Embed Size (px)

Citation preview

Page 1 of 13

INITIATING COVERAGE 23 October 2017

Tasek Corporation Berhad Between hammer and anvil: Cost rising yet price dropping

SELL Analyst Consensus: Buy 0 Hold 1 Sell 0

One of the few integrated cement plants with 53-year history

Cost rising due to raw material, diesel and maintenance

Price dropping due to overcapacity and weak demand

2Q17 earnings declined 90% yoy in tandem with revenue

Gloomy earnings outlook pending more projects from Budget

Summary

One of the few integrated cement plants with 53-year history Began operations in 1964, Tasek has an integrated manufacturing plant with clinker annual capacity of 2.3 million tonnes in Ipoh and distribution terminal in Sungai Buloh. Tasek supplies cement to some 30+ long term customers, including its Sabah associate. In 2006, Tasek ventures into ready mixed concrete and currently has 12 concrete plants in 9 locations.

Cost rising due to raw material, diesel and maintenance

Rising raw material cost driven by limited supply and rising cartage cost driven by diesel cost cause the squeeze in margin. The two operation lines are subjected to annual maintenance capex of RM 30 million in total.

Price dropping due to overcapacity and weak demand

The net price of cement has declined to RM 200-220 per tonne across industry after the rebate was given. The expansion of capacity was initiated by certain industry players 2 years ago, making them in a loss position if they were to abandon it.

The weak cement demand is mainly due to: (i) delay in construction award flow, (ii) slowdown in residential and commercial property market, and (iii) mega infrastructure projects in initial phases. The whole cement industry demand is around 18 million MT for 2017F (used to be >20 million MT) while the industry capacity is about 30 million MT excluding additional capacity coming onstream in 2017-2018.

2Q17 earnings declined 90% yoy in tandem with revenue

Tasek’s quarterly revenue saw a negative 5.4% compounded growth rate from 4Q15 to 2Q17. Earnings declined along in the same period, down to RM 1.5 million in 2Q17 that is less than 10% of RM 18 million in 2Q16.

Gloomy earnings outlook pending more projects from Budget We estimate net profit growth will be -80% for 2017 as it is dampened by the weak cement demand and overcapacity in the industry. Pending more projects such as affordable housing from Budget 2018, cement price is likely to normalise gradually. Considering the unfavourable cement price, marked increase in opex such as raw materials and decreasing dividend payment, we initiate coverage with a SELL call.

Share price RM2.30

Fundamental Score 2.35/3

Valuation Score 1.10/3

Company Description

Manufactures and sells cement and related products. It operates as an integrated cement plant. It also involved in the manufacture and trade of ready-mixed concrete; and quarry operations.

Stock Information

Industry Building materials

Sub-industry Cement & Concrete

Bursa Code 4448

Bloomberg Ticker TC MK

Listing Main

Outstanding Shares 121.1 mil

Market Cap RM 1,550.6 mil

52-week Range 12.50-14.82

Est. Free Float 22.0 %

Beta 0.21

200-day Avg Vol. 6,264

Price Performance (%)

1M 3M 12M

Stock 0.6 0.0 -9.5

FBMKLCI -1.7 -1.1 4.2

Major Shareholders

HL Cement (M) Sdn Bhd

74.28%

Aberdeen AM PLC 11.69%

Earnings Forecast 16A 17E 18E

Net Profit (RM mil) 50.3 11.2 38.5

EPS (sen) 41.5 9.3 31.8

EPS Growth (%) -45 -78 243

P/E (x) 29 136 40

DPS (sen) 70 50 70

Dividend Yield (%) 5.5 3.9 5.5

NTA/share (RM) 5.4 5.0 4.7

P/NTA (x) 2.3 2.5 2.7

Net Gearing (%) na na Na

ROA (%) 7.1 1.7 6.3

ROE (%) 7.4 1.8 6.6

Page 2 of 13

Background

Company profile

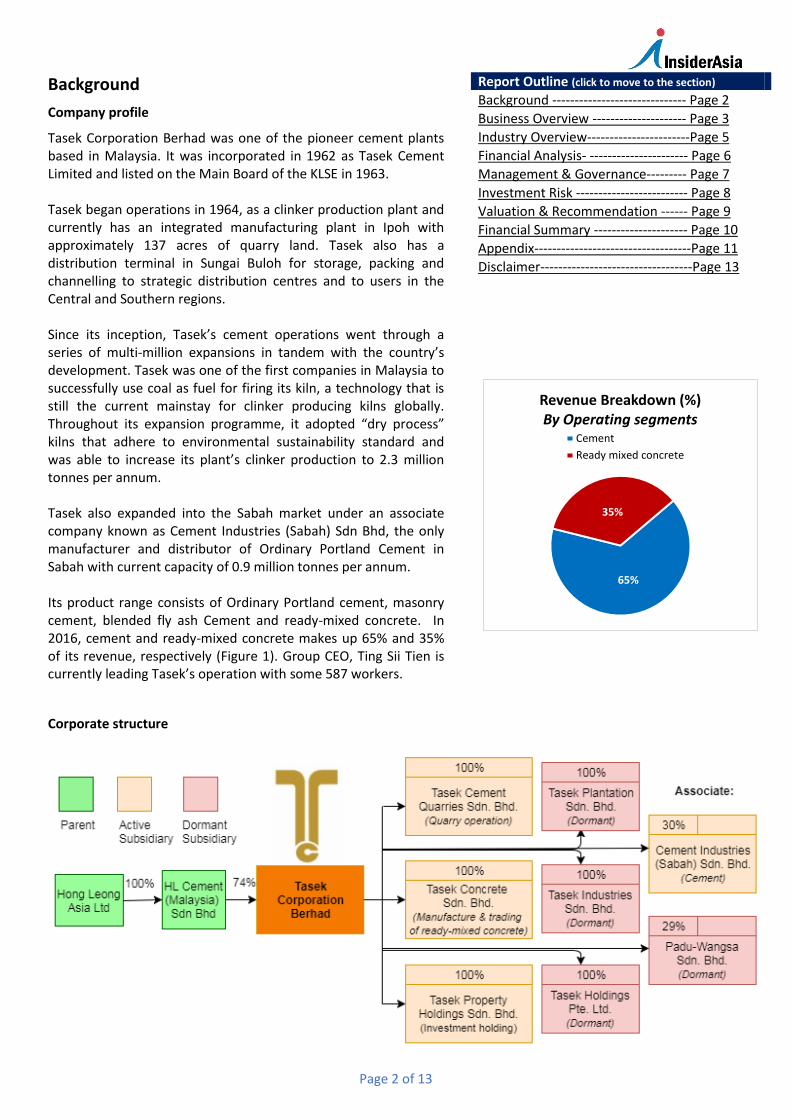

Tasek Corporation Berhad was one of the pioneer cement plants based in Malaysia. It was incorporated in 1962 as Tasek Cement Limited and listed on the Main Board of the KLSE in 1963. Tasek began operations in 1964, as a clinker production plant and currently has an integrated manufacturing plant in Ipoh with approximately 137 acres of quarry land. Tasek also has a distribution terminal in Sungai Buloh for storage, packing and channelling to strategic distribution centres and to users in the Central and Southern regions. Since its inception, Tasek’s cement operations went through a series of multi-million expansions in tandem with the country’s development. Tasek was one of the first companies in Malaysia to successfully use coal as fuel for firing its kiln, a technology that is still the current mainstay for clinker producing kilns globally. Throughout its expansion programme, it adopted “dry process” kilns that adhere to environmental sustainability standard and was able to increase its plant’s clinker production to 2.3 million tonnes per annum. Tasek also expanded into the Sabah market under an associate company known as Cement Industries (Sabah) Sdn Bhd, the only manufacturer and distributor of Ordinary Portland Cement in Sabah with current capacity of 0.9 million tonnes per annum. Its product range consists of Ordinary Portland cement, masonry cement, blended fly ash Cement and ready-mixed concrete. In 2016, cement and ready-mixed concrete makes up 65% and 35% of its revenue, respectively (Figure 1). Group CEO, Ting Sii Tien is currently leading Tasek’s operation with some 587 workers.

