Embed Size (px)

Citation preview

Kepada Yth. Bapak/Ibu :

• Pimpinan/Sales Kantor Cabang PT. Phillip Securities Indonesia • Sales PT. Phillip Securities Indonesia • Nasabah PT. Phillip Securities Indonesia

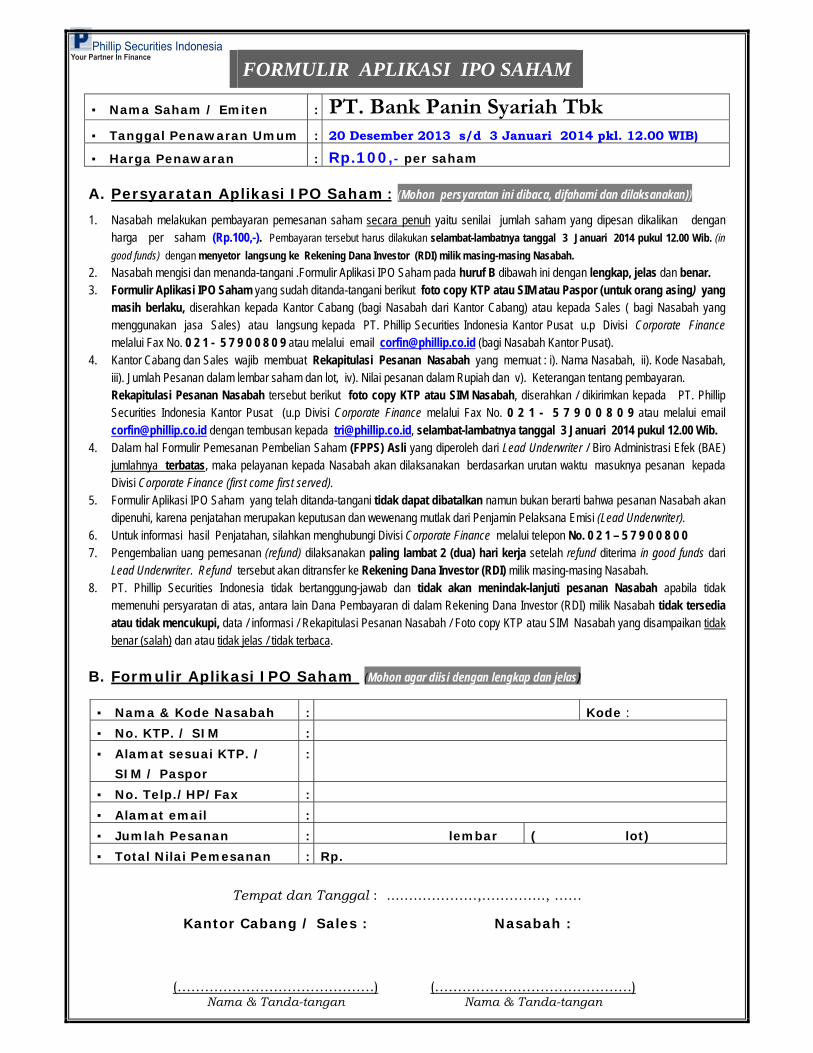

di- Tempat =========================================================================================== Dengan hormat kami informasikan bahwa Penawaran Umum Perdana (Initial Public Offering / IPO) Saham PT. Bank Panin Syariah Tbk., akan dilaksanakan pada tanggal 2 - 8 Januari 2014. Sehubungan dengan hal tersebut, terlampir kami sampaikan :

• Formulir Aplikasi IPO Saham • Materi Presentasi Pada Acara Due Diligence Meeting & Public Expose (DDM

& PE) • IPO Report (Buku Riset) dari PT. Bank Panin Syariah Tbk dimaksud.

Selanjutnya, perkenankan kami menyampaikan hal-hal sbb. :

• Penawaran Umum Perdana (IPO) Saham tersebut di Phillip Securities Indonesia sudah dapat dimulai sejak tanggal 20 Desember 2013, tetapi dibatasi hanya sampai dengan tanggal 3 Januari 2014 pukul 12.00 WIB.

• Harga Penawaran Umum adalah Rp.100,- setiap saham • Tanggal Listing di Bursa Efek Indonesia (BEI) : 15 Januari 2014. • Bapak/Ibu Nasabah yang berminat memesan saham tersebut, silahkan

mengisi Formulir Aplikasi IPO Saham terlampir dengan membaca secara seksama, memahami dan melaksanakan semua ketentuan dan tata-cara yang tercantum di dalam Formulir tersebut.

Catatan : Formulir Aplikasi IPO Saham ini , juga dapat diunduh dari www.poems.co.id Demikian informasi ini kami sampaikan, atas pengertian dan kerja-sama yang baik dari Bapak/Ibu, kami ucapkan terima kasih. Best Regards, M. N a b a b a n Corporate Finance Division PT. Phillip Securit ies Indonesia Telp. : (021) 57900800 Ext. 148 Fax : (021) 57900809 Mobile : 0811810732 Email : [email protected]

PT Evergreen Capital

DUE DILIGENCE MEETING & PUBLIC EXPOSEPENAWARAN UMUM PERDANA SAHAM TAHUN 2013

Materi Presentasi

Penjamin Pelaksana Emisi Efek

PT BANK PANIN SYARIAH Tbk

Jakarta, 2 Desember 2013Assembly Hall – Plaza Bapindo Lt.9

2

Selayang Pandang 3 Operasional Perbankan 14Kinerja Keuangan 22Struktur Penawaran 26Pertimbangan Investasi 30Lampiran 32

2

Daftar Isi

Selayang Pandang

4 4

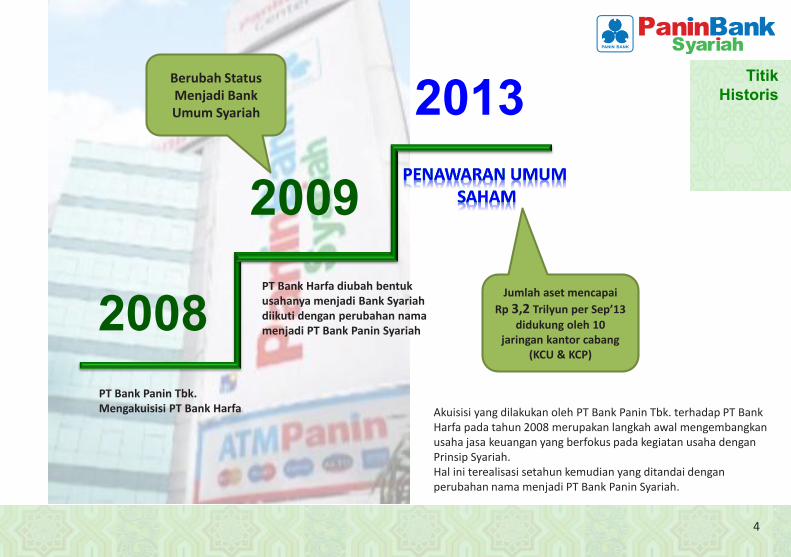

2008PT Bank Panin Tbk. Mengakuisisi PT Bank Harfa

PT Bank Harfa diubah bentuk usahanya menjadi Bank Syariah diikuti dengan perubahan nama menjadi PT Bank Panin Syariah

Berubah Status Menjadi Bank Umum Syariah

Jumlah aset mencapai Rp 3,2 Trilyun per Sep’13

didukung oleh 10 jaringan kantor cabang

(KCU & KCP)

2009

2013

Akuisisi yang dilakukan oleh PT Bank Panin Tbk. terhadap PT Bank Harfa pada tahun 2008 merupakan langkah awal mengembangkan usaha jasa keuangan yang berfokus pada kegiatan usaha dengan Prinsip Syariah. Hal ini terealisasi setahun kemudian yang ditandai dengan perubahan nama menjadi PT Bank Panin Syariah.

Titik Historis

5

“Menjadi Bank Ritel yang Amanah,Bertanggungjawab dan Membawa Berkah bagi

Masyarakat”

5

Mewujudkan layanan keuangan Syariah secara profesional, amanah dan bertanggung jawab

Memberikan produk dan layanan dengan standar terbaik sesuai kebutuhan nasabah

Menjalin hubungan muamalah yang saling menguntungkan dan profesional dengan seluruh Stakeholder

Menumbuhkan dan menjaga pertumbuhan usaha Bank yang sehat.

Visi – Misi

66

Dewan Komisaris

Aries Muftie Komisaris Utama

Independen

Jasman Ginting Munthe Komisaris

Yumirati Kartina Komisaris Independen

Dewan Pengawas Syariah

Berpengalaman selama hampir 30 tahun dalam

dunia perbankan. Pernah menjabat sebagai Direktur pada Bank Muamalat dan

PNM

Berpengalaman selama hampir 23 tahun di

perbankan. Saat ini juga menjabat sebagai Corporate

Secretary PT Bank Panin

Memiliki pengalaman selama hampir 25 tahun di

perbankan. Pernah menjabat sebagai Asisten Direktur Bank Muamalat

DR. KH. Ahmad Munif Suratmaputra, MA. Ketua Dewan Pengawas Syariah

Drs. H. Aminudin Yakub, MA. Anggota Dewan Pengawas Syariah

Memulai karir dalam dunia pendidikan Islam pada tahun 1982 dengan posisi terakhir

sebagai Sekretaris Rektor IIQ. Saat ini juga menjabat sebagai Anggota Komisi Fatwa MUI dan Dewan Pengawas Syariah untuk

Trust Finance, BPRS Wakalumi dan Asuransi Bintang (Unit Syariah)

Memulai karir dalam dunia pendidikan Islam pada tahun 1997. Saat ini juga menjabat sebagai Dewan Pengawas

Syariah untuk Citibank Custodian dan FIF.

Dewan Komisaris

& Dewan

Pengawas Syariah

7 7

Deny Hendrawati Direktur Utama

Hadi Purnomo Direktur

Budi Prakoso Direktur

Tri Bhakti Irianto Direktur

Dewan Direksi

Berpengalaman selama 23 tahun di industri perbankan.

Bergabung pada tahun 2010 sebagai

Direktur Bisnis

Berpengalaman selama 22 tahun di industri

perbankan Pernah menjabat sebagai

Corporate & Investment Banking Head di Bank

Syariah Mandiri. Bergabung pada bulan

Februari 2013 sebagai GM Bisnis

Berpengalaman selama 27 tahun di dunia

perbankan. Pernah menjabat sebagai

Operation Head di Bank Mega Syariah.

Bergabung pada bulan Maret 2013 sebagai GM

Operation

Berpengalaman selama 26 tahun di dunia perbankan.

Pernah menjabat beberapa posisi seperti Audit,

Financing Operation dan Risk Management Head di

Bank Mega Syariah. Bergabung pada tahun 2011 sebagai Direktur

Kepatuhan

Tim Manajemen

Kunci

88

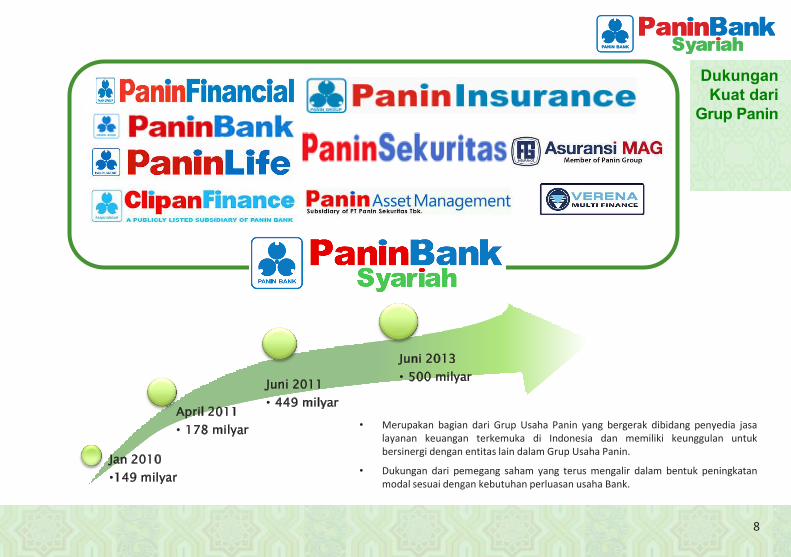

• Merupakan bagian dari Grup Usaha Panin yang bergerak dibidang penyedia jasa layanan keuangan terkemuka di Indonesia dan memiliki keunggulan untuk bersinergi dengan entitas lain dalam Grup Usaha Panin.

• Dukungan dari pemegang saham yang terus mengalir dalam bentuk peningkatan modal sesuai dengan kebutuhan perluasan usaha Bank.

Jan 2010 •149 milyar

April 2011 • 178 milyar

Juni 2011 • 449 milyar

Juni 2013 • 500 milyar

Dukungan Kuat dari

Grup Panin

9

Title:Source:

Please�fill�in�the�values�above�to�have�them�entered�in�your�report

0

1

2

3

4

5

6

0

20

40

60

80

100

120

140

160

180

2005 2006 2007 2008 2009 2010 2011 2012 Aug-13

(%)(IDRtrn)

Islamic bank deposit (LHS)

Islamic bank deposit as % of conventional bank deposit (RHS) �

Title:Source:

Please�fill�in�the�values�above�to�have�them�entered�in�your�report

0

10

20

30

40

50

60

2006 2007 2008 2009 2010 2011 2012 Aug-13

(y-o-y %)

Islamic bank deposit growth Commercial bank deposit growth �

9

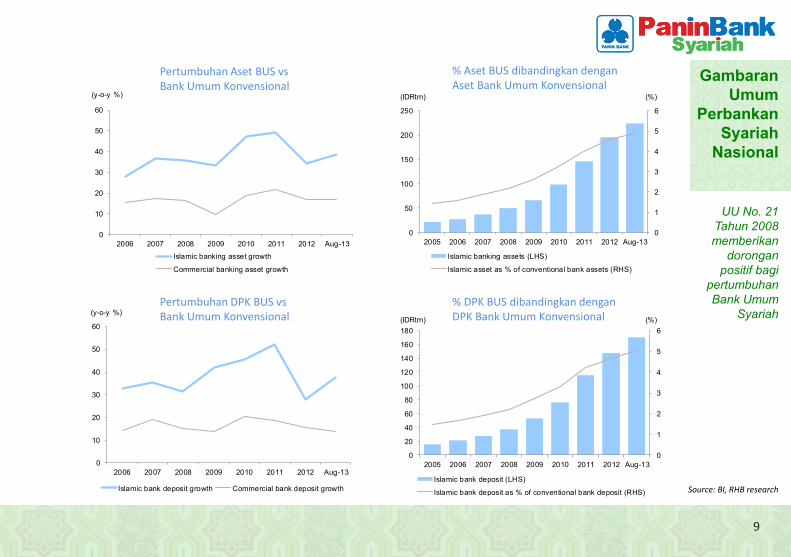

UU No. 21 Tahun 2008memberikan

dorongan positif bagi

pertumbuhan Bank Umum

Syariah

Title:Source:

Please�fill�in�the�values�above�to�have�them�entered�in�your�report

0

10

20

30

40

50

60

2006 2007 2008 2009 2010 2011 2012 Aug-13

(y-o-y %)

Islamic banking asset growth

Commercial banking asset growth �

Title:Source:

Please�fill�in�the�values�above�to�have�them�entered�in�your�report

0

1

2

3

4

5

6

0

50

100

150

200

250

2005 2006 2007 2008 2009 2010 2011 2012 Aug-13

(%)(IDRtrn)

Islamic banking assets (LHS)

Islamic asset as % of conventional bank assets (RHS) �

Pertumbuhan Aset BUS vs Bank Umum Konvensional

% Aset BUS dibandingkan dengan Aset Bank Umum Konvensional

Pertumbuhan DPK BUS vs Bank Umum Konvensional

% DPK BUS dibandingkan dengan DPK Bank Umum Konvensional

Source: BI, RHB research

Gambaran Umum

Perbankan Syariah

Nasional

1010

Title:Source:

Please�fill�in�the�values�above�to�have�them�entered�in�your�report

0

10

20

30

40

50

60

2006 2007 2008 2009 2010 2011 2012 Aug-13

(y-o-y %)

Islamic bank financing growth Commercial bank loans growth �

Title:Source:

Please�fill�in�the�values�above�to�have�them�entered�in�your�report

0

1

2

3

4

5

6

0

20

40

60

80

100

120

140

160

180

200

2005 2006 2007 2008 2009 2010 2011 2012 Aug-13

(%)(IDRtrn)

Islamic bank financing (LHS)

Islamic bank financing as % of conventional bank loans (RHS) �

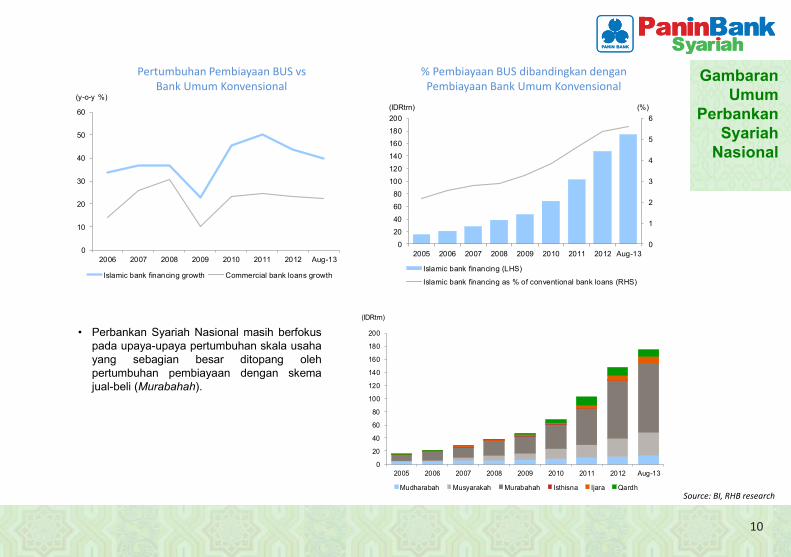

Pertumbuhan Pembiayaan BUS vs Bank Umum Konvensional

% Pembiayaan BUS dibandingkan dengan Pembiayaan Bank Umum Konvensional

Source: BI, RHB research

• Perbankan Syariah Nasional masih berfokus pada upaya-upaya pertumbuhan skala usaha yang sebagian besar ditopang oleh pertumbuhan pembiayaan dengan skema jual-beli (Murabahah).

