Embed Size (px)

Citation preview

To Downsize or Not

To Downsize or not to Downsize – What does the Empirical Evidence Suggest?

Abstract

There has been much written about the effects of downsizing on the financial health and the market valuation of companies that engage in this practice. But this literature is fragmented, focusing on various aspects of companies, various reasons for downsizing, and various financial and market outcome measures. The present study was conducted to try and address some of this fragmentation by comparing those companies that downsized in 2008, while financially healthy or not, with those companies that did not downsize. The impact of the downsizing event was assessed by using various financial measures as well as a measure of company market valuation over the short-term (2009-2011) and long-term (2009-2014). Findings indicate that across all financial measures, except Return on Equity, downsizing makes no difference to the financial health of a company either in the short term (up to 3 years after the downsizing) or in the long-term (up to 6 years after the downsizing). And with regards to Return on Equity, downsizing companies immediately after the downsizing were more inefficient in their use of equity. A theory is proposed to explain the persistence of the use of downsizing in the face of evidence that suggests it is not effective in addressing financial and market difficulties. The hope is that this work will better inform, not only scholars, but also senior leaders faced with a decision to downsize or not to downsize.

Michael S. Carriger, M.S., D.Mgt.Sacred Heart University

Welch College of Business

Keywords: downsizing, financial health, impact of downsizing, proactive downsizing, reactive downsizing

1

To Downsize or Not

A CEO is faced with a saturated market, falling sales, declining revenue, little

strategic direction, and a parent company clamoring for its return on budgeted revenue.

What does the CEO do? The CEO of this actual company (identifying details withheld to

protect the anonymity of the company) does the unthinkable, at least at this company, he

downsizes in order to cut costs and make the return to the parent company. After

shedding 7% of his workforce, the CEO addresses the remaining employees. He tells

them how hard this decision was to make. The company has never laid off workers

before. He tells them that this was not a “downsizing” but a “rightsizing”. That this was

necessary in order to adjust the company to new market demands. He tells them that this

was a one time event precipitated by change in the market place and financial demands.

He tells them that this “rightsizing” will put the company back on the track to success.

One year later the market is still saturated, sales continue to decline, revenue is still

stagnant, and the parent is still clamoring for its return. So, the CEO downsizes again.

He gives the remaining employees a slightly different message this time. He

underestimated how much “rightsizing” was necessary. This additional “rightsizing” will

fix the problem. But he doesn’t mention that this is a one-time event, as it obviously

isn’t. Over the course of the next three years … four more lay offs … or “rightsizings”.

Obviously, the downsizing did not solve this company’s problems. Yet it

disrupted countless employees lives, both employees downsized and employees

remaining with the company, as well as the community surrounding this company.

Although there has been quite a bit written about the effects of downsizing on the

financial health and the market valuation of companies, this literature is fragmented,

focusing on various aspects of companies, various reasons for downsizing, and various

2

To Downsize or Not

financial and market outcome measures. Additionally, this work has appeared to have

little to no practical impact on the corporate practice of downsizing. One might ask, why

another study on the financial impact of downsizing on corporations. The hope is that a

single, comprehensive, and empirically grounded view of the impact of downsizing could

consolidate opinion about downsizing and impact actual management decisions to:

downsize or not. That is what this paper provides, a brief review of the available research

literature on the impact of downsizing on the ongoing financial health and market

valuation of companies and an analysis of a comprehensive data set looking at the short-

and long-term impact of downsizing on the financial health and market valuation of

companies that were initially financially struggling or financially healthy. The objective

is to show that despite the significant human impact of downsizing, the downsizing

actually does not significantly improve the downsizing company’s financial health or

market valuation.

Literature Review

A review of the research literature on the impact of downsizing suggests that this

literature can be divided into two categories. One set of research, primarily published in

the management literature, has looked at the impact of downsizing on a company’s

financial health. A second set, primarily published in the finance literature, has looked at

the impact of downsizing on a company’s market valuation. In both cases it is clear that

the downsizing did not significantly improve the financial health or market valuation of

the downsizing companies.

Management Literature

3

To Downsize or Not

With regards to the management literature, Demeuse and colleagues (DeMeuse,

Vanderheiden, & Bergman, 1994; DeMeuse, Bergmann, Vanderheiden & Roraff, 2004;

DeMeuse & Dai, 2013) conducted three studies. In all three studies the authors focused

on the impact of downsizing on the subsequent financial performance of the companies

that downsized. They employed financial outcome measures such as profit margin,

return on assets, return on equity, asset turnover, and market-to-book ratio (DeMeuse, et.

al., 1994; DeMeuse, et. als., 2004) and return on assets, profit margin, revenue growth,

and market capitalization (DeMeuse & Dai, 2013). They followed the companys’

financial progress for 3 years (DeMeuse, et. al., 1994), 4 years (DeMeuse & Dai, 2013)

and 12 years (DeMeuse, et. al., 2004) after the downsizing event. These authors found

that downsizing lead to worse financial performance (DeMeuse, et. al., 1994) two years

after downsizing, with improvement in the third year (DeMeuse, et. al., 2004). They

found that companies engaging in smaller scale downsizing performed better, and

companies engaging in less frequent downsizing performed better (DeMeuse, et. al.,

2004). And they found that non-downsizing companies out performed downsizing

companies, but that this difference diminished over time (DeMeuse & Dai, 2013).

Casio and colleagues (Cascio, Young, & Morris, 1997), looking at return on

assets and return on common stock up to 2 years after a downsizing event, also found that

downsizing did not lead to higher returns, however, downsizing plus asset restructuring

did. Ballester and colleagues (Ballester, Livnat, & Sinha, 1999) considered return on

sales and return on common stock in companies one year after downsizing and found that

downsizing lead to improved stock position but poorer financial performance. Chalos

and Chen (2002), looking at the reasons for downsizing, compared those companies that

4

To Downsize or Not

downsized in reaction to poor financial performance (reactive downsizers) with those

companies that downsized in anticipation of market changes (proactive downsizers) for

three years after the downsizing and found that proactive downsizing was more

successful than reactive downsizing in terms of ongoing financial performance, however,

financial performance did not always correspond with market reaction. Guthrie and

Datta (2008), investigating solely return on assets, though also considering moderator

variables such as industry conditions and human resources policies and procedures, one

year after a downsizing event, found that downsizing had a negative effect on financial

performance, but that industry context moderates the effect. Brauer (2010), again

looking at return on assets, but also considering characteristics of the downsizing process,

one year after a downsizing event, found that smaller layoffs were less damaging than

larger layoffs to the ongoing financial health of the companies and that industry sector

and economic conditions, as well as how the downsizing was communicated, moderated

the effect.

