Embed Size (px)

Citation preview

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 1 (of 40)

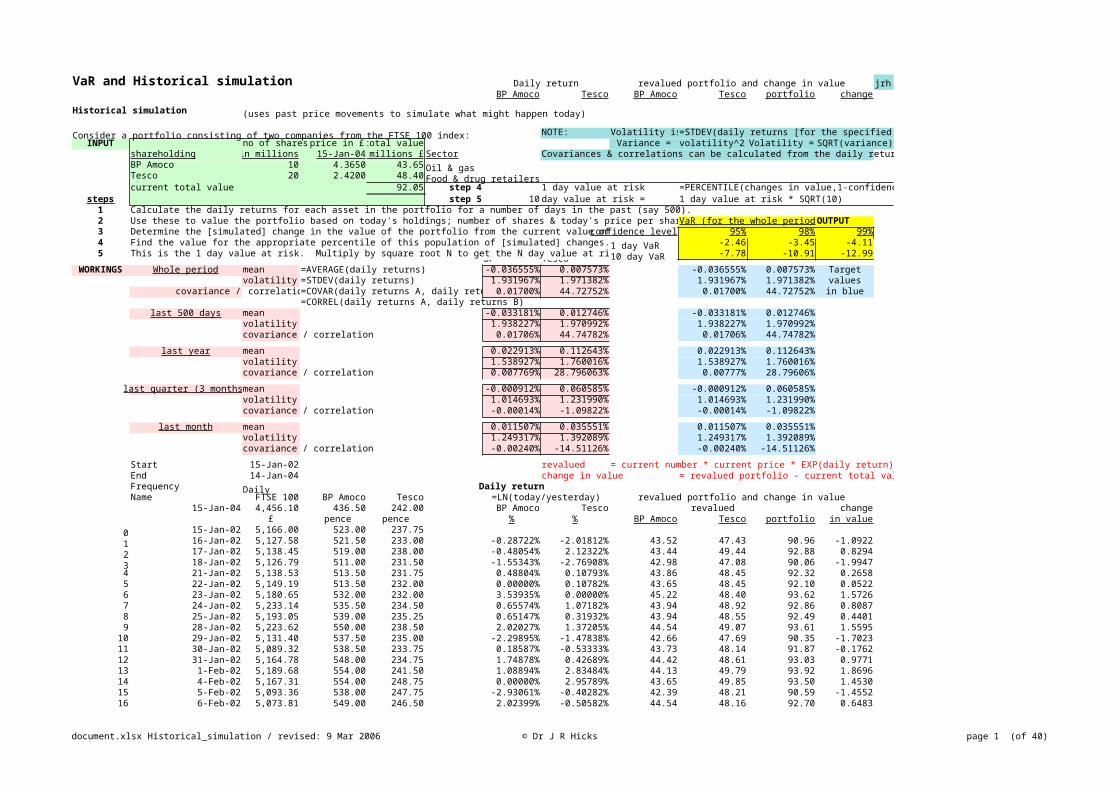

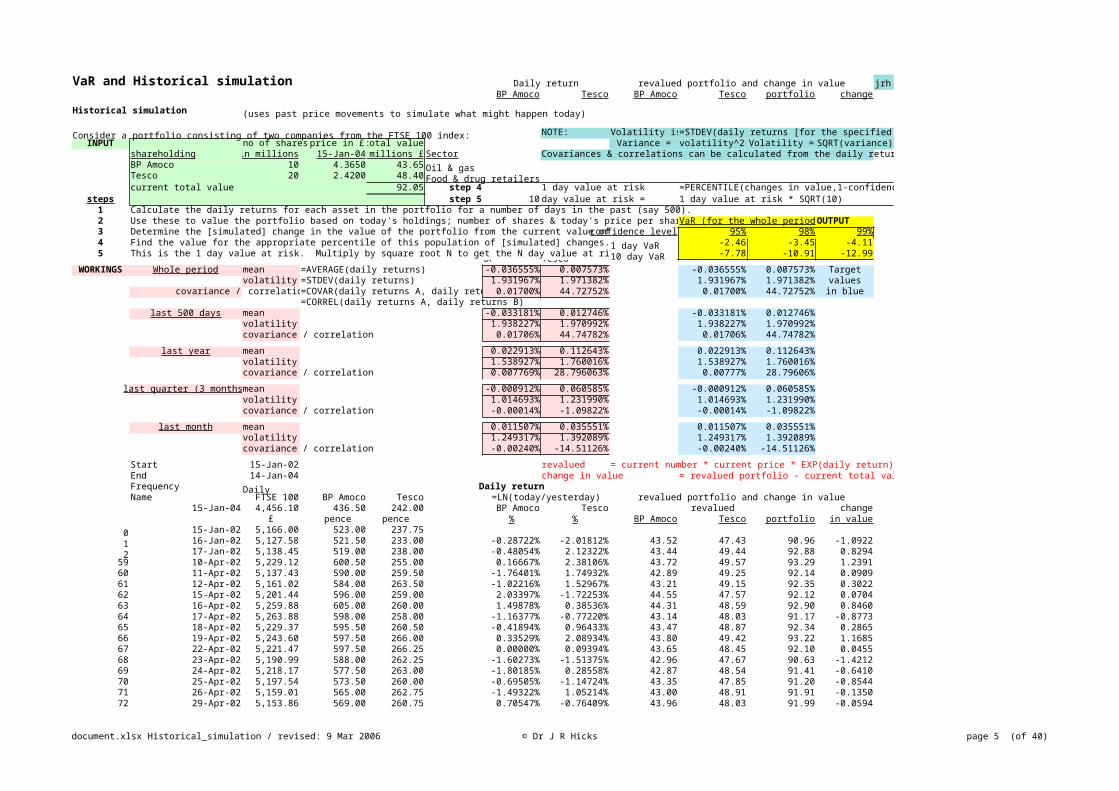

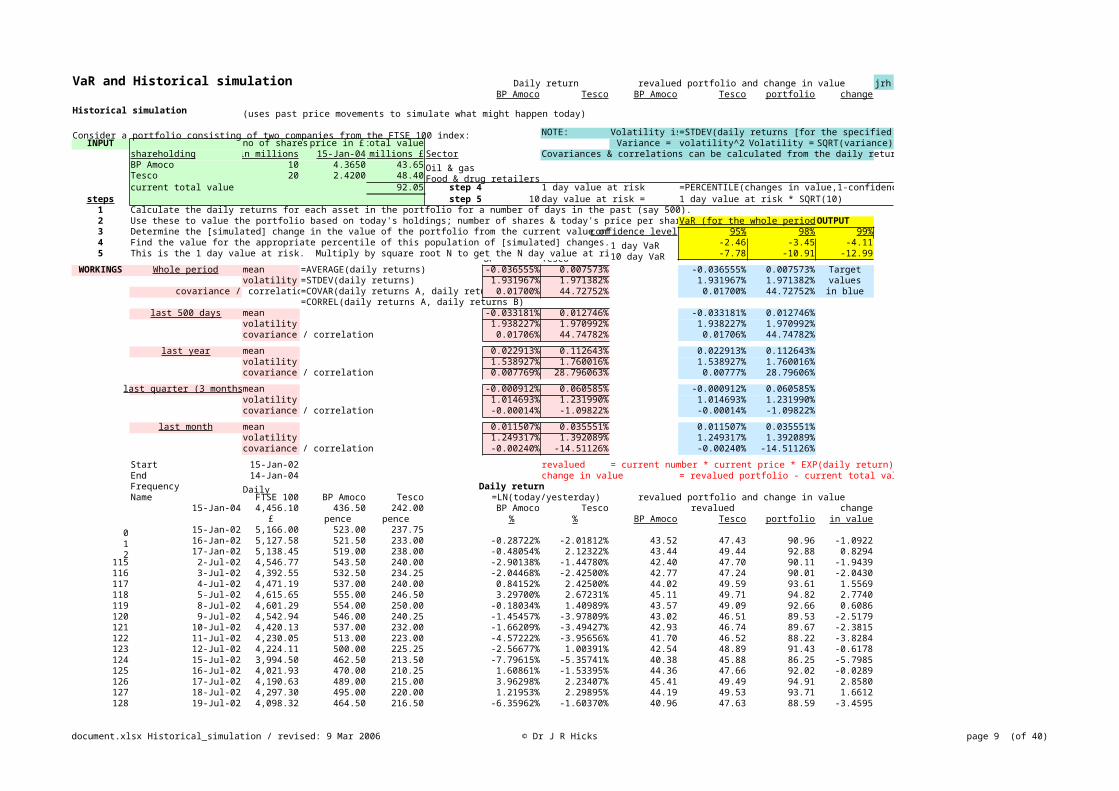

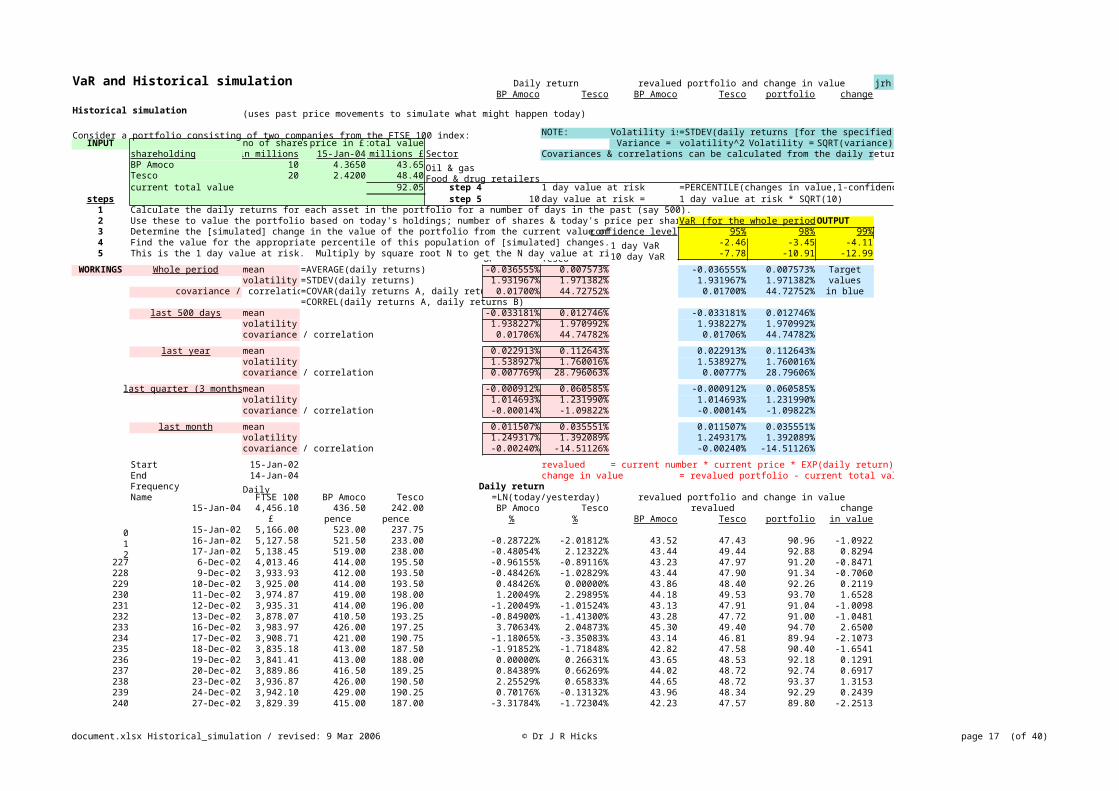

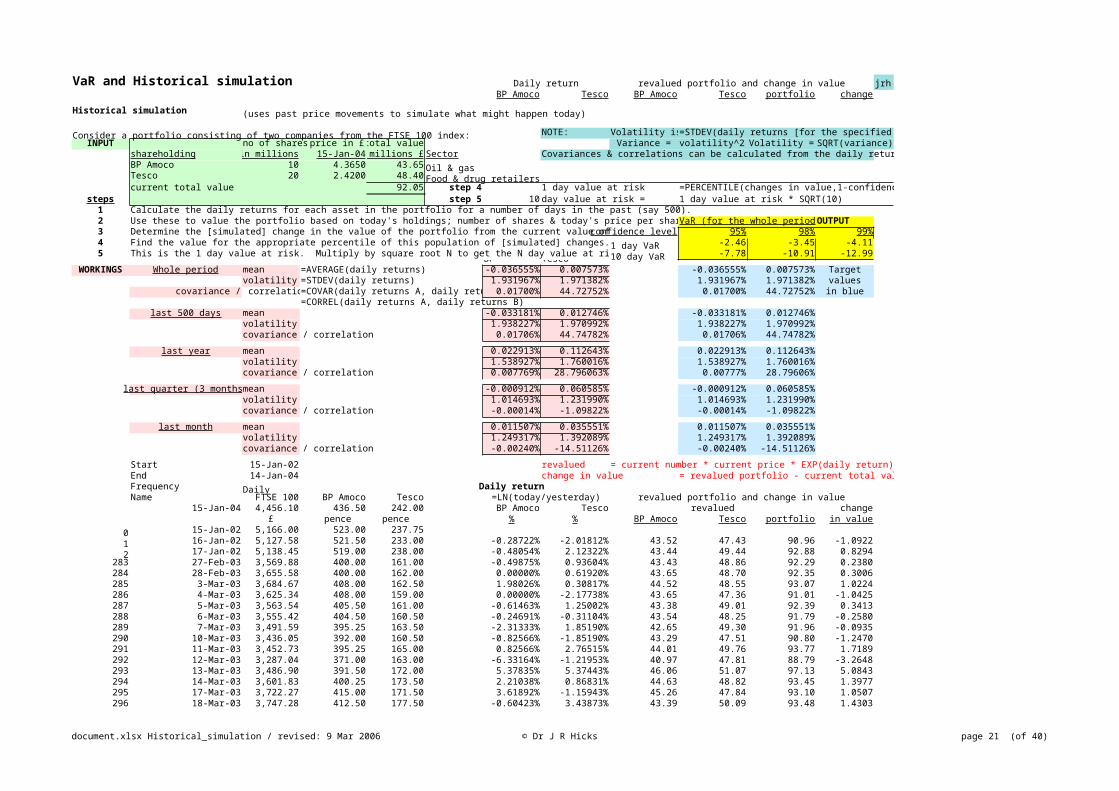

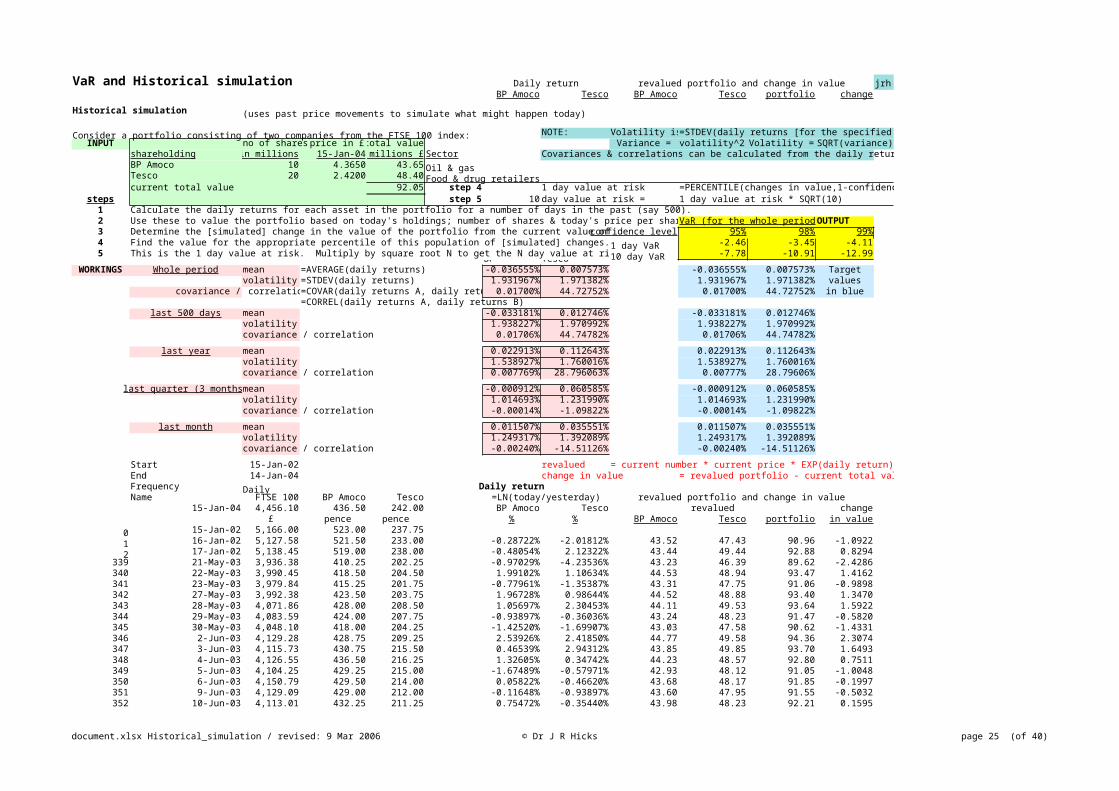

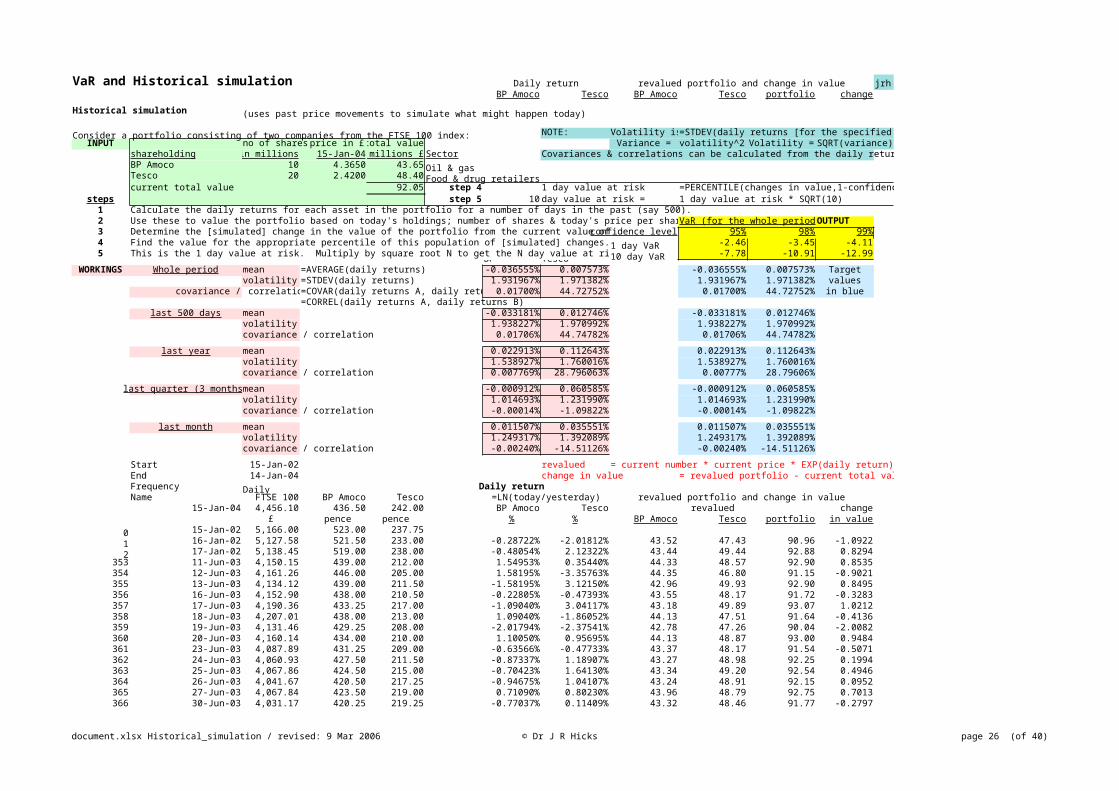

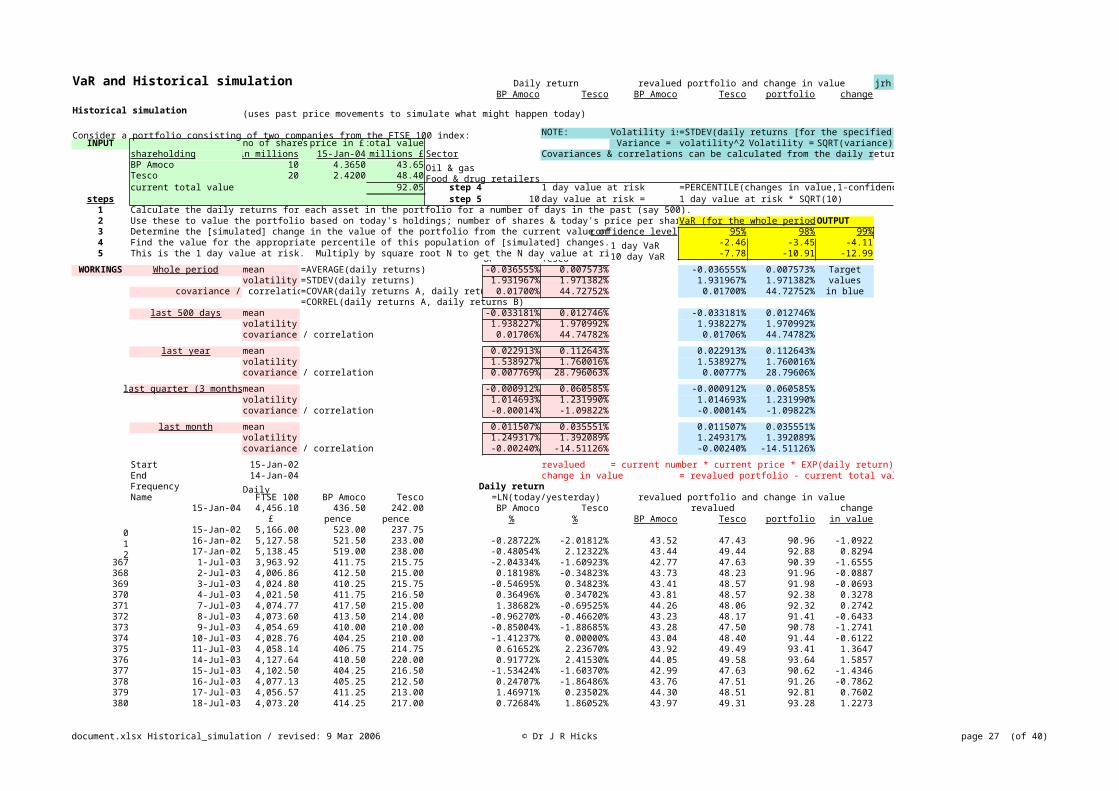

