Embed Size (px)

Citation preview

CONFIDENTIAL

Investor Presentation

Note: All $ in AUD unless otherwise stated and all financial data presented is as at the date of this presentation unless otherwise stated. The images in this presentation are not assets of US Residential Fund (USR) and have been inserted for explanatory purposes.

CONFIDENTIAL

US Residential Fund

Slide 2

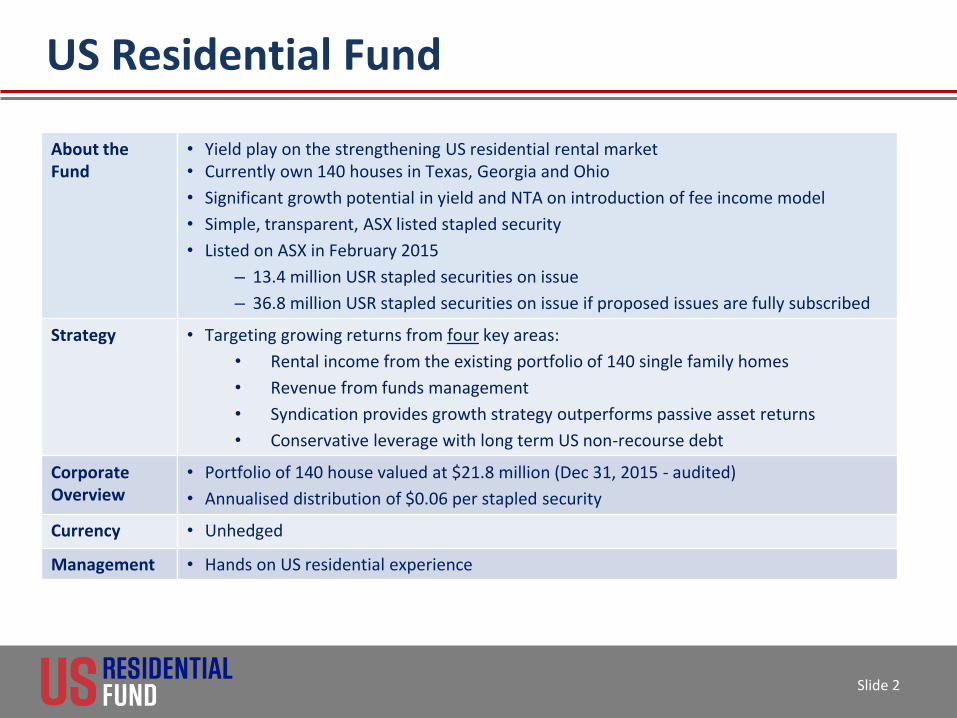

About the Fund

• Yield play on the strengthening US residential rental market • Currently own 140 houses in Texas, Georgia and Ohio

• Significant growth potential in yield and NTA on introduction of fee income model

• Simple, transparent, ASX listed stapled security

• Listed on ASX in February 2015

– 13.4 million USR stapled securities on issue

– 36.8 million USR stapled securities on issue if proposed issues are fully subscribed

Strategy • Targeting growing returns from four key areas:

• Rental income from the existing portfolio of 140 single family homes

• Revenue from funds management

• Syndication provides growth strategy outperforms passive asset returns

• Conservative leverage with long term US non-recourse debt

Corporate Overview

• Portfolio of 140 house valued at $21.8 million (Dec 31, 2015 - audited)

• Annualised distribution of $0.06 per stapled security

Currency • Unhedged

Management • Hands on US residential experience

CONFIDENTIAL

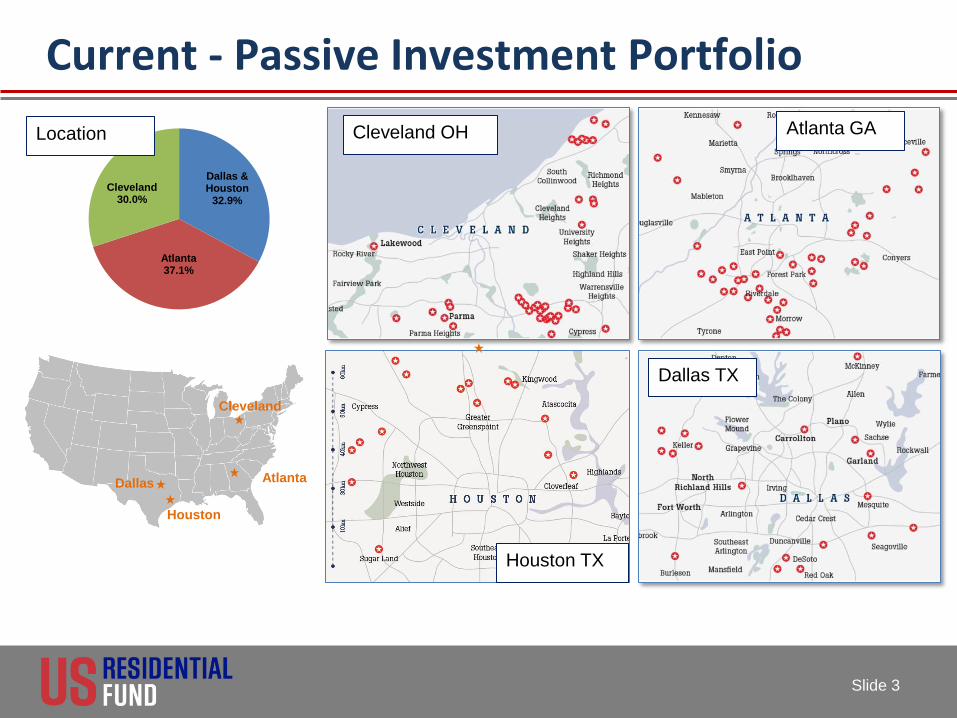

Current - Passive Investment Portfolio

Cleveland OH Atlanta GA

Houston TX

Dallas TX

Slide 3

Dallas & Houston

32.9%

Atlanta 37.1%

Cleveland30.0%

Location

Houston

Dallas

Cleveland

Atlanta

CONFIDENTIAL

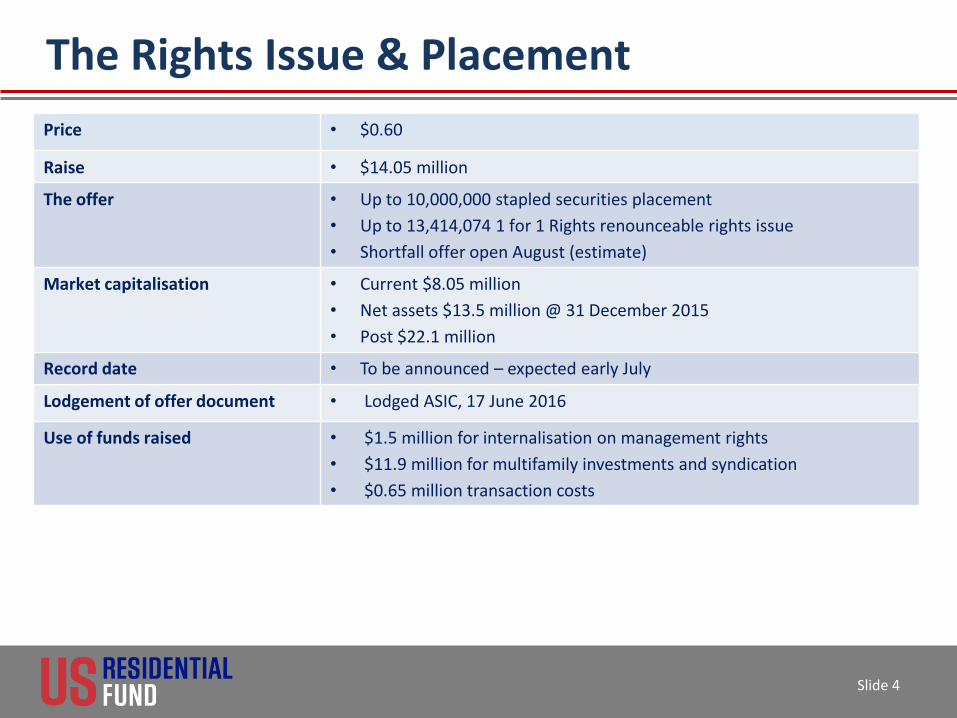

The Rights Issue & Placement

Slide 4

Price • $0.60

Raise • $14.05 million

The offer • Up to 10,000,000 stapled securities placement

• Up to 13,414,074 1 for 1 Rights renounceable rights issue

• Shortfall offer open August (estimate)

Market capitalisation • Current $8.05 million

• Net assets $13.5 million @ 31 December 2015

• Post $22.1 million

Record date • To be announced – expected early July

Lodgement of offer document • Lodged ASIC, 17 June 2016

Use of funds raised • $1.5 million for internalisation on management rights

• $11.9 million for multifamily investments and syndication

• $0.65 million transaction costs

CONFIDENTIAL

US Economy

Gross Domestic Product

• 2.4% - 31 December 2015 • 2.34% p.a. - 1996 to 2015 (31 December) • 3% p.a. – 1930 to 2015 (31 December)

US economy counter cyclical to resource depended economies

Rental Markets

Dallas - Fort Worth • Jobs growing at 4%p.a growth, rent growth 6%+p.a.

