Embed Size (px)

Citation preview

Life, Pensions, and Investments: What do you want to be famous for?

Becoming the progressive provider of the future

2

3

The UK LP&I marketplace is ripe for change. Digital has arrived, and it’s changing everything, empowering consumers, reshaping their behaviours and presenting opportunities for providers to build new, longer-lasting customer relationships. Driven by the increasing waves of regulation the market is fragmenting. We’re seeing new players emerging and staking their claim to core segments of the traditional LP&I value chain.

With every area of their marketplace being disrupted, providers are reassessing distribution arrangements, changing product propositions and targeting operational excellence across their operations. These are all core priorities, but they come second place to what must be the overriding objective from now on – ensuring an in-depth understanding of each consumer journeys and expectations, identifying where long-term value can be generated in each one, and developing the capabilities that will be needed to achieve this goal.

LP&I providers that fail to address this priority will risk being sidelined as ‘financial utilities’ and/or becoming increasingly disconnected from customer needs (and being perceived as slow to react to fast-changing shifts in the marketplace).

To help them navigate their journeys towards becoming the ‘progressive providers of the future’, we’ve used this study to identify what we believe to be the key forces of disruption in the LP&I market over the next 10 years – as well as the business models that can be adopted to seize opportunity from these ‘disrupters’ and build value for the long term.

What do you want to be famous for?

Executive summary

4

Driven mainly by government reforms to the pensions industry, there’s been a significant drop in investor premium over the past 12 months. Figure 1 highlights this trend, showing a 5 per cent drop in the UK average in March 2014, coinciding with the UK Budget announcements of pensions reforms, and a 12 per cent drop during July and August, when further announcements of reforms to annuities were made.

Clearly, investor confidence has declined and expectations for the future value of LP&I companies have now been reset at a lower level. It’s apparent that while they remain positive about short-term prospects for the industry, investors are less certain about where providers are headed in the long term.

While they are setting off from a different position and with a different dynamic, LP&I providers are all facing a future that will be reshaped and driven by a number of common trends. To rebuild confidence in their operations as sustainable businesses, it’s essential for each one of them to demonstrate exactly how they plan to build value for the long term.

Investors’ reduced expectations of future performance are the result of a steady erosion of the traditional LP&I business model. Each time a new regulatory announcement is made, every stage of the LP&I value chain is affected – from fund management, front- and back-office processing and marketing through to distribution.

Of course, while it is a key influence, regulation is far from being the only driver of change. The LP&I landscape is also being transformed by a range of other factors. Shifting customer expectations and behaviours are driving providers to rethink customer segmentation, the arrival of new competitors recalibrates the market dynamic, and changing revenue streams and evolving cost structures impact established business models.

Marketing, CRM and distribution must adapt to a new demographic, with longer life expectancies and improvements in long-term health combining with increased spending on retirement and limited awareness of what LP&I providers have to offer. At a high level, customers do not trust the industry, nor do they find providers easy to deal with. Accenture research shows that the insurance industry currently ranks below many other sectors on both of those issues1. Indeed, our study found more consumers agree that banks are trustworthy and easy to deal with. This explains, at least in part, the high level of consumer disengagement with LP&I providers. Having remained stagnant over the years, barely shifting since our 2011 survey, customer satisfaction and recommendation levels are now lower for LP&I than for any other financial services sector2.

Along with this continuing evidence of disengagement and cynicism, customers are becoming increasingly dissatisfied as providers fail to meet their expectations across a number of vital areas – from the clarity and simplicity of products to digital servicing capabilities3. Crucially too, the use of channels is in flux. This is partly because old advisor models have been transformed by the Retail Distribution Review (RDR), which resulted in a significant decrease in IFA numbers and a decline in Bancassurance as a proportion of new business. At the same time, weak customer relationships are giving increasing cause for concern: some 70 per cent of LP&I customers say they have had no contact with their provider in the past 12 months4.

Auto-enrolment means that new front- and back-office processes and services are needed, creating additional costs for employers and LP&I providers. Some companies have already achieved success in this area. L&G, for example, has enrolled over 500,000 new members into company schemes since staging started in 2013 (due, in large part, to early staging dates, along with automated and straight-through processing of auto enrolment processes). More widely, lessons can be learned from the Australian experience which underlined the importance of providing automated offerings that can deliver relevant solutions at acceptable price points.

Introduction: Making the case for changeWhile UK LP&I providers have lived with near-constant change for the past 30 years, we believe an inflection point has now been reached.

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

L&G - 1.01Aviva - 0.98

Standard Life - 1.10

Friends Life - 0.70

Prudential - 0.91

Evolution of Price to Tangible Book Value, 2014Rebased, 1 Jan to 22 Oct

22nd MarchUK Budget

5% Drop on UK Ave.

1 Jan 1 Feb 1 Mar 1 Apr 1 May 1 Jun 1 Jul 1 Aug 1 Sep 1 Oct 1 Nov

12% Drop on UK Ave.

July - AugustFurther annuities reform announcements

5

Figure 1: Decline in LP&I investor premium

Every area of the value chain is under pressure from asymmetric growth in the industry, with new platform providers expanding their asset base and new market entrants hitting the UK stage. Changing revenue streams are a fact of life too, with the UK’s contribution to global premiums in decline, annuity sales collapsing and savings near historic lows. And, of course, diminished profits and increasing administrative costs present persistent and continual challenges to existing business models.

1 Accenture’s 2014 UK Financial Services Customer Survey: UK Life & Pensions: Winning the race for relevance with insurance customers.

2 ibid.

3 Accenture’s 2014 UK Financial Services Customer Survey: UK Life & Pensions: Winning the race for relevance with insurance customers.

4 Accenture’s 2014 UK Financial Services Customer Survey: UK Life & Pensions: Winning the race for relevance with insurance customers.