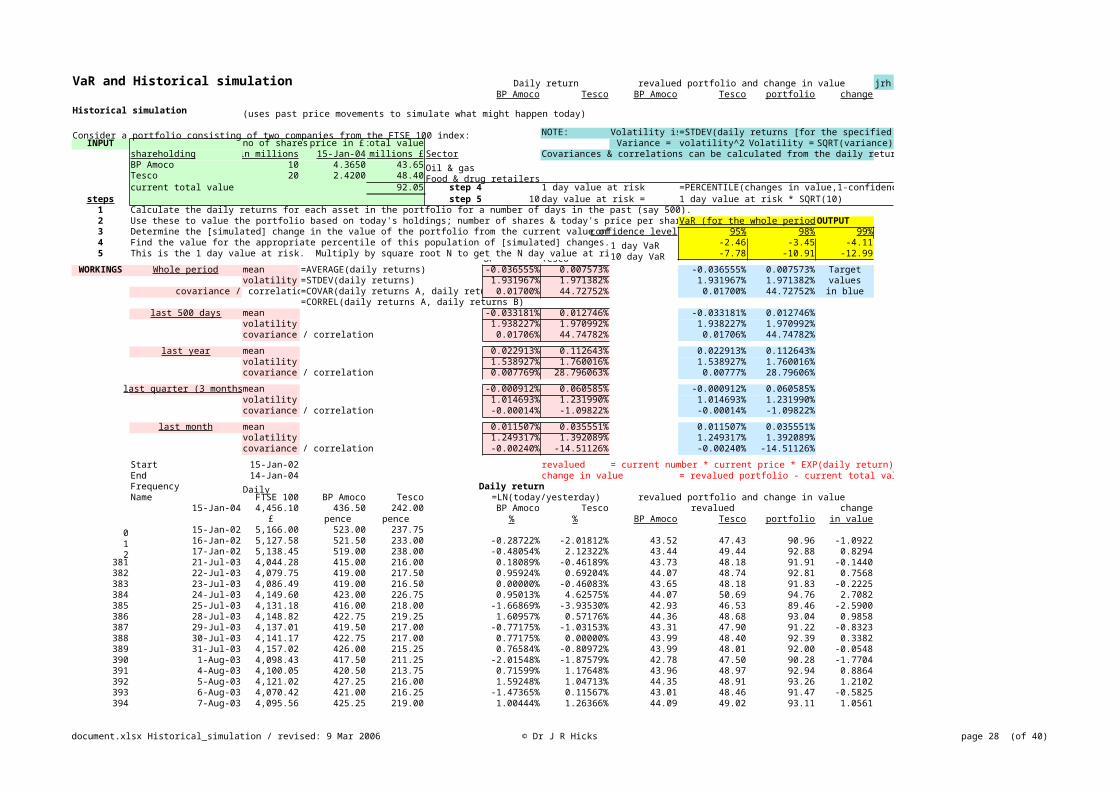

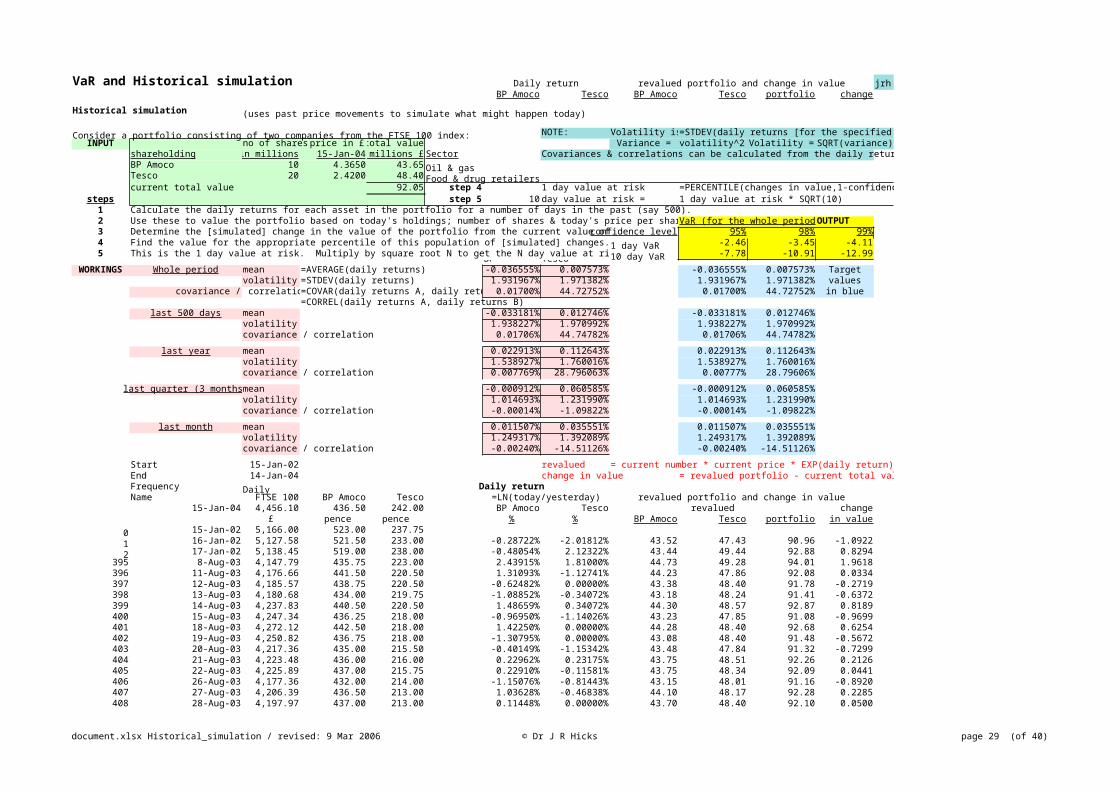

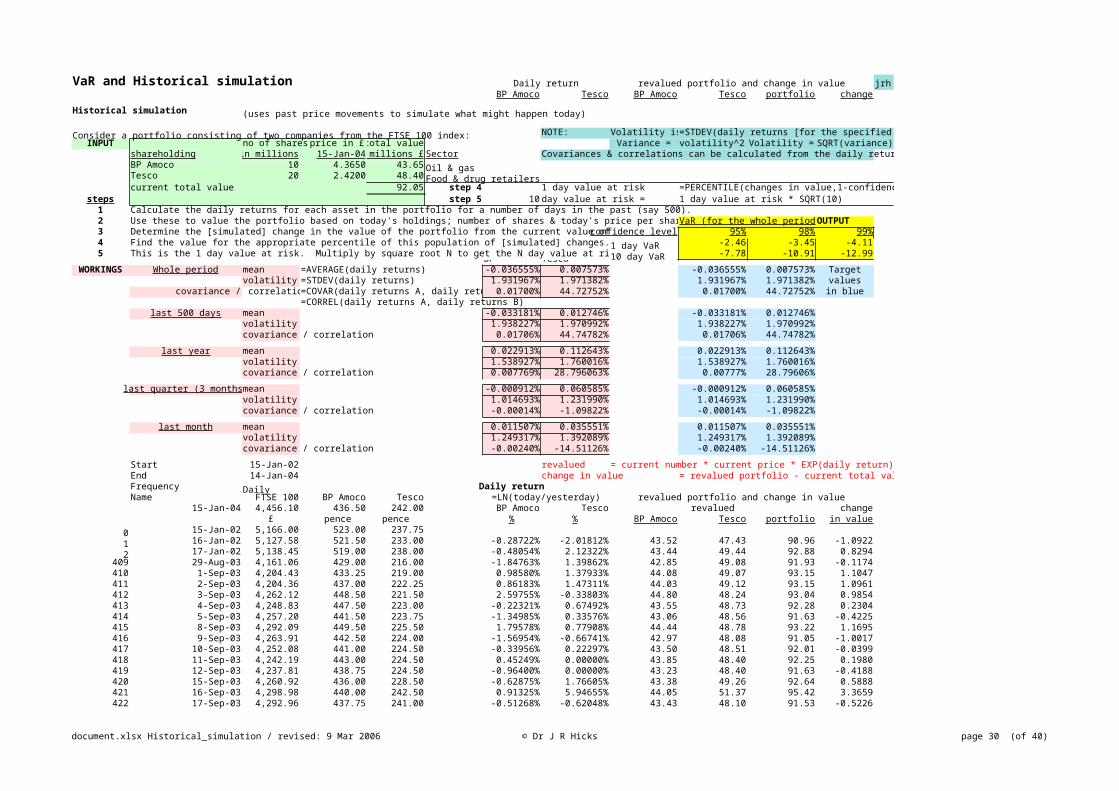

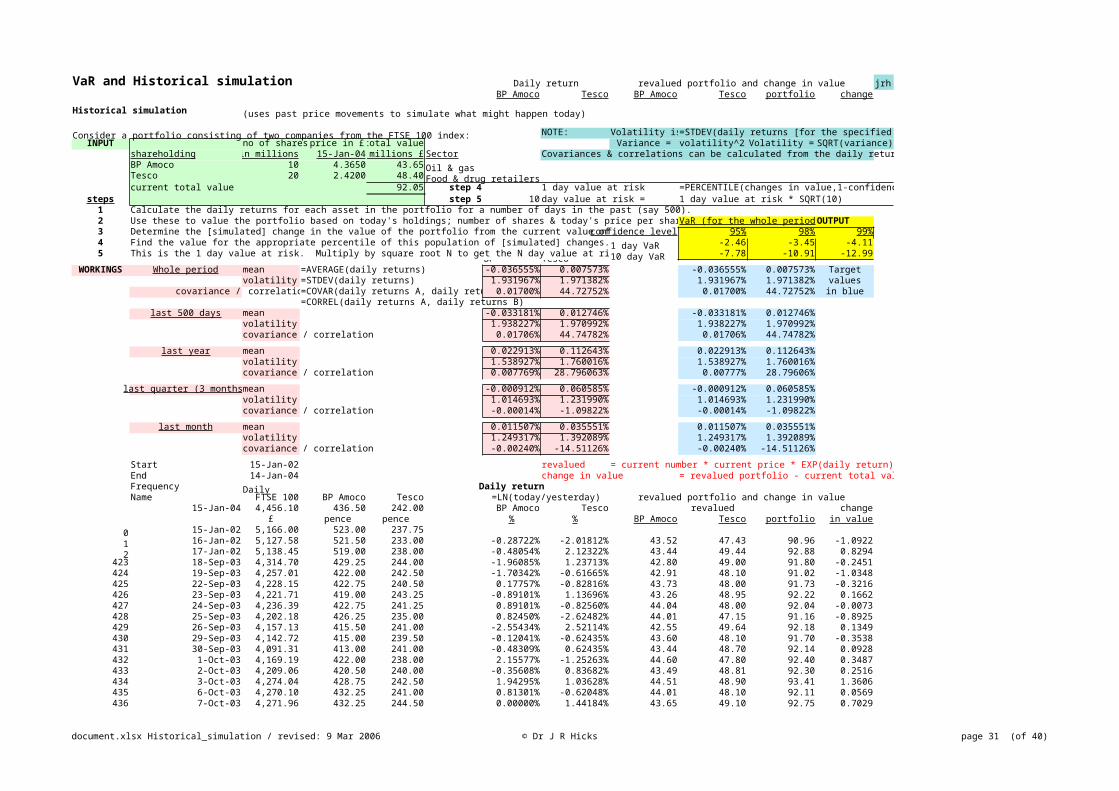

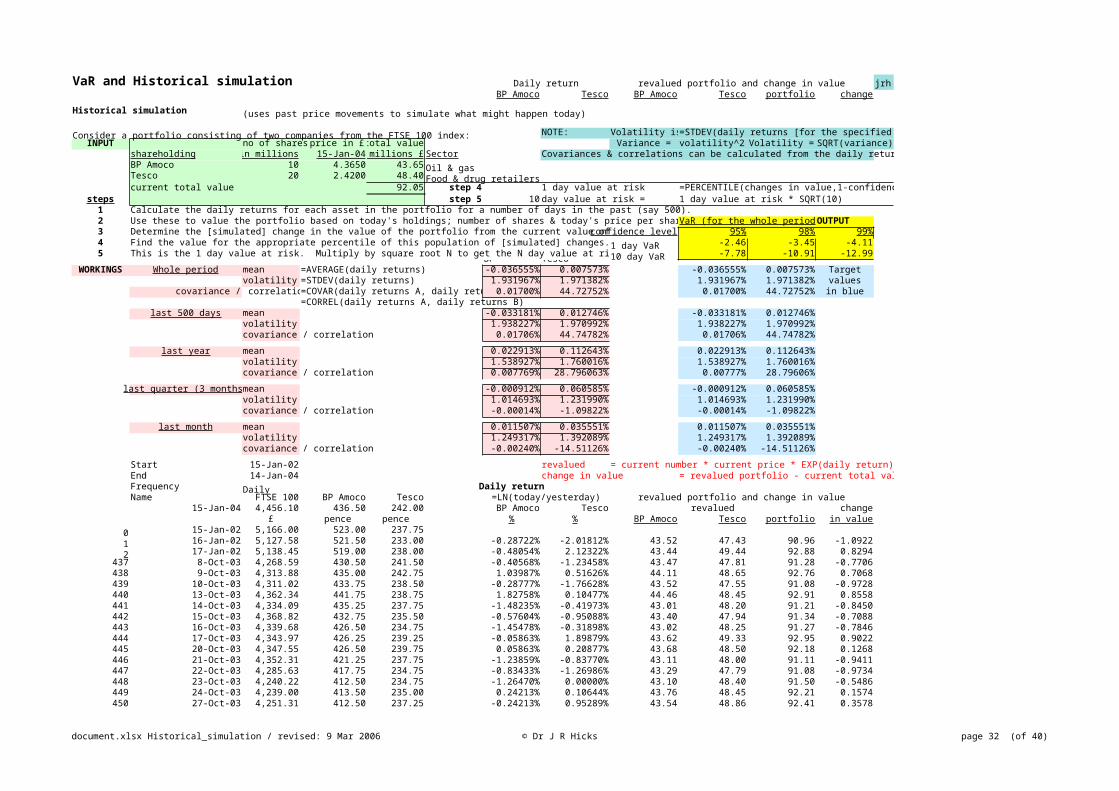

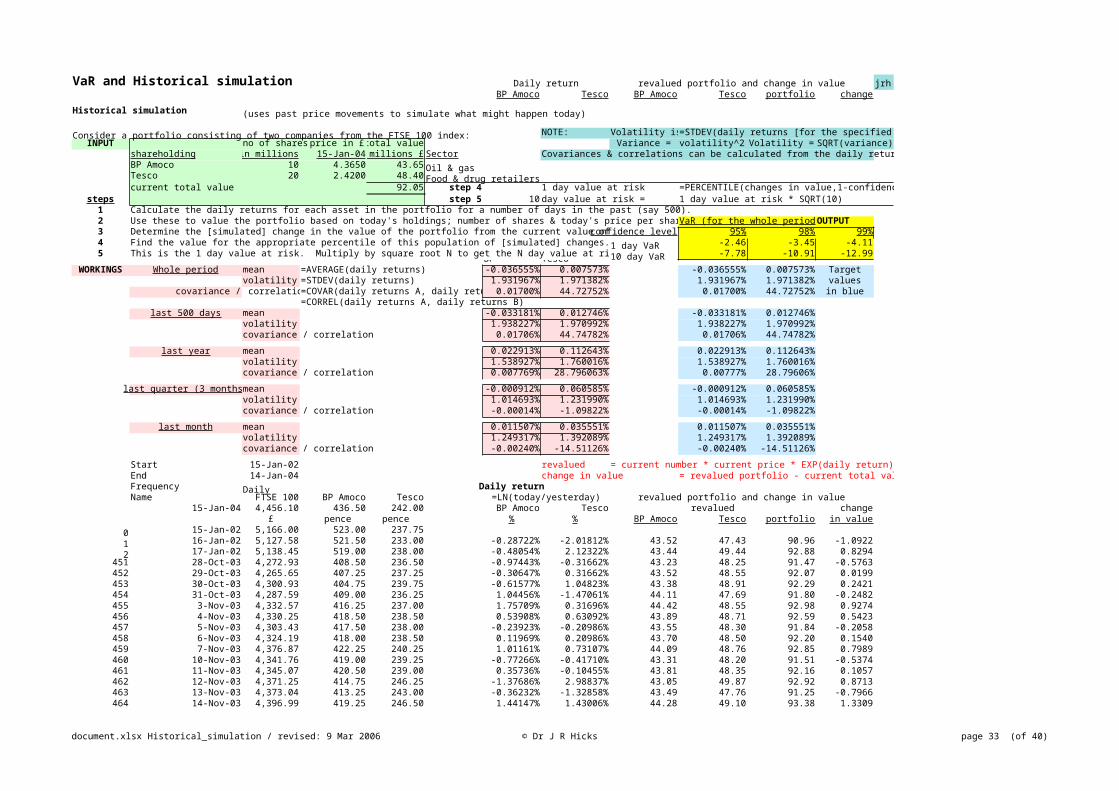

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.82943 18-Jan-02 5,126.79 511.00 231.50 -1.55343% -2.76908% 42.98 47.08 90.06 -1.99474 21-Jan-02 5,138.53 513.50 231.75 0.48804% 0.10793% 43.86 48.45 92.32 0.26585 22-Jan-02 5,149.19 513.50 232.00 0.00000% 0.10782% 43.65 48.45 92.10 0.05226 23-Jan-02 5,180.65 532.00 232.00 3.53935% 0.00000% 45.22 48.40 93.62 1.57267 24-Jan-02 5,233.14 535.50 234.50 0.65574% 1.07182% 43.94 48.92 92.86 0.80878 25-Jan-02 5,193.05 539.00 235.25 0.65147% 0.31932% 43.94 48.55 92.49 0.44019 28-Jan-02 5,223.62 550.00 238.50 2.02027% 1.37205% 44.54 49.07 93.61 1.5595