Report Outline (click to move to the section)

Background Page 2

Business Overview Page 3

Industry Overview-----------------------Page 5

Financial Analysis- Page 6

Management & Governance Page 7

Investment Risk Page 8

Valuation & Recommendation Page 9

Financial Summary Page 10

Appendix-----------------------------------Page 11

Disclaimer----------------------------------Page 13

65%

35%

Revenue Breakdown (%)By Operating segments

Cement

Ready mixed concrete

Corporate structure

Page 3 of 13

Business overview

Cement manufacturing process

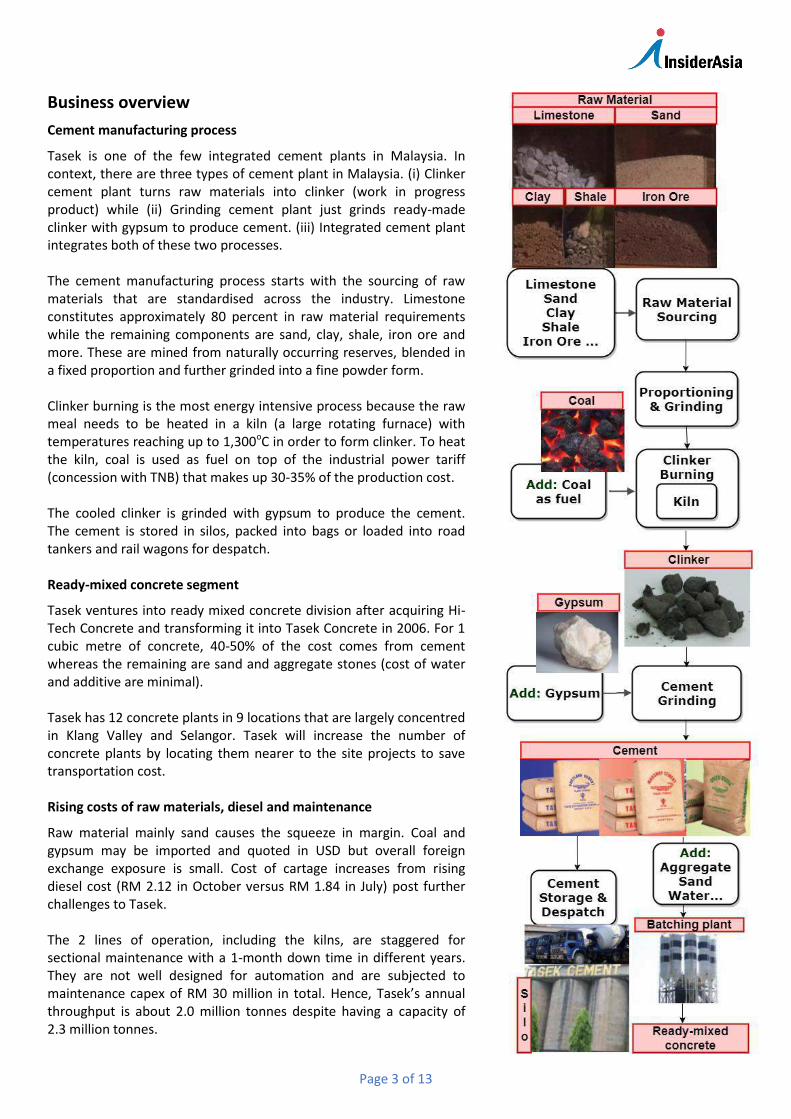

Tasek is one of the few integrated cement plants in Malaysia. In context, there are three types of cement plant in Malaysia. (i) Clinker cement plant turns raw materials into clinker (work in progress product) while (ii) Grinding cement plant just grinds ready-made clinker with gypsum to produce cement. (iii) Integrated cement plant integrates both of these two processes. The cement manufacturing process starts with the sourcing of raw materials that are standardised across the industry. Limestone constitutes approximately 80 percent in raw material requirements while the remaining components are sand, clay, shale, iron ore and more. These are mined from naturally occurring reserves, blended in a fixed proportion and further grinded into a fine powder form. Clinker burning is the most energy intensive process because the raw meal needs to be heated in a kiln (a large rotating furnace) with temperatures reaching up to 1,300oC in order to form clinker. To heat the kiln, coal is used as fuel on top of the industrial power tariff (concession with TNB) that makes up 30-35% of the production cost. The cooled clinker is grinded with gypsum to produce the cement. The cement is stored in silos, packed into bags or loaded into road tankers and rail wagons for despatch. Ready-mixed concrete segment

Tasek ventures into ready mixed concrete division after acquiring Hi-Tech Concrete and transforming it into Tasek Concrete in 2006. For 1 cubic metre of concrete, 40-50% of the cost comes from cement whereas the remaining are sand and aggregate stones (cost of water and additive are minimal). Tasek has 12 concrete plants in 9 locations that are largely concentred in Klang Valley and Selangor. Tasek will increase the number of concrete plants by locating them nearer to the site projects to save transportation cost. Rising costs of raw materials, diesel and maintenance

