Embed Size (px)

Citation preview

CEE INGS

Twenty-sixth Annual Meeting

Theme:

"Markets and Management in an Era ofDeregulation"

November 13-15, 1985

Amelia Island PlantationJacksonville, Florida

Volume XXVI Number 1 1985

TRANSPORTATION RESEARCH FORUMIn conjunction with

4 CANADIAN TRANSPORTATIONRESEARCH FORM

58 CANADIAN TRANSPORTATION RESEARCH FORUM

Ownership and Control in Shipping:Problems in Developing Nations

By Mary R. Brooks*

ABSTRACT

In the early 1970s the United Nations called forthe development of a New International EconomicOrder and the redistribution of world wealth throughfor example greater participation by developing na-tions in international shipping. Although interna-tional conventions, such as the UNCTAD LinerCode of Conduct, provide the means by which de-veloping countries can increase their share of theshipping pie, many nations are introducing addi-tional national legislation designed to promote fleetdevelopment even further, particularly as fleet regis-try does not necessarily imply control.

This paper reviews fleet ownership and control,examining the extent of public and private sectorownership in the ASEAN countries of Singapore,Malaysia, Thailand, Indonesia, and the Philippines.Other mechanisms designed too increase control,such as the formation of shippers' councils and na-tional legislation, will also be discussed, as will theability of such countries to engage in increased ship-ping control. The author will draw conclusions onthe future control of shipping exerted by developingnations in general.

I. AN HISTORICAL OVERVIEW

International shipping, for the ASEAN countries,has been dominated for years by companies head-quartered in the developed world, largely due to thecolonial status held by many of these countries untilrecent years. Dutch control of shipping in andaround the Dutch East Indies, now Indonesia, wasnot severed until after World War II. Malaysia didnot achieve independence from Britain until 1957and, although the State of Singapore came into beingin June of 1959, Singapore did not gain completeindependence from Britain until 1965. AlthoughThailand was never colonised, it has never had astrong fleet of its own. Of all these countries, thePhilippines, which won independence from theUnited States in 1946, has had a strong privatesector in domestic shipping and a steadily growingnational flag fleet throughout the 1950s and 1960s.The efforts of the ASEAN nations to gain greater

control over international shipping are based on therationale that the benefits which accrue to the car-rier—foreign exchange generation, employment fornationals, the development of spin-off industries,etc.—should accrue, in some measure, to the cargo

* Associate Professor of Marketing and Transporta-tion, School of Business Administration, and aResearch Associate of the Canadian MarineTransportation Centre, both at Dalhousie Univer-sity, Halifax, Canada.

generator. It is this philosophy coupled with thepolitical diversity of the ASEAN region which hasled to a variety in the efforts made to gain control ofshipping.

Historically, cargo control and national flag fleetpromotion have been suggested as solutions to theproblems of freight rate costs and shipping control.Yeats, in his study of shipping and national develop-ment, concluded that "shipping costs may pose a farmore important barrier to developing country ex-ports than current MFN [Most Favored Nation] tar-iffs."' One of the institutional solutions that he pro-poses for such disparities is national fleet develop-ment.

In the late 1960s Singapore and Malaysia believedthat their trade was being strangled by the Far East-ern Freight Conference (FEFC), and this belief wasreinforced by the continuing European chairmanshipof the conference.' By developing national flag linerservices which could operate within the conferencestructure, both Singapore and Malaysia had hoped tobe able to influence conference pricing and service.The admission of Neptune Orient Line (NOL), thenational line of Singapore, and the Malaysian Inter-national Shipping corporation (MISC), Malaysia'snational line, to the FEFC appears to have had littleinfluence on the continued dominance of the FEFCby its European founding members. The conferencehas retained its reputation for toughness in its deal-ings with shippers, and it is questionable whetherconference membership by developing countries hasbenefitted their shippers or not; of the 33 membersof the FEFC, those companies affiliated with devel-oping or newly industrialized countries still form aminority.'Chia and Lim, in their study of Southeast Asian

shipping, conclude that:

"The ability of the liner conferences to maintainand in fact to continue to increase freight rates inthe face of strong objections by shippers demon-strates the firm hold on the liner trade by theconferences to the chagrin of ASEAN shippersand governments."4

But first, let's examine the extent of public sectorownership and participation in ASEAN the nationalflag shipping.

