-

8/3/2019 10302011 Weekly Strategic Plan

1/13

Liquidity Cycle Update: Bounce or Bull?

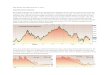

Here are the weekly and daily SP 500 charts:

Pretty solid and fast move back into congestion as very negative

sentiment is reversed by

announcement of a plan for Europe. The US indicator moved out of

lower congestionbefore the big rally last week but mostly

consolidated during the week. The Global

indicator popped sharply however as most global equity markets

responded with sharp

rallies.

The next two charts show something new is happening as the mid

cycle components of

the equity markets have actually outperformed the early stage

groups and the defensivesfor the last couple of weeks. This is

interesting because it indicates the entire cycle is

running very fast. The normal roughly 4 year periodicity seems

to be cut in half or evenmore. I believe this is a function of the

extraordinary government efforts to manipulate

markets rather than allow giant imbalances to sort themselves

out. The interventions

overwhelm fundamentals temporarily and incite very rapid

sentiment change amongmarket participants. History does not

indicate these policies will have a happy outcome.Here is one such

historian on the subject:

Rogoff: Nice Try, But Greece Will Leave The Euro

-

8/3/2019 10302011 Weekly Strategic Plan

2/13

Now the two charts mentioned: The stage 2 groups begin to

outperform. These includematerials, energy, industrials and other

markets which have been correlated with Asian

growth so it is no coincidence that we see plurality in related

equity markets.

The markets reacted to the refinancing solution proposed for

Europe by ratcheting upglobal growth forecasts and while I am

personally skeptical that growth will be robust,

that is the way to bet at present.

Copper daily, Freeport Mc Moran Copper and Gold

David Fullermoney discusses the plurality new signals in the

Asian equitymarkets.

Fullermoneys interesting charts - Price charts enable

disciplined observersto monitor trend consistency and momentum, and

also to recognise thedynamics of eventual trend change.

-

8/3/2019 10302011 Weekly Strategic Plan

3/13

China's Shanghai A-Shares Index(weekly & daily)

has had a number of false starts over the last two years, during

which theeconomy has continued to grow strongly, enabling

valuations to improve.

Interestingly, after a significant decline since April, we have

seen twoupside key day reversals off reaction lows this month, and

a weekly keyreversal has also occurred over the last five days.

These reversal dynamicsindicate that a low of at least near-term

significance has been reached anda new closing low for the year

would be required to offset current scope for

sideways to higher ranging in a further recovery over the next

few months.

-

8/3/2019 10302011 Weekly Strategic Plan

4/13

Hong Hong's HSI Index (weekly & daily)

accelerated to a low in early October and has seen its biggest

rally thismonth since the high at 25,000 one year ago. This

indicates that apotentially important low has been established and

that downside risk isnow limited to a partial retracement of recent

gains in a support building

process prior to an additional recovery.

India's Sensex Index(weekly & daily

as rallied from lateral support near 16,000 to lateral trading

near 18,000which has provided both support and resistance over the

last year. TheSensex has also approached its downward trending

200-day MA.Consequently, it is at an interesting level as further

strength would breakthe downward trend, although this would not be

fully confirmed until theprogression of lower rally highs - the

last one was in July - is broken.Conversely, a decline back beneath

17,000 would begin to suggest thatsupply had regained the upper

hand. In what is a finely balanced technical

picture, I would give the upside the benefit of the doubt,

unless provedotherwise, due to the rebound in global stock markets,

although anoffsetting factor may be the Bombay Banks Index's

currentunderperformance.

-

8/3/2019 10302011 Weekly Strategic Plan

5/13

Singapore's Straits Times Index(weekly & daily)

has surged higher since its early-October low. This increases

the possibility that asustainable low has been reached. However, a

partial pullback and additionalsupport building phase may be

required before potential resistance from

overhead trading, the declining MA and lateral trading near the

psychological 3000level is successfully challenged.

Indonesia's JCI Index (weekly & daily),

so often an upside leader, has regained approximately two-thirds

of its declinefrom the August high. This increases chances that the

late-September low willhold, although resistance from the upper

boundary may make further upwardprogress more laboured.