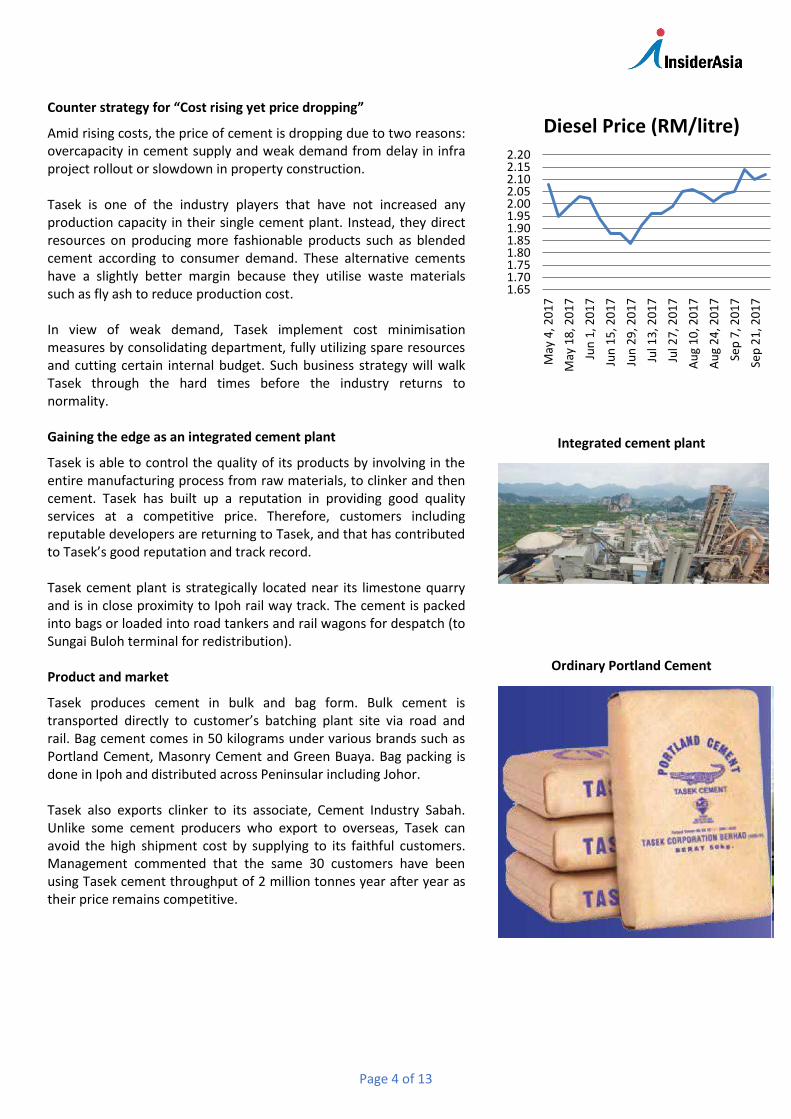

Raw material mainly sand causes the squeeze in margin. Coal and gypsum may be imported and quoted in USD but overall foreign exchange exposure is small. Cost of cartage increases from rising diesel cost (RM 2.12 in October versus RM 1.84 in July) post further challenges to Tasek. The 2 lines of operation, including the kilns, are staggered for sectional maintenance with a 1-month down time in different years. They are not well designed for automation and are subjected to maintenance capex of RM 30 million in total. Hence, Tasek’s annual throughput is about 2.0 million tonnes despite having a capacity of 2.3 million tonnes.

Page 4 of 13

Counter strategy for “Cost rising yet price dropping”

Amid rising costs, the price of cement is dropping due to two reasons: overcapacity in cement supply and weak demand from delay in infra project rollout or slowdown in property construction. Tasek is one of the industry players that have not increased any production capacity in their single cement plant. Instead, they direct resources on producing more fashionable products such as blended cement according to consumer demand. These alternative cements have a slightly better margin because they utilise waste materials such as fly ash to reduce production cost. In view of weak demand, Tasek implement cost minimisation measures by consolidating department, fully utilizing spare resources and cutting certain internal budget. Such business strategy will walk Tasek through the hard times before the industry returns to normality. Gaining the edge as an integrated cement plant

Tasek is able to control the quality of its products by involving in the entire manufacturing process from raw materials, to clinker and then cement. Tasek has built up a reputation in providing good quality services at a competitive price. Therefore, customers including reputable developers are returning to Tasek, and that has contributed to Tasek’s good reputation and track record. Tasek cement plant is strategically located near its limestone quarry and is in close proximity to Ipoh rail way track. The cement is packed into bags or loaded into road tankers and rail wagons for despatch (to Sungai Buloh terminal for redistribution). Product and market

Tasek produces cement in bulk and bag form. Bulk cement is transported directly to customer’s batching plant site via road and rail. Bag cement comes in 50 kilograms under various brands such as Portland Cement, Masonry Cement and Green Buaya. Bag packing is done in Ipoh and distributed across Peninsular including Johor. Tasek also exports clinker to its associate, Cement Industry Sabah. Unlike some cement producers who export to overseas, Tasek can avoid the high shipment cost by supplying to its faithful customers. Management commented that the same 30 customers have been using Tasek cement throughput of 2 million tonnes year after year as their price remains competitive.

1.651.701.751.801.851.901.952.002.052.102.152.20

May

4, 2

01

7

May

18

, 20

17

Jun

1, 2

01

7

Jun

15

, 20

17

Jun

29

, 20

17

Jul 1

3, 2

01

7

Jul 2

7, 2

01

7

Au

g 1

0, 2

01

7

Au

g 2

4, 2

01

7

Sep

7, 2

01

7

Sep

21

, 20

17

Diesel Price (RM/litre)

Integrated cement plant

Ordinary Portland Cement

Page 5 of 13

Industry overview

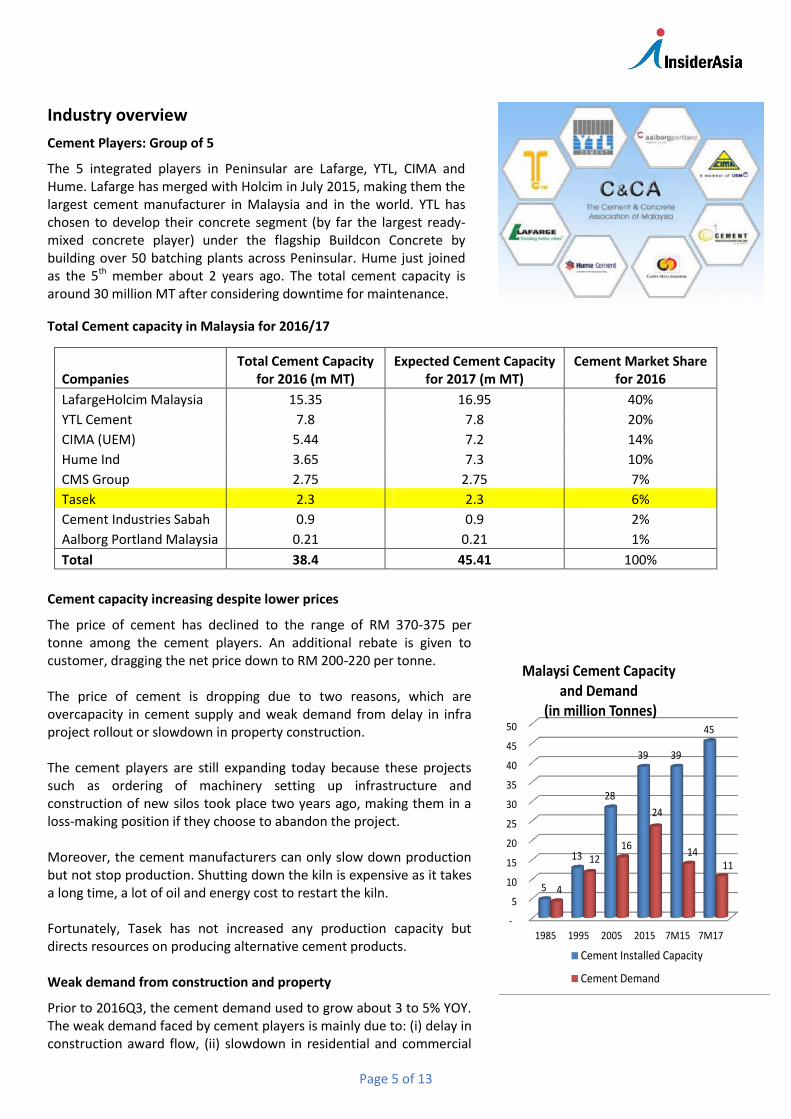

Cement Players: Group of 5

The 5 integrated players in Peninsular are Lafarge, YTL, CIMA and Hume. Lafarge has merged with Holcim in July 2015, making them the largest cement manufacturer in Malaysia and in the world. YTL has chosen to develop their concrete segment (by far the largest ready-mixed concrete player) under the flagship Buildcon Concrete by building over 50 batching plants across Peninsular. Hume just joined as the 5th member about 2 years ago. The total cement capacity is around 30 million MT after considering downtime for maintenance.