Finally, Datta, Guthrie, Basuil, and Pandey (2010) conducted a narrative review

of the literature including 91 studies conducted between 1984 and 2008, 20 of the studies

focused on the market valuation of the downsizing companies, 19 of the studies focused

on the financial returns of the downsizing companies. The authors found that on average

downsizing announcements had a negative impact on stock price; but that downsizing

had a mixed impact on financial performance. Only two of the studies looked at long-

term impact on stock returns. Most studies used static, cross-sectional rather than

longitudinal design. And studies gave little consideration to alternatives to downsizing as

an approach to address the companies’ issues.

5

To Downsize or Not

In summary, the management literature on downsizing suggests that downsizing

has an overall negative impact on the ongoing financial health of the organization

engaging in such a practice. This effect may be greater for those companies downsizing

in response to previous poor financial performance, may or may not have the same

negative impact on the market valuation of the company, and may dissipate over time.

Additionally, other variables, such as the size and frequency of downsizing, as well as

industry conditions, and the way in which the downsizing was communicated might

moderate these negative financial impacts. However, this group of studies focused

primarily on the short-term impact of downsizing (1 to 3 years after the downsizing

event, with the except of the DeMesue, et. al., 2004 study), only occasionally considered

the reasons for the downsizing (reacting to poor financial performance or proactively

responding to anticipated changes in the market), and only looked at a relatively small set

of financial outcome measures and only occasionally considered the impact on market

valuation. The present study builds on this literature by considering longitudinally the

short-term (1 to 3 years) and long-term (1 to 6 years) impact of downsizing on a wide

range of financial measures of profitability, debt, efficiency, and revenue.

Finance Literature

With regards to the finance literature, Worrell and colleagues (Worrell, Davidson,

& Sharma, 1991), Lee (1997), Brookman and colleagues (Brookman, Chang, & Rennie,

2007), Cagle and colleagues (Cagle, Sen, & Pawlukiewicz, 2009), and Bordeman and

colleagues (Bordeman, Kannan, & Pinheiro, unpublished) looked at the impact of

downsizing announcements on the return on common stock anywhere from 3 (Bordeman,

et. al., unpublished) to 180 (Worrell, et. al., 1991) days after the announcement. Worrell

6

To Downsize or Not

and colleagues (Worrell, et. al., 1991) found a general negative market reaction to a

downsizing announcement, especially if the downsizing were reactive, large, and

permanent. Lee (1997) similarly found a negative market reaction to a downsizing

announcement in both US and Japanese companies, especially if the downsizing were

reactive, frequent, large, and permanent. Cagle and colleagues (Cagle, et. al., 2009)

found that the industry in which the downsizing occurred moderated the market reaction

to the downsizing, with the banking industry receiving a generally positive reaction to

downsizing (irrespective of size, reason, or corporate governance) and the securities

industry receiving a general negative reaction. Bordeman and colleagues (Bordeman, et.

al., unpublished) found the market reaction to a downsizing announcement was more

negative when the downsizing company was in a strong competitive environment. On

the other hand, Brookman and colleagues (Brookman, et. al., 2007) found that CEOs

announcing downsizing received more total pay the year after the downsizing than did

other CEOs and that downsizing increased shareholder value.

Gombola and Tsetsekos (1992), Chen and colleagues (Chen, Mehrota, Sivakumar,

& Yu, 2001), Hiller and colleagues (Hiller, Marshall, McColgan, & Werema, 2007) and

Marshall and colleagues (Marshall, McColgan, & McLeish, 2012) considered the impact

of downsizing on stock price, as well as a number of other financial measures from a few

days up to three years after the downsizing event. Gombola and Tsetsekos (1992) found

that downsizing do to plant closing had a negative impact on, not only the financial

performance of a company but also, the company’s stock performance. Chen and

colleagues (Chen, et. al., 2001) found that, in the companies they studied, operating

performance declined leading up to a downsizing event and then improved after the

7

To Downsize or Not

downsizing, however, the downsizing announcement led to a negative market response

(especially if the downsizing was reactive). Hiller and colleagues (Hiller, et. al., 2007)

found that in those companies in which poor operating performance preceded the

downsizing, downsizing had a significant negative impact on stock prices, but

downsizing increased productivity and corporate focus. On the other hand, Marshall

(Marshall, et. al., 2012) found a positive market reaction to downsizing when it occurred

in a good economy but poor reaction in a bad economy, irrespective of the stated reasons

for the downsizing.

Finally, Capelle-Blancard and Couder (2008) conducted a meta-analysis of 41

studies conducted between 1990 and 2006, looking at the market reaction to a downsizing

announcement. The authors found that a downsizing announcement had a negative

impact on stock price, especially if the downsizing was proactive.

In summary, the finance literature on downsizing suggests that downsizing leads

to a negative market reaction both in terms of return on common stock and stock price.

This negative reaction was particularly prominent when the downsizing was reactive (to

previous and current financial struggles), large, frequent, and permanent. This negative

reaction was observed in both the US and Japanese markets. And, the industry and the

competitive environment in which the company existed moderated this negative reaction.

However, some studies found that a downsizing announcement lead to a positive market

reaction, especially if the downsizing occurred in a good economy, and lead to an

increase in productivity and corporate focus. This group of studies focused primarily on

the very short-term impact of the downsizing announcement (within days of the

announcement) on return on common stock and stock price rather than the impact of the

8

To Downsize or Not

actual downsizing event itself and typically did not compare the impact of the downsizing

on both the market valuation and financial performance of the companies studied. The

present study additionally builds on this literature by adding measure of market valuation

(stock equity) to the wide range of financial measures, thus comparing the impact of

downsizing on both the financial health and market valuation of corporations

longitudinally in the short-term (1 to 3 years) and in the long-term (1 to 6 years) after

downsizing.

[Insert Table 9 about here]

It is puzzling why companies would continue to employee downsizing as a

strategy when the empirical literature suggests that downsizing is not effective in

addressing the financial health or market valuation of the company. Theoretically, Tsai,

Wu, Wang, & Huang (2006) suggest that the use of Institutional Theory may account for

the reasons companies downsize in the face of evidence that downsizing will not help.

The authors (Tsai, et. al., 2006) leveraging McKinley’s work on the social cognitive

interpretation of downsizing suggest that the urge to downsize might be driven by

economic, institution, and social cognitive factors even though financial health and

market valuation may not be impacted. McKinley and collegues (McKinley, Zhao, &

Rust, 2000) originally concluded that theoretically “the typical downsizing decision is

likely to be informed by a mixture of future performance expectations, conformity

to institutional rules defining downsizing as legitimate and effective, and the

sociocognitive dynamics that underlie the origins of those rules.” (p. 238).