6

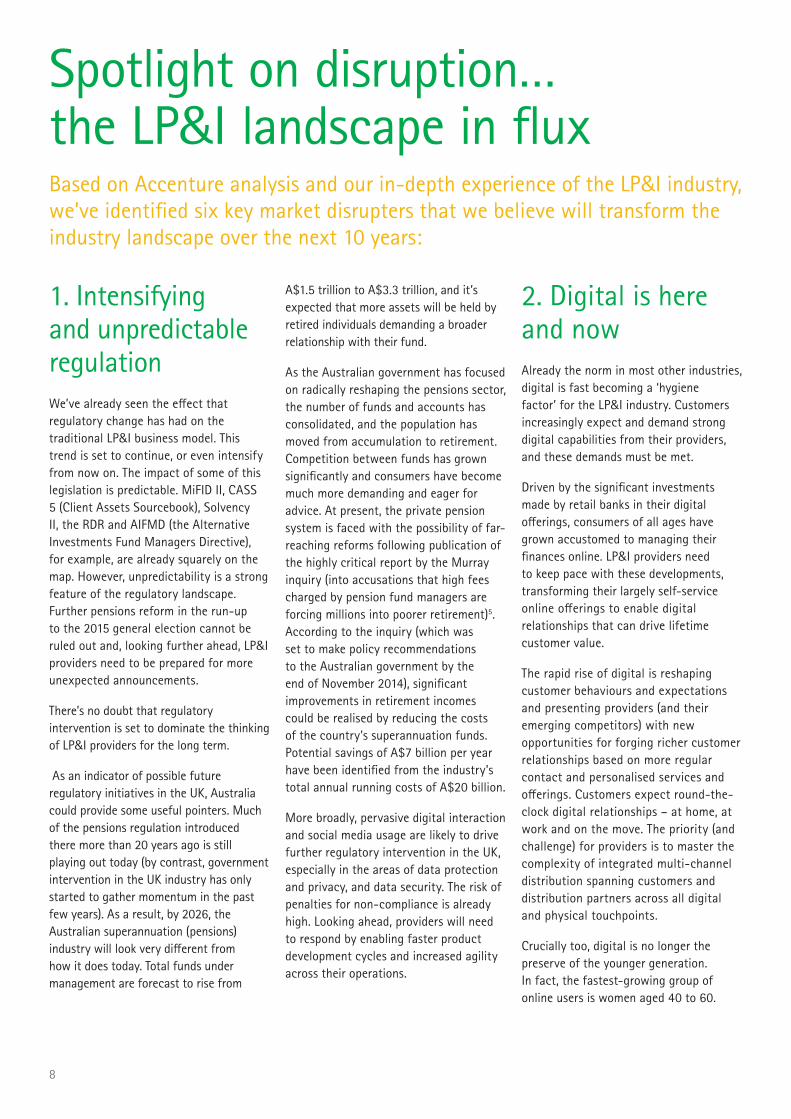

Challenges with current business models by value chain component

Changes to customer segments• Health improving: Health of pensioners flat in 20 year period• But retirement more costly: Spending on retirement grown at 8%• And limited awareness: 55% of L&P customers have never

sought advice

Fund Management Front O�ce Processing Back O�ce Processing Marketing / CRM Distribution

Opportunities and threats from partners• Asymmetric growth; Growth of new platform providers; e.g. Hargreaves have grown asset base to c.£500bn (est.) by 2015 (vs. £40bn in 2001)• New entrants’ BlackRock intend to start o�ering US products such as LifePath

Evolving cost structures• Persistent cost pressures: Operating Profit / NPE from 63.8% to 61.5% from 2008 – 2012 • Increase of Admin Costs: As a / NPE of 10% CAGR from 2008 – 2012 due to expense of managing legacy positions

Changing revenue streams• Shrinking place on the global stage: UK contribution to Global Premiums declined 10.1% CAGR from 2007 – 2012• Annuity sales collapse; for some, 2014 Q3 quarter-on-quarter sales down 50% and down 75% year-on-year• Savings are near historic lows: households only save around 4.8% of their incomes with less being held in cash savings than in the past• Over-reliance on volatile investment income: 4.4% contribution to income growth from 2003 – 12)

Evolving relationship with customers• Distribution models changing: Integrated distribution

sales force numbers are down 18% CAGR• Consumers not engaged; 40% of customers thinking

L&P are too complicated and confusing

Use of channels• Old adviser models disrupted; Bancassurance dropped from 11.7% of new business to 5.1% as

a result of RDR• Weak customer relationships; 70% of L&P customers

have had no contact with provider in last 12 months

Changing activities• New processes and services needed;

Auto-enrolment has created an additional cost for both employers and L&P providers through having to set up new services (e.g. Aviva Auto-enrolment Planner / Modeller)

Figure 2: Challenges across the LP&I value chain

Highlighted in Figure 2, these various factors are placing enormous stress on the entire LP&I value chain. With this in mind, it’s clear that incremental change programmes are no longer enough. Instead, the time for bold and decisive change has arrived. For organisations that show themselves willing to step up and seize the initiative, the scale of opportunity is enormous.

We believe that providers must take action now – first by deciding exactly what they want to be famous for in the new LP&I marketplace, and then by identifying the new business model that will position them as the progressive LP&I provider of the future. To help providers map out this journey, we’ve identified what we believe to be the principal sources of disruption

for the industry from now on, before identifying the new business models that we believe will emerge to respond to these ‘market disrupters’.

7

8

1. Intensifying and unpredictable regulationWe’ve already seen the effect that regulatory change has had on the traditional LP&I business model. This trend is set to continue, or even intensify from now on. The impact of some of this legislation is predictable. MiFID II, CASS 5 (Client Assets Sourcebook), Solvency II, the RDR and AIFMD (the Alternative Investments Fund Managers Directive), for example, are already squarely on the map. However, unpredictability is a strong feature of the regulatory landscape. Further pensions reform in the run-up to the 2015 general election cannot be ruled out and, looking further ahead, LP&I providers need to be prepared for more unexpected announcements.

There’s no doubt that regulatory intervention is set to dominate the thinking of LP&I providers for the long term.

As an indicator of possible future regulatory initiatives in the UK, Australia could provide some useful pointers. Much of the pensions regulation introduced there more than 20 years ago is still playing out today (by contrast, government intervention in the UK industry has only started to gather momentum in the past few years). As a result, by 2026, the Australian superannuation (pensions) industry will look very different from how it does today. Total funds under management are forecast to rise from

A$1.5 trillion to A$3.3 trillion, and it’s expected that more assets will be held by retired individuals demanding a broader relationship with their fund.

As the Australian government has focused on radically reshaping the pensions sector, the number of funds and accounts has consolidated, and the population has moved from accumulation to retirement. Competition between funds has grown significantly and consumers have become much more demanding and eager for advice. At present, the private pension system is faced with the possibility of far-reaching reforms following publication of the highly critical report by the Murray inquiry (into accusations that high fees charged by pension fund managers are forcing millions into poorer retirement)5. According to the inquiry (which was set to make policy recommendations to the Australian government by the end of November 2014), significant improvements in retirement incomes could be realised by reducing the costs of the country’s superannuation funds. Potential savings of A$7 billion per year have been identified from the industry’s total annual running costs of A$20 billion.

More broadly, pervasive digital interaction and social media usage are likely to drive further regulatory intervention in the UK, especially in the areas of data protection and privacy, and data security. The risk of penalties for non-compliance is already high. Looking ahead, providers will need to respond by enabling faster product development cycles and increased agility across their operations.

2. Digital is here and now Already the norm in most other industries, digital is fast becoming a ‘hygiene factor’ for the LP&I industry. Customers increasingly expect and demand strong digital capabilities from their providers, and these demands must be met.

Driven by the significant investments made by retail banks in their digital offerings, consumers of all ages have grown accustomed to managing their finances online. LP&I providers need to keep pace with these developments, transforming their largely self-service online offerings to enable digital relationships that can drive lifetime customer value.