Total Cement capacity in Malaysia for 2016/17

Companies Total Cement Capacity

for 2016 (m MT) Expected Cement Capacity

for 2017 (m MT) Cement Market Share

for 2016

LafargeHolcim Malaysia 15.35 16.95 40%

YTL Cement 7.8 7.8 20%

CIMA (UEM) 5.44 7.2 14%

Hume Ind 3.65 7.3 10%

CMS Group 2.75 2.75 7%

Tasek 2.3 2.3 6%

Cement Industries Sabah 0.9 0.9 2%

Aalborg Portland Malaysia 0.21 0.21 1%

Total 38.4 45.41 100%

Cement capacity increasing despite lower prices

The price of cement has declined to the range of RM 370-375 per tonne among the cement players. An additional rebate is given to customer, dragging the net price down to RM 200-220 per tonne. The price of cement is dropping due to two reasons, which are overcapacity in cement supply and weak demand from delay in infra project rollout or slowdown in property construction. The cement players are still expanding today because these projects such as ordering of machinery setting up infrastructure and construction of new silos took place two years ago, making them in a loss-making position if they choose to abandon the project. Moreover, the cement manufacturers can only slow down production but not stop production. Shutting down the kiln is expensive as it takes a long time, a lot of oil and energy cost to restart the kiln. Fortunately, Tasek has not increased any production capacity but directs resources on producing alternative cement products. Weak demand from construction and property

Prior to 2016Q3, the cement demand used to grow about 3 to 5% YOY. The weak demand faced by cement players is mainly due to: (i) delay in construction award flow, (ii) slowdown in residential and commercial

-

5

10

15

20

25

30

35

40

45

50

1985 1995 2005 2015 7M15 7M17

5

13

28

39 39

45

4

12 16

24

14 11

Malaysi Cement Capacity and Demand

(in million Tonnes)

Cement Installed Capacity

Cement Demand

Page 6 of 13

property markets, and (iii) mega infrastructure projects in initial phases. The whole cement industry demand is around 18 million MT for 2017F (used to be >20 million MT) while the total industry capacity is about 30 million MT, excluding the additional capacity coming onstream in 2017-2018 by Lafarge, YTL, CIMA and Hume. Moving forward, the property development market is expected to remain sluggish due to overbuilding of property in the last few years. The government announced RM 49.5 billion worth of construction projects under Budget 2017, mainly on infrastructure work such as MRT2, LRT3, SUKE, DASH, TRX and BBCC. These upcoming infrastructure projects may lift the demand but not as large as perceived because these “mega projects” on an individual basis only accounts for <1% of industry capacity. Export of cement is not desirable because freight cost is high. Due to the overcapacity in cement supply and slowdown in project, the low pricing in cement after rebate is expected to stay.

Financial Analysis

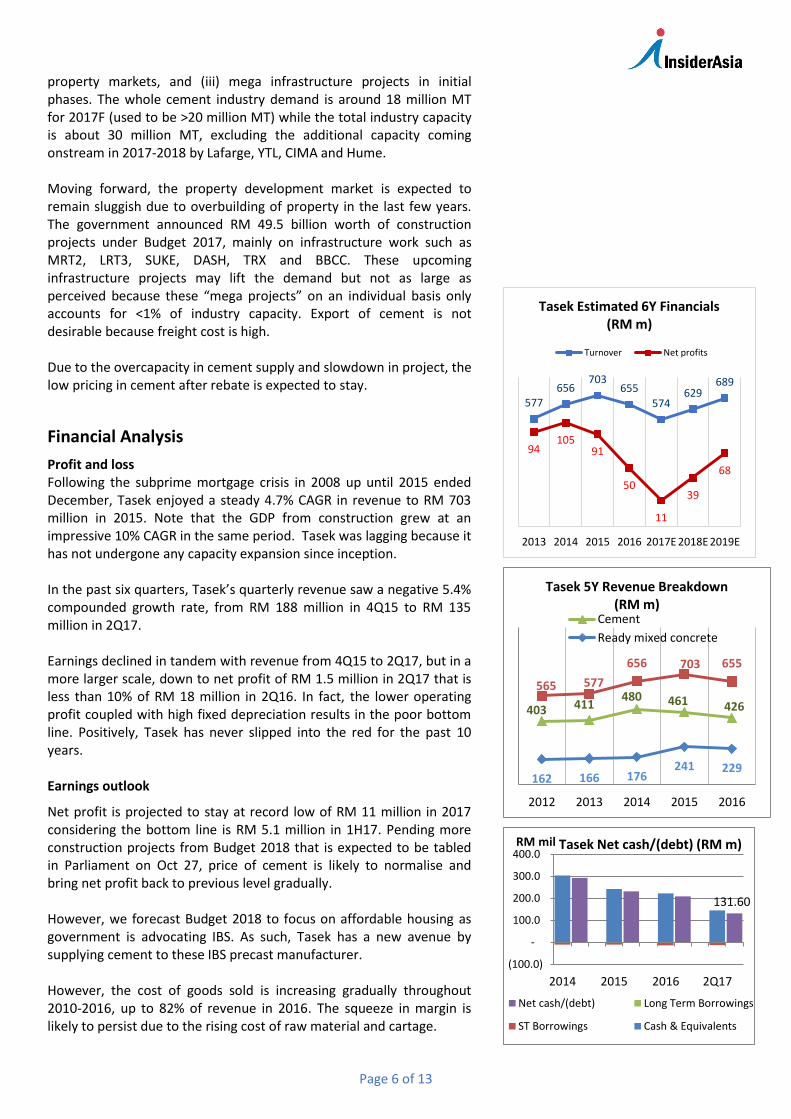

Profit and loss Following the subprime mortgage crisis in 2008 up until 2015 ended December, Tasek enjoyed a steady 4.7% CAGR in revenue to RM 703 million in 2015. Note that the GDP from construction grew at an impressive 10% CAGR in the same period. Tasek was lagging because it has not undergone any capacity expansion since inception. In the past six quarters, Tasek’s quarterly revenue saw a negative 5.4% compounded growth rate, from RM 188 million in 4Q15 to RM 135 million in 2Q17. Earnings declined in tandem with revenue from 4Q15 to 2Q17, but in a more larger scale, down to net profit of RM 1.5 million in 2Q17 that is less than 10% of RM 18 million in 2Q16. In fact, the lower operating profit coupled with high fixed depreciation results in the poor bottom line. Positively, Tasek has never slipped into the red for the past 10 years. Earnings outlook

Net profit is projected to stay at record low of RM 11 million in 2017 considering the bottom line is RM 5.1 million in 1H17. Pending more construction projects from Budget 2018 that is expected to be tabled in Parliament on Oct 27, price of cement is likely to normalise and bring net profit back to previous level gradually. However, we forecast Budget 2018 to focus on affordable housing as government is advocating IBS. As such, Tasek has a new avenue by supplying cement to these IBS precast manufacturer. However, the cost of goods sold is increasing gradually throughout 2010-2016, up to 82% of revenue in 2016. The squeeze in margin is likely to persist due to the rising cost of raw material and cartage.