By longitudinally comparing those companies, currently in the Fortune 500 who

were also in the Fortune 500 in 2008, that downsized in 2008 while financially healthy or

9

To Downsize or Not

while financially unhealthy, with those companies that did not downsize in 2008, under

both financial health or non-health, this study hopes to show that downsizing has no

significant effect and, given the significant human impact downsizing causes, should be

considered counterproductive. The index year of 2008 was selected for analysis as this

represented the beginning of the financial crisis in the US and increased the likelihood of

finding companies in poor financial health and that downsized. Rather than employing

an event methodology, which is currently popular in the downsizing literature, a

combination of repeated measures analysis of variance and partial correlation, controlling

for downsizing, was used to get a broader longitudinal assessment over not only the short

term (1 to 3 years after downsizing) but also the long term (1 to 6 years after the

downsizing). Finally, the impact of the downsizing event was assessed using a wide

range of financial outcome measures as well as a measure of market valuation. The hope

is that this brief review of the effects of downsizing on financial performance and market

valuation and the comprehensive study reported here will better inform scholars and

practitioners, as well as senior leaders who find themselves in a position to have to decide

whether: to downsize or not to downsize.

[Insert Graphic 1 about here]

Methods

Those members of the 2014 Fortune 500 that were also on the Fortune 500 in

2008 were identified as the initial subjects for this research. This consisted of 482

companies. Of these, 68 companies were excluded from analysis do to missing data,

leaving a total subject pool of 414 companies. Missing data included primarily employee

10

To Downsize or Not

headcount for the years 2008 and/or 2009 such that the companies could not be

categorized as downsizing or not in 2008.

The 414 companies were categorized as downsizers or non-downsizers in the year

2008 based on percent change in headcount in that year. Those companies that showed a

percent decrease in headcount of 5% or more were categorized as downsizers. All others

were categorized as non-downsizers. This method of categorizing companies as

downsizers or not was chosen specifically because this was the approach taken by

previous studies on downsizing in the management literature.

Similarly, the 414 companies were categorized as financially healthy or unhealthy

in the year 2008 based on percent change in cash flow from operations. Cash flow from

operations is a measure of how well a company can generate cash flow from it’s normal

operations in order to maintain those operations and grow. Those companies that showed

a percent decrease in cash flow from operations of 5% or more were categorized as

financially unhealthy. All others were categorized as financially healthy. The 5% cut-off

was chosen to parallel the approach to categorizing downsizing.

Thus four groups were created for analysis: financially healthy companies that

downsized, financially unhealthy companies that downsized, financially healthy

companies that did not downsize, and financially unhealthy companies that did not

downsize.

[Insert Table 10 about here]

For the financially healthy companies that downsized, the average change in cash

flow from operations was 1087.08% and the average change in employee headcount was

-11.75% from 2008 to 2009. For the financially unhealthy companies that downsized, the

11

To Downsize or Not

average change in cash flow from operations was -230.27% and the average change in

employee headcount was -12.39% from 2008 to 2009. For the financially healthy

companies that did not downsize, the average change in cash flow from operations was

131.55% and the average change in employee headcount was 5.14% from 2008 to 2009.

Finally, for the financially unhealthy companies that did not downsize, the average

change in cash flow from operations was -105.61% and the average change in employee

headcount was 15.30% from 2008 to 2009. The average percent change in cash flow

from operations showed a trend toward differing among the four groups overall (F =

2.120, p = 0.097). The average percent change in employee headcount differed

significantly among the four groups (F = 12.323, p = 0.000).

Data on each of the 414 companies was extracted from the Mergent Online ™

database for the period 2008 through 2014. Number of Employees and Cash flow from

Operations were extracted in order to categorize the companies in 2008 as downsizers or

not and as financially healthy or not. Financial performance measures that were extracted

from the database included: Profitability Measures - Return on Equity (ROE – a

profitability ratio which measures the efficient use of equity or income per dollar of

equity (Block and Hirt, 2005)), Return on Assets (ROA – a profitability ratio which

measures the efficient use of assets or income per dollar of assets (Block and Hirt,

2005)), Return on Investment (ROI – a profitability ratio which measures the efficient use

of investment, or income per dollar of investment (long-term commitment) (Block and

Hirt, 2005)), Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA

– measures the operating income of the company before deductions for financial charges,

taxes, and costs of assets (Block and Hirt, 2005)); Debt Measures - Current Ratio

12

To Downsize or Not

(liquidity ratio which measures a company’s ability to meet its current cash needs (Block

and Hirt, 2005)), Long-term Debt (measures how much of a company’s operations are

financed by debt that lasts longer than one year (including bond issues, leases,

bank loans)); Efficiency Measures - Inventory Turnover (measures the efficient use of

inventory or sales per dollar of inventory (Block and Hirt, 2005)), Revenue per Employee

(measures employee productivity or revenue generated per employee), Total Asset

Turnover (measures the efficient use of assets or sales per dollar of total assets (Block

and Hirt, 2005)); and Revenue Measure - Total Revenue (measures total receipts from

sales or total income for the business). The market valuation measure that was extracted

from the database was Stock Equity (measures the total contribution to and ownership

interest of the stockholders in the company (Block and Hirt, 2005)).

The financial performance and market valuation of each company were analyzed

for the years 2009 through 2011 (short-term analysis) and 2009 through 2014 (long-term

analysis).

A series of repeated measures ANOVAs were conducted, employing Hotelling’s

Trace statistic and Least Significant Difference post-hoc statistic with category

(financially healthy companies that downsized, financially unhealthy companies that

downsized, financially healthy companies that did not downsize, and financially

unhealthy companies that did not downsize) as a between-subject variable and year (2009

through 2011 for the short-term analysis and 2009 through 2014 for the long-term

analysis) as a within-subject variable on each of the financial and market valuation

measures. On those financial measures showing a significant interaction of year by

category on the repeated measures ANOVA an additional partial correlation analysis was

13

To Downsize or Not

conducted, holding categories constant, to assess whether the financial differences existed

independent of category.

This method of using a repeated measures ANOVA and partial correlation

analysis was specifically chosen over the more recently employed event methodology in

order to allow for a longitudinal study of the impact of downsizing over time. In order to

address the concern that factors other than downsizing might emerge over time that

confound the relationship between downsizing and outcome measures, a partial

correlation analysis was added to the repeated measures ANOVA analysis, controlling for

or partialing out the effect of downsizing, on the year-by-year correlations of the outcome

measures. If the significance of the correlations disappear, that would signal that

downsizing was the main contributor to the year-by-year correlation. Therefore, the

combination of repeated measures ANOVA and partial correlation analysis allows for a

longitudinal study but inversely controlling for the effect of other confounding variables.