The rapid rise of digital is reshaping customer behaviours and expectations and presenting providers (and their emerging competitors) with new opportunities for forging richer customer relationships based on more regular contact and personalised services and offerings. Customers expect round-the-clock digital relationships – at home, at work and on the move. The priority (and challenge) for providers is to master the complexity of integrated multi-channel distribution spanning customers and distribution partners across all digital and physical touchpoints.

Crucially too, digital is no longer the preserve of the younger generation. In fact, the fastest-growing group of online users is women aged 40 to 60.

Spotlight on disruption… the LP&I landscape in fluxBased on Accenture analysis and our in-depth experience of the LP&I industry, we’ve identified six key market disrupters that we believe will transform the industry landscape over the next 10 years:

9

Providers need digital to appeal to all of their customers and should focus on designing highly usable digital offerings that meet the requirements of every age group. As they do so, other trends must be taken into account. Social media is no fad. Emphatically here to stay, it presents opportunities for providers to enhance and strengthen their relationships with consumers. And with the desire for personalisation and relevance on the rise, providers can respond by using smart location technology to develop location-based loyalty and reward schemes.

The bottom line? Far from being an add-on option, digital is becoming integral to the entire customer journey.

3. The changing consumerEmpowered and emboldened by digital, a new breed of customer is emerging, driven by the belief that there are better deals on offer, and better ways of making savings and investment products work for them at different stages in their life journeys.

Customers are becoming less brand loyal, more price savvy and increasingly comfortable buying products through

digital and/or non-traditional players. What’s driving these new behaviours? Along with technology innovation, we’re seeing increasing competition from other market segments (e.g. retailers including Marks & Spencer, Sainsbury’s and Tesco) and declining trust in traditional financial services providers.

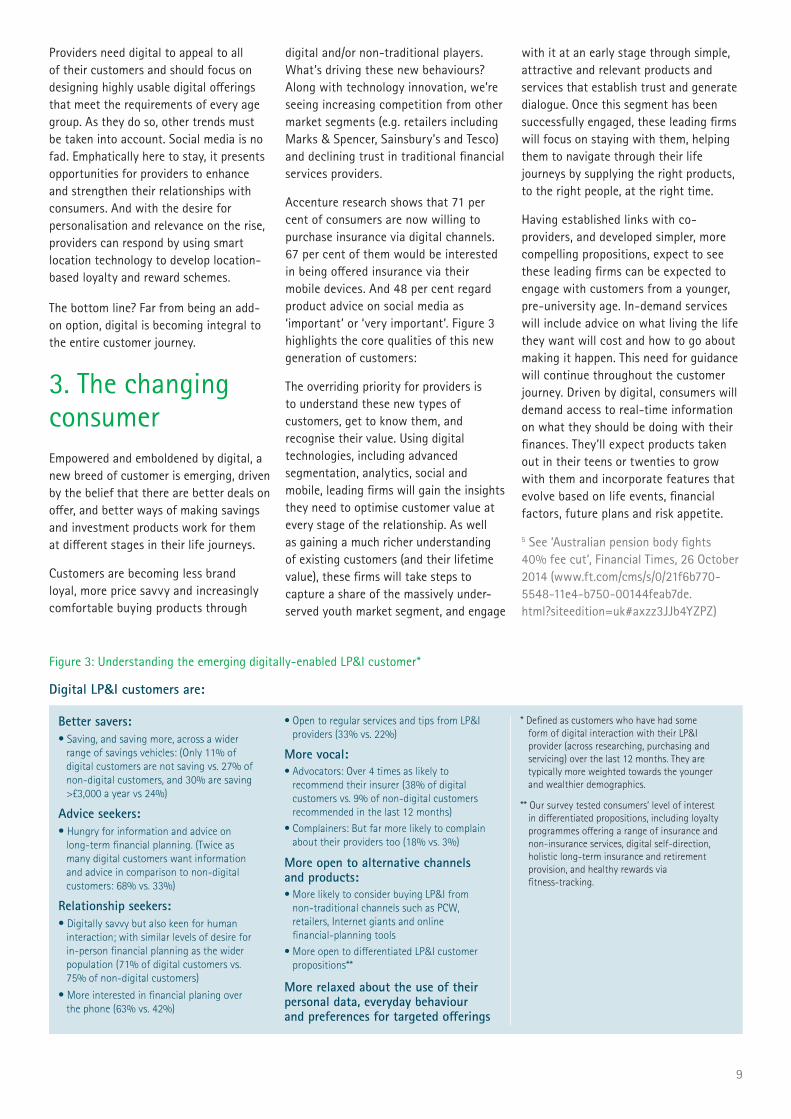

Accenture research shows that 71 per cent of consumers are now willing to purchase insurance via digital channels. 67 per cent of them would be interested in being offered insurance via their mobile devices. And 48 per cent regard product advice on social media as ‘important’ or ‘very important’. Figure 3 highlights the core qualities of this new generation of customers:

The overriding priority for providers is to understand these new types of customers, get to know them, and recognise their value. Using digital technologies, including advanced segmentation, analytics, social and mobile, leading firms will gain the insights they need to optimise customer value at every stage of the relationship. As well as gaining a much richer understanding of existing customers (and their lifetime value), these firms will take steps to capture a share of the massively under-served youth market segment, and engage

with it at an early stage through simple, attractive and relevant products and services that establish trust and generate dialogue. Once this segment has been successfully engaged, these leading firms will focus on staying with them, helping them to navigate through their life journeys by supplying the right products, to the right people, at the right time.

Having established links with co-providers, and developed simpler, more compelling propositions, expect to see these leading firms can be expected to engage with customers from a younger, pre-university age. In-demand services will include advice on what living the life they want will cost and how to go about making it happen. This need for guidance will continue throughout the customer journey. Driven by digital, consumers will demand access to real-time information on what they should be doing with their finances. They’ll expect products taken out in their teens or twenties to grow with them and incorporate features that evolve based on life events, financial factors, future plans and risk appetite.

5 See ‘Australian pension body fights 40% fee cut’, Financial Times, 26 October 2014 (www.ft.com/cms/s/0/21f6b770-5548-11e4-b750-00144feab7de.html?siteedition=uk#axzz3JJb4YZPZ)

Figure 3: Understanding the emerging digitally-enabled LP&I customer*

Better savers:• Saving, and saving more, across a wider

range of savings vehicles: (Only 11% of digital customers are not saving vs. 27% of non-digital customers, and 30% are saving >£3,000 a year vs 24%)

Advice seekers:• Hungry for information and advice on

long-term financial planning. (Twice as many digital customers want information and advice in comparison to non-digital customers: 68% vs. 33%)

Relationship seekers:• Digitally savvy but also keen for human

interaction; with similar levels of desire for in-person financial planning as the wider population (71% of digital customers vs. 75% of non-digital customers)

• More interested in financial planing over the phone (63% vs. 42%)

• Open to regular services and tips from LP&I providers (33% vs. 22%)

More vocal:• Advocators: Over 4 times as likely to

recommend their insurer (38% of digital customers vs. 9% of non-digital customers recommended in the last 12 months)

• Complainers: But far more likely to complain about their providers too (18% vs. 3%)

More open to alternative channels and products:• More likely to consider buying LP&I from

non-traditional channels such as PCW, retailers, Internet giants and online financial-planning tools

• More open to di�erentiated LP&I customer propositions**

More relaxed about the use of their personal data, everyday behaviour and preferences for targeted o�erings

* Defined as customers who have had some form of digital interaction with their LP&I provider (across researching, purchasing and servicing) over the last 12 months. They are typically more weighted towards the younger and wealthier demographics.