Title:Source:

Please�fill�in�the�values�above�to�have�them�entered�in�your�report

0

20

40

60

80

100

120

140

160

180

200

2005 2006 2007 2008 2009 2010 2011 2012 Aug-13

(IDRtrn)

Mudharabah Musyarakah Murabahah Isthisna Ijara Qardh �

Gambaran Umum

Perbankan Syariah

Nasional

1111

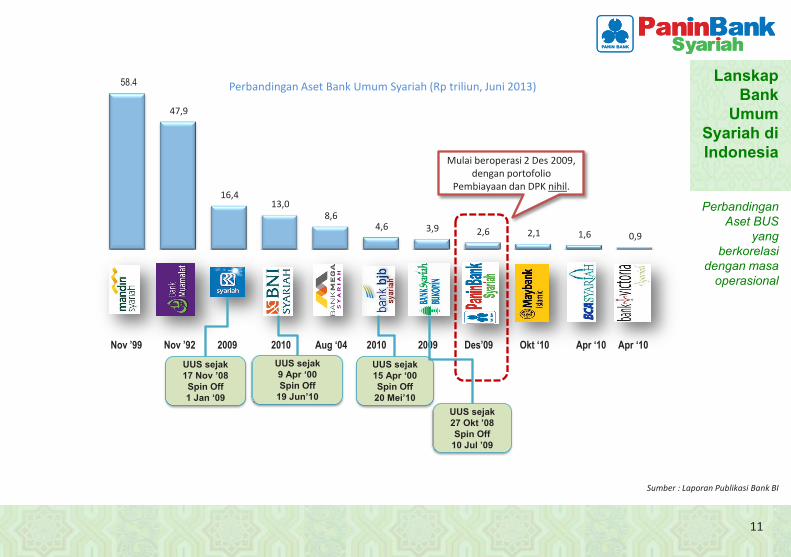

Perbandingan Aset BUS

yang berkorelasi

dengan masa operasional

Perbandingan Aset Bank Umum Syariah (Rp triliun, Juni 2013)

Sumber : Laporan Publikasi Bank BI

Nov ’99 Nov ’92 2009 2010 Aug ‘04 2010 2009 Des’09 Okt ‘10 Apr ‘10 Apr ‘10

58.4

47,9

16,4 13,0

8,6 4,6 3,9 2,6 2,1 1,6 0,9

UUS sejak 17 Nov ‟08Spin Off 1 Jan „09

UUS sejak 9 Apr „00Spin Off

19 Jun‟10

UUS sejak 15 Apr „00Spin Off

20 Mei‟10UUS sejak 27 Okt ‟08Spin Off

10 Jul ‟09

Mulai beroperasi 2 Des 2009, dengan portofolio

Pembiayaan dan DPK nihil.

Lanskap Bank

Umum Syariah di Indonesia

1212

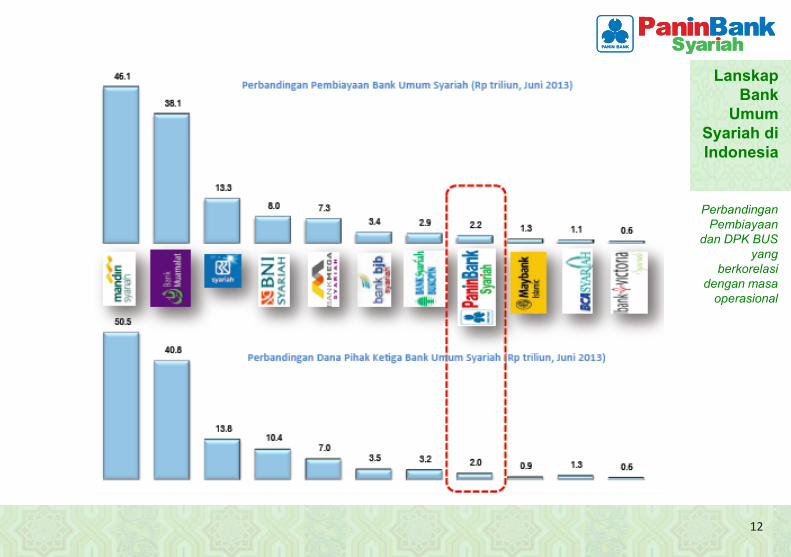

Perbandingan Pembiayaan

dan DPK BUS yang

berkorelasi dengan masa

operasional

Lanskap Bank

Umum Syariah di Indonesia

1313

2012 2013

Sangat Bagus Kinerja Keuangan 2011

Infobank Sharia Award Oktober 2012

Sangat Bagus Kinerja Keuangan 2011

Infobank Rating 120 Bank Juli 2012

Best Performance Banking 2012 Kinerja Keuangan 2011, Kategori Aset s/d 5 T

Tempo Perbanas Award, Agustus 2012

Sangat Bagus Kinerja Keuangan 2012 Infobank Sharia Award

November 2013

Sangat Bagus Kinerja Keuangan 2012

Infobank Rating 120 Bank Juli 2013

Best Performance Banking 2013 Kinerja Keuangan 2012,

Kategori Bank Syariah Buku 1 Tempo Perbanas Award, Oktober 2013

Best Syariah 2013 Kinerja Keuangan 2012,

Kategori Bank Syariah Aset < 10 T Majalah Investor Juli 2013

Penghargaan

Operasional Perbankan

1515

Fokus &Strategi

Usaha Perbankan

2013 2014 2015 2016

F O K U S

Percepatan Pertumbuhan Bisnis

Pengembangan Produk Inovatif dan Brand Image

Meletakkan fondasi bisnis ritel dan komersial guna peningkatan daya saing di pasar

1. Mengoptimalkan low cost funding. 2. Membangun bisnis ritel melalui B2B

dan B2C. 3. Meningkatkan pembiayaan komersial

sesuai potensi daerah. 4. Mengembangkan jaringan kantor di

beberapa Propinsi. 5. Meningkatkan sinergi dengan

perusahaan induk (PaninBank). 6. Membangun sistem direct

sales/telemarketing. 7. Memperkuat fungsi pengelolaan risiko. 8. Mengembangkan infrastruktur:

operations & IT.

1. Meningkatkan kerjasama B2B dan mengembangkan B2C.

2. Meningkatkan ekspansi jaringan kantor. 3. Menjalankan innovative bundled solutions product

kepada segmen usaha ritel dan komersial. 4. Refresh brand image. 5. Mengembangkan pengelolaan risiko secara

terintegrasi.

Roadmap

1616

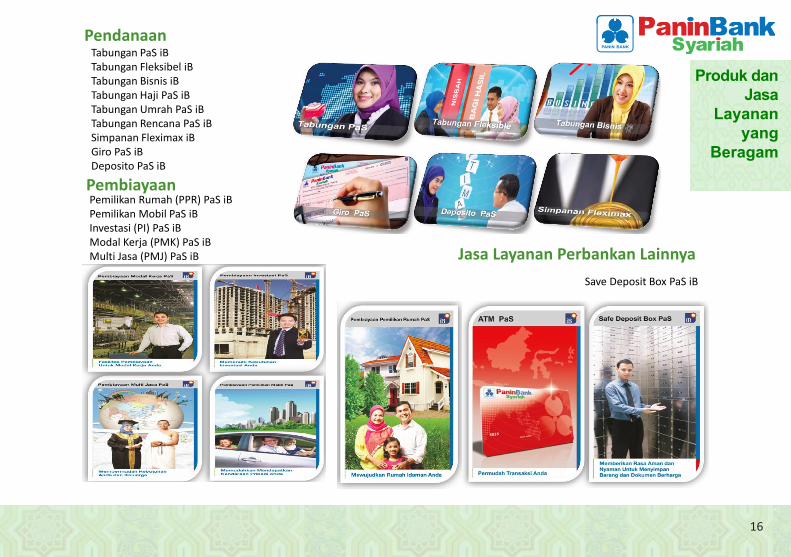

Pendanaan

Pembiayaan

Jasa Layanan Perbankan Lainnya

Pemilikan Rumah (PPR) PaS iB Pemilikan Mobil PaS iB Investasi (PI) PaS iB Modal Kerja (PMK) PaS iB Multi Jasa (PMJ) PaS iB

Tabungan PaS iB Tabungan Fleksibel iB Tabungan Bisnis iB Tabungan Haji PaS iB Tabungan Umrah PaS iB Tabungan Rencana PaS iB Simpanan Fleximax iB Giro PaS iB Deposito PaS iB

Save Deposit Box PaS iB

Produk dan Jasa

Layanan yang

Beragam

1717

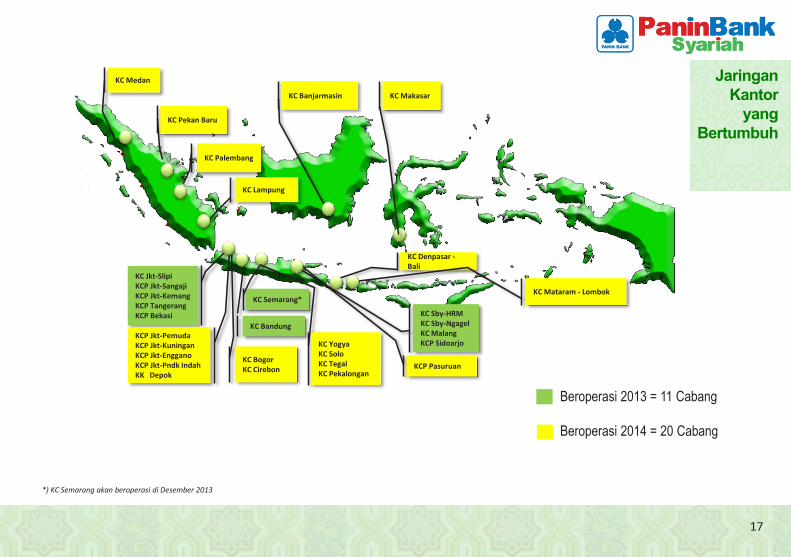

KC Jkt-Slipi KCP Jkt-Sangaji KCP Jkt-Kemang KCP Tangerang KCP Bekasi

KCP Jkt-Pemuda KCP Jkt-Kuningan KCP Jkt-Enggano KCP Jkt-Pndk Indah KK Depok

KC Sby-HRM KC Sby-Ngagel KC Malang KCP Sidoarjo

KC Bogor KC Cirebon

KC Bandung

KC Semarang*

KCP Pasuruan

KC Medan

KC Pekan Baru

KC Palembang

KC Lampung

KC Banjarmasin KC Makasar

KC Yogya KC Solo KC Tegal KC Pekalongan

KC Denpasar - Bali

KC Mataram - Lombok

Beroperasi 2013 = 11 Cabang Beroperasi 2014 = 20 Cabang

*) KC Semarang akan beroperasi di Desember 2013

Jaringan Kantor

yang Bertumbuh

1818

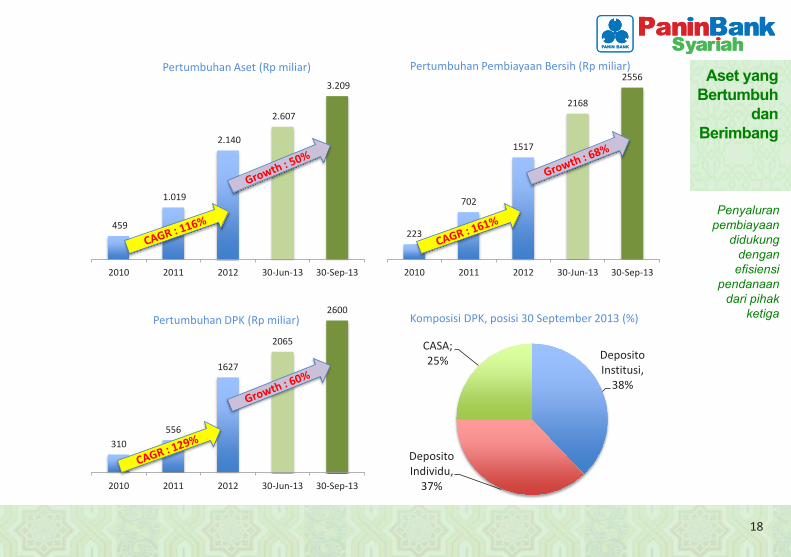

Penyaluran pembiayaan

didukung dengan

efisiensipendanaan

dari pihak ketiga

Pertumbuhan Aset (Rp miliar)

459

1.019

2.140

2.607

3.209

2010 2011 2012 30-Jun-13 30-Sep-13

223

702

1517

2168

2556

2010 2011 2012 30-Jun-13 30-Sep-13

Pertumbuhan Pembiayaan Bersih (Rp miliar)

310 556

1627

2065

2600

2010 2011 2012 30-Jun-13 30-Sep-13

Pertumbuhan DPK (Rp miliar)

Deposito Institusi,

38%

Deposito Individu,

37%

CASA; 25%

Komposisi DPK, posisi 30 September 2013 (%)

Aset yang Bertumbuh

dan Berimbang

1919

Title:Source:

Please fill in the values above to have them entered in your report

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2Q13

(IDRbn)

Murabahah Mudharabah Musyarakah �

Title:Source:

Please fill in the values above to have them entered in your report

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2Q13

(IDRbn)

Investment Consumer Working capital �

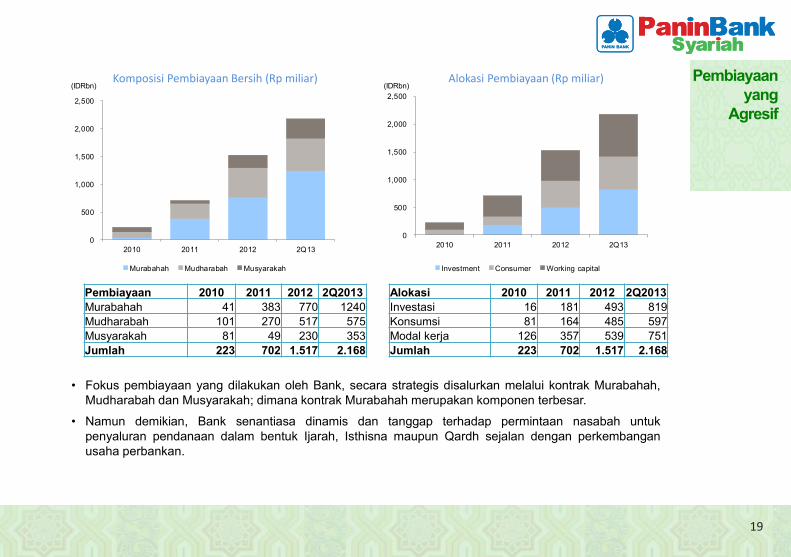

Komposisi Pembiayaan Bersih (Rp miliar) Alokasi Pembiayaan (Rp miliar)

• Fokus pembiayaan yang dilakukan oleh Bank, secara strategis disalurkan melalui kontrak Murabahah, Mudharabah dan Musyarakah; dimana kontrak Murabahah merupakan komponen terbesar.

• Namun demikian, Bank senantiasa dinamis dan tanggap terhadap permintaan nasabah untuk penyaluran pendanaan dalam bentuk Ijarah, Isthisna maupun Qardh sejalan dengan perkembangan usaha perbankan.

Pembiayaan 2010 2011 2012 2Q2013Murabahah 41 383 770 1240Mudharabah 101 270 517 575Musyarakah 81 49 230 353Jumlah 223 702 1.517 2.168

Alokasi 2010 2011 2012 2Q2013Investasi 16 181 493 819Konsumsi 81 164 485 597Modal kerja 126 357 539 751Jumlah 223 702 1.517 2.168

Pembiayaan yang

Agresif

2020

Title:Source:

Please fill in the values above to have them entered in your report0.86

0.19

0.56

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0

2

4

6

8

10

12

14

2011 2012 2Q13

(%)(IDRbn)

NPF (LHS) NPF (RHS) �

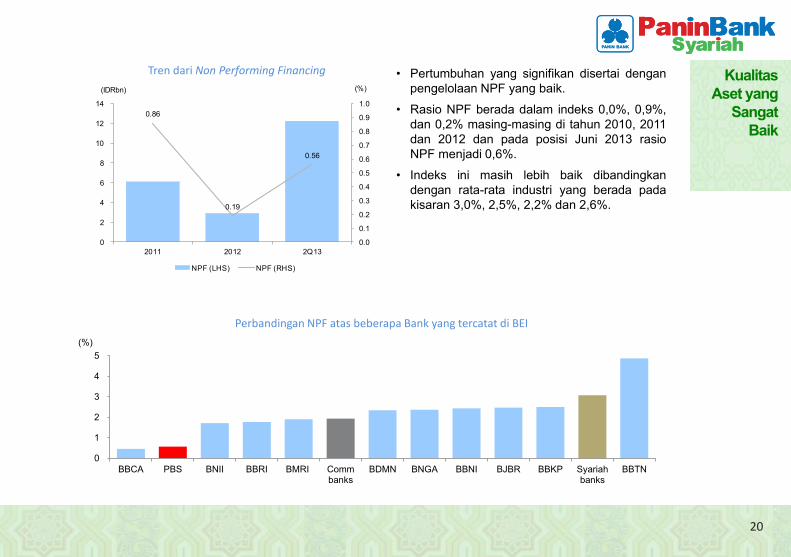

Tren dari Non Performing Financing • Pertumbuhan yang signifikan disertai dengan pengelolaan NPF yang baik.

• Rasio NPF berada dalam indeks 0,0%, 0,9%, dan 0,2% masing-masing di tahun 2010, 2011 dan 2012 dan pada posisi Juni 2013 rasio NPF menjadi 0,6%.