No additional control variables, other than financial health of the company, were

used in the analysis. As the data sample was drawn from the Fortune 500, the sample

was statistically large, and the Fortune 500 by definition is homogeneous in terms of size

(large) of company and success (successful) of company, the use of additional control

variables was deemed unnecessary. Further, since the index year of 2008 was

specifically chosen to capitalize on the difficult economic period, to increase the

likelihood of finding companies in financial distress and/or that downsized, controlling

for economic conditions was also deemed unnecessary.

Results

14

To Downsize or Not

To verify the effectiveness of the categorization process of identifying downsizing

and non-downsizing as well as financially healthy and financially unhealthy companies,

repeated measures ANVOAs on number of employees and cash flow from operations

were conducted separately. With regards to number of employees, the ANOVA yielded a

significant main effect for year (F = 15.195, p = 0.000), indicating that overall the

number of employees grew each year from 2008 to 2011. Additionally, a significant

interaction between year and category of company was found (F = 6.497, p = 0.000),

indicating that although the non-downsizing companies showed a steady increase in

number of employees, the downsizing companies, regardless of financial health, showed

an initial decline in number of employees, followed by a stablization from 2008 to 2011.

A long-term analysis, looking at the years 2008 through 2014, replicated the above

analysis yielding a significant main effect for year (F = 5.370, p = 0.000) and year by

category interaction (F = 3.221, p = 0.000).

[insert figure 1 about here]

With regards to cash flow from operations, the ANOVA yielded a significant

main effect for year (F = 8.438, p = 0.000), indicating that overall cash flow from

operations steadily increased to 2011. A long-term analysis, looking at the years 2008

through 2014, replicated the above analysis yielding a significant main effect for year (F

= 2.340, p = 0.037) but additionally a year by category interaction (F = 3.605, p = 0.000),

indicating that the financially unhealthy companies initially significantly declined then

steadily increased whereas the financially healthy companies showed a steady increase.

[insert figure 2 about here]

Financial Outcome Measures

15

To Downsize or Not

In order to investigate the impact of downsizing on the ongoing financial strength

of organizations, a series of separate repeated measures ANOVAs were conducted on

various financial measures with category of company (financially unhealthy downsizers,

financially healthy downsizers, financially unhealthy non-downsizers, and financially

healthy non-downsizers) as a between-subject variable and year (2009 through 2011 for

the short-term analysis and 2009 through 2014 for the long-term analysis) as a within

subject variable.

Profitability Measures

With regards to return on equity (ROE), the ANOVA yielded a significant main

effect for year (F = 4.447, p = 0.012) and for category of company (F = 3.302, p = 0.025),

as well as a year by category of company interaction (F = 2.063, p = 0.055). Companies

that downsized whether financially healthy or not showed more inefficient use of equity

than did companies that did not downsize in the short term. The downsizing companies

that were financially healthy initially recovered the efficient use of equity more quickly

than did the downsizing companies that were financially unhealthy initially. The result

washed out though when submitted to a long-term analysis. The long-term analysis

revealed a significant main effect for year (F = 6.451, p = 0.000), indicating a steady

increase in ROE from 2009 through 2014. But no year by category interaction, indicating

that by 2014 all companies regardless of financial health or downsizing showed

increasing ROE. The result was partially supported by a partial correlation analysis.

Partial, year-by-year correlations, holding category of company constant showed that the

significant year-by-year correlation faded between 2009 and 2010, between 2009 and

2012, and between 2009 and 2014. All other year-by-year partial correlations from 2010

16

To Downsize or Not

through 2014 were significant at the 0.05 level or greater. This indicated that category of

company had an effect on the year-by-year relationship of this financial variable one year

after downsizing but not beyond that.

[insert figure 3 about here]

[insert table 1 about here]

With regards to return on assets (ROA), the ANOVA yielded a significant main

effect for year (F = 34.364, p = 0.000) and for category of company (F = 6.568, p =

0.000), as well as a year by category of company interaction (F = 3.178, p = 0.004). This

indicated that all companies, whether financially healthy or not or downsizers or not,

showed a steady increase in ROA through 2011, with downsizing companies increasing

more. Financially healthy companies did better overall than did financially unhealthy

companies, regardless of downsizing. And downsizing companies did worse than did

non-downsizing companies regardless of financial health with the financially unhealthy

downsizers doing worst overall. The result washed out again when submitted to a long-

term analysis. The long-term analysis revealed a significant main effect for year (F =

8.921, p = 0.000), indicating a steady increase in ROA from 2009 through 2014. But no

year by category interaction, indicating that by 2014 all companies regardless of financial

health or downsizing showed increasing ROA. The short-term analysis was also not

supported by the partial correlation analysis. Partial, year-by-year correlations, holding

category of company constant showed that category of company had no effect on the

year-by-year relationship of this financial variable after downsizing.

[insert figure 4 about here]

[insert table 2 about here]