II. GOVERNMENT PARTICIPATION

A. Singapore and Malaysia

In Singapore, the promotion of national flag ship-ping was undertaken by two means: the opening ofthe register to foreign shipowners and the develop-ment of a national flag line, NOL, supported bypublic funds. It was hoped that both would increase

OWNERSHIP AND CONTROL IN SHIPPING 59

the measure of control exerted by Singaporeans andprovide an effective means of gaining Singaporeanexpertise in shipping.

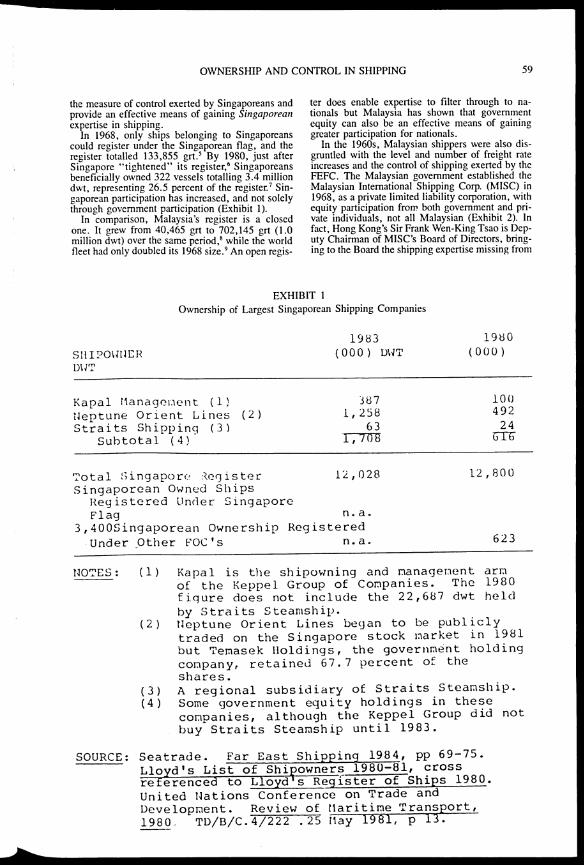

In 1968, only ships belonging to Singaporeanscould register under the Singaporean flag, and theregister totalled 133,855 grt.5 By 1980, just afterSingapore "tightened" its register,' Singaporeansbeneficially owned 322 vessels totalling 3.4 milliondwt, representing 26.5 percent of the register.' Sin-gaporean participation has increased, and not solelythrough government participation (Exhibit 1).

In comparison, Malaysia's register is a closedone. It grew from 40,465 grt to 702,145 grt (1.0million dwt) over the same period,' while the worldfleet had only doubled its 1968 size.' An open regis-

SHIPOWNER

DWT

ter does enable expertise to filter through to na-tionals but Malaysia has shown that governmentequity can also be an effective means of gaininggreater participation for nationals.

In the 1960s, Malaysian shippers were also dis-gruntled with the level and number of freight rateincreases and the control of shipping exerted by theFEFC. The Malaysian government established theMalaysian International Shipping Corp. (MISC) in1968, as a private limited liability corporation, withequity participation from both government and pri-vate individuals, not all Malaysian (Exhibit 2). Infact, Hong Kong's Sir Frank Wen-King Tsao is Dep-uty Chairman of MISC's Board of Directors, bring-ing to the Board the shipping expertise missing from

EXHIBIT 1

Ownership of Largest Singaporean Shipping Companies

1983(000) DWT

1980

(000)

Kapal Management (1)Neptune Orient Lines (2)Straits Shipping (3)

Subtotal (4)

3871,258

63 1,-708

10049224GTE-

Total Singapore IZegisterSingaporean Owned Ships

Registered Under SingaporeFlag n.a.

3,400Singaporean Ownership Registered

-UnderPther FOC's n.a.

