Embed Size (px)

Citation preview

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 1/41

Transer pricingperspectives*

The emerging perect storm o transerpricing audits and disputes

*connectedthinking

Thought Leadership Journal

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 2/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

Table o contents The emerging “perect storm” 3

Permanent establishments: The denitional battleground 9

Global best practices in avoiding transer pricing audits and disputes 19

Mandatory binding arbitration 29

The challenge o “triangular” transer pricing cases 41

APA and MAP programs: Steps or improvements 49

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 3/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

The emerging “perect storm”

Global tax audits, controversies, anddispute resolutionToday’s multinational corporations (MNCs) are acing the most challenging

tax environment in history because o a combination o our global orcesconverging to create a “perect storm.” The unstable environment createdby these orces is resulting in a substantial increase in the number and sizeo transer pricing audits, adjustments and disputes. This new environmentplaces a premium on audit and dispute avoidance techniques. This paperdiscusses these our global orces and looks at proactive steps, includingresolution techniques, MNCs can take to weather the storm.

The rst o these global orces is creating a surge o transer pricing auditsand disputes around the world. Fiscal demands on developed and emergingcountries (including inrastructure and entitlement demands) are placingsignicant pressure on governments to raise revenue and prevent baseerosion. At the same time, the Organisation or Economic Cooperation andDevelopment (OECD) has reported that tax revenue in 20 o the largestcountries is near all-time highs as a percentage o gross domestic product.These actors are orcing nations to continually pursue revenue enhancementinitiatives and enorcement activities to meet increasing scal demands.

As nations step up their eorts, the number o transer pricing audits anddisputes climbs.

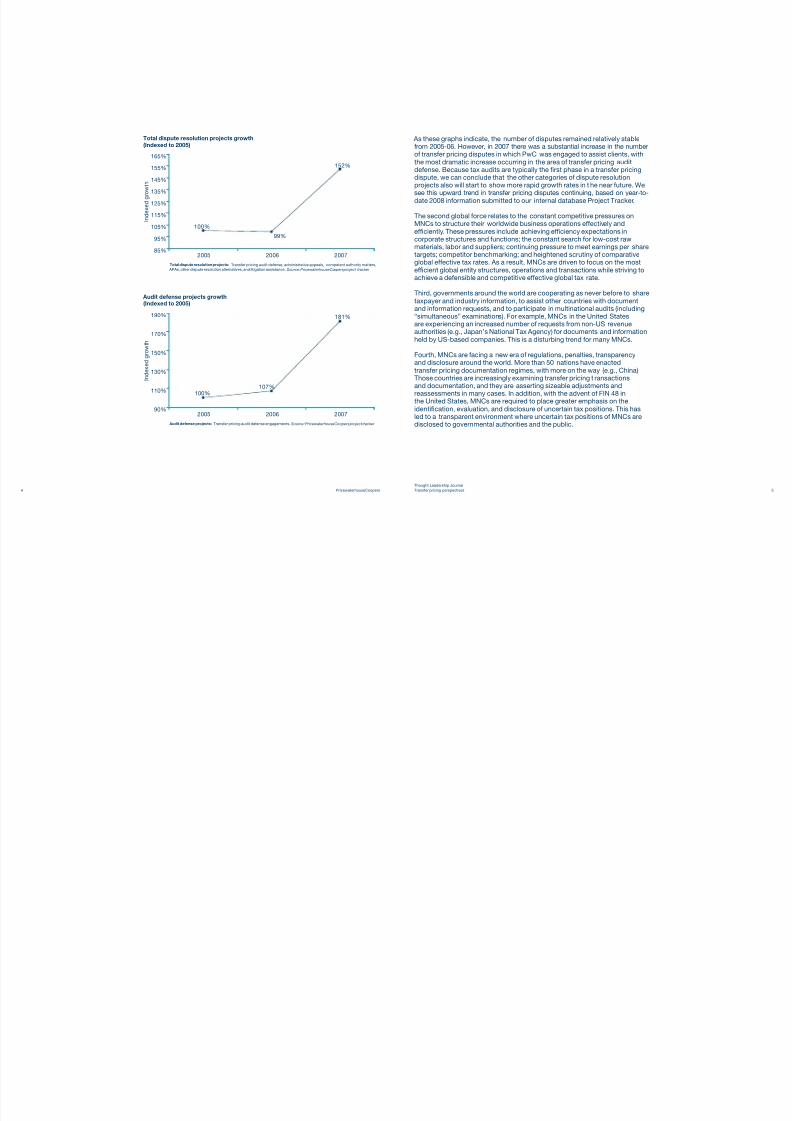

Evidence o this trend can be seen in data obtained during a clientengagement by a team o transer pricing specialists across our globalnetwork o rms. The graphs below show the trend lines or (i) transer pricingdispute engagements, which totals in the hundreds, and (ii) a subcategory odisputes—total transer pricing audit deense engagements—or the period

rom 2005-07 (with the index base years set as o 2005). We have broadlydened “disputes” or this analysis to include audits, administrative appeals,competent authority matters, advance pricing agreements (APAs), litigationassistance, and other dispute resolution alternatives.

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 4/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

As these graphs indicate, the number o disputes remained relatively stablerom 2005-06. However, in 2007 there was a substantial increase in the numbero transer pricing disputes in which PwC was engaged to assist clients, withthe most dramatic increase occurring in the area o transer pricing auditdeense. Because tax audits are typically the rst phase in a transer pricingdispute, we can conclude that the other categories o dispute resolutionprojects also will start to show more rapid growth rates in t he near uture. We

see this upward trend in transer pricing disputes continuing, based on year-to-date 2008 inormation submitted to our internal database Project Tracker.

The second global orce relates to the constant competitive pressures onMNCs to structure their worldwide business operations eectively andeciently. These pressures include achieving eciency expectations incorporate structures and unctions; the constant search or low-cost rawmaterials, labor and suppliers; continuing pressure to meet earnings per sharetargets; competitor benchmarking; and heightened scrutiny o comparativeglobal eective tax rates. As a result, MNCs are driven to ocus on the mostecient global entity structures, operations and transactions while striving toachieve a deensible and competitive eective global tax rate.

Third, governments around the world are cooperating as never beore to sharetaxpayer and industry inormation, to assist other countries with documentand inormation requests, and to participate in multinational audits (including“simultaneous” examinations). For example, MNCs in the United Statesare experiencing an increased number o requests rom non-US revenueauthorities (e.g., Japan’s National Tax Agency) or documents and inormationheld by US-based companies. This is a disturbing trend or many MNCs.

Fourth, MNCs are acing a new era o regulations, penalties, transparencyand disclosure around the world. More than 50 nations have enactedtranser pricing documentation regimes, with more on the way (e.g., China).Those countries are increasingly examining transer pricing t ransactionsand documentation, and they are asserting sizeable adjustments and

reassessments in many cases. In addition, with the advent o FIN 48 inthe United States, MNCs are required to place greater emphasis on theidentication, evaluation, and disclosure o uncertain tax positions. This hasled to a transparent environment where uncertain tax positions o MNCs aredisclosed to governmental authorities and the public.

Total dispute resolution projects growth

(Indexed to 2005)

Audit deense projects growth(Indexed to 2005)

2005 2006 200790%

110%

130%

150%

170%

190%

I n d e x e d g r o w t h

Audit defense projects: Transfer pricing audit defense engagements. Source: PricewaterhouseCoopers project tracker

100%

107%

181%

2005 2006 200785%

95%

105%

115%

125%

135%

145%

155%

165%

I n d e x e d g r

o w t h

Total dispute resolution projects: Transfer pricing audit defense, administrative appeals, competent authority matters,

APAs, other dispute resolution alternatives, and litigation assistance. Source: PricewaterhouseCoopers project tracker

100%

99%

152%

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 5/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

MNCs need to develop centralized points o contact within the globalenterprise, and they need t o apply coordinated actions in monitoring andresponding to transer pricing examinations and disputes. Because theresolution o a transer pricing dispute in one country may have prooundramications or the same taxpayer in other jurisdictions, MNCs need torevisit their use o one-o approaches to handling audits and disputes in theirorganizations. The key to achieving successul results will be coordinated

global strategic planning, with local tactical implementation. I properlyplanned and implemented, these steps should assist MNCs in avoiding certaintranser pricing audits and disputes and ultimately achieving the most ecientand avorable results or the company.