17

To Downsize or Not

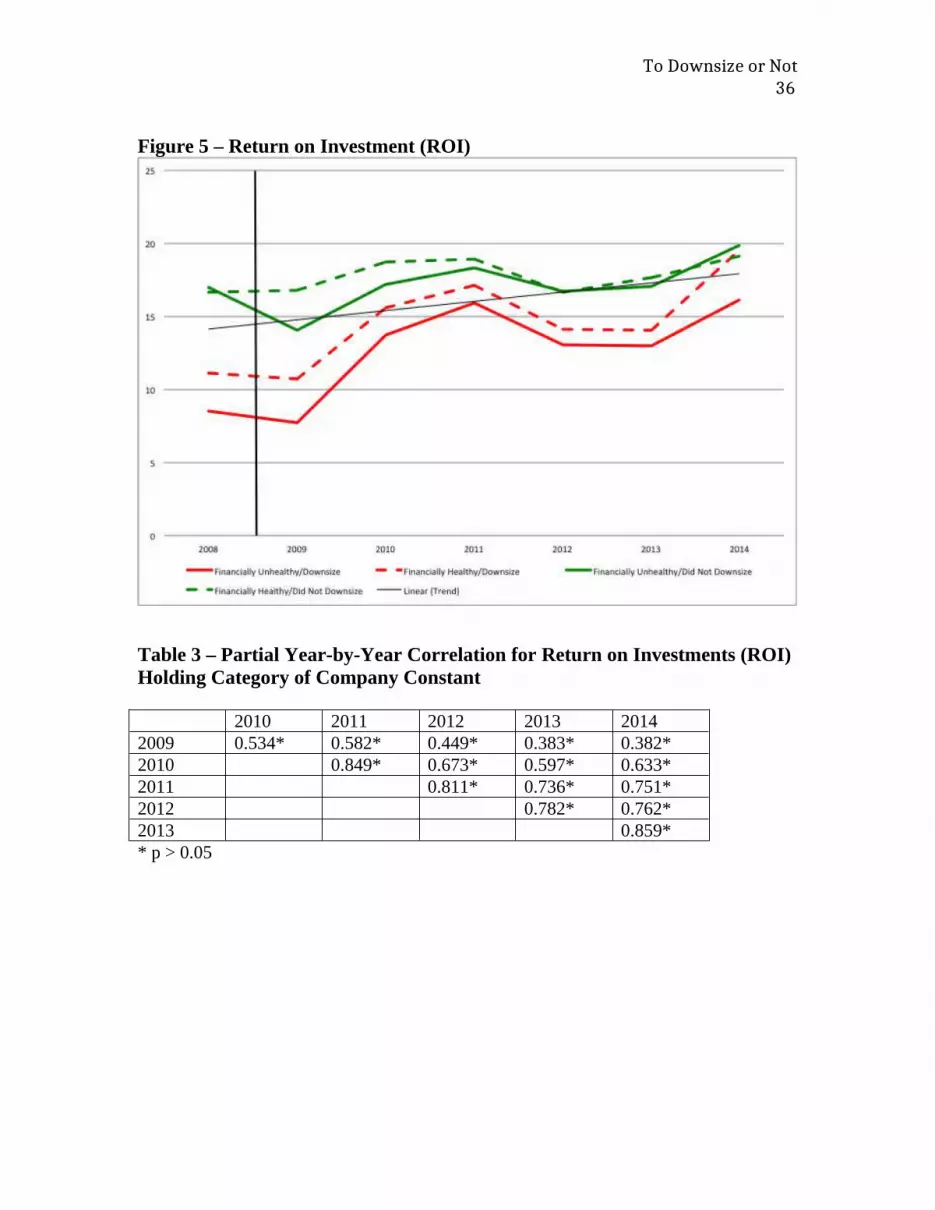

With regards to return on investment (ROI), the ANOVA yielded a significant

main effect for year (F = 37.373, p = 0.000) and for category of company (F = 5.427, p =

0.001), as well as a year by category of company interaction (F = 2.976, p = 0.007). This

indicated that all companies, whether financially healthy or not or downsizers or not,

showed a steady increase in ROI through 2011, with downsizing companies increasing

more. Financially healthy companies did better overall than did financially unhealthy

companies, regardless of downsizing. And downsizing companies did worse than did

non-downsizing companies regardless of financial health, again, with the financially

unhealthy downsizers doing worst overall. This result washed out as well when

submitted to a long-term analysis. The long-term analysis revealed a significant main

effect for year (F = 8.552, p = 0.000), indicating a steady increase in ROI from 2009

through 2014. But no year by category interaction, indicating that by 2014 all companies

regardless of financial health or downsizing showed increasing ROI. The short-term

analysis was also not supported by the partial correlation analysis. Partial, year-by-year

correlations, holding category of company constant showed that category of company had

no effect on the year-by-year relationship of this financial variable after downsizing.

[insert figure 5 about here]

[insert table 3 about here]

With regards to earnings before interest, taxes, depreciation, and amortization

(EBITDA), the ANOVA yielded a significant main effect for year (F = 7.274, p = 0.001)

but not for category of company nor a year by category of company interaction. The

result was replicated when submitted to a long-term analysis. The long-term analysis

revealed a significant main effect for year (F = 4.455, p = 0.001).

18

To Downsize or Not

[insert figure 6 about here]

Debt Measures

With regards to current ratio, the ANOVA yielded a significant main effect for

year (F = 3.918, p = 0.021) but not for category of company nor a year by category of

company interaction. The long-term analysis revealed no significant main effects or

interaction.

[insert figure 7 about here]

With regards to long-term debt, the ANOVA yielded a significant year by

category of company interaction effect (F = 2.091, p = 0.002) but no main effect for year

or for category of company. This indicated that, between 2009 and 2011, financially

unhealthy downsizers decreased long-term debt, financially healthy downsizers

maintained long-term debt, and regardless of financial health non-downsizers increased

long-term debt. The result changed however when submitted to a long-term analysis.

The long-term analysis revealed a significant main effect for year (F = 5.834, p = 0.000),

indicating that long-term debt trended up a bit when looked at from 2009 through 2014.

However, again, this shifting result was not supported by the partial correlation analysis.

Partial, year-by-year correlations, holding category of company constant showed that

category of company had no effect on the year-by-year relationship of this financial

variable after downsizing.

[insert figure 11 about here]

[insert table 6 about here]

Efficiency Measures

19

To Downsize or Not

With regards to inventory turnover, the ANOVA yielded a significant main effect

for year (F = 13.085, p = 0.000) but not for category of company nor a year by category

of company interaction. The long-term analysis revealed a significant main effect for

year (F = 2.383, p = 0.044).

[insert figure 8 about here]

With regards to revenue per employee, the ANOVA yielded a significant main

effect for year (F = 6.153, p = 0.002) and for category of company (F = 3.248, p = 0.022),

as well as a year by category of company interaction (F = 2.275, p = 0.035). This

indicated that companies that downsized, whether financially healthy or not, showed a

steady increase in revenue per employee through 2011 with the financially unhealthy

downsizers increasing more. However, financially unhealthy companies that nonetheless

did not downsize in 2008 showed a very high growth in revenue per employee. The

result washed out though when submitted to a long-term analysis. The long-term analysis

revealed a significant main effect for year (F = 2.864, p = 0.018), indicating a steady

decline in revenue per employee from 2009 through 2014. But no year by category

interaction, indicating that by 2014 all companies regardless of financial healthy or

downsizing showed decreasing revenue per employee. The short-term analysis was also

not supported by the partial correlation analysis. Partial, year-by-year correlations,

holding category of company constant showed that category of company had no effect on

the year-by-year relationship of this financial variable after downsizing.

[insert figure 9 about here]

[insert table 4 about here]

20

To Downsize or Not

With regards to total asset turnover, the ANOVA yielded a significant main effect

for year (F = 9.836, p = 0.000) but not for category of company nor a year by category of

company interaction. The result changed however when submitted to a long-term

analysis. The long-term analysis revealed a significant main effect for year (F = 2.653, p

= 0.027), indicating a steady increase in total asset turnover from 2009 through 2014.

But the long-term analysis also revealed a year by category interaction (F = 2.035, p =

0.013), indicating that by 2014 all the financially healthy companies whether they

downsized or not showed a large increase in total asset turnover, with financially healthy

downsizers increasing the most. However, the shifting result was not supported by the

partial correlation analysis. Partial, year-by-year correlations, holding category of

company constant showed that category of company had no effect on the year-by-year

relationship of this financial variable after downsizing.