10 29-Jan-02 5,131.40 537.50 235.00 -2.29895% -1.47838% 42.66 47.69 90.35 -1.702311 30-Jan-02 5,089.32 538.50 233.75 0.18587% -0.53333% 43.73 48.14 91.87 -0.176212 31-Jan-02 5,164.78 548.00 234.75 1.74878% 0.42689% 44.42 48.61 93.03 0.977113 1-Feb-02 5,189.68 554.00 241.50 1.08894% 2.83484% 44.13 49.79 93.92 1.869614 4-Feb-02 5,167.31 554.00 248.75 0.00000% 2.95789% 43.65 49.85 93.50 1.453015 5-Feb-02 5,093.36 538.00 247.75 -2.93061% -0.40282% 42.39 48.21 90.59 -1.455216 6-Feb-02 5,073.81 549.00 246.50 2.02399% -0.50582% 44.54 48.16 92.70 0.6483

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 2 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

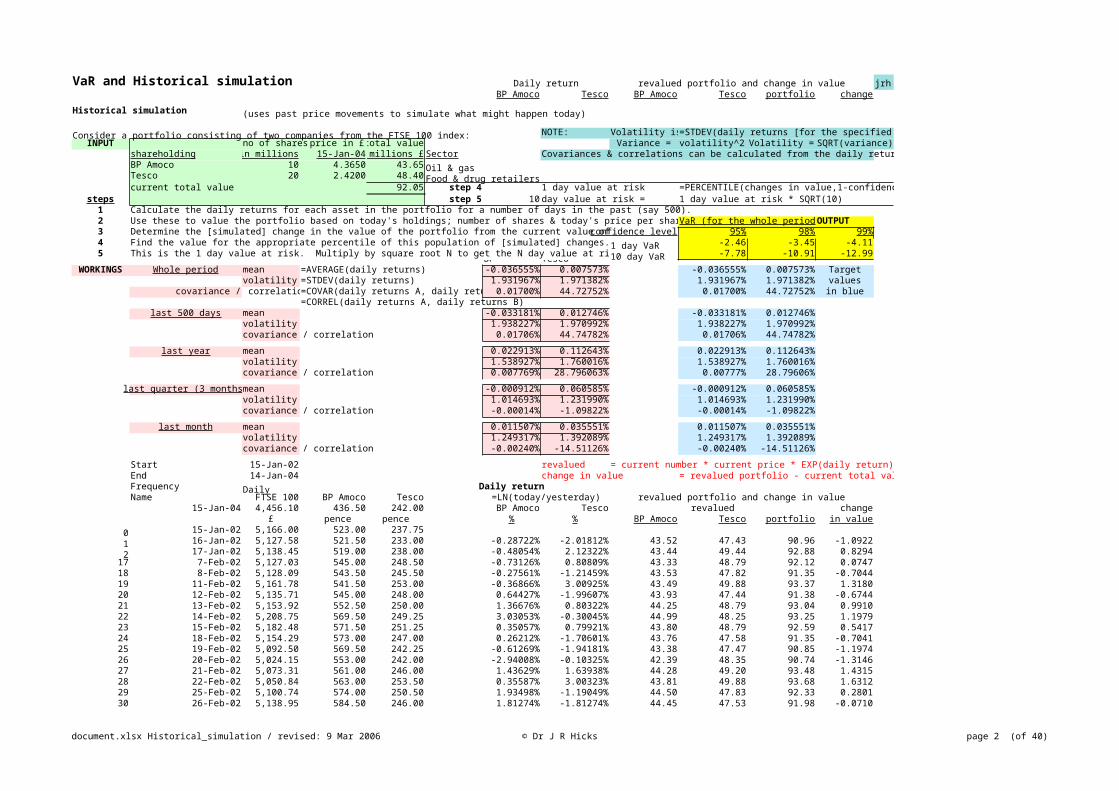

17 7-Feb-02 5,127.03 545.00 248.50 -0.73126% 0.80809% 43.33 48.79 92.12 0.074718 8-Feb-02 5,128.09 543.50 245.50 -0.27561% -1.21459% 43.53 47.82 91.35 -0.704419 11-Feb-02 5,161.78 541.50 253.00 -0.36866% 3.00925% 43.49 49.88 93.37 1.318020 12-Feb-02 5,135.71 545.00 248.00 0.64427% -1.99607% 43.93 47.44 91.38 -0.674421 13-Feb-02 5,153.92 552.50 250.00 1.36676% 0.80322% 44.25 48.79 93.04 0.991022 14-Feb-02 5,208.75 569.50 249.25 3.03053% -0.30045% 44.99 48.25 93.25 1.197923 15-Feb-02 5,182.48 571.50 251.25 0.35057% 0.79921% 43.80 48.79 92.59 0.541724 18-Feb-02 5,154.29 573.00 247.00 0.26212% -1.70601% 43.76 47.58 91.35 -0.704125 19-Feb-02 5,092.50 569.50 242.25 -0.61269% -1.94181% 43.38 47.47 90.85 -1.197426 20-Feb-02 5,024.15 553.00 242.00 -2.94008% -0.10325% 42.39 48.35 90.74 -1.314627 21-Feb-02 5,073.31 561.00 246.00 1.43629% 1.63938% 44.28 49.20 93.48 1.431528 22-Feb-02 5,050.84 563.00 253.50 0.35587% 3.00323% 43.81 49.88 93.68 1.631229 25-Feb-02 5,100.74 574.00 250.50 1.93498% -1.19049% 44.50 47.83 92.33 0.280130 26-Feb-02 5,138.95 584.50 246.00 1.81274% -1.81274% 44.45 47.53 91.98 -0.0710

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 3 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

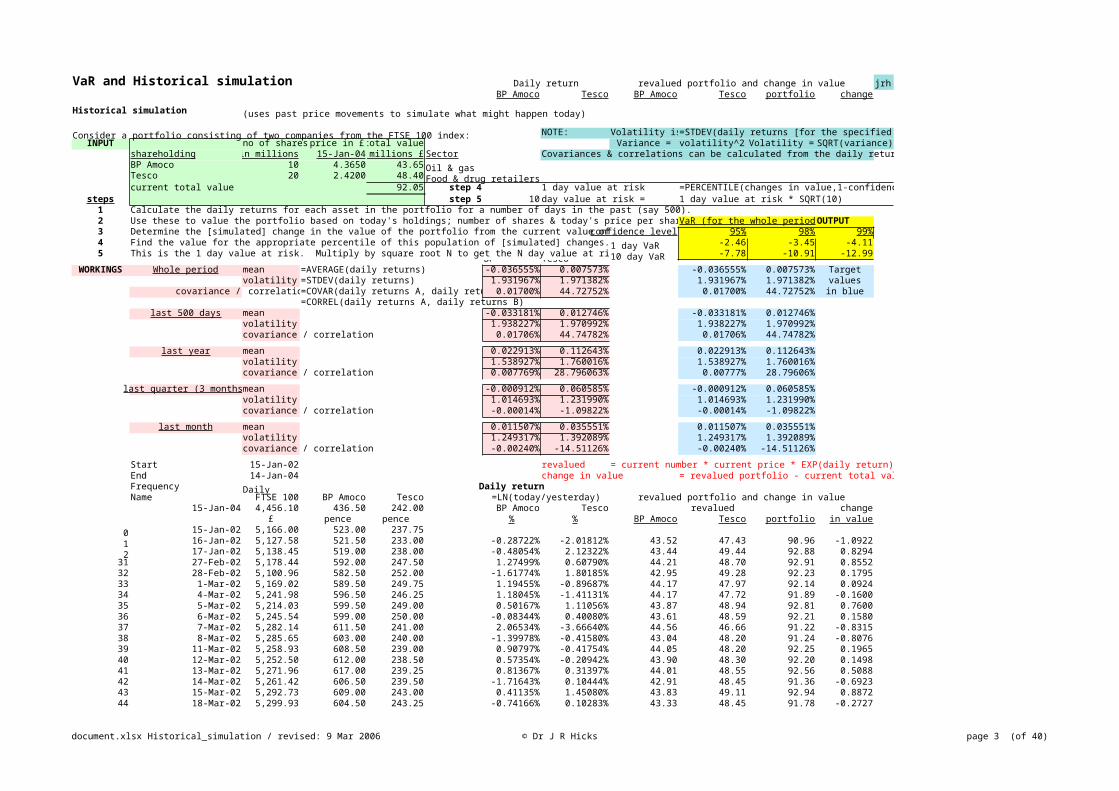

31 27-Feb-02 5,178.44 592.00 247.50 1.27499% 0.60790% 44.21 48.70 92.91 0.855232 28-Feb-02 5,100.96 582.50 252.00 -1.61774% 1.80185% 42.95 49.28 92.23 0.179533 1-Mar-02 5,169.02 589.50 249.75 1.19455% -0.89687% 44.17 47.97 92.14 0.092434 4-Mar-02 5,241.98 596.50 246.25 1.18045% -1.41131% 44.17 47.72 91.89 -0.160035 5-Mar-02 5,214.03 599.50 249.00 0.50167% 1.11056% 43.87 48.94 92.81 0.760036 6-Mar-02 5,245.54 599.00 250.00 -0.08344% 0.40080% 43.61 48.59 92.21 0.158037 7-Mar-02 5,282.14 611.50 241.00 2.06534% -3.66640% 44.56 46.66 91.22 -0.831538 8-Mar-02 5,285.65 603.00 240.00 -1.39978% -0.41580% 43.04 48.20 91.24 -0.807639 11-Mar-02 5,258.93 608.50 239.00 0.90797% -0.41754% 44.05 48.20 92.25 0.196540 12-Mar-02 5,252.50 612.00 238.50 0.57354% -0.20942% 43.90 48.30 92.20 0.149841 13-Mar-02 5,271.96 617.00 239.25 0.81367% 0.31397% 44.01 48.55 92.56 0.508842 14-Mar-02 5,261.42 606.50 239.50 -1.71643% 0.10444% 42.91 48.45 91.36 -0.692343 15-Mar-02 5,292.73 609.00 243.00 0.41135% 1.45080% 43.83 49.11 92.94 0.887244 18-Mar-02 5,299.93 604.50 243.25 -0.74166% 0.10283% 43.33 48.45 91.78 -0.2727

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 4 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