In responding to the emerging “perect storm,” this issue o Transer PricingPerspectives ocuses on several important global dispute resolution topics,including recent developments involving the taxation o PEs, recommendedimprovements to APAs and Mutual Agreement Procedures (MAPs) around theworld, and “best practices” in the global dispute resolution arena. This editionalso will identiy the challenges presented by “triangular” transer pricing casesand consider the possible eect o t he new mandatory binding arbitrationprovisions in several recent international tax treaties. This new era o globaltax audits and disputes raises numerous challenges or MNCs and theiradvisors—are you prepared or the storm?

C. David Swenson

Washington, D.C.PwC’s Global Tax Dispute Resolution Leader

Garry B. Stone

Chicago, ILPwC’s Global Transer Pricing Leader

These our global orces have coalesced to create an unstable climate orMNCs, resulting in a substantial increase in the number and size o transerpricing audits, adjustments, and disputes. As part o this process, weare experiencing an unusual “commonality o issues and controversies”around the world, ranging rom permanent establishment (PE) audits andcontroversies in India, Korea and France; to “guarantee ee” cases in Canada,

Australia and Japan; to “marketing intangibles” issues in the United States,

the United Kingdom and many other countries. Likewise, disputes areincreasingly commonplace throughout the world concerning the allocation omanagement ees and the proper treatment o “equity-based” compensationin cost pools or transer pricing purposes.

This surge in audits and disputes is placing signicant strain on the traditionalmethods o resolving transer pricing controversies: audit-level settlements,administrative appeals, mediation, APAs (with rollback eatures), competentauthority negotiations, arbitration, and litigation. In addition, many expertsexpect that growing pressure rom the FIN 48 disclosure requirementsmay lead a large number o companies to seek the certainty o traditionalbilateral advance pricing agreements, thereby increasing the demands on

APA and competent authority oces around the globe. Furthermore, thelatest statistics show that more than 75 percent o the inventory o the UScompetent authority oce relates to “oreign initiated” adjustments, and thishas led to an increased Internal Revenue Service ocus on the “exhaustiono remedies” by US taxpayers in non-US jurisdictions, as well as the relatedoreign tax credit ramications.

This new environment places a premium on audit and dispute avoidancetechniques. Transer pricing audit and dispute avoidance includes not only thepreparation o “quality” transer pricing documentation, but also the properstructuring o entities, unctions and risks; the preparation o appropriateintercompany agreements; and periodic “course o conduct” audits. In thenew global tax environment, MNCs must be proactive (not reactive), and theyneed to adopt holistic approaches (not ragmented responses) to tax audits

and controversies. These steps include implementing policies to avoid transerpricing audits and disputes rom the beginning o a project or transaction,including proactive use o APAs.

David Swenson

Garry Stone

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 6/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

Permanent establishments:

The denitional backgroundBy: Joseph Andrus (US) and Richard Stuart Collier (UK)

Rules dening tax jurisdiction are a oundational element o any system ointernational taxation. Although domestic tax statutes oten assert broad

jurisdictional rules, which are constrained primarily by the practical limits othe country’s enorcement powers, modern treaty practice has been morerestrained. Under treaties, at least those based on the Organisation orEconomic Cooperation and Development (OECD) model, the outer limit oa country’s jurisdiction to tax the business-related income o nonresidententerprises is dened by reerence to the permanent establishment (PE)concept. The undamental contours o the PE denition are old (at least bythe standards o modern taxation), and have been broadly adopted andremarkably stable or many years.

Despite the longstanding nature o these denitions, a t horough rethinking othe treaty rules relating to taxing jurisdiction is underway. This new school othought is motivated, in part, by technological and other changes in the conducto international business, such as the growing importance o services andglobally integrated service businesses in the international economy; governmentperception in many quarters that multinational corporations have sometimesengaged in unduly aggressive tax planning and transer pricing practices;and by a desire o some countries, usually thought o as capital importersor “source” countries, to claim a larger piece o the tax pie. Developmentsrefecting these pressures include, but are not limited to, the ollowing:

Various publications o the OECD, including recently released amendments•

to the model treaty commentary, in connection with OECD’s long-runningproject on the attribution o income to PEs under Article 7 o the model treaty

The OECD’s ongoing business restructurings project, which recently has•

given rise to a separate project specically ocused on PE denitional issues

Recent and proposed changes to the OECD model treaty commentary on•

Article 5 relating to the PE denition in a service business context

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 7/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

The PE defnition

Under the OECD model treaty, a PE exists, and jurisdiction to tax businessincome is created when either o two conditions is satised. First, i anonresident enterprise maintains an oce or other xed place o business ina country, it generally will be deemed to have a PE and be subject to tax inthat country. Second, i a nonresident enterprise has, in the host country, a“dependent agent” that habitually exercises the power to contractually bind its

principal, the enterprise will be deemed to have a PE. Under the OECD modeltreaty, these are the exclusive jurisdictional tests. Without either a xed placeo doing business in the source country or a dependent agent that possessesthe power to contract on behal o its principal in the source country, thebusiness prots o an enterprise cannot be subjected to the taxing jurisdictiono the source country.

Implicit in the jurisdictional lines drawn in these provisions o the model treatyis the virtually sel-evident principle that a variety o business activities, withclear economic consequences inside the borders o the source country, maybe undertaken without bringing the enterprise inside the jurisdictional taxnet o the source country. For example, the sale o products or services romoutside the source country to customers inside the source country does notgive rise to tax liability o the seller in the customer’s country o residenceunder the OECD model treaty ormulation. This is true regardless o whetherthe purchaser o the product is related to the seller. Thus, under the traditionalreading o the model treaty rules, the activities o a buy-sell distributionsubsidiary almost certainly will not create tax jurisdiction over the relatedsupplier. Similarly, the provision o incidental services by employees o anenterprise resident in the source or host country to an aliate nonresidentin the source country ordinarily should not create tax liability or thenonresident entity, provided it has no oce or xed place o business in thesource country.

The growing importance in the economy o businesses perorming•

nancial intermediary unctions that operate on an integrated and virtuallyborderless basis

Court decisions including those involving Philip Morris in Italy, National•

Westminster Bank in the United States, Zimmer in France, and severalcases in India that address certain PE issues

Aggressive and widespread audit activity in many countries involving broad•

assertions o taxing jurisdiction, particularly assertions o taxing jurisdictionover nonresident aliates o a sales or manuacturing subsidiary, or anonresident aliate o an entity engaging in nancial services transactions

Expansion o the US APA program t o cover allocations o income to PEs•

A signicant increase in the percentage o pending competent authority•

matters involving assertions o the existence o a PE, many o which haveproved dicult or impossible to resolve.

Because o the variety o these recent developments and because the OECDand government tax authorities have not pursued expansion o the rulesrelating to taxing jurisdiction in an integrated or holistic ashion, the currentPE debate has something o a stealth quality to it. It is legitimate to questionwhether the revolutionary developments in communications technologyo the past two decades and the resulting global integration o businessmodels have given rise to a need to rethink undamental concepts relatingto jurisdiction to tax. However, the OECD and global tax administratorshave come to the point o posing these questions in a rather roundaboutmanner. Thereore, one wonders whether the current exercises at the OECDand elsewhere represent mere ne-tuning o the existing rules to refectcurrent business conditions, or whether a more undamental change in theadministration o international tax law is underway.

s legitimate toestion whether

e revolutionaryevelopments in

mmunicationschnology o theast two decadesd the resulting

obal integration osiness models have

ven rise to a need tothink undamentalncepts relating toisdiction to tax.

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 8/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

Pressures on the traditional rules and historical practice

Three distinct sets o pressures have emerged in recent years testing thecontinuing delity o the international tax community to the traditional treatyrules on jurisdiction to tax business income. One o these pressures derivesrom developing communications technology and the consequences othat technology or the manner in which businesses organize themselvesand their cross-border business aairs. Another relates to the prevalent

application o tax planning strategies intended to limit taxable income in hightax jurisdictions and enhance taxable income in low tax jurisdictions, to theextent permitted by applicable transer pricing rules. The third involves thegrowing economic importance o countries, such as India and South Korea,which have traditionally viewed themselves as capital importers with a stronginterest in aggressive assertion o their jurisdiction to tax.