[insert figure 10 about here]

[insert table 5 about here]

Revenue Measure

With regards to total revenue, the ANOVA yielded a significant main effect for

year (F = 20.205, p = 0.000) but not for category of company nor a year by category of

company interaction. The long-term analysis revealed a significant main effect for year

(F = 4.118, p = 0.002).

[insert figure 12 about here]

Market Valuation Measure

Finally, with regards to stock equity, the ANOVA yielded a significant main

effect for year (F = 25.671, p = 0.000) but not for category of company nor a year by

21

To Downsize or Not

category of company interaction. The result changed however when submitted to a long-

term analysis. The long-term analysis revealed a significant main effect for year (F =

7.621, p = 0.000), indicating a steady increase in stock equity from 2009 through 2014.

But the long-term analysis also revealed a trend toward a main effect for category of

company (F = 2.345, p = 0.077), indicating that by 2014 the financially unhealthy

companies that did not downsize had the highest stock equity of all companies, trending

up as all other companies began to fall. However, this shifting result was not supported

by the partial correlation analysis. Partial, year-by-year correlations, holding category of

company constant showed that category of company had no effect on the year-by-year

relationship of this financial variable after downsizing.

[insert figure 13 about here]

[insert table 7 about here]

Table 8 summarizes the results found here.

[insert table 8 about here]

Discussion

Given the disruptive nature of downsizing on many individuals’ lives from the

employees affected (Datta, Guthrie, Basuil & Pandey, 2010), to those that remain in the

downsizing company (Mishra & Speitzer, 1998; Trevor & Nyberg, 2008, Datta, Guthrie,

Basuil & Pandey, 2010), to the larger community within which the downsizing company

is situated (Gombola & Tsetsekos, 1992; Atanassov & Kim, 2009, Datta, Guthrie, Basuil

& Pandey, 2010), one would expect that downsizing would at least meet the financial and

market needs of the company. One would at least expect that the downsizing company,

22

To Downsize or Not

through downsizing, would return from the event financially stronger, continuing to

provide employment, service to customers, and a presence in the community. But the

present research indicates this is not the case. It is not the case that downsizing had an

appreciable impact, positive or negative, on the financial or market condition of the

company that downsized.

Companies that downsized, regardless of financial health preceding the

downsizing, on average, began to rebuild their employee headcount almost immediately.

Within three years of the downsizing the downsized companies, on average, re-built their

employee headcount almost to pre-downsizing levels.

In terms of profitability (profitability ratios – ROE, ROA, and ROI), downsizing

companies did no better, and actually worse in the short-term, than non-downsizing

companies, regardless of the financial health of the companies. The minimal differences

among downsizing and non-downsizing companies observed, washed out in the long run,

over 6 years post-downsizing. Downsizing also had no impact on other measures of

profitability or revenue (EBITDA, Total Revenue) either immediately after the

downsizing (within 3 years) or over the long-term (up to 6 years post-downsizing).

In terms of the companies’ liabilities and ability to meet these liabilities (current

ratio and long-term debt), companies that were suffering financial ill-health and then

downsized did decrease their long-term debt, on average, over 3 years. Downsizing did

not make any difference in a company’s ability to immediately meet its current liabilities,

3 years after the downsizing, or meet its current liabilities for the 6 years after

downsizing. All other companies (financially healthy companies that nonetheless

downsized or non-downsizing companies regardless of financial health) increased their

23

To Downsize or Not

long-term debt over 3 years. Interestingly, those financially unhealthy, downsizing

companies that decreased their long-term debt over the 3 years subsequent to the

downsizing, re-built that debt over the long term, over 6 years.

In terms of efficiency, management efficient (inventory turnover), employee

efficiency (revenue per employee), or asset use efficiency (asset turnover), downsizing

had no impact. On the contrary, those companies that were financially unhealthy but did

not downsize used their employees more efficiently in the short-term, over the next 3

years, but not in the long term, over the entire 6 years, than did financially healthy

companies.

Finally, in terms of market valuation (stock equity), downsizing made no

immediate difference in terms of stockholder investment in the company. However, 5 to

6 years post-downsizing, it was the initially unhealthy companies that nonetheless did not

downsize that showed an increase in stock equity, with all other companies falling. It is

unclear whether this long-term impact was related to the downsizing event and was

simply delayed do to delays in flow of information and decision making by the market or

wholly unrelated to the downsizing and attributed to some other yet undetermined aspect

of the companies 6 years later. The later explanation is more likely given the long-term

changes in stock equity uncovered by the analysis were not supported by partial

correlations.

In summary, downsizing companies replaced their downsized workers almost

immediate. Downsizing did not help profitability either in the short-term or in the long-

term. Downsizing did not help companies meet their current liabilities either in the short-

term or the long-term. Though, downsizing did help companies decrease long-term debt

24

To Downsize or Not

in the short-term. Downsizing did not impact efficiency of either management,

employees, or use of assets. In fact, financially unhealthy companies that nonetheless did

not downsize exhibited an increase in employee efficiency, at least in the short term.

Finally, the market seemed to respond negatively to downsizing in the long-term, only

possibly responding positively to companies that found themselves in financial unhealthy

but nonetheless did not downsize.

These results may not be surprising as the downsizing may be seen as applying a

short-term fix to an otherwise long-term problem. Simply decreasing headcount, while

immediately impacting cost or debt, does not address the underlying financial, market,

industry, and/or strategic issues that, whether explicitly acknowledged or not, led to the

downsizing decision. It is analogous to placing a Band-Aid on an otherwise deeper, more

fundamental wound. Often referred to in medicine, the theory of a “Band-Aid solution”

may explain the ineffectiveness of the downsizing effort. A “Band-Aid solution” in

medical terms is “… any partial or ‘cosmetic’ solution to a problem, often referring to a

treatment that falls far short of that demanded by the disease being treated” (Band-Aid

Solution, n.d.). In this case, downsizing is the partial or cosmetic solution to an

underlying financial, market, industry, or strategic “disease”, falling short of treating the

“disease”.

Limitations and Future Research

Although seemly robust, the findings here do suffer from a few limitations. All

companies included in this data set were on the Fortune 500 list in 2014 and were found

to also have been on the Fortune 500 list in 2008. Therefore, all companies included in

25

To Downsize or Not

this data set, whether suffering from financial ill-health or not, and whether downsizing

or not, were by definition larger, successful companies. And one would expect the

companies to have succeeded from 2008 through 2014. It is unclear from this data, what

impact downsizing might have on non-Fortune 500 companies over the same time span.

