Embed Size (px)

Citation preview

September 2021

First Quarterly Report 2021/22

2

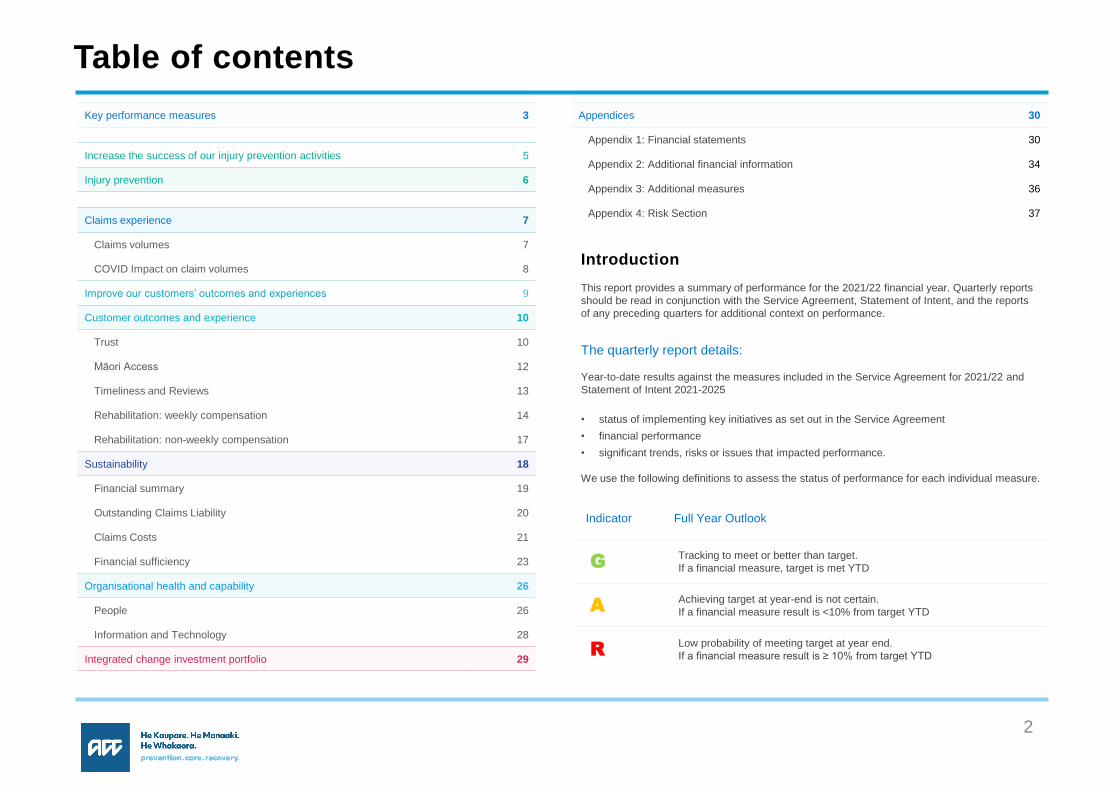

Table of contents

Key performance measures 3

Increase the success of our injury prevention activities 5

Injury prevention 6

Claims experience 7

Claims volumes 7

COVID Impact on claim volumes 8

Improve our customers’ outcomes and experiences 9

Customer outcomes and experience 10

Trust 10

Māori Access 12

Timeliness and Reviews 13

Rehabilitation: weekly compensation 14

Rehabilitation: non-weekly compensation 17

Sustainability 18

Financial summary 19

Outstanding Claims Liability 20

Claims Costs 21

Financial sufficiency 23

Organisational health and capability 26

People 26

Information and Technology 28

Integrated change investment portfolio 29

Introduction

This report provides a summary of performance for the 2021/22 financial year. Quarterly reports

should be read in conjunction with the Service Agreement, Statement of Intent, and the reports

of any preceding quarters for additional context on performance.

Year-to-date results against the measures included in the Service Agreement for 2021/22 and

Statement of Intent 2021-2025

• status of implementing key initiatives as set out in the Service Agreement

• financial performance

• significant trends, risks or issues that impacted performance.

We use the following definitions to assess the status of performance for each individual measure.

Indicator Full Year Outlook

G Tracking to meet or better than target.

If a financial measure, target is met YTD

A Achieving target at year-end is not certain.

If a financial measure result is <10% from target YTD

R Low probability of meeting target at year end.

If a financial measure result is ≥ 10% from target YTD

The quarterly report details:

Appendices 30

Appendix 1: Financial statements 30

Appendix 2: Additional financial information 34

Appendix 3: Additional measures 36

Appendix 4: Risk Section 37

3

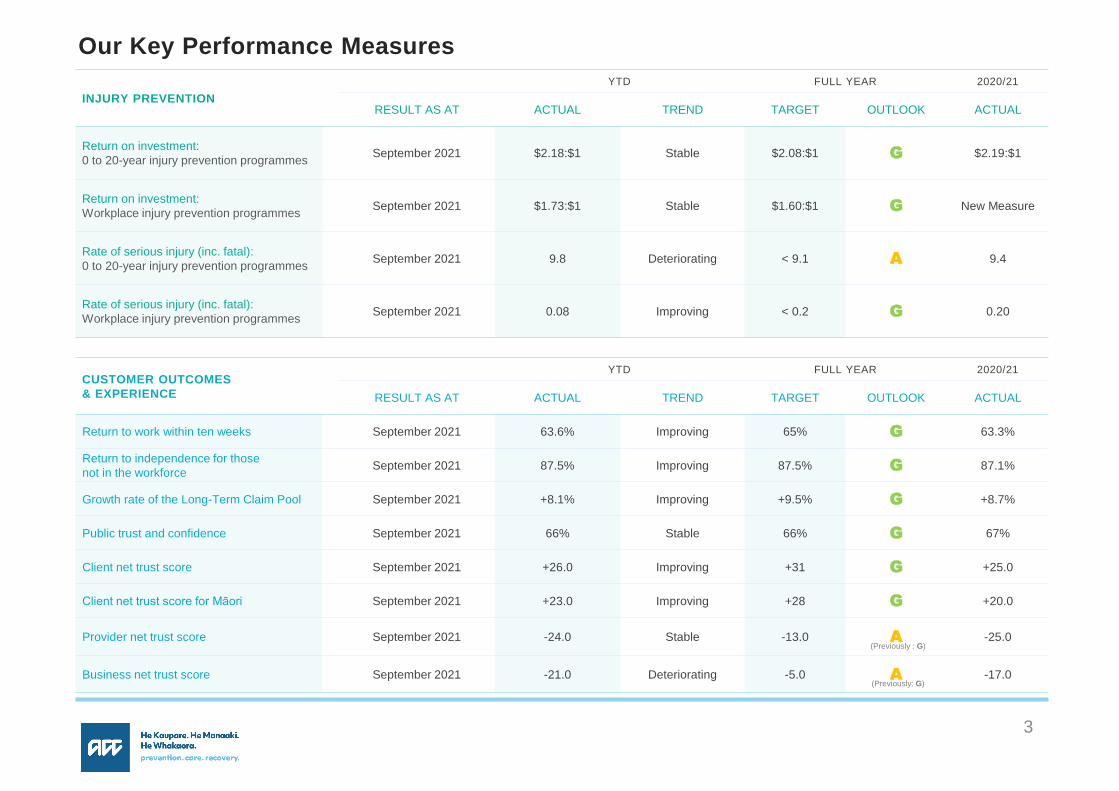

INJURY PREVENTION

YTD FULL YEAR 2020/21

RESULT AS AT ACTUAL TREND TARGET OUTLOOK ACTUAL

Return on investment:

0 to 20-year injury prevention programmesSeptember 2021 $2.18:$1 Stable $2.08:$1 G $2.19:$1

Return on investment:

Workplace injury prevention programmesSeptember 2021 $1.73:$1 Stable $1.60:$1 G New Measure

Rate of serious injury (inc. fatal):

0 to 20-year injury prevention programmesSeptember 2021 9.8 Deteriorating < 9.1 A 9.4

Rate of serious injury (inc. fatal):

Workplace injury prevention programmes September 2021 0.08 Improving < 0.2 G 0.20

CUSTOMER OUTCOMES

& EXPERIENCE

YTD FULL YEAR 2020/21

RESULT AS AT ACTUAL TREND TARGET OUTLOOK ACTUAL

Return to work within ten weeks September 2021 63.6% Improving 65% G 63.3%

Return to independence for those

not in the workforceSeptember 2021 87.5% Improving 87.5% G 87.1%

Growth rate of the Long-Term Claim Pool September 2021 +8.1% Improving +9.5% G +8.7%

Public trust and confidence September 2021 66% Stable 66% G 67%

Client net trust score September 2021 +26.0 Improving +31 G +25.0

Client net trust score for Māori September 2021 +23.0 Improving +28 G +20.0

Provider net trust score September 2021 -24.0 Stable -13.0 A -25.0

Business net trust score September 2021 -21.0 Deteriorating -5.0 A -17.0

Our Key Performance Measures

(Previously : G)

(Previously: G)