In addition, it has become increasingly obvious at a technical level that theremay be stark dierences between the income allocation outcome under anintra-entity approach under Article 7 and the result under a pure inter-entitytranser-pricing approach. This is because the PE allocation exercise under

Article 7 oten will become an all-or-nothing aair. In other words, i a PE isdeemed to exist, and i one ollows a “people unction” approach under Article7, 100 percent o the prots at issue will oten be allocable to that PE andtaxed in the location o a provider o services. However, i a transer pricingsolution alone had been applied, a lower level o prot arguably would beattributable to the location o the service provider because risk assumptionand business capital would be deemed to reside outside the service provider’s

jurisdiction. This “all-or-nothing” eature o PE disputes makes the route oalleging a PE a more potent weapon or the tax authorities when comparedwith a challenge to the transer pricing arrangements.

Moreover, the model treaty takes substantial pains to suggest that taxing jurisdictions should not be created in some situations in which the nonresidententerprise actually maintains an oce or xed place o business or a dependentagent in the source country. So-called preparatory and auxiliary activitiesmay be perormed through a xed place o business in the country withoutbringing the enterprise within that country’s tax net. For example, a nonresidententerprise that maintains a supply o goods at a xed place o business inside

the source country rom which it lls orders does not thereby become subjectto the source country’s taxing jurisdiction. Similarly, an enterprise establishinga purchasing oce in the source country does not thereby subject itsel to thecountry’s taxing jurisdiction. These rules traditionally have served to enhancethe ree fow o trade in goods and services without creating an undue tax drag.

When controversy has arisen regarding the existence o a PE, oten it hasbeen possible to resolve the controversy on transer pricing grounds. Ian allegation is made that a sales subsidiary in a local country acts as thedependent agent o, and t hereore constitutes a PE o its supplier, it has beenpossible to resolve the controversy on transer pricing grounds by agreeing onthe amount o income to be reported by the local sales aliate. Similarly, in anancial services context, i a broker dealer resident in Country A establishesan aliate in Country B to originate business and develop client relationshipsin Country B, it generally has been possible to nesse the question o whetherthe Country B aliate constitutes a PE o the Country A broker dealer merelyby agreeing to allocate an appropriate share o the enterprise’s global incometo the Country B aliate under transer pricing principles.

None o this is to say that the PE rules are always clear in their application.Essentially, the actual nature o jurisdiction to tax questions has given riseto learned debate and practical controversy. Until recently, however, mostsuch controversy could be resolved on the basis o transer pricing/incomeallocation principles.

This “all-or-noeature o PEdisputes makeroute o allegin

PE a more potweapon or theauthorities whcompared withchallenge to thtranser pricingarrangements

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 9/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

that would not be possible i the same business operations were conductedin a single legal entity operating under the new OECD Article 7 principles. Itbecame evident to tax jurisdictions that, rather than creating a transer pricingsystem o income allocation or real branch operations that ignored “articial”and “questionable” allocations o risk between separate related entities,a more potent challenge could be made based on a broad reading o PEtaxing powers.

Tax administrators in developed markets with higher tax rates have viewedthe emergence o principal company structures, involving overt allocations obusiness risk to lower tax jurisdictions, with increasing alarm. They also haveexpressed concern over some nancial intermediaries that have sought toisolate business risk rom operational unctions by treating high tax countrytraders and other key personnel as service providers and allocating riskand associated returns to lower tax jurisdictions. The perception, thereore,grew that assertions o expanded taxing jurisdiction under the PE denitioncould be used as one tool to attack t he tax structures giving rise to theseconcerns. Further, although the new Article 7 approach, based exclusivelyon people unctions, may be clear in conceptual terms, its application (e.g.,at the “eld agent” level o discussion) can be vague and uncertain, addingurther potential or the PE approach to be pressed into service. That hasrefected itsel in audits and tax controversies around the world. Inevitably,however, the coalescing pressures leading governments to assert expandedtax jurisdiction have reached the point o bumping up against the limits o thetraditional PE denition, giving rise to pressure to reconsider the denitionalrules themselves.

The eect o these practical and technical pressures became evident duringthe course o OECD work on the attribution o income to PEs under Article 7.In ocusing on how income should be allocated among the various branchesor PEs o a nancial institution, the OECD sought to adopt rules ostensiblyconsistent with existing transer pricing principles. In doing so, the OECDthought it important to adopt a system that disregarded potentially articial ormodiable activities, such as the location where nancial assets are booked

or nancing transactions executed. Instead, it ocused on the location othe people undertaking key business activities and making critical businessdecisions. In particular, the OECD eectively concluded that no weight shouldbe given to arbitrary taxpayer determinations as to where, within the samelegal entity, particular nancial risks associated with the business were borne.

It was a short step rom the adoption o a “unctional substance-based”system or allocating income among branches o a single legal entity to therealization that, where separate related legal entities are involved, a similar“substance-based” result could be more dicult or governments to achieve.One o the core building blocks o modern transer pricing rules under theOECD transer pricing guidelines and the US transer pricing regulations isthat agreements between related entities regarding the allocation o businessrisks generally are to be respected by the tax authorities, provided thosearrangements have economic substance. Tax administrators increasinglyobserved that taxpayers sometimes seek to take advantage o this principleto allocate business risks o all kinds (and the income arguably associatedwith those risk bearing unctions) to a “principal” company operating in alower tax jurisdiction. In some o these situations, taxpayers may seek toseparate risk bearing and risk management to achieve transer pricing results

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 10/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

expressly permitted by the tax authorities in relation to the transer pricingarrangements), one can question whether it is appropriate or sensible todebate questions o the existence o inadvertent PEs.

Because these issues arise in a context where the group has conceded thatit is subject to the state’s tax jurisdiction, it should be clear to all involved inthe debate that jurisdictional principles are being used as a stalking horse

to address more undamental income allocation concerns. We seem tohave come ull circle rom a situation where more fexible income allocationprinciples routinely were used to nesse and resolve dicult questionsunder the PE denition, to a world where expansive jurisdictional argumentsare being used to address perceived income allocation abuses. The risk,o course, is that by proceeding in this roundabout way, the jurisdictionalrestraint refected in the existing PE denition may be lost.

Expansive claims o jurisdiction to tax can have serious consequences orthe system o international tax and trade. Broad, competing jurisdictionalclaims increase the tax and tax compliance burden on internationalbusiness. Moreover, the controversies engendered by such broad claims areextraordinarily dicult to resolve. The all-or-nothing nature o a dispute overwhether a PE exists makes the compromise o such a dispute in the mutualagreement process hard to achieve. Recent comments by Internal RevenueService (IRS) ocials, suggesting the IRS may become increasingly unwillingto allow oreign tax credits or taxes imposed under jurisdictional claims andother theories o non-US tax administrators with which they disagree, wouldseem to only heighten this concern.

As the OECD turns overt attention to PE denitional issues, these concernsshould be kept rmly in mind. Notwithstanding the path that has broughtthe debate to the place it currently occupies, it may be a better idea to try toaddress the income allocation concerns o tax administrators directly, ratherthan expanding the PE denition to “x” an income allocation “problem.”

The coming defnitional debate

The OECD recently has indicated that it will undertake a separate projectrelated to the Article 5 PE denition in the context o its work on businessrestructurings. It also recently published alternative treaty language andcommentary allowing countries to assert taxing jurisdiction over serviceentities, even in situations where the entity has no xed place o business in a

jurisdiction. These developments are taking place only a ew short years ater

a thorough OECD review o the challenges to the international tax systempresented by electronic commerce concluded that the traditional PE ruleswere suciently robust to resolve the jurisdictional issues raised by changingbusiness models.

It is a curious act that, even though the PE rules are designed primarily topermit determinations as to when a global business enterprise will becomesubject to tax in a source jurisdiction, some o the most dicult questionsraised under those rules arise in situations where a multinational group ocompanies has conceded it is subject to tax in the country by establishinga local resident aliate. For example, particularly dicult issues haveincluded: the determination o whether a local resident sales aliate or“commissionaire” will be treated as a dependent or an independent agent o arelated enterprise; the conditions under which a local sales or manuacturingaliate will be deemed to contractually bind aliated suppliers or customers;the conditions under which acilities o a local aliate or customer are“made available” to the nonresident enterprise; and whether with sucientregularity and permanence they will become a xed place o business o thatnonresident enterprise.