Additionally, although used in a number of pervious studies, the measure of

downsizing was somewhat arbitrary, defined as a decrease in employee headcount by 5%.

Would the results look different if a different percent decrease in employee headcount

were used? Some pervious studies have looked at the differences between companies

with relatively small and relatively large downsizing events (DeMeuse, et. al., 2004;

Brauer, 2010) and the size of the decrease in employee headcount does seem to make a

difference. Perhaps using a different percent decrease in employee headcount to define

downsizing would have led to different results here. Or, perhaps looking at absolute size

of headcount change would have led to different results here.

Additionally, like the measure of downsizing, the measure of financial health,

defined as a decrease in cash flow from operations by 5%, may have been artificial.

Alternative percent decreases in cash flow from operations might have been used, or

other financial measures might have been used to determine financial health of these

companies. Typically, studies comparing financially healthy downsizers with financially

unhealthy downsizers look to the companies’ stated reasons for the downsizing as

reported to the SEC and categorize those companies downsizing in response to financial

trouble as reactive downsizers and those companies downsizing in response to market or

industry conditions, merger or acquisition, or consolidation as proactive downsizers

(Worrell, et. al, 1991; Lee, 1997; Chalos & Chen, 2002; Chen, et. al., 2001; Capelle-

26

To Downsize or Not

Blancard & Couder, 2008; Brauer, 2010; Marshall, et. al., 2012). Perhaps using a

different approach to determining financial health would have lead to different results

here.

Finally, the selection of research method and statistical analysis may have limited

the conclusion drawn. More recently researchers looking at downsizing have employed

an event methodology approach: essentially estimating the impact on financial measures

and/or market valuation of the company for several days before, during, and several days

after a downsizing event and looking for normal (estimated) and abnormal (non-

estimated) results. Using this method one can be more confident that the results found

were directly do to the event (downsizing) rather than some other extraneous variable or

variables. However, this pushes one into a cross-section rather than longitudinal design.

In the present research the partial correlation analysis was used in an otherwise

longitudinal approach to try to rule out extraneous variables. However, a direct

comparison of results from an event methodology and the longitudinal approach taken

here would substantiate this use of partial correlation.

Finally, industry was not included as a control variable in this research. The

present study controlled for economic conditions, size of company, and success of

company through the selection of index year and company sample. But others (see for

example, Guthrie & Datta, 2008 and Cagle, et. al., 2009) have noted the impact of

industry on downsizing and financial outcomes or market valuation. Replication of the

present findings controlling for industry would seem important.

Future research might also consider the very interesting case of those companies

that were in financial ill-health but chose not to downsize. What did these companies do

27

To Downsize or Not

as an alternative to downsizing? Additionally, future research could look at the ways in

which the downsizing event is handled and the impact this has on the various

stakeholders in the company as well as the financial and market health of the company.

DeWitt (1998) as well as Trevor and Nyberg (2008) looked at various approaches to

downsizing. Could the practices used to announce and execute the downsizing impact

the effect the downsizing event has on the financial and market health of the

organizations? Could those companies that downsized in the present study show more

positive impact on financial and market health if the downsizing was handled in a

particular way?

Finally, previous studies have considered the size and frequency of downsizing.

However, future research might look at the direct relationship between any change in

headcount (positive or negative), regardless of whether labeled as downsizing, and

financial outcomes. Similarly, future research might look at the direct relationship

between the frequency of headcount change (positive or negative), regardless of whether

these are labeled downsizing, and financial outcomes.

Conclusion

Given the present findings, taking into consideration the limitations of the present

study and future directions for research, what can a senior leader presented with a

potential downsizing event decide? Very simply: don’t downsize. The research here

indicates downsizing will not help. It will be a “Band-Aid” solution, a partial or cosmetic

solution that does not address the underlying financial, market, industry, or strategic

problem that lead to the downsizing decision in the first place. And given the rather

significant impact downsizing can have on various stakeholders, to downsize would seem

28

To Downsize or Not

to be not only counter-productive but perhaps also unethical. So, when in doubt, don’t

downsize.

29

To Downsize or Not

References

Atanassov, J. & Kim, E. H. (2009). Labor and corporate governance: International evidence from restructuring decisions. Journal of Finance, 64 (1), 341-374.

Ballester, M.; Livnat, J.; & Sinha, N. (1999). Corporate reorganizations: Changes in the intensity of labor and capital expenditures. Journal of Business Finance & Accounting, 26 (9), 1205-1238.

Block, S. B. & Hirt, G. A. (2005). Foundations of Financial Management (Eleventh Edition). McGraw Hill: Boston, MA.

Band-Aid Solution. (n.d.) Segen's Medical Dictionary. (2011). Retrieved October 14 2015 from http://medical-dictionary.thefreedictionary.com/Band-Aid+Solution

Bordeman, A.; Kannan, B.; & Pinheiro, R. (2014). Intra-industry contagion effects of layoff announcements, Unpublished Manuscript.

Brauer, M. (2010). The implications of magnitude, timing, & realization of workforce downsizing on firm profitability. Academy of Management Annual Meetings Proceedings, 1-6.

Brookman, J. T.; Chang, S.; & Rennie, C. G. (2007). CEO equity portfolio incentives and layoff decisions. Journal of Financial Research, 30 (2), 259-281.

Cagle, J. A. B.; Sen, A.; & Pawlukiewicz, J. E. (2009). Journal of Economics and Finance, 33 (1), 100-110.

Capelle-Blanchard, G. & Couderc, N. (2007). How do shareholders respond to layoff announcements? A meta-analysis. Unpublished Manuscript.

Cascio, W. F.; Young, C. E.; & Morris, J. R. (1997). Financial consequences of employment-change decisions in major U.S. corporations. Academy of Management Journal, 40 (5), 1175-1189.

Chalos, P. & Chen, C. J. P. (2002). Employee downsizing strategies: Market reaction and post announcement financial performance. Journal of Business Finance & Accounting, 29 (5), 847-870.

Chen, P.; Mehrotra, V.; Sivakumar, R.; & Yu, W. W. (2001). Layoffs, shareholders’ wealth, and corporate performance. Journal of Empirical Finance, 8 (2), 171-199.

Datta, D. K.; Guthrie, J. P.; Basuil, D.; & Pandey, A. (2010). Causes and effects of employee downsizing: A review and synthesis. Journal of Management, 36 (1), 281-348.

30

To Downsize or Not

DeMeuse, K. P.; Bergmann, T. J.; Vanderheiden, P. A.; & Roraff, C. E. (2004). New evidence regarding organizational downsizing and a firm’s financial performance: A long-term analysis. Journal of Managerial Issues, 16 (2), 155-176.