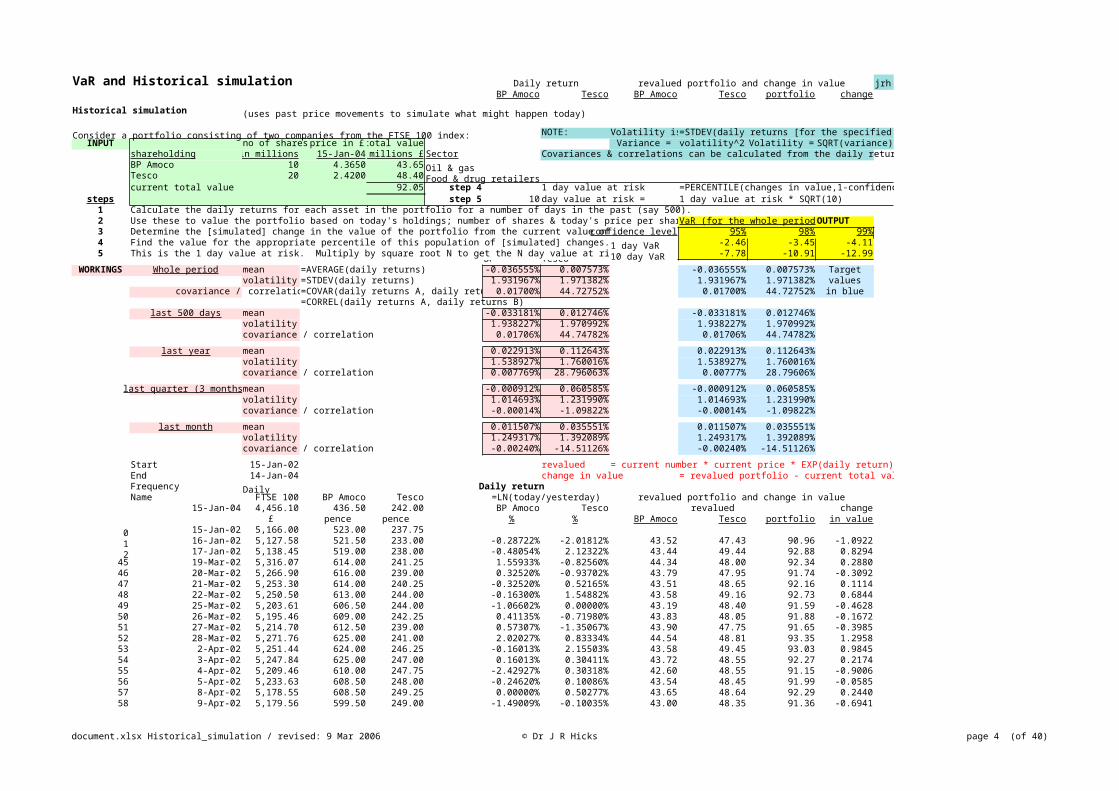

45 19-Mar-02 5,316.07 614.00 241.25 1.55933% -0.82560% 44.34 48.00 92.34 0.288046 20-Mar-02 5,266.90 616.00 239.00 0.32520% -0.93702% 43.79 47.95 91.74 -0.309247 21-Mar-02 5,253.30 614.00 240.25 -0.32520% 0.52165% 43.51 48.65 92.16 0.111448 22-Mar-02 5,250.50 613.00 244.00 -0.16300% 1.54882% 43.58 49.16 92.73 0.684449 25-Mar-02 5,203.61 606.50 244.00 -1.06602% 0.00000% 43.19 48.40 91.59 -0.462850 26-Mar-02 5,195.46 609.00 242.25 0.41135% -0.71980% 43.83 48.05 91.88 -0.167251 27-Mar-02 5,214.70 612.50 239.00 0.57307% -1.35067% 43.90 47.75 91.65 -0.398552 28-Mar-02 5,271.76 625.00 241.00 2.02027% 0.83334% 44.54 48.81 93.35 1.295853 2-Apr-02 5,251.44 624.00 246.25 -0.16013% 2.15503% 43.58 49.45 93.03 0.984554 3-Apr-02 5,247.84 625.00 247.00 0.16013% 0.30411% 43.72 48.55 92.27 0.217455 4-Apr-02 5,209.46 610.00 247.75 -2.42927% 0.30318% 42.60 48.55 91.15 -0.900656 5-Apr-02 5,233.63 608.50 248.00 -0.24620% 0.10086% 43.54 48.45 91.99 -0.058557 8-Apr-02 5,178.55 608.50 249.25 0.00000% 0.50277% 43.65 48.64 92.29 0.244058 9-Apr-02 5,179.56 599.50 249.00 -1.49009% -0.10035% 43.00 48.35 91.36 -0.6941

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 5 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

59 10-Apr-02 5,229.12 600.50 255.00 0.16667% 2.38106% 43.72 49.57 93.29 1.239160 11-Apr-02 5,137.43 590.00 259.50 -1.76401% 1.74932% 42.89 49.25 92.14 0.090961 12-Apr-02 5,161.02 584.00 263.50 -1.02216% 1.52967% 43.21 49.15 92.35 0.302262 15-Apr-02 5,201.44 596.00 259.00 2.03397% -1.72253% 44.55 47.57 92.12 0.070463 16-Apr-02 5,259.88 605.00 260.00 1.49878% 0.38536% 44.31 48.59 92.90 0.846064 17-Apr-02 5,263.88 598.00 258.00 -1.16377% -0.77220% 43.14 48.03 91.17 -0.877365 18-Apr-02 5,229.37 595.50 260.50 -0.41894% 0.96433% 43.47 48.87 92.34 0.286566 19-Apr-02 5,243.60 597.50 266.00 0.33529% 2.08934% 43.80 49.42 93.22 1.168567 22-Apr-02 5,221.47 597.50 266.25 0.00000% 0.09394% 43.65 48.45 92.10 0.045568 23-Apr-02 5,190.99 588.00 262.25 -1.60273% -1.51375% 42.96 47.67 90.63 -1.421269 24-Apr-02 5,218.17 577.50 263.00 -1.80185% 0.28558% 42.87 48.54 91.41 -0.641070 25-Apr-02 5,197.54 573.50 260.00 -0.69505% -1.14724% 43.35 47.85 91.20 -0.854471 26-Apr-02 5,159.01 565.00 262.75 -1.49322% 1.05214% 43.00 48.91 91.91 -0.135072 29-Apr-02 5,153.86 569.00 260.75 0.70547% -0.76409% 43.96 48.03 91.99 -0.0594

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 6 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

73 30-Apr-02 5,165.58 585.50 263.00 2.85857% 0.85919% 44.92 48.82 93.73 1.683474 1-May-02 5,125.51 578.00 258.25 -1.28923% -1.82259% 43.09 47.53 90.62 -1.433375 2-May-02 5,174.06 577.50 258.75 -0.08654% 0.19342% 43.61 48.49 92.11 0.055976 3-May-02 5,203.05 594.00 262.00 2.81709% 1.24822% 44.90 49.01 93.91 1.855177 7-May-02 5,119.90 576.00 260.50 -3.07717% -0.57416% 42.33 48.12 90.45 -1.599878 8-May-02 5,209.10 583.00 262.00 1.20795% 0.57416% 44.18 48.68 92.86 0.809279 9-May-02 5,197.58 587.00 263.50 0.68376% 0.57089% 43.95 48.68 92.63 0.576680 10-May-02 5,171.24 585.00 263.00 -0.34130% -0.18993% 43.50 48.31 91.81 -0.240681 13-May-02 5,204.84 590.00 262.00 0.85107% -0.38095% 44.02 48.22 92.24 0.189082 14-May-02 5,239.47 606.00 260.75 2.67574% -0.47824% 44.83 48.17 93.00 0.952883 15-May-02 5,259.11 596.00 260.25 -1.66393% -0.19194% 42.93 48.31 91.24 -0.813184 16-May-02 5,248.53 596.00 260.75 0.00000% 0.19194% 43.65 48.49 92.14 0.093085 17-May-02 5,217.98 592.00 261.50 -0.67340% 0.28722% 43.36 48.54 91.90 -0.153786 20-May-02 5,208.10 589.50 259.75 -0.42319% -0.67147% 43.47 48.08 91.54 -0.5082

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 7 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

87 21-May-02 5,197.21 596.00 258.25 1.09659% -0.57915% 44.13 48.12 92.25 0.201888 22-May-02 5,151.89 584.00 255.50 -2.03397% -1.07057% 42.77 47.88 90.66 -1.394389 23-May-02 5,175.31 584.00 258.75 0.00000% 1.26399% 43.65 49.02 92.67 0.615790 24-May-02 5,169.07 591.00 254.00 1.19150% -1.85281% 44.17 47.51 91.68 -0.365391 27-May-02 5,136.26 588.00 249.50 -0.50891% -1.78754% 43.43 47.54 90.97 -1.079192 28-May-02 5,074.22 573.50 246.25 -2.49690% -1.31116% 42.57 47.77 90.34 -1.706993 29-May-02 5,082.98 580.00 250.00 1.12702% 1.51136% 44.14 49.14 93.28 1.231894 30-May-02 5,040.75 576.50 251.00 -0.60528% 0.39920% 43.39 48.59 91.98 -0.069895 31-May-02 5,085.07 585.00 258.00 1.46365% 2.75066% 44.29 49.75 94.04 1.993496 5-Jun-02 4,989.15 565.00 252.50 -3.47861% -2.15483% 42.16 47.37 89.53 -2.524197 6-Jun-02 4,957.63 564.00 257.75 -0.17715% 2.05789% 43.57 49.41 92.98 0.929198 7-Jun-02 4,920.40 558.00 258.50 -1.06953% 0.29056% 43.19 48.54 91.73 -0.323599 10-Jun-02 4,928.21 555.50 255.25 -0.44904% -1.26522% 43.45 47.79 91.25 -0.8041

100 11-Jun-02 4,934.82 560.00 256.50 0.80682% 0.48852% 44.00 48.64 92.64 0.5906

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 8 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

101 12-Jun-02 4,851.67 551.00 252.00 -1.62020% -1.76996% 42.95 47.55 90.50 -1.5506102 13-Jun-02 4,771.91 542.50 254.50 -1.55467% 0.98717% 42.98 48.88 91.86 -0.1932103 14-Jun-02 4,630.77 523.50 239.50 -3.56511% -6.07474% 42.12 45.55 87.67 -4.3814104 17-Jun-02 4,756.75 540.00 248.75 3.10321% 3.78950% 45.03 50.27 95.30 3.2451105 18-Jun-02 4,702.01 541.00 246.50 0.18501% -0.90864% 43.73 47.96 91.69 -0.3570106 19-Jun-02 4,652.43 538.00 245.00 -0.55607% -0.61038% 43.41 48.11 91.51 -0.5366107 20-Jun-02 4,580.34 538.50 241.25 0.09289% -1.54245% 43.69 47.66 91.35 -0.7002108 21-Jun-02 4,605.35 532.00 239.00 -1.21440% -0.93702% 43.12 47.95 91.07 -0.9783109 24-Jun-02 4,541.87 531.00 240.00 -0.18815% 0.41754% 43.57 48.60 92.17 0.1205110 25-Jun-02 4,630.96 545.50 241.25 2.69408% 0.51948% 44.84 48.65 93.49 1.4440111 26-Jun-02 4,531.01 534.50 238.00 -2.03711% -1.35631% 42.77 47.75 90.52 -1.5322112 27-Jun-02 4,540.65 535.00 238.50 0.09350% 0.20986% 43.69 48.50 92.19 0.1425113 28-Jun-02 4,656.36 551.00 238.50 2.94681% 0.00000% 44.96 48.40 93.36 1.3054114 1-Jul-02 4,685.76 559.50 243.50 1.53087% 2.07476% 44.32 49.41 93.74 1.6880

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 9 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

