Embed Size (px)

Citation preview

Medica RestrictedDocument classification:

medica.co.uk

2021 Interim Results

Analyst Presentation

Stuart Quin (CEO), Richard Jones (CFO) and Dr. Robert Lavis (Group Medical Director)

27 September 2021

Medica RestrictedDocument classification:medicagroupplc.com

Agenda

1. H1 2021 highlights

2. Financial review

3. Trading and market update a. UK

b. Ireland and US

4. Strategy update and FY21 outlook

5. Q&A

2

Medica RestrictedDocument classification:

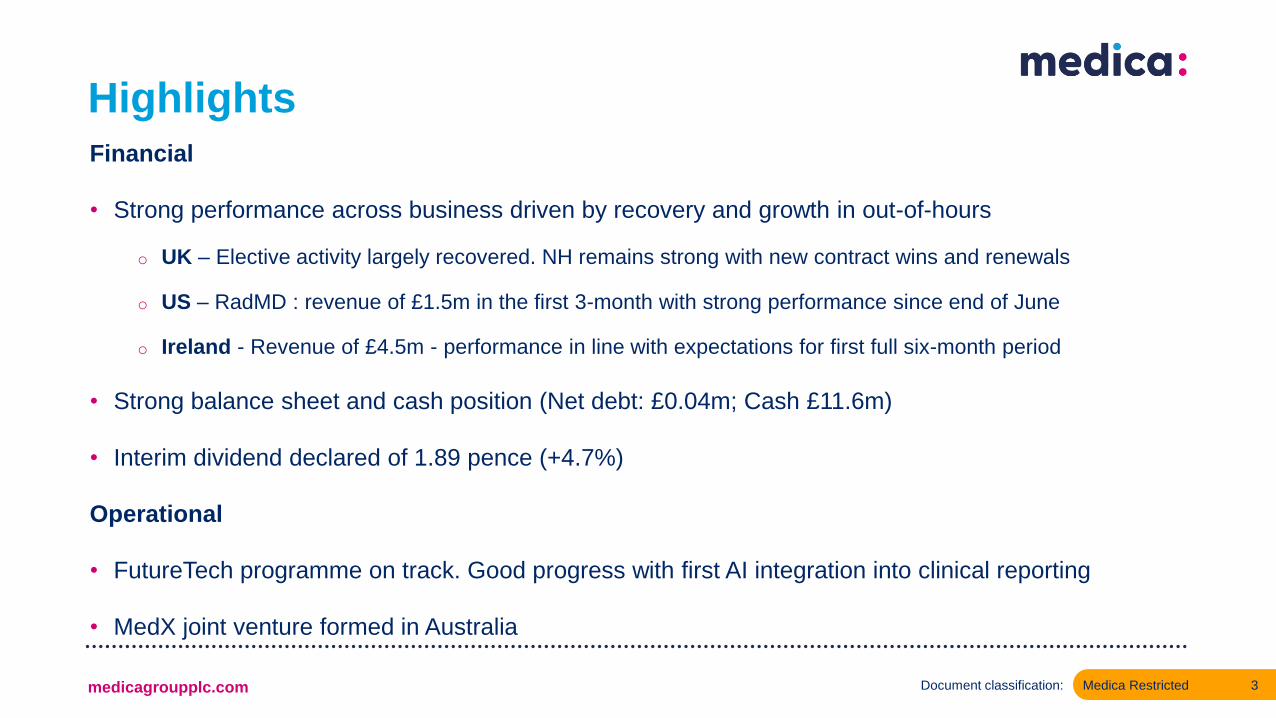

HighlightsFinancial

• Strong performance across business driven by recovery and growth in out-of-hours

o UK – Elective activity largely recovered. NH remains strong with new contract wins and renewals

o US – RadMD : revenue of £1.5m in the first 3-month with strong performance since end of June

o Ireland - Revenue of £4.5m - performance in line with expectations for first full six-month period

• Strong balance sheet and cash position (Net debt: £0.04m; Cash £11.6m)

• Interim dividend declared of 1.89 pence (+4.7%)

Operational

• FutureTech programme on track. Good progress with first AI integration into clinical reporting

• MedX joint venture formed in Australia

3medicagroupplc.com

Medica RestrictedDocument classification:

Financial review H1 ‘21

Richard Jones, CFO

Medica RestrictedDocument classification:

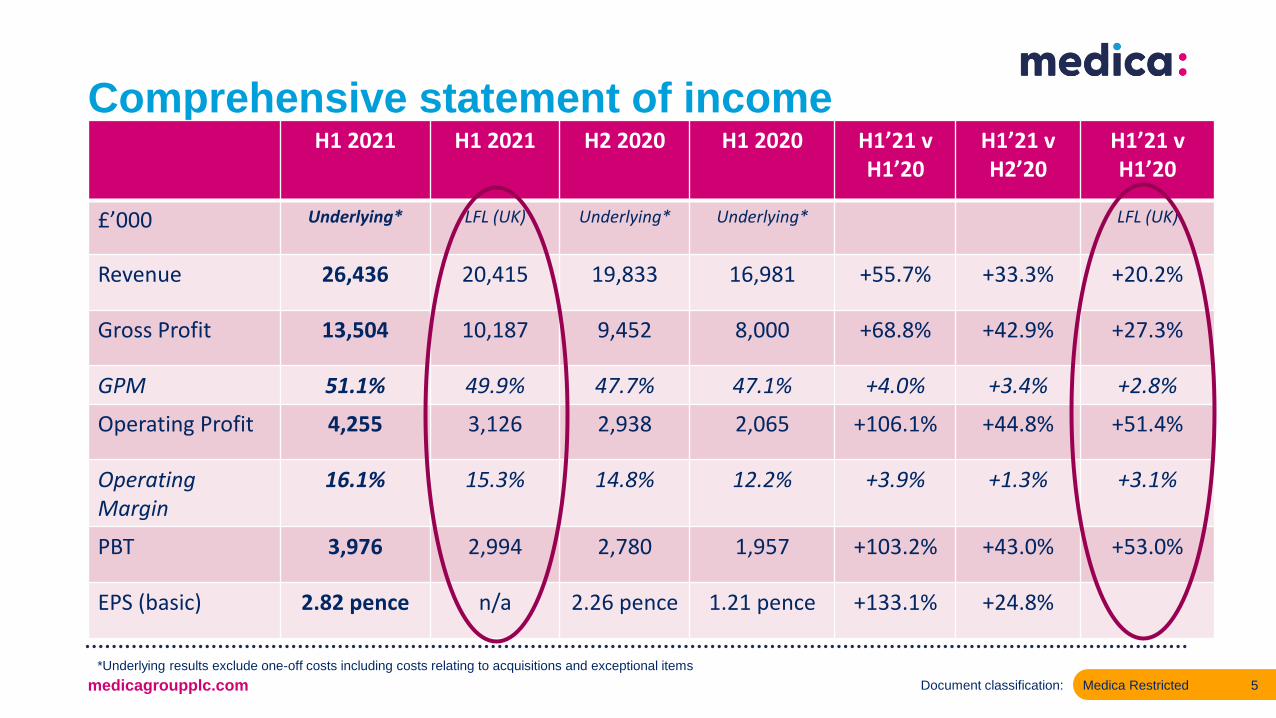

Comprehensive statement of income

• Strong improvement

• LFL revenue increased

• LFL Operating Profit

5

H1 2021 H1 2021 H2 2020 H1 2020 H1’21 v H1’20

H1’21 v H2’20

H1’21 v H1’20

£’000 Underlying* LFL (UK) Underlying* Underlying* LFL (UK)

Revenue 26,436 20,415 19,833 16,981 +55.7% +33.3% +20.2%

Gross Profit 13,504 10,187 9,452 8,000 +68.8% +42.9% +27.3%

GPM 51.1% 49.9% 47.7% 47.1% +4.0% +3.4% +2.8%

Operating Profit 4,255 3,126 2,938 2,065 +106.1% +44.8% +51.4%

Operating Margin

16.1% 15.3% 14.8% 12.2% +3.9% +1.3% +3.1%

PBT 3,976 2,994 2,780 1,957 +103.2% +43.0% +53.0%

EPS (basic) 2.82 pence n/a 2.26 pence 1.21 pence +133.1% +24.8%

medicagroupplc.com

*Underlying results exclude one-off costs including costs relating to acquisitions and exceptional items

Medica RestrictedDocument classification:

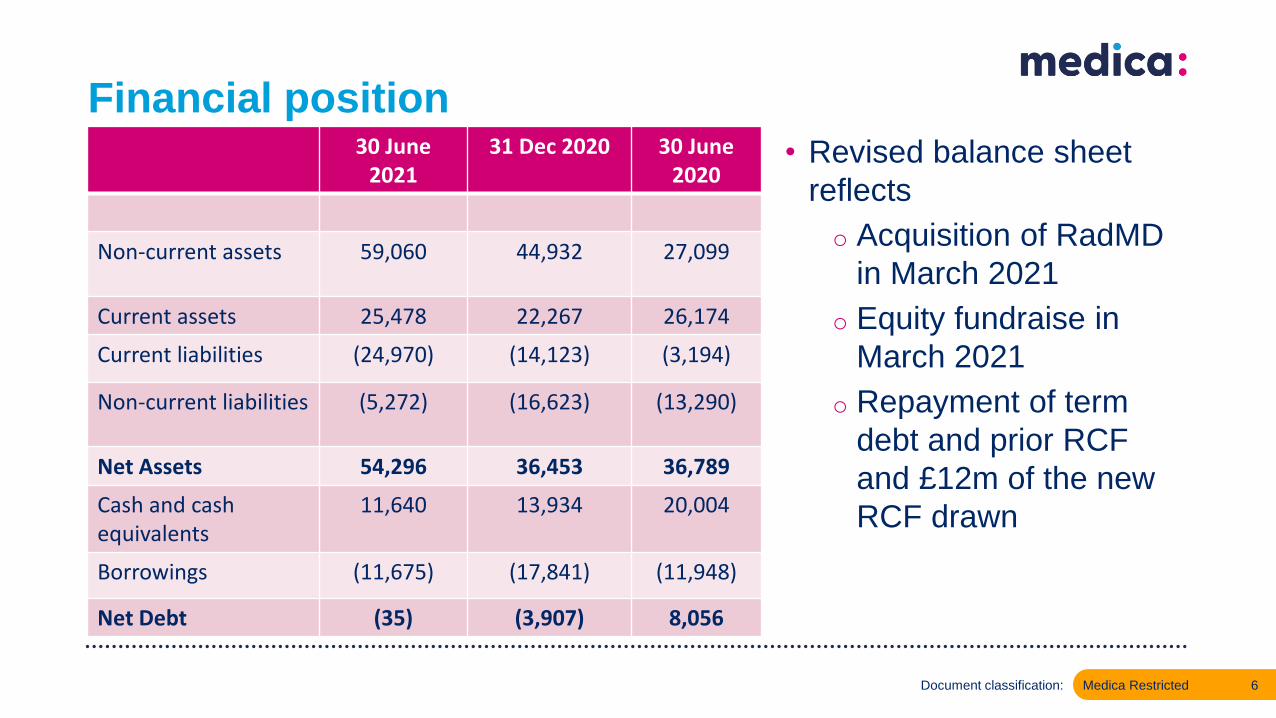

Financial position

• Results in line with trading statement on

6

30 June 2021

31 Dec 2020 30 June 2020

Non-current assets 59,060 44,932 27,099

Current assets 25,478 22,267 26,174

Current liabilities (24,970) (14,123) (3,194)

Non-current liabilities (5,272) (16,623) (13,290)

Net Assets 54,296 36,453 36,789

Cash and cash equivalents

11,640 13,934 20,004

Borrowings (11,675) (17,841) (11,948)

Net Debt (35) (3,907) 8,056

• Revised balance sheet

reflects

o Acquisition of RadMD

in March 2021

o Equity fundraise in

March 2021

o Repayment of term

debt and prior RCF

and £12m of the new

RCF drawn

Medica RestrictedDocument classification:

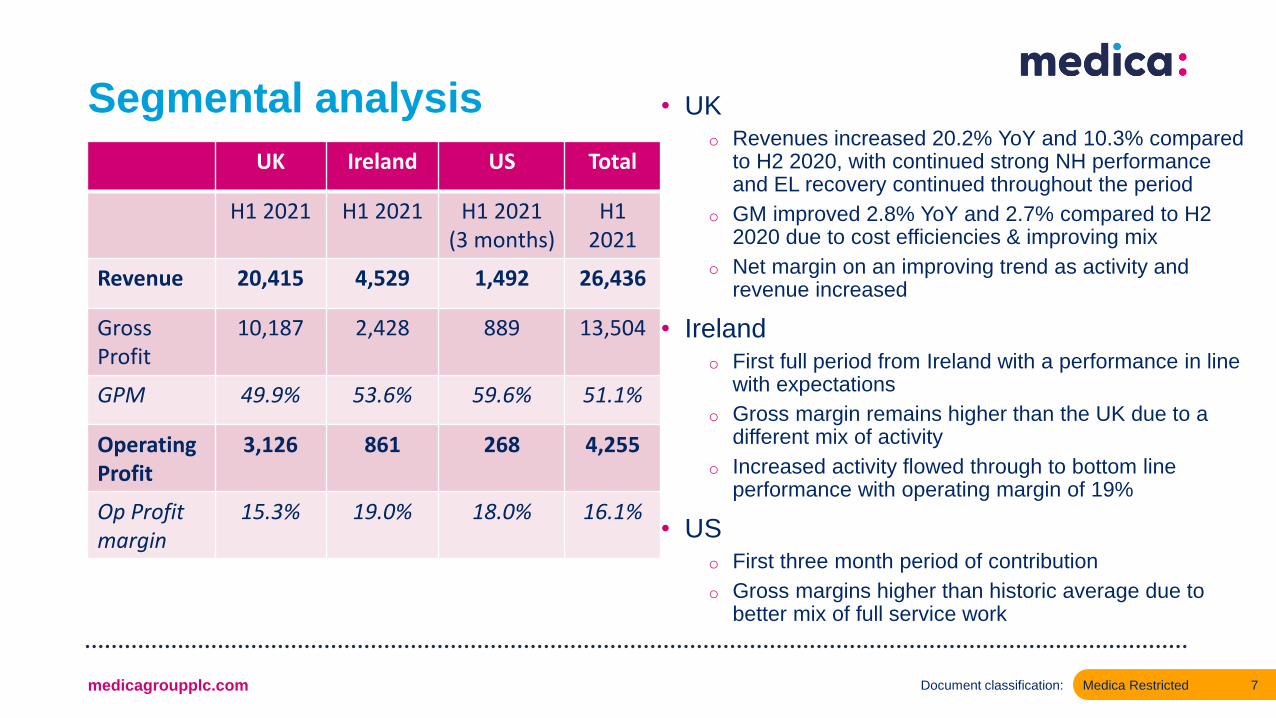

Segmental analysis • UK o Revenues increased 20.2% YoY and 10.3% compared

to H2 2020, with continued strong NH performance and EL recovery continued throughout the period

o GM improved 2.8% YoY and 2.7% compared to H2 2020 due to cost efficiencies & improving mix

o Net margin on an improving trend as activity and revenue increased

• Irelando First full period from Ireland with a performance in line

with expectations

o Gross margin remains higher than the UK due to a different mix of activity

o Increased activity flowed through to bottom line performance with operating margin of 19%

• USo First three month period of contribution

o Gross margins higher than historic average due to better mix of full service work

7

UK Ireland US Total

H1 2021 H1 2021 H1 2021(3 months)

H1 2021

Revenue 20,415 4,529 1,492 26,436

Gross Profit

10,187 2,428 889 13,504

GPM 49.9% 53.6% 59.6% 51.1%

Operating Profit

3,126 861 268 4,255

Op Profit margin

15.3% 19.0% 18.0% 16.1%

medicagroupplc.com

Medica RestrictedDocument classification:

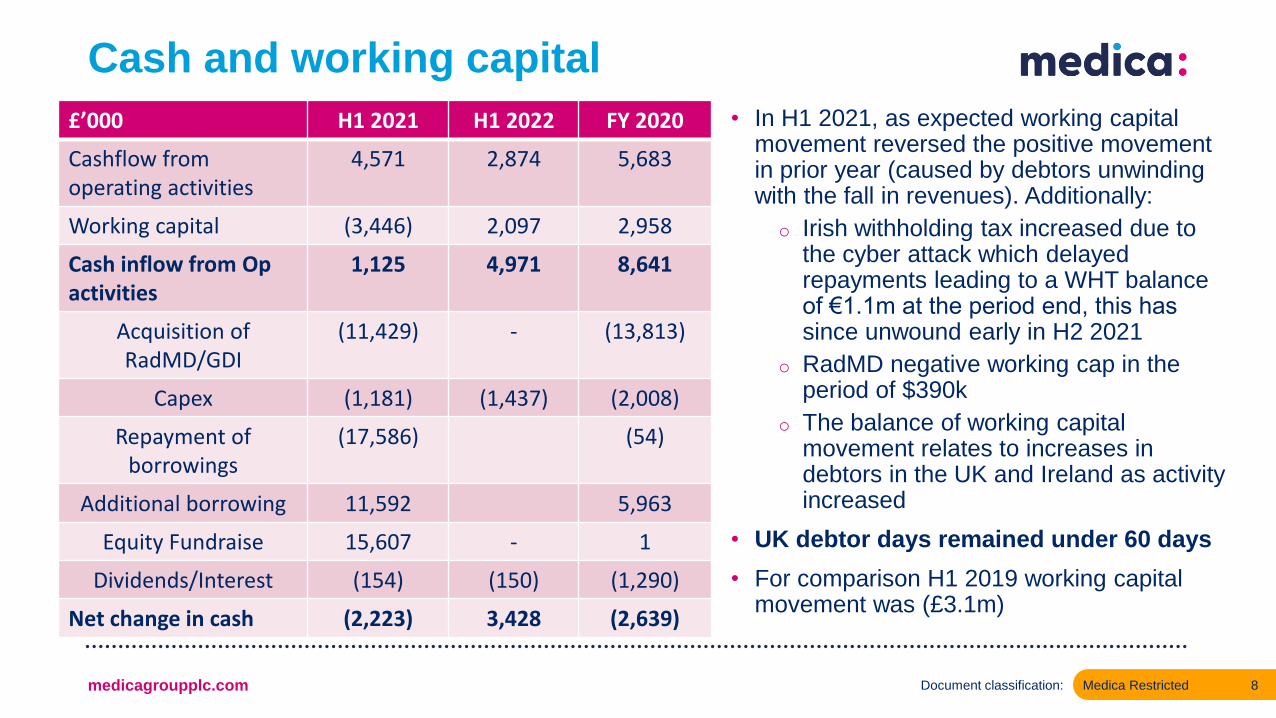

Cash and working capital

8

£’000 H1 2021 H1 2022 FY 2020

Cashflow from operating activities

4,571 2,874 5,683

Working capital (3,446) 2,097 2,958

Cash inflow from Op activities

1,125 4,971 8,641

Acquisition of RadMD/GDI

(11,429) - (13,813)