• Indeks ini masih lebih baik dibandingkan dengan rata-rata industri yang berada padakisaran 3,0%, 2,5%, 2,2% dan 2,6%.

0

1

2

3

4

5

BBCA PBS BNII BBRI BMRI Commbanks

BDMN BNGA BBNI BJBR BBKP Syariahbanks

BBTN

(%)

Perbandingan NPF atas beberapa Bank yang tercatat di BEI

Kualitas Aset yang

Sangat Baik

21

Pendidikan

Acara Keagamaan

Yatim dan Dhuafa

21

Komitmen Sosial

Kinerja Keuangan

2323

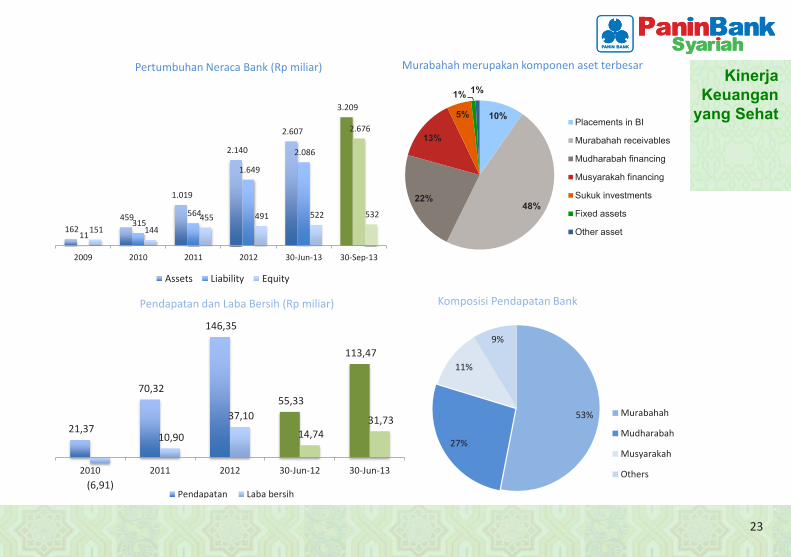

Pertumbuhan Neraca Bank (Rp miliar)

10%

48%22%

13%

5%

1% 1%

Placements in BI

Murabahah receivables

Mudharabah financing

Musyarakah financing

Sukuk investments

Fixed assets

Other asset

Murabahah merupakan komponen aset terbesar

162 459

1.019

2.140

2.607

3.209

11 315

564

1.649

2.086

2.676

151 144 455 491 522 532

2009 2010 2011 2012 30-Jun-13 30-Sep-13

Assets Liability Equity

Komposisi Pendapatan Bank Pendapatan dan Laba Bersih (Rp miliar)

53%

27%

11%

9%

Murabahah

Mudharabah

Musyarakah

Others

21,37

70,32

146,35

55,33

113,47

(6,91)

10,90

37,10

14,74 31,73

2010 2011 2012 30-Jun-12 30-Jun-13

Pendapatan Laba bersih

Kinerja Keuangan

yang Sehat

2424

55% 62%

32% 23%

2010 2011 2012 Juni 2013

CAR

7,0%

5,3%

6,7% 6,2%

2010 2011 2012 Juni 2013

NIM

-4,5%

3,3%

8,2% 7,4%

2010 2011 2012 Juni 2013

ROE

-3,6%

2,1%

3,5%

1,9%

2010 2011 2012 Juni 2013

ROA

Rasio Keuangan

Bank

2525

0,00% 0,69% 0,19% 0,47%

2010 2011 2012 Juni 2013

NPF

178%

69% 48%

69%

2010 2011 2012 Juni 2013

BOPO

182.31%

74.30%

50.76% 64.34%

2010 2011 2012 Jun-13

COST TO REVENUE

Rasio Keuangan

Bank

Struktur Penawaran

27

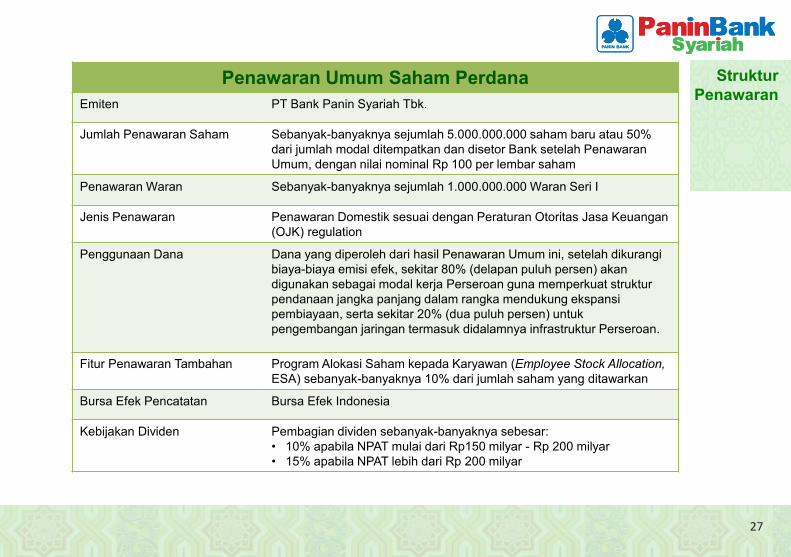

Penawaran Umum Saham Perdana Emiten PT Bank Panin Syariah Tbk.

Jumlah Penawaran Saham Sebanyak-banyaknya sejumlah 5.000.000.000 saham baru atau 50%dari jumlah modal ditempatkan dan disetor Bank setelah Penawaran Umum, dengan nilai nominal Rp 100 per lembar saham

Penawaran Waran Sebanyak-banyaknya sejumlah 1.000.000.000 Waran Seri I

Jenis Penawaran Penawaran Domestik sesuai dengan Peraturan Otoritas Jasa Keuangan(OJK) regulation

Penggunaan Dana Dana yang diperoleh dari hasil Penawaran Umum ini, setelah dikurangi biaya-biaya emisi efek, sekitar 80% (delapan puluh persen) akandigunakan sebagai modal kerja Perseroan guna memperkuat strukturpendanaan jangka panjang dalam rangka mendukung ekspansipembiayaan, serta sekitar 20% (dua puluh persen) untukpengembangan jaringan termasuk didalamnya infrastruktur Perseroan.

Fitur Penawaran Tambahan Program Alokasi Saham kepada Karyawan (Employee Stock Allocation, ESA) sebanyak-banyaknya 10% dari jumlah saham yang ditawarkan

Bursa Efek Pencatatan Bursa Efek Indonesia

Kebijakan Dividen Pembagian dividen sebanyak-banyaknya sebesar: • 10% apabila NPAT mulai dari Rp150 milyar - Rp 200 milyar • 15% apabila NPAT lebih dari Rp 200 milyar

27

Struktur Penawaran

28

Lembaga & Profesi Penunjang Pasar Modal

Penjamin Pelaksana Emisi

Akuntan Publik Osman Bing Satrio & Eny (Member of Deloitte Touche Tohmatsu Limited)

Konsultan Hukum Lasutlay & Pane

Notaris Fathiah Helmi SH.

Biro Administrasi Efek PT Blue Chip Mulia

28

Indikasi Jadwal

Masa Penawaran Awal 2 – 13 Desember 2013 Distribusi Saham 13 Januari 2014

Penetapan Harga 13 Desember 2013 Tanggal Pencatatan 14 Januari 2014

Pernyataan Efektif 30 Desember 2013 Masa Perdagangan Waran 14 Januari 2014 – 13 Januari 2017

Masa Penawaran Umum 2 – 8 Januari 2014 Masa Pelaksanaan Waran 14 Januari 2014 – 13 Januari 2017

Struktur Penawaran

29

29

RENTANG HARGA PENAWARAN UMUM SAHAM PERDANA

Rp _______________ sampai dengan Rp _______________

per lembar saham

Harga Penawaran

Pertimbangan Investasi

31

31

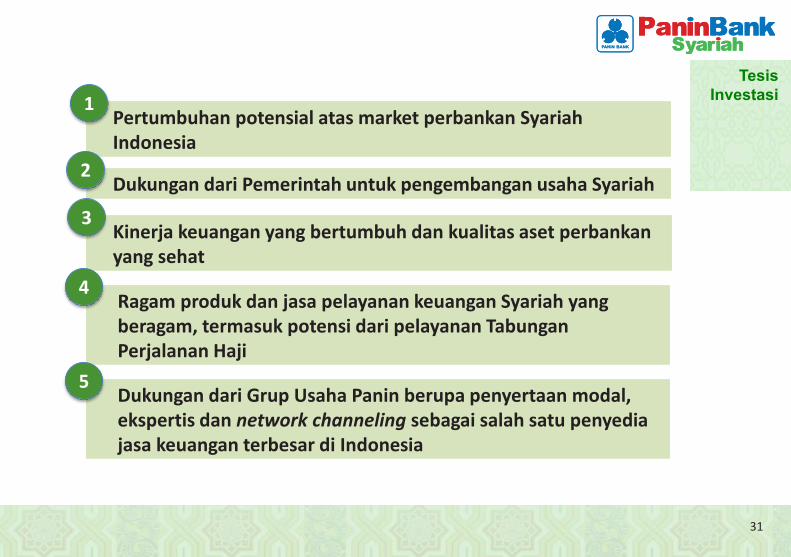

Pertumbuhan potensial atas market perbankan Syariah Indonesia

1

Dukungan dari Pemerintah untuk pengembangan usaha Syariah 2

Kinerja keuangan yang bertumbuh dan kualitas aset perbankan yang sehat

3

Ragam produk dan jasa pelayanan keuangan Syariah yang beragam, termasuk potensi dari pelayanan Tabungan Perjalanan Haji

4

Dukungan dari Grup Usaha Panin berupa penyertaan modal, ekspertis dan network channeling sebagai salah satu penyedia jasa keuangan terbesar di Indonesia

5

Tesis Investasi

Lampiran

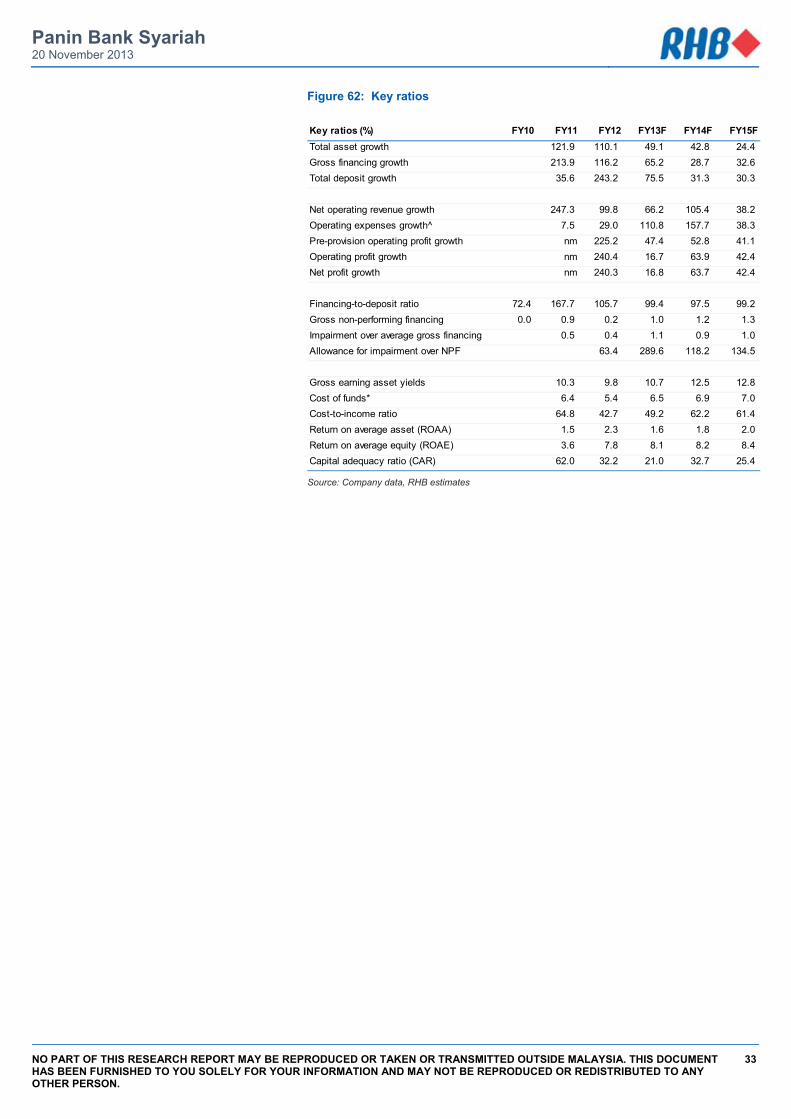

33

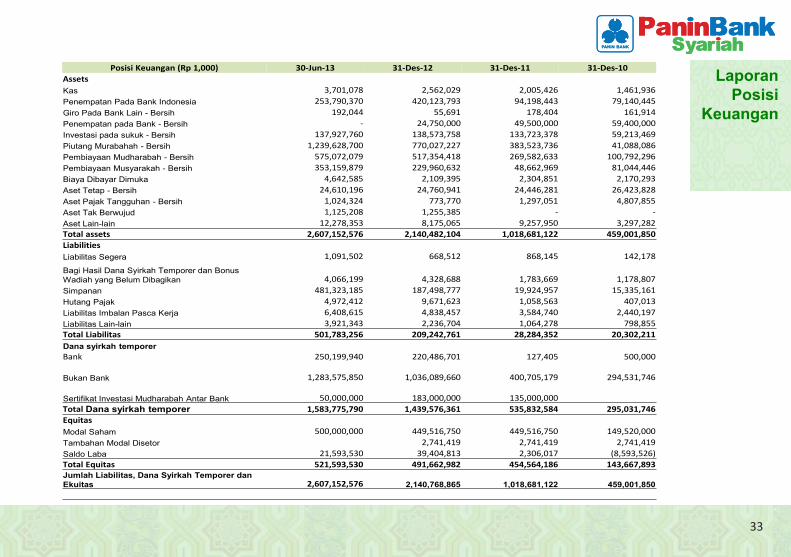

Posisi Keuangan (Rp 1,000) 30-Jun-13 31-Des-12 31-Des-11 31-Des-10 Assets Kas 3,701,078 2,562,029 2,005,426 1,461,936 Penempatan Pada Bank Indonesia 253,790,370 420,123,793 94,198,443 79,140,445 Giro Pada Bank Lain - Bersih 192,044 55,691 178,404 161,914 Penempatan pada Bank - Bersih - 24,750,000 49,500,000 59,400,000 Investasi pada sukuk - Bersih 137,927,760 138,573,758 133,723,378 59,213,469 Piutang Murabahah - Bersih 1,239,628,700 770,027,227 383,523,736 41,088,086 Pembiayaan Mudharabah - Bersih 575,072,079 517,354,418 269,582,633 100,792,296 Pembiayaan Musyarakah - Bersih 353,159,879 229,960,632 48,662,969 81,044,446 Biaya Dibayar Dimuka 4,642,585 2,109,395 2,304,851 2,170,293 Aset Tetap - Bersih 24,610,196 24,760,941 24,446,281 26,423,828 Aset Pajak Tangguhan - Bersih 1,024,324 773,770 1,297,051 4,807,855 Aset Tak Berwujud 1,125,208 1,255,385 - - Aset Lain-lain 12,278,353 8,175,065 9,257,950 3,297,282 Total assets 2,607,152,576 2,140,482,104 1,018,681,122 459,001,850 Liabilities Liabilitas Segera 1,091,502 668,512 868,145 142,178

Bagi Hasil Dana Syirkah Temporer dan Bonus Wadiah yang Belum Dibagikan 4,066,199 4,328,688 1,783,669 1,178,807 Simpanan 481,323,185 187,498,777 19,924,957 15,335,161 Hutang Pajak 4,972,412 9,671,623 1,058,563 407,013 Liabilitas Imbalan Pasca Kerja 6,408,615 4,838,457 3,584,740 2,440,197 Liabilitas Lain-lain 3,921,343 2,236,704 1,064,278 798,855 Total Liabilitas 501,783,256 209,242,761 28,284,352 20,302,211 Dana syirkah temporer Bank 250,199,940 220,486,701 127,405 500,000

Bukan Bank 1,283,575,850 1,036,089,660 400,705,179 294,531,746

Sertifikat Investasi Mudharabah Antar Bank 50,000,000 183,000,000 135,000,000 Total Dana syirkah temporer 1,583,775,790 1,439,576,361 535,832,584 295,031,746 Equitas Modal Saham 500,000,000 449,516,750 449,516,750 149,520,000 Tambahan Modal Disetor 2,741,419 2,741,419 2,741,419 Saldo Laba 21,593,530 39,404,813 2,306,017 (8,593,526) Total Equitas 521,593,530 491,662,982 454,564,186 143,667,893 Jumlah Liabilitas, Dana Syirkah Temporer dan Ekuitas 2,607,152,576 2,140,768,865 1,018,681,122 459,001,850

Laporan Posisi

Keuangan

34

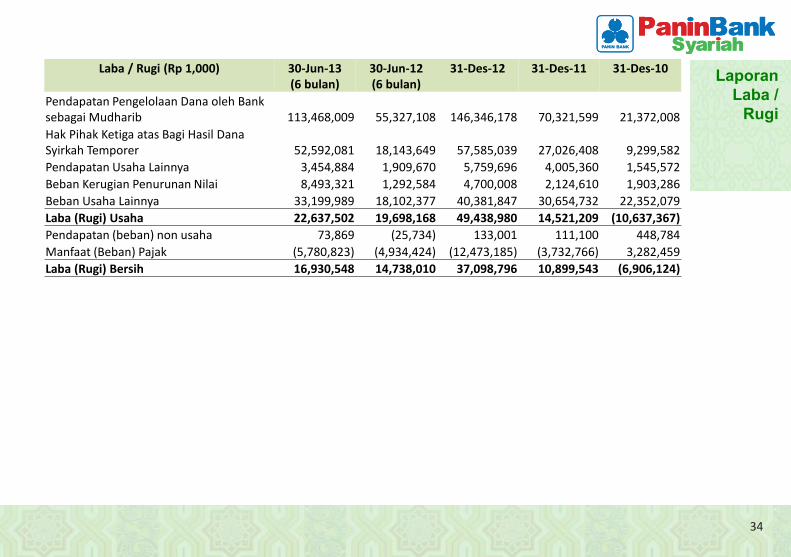

Laba / Rugi (Rp 1,000) 30-Jun-13 (6 bulan)