577656

703655

574629

689

94105

91

50

11

39

68

2013 2014 2015 2016 2017E 2018E 2019E

Tasek Estimated 6Y Financials (RM m)

Turnover Net profits

403 411480 461 426

162 166 176241 229

565 577

656 703 655

2012 2013 2014 2015 2016

Tasek 5Y Revenue Breakdown (RM m)

Cement

Ready mixed concrete

131.60

(100.0)

-

100.0

200.0

300.0

400.0

2014 2015 2016 2Q17

RM mil Tasek Net cash/(debt) (RM m)

Net cash/(debt) Long Term Borrowings

ST Borrowings Cash & Equivalents

Page 7 of 13

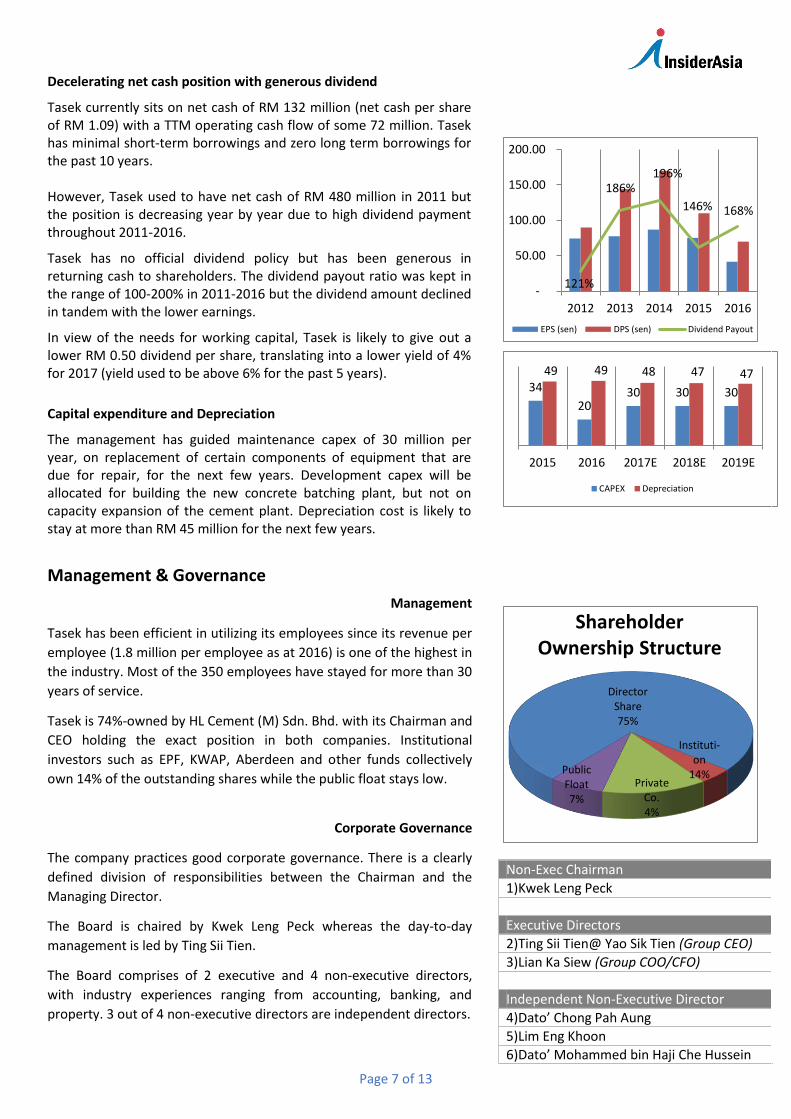

Decelerating net cash position with generous dividend

Tasek currently sits on net cash of RM 132 million (net cash per share of RM 1.09) with a TTM operating cash flow of some 72 million. Tasek has minimal short-term borrowings and zero long term borrowings for the past 10 years. However, Tasek used to have net cash of RM 480 million in 2011 but the position is decreasing year by year due to high dividend payment throughout 2011-2016.

Tasek has no official dividend policy but has been generous in returning cash to shareholders. The dividend payout ratio was kept in the range of 100-200% in 2011-2016 but the dividend amount declined in tandem with the lower earnings.

In view of the needs for working capital, Tasek is likely to give out a lower RM 0.50 dividend per share, translating into a lower yield of 4% for 2017 (yield used to be above 6% for the past 5 years).

Capital expenditure and Depreciation

The management has guided maintenance capex of 30 million per year, on replacement of certain components of equipment that are due for repair, for the next few years. Development capex will be allocated for building the new concrete batching plant, but not on capacity expansion of the cement plant. Depreciation cost is likely to stay at more than RM 45 million for the next few years.

Management & Governance

Management

Tasek has been efficient in utilizing its employees since its revenue per

employee (1.8 million per employee as at 2016) is one of the highest in

the industry. Most of the 350 employees have stayed for more than 30

years of service.

Tasek is 74%-owned by HL Cement (M) Sdn. Bhd. with its Chairman and

CEO holding the exact position in both companies. Institutional

investors such as EPF, KWAP, Aberdeen and other funds collectively

own 14% of the outstanding shares while the public float stays low.

Corporate Governance

The company practices good corporate governance. There is a clearly

defined division of responsibilities between the Chairman and the

Managing Director.

The Board is chaired by Kwek Leng Peck whereas the day-to-day

management is led by Ting Sii Tien.

The Board comprises of 2 executive and 4 non-executive directors,

with industry experiences ranging from accounting, banking, and

property. 3 out of 4 non-executive directors are independent directors.

121%

186%196%

146% 168%

-

50.00

100.00

150.00

200.00

2012 2013 2014 2015 2016

EPS (sen) DPS (sen) Dividend Payout

34

2030 30 30

49 49 48 47 47

2015 2016 2017E 2018E 2019E

CAPEX Depreciation

Director Share75%

Private Co.4%

Instituti-on

14%Public Float7%

Shareholder Ownership Structure

Non-Exec Chairman

1)Kwek Leng Peck

Executive Directors

2)Ting Sii Tien@ Yao Sik Tien (Group CEO)

3)Lian Ka Siew (Group COO/CFO)