12,028 12,800

623

NOTES: (1)

(2)

(3)(4)

Kapal is the shipowning and management arm

of the Keppel Group of Companies. The 1980

figure does not include the 22,687 dwt held

by Straits Steamship.Neptune Orient Lines began to be publicly

traded on the Singapore stock market in 1981

but Temasek Holdings, the government holding

company, retained 67.7 percent of the

shares.A regional subsidiary of Straits Steamship.

Some government equity holdings in these

companies, although the Keppel Group did not

buy Straits Steamship until 1983.

SOURCE: Seatrade. Far East Shipping 1984, pp 69-75.

Lloyd's List of Shipowners 1980-81, cross

referenced to Lloyd's Register of Ships 1980.

United Nations Conference on Trade and

Development. Review of Haritime Transport,

1980. TD/B/C.4/222 .25 May 1981, p 13.

60 CANADIAN TRANSPORTATION RESEARCH FORUM

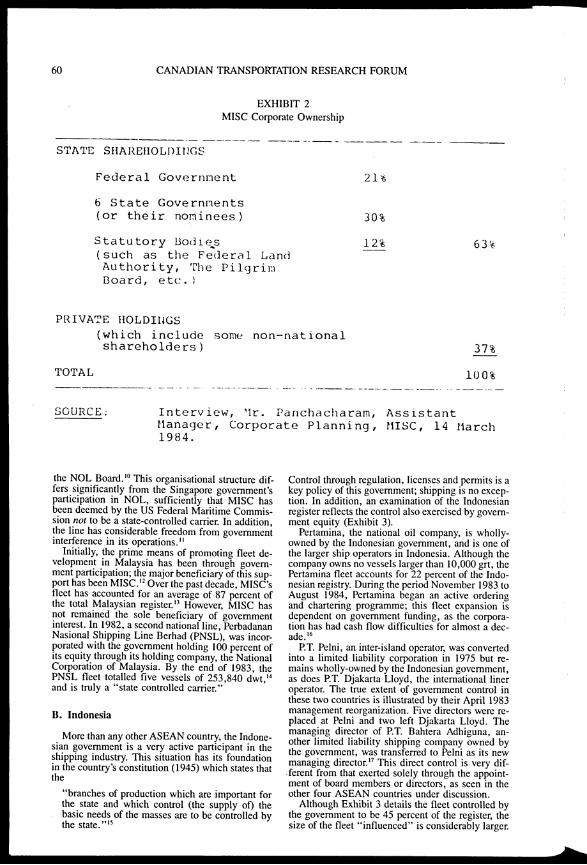

EXHIBIT 2MISC Corporate Ownership

STATE SIIAREIIOLDITIGS

Federal Government 21t

6 State Governments(or their nominees) 30%

Statutory Bodies 12%(such as the Federal LandAuthority, The PilgrimBoard, etc.)

PRIVATE HOLDINGS

(which include some non-nationalshareholders)

TOTAL

SOURCE;

63%

37%

10 0 %

Interview, "Ir. Panchacharam, AssistantManager, Corporate Planning, MISC, 14 March1984.

the NOL Board.' This organisational structure dif-fers significantly from the Singapore government'sparticipation in NOL, sufficiently that MISC hasbeen deemed by the US Federal Maritime Commis-sion not to be a state-controlled carrier. In addition,the line has considerable freedom from governmentinterference in its operations."

Initially, the prime means of promoting fleet de-velopment in Malaysia has been through govern-ment participation; the major beneficiary of this sup-port has been MISC.' Over the past decade, MISC'sfleet has accounted for an average of 87 percent ofthe total Malaysian register." However, MISC hasnot remained the sole beneficiary of governmentinterest. In 1982, a second national line, PerbadananNasional Shipping Line Berhad (PNSL), was incor-porated with the government holding 100 percent ofits equity through its holding company, the NationalCorporation of Malaysia. By the end of 1983, thePNSL fleet totalled five vessels of 253,840 dwt,"and is truly a "state controlled carrier."