Capex (1,181) (1,437) (2,008)

Repayment of borrowings

(17,586) (54)

Additional borrowing 11,592 5,963

Equity Fundraise 15,607 - 1

Dividends/Interest (154) (150) (1,290)

Net change in cash (2,223) 3,428 (2,639)

• In H1 2021, as expected working capital movement reversed the positive movement in prior year (caused by debtors unwinding with the fall in revenues). Additionally:

o Irish withholding tax increased due to the cyber attack which delayed repayments leading to a WHT balance of €1.1m at the period end, this has since unwound early in H2 2021

o RadMD negative working cap in the period of $390k

o The balance of working capital movement relates to increases in debtors in the UK and Ireland as activity increased

• UK debtor days remained under 60 days

• For comparison H1 2019 working capital movement was (£3.1m)

medicagroupplc.com

Medica RestrictedDocument classification:

UK Update Core market remains strong

Richard Jones, CFO

Dr. Robert Lavis, Group Medical Director

Medica RestrictedDocument classification:

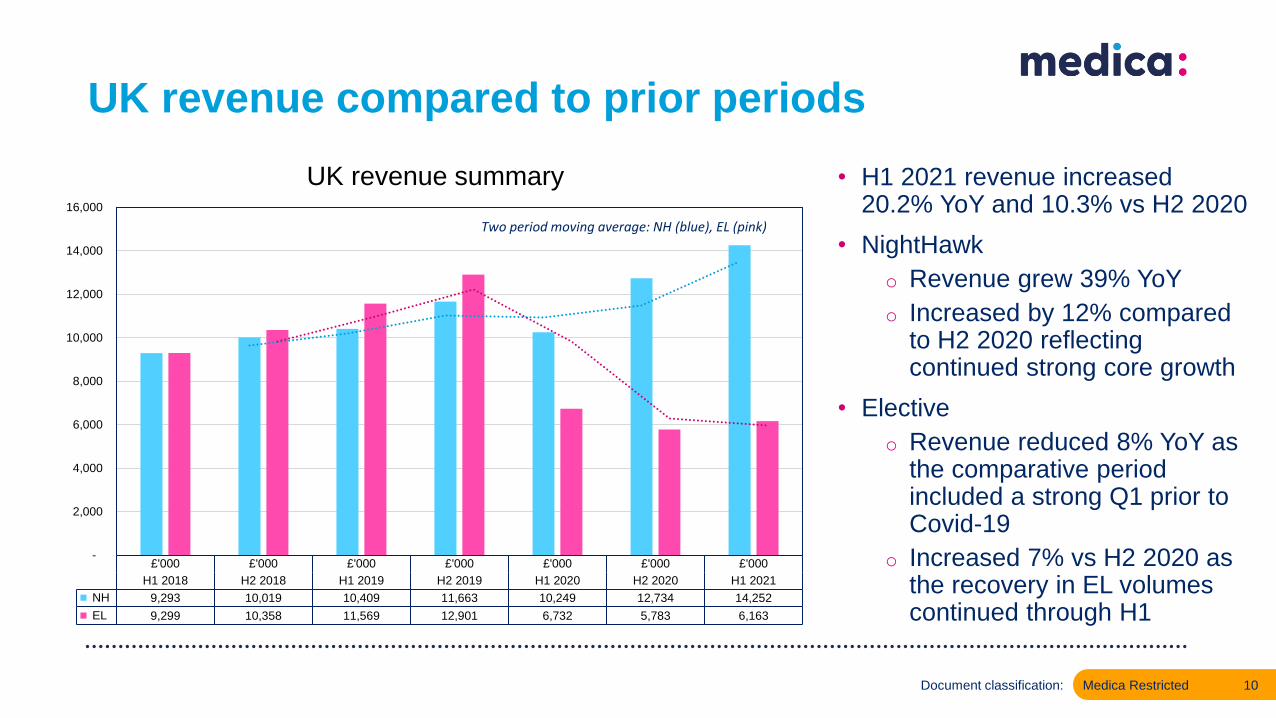

UK revenue compared to prior periods

• H1 2021 revenue increased 20.2% YoY and 10.3% vs H2 2020

• NightHawk

o Revenue grew 39% YoY

o Increased by 12% compared to H2 2020 reflecting continued strong core growth

• Elective

o Revenue reduced 8% YoY as the comparative period included a strong Q1 prior to Covid-19

o Increased 7% vs H2 2020 as the recovery in EL volumes continued through H1

10

£'000 £'000 £'000 £'000 £'000 £'000 £'000

H1 2018 H2 2018 H1 2019 H2 2019 H1 2020 H2 2020 H1 2021

NH 9,293 10,019 10,409 11,663 10,249 12,734 14,252

EL 9,299 10,358 11,569 12,901 6,732 5,783 6,163

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

UK revenue summary

Two period moving average: NH (blue), EL (pink)

Medica RestrictedDocument classification:

UK Elective activity progress FY 2021 YTD

• Elective activity has maintained positive momentum through FY 2021 to date and is now close to pre-pandemic levels (Jan-Feb 2020)

• Current growth trend expected to continue driven by

o Increasing activity from existing clients

o Demand returning from dormant clients

o New client connectionso Additional scanning

capacity (e.g. CDH locations) operational by year end

11

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

04/01/2021 04/02/2021 04/03/2021 04/04/2021 04/05/2021 04/06/2021 04/07/2021 04/08/2021 04/09/2021

