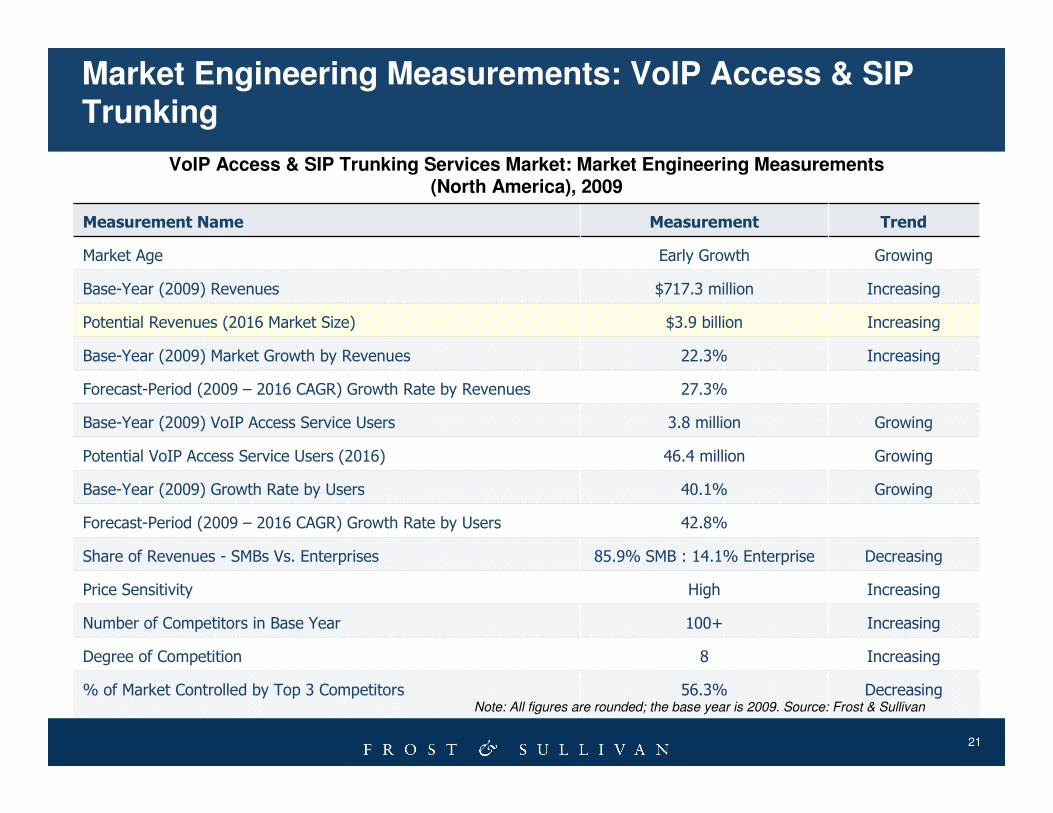

Market Engineering Measurements: VoIP Access & SIP Trunking

Increasing8Degree of Competition

Increasing100+Number of Competitors in Base Year

56.3%

High

85.9% SMB : 14.1% Enterprise

42.8%

40.1%

46.4 million

3.8 million

27.3%

22.3%

$3.9 billion

$717.3 million

Early Growth

Measurement

Forecast-Period (2009 – 2016 CAGR) Growth Rate by Users

DecreasingShare of Revenues - SMBs Vs. Enterprises

IncreasingPrice Sensitivity

GrowingPotential VoIP Access Service Users (2016)

GrowingBase-Year (2009) Growth Rate by Users

IncreasingBase-Year (2009) Market Growth by Revenues

Decreasing

Growing

Increasing

Increasing

Growing

Trend

Forecast-Period (2009 – 2016 CAGR) Growth Rate by Revenues

% of Market Controlled by Top 3 Competitors

Base-Year (2009) VoIP Access Service Users

Potential Revenues (2016 Market Size)

Base-Year (2009) Revenues

Market Age

Measurement Name

VoIP Access & SIP Trunking Services Market: Market Engineering Measurements (North America), 2009