B. Indonesia

More than any other ASEAN country, the Indone-sian government is a very active participant in theshipping industry. This situation has its foundationin the country's constitution (1945) which states thatthe

"branches of production which are important forthe state and which control (the supply of) thebasic needs of the masses are to be controlled bythe state. "15

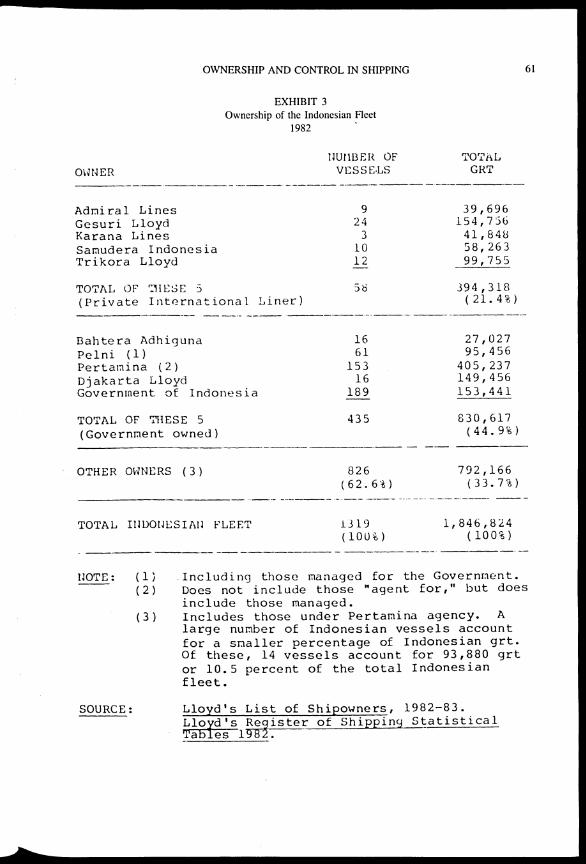

Control through regulation, licenses and permits is akey policy of this government; shipping is no excep-tion. In addition, an examination of the Indonesianregister reflects the control also exercised by govern-ment equity (Exhibit 3).

Pertamina, the national oil company, is wholly-owned by the Indonesian government, and is one ofthe larger ship operators in Indonesia. Although thecompany owns no vessels larger than 10,000 grt, thePertamina fleet accounts for 22 percent of the Indo-nesian registry. During the period November 1983 toAugust 1984, Pertamina began an active orderingand chartering programme; this fleet expansion isdependent on government funding, as the corpora-tion has had cash flow difficulties for almost a dec-ade.'

P.T. Pelni, an inter-island operator, was convertedinto a limited liability corporation in 1975 but re-mains wholly-owned by the Indonesian government,as does P.T. Djakarta Lloyd, the international lineroperator. The true extent of government control inthese two countries is illustrated by their April 1983management reorganization. Five directors were re-placed at Pelni and two left Djakarta Lloyd. Themanaging director of RT. Bahtera Adhiguna, an-other limited liability shipping company owned bythe government, was transferred to Pelni as its newmanaging director." This direct control is very dif-ferent from that exerted solely through the appoint-ment of board members or directors, as seen in theother four ASEAN countries under discussion.

Although Exhibit 3 details the fleet controlled bythe government to be 45 percent of the register, thesize of the fleet "influenced" is considerably larger.

OWNER

OWNERSHIP AND CONTROL IN SHIPPING 61

Admiral LinesGesuri LloydKarana LinesSamudera IndonesiaTrikora Lloyd

EXHIBIT 3Ownership of the Indonesian Fleet

1982

NUMER OFVESSELS

92431012

TOTAL OF THESE 3 58

(Private International Liner)

Bahtera Adhiguna 16

Pelni (1) 61

Pertamina (2) 153

Djakarta Lloyd 16

Government of Indonesia 189

TOTAL OF THESE 5 435

(Government owned)

OTHER OWNERS (3)

TOTAL INDONESIAN FLEET

826(62.6%)

1319(100%)

TOTALGRT

39,696154,73641,84858,26399,755

394,318(21.4%)

27,02795,456

405,237149,456153,441

830,617(44.9%)

792,166(33.7%)

1,846,824(100%)

NOTE: (1) Including those managed for the Government.

(2) Does not include those "agent for," but does

include those managed.

(3) Includes those under Pertamina agency. A

large number of Indonesian vessels account

for a smaller percentage of Indonesian grt.Of these, 14 vessels account for 93,880 grt

or 10.5 percent of the total Indonesian

fleet.