Houston • Jobs growth has slowed, unemployment up, rent growth 2.5%+p.a

Atlanta • Jobs growing at 2.3%p.a unemployment down, rent growth 7.1%+p.a

Cleveland • Jobs growing at 1%p.a unemployment below US Average down, rent growth 2.73%+p.a

Slide 5

CONFIDENTIAL

Fund Performance

Slide 6

0.85

0.9

0.95

1

1.05

1.1

Pre IPO 10/2/2015 30/6/2015 31/2/2015

NTA Distrubution CPU

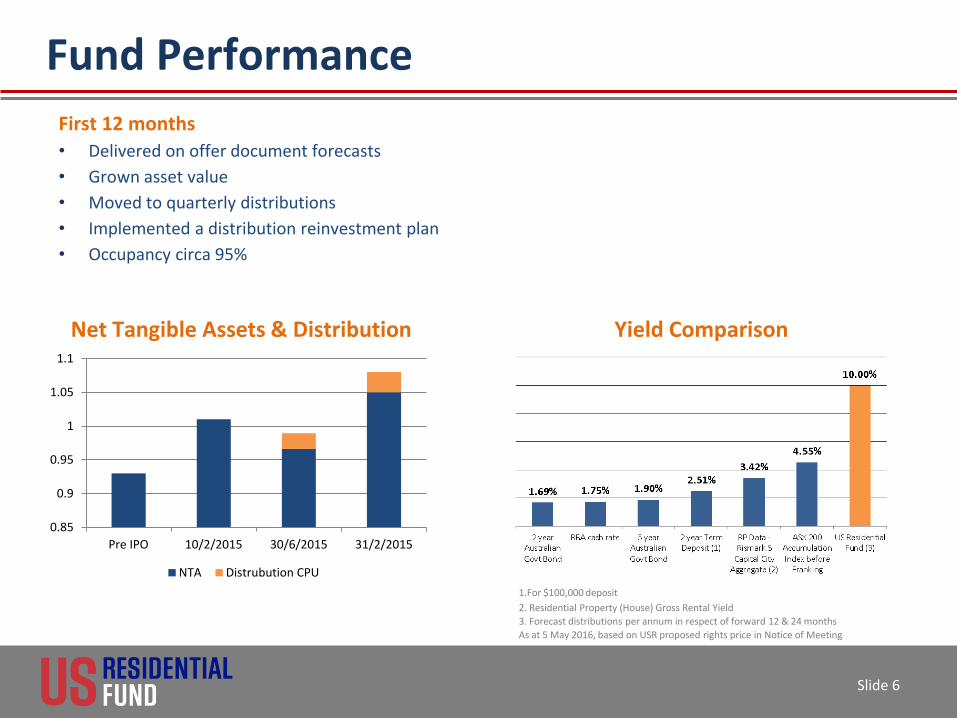

First 12 months • Delivered on offer document forecasts

• Grown asset value

• Moved to quarterly distributions

• Implemented a distribution reinvestment plan

• Occupancy circa 95%

Net Tangible Assets & Distribution Yield Comparison

1.For $100,000 deposit

2. Residential Property (House) Gross Rental Yield

3. Forecast distributions per annum in respect of forward 12 & 24 months

As at 5 May 2016, based on USR proposed rights price in Notice of Meeting

CONFIDENTIAL

Future Strategy

Grow earnings and distributions through:

• Increasing the scale of individual assets while maintaining tenant diversification • Increase the Fund’s growth profile by more efficiently using capital

• Acquire multifamily residential apartment complexes • Syndicate those assets to third party investors

• Generate greater income that passive buy and hold • Recycling of capital • Reduce capital requirements

• Internalisation of management rights;

• Enables USR to add fee income to property income • Earnings enhancing • No fee leakages • Simplifies operational structure • Acquire intellectual property including syndication model

• Improving asset management efficiency

Slide 7

CONFIDENTIAL

Why the rights issue and placement?

To grow earnings and distributions through:

• Increase balance sheet • bring asset on balance sheet – co-investment and syndication • take advantage of the demand for investment in apartment complexes • USD 680 million in property syndicated using electronic platforms in 2015

• Increase cashflow over passive buy and hold – through syndication

• Syndication increases fee income – approx 27% more cash to Fund in year one • Efficient use of capital to seed multifamily syndicates

• Broadening the Fund’s exposure to the US residential market

• Acquisition of management rights to:

• eliminate fee leakage • increase efficiencies through vertical integration

• Funds management income from syndication to:

• generate fee income • create non dilutive annuity income

Slide 8

CONFIDENTIAL

Multifamily residential apartments

Multifamily Residential Apartment Complexes

• Apartments purposely built for rental • One title • Commercial property asset class • Graded A to D • On-site management • Often include a resort style clubhouse, a pool and gym • Landscaped grounds

Our focus

• 240+ apartments • On-site management and maintenance • A grade regional • B grade with value add opportunity • 14 key growth markets targeted • Price range US$15 to US$30 million • Gross rental yields approximately 14%

Slide 9

CONFIDENTIAL

Examples – High Rise & Garden

Vertical – High and Mid Rise

Video Watermarke LA

Garden Style

Video Timber Oaks

• Premium - A Grade

• 35 floor – 300 Apartments

• US $160 million

• Los Angeles, California

• Located near Staples Center & LA Live, downtown

• Tenants include:

▪ Disney Center staff, US Bank pilots, Entertainers (Demi Lavarto), America’s top model films there, (Penthouses vacant for filming), PWC

• 1 bedroom US$3,088 per month

Slide 10

• A Grade • 180 Apartments • US $18.8 million • Midlothian, Texas (40 Km from Dallas) • Hub of the cement industry in N.Texas • Tenants include:

Educators, Holcim Cement employees, Hospital staff, National Power employees

• 1 bedroom US$785 to 960 per month

CONFIDENTIAL

Multifamily Market Overview

Slide 11

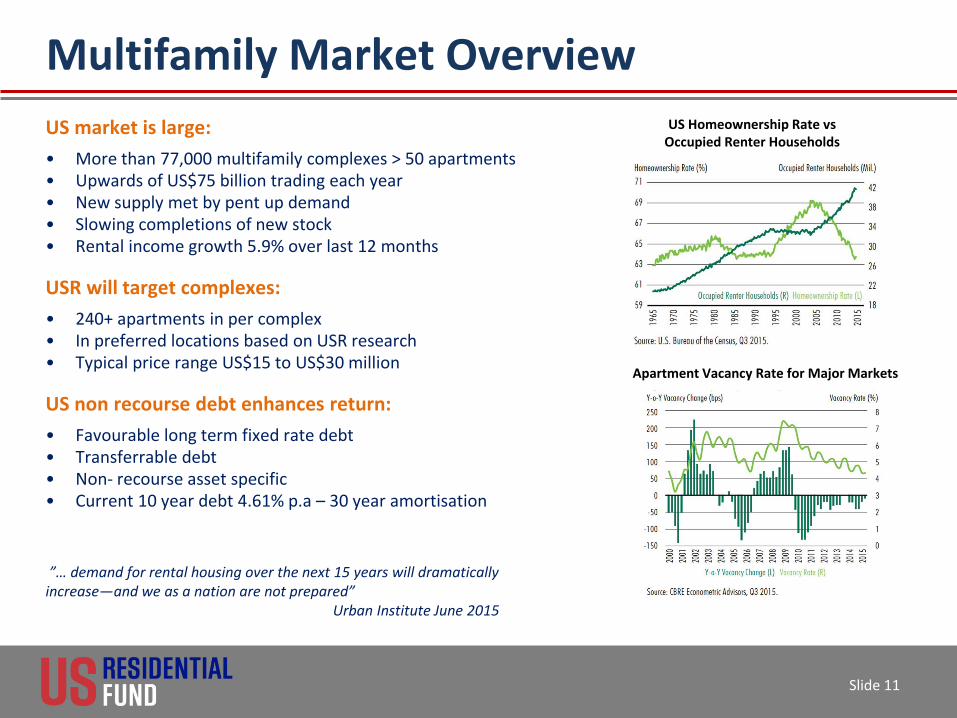

US market is large:

• More than 77,000 multifamily complexes > 50 apartments • Upwards of US$75 billion trading each year • New supply met by pent up demand • Slowing completions of new stock • Rental income growth 5.9% over last 12 months USR will target complexes:

• 240+ apartments in per complex • In preferred locations based on USR research • Typical price range US$15 to US$30 million US non recourse debt enhances return:

• Favourable long term fixed rate debt • Transferrable debt • Non- recourse asset specific • Current 10 year debt 4.61% p.a – 30 year amortisation

”… demand for rental housing over the next 15 years will dramatically increase—and we as a nation are not prepared” Urban Institute June 2015

US Homeownership Rate vs Occupied Renter Households

Apartment Vacancy Rate for Major Markets

CONFIDENTIAL

Syndication Opportunity

Growing investor demand:

• Low interest rate environment, volatile capital markets • Demand for hard assets • Demand from non US investors for US real estate; • Demand for investment in US multifamily properties • Through unlisted single property syndicates that provide:

• Yield • Capital growth over the medium term

• Growing access to investment through online platforms • Online raised US$ 680m last year • Online augmenting traditional distribution channels

Slide 12

More information US electronic distribution platforms

CONFIDENTIAL

USR Uniquely Positioned to Execute

Strong Balance Sheet

• Key to securing properties for syndication Established Partnerships

• Multifamily sourcing avenues established • Strong US legal and banking relationships • Access to established real estate crowd funding platforms Operating structures and licenses

• Offices located in Dallas and Melbourne • Acquisition agreements in place to internalise asset and property management • Syndication framework and vertically integrated financial model established • USR holds an Australian Financial Services Licence Expertise

• Management team with over 100 years of real estate syndication experience including implementation of cross border structures

• Board and senior executive expertise in underwriting of over $1 billion property acquisitions • Executive team in place with significant multifamily and single family property management and operating

experience

Slide 13

CONFIDENTIAL

Target Markets

Slide 14

Areas considered for investment

• In addition to Texas and

Florida; Atlanta, Charlotte, Nashville, Phoenix, Las Vegas, and Oklahoma City are also among locations under review.

• Consideration of both the operational footprint and underwriting support requirements will be taken into account.

Multifamily Markets Under Consideration

CONFIDENTIAL

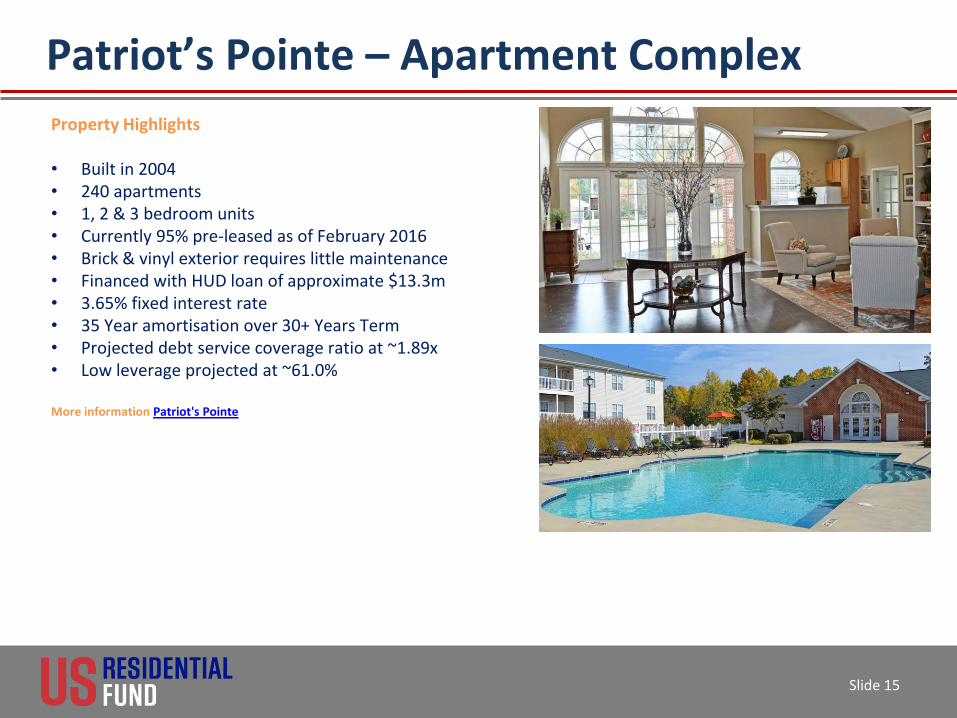

Patriot’s Pointe – Apartment Complex

Slide 15

Property Highlights • Built in 2004 • 240 apartments • 1, 2 & 3 bedroom units • Currently 95% pre-leased as of February 2016 • Brick & vinyl exterior requires little maintenance • Financed with HUD loan of approximate $13.3m • 3.65% fixed interest rate • 35 Year amortisation over 30+ Years Term • Projected debt service coverage ratio at ~1.89x • Low leverage projected at ~61.0%

More information Patriot's Pointe

CONFIDENTIAL

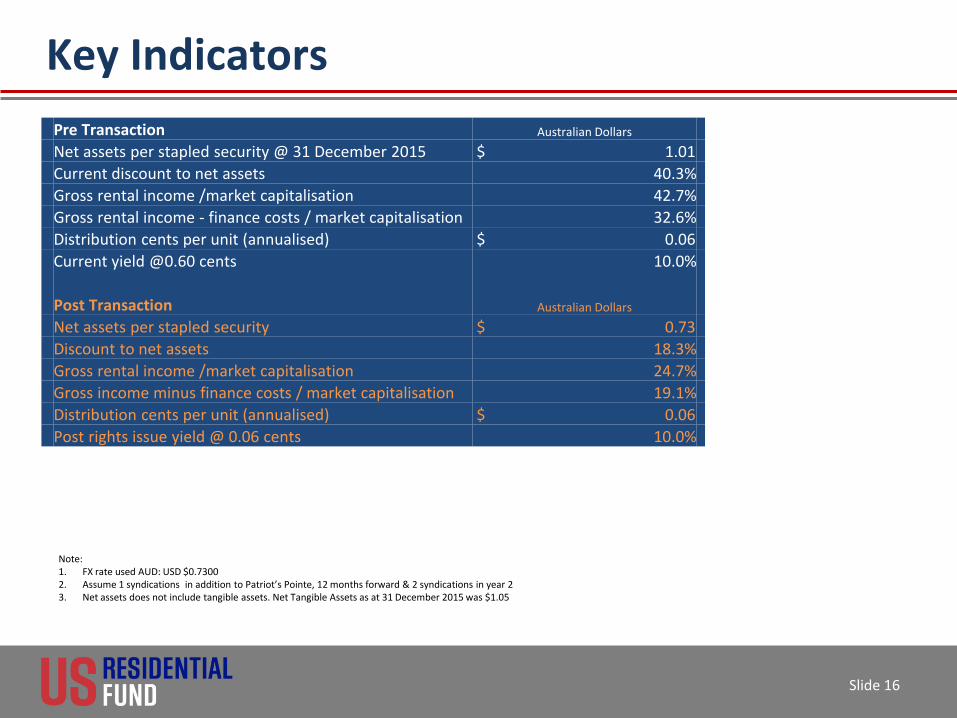

Key Indicators

Slide 16

Note: 1. FX rate used AUD: USD $0.7300 2. Assume 1 syndications in addition to Patriot’s Pointe, 12 months forward & 2 syndications in year 2 3. Net assets does not include tangible assets. Net Tangible Assets as at 31 December 2015 was $1.05