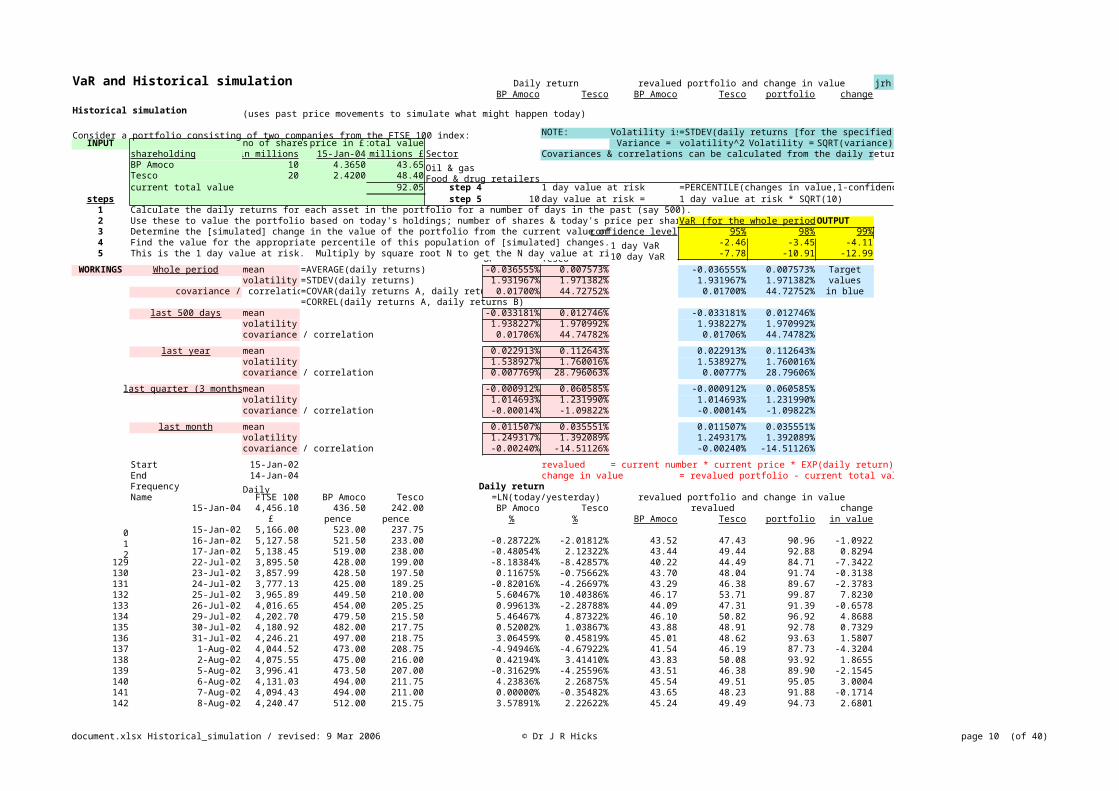

115 2-Jul-02 4,546.77 543.50 240.00 -2.90138% -1.44780% 42.40 47.70 90.11 -1.9439116 3-Jul-02 4,392.55 532.50 234.25 -2.04468% -2.42500% 42.77 47.24 90.01 -2.0430117 4-Jul-02 4,471.19 537.00 240.00 0.84152% 2.42500% 44.02 49.59 93.61 1.5569118 5-Jul-02 4,615.65 555.00 246.50 3.29700% 2.67231% 45.11 49.71 94.82 2.7740119 8-Jul-02 4,601.29 554.00 250.00 -0.18034% 1.40989% 43.57 49.09 92.66 0.6086120 9-Jul-02 4,542.94 546.00 240.25 -1.45457% -3.97809% 43.02 46.51 89.53 -2.5179121 10-Jul-02 4,420.13 537.00 232.00 -1.66209% -3.49427% 42.93 46.74 89.67 -2.3815122 11-Jul-02 4,230.05 513.00 223.00 -4.57222% -3.95656% 41.70 46.52 88.22 -3.8284123 12-Jul-02 4,224.11 500.00 225.25 -2.56677% 1.00391% 42.54 48.89 91.43 -0.6178124 15-Jul-02 3,994.50 462.50 213.50 -7.79615% -5.35741% 40.38 45.88 86.25 -5.7985125 16-Jul-02 4,021.93 470.00 210.25 1.60861% -1.53395% 44.36 47.66 92.02 -0.0289126 17-Jul-02 4,190.63 489.00 215.00 3.96298% 2.23407% 45.41 49.49 94.91 2.8580127 18-Jul-02 4,297.30 495.00 220.00 1.21953% 2.29895% 44.19 49.53 93.71 1.6612128 19-Jul-02 4,098.32 464.50 216.50 -6.35962% -1.60370% 40.96 47.63 88.59 -3.4595

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 10 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

129 22-Jul-02 3,895.50 428.00 199.00 -8.18384% -8.42857% 40.22 44.49 84.71 -7.3422130 23-Jul-02 3,857.99 428.50 197.50 0.11675% -0.75662% 43.70 48.04 91.74 -0.3138131 24-Jul-02 3,777.13 425.00 189.25 -0.82016% -4.26697% 43.29 46.38 89.67 -2.3783132 25-Jul-02 3,965.89 449.50 210.00 5.60467% 10.40386% 46.17 53.71 99.87 7.8230133 26-Jul-02 4,016.65 454.00 205.25 0.99613% -2.28788% 44.09 47.31 91.39 -0.6578134 29-Jul-02 4,202.70 479.50 215.50 5.46467% 4.87322% 46.10 50.82 96.92 4.8688135 30-Jul-02 4,180.92 482.00 217.75 0.52002% 1.03867% 43.88 48.91 92.78 0.7329136 31-Jul-02 4,246.21 497.00 218.75 3.06459% 0.45819% 45.01 48.62 93.63 1.5807137 1-Aug-02 4,044.52 473.00 208.75 -4.94946% -4.67922% 41.54 46.19 87.73 -4.3204138 2-Aug-02 4,075.55 475.00 216.00 0.42194% 3.41410% 43.83 50.08 93.92 1.8655139 5-Aug-02 3,996.41 473.50 207.00 -0.31629% -4.25596% 43.51 46.38 89.90 -2.1545140 6-Aug-02 4,131.03 494.00 211.75 4.23836% 2.26875% 45.54 49.51 95.05 3.0004141 7-Aug-02 4,094.43 494.00 211.00 0.00000% -0.35482% 43.65 48.23 91.88 -0.1714142 8-Aug-02 4,240.47 512.00 215.75 3.57891% 2.22622% 45.24 49.49 94.73 2.6801

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 11 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

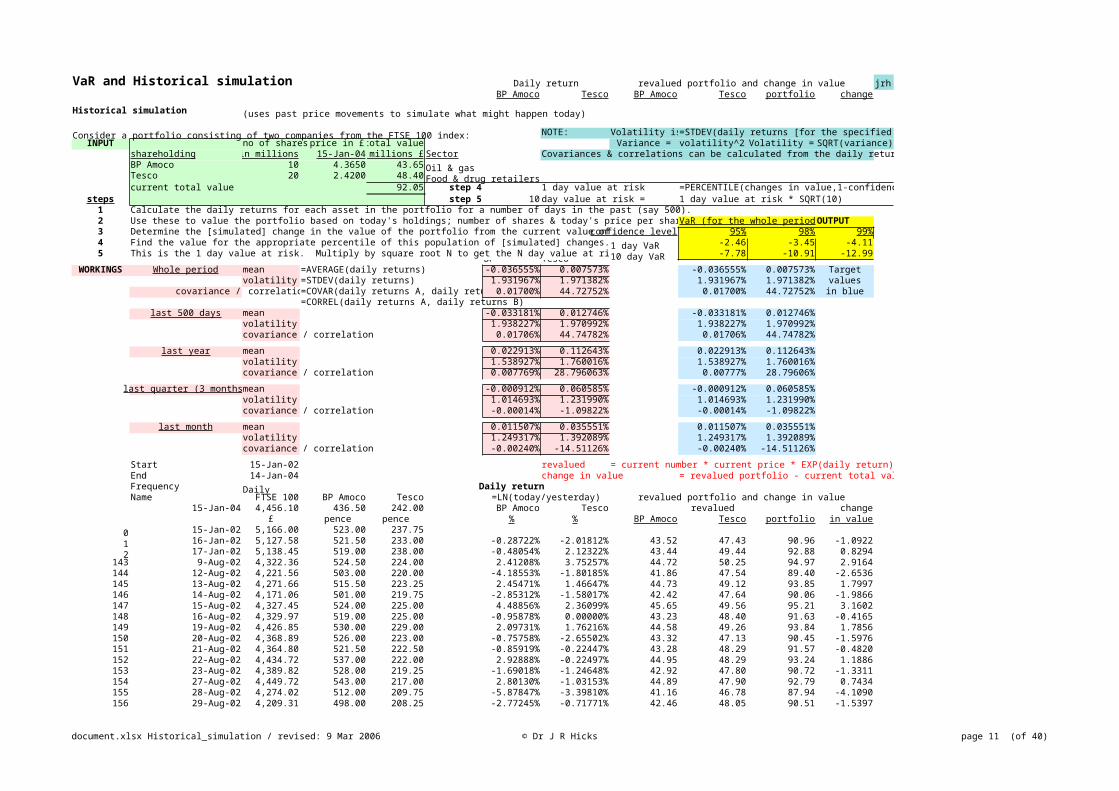

143 9-Aug-02 4,322.36 524.50 224.00 2.41208% 3.75257% 44.72 50.25 94.97 2.9164144 12-Aug-02 4,221.56 503.00 220.00 -4.18553% -1.80185% 41.86 47.54 89.40 -2.6536145 13-Aug-02 4,271.66 515.50 223.25 2.45471% 1.46647% 44.73 49.12 93.85 1.7997146 14-Aug-02 4,171.06 501.00 219.75 -2.85312% -1.58017% 42.42 47.64 90.06 -1.9866147 15-Aug-02 4,327.45 524.00 225.00 4.48856% 2.36099% 45.65 49.56 95.21 3.1602148 16-Aug-02 4,329.97 519.00 225.00 -0.95878% 0.00000% 43.23 48.40 91.63 -0.4165149 19-Aug-02 4,426.85 530.00 229.00 2.09731% 1.76216% 44.58 49.26 93.84 1.7856150 20-Aug-02 4,368.89 526.00 223.00 -0.75758% -2.65502% 43.32 47.13 90.45 -1.5976151 21-Aug-02 4,364.80 521.50 222.50 -0.85919% -0.22447% 43.28 48.29 91.57 -0.4820152 22-Aug-02 4,434.72 537.00 222.00 2.92888% -0.22497% 44.95 48.29 93.24 1.1886153 23-Aug-02 4,389.82 528.00 219.25 -1.69018% -1.24648% 42.92 47.80 90.72 -1.3311154 27-Aug-02 4,449.72 543.00 217.00 2.80130% -1.03153% 44.89 47.90 92.79 0.7434155 28-Aug-02 4,274.02 512.00 209.75 -5.87847% -3.39810% 41.16 46.78 87.94 -4.1090156 29-Aug-02 4,209.31 498.00 208.25 -2.77245% -0.71771% 42.46 48.05 90.51 -1.5397

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 12 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

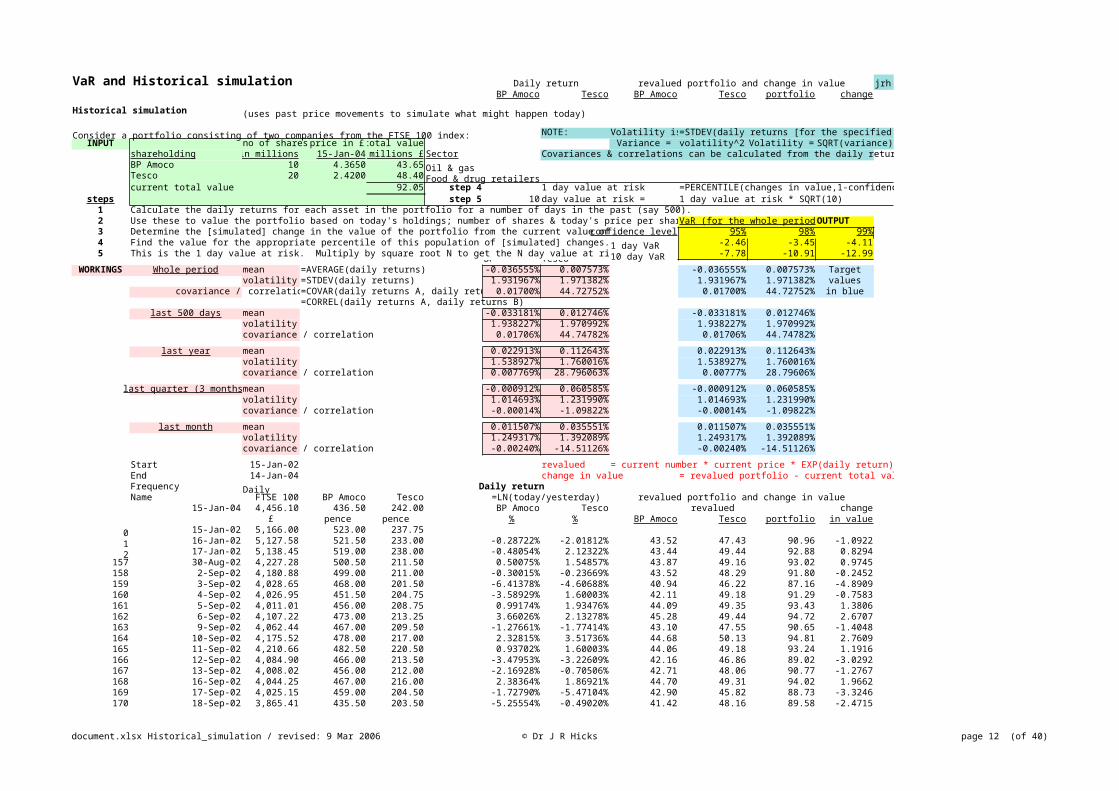

157 30-Aug-02 4,227.28 500.50 211.50 0.50075% 1.54857% 43.87 49.16 93.02 0.9745158 2-Sep-02 4,180.88 499.00 211.00 -0.30015% -0.23669% 43.52 48.29 91.80 -0.2452159 3-Sep-02 4,028.65 468.00 201.50 -6.41378% -4.60688% 40.94 46.22 87.16 -4.8909160 4-Sep-02 4,026.95 451.50 204.75 -3.58929% 1.60003% 42.11 49.18 91.29 -0.7583161 5-Sep-02 4,011.01 456.00 208.75 0.99174% 1.93476% 44.09 49.35 93.43 1.3806162 6-Sep-02 4,107.22 473.00 213.25 3.66026% 2.13278% 45.28 49.44 94.72 2.6707163 9-Sep-02 4,062.44 467.00 209.50 -1.27661% -1.77414% 43.10 47.55 90.65 -1.4048164 10-Sep-02 4,175.52 478.00 217.00 2.32815% 3.51736% 44.68 50.13 94.81 2.7609165 11-Sep-02 4,210.66 482.50 220.50 0.93702% 1.60003% 44.06 49.18 93.24 1.1916166 12-Sep-02 4,084.90 466.00 213.50 -3.47953% -3.22609% 42.16 46.86 89.02 -3.0292167 13-Sep-02 4,008.02 456.00 212.00 -2.16928% -0.70506% 42.71 48.06 90.77 -1.2767168 16-Sep-02 4,044.25 467.00 216.00 2.38364% 1.86921% 44.70 49.31 94.02 1.9662169 17-Sep-02 4,025.15 459.00 204.50 -1.72790% -5.47104% 42.90 45.82 88.73 -3.3246170 18-Sep-02 3,865.41 435.50 203.50 -5.25554% -0.49020% 41.42 48.16 89.58 -2.4715