30-Jun-12 (6 bulan)

31-Des-12 31-Des-11 31-Des-10

Pendapatan Pengelolaan Dana oleh Bank sebagai Mudharib 113,468,009 55,327,108 146,346,178 70,321,599 21,372,008 Hak Pihak Ketiga atas Bagi Hasil Dana Syirkah Temporer 52,592,081 18,143,649 57,585,039 27,026,408 9,299,582 Pendapatan Usaha Lainnya 3,454,884 1,909,670 5,759,696 4,005,360 1,545,572 Beban Kerugian Penurunan Nilai 8,493,321 1,292,584 4,700,008 2,124,610 1,903,286 Beban Usaha Lainnya 33,199,989 18,102,377 40,381,847 30,654,732 22,352,079 Laba (Rugi) Usaha 22,637,502 19,698,168 49,438,980 14,521,209 (10,637,367) Pendapatan (beban) non usaha 73,869 (25,734) 133,001 111,100 448,784 Manfaat (Beban) Pajak (5,780,823) (4,934,424) (12,473,185) (3,732,766) 3,282,459 Laba (Rugi) Bersih 16,930,548 14,738,010 37,098,796 10,899,543 (6,906,124)

Laporan Laba /

Rugi

3535

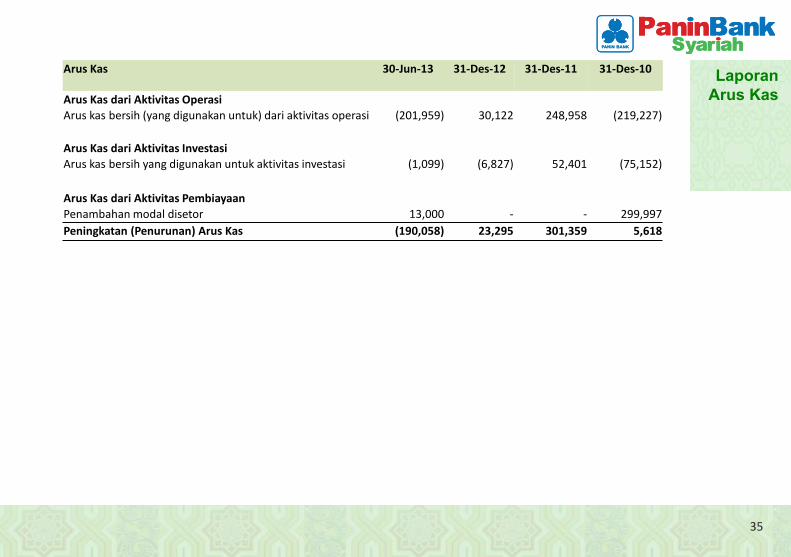

Arus Kas 30-Jun-13 31-Des-12 31-Des-11

31-Des-10

Arus Kas dari Aktivitas Operasi Arus kas bersih (yang digunakan untuk) dari aktivitas operasi (201,959) 30,122 248,958 (219,227)

Arus Kas dari Aktivitas Investasi Arus kas bersih yang digunakan untuk aktivitas investasi (1,099) (6,827) 52,401 (75,152)

Arus Kas dari Aktivitas Pembiayaan Penambahan modal disetor 13,000 - - 299,997 Peningkatan (Penurunan) Arus Kas (190,058) 23,295 301,359 5,618

Laporan Arus Kas

36

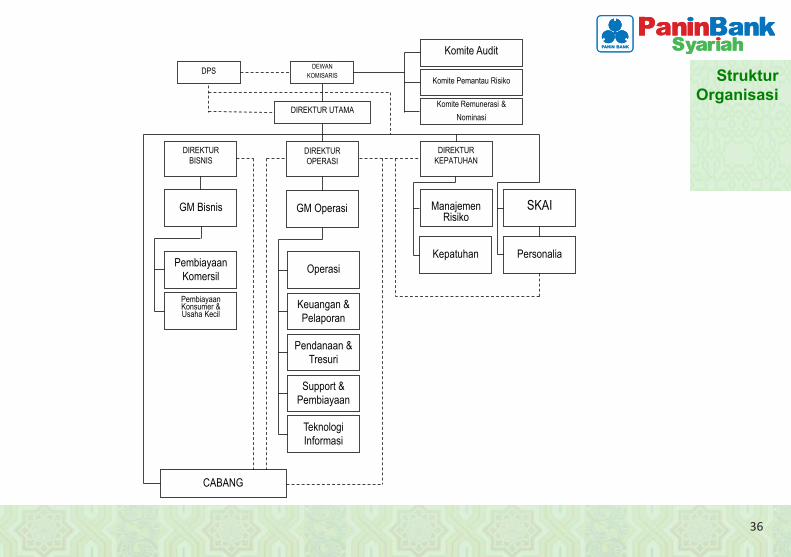

DIREKTUR BISNIS

DIREKTUR KEPATUHAN

Manajemen

Risiko

Kepatuhan

SKAI

Personalia

GM Bisnis

Pembiayaan Komersil

Pembiayaan Konsumer & Usaha Kecil

CABANG

DIREKTUR UTAMA

DIREKTUR OPERASI

GM Operasi

Operasi

Keuangan & Pelaporan

Pendanaan & Tresuri

Support & Pembiayaan

Teknologi Informasi

DPS DEWAN KOMISARIS

Komite Audit

Komite Pemantau Risiko

Komite Remunerasi &

Nominasi

Struktur Organisasi

37

Jakarta : KCU Slipi Gd. Panin Life Center Lt. Dasar Jl. Letjend. S. Parman Kav. 91, Slipi Jakarta Barat – 11420Ph. 021 – 56956100Fax. 021 – 56956105

Jakarta Barat : KCP Sangaji Jl. AM Sangaji Raya No. 15 – 17AJakarta Barat Ph. 021 – 63867616Fax. 021 – 63867615

Jakarta Selatan : KCP Kemang Jl. Kemang Raya No. 112A Jakarta Selatan Ph. 021 – 7180360Fax. 021 – 7180359

Tangerang : KCP Tangerang Jl. Merdeka No. 140 Tangerang – Banten Ph. 021 – 5526909Fax. 021 – 5526989

Bandung : KCU Asia Afrika Jl. Asia Afrika No 66 - 70Bandung – Jawa Barat Ph. 022 – 4267266Fax. 022 – 4267267

37

Surabaya : KCU HR Muhammad Ruko HR Muhammad Square Blok C.19 – 20 & Blok C.29 – 30,Surabaya – Jawa Timur Ph. 031 – 738 6388 Fax. 031 – 732 8299

Surabaya : KCU Ngagel Ruko RMI Jl. Ngagel Jaya Selatan Surabaya – Jawa Timur Ph. 031 – 504 8343 Fax. 031 – 504 8341

Malang : KCU Malang Jl. Mgr. Sugiopranoto No. 7 Malang – Jawa Timur Ph. 0341 – 361 383 Fax. 0341 – 361 861

Sidoarjo : KCP Sidoarjo Ruko Graha Mutiara Delta Jl. Diponegoro A - 6 Sidoarjo – Jawa Timur Ph. 031 – 896 2828 Fax. 031 – 895 8739

KCU : Kantor Cabang Utama KCP : Kantor Cabang Pembantu

Bekasi : KCP Bekasi Ruko Kalimalang Plaza No. 9 Jl. KH. Noer Ali, Bekasi – Jawa Barat Ph. 021 – 8896 7366 Fax 021 – 8896 7363

Jaringan Kantor

Terima KasihKantor Pusat:

Gedung Panin Life Center, 3rd FloorJl. Letjend S. ParmanKav 91, SlipiJakarta Barat 11420Indonesia www.paninbanksyariah.co.id

39

The information that follows is a presentation of general background information about PT Bank Panin Syariah Tbk. (the “Bank”) prepared by the Bank as of 2 December 2013. The information contained in this presentation shall be treated as strictly confidential.

This presentation has been prepared for information purposes only. This presentation does not constitute as prospectus or other offering memorandum in whole or in part. None of the information appearing in this presentation may be distributed to the press or other media orreproduced or redistributed in the whole or in part in any form at any time. Any recipient of this presentation and its directors, officers, employees, agents and affiliates must hold this presentation and any information provided in connection with this presentation in strict confidence and may not communicate, reproduce, distribute or disclose to any other person, or refer to them publicly, in whole or in part.

The information contained in this presentation is not intended for potential investors and does not constitute an offer to sell or the solicitation of an offer to buy any securities in the United States, Indonesia or any other jurisdiction, and neither this presentation nor anything contained herein shall form the basis of or be relied on in connection with any contract or commitment whatsoever. Certainstatements in this document may constitute “forward-looking statements”, including statements regarding the Company’s expectationsand projections for future operating performance and business prospects. Such forward-looking statements are based on numerousassumptions regarding the Bank’s present and future business strategies and the environment in which the Bank will operate in thefuture. Such forward-looking statements speak only as of the date on which they are made. Accordingly, the Bank expressly disclaimsany obligation to update or revise any forward looking statement contained herein to reflect any change in the Bank’s expectations withregard to new information, future events or other circumstances. The Bank does not make any representation, warranty or prediction thatthe results anticipated by such forward looking statements will be achieved, and such forward looking statements represent, in eachcase, only on of many possible scenarios and should not be viewed as the most likely or standard scenario.

Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on the fairness, accuracy, completeness or correctness of the information and opinions in this presentation, nor is it intended to be a complete statementor summary of the resources markets or developments referred to in this presentation. Accordingly, none of the Bank or any of its agentsor advisers, or any of their respective affiliates, advisers or representatives, undertake to update or revise any information, includingforward-looking statements, whether as a result of new information, future events or otherwise and none of them shall have any liability(in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising inconnection with this presentation. It should not be regarded by recipients as a substitute for the exercise of their own judgment.

By accepting delivery of all or part of this presentation, the recipient agrees to maintain absolute confidentiality regarding the information disclosed in this presentation and to be bound by the statements, restrictions and limitations set forth herein and agrees to keep confidential the existence and scope of this presentation and of all conversations. Any failure to comply with these restrictions may constitute a violation of applicable securities law.

39

Important Disclaimer

Rocky In(65) 6232rocky.ind

20 No

ndrawan 2 3832 drawan@sg

ovember 2

g.oskgroup.c

013

com

THIS REPORSTATES, CASPECIAL ADSOLELY FORTO ANY OTRESTRICTIOAPPLY.

Ple

RTS MAY NOTANADA, THE DMINISTRATIVR YOUR INFORHER PERSON

ONS AS SET O

Pa

ease read im

T BE DISTRIBUPEOPLE’S RE

VE REGION) ORMATION AND IN ANY FORM

OUT IN THE IN

nin B

mportant dis

PANIN B

UTED, DIRECTLEPUBLIC OF OR JAPAN. IT

D MAY NOT BE M. IT MAY NONSIDE AND BA

Bank S

sclosures a

BANK SYAR

LY, OR INDIRECHINA (EXCL

T HAS BEEN REPRODUCET BE SENT TOACK COVER O

Syaria

t the end of

RIAH

ECTLY, IN THELUDING HONGFURNISHED TD OR REDISTRO THE MEDIAOF THE THIS

ah

IPO REP

f this report.

UNITED G KONG TO YOU RIBUTED . OTHER REPORT

PORT

.

These materials are not an offer for sale of the securities of the Company in the United States. The securities may not be offered orsold in the United States absent registration or an exemption from registration under the U.S. Securities Act of 1933, as amended. TheCompany does not intend to register any portion of the offering in the United States or to conduct a public offering of its securities inthe United States.

Power

1

Disclaimers This Report is based on current information that we consider reliable. However, as the information contained in this Report has not been independently verified, no representation or warranty, express or implied, is made as to the fairness, accuracy or completeness of the information and opinions contained in this report and it is not the author’s intention to provide, and the recipient may not rely on this report as providing, a complete or comprehensive analysis of Panin Bank Syariah’s financial or trading position or prospects. Without limiting the generality of the foregoing, liability for negligent misstatement in respect of the contents of, or any omission from, this Report is hereby expressly excluded. The information and opinions in this report are subject to change without notice. Any opinions and projections contained in this document are entirely those of RHB. Neither Panin Bank Syariah, RHB or any other person accepts any liability whatsoever for any loss howsoever arising from any use of this Report or its contents or otherwise arising in connection therewith.

This Report is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute and shall not be construed as a proposal to make available, offer for subscription or purchase or issue an invitation to subscribe for or purchase securities, nor does it refer and shall not be construed as referring, whether directly or indirectly, to any prospectus in respect of securities of a corporation, an issue, intended issue, offer, intended offer, invitation or intended invitation in respect of securities, or to any other notice that refers to a prospectus in relation to an issue, intended issue, offer, intended offer, invitation or intended invitation in respect of securities.

This Report is furnished solely for your information and no part of this material may be (i) copied, photocopied or duplicated in any form by any means; or (ii) distributed to the press or other media or redistributed by mail, facsimile, electronic or computer transmission or by any other means to any other person without the prior written consent of RHB. By accepting this document you agree to be bound by the foregoing limitations.

MALAYSIA

This document has not been and will not be registered as a prospectus or lodged with the Securities Commission of Malaysia under the Capital Markets and Services Act, 2007 and may not be circulated or distributed to any person in Malaysia other than to specific persons specified under Schedules 6 or 7 of the Capital Markets and Services Act, 2007. The person receiving this document represents and warrants that if it receives this document in Malaysia as a specified person under Schedules 6 or 7 of the Capital Markets and Services Act, 2007. Additionally, the information contained in this Report should not be disclosed by the recipient to any other person.

SINGAPORE

This document has not been and will not be registered as an offering memorandum or prospectus with the Monetary Authority of Singapore under the Securities And Futures Act, Chapter 289 of Singapore (the “SFA”) and accordingly, this document may not be distributed, either directly or indirectly, to the public or any member of the public in Singapore, other than to institutional investors and/or accredited investors (both as defined in Section 4A of the SFA). In Singapore, in accordance, with the provisions of the SFA and the regulations made thereunder. The person receiving this document represents and warrants that if it receives this document in Singapore it is an institutional investor. Additionally, the information contained in this Report should not be disclosed by the recipient to any other person.

HONG KONG

The contents of this document have not been reviewed or approved by any regulatory authority in Hong Kong. This document may not be issued in any manner which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong, and is for distribution only to “professional investors” within the meaning of the Securities and Futures Ordinance (Cap. 571 of the Laws of Hong Kong) of Hong Kong and any rules promulgated thereunder. The person receiving this document represents and warrants that if it receives this document in Hong Kong it is a “professional investor” as defined above. Additionally, the information contained in this Report should not be disclosed by the recipient to any other person.

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

2

Contents

1. Executive Summary 3

2. Valuation Summar 4

3. Company Profile 5

4. Industry Overview and Outlook 10

5. Key Investment Themes 20

6. Key Risks 21

7. Financial Analysis and Forecasts 23

8. Financial Exhibits 32

9. Appendix 34

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

3

Executive Summary Panin Bank Syariah (PBS)’s enlarged capital, post IPO, will allow it to: i) develop new products, ii) generate new businesses, iii) expand its footprint, and iv) improve profitability. Indonesia’s favourable demographic profile and supportive regulators provide a solid foundation for the growth of sharia banks. The pathway for robust growth lies ahead, although it is not without challenges.

Riding the strong expansion of sharia banks.The growth of sharia banks in the last several years have outpaced conventional ones, given the: i) rising awareness, ii) deepening penetration, iii) support from regulators, and iv) various untapped pockets of business opportunities. The relative asset size of the former remainssmall – at 5% of the latter – but has been rising steadily. PBS is no exception. Its 3-year CAGR (2010-2013F) for asset, financing, operating revenue are 91%, 124% and 126% respectively. Meanwhile, the bank’s net loss in its first full year of operation (2010) has been turned into profits, with 2013F ROAA and ROAE of 1.6% and 8.1% respectively.

Fresh capital to spawn exciting new businesses. Post-IPO, PBS’ core capital will rise to IDR1trn, which will elevate it to a BUKU II status bank. This opens up an array of new opportunities, which were previously unavailable for PBS. Among many, the bank will now be able to tap into the growing hajj/umroh pilgrim market, develop a bancassurance business and establishan Internet banking platform. The enlarged capital will also enable PBS to grow its footprint, as it aspires to more than double its existing branch network in 2014.

Operates in a favourable environment. Indonesia is the world’s largest Muslim country, with roughly 87% of its ~250m population being adherents of this faith. Yet Islamic banking/financing makes up a mere 6% of conventional bank loans,while nationwide loans-to-GDP is only 35%. This indicates a bright growth potential ahead, as it is in stark contrast to Malaysia where Islamic banks command a 20% market share and where Islamic banking products are more developed. Surveys have suggested that awareness of sharia banks in Indonesia is prevalent.However, understanding and familiarity with their products and principles remain somewhat poor, which suggeststhat it requires a combination of penetration and education to increase the market share of sharia banks in Indonesia.

Regulators are supportive too. Via various regulations and initiatives, Bank Indonesia (BI)– together with the Government – has shown support for sharia banks. In 2008 the Islamic Banking Act was enacted and BI unveiled the Islamic banks developmentmaster plan. Over the past six years the central bank has introduced various regulations to improve prudence in sharia banks, while it encourages their expansion by assigning lower capital costs for shariabank branches.