Pre Transaction Australian Dollars

Net assets per stapled security @ 31 December 2015 $ 1.01

Current discount to net assets 40.3%

Gross rental income /market capitalisation 42.7%

Gross rental income - finance costs / market capitalisation 32.6%

Distribution cents per unit (annualised) $ 0.06

Current yield @0.60 cents 10.0%

Post Transaction Australian Dollars

Net assets per stapled security $ 0.73

Discount to net assets 18.3%

Gross rental income /market capitalisation 24.7%

Gross income minus finance costs / market capitalisation 19.1%

Distribution cents per unit (annualised) $ 0.06

Post rights issue yield @ 0.06 cents 10.0%

CONFIDENTIAL

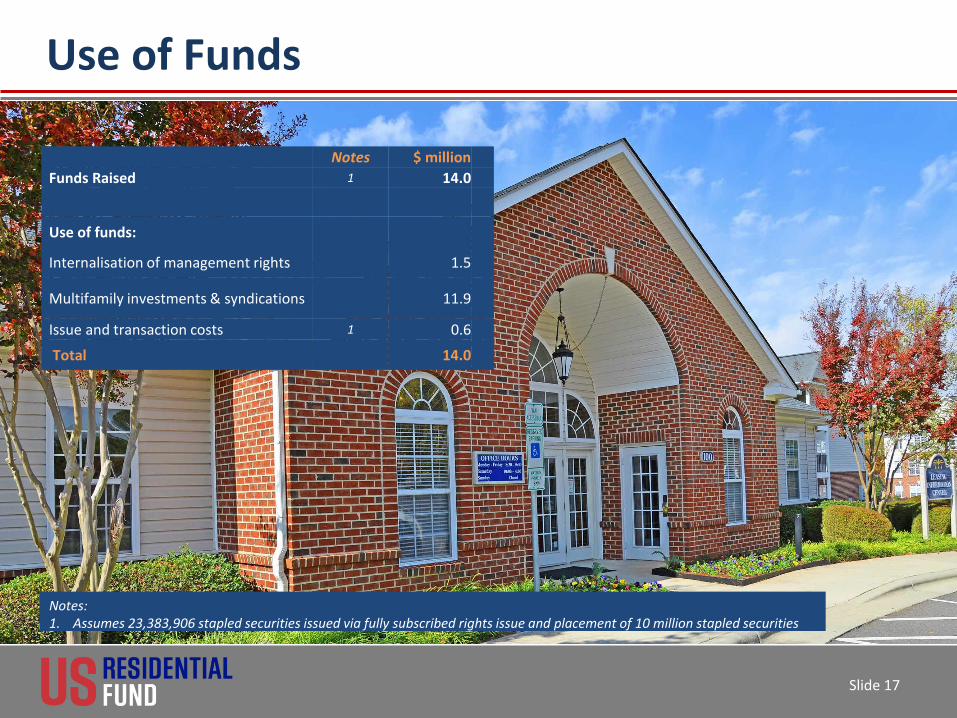

Use of Funds

Slide 17

Notes: 1. Assumes 23,383,906 stapled securities issued via fully subscribed rights issue and placement of 10 million stapled securities

Notes $ million

Funds Raised 1 14.0

Use of funds:

Internalisation of management rights 1.5

Multifamily investments & syndications 11.9

Issue and transaction costs 1 0.6

Total 14.0

CONFIDENTIAL

3.18% 3.55%

4.48% 4.56% 4.64% 4.71% 5.04% 5.05%

5.57% 5.77% 6.22% 6.34%

6.65%

7.46% 7.78%

10.00%

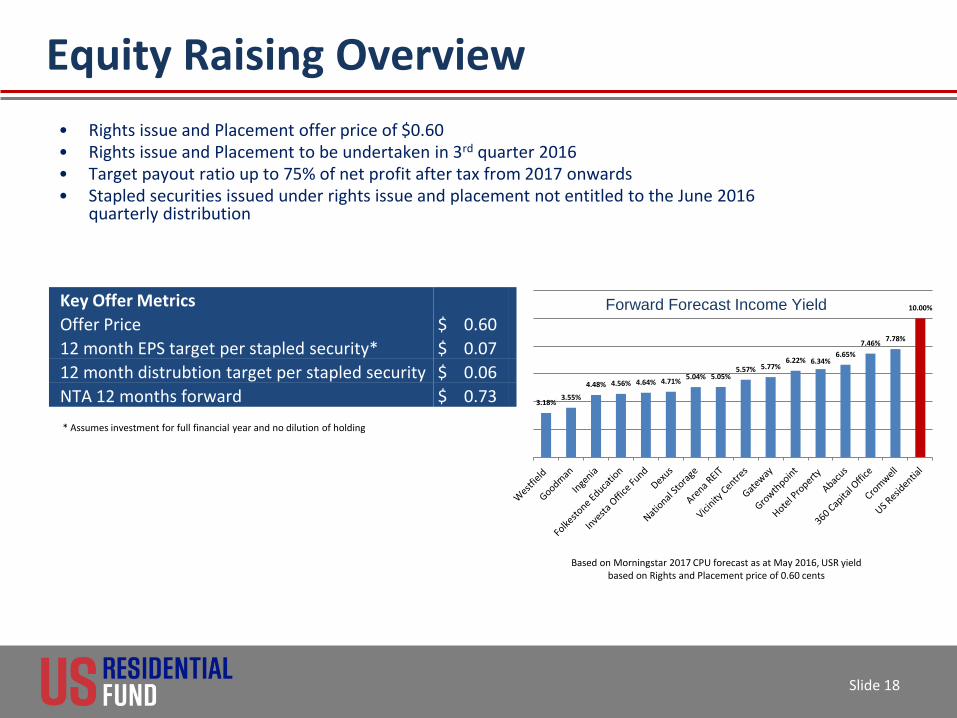

Equity Raising Overview

• Rights issue and Placement offer price of $0.60 • Rights issue and Placement to be undertaken in 3rd quarter 2016 • Target payout ratio up to 75% of net profit after tax from 2017 onwards • Stapled securities issued under rights issue and placement not entitled to the June 2016

quarterly distribution * Assumes investment for full financial year and no dilution of holding

Slide 18

Forward Forecast Income Yield

Based on Morningstar 2017 CPU forecast as at May 2016, USR yield based on Rights and Placement price of 0.60 cents

Key Offer Metrics

Offer Price $ 0.60

12 month EPS target per stapled security* $ 0.07

12 month distrubtion target per stapled security $ 0.06

NTA 12 months forward $ 0.73

CONFIDENTIAL

Slide 19

Appendices:

1. Syndication & Management Model

2. Multifamily – Why focus on it

3. US Commercial Real Estate – Strong returns

4. Target Markets

5. Example Multifamily Properties

6. Current Single Family Home Portfolio

7. Acquisition of Management Rights

8.Financial Forecasts

9.Syndication Case Study

10.Securitised Loans

11.Management Team

CONFIDENTIAL

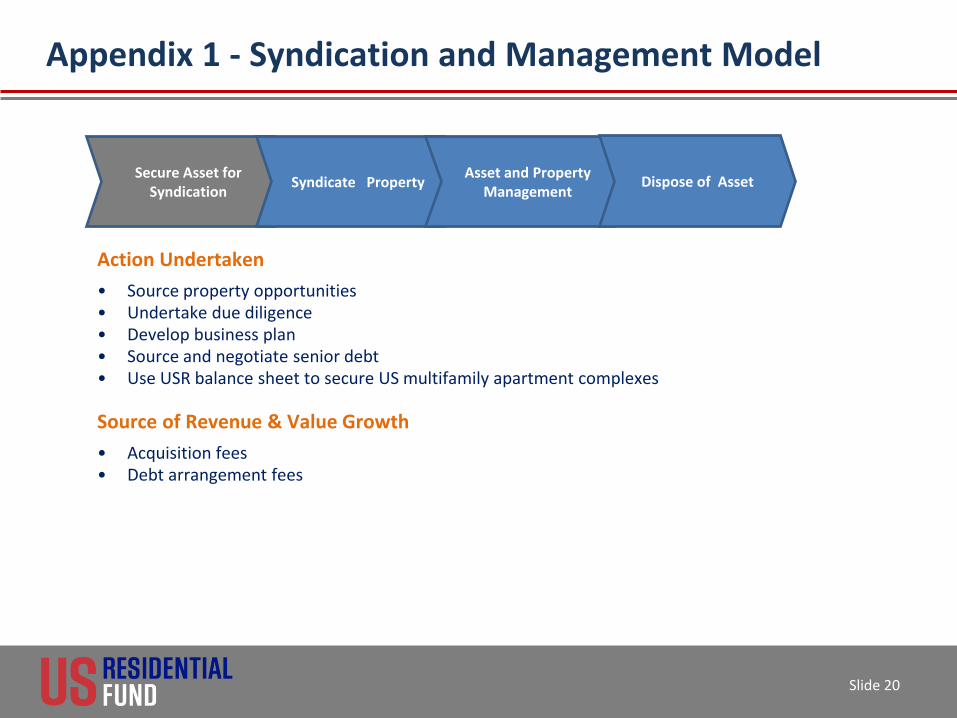

Appendix 1 - Syndication and Management Model

Slide 20

Secure Asset for Syndication

Syndicate Property Asset and Property

Management Dispose of Asset

Action Undertaken

• Source property opportunities • Undertake due diligence • Develop business plan • Source and negotiate senior debt • Use USR balance sheet to secure US multifamily apartment complexes