** Our survey tested consumers’ level of interest in di�erentiated propositions, including loyalty programmes o�ering a range of insurance and non-insurance services, digital self-direction, holistic long-term insurance and retirement provision, and healthy rewards via fitness-tracking.

Digital LP&I customers are:

10

4. Re-emergence of the workplaceBy 2025, expect to see the workplace re-established as a key marketplace – and employers recognised as key consumers in their own right. Until now, the retraction of defined benefit schemes has seen workplace pensions declining in significance. No longer. Due to auto-enrolment, as well as recent and ongoing pension reforms, and employers seeking to motivate/ retain employees, the provision of pension schemes for employers is set to be a priority growth area.

From now on, we expect to see a number of mega-trends in the UK combining to position the workplace as the gateway to the mass market:

• The economy – strained household incomes in a low-growth environment, a shortfall in retirement, and inadequate levels of financial literacy will combine with employers seeking new ways to attract and retain talent to drive uptake in workplace pensions

• Distribution channels – closure of advisory arms in high street banks and/or the high cost of obtaining advice will limit the availability of mass market advice; at the same time, providers will be attracted towards lower-cost distribution models, and IFAs will be driven to explore advice opportunities beyond the mass market in order to build recurring revenue streams

• Consumers – lack of trust in financial services institutions and the desire for ease of access to financial information (if possible, from a single source) will add to the importance of the workplace as a key channel

• Digital – consumers’ increasing confidence in technology to self-serve in research, advice and policy management will give employers a strong hand in providing easily administered workplace pension solutions

• Regulation – increased engagement from the regulators in workplace pensions reforms (e.g. auto enrolment and NESTs) will continue to drive the resurgence of the workplace channel.

The onus will be on providers to offer a compelling workplace proposition above and beyond a workplace pension. Various opportunities will arise. Employers will need education in the value of workplace schemes; add-on services will win loyalty, from aggregate bicycle schemes, to gym membership and linked discounts; and more focus will be needed on the savings benefits provided by collective purchasing of savings, investments and other financial products.

Employee benefits platforms will have an essential role to play. And while this market is still in the early stages of development, with few ‘full’ platforms available, some initiatives have already scored notable successes in this area. BenPal, JLT’s international online employee benefits management system, is one of them6. Now deployed in 12 countries and used by over 150

companies to securely communicate employee benefits to over 300,000 employees, BenPal is designed to provide users with 24/7 control of their benefits. Bringing together benefits information in one place, the system makes it easy for employers and employees to see accurate information about benefits at any time. Extremely flexible, it can also be used to communicate and administer total reward statements, fixed, voluntary and/or flexible style employee benefits.

5. Fierce competitionTraditional LP&I providers are already under attack from non-core adjacent competitors (e.g. Hargreaves Lansdown becoming a major product provider in its own right), as well as from non-standard customer-focused competitors such as Tesco and Sainsbury’s. Looking ahead, as the pace of change accelerates, expect to see disruptive new competition from online platforms like Amazon and Google.

Competition from now on will only become more fierce. Increasing disintermediation of providers by asset managers, distributors and new platforms will intensify pressure right across the LP&I value chain. As customer relationships are identified as a major source of value, traditional distinctions between players in this marketplace will begin to dissolve. Forthcoming regulation is set to further blur value chain boundaries and allow non-core competition to stake a claim to a slice of the profits.

Figure 4: The new LP&I ecosystem – putting the customer front and centre

CONTINUOUSMONITORING

BETTEROUTCOMES

EVERYWHERE24/7

COMMUNITIES

PERSONAL IS AT ION & C US TOMER C E N TR IC I T Y

RISK ASSESSMENT& CAPITALMANAGEMENT

PREFERREDDIGITAL PLATFORMS

INSIGHT-DRIVENACTIONS

My DataL IF E S T Y L E

C OL L ABOR AT IONINSIGHTACTION

CONTINUOUUSSMONITORIOR NNGG

SOC IAL

INDUS T RY

BEHAV IOUR

PARTNERSHIPSHE ALT H RISK

VALUE ADDED SERVICES & PARTNERSHIPS

OPTIMISEDSUPPLY CHAIN

SUPERIORSERVICE

“PROTECT ME”