Also troubling is that a similar theme is emerging in situations that seeminglyhave nothing to do with the tax authority concerns reerred to earlier. Forexample, where prot-splitting arrangements between related partiesconducting an integrated business are in place (perhaps having been

It should be cleainvolved in the dthat jurisdictioprinciples are

being used asa stalking horsto address moundamental inallocation con

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 11/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

Global best practices in avoidingtranser pricing audits and disputes By: David Swenson (US), Helen Fazzino (Australia) and Mauricio Hurtado (Mexico)

“Prevention,” goes the saying, “is better than the cure.” This holds true orglobal tax disputes. Although it is impossible to avoid every tax dispute orcontroversy, it is possible—and desirable—to ensure that steps are takento minimize the chances o an adverse audit and the related possibilities oadjustments and assessments leading to a dispute.

Disputes are protracted and expensive. In addition to the direct costs,signicant management time is required by the relevant revenue authorities.Some companies nd themselves the subject o recurring audits, with theirtranser pricing policies being questioned in numerous jurisdictions. Inaddition to the signicant costs and penalties that may be imposed, recurringaudits may be indicative o a deeper malaise within the organization.

In contrast to recurring audits, our experience suggests that some companiescan consistently get their approach endorsed by the relevant revenueauthorities. Some o these companies simply have not been subject toas much audit activity as others, but in many cases the companies tookproactive steps to achieve this avorable position.

It is not possible—or perhaps even desirable—to avoid all risks and disputes.Rather, the approach should be to manage risks so that global commercialobjectives can be achieved within the risk tolerances o the local scalauthorities. This article looks at steps companies should take to ensurethey can receive a clean bill o health rom—and avoid the costs o disputeswith—tax authorities involving their transer pricing arrangements.

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 12/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

Engaging the right stakeholders

Depending on the magnitude and complexity o the specic business activityenvisaged, the process o creating a plan will draw in a range o stakeholders.The corporate tax department is likely to drive the process o identiyingtranser pricing issues, but it is also likely that a tax/transer pricing /legal teamwill need to be involved as well as intellectual property specialists, particularlywhere there are considerable intangible assets at issue. It is essential to

assemble a dedicated team o people who represent the dierent disciplinesrequired and are amiliar with the disparate issues involved. This will ensurethat no issues are overlooked. O course, operational unctions should be parto the team because it is their business requirements that largely will drive therelevant changes.

A common approach

Although the scale and complexity o projects or which transer pricingplans are required may vary considerably, the same approach should holdtrue in all contexts. A meticulous approach to upront strategy development/ transaction planning should apply as much in comparatively challengingsituations—such as where a high value intangible is being transerred to a tax-avored jurisdiction—as it applies to a standard structure—whereby a productis produced in one country and then shipped to another or distribution.The steps discussed here are valid and appropriate or either one. Theocus should be on proper planning to comply with local regulations and toavoid disputes.

Starting at the beginning

From the outset o any planned development involving the cross-bordercreation or relocation o related corporate entities, there is a need to perormwhat oten is called a transer pricing study, or plan. This plan is developedor a variety o business circumstances that may include a specic unction,product development or production. In the course o developing a study orplan, it is important to ensure that relevant transer pricing issues are identied

as early as possible. This should include not only a review o various “hot”issues in the specic countries concerned, but also other developmentsaround the world. We live in an increasingly connected global tax environment,and governments are increasingly identiying certain issues and examiningthose issues in their tax environment. A current example o an issue identiedwould be matters relating to the taxation o permanent establishments (PEs).

Developing a plan should cover the suggested corporate structure andtransaction fows required or the particular business activity and theidentication o the appropriate transer pricing methodologies associatedwith those corporate structures and transaction fows. This process shouldaddress the overall transer pricing ramework and strategy (i.e., how basictransactions are dealt with, how unctions are remunerated, and how risksare moved and structured), as well as the transer pricing modus operandiwhen executing business strategies and transactions. All material transactionsneed to be managed by the same process, using the simplest approachpossible to deal with standard issues. The process also should recognize thatsome transactions will have signicant eects. For example, issues relatingto moving intellectual property rom one jurisdiction to another will need tobe addressed with greater particularity. Having established the undamentalapproach, the strategy process can then engage the right stakeholders atheadquarters and in the local jurisdictions.

It is essentialto assemble adedicated teamo people who

represent the ddisciplines reqand are amiliawith the dispaissues involved

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 13/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

relationships that unrelated parties would enter into. For example, a mismatchin the allocation o risks between entities creates issues or tax authoritiesto investigate. Worse, it could provide an entrée or them to question thecommerciality o the overall arrangement. A ocus on the quality o the transerpricing documentation should not detract rom attention to the quality anddetail o the intercompany agreements created at the outset. Investing in thatdocumentation is a key step, but one that can be overlooked in the concern

to ensure that transer pricing documents meet the highest standards. By thisstage, completing documentation should be a simple process demonstratingthat the dealings and agreements are at arm’s length.

Aligning orm and substance

Matching orm with substance in this way is essential. Oten intercompanyagreements dier considerably rom the transactions that take place, andthis can create signicant problems down the line. To prevent this, manualsdetailing standard operating procedures should be adopted, especially in thecontext o large projects. In one example, a multinational company (MNC)decided to migrate a global brand to a specic, tax-avored jurisdiction.Standard operating procedures were prescribed in detail that laid out whatemployees needed to do to ensure that substance and orm were kept instrict alignment.

Once a structure is established and unctionally operational, it is important toimplement a periodic review to test the “course o conduct.” This review looksat a suitable time lapse to validate structures, operations and transactionfows ater they have been established to ensure the match betweensubstance and orm continues to hold. Such a review also can ensure thatas business develops, operational activities are not inadvertently creatinga mismatch between orm and substance. The testing should include ananalysis o nancial results and the application o the selected transer pricingmethodologies to assess whether the related structures and operations arewithin the appropriate range.

Building solid oundations

When a company plans to evaluate the options or restructuring the provisiono intercompany services, transer pricing is an important element o thatreview. A company may conclude that certain unctions should be located inparticular countries and identiy the transaction fows between certain entitieswithin the corporate group. The corporate tax unction must then interacteectively with the appropriate corporate operational ocers, the general

counsel, the human resources department and others, depending on the sizeand parameters o the project.

Having completed the planning phase o identiying the appropriatestructures, transaction fows and pricing, implementation is the next phase.Here, it is essential that the rigor and details that have applied to the planningare translated into eective implementation “on the ground.”

Establishing the corporate entities and accurately documenting theintercompany agreements are vital. Commercial documentation precedesthe establishment o the transer pricing documents that support thevarious methodologies chosen or pricing, services rendered, and unctionsperormed. The corporate documents in question should describe in detailthe commercial agreements that establish the unctions and risks o therespective corporate entities, ensuring the proper debt-equity ratios andintercompany agreements are in place.

Once the corporate phase is complete, the required transer pricing policiesare drated to support the nancial results and the fows o income andcosts related to the unctions and methodologies that are used. Althoughthis is the phase that generally receives the greatest attention, it is criticalthat the transer pricing documentation is refective o the economic realityas identied in the prepared corporate documentation. We encountertranser pricing documentation and agreements that do not accuratelyrefect the underlying corporate structures and relationships or the t ype o

s critical thate transer pricingocumentation isfective o the

onomic realityidentied in the

epared corporateocumentation.

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 14/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

The importance o a global transer pricing dispute strategy

The issue o cost-sharing identied above is just one example o a number oissues that MNCs are acing rom tax authorities around the world. MNCs haveoperations in more countries than ever beore, so there is a greater emphasison transer pricing. This leads to a greater probability o exposure to audits andassessments. One company with which we are amiliar has 16 audits relatedto PEs in progress in dierent countries around the world; another has 30

dierent kinds o audits in progress worldwide. There is a new global disputeenvironment, and it is orcing companies to adopt a similarly global response.

In the not-so-distant past, companies tended to handle audits and disputeson a local basis. A local aliate would handle the audit and report back on theresult o a specic case. Today, a number o actors are orcing a change in thatapproach. Audits are emerging around the world with a commonality o issues,and the implications o settling an audit in one country can have a potentiallydramatic eect in other countries. In addition, tax authorities are sharinginormation through mutual agreement procedures and dispute resolutionprocesses, bilateral and multilateral advance pricing agreements (APAs), taxinormation exchange agreements, and wider use o tax treaty networks.