Source of Revenue & Value Growth

• Acquisition fees • Debt arrangement fees

CONFIDENTIAL

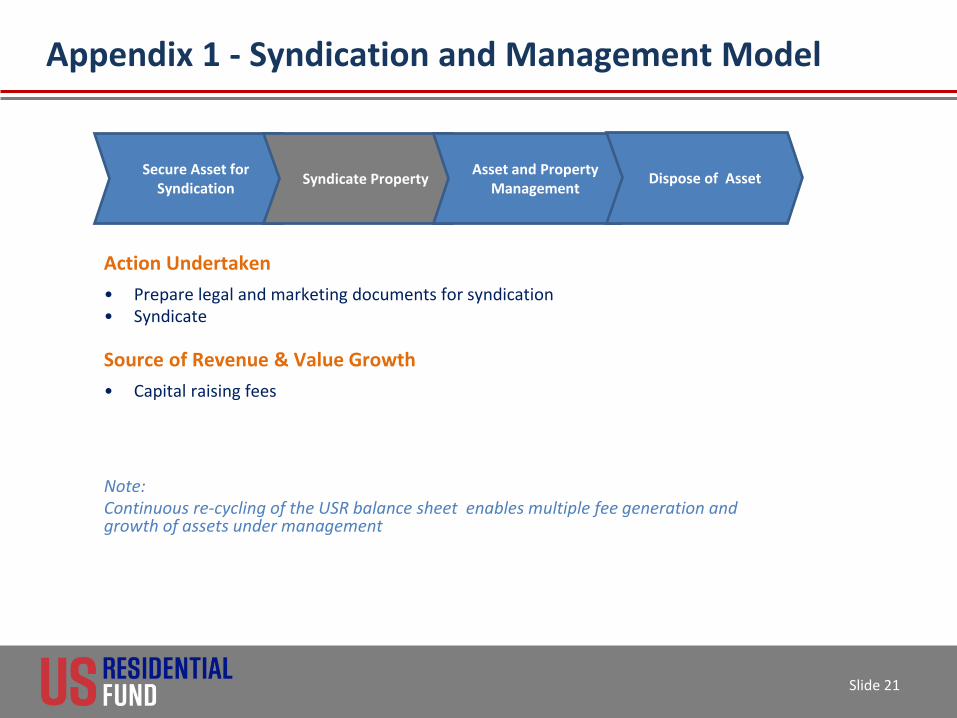

Appendix 1 - Syndication and Management Model

Slide 21

Secure Asset for Syndication

Syndicate Property Asset and Property

Management Dispose of Asset

Action Undertaken

• Prepare legal and marketing documents for syndication • Syndicate

Source of Revenue & Value Growth

• Capital raising fees

Note: Continuous re-cycling of the USR balance sheet enables multiple fee generation and growth of assets under management

CONFIDENTIAL

Appendix 1 - Syndication and Management Model

Slide 22

Secure Asset for Syndication

Syndicate Property Asset and Property

Management Dispose of Asset

Action Undertaken

• Oversight of syndicate including investor and lender liaison • Property management

Source of Revenue & Value Growth

• Property and asset management fees • Performance fees

CONFIDENTIAL

Appendix 1 - Syndication and Management Model

Slide 23

Secure Asset for Syndication

Syndicate Property Asset and Property

Management Dispose of Asset

(Est 5 - 7 yrs)

Action Undertaken

• Appoint sales broker & prepares sales materials • Negotiate sale with prospective buyers • Arrange to assign or pay out senior lender • Provide returns to investors

Source of Revenue & Value Growth

• Disposition fees • Profit Share of sales proceeds

CONFIDENTIAL

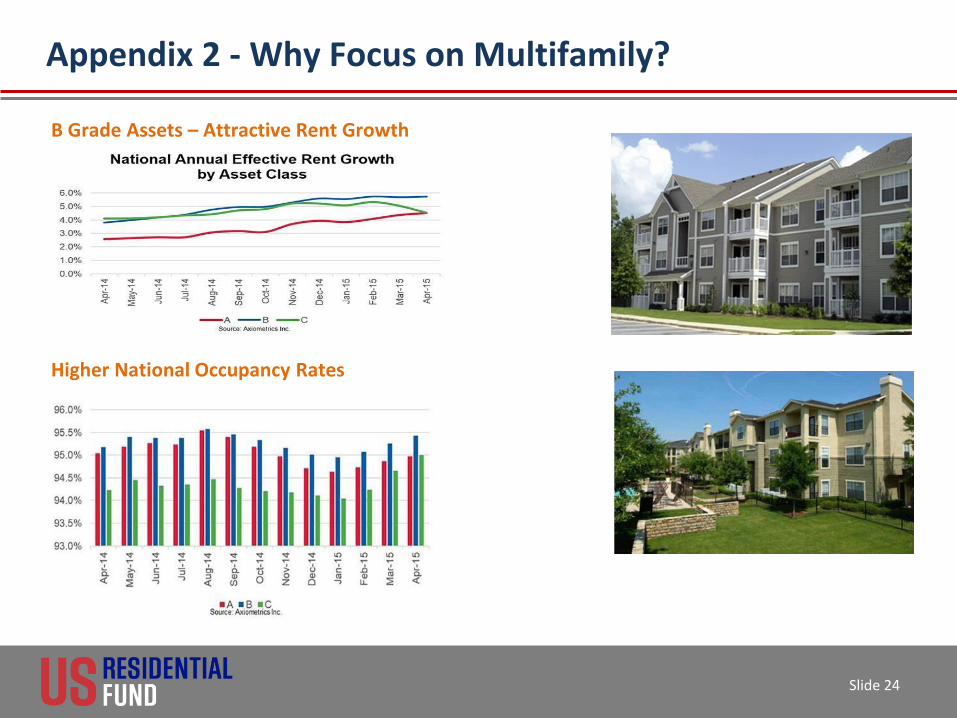

Appendix 2 - Why Focus on Multifamily?

Slide 24

B Grade Assets – Attractive Rent Growth

Higher National Occupancy Rates

CONFIDENTIAL

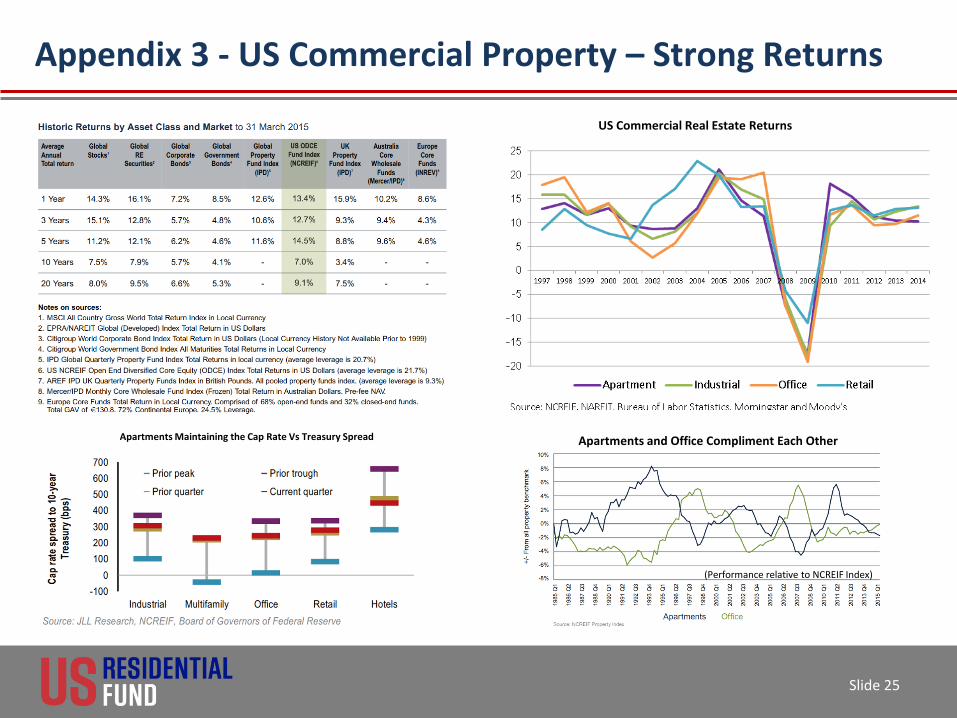

Appendix 3 - US Commercial Property – Strong Returns

Slide 25

US Commercial Real Estate Returns

Apartments Maintaining the Cap Rate Vs Treasury Spread Apartments and Office Compliment Each Other