C ON T INUOUS INNOVAT ION

InsurersDigital

GOV ERNMEN T

11

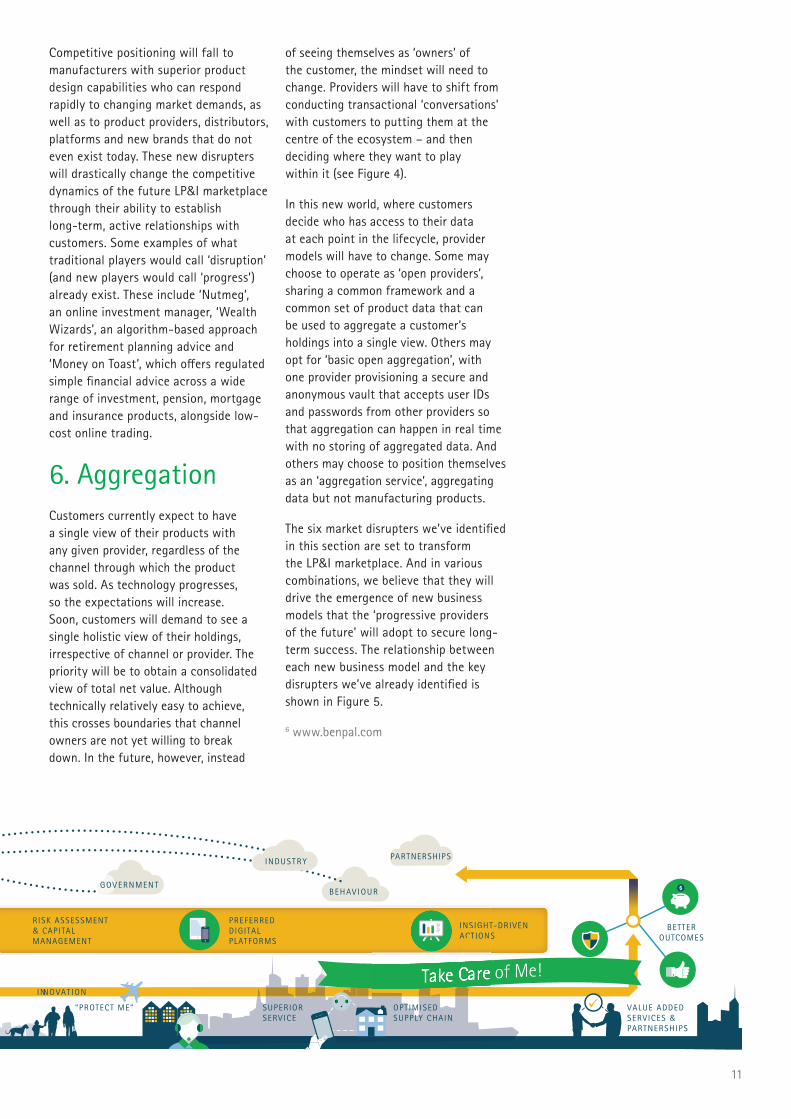

Competitive positioning will fall to manufacturers with superior product design capabilities who can respond rapidly to changing market demands, as well as to product providers, distributors, platforms and new brands that do not even exist today. These new disrupters will drastically change the competitive dynamics of the future LP&I marketplace through their ability to establish long-term, active relationships with customers. Some examples of what traditional players would call ‘disruption’ (and new players would call ‘progress’) already exist. These include ‘Nutmeg’, an online investment manager, ‘Wealth Wizards’, an algorithm-based approach for retirement planning advice and ‘Money on Toast’, which offers regulated simple financial advice across a wide range of investment, pension, mortgage and insurance products, alongside low-cost online trading.

6. AggregationCustomers currently expect to have a single view of their products with any given provider, regardless of the channel through which the product was sold. As technology progresses, so the expectations will increase. Soon, customers will demand to see a single holistic view of their holdings, irrespective of channel or provider. The priority will be to obtain a consolidated view of total net value. Although technically relatively easy to achieve, this crosses boundaries that channel owners are not yet willing to break down. In the future, however, instead

of seeing themselves as ‘owners’ of the customer, the mindset will need to change. Providers will have to shift from conducting transactional ‘conversations’ with customers to putting them at the centre of the ecosystem – and then deciding where they want to play within it (see Figure 4).

In this new world, where customers decide who has access to their data at each point in the lifecycle, provider models will have to change. Some may choose to operate as ‘open providers’, sharing a common framework and a common set of product data that can be used to aggregate a customer’s holdings into a single view. Others may opt for ‘basic open aggregation’, with one provider provisioning a secure and anonymous vault that accepts user IDs and passwords from other providers so that aggregation can happen in real time with no storing of aggregated data. And others may choose to position themselves as an ‘aggregation service’, aggregating data but not manufacturing products.

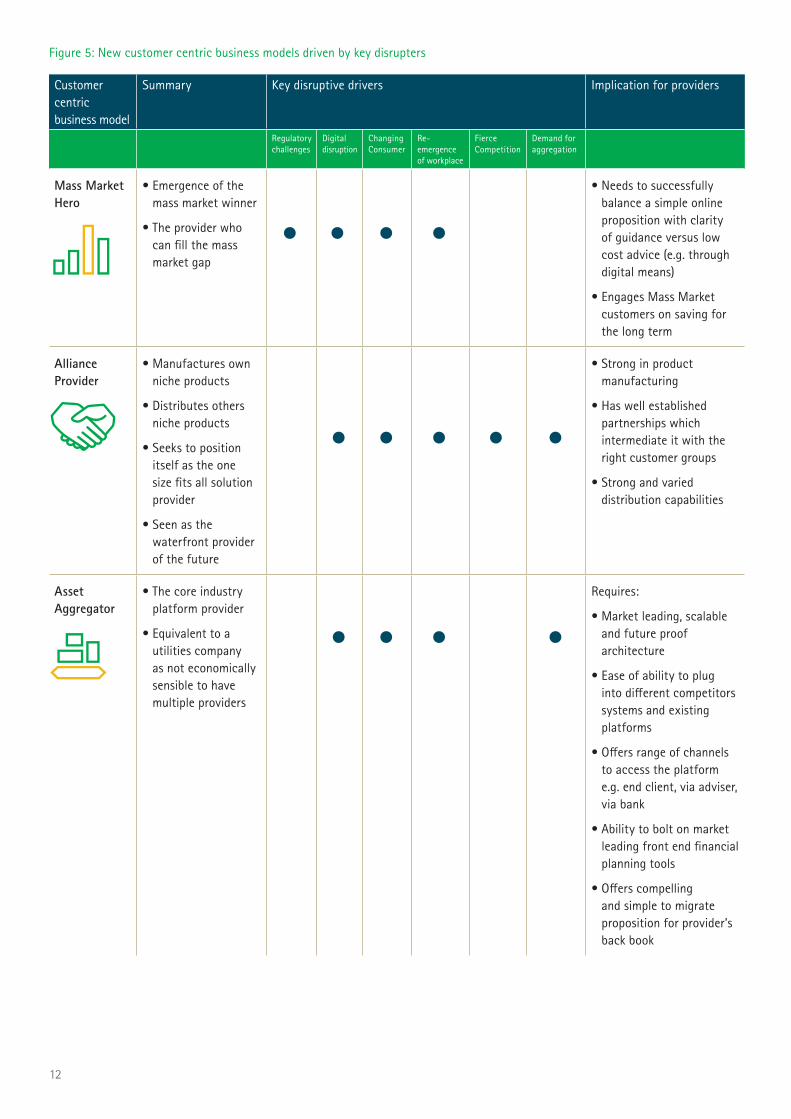

The six market disrupters we’ve identified in this section are set to transform the LP&I marketplace. And in various combinations, we believe that they will drive the emergence of new business models that the ‘progressive providers of the future’ will adopt to secure long-term success. The relationship between each new business model and the key disrupters we’ve already identified is shown in Figure 5.