4

SUSTAINABILITY

& GOVERNANCE

YTD FULL YEAR 2020/21

RESULT AS AT ACTUAL TREND TARGET OUTLOOK ACTUAL

Change in average

treatment cost per claimSeptember 2021 +6.0% Stable ≤5% A +6.1%

Average care hours

per serious injury claimSeptember 2021 1,393 Stable 1,387 G 1,396

Actuarial movement June 2021 +1.08% Bi-annualWithin

-3 to +1% G +1.08%

Investment performance

after costs relative to benchmarkSeptember 2021 +0.32% Improving +0.15% G +1.90%

ORGANISATIONAL HEALTH

AND CAPABILITY INTENTIONS

YTD FULL YEAR 2020/21

RESULT AS AT ACTUAL TREND TARGET OUTLOOK ACTUAL

Employee net promoter score June 2021 +0 Stable +12 G +0

Total recordable injury frequency rate September 2021 2.0 Stable < 3.5 G 1.7

Number of category 3, 4 and 5

privacy breaches and near missesSeptember 2021 0 Stable < 3

No Category 5G 0

Overall operational system availability September 2021 99.9% Stable 99.5% G 99.9%

OTHER TRANSFORMATION

MEASURES

YTD FULL YEAR 2020/21

RESULT AS AT ACTUAL TREND TARGET OUTLOOK ACTUAL

Claims processed per FTE September 2021 549 Deteriorating 583 A 580

Average WC days paid September 2021 103.9 Days(-6.6 Days)

Improving 102.3 Days(-4.9 Days)

A 105.9 Days(-8.5 Days)

Our Key Performance Measures

(Previously: G)

5

Increase the success of our injury prevention activities

• We piloted Nymbl as part of our Live Stronger for Longer programme. Nymbl is an

in-home balance app that has helped thousands of people across the world get

better balance, lead active lives and live falls free.

• In the pilot over 15,000 people signed up the Nymbl app. We have evidence Nymbl

is reaching a higher risk of falls group. The falls claim history of the people who

completed Nymbl is higher as a rate for falls than the rest of the 65+ population.

• From the group who completed the minimum desired number of trainings, there

were fewer claims (adjusting for risk bias and claim bias) as a rate compared to the

65+ population. There was a 27% difference in the falls claim rate of those who

completed Nymbl and the 65+ populations. However not all people completed the

minimum of four training sessions.

Grants and Subsidies

• We have completed the third funding round of Workplace Injury Prevention grants.

The funding round prioritised proposals that aligned to one of the following

investment priorities:

• Lead, build and deliver solutions to reduce the risk of work-related sprains

and strains in high-risk sectors of Construction, Manufacturing, Agriculture,

and Transport.

• Strengthen the role of sector groups in leading initiatives to lift outcomes

across workplaces, particularly where there is a high risk of injury.

• Four organisations are being awarded a total of $3m in grants to deliver

interventions that will help reduce injuries in the workplace. The recipients are:

• Dairy NZ Ltd - Addressing dairy farming sprains and strains presents a large

opportunity to improve farmer wellbeing.

• Massey University - Identify and monitor all work-related sprains and strains

claims in the Hawkes Bay region between 2021-2023, applying prevention

through design principles to develop specific interventions to prevent those

injuries.

Nymbl

• SaferMe Inc., development and implementation of an algorithm and risk mitigation

solution that enables risk to be identified at the individual level and supports targeted

mitigation actions for high-risk construction workers.

• Horticulture NZ Inc, building system capability and establishing health and safety

leadership in the Horticulture industry.

6

Injury Prevention

MEASURE MOST RECENT

RESULT

YTD

ACTUAL

TREND FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Return on investment:

0 to 20-year injury prevention programmesSeptember 2021 $2.18:$1 Stable $2.08:$1 G $2.19:$1

Return on investment:

Workplace injury prevention programmesSeptember 2021 $1.73:$1 Stable $1.60:$1 G New Measure

Number of claims avoided through our injury prevention initiatives September 2021 1,804 Stable 14,641 G 14,240

Investment in Kaupapa Māori programmes September 2021 $1.6m Stable $7m G $5.8m

Rate of serious injury (inc. fatal):

0 to 20-year injury prevention programmesSeptember 2021 9.8 Deteriorating < 9.1 A 9.4

Rate of serious injury (inc. fatal):

Workplace injury prevention programmesSeptember 2021 0.08 Improving < 0.2 G 0.20

Rate of Serious Injury:

• The 0-20 Fatal & Serious Injury result is tracking as we forecasted and is still

unfavourable. Based on current forecasting it is likely to be unfavourable until at

least the end of the second quarter, and we are working to understand the drivers.

Part of this work will be to understand whether there are more fatal accidents

occurring or more claims being made for these accidents. Our continuing work with

Nymbl will help to reduce older age falls.

7

MEASURE MOST RECENT

RESULT

YTD

ACTUAL

FULL YEAR

BUDGET

2020/21

ACTUAL

New claims registered

(rolling 12 months)September 2021 1,994,464 2,151,105 2,105,833

New Weekly Compensation

claims (rolling 12 months)September 2021 93,284 94,997 95,381

MEASURE 12-MONTH

ROLLING GROWTH

FY

BUDGET

New claims registered +5.8% +1.1%

New Weekly Compensation claims +11.9% +3.1%

• New claims registered volumes increased by 5.8% for the rolling 12 months to September 2021,

but COVID lockdowns have affected volumes.

• Volumes in September 2021 (~120,000) are approximately 45k lower than July 2021, September

2019, and 57k lower than September 2020.

NEW CLAIMS GROWTH RATES - ROLLING 12 MONTHS

New Weekly Comp New Registrations

Claims Experience: Claims Volumes

• New WC commencements increased 11.9% for the rolling 12 months to September

2021. Volumes have dropped off since COVID lockdown.

• Volumes in September 2021 (~5,600) are 800 lower than September 2019 and

2,500 lower than September 2020 and July 2021.

0

2,000

4,000

6,000

8,000

10,000

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

5,618

VOLUME OF WC COMMENCEMENTS - MONTHLY

2020/21 2021/22

0

50,000

100,000

150,000

200,000

250,000

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

119,655

VOLUME OF NEW REGISTRATIONS - MONTHLY

2020/21 2021/22

-8.1%

-3.7%

1.1%

3.1%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May

2019/20 2020/21 2021/22

5.8%

11.9%

END OF

YEAR TARGETS

8

Lower claim volumes is consistent with the 2020 lockdown

• For the initial August 2021 lockdown period, the fall in claim

volumes are similar when compared to the 2020 lockdown.

• Claim volume growth seen from week 35, is starting to flatline

as Auckland remains in level 3 lockdown. With more regions

in level 3 now too, we expect this will have a flow on effect to

claim volumes.

Claims Experience: COVID Impact to Claims Volumes

Comparing lockdowns

• The two lockdowns happened at two different times of the

annual claims cycle e.g. winter sports were just starting in the

2020 lockdown but had finished in 2021 lockdown.

• Before the August 2021 lockdown, the claim volumes were

more consistent with 2019 and non-lockdown periods in

2020.

• The initial return to level 2 in 2021 for all of NZ (except

Auckland), is similar to the second week of 2020 at level 2.

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

AC

CE

PT

ED

CLA

IMS

RE

GIS

TE

RE

D

WEEK OF CALENDAR YEAR

CLAIM REGISTRATION CHANGES OVER LOCKDOWN

COVID IMPACT TO ALL REGISTERED CLAIMS

2020LEVEL 4

2020LEVEL 3

2020LEVEL 2

-80%

-60%

-40%

-20%

0%

20%

PE

RC

EN

TA

GE

CH

AN

GE

OV

ER

LO

CK

DO

WN

WEEKS PRIOR TO LOCKDOWNS

Outside of Auckland,

NZ moves to level 2

2020 Calendar year 2021 Calendar year

2020 Calendar year 2021 Calendar year

2019 Calendar year

Auckland moves

down to level 3

Waikato moves

up to level 3

9

Improve our customers’ outcomes and experiences

Improved timeliness of responses and first call resolution

Improving the experience for customers by enabling faster contact with ACC and

providing first call resolution remains a key focus for ACC.

In the first quarter we increased the channels for customers to make direct contact, with

the introduction of ‘Live Support’. This gives clients the ability to chat online with an ACC

staff member using the MyACC self-service digital platform.

This quarter within the Contact Centre (the primary point of initial contact for the majority

of ACC customers), we provided timely responses with the following average response

rates to incoming calls, emails and live chat:

• Calls (Client and Provider): 3 minutes

• Calls (Business Customer): 6 minutes

• Email (all customer groups): < 1 day

• Live Chat (MyACC): < 1 minute

Across all these interactions, 83% had first contact resolution. Overall customer

satisfaction of the call experience remains high at 85%.

We are considering different approaches to measuring health outcomes. We are working

on Proof of Concepts (PoC) to measure health outcomes for four specific groups of

clients who:

• Have an upper or lower limb fracture

• Have concussion

• Access physiotherapy

• Have a sensitive claim

It is expected that the PoCs will run until approximately mid-2022, at which time they will

be evaluated.