(Performance relative to NCREIF Index)

CONFIDENTIAL

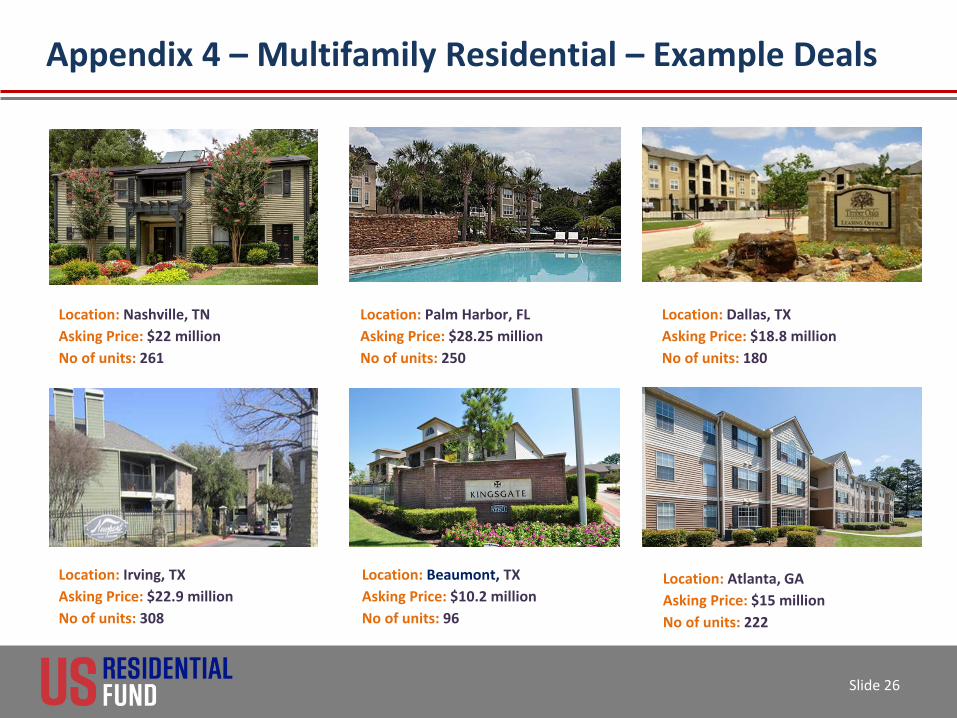

Appendix 4 – Multifamily Residential – Example Deals

Slide 26

Location: Nashville, TN

Asking Price: $22 million

No of units: 261

Location: Palm Harbor, FL

Asking Price: $28.25 million

No of units: 250

Location: Dallas, TX

Asking Price: $18.8 million

No of units: 180

Location: Irving, TX

Asking Price: $22.9 million

No of units: 308

Location: Beaumont, TX

Asking Price: $10.2 million

No of units: 96

Location: Atlanta, GA

Asking Price: $15 million

No of units: 222

CONFIDENTIAL

Appendix 5 - Current Investment Portfolio

Locations • Texas: Houston • Texas: Dallas • Georgia: Atlanta • Ohio: Cleveland

Single Family Houses in

Portfolio

140

Portfolio Valuation

USD$15.9m (as at Dec 31, 2015)

Gross Rent Roll

USD$2.16m (as at December 31, 2015)

GA and TX above US average • GDP growth • Job growth

• Population and household growth

Slide 27

CONFIDENTIAL

Appendix 6 – Acquisitions

Asset Management:

• External manager currently holds USR management contract with 9 years remaining • Operational entity and human resource assets • Intellectual property including syndication model • Offices in Dallas and Melbourne

Consideration for management rights and syndication assets:

• $1.5 million cash • 5 million performance shares

• FUM and share price hurdles • Supported by independent experts report prepared by Moore Stephens

Advantages:

• Enables USR to add fee income to property income • Earnings enhancing, through recurring syndication revenue stream • No fee leakages • Simplifies operational structure

Slide 28

CONFIDENTIAL

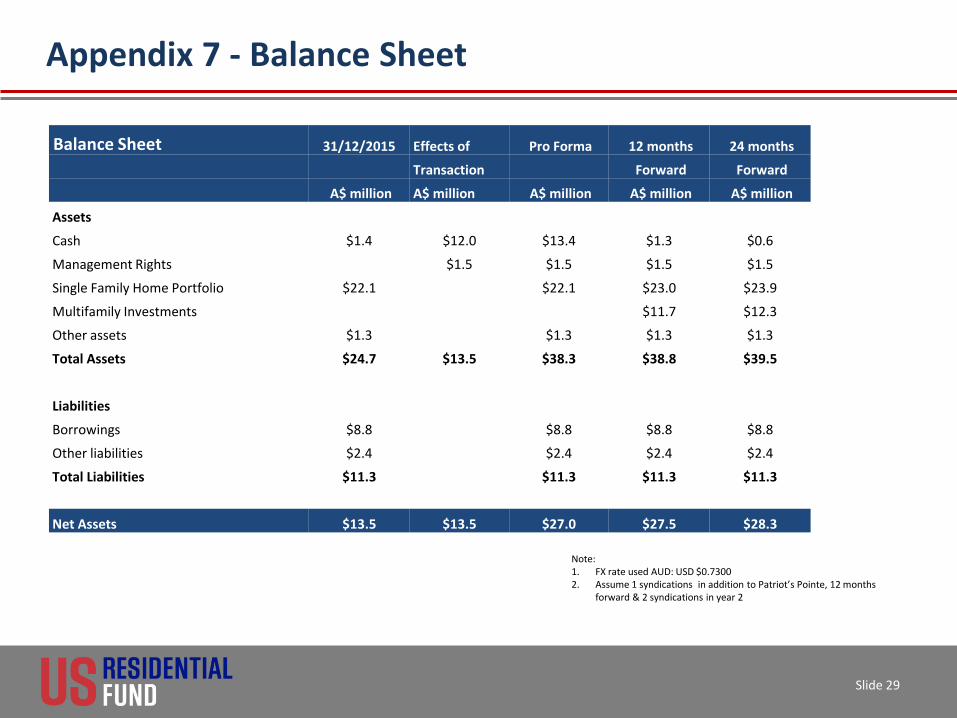

Appendix 7 - Balance Sheet

Slide 29

Balance Sheet 31/12/2015 Effects of Pro Forma 12 months 24 months

Transaction Forward Forward

A$ million A$ million A$ million A$ million A$ million

Assets

Cash $1.4 $12.0 $13.4 $1.3 $0.6

Management Rights $1.5 $1.5 $1.5 $1.5

Single Family Home Portfolio $22.1 $22.1 $23.0 $23.9

Multifamily Investments $11.7 $12.3

Other assets $1.3 $1.3 $1.3 $1.3

Total Assets $24.7 $13.5 $38.3 $38.8 $39.5

Liabilities

Borrowings $8.8 $8.8 $8.8 $8.8

Other liabilities $2.4 $2.4 $2.4 $2.4

Total Liabilities $11.3 $11.3 $11.3 $11.3

Net Assets $13.5 $13.5 $27.0 $27.5 $28.3

Note: 1. FX rate used AUD: USD $0.7300 2. Assume 1 syndications in addition to Patriot’s Pointe, 12 months