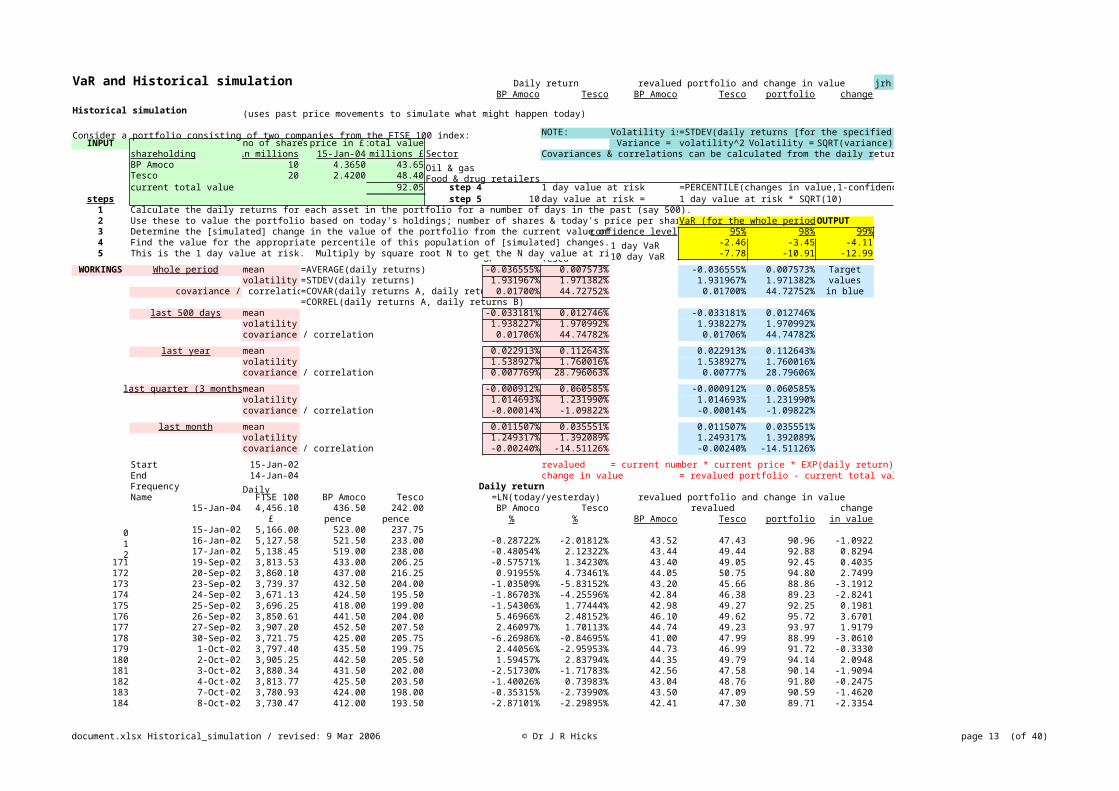

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 13 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

171 19-Sep-02 3,813.53 433.00 206.25 -0.57571% 1.34230% 43.40 49.05 92.45 0.4035172 20-Sep-02 3,860.10 437.00 216.25 0.91955% 4.73461% 44.05 50.75 94.80 2.7499173 23-Sep-02 3,739.37 432.50 204.00 -1.03509% -5.83152% 43.20 45.66 88.86 -3.1912174 24-Sep-02 3,671.13 424.50 195.50 -1.86703% -4.25596% 42.84 46.38 89.23 -2.8241175 25-Sep-02 3,696.25 418.00 199.00 -1.54306% 1.77444% 42.98 49.27 92.25 0.1981176 26-Sep-02 3,850.61 441.50 204.00 5.46966% 2.48152% 46.10 49.62 95.72 3.6701177 27-Sep-02 3,907.20 452.50 207.50 2.46097% 1.70113% 44.74 49.23 93.97 1.9179178 30-Sep-02 3,721.75 425.00 205.75 -6.26986% -0.84695% 41.00 47.99 88.99 -3.0610179 1-Oct-02 3,797.40 435.50 199.75 2.44056% -2.95953% 44.73 46.99 91.72 -0.3330180 2-Oct-02 3,905.25 442.50 205.50 1.59457% 2.83794% 44.35 49.79 94.14 2.0948181 3-Oct-02 3,880.34 431.50 202.00 -2.51730% -1.71783% 42.56 47.58 90.14 -1.9094182 4-Oct-02 3,813.77 425.50 203.50 -1.40026% 0.73983% 43.04 48.76 91.80 -0.2475183 7-Oct-02 3,780.93 424.00 198.00 -0.35315% -2.73990% 43.50 47.09 90.59 -1.4620184 8-Oct-02 3,730.47 412.00 193.50 -2.87101% -2.29895% 42.41 47.30 89.71 -2.3354

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 14 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

185 9-Oct-02 3,742.40 407.00 193.00 -1.22102% -0.25873% 43.12 48.27 91.40 -0.6548186 10-Oct-02 3,777.28 412.00 194.25 1.22102% 0.64558% 44.19 48.71 92.90 0.8497187 11-Oct-02 3,953.38 427.50 207.00 3.69309% 6.35728% 45.29 51.58 96.87 4.8190188 14-Oct-02 3,931.64 423.00 199.00 -1.05821% -3.94140% 43.19 46.53 89.72 -2.3300189 15-Oct-02 4,130.33 448.00 206.00 5.74211% 3.45713% 46.23 50.10 96.33 4.2823190 16-Oct-02 4,057.71 445.00 204.25 -0.67190% -0.85314% 43.36 47.99 91.35 -0.7035191 17-Oct-02 4,170.68 456.00 205.50 2.44185% 0.61013% 44.73 48.70 93.43 1.3752192 18-Oct-02 4,130.54 458.50 199.75 0.54675% -2.83794% 43.89 47.05 90.94 -1.1149193 21-Oct-02 4,133.77 452.00 200.00 -1.42781% 0.12508% 43.03 48.46 91.49 -0.5582194 22-Oct-02 4,118.88 427.50 202.25 -5.57279% 1.11872% 41.28 48.94 90.23 -1.8215195 23-Oct-02 4,006.91 420.00 200.00 -1.76996% -1.11872% 42.88 47.86 90.75 -1.3042196 24-Oct-02 4,103.69 434.00 207.00 3.27898% 3.44014% 45.11 50.09 95.20 3.1490197 25-Oct-02 4,051.09 426.50 204.50 -1.74322% -1.21508% 42.90 47.82 90.71 -1.3389198 28-Oct-02 4,090.46 423.00 205.25 -0.82402% 0.36608% 43.29 48.58 91.87 -0.1807

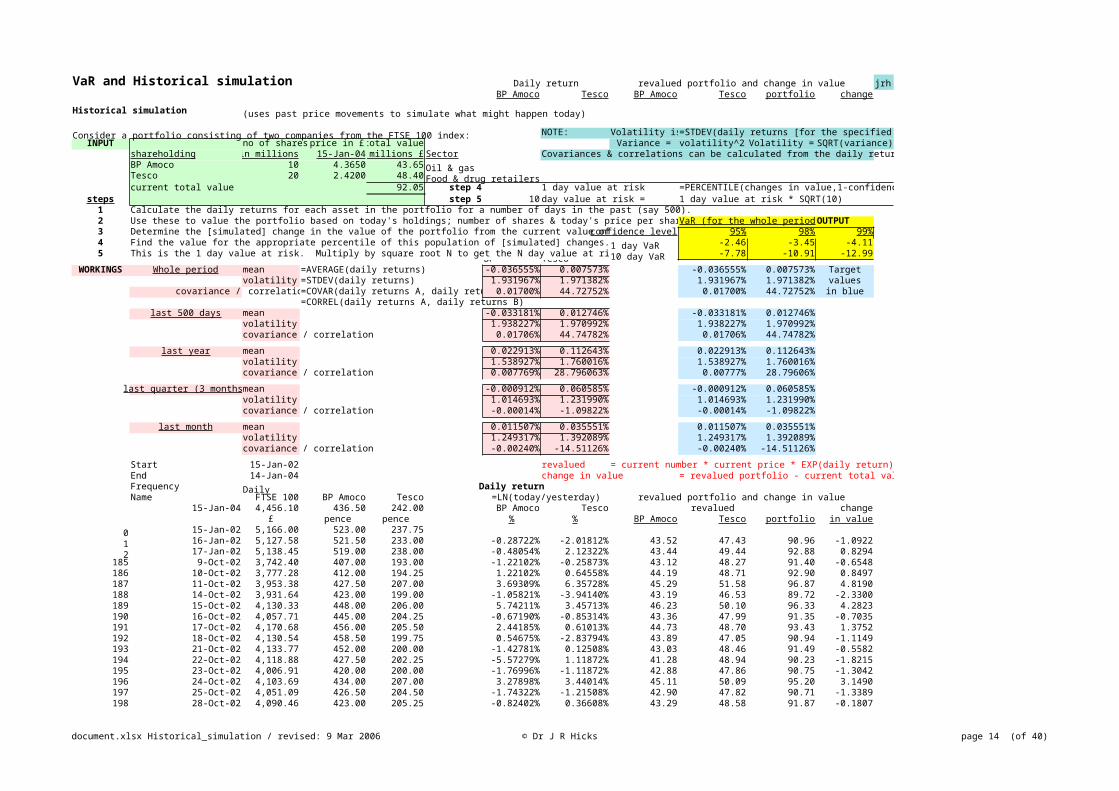

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 15 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

199 29-Oct-02 3,935.93 392.50 203.00 -7.48356% -1.10228% 40.50 47.87 88.37 -3.6779200 30-Oct-02 4,002.65 404.00 197.25 2.88783% -2.87340% 44.93 47.03 91.96 -0.0920201 31-Oct-02 4,039.66 410.00 198.25 1.47423% 0.50569% 44.30 48.65 92.94 0.8936202 1-Nov-02 3,996.98 418.00 197.00 1.93243% -0.63251% 44.50 48.09 92.60 0.5465203 4-Nov-02 4,141.46 411.50 203.50 -1.56724% 3.24623% 42.97 50.00 92.97 0.9182204 5-Nov-02 4,146.13 406.50 204.50 -1.22251% 0.49020% 43.12 48.64 91.76 -0.2925205 6-Nov-02 4,103.72 399.50 208.50 -1.73702% 1.93711% 42.90 49.35 92.25 0.1950206 7-Nov-02 4,081.26 396.50 204.75 -0.75377% -1.81493% 43.32 47.53 90.85 -1.1983207 8-Nov-02 4,034.58 403.00 201.00 1.62605% -1.84848% 44.37 47.51 91.88 -0.1709208 11-Nov-02 4,015.58 405.50 203.50 0.61843% 1.23611% 43.92 49.00 92.92 0.8728209 12-Nov-02 4,085.05 408.50 204.00 0.73710% 0.24540% 43.97 48.52 92.49 0.4419210 13-Nov-02 4,029.38 403.00 198.25 -1.35554% -2.85911% 43.06 47.04 90.10 -1.9519211 14-Nov-02 4,053.14 402.50 199.00 -0.12415% 0.37760% 43.60 48.58 92.18 0.1289212 15-Nov-02 4,091.62 410.00 200.50 1.84621% 0.75094% 44.46 48.76 93.23 1.1782

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 16 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

213 18-Nov-02 4,115.99 413.50 200.00 0.85004% -0.24969% 44.02 48.28 92.30 0.2519214 19-Nov-02 4,096.51 418.50 200.50 1.20194% 0.24969% 44.18 48.52 92.70 0.6488215 20-Nov-02 4,094.86 407.00 200.25 -2.78637% -0.12477% 42.45 48.34 90.79 -1.2598216 21-Nov-02 4,190.00 412.00 201.75 1.22102% 0.74627% 44.19 48.76 92.95 0.8988217 22-Nov-02 4,175.23 404.00 196.00 -1.96085% -2.89146% 42.80 47.02 89.82 -2.2270218 25-Nov-02 4,122.21 402.50 194.50 -0.37198% -0.76825% 43.49 48.03 91.52 -0.5325219 26-Nov-02 4,070.96 400.00 194.50 -0.62305% 0.00000% 43.38 48.40 91.78 -0.2711220 27-Nov-02 4,144.19 417.00 200.50 4.16217% 3.03821% 45.51 49.89 95.40 3.3482221 28-Nov-02 4,185.40 423.00 203.50 1.42860% 1.48518% 44.28 49.12 93.40 1.3522222 29-Nov-02 4,169.41 418.50 203.00 -1.06953% -0.24600% 43.19 48.28 91.47 -0.5833223 2-Dec-02 4,154.27 412.50 202.50 -1.44407% -0.24661% 43.02 48.28 91.30 -0.7450224 3-Dec-02 4,075.39 415.50 198.50 0.72464% -1.99508% 43.97 47.44 91.41 -0.6386225 4-Dec-02 4,048.60 414.00 199.75 -0.36166% 0.62775% 43.49 48.70 92.20 0.1472226 5-Dec-02 4,032.42 418.00 197.25 0.96155% -1.25946% 44.07 47.79 91.87 -0.1840