Staying on the fast lane. PBS’ growth trajectory will remain robust in the next three years, supported by new businesses, expanded network and sufficient capital. We forecast its forward 3-year CAGR (2012-2015F) of financing, asset, operating revenue and net income at 41%, 38%, 68% and 40% respectively. We also expect ROAA/ROAE to expand gradually to 2.0%/8.4%by 2015F.

Valuation. PBS’ existing ROE profile (2013F: 7.4%) is below the estimated cost of equity (ie 14.5%). It is also inferior to both the industry average and the bank’sconventional peers.Therefore, we see it fair to assign no premium over its book value. We estimate PBS’ FV to be approximately IDR1.15trn, which is based on 2014F target P/BV multiple of 1x.

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

4

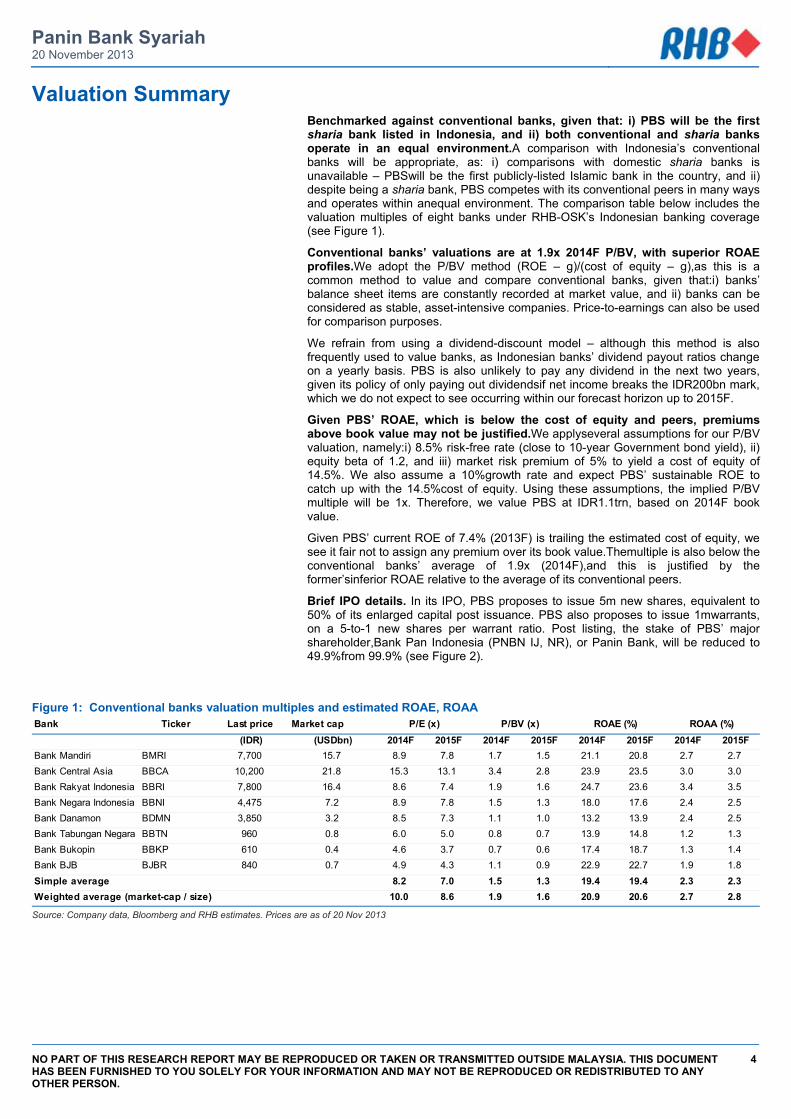

Valuation Summary Benchmarked against conventional banks, given that: i) PBS will be the first sharia bank listed in Indonesia, and ii) both conventional and sharia banks operate in an equal environment.A comparison with Indonesia’s conventional banks will be appropriate, as: i) comparisons with domestic sharia banks is unavailable – PBSwill be the first publicly-listed Islamic bank in the country, and ii) despite being a sharia bank, PBS competes with its conventional peers in many ways and operates within anequal environment. The comparison table below includes the valuation multiples of eight banks under RHB-OSK’s Indonesian banking coverage (see Figure 1).

Conventional banks’ valuations are at 1.9x 2014F P/BV, with superior ROAE profiles.We adopt the P/BV method (ROE – g)/(cost of equity – g),as this is a common method to value and compare conventional banks, given that:i) banks’ balance sheet items are constantly recorded at market value, and ii) banks can be considered as stable, asset-intensive companies. Price-to-earnings can also be used for comparison purposes.

We refrain from using a dividend-discount model – although this method is also frequently used to value banks, as Indonesian banks’ dividend payout ratios change on a yearly basis. PBS is also unlikely to pay any dividend in the next two years, given its policy of only paying out dividendsif net income breaks the IDR200bn mark, which we do not expect to see occurring within our forecast horizon up to 2015F.

Given PBS’ ROAE, which is below the cost of equity and peers, premiums above book value may not be justified.We applyseveral assumptions for our P/BV valuation, namely:i) 8.5% risk-free rate (close to 10-year Government bond yield), ii) equity beta of 1.2, and iii) market risk premium of 5% to yield a cost of equity of 14.5%. We also assume a 10%growth rate and expect PBS’ sustainable ROE to catch up with the 14.5%cost of equity. Using these assumptions, the implied P/BV multiple will be 1x. Therefore, we value PBS at IDR1.1trn, based on 2014F book value.

Given PBS’ current ROE of 7.4% (2013F) is trailing the estimated cost of equity, we see it fair not to assign any premium over its book value.Themultiple is also below the conventional banks’ average of 1.9x (2014F),and this is justified by the former’sinferior ROAE relative to the average of its conventional peers.

Brief IPO details. In its IPO, PBS proposes to issue 5m new shares, equivalent to 50% of its enlarged capital post issuance. PBS also proposes to issue 1mwarrants, on a 5-to-1 new shares per warrant ratio. Post listing, the stake of PBS’ major shareholder,Bank Pan Indonesia (PNBN IJ, NR), or Panin Bank, will be reduced to 49.9%from 99.9% (see Figure 2).

Figure 1: Conventional banks valuation multiples and estimated ROAE, ROAA

Source: Company data, Bloomberg and RHB estimates. Prices are as of 20 Nov 2013

Bank Ticker Last price Market cap(IDR) (USDbn) 2014F 2015F 2014F 2015F 2014F 2015F 2014F 2015F

Bank Mandiri BMRI 7,700 15.7 8.9 7.8 1.7 1.5 21.1 20.8 2.7 2.7Bank Central Asia BBCA 10,200 21.8 15.3 13.1 3.4 2.8 23.9 23.5 3.0 3.0Bank Rakyat Indonesia BBRI 7,800 16.4 8.6 7.4 1.9 1.6 24.7 23.6 3.4 3.5Bank Negara Indonesia BBNI 4,475 7.2 8.9 7.8 1.5 1.3 18.0 17.6 2.4 2.5Bank Danamon BDMN 3,850 3.2 8.5 7.3 1.1 1.0 13.2 13.9 2.4 2.5Bank Tabungan Negara BBTN 960 0.8 6.0 5.0 0.8 0.7 13.9 14.8 1.2 1.3Bank Bukopin BBKP 610 0.4 4.6 3.7 0.7 0.6 17.4 18.7 1.3 1.4Bank BJB BJBR 840 0.7 4.9 4.3 1.1 0.9 22.9 22.7 1.9 1.8Simple average 8.2 7.0 1.5 1.3 19.4 19.4 2.3 2.3

10.0 8.6 1.9 1.6 20.9 20.6 2.7 2.8

P/E (x) P/BV (x) ROAE (%) ROAA (%)

Weighted average (market-cap / size)

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

5

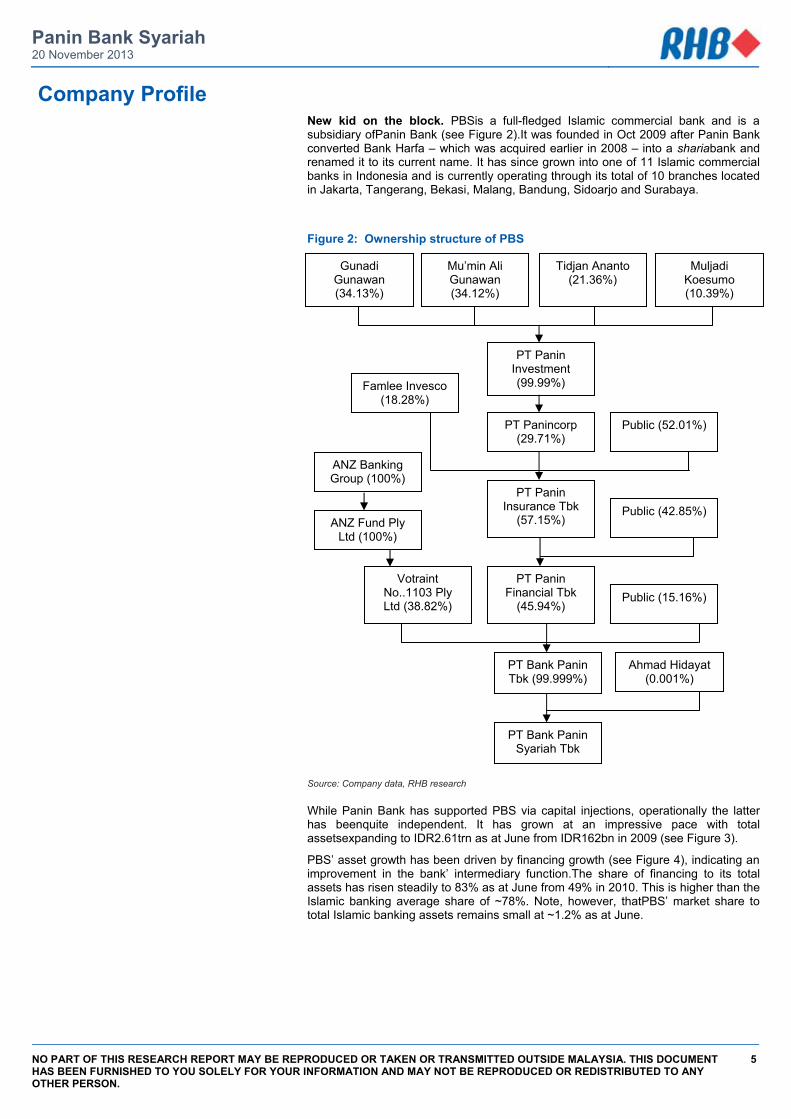

Company Profile New kid on the block. PBSis a full-fledged Islamic commercial bank and is a subsidiary ofPanin Bank (see Figure 2).It was founded in Oct 2009 after Panin Bank converted Bank Harfa – which was acquired earlier in 2008 – into a shariabank and renamed it to its current name. It has since grown into one of 11 Islamic commercial banks in Indonesia and is currently operating through its total of 10 branches located in Jakarta, Tangerang, Bekasi, Malang, Bandung, Sidoarjo and Surabaya.

Figure 2: Ownership structure of PBS

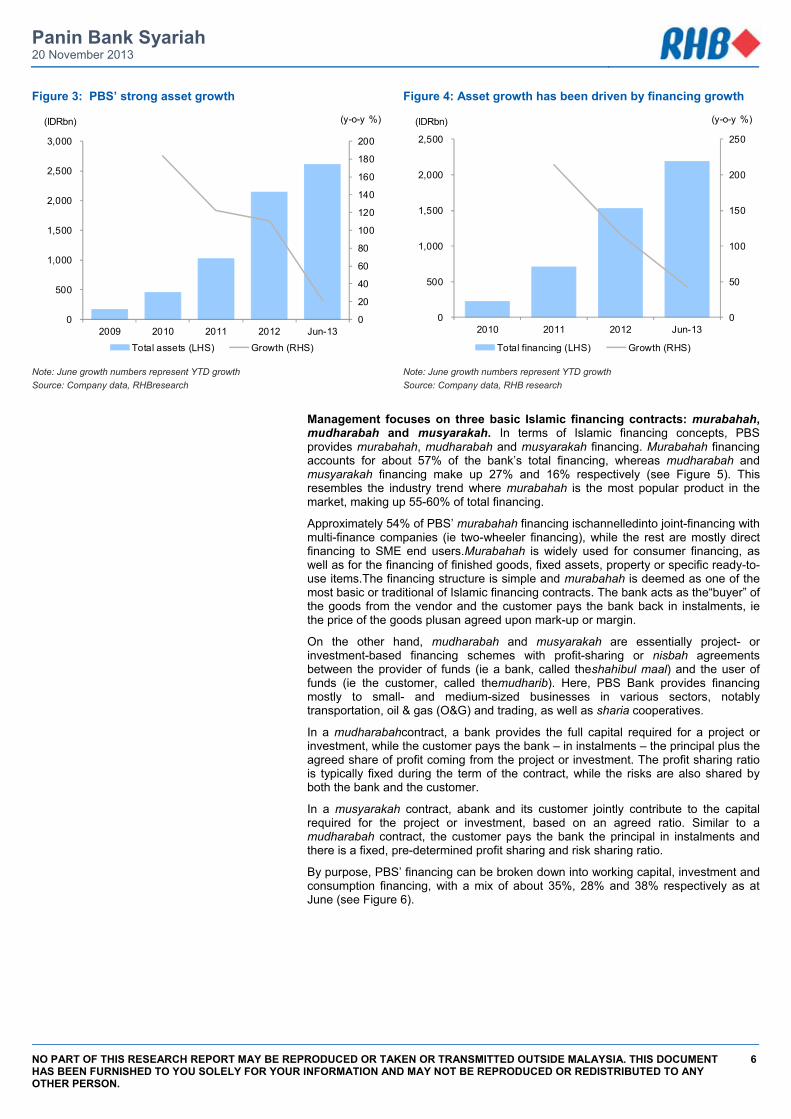

Source: Company data, RHB research While Panin Bank has supported PBS via capital injections, operationally the latter has beenquite independent. It has grown at an impressive pace with total assetsexpanding to IDR2.61trn as at June from IDR162bn in 2009 (see Figure 3).

PBS’ asset growth has been driven by financing growth (see Figure 4), indicating an improvement in the bank’ intermediary function.The share of financing to its total assets has risen steadily to 83% as at June from 49% in 2010. This is higher than the Islamic banking average share of ~78%. Note, however, thatPBS’ market share to total Islamic banking assets remains small at ~1.2% as at June.

Gunadi Gunawan (34.13%)

Mu’min Ali Gunawan (34.12%)

Tidjan Ananto (21.36%)

Muljadi Koesumo (10.39%)

PT Panin Investment (99.99%)

PT Panincorp (29.71%)

Public (52.01%)

Famlee Invesco (18.28%)

PT Panin Insurance Tbk

(57.15%)

PT Panin Financial Tbk

(45.94%)

Public (42.85%)

Public (15.16%) Votraint

No..1103 Ply Ltd (38.82%)

ANZ Fund Ply Ltd (100%)

ANZ Banking Group (100%)

PT Bank Panin Tbk (99.999%)

PT Bank Panin Syariah Tbk

Ahmad Hidayat (0.001%)

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

6

Figure 3: PBS’ strong asset growth Figure 4: Asset growth has been driven by financing growth

Note: June growth numbers represent YTD growth Source: Company data, RHBresearch

Note: June growth numbers represent YTD growth Source: Company data, RHB research

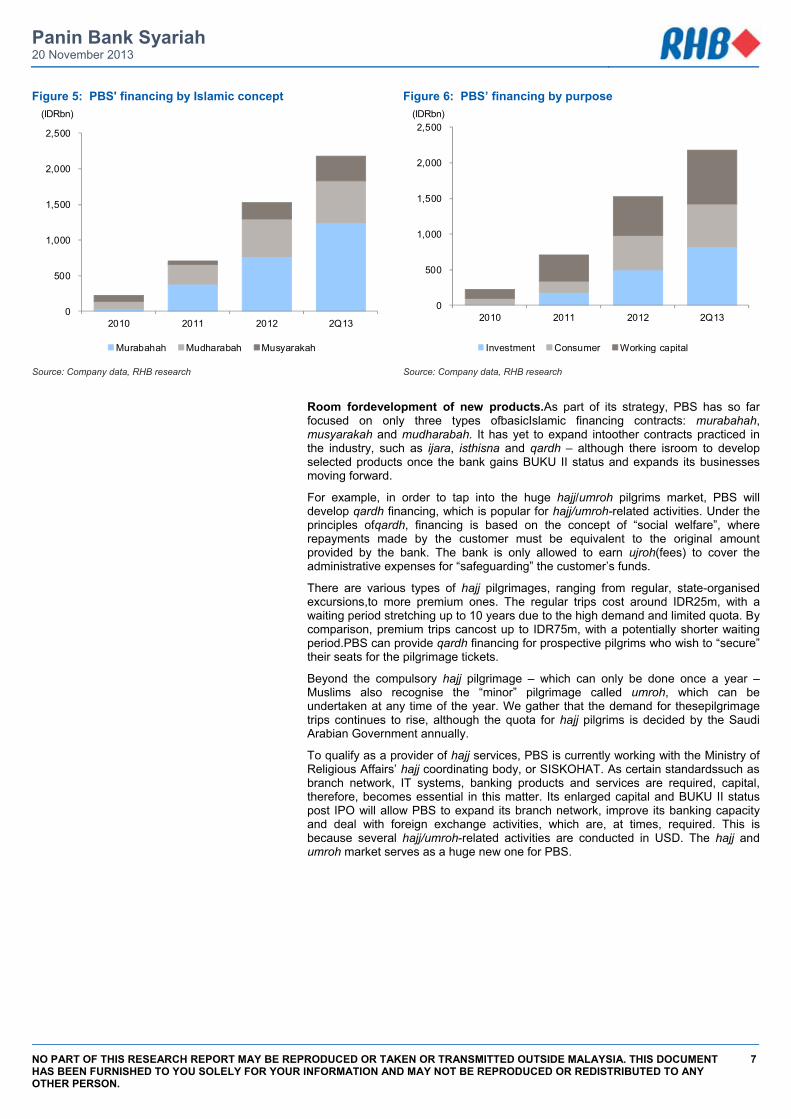

Management focuses on three basic Islamic financing contracts: murabahah, mudharabah and musyarakah. In terms of Islamic financing concepts, PBS provides murabahah, mudharabah and musyarakah financing. Murabahah financing accounts for about 57% of the bank’s total financing, whereas mudharabah and musyarakah financing make up 27% and 16% respectively (see Figure 5). This resembles the industry trend where murabahah is the most popular product in the market, making up 55-60% of total financing.