Measuring client outcomes

ACC continues to focus on improving the accessibility and range of digital self-

management services. This ensures customers can choose the best options to suit their

needs when they need to complete certain tasks, require support, or are seeking

information from ACC.

Early indications from ‘Live Support’ are positive; ~ 2,000 clients using this service with

over 85% customer satisfaction reported.

Work is underway to increase the capability of MyACC for Business. This will enable

employers to view information about their employee’s injuries. The initial focus is on

workplace accidents, giving employers visibility of medical certificates and details of

incapacity. This will provide employers with increased understanding of return to work

due dates and the extent to which the employee can return to work. The initial stage of

these changes are planned for the third quarter.

We are developing a single provider hub. This is a new self-service platform that

providers can access for all their digital interactions with ACC. This quarter focus has

been on the technology build to enable Providers who do not use practice management

systems to also utilise the hub for tasks such as submitting claims and invoices to

ACC. It is anticipated the platform will commence go live in the fourth quarter.

Increase the range of self-service options

10

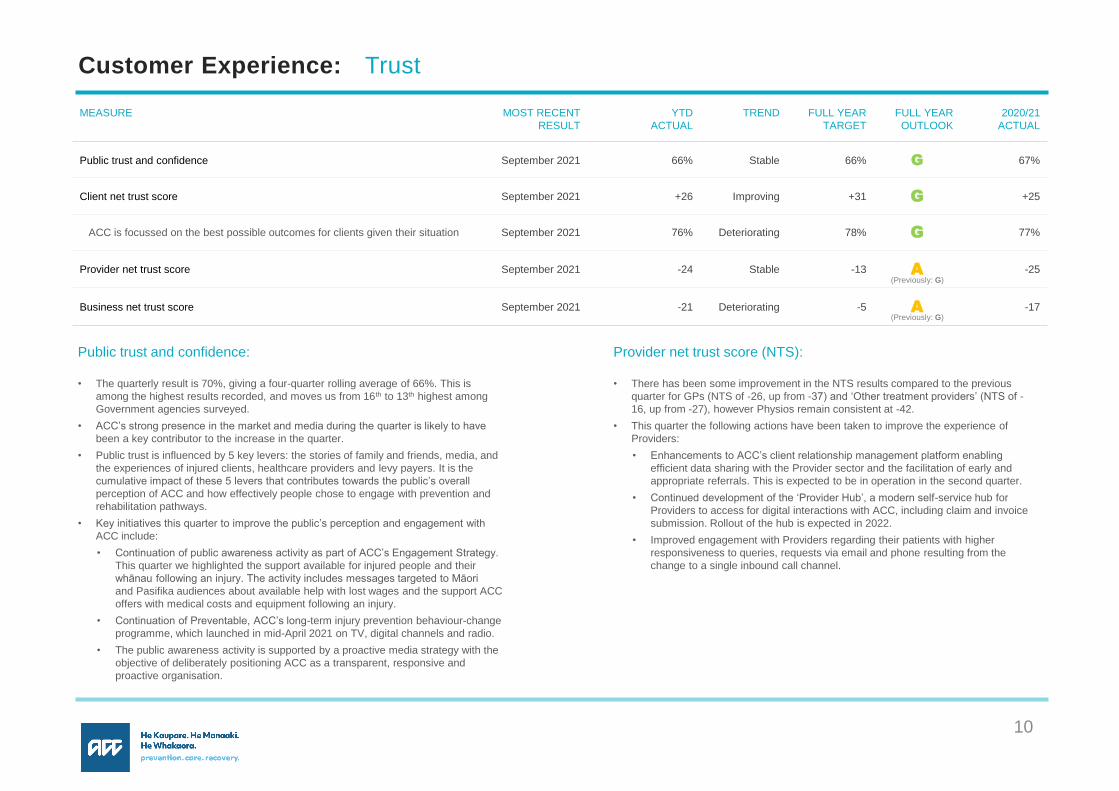

Customer Experience:

MEASURE MOST RECENT

RESULT

YTD

ACTUAL

TREND FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Public trust and confidence September 2021 66% Stable 66% G 67%

Client net trust score September 2021 +26 Improving +31 G +25

ACC is focussed on the best possible outcomes for clients given their situation September 2021 76% Deteriorating 78% G 77%

Provider net trust score September 2021 -24 Stable -13 A -25

Business net trust score September 2021 -21 Deteriorating -5 A -17

Trust

Public trust and confidence:

• The quarterly result is 70%, giving a four-quarter rolling average of 66%. This is

among the highest results recorded, and moves us from 16th to 13th highest among

Government agencies surveyed.

• ACC’s strong presence in the market and media during the quarter is likely to have

been a key contributor to the increase in the quarter.

• Public trust is influenced by 5 key levers: the stories of family and friends, media, and

the experiences of injured clients, healthcare providers and levy payers. It is the

cumulative impact of these 5 levers that contributes towards the public’s overall

perception of ACC and how effectively people chose to engage with prevention and

rehabilitation pathways.

• Key initiatives this quarter to improve the public’s perception and engagement with

ACC include:

• Continuation of public awareness activity as part of ACC’s Engagement Strategy.

This quarter we highlighted the support available for injured people and their

whānau following an injury. The activity includes messages targeted to Māori

and Pasifika audiences about available help with lost wages and the support ACC

offers with medical costs and equipment following an injury.

• Continuation of Preventable, ACC’s long-term injury prevention behaviour-change

programme, which launched in mid-April 2021 on TV, digital channels and radio.

• The public awareness activity is supported by a proactive media strategy with the

objective of deliberately positioning ACC as a transparent, responsive and

proactive organisation.

• There has been some improvement in the NTS results compared to the previous

quarter for GPs (NTS of -26, up from -37) and ‘Other treatment providers’ (NTS of -

16, up from -27), however Physios remain consistent at -42.

• This quarter the following actions have been taken to improve the experience of

Providers:

• Enhancements to ACC’s client relationship management platform enabling

efficient data sharing with the Provider sector and the facilitation of early and

appropriate referrals. This is expected to be in operation in the second quarter.

• Continued development of the ‘Provider Hub’, a modern self-service hub for

Providers to access for digital interactions with ACC, including claim and invoice

submission. Rollout of the hub is expected in 2022.

• Improved engagement with Providers regarding their patients with higher

responsiveness to queries, requests via email and phone resulting from the

change to a single inbound call channel.

Provider net trust score (NTS):

(Previously: G)

(Previously: G)

11

Customer Experience: Trust

• Analysis of the results reflect that the decline, although not significant, is driven by

declines for small businesses at -24 (previously -15) and medium businesses at -20

(previously -4), with most survey questions reflecting lower endorsement compared to

previous quarters.

• Overall, less than half of all businesses (44%) agree ACC provides them with real

benefits and value, which is a slight decline compared to last quarter (47%), largely

due to small (from 47% to 40%) and medium businesses (from 68% to 62%).

• Improving the ease of doing business and more effective engagement, including

greater involvement in the rehabilitation of injured employees, remain key focus areas

for ACC to improve the experience of Business Customers. This quarter the following

initiatives were focused on:

• Continued work to develop digital functionality for employers within MyACC for

Business to access claims information about employees with work injuries. This will

improve business customers interaction and engagement by providing timely

information and enabling the employer to play a more proactive role in the recovery of

their injured employee. Currently we expect to go live with these tools in the third

quarter.

• The Recovery at Work Business Customer Resources and Education Campaign aims

to empower business customers to self-manage recovery at work for their injured

employees. Information and resources are being developed. This will go-live in the

second quarter

• We completed the pre-2021 invoicing proactive communication programme this

quarter. This provided business customers with early notification and information

regarding their invoice, allowing them the opportunity to update key information used

to calculate levies prior to receiving it. Evaluation of this programme showed the

positive impact of these communications.

• Peak annual levy invoicing: Annual invoicing commenced for companies in July and

for Self-Employed in September. This period is known to negatively impact NTS

results.

• Levy Consultation: ACC released its proposed levy rates for public consultation which

included a proposed decrease to the average work account levy and an increase in

the levy rates for the Earners’ Account and the Motor Vehicle Account. Early analysis

from feedback received indicates broad support across the Work Account proposals.

• Analysis indicates that the slight increase in NTS is likely driven by some

improvements regarding ease of dealing with ACC and communication, along with

stable results relating to provision of treatment and support.

• Improvements were seen in some ease/effort related measures for Assisted

Recovery (NTS increased to +28 from +25). Specifically, satisfaction increased

relating to handling of claims, and agreement regarding reaching ACC staff without

difficulty.

• However, there has been a downward trend evident in Supported Recovery across

the last few quarters, with NTS at +2 (from +9). This decline appears to be driven by

a decrease in the proportion of clients who agree it takes little effort to deal with

ACC.

• These key areas continue to be our focus to improve the experience of clients. This

quarter the following initiatives were focused on:

• A new dedicated team to provide welcome conversations to clients within

Assisted Recovery and connect with the client’s employer. These conversations

ensure the employer understands their role in their employee’s recovery. This

will improve timeliness to onboard clients, provide consistent expectations on

entitlements (as well as timely set up), and establish appropriate rehabilitation

journeys.