Thereore, it is increasingly advisable or a large MNC to take a two-sided andeven global perspective o its transer pricing arrangements and acknowledgethat the disputes to which its activities give rise need to be seen rom multipleviewpoints. In this environment, companies are realizing a signicant premiumattributable to global strategic planning. This type o planning typicallyinvolves a team dedicated to monitoring audits and the issues that arebeing raised. Team members identiy “hot” issues around the world, such asmarketing intangibles and PEs. They also have a centralized point o contactwithin the company who works with them as well as outside advisors tomonitor developments on a global basis.

I a company cannot avoid an audit, taking the steps briefy outlined herewill ensure that the company has high-quality, robust and consistentdocumentation. Today, more and more companies are taking these steps.But many are not necessarily doing so in a complete or structured way,leaving them vulnerable to audits and disputes. Focusing on transer pricingdocumentation, regardless o its quality, is not enough. The commercialcontracts and agreements underpinning corporate structures must be o an

equally high quality to prevent or mitigate any potential dispute.

O course, sometimes the best planning and implementation will not avoid adispute because there is a conceptual chasm between the revenue authoritiesand the taxpayer. For example, this presently is the case in the UnitedStates on issues relating to cost sharing. There is a signicant philosophicaldierence between what the revenue authorities believe taxpayers should doand what taxpayers and their advisors believe is necessary and appropriate.In such cases, no amount o careul planning or implementation can bridgethe divide between the two parties. But even in these instances, makingsure that the steps taken are consistent with best practices should make itpossible to deend a position eectively. The steps required to do this maybe: rst, to identiy when this situation exists; then to assess the likely risks;and nally, to ensure that the arrangement, analysis and documentation eithermaximize the chance o acceptance by the tax authorities or minimize thelikelihood o penalties.

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 15/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

Global management o tax obligations

In addition, teams members need to address tax obligations on asimilarly global basis. They need to have an overall view o the company’sopportunities to use oreign tax credits, separate country loss utilization,and oreign currency exposures and opportunities. In eect, such a globalstrategic plan looks at a wide variety o issues to determine where prot andloss can be located and how to resolve disputes in a avorable way. Looking

at the tax attributes o a company rom a global perspective creates the abilityto identiy the advantages and disadvantages o resolving particular disputeson the most avorable possible basis. Similarly, where operations in some

jurisdictions are experiencing periods o commercial weakness, the globaltranser pricing system can be altered to ensure that inadvertent outcomes donot expose the business to transer pricing risks.

A global team also can help develop a consistent approach to economicacts and theories on a worldwide basis. Inconsistent positions previouslycould be used and arbitraged rom one country to another. Today, however, anumber o drivers are making a globally consistent approach vitally important.Governments are communicating more eectively, audits are merging witha commonality o issues and the OECD is taking a more prominent role inguiding tax policies. Consequently, developing a consistent approach aroundthe world is rapidly becoming a necessary capability to avoid disputes withincreasingly connected and well-inormed tax authorities.

Some o the largest companies operate with just such an in-house transerpricing group that uses specic tools and databases to centralize inormationabout transer pricing documentation or dierent geographies in additionto other supporting documentation such as contracts and intercompanyagreements. Having the right tools and ensuring their availability is a bestpractice in and o itsel.

In addition to collecting inormation and gathering relevant intelligence, globalteams are taking a proactive approach to addressing their global transerpricing strategy. For example, one company has a cascading APA approachthat obtains APAs in certain countries and then appropriately leverages theresults o those agreements with other countries. O course, this approachwould not be appropriate or all companies, but it exemplies the importanceo having the ability to develop and implement a strategically proactiveglobal approach.

As global transer pricing teams understand the specic exposures acrosstheir transer pricing system, they can adjust their arrangements to avoidbeing penalized or poor arrangements in more than one country. Furthermore,they can adjust their global approaches to intellectual property managementand cost-sharing.

Today, howevenumber o drivare making aglobally consis

approach vitalimportant.

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 16/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

Mandatory binding arbitration

A new avenue or dispute resolution or a meansto increase the pressure on swit settlemento Mutual Agreement Procedure cases?By: Isabel Verlinden (Belgium), David Swenson (US) and Steve Nauheim (US)

Because o a signicant increase in audit, assessment and adjustment activityby tax authorities, the number o tax disputes continues to rise. As a result,the demand likely will escalate or alternative means to achieving resolutiono disputes. A number o recent developments have brought the issue oarbitration as a means o resolving international tax disputes—and particularlythose involving transer pricing—into the spotlight. In Europe, the EuropeanUnion (EU) Arbitration Convention has been heavily discussed. In the UnitedStates, two tax treaties (Germany and Belgium) with provisions or mandatorybinding arbitration recently passed through the political approval process(a third treaty, with Canada, is pending ratication). But does mandatoryarbitration represent a new avenue or resolving international disputes orwill its introduction serve as a catalyst or more ecient avenues to achieveresolutions o controversies? This article discusses the background to theissues and considers the extent to which those issues may encourage ordeter taxpayers and tax authorities rom considering arbitration as a useuladdition to the dispute resolution mechanisms used today.

The Apple legacy

As a means o tax dispute resolution per se, arbitration does not enjoy aparticularly avorable reputation in the United States. This may be largely dueto the outcome o a 1993 arbitration procedure between Apple Inc. and theInternal Revenue Service (IRS), in which Apple lost the dispute. Deploying the

“baseball” approach—whereby the independent arbiter chooses one viewthat prevails over the other—the arbitration panel’s decision in avor o the IRSin the Apple case sent a chilling eect through the US business community.

Although in that instance the arbitration was directed toward the resolution o atax dispute between the taxpayer and the IRS, the unavorable outcome or thetaxpayer meant that arbitration, in the domestic context, was widely perceivedas an unattractive alternative to the other means o resolving tax disputes.

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 17/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

Will the provisions o the new treaties generate dierent results? Will theavailability o mandatory binding arbitration open a new avenue or disputeresolution, or will it put needed pressure on revenue authorities to improvetheir processes?

Frustration with competent authority proceedings

Beore addressing those questions, it is worth looking at the context inwhich these new treaties have been agreed. When disputes prove insolvable,disputing parties have recourse under existing treaties to competent authorityproceedings as part o the MAPs that seek to resolve issues o double taxationbetween countries, among other measures. But these procedures long havebeen a source o rustration to taxpayers and their advisors, principally dueto the average length o time that it takes to reach a resolution—generallybetween two and six years. Indeed, the provision in double-taxation treatiesor MAPs provides only that competent authorities should “endeavor” to nda solution to double taxation. In certain complex cases, competent authoritiesmay conclude that a solution to the double taxation in question has not beenound or that more time is required to nd one.

The intention behind the mandatory binding arbitration provisions in the newUS agreements with Belgium and Germany may be to pressure competentauthorities to reach agreement within a certain period o time. Such agreementwould help prevent the need or arbitration, which occurs i competentauthorities ail to reach an agreement within a set timerame. The arbitrationprocess will ollow the “baseball” approach, under which one o the positionswill prevail, with no compromise available between the competing positions othe competent authorities.

A push or switer resolution

Fiteen years later, the revenue authorities and the US business communityare becoming more critical o what they perceive to be a protracted timetableor the resolution o disputes between countries. They are also more critical osituations in which competent authorities seem unable to reach an agreement.Revenue authorities and businesses, thereore, see the threat o mandatoryarbitration as a useul means to apply pressure on tax authorities to resolve

disputed cases more quickly. This view was summed up in a letter romthe Securities Industry and Financial Markets A ssociation in response tothe US Treasury Department’s Model Income Tax Convention, which said:“The incorporation o arbitration procedures in U.S. tax treaties will increasethe likelihood that a dispute will be resolved in MAP (mutual agreementprocedures) because both parties will have the incentive to reach agreement,as neither will be able to delay indenitely the resolution o a case.”