Approximately 54% of PBS’ murabahah financing ischannelledinto joint-financing with multi-finance companies (ie two-wheeler financing), while the rest are mostly direct financing to SME end users.Murabahah is widely used for consumer financing, as well as for the financing of finished goods, fixed assets, property or specific ready-to-use items.The financing structure is simple and murabahah is deemed as one of the most basic or traditional of Islamic financing contracts. The bank acts as the“buyer” of the goods from the vendor and the customer pays the bank back in instalments, ie the price of the goods plusan agreed upon mark-up or margin.

On the other hand, mudharabah and musyarakah are essentially project- or investment-based financing schemes with profit-sharing or nisbah agreements between the provider of funds (ie a bank, called theshahibul maal) and the user of funds (ie the customer, called themudharib). Here, PBS Bank provides financing mostly to small- and medium-sized businesses in various sectors, notably transportation, oil & gas (O&G) and trading, as well as sharia cooperatives.

In a mudharabahcontract, a bank provides the full capital required for a project or investment, while the customer pays the bank – in instalments – the principal plus the agreed share of profit coming from the project or investment. The profit sharing ratio is typically fixed during the term of the contract, while the risks are also shared by both the bank and the customer.

In a musyarakah contract, abank and its customer jointly contribute to the capital required for the project or investment, based on an agreed ratio. Similar to a mudharabah contract, the customer pays the bank the principal in instalments and there is a fixed, pre-determined profit sharing and risk sharing ratio.

By purpose, PBS’ financing can be broken down into working capital, investment and consumption financing, with a mix of about 35%, 28% and 38% respectively as at June (see Figure 6).

0

20

40

60

80

100

120

140

160

180

200

0

500

1,000

1,500

2,000

2,500

3,000

2009 2010 2011 2012 Jun-13

(y-o-y %)(IDRbn)

Total assets (LHS) Growth (RHS)

0

50

100

150

200

250

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 Jun-13

(y-o-y %)(IDRbn)

Total financing (LHS) Growth (RHS)

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

7

Figure 5: PBS' financing by Islamic concept Figure 6: PBS’ financing by purpose

Source: Company data, RHB research Source: Company data, RHB research

Room fordevelopment of new products.As part of its strategy, PBS has so far focused on only three types ofbasicIslamic financing contracts: murabahah, musyarakah and mudharabah. It has yet to expand intoother contracts practiced in the industry, such as ijara, isthisna and qardh – although there isroom to develop selected products once the bank gains BUKU II status and expands its businesses moving forward.

For example, in order to tap into the huge hajj/umroh pilgrims market, PBS will develop qardh financing, which is popular for hajj/umroh-related activities. Under the principles ofqardh, financing is based on the concept of “social welfare”, where repayments made by the customer must be equivalent to the original amount provided by the bank. The bank is only allowed to earn ujroh(fees) to cover the administrative expenses for “safeguarding” the customer’s funds.

There are various types of hajj pilgrimages, ranging from regular, state-organised excursions,to more premium ones. The regular trips cost around IDR25m, with a waiting period stretching up to 10 years due to the high demand and limited quota. By comparison, premium trips cancost up to IDR75m, with a potentially shorter waiting period.PBS can provide qardh financing for prospective pilgrims who wish to “secure” their seats for the pilgrimage tickets.

Beyond the compulsory hajj pilgrimage – which can only be done once a year – Muslims also recognise the “minor” pilgrimage called umroh, which can be undertaken at any time of the year. We gather that the demand for thesepilgrimage trips continues to rise, although the quota for hajj pilgrims is decided by the Saudi Arabian Government annually.

To qualify as a provider of hajj services, PBS is currently working with the Ministry of Religious Affairs’ hajj coordinating body, or SISKOHAT. As certain standardssuch as branch network, IT systems, banking products and services are required, capital, therefore, becomes essential in this matter. Its enlarged capital and BUKU II status post IPO will allow PBS to expand its branch network, improve its banking capacity and deal with foreign exchange activities, which are, at times, required. This is because several hajj/umroh-related activities are conducted in USD. The hajj and umroh market serves as a huge new one for PBS.

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2Q13

(IDRbn)

Murabahah Mudharabah Musyarakah

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2Q13

(IDRbn)

Investment Consumer Working capital

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

8

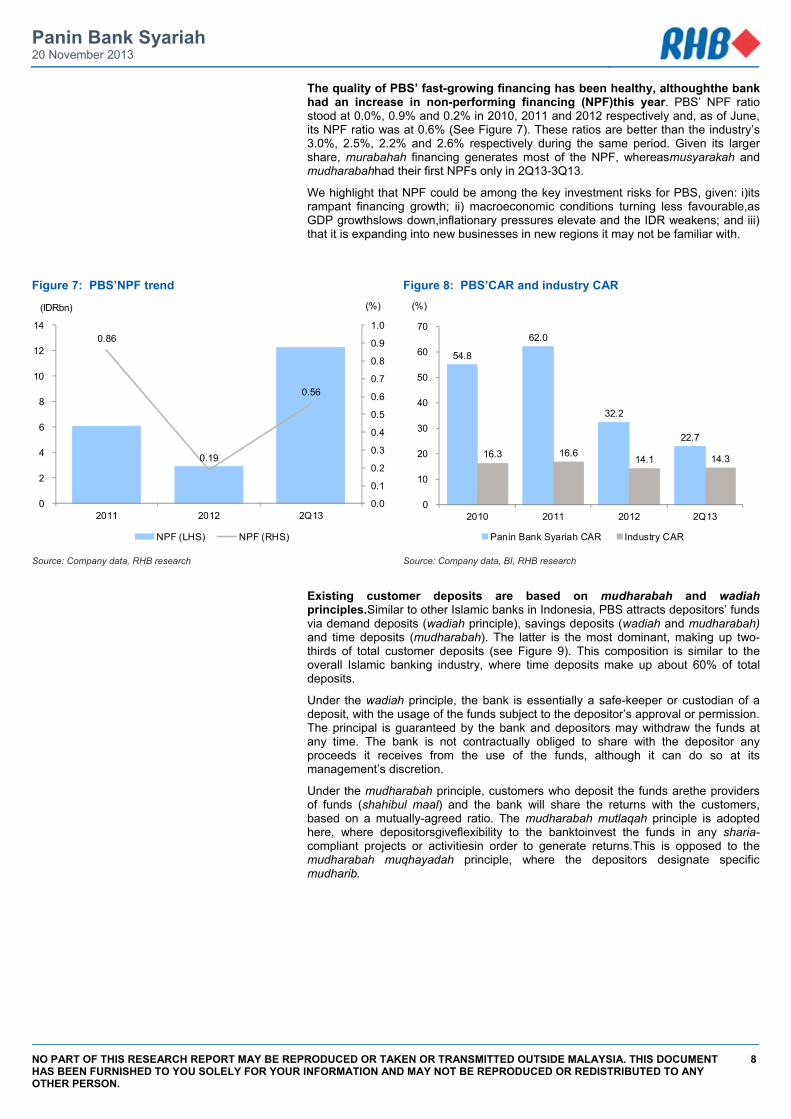

The quality of PBS’ fast-growing financing has been healthy, althoughthe bank had an increase in non-performing financing (NPF)this year. PBS’ NPF ratio stood at 0.0%, 0.9% and 0.2% in 2010, 2011 and 2012 respectively and, as of June, its NPF ratio was at 0.6% (See Figure 7). These ratios are better than the industry’s 3.0%, 2.5%, 2.2% and 2.6% respectively during the same period. Given its larger share, murabahah financing generates most of the NPF, whereasmusyarakah and mudharabahhad their first NPFs only in 2Q13-3Q13.

We highlight that NPF could be among the key investment risks for PBS, given: i)its rampant financing growth; ii) macroeconomic conditions turning less favourable,as GDP growthslows down,inflationary pressures elevate and the IDR weakens; and iii) that it is expanding into new businesses in new regions it may not be familiar with.

Figure 7: PBS’NPF trend Figure 8: PBS’CAR and industry CAR

Source: Company data, RHB research Source: Company data, BI, RHB research

Existing customer deposits are based on mudharabah and wadiah principles.Similar to other Islamic banks in Indonesia, PBS attracts depositors’ funds via demand deposits (wadiah principle), savings deposits (wadiah and mudharabah) and time deposits (mudharabah). The latter is the most dominant, making up two-thirds of total customer deposits (see Figure 9). This composition is similar to the overall Islamic banking industry, where time deposits make up about 60% of total deposits.

Under the wadiah principle, the bank is essentially a safe-keeper or custodian of a deposit, with the usage of the funds subject to the depositor’s approval or permission. The principal is guaranteed by the bank and depositors may withdraw the funds at any time. The bank is not contractually obliged to share with the depositor any proceeds it receives from the use of the funds, although it can do so at its management’s discretion.

Under the mudharabah principle, customers who deposit the funds arethe providers of funds (shahibul maal) and the bank will share the returns with the customers, based on a mutually-agreed ratio. The mudharabah mutlaqah principle is adopted here, where depositorsgiveflexibility to the banktoinvest the funds in any sharia-compliant projects or activitiesin order to generate returns.This is opposed to the mudharabah muqhayadah principle, where the depositors designate specific mudharib.

0.86

0.19

0.56

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0

2

4

6

8

10

12

14

2011 2012 2Q13

(%)(IDRbn)

NPF (LHS) NPF (RHS)

54.8

62.0

32.2

22.7

16.3 16.6 14.1 14.3

0

10

20

30

40

50

60

70

2010 2011 2012 2Q13

(%)

Panin Bank Syariah CAR Industry CAR

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

9

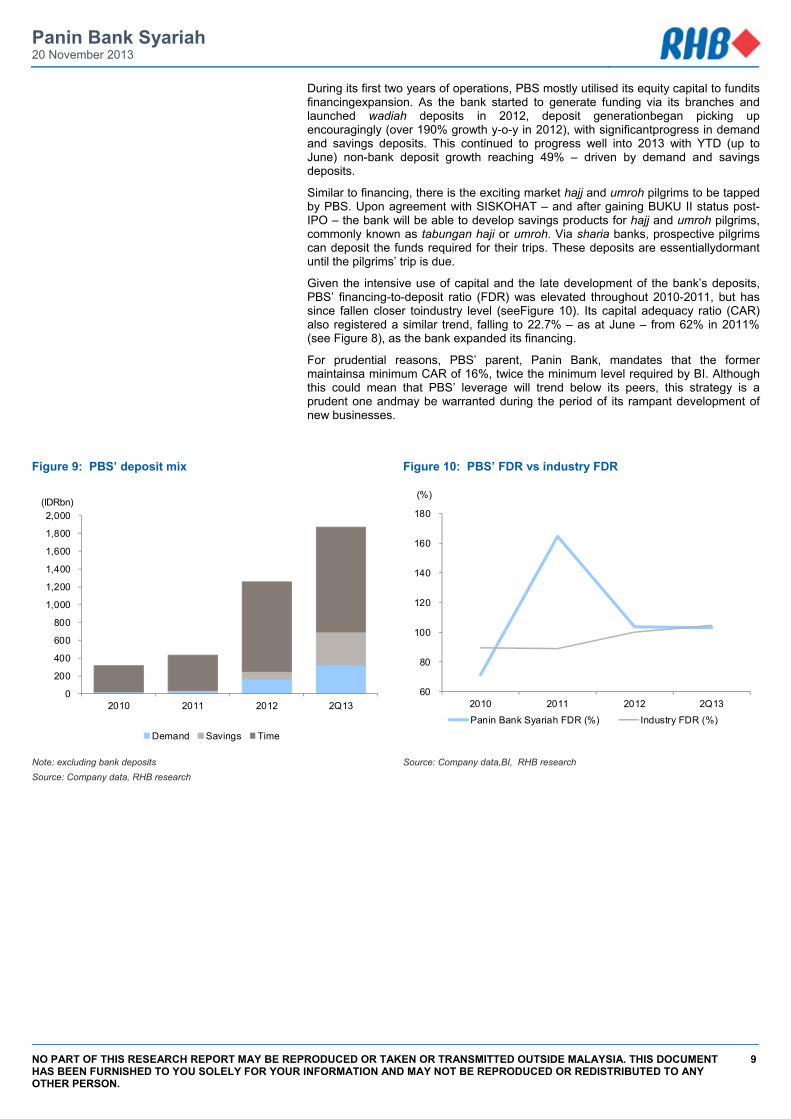

During its first two years of operations, PBS mostly utilised its equity capital to fundits financingexpansion. As the bank started to generate funding via its branches and launched wadiah deposits in 2012, deposit generationbegan picking up encouragingly (over 190% growth y-o-y in 2012), with significantprogress in demand and savings deposits. This continued to progress well into 2013 with YTD (up to June) non-bank deposit growth reaching 49% – driven by demand and savings deposits.

Similar to financing, there is the exciting market hajj and umroh pilgrims to be tapped by PBS. Upon agreement with SISKOHAT – and after gaining BUKU II status post-IPO – the bank will be able to develop savings products for hajj and umroh pilgrims, commonly known as tabungan haji or umroh. Via sharia banks, prospective pilgrims can deposit the funds required for their trips. These deposits are essentiallydormant until the pilgrims’ trip is due.

Given the intensive use of capital and the late development of the bank’s deposits, PBS’ financing-to-deposit ratio (FDR) was elevated throughout 2010-2011, but has since fallen closer toindustry level (seeFigure 10). Its capital adequacy ratio (CAR) also registered a similar trend, falling to 22.7% – as at June – from 62% in 2011% (see Figure 8), as the bank expanded its financing.

For prudential reasons, PBS’ parent, Panin Bank, mandates that the former maintainsa minimum CAR of 16%, twice the minimum level required by BI. Although this could mean that PBS’ leverage will trend below its peers, this strategy is a prudent one andmay be warranted during the period of its rampant development of new businesses.

Figure 9: PBS’ deposit mix Figure 10: PBS’ FDR vs industry FDR

Note: excluding bank deposits Source: Company data, RHB research

Source: Company data,BI, RHB research

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2010 2011 2012 2Q13

(IDRbn)

Demand Savings Time

60

80

100

120

140

160

180

2010 2011 2012 2Q13

(%)

Panin Bank Syariah FDR (%) Industry FDR (%)

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

10

Industry Overview And Outlook

Brief overview of Indonesian Islamic banking industry. The Indonesian Islamic banking industry began in 1991-92, when the first Islamic bank in the country, Bank Muamalat Indonesia, was founded. The country allowsfor the establishment of Islamic banks alongside conventional ones and the landscape remains unchanged until today.

Although Islamic banking started in the early 1990’s, it was only in 2008 that specific regulations concerning Islamic banking (ie Act of Republic of Indonesia Number 21 of 2008) and sukuk were enacted. The Acts not only functions as a legal foundation to develop Islamic banking, but it also suggested that the Government recognised thespecial characteristics and thegrowth potential ofthe sharia banking industry.

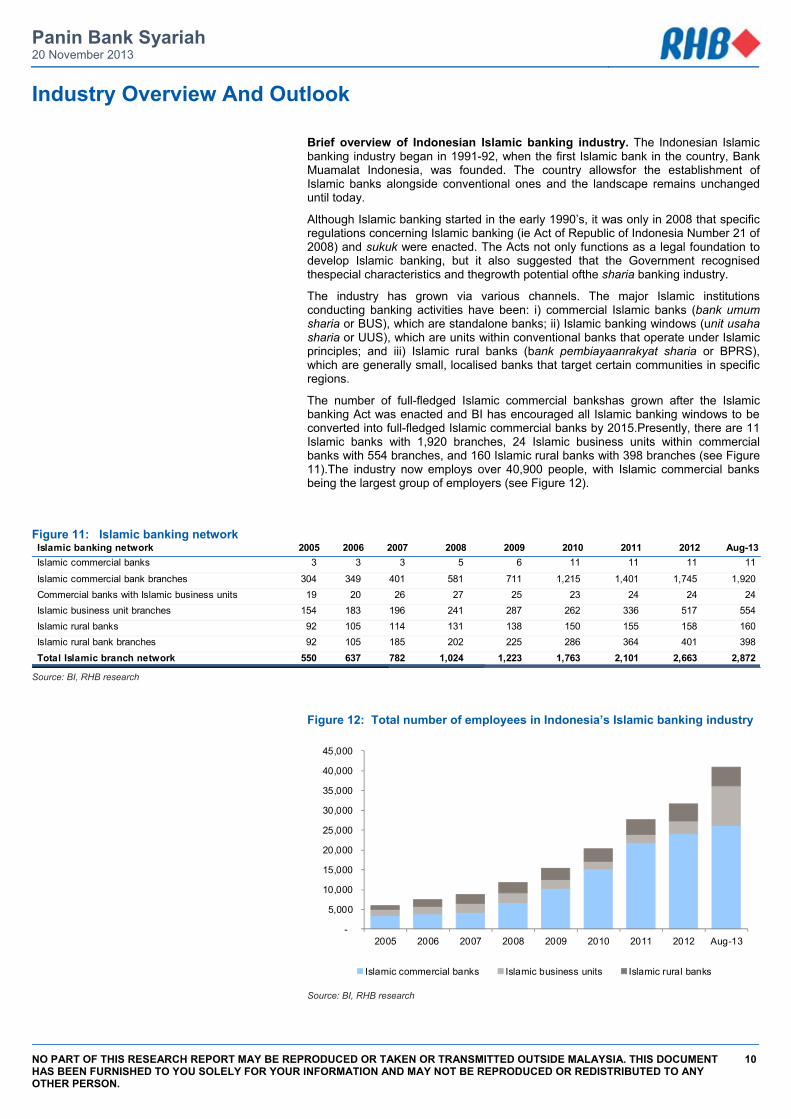

The industry has grown via various channels. The major Islamic institutions conducting banking activities have been: i) commercial Islamic banks (bank umum sharia or BUS), which are standalone banks; ii) Islamic banking windows (unit usaha sharia or UUS), which are units within conventional banks that operate under Islamic principles; and iii) Islamic rural banks (bank pembiayaanrakyat sharia or BPRS), which are generally small, localised banks that target certain communities in specific regions.