SOURCE: Lloyd's List of Shipowners, 1982-83.

Lloyd's Register of Shipping Statistical Tables 1982.

62 CANADIAN TRANSPORTATION RESEARCH FORUM

The big five private liner operators account for 21percent of the national flag fleet but their operationson the largest routes are rationalized with those ofthe state-owned Djakarta Lloyd. The governmentalso has tremendous influence on the day-to-dayoperating decisions of the privately-owned fleetthrough its decrees, regulatory policy and numerouslicensing requirements. Some of these cobwebs werecleared away when, recently, the government elimi-nated 17 of the licenses required in the inter-islandtrades," but licensing remains a major control mech-anism for the government. Perhaps it is to avoidgovernment influence in operations that Indonesianshipowners registered almost 1.2 million dwt (75vessels) under flags of convenience in 1980.'

C. The Philippines and Thailand

Although the Philippines has cargo-sharing phi-losophies in common with Indonesia, the Philip-pines has relied less on government participation inshipping than most of her ASEAN partners, prefer-ring to leave shipping development to the privatesector. In fact, many of the large shipowning corpo-rations do not register their vessels solely under thePhilippine flag, but operate under joint registry(with Panama). However, this is not to say that therehas been no government participation, although suchparticipation has been limited, and limited to the

OWNER

past decade. The oil crisis of 1973 forced govern-ment involvement in PNOC Shipping and TransportCorporation, a subsidiary of the state-owned Philip-pine National Oil Company. PNOC Shipping andTransport Corporation, in spite of working capitaland foreign exchange difficulties, has managed tooperate as any other private sector shipping com-pany;' its methods of financing and its investmentstrategies reinforce the private sector orientation ofPhilippine government.

In recent years, this orientation has been moredifficult for the government to maintain. Government involvement has reluctant, reacting to the fi-nancial difficulties of major operators. In 1982, thePhilippine International Shipping Corporation(PISC) defaulted on loans and interest of 600 millionpesos and the Philippine National Bank (govern-ment-owned) was forced to attach all six of its bulkcarriers (249,744 grt); PISC was liquidated. GalleonShipping, a private joint venture, was also on theroad to bankruptcy when, in August 1981, the Na-tional Development Corporation (NDC), a govern-ment controlled holding company, took over Gal-leon Shipping, installed a new management team,and renamed the company National Galleon Ship-ping Corporation in April 1982.2' Direct governmentparticipation in shipping is currently limited (Exhibit4) to its holdings in National Galleon and PNOCShipping and Transport.Government equity in Thailand is limited; two

government-owned carriers, Thai Maritime Naviga-

EXHIBIT 4Ownership of the Philippine Fleet

1983

'TIMBER OFVESSELS

TOTALGRT

National Galleon 6

Philippine InternationalShipping Corp. (1) 6

PNOC Shippimj and TransportCompany

TOTAL GOVERNMENT OWNERSHIP

% OF TOTAL FLEET

PHILIPPINE REGISTER

11

23

2.6%

8b4

78,809

249,774

339,776

668,359

22.5%

2,964 k

NOTE: (1) Company bankrupt; ships atPhilippine National Bank d

SOURCE: Lloyd's List of Shipowners Lloyd's Register of ShippiTables 1983.

tached by theuring 1983.

, 1983-84 andn9 Statistical

OWNERSHIP AND CONTROL IN SHIPPING 63

tion Company (TMNC) and United Thai ShippingCompany (Unithai), only owns 9 ships of the total1983 Thai fleet of 148 vessels. The governmentequity in the former is greater (99 percent) than inthe latter (33 percent). Seatrade's Far East Shipping1984 indicates, however, that four more companies,Jutha Maritime Co. Ltd., Thai Petroleum TransportCo. Ltd., Jalaprathan Cement Co. Ltd. and Van-akarn Co. Ltd., are state-owned (the equity percent-age in each is not indicated) bringing the govern-ment total to 20 ships, totalling 142,735 dwt, or 21percent of the fleet."

In future, the government plans to expand theThai fleet through new acquisitions by TMNC,23with the intention of increasing Thai participation inthe carriage of her foreign trade, but has indicatedthat further development of the fleet through govern-ment equity in new companies is unlikely in theshort-term.'