• A review of clients within Supported Recovery who have been with ACC for 1-

2.5 years commenced this quarter. This work will ensure clients are receiving

the appropriate level of service to support their rehabilitation.

• Embedding ACC’s single inbound call channel, reducing reduced call wait times

and improving task responsiveness. This is also increasing the capacity of staff

to focus on the rehabilitation needs of injured clients.

• Adding an additional key moment to Heartbeat, ACC closed loop feedback

platform, to monitor the experience of clients being transitioned between

recovery teams and take action to recover service experience when required.

Client NTS: Business NTS:

12

Customer Experience: Māori Access

MEASURE MOST RECENT

RESULT

YTD

ACTUAL

TREND FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Client net trust score for Māori September 2021 +23 Improving +28 G +20

Māori lodgement ratio September 2021 0.82 Stable 0.83 G 0.82

• A contributor to the increase in Client NTS for Māori this quarter may relate to an

external engagement campaign that was run to promote the understanding

and uptake of the Rongoā Māori Service and support improved access, experience

and outcomes for injured Māori. This campaign included social media activity, which

had strong reach and positive engagement, and media coverage across national and

regional platforms.

Actions underway

• We currently have a number of initiatives underway that support improving equity of

access, experience and outcomes for Māori who are injured:

• Rongoā Māori Service: We are continuing to build relationships with more

practitioners across Aotearoa and strengthen service controls. We have

completed the national education programme to support the cultural capability

of our client-facing kaimahi. This included learning huddles, support resources,

and workshops with Māori Health kaimahi.

• Kaupapa Māori Health Services: Progress to develop a new pathway for

ACC clients and whānau continues. The current focus is on the procurement

phase of the first tranche of this developing pathway, in the Tainui rohe,

following a temporary pause due to COVID-19 restrictions.

• Raranga: This new project intends to focus on uplifting the cultural safety of all

ACC services in order to improve access, experience and outcomes for Māori,

and for all. The project team’s initial responsibility will include reviewing existing

cultural safety standards in ACC contracts and documents and exploring

opportunities for improvement. The term ‘raranga’ means ‘to weave’ and

reflects the respectful braiding and balancing of te ao Māori and ‘universal’

worldviews, knowledge and practises that ACC intend to bring to its services.

• Hāpai: The Hāpai – Te Pihinga pilot launched in the Kāhui o te Uriteria region

this quarter. The pilot will enable clients to engage with ACC in a more te ao

Māori way. The pilot will run for six months through until January 2022.

13

MEASURE MOST RECENT

RESULT

YTD

ACTUAL

TREND FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Speed of cover decisions - non-complicated claims September 2021 0.9 days Stable <0.9 days G 0.9 days

Speed of cover decisions - complicated claims September 2021 72 days Deteriorating <70 days G 66.9 days

Customer Experience: Timeliness and Reviews

• The September monthly complicated cover decision result was 72 days; improved

from 73.3 days in August.

• The performance in the earlier part of the current rolling 12-months was much better

than it is now.

• Deterioration is primarily driven by Treatment Injury and Late Lodged decisions.

However, Late Lodged timeliness has improved from 68 days in August to 60 days in

September.

Speed of cover decisions – Complicated claims

MEASURE MOST RECENT

RESULT

YTD

ACTUAL

TREND FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Reviews as a percentage of decline decisions September 2021 8.2% Stable ≤ 8.7% G 8.5%

Average time to resolution for claims with reviews September 2021 121.3 days Stable ≤ 130 days G New Measure

Proportion of ACC reviews upheld (in favour of ACC) September 2021 90.6% Stable ≥ 86% G 90.6%

• Work is underway to understand the drivers behind why clients review suspension

decisions, outcomes at review, increase consistency across suspension decisions,

and implement strategies to improve the management of these type of reviews.

• We continue to focus on internal process changes that enable earlier engagement

with customers to discuss the review process and what resolution options are

available for them.

Actions underway to improve review performance

• Alternative Dispute Resolution provides the opportunity to engage in

meaningful conversations with an independent party to find a way forward or

resolution without the need for a formal review hearing. With the introduction of

a new ADR initiative, in September 2021 60 cases were referred through to

Talk-Meet-Resolve (August 2021 30 cases).

• We continue to focus on Hearing Loss and Treatment Injury claim decisions

which are key contributors to the deterioration:

• Hearing Loss telephone scripting has been reintroduced. This shortens

the time taken for information gathering, before a claim is assessed.

• Utilisation of reporting to stream work quicker (Treatment Injury and Late

Lodged) continues, while also building capability of decision makers.

* The average time to resolution for claims with reviews is a new measure this year. Definition: The average time (in calendar days) for reviews to be resolved from review lodgement to review outcome.

14

Customer Experience: Short-term rehabilitation: Weekly Compensation

MEASURE MOST RECENT

RESULT

YTD

ACTUAL

TREND FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Return to work within ten weeks September 2021 63.6% Improving 65% G 63.3%

Return to work within nine months September 2021 90.8% Improving 91% G 90.4%

Durable return to work September 2021 74% Stable1% Higher

than Aus 1 G 72%

Average in weekly compensation days paid September 2021103.9 days

(-6.6 days)Improving

102.3 Days(-4.9 days)

A 105.9 Days(-8.5 days)

1 The Australian RTW survey.

92.4%

91.0%

90.4%

66.8%

65.0%

63.3%

62%

64%

66%

68%

85%

87%

89%

91%

93%

Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Sep-21

63.6%

90.8%

10 Week (RHS)9 Month (LHS) 10 Week Target (RHS)

RETURN TO WORK WITHIN TEN WEEKS AND NINE MONTHS - 52 WEEK ROLLING

9 Month Target (LHS)

• The ten-week and nine-month return to work rehabilitation rate has continued to

improve.

The improving trend in the past months for both measures has been largely driven by:

• The return to usual claim mix, as the proportions of shorter duration weekly

compensation claims continued to move closer to those seen in pre-COVID times

• the rolling off of the most severely impacted periods due to COVID lockdowns from

last year meaning less impact on the current measure

• continued lift in outcomes being achieved from the rehabilitation focused initiatives

that started earlier in the year

• The lag in the measures between a client ceasing weekly compensation (WC) and

subsequently being reported as an outcome means the August 2021 COVID lockdown

has not significantly affected these results yet. Based on experience from the 2020

lockdown, the impact on weekly performance results peaked approximately 9-10

weeks after the start of the lockdown. For the current lockdown, we expect to see a

similar decline in weekly short term rehabilitation results, from mid-late October 2021

for the shorter duration measures (such as the 70-day rate).

• The August 2021 lockdown has resulted in a decline in new WC claim volumes of

similar magnitude to the 2020 lockdown. However, due to a number of reasons such as

the lockdown starting at a different time in the year compared to 2020, shorter

restrictions for regions other than Auckland, and healthier economic conditions, it is

expected that the claim volume recovery will be sharper with less severe impacts on

the short term rehabilitation performance over the months ahead.

Ten-week and nine-month return to work rates

• We expect some additional deterioration relating to clients issued a suspension or vocational

independence decision immediately prior to lockdown. We have extended notice periods during

the level 3 and 4 lockdown period.

• Given that most of the rehabilitation performance measures are a 52 week/12 month rolling

average, the impact of the current lockdown can be expected to last for much of the financial year,

and will only start to unwind as volumes normalise.

15

Customer Experience: Short-term rehabilitation: Weekly Compensation

• The Average Weekly Compensation Days paid (AWCDP) has continued to improve

month on month and over much of the last quarter.

• The AWCDP measure reflects WC exits between 29 and 365 days. The changing profile

over the last few months of the WC exits has had a direct impact on the results:

• The proportion of claims with 29 - 70 days WC in the WC exits total has remained

largely unchanged over the last two months however the proportion of WC exits with

71 – 182 days improved over last month by ~ 0.5 percentage points.

• Overall, WC exits within 365 days continued with an improving trend (an additional 884

WC exits achieved last month compared to August). There was a small increase in the

proportions within 365 days from the previous month; however, there was an overall

increase in the WC exit volumes and in particular in the band 29 -365 WC days.

• The improvement in WC exit volumes within 365 days is not only having a positive

impact on the AWCD measure but it is also contributing to the improving trend of the

growth rate of the long-term claims pool.

Average weekly compensation days paidRETURN TO WORK WITHIN TEN WEEKS AND NINE MONTHS - 13 WEEK ROLLING

• The 13-week rolling averages reflect a more recent performance profile compared to the 52-week

rolling averages. It highlights performance that has been improving over the last six months has

stabilised over the last couple of months with the impact of the recent COVID lockdowns yet to be

seen.

• The Rehabilitation Outcome Groups are continuing to focus on at risk claims between 1-

182 and 183-365 days of weekly compensation. These claims are being identified

weekly using pre-defined data points. Results have remained strong and progress has

been made in the following areas;

• Automating the identification of claims at risk is being tested (initially in low numbers)

within the Rehabilitation Outcome Groups. The success of this versus the manually

identified ones will feed into continuously improving the accuracy of the modelling and

ultimately lead to a fully automated solution.