forward & 2 syndications in year 2

CONFIDENTIAL

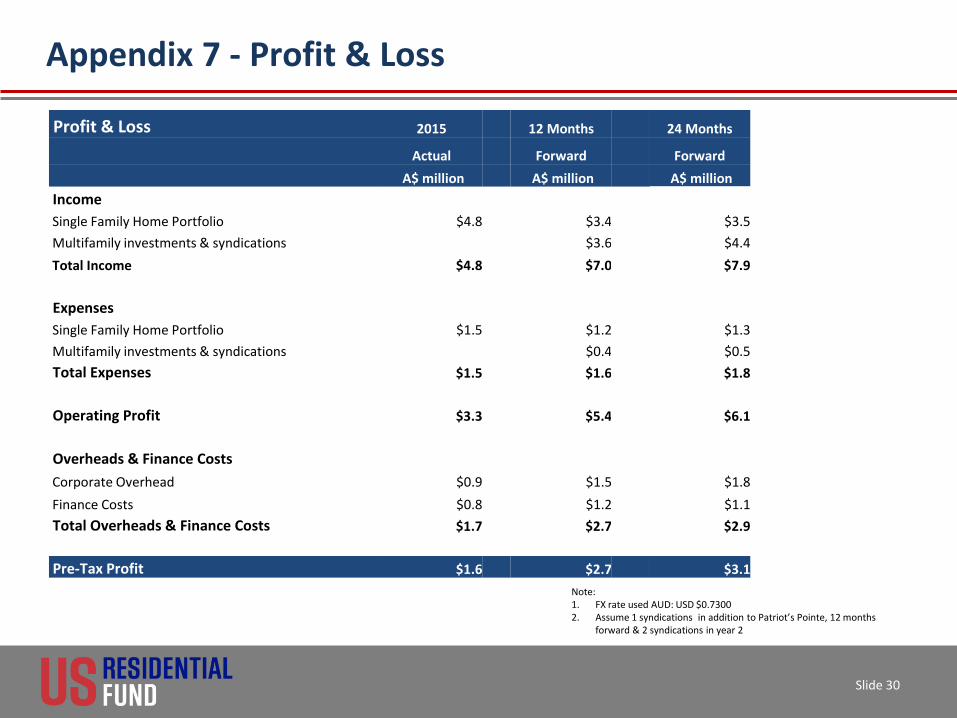

Appendix 7 - Profit & Loss

Slide 30

Note: 1. FX rate used AUD: USD $0.7300 2. Assume 1 syndications in addition to Patriot’s Pointe, 12 months

forward & 2 syndications in year 2

Profit & Loss 2015 12 Months 24 Months

Actual Forward Forward

A$ million A$ million A$ million

Income

Single Family Home Portfolio $4.8 $3.4 $3.5

Multifamily investments & syndications $3.6 $4.4

Total Income $4.8 $7.0 $7.9

Expenses

Single Family Home Portfolio $1.5 $1.2 $1.3

Multifamily investments & syndications $0.4 $0.5

Total Expenses $1.5 $1.6 $1.8

Operating Profit $3.3 $5.4 $6.1

Overheads & Finance Costs

Corporate Overhead $0.9 $1.5 $1.8

Finance Costs $0.8 $1.2 $1.1

Total Overheads & Finance Costs $1.7 $2.7 $2.9

Pre-Tax Profit $1.6 $2.7 $3.1

CONFIDENTIAL

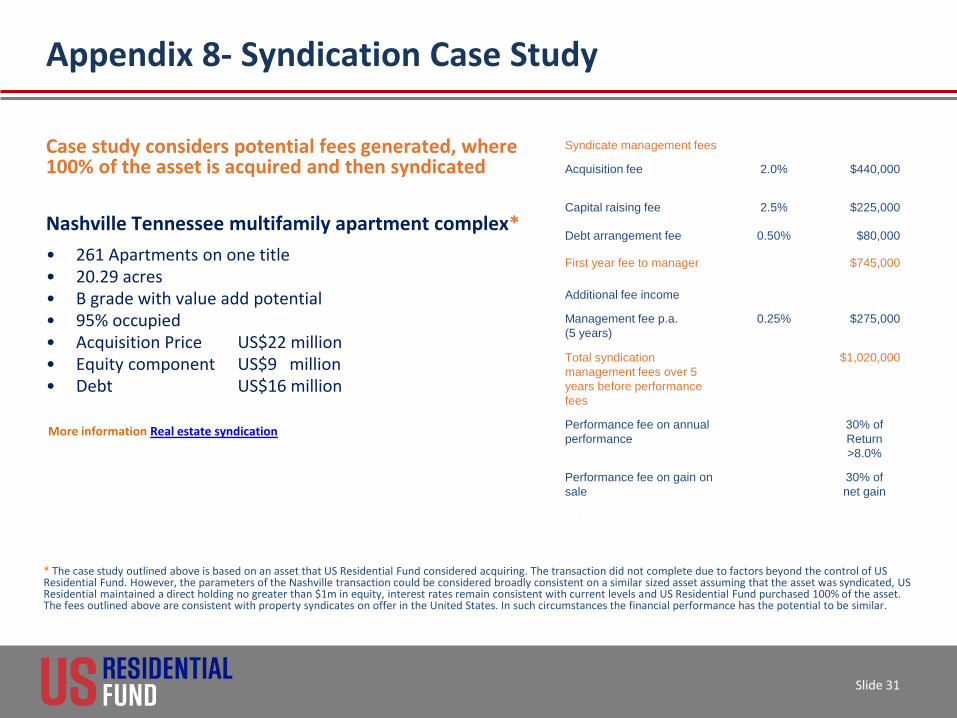

Appendix 8- Syndication Case Study

Slide 31

Case study considers potential fees generated, where 100% of the asset is acquired and then syndicated

Nashville Tennessee multifamily apartment complex*

• 261 Apartments on one title • 20.29 acres • B grade with value add potential • 95% occupied • Acquisition Price US$22 million • Equity component US$9 million • Debt US$16 million

Syndicate management fees

Acquisition fee

2.0% $440,000

Capital raising fee 2.5% $225,000

Debt arrangement fee 0.50% $80,000

First year fee to manager $745,000

Additional fee income

Management fee p.a.

(5 years)

0.25% $275,000

Total syndication

management fees over 5

years before performance

fees

$1,020,000

Performance fee on annual

performance

30% of

Return

>8.0%

Performance fee on gain on

sale

30% of

net gain

* The case study outlined above is based on an asset that US Residential Fund considered acquiring. The transaction did not complete due to factors beyond the control of US Residential Fund. However, the parameters of the Nashville transaction could be considered broadly consistent on a similar sized asset assuming that the asset was syndicated, US Residential maintained a direct holding no greater than $1m in equity, interest rates remain consistent with current levels and US Residential Fund purchased 100% of the asset. The fees outlined above are consistent with property syndicates on offer in the United States. In such circumstances the financial performance has the potential to be similar.

More information Real estate syndication

CONFIDENTIAL

Appendix 9 - Securitisation - Loans

Slide 32

In the US the vast majority of loans for apartment complexes are securitised -

Therefore their structure is different from loans in Australia

Key Areas of Difference

• Loan to Valuation Ratio’s (LVR) in the Australian are NOT the same as US Loan To Valuation ratios (LTV) • LTV’s are a risk tool used by US lenders at loan establishment date • Unlike Australia LTV’s are NOT revisited until maturity • This means in a market downturn the lender can not request a revaluation • Lenders are income ratio focused • This means they will not lend unless current cash flow supports interest after expenses • Fixed term rates are fixed and not subject to resets due to economic circumstances • Lenders are very reluctant to take possession if breaches occur – they prefer workouts • Lenders expect higher LTV’s than we typically see in Australia

Downside

• Paying out loans early has a break fee • Sourcing low LTV loans is uncommercial for USR and the lenders

CONFIDENTIAL

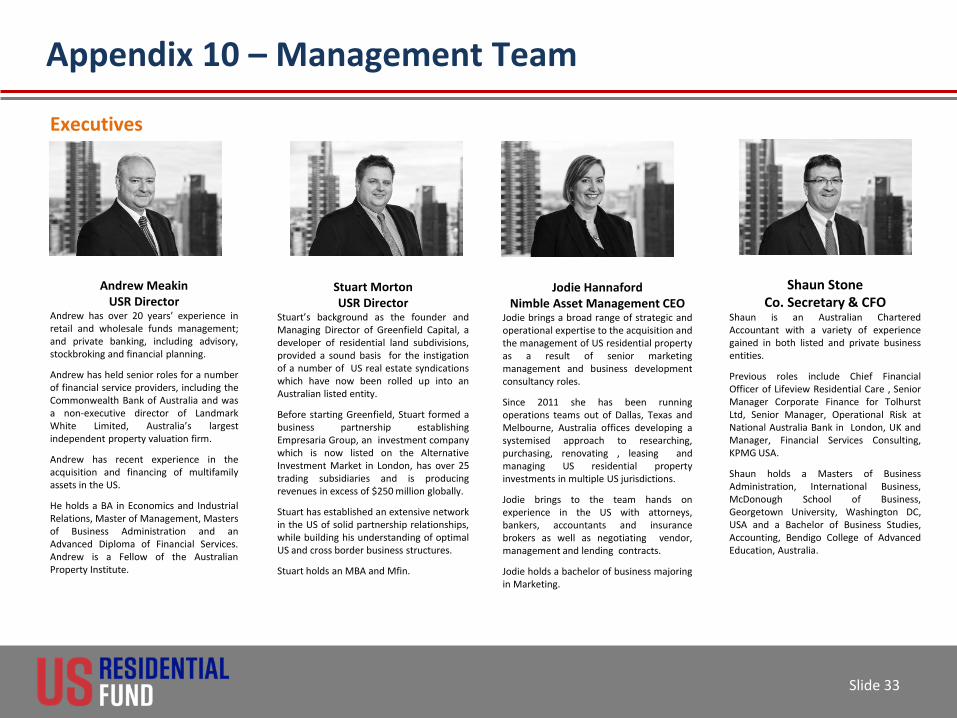

Appendix 10 – Management Team

Slide 33

Executives

Andrew Meakin USR Director

Andrew has over 20 years’ experience in retail and wholesale funds management; and private banking, including advisory, stockbroking and financial planning.