Independent Non-Executive Director

4)Dato’ Chong Pah Aung

5)Lim Eng Khoon

6)Dato’ Mohammed bin Haji Che Hussein

Page 8 of 13

Investment Risk

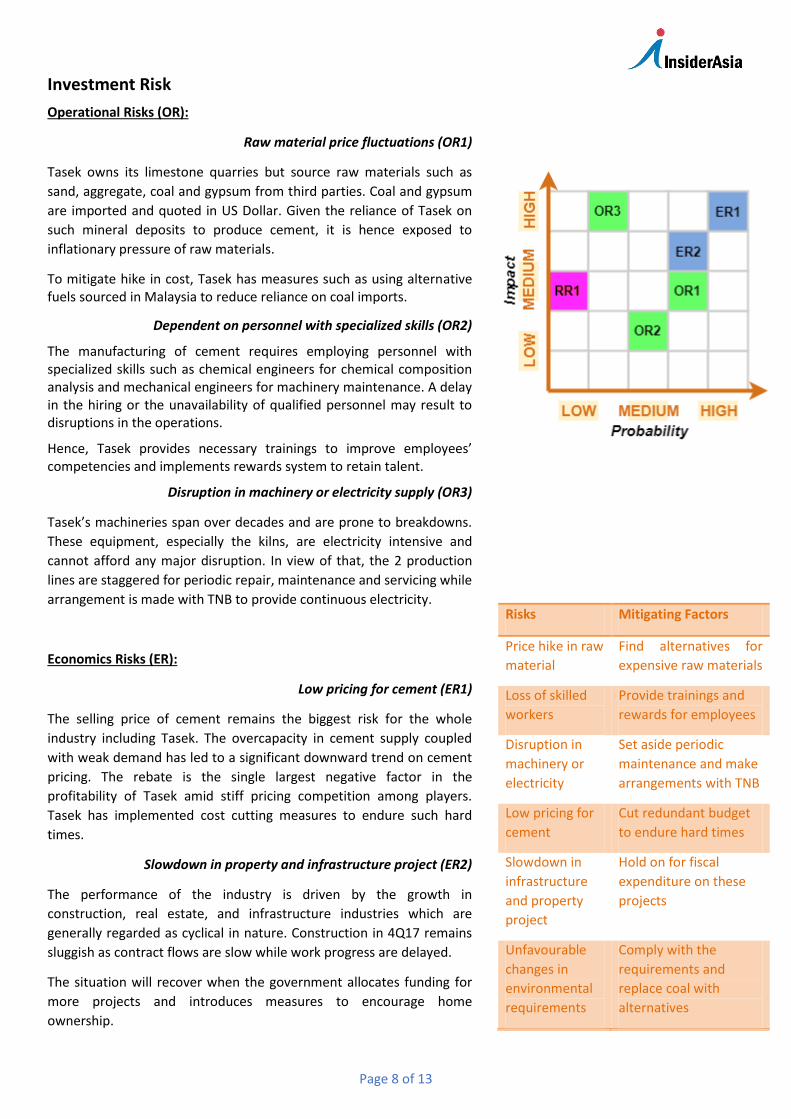

Operational Risks (OR):

Raw material price fluctuations (OR1)

Tasek owns its limestone quarries but source raw materials such as

sand, aggregate, coal and gypsum from third parties. Coal and gypsum

are imported and quoted in US Dollar. Given the reliance of Tasek on

such mineral deposits to produce cement, it is hence exposed to

inflationary pressure of raw materials.

To mitigate hike in cost, Tasek has measures such as using alternative fuels sourced in Malaysia to reduce reliance on coal imports.

Dependent on personnel with specialized skills (OR2)

The manufacturing of cement requires employing personnel with specialized skills such as chemical engineers for chemical composition analysis and mechanical engineers for machinery maintenance. A delay in the hiring or the unavailability of qualified personnel may result to disruptions in the operations.

Hence, Tasek provides necessary trainings to improve employees’ competencies and implements rewards system to retain talent.

Disruption in machinery or electricity supply (OR3)

Tasek’s machineries span over decades and are prone to breakdowns.

These equipment, especially the kilns, are electricity intensive and

cannot afford any major disruption. In view of that, the 2 production

lines are staggered for periodic repair, maintenance and servicing while

arrangement is made with TNB to provide continuous electricity.

Economics Risks (ER):

Low pricing for cement (ER1)

The selling price of cement remains the biggest risk for the whole

industry including Tasek. The overcapacity in cement supply coupled

with weak demand has led to a significant downward trend on cement

pricing. The rebate is the single largest negative factor in the

profitability of Tasek amid stiff pricing competition among players.

Tasek has implemented cost cutting measures to endure such hard

times.

Slowdown in property and infrastructure project (ER2)

The performance of the industry is driven by the growth in

construction, real estate, and infrastructure industries which are

generally regarded as cyclical in nature. Construction in 4Q17 remains

sluggish as contract flows are slow while work progress are delayed.

The situation will recover when the government allocates funding for

more projects and introduces measures to encourage home

ownership.

Risks Mitigating Factors

Price hike in raw

material

Find alternatives for

expensive raw materials

Loss of skilled

workers

Provide trainings and

rewards for employees

Disruption in

machinery or

electricity

Set aside periodic

maintenance and make

arrangements with TNB

Low pricing for

cement

Cut redundant budget

to endure hard times

Slowdown in

infrastructure

and property

project

Hold on for fiscal

expenditure on these

projects

Unfavourable

changes in

environmental

requirements

Comply with the

requirements and

replace coal with

alternatives

Page 9 of 13

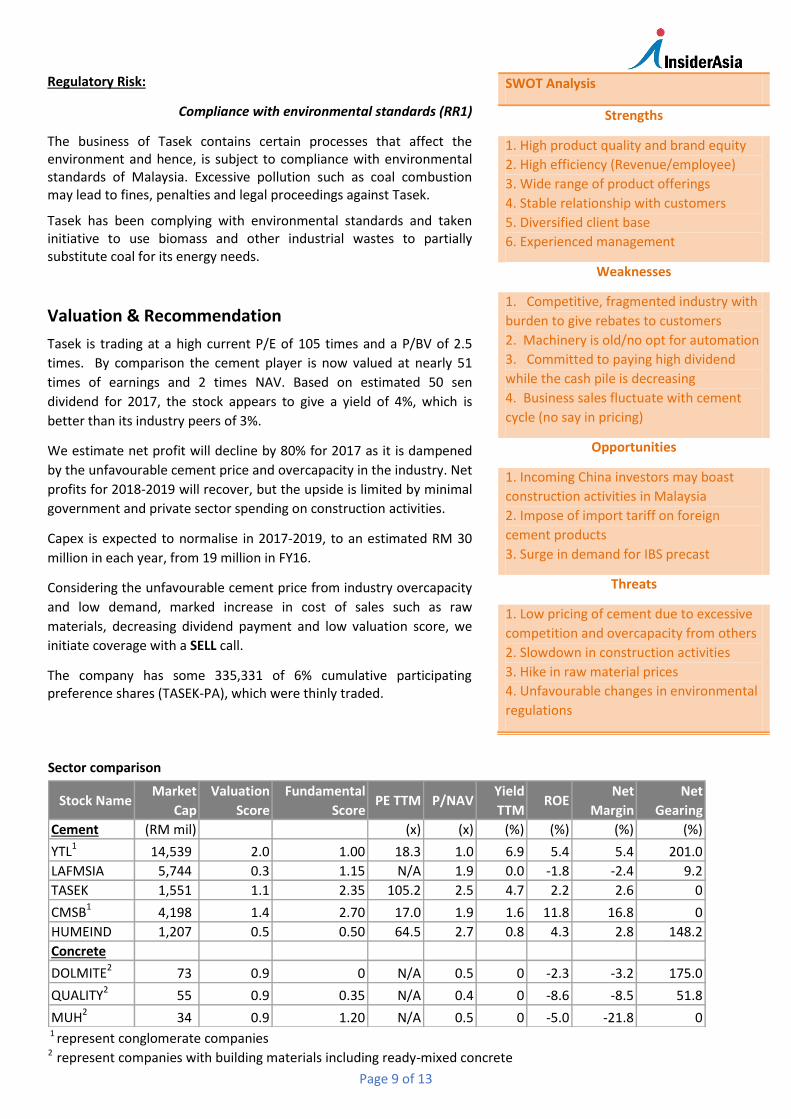

Regulatory Risk:

Compliance with environmental standards (RR1)

The business of Tasek contains certain processes that affect the environment and hence, is subject to compliance with environmental standards of Malaysia. Excessive pollution such as coal combustion may lead to fines, penalties and legal proceedings against Tasek.

Tasek has been complying with environmental standards and taken initiative to use biomass and other industrial wastes to partially substitute coal for its energy needs.

Valuation & Recommendation

Tasek is trading at a high current P/E of 105 times and a P/BV of 2.5

times. By comparison the cement player is now valued at nearly 51

times of earnings and 2 times NAV. Based on estimated 50 sen

dividend for 2017, the stock appears to give a yield of 4%, which is

better than its industry peers of 3%.

We estimate net profit will decline by 80% for 2017 as it is dampened

by the unfavourable cement price and overcapacity in the industry. Net

profits for 2018-2019 will recover, but the upside is limited by minimal

government and private sector spending on construction activities.

Capex is expected to normalise in 2017-2019, to an estimated RM 30

million in each year, from 19 million in FY16.