• In Supported Recovery, capability-based allocations is being piloted in two geographical

areas. The intention here is to ensure that claims with inherent outcome risks are

allocated to Recovery staff with the capability to manage those risks.

• In Assisted Recovery the dedicated teams of people focusing on client and employer

welcome conversations and recovery check-ins have achieved significant results that we

expect to flow through to tighter duration management. Welcome conversations are

being undertaken within 2 days and recovery check-ins have reduced by ~6,000.

Monitoring has verified the quality of interactions is also high.

Actions

50%

55%

60%

65%

70%

75%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21

75%

80%

85%

90%

95%

100%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

273-day rate (CY-20) 273-day rate (CY-21)

• The charts below represent weekly results for the ten week and the nine month rates over the

2020 and 2021 calendar years. The 2020 results (light blue line) show that weekly performance

dropped sharply about 9-10 weeks after the start of the lockdown. For the current lockdown, the

expectation is for a similar decline in short term rehabilitation results, which will be reflected in a

sharp decline in the weekly results over the coming month.

25%

35%

45%

55%

65%

75%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

70-day rate (CY-20) 70-day rate (CY-21)

90.7%

64.0%

WEEKLY TEN WEEK RATE PERFORMANCE WEEKLY NINE MONTH RATE PERFORMANCE

10 Week Rehab Rate (RHS)9 Month Rehab Rate (LHS) 10 Week Target (RHS)9 Month Target (LHS)

16

Customer Experience: Long-term rehabilitation: Weekly Compensation

MEASUREMOST RECENT

RESULT

YTD

ACTUALTREND

FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Growth rate of the long-term claims pool September 2021 +8.1% Improving +9.5% G +8.7%

Long-term claims pool returns to independence September 2021 5,174 Improving 5,200 G 4,978

Rate of long-term clients in part-time work September 2021 12.9% Stable 11.5% G 12.6%

2 Claims receiving WC for greater than 365 days.

5,200

0

1,000

2,000

3,000

4,000

5,000

6,000

31JUL2018 31DEC2018 31MAY2019 31OCT2019 31MAR2020 31AUG2020 31JAN2021 30JUN2021 30NOV2021 30APR2022

LONG-TERM CLAIMS POOL RETURN TO INDEPENDENCE

• Growth of the long-term claims pool 2 (LTCP) has improved in the last two

quarters following low WC commencements last year due to the national COVID

lockdown. There has also been improvement in short-term rehabilitation

performance which has slowed new entries.

• In recent months, exit volumes have continued to remain relatively high.

Because of the lag in our reporting from when a client ceases WC to being

counted as an exit, results for August were similar to other months.

However, since early September the volume of LTCP exits have been lower.

• Following the August COVID lockdown, we expect some delays for long-

term clients accessing providers for medical and vocational assessments,

and other services. These delays are expected to slow the progress of

returning some clients to independence in future months.

• At this stage our full year outlook for these measures remains green.

However following the August COVID lockdown there is a degree of

uncertainty as to what our June 2022 position will be.

• All non-serious injury related return to work rates for long-term WC clients have

returned to, pre-COVID levels in March 2020.

Growth rate of the long-term claims pool

• The work in Supported Recovery focused on LTCP claims under 912 days is

continuing. So far over 500 claims have been reviewed with approximately

68% being considered on track, the balance are being considered for more

intense rehabilitation, commencement of the Vocational Independence

process or suspension of entitlements. This work is now being replicated in

Assisted Recovery.

GROWTH IN LONG-TERM CLAIMS POOL

9.5%

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

0%

2%

4%

6%

8%

10%

12%

14%

16%

Jul-18 Nov-18 Mar-19 Jul-19 Nov-19 Mar-20 Jul-20 Nov-20 Mar-21 Jul-21 Nov-21 Mar-22

CL

AIM

CO

UN

T

GR

OW

TH

RA

TE

(%

)

Actions

LTCP Return to Independence Target

LTCP Claim Volumes TargetGrowth Rate

5,174

8.1%

17

Customer Experience: Rehabilitation: non-weekly compensation

• September’s result for this measure has improved, up from 87.2% in both July

and August 2021 and 87.1% in June.

• Results for this measure have declined noticeably since its peak in May 2020,

which was temporarily inflated by impacts of last year’s COVID lockdown. As

this measure checks the status of new registrations after 12 months, the effects

of last year’s alert level restrictions were felt later on.

• Although there has been some improved results in recent months, we may see

another temporary rise in this rate soon. This is because clients who are not

able to access services during the 2021 COVID lockdown may be counted as

having returned to independence when they may in fact still require further

services. However, at this point in time it is too early to say how this will affect

results.

Return to independence for those not in the workforce.

MEASURE MOST RECENT

RESULT

YTD

ACTUAL

TREND FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Return to independence for those not in the workforce September 2021 87.5% Improving 87.5% G 87.1%

RETURN TO INDEPENDENCE FOR THOSE NOT IN WORKFORCE - 52 WEEK ROLLING

87.5%

RTI for those not in the workforce Target

85%

86%

87%

88%

89%

90%

Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21

18

Sustainability: Financial KPIs

MEASURE MOST RECENT

RESULT

YTD

ACTUAL

TREND FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Actuarial movement June 2021 +1.08% StableWithin

-3% to +1.5% G +1.08%

Investment performance after costs relative to benchmark September 2021 +0.32% Improving +0.15% G +1.90%

Investment management costs as a proportion of total funds under management September 2021 0.15% Stable 0.15% G 0.14%

Change in average treatment cost per claim September 2021 +6.0% Stable ≤ 5% A +6.1%

Administration cost per claim September 2021 $1,509 Stable $1,4593 A $2,403

Percentage of total expenditure paid directly to clients or for services to clients September 2021 87.7% Stable 88.2%3 A 88.3%

Claims processed per FTE September 2021 549 Deteriorating 583 A 580

Average care hours per serious injury claim September 2021 1,393 Stable 1,387 G 1,396

Change in average treatment cost per claim September 2021 +6.0% Stable ≤ +5.0% A +6.1%

• Decreased to 549 reflects 157,000 fewer claims and 58 fewer FTE than Budget. Year-end

performance is at risk.

• Our current forecast includes a ~150 increase in FTE compared with budget. Most of this

increase is additional resources to support all our customers recovering from injury

through the customer contact centre (One Front Door). Other growth areas are the

Customer Group restructure, Pae Ora and Investments.

• The reduction in new claims volumes resulting from the COVID alert level 4 lockdown

could affect this result further. We do however expect claim volumes to bounce back as

we come out of lockdown.

Claims processed per FTE

Administration cost per claim and % of expenditure paid directly to clients

• Increased FTE forecast increases administration costs. The COVID lockdown may reduce

claims costs. This makes achieving this target uncertain.

3 Presented on a YTD basis for comparability. Full year targets are $2,762 and 88.5% as outlined in the Service Agreement 2021/22.

(Previously: G)

(Previously: G)

• The rolling 12-month growth in average treatment cost per claim increased 0.2% ($4)

to +6.0% ($35) in September 2021. This measure includes the change in the volume

of claims accessing services, price and utilisation of services.

• With in-person access to many services extremely limited during alert levels 3 and

4,claims mix changes occur due to fewer clients with lower acuity injuries accessing

treatment. This increases the ratio of clients with higher acuity injuries, which tend to

have higher treatments per claim.

• Counselling, Hand Therapy, Dental and Physiotherapy all currently have above

budget increases in costs per claim. These are offset by lower than budget Surgery,

Audiology and Radiology costs

• Fewer minor injury claims and reduced access to services as a result of COVID

restrictions will influence this measure over the next 12 months.

Average treatment cost per claim

19

Sustainability: Financial Summary

$m YTD

ACTUAL

YTD

BUDGET

YTD

STATUS

FULL YEAR

BUDGET

Income

Levy revenue 1,269 1,279 A 5,175

Interest, dividend and rental income 4 329 289 G 1,044

Other income - 1 1

Total income 1,598 1,569 G 6,220

Expenditure

Claims paid (1,355) (1,433) G (5,759)

OCL expected (increase)/decrease (329) (306) A (1,523)

OCL net losses from other factors - - -

URL (increase)/decrease 411 337 G (8)

Core operating costs (124) (124) G (501)

Other operating costs (72) (74) G (278)

Total operating costs (196) (198) G (780)

Total expenditure (1,469) (1,600) G (8,070)

Surplus / (deficit) from insurance

operations129 (31) G (1,850)

Net gains (losses) on investments147 69 389

Net gains (losses) in discount and

inflation rates on OCL(3,026) 0 -

Net (deficit) surplus (2,750) 38 (1,461)

• Levy revenue is $10m or 0.9%, below budget year to date, mainly from

unfavourable variances in the Work Account $6m and Earners Account $10m.

This is offset by favourable variances in the Motor Vehicle Account and Non-

Earner’s Account. The unfavourable variances are due to reduced liable earnings

for self-employed (Work and Earners accounts) and a reduction in the weighted

average levy rate for standard employers reflecting a lower rate achieved to date

on provisional invoices issued for the 2021/22 year.

• Total investment income of $476m is $118m higher than budget of $358m year to

date. The investment reserves portfolio has returned 1.00% after costs September

year to date, outperforming the benchmark by 0.32% after costs.