Andrew has held senior roles for a number of financial service providers, including the Commonwealth Bank of Australia and was a non-executive director of Landmark White Limited, Australia’s largest independent property valuation firm.

Andrew has recent experience in the acquisition and financing of multifamily assets in the US.

He holds a BA in Economics and Industrial Relations, Master of Management, Masters of Business Administration and an Advanced Diploma of Financial Services. Andrew is a Fellow of the Australian Property Institute.

Stuart Morton USR Director

Stuart’s background as the founder and Managing Director of Greenfield Capital, a developer of residential land subdivisions, provided a sound basis for the instigation of a number of US real estate syndications which have now been rolled up into an Australian listed entity.

Before starting Greenfield, Stuart formed a business partnership establishing Empresaria Group, an investment company which is now listed on the Alternative Investment Market in London, has over 25 trading subsidiaries and is producing revenues in excess of $250 million globally.

Stuart has established an extensive network in the US of solid partnership relationships, while building his understanding of optimal US and cross border business structures.

Stuart holds an MBA and Mfin.

Jodie Hannaford Nimble Asset Management CEO

Jodie brings a broad range of strategic and operational expertise to the acquisition and the management of US residential property as a result of senior marketing management and business development consultancy roles.

Since 2011 she has been running operations teams out of Dallas, Texas and Melbourne, Australia offices developing a systemised approach to researching, purchasing, renovating , leasing and managing US residential property investments in multiple US jurisdictions.

Jodie brings to the team hands on experience in the US with attorneys, bankers, accountants and insurance brokers as well as negotiating vendor, management and lending contracts.

Jodie holds a bachelor of business majoring in Marketing.

Shaun Stone Co. Secretary & CFO

Shaun is an Australian Chartered Accountant with a variety of experience gained in both listed and private business entities.

Previous roles include Chief Financial Officer of Lifeview Residential Care , Senior Manager Corporate Finance for Tolhurst Ltd, Senior Manager, Operational Risk at National Australia Bank in London, UK and Manager, Financial Services Consulting, KPMG USA.

Shaun holds a Masters of Business Administration, International Business, McDonough School of Business, Georgetown University, Washington DC, USA and a Bachelor of Business Studies, Accounting, Bendigo College of Advanced Education, Australia.

CONFIDENTIAL

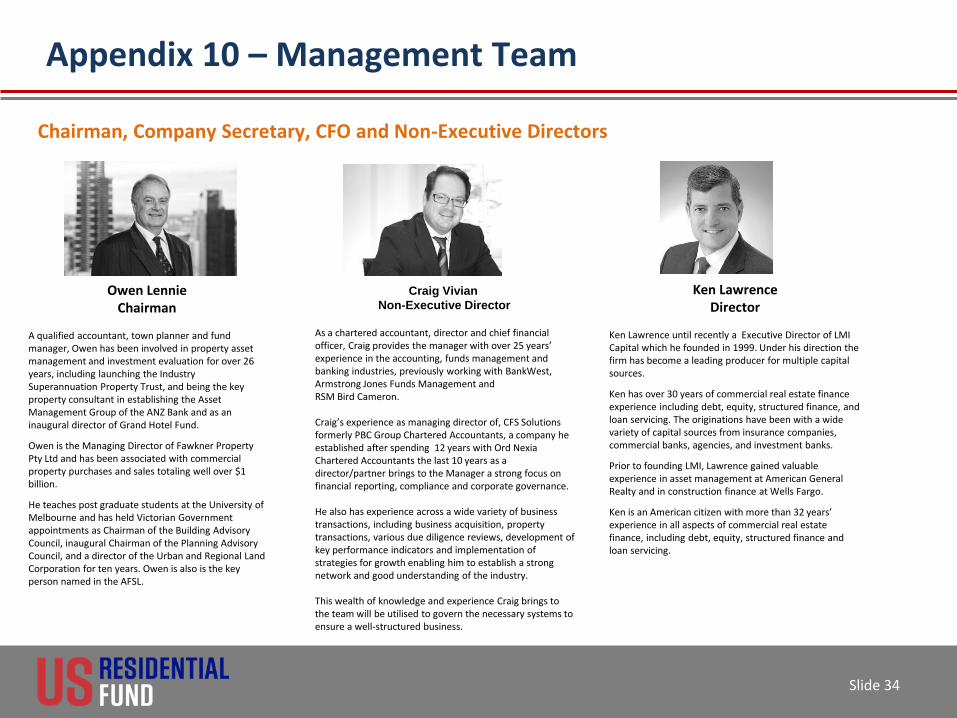

Appendix 10 – Management Team

Slide 34

Chairman, Company Secretary, CFO and Non-Executive Directors

Owen Lennie Chairman

A qualified accountant, town planner and fund manager, Owen has been involved in property asset management and investment evaluation for over 26 years, including launching the Industry Superannuation Property Trust, and being the key property consultant in establishing the Asset Management Group of the ANZ Bank and as an inaugural director of Grand Hotel Fund.

Owen is the Managing Director of Fawkner Property Pty Ltd and has been associated with commercial property purchases and sales totaling well over $1 billion.

He teaches post graduate students at the University of Melbourne and has held Victorian Government appointments as Chairman of the Building Advisory Council, inaugural Chairman of the Planning Advisory Council, and a director of the Urban and Regional Land Corporation for ten years. Owen is also is the key person named in the AFSL.

Ken Lawrence Director

Ken Lawrence until recently a Executive Director of LMI Capital which he founded in 1999. Under his direction the firm has become a leading producer for multiple capital sources.

Ken has over 30 years of commercial real estate finance experience including debt, equity, structured finance, and loan servicing. The originations have been with a wide variety of capital sources from insurance companies, commercial banks, agencies, and investment banks.

Prior to founding LMI, Lawrence gained valuable experience in asset management at American General Realty and in construction finance at Wells Fargo.

Ken is an American citizen with more than 32 years’ experience in all aspects of commercial real estate finance, including debt, equity, structured finance and loan servicing.

Craig Vivian

Non-Executive Director

As a chartered accountant, director and chief financial officer, Craig provides the manager with over 25 years’ experience in the accounting, funds management and banking industries, previously working with BankWest, Armstrong Jones Funds Management and RSM Bird Cameron. Craig’s experience as managing director of, CFS Solutions formerly PBC Group Chartered Accountants, a company he established after spending 12 years with Ord Nexia Chartered Accountants the last 10 years as a director/partner brings to the Manager a strong focus on financial reporting, compliance and corporate governance. He also has experience across a wide variety of business transactions, including business acquisition, property transactions, various due diligence reviews, development of key performance indicators and implementation of strategies for growth enabling him to establish a strong network and good understanding of the industry. This wealth of knowledge and experience Craig brings to the team will be utilised to govern the necessary systems to ensure a well-structured business.

CONFIDENTIAL

Disclaimer

This Presentation is not a prospectus, product disclosure statement or other offering document under Australian law, including the Corporations Act 2001 (CwIth) ("Corporations Act") or any other law. The Presentation has not been, nor will it be, lodged with the Australian Securities and Investments Commission.

By accepting, assessing or reviewing this Presentation, or attending any associated presentation or briefing, you agree to be bound by the following.

Images of properties in this presentation may not be assets of the Fund.

Summary Information The information in this Presentation is INFORMATION ONLY of a general nature and is not intended to be used as the basis for making an investment decision. This Presentation does not purport to be complete nor does it contain all the information which a prospective investor may require in evaluating a possible investment in USR or that would be required in a prospectus or product disclosure statement prepared in accordance with the requirements of the Corporations Act. This Presentation is not a recommendation nor financial product advice.

No member of USR or any of its related bodies corporate and their respective directors, employees, officers and advisers offer any warranties in relation to the statements and information in this Presentation.

Statements made in this Presentation are made only as of the date of this Presentation. The information in this Presentation remains subject to change without notice.

. Slide 35