Unblocking the dispute logjam

The mandatory nature o the arbitration clauses in two new US treaties withBelgium and Germany (and the pending treaty with Canada) represents adeparture rom previous experience in the United States. The rst treaty towhich the United States was a party that contained an arbitration clause wasthe US-Germany Double Taxation Treaty in 1989. In that instance, arbitrationwas voluntary. Perhaps unsurprisingly, no relevant cases were settled througharbitration under the auspices o that treaty. John Harrington, international taxcounsel or the US Treasury, outlined in testimony beore the Senate ForeignRelations Committee the reasons why he believed the voluntary nature othe arbitration provision in the treaty with Germany had not been eectivein seeing disputes move into arbitration. He told the committee: “Althoughwe believe that the presence o these voluntary arbitration provisions mayhave provided some limited assistance in reaching mutual agreements, ithas become clear that the ability to enter into voluntary arbitration does notprovide sucient incentive to resolve problem cases in a timely ashion.”

In certain comcases, compeauthorities maconclude that

solution to the taxation in quehas not been or that more tirequired to n

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 18/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

To date, the progress o the three agreements through the US Senate approvalprocess has been relatively smooth. Although the German and Belgianagreements were held up briefy during the Senate approval process in late2007, each agreement has been approved, and the Canadian agreementis expected to be approved in late 2008. Previous treaties were rejected orheld up in the United States as a direct result o arbitration clauses and someSenators’ concerns, including a perceived threat to tax sovereignty that

mandatory arbitration provisions may represent.

As the treaties go through the approval process, a number o keyquestions remain to be addressed. Until they are answered, it will not bepossible to assess whether the use o mandatory arbitration is a likelynew route to achieve resolution o international tax disputes or whetherthe threat o mandatory arbitration will be sucient to expedite competentauthority proceedings.

Questions that need to be addressed include:

Is mandatory arbitration truly mandatory? Is it truly “binding”?•

Under the 1989 US-Germany treaty, voluntary arbitration was provided. Butno cases were brought under it, suggesting perhaps that, or arbitration tobe an eective mechanism, a mandatory element is required. The questioninvolves the extent to which the arbitration procedure is truly “mandatory”and “binding,” as taxpayers may decide not to participate in the process, orto reject the results o arbitration.

When should arbitration start?•

I arbitration is to start at a dened point (such as a date based on wheninormation necessary to undertake substantive consideration or a mutualagreement is received by both competent authorities), a key issue is howthat date should be determined. Much debate has taken place in Europein connection with the same issue as it applies to the EU ArbitrationConvention. Challenge and debate over when the arbitration processshould start has arisen as countries seek to prolong their ability to manage

their tax decisions and policies.

Taxpayers seek certainty

Another pressure point or competent authority proceedings is that taxpayersare seeking more certainty in managing their tax risks and potential exposureto risks. One means t o achieve this is through advance pricing agreements(APAs). The United States has oered an APA program since 1991, and sincethen many other countries have ollowed with their own programs. The APAprocess also may trigger a competent authority proceeding, which urther

adds to the inventory caseload or the competent authorities concerned.So the pressure on competent authorities will continue to increase, not onlybecause o the increase in disputes arising rom audits and assessments, butalso because more companies are seeking to use the APA process to achievea measure o certainty to manage their international tax risks more eectively.Because o these pressures, the inventory o competent authority cases likelywill increase, which will do little to mitigate taxpayers’ concerns regarding thetimetable or resolving disputes. What can governments do t o expedite thecompetent authority process?

This is where the concept o mandatory binding arbitration may play a role,and the United States arguably has taken the lead in seeking to includemandatory binding arbitration within bilateral treaties.

Many questions remain

A number o signicant question marks hang over the detail o the envisagedarbitration process and whether taxpayers will seek to make use o the newmechanism to solve their disputes. A number o indicators suggest thatthe threat o arbitration, rather than its use, is seen as the main lever orexpediting competent authority proceedings. This perception was conrmedin the testimony o Harrington beore the Senate Foreign Relations Committeeon pending income tax agreements when he said: “It is our expectation thatthese arbitration provisions will be rarely utilized, but that their presence willencourage the competent authorities to take approaches to their negotiations

that result in mutually agreeable conclusions.”

number odicators suggestat the threat obitration, rather

an its use, isen as the mainver or expeditingmpetent authorityoceedings.

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 19/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

What is the applicable authority?•

In reaching nal arbitral decisions, what should be the appropriatehierarchy o authority running rom the treaty provisions to OECD principlesto each country’s domestic law? What priorities should be accorded tothose authorities?

Should decisions create precedent?•

Under the 1989 US-Germany treaty, decisions reached by the arbiters

theoretically would be accompanied with a rationale or a decision thatcould be taken orward as precedent or, at a minimum, be considered inlater cases with similar circumstances. This, in eect, would create anadditional body o law above the provisions contained in the treaties. I therationale o the arbiters were not made public, however, arbitration wouldnot create a body o eective guidance. Further, the strict condentialityapplying to arbitration means that it would be challenging to see how abody o eective guidance and precedent could be created without makingdetails o the arbitration public.

Should decisions be binding on taxpayers?•

The decision o the arbitration panel is binding on the governmentsinvolved. Should the decisions also be binding on the taxpayers?Taxpayers may still have t he ability to reuse to accept the decisionso an arbitration panel and pursue litigation i they are dissatised withthe outcome.

How will eective dates be established?•

When are the provisions under the t reaties eective? How and in whatorder will they address pending cases? What priorities will be given tocases that have been pending or a number o years? Should those caseshave the highest priority or will a “trigger” date or arbitration mean that twomore years are required.

What issues are eligible?•

What are considered eligible issues or arbitration? There is somedierence as to which issues are eligible or arbitration under the threetreaty provisions in the US agreements with Belgium, Germany andCanada. Should all subjects covered by a treaty be eligible or arbitration?I eligibility should have limits, how should these be determined?

Should taxpayers participate?•

What level—i any—o taxpayer participation will be permitted? Taxpayerparticipation in other orms o dispute resolution, including competentauthority proceedings, is seen as a vital element in reaching satisactoryoutcomes. Limitations on taxpayer input to arbitration may mean thattaxpayers will be unwilling to make use o this potential avenue orresolving transer pricing disputes. Taxpayers should be allowed toparticipate in the process in an appropriate and limited ashion.

How should arbiters be selected?•

What standards will be set or selecting the arbiters, and what timetable willbe established within which they need to reach a decision? Selecting theappropriate arbitration panel with members who have sucient knowledgeand standing as well as the requisite neutrality to reach a decision may bea challenging prospect. Will the relative scarcity o such individuals imposea limit on the caseload that can be realistically addressed?

Baseball arbitration or a negotiated settlement?•

Deciding the arbitration approach is clearly critical. Whether to use the naloer approach (baseball arbitration), or an independent opinion approachis a signicant issue. Would better outcomes be secured i arbiters wereencouraged to reach a reasoned decision and opinion in much the sameway as a judicial body does, or should the stress on timely resolution meanthat arbiters should aim to reach a decision quickly and select one o thetwo nal positions as they do under baseball arbitration?

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 20/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

The role o the EU Joint Transer Pricing Forum

The orum’s aims

Making arbitration work in reality is a subject that continually gives riseto raised eyebrows within Europe, both or tax authorities and taxpayers.Consequently, arbitration has become one o the key topics to be addressedby the EU Joint Transer Pricing Forum. The European Commission

established this orum in late 2002. Its aim is to come up with nonlegislativerecommendations to help companies operating across the EU manage theirtranser pricing challenges in harmony. Besides representatives rom the taxadministrations o the EU member states, the orum also includes 15 businesssector experts, an independent chairman, and observers (such as the OECD).

Ater an initial two-year term, the orum was extended or another two yearsand was smoothly reinstituted again in 2007.

Achievements to date

The proceedings o the orum have resulted in three communications. Therst was a code o conduct on the EU Arbitration Convention, which aimedto enhance the convention’s role as an eective tool or resolving economicdouble taxation within the EU. The second communication presented a codeo conduct on transer pricing documentation compliance in the region.In February 2007, the EU Commission published a third communicationon the proceedings o the orum. It invited the EU Council to endorseproposed guidelines on APAs and asked the member states to implementthe recommendations included in the guidelines in their national legislationor administrative rules. The purpose was also to put emphasis on disputeavoidance through upront agreements (APAs) rather than purely ocusing ondispute resolution (through arbitration) to mitigate the risk o wasting valuablemanagement time in addressing past transactions.