D. Commentary

The ASEAN countries are not the only ones em-barking on a course of fleet development andgrowth; newspapers and trade journals announce thenew plans of many developing nations on a regularbasis. In the traditional shipowning countries, how-ever, government participation in the industry hasbeen very low; these governments have tended toleave shipping as a private sector industry and placegreater emphasis on its regulation. The relationshipbetween the industry and government has generallyfocussed on those measures intended to insure acompetitive and efficient world market for shippingservices. Government response has generally notbeen participatory, although it has played the role of"godfather" on occasion, promoting shipping in-vestment through fiscal benefits.

III. MECHANISMS FOR CONTROL

We have already seen the extent of public sectorownership in the shipping development of each ofthe five ASEAN countries. This development hasbeen supported by government policies, such ascabotage, fiscal incentives and cargo-sharing. How-ever, registration of a national flag fleet does notnecessarily imply control, and governments havesought alternate methods of increasing national con-trol by, for example, mechanisms designed to shiftnegotiating power from the carrier (often foreign) tothe shipper (a national).To counter the power of the conferences serving

the area, strong shippers' councils are consideredessential. Co-operation between shippers' councilswas formalized with the establishment of the Federa-tion of ASEAN Shippers' Councils (FASC) in Ma-nila in October of 1974. Mr. Warut Siwasariyanon,in his thesis on ASEAN shipping costs, concludesthat the FASC has not been influential in preventingthe frequent FEFC rate increases.' The Federationcontinues to complain of problems encountered byASEAN shippers in their dealings with the FEFC,calling the conference "intransigent."" •

In addition to the formation of shipper's councils,umbrella organizations, such as Thailand's Office ofthe Merchantile Marine Promotion Commission,have been established to develop a co-ordinated na-

tional shipping policy; Indonesia and the Philippineshave given the Directorate of Sea Communicationsand Maritime Industry Authority (MARINA), re-spectively, similar mandates. These agencies pro-vide a means of potential government control overprivate sector activity. MARINA, for example, candirect investment through the allocation of foreignexchange providing a measure of government con-trol over private sector investment in ships.The development of cargo affreightment/consol-

idation agencies and the establishment of freightstudy units have also been touted as the means tocounter conference strength. The former enablesshippers to negotiate from a position of strength;sufficient cargo may even lead to the ability tocharter vessels and bypass the conference structurealtogether. Through Malaysia's new Freight BookingCentre, it is anticipated that Malaysians will controlcarrier selection for 70-75 percent of Malaysia'sexports.' On the other hand, freight study unitsprovide the information necessary for successful ne-gotiation: the volume, seasonality and vagaries ofcargo flows into and out of a particular country.However enthusiastic the individual ASEAN coun-tries are about such units, data collection problemshave been encountered, and so their impact can notbe readily assessed.

Recently the strength of the FEFC has dwindledslightly. This situation has been caused by the in-creasing incursion of non-ASEAN non-conferencecarriers into the traditional conference-dominatedtrades. Therefore, control of conference shipping, asexemplified by the FEFC, has not shifted from Eu-ropean hands due to the presence of NOL, MISC orUnithai within the conference or from pressure ex-erted by shippers' councils. The shift to a shipperorientation has been attributed to non-conferencepressure by outsiders, such as Taiwan's Evergreenline.

IV. FACTORS WHICH ASSIST OR HINDERTHE INVESTMENT IN CONTROL

Finally, the ability to gain increased control ofshipping through government measures designed topromote private sector investment in shipping is tiedto the ability of companies to engage in such invest-ment.

First of all, there is the ability of companies toconsider any form of expansion whatsoever. Givensuitable market conditions, companies consideringexpansion must be financially capable of weatheringshort-term losses until the revenue generated by theinvestment is sufficient to counter the capital repay-ments and operating expenses of the investment. Ofthe largest Filipino shipping corporations, the Mar-itime Company of the Philippines (MCP) is the mostable to meet its debts (liquidity) and is one of themore profitable," but this company withdrew fromoperations during 1984 because it was incapable ofmeeting its financial obligations. Consider the abil-ity of the balance of the Philippine fleet to undertakeexpansion.