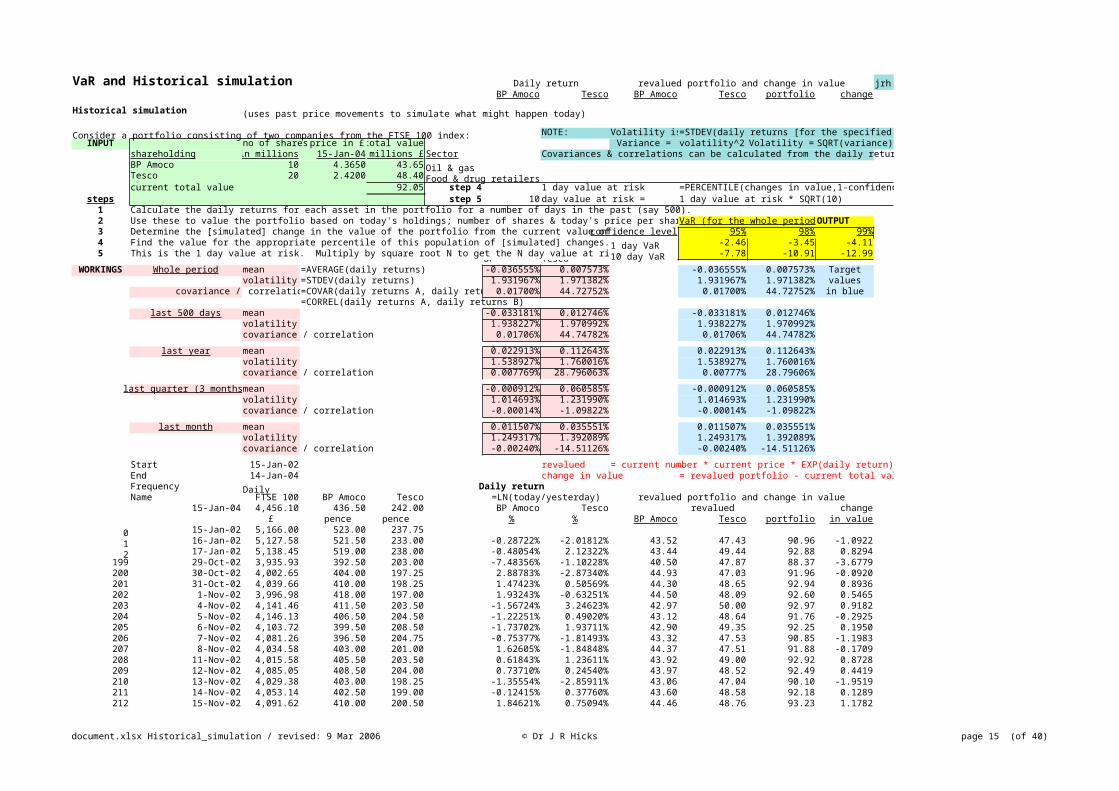

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 17 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

227 6-Dec-02 4,013.46 414.00 195.50 -0.96155% -0.89116% 43.23 47.97 91.20 -0.8471228 9-Dec-02 3,933.93 412.00 193.50 -0.48426% -1.02829% 43.44 47.90 91.34 -0.7060229 10-Dec-02 3,925.00 414.00 193.50 0.48426% 0.00000% 43.86 48.40 92.26 0.2119230 11-Dec-02 3,974.87 419.00 198.00 1.20049% 2.29895% 44.18 49.53 93.70 1.6528231 12-Dec-02 3,935.31 414.00 196.00 -1.20049% -1.01524% 43.13 47.91 91.04 -1.0098232 13-Dec-02 3,878.07 410.50 193.25 -0.84900% -1.41300% 43.28 47.72 91.00 -1.0481233 16-Dec-02 3,983.97 426.00 197.25 3.70634% 2.04873% 45.30 49.40 94.70 2.6500234 17-Dec-02 3,908.71 421.00 190.75 -1.18065% -3.35083% 43.14 46.81 89.94 -2.1073235 18-Dec-02 3,835.18 413.00 187.50 -1.91852% -1.71848% 42.82 47.58 90.40 -1.6541236 19-Dec-02 3,841.41 413.00 188.00 0.00000% 0.26631% 43.65 48.53 92.18 0.1291237 20-Dec-02 3,889.86 416.50 189.25 0.84389% 0.66269% 44.02 48.72 92.74 0.6917238 23-Dec-02 3,936.87 426.00 190.50 2.25529% 0.65833% 44.65 48.72 93.37 1.3153239 24-Dec-02 3,942.10 429.00 190.25 0.70176% -0.13132% 43.96 48.34 92.29 0.2439240 27-Dec-02 3,829.39 415.00 187.00 -3.31784% -1.72304% 42.23 47.57 89.80 -2.2513

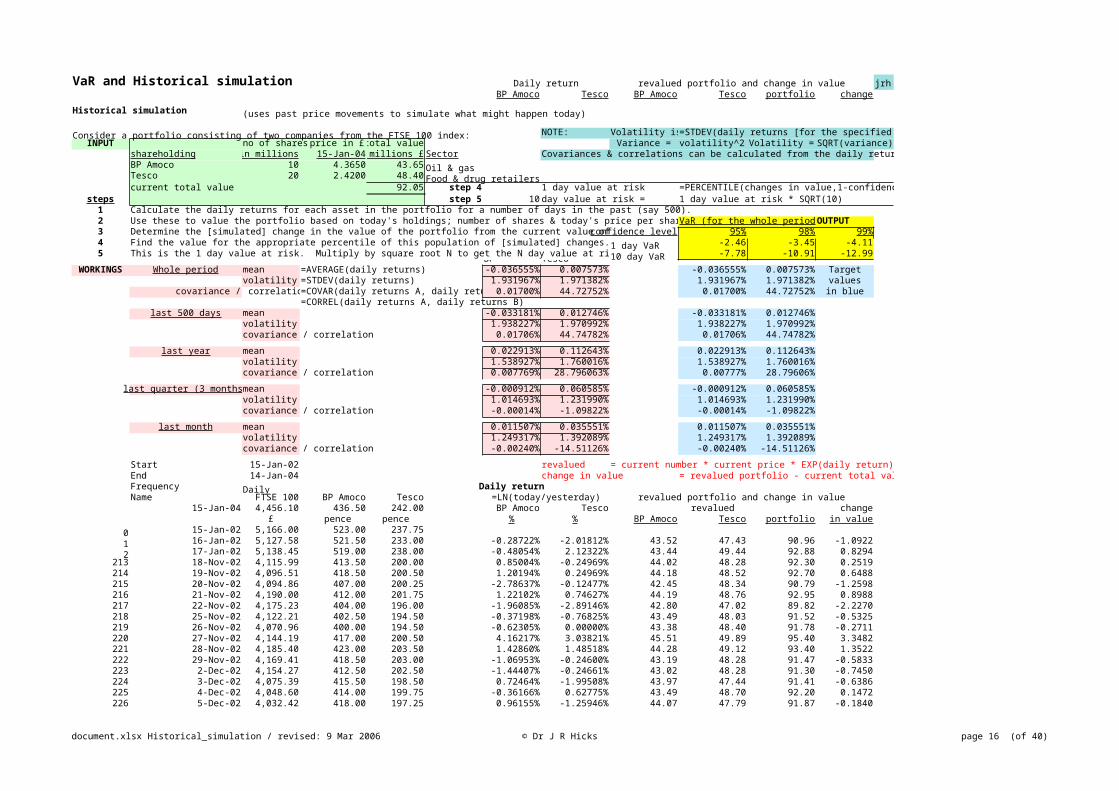

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 18 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%

last quarter (3 months)mean -0.000912% 0.060585% -0.000912% 0.060585%volatility 1.014693% 1.231990% 1.014693% 1.231990%covariance / correlation -0.00014% -1.09822% -0.00014% -1.09822%

last month mean 0.011507% 0.035551% 0.011507% 0.035551%volatility 1.249317% 1.392089% 1.249317% 1.392089%covariance / correlation -0.00240% -14.51126% -0.00240% -14.51126%

Start 15-Jan-02 revalued = current number * current price * EXP(daily return)End 14-Jan-04 change in value = revalued portfolio - current total valueFrequency Daily Daily returnName FTSE 100 BP Amoco Tesco =LN(today/yesterday) revalued portfolio and change in value

15-Jan-04 4,456.10 436.50 242.00 BP Amoco Tesco revalued change£ pence pence % % BP Amoco Tesco portfolio in value

0 15-Jan-02 5,166.00 523.00 237.751 16-Jan-02 5,127.58 521.50 233.00 -0.28722% -2.01812% 43.52 47.43 90.96 -1.09222 17-Jan-02 5,138.45 519.00 238.00 -0.48054% 2.12322% 43.44 49.44 92.88 0.8294

241 30-Dec-02 3,900.62 424.00 193.25 2.14549% 3.28761% 44.60 50.02 94.61 2.5643242 31-Dec-02 3,940.36 427.00 194.00 0.70506% 0.38735% 43.96 48.59 92.55 0.4967243 2-Jan-03 4,009.46 428.00 195.75 0.23392% 0.89802% 43.75 48.84 92.59 0.5388244 3-Jan-03 4,004.95 427.00 192.50 -0.23392% -1.67422% 43.55 47.60 91.14 -0.9056245 6-Jan-03 4,001.37 429.00 196.50 0.46729% 2.05663% 43.85 49.41 93.26 1.2102246 7-Jan-03 3,957.39 424.00 198.75 -1.17235% 1.13853% 43.14 48.95 92.10 0.0455247 8-Jan-03 3,924.82 418.50 201.00 -1.30566% 1.12572% 43.08 48.95 92.03 -0.0183248 9-Jan-03 3,933.98 420.25 192.75 0.41729% -4.19109% 43.83 46.41 90.25 -1.8040249 10-Jan-03 3,974.12 424.00 186.75 0.88837% -3.16232% 44.04 46.89 90.93 -1.1171250 13-Jan-03 3,948.27 416.00 183.00 -1.90482% -2.02847% 42.83 47.43 90.25 -1.7955251 14-Jan-03 3,945.59 410.50 185.75 -1.33093% 1.49155% 43.07 49.13 92.20 0.1502252 15-Jan-03 3,887.75 405.75 182.00 -1.16387% -2.03950% 43.14 47.42 90.57 -1.4822253 16-Jan-03 3,881.81 408.75 183.00 0.73665% 0.54795% 43.97 48.67 92.64 0.5887254 17-Jan-03 3,820.57 403.50 183.50 -1.29272% 0.27285% 43.09 48.53 91.62 -0.4284

document.xlsx Historical_simulation / revised: 9 Mar 2006 © Dr J R Hicks page 19 (of 40)

VaR and Historical simulation Daily return revalued portfolio and change in value jrhBP Amoco Tesco BP Amoco Tesco portfolio change

Historical simulation (uses past price movements to simulate what might happen today)

Consider a portfolio consisting of two companies from the FTSE 100 index: NOTE: Volatility is=STDEV(daily returns [for the specified period])INPUT no of shares price in £ total value Variance = volatility^2 Volatility = SQRT(variance)

shareholding in millions 15-Jan-04 millions £ Sector Covariances & correlations can be calculated from the daily returns.BP Amoco 10 4.3650 43.65 Oil & gasTesco 20 2.4200 48.40 Food & drug retailerscurrent total value 92.05 step 4 1 day value at risk =PERCENTILE(changes in value,1-confidence level)

steps step 5 10 day value at risk = 1 day value at risk * SQRT(10)1 Calculate the daily returns for each asset in the portfolio for a number of days in the past (say 500).2 Use these to value the portfolio based on today's holdings; number of shares & today's price per sharVaR (for the whole periodOUTPUT3 Determine the [simulated] change in the value of the portfolio from the current value ofconfidence level 95% 98% 99%4 Find the value for the appropriate percentile of this population of [simulated] changes.1 day VaR -2.46 -3.45 -4.115 This is the 1 day value at risk. Multiply by square root N to get the N day value at ri10 day VaR -7.78 -10.91 -12.99BP Tesco

WORKINGS Whole period mean =AVERAGE(daily returns) -0.036555% 0.007573% -0.036555% 0.007573% Targetvolatility =STDEV(daily returns) 1.931967% 1.971382% 1.931967% 1.971382% values

covariance / correlatio=COVAR(daily returns A, daily retu 0.01700% 44.72752% 0.01700% 44.72752% in blue=CORREL(daily returns A, daily returns B)

last 500 days mean -0.033181% 0.012746% -0.033181% 0.012746%volatility 1.938227% 1.970992% 1.938227% 1.970992%covariance / correlation 0.01706% 44.74782% 0.01706% 44.74782%

last year mean 0.022913% 0.112643% 0.022913% 0.112643%volatility 1.538927% 1.760016% 1.538927% 1.760016%covariance / correlation 0.007769% 28.796063% 0.00777% 28.79606%