• Total claims paid YTD are $78m or 5.4% under budget. This is mainly due to the

lockdown impact on treatment volumes along with smaller variances in some

rehabilitation services. Weekly compensation is over budget due to increased

claims volumes, but partly offset by the lockdown impact on new claims as well as

lower wage inflation.

• New registered claims growth is up 9.7% and new weekly compensation claims

growth is up 17.4%.

• Total operating costs are $2m or 1.0% under budget. This includes

• Injury Prevention costs are $7m or 23.3% under budget which but is still

expected to be on budget full year. Risk exist with some programme delivery

impacted by the COVID lockdowns.

• Enterprise Change Programme operating costs are $5m or 20.0% over budget

due to the additional effort for initiatives supporting the data centre exits,

including Health Sector Strategy Tech ART (T-ART) and Te Kahu (Corporate

Enterprise Resource Planning) project.

Key points

4 In line with the intention to exclude gains and losses on investments relating to market movement and economic factors impacting OCL

within the return from insurance operations sub-total, income relating to interest, dividend and rental income are recorded separately.

20

The OCL has increased by $3.4b YTD to $58.7b. Economic movements resulted in a YTD

increase of $3.0b.

OUTSTANDING CLAIMS LIABILITY

• The single effective discount rate decreased 7 basis points to 2.87% in September

(3.0% in June 2021).

• A new 30 year bond was issued in September. This has changed the shape of the

discount rate curve and means reaching the long term discount rate of 4.30% has

been pushed out a further 10 years.

• The YTD OCL increase due to discount rates is $2.0 billion.

• The projected inflation over the medium term (up to 2037) increased 7 basis points

to 2.01% at the end of September 2021 (1.88% June 2021).

• The YTD OCL increase due to inflation projections ($962 million), and the

difference between actual versus expected inflation ($92 million) totals $1,054

million.

Inflation Rate movements.

Sustainability: Outstanding Claims Liability

FUNDING SUFFICIENCY

125.7%

106.7%

115.1%

76.3%

72.9%

153.0%

2017/18 2018/19 2019/20 2020/21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 2021/22Budget

Earners' portion of Treatment

Injury - pre and post 1999Work Motor Vehicle Earners’

Non-earners’ – Post 2001 Funding Ratio TargetNon-earners' portion of

Treatment Injury - post 2001

153.5%

123.7%

114.5%

106.5%

76.8%

75.6%

LEVIED AND NON-LEVIED FUNDING RATIOS

• The funding position is the measure of the applicable assets available to cover the value of what is

intended to be the fully funded portion of the liabilities in each Account. The funding position is

expressed as a ratio of the assets divided by the liabilities for each Account. The calculation of the

applicable assets and liabilities is defined in the funding policy.

• Where there is a positive funding balance, the assets exceed the liabilities and the funding ratio is

greater than 100%. When there is a negative funding balance, the assets are less than the

liabilities and the funding ratio is less than 100%.

• The funding position is influenced by several factors including our investments, economic factors,

claiming behaviour being different to expectations and approval of recommended levy changes.

These have a cumulative impact to result in under or over funding of the Accounts.

• All funding ratios have improved from June mainly due to the affect of changes in external

economic factors on the Outstanding Claims Liability.

Discount rates continues to fluctuate.

55,387

58,742

329

1,054

1,972

50,000

52,000

54,000

56,000

58,000

60,000

OCL as at

01/07/2021

Expected increase Inflation related

changes

Discount rate

assumptions

OCL as at

30/09/2021

OCL: ANALYSIS OF CHANGE ($m) YTD

215 The OCL multipliers are calculated by dividing the OCL by the 2020/21 cash cost. Multipliers can be used as a proxy for duration and

represent the sensitivity of OCL to the movement in cash costs. Sensitive claims are modelled as a separate payment type in the OCL now.

The impact of these claims is not included in the above multipliers. Sensitive claims impact weekly compensation and medical treatment.

$m AVE ANNUAL GROWTH

FY19 – FY21

GROWTH ON

PRIOR YTD

YTD

ACTUAL

YTD

BUDGET

VARIANCE % VARIANCE YTD

STATUS

FY

BUDGET

OCL

MULTIPLIER5

Weekly compensation (15)% (12)% 467 458 (9) (2)% A 1,870 X7.7

Other compensation 5% 8% 48 53 5 9% G 210

Total compensation (12)% (10)% 515 511 (4) (1)% A 2,080

Vocational rehabilitation 13% 32% 14 23 9 39% G 96 X3.1

Social rehabilitation (10)% (10)% 252 267 15 6% G 1,076 X28.5

Serious injury (5)% (22)% 154 161 (7) (5)% A 648 X41.5

Non-serious injury (21)% 13% 98 106 8 8% G 428 X6.4

Total rehabilitation (7)% (6)% 266 291 25 8% G 1,172

Medical treatment (9)% 5% 232 269 37 14% G 1,081 X2.9

Elective surgery (10)% 7% 112 125 13 10% G 481 X9.6

Public health acute services (6)% (13)% 163 157 (6) (3)% A 630

Other treatments (15)% (7)% 58 62 4 6% G 246

Total treatment (9)% 0% 565 613 48 8% G 2,438

All Other misc. expenses 1% 15% 9 18 9 47% G 69

Total claims paid (10)% (5)% 1,355 1,433 78 5% G 5,759

Increases in costs and higher costs than budget are depicted as negative percentages

Sustainability: Claims Costs – 30 September 2021

22

Sustainability: Claims Costs

• Total claims costs are under budget $78m (5%) YTD.

• COVID alert level restrictions have resulted in fewer treatment and rehabilitation

services being delivered, particularly in Auckland. This impacts not only on treatment

volumes but also lowers the average cost per claim. Uncertainty remains on when

Auckland will move to level 2 restrictions, or whether other parts of the country will

move into level 3 restrictions. Once Auckland returns to level 2, we expect to see a

catch up wave of both new claim volumes and increased service provision costs.

• Compensation costs are unfavourable by $4.6m (0.9%) YTD. For the month of

September compensation is favourable by $4.4m (2.6%) primarily as a result of fewer

new weekly compensation claims from alert level restrictions. We stopped all

suspension of weekly compensation decisions during level 4, and in level 3

suspension decisions need Client Service Leader approval. If a suspension decision

is made, clients will be provided with an additional two weeks notice than business as

usual timeframes. This will result in additional costs whilst level 3 continues but will be

offset by fewer claims.

• Further information on Weekly Compensation and Social Rehabilitation costs and

their impact on the OCL follows.

• Telehealth can be used where clinically appropriate for most treatment and

rehabilitation services under alert level 3 and 4 restrictions. This is dependent on

clients and providers both having access and capability to use the technology. The

largest users of telehealth are Physiotherapists, Hand Therapists and GPs. Over

35,000 telehealth consultations took place in the first full week of lockdown.

Telehealth utilisation has declined from 7 September when areas outside of Auckland

moved to level 2.

• Elective Surgery volumes continue to be impacted by the alert level restrictions in

Auckland. Costs are $13m (10%) favourable YTD. While most elective surgery in

Auckland could take place from 21 September (alert levels dropped), we are yet to

see volumes move closer to expected levels. This should align more closely to

expectations in October 2021.

Other services

Total claims paid

• Public Health Acute Services (PHAS): As per the June 2021 Board paper,

approved PHAS costs are $21m higher than budget. This is due to the final price

increase (12.35%) being higher than the budgeted price increase (8.9%). This

increase reflects demographic and cost pressures, and funding to support reducing

the Ministry of Health estimated gap between the PHAS price and the cost of

delivering PHAS services to clients. This has been incorporated into current

forecasts.

• Social rehabilitation non-capital costs: Factors such as pay equity agreement

changes, payment rates for in-between travel and workforce shortages / skill mix

changes will potentially put pressure on care costs.

• Non-Acute Rehabilitation (NAR): DHBs have requested that ACC reviews NAR

pricing. The DHBs cited a ~30% discrepancy between the rate ACC uses (for both

existing NAR and new Non-Acute Rehab Pathways contracts) and the cost to DHBs

(using rates from four DHBs). Three major DHBs have yet to sign the new contracts

due to pricing concerns but continue to provide services. A pricing review is

underway. Additional washups from the original pilot exceeded the accrued amount

putting pressure on 2021/22 budgets.

• Sick leave and Public holidays: Part year risk of potentially applying the increase in

sick leave allowances and the Matariki public holiday into the labour cost component

of our contract pricing from late 2021 This affects services such a Residential Support

Services and Home and Community Support Services.

• Air Ambulance cost pressures: Additional funding will be required to cover flight

hours where agreed annual limits have already been exceeded.

• High Tech Imaging (HTI): HTI volumes and demand are likely to continue to grow,

with both surgeons and client’s expectations of using HTI to support diagnosis and

treatment becoming more common. ACC received an external review of HTI services

in September 2021 and is currently considering the findings in the report in order to

plan how best to respond.