The EU experience: The Arbitration Convention

The European experience with arbitration in complex international transerpricing disputes has a long, detailed history. The EU Arbitration Conventionwas implemented as a means to orce resolution o transer pricing disputesbetween EU member states. Conceived as a directive, which is adoptedinto member states’ domestic legislation, the member states perceived itas a threat to their tax sovereignty and objected. As a result, the arbitration

directive was withdrawn and replaced by t he EU Arbitration Convention. Approval o the EU Arbitration Convention was a tortuous process but wasratied in its present orm in 2004. It is extended every ve years, providedthat no contracting member state objects.

The EU Arbitration Convention requires competent authorities to reach ullagreement on double-taxation issues arising rom transer pricing disputes.Disputes must be resolved within two years, or the matter is transerred to anadvisory commission that will reach a decision within six months. Competentauthorities have one nal chance to reach an agreement within that timeperiod. I they ail to do so, the commission’s decision is binding on bothparties. Though it is unclear how many cases have been settled by suchan arbitration process, the implied threat o removing jurisdiction rom thecompetent authorities in each country has motivated many to resolve caseswithin the two-year time period. Here again, it is the potential or arbitrationrather than the process itsel that is seen to be eective in expediting cross-border transer pricing disputes within the European Union.

e implied threat omoving jurisdictionom the competentthorities in

ch country hasotivated manyresolve casesthin the two-year

me period.

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 21/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

i the distributor’s margin is perceived as too slim. In such a situation, wereject the idea o allowing countries the ree choice to “reeze” the arbitrationcase until an investigation under competent authority provisions with theUnited States has taken place. Moreover, at the end o the day, tax authoritiesmight also have less appetite to see the case end up in a binding arbitrationas it cannot lead to a “splitting the baby” type o settlement under the rules obaseball arbitration.

The OECD’s plea or binding arbitration

As set out above, under the current state o play, the MAP according to thetreaty can drag on indenitely as countries are required only to “endeavor toagree.” The OECD has stepped into the breach by urging a clear timerameand greater certainty in dispute resolution. In 2004, only a week prior to the EUmember states completing the ratication procedures to extend indenitelythe EU Arbitration Convention, the OECD released its drat progress report,“Improving the Process or Resolving International Tax Disputes.” That reportsuggested arbitration as a supplementary mechanism or the settlement o taxtreaty disputes.

In February 2007, the OECD released the nal report containing a number oproposals to improve the resolution o international tax disputes. The mostimportant in the context o this article is a proposal to add to the OECD ModelTax Treaty a provision that calls or mandatory arbitration. Consequently, theOECD’s Committee on Fiscal Aairs has agreed to modiy the basis or mostnegotiations between countries on tax matters by including the possibility oarbitration in cross-border disputes i they remain unresolved or two years.The business community will welcome this idea, and we sincerely hope thatthis will become a widespread tool or achieving eective dispute resolutionwithin an acceptable timerame.

Mandatory binding arbitration o international tax disputes is a new andemerging alternative. It is controversial, and its long-term eect is uncertain.

The business community hopes arbitration proves a viable alternative orresolving disputes on a more timely and cost-eective basis.

Where did these initiatives lead to in Europe?

The role o the orum is to acilitate actions on both the avoidance (through APAs and robust documentation) and resolution o double-taxation issues(through making the EU Arbitration Convention work smoothly). As mentionedabove, however, to date there is no convincing evidence on whetherarbitration is being called upon switly. Even though there are no ormalstatistics, our experience and research suggest that an increasing number o

taxpayers appear to be making requests with their local tax authorities to taketheir cases to arbitration. But it looks as i those requests are simply used as ameans to increase the pressure or a settlement that at least partly addressesthe double taxation.

Very ew cases have resulted in an actual arbitration, although there havebeen a number o instances where a panel o arbiters has been set up and hasreached a decision to resolve the double taxation, as well as cases in progressor which a panel has been set up. A landmark case involves a dispute in 2003between France and Italy over the pricing within the Electrolux group betweena manuacturing and distribution entity, respectively.

Agenda

It is clear that the business community has high expectations o the potentialor arbitration to become a more easily accessible route among the array ostrategic options to avoid double taxation. In this context, it will be interestingto observe the developments relating to the interaction o the EU ArbitrationConvention with other procedures. For instance, the resolution o so-called“triangular cases” involving a non-EU taxpayer will be a particularly hardnut to crack. Consequently, a burning issue will be how to marry treatydevelopments on binding arbitration (such as in the above-mentioned UStreaties) with the EU Arbitration Convention. An example o this situationmight be a case in which a US manuacturing entity sells products into aBelgian logistics center, which then sells the goods to a German distributor

or commercialization in the market. In such a case, even though the Belgiantax authorities might be happy with the intercompany price (perhaps undera cost-plus method or the role o the logistics center as a mere serviceprovider), the German tax authorities might challenge the intercompany price

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 22/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

The challenge o “triangular”transer pricing cases By: David Swenson(US), Hugo Vollebregt (The Netherlands), Isabel Verlinden(Belgium) and Spencer Chong (China)

As the economy globalizes, the numerous processes in the research anddevelopment, manuacture, sale, and distribution o goods and servicesincreasingly are perormed by separate entities within a multinational group.The fow o products and services through intercompany transactionsrequently involves three or more countries.

Initially, transer pricing cases generally arose rom the transer o tangible orintangible property between two related companies in two tax jurisdictions. Inthose cases, the assessments made by the tax authorities in each jurisdictionat times created bilateral disputes. The diculties and complexities involvedwith resolving those cases are well documented. Now, however, we areseeing a new development in transer pricing cases that is adding a layero complexity and raising challenging—and as yet unanswered—questions.We are observing an increasing number o situations whereby multinationalentities are involved in transaction fows that give rise to transer pricingdisputes in more than two countries, otherwise known as a “triangularcase.” These new multilateral cases generate many dicult procedural andsubstantive issues and increase the diculties o reaching a global agreementamong all countries involved.

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 23/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

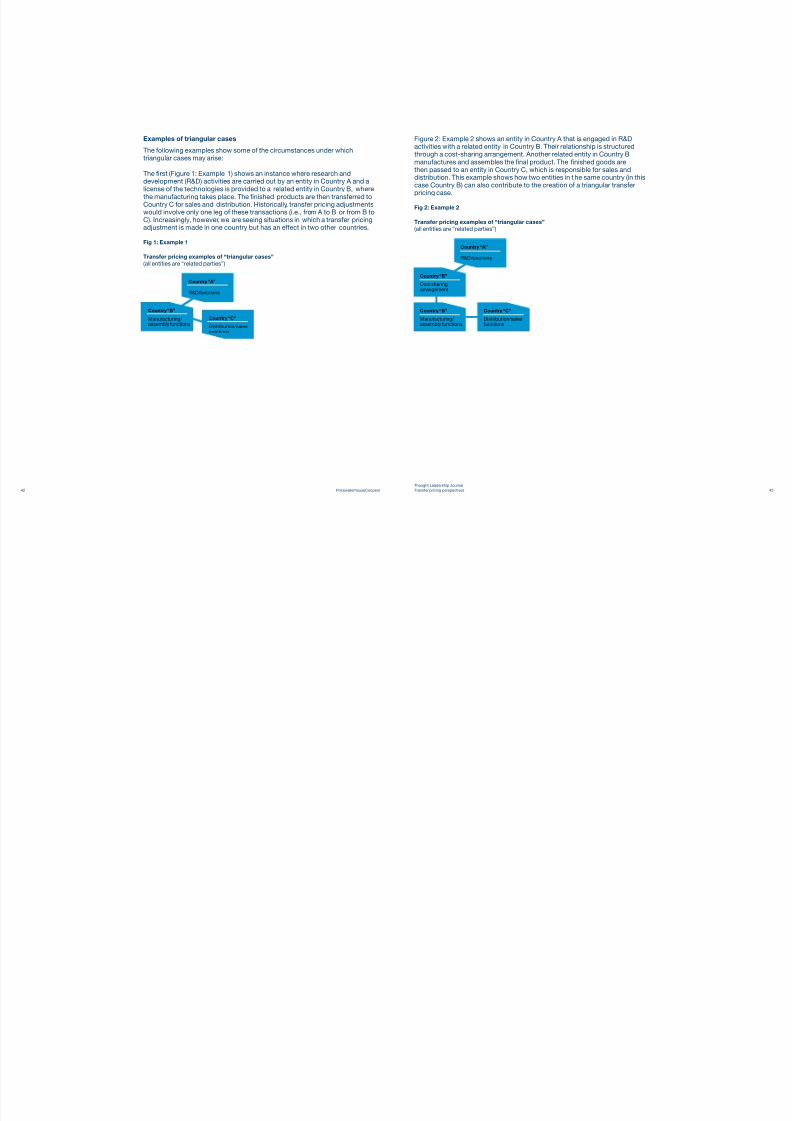

Figure 2: Example 2 shows an entity in Country A that is engaged in R&Dactivities with a related entity in Country B. Their relationship is structuredthrough a cost-sharing arrangement. Another related entity in Country Bmanuactures and assembles the nal product. The nished goods arethen passed to an entity in Country C, which is responsible or sales anddistribution. This example shows how two entities in t he same country (in thiscase Country B) can also contribute to the creation o a triangular transer

pricing case.