6 www.benpal.com

CONTINUOUSMONITORING

BETTEROUTCOMES

EVERYWHERE24/7

COMMUNITIES

PERSONAL IS AT ION & C US TOMER C E N TR IC I T Y

RISK ASSESSMENT& CAPITALMANAGEMENT

PREFERREDDIGITAL PLATFORMS

INSIGHT-DRIVENACTIONS

My DataL IF E S T Y L E

C OL L ABOR AT IONINSIGHTACTION

CONTINUOUUSSMONITORIOR NNGG

SOC IAL

INDUS T RY

BEHAV IOUR

PARTNERSHIPSHE ALT H RISK

VALUE ADDED SERVICES & PARTNERSHIPS

OPTIMISEDSUPPLY CHAIN

SUPERIORSERVICE

“PROTECT ME”

C ON T INUOUS INNOVAT ION

InsurersDigital

GOV ERNMEN T

12

Customer centric business model

Summary Key disruptive drivers Implication for providers

Regulatory challenges

Digital disruption

Changing Consumer

Re-emergence of workplace

Fierce Competition

Demand for aggregation

Mass Market Hero

• Emergence of the mass market winner

• The provider who can fill the mass market gap

• Needs to successfully balance a simple online proposition with clarity of guidance versus low cost advice (e.g. through digital means)

• Engages Mass Market customers on saving for the long term

Alliance Provider

• Manufactures own niche products

• Distributes others niche products

• Seeks to position itself as the one size fits all solution provider

• Seen as the waterfront provider of the future

• Strong in product manufacturing

• Has well established partnerships which intermediate it with the right customer groups

• Strong and varied distribution capabilities

Asset Aggregator

• The core industry platform provider

• Equivalent to a utilities company as not economically sensible to have multiple providers

Requires:

• Market leading, scalable and future proof architecture

• Ease of ability to plug into different competitors systems and existing platforms

• Offers range of channels to access the platform e.g. end client, via adviser, via bank

• Ability to bolt on market leading front end financial planning tools

• Offers compelling and simple to migrate proposition for provider’s back book

Figure 5: New customer centric business models driven by key disrupters

13

Customer centric business model

Summary Key disruptive drivers Implication for providers

Regulatory challenges

Digital disruption

Changing Consumer

Re-emergence of workplace

Fierce Competition

Demand for aggregation

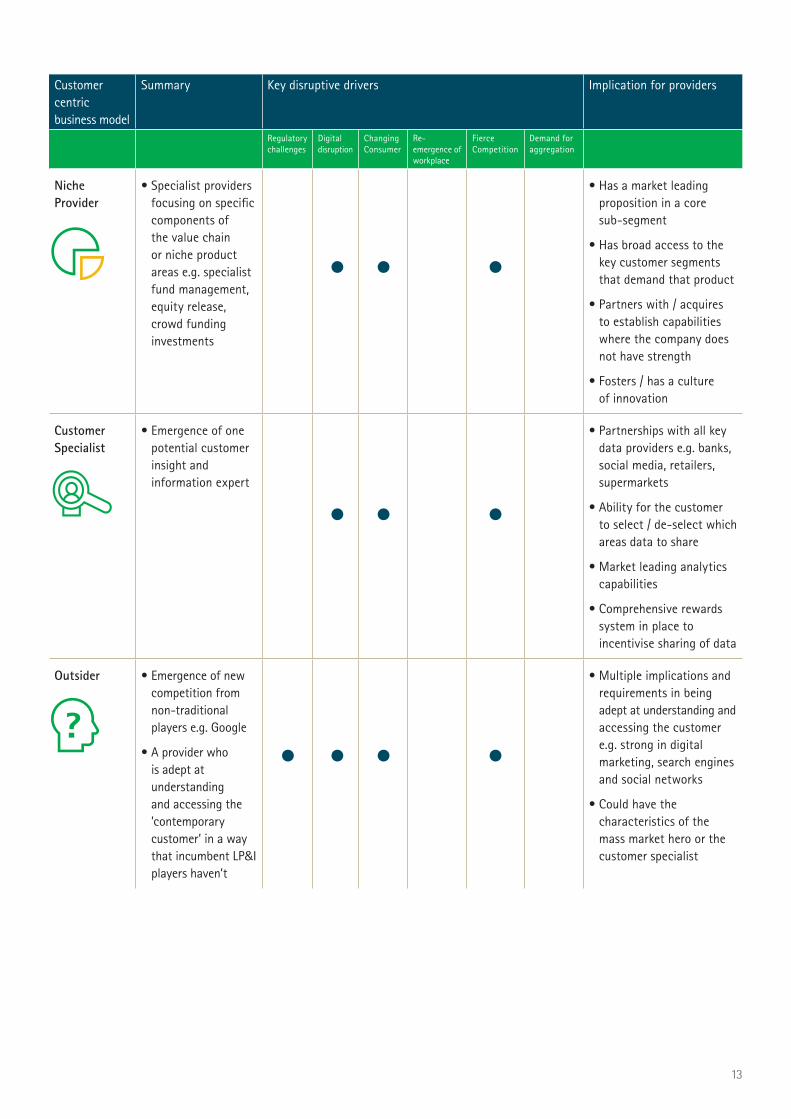

Niche Provider

• Specialist providers focusing on specific components of the value chain or niche product areas e.g. specialist fund management, equity release, crowd funding investments

• Has a market leading proposition in a core sub-segment

• Has broad access to the key customer segments that demand that product

• Partners with / acquires to establish capabilities where the company does not have strength

• Fosters / has a culture of innovation

Customer Specialist

• Emergence of one potential customer insight and information expert

• Partnerships with all key data providers e.g. banks, social media, retailers, supermarkets

• Ability for the customer to select / de-select which areas data to share

• Market leading analytics capabilities

• Comprehensive rewards system in place to incentivise sharing of data

Outsider • Emergence of new competition from non-traditional players e.g. Google

• A provider who is adept at understanding and accessing the ’contemporary customer’ in a way that incumbent LP&I players haven’t

• Multiple implications and requirements in being adept at understanding and accessing the customer e.g. strong in digital marketing, search engines and social networks

• Could have the characteristics of the mass market hero or the customer specialist