Elective Units as % of Jan/Feb 20 average

Elective Units as % of budget Linear (Elective Units as % of budget)

Medica RestrictedDocument classification:

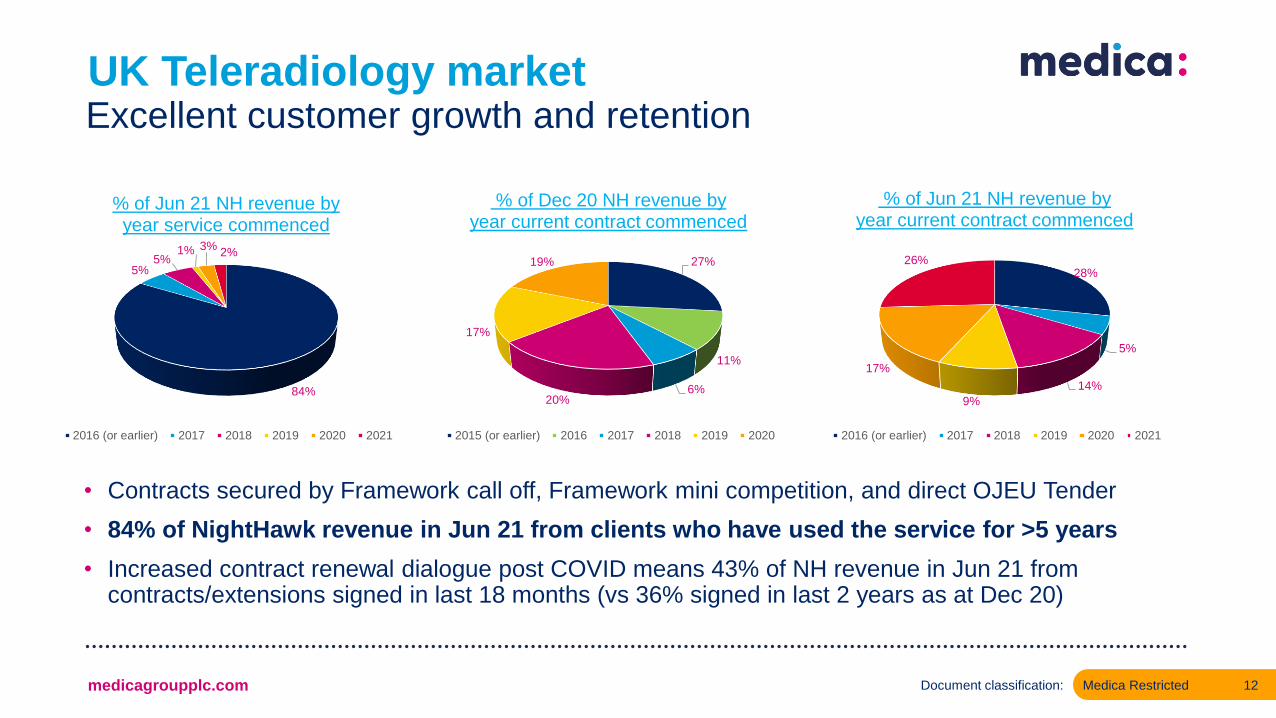

UK Teleradiology market

• Contracts secured by Framework call off, Framework mini competition, and direct OJEU Tender

• 84% of NightHawk revenue in Jun 21 from clients who have used the service for >5 years

• Increased contract renewal dialogue post COVID means 43% of NH revenue in Jun 21 from contracts/extensions signed in last 18 months (vs 36% signed in last 2 years as at Dec 20)

medicagroupplc.com

84%

5%5%

1% 3%2%

% of Jun 21 NH revenue by year service commenced

2016 (or earlier) 2017 2018 2019 2020 2021

28%

5%

14%

9%

17%

26%

% of Jun 21 NH revenue by year current contract commenced

2016 (or earlier) 2017 2018 2019 2020 2021

27%

11%

6%20%

17%

19%

% of Dec 20 NH revenue by year current contract commenced

2015 (or earlier) 2016 2017 2018 2019 2020

Excellent customer growth and retention

12

Medica RestrictedDocument classification:

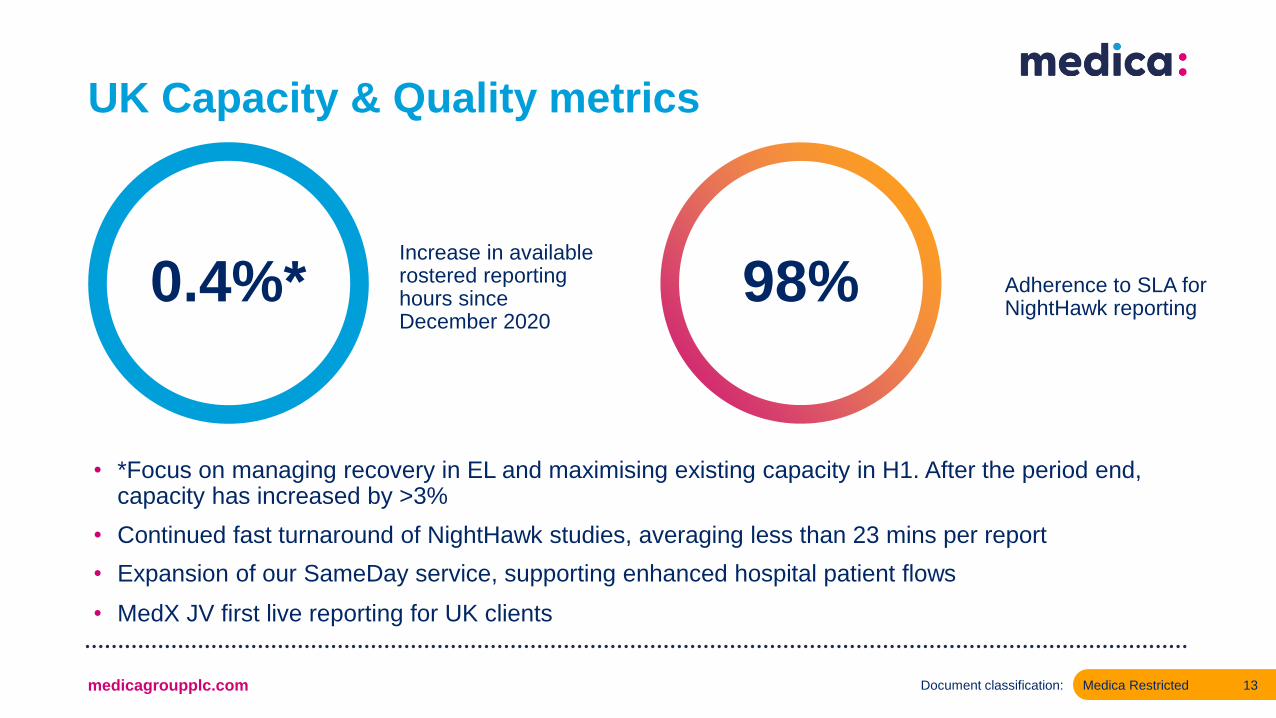

UK Capacity & Quality metrics

Increase in available rostered reporting hours since December 2020

0.4%*

13

• *Focus on managing recovery in EL and maximising existing capacity in H1. After the period end, capacity has increased by >3%

• Continued fast turnaround of NightHawk studies, averaging less than 23 mins per report

• Expansion of our SameDay service, supporting enhanced hospital patient flows

• MedX JV first live reporting for UK clients

medicagroupplc.com

98% Adherence to SLA for NightHawk reporting

Medica RestrictedDocument classification:

Augmented Intelligence in the real world

Processed cases flagged as critical by qER

Faster reporting time for cases flagged as critical (= 60s)

13% 7%

14

Excellent results from first AI rollout

• 90,000+ exams processed with qER so far

• From a continuous sample of over 8000 cases processed in August:

Critical exams were reported in an average of 13 minutes 24 seconds from the receipt of the last image.

medicagroupplc.com

Medica RestrictedDocument classification:

Ireland and US update: Performance of acquisitions on track

Stuart Quin, CEO

Medica RestrictedDocument classification:

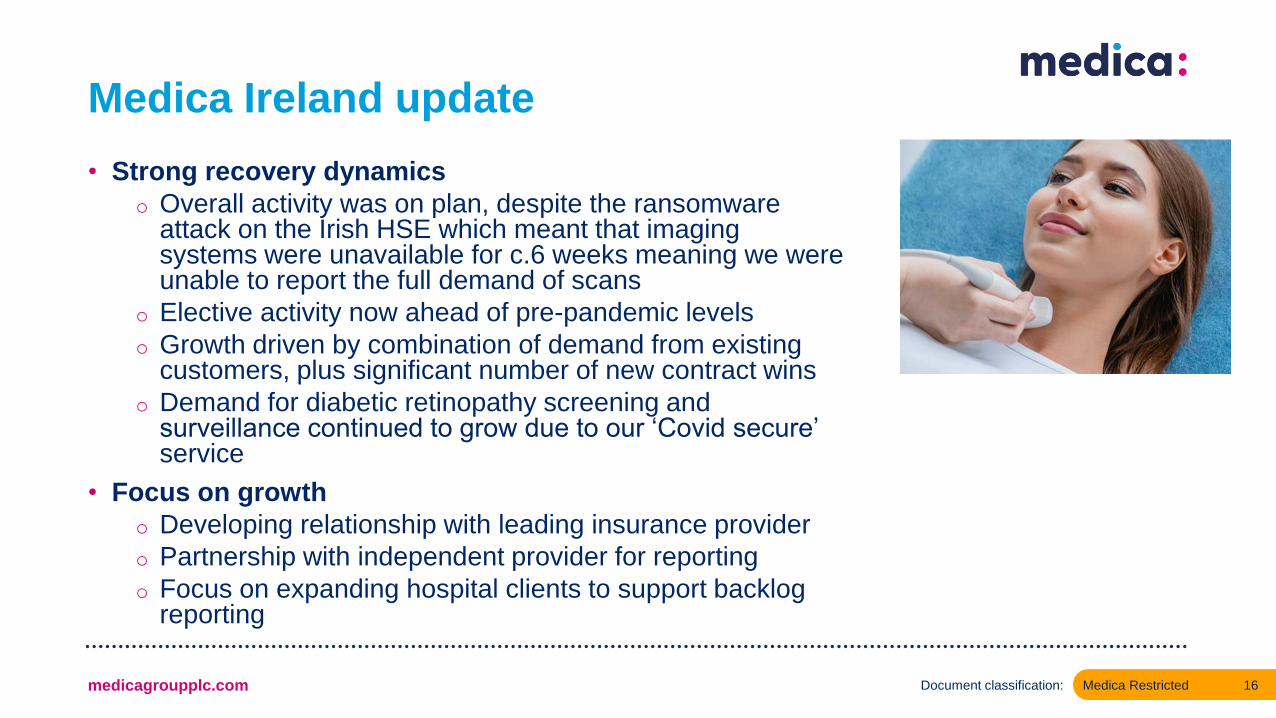

Medica Ireland update

• Strong recovery dynamics

o Overall activity was on plan, despite the ransomware attack on the Irish HSE which meant that imaging systems were unavailable for c.6 weeks meaning we were unable to report the full demand of scans

o Elective activity now ahead of pre-pandemic levels

o Growth driven by combination of demand from existing customers, plus significant number of new contract wins

o Demand for diabetic retinopathy screening and surveillance continued to grow due to our ‘Covid secure’ service

• Focus on growth

o Developing relationship with leading insurance provider

o Partnership with independent provider for reporting

o Focus on expanding hospital clients to support backlog reporting

16medicagroupplc.com

Medica RestrictedDocument classification:

US (RadMD) update

17medicagroupplc.com

• Initial delays to patient recruitment easing o RadMD acquired on 26 March. First 3 months in reporting period

has seen activity increase. Also new contract wins have converted into revenue post-period end

o Pipeline and contracted order book have both continued to grow since the period end providing good visibility and prospects for the remainder of 2021 and into 2022

• Focus on growtho New senior team in place - Chief Commercial Officer, as well as

Head of Operations, Finance Director

o Focus on new clients including medical devices and AI companies, as well as developing more strategic approach with larger existing clients

o Image acquisition and analysis system under review to improve functionality

Medica RestrictedDocument classification:

Strategy update and outlook: Delivering on strategy to meet growth targets

Stuart Quin, CEO

Medica RestrictedDocument classification:

Medica strategy

Invest in our people & systems

Telemedicine company of choice for

specialist doctors

Trusted, go-to partner

enhancing patient outcomes

Delivering profitable

growth with diversification

19

Delivering sustainable growth to enhance patient outcomes

1. Invest in our people and systems to build an

engaged and motivated team

2. Be the company of choice for specialist doctors

and clinicians wanting to expand their expertise in

telemedicine

3. Be the trusted, go-to partner for healthcare

providers with a reputation for reliability and

transparency to enhance patient outcomes

4. Deliver profitable, diversified growth

underpinned by commitment to ESG with focus

on market-leading clinical governance

medicagroupplc.co.uk

Capital Markets

Day

Medica RestrictedDocument classification:

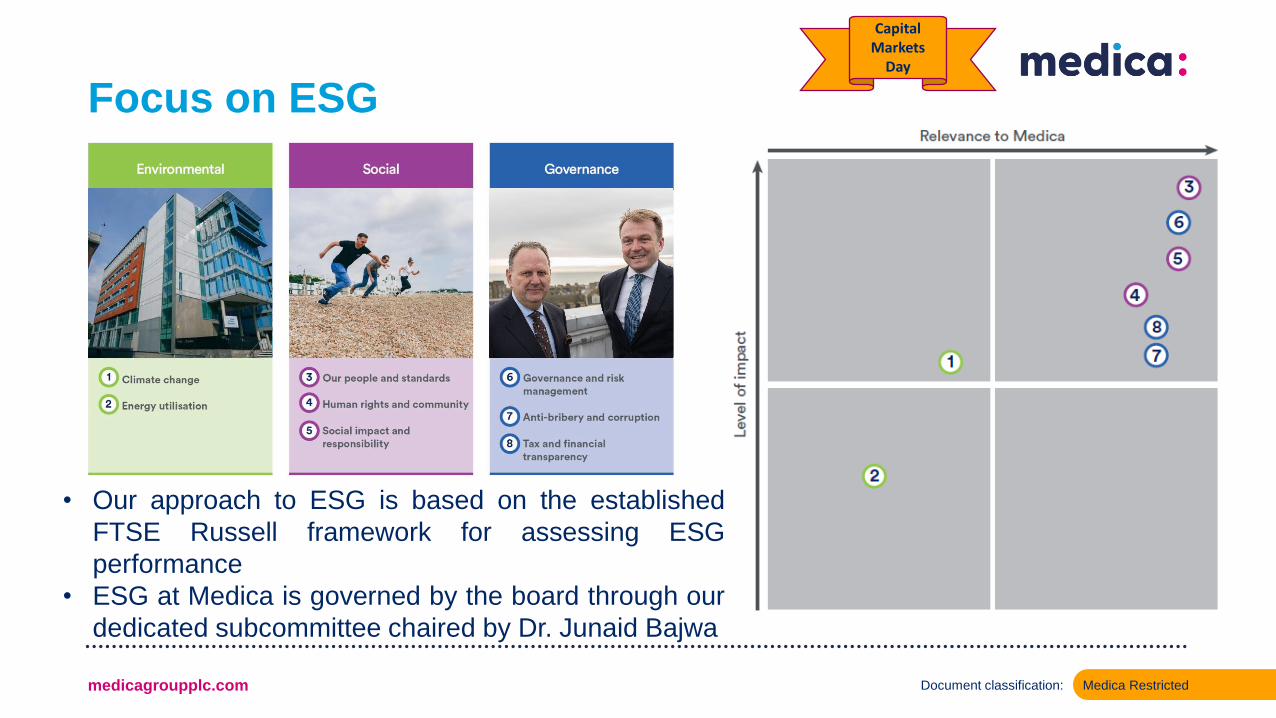

Focus on ESG

medicagroupplc.com

• Our approach to ESG is based on the established

FTSE Russell framework for assessing ESG

performance

• ESG at Medica is governed by the board through our

dedicated subcommittee chaired by Dr. Junaid Bajwa

Capital Markets

Day

Medica RestrictedDocument classification:

Short to Medium Term Financial and Investment targets

• Group Growth Rate and Revenue Target – Growth of core UK

business at 12-14% and recently acquired US and Irish companies

by over 15% in the short to medium term with an overall target of

c.£100m revenues in 3-5 years excluding any non-organic growth

• Target Margins – Gross Margins of over 45% and underlying

operating profit margins of over 20% in the short to medium term

• Target Return on Capital Employed (ROCE) – ROCE of at least

15% within a reasonable period for such opportunities whilst looking

to maintain group ROCE above 20% overall

• Target Cash Conversion – Underlying Operating Profit to Cash

conversion of at least 80%

medicagroupplc.com 21

Capital Markets

Day

Medica RestrictedDocument classification:

Summary

➢ Strong H1 performance driven by recovery in Elective volumes and continued NH growth

➢ Positive contribution from Ireland and US to H1 results

➢ Strategy execution well underway: successful first Capital Markets Day showcased progress

➢ Opportunities to drive additional growth via selective M&A in adjacent areas of telemedicine & new geographies

➢ Outlook: ➢ Patient backlogs will continue to drive activity through

Q4 and into 2022

➢ Focus on building pipeline in imaging CRO business

medicagroupplc.com 22

Medica RestrictedDocument classification:

Q&A

Thank you for your attention

Medica RestrictedDocument classification:

Appendices

Medica RestrictedDocument classification:

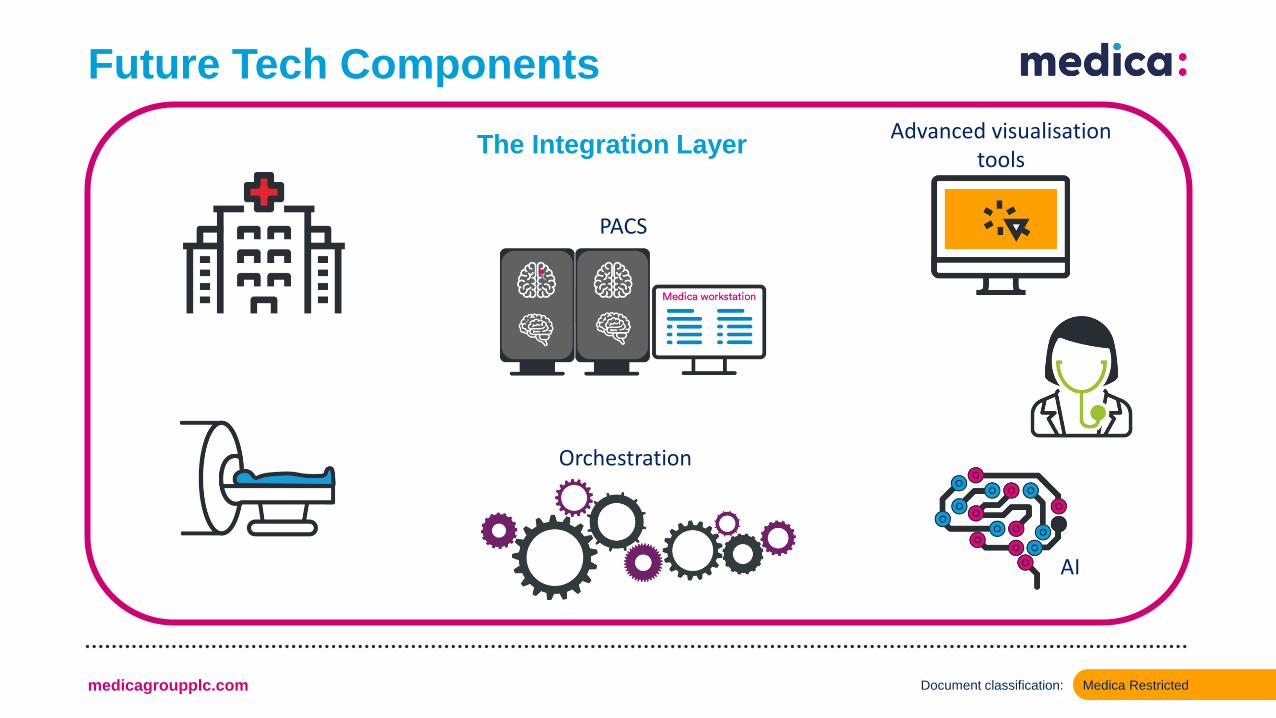

Future Tech Components

PACS

The Integration Layer

Orchestration

Advanced visualisation tools

AI

medicagroupplc.com

Medica RestrictedDocument classification:

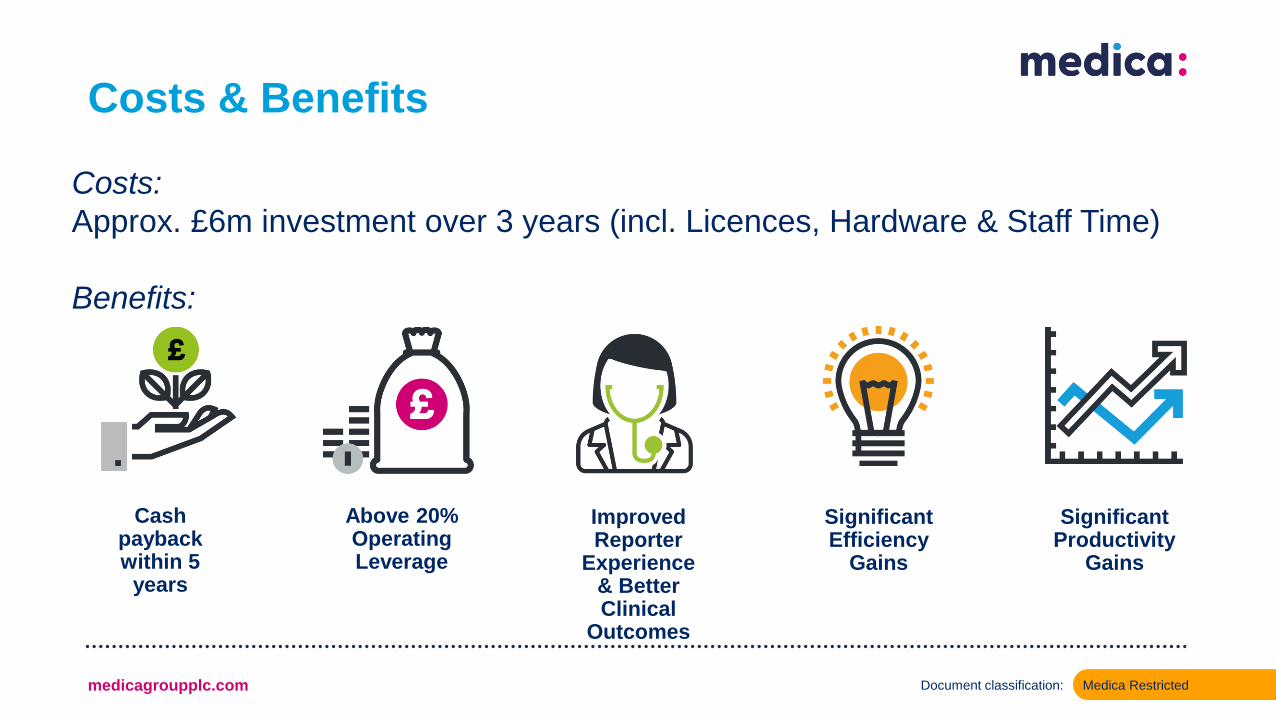

Costs & Benefits

Cash payback within 5

years

Above 20% Operating Leverage

Improved Reporter

Experience & Better Clinical

Outcomes

Significant Efficiency

Gains

Significant Productivity

Gains

Costs:

Approx. £6m investment over 3 years (incl. Licences, Hardware & Staff Time)

Benefits:

medicagroupplc.com

Medica RestrictedDocument classification:

Programme Timeline

27

Q420 Q121 Q221 Q321 Q222Q122Q421 Q322 Q422

PACS1 & Integration Layer Development

AI

qER Live

PACS1 Live

PACS1 Production Ready

PACS 2aPACS

2bPACS 2c

qER Shortlisted for APMTechnology Project of the Year

Orchestration

Terarecon AV

Mirada AV

AI

Client Portal

L2P & WFM Digitise Doc Details

medicagroupplc.com