Risks to budget

23

KEY INSIGHTS CLAIMS COSTS

OCL IMPACT ACTIONS TO ADDRESS

OCL @ 30 September 2021: $13.2b

Claims < 5 years: ~$5.4b

Claims > 5 years: ~$7.8b

Influenceable OCL impact

@ 30 June 2021:(valuation result using 31 March

2021 data)

$503m

strain

Influenceable strain over past 7

years to 30 June 2021:$1,973m

• June 2021 quarter payments were only 0.1% higher than

expected based on the June 2021 OCL valuation. The

number of active weekly compensation claims was 4.3%

higher than expected, mainly caused by more new claims

for the 2021 accident year. This was partially offset by

average claim costs for the June quarter being 4% below

expected in most accident years including 2021.

• It is unclear at this stage how long the COVID-19

restrictions will be in place and how this may impact

rehabilitation rates.

• Claims over 5 years old are staying on claim longer than

expected. If this trend continues, this could result in

significant OCL strain (>$100 million) at the December

valuation

• The June 2021 quarter actual claim payments are indicating an OCL strain of around $15 million for the December

2021 valuation (excluding the strain for claims over 5 years risk mentioned above). Most of the strain is currently

coming through the Earners’ and Work accounts. There are small releases in Motor Vehicle and Non-Earners’.

WEEKLY COMPENSATIONOCL $13.2b to June 2021 BUDGET $1,870m

OCL6 BREAKDOWN

• The volume of new claims has fallen during the lockdowns due to a decline in injuries, especially outside the

home. Existing claims are staying on claim longer than expected, with the pause of weekly compensation

suspensions during these periods a contributing factor. The fall in new claims offset the higher continuance rates

for existing claims.

• Last lockdown, it took a significant period to see rehabilitation measures recover. It remains unclear how

rehabilitation performance may be impacted by this lockdown.

• During previous lockdowns, there was an expectation that unemployment would increase significantly, and the

economy would take some time to recover. The economic recovery was faster than expected and employment

levels returned close to pre-COVID-19 levels. This meant that new weekly compensation claims returned to

normal levels quickly. We expect similar results to follow the current lockdown.

POTENTIAL COVID-19 LOCKDOWN IMPACT

• Total compensation costs are $5m (1%) over budget YTD. The

weekly compensation component is $9.3m overbudget YTD.

For September 2021, compensation costs are $4m (2.6%)

favourable of which, the weekly compensation component is

$3m (2.1%) favourable.

• Higher than expected volumes and durations YTD have

increased compensation costs by 1.6%. Lower than estimated

wage inflation, has however provided an offset of 2.0%.

• We expect that impacts from this COVID outbreak will be felt

for several months due to an extended period of lockdown for

Auckland and changes to suspension of weekly compensation

decisions whilst businesses are unable to operate in level 3.

• Factors outside of ACC’s control such as capacity issues for

specialist assessment and treatment may result in a prolonged

recovery and clients requiring longer periods receiving weekly

compensation.

• Further comments on weekly compensation, rehabilitation

performance and actions to address cost growth are included

in the previous short-term and long-term rehabilitation sections.

6 All OCL figures quoted in this paper include risk margin, liability for the Accredited Employers

Programme and exclude liability for gradual process Incurred But Not Reported claims.

24

OCL @ 30 September 2021: $22.2b

Claims < 5 years: ~$5.1b

Claims > 5 years: ~$17.1b

Influenceable OCL impact

@ 30 June 2021:(valuation result using 31 March

2021 data)

$129m

Strain

Influenceable strain over past

7 years to 30 June 2021:$1,439m

Non-Serious Injury non-capital:

• June quarter actual claim payments were 5.9% higher than

expected in the June 2021 valuation. Both active claims (4.3%)

and average costs (1.5%) were higher than expected.

Serious Injury non-capital:

• June quarter payments for attendant care were 3.1% lower than

expected in the June 2021 valuation. Attendant care hours were

1.7% below expected.

• The mix in care (between contracted and non-contracted) over

the quarter resulted in the average care rate being 2% lower than

expected. New serious injury claims are close to expected for the

June 2021 quarter but are still lower than pre-COVID-19 levels.

Non-Serious Injury: The experience is indicating a strain of around $6.5 million.

Serious Injury: Serious injury OCL impact is reassessed half-yearly.

SOCIAL REHABILITATION NON-CAPITAL OCL $22.2b, 2021/22 BUDGET $648m(non-capital payments includes attendant care, residential care, travel, assessments and active rehabilitation such as training for independence)

OCL BREAKDOWN KEY INSIGHTS

OCL IMPACTACTIONS TO ADDRESS

• We expect fewer new claims (both serious and non-serious) that require social rehabilitation

services. This is due to less traffic on the roads and fewer people taking part in higher risk

activities. After previous lockdowns, there was a significant catch up in the number of non-

serious injury claims. We expect a similar trend after this lockdown.

• Contracted and non-contracted care hours for existing clients may increase, as it did during

the previous lockdowns, due to increased support requirements while clients have limited or

constrained access to normal support services.

• It took some time to return clients back to normal care hours after the last lockdown. If

additional support hours remain in place, this will result in a significant OCL strain.

POTENTIAL COVID-19 LOCKDOWN IMPACT

CLAIMS COSTS

7 Personal supports include home care, residential care and inpatient rehabilitation

• While average care hours for serious injury claims have been reducing, there has

been growth in non-serious injury care hours per claim. We will review how

sustainable the actions implemented following the Attendant Care Proposition

Design earlier in 2021 have been. This will help us understand any further actions

needed to ensure appropriate controls are in place. Considerable work is still

needed in both contracted and non-contracted care hours to be able to realise

the targeted OCL release.

• Changes were made to the TFI adults with other injuries contract, and training

provided to frontline staff to ensure referrals for TFI programmes were targeted at

the right clients. Analysis has shown that these changes had made an impact

prior to the August lockdowns. Further work will take place to consider how to

optimise service utilisation across the range of different TFI services and ensure

clients who are not appropriate for TFI are referred onto other suitable services.

• Personal supports costs7 are $5.6m (3.4%) favourable

YTD.

• Average cost per claim for contracted care is over

budget for both serious injury and non-serious injury

clients. This is offset by under budget non-contracted

care (lower average costs and volumes).

• An improving trend in average care hours per serious

injury claim has been seen in the last quarter although

the impact of COVID lockdowns has resulted in

additional care hours being provided during August and

September. This is to ensure client needs are met while

access to other services (e.g. schools / daytime

activities) are restricted.

• Training for Independence (TFI) costs are $1.6m

favourable YTD. The significant growth seen over recent

years has started to abate as a result of targeted

actions to ensure the right clients are referred into TFI

services.

25

KEY INSIGHTS

OCL IMPACT ACTIONS TO ADDRESS

OCL @ 30 September 2021: $3.5b

Claims < 5 years: ~$0.8b

Claims > 5 years: ~$2.7b

Influenceable OCL impact

@ 30 June 2021:(valuation result using 31 March

2021 data)

$4m

strain

Influenceable strain over past

7 years to 30 June 2021:$600m

Non-Serious Injury

• Actual claim payments were 15.8% above expected in the June 2021 quarter.

Both active claim volumes (10.7%) and payments per active claim (4.6%) are

higher than expected.

• This was largely due to housing modifications increasing in volumes and cost.

Serious Injury

• June quarter actual payments were 4.3% higher than expected in the valuation,

mainly driven by spending on housing modifications and consumables.

• We anticipate a resurgence in demand for capital equipment following the

lockdown. This is unlikely to have a significant impact on the Outstanding

Claims Liability.

• Higher than expected capital claims growth has occurred at the same time as

higher than expected attendant care growth. It is reasonable to expect some

capital items purchased should reduce the requirement for attendant care. For

example, housing modifications making it possible for an injured client to do

more independently. It is not clear why there is no obvious offset to the amount

spent on capital and attendant care hours.

Non-Serious Injury: If experience continues there will be a strain, potentially up to

$30 million, in December.

Serious Injury: Serious injury OCL impact is reassessed half-yearly.

SOCIAL REHABILITATION CAPITAL OCL $3.5b, 2021/22 BUDGET $205m

OCL BREAKDOWN CLAIMS COSTS

• During the previous lockdowns, we saw an underspend in equipment and

modifications (vehicle and housing). This was followed by a significant catch-up and

resurgence in claims in the following quarters. We expect a similar trend to occur.

•

• Supply chain pressures in the construction industry partly driven by lockdowns are

causing delays and cost pressure on housing modifications.

• New claim volumes are likely to be low during level 4 and 3 lockdowns but return to

normal levels from level 2.

POTENTIAL COVID-19 LOCKDOWN IMPACT

• Capital costs continue to be affected by factors outside of ACC’s control, e.g. higher labour

and material costs in construction services, higher importation costs for motor vehicles etc.

This creates additional challenges in achieving a sustained change in trajectory that would

impact positively on OCL strain.

• Training has been rolled out this quarter across Partnered and Supported recovery teams to

improve participation in site visits. This aims to mitigate risks of scope creep and enable ACC

to be clear on expectations on what can and cannot be funded from the outset. Technological

options are being used to facilitate virtual visits when a physical presence is not feasible.