Nevertheless, a close backbeneath 3600 would berequired to question

the current outlook for sideways to higher ranging.

-

8/3/2019 10302011 Weekly Strategic Plan

6/13

Australia's AS51 Index

(weekly & daily) accelerated to a low in August and

continued to buildsupport above its 2008-2009 base for the next two

months. Overheadsupply may make further upward progress laboured

but a close beneath4130 would now be required to question evidence

that demand has

regained the upper hand.

Plurality in this rally was extraordinary the magnitude of the

rallies already raisesissues of too far too fast but the developed

monetary authorities have suppliedvast liquidity and the Europeans

are now promising more while in the US hints ofa QE3 program

promises even more to come. Liquidity and money printingseems to be

reflected in equity markets first. My advice is give this move

thebenefit of the doubt but stick to balance sheet strength and

dividends for theirdefensive support.

Risk factors remain in the form of three major areas: First as

the details of the

European plan are evaluated doubts are going to arise quickly.

This was a bareminimum not a bazooka and many of the features are

only minimally credible.

Second results of the super committee are due soon and real

positive results arestill a low odds proposition. The lack of

leaked material so far is a small positive,but I would not bet your

money on the current crop of elected miscreants.

Third policy changes in China and other big Asian economies must

becomesomewhat easier. The high food component of price indices in

these economiesmeans inflation is especially dangerous. So far very

little inflation relief hasshown up making it difficult for

officials to publicly abandon the fight against

higher food prices. But the threat of hard landings is growing

and policy has along lead time so the time to ease up is nearing.

Failure to act will abort thenascent global recovery.

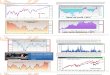

Technically the market has corrected so quickly that the number

of stocks abovetheir 50 ma has actually climbed into overbought

readings as the next chartshows. However, the number of issues

above the 200 ma is in much saferterritory as the second following

chart shows. Charts from The Chartstore.com

-

8/3/2019 10302011 Weekly Strategic Plan

7/13

50 day

200 day

-

8/3/2019 10302011 Weekly Strategic Plan

8/13

Market Environment: A lot of markets have turned to volatile

this past week.

-

8/3/2019 10302011 Weekly Strategic Plan

9/13

Global Equity Environment

Note the green uptrend indicator came on for the US the best

other markets cando so far is turn off the sell indicator. This

means the US market is the only onewith open buy permission and the

other rankings pertain to relative value trades.

-

8/3/2019 10302011 Weekly Strategic Plan

10/13

Seasonality and Spreads

The Gold chart from Hinde Capital indicates gold is responding

to its seasonalinitiation of strength lending support to the

likelihood that recent lows will holdand the long uptrend is stil

in control.

Energy spreads were dramatic this week driven both by changing

growth prospects butalso by the promise of a return to more normal

availability of Libyan light crude. Also the

oversupply of inventory in Cushing appears to be improving thus

reducing that discount.

A very big shift in the WTI curve confirming the up move in WTI

prices.

-

8/3/2019 10302011 Weekly Strategic Plan

11/13

Brent prices remained up near resistance and the spreads moved

to confirm slightly.

But the real change is the shrinking discount of WTI. I like

this to continue.

Too early to tell how far the discount may shrink because a risk

premium for light Middle

Eastern oil will likely remain due to potential for renewed Arab

Spring like violenceand thus uncertainty.

Grain prices moved up during the week and spread prices were

relatively benign in cornand in first year wheat. Soybeans saw

dramatic spread strength in the next crop year and

wheat also showed extra strength in next crop year prices.

Global supply demandevidence makes it increasingly clear the world

ending stocks are tight and need strong

crops again next year. Cotton prices had a notable advance with

spreads quiet.

-

8/3/2019 10302011 Weekly Strategic Plan

12/13

The Eurodollar futures curve moved down in the backend

reflecting the increasedprospect for global growth and thus higher

interest rates further out the curve. This was

consistent with the bullish rebounds in global equity

indices.

-

8/3/2019 10302011 Weekly Strategic Plan

13/13