Note: All figures are rounded; the base year is 2009. Source: Frost & Sullivan

22

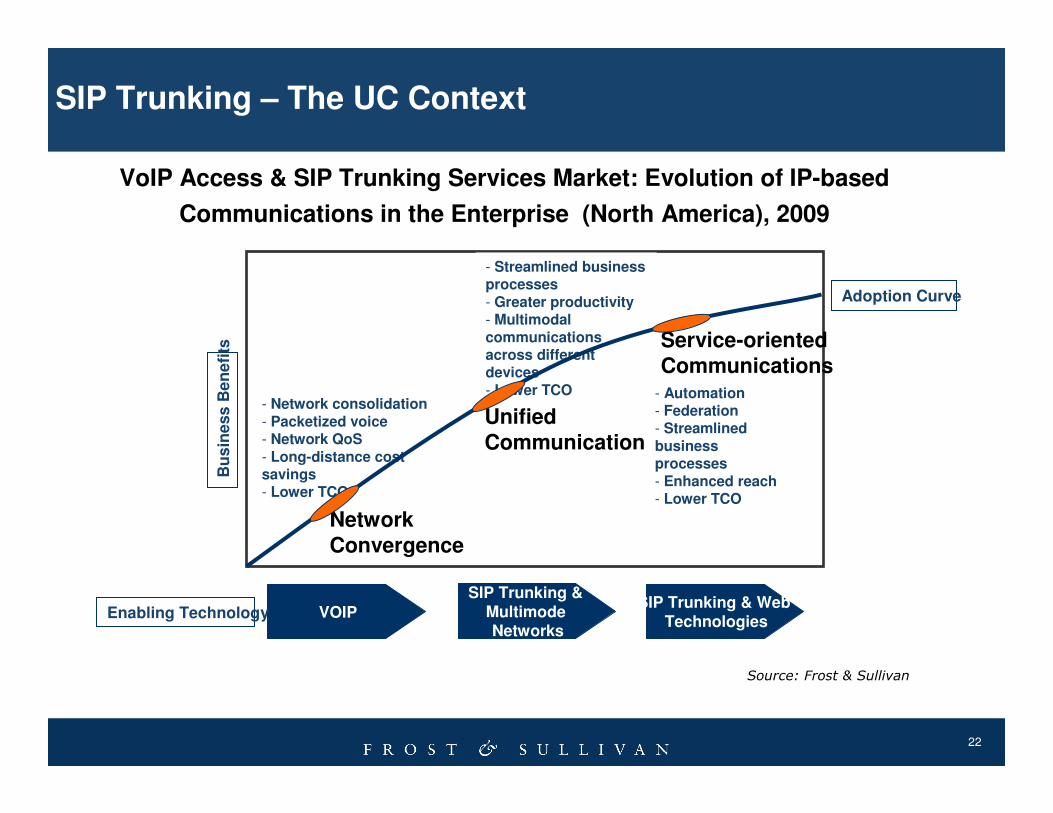

SIP Trunking – The UC Context

Network

Convergence

VOIP

SIP Trunking & Multimode Networks

SIP Trunking & Web Technologies

- Network consolidation

- Packetized voice- Network QoS

- Long-distance cost savings- Lower TCO

Enabling Technology

Bu

sin

ess

Be

ne

fits

Unified

Communications

Service-oriented

Communications

Adoption Curve

- Streamlined business processes

- Greater productivity- Multimodal

communicationsacross different devices

- Lower TCO - Automation- Federation- Streamlined

businessprocesses

- Enhanced reach- Lower TCO

Source: Frost & Sullivan

VoIP Access & SIP Trunking Services Market: Evolution of IP-based

Communications in the Enterprise (North America), 2009

23

Conclusions and Recommendations

24

Sales Strategies and Recommendations

Sell customers on IPT first, then upgrade them to other applications and fully integrated UC.

Open systems are a must to allow customers to future-proof their investments.

Involve more stakeholders than the usual IT or telecom buyers.

Develop the necessary skills to implement UC and advise customers on best practices.

Understand key business processes for your biggest customers or leading industries, and be prepared to help clients implement CEBP for maximum return.

25

Thank You!

Time for Q & A

26

Next Steps

Request a proposal for a Growth Partnership Service to support you and your team to accelerate the growth of your company. ([email protected])1-877-GoFrost (1-877-463-7678)

Join us at our annual Growth, Innovation, and Leadership 2010: Silicone

Valley - A Frost & Sullivan Global Congress on Corporate Growth,

September 12-14 2010, Fairmont Hotel, San Jose, CA (www.gil-global.com)

Register for the next Chairman’s Series on Growth: The CEO’s Growth Partnership: Developing a comprehensive action-based strategy to reinvigorate yourself (Tuesday, July 6) (http://www.frost.com/growth)

Register for Frost & Sullivan’s Growth Opportunity Newsletter and keep abreast of innovative growth opportunities(www.frost.com/news)

27

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

28

Follow Frost & Sullivan on Twitter

http://twitter.com/Frost_Sullivan

Frost & Sullivan on Twitter

29

For Additional Information

Jake Wengroff

Corporate Communications

(210) 247-3806

Elka Popova

Program Director

Unified Communications

(416) 792-0160

Melanie Turek

Principal Analyst

Unified Communications

(970) 871-6110