• A new supplier has been selected to supply Managed Rehabilitation Equipment Services from

1 November 2021. Work is underway to transition the service following which, a co-design

process will be used to develop improved cost management outcomes with the new supplier.

• Capital costs for home modifications are $1.6m

favourable YTD (19%), Higher costs for complex

housing modifications as a result of increasing

labour and materials costs are offset by lower

claim volumes and average costs per claim from

alert level restrictions

• Equipment costs are $4.4m favourable YTD with

lower volumes being offset to some extent by

higher costs per claim.

• Motor vehicle modifications are $0.7m

favourable (14.4%), again with lower costs per

claim and volumes.

26

Organisational Capability: People

MEASURE MOST RECENT

RESULT

YTD

ACTUAL

TREND FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Employee net promoter score June 2021 0 Stable +12 G 0

Proportion of ACC staff who identify as Māori June 2021 11.4% Stable 12.5% A 11.4%

Proportion of ACC staff who identify as having a disability June 2021 12.2% Stable 14.0% A 12.2%

Total recordable injury frequency rate September 2021 2.0 Stable <3.5 G 1.7

Lost-time injury frequency rate September 2021 1.5 Stable <1.1 G 1.1

Employee engagement Diversity and Inclusion

• The Executive engagement action plan is still a key focus and regular agenda

item with particular emphasis on flexibility, workload and communications.

There has been significant interest and positive feedback about the home

technology packages and well-being days. Both initiatives contribute to our

wider flexibility and well-being agenda. Over 1,800 technology packages have

been taken up so far and the offer of well-being days has been well received by

our people.

• The Pulse survey will open on 3 November, with results scheduled to be

shared in the first week of December.

• ACC’s employee turnover rate (12 month rolling) is increasing and is currently

16.8% (annualised). This is up from 11.2% at the same time last year but still

below the rate of 17.5% two years ago. We expect that the turnover rate will

continue to increase with the current employment market conditions and the Te

Kawa Mataaho pay guidance impact. We continue to focus on our people’s

development and targeted remuneration initiatives where required for retention.

• The participation of Māori and disabled staff continues to be an area of focus.

Our recruitment during September resulted in:

• 12.4% of external candidates who were offered roles were Māori;

• 11.3% of new hires were Māori, compared to 14.6% of all applicants.

• We continue our focus on disabled candidates through the recruitment

process, however the numbers are often under-represented as candidates

choose not to disclose their disability status at the time. During September

10.5% of external candidates who were hired identified as having a disability,

compared to 9.7% of all applicants.

27

Organisational Capability: People

Health, Safety and Wellbeing

• There were no recordable injuries during September. The lost time injury

frequency rate is above target for the year but we expect it to reduce over

the coming months. For the total recordable injury frequency rate, we are

ahead of target.

• ACC is continuing to actively manage stress incident claims received from

our people. This month we recorded our equal lowest level of workplace

stress incidents since January 2021. We are providing a deep dive into

workplace stress incidents at the October People and Remuneration

Committee meeting.

3.5

1.1

0

6

Jun-20 Aug-20 Oct-20 Dec-20 Feb-21 Apr-21 Jun-21 Aug-21 Oct-21 Dec-21

2.0

1.5

Other Recordable InjuriesLost Time Injuries TRIFR(12 Months)

LTIFR(12 Months)

TRIFR Target(12 Months)

LTIFR Target(12 Months)

NUMBER OF WORK RELATED STRESS INCIDENTS (REPORTED: 01/07/2020 – 30/09/2021)

6

12

13

15

14

10

4

17

20

24

27

21

12

20

12

0

5

10

15

20

25

30

31/07/2020 30/09/2020 30/11/2020 31/01/2021 31/03/2021 31/05/2021 31/07/2021 31/09/2021

NU

MB

ER

OF

IN

CID

EN

TS

28

Organisational Capability: Information and Technology

MEASUREMOST RECENT

RESULT

YTD

ACTUALTREND

FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

The number of category 3, 4 or 5 privacy breaches and near misses September 2021 0 Stable< 3

No Category 5 G 0

• 37 breaches were reported in September 2021, one at harm level

two and 36 at harm level one.

• The level of low-level breaches continues to be high, however

incidents are being well managed at the frontline.

• We have established a working group to review privacy issues

occurring in frontline teams. Privacy messaging to frontline staff

continues on a fortnightly basis.

MEASUREMOST RECENT

RESULT

YTD

ACTUALTREND

FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

Overall operational system availability September 2021 99.9% Stable 99.5% G 99.9%

• There were 2 incidents in September, including one medium impact event

(EOS) and one with no impact.

• The medium impact event meant frontline staff were unable to open

documents in EOS for reference when speaking with clients one morning until

8:45am. This was an unexpected consequence from a planned change and

was rolled back.

Operational Performance and incidents

29

ICIP: Integrated Change Investment Portfolio

The following is a summary of the status of our integrated change investment portfolio expenditure and benefit measures

$mMOST RECENT

RESULT

LIFE TO DATE

ACTUAL

LIFE TO DATE

BUDGET

FULL YEAR

OUTLOOK

LIFE TO DATE

JUNE 2021

WHOLE LIFE

BUDGET

Total cost September 2021 541 546 G 524 669

MEASUREMOST RECENT

RESULT

YTD

ACTUAL

FULL YEAR

TARGET

FULL YEAR

OUTLOOK

2020/21

ACTUAL

PAGE

REFERENCE

Client net trust score September 2021 +26.0 +31 G +25.0 10

Provider net trust score September 2021 -24.0 -13.0 A -25.0 10

Business net trust score September 2021 -21.0 -5.0 A -17.0 10

Claims processed per FTE September 2021 549 583 A 580 18

Average in weekly compensation days paid September 2021103.9 days

(-6.6 days)

102.3 Days(-4.9 days)

A 105.9 Days(-8.5 days)

14

Employee net promoter score June 2021 0 +12 G 0 26

30

Appendices: Appendix 1: Financial statements to 30 September 2021

$m YEAR TO DATE FULL YEAR 2021/22

ACTUAL8 BUDGET PRIOR YEAR ACTUAL BUDGET

Levy revenue 1,269 1,279 1,181 5,175

Interest, dividend and rental income 9 329 289 325 1,044

Other income - 1 - 1

Total income 1,598 1,569 1,506 6,220

Treatment (565) (613) (563) (2,438)

Rehabilitation (266) (291) (250) (1,172)

Compensation (515) (511) (469) (2,080)

Miscellaneous (9) (18) (11) (69)

Total claims paid (1,355) (1,433) (1,293) (5,759)

Expected increase in OCL (329) (306) (491) (1,523)

Impact of claims experience and modelling on OCL - - - -

Impact on other factors on OCL - - - -

Expected increase in URL 411 337 397 (8)

OCL and URL movement 82 31 (94) (1,531)

Investment management costs (excl. external management fees) (7) (7) (7) (31)

Injury prevention costs (23) (30) (21) (110)

Enterprise change programme (30) (25) (21) (92)

Depreciation & amortisation (12) (12) (12) (49)

Core operating costs (124) (124) (118) (498)

Total operating costs (196) (198) (179) (780)

Total expenditure (1,469) (1,600) (1,566) (8,070)

Performance from insurance operations 129 (31) (60) (1,850)

Net gains / (loss) on investments (incl. external management fees) 147 69 2,172 389

Net gains / (loss) from changes in discount and inflation rates on OCL (3,026) - (4,120) -

External factors (2,879) 69 (1,948) 389

Surplus / (deficit) (2,750) 38 (2,008) (1,461)

8 Actual – OCL adjustment is based on the full year valuation at 30 June 2021 and using the actual discount rate at 30 September 2021.

9 Investment returns are budgeted at between 2.63% - 4.13% for each Account. ACC chooses to incur many of the market risk exposures

through its investment portfolios, either because they provide a natural offset to risks inherent in the outstanding claims l iability, or

because it expects to enhance returns through prudent exposure to these risks.

Statement of financial performance

31

Appendices: Appendix 1: Financial statements to 30 September 2021

$m YEAR TO DATE 2021/22

ACTUAL BUDGET PRIOR YEAR ACTUAL BUDGET

Levy Revenue 205 210 188 850

Interest, dividend and rental income 73 69 75 248

Other income - - - -

Total Income 278 279 263 1,098

Total claims paid (244) (253) (238) (1,024)

Increase / (decrease) in outstanding claims liability (21) (7) (24) (76)

Movement in unexpired risk liability 125 99 125 (10)

Total operating costs (60) (59) (57) (231)

Total expenditure (200) (220) (194) (1,341)

Performance from Insurance Operations 78 59 69 (243)

Net gains / (loss) on investments (incl. external management fees) 19 4 440 40

Net gains / (loss) from changes in discount and inflation rates on OCL (303) - (512) -

External factors (284) 4 (72) 40

Surplus / (Deficit) (206) 63 (3) (203)

Work account

Motor Vehicle account

$m YEAR TO DATE 2021/22

ACTUAL BUDGET PRIOR YEAR ACTUAL BUDGET

Levy Revenue 118 114 102 460

Interest, dividend and rental income 101 92 99 332

Other income - - - -

Total Income 219 206 201 792

Total claims paid (170) (216) (165) (871)