The number of full-fledged Islamic commercial bankshas grown after the Islamic banking Act was enacted and BI has encouraged all Islamic banking windows to be converted into full-fledged Islamic commercial banks by 2015.Presently, there are 11 Islamic banks with 1,920 branches, 24 Islamic business units within commercial banks with 554 branches, and 160 Islamic rural banks with 398 branches (see Figure 11).The industry now employs over 40,900 people, with Islamic commercial banks being the largest group of employers (see Figure 12).

Figure 11: Islamic banking network

Source: BI, RHB research

Figure 12: Total number of employees in Indonesia’s Islamic banking industry

Source: BI, RHB research

Islamic banking network 2005 2006 2007 2008 2009 2010 2011 2012 Aug-13Islamic commercial banks 3 3 3 5 6 11 11 11 11

Islamic commercial bank branches 304 349 401 581 711 1,215 1,401 1,745 1,920 Commercial banks with Islamic business units 19 20 26 27 25 23 24 24 24 Islamic business unit branches 154 183 196 241 287 262 336 517 554 Islamic rural banks 92 105 114 131 138 150 155 158 160 Islamic rural bank branches 92 105 185 202 225 286 364 401 398 Total Islamic branch network 550 637 782 1,024 1,223 1,763 2,101 2,663 2,872

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2005 2006 2007 2008 2009 2010 2011 2012 Aug-13

Islamic commercial banks Islamic business units Islamic rural banks

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

11

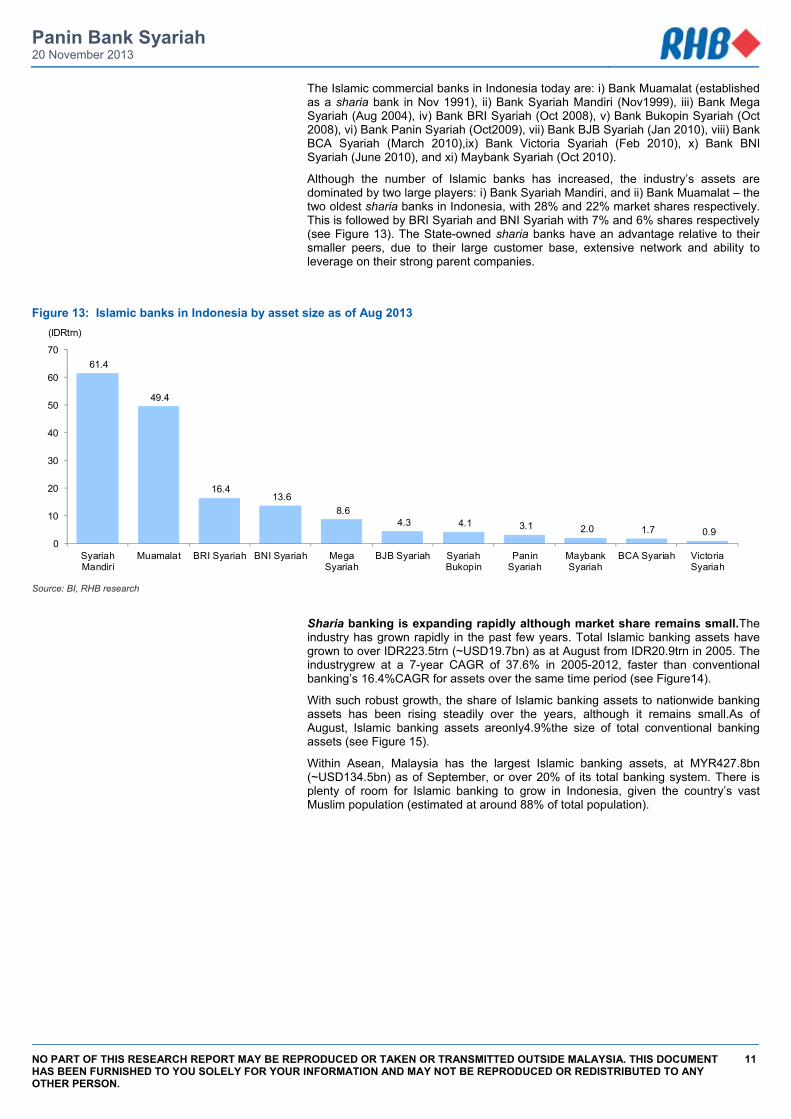

The Islamic commercial banks in Indonesia today are: i) Bank Muamalat (established as a sharia bank in Nov 1991), ii) Bank Syariah Mandiri (Nov1999), iii) Bank Mega Syariah (Aug 2004), iv) Bank BRI Syariah (Oct 2008), v) Bank Bukopin Syariah (Oct 2008), vi) Bank Panin Syariah (Oct2009), vii) Bank BJB Syariah (Jan 2010), viii) Bank BCA Syariah (March 2010),ix) Bank Victoria Syariah (Feb 2010), x) Bank BNI Syariah (June 2010), and xi) Maybank Syariah (Oct 2010).

Although the number of Islamic banks has increased, the industry’s assets are dominated by two large players: i) Bank Syariah Mandiri, and ii) Bank Muamalat – the two oldest sharia banks in Indonesia, with 28% and 22% market shares respectively. This is followed by BRI Syariah and BNI Syariah with 7% and 6% shares respectively (see Figure 13). The State-owned sharia banks have an advantage relative to their smaller peers, due to their large customer base, extensive network and ability to leverage on their strong parent companies.

Figure 13: Islamic banks in Indonesia by asset size as of Aug 2013

Source: BI, RHB research

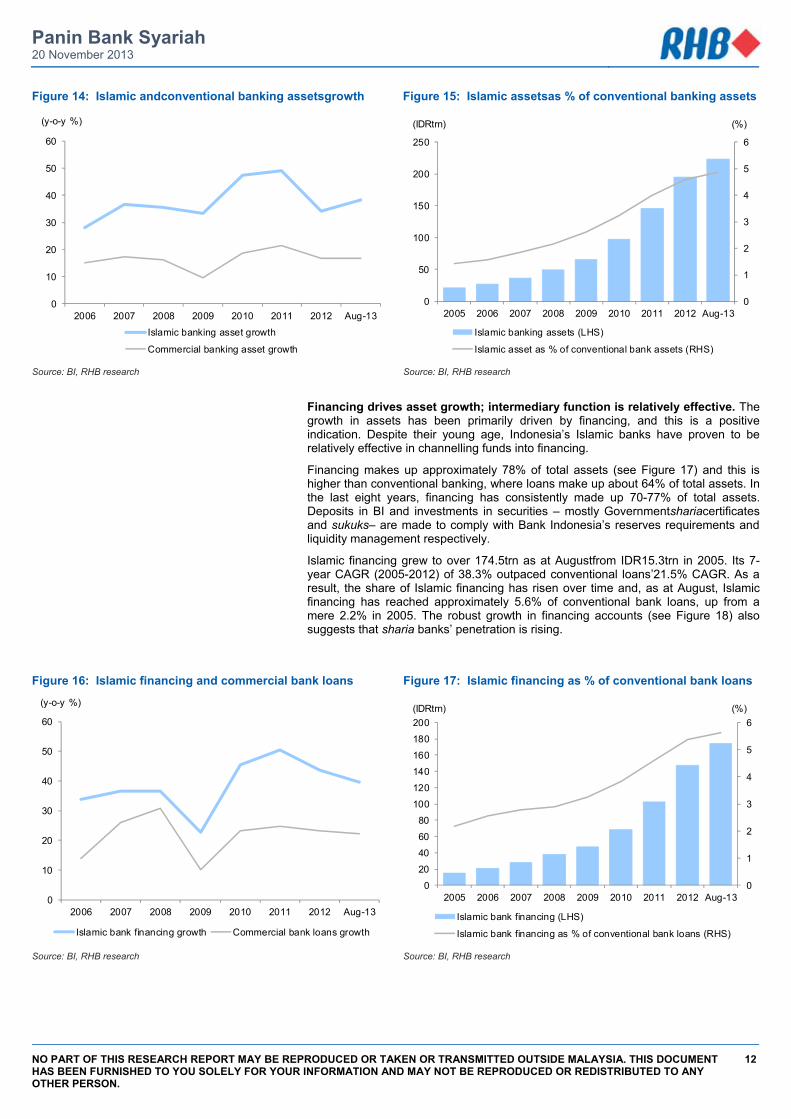

Sharia banking is expanding rapidly although market share remains small.The industry has grown rapidly in the past few years. Total Islamic banking assets have grown to over IDR223.5trn (~USD19.7bn) as at August from IDR20.9trn in 2005. The industrygrew at a 7-year CAGR of 37.6% in 2005-2012, faster than conventional banking’s 16.4%CAGR for assets over the same time period (see Figure14).

With such robust growth, the share of Islamic banking assets to nationwide banking assets has been rising steadily over the years, although it remains small.As of August, Islamic banking assets areonly4.9%the size of total conventional banking assets (see Figure 15).

Within Asean, Malaysia has the largest Islamic banking assets, at MYR427.8bn (~USD134.5bn) as of September, or over 20% of its total banking system. There is plenty of room for Islamic banking to grow in Indonesia, given the country’s vast Muslim population (estimated at around 88% of total population).

61.4

49.4

16.4 13.6

8.6 4.3 4.1 3.1 2.0 1.7 0.9

0

10

20

30

40

50

60

70

SyariahMandiri

Muamalat BRI Syariah BNI Syariah MegaSyariah

BJB Syariah SyariahBukopin

PaninSyariah

MaybankSyariah

BCA Syariah VictoriaSyariah

(IDRtrn)

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

12

Figure 14: Islamic andconventional banking assetsgrowth Figure 15: Islamic assetsas % of conventional banking assets

Source: BI, RHB research Source: BI, RHB research

Financing drives asset growth; intermediary function is relatively effective. The growth in assets has been primarily driven by financing, and this is a positive indication. Despite their young age, Indonesia’s Islamic banks have proven to be relatively effective in channelling funds into financing.

Financing makes up approximately 78% of total assets (see Figure 17) and this is higher than conventional banking, where loans make up about 64% of total assets. In the last eight years, financing has consistently made up 70-77% of total assets. Deposits in BI and investments in securities – mostly Governmentshariacertificates and sukuks– are made to comply with Bank Indonesia’s reserves requirements and liquidity management respectively.

Islamic financing grew to over 174.5trn as at Augustfrom IDR15.3trn in 2005. Its 7-year CAGR (2005-2012) of 38.3% outpaced conventional loans’21.5% CAGR. As a result, the share of Islamic financing has risen over time and, as at August, Islamic financing has reached approximately 5.6% of conventional bank loans, up from a mere 2.2% in 2005. The robust growth in financing accounts (see Figure 18) also suggests that sharia banks’ penetration is rising.

Figure 16: Islamic financing and commercial bank loans Figure 17: Islamic financing as % of conventional bank loans

Source: BI, RHB research Source: BI, RHB research

0

10

20

30

40

50

60

2006 2007 2008 2009 2010 2011 2012 Aug-13

(y-o-y %)

Islamic banking asset growth

Commercial banking asset growth

0

1

2

3

4

5

6

0

50

100

150

200

250

2005 2006 2007 2008 2009 2010 2011 2012 Aug-13

(%)(IDRtrn)

Islamic banking assets (LHS)

Islamic asset as % of conventional bank assets (RHS)

0

10

20

30

40

50

60

2006 2007 2008 2009 2010 2011 2012 Aug-13

(y-o-y %)

Islamic bank financing growth Commercial bank loans growth

0

1

2

3

4

5

6

0

20

40

60

80

100

120

140

160

180

200

2005 2006 2007 2008 2009 2010 2011 2012 Aug-13

(%)(IDRtrn)

Islamic bank financing (LHS)

Islamic bank financing as % of conventional bank loans (RHS)

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

13

Figure 18: Growth of financing accounts in Islamic banks Figure 19: Composition of assets in Islamic banks

Source: BI, RHB research Source: BI, RHB research

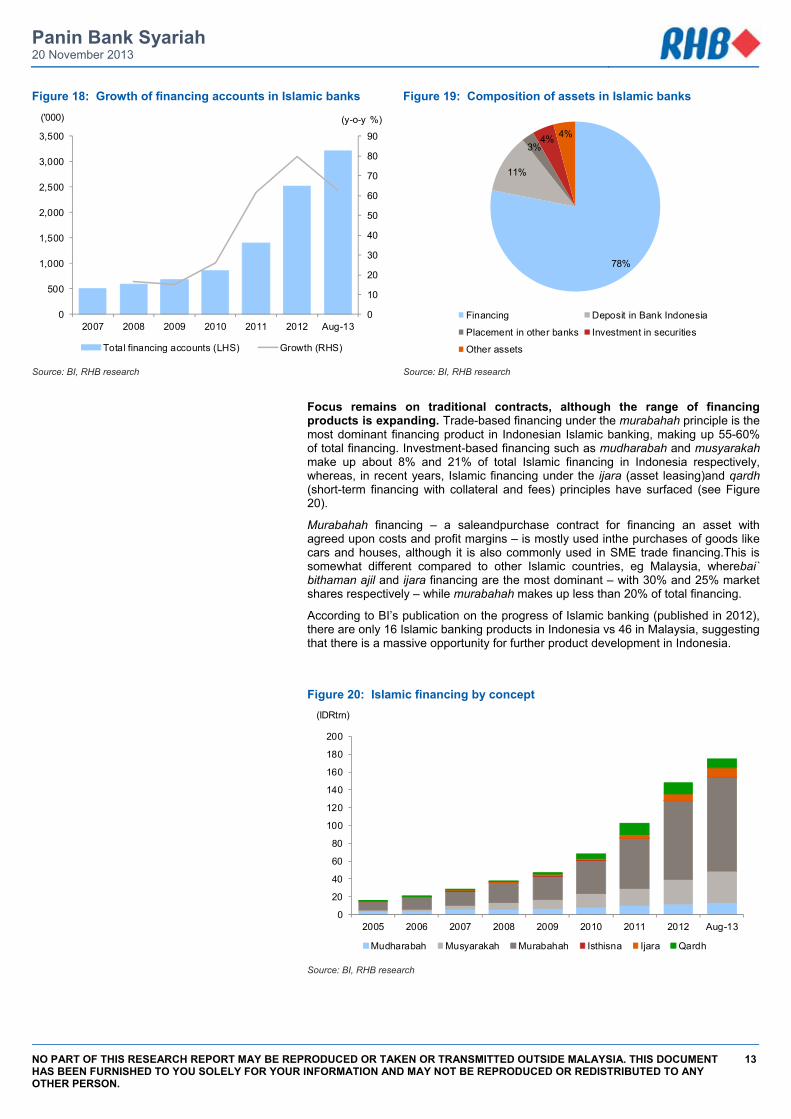

Focus remains on traditional contracts, although the range of financing products is expanding. Trade-based financing under the murabahah principle is the most dominant financing product in Indonesian Islamic banking, making up 55-60% of total financing. Investment-based financing such as mudharabah and musyarakah make up about 8% and 21% of total Islamic financing in Indonesia respectively, whereas, in recent years, Islamic financing under the ijara (asset leasing)and qardh (short-term financing with collateral and fees) principles have surfaced (see Figure 20).

Murabahah financing – a saleandpurchase contract for financing an asset with agreed upon costs and profit margins – is mostly used inthe purchases of goods like cars and houses, although it is also commonly used in SME trade financing.This is somewhat different compared to other Islamic countries, eg Malaysia, wherebai` bithaman ajil and ijara financing are the most dominant – with 30% and 25% market shares respectively – while murabahah makes up less than 20% of total financing.

According to BI’s publication on the progress of Islamic banking (published in 2012), there are only 16 Islamic banking products in Indonesia vs 46 in Malaysia, suggesting that there is a massive opportunity for further product development in Indonesia.