DeMeuse, K. P. & Dai, G. (2013). Organizational downsizing: Its effects on financial performance over time. Journal of Managerial Issues, 25 (4), 324-344.

DeMeuse, K.P.; Vanderheiden, P. A.; & Bergmann, T. J. (1994). Announced layoffs: Their effect on corporate financial performance. Human Resource Management, 33 (4), 509-530.

Dewitt, R. (1998). Firm, industry, and strategy influences on choice of downsizing approach. Strategic Management Journal, 19 (1), 59-79.

Gombola, M. J. & Tsetsekos, G. P. (1992). The information content of plant closing announcements: Evidence from financial profiles and the stock price reaction. Financial Management, 21 (2), 31-40.

Guthrie, J. P. & Datta, D. K. (2008). Dumb and dumber: The impact of downsizing on firm performance as moderated by industry conditions. Organizational Science, 19 (1), 108-123.

Hillier, D.; Marshall, A.; McColgan, P.; & Werema, S. (2007). Employee layoffs, shareholder wealth and firm performance: Evidence from the UK. Journal of Business Finance & Accounting, 34 (3), 467-494.

Lee, P. M. (1997). A comparative analysis of layoff announcements and stock price reactions in the United States and Japan. Strategic Management Journal, 18 (1), 879-894.

Marshall, A. & McColgan, P. (2012). Why do stock prices decline in response to employee layoffs? UK evidence from the 2008 global financial crisis. Journal of Financial Research, 35 (3), 375-396.

Mckinley, W., Zhao, J., & Rust, K. G. (2000). A sociocognitive interpretation of organizational downsizing. Academy of Management Review, 25 (1), 227-243.

Mishra, A. K. & Spreitzer, G. M. (1998). Explaining how survivors respond to downsizing: The roles of trust, empowerment, justice, and work redesign. Academy of Management Review, 23 (3), 567-588.

Trevor, C. O. & Nyberg, A. J. (2008). Keeping your headcount when all about you are losing theirs: downsizing, voluntary turnover rates, and the moderating role of HR practices. Academy of Management Journal, 51 (2), 259-276.

31

To Downsize or Not

Tsai, P. C., & Yen, Y. (2015). Development of institutional downsizing theory: evidence from the MNC downsizing strategy and HRM practices in Taiwan. Total Quality Management & Business Excellence, 26 (3/4), 248-262.

Worrell, D. L.; Davidson, W. N.: & Sharma, V. M. (1991). Layoff announcements and stockholder wealth. Academy of Management Journal, 34 (3), 662-678

32

To Downsize or Not

Figure 1 – Number of Employees

Figure 2 – Cash Flow

33

To Downsize or Not

Figure 3 – Return on Equity (ROE)

Table 1 – Partial Year-by-Year Correlation for Return on Equity (ROE) Holding Category of Company Constant

2010 2011 2012 2013 20142009 0.081 0.368* 0.179 0.208* 0.1802010 0.734* 0.447* 0.439* 0.435*2011 0.643* 0.643* 0.599*2012 0.522* 0.566*2013 0.790** p > 0.05

34

To Downsize or Not

Figure 4 – Return on Assets (ROA)

Table 2 – Partial Year-by-Year Correlation for Return on Assets (ROA) Holding Category of Company Constant

2010 2011 2012 2013 20142009 0.410* 0.523* 0.305* 0.337* 0.280*2010 0.781* 0.552* 0.576* 0.633*2011 0.593* 0.647* 0.649*2012 0.677* 0.683*2013 0.830** p > 0.05

35

To Downsize or Not

Figure 5 – Return on Investment (ROI)

Table 3 – Partial Year-by-Year Correlation for Return on Investments (ROI) Holding Category of Company Constant

2010 2011 2012 2013 20142009 0.534* 0.582* 0.449* 0.383* 0.382*2010 0.849* 0.673* 0.597* 0.633*2011 0.811* 0.736* 0.751*2012 0.782* 0.762*2013 0.859** p > 0.05

36

To Downsize or Not

Figure 6 – Earnings before Interest, Taxes, Depreciation, Amortization

Figure 7 – Current Ratio

37

To Downsize or Not

Figure 8 – Inventory Turnover

38

To Downsize or Not

Figure 9 – Revenue per Employee

Table 4 – Partial Year-by-Year Correlation for Revenue per Employee Holding Category of Company Constant

2010 2011 2012 2013 20142009 1.000* 1.000* 0.999* 0.994* 0.997*2010 0.999* 0.999* 0.996* 0.981*2011 1.000* 0.994* 0.976*2012 0.995* 0.997*2013 0.993** p > 0.05

39

To Downsize or Not

Figure 10 – Total Asset Turnover

Table 5 – Partial Year-by-Year Correlation for Total Asset Turnover Holding Category of Company Constant

2010 2011 2012 2013 20142009 0.986* 0.992* 0.975* 0.899* 0.826*2010 0.996* 0.994* 0.952* 0.899*2011 0.993* 0.939* 0.877*2012 0.971* 0.924*2013 0.983** p > 0.05

40

To Downsize or Not

Figure 11 – Long Term Debt

Table 6 – Partial Year-by-Year Correlation for Long-Term Debt Holding Category of Company Constant

2010 2011 2012 2013 20142009 0.993* 0.966* 0.942* 0.918* 0.873*2010 0.982* 0.963* 0.939* 0.899*2011 0.974* 0.947* 0.917*2012 0.973* 0.942*2013 0.970** p > 0.05

41

To Downsize or Not

Figure 12 – Total Revenue

42

To Downsize or Not

Figure 13 – Stock Equity

Table 7 – Partial Year-by-Year Correlation for Stock Equity Holding Category of Company Constant

2010 2011 2012 2013 20142009 0.987* 0.944* 0.845* 0.848* 0.858*2010 0.980* 0.912* 0.913* 0.917*2011 0.970* 0.967* 0.967*2012 0.996* 0.987*2013 0.994** p > 0.05

43

To Downsize or Not

Table 8 – Summary of Results

Measure Short-Term Effect

Long-Term Effect

Supported by Partial Correlation

ROE Yes No YesROA Yes No NoROI Yes No NoEBITDA No No NoCurrent Ratio No No NoLong-Term Debt Yes No NoInventory Turnover No No NoRevenue Per Employee Yes No NoAsset Turnover No Yes NoTotal Revenue No No NoStock Equity No Yes No

44

To Downsize or Not

Table 9 – Summary of Literature Review

45

To Downsize or Not

Table 10 – Sample Size by Category of Company

46

To Downsize or Not

Graphic 1 – Research Model

47