Considering the unfavourable cement price from industry overcapacity

and low demand, marked increase in cost of sales such as raw

materials, decreasing dividend payment and low valuation score, we

initiate coverage with a SELL call.

The company has some 335,331 of 6% cumulative participating preference shares (TASEK-PA), which were thinly traded.

SWOT Analysis

Strengths

1. High product quality and brand equity

2. High efficiency (Revenue/employee)

3. Wide range of product offerings

4. Stable relationship with customers

5. Diversified client base

6. Experienced management

Weaknesses

1. Competitive, fragmented industry with

burden to give rebates to customers

2. Machinery is old/no opt for automation

3. Committed to paying high dividend

while the cash pile is decreasing

4. Business sales fluctuate with cement

cycle (no say in pricing)

Opportunities

1. Incoming China investors may boast

construction activities in Malaysia

2. Impose of import tariff on foreign

cement products

3. Surge in demand for IBS precast

Threats

1. Low pricing of cement due to excessive

competition and overcapacity from others

2. Slowdown in construction activities

3. Hike in raw material prices

4. Unfavourable changes in environmental

regulations

Sector comparison

Stock NameMarket

Cap

Valuation

Score

Fundamental

ScorePE TTM P/NAV

Yield

TTMROE

Net

Margin

Net

Gearing

Cement (RM mil) (x) (x) (%) (%) (%) (%)

YTL1

14,539 2.0 1.00 18.3 1.0 6.9 5.4 5.4 201.0

LAFMSIA 5,744 0.3 1.15 N/A 1.9 0.0 -1.8 -2.4 9.2

TASEK 1,551 1.1 2.35 105.2 2.5 4.7 2.2 2.6 0

CMSB14,198 1.4 2.70 17.0 1.9 1.6 11.8 16.8 0

HUMEIND 1,207 0.5 0.50 64.5 2.7 0.8 4.3 2.8 148.2

Concrete

DOLMITE273 0.9 0 N/A 0.5 0 -2.3 -3.2 175.0

QUALITY2

55 0.9 0.35 N/A 0.4 0 -8.6 -8.5 51.8

MUH2

34 0.9 1.20 N/A 0.5 0 -5.0 -21.8 0 1 represent conglomerate companies 2 represent companies with building materials including ready-mixed concrete

Page 10 of 13

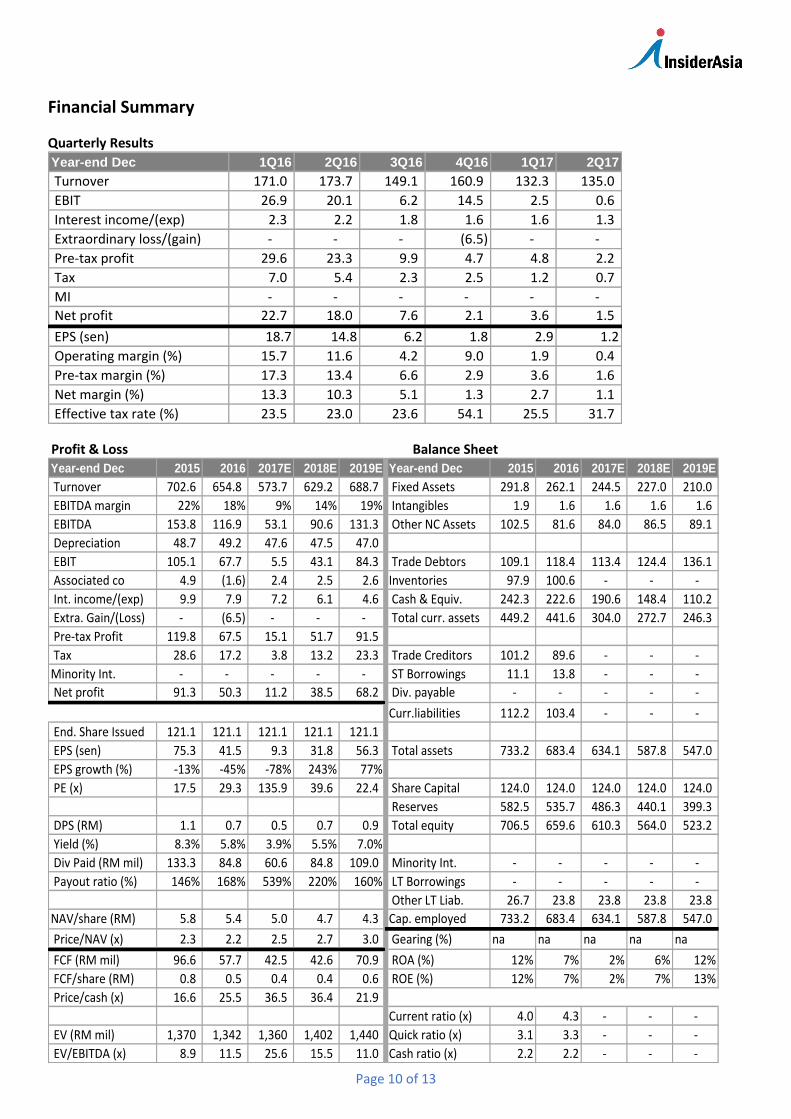

Financial Summary

Quarterly Results

Year-end Dec 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

Turnover 171.0 173.7 149.1 160.9 132.3 135.0

EBIT 26.9 20.1 6.2 14.5 2.5 0.6

Interest income/(exp) 2.3 2.2 1.8 1.6 1.6 1.3

Extraordinary loss/(gain) - - - (6.5) - -

Pre-tax profit 29.6 23.3 9.9 4.7 4.8 2.2

Tax 7.0 5.4 2.3 2.5 1.2 0.7

MI - - - - - -

Net profit 22.7 18.0 7.6 2.1 3.6 1.5

EPS (sen) 18.7 14.8 6.2 1.8 2.9 1.2

Operating margin (%) 15.7 11.6 4.2 9.0 1.9 0.4

Pre-tax margin (%) 17.3 13.4 6.6 2.9 3.6 1.6

Net margin (%) 13.3 10.3 5.1 1.3 2.7 1.1

Effective tax rate (%) 23.5 23.0 23.6 54.1 25.5 31.7

Profit & Loss Balance Sheet

Year-end Dec 2015 2016 2017E 2018E 2019E Year-end Dec 2015 2016 2017E 2018E 2019E

Turnover 702.6 654.8 573.7 629.2 688.7 Fixed Assets 291.8 262.1 244.5 227.0 210.0

EBITDA margin 22% 18% 9% 14% 19% Intangibles 1.9 1.6 1.6 1.6 1.6

EBITDA 153.8 116.9 53.1 90.6 131.3 Other NC Assets 102.5 81.6 84.0 86.5 89.1

Depreciation 48.7 49.2 47.6 47.5 47.0

EBIT 105.1 67.7 5.5 43.1 84.3 Trade Debtors 109.1 118.4 113.4 124.4 136.1

Associated co 4.9 (1.6) 2.4 2.5 2.6 Inventories 97.9 100.6 - - -

Int. income/(exp) 9.9 7.9 7.2 6.1 4.6 Cash & Equiv. 242.3 222.6 190.6 148.4 110.2

Extra. Gain/(Loss) - (6.5) - - - Total curr. assets 449.2 441.6 304.0 272.7 246.3