Fig 2: Example 2

Transer pricing examples o “triangular cases”

(all entities are “related parties”)

Examples o triangular cases

The ollowing examples show some o the circumstances under whichtriangular cases may arise:

The rst (Figure 1: Example 1) shows an instance where research anddevelopment (R&D) activities are carried out by an entity in Country A and alicense o the technologies is provided to a related entity in Country B, where

the manuacturing takes place. The nished products are then transerred toCountry C or sales and distribution. Historically, transer pricing adjustmentswould involve only one leg o these transactions (i.e., rom A to B or rom B toC). Increasingly, however, we are seeing situations in which a transer pricingadjustment is made in one country but has an eect in two other countries.

Fig 1: Example 1

Transer pricing examples o “triangular cases”

(all entities are “related parties”)

Country “A”

R&D unctions

Country “C”

Distribution/salesunctions

Country “B”

Manuacturing/ assembly unctions

Country “A”

R&D unctions

Country “C”

Distribution/salesunctions

Country “B”

Cost sharingarrangement

Country “B”

Manuacturing/ assembly unctions

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 24/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

The amount o prot in the economic amily o the three or more partiesis a constant. The question is how the pool should be divided to refect aair allocation among all o the aected parties. The allocation o prot is,in eect, a “zero-sum” game. As more countries show interest in transerpricing issues and audit transactions and raise assessments to maximizetheir share o global tax revenue, these economic considerations will becomemore pressing.

Although these situations are rare at present, we believe these types o caseswill increase steadily. The emerging world o complex R&D pushes productsthrough multiple countries. As a result, multinational corporations—as well astax authorities—will be aced with a number o challenges as they addressthese triangular cases.

What are the issues?

The issues raised by trying to address and resolve triangular cases areprocedural and substantive.

Is it possible, or example, to create a tripartite mutual agreement procedure(MAP)? Tax treaties generally operate between two countries. Although eachcountry involved may have tax treaties with the other countries, these treatieswill not address the relationship among three or more countries. Thereore,the procedural issues include how the resolution o such a case will proceed.Is there a sequential order to be ollowed? I so, how is it established? In theexample described above in Figure 3, would a MAP be instituted betweenthe rst two countries (B and C), and then, depending on the result o thatprocess, would a new competent authority matter between the other twocountries (B and A) be required? Or, should there be a more creative approachthat rolls together the issues rom the beginning?

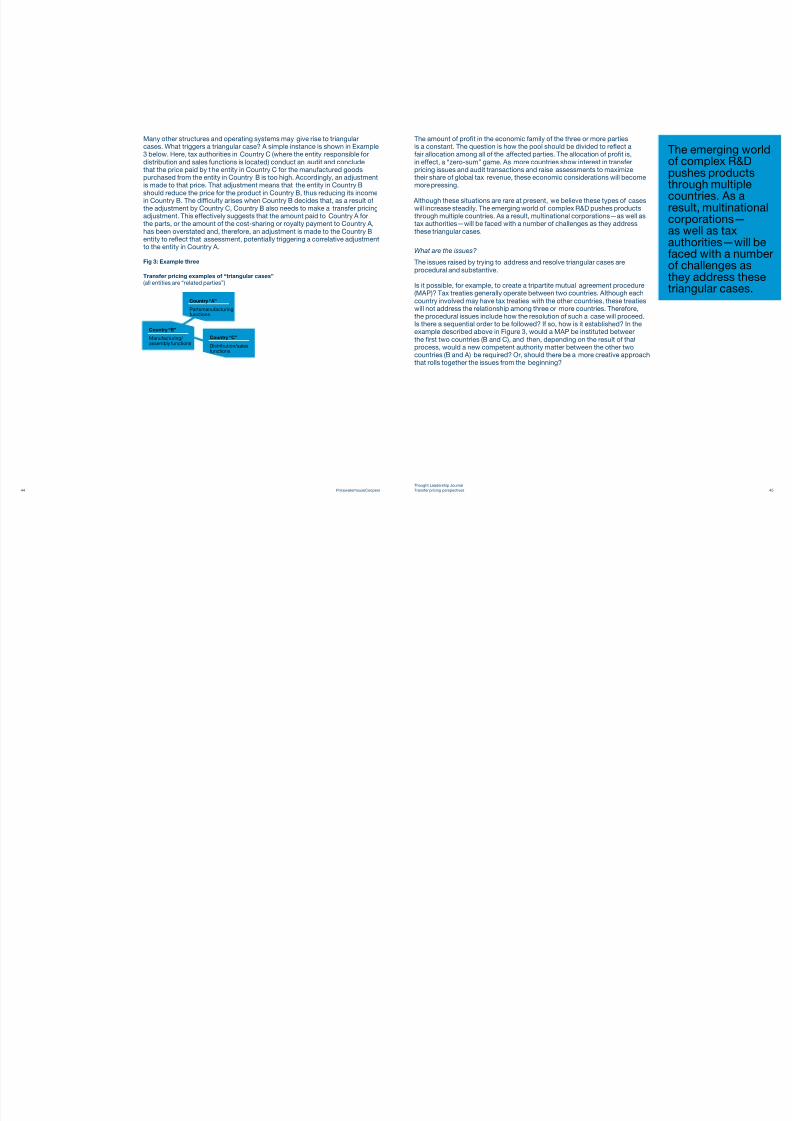

Many other structures and operating systems may give rise to triangularcases. What triggers a triangular case? A simple instance is shown in Example3 below. Here, tax authorities in Country C (where the entity responsible ordistribution and sales unctions is located) conduct an audit and concludethat the price paid by t he entity in Country C or the manuactured goodspurchased rom the entity in Country B is too high. Accordingly, an adjustmentis made to that price. That adjustment means that the entity in Country B

should reduce the price or the product in Country B, thus reducing its incomein Country B. The diculty arises when Country B decides that, as a result othe adjustment by Country C, Country B also needs to make a transer pricingadjustment. This eectively suggests that the amount paid to Country A orthe parts, or the amount o the cost-sharing or royalty payment to Country A,has been overstated and, thereore, an adjustment is made to the Country Bentity to refect that assessment, potentially triggering a correlative adjustmentto the entity in Country A.

Fig 3: Example three

Transer pricing examples o “triangular cases”

(all entities are “related parties”)

Country “A”

Parts manuacturingunctions

Country “C”

Distribution/salesunctions

Country “B”

Manuacturing/ assembly unctions

The emerging o complex R&pushes producthrough multip

countries. As aresult, multinacorporations—as well as taxauthorities—waced with a no challenges they address ttriangular case

8/3/2019 09-0002 Thought Leadership Journal com

http://slidepdf.com/reader/full/09-0002-thought-leadership-journal-com 25/41

PricewaterhouseCoopers

Thought Leadership Journal

Transer pricing perspectives

The EU Joint Transer Pricing Forum

The EU Joint Transer Pricing Forum is one o the ew international bodies todate that has specically addressed the issue o triangular cases. The orumlooked at triangular cases in the context o the EU Arbitration Convention.The orum’s paper examines the possible eects triangular cases will haveon the way the Arbitration Convention works. Specically, the paper arguesthat triangular cases should not be allowed to infuence the operation o

the Arbitration Convention, particularly in light o the perceived benetsthe Arbitration Convention has conerred by expediting the resolution ocompetent authority proceedings.