Assuming a particular company has acceptableliquidity and profitability, the ability to raise funds(with or without government guarantees) in the mar-ketplace is also important arises. There are twomajor commercial sources of funds available toshipowners: equity markets (where an infusion of

64 CANADIAN TRANSPORTATION RESEARCH FORUM

funds can be garnered from private investors throughthe sale of shares) and commercial lending institu-tions. The ability to use the latter depends verymuch on the individual company's ability to supportadditional debt, unless government guaranteeswaive this requirement, as has been the case withMISC.One measure of the debt capacity of the shipping

company is the debt/total assets (or gearing) ratio.The greater the level of capitalization of a company,the less reliance the company must place on banksand other lenders and, generally, the lower theamount of operating profit which must be used tocover interest payments on the debt incurred by thecompany. Too much reliance on equity, and thecompany is not taking advantage of leverage pos-sibilities to ensure its survival. This is not usuallythe problem. Throughout Thailand, Malaysia, Indo-nesia and the Philippines are numerous under-capitalized, bankrupt shipping companies. Only theSingaporean companies have maintained the abilityto seek commercial funding for expansion activities.

In addition to borrowing funds for expansion,shipping companies can interest private investors infinancing expansion through acquiring shares in thecorporation. This option is available only wheregovernment restrictions on this particular source ofcapital permit, and when existing shareholders arenot adverse to the dilution of their shares. For exam-ple, NOL was recently forced to raise funds througha rights issue of unsecured loan stock as TemasekHoldings (the government holding company) wouldnot allow its shareholding to be diluted by a shareissue."

Therefore, the strength of local capital marketscan abet or hamper a company's ability to takeadvantage of government measures or market oppor-tunities. Singapore's stock exchange has seen privateinvestor support for shipping,' whereas the stockmarkets of Thailand, Indonesia and the Philippinesall have problems. The Stock Exchange of Thailandis a poor equity market, with little hope for improve-ment in either the short- or medium-term.' Indo-nesia is faced with a similar situation,' and Malay-sia has not managed to counter difficulties withstock market manipulation.

Indonesia and the Philippines are also faced withsevere currency exchange limitations which preventfleet expansion in spite of cargo reservation legisla-tion to support such fleet growth. Such cargo reser-vation can only be effective if the beneficiaries areable to develop the capacity to carry their share. Inispite of cargo reservation legislation, Filipino oper-ators were unable to take advantage of this legisla-tion in the Philippines/US trades in 1983, because ofan inability to finance the necessary expansion. Thesuccess of legislation to increase participation inshipping is tied to the ability to finance the expan-sion.

Finally, countries may resort, as Indonesia hasdone, to financing fleet expansion through govern-ment budgetary means. However, such expansionmust be absorbable by the market. Financing aloneis inadequate; market demand must exist. The mostpopular means of achieving this has been cargoreservation, the success of which is tied to the politi-cal reactions of one's trading partners, and the abil-ity to increase capacity as required. In ASEAN over-capacity exists; load factors average only 60 per-cent,33 when 80 percent is more acceptable level for

efficient and profitable operations. Perhaps cargoreservation will solve this difficulty but time must begiven to allow current excess capacity to be ab-sorbed.

V. CONCLUSIONS

Future economic growth in ASEAN is not ex-pected to equal historical growth rates and the cur-rent rate of fleet expansion is questionable ifsubstantial additional cargo is not generated. With-out a strong capital market like Singapore's, andwithout sufficient company strength to generate cap-ital from commercial banks, fleet expansion formany ASEAN companies will need to continue to besupported by government funds. In the case ofThailand, these funds are needed for the economicdevelopment projects currently planned, and it isunlikely that fleet development will be any morerapid than its recent pace. The inability of manyIndonesian or Filipino companies to purchase shipsfrom international shipyards, because of currencyproblems, suggest limited growth in private sectorshipping for these two as well. The influence ofgovernment in shipping will grow if these govern-ments are determined to achieve national objectives.With chronic overcapacity and current load factors,the region's existing direction of fleet expansion is aquestionable strategy likely to result in greater debt,not greater wealth.The experience of the ASEAN countries is typical

of many developing and newly industrialized econo-mies; traditional developed country shipowners,who are flagging out for tax benefits or to avoid thehigh labour costs, are retaining operating control. Soin spite of all efforts being made by developingnations to promote greater control over shipping,they are hampered by financial difficulties andchronic industry overcapacity. Therefore, the institu-tional solutions currently being attempted will take along time to change the balance of control.