Pre-tax Profit 119.8 67.5 15.1 51.7 91.5

Tax 28.6 17.2 3.8 13.2 23.3 Trade Creditors 101.2 89.6 - - -

Minority Int. - - - - - ST Borrowings 11.1 13.8 - - -

Net profit 91.3 50.3 11.2 38.5 68.2 Div. payable - - - - -

Curr.liabilities 112.2 103.4 - - -

End. Share Issued 121.1 121.1 121.1 121.1 121.1

EPS (sen) 75.3 41.5 9.3 31.8 56.3 Total assets 733.2 683.4 634.1 587.8 547.0

EPS growth (%) -13% -45% -78% 243% 77%

PE (x) 17.5 29.3 135.9 39.6 22.4 Share Capital 124.0 124.0 124.0 124.0 124.0

Reserves 582.5 535.7 486.3 440.1 399.3

DPS (RM) 1.1 0.7 0.5 0.7 0.9 Total equity 706.5 659.6 610.3 564.0 523.2

Yield (%) 8.3% 5.8% 3.9% 5.5% 7.0%

Div Paid (RM mil) 133.3 84.8 60.6 84.8 109.0 Minority Int. - - - - -

Payout ratio (%) 146% 168% 539% 220% 160% LT Borrowings - - - - -

Other LT Liab. 26.7 23.8 23.8 23.8 23.8

NAV/share (RM) 5.8 5.4 5.0 4.7 4.3 Cap. employed 733.2 683.4 634.1 587.8 547.0

Price/NAV (x) 2.3 2.2 2.5 2.7 3.0 Gearing (%) na na na na na

FCF (RM mil) 96.6 57.7 42.5 42.6 70.9 ROA (%) 12% 7% 2% 6% 12%

FCF/share (RM) 0.8 0.5 0.4 0.4 0.6 ROE (%) 12% 7% 2% 7% 13%

Price/cash (x) 16.6 25.5 36.5 36.4 21.9

Current ratio (x) 4.0 4.3 - - -

EV (RM mil) 1,370 1,342 1,360 1,402 1,440 Quick ratio (x) 3.1 3.3 - - -

EV/EBITDA (x) 8.9 11.5 25.6 15.5 11.0 Cash ratio (x) 2.2 2.2 - - -

Page 11 of 13

Appendix

Appendix 1: Location of Cement Plants in Malaysia

Page 12 of 13

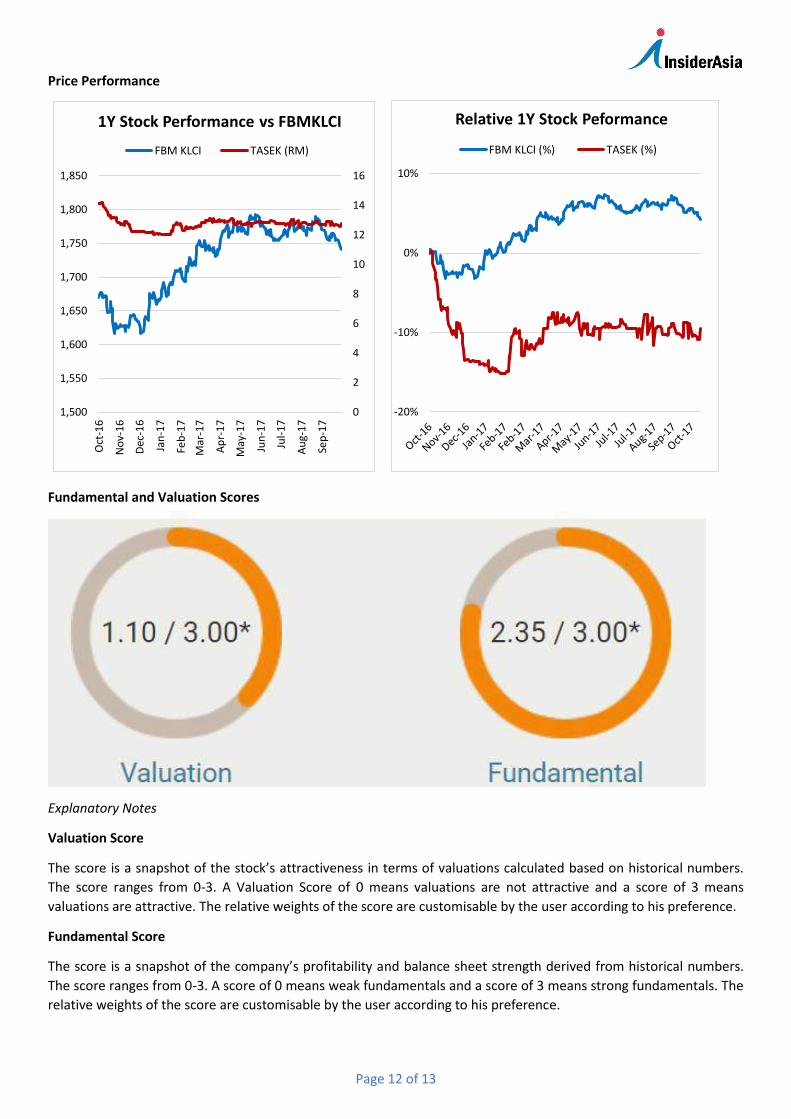

Price Performance

0

2

4

6

8

10

12

14

16

1,500

1,550

1,600

1,650

1,700

1,750

1,800

1,850

Oct

-16

No

v-1

6

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

1Y Stock Performance vs FBMKLCI

FBM KLCI TASEK (RM)

-20%

-10%

0%

10%

Relative 1Y Stock Peformance

FBM KLCI (%) TASEK (%)

Fundamental and Valuation Scores

Explanatory Notes

Valuation Score

The score is a snapshot of the stock’s attractiveness in terms of valuations calculated based on historical numbers.

The score ranges from 0-3. A Valuation Score of 0 means valuations are not attractive and a score of 3 means

valuations are attractive. The relative weights of the score are customisable by the user according to his preference.

Fundamental Score

The score is a snapshot of the company’s profitability and balance sheet strength derived from historical numbers.

The score ranges from 0-3. A score of 0 means weak fundamentals and a score of 3 means strong fundamentals. The

relative weights of the score are customisable by the user according to his preference.

Page 13 of 13

Disclaimer

This report is intended for Malaysian residents only and has been prepared without regard to your specific

investment objectives, financial situation or particular needs.

Neither the information nor any opinion expressed constitutes an offer, or an invitation to make an offer, to buy or

sell any securities or related financial instruments.

The information herein is obtained from various sources and we do not guarantee its accuracy or completeness.

All views and advice are given in good faith but without legal responsibility. You should not regard the reports as a

substitute for the exercise of your own judgment and you should seek professional advice for your specific

investment needs. Any opinions expressed in this report are subject to change without notice.

Our shareholders, directors and employees may have positions in or may be materially interested in any of the

stocks. We may also have or have had dealings with or may provide or have provided content services to the

companies mentioned in the reports.

This report has been prepared by Asia Analytica Sdn Bhd pursuant to the Mid and Small Cap Research Scheme (MidS)

administered by Bursa Malaysia Berhad. This report has been produced independent of any influence from Bursa

Malaysia Berhad or the subject company. Bursa Malaysia Berhad and its group of companies disclaim any and all

liability, howsoever arising, out of or in relation to the administration of the MidS and/or this report.

For other research reports under the MidS, please visit Bursa Marketplace at http://www.bursamids.com.

Linda Koh

603-77218060

Asia Analytica Sdn Bhd

Suite 3D, Level 3, Menara KLK

1 Jalan PJU7/6 Mutiara Damansara

47810 Petaling Jaya

Selangor

Malaysia