14

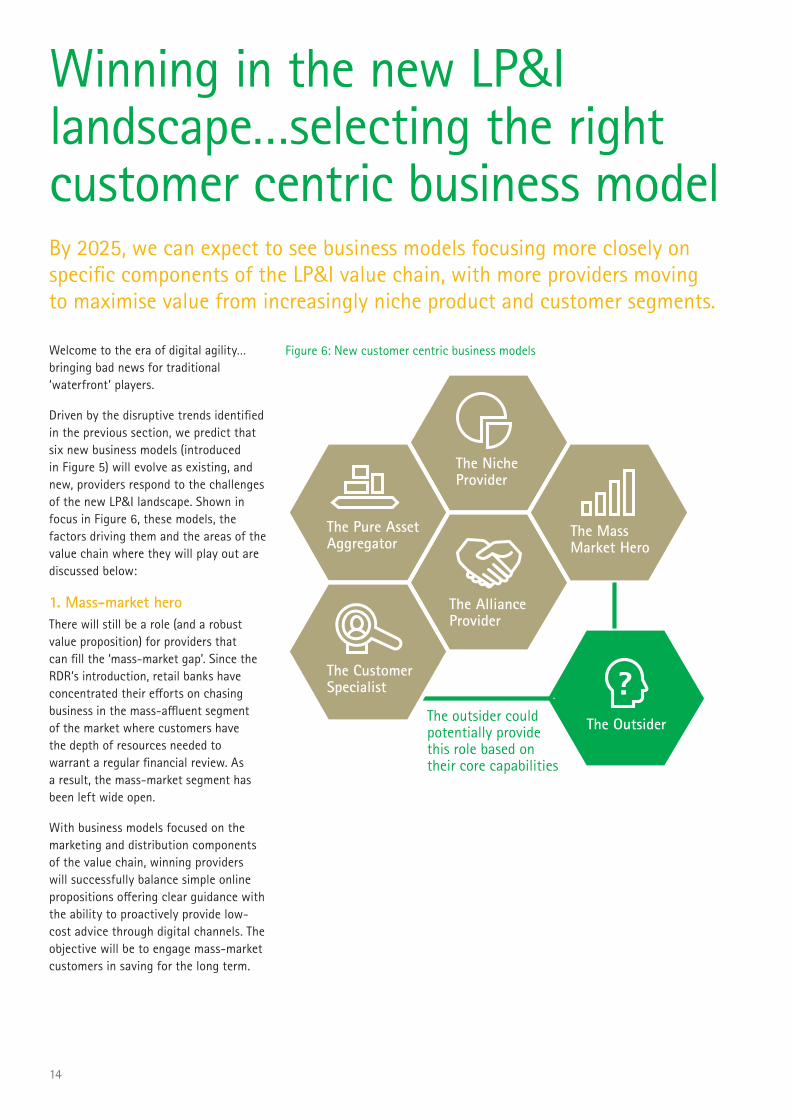

Welcome to the era of digital agility…bringing bad news for traditional ‘waterfront’ players.

Driven by the disruptive trends identified in the previous section, we predict that six new business models (introduced in Figure 5) will evolve as existing, and new, providers respond to the challenges of the new LP&I landscape. Shown in focus in Figure 6, these models, the factors driving them and the areas of the value chain where they will play out are discussed below:

1. Mass-market heroThere will still be a role (and a robust value proposition) for providers that can fill the ‘mass-market gap’. Since the RDR’s introduction, retail banks have concentrated their efforts on chasing business in the mass-affluent segment of the market where customers have the depth of resources needed to warrant a regular financial review. As a result, the mass-market segment has been left wide open.

With business models focused on the marketing and distribution components of the value chain, winning providers will successfully balance simple online propositions offering clear guidance with the ability to proactively provide low-cost advice through digital channels. The objective will be to engage mass-market customers in saving for the long term.

Winning in the new LP&I landscape…selecting the right customer centric business model

The outsider could potentially provide this role based on their core capabilities

The Niche Provider

The Mass Market Hero

The Customer Specialist

The Alliance Provider

The Pure Asset Aggregator

The Outsider

Figure 6: New customer centric business models

By 2025, we can expect to see business models focusing more closely on specific components of the LP&I value chain, with more providers moving to maximise value from increasingly niche product and customer segments.

15

2. Alliance providerTaking advantage of an increasingly fragmented LP&I marketplace, alliance builders seek to position themselves as the ‘one size fits all’ solution provider. Manufacturing their own niche products, as well as distributing niche offerings from other providers, these players will have proven strengths in product manufacturing, alongside well-established partnerships that intermediate them with the right customer groups.

Just as HSBC successfully combined strong and varied distribution capabilities with the ability to manufacture some of its own products and underwrite risk, so other players with similar resources will seek to step into this space and position themselves as the waterfront providers of the future.

3. Asset aggregatorOngoing digital innovation and changing consumer behaviours will drive the emergence of this business model. Operating as the core industry platform provider, the asset aggregator will play a key role in the new LP&I marketplace by bringing together all provider propositions in one place.

With consumers increasingly demanding to see a single holistic view of their holdings in one place, irrespective of channel or provider, this function is aligned with the true customer-centricity that will differentiate leading providers from now on. Customers with multiple pension pots from various employers/providers will be able to log into the asset aggregator’s platform and obtain a single holistic view of their aggregated financial information.

Of course, the challenge here is that this is an ‘all or nothing’ model. For it to succeed, all LP&I providers need to trust the platform and be willing to share their information through it. To secure this trust, asset aggregators will need market-leading, scalable, secure and future-proof technology architectures that can easily plug into competitors’ systems and existing platforms. With a

range of channels available for accessing the platform (e.g. end-client, via adviser, via bank), the platform will also offer the ability to bolt on market-leading front-end financial planning tools (and tailor these to the distributor’s own brand).

4. Niche providerThese specialist providers will focus on specific components of the value chain or niche product areas where they can develop and sustain a market-leading value proposition (e.g. specialist fund management, equity release or crowd-funding investments). Happy to operate in discrete segments, they will be ready to collaborate as needed to develop the bolt-on capabilities they need.

With the large-scale, traditional providers increasingly likely to play it safe, expect to see new product innovation being driven by this business model. The providers that select this approach will have broad access to the key customer segments demanding their products – they may already exist, or they may emerge as true market disrupters from now on. Potential candidates for this role could include specialist providers of lifestyle financial products (such as Just Retirement), or online platforms that have yet to target consumer finance business.

5. Customer specialistDriven by ongoing digital disruption and changing consumer behaviours, this business model sees the emergence of a single ‘customer specialist’ that can position itself as the ‘go to’ repository of customer data. By forging partnerships with all key data providers (e.g. banks, social media, supermarkets), this provider would give customers the ability to select/de-select which areas of their data should be made available to LP&I providers. Offering market-leading analytics capabilities, including propensity analysis, fraud analysis and flexible micro-segmentation techniques, this platform would serve as a secure source of data to which LP&I providers could be given secure access. With the ability to tap into detailed lifestyle,

financial or medical data, providers would be able to offer individual customers more attractive, tailored quotes for their products.

6. Outsider In a digital marketplace, the emergence of new sources of competition from non-traditional players is always a possibility. Organisations that select the ‘Outsider’ business model will be adept at understanding and accessing the ‘contemporary customer’ in a way that incumbent LP&I providers cannot. Depending on the particular capabilities they can bring to bear, these new players may decide to target any area of the value chain. But whether they are established retailers, or online platforms, the key to their future success will be their ability to turn digital disruption and changing consumer behaviours to their own advantage. Winning providers in this space will have in-depth strengths in digital marketing, search engines and social networks, perhaps combined with some of the qualities of the ‘mass-market hero’ or ‘customer specialist’.

Expect imminent developments. Remember, Google already has a traditional banking licence, Facebook recently secured an e-money licence to offer financial services in Europe, and T-Mobile now has some 50 million customers, 70,000 stores and 40,000 fee-free ATMs in its T-Mobile Mobile Money network.

Just how quickly these players can transition to new market opportunities was underlined by the recent announcement that Amazon Web Services and Accenture had expanded their relationship to develop new end-to-end cloud migration and management services for enterprise clients.

16

17

Digital’s arrived…and it’s changing everythingThe LP&I marketplace is undergoing an unprecedented transformation. Digital has arrived and it’s changing everything – reshaping consumer behaviours and expectations and presenting providers with new opportunities for redefining customer relationships and rethinking business models. Driven by digital, the way that consumers choose to conduct their financial planning, and interact with their insurers and pension providers, is changing at pace. At the same time, their digital expectations are feeding into and driving the industry. Customers now benchmark LP&I providers against their broader digital experiences. To differentiate themselves from now on, providers must make themselves distinct across every channel, digital and physical.

Further fragmentation and disruption are inevitable

Market fragmentation is underway. We’re already seeing the emergence of disruptive new players across the LP&I segment – many more will follow in the years ahead. And with ongoing waves of regulation set to be a fact of life from now on, further fragmentation and disruption is inevitable. Few can predict what course this may take, although the example of Australia provides what may turn out to be a useful signpost. Based on Australia’s experience of auto-enrolment, we should expect to see a continued shift from defined benefit to defined contribution, along with a significant reduction in the number of funds. A drive towards transparency for all funds is also likely, particularly where returns and costs are concerned.

Know your customer In the LP&I marketplace that is now taking shape, ‘traditional’ LP&I providers face mounting pressure from some surprising competitors. Having installed themselves along the value chain, these disruptive players are leveraging new, lower-cost distribution formats to powerful effect. Against this backdrop, and with digital disruption well and truly underway, competition is becoming ever more fierce, with increased disintermediation of existing providers by new asset managers, distributors and platforms.

Seeking to secure their position in this fast-changing landscape, providers are reassessing existing distribution arrangements, changing their product propositions and targeting operational excellence across their businesses. However, a successful outcome in any of these core areas hinges on resetting existing customer relationships, as well as building new ones. Increasingly, lifetime customer relationships are being recognised as a major source of value, helping to drive profitable growth strategies for the long term.

In a more direct, digital world, providers will establish these long-lasting relationships by creating a ‘joined-up’ customer experience across multiple touchpoints, with simple transparent product propositions and trusted guidance that meets customer needs and delivers value across all life-stages.

From now on, competitive advantage will accrue to product manufacturers with superior product design capabilities that can respond to fast-changing market demands, as well as to the distributors, platforms and, potentially, new brands that are able to establish long-term active relationships.

Staking your claim amid digital disruption

18

Deciding where to play…and being the best you can beThe market is changing at pace, beyond question. New priorities, new dynamics and new competitors are all facts of life. To respond to the challenges the industry is facing and win out in the LP&I market of the future, leaders need to ask themselves what they want to be famous for – and then select the business model that will maximise value in their chosen market segment/s.

In this paper, we’ve identified the six business models that we believe will drive the market through to 2025 and beyond. Some providers may select a pure-play model (asset aggregator or niche provider, for example), others may pursue a hybrid combination of two or more models. Whatever course they decide to follow, the objective must be to define and organise their operations around the core capabilities required to support that model.

In a fragmented marketplace, differentiation through clear, simple product propositions is key to success. Focus will be essential. Investment opportunities must be rigorously prioritised to support new business model enablers and optimised according to the value delivered for every pound actually invested. And at every level – from their operating model and culture through to their execution capabilities – providers will have to commit to being the best they can be.

Getting started…Of course, implementing radical change is never easy, especially when firms have extensive legacy systems and operations. So how to get started? The essential first steps are to concentrate on developing customer-centric operating models, using advanced segmentation and data analytics to target customer segments and rationalise product focus.

Initiating collaborations with new partners across the value chain will facilitate the transformation ahead. And, crucially, harnessing digital technologies will enable firms to understand their customers and engage with them more effectively and at lower cost.

Further industry disruption is inevitable. With that in mind, UK LP&I providers must take action now to stake their claim as the progressive providers of the future. The case studies below show what can be achieved by companies that have seized the initiative to shift their role in the industry.

19

Launched in 1998 by Prudential as the UK’s first internet bank, Egg stormed to success, becoming the world’s largest pure online bank in just a few years. Providing banking, insurance, investments and mortgages through its website and other distribution channels, Egg’s market share grew robustly at the same time as it built a sustainably profitable business. Successful leverage of economies of scale, excellent brand awareness and increased automation drove operating and marketing costs down.

Of real significance to today’s LP&I providers, Egg managed to deliver all this in an increasingly competitive and fast-changing marketplace. Within five years of its launch, many other online entrants were jostling for position, along with established offline banks that had launched their own separate internet brands.

Egg’s success was built on much more than price alone. Crucially, the company recognised the value of genuine, long-lasting customer relationships and exploited the opportunities offered by technology to establish them. By attracting market share from traditional banking and financial service providers, Egg underlined what can be achieved by using digital and technology to build a strong consumer brand in a highly commoditised, product-led market.

Established in 1981, Hargreaves Lansdown was for many years a respected adviser to private investors in the UK on investment management products and services. More recently, the firm has successfully repositioned itself as a one-stop shop in the financial services sector. With a strong brand, and the ability to monetise assets better than its peers through customer-centric technology, services and channels, Hargreaves Lansdown is now recognised as a D2C platform leader. The firm now has over £36 billion in assets under management (a 32 per cent increase in AUM since 2009), and is consistently top-ranked for the quality of its customer service.

‘Vantage’, the firm’s flagship service, is a direct-to-private-investor fund platform targeted at well-defined customer segments. Ongoing investments in technology have paid dividends by enabling greater speed and storage capabilities. In 2011, the firm deployed its digital strategy. This provided further differentiation through mobile media, with iPhone and android apps providing free downloadable content with full functionality.

Technology innovation and customer centricity have underpinned the success of Hargreaves Lansdown’s reinvention. Unlike its competitors, the firm remains very active in ongoing employee communications. This has translated into a high penetration of non-pension offerings. Some 16 per cent of the 15,000 employees using its platform also have a stocks and shares ISA with Hargreaves Lansdown – far higher sales than any other workplace savings platform.

Case study 2: Hargreaves Lansdown – repositioned as a D2C leader

Case study 1: Egg – an idea ahead of its time

About Accenture

Accenture is a global management consulting, technology services and outsourcing company, with more than 305,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’s most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$30.0 billion for the fiscal year ended Aug. 31, 2014. Its home page is www.accenture.com.

Learn more

If you would like to hear more about Accenture’s views on this topic or would like to discuss how you can address the issues highlighted in this paper, please contact:

William Pritchett

Managing Director, Insurance Head of Accenture UK&I Life & Pensions [email protected] +44 20 7844 5485

Disclaimer

This report has been prepared by and distributed by Accenture. This document is for information purposes. No part of this document may be reproduced in any manner without the written permission of Accenture. While we take precautions to ensure that the source and the information we base our judgments on is reliable, we do not represent that this information is accurate or complete and it should not be relied upon as such. It is provided with the understanding that Accenture is not acting in a fiduciary capacity. Opinions expressed herein are subject to change without notice.

14-5712

Copyright © 2014 Accenture All rights reserved.

This document is subject to contract and contains confidential and proprietary information.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture.