Embed Size (px)

Citation preview

CAPE ACCOUNTINGUnit 1Module 1

ACCOUNTING THEORY & CONTROL SYSTEMS Describe the nature and scope of Financial

Accounting Discuss accounting methods for recording

financial information Justify the use of Standards in Accounting

DEVELOPMENTAccounting began as a simple system of

clay tokens to keep track of goods and animals, but has developed throughout history into a way of keeping track of complex transactions and other financial information. Throughout much of ancient history and the Middle Ages, accountancy remained a fairly simple affair.

Luca Pacioli is often called the "Father of Accounting" because he first published a math book titled "Summa de arithmetica, geometria, proportione et proportionalita," which contained a description of double-entry accounting.

Particularly in the United States during the Great Depression, demands were made for better standardization of accounting practices and a set code of professional guidelines. Today, the Generally Accepted Accounting Principles, or GAAP, set forth the standards by which public accountants must do business. Every country has a similar set of accounting guidelines.

Specialized branches of accounting have developed. In addition to traditional financial accounting, there are now subdivisions, such as tax accounting, management accounting and cost accounting. Professional accountants are required for these fields, as they involve the need for a thorough and specific understanding of business needs and accountancy practices.

Regional RegulatorsInstitute of Chartered Accountants of the CaribbeanInstitute of Chartered Accountants of Jamaica

THE USERS OF FINANCIAL INFORMATION AND THEIR NEEDS The users may be classified into internal and external

users.Internal users refer to managers who use

accounting information in making decisions related to the company's operations.

External users, on the other hand, are not involved in the operations of the company but hold some financial interest. They may be classified further into users with direct financial interest – the owners, investors, lenders and creditors, and users with indirect financial interest – government, employees, customers and the others.

Owners or investors – Stockholders of corporations need financial information to help them make decisions on what to do with their investments (shares of stock), i.e. hold, sell, or buy more.

Prospective investors need information to assess the company's potential for success and profitability. In the same way, small business owners need financial information to determine if the business is profitable and whether to continue or drop it.

Management – Managers, whether owner or hired, regularly face economic decisions – How much supplies will we purchase? Do we have enough cash? How much did we make last year? Did we meet our targets? All those, and many other decisions, require analysis of accounting information.

Lenders – Lenders of funds such as banks and other financial institutions are interested in the company’s ability to pay liabilities upon maturity (solvency).

Trade creditors or suppliers – Like lenders, trade creditors or suppliers are interested in the company’s ability to pay obligations when they become due. They are nonetheless especially interested in the company's liquidity -- its ability to pay short-term obligations.

Government – Governing bodies of the state, especially the tax authorities, are interested in an entity's financial information for taxation and regulatory purposes. Taxes are computed based on the results of operations and other tax bases. In general, the state would like to know how much the taxpayer is making to determine the tax due thereon.

Employees – Employees are interested in the company’s profitability and stability. They are after the ability of the company to pay salaries and provide employee benefits. They may also be interested in the company’s financial position and performance to assess the possibility of company expansion and career opportunities.

Customers – When there is a long-term involvement or contract between the company and its customers, the customers may be interested in the company’s ability to continue existence and its stability of operations. This need is also heightened in cases where the customers depend upon the entity.

General Public – Anyone outside the company such as researchers, students, analysts and others are interested in the financial statements of a company for some valid reason.

THE ACCOUNTING CYCLE This is the name given to the collective process of

recording and processing the accounting events of a company. The series of steps begin when a transaction occurs and end with its inclusion in the financial statements. As a bookkeeper, you complete your work by completing the tasks of the accounting cycle. It’s called a cycle because the accounting workflow is circular: entering transactions, manipulating the transactions through the accounting cycle, closing the books at the end of the accounting period, and then starting the entire cycle again for the next accounting period.

ACCOUNTING METHODSBefore you can start recording

business transactions, you must decide whether to use cash-basis or accrual accounting. The crucial difference between these two accounting processes is in how you record your cash transactions.

The cash method of accounting records revenue when cash is received, and records expenses when cash is paid. The accrual method records income items when they are earned and records deductions when expenses are incurred

WAITING FOR FUNDS WITH CASH-BASIS ACCOUNTINGFor a business invoicing for an item sold, or

work done, the corresponding amount will not appear in the books until payment is received - and similarly, debts owed by the business will not appear until they have been paid. Cash basis accounting records all transactions in the books when cash actually changes hands, meaning when cash payment is received by the company from customers or paid out by the company for purchases or other services.

Cash-basis accounting does a good job of tracking cash flow, but it does a poor job of matching revenues earned with money paid out for expenses. This deficiency is a problem particularly when, as it often happens, a company buys products in one month and sells those products in the next month. For example, you buy products in June with the intent to sell and pay $1,000 cash. You don't sell the products until July, and that's when you receive cash for the sales. When you close the books at the end of June, you have to show the $1,000 expense with no revenue to offset it, meaning you have a loss that month. When you sell the products for $1,500 in July, you have a $1,500 profit. So, your monthly report for June shows a $1,000 loss, and your monthly report for July shows a $1,500 profit, when in actuality you had revenues of $500 over the two months.

RECORDING RIGHT AWAY WITH ACCRUAL ACCOUNTINGFor a business invoicing for an item sold, or

work done, the corresponding amount will appear in the books even though no payment has yet been received – and debts owed by the business show as they are incurred, even though they may not be paid until much later.

Like cash-basis accounting, accrual accounting has its drawbacks. It does a good job of matching revenues and expenses, but it does a poor job of tracking cash. Because you record revenue when the transaction occurs and not when you collect the cash, your income statement can look great even if you don't have cash in the bank.

CONCEPTUAL FRAMEWORK

A conceptual framework is a theory of accounting prepared by a standard-setting body against which practical problems can be tested objectively.

A conceptual framework deals with fundamental financial reporting issues such as the objectives and users of financial statements, the characteristics that make accounting information useful, the basic elements of financial statements (e.g., assets, liabilities, equity, income, and expenses), and the concepts for recognising and measuring these elements in the financial statements.

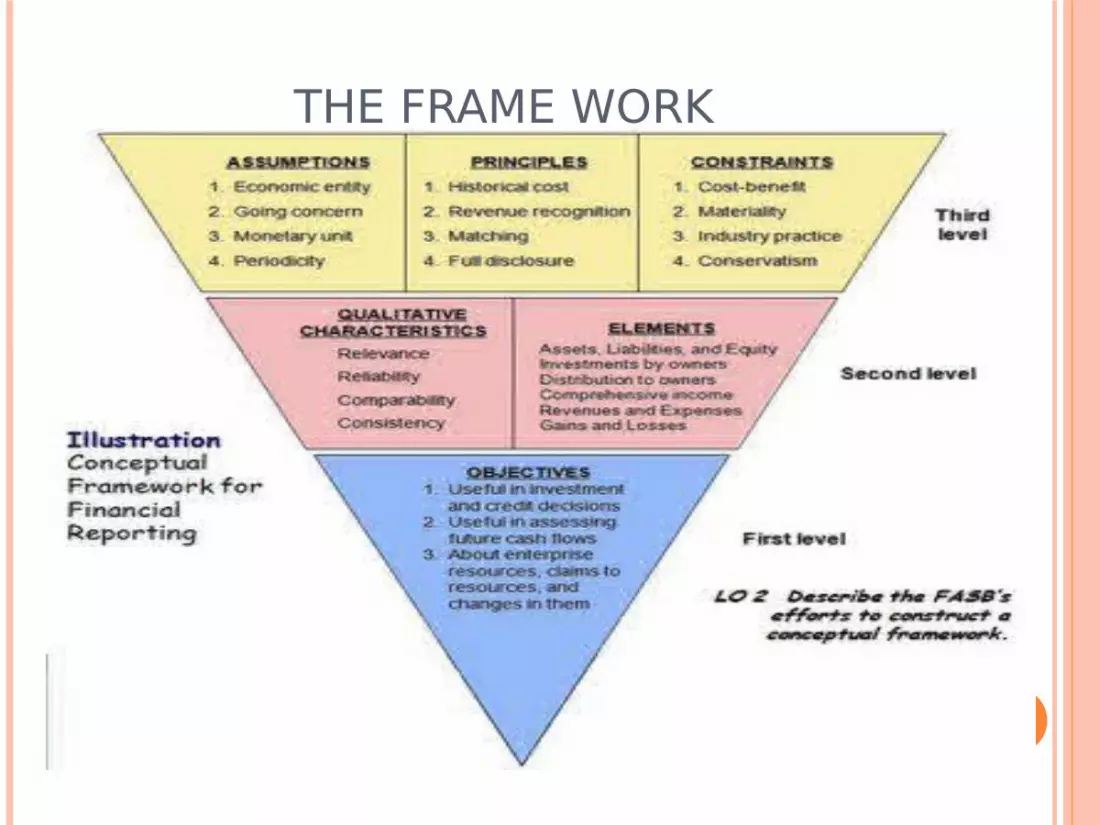

THE FRAME WORK

LEVEL 1OBJECTIVES OF FINANCIAL

REPORTINGThe main objective of Financial Reporting

is to provide financial information to be used in making reasonable decisions :Useful to those making investment

and credit decisions Helpful in projecting future cash flows

of the businessIdentifies the economic resources

(assets) the claims to those resources ( liabilities) and the changes in those resources

LEVEL 2QUALITATIVE CHARACTERISTICS OF

ACCOUNTING INFORMATION’Qualitative Characteristics

What make financial information useful?RelevanceReliabilityConsistencyComparabilityUnderstandability

RelevanceInformation capable of making a difference in a

decision contextThis information had the ability to influence decision.

It must be available to its users before it is no longer able to influence their decisions

ReliabilityInformation is a complete and true representation of the situation.

It is verifiable, free from material error and free from bias

ConsistencyThe same accounting treatment is applied to similar events

ComparabilitySimilar measurements and reporting for different enterprises and different time periods

Understandability Users should be able to perceive and understand the information

LEVEL 2 ELEMENTS OF FINANCIAL

STATEMENTSFinancial Statements are the main methods of

presenting financial information to persons outside the business.

The main statements used are:Statement of Financial PositionStatement of Comprehensive IncomeStatement of Changes in EquityStatement of Cash flow

Statement of Financial Position (Balance Sheet)

Gives the financial condition of a business on a specific date.

Shows the assets, liabilities and the amount of capital invested by the owners

Statement of Comprehensive Income (Profit and Loss Account)

Shows the profitability of a business over a period of time.

Shows the revenues and expenses of a business

Statement of Owners Equity Explains certain changes in the amounts of

capital Statement of Cash Flow

Shows where money was received from and how it was spent during the accounting period.

It is a summary of cash receipts and cash payments

Other elementsInvestments by owners – money invested

after the business as startedDistribution to owners – dividendsGains – increases in net assets/equity from

transactions other than by revenues or investments by owners

Losses – decreases in equity from transactions other than expenses or distribution to owners

LEVEL 3ACCOUNTING PRINCIPLES AND

CONVENTIONSAssumption

Separate EntityGoing ConcernUnit of Measure

PrinciplesCost principleRevenue principleMatching principleFull disclosure

ConstraintsConservatismMateriality

Separate EntityThe business is treated as a legal person in

its own right.The transactions recorded in the financial

statements must be related only to the business and not include any that relate to the owners’ private lives.

Going ConcernFinancial records are prepared assuming

that the business has an indefinite life ( it will continue into the foreseeable future.

Unit of MeasureAssumes that money is the common

denominator of economic activity for financial reporting.

Assumes that the monetary unit is a stable measure without changing values.

Cost PrincipleAssets & Liabilities are accounted for based

on acquisition cost.The cost price is used because it represents the

price paid and it is verifiable

Revenue PrincipleRevenue is recognized (1) when realized or

realizable and (2) when earned.

Matching PrincipleExpenses are recorded in the period in

which they are incurred even if the expenses are not paid

Full Disclosure PrincipleIn the preparation of financial statements,

sufficient information should included to permit the knowledgeable reader to make an informed judgment about the financial condition of the enterprise in question

ConstraintsConservatism

When in doubt, an accountant should choose a solution that will be least likely to overstate assets and income. The conservatism constraint should be applied only when doubt exists. An intentional understatement of assets or income is not acceptable accounting

MaterialityIn the application of basic accounting theory, an amount may be considered less important because of its size in comparison with revenues and expenses, assets and liabilities, or net income. Deciding when an amount is material in relation to other amounts is a matter of judgment and professional expertise.

Assumptions: (1) Economic entity (2) Going concern (3) Monetary unit (4) PeriodicityPrincipals: (1) Historical Cost (2) Revenue recognition (3) Matching (4) Full DisclosureConstraints: (1) Cost-benefit (2) materiality (3) Industry practice (4) Conservatism

Objectives: (1) Useful in investment and credit decisions (2) Useful in assessing future cash flows (3) About enterprise resources, claims to resources and changes in them

Qualitative Characteristics: Primary: Relevance and Reliability Secondary: Comparability and Consistency

Elements Assets, Liabilities, Equity Investment/Distribution by owners Comprehensive IncomeRevenues, ExpensesGains, Losses

SUMMARY