Figure 20: Islamic financing by concept

Source: BI, RHB research

0

10

20

30

40

50

60

70

80

90

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2007 2008 2009 2010 2011 2012 Aug-13

(y-o-y %)('000)

Total financing accounts (LHS) Growth (RHS)

78%

11%

3%4% 4%

Financing Deposit in Bank Indonesia

Placement in other banks Investment in securities

Other assets

0

20

40

60

80

100

120

140

160

180

200

2005 2006 2007 2008 2009 2010 2011 2012 Aug-13

(IDRtrn)

Mudharabah Musyarakah Murabahah Isthisna Ijara Qardh

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

14

Figure 21: Islamic financing mix by purpose Figure 22: Islamic financing growth by purpose

Source: BI, RHB research Source: BI, RHB research

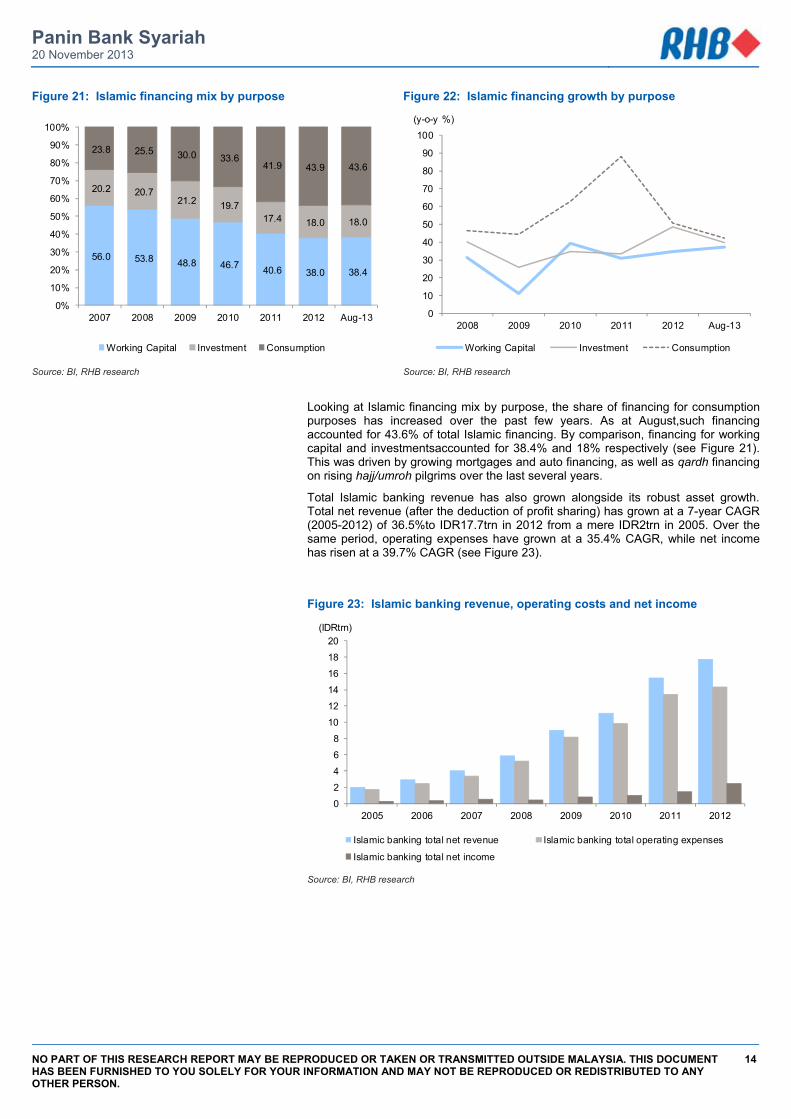

Looking at Islamic financing mix by purpose, the share of financing for consumption purposes has increased over the past few years. As at August,such financing accounted for 43.6% of total Islamic financing. By comparison, financing for working capital and investmentsaccounted for 38.4% and 18% respectively (see Figure 21). This was driven by growing mortgages and auto financing, as well as qardh financing on rising hajj/umroh pilgrims over the last several years.

Total Islamic banking revenue has also grown alongside its robust asset growth. Total net revenue (after the deduction of profit sharing) has grown at a 7-year CAGR (2005-2012) of 36.5%to IDR17.7trn in 2012 from a mere IDR2trn in 2005. Over the same period, operating expenses have grown at a 35.4% CAGR, while net income has risen at a 39.7% CAGR (see Figure 23).

Figure 23: Islamic banking revenue, operating costs and net income

Source: BI, RHB research

56.0 53.8 48.8 46.7 40.6 38.0 38.4

20.2 20.7 21.2 19.7

17.4 18.0 18.0

23.8 25.5 30.0 33.6 41.9 43.9 43.6

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 Aug-13

Working Capital Investment Consumption

0

10

20

30

40

50

60

70

80

90

100

2008 2009 2010 2011 2012 Aug-13

(y-o-y %)

Working Capital Investment Consumption

0

2

4

6

8

10

12

14

16

18

20

2005 2006 2007 2008 2009 2010 2011 2012

(IDRtrn)

Islamic banking total net revenue Islamic banking total operating expenses

Islamic banking total net income

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

15

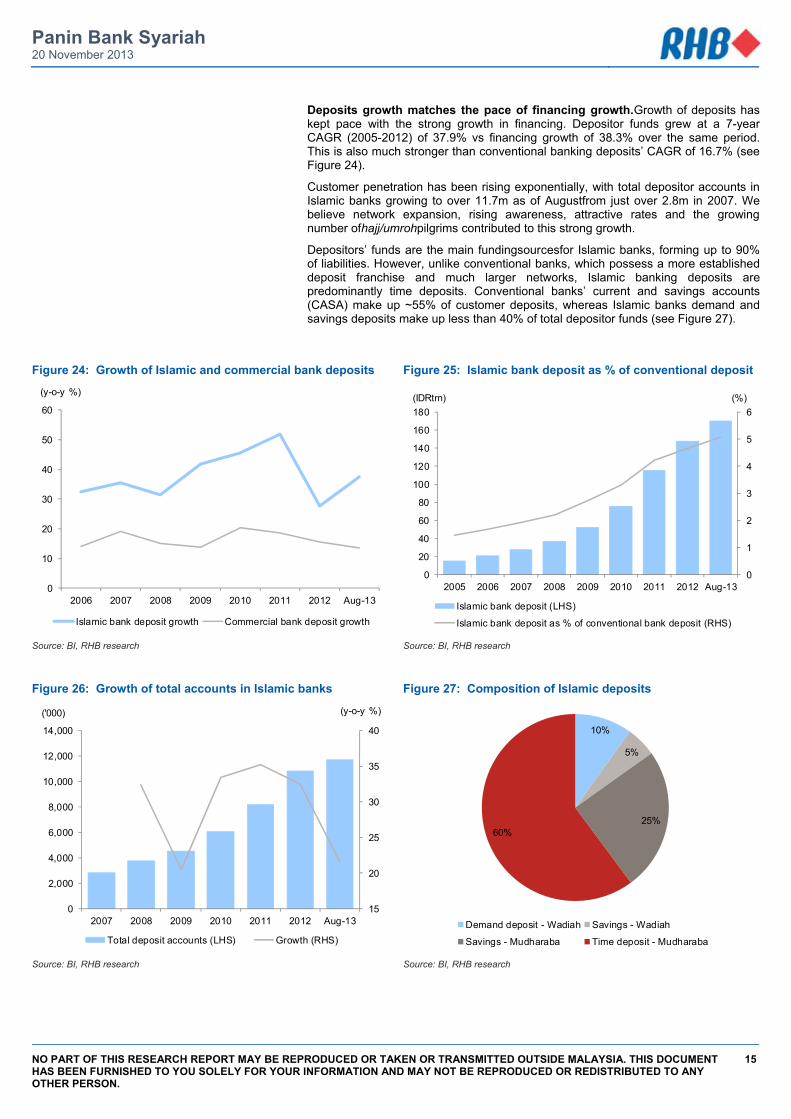

Deposits growth matches the pace of financing growth.Growth of deposits has kept pace with the strong growth in financing. Depositor funds grew at a 7-year CAGR (2005-2012) of 37.9% vs financing growth of 38.3% over the same period. This is also much stronger than conventional banking deposits’ CAGR of 16.7% (see Figure 24).

Customer penetration has been rising exponentially, with total depositor accounts in Islamic banks growing to over 11.7m as of Augustfrom just over 2.8m in 2007. We believe network expansion, rising awareness, attractive rates and the growing number ofhajj/umrohpilgrims contributed to this strong growth.

Depositors’ funds are the main fundingsourcesfor Islamic banks, forming up to 90% of liabilities. However, unlike conventional banks, which possess a more established deposit franchise and much larger networks, Islamic banking deposits are predominantly time deposits. Conventional banks’ current and savings accounts (CASA) make up ~55% of customer deposits, whereas Islamic banks demand and savings deposits make up less than 40% of total depositor funds (see Figure 27).

Figure 24: Growth of Islamic and commercial bank deposits Figure 25: Islamic bank deposit as % of conventional deposit

Source: BI, RHB research Source: BI, RHB research

Figure 26: Growth of total accounts in Islamic banks Figure 27: Composition of Islamic deposits

Source: BI, RHB research Source: BI, RHB research

0

10

20

30

40

50

60

2006 2007 2008 2009 2010 2011 2012 Aug-13

(y-o-y %)

Islamic bank deposit growth Commercial bank deposit growth

0

1

2

3

4

5

6

0

20

40

60

80

100

120

140

160

180

2005 2006 2007 2008 2009 2010 2011 2012 Aug-13

(%)(IDRtrn)

Islamic bank deposit (LHS)

Islamic bank deposit as % of conventional bank deposit (RHS)

15

20

25

30

35

40

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2007 2008 2009 2010 2011 2012 Aug-13

(y-o-y %)('000)

Total deposit accounts (LHS) Growth (RHS)

10%

5%

25%60%

Demand deposit - Wadiah Savings - Wadiah

Savings - Mudharaba Time deposit - Mudharaba

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

16

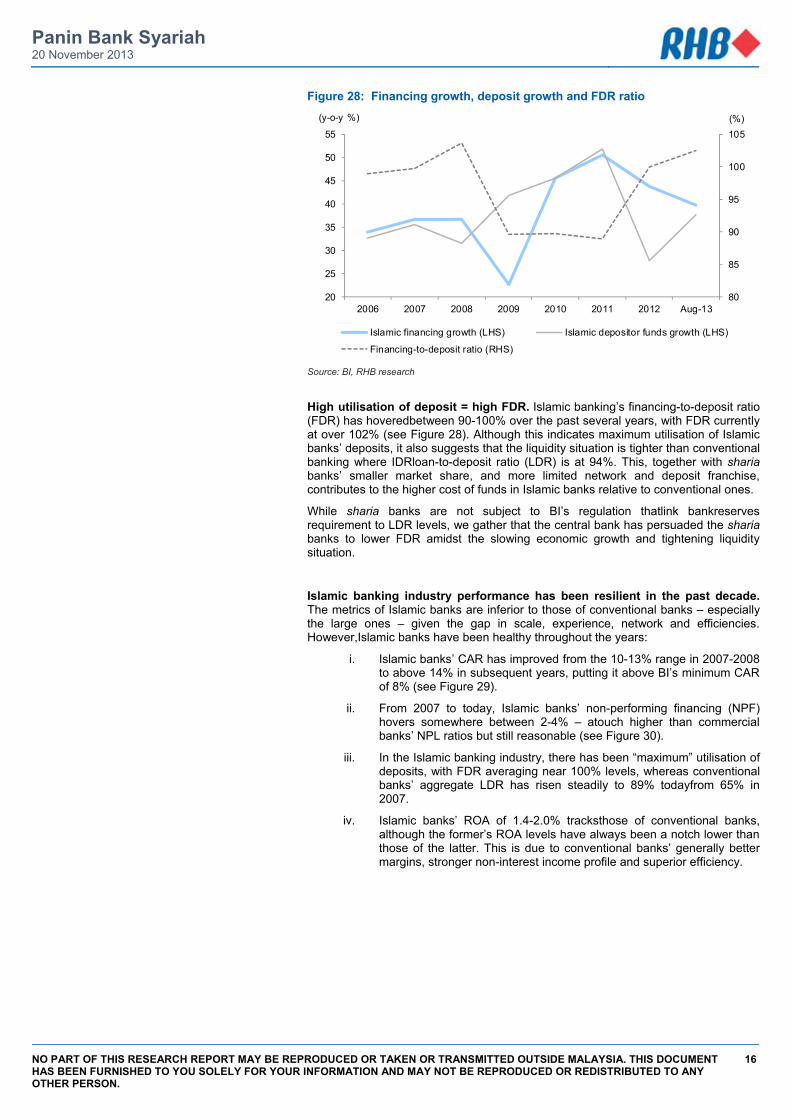

Figure 28: Financing growth, deposit growth and FDR ratio

Source: BI, RHB research

High utilisation of deposit = high FDR. Islamic banking’s financing-to-deposit ratio (FDR) has hoveredbetween 90-100% over the past several years, with FDR currently at over 102% (see Figure 28). Although this indicates maximum utilisation of Islamic banks’ deposits, it also suggests that the liquidity situation is tighter than conventional banking where IDRloan-to-deposit ratio (LDR) is at 94%. This, together with sharia banks’ smaller market share, and more limited network and deposit franchise, contributes to the higher cost of funds in Islamic banks relative to conventional ones.

While sharia banks are not subject to BI’s regulation thatlink bankreserves requirement to LDR levels, we gather that the central bank has persuaded the sharia banks to lower FDR amidst the slowing economic growth and tightening liquidity situation.

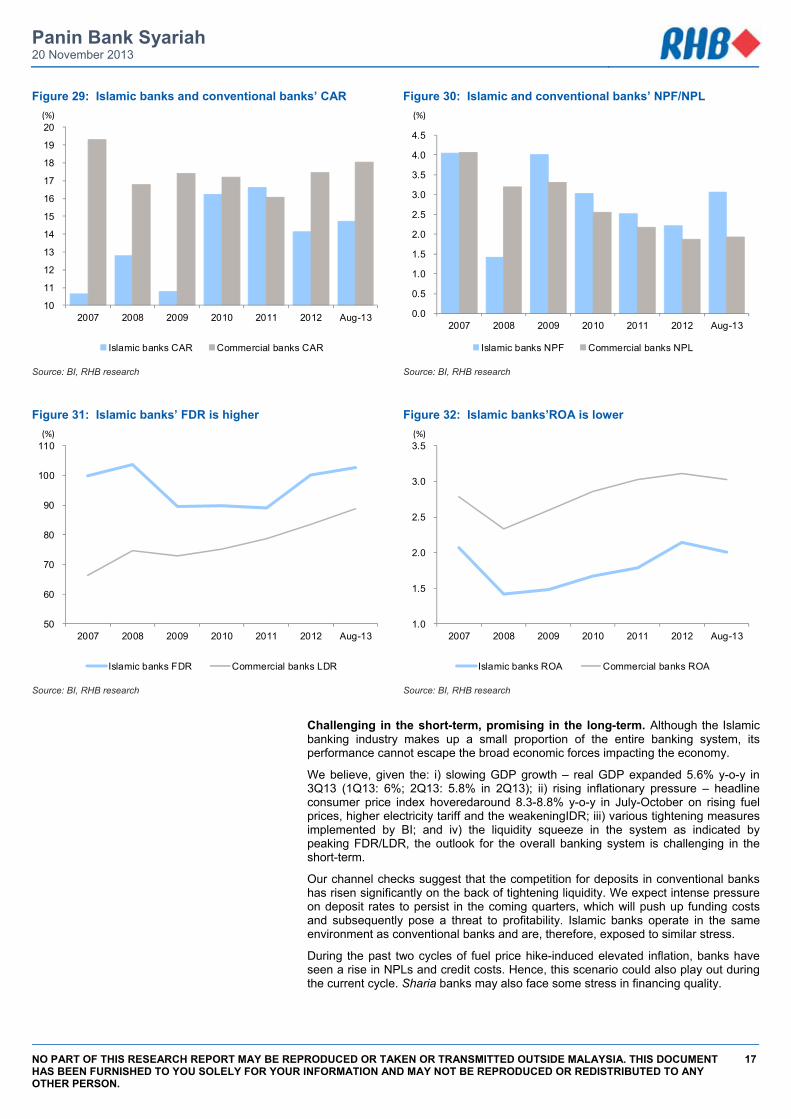

Islamic banking industry performance has been resilient in the past decade. The metrics of Islamic banks are inferior to those of conventional banks – especially the large ones – given the gap in scale, experience, network and efficiencies. However,Islamic banks have been healthy throughout the years:

i. Islamic banks’ CAR has improved from the 10-13% range in 2007-2008 to above 14% in subsequent years, putting it above BI’s minimum CAR of 8% (see Figure 29).

ii. From 2007 to today, Islamic banks’ non-performing financing (NPF) hovers somewhere between 2-4% – atouch higher than commercial banks’ NPL ratios but still reasonable (see Figure 30).

iii. In the Islamic banking industry, there has been “maximum” utilisation of deposits, with FDR averaging near 100% levels, whereas conventional banks’ aggregate LDR has risen steadily to 89% todayfrom 65% in 2007.

iv. Islamic banks’ ROA of 1.4-2.0% tracksthose of conventional banks, although the former’s ROA levels have always been a notch lower than those of the latter. This is due to conventional banks’ generally better margins, stronger non-interest income profile and superior efficiency.

80

85

90

95

100

105

20

25

30

35

40

45

50

55

2006 2007 2008 2009 2010 2011 2012 Aug-13

(%)(y-o-y %)

Islamic financing growth (LHS) Islamic depositor funds growth (LHS)

Financing-to-deposit ratio (RHS)

Panin Bank Syariah 20 November 2013

NO PART OF THIS RESEARCH REPORT MAY BE REPRODUCED OR TAKEN OR TRANSMITTED OUTSIDE MALAYSIA. THIS DOCUMENT HAS BEEN FURNISHED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON.

17

Figure 29: Islamic banks and conventional banks’ CAR Figure 30: Islamic and conventional banks’ NPF/NPL

Source: BI, RHB research Source: BI, RHB research

Figure 31: Islamic banks’ FDR is higher Figure 32: Islamic banks’ROA is lower

Source: BI, RHB research Source: BI, RHB research

Challenging in the short-term, promising in the long-term. Although the Islamic banking industry makes up a small proportion of the entire banking system, its performance cannot escape the broad economic forces impacting the economy.

We believe, given the: i) slowing GDP growth – real GDP expanded 5.6% y-o-y in 3Q13 (1Q13: 6%; 2Q13: 5.8% in 2Q13); ii) rising inflationary pressure – headline consumer price index hoveredaround 8.3-8.8% y-o-y in July-October on rising fuel prices, higher electricity tariff and the weakeningIDR; iii) various tightening measures implemented by BI; and iv) the liquidity squeeze in the system as indicated by peaking FDR/LDR, the outlook for the overall banking system is challenging in the short-term.

Our channel checks suggest that the competition for deposits in conventional banks has risen significantly on the back of tightening liquidity. We expect intense pressure on deposit rates to persist in the coming quarters, which will push up funding costs and subsequently pose a threat to profitability. Islamic banks operate in the same environment as conventional banks and are, therefore, exposed to similar stress.