ENDNOTES

1. Alexander J. Yeats, Shipping and DevelopmentPolicy: An Integrated Assessment, New York:Praeger Press, 1981, p 74.

2. Eric Jennings, Cargoes: A Centenary Story ofthe Far Eastern Freight Conference, Singapore:Meridien Communications Pte Ltd., 1980, p57.

3. Ibid., p 694. Chia Lin Sien and Teresa Lim, "Shipping De-

velopment in ASEAN: Problems and Pros-pects" in Southeast Asian Seas—Frontiers forDevelopment, Chia Lin Sien and Colin MacAndrews, eds., McGraw-Hill, 1983, p 181.

5. Lloyd's Register of Shipping Statistical Tables.6. The new registry rules included age limits and

full disclosure of beneficial ownership.7. United Nations (UNCTAD), Review of Mar-

itime Transport 1980, TD/B/C.4/222, 25 May1981, p 13.

8. Lloyd's Register of Shipping Statistical Tables.9. Ibid.

10. 'bid, compared with figures provided in Misc: ACorporate Insight, a company publicity bro-chure.

OWNERSHIP AND CONTROL IN SHIPPING 65

11. Ibid.12. Based on a review of the Board of Directors of

Neptune Orient Lines as provided in the 1983company publicity brochure, The Trident Serv-ice, p 6.

13. Shipping Times, 5 January 1984, p I; Con-tainerisation International, February 1984, p33 and April 1984, p 9.

14. Shipping Times, 4 April 1984, p I.15. Robert C. Rice's translation as quoted in Robert

C. Rice, "The Origins of Basic Economic Ideasand their Impact on 'New Order' Policies" inBulletin of Indonesian Economic Studies, Au-gust 1983, p 61.

16. Business International, Investing, Licensingand Trading (Indonesia), August 1983, p 1;Lloyd's List, 14 August 1984, p 3 and 24 Au-gust 1984, p 1.

17. Cargonews Asia, April 1983, p 2.18. Business Asia, 27 April 1984, p 136.19. UNCTAD, Op Cit.20. Based on operating information supplied by Mr.

E.F. Verano, Vice President and General Man-ager, PNOC Shipping and Transport Corpora-tion, Manila, Philippines.

21. Containerisation International, September1983, p 59.

22. Based on detailed fleet statistics provided by heSea Transport Economics Division of the Mer-chantile Marine Promotion Commission,Bangkok, Thailand.

23. Maritime Asia, November 1981, p 49.24. Government interest has waned because private

sector support is not forthcoming. Asian Ship-ping, January 1983, p 3.

25. Warut Siwasariyanon, The Incidence of Ship-ping Costs in ASEAN International Trade,M.Ec. Thesis: Thammasat University,Bangkok, 1981, p 125.

26. Lloyd's List, 20 August 1984, p 1 and 21 Au-gust 1984, p 1.

27. Shipping Times, 1 February 1984, p1; MaritimeAsia, March 1984, p 7.

28. SEC Businessday's 1000 Top Corporations in

the Philippines, Quezon City: BusinessdayCorp., 1980.

29. Containerization International, February 1984,

pp 31-3.30. Both in the NOL public offering and more re-

cently in the listing of Chuan Hup Marine.(Seatrade, Far East Shipping 1984, p 69).

31. Business Asia, 4 May 1984, p 143.32. Business Asia, 1 June 1984, p 175.33. Maritime Asia, March 1981, p 18.

This paper has been developed from materials col-

lected for a forthcoming monograph by Mary R.

Brooks entitled, "Fleet Development and the Con-

trol of Shipping in Southeast Asia", to be published

by the Publications Unit of the Institute of Southeast

Asian Studies, Heng Mui Keng Terrace, Pasir Pan-

jang, Singapore 0